Embed Size (px)

Citation preview

Top 30 Chilean Companies - April 2007 3

44 IInnttrroodduuccttiioonn

CCoommmmeennttaarriieess6 Understanding Chile's Sovereign Credit Fundamentals 15 Chile’s Economic Growth And Fiscal Position: How Important Are

They From A Ratings Perspective?18 2007's Top 5 Credit Factors For Corporate Credit Quality In Chile20 Chilean Banks Look To Improve On 2006 Performance In 2007

CCrreeddiitt SSttaattiissttiiccss 24 Peer Comparison Table

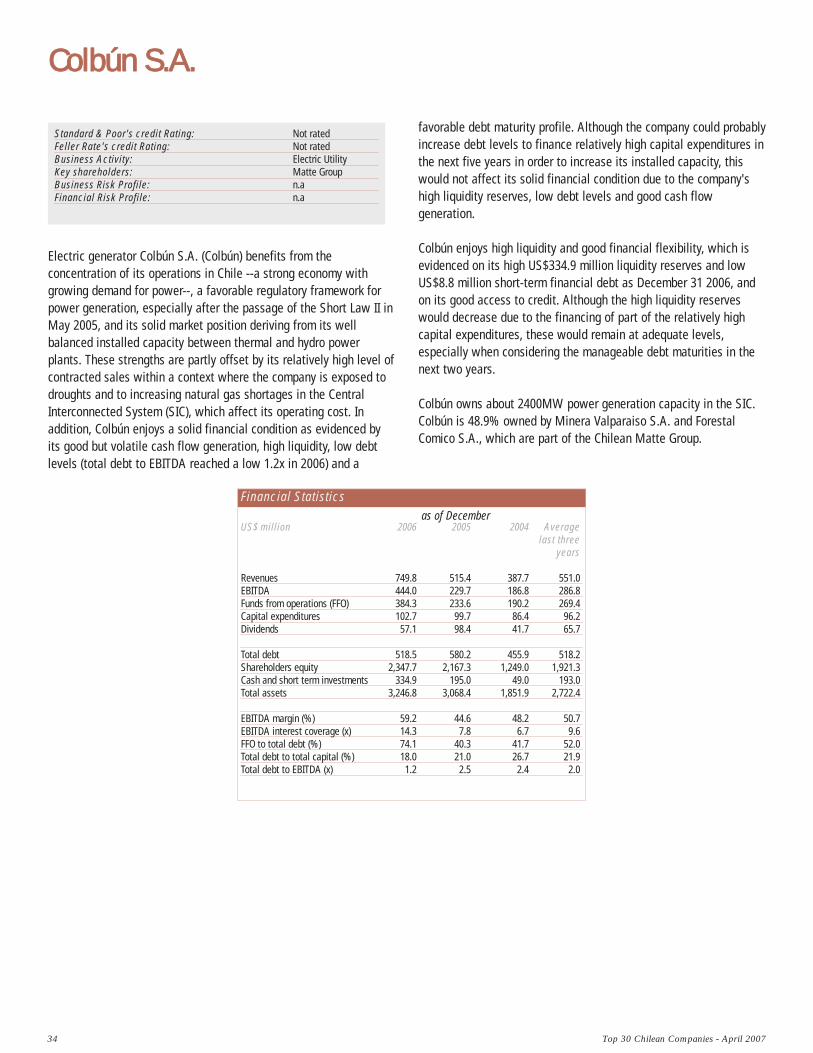

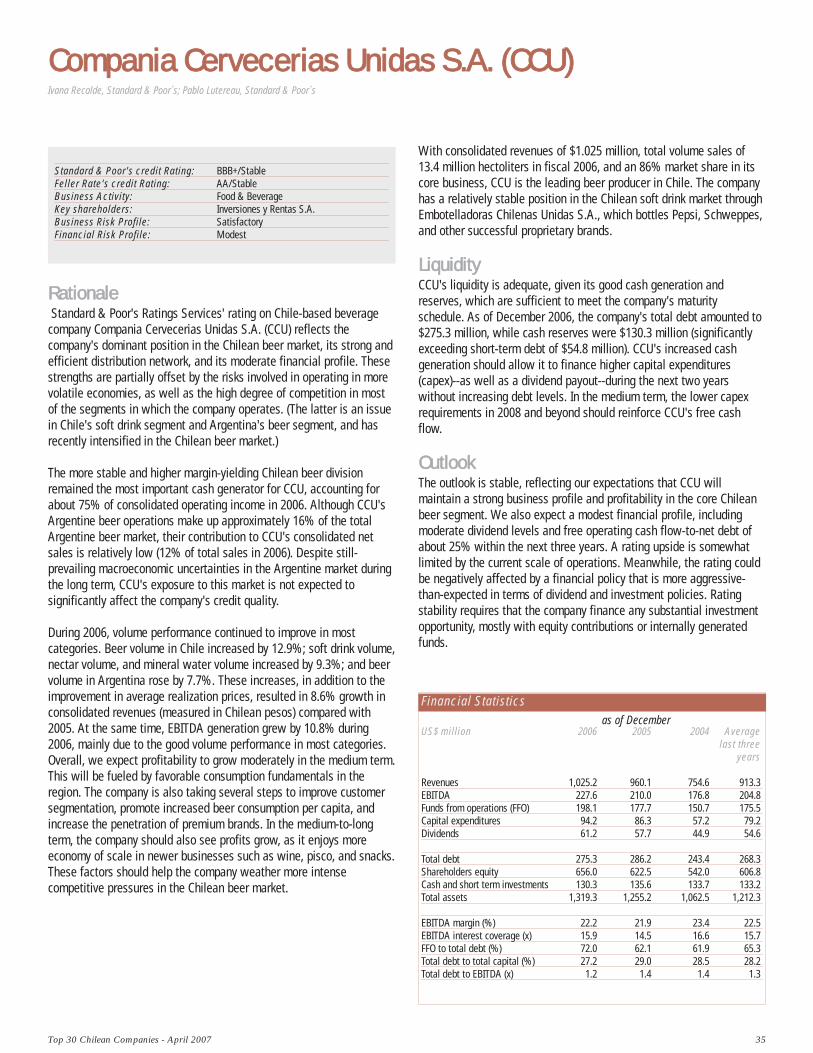

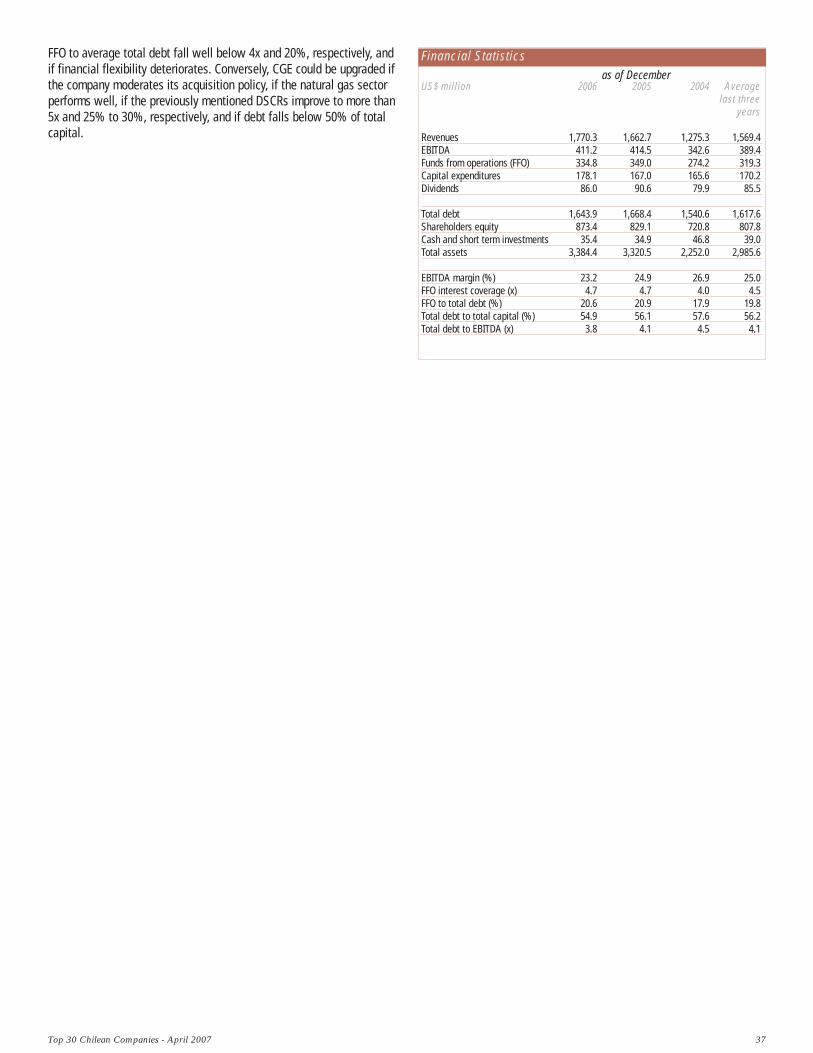

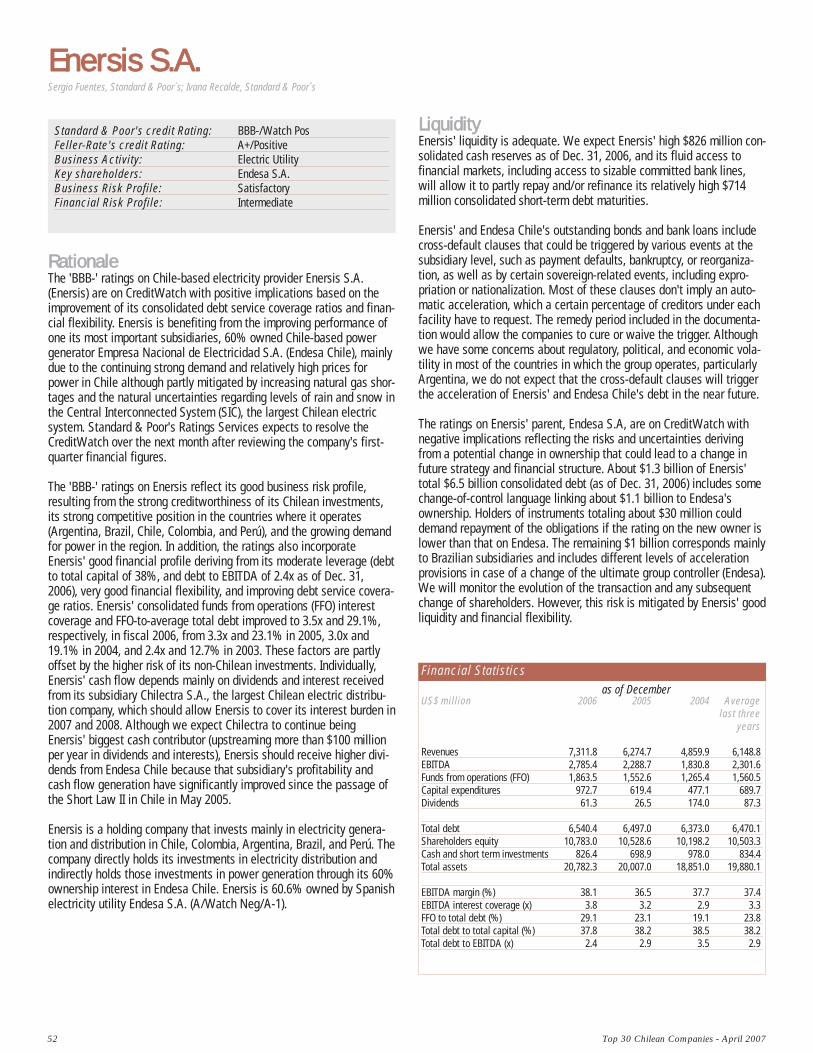

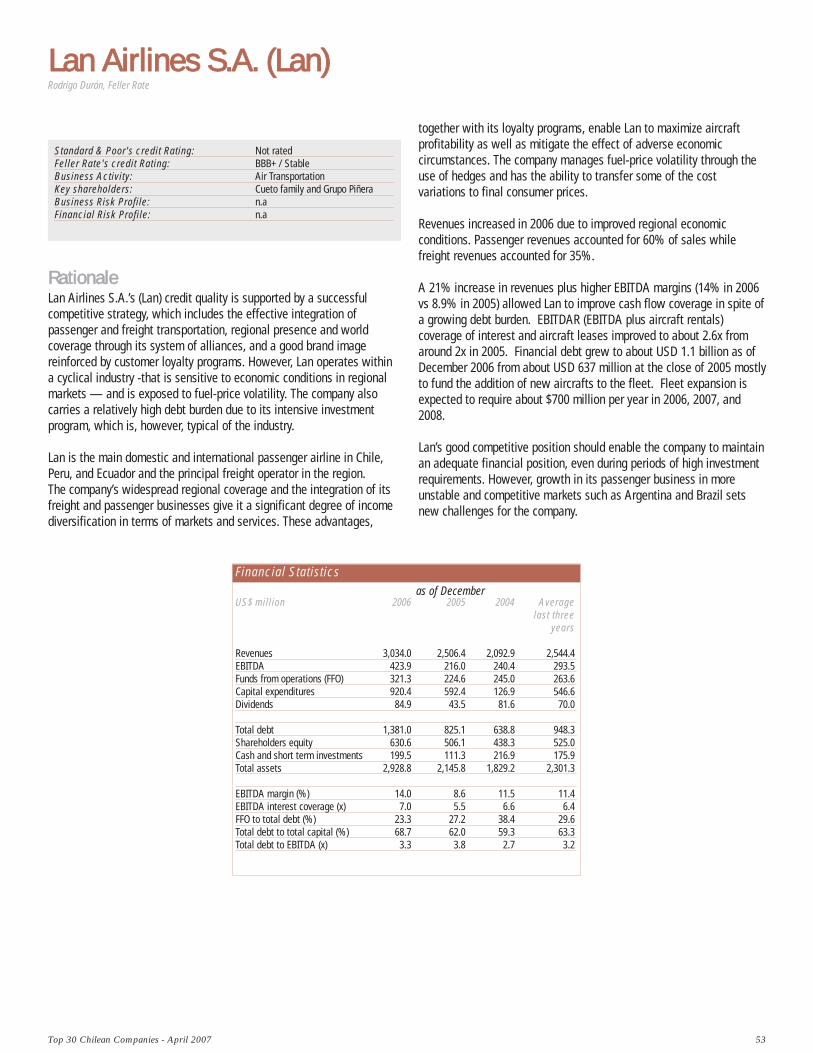

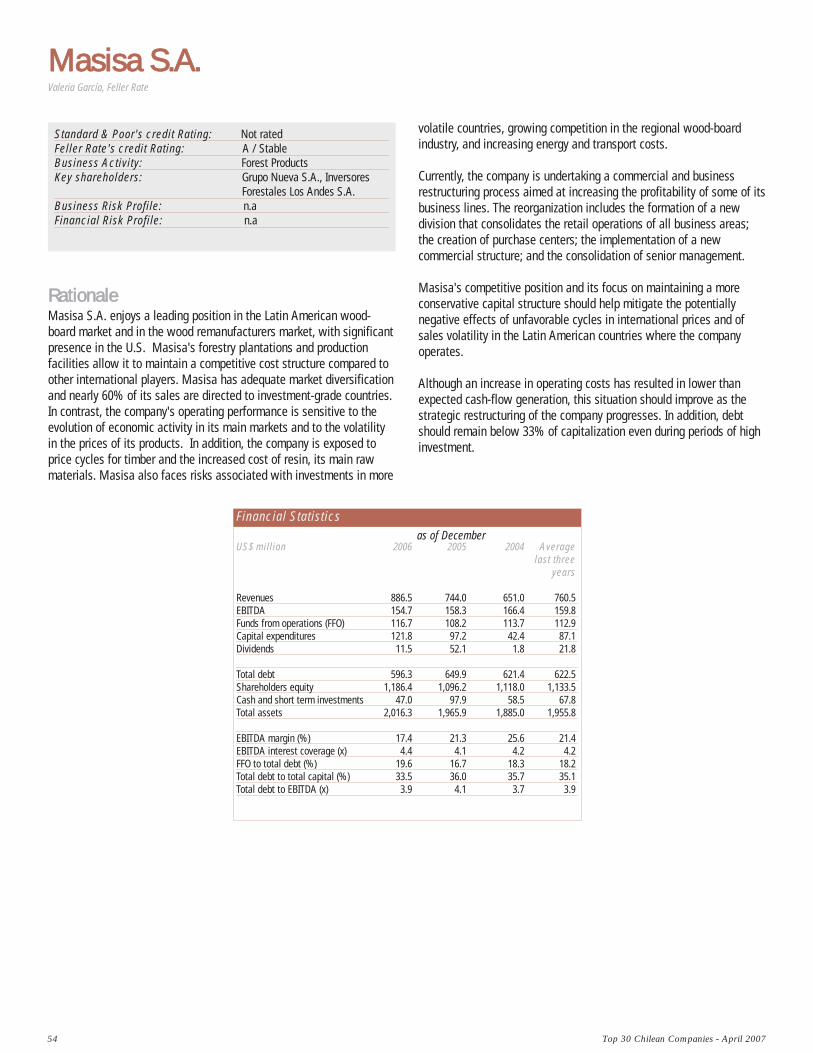

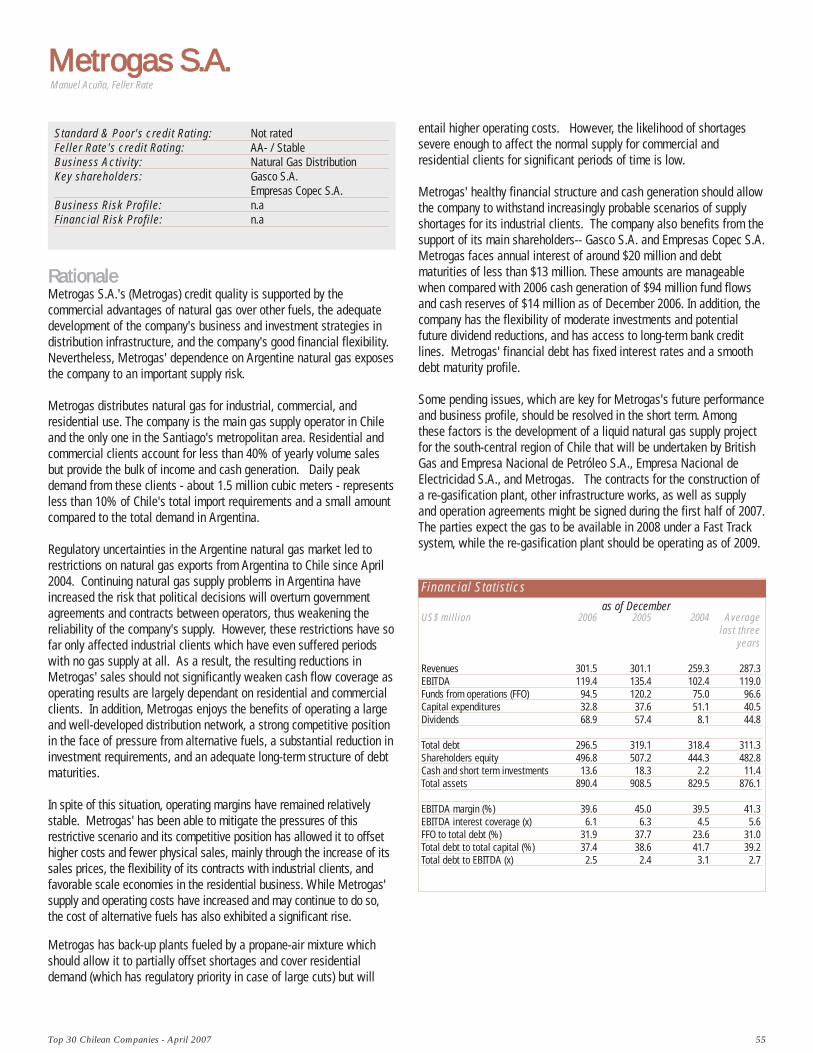

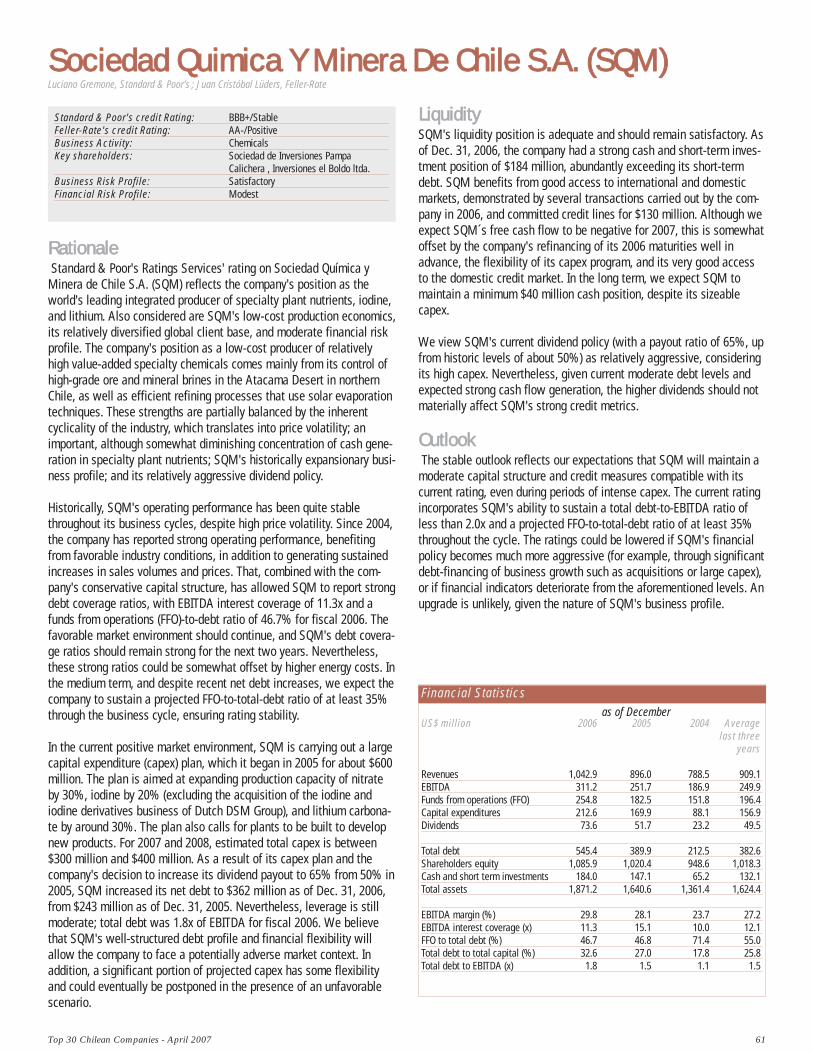

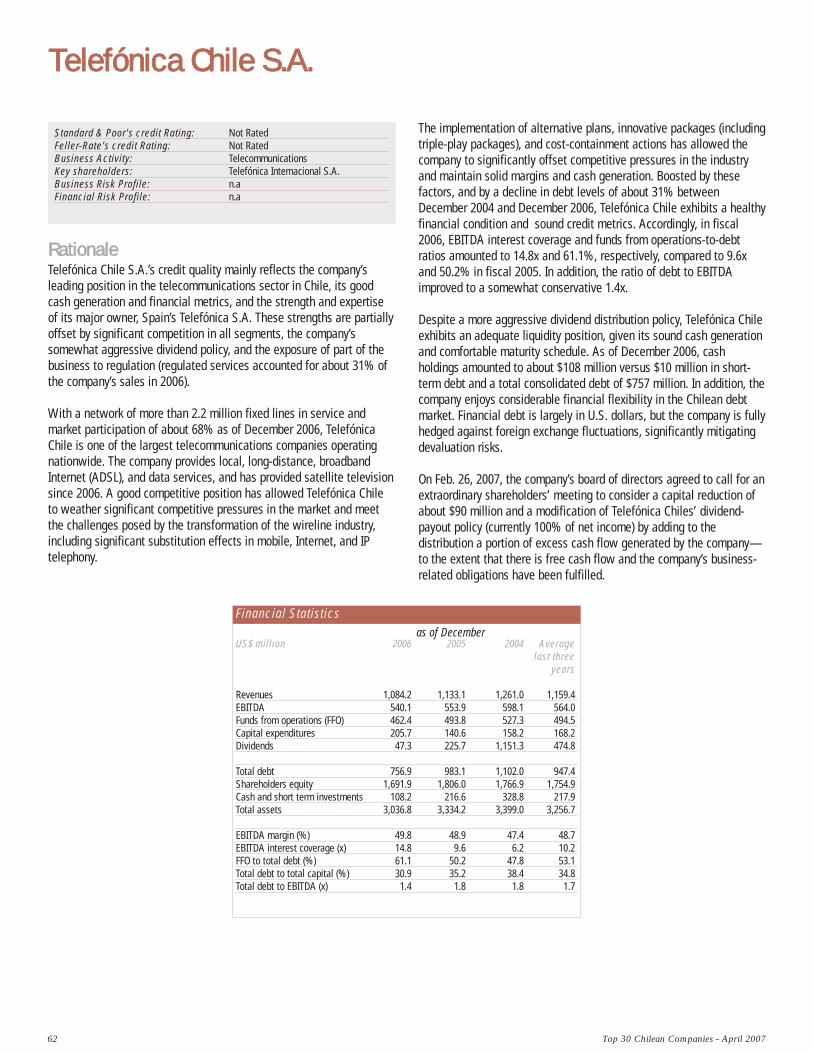

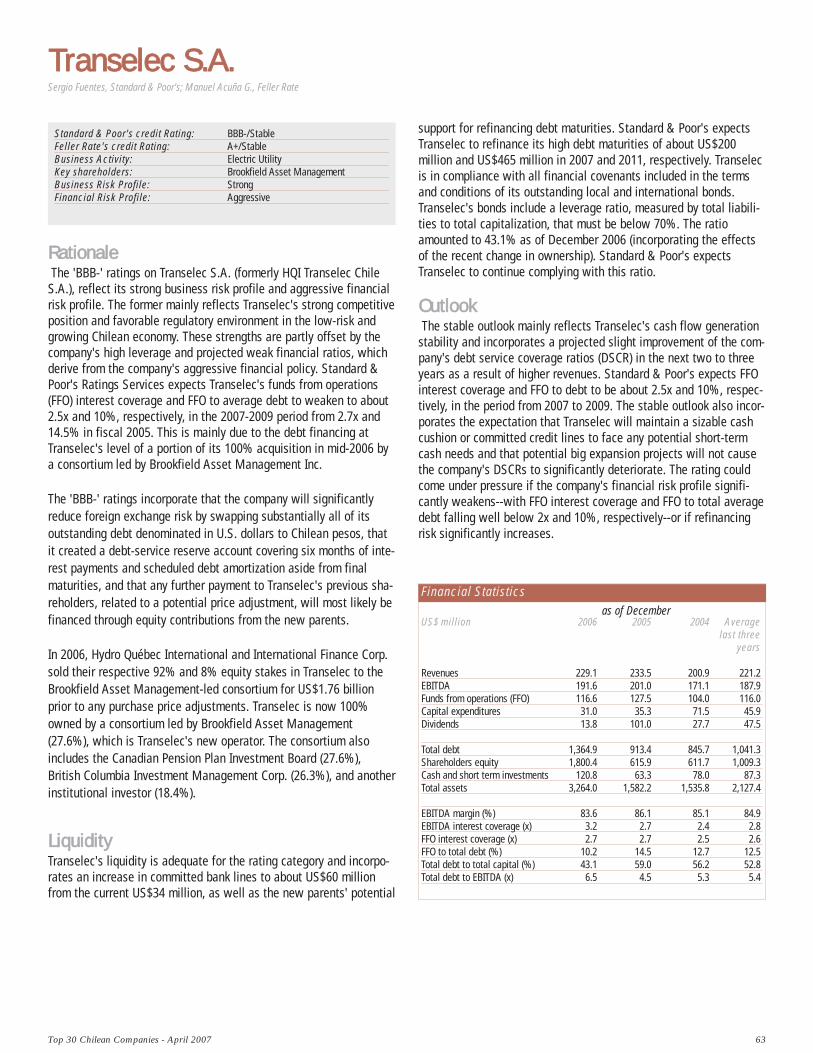

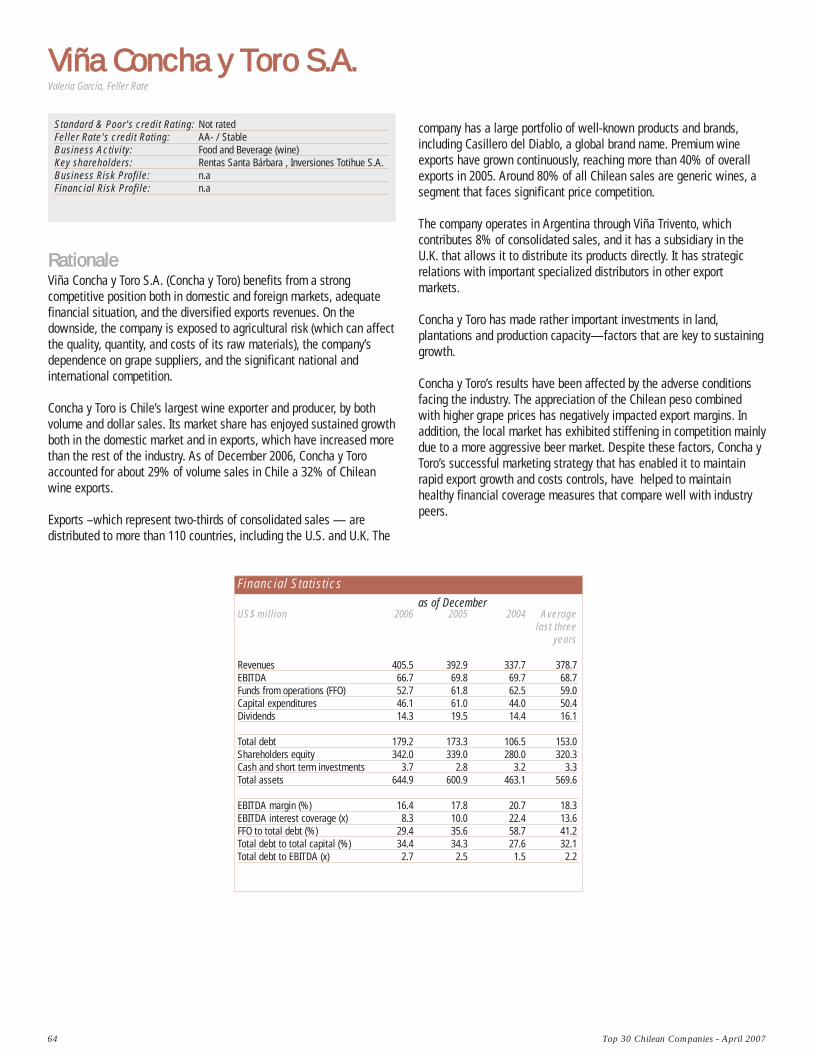

CCrreeddiitt RReeppoorrttss28 AES Gener S.A. 30 CAP S.A. 31 Celulosa Arauco y Constitución S.A. 32 Cementos Bío Bío S.A. 33 Cencosud S.A. 34 Colbún S.A. 35 Compañía Cervecerías Unidas S.A. 36 Compañía General de Electricidad S.A. 38 Corporación Nacional del Cobre de Chile 40 Distribución y Servicios D & S S.A. 41 Embotelladora Andina S.A. 43 Empresa Nacional de Electricidad S.A. 45 Empresa Nacional de Petróleo 47 Empresa Nacional de Telecomunicaciones S.A. 48 Empresas Carozzi S.A. 49 Empresas CMPC S.A. 51 Empresas Copec S.A. 52 Enersis S.A. 53 LAN Airlines S.A. 54 Masisa S.A. 55 Metrogas S.A. 56 Minera Escondida Limitada 57 Quiñenco S.A. 58 Ripley Chile S.A. 59 S.A.C.I Falabella60 Sigdo Koppers S.A.61 Sociedad Química y Minera De Chile S.A.62 Telefónica Chile S.A.63 Transelec S.A.64 Viña Concha y Toro S.A.

DDeeffiinniittiioonnss66 Standard & Poor's Role In The Financial Markets 68 Glossary Of Financial Ratio Definitions 69 Standard & Poor's Rating Definitions71 Feller Rate's - Rating Definitions

7755 CCoonnttaacctt LLiisstt

Table of Contents

4 Top 30 Chilean Companies - April 2007

Introduction

Standard & Poor's Ratings Services and Feller Rate Clasificadora deRiesgo are pleased to present "Chilean Top 30 Corporates," theinaugural joint analytical report since our renewed affiliation inNovember 2006. Our analysts have reviewed the business and financialprofiles of Chile's top 30 companies with both a global perspective andin-depth knowledge of the domestic operating environment. Thesecompanies are either key players in the country's major industrialsectors or active participants in the international or domestic bondmarkets, and have adequate financial disclosure.

Chile's solid economic performance, stable indicators, and reliableinstitutional framework have also shaped the country's corporate sectorduring the past decade. The fate of most of the major corporations istied to the swings of the global economy, especially the evolution ofcommodities in general and copper in particular. Nevertheless, prudentfinancial policies and cash management as well as good access tocredit have allowed most players to grow and withstand externalshocks while maintaining their strong creditworthiness through thecycle.

These characteristics will be evident from the individual analysesincluded in this publication. We have also included commentaries onthe sovereign rating of Chile, the financial system, the corporate sectorin general, and information on criteria and methodology to provide abroader analytical framework.

We trust that the investment community, both in Chile and overseas,will find this report an important reference tool that will facilitateinvestment decisions.

Marta CastelliOffice HeadStandard & Poor's

Other analysts who have contributed to this publication:

Standard & Poor's AnalystsPablo Lutereau, DirectorSergio Fuentes, DirectorIvana Recalde, Associate DirectorLuciano Gremone, AssociateEzequiel Gómez Cáceres, Rating SpecialistJavier Vieiro Cobas, Rating Analyst

Feller Rate AnalystManuel Acuña, Subgerente

Commentaries

6 Top 30 Chilean Companies - April 2007

Sebastian Briozzo, Buenos Aires (54) 11 4891 2120; [email protected] ; Joydeep Mukherji, New York (1) 212-438-7351;[email protected]

Understanding CChile's SSovereign CCredit FFundamentals

MMaajjoorr RRaattiinngg FFaaccttoorrss

Strengths:A strong policy framework founded on rules-based fiscal and monetary policies and a political commitment to an open economy. A matured political consensus on key elements of economic policies. A low and declining public debt burden.

Weaknesses:A relatively narrow economic base and resulting vulnerability to cyclical economic performance due to the fluctuating price of copper. A relatively high (albeit declining) external debt burden.

RRaattiioonnaallee The ratings and outlooks on the Republic of Chile reflect Standard &Poor’s Ratings Services’ expectation that the combination ofappropriate economic policy management and a strong improvement inmost of the country’s indicators will increase the sovereign’s chance ofcontinuing its upward trend in creditworthiness.

Chile is one of the few emerging-market economies to gain strongcredentials thanks to the implementation of countercyclical fiscal andmonetary policies. These policies are of particular importance given thecountry’s dependence upon commodities, copper in particular. Thispolicy framework was consolidated and strengthened through thepassage of a Fiscal Responsibility Law, which was supported acrossthe political spectrum. Government authorities are currently addressingstill-pending issues on the macroeconomic agenda with medium- tolong-term impact, such as additional modifications to the already-reformed pension system, the capitalization of the central bank, andmeasures targeting competitiveness. The pension reform will allowChile to move toward wider and more generous coverage in a prudentand fiscally sustainable way. Authorities have also announced newmeasures that will increase transparency in the management of thegovernment’s countercyclical fiscal funds. This reform is expected tocontinue to reduce economic growth volatility over the medium andlong term, matching Chile’s economic performance to that of higher-rated governments.

The implementation of Chile’s structural fiscal rule (now supported bylaw) in the context of extraordinarily high copper prices is resulting instrong fiscal surpluses and, therefore, a rapid decline in debt levels.Chile’s general government is expected to have reached a fiscal surplusequivalent to 7.9% of GDP by year-end 2006, and positive balances arealso expected for 2007 and 2008. As a result of this performance,Chile’s net general government debt level is approaching zero (only 3%of GDP by year-end 2006) once government assets saved in thecountercyclical fiscal funds are taken into account.

Consensus on the need to maintain this conservative approach in orderto continue to protect Chile’s macroeconomic framework from volatilecommodity prices is high across the political spectrum. While thecurrent target of 1% of GDP for the structural fiscal surplus could varyin the future depending upon the progress in dealing with the issuesthat justify the surplus (future pension costs and capitalization of thecentral bank), the strong commitment from Chilean Administrations tosound fiscal policies is expected to remain.

Despite recent improvements, Chile’s credit rating will continue to beconstrained by the presence of a less-wealthy and narrower economicstructure than found in most of its ‘A’ rated peers.

OOuuttllooookk The positive outlook is based upon the expectation that Chile’s already-strong macroeconomic framework will continue to be strengthened,bringing additional stability to GDP performance over the medium andlong term in line with that of higher-rated credits. Recent governmentefforts to address pending issues, in particular on the pension front,will continue to diminish the risk the Chilean economy will face overthe medium term, bringing additional signs of predictability to Chile’smedium- and long-term economic prospects. Continuation of thecurrent economic policy set, combined with the strong results shown inthe economic, fiscal, and external indicators—even in the case of aexpected decrease in copper prices to more moderate levels (albeit stillhigh by historical standards—could lead to a rating upgrade.

Top 30 Chilean Companies - April 2007 7

CCoommppaarraattiivvee AAnnaallyyssiiss:: AAlltthhoouugghh LLeessss WWeeaalltthhyy,,CChhiillee CCoommppaarreess WWeellll TToo RRaatteedd PPeeeerrss

Chile’s growth prospects are similar to the levels in rated peers; Fiscal balances and debt burden compare favorably with those of rated peers; and Chile’s declining external debt and debt-service burden are approaching the median levels in rated peers.

The ratings on Chile are the highest in Latin America and reflect thecountry’s successful use of monetary, exchange-rate, and fiscal policiesto reduce external vulnerability, increase economic flexibility, andsustain GDP growth. Rising standards of governance, a low and fallingpublic debt burden, and a strong policy framework place Chile in the ‘A’category of sovereigns.

The political consensus behind market-oriented policies is sturdy and isexpected to remain strong. Unlike other countries in Latin America, thestrong consensus on macroeconomic issues has allowed the politicaldebate to move toward the microeconomic arena. The macroeconomicpolicy consensus is sustained by Chile’s success in reducing poverty. Itspoverty rate decreased to 18% in 2006 from 39% in 1990, comparedwith a fall to 39% from 48% for the Latin region as a whole during thesame period. However, significant challenges remain ahead in terms ofimproving Chile’s still highly unequal income distribution. Its Ginicoefficient of about 0.57 is one of the highest (more inequality) in theworld, only surpassed by that of some African nations as well asBolivia (B-/Negative; all ratings herein are long-term foreign currency sovereign credit ratings/outlook), Haiti (not rated), Colombia(BB/Positive), and Paraguay (B-/Positive) and the Federative Republic ofBrazil (BB/Positive), according to the U.N. Human Development Reportfor 2006 (although the data for Chile in the report corresponds to 2000,the situation has not significantly changed since).

Chile’s public institutions are stronger than those in its counterparts inother Latin American countries and the level of corruption is perceivedto be lower, according to international surveys. Chile’s civil service,however, is not as professional as its counterpart in highly rated

European and Commonwealth countries. Chile generally scores betterthan other Latin countries on most measures of competitiveness butscores worse than lower rated countries like Malaysia (A-/Stable) andthe Republic of Hungary (BBB+/Stable) in terms of the costs anddifficulties of doing business, especially new-firm startups. Chile’s long-term productivity and growth prospects should improve throughgrowing investment in infrastructure and education, but its workforce isless educated on average than the workforce of similarly ratedRepublic of Korea (A/Stable).

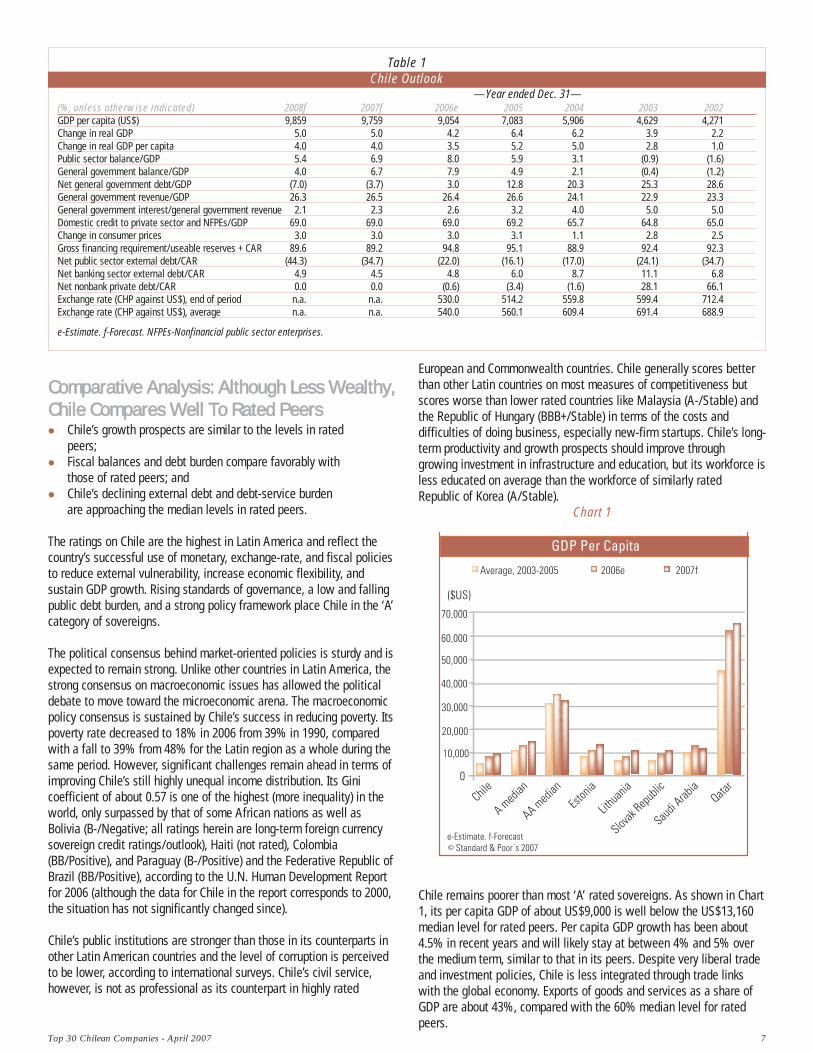

Chart 1

Chile remains poorer than most ‘A’ rated sovereigns. As shown in Chart1, its per capita GDP of about US$9,000 is well below the US$13,160median level for rated peers. Per capita GDP growth has been about4.5% in recent years and will likely stay at between 4% and 5% overthe medium term, similar to that in its peers. Despite very liberal tradeand investment policies, Chile is less integrated through trade linkswith the global economy. Exports of goods and services as a share ofGDP are about 43%, compared with the 60% median level for ratedpeers.

Table 1Chile Outlook

—Year ended Dec. 31— (%, unless otherwise indicated) 2008f 2007f 2006e 2005 2004 2003 2002 GDP per capita (US$) 9,859 9,759 9,054 7,083 5,906 4,629 4,271 Change in real GDP 5.0 5.0 4.2 6.4 6.2 3.9 2.2 Change in real GDP per capita 4.0 4.0 3.5 5.2 5.0 2.8 1.0 Public sector balance/GDP 5.4 6.9 8.0 5.9 3.1 (0.9) (1.6) General government balance/GDP 4.0 6.7 7.9 4.9 2.1 (0.4) (1.2) Net general government debt/GDP (7.0) (3.7) 3.0 12.8 20.3 25.3 28.6 General government revenue/GDP 26.3 26.5 26.4 26.6 24.1 22.9 23.3 General government interest/general government revenue 2.1 2.3 2.6 3.2 4.0 5.0 5.0 Domestic credit to private sector and NFPEs/GDP 69.0 69.0 69.0 69.2 65.7 64.8 65.0 Change in consumer prices 3.0 3.0 3.0 3.1 1.1 2.8 2.5 Gross financing requirement/useable reserves + CAR 89.6 89.2 94.8 95.1 88.9 92.4 92.3 Net public sector external debt/CAR (44.3) (34.7) (22.0) (16.1) (17.0) (24.1) (34.7) Net banking sector external debt/CAR 4.9 4.5 4.8 6.0 8.7 11.1 6.8 Net nonbank private debt/CAR 0.0 0.0 (0.6) (3.4) (1.6) 28.1 66.1 Exchange rate (CHP against US$), end of period n.a. n.a. 530.0 514.2 559.8 599.4 712.4 Exchange rate (CHP against US$), average n.a. n.a. 540.0 560.1 609.4 691.4 688.9

e-Estimate. f-Forecast. NFPEs-Nonfinancial public sector enterprises.

8 Top 30 Chilean Companies - April 2007

Although advancing rapidly in this regard, Chile’s economy remainsvulnerable to commodity prices. The country’s comparatively narroweconomic base has been a constraint on the rating, but it has beenloosening due to fiscal and monetary policies that have contributed torising productivity while dampening the impact of sharp changes in theterms of trade on economic performance.

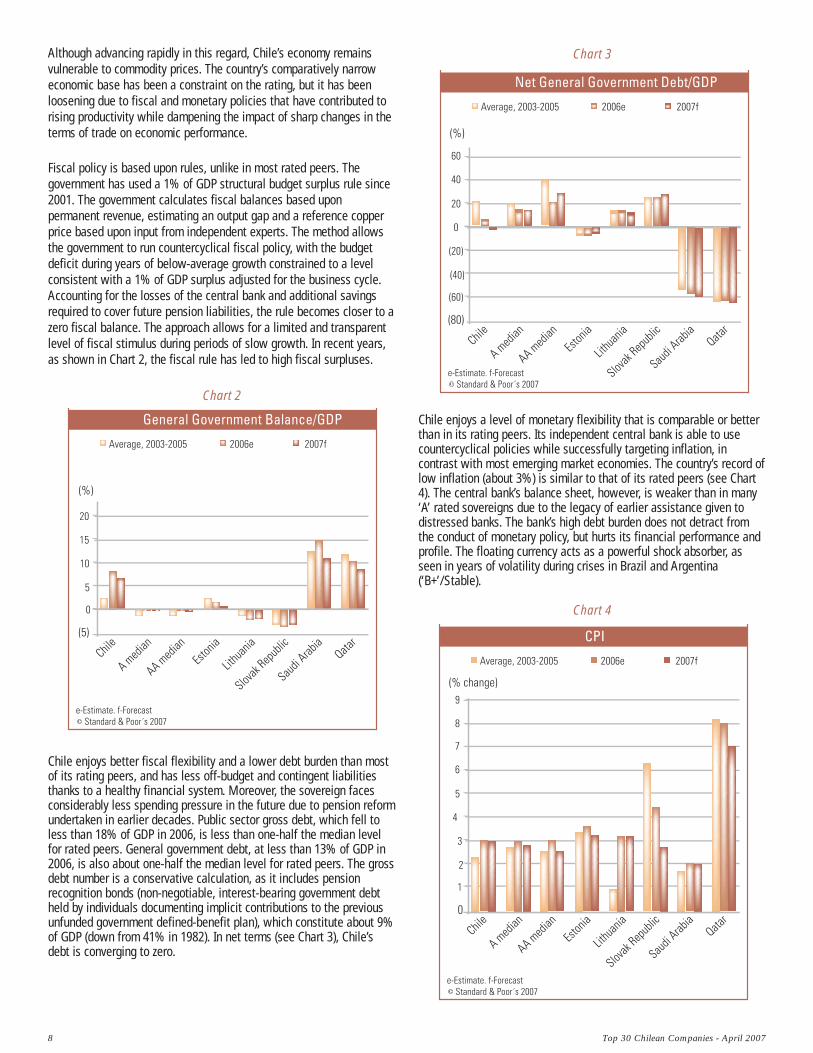

Fiscal policy is based upon rules, unlike in most rated peers. Thegovernment has used a 1% of GDP structural budget surplus rule since2001. The government calculates fiscal balances based uponpermanent revenue, estimating an output gap and a reference copperprice based upon input from independent experts. The method allowsthe government to run countercyclical fiscal policy, with the budgetdeficit during years of below-average growth constrained to a levelconsistent with a 1% of GDP surplus adjusted for the business cycle.Accounting for the losses of the central bank and additional savingsrequired to cover future pension liabilities, the rule becomes closer to azero fiscal balance. The approach allows for a limited and transparentlevel of fiscal stimulus during periods of slow growth. In recent years,as shown in Chart 2, the fiscal rule has led to high fiscal surpluses.

Chart 2

Chile enjoys better fiscal flexibility and a lower debt burden than mostof its rating peers, and has less off-budget and contingent liabilitiesthanks to a healthy financial system. Moreover, the sovereign facesconsiderably less spending pressure in the future due to pension reformundertaken in earlier decades. Public sector gross debt, which fell toless than 18% of GDP in 2006, is less than one-half the median levelfor rated peers. General government debt, at less than 13% of GDP in2006, is also about one-half the median level for rated peers. The grossdebt number is a conservative calculation, as it includes pensionrecognition bonds (non-negotiable, interest-bearing government debtheld by individuals documenting implicit contributions to the previousunfunded government defined-benefit plan), which constitute about 9%of GDP (down from 41% in 1982). In net terms (see Chart 3), Chile’sdebt is converging to zero.

Chart 3

Chile enjoys a level of monetary flexibility that is comparable or betterthan in its rating peers. Its independent central bank is able to usecountercyclical policies while successfully targeting inflation, incontrast with most emerging market economies. The country’s record oflow inflation (about 3%) is similar to that of its rated peers (see Chart4). The central bank’s balance sheet, however, is weaker than in many‘A’ rated sovereigns due to the legacy of earlier assistance given todistressed banks. The bank’s high debt burden does not detract fromthe conduct of monetary policy, but hurts its financial performance andprofile. The floating currency acts as a powerful shock absorber, asseen in years of volatility during crises in Brazil and Argentina(‘B+’/Stable).

Chart 4

Top 30 Chilean Companies - April 2007 9

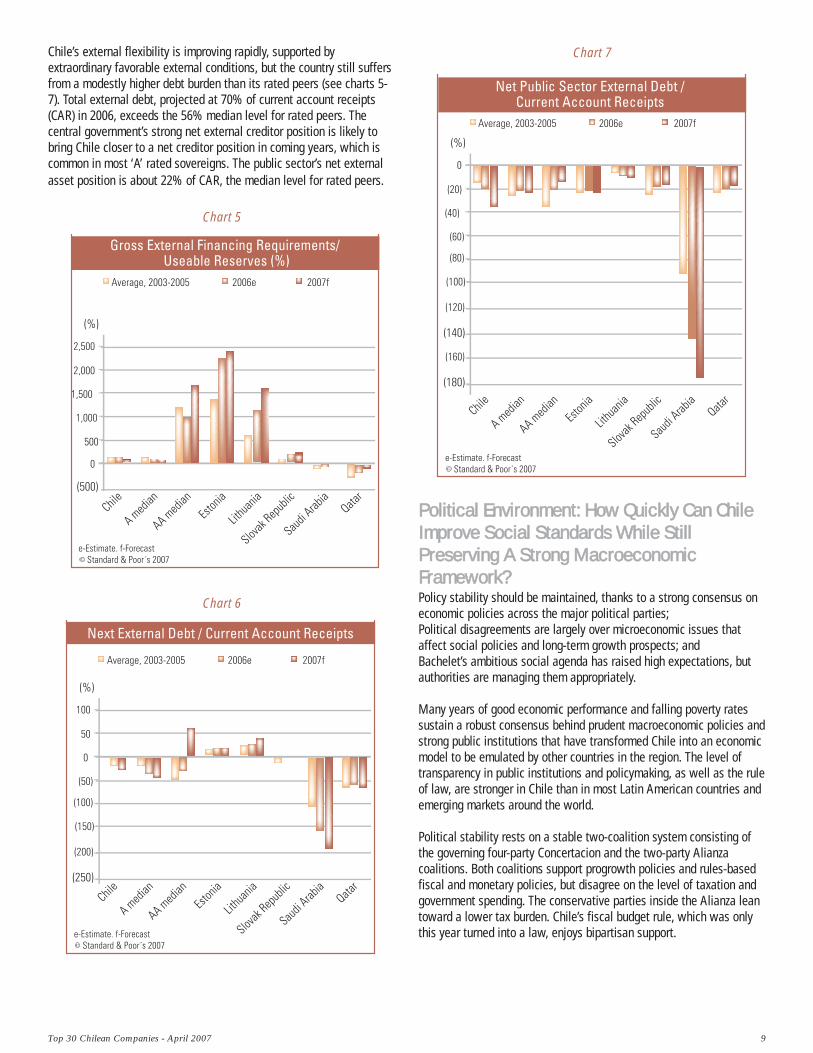

Chile’s external flexibility is improving rapidly, supported byextraordinary favorable external conditions, but the country still suffersfrom a modestly higher debt burden than its rated peers (see charts 5-7). Total external debt, projected at 70% of current account receipts(CAR) in 2006, exceeds the 56% median level for rated peers. Thecentral government’s strong net external creditor position is likely tobring Chile closer to a net creditor position in coming years, which iscommon in most ‘A’ rated sovereigns. The public sector’s net externalasset position is about 22% of CAR, the median level for rated peers.

Chart 5

Chart 6

Chart 7

PPoolliittiiccaall EEnnvviirroonnmmeenntt:: HHooww QQuuiicckkllyy CCaann CChhiilleeIImmpprroovvee SSoocciiaall SSttaannddaarrddss WWhhiillee SSttiillllPPrreesseerrvviinngg AA SSttrroonngg MMaaccrrooeeccoonnoommiiccFFrraammeewwoorrkk?? Policy stability should be maintained, thanks to a strong consensus oneconomic policies across the major political parties; Political disagreements are largely over microeconomic issues thataffect social policies and long-term growth prospects; and Bachelet’s ambitious social agenda has raised high expectations, butauthorities are managing them appropriately.

Many years of good economic performance and falling poverty ratessustain a robust consensus behind prudent macroeconomic policies andstrong public institutions that have transformed Chile into an economicmodel to be emulated by other countries in the region. The level oftransparency in public institutions and policymaking, as well as the ruleof law, are stronger in Chile than in most Latin American countries andemerging markets around the world.

Political stability rests on a stable two-coalition system consisting ofthe governing four-party Concertacion and the two-party Alianzacoalitions. Both coalitions support progrowth policies and rules-basedfiscal and monetary policies, but disagree on the level of taxation andgovernment spending. The conservative parties inside the Alianza leantoward a lower tax burden. Chile’s fiscal budget rule, which was onlythis year turned into a law, enjoys bipartisan support.

10 Top 30 Chilean Companies - April 2007

Table 2Economic Indicators

—Year ended Dec. 31— (%, unless otherwise indicated) 2008f 2007f 2006e 2005 2004 2003 2002 Nominal GDP (Bil. US$) 165.2 162.0 148.8 115.3 95.0 73.7 67.3 GDP per capita (US$) 9,859 9,759 9,054 7,083 5,906 4,629 4,271 Change in real GDP 5.0 5.0 4.2 6.4 6.2 3.9 2.2 Change in real GDP per capita 4.0 4.0 3.5 5.2 5.0 2.8 1.0 Change in real exports 4.0 6.0 5.9 6.1 11.8 6.5 1.6 Exports/GDP 38.2 43.1 43.7 41.8 40.8 36.6 34.0 Gross domestic investment/GDP 22.0 22.3 22.2 23.0 21.4 22.0 21.7 Domestic credit to private sector and NFPEs/GDP 69.0 69.0 69.0 69.2 65.7 64.8 65.0 Change in consumer price 3.0 3.0 3.0 3.1 1.1 2.8 2.5

e-Estimate. f-Forecast. NFPE-Nonfinancial public sector enterprises.

The 2005 presidential elections did not alter the course of economicpolicies. The election has focused on social issues, including education,health care, crime and jobs, as well as the need to increase spendingon research and development. Health and education reform will proveto be protracted, as higher spending in recent years has not resulted inthe expected better results.

Changes to the Constitution enacted in 2005 removed key clausesinserted by the previous military regime to constrain the power of thenew civilian governments that followed it, abolishing the posts of nineunelected senators starting in 2006, restoring the president’s power todismiss senior military leaders, and reducing the presidential term tofour years from six. These laws have maintained thus far the binominalsystem of elections in each constituency (the number of candidateselected by a party in a voting district is based upon voting thresholds),which has encouraged political parties to form coalitions and to seekconsensus.

The current Administration has given strong priority to an ambitioussocial agenda. High expectations created during the campaign and inthe first months after the elections led to social demonstrations, inparticular from high school students demanding better conditions andsubsidies. The government’s response to these pressures was areaffirmation of the strong premise that improvement in socialstandards (through increase expenditure and efficient) will have tooccur within margins that do not put at risk the strong macroeconomicframework that is a precondition to maintaining economic stability overthe medium and long term. Government authorities have raised thenotion of increasing the financing for a system of social protection, butonly in a sustainable way. This was well exemplified in 2006 by theapproval of the Fiscal Responsibility Law, which gives a more formalstatus to the structural fiscal surplus rule. Reaffirmation of the strongsupport for the fiscal rule is particularly important, given the strongfiscal surplus that Chile achieved in 2006 (of about 7.9% of GDP) in thecontext of still-very-strong social demands. Although there could bedisagreement on the dimension of the fiscal adjustment, even withinthe Concertacion Coalition, there is a strong consensus on the need tomaintain the fiscal rule.

The question remains how ambitious governments in Chile can be insetting a more dramatic adjustment to social conditions, given the

already-strong credentials the Chilean governments has onmacroeconomic stability. The fact that the Chilean government isrunning out of debt, in net terms, is probably one sign that a moreaggressive agenda could be implemented. Should a government in acountry at this stage of economic development be a strong net fiscalcreditor? The answer is probably no. However, other weaknesses, inparticular the still-high dependency on copper, highlights theimportance of very low debt levels to assure stability.

EEccoonnoommiicc PPrroossppeeccttss:: AA GGDDPP PPeerrffoorrmmaanncceeWWiitthh LLeessss VVoollaattiilliittyy

Medium-term growth prospects are favorable, with potential GDP continuing to expand; Macroeconomic stability should be sustained and enhanced by Chile’s ability to use countercyclical fiscal and monetary policies to smooth economic fluctuations; and The medium-term challenge will be to raise productivity and growththrough microeconomic policies, including creating a better-educated workforce.

Chile has been a model of economic reform, leading to a strong fiscalperformance, low inflation, and a sound financial system. Sound andconsistent economic policies have sustained high savings andproductivity growth rates, helping delink Chile’s economic performancefrom the more-volatile trajectory of most of its regional neighbors inrecent years. Chile has raised productivity by building on its base ofagricultural and natural resources, despite its long distance from mostof its export markets (see table 2). Table 2: Chile Economic Indicators Chile has done a better job than most commodity exporting countries inattaining macroeconomic stability despite export price fluctuations,thanks to rules-based fiscal and monetary policies. The combination ofa flexible exchange rate, a credible inflation-targeting monetary policyconducted by an independent central bank, a modest external debtburden, and open trade and capital accounts should sustain bothgrowth and macroeconomic stability in the coming years (see Chart 8).

Top 30 Chilean Companies - April 2007 11

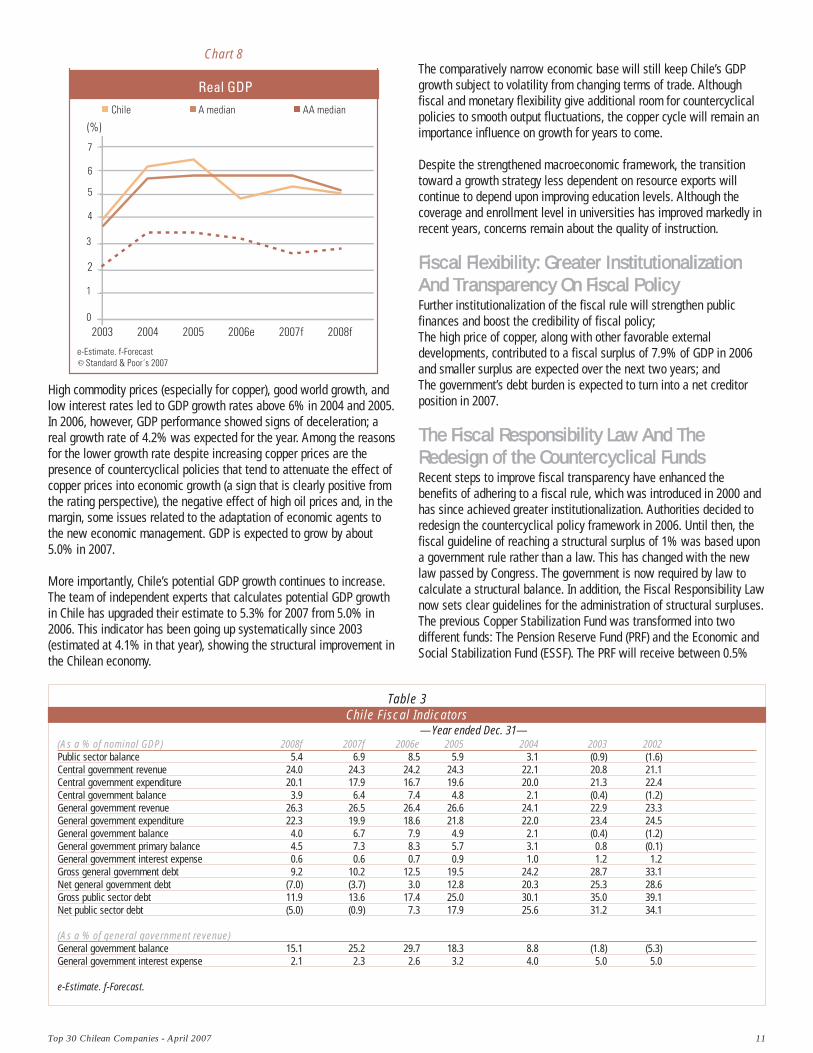

Chart 8

High commodity prices (especially for copper), good world growth, andlow interest rates led to GDP growth rates above 6% in 2004 and 2005.In 2006, however, GDP performance showed signs of deceleration; areal growth rate of 4.2% was expected for the year. Among the reasonsfor the lower growth rate despite increasing copper prices are thepresence of countercyclical policies that tend to attenuate the effect ofcopper prices into economic growth (a sign that is clearly positive fromthe rating perspective), the negative effect of high oil prices and, in themargin, some issues related to the adaptation of economic agents tothe new economic management. GDP is expected to grow by about5.0% in 2007.

More importantly, Chile’s potential GDP growth continues to increase.The team of independent experts that calculates potential GDP growthin Chile has upgraded their estimate to 5.3% for 2007 from 5.0% in2006. This indicator has been going up systematically since 2003(estimated at 4.1% in that year), showing the structural improvement inthe Chilean economy.

The comparatively narrow economic base will still keep Chile’s GDPgrowth subject to volatility from changing terms of trade. Althoughfiscal and monetary flexibility give additional room for countercyclicalpolicies to smooth output fluctuations, the copper cycle will remain animportance influence on growth for years to come.

Despite the strengthened macroeconomic framework, the transitiontoward a growth strategy less dependent on resource exports willcontinue to depend upon improving education levels. Although thecoverage and enrollment level in universities has improved markedly inrecent years, concerns remain about the quality of instruction.

FFiissccaall FFlleexxiibbiilliittyy:: GGrreeaatteerr IInnssttiittuuttiioonnaalliizzaattiioonnAAnndd TTrraannssppaarreennccyy OOnn FFiissccaall PPoolliiccyy Further institutionalization of the fiscal rule will strengthen publicfinances and boost the credibility of fiscal policy; The high price of copper, along with other favorable externaldevelopments, contributed to a fiscal surplus of 7.9% of GDP in 2006and smaller surplus are expected over the next two years; and The government’s debt burden is expected to turn into a net creditorposition in 2007.

TThhee FFiissccaall RReessppoonnssiibbiilliittyy LLaaww AAnndd TThheeRReeddeessiiggnn ooff tthhee CCoouunntteerrccyycclliiccaall FFuunnddssRecent steps to improve fiscal transparency have enhanced thebenefits of adhering to a fiscal rule, which was introduced in 2000 andhas since achieved greater institutionalization. Authorities decided toredesign the countercyclical policy framework in 2006. Until then, thefiscal guideline of reaching a structural surplus of 1% was based upona government rule rather than a law. This has changed with the newlaw passed by Congress. The government is now required by law tocalculate a structural balance. In addition, the Fiscal Responsibility Lawnow sets clear guidelines for the administration of structural surpluses.The previous Copper Stabilization Fund was transformed into twodifferent funds: The Pension Reserve Fund (PRF) and the Economic andSocial Stabilization Fund (ESSF). The PRF will receive between 0.5%

Table 3Chile Fiscal Indicators

—Year ended Dec. 31— (As a % of nominal GDP) 2008f 2007f 2006e 2005 2004 2003 2002 Public sector balance 5.4 6.9 8.5 5.9 3.1 (0.9) (1.6) Central government revenue 24.0 24.3 24.2 24.3 22.1 20.8 21.1 Central government expenditure 20.1 17.9 16.7 19.6 20.0 21.3 22.4 Central government balance 3.9 6.4 7.4 4.8 2.1 (0.4) (1.2) General government revenue 26.3 26.5 26.4 26.6 24.1 22.9 23.3 General government expenditure 22.3 19.9 18.6 21.8 22.0 23.4 24.5 General government balance 4.0 6.7 7.9 4.9 2.1 (0.4) (1.2) General government primary balance 4.5 7.3 8.3 5.7 3.1 0.8 (0.1) General government interest expense 0.6 0.6 0.7 0.9 1.0 1.2 1.2 Gross general government debt 9.2 10.2 12.5 19.5 24.2 28.7 33.1 Net general government debt (7.0) (3.7) 3.0 12.8 20.3 25.3 28.6 Gross public sector debt 11.9 13.6 17.4 25.0 30.1 35.0 39.1 Net public sector debt (5.0) (0.9) 7.3 17.9 25.6 31.2 34.1

(As a % of general government revenue)General government balance 15.1 25.2 29.7 18.3 8.8 (1.8) (5.3) General government interest expense 2.1 2.3 2.6 3.2 4.0 5.0 5.0

e-Estimate. f-Forecast.

12 Top 30 Chilean Companies - April 2007

used to cover future minimum pensions, as established by the proposedpension reform. The new scheme also provides the mechanism for theMinistry of Finance (although it is not obliged to) to capitalize thecentral bank with up to 0.5% of GDP per year over a five-year period.Lastly, resources exceeding an effective fiscal surplus of 1% of GDPwill be transferred to the recently created ESSF. These funds will onlybe available if copper prices fall below the long-term price of copperestimated by the committee of experts. By year-end 2006, PRF andESSF were expected to have accumulated US$600 million and US$ 6.6billion, respectively. Most of these assets are deposited outside Chile,a policy directed toward contributing to the stabilization of theexchange rate in Chile.

As mentioned above, even though the target of the structural surpluscalculation could vary in the future (its level is not determined by law),as some of the problems that justify the 1% are addressed (such as thepension or central bank issues), the strong commitment to a rule-basedfiscal policy is expected to remain.

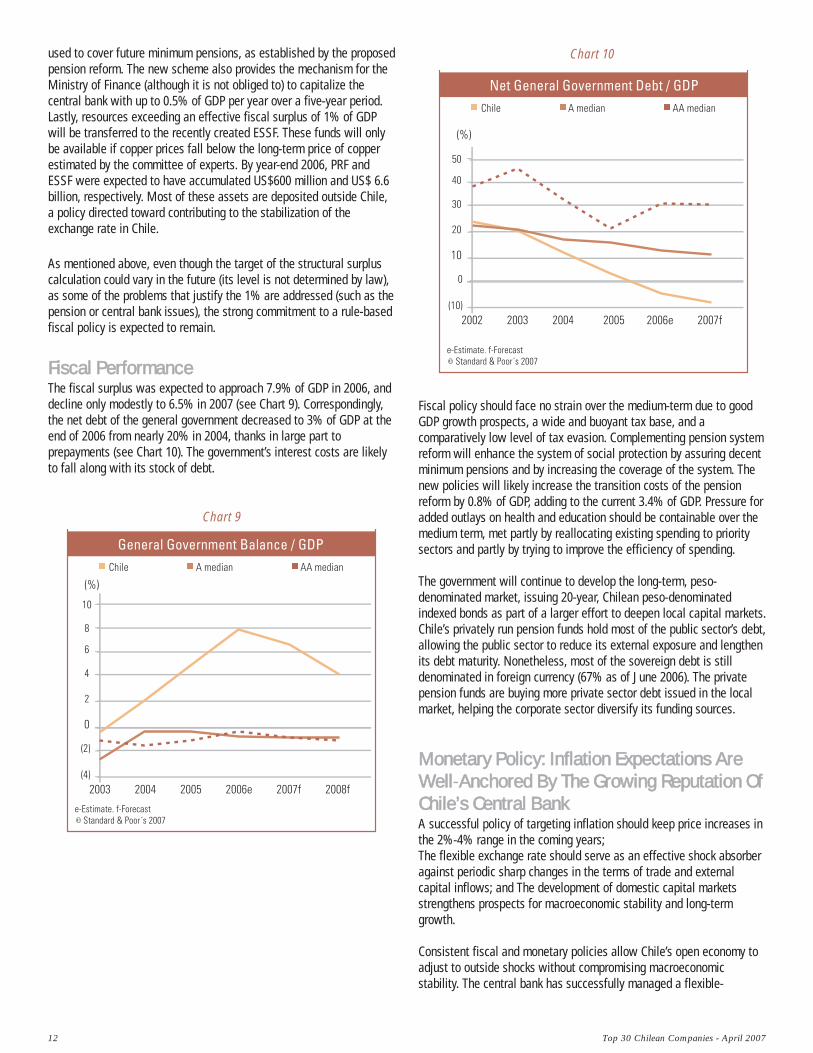

FFiissccaall PPeerrffoorrmmaanncceeThe fiscal surplus was expected to approach 7.9% of GDP in 2006, anddecline only modestly to 6.5% in 2007 (see Chart 9). Correspondingly,the net debt of the general government decreased to 3% of GDP at theend of 2006 from nearly 20% in 2004, thanks in large part toprepayments (see Chart 10). The government’s interest costs are likelyto fall along with its stock of debt.

Chart 9

Chart 10

Fiscal policy should face no strain over the medium-term due to goodGDP growth prospects, a wide and buoyant tax base, and acomparatively low level of tax evasion. Complementing pension systemreform will enhance the system of social protection by assuring decentminimum pensions and by increasing the coverage of the system. Thenew policies will likely increase the transition costs of the pensionreform by 0.8% of GDP, adding to the current 3.4% of GDP. Pressure foradded outlays on health and education should be containable over themedium term, met partly by reallocating existing spending to prioritysectors and partly by trying to improve the efficiency of spending.

The government will continue to develop the long-term, peso-denominated market, issuing 20-year, Chilean peso-denominatedindexed bonds as part of a larger effort to deepen local capital markets.Chile’s privately run pension funds hold most of the public sector’s debt,allowing the public sector to reduce its external exposure and lengthenits debt maturity. Nonetheless, most of the sovereign debt is stilldenominated in foreign currency (67% as of June 2006). The privatepension funds are buying more private sector debt issued in the localmarket, helping the corporate sector diversify its funding sources.

MMoonneettaarryy PPoolliiccyy:: IInnffllaattiioonn EExxppeeccttaattiioonnss AArreeWWeellll-AAnncchhoorreedd BByy TThhee GGrroowwiinngg RReeppuuttaattiioonn OOffCChhiillee’’ss CCeennttrraall BBaannkk A successful policy of targeting inflation should keep price increases inthe 2%-4% range in the coming years; The flexible exchange rate should serve as an effective shock absorberagainst periodic sharp changes in the terms of trade and externalcapital inflows; and The development of domestic capital marketsstrengthens prospects for macroeconomic stability and long-termgrowth.

Consistent fiscal and monetary policies allow Chile’s open economy toadjust to outside shocks without compromising macroeconomicstability. The central bank has successfully managed a flexible-

Top 30 Chilean Companies - April 2007 13

exchange-rate and inflation-targeting policy. The authorities wereable to adopt a countercyclical monetary stance in recent yearswithout jeopardizing inflation targets.

The credibility of the central bank helps dampen the level of pass-through from recent exchange rate changes. Inflation has been justabout 3% over the past four years, and its volatility declined whilethe currency has been floating. High oil prices and rising powertariffs contributed to inflationary pressure in 2005 and 2006. Thisled the central bank to withdraw monetary stimulus beginning inSeptember 2004, raising its overnight policy rate to containdemand. However, deceleration in economic activity in mid 2006interrupted the pace of interest rates hikes in August 2006, leavingthe reference interest rate at 5.25% as of December 2006.

The central bank has become more transparent in its operationsand has not intervened in the foreign exchange market in recentyears, allowing the market to set the exchange rate. Politicalpressure from exporters to staunch the recent appreciation of thecurrency against the U.S. dollar has not resulted in any officialintervention in the foreign exchange market.

The bank often runs a quasi-fiscal deficit, partly due to the legacyof commercial bank bailouts nearly two decades ago. Itspreponderance of assets is in dollars, but liabilities in pesos,renders its net worth vulnerable to exchange-rate changes. Thegovernment is currently addressing this weakness by anticipatingsome debt payments to the monetary authority and capitalizing thecentral bank. Such steps would improve the bank’s balance sheet,bringing it into line with central banks in other highly ratedsovereigns.

The Chilean banking system remains strong thanks to a soundregulatory framework and the country’s reduced economicvolatility. The positive economic environment resulted in thebanking system’s continued growth during 2006, maintainingstrong asset quality indicators and adequate capitalization levels.Asset quality indicators were reduced to unprecedented levels,with the nonperforming loans-to-total-loans ratio at 0.8% as of

Sept. 30, 2006. Despite the system’s assets growth, capitalizationremained adequate at 12.8%. Although profitability margins have beenunder pressure given increasing competition (with a return on averageassets at 1.37% during the last 12 months, as of Sept. 30, 2006), bankshave been able to gradually improve profitability thanks to increasingparticipation in higher-yielding segments and better operatingefficiencies. In the short to medium term, Standard & Poor’s expectsthe Chilean financial system to continue to benefit from the country’spositive economic and social perspectives.

The country’s long-term debt markets are growing, with theintroduction recently of 30-year mortgages. The government’s issuanceof new 10-, five-, and two-year indexed peso debt in 2006 will continueto allow it to gradually replace dollar-denominated sovereign debt wasissued to the central bank to provide support during an earlier bankingcrisis. The step will strengthen the local yield curve and graduallyreduce the currency mismatch that affects the central bank’s balancesheet.

EExxtteerrnnaall FFiinnaanncceess:: FFaavvoorraabbllee EExxtteerrnnaallCCoonnddiittiioonnss HHaavvee RReessuulltteedd IInn AA MMaajjoorrAAddjjuussttmmeenntt A flexible exchange rate, investor confidence, and an open tradingregime augur well for external flexibility; The current account balance is likely to remain in a surplus in 2007 and2008, thanks to booming export revenue; and Chile’s gross external debt burden is likely to remain stable or declinemodestly (at best) in coming years, but external assets should rise as itincreasingly integrates with international financial markets.

As a small, open economy, Chile is more prone to volatility in the faceof exogenous shocks than most member countries of the Organizationfor Economic Co-operation and Development. However, the country’sability to absorb the impact of external shock is likely to strengthenover time thanks to monetary flexibility, a rules-based fiscal policy, andcapital market development.

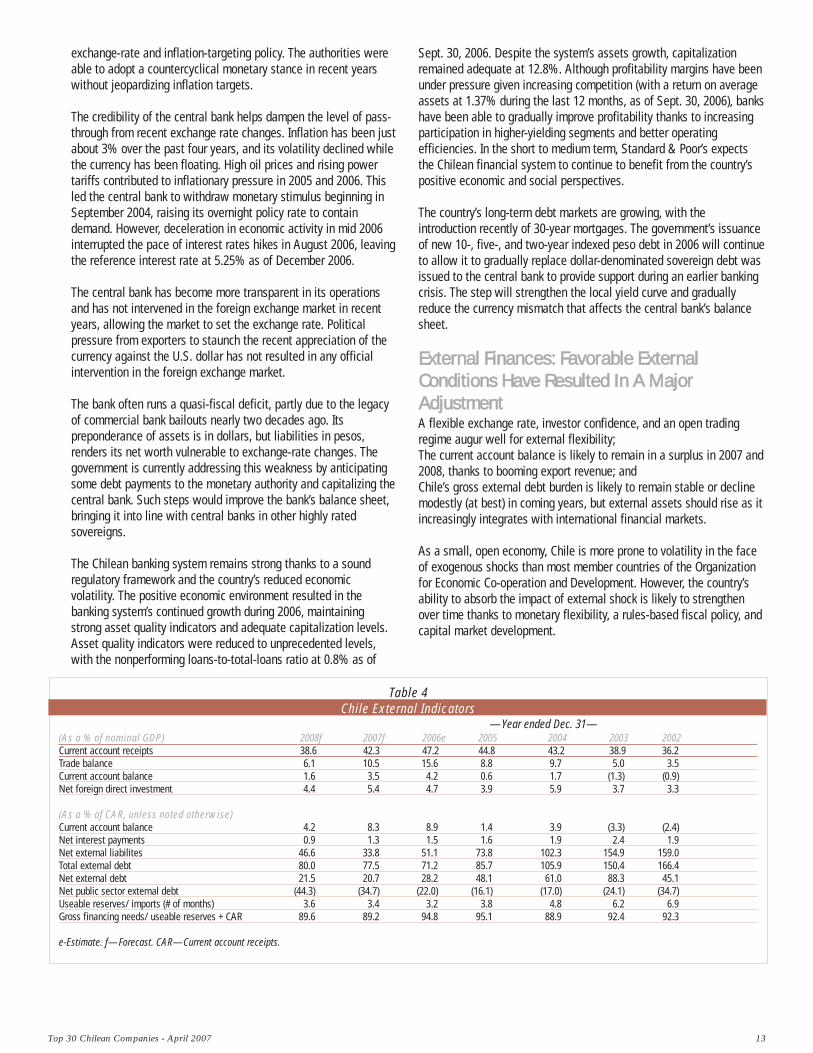

Table 4Chile External Indicators

—Year ended Dec. 31— (As a % of nominal GDP) 2008f 2007f 2006e 2005 2004 2003 2002 Current account receipts 38.6 42.3 47.2 44.8 43.2 38.9 36.2 Trade balance 6.1 10.5 15.6 8.8 9.7 5.0 3.5 Current account balance 1.6 3.5 4.2 0.6 1.7 (1.3) (0.9) Net foreign direct investment 4.4 5.4 4.7 3.9 5.9 3.7 3.3

(As a % of CAR, unless noted otherwise)Current account balance 4.2 8.3 8.9 1.4 3.9 (3.3) (2.4) Net interest payments 0.9 1.3 1.5 1.6 1.9 2.4 1.9 Net external liabilites 46.6 33.8 51.1 73.8 102.3 154.9 159.0 Total external debt 80.0 77.5 71.2 85.7 105.9 150.4 166.4 Net external debt 21.5 20.7 28.2 48.1 61.0 88.3 45.1 Net public sector external debt (44.3) (34.7) (22.0) (16.1) (17.0) (24.1) (34.7) Useable reserves/ imports (# of months) 3.6 3.4 3.2 3.8 4.8 6.2 6.9 Gross financing needs/ useable reserves + CAR 89.6 89.2 94.8 95.1 88.9 92.4 92.3

e-Estimate. f—Forecast. CAR—Current account receipts.

14 Top 30 Chilean Companies - April 2007

After several years of deficits, Chile’s current account balance swungsharply into a 1.7% of GDP surplus thanks to a more than 20%improvement in the country’s terms of trade in 2004. The 2005 currentaccount surplus declined to a 0.6% of GDP due to rising imports of oiland capital goods. The rise in the price of copper (which constitutedabout 50% of total exports in 2005 and 2006) outweighs the negativeimpact of higher oil prices on Chile’s external balance and led to astrong current account surplus in 2006, estimated in 4.2% of GDP.Manufactured and other noncommodity exports are also growing welldespite the nominal appreciation of the peso, auguring well for long-term export prospects when copper prices fall.

Chile is likely to enjoy a declining, but still substantial, trade surplus(about 5% of GDP) in the coming years, as copper prices return to moremoderate levels in 2008 and beyond.

About two-thirds of Chile’s exports now enter external markets undersome form of preferential access, and the country’s own effective tariffrate is about 3%. Chile has free-trade agreements with the U.S. andthe European Union, as well as with many countries in the WesternHemisphere and Asia. Growing commodity demand in Asia, especiallyin China, is shifting the direction of Chilean trade, making itincreasingly a Pacific-oriented economy.

Fiscal surpluses and current account surpluses have reduced thecountry’s external debt burden, with the government prepaying some ofits external debt. Total external debt is likely to reach 70% of CAR in2006, compared with 166% in 2002. The central government is likely toremain a net external creditor over the coming years, while the bankingand corporate sectors continue to reduce their net external debtorposition—supported by favorable external conditions, among otherthings.

The risk posed to the sovereign from nonsovereign external debt islikely less than indicated by the numbers alone. For example, more thanone-half of the nonbank private sector’s external debt is owed byforeign enterprises located in Chile, and about 15% of that is owed toparents or related companies abroad, giving it the quality of foreigndirect investment (FDI). More than half of Chile’s external debt is atfixed interest rates, reducing the shock of an eventual rise in globalinterest rates. Furthermore, the growing use of currency forwardsfurther reduces the risk of exchange-rate changes for nonbank privatesector external debt.

Chile’s external assets and liabilities have been growing more thantwice as fast as GDP in recent years as the country integrates withinternational capital markets, complementing its growing trade links.External assets are likely to increase due to growing investmentoverseas by private sector pension funds, which can invest up to 30%of their money abroad, as well as due to outward FDI.

(For additional ratings history, see “Sovereign Ratings HistorySince 1975,” available on RatingsDirect.)

Ratings Detail (As Of 09-Feb-2007)*

Chile (Republic of)

Sovereign Credit RatingForeign Currency A/Positive/A-1Local Currency AA/Stable/A-1+

Senior UnsecuredForeign Currency ALocal Currency AA

Short-Term DebtLocal Currency A-1+

Sovereign Credit Ratings History14-Dec-2006 Foreign Currency A/Positive/A-114-Jan-2004 A/Stable/A-116-Apr-2002 A-/Positive/A-107-Aug-1997 Local Currency AA/Stable/A-1+

30-Nov-1992 AA/Stable/--

Default HistoryForeign currency bank debt, 1983-1990

Population 16.4 million Per Capita GDP US$9,000

Current GovernmentPresidential government headed by Michelle Bachelet of the Concertacion coalition.

Election SchedulePresidential Last: December 2005 Next: December 2009

*Unless otherwise noted, all ratings in this report are global scale ratings. Standard &Poor's credit ratings on the global scale are comparable across countries. Standard &Poor's credit ratings on a national scale are relative to obligors or obligations withinthat specific country.

Top 30 Chilean Companies - April 2007 15

Two major subjects seem to dominate the economic debate on theRepublic of Chile (A/Positive/A-1 foreign currency sovereign creditratings). First, economic growth was lower than expected in 2006, withGDP growth reaching 4.2%. Second, a strong fiscal performance basedupon a structural fiscal surplus rule, with the general governmentsurplus reaching 7.9% of GDP in 2006, is transforming the Chileangovernment into a net fiscal creditor (government assets exceedingfinancial liabilities).

This commentary examines these two issues from a ratingsperspective, and highlights their respective relevance in the context ofthe positive outlook Standard & Poor’s Ratings Services assigned toChile’s foreign current rating on Dec. 14, 2006.

CChhiillee’’ss RRaattiinnggss BBaacckkggrroouunndd The benefits of the Chilean economic model are already well proven.Chile doubled its GDP per capita over the last 10 years, and its ‘A’ long-term foreign currency rating is not only the highest rating in LatinAmerica but one of the highest among emerging market economies.Chile’s upward rating performance is illustrated in table 1. Standard &Poor’s December 2006 revision of its outlook acknowledges structuralimprovements in both the economy and the policymaking process andthe excellent prospects for Chile’s economy over the medium term.

EEccoonnoommiicc GGrroowwtthh:: SShhoouulldd LLoowweerr GGrroowwtthh BBee AACCoonncceerrnn?? Chile’s 4.2% GDP growth in 2006 caused a large degree of localdisappointment. The reasons behind this are clear when reviewingmarket expectations at the beginning of 2006. According to theInflation Report published in January 2006, the Chilean central bankwas working under a base-case scenario for the year that assumed aprice for copper of US$1.70 per pound and, correspondingly, a negativeterms-of-trade shock (a measure of the variation of export and importprices) of 4.4%. These parameters led at the time to a GDP growthforecast of between 5.25% and 6.25% for 2006. A year later, contraryto what was expected, a review of the economy in 2006 shows that the

price of copper was US$3.05 per pound and Chile faced a positiveterms-of-trade shock of 30.1%. Notwithstanding the overwhelminglybetter external scenario, growth was significantly below the originalrange.

A variety of explanations justify this underperformance, and theimportance of each depends upon the presenter. The list includes a) thestrengthening of countercyclical fiscal and monetary policies that helpdecelerate economic growth in periods of high copper prices, b)increasing energy prices, with both high oil prices (Chile imports 100%of its oil resources and the price of oil in 2006 was 16% higher thanexpected by the central bank) and less availability of gas fromArgentina, and c) moderate pessimism domestically on the ability ofthe current administration to deliver economic growth.

From a ratings perspective, however, this performance is notnecessarily bad news. One of the major credit strengths of higher-ratedgovernments is the stability of their growth performance. The wholepurpose of countercyclical policies—which Standard & Poor’semphasize in the case of Chile as not only one of its major creditstrengths, but also as a model for other emerging markets—is theircontribution toward detaching economic performance from theevolution of copper prices. Standard & Poor’s recognizes that thepresence of countercyclical policies is not the only factor explainingChile’s lower economic growth in 2006. However, their strength is oneof the critical rating factors supporting both the current positive outlookon the rating and the chance that Chile will continue its climb up therating scale.

Chile is a medium income country. Its estimated GDP per capita ofabout US$9,700 for 2007 still ranks significantly below the ‘A’ median’sUS$16,000. Achieving higher levels of wealth over time will naturallyhave an impact on the rating. However, the sustainability of economicgrowth at reasonable levels over a long period of time seems moreimportant from a ratings perspective at this point. A stable economicgrowth pattern is particular relevant in Chile, whose economy is stilldependent upon commodities. Continuing to sterilize the effect of thenatural business cycle of commodities prices into the Chilean economyconstitutes a major credit strength. Although growing at lower ratesmight not be politically compelling when the price of copper is aboveits long-term level, the real test will come when the price of the metaldrops below the long-term price estimate and Chile uses itscountercyclical policies to boost economic growth.

Although Chile has economically detached itself from the rest of LatinAmerica in many areas (as the ratings show), it still shares with therest of the region a past of economic volatility. Growing fast has notbeen a major obstacle in Chile’s recent economic history. In the fourdecades before the recent global economic recovery in 2002 (most

Chile’s EEconomic GGrowth AAnd FFiscal PPosition: HHowImportant AAre TThey FFrom AA RRatings PPerspective?

Table 1Chile Foreign Currency Rating

Date To Dec. 14, 2006 A/Positive/A-1Jan, 14, 2004 A/Stable/A-1April 16, 2002 A-/Positive/A-1Aug. 7, 1997 A-/Stable/A-1July 11, 1995 A-/Stable/—Dec. 21, 1993 BBB+/Stable/—Aug. 17, 1992 BBB/Stable/—

Sebastian Briozzo, Buenos Aires (54) 11 4891 2120; [email protected] ; Joydeep Mukherji, New York (1) 212-438-7351; [email protected]

16 Top 30 Chilean Companies - April 2007

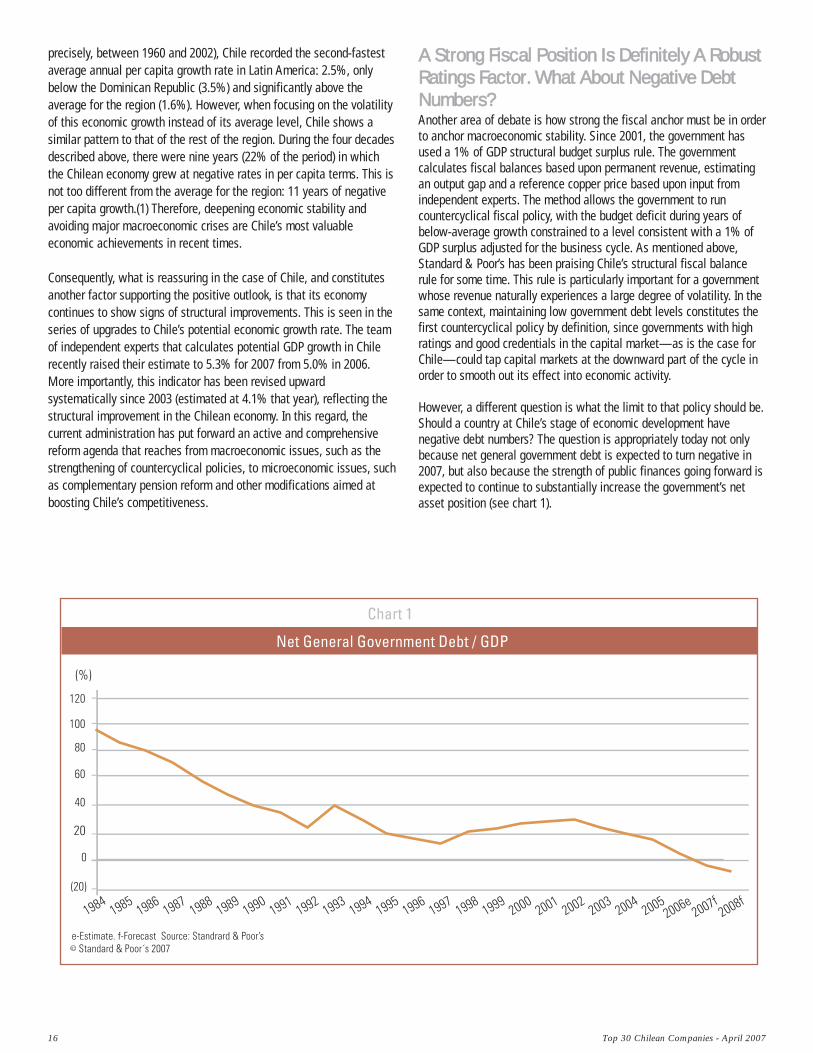

AA SSttrroonngg FFiissccaall PPoossiittiioonn IIss DDeeffiinniitteellyy AA RRoobbuussttRRaattiinnggss FFaaccttoorr.. WWhhaatt AAbboouutt NNeeggaattiivvee DDeebbttNNuummbbeerrss?? Another area of debate is how strong the fiscal anchor must be in orderto anchor macroeconomic stability. Since 2001, the government hasused a 1% of GDP structural budget surplus rule. The governmentcalculates fiscal balances based upon permanent revenue, estimatingan output gap and a reference copper price based upon input fromindependent experts. The method allows the government to runcountercyclical fiscal policy, with the budget deficit during years ofbelow-average growth constrained to a level consistent with a 1% ofGDP surplus adjusted for the business cycle. As mentioned above,Standard & Poor’s has been praising Chile’s structural fiscal balancerule for some time. This rule is particularly important for a governmentwhose revenue naturally experiences a large degree of volatility. In thesame context, maintaining low government debt levels constitutes thefirst countercyclical policy by definition, since governments with highratings and good credentials in the capital market—as is the case forChile—could tap capital markets at the downward part of the cycle inorder to smooth out its effect into economic activity.

However, a different question is what the limit to that policy should be.Should a country at Chile’s stage of economic development havenegative debt numbers? The question is appropriately today not onlybecause net general government debt is expected to turn negative in2007, but also because the strength of public finances going forward isexpected to continue to substantially increase the government’s netasset position (see chart 1).

precisely, between 1960 and 2002), Chile recorded the second-fastestaverage annual per capita growth rate in Latin America: 2.5%, onlybelow the Dominican Republic (3.5%) and significantly above theaverage for the region (1.6%). However, when focusing on the volatilityof this economic growth instead of its average level, Chile shows asimilar pattern to that of the rest of the region. During the four decadesdescribed above, there were nine years (22% of the period) in whichthe Chilean economy grew at negative rates in per capita terms. This isnot too different from the average for the region: 11 years of negativeper capita growth.(1) Therefore, deepening economic stability andavoiding major macroeconomic crises are Chile’s most valuableeconomic achievements in recent times.

Consequently, what is reassuring in the case of Chile, and constitutesanother factor supporting the positive outlook, is that its economycontinues to show signs of structural improvements. This is seen in theseries of upgrades to Chile’s potential economic growth rate. The teamof independent experts that calculates potential GDP growth in Chilerecently raised their estimate to 5.3% for 2007 from 5.0% in 2006.More importantly, this indicator has been revised upwardsystematically since 2003 (estimated at 4.1% that year), reflecting thestructural improvement in the Chilean economy. In this regard, thecurrent administration has put forward an active and comprehensivereform agenda that reaches from macroeconomic issues, such as thestrengthening of countercyclical policies, to microeconomic issues, suchas complementary pension reform and other modifications aimed atboosting Chile’s competitiveness.

Top 30 Chilean Companies - April 2007 17

interesting analytical exercise to have a better sense of theimportance of this phenomenon in Chile is to compare its debt ratios tothose of other countries of the world. Out of the 113 sovereigngovernments currently rated by Standard & Poor’s, only 25 are expectedto reach negative debt numbers by the end of 2007. Those sovereigns,along with their net general government debt to GDP ratio, GDP percapita, and ratings are presented in table 2.

As can be seen in the table, most of the countries are either majorfinancial centers or large commodity producers, in particular oilproducers. All the governments on the list (with the exception ofVenezuela) are rated within the investment-grade category, whichseems reasonable given that the rating is an assessment on thecapacity (but also willingness) to repay debt, which in all thesecountries is very low in absolute terms. However, one interestingcharacteristic is that most of the countries in the list are high incomeeconomies. In fact, ranking the countries by GDP per capita will locateChile as the fifth less-wealthy country on the list. In addition, Chile hassignificantly less debt than the ‘A’ median (at 14.7% of GDP for 2007)and about half the GDP per capita.

Therefore, from a purely creditworthiness perspective, Chile’s ratingscould continue their upward trend over the medium term, even withhigher debt levels, as long as consistent and rule-based fiscal policyimplementation continues. This already-strong commitment wasenhanced in 2006 by the approval of the Fiscal Responsibility Law,which established a formal legal framework and requirement for thecalculation of the structural fiscal balance (although it does not set atarget). Standard & Poor’s does not necessarily expect a government atChile’s stage of development to maintain negative debt numbers.

There is a rationale behind Chile’s 1% structural surplus target. Theidea is that the government has to maintain savings over the mediumterm to deal with three major sources of spending pressure:

Future minimum pension liabilities, The capitalization of the central bank, and Potential liabilities resulting from the fact that most of Chile’s debt

is denominated in foreign currency.

As Chilean administrations continue to address each of these issuesand fiscal surpluses continue to boost government assets, there couldbe less justification for the current target in the future.

TThhee RRaattiioonnaallee BBeehhiinndd CChhiillee’’ss PPoossiittiivvee OOuuttllooookk As mentioned above, Standard & Poor’s revised its outlook on Chile’slong-term foreign currency rating to positive last December. Therefore,what would take for the positive outlook to lead to an upgrade? At highlevels of creditworthiness, such as currently exist in Chile, ratingchanges do not generally depend upon one specific rating factor or thechange in one single variable. Standard & Poor’s positive outlook onChile is therefore based upon the expectation that the country’salready-strong macroeconomic framework will continue to graduallystrengthen, bringing additional stability to GDP performance over themedium and long term in line with that of higher-rated credits.Government efforts to address pending issues, in particular on thepension front, will continue to diminish the risk the Chilean economywill face over the medium term, bringing additional signs ofpredictability to Chile’s medium- and long-term economic prospects.The continuation of the current economic policy set, combined with thestrong results in the economic, fiscal, and external indicators—even inthe case of a expected decrease in copper prices to more moderatelevels (albeit still high by historical standards)—could eventually leadto a rating upgrade.

Notes (1) According to data published by the Economic Commissionfor Latin America and the Caribbean.

Table 2Negative Debt And GDP Per Capita, 2007 Forecast

Long-term foreign Net general governmet GDP per currency rating debt (% of GDP) capita

(US$) Liechtenstein AAA (97.6) 113,323 Luxembourg AAA (31.8) 99,558 Bermuda AA (21.3) 84,873 Norway AAA (130.6) 74,831 Qatar A+ (66.1) 65,450 Sweden AAA (1.6) 47,734 Finland AAA (12.6) 44,203 Isle of Man AAA (44.9) 42,091 Andorra AA (15.6) 41,383 Australia AAA (3.3) 35,864 Singapore AAA (105.4) 30,717 Kuwait A+ (234.4) 29,872 Hong Kong AA (17.9) 28,323 New Zealand AA+ (0.4) 25,550 Bahrain A (58.2) 21,226 Trinidad and Tobago A- (5.9) 16,253 Oman A- (93.6) 14,879 Estonia A (6.2) 13,587 Saudi Arabia A+ (61.6) 11,540 Montserrat BBB- (23.3) 9,841 Chile A (3.7) 9,759 Venezuela BB- (5.2) 8,363 Russia BBB+ (6.6) 7,809 Botswana A (15.8) 6,354 Kazakhstan BBB (15.3) 5,794 AA median 30.1 32,167 A median 14.7 16,076 Source: Standard & Poor’s.

18 Top 30 Chilean Companies - April 2007

2007’s TTop 55 CCredit FFactors FFor CCorporate CCredit QQualityIn CChile

Chile’s solid economic performance, stable indicators, and reliableinstitutional framework have shaped the country’s corporate sectorduring the past decade. The fate of most major corporations is tied tothe changes in the global economy, especially the evolution ofcommodities in general and copper, in particular. Nevertheless, prudentfinancial policies and cash management as well as good access tocredit have allowed most players to grow and withstand externalshocks, while maintaining their strong creditworthiness through thecycle.

These characteristics are, of course, reflected in the rating profile ofChilean corporations. Of the 32 corporates in Chile that Standard &Poor’s Ratings Services rates, 84% are rated at the investment-gradelevel (‘BBB-’ and above) and 89% have stable outlooks. This indicatesour expectations that these entities will continue to maintain credithealth, even under softening GDP growth and commodity prices.

WWhhaatt ffaaccttoorrss wwiillll bbee mmoorree rreelleevvaanntt ffoorr ccrreeddiittqquuaalliittyy iinn 22000077?? Strong commodity pricesCommodity prices are key determinants of financial performance for alarge part of Chile’s corporate sector (mainly copper and forestproducts). While the pricing environment could become less favorablein 2007, we expect prices to remain above historical averages,sustaining the good performance of companies such as Codelco,Escondida, Arauco, and CMPC. Copper prices will probably weaken tolevels closer to an average of $2.30 per pound in 2007 (after $3.05 perpound in 2006), allowing copper producers to continue generatingsignificant amounts of operating cash flow, but also to pursueaggressive expansion plans that should consume a large portion ofcash generation. In the forest product segment, we expect animprovement in credit metrics as large investments from the the pasttwo years start generating cash in a continually rising priceenvironment. Pulp and paper companies should continue benefitingfrom rising margins, stemming from production cost advantages; thefirm, worldwide demand for pulp; and the more regional demand forpaper products. Furthermore, international pulp and paper prices arelikely to remain high due to capacity closures in North America.

Sustained (albeit lower than anticipated) economicgrowth and macroeconomic stabilityGDP grew about 4.2% in 2006. This level of growth was disappointingfor many market participants when compared to the initial consensusforecast of 5%-6% for 2006. Nevertheless, consumption grew to morethan 7%, while inflation remained under control, which is a beneficialcombination for companies targeting the domestic market. The telecomand bottler sectors benefited from positive consumption fundamentals,with growth rates that, in many cases, significantly exceeded GDPrates. The mobile phone sector grew by about 20% in 2006, (compared

Marta Castelli, Buenos Aires (54) 114-891-2128; [email protected]

to 2005) reaching about 80% penetration. In addition, beer volumesales increased by about 15% in 2006 (compared to 2005). Sales in thejuice, purified water and, functional drinks segment also increased.While we usually use conservative growth estimates for long-termprojections, we expect the corporate sector to continue enjoying astrong domestic demand in 2007 and probably 2008.

Increasing energy costsTwo elements have deeply affected energy costs in Chile in the pastthree years: the reduction in exports of natural gas from Argentina andthe spike in oil prices. While the increase in oil prices may causetemporary disruptions, increasing natural gas shortages have required astructural change in Chile’s energy policies geared to ensure thereliability of power supply. On the positive side, the governmentreacted quickly, and modified the regulatory framework to recognize thenew cost of power generation and to encourage sizable investments inboth hydro and coal power plants, which should lead to the growth anddiversification of the country’s generation capacity. On the other hand,the resulting increase in reliability was accompanied by an increase inenergy costs, compounded, in the past two years, by the prevalent highprices for crude oil. As energy is such a basic input, the increase inprices has impacted margins throughout the economy and temperedprofitability increases.

A strong Chilean PesoGiven the relatively small domestic market and Chile’s comparativeadvantage in the production of commodities, including copper andforest products, the performance of the external sector is a key elementfor corporate credit quality. More specifically, the appreciation ordevaluation of the peso directly affects operating margins and debtservice requirements, especially when there is a currency mismatchbetween costs and revenues. In this regard, the strong revaluation ofthe Chilean peso (CHP) against the U.S. dollar during the past fouryears (CHP534.43/$1 at the close of 2006 vs. CHP712.38/$1 at the endof 2002) has affected the cost structure of several companies,benefiting some and hurting others. While the revaluation against thedollar raises questions on the potential loss of competition amongChilean exports, the effect is not so clear when analyzing the realeffective exchange rate, which incorporates the variation of the peso inreal terms, versus the currencies of the countries with which Chiletrades. We expect the peso to remain strong in 2007; however, thefactor’s final effect will vary significantly from corporate to corporate.

Refinancing riskIn general, refinancing risk is not a significant concern for rated Chileancorporates in the short to medium term. Many of the largest entitiesrefinance maturities well in advance as a matter of policy. We expectthat trend to continue, especially considering the current liquidity of theworld’s capital markets. These factors, as well as other industry and company specific risks, will

Top 30 Chilean Companies - April 2007 19

have a different impact on specific credits. Other factors to monitorinclude capital expenditures (capex), maturity of past investments,regulations, dividends, and the like. For the mining sector, capex willremain a relevant variable since we expect high prices to continue tofoster expansion capacity. In the pulp and paper sector, we will monitorthe companies’ ability increase free cash flow and to deleverage. Fortelecom companies, we will pay close attention to the evolution ofoverall competition, regulations, and substitution effects in the fixedsegment, while competitive and margin pressures will be key forbottlers.

20 Top 30 Chilean Companies - April 2007

Chilean BBanks LLook TTo IImprove OOn 22006 PPerformanceIn 22007

The extent of a country’s economic development goes hand in handwith the depth of its financial system. This is particularly true in thecase of Chile. Although extremely favorable macroeconomic conditionsacross Latin America have been accompanied by positive performancein most Latin American financial systems, the underlying strength ofthe Chilean system remains unparalleled throughout the region.

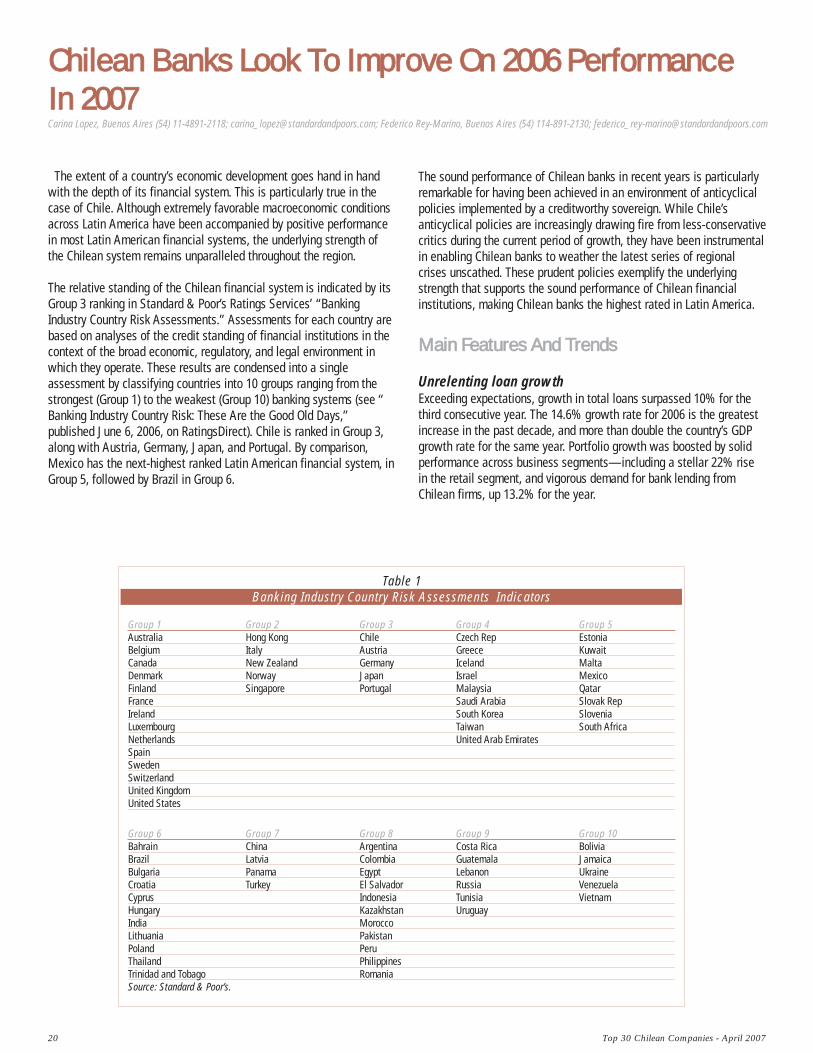

The relative standing of the Chilean financial system is indicated by itsGroup 3 ranking in Standard & Poor’s Ratings Services’ “BankingIndustry Country Risk Assessments.” Assessments for each country arebased on analyses of the credit standing of financial institutions in thecontext of the broad economic, regulatory, and legal environment inwhich they operate. These results are condensed into a singleassessment by classifying countries into 10 groups ranging from thestrongest (Group 1) to the weakest (Group 10) banking systems (see “Banking Industry Country Risk: These Are the Good Old Days,”published June 6, 2006, on RatingsDirect). Chile is ranked in Group 3,along with Austria, Germany, Japan, and Portugal. By comparison,Mexico has the next-highest ranked Latin American financial system, inGroup 5, followed by Brazil in Group 6.

The sound performance of Chilean banks in recent years is particularlyremarkable for having been achieved in an environment of anticyclicalpolicies implemented by a creditworthy sovereign. While Chile’santicyclical policies are increasingly drawing fire from less-conservativecritics during the current period of growth, they have been instrumentalin enabling Chilean banks to weather the latest series of regionalcrises unscathed. These prudent policies exemplify the underlyingstrength that supports the sound performance of Chilean financialinstitutions, making Chilean banks the highest rated in Latin America.

MMaaiinn FFeeaattuurreess AAnndd TTrreennddss

Unrelenting loan growthExceeding expectations, growth in total loans surpassed 10% for thethird consecutive year. The 14.6% growth rate for 2006 is the greatestincrease in the past decade, and more than double the country’s GDPgrowth rate for the same year. Portfolio growth was boosted by solidperformance across business segments—including a stellar 22% risein the retail segment, and vigorous demand for bank lending fromChilean firms, up 13.2% for the year.

Table 1Banking Industry Country Risk Assessments Indicators

Group 1 Group 2 Group 3 Group 4 Group 5 Australia Hong Kong Chile Czech Rep Estonia Belgium Italy Austria Greece Kuwait Canada New Zealand Germany Iceland Malta Denmark Norway Japan Israel Mexico Finland Singapore Portugal Malaysia Qatar France Saudi Arabia Slovak Rep Ireland South Korea Slovenia Luxembourg Taiwan South Africa Netherlands United Arab Emirates Spain Sweden Switzerland United Kingdom United States

Group 6 Group 7 Group 8 Group 9 Group 10 Bahrain China Argentina Costa Rica Bolivia Brazil Latvia Colombia Guatemala Jamaica Bulgaria Panama Egypt Lebanon Ukraine Croatia Turkey El Salvador Russia Venezuela Cyprus Indonesia Tunisia Vietnam Hungary Kazakhstan Uruguay India Morocco Lithuania Pakistan Poland Peru Thailand Philippines Trinidad and Tobago Romania Source: Standard & Poor’s.

Carina Lopez, Buenos Aires (54) 11-4891-2118; [email protected]; Federico Rey-Marino, Buenos Aires (54) 114-891-2130; [email protected]

Top 30 Chilean Companies - April 2007 21

Growth in lending to companies is especially good news given thetrend toward disintermediation among large corporations. Increasingly,big companies are tapping local and cross-border capital marketsdirectly, replacing banks as sources of funding. As a result, a higherproportion of the financial system’s loans are funneled to midsize andsmall firms, which tends to reduce the concentration of banks’ creditportfolios. Additionally, growth in this smaller-debtors segment can fuela virtuous cycle—signaling more spillover effects on the real economy,as well as the degree to which midsize companies are funding newinvestments in the positive economic environment.

Despite the significant progress achieved in the middle-market firmssegment, it is only the growth in loans to individuals (consumer andmortgages) that has been systematically outperforming the system’saverage. The intensification of retail lending is explained by theincreasingly strong consumer confidence in the context of benignmacroeconomic conditions and the reduction in the unemployment rate,as well as by the more aggressive stance of Chilean banks, who in thisrespect follow similar strategies to those of most financial systems inLatin America and worldwide. In Chile, however, banks are challengedby fierce competition from nonbanks operating in the consumersegment (retail stores, supermarkets, mutual entities, insurers, and carfinance companies). Nonbanks ended the past decade with a 27%share of total consumer financing available in the economy andincreased their participation to a peak of 35% in 2003. As banksbecame more focused and put their machinery to work on the consumersegment, the nonbank share declined to 32%, stabilizing at that levelsince 2004. Customers were the ultimate winners of this competitionbetween banks and nonbanks, benefiting from lower rates and longertenors.

As in many other countries, the change in the business mix due to thehigher-yielding consumer segment becoming the starring business isallowing financial institutions to maintain and/or increase marginsdespite the low interest rate environment and competitive pressures.Although rapid penetration in any segment should raise concerns for afuture potential deterioration in asset quality, in the case of Chile,household borrowings are still low relative to income (unlike in theU.S., for instance), giving room for significant medium-term expansionat current rates before hurting current healthy fundamentals.Although Chile leads the region in terms of its financial system’s depthand coverage, it still lags the degree of penetration typical of mostdeveloped countries. Total loans to households represent around 20%of GDP, whereas this figure is 75% in Spain. This is another indicationthat Chilean banks’ recent efforts to expand the level of bancarizationin the economy by seeking increased penetration in lower incomesegments are likely to keep succeeding in the medium term. Furtherexpansion of the client base (number of debtors grew 8.5% to 3.96million in 2006) and increased coverage of the banks’ networks (numberof offices and ATMs increased 7% to 7,151 in 2006) will continueplaying key roles in deepening the bancarization in Chile. In 2007,lending to individuals and small and midsize enterprises (SMEs) islikely to remain the main driver of growth.

Asset quality is still good newsThe auspicious economic environment coupled with overallconservative policies has resulted in an improving asset quality trendduring the past years, with nonperforming loans (NPLs) reducing to alow 0.8% of total loans by the end of 2006. Even during the Chileaneconomy’s relative stagnation and the pressure resulting from theregion’s uncertain economic environment (1999-2002), past-due loanfigures deteriorated only mildly and remained at low levels incomparison with the rest of Latin America.

Coverage with provisions also showed a welcome trend, with theprovisioning cushion increasing to 162% by the end of 2006 from the100% reported by the Chilean banking system at the beginning of thedecade.

So far, the growth in lending to allegedly riskier segments (i.e., retailand SMEs) has not resulted in asset quality deterioration, possiblybecause the effects of increased indebtedness were mitigated byprogressively more favorable credit conditions (namely record lowinterest rate environment and longer tenors). Nevertheless, current NPLlevels are likely to have found a floor as banks continue to increasepenetration in lower-income segments.

Mixed signals in profitabilitySince the beginning of the decade, Chilean banks’ profitabilitymeasured as results over assets has shown a moderately positivetrend, with the exception of 2002, when profits were hurt as a result ofthe extraordinary cost of the two large mergers that took place thatyear. When measuring profitability as results over capital, performanceseems even better as a result of the average increase in banks’leverage in the past few years.

In this area, one of the Chilean system’s main long-term achievementsis the growing operating efficiency. The ratio of operating expenses togross margins reduced to 50% in 2006 from 66% 10 years before.Other factors positively affecting profitability are low provisioningneeds in the favorable economic environment, and increasedcontribution of successful banks’ subsidiaries to overall profits (mostlyasset managers, insurers, and brokerage houses) that accounted for16% of the financial system’s profits in 2006. In recent years, thebanks’ successful efforts to grow fee income (widening the array ofservices provided in combination with cross selling initiatives andsharper pricing) were also positive contributors to profitability.

Negative factors conditioning Chilean banks’ results include the strongcompetition suffered by entities in all segments, as banks hurt theirmargins trying to increase intermediation levels by beating capitalmarkets and retail stores. The extremely low interest rate environmentthat still persists is also pressuring banks’ margins, although thecurrent business mix with increased participation of the higher-yieldingconsumer segments has succeeded at offsetting margin reduction.

22 Top 30 Chilean Companies - April 2007

In this context, during 2006, ROA was 1.4%, while ROE reached amaximum of 23%. While these figures compare favorably with those ofother developed countries, the Chilean system is somewhat lagging theriskier Mexican (annualized ROA of 2.74% in the nine-month periodended September 2006) and Brazilian banks (annualized ROA of 2.5% inthe six-month period ended June 2006).

Solvent banks, but further growth requires investmentAverage capitalization for the financial system declined to 12.5% ofrisk weighted assets by the end of 2006. Although all banks postfigures above 10% (well beyond the minimum 8% required byregulations), 11 institutions are now in the lowest 10% to 12% bucket(from eight banks at the end of 2005). Despite the still-adequatesolvency levels, since 2004, capitalization ratios have shown adownward trend as a result of the acceleration in asset growth. During2006, a greater number of banks decided to capitalize a larger portionof profits and/or issued subordinated debt to maintain high-qualitycapital indicators. As we expect vigorous growth in lending to remainthe rule in 2007, banks will continue to look for additional ways tomaintain adequate capital levels.

Consolidation, integration, and other market newsThe financial system’s concentration process peaked with the largemergers that took place in 2002, when Banco Santander-Chile S.A.acquired Banco Santiago to become the largest bank in Chile, andBanco de Chile S.A. merged with Banco Edwards to become the secondlargest. The two institutions managed to control more than 40% of themarket at the time. Since then, concentration has stabilized. Initially,the share of the two largest banks reduced due to midsize banksgaining market share as certain clients were expelled by the mergedbanks’ revised policies, or other clients fled from the lower quality ofservice that typically accompanies a cumbersome merger process.Moreover, the success of a number of relatively new entities (Fallabellastarted operations in 1999, Ripley in 2002, Monex and HNS in 2003,Penta and Paris in 2004) proved that there was enough room for nicheplayers to carry out thriving operations. Midsize banks focused on theless-standardized products and services also proved that competingsuccessfully with the two giants in the industry was possible.

In the past year, a number of financial industry-related transactionsproved that abundant business opportunities are still perceived by localand foreign market players. Brazilian Banco Itau acquiring localBankboston’s unit from Bank of America, Banco Internacional beingsold to local investors, BBVA buying a controlling stake in one of thelargest car finance companies (Forum), or Grupo Security getting holdof AIG life annuity unit (following their acquisition of Dresdner in 2004)were probably the most significant transactions. In this respect, weexpect 2007 to continue being prolific in market news and localplayers’ strong strategic moves. Acquisitions and alliances are likely tobe triggered by the potential change in regulations by which bankswould become authorized to participate directly in the large Chileanpension industry, which is in line with the worldwide tendency toincrease integration in the financial services industry, with playersmaximizing cross selling of a wide array of products to their still notcomprehensively serviced customer base.

Chilean banks’ regulators will get no rest in 2007During this year, Basel II implementation will continue to demandconsiderable efforts and investments on the part of Chilean banks andregulators, as institutions are expected to continue running parallelexercises on the standardized approach for credit risk (including modelsusing ratings in domestic scale in June and September of this year).Exercises will also address additional deliverables on market riskmeasures depending on the approach chosen by each bank(standardized or internal models of VaR) and producing supplementarydata toward breaking down operating margins by business line forbanks choosing to implement the standardized approach for thecalculation of operational risk capital requirements. Additionally, following nontrivial preparatory work during 2006,regulators will focus on upgrading some of the current accounting rulesto international standards, in particular those aiming to provideconsistent data toward complying with transparency and disclosure ofinformation required by Pillar III of the Basel Accord.

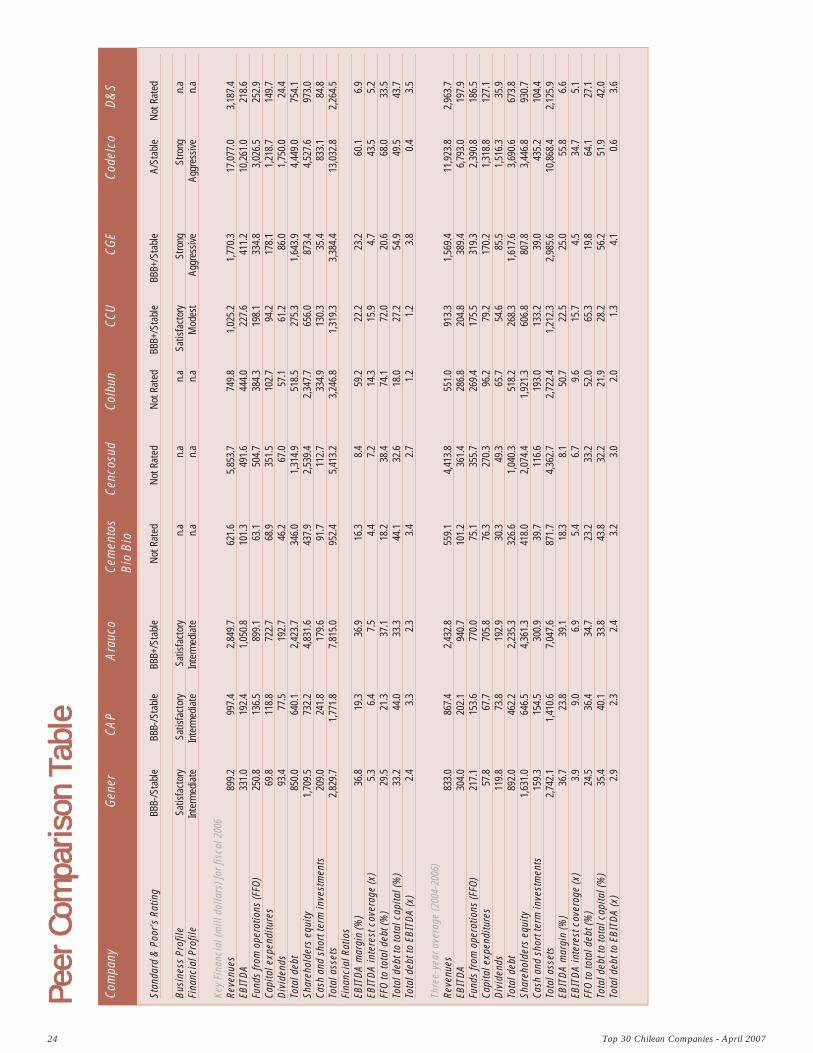

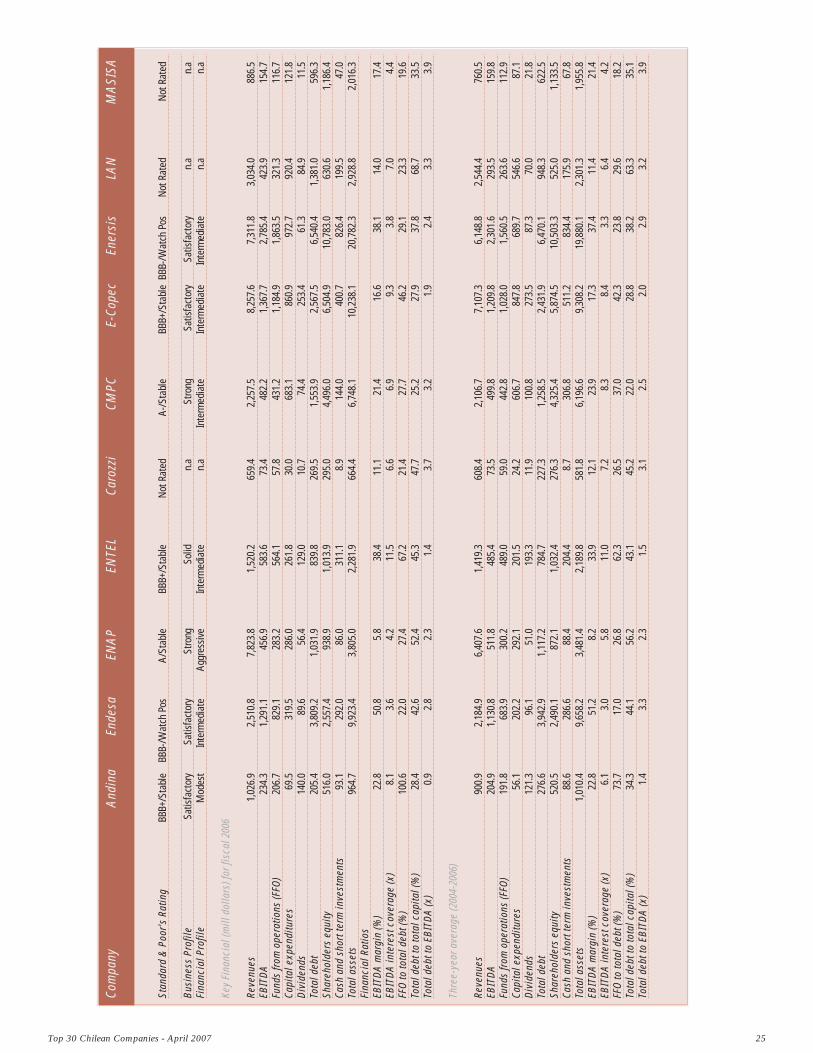

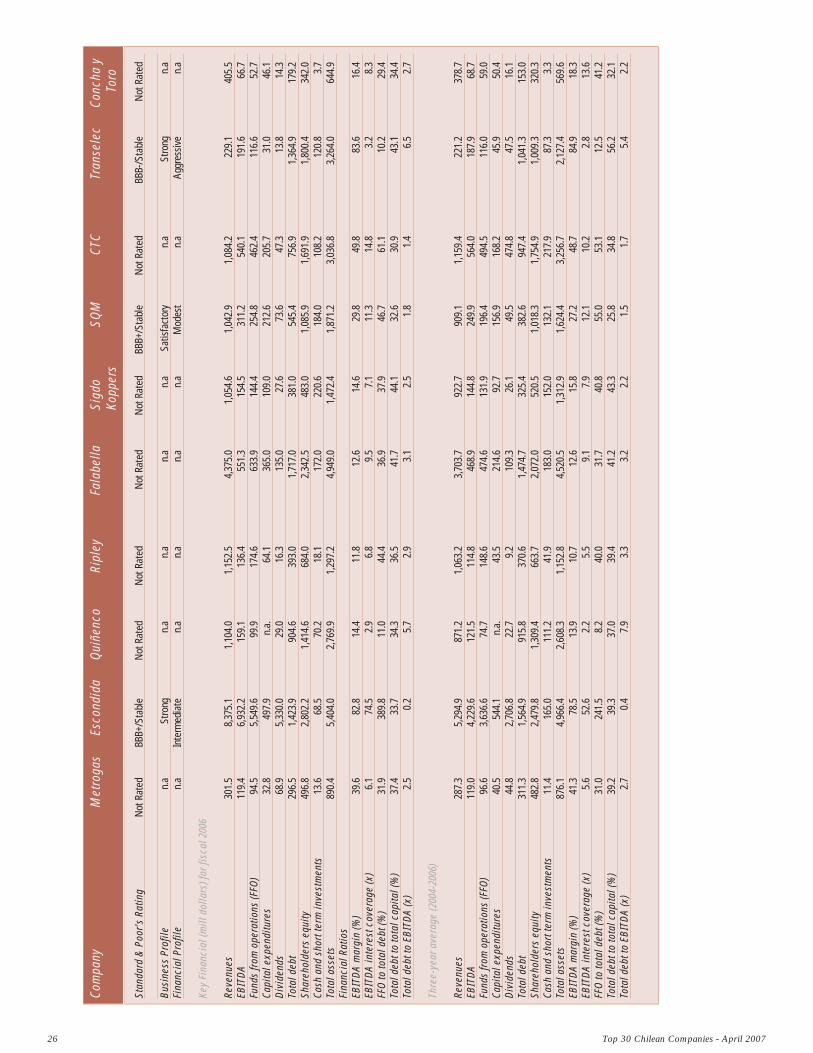

Credit Statistics

Com

pany

G

ener

CA

PA

rauc

oCe

men

tos

Cenc

osud

Co

lbun

CC

UCG

ECo

delc

oD

&S

Bio

Bio

Stan

dard

& P

oor's

Rat

ing

BBB-

/Sta

ble

BBB-

/Sta

ble

BBB+

/Sta

ble

Not

Rat

edN

ot R

ated

Not

Rat

edBB

B+/S

tabl

eBB

B+/S

tabl

eA/

Stab

leN

ot R

ated

Bus

ines

s Pr

ofile

Satis

fact

ory

Satis

fact

ory

Satis

fact

ory

n.a

n.a

n.a

Satis

fact

ory

Stro

ngSt

rong

n.a

Fina

ncia

l Pro

file

Inte

rmed

iate

Inte

rmed

iate

Inte

rmed

iate

n.a

n.a

n.a

Mod

est

Aggr

essi

veAg

gres

sive

n.a

Key

Fina

ncia

l (m

ill d

olla

rs) f

or fi

scal

200

6Re

venu

es89

9.2

997.

42,

849.

762

1.6

5,85

3.7

749.

81,

025.

21,

770.

317

,077

.03,

187.

4EB

ITD

A33

1.0

192.

41,

050.

810

1.3

491.

644

4.0

227.

641

1.2

10,2

61.0

218.

6Fu

nds

from

ope

ratio

ns (F

FO)

250.

813

6.5

899.

163

.150

4.7

384.

319

8.1

334.

83,

026.

525

2.9

Capi

tal e

xpen

ditu

res

69.8

118.

872

2.7

68.9

351.

510

2.7

94.2

178.

11,

218.

714

9.7

Div

iden

ds93

.477

.519

2.7

46.2

67.0

57.1

61.2

86.0

1,75

0.0

24.4

Tota

l deb

t85

0.0

640.

12,

423.

734

6.0

1,31

4.9

518.

527

5.3

1,64

3.9

4,44

9.0

754.

1Sh

areh

olde

rs e

quity

1,70

9.5

732.

24,

831.

643

7.9

2,53

9.4

2,34

7.7

656.

087

3.4

4,52

7.6

973.

0Ca

sh a

nd s

hort

term

inve

stm

ents

209.

024

1.8

179.

691

.711

2.7

334.

913

0.3

35.4

833.

184

.8To

tal a

sset

s2,

829.

71,

771.

87,

815.

095

2.4

5,41

3.2

3,24

6.8

1,31

9.3

3,38

4.4

13,0

32.8

2,26

4.5

Fina

ncia

l Rat

ios

EBIT

DA

mar

gin

(%)

36.8

19.3

36.9

16.3

8.4

59.2

22.2

23.2

60.1

6.9

EBIT

DA

inte

rest

cov

erag

e (x

)5.

36.

47.

54.

47.

214

.315

.94.

743

.55.

2FF

O to

tota

l deb

t (%

)29

.521

.337

.118

.238

.474

.172

.020

.668

.033

.5To

tal d

ebt t

o to

tal c

apita

l (%

)33

.244

.033

.344

.132

.618

.027

.254

.949

.543

.7To

tal d

ebt t

o EB

ITD

A (x

)2.

43.

32.

33.

42.

71.

21.

23.

80.

43.

5

Thre

e-ye

ar a

vera

ge (2

004-

2006

)Re

venu

es83

3.0

867.

42,

432.

855

9.1