Embed Size (px)

Citation preview

© Steven J. Willis 2006 1

INTRODUCTION TO TAX SCHOOL

Top 100 Cases

Lucas v. Earl, 281 U.S. 111 (1930)Poe v. Seaborn, 282 U.S. 101 (1930)

INTRODUCTION TO TAX SCHOOL

Top 100 Cases

Lucas v. Earl, 281 U.S. 111 (1930)Poe v. Seaborn, 282 U.S. 101 (1930)

© Steven J. Willis 2006 2

Lucas v. Earl, 281 U.S. 111 (1930)

• Lucas v. Earl is famous for two important overlapping propositions:

– The Claim of Right Doctrine.

– Every Year Stands Alone.

• This second proposition is conjunction with two other famous cases:

– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

© Steven J. Willis 2006 3

Lucas v. Earl, 281 U.S. 111 (1930)

• Lucas v. Earl is famous for two important overlapping propositions:

– The Claim of Right Doctrine.

– Every Year Stands Alone.

• This second proposition is conjunction with two other famous cases:

– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

© Steven J. Willis 2006 4

Lucas v. Earl, 281 U.S. 111 (1930)

• Lucas v. Earl is famous for two important overlapping propositions:

– The Claim of Right Doctrine.

– Every Year Stands Alone.

• This second proposition is conjunction with two other famous cases:

– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Fruit and Tree AnalogyThe Fruit and Tree Analogy

The Assignment of Income DoctrineThe Assignment of Income Doctrine

© Steven J. Willis 2006 5

Lucas v. Earl, 281 U.S. 111 (1930)

• Lucas v. Earl is famous for two important overlapping propositions:

– The Claim of Right Doctrine.

– Every Year Stands Alone.

– The first proposition more precisely states:

– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

The Fruit and Tree AnalogyThe Fruit and Tree Analogy

© Steven J. Willis 2006 6

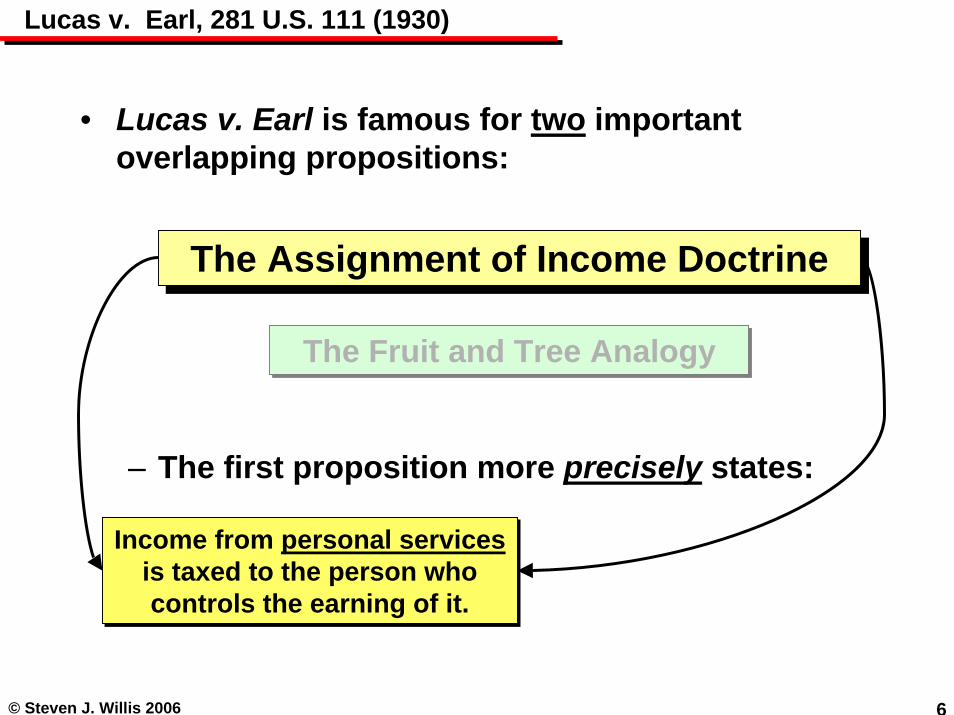

Lucas v. Earl, 281 U.S. 111 (1930)

• Lucas v. Earl is famous for two important overlapping propositions:

– The Claim of Right Doctrine.

– Every Year Stands Alone.

– The first proposition more precisely states:

– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

The Fruit and Tree AnalogyThe Fruit and Tree Analogy

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

© Steven J. Willis 2006 7

Lucas v. Earl, 281 U.S. 111 (1930)

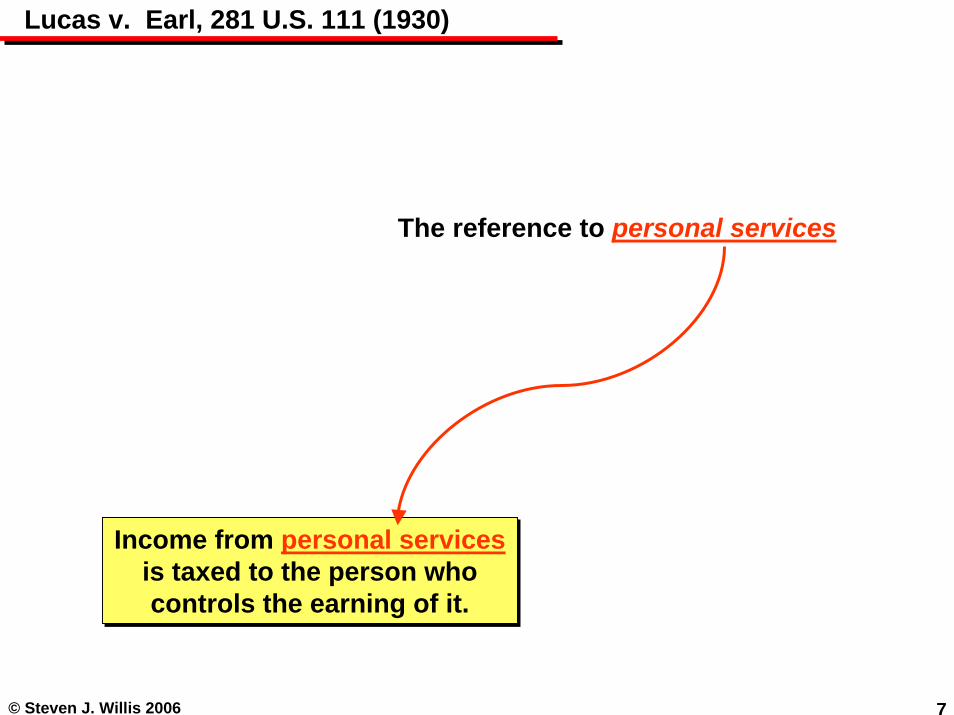

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

© Steven J. Willis 2006 8

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

© Steven J. Willis 2006 9

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

© Steven J. Willis 2006 10

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

© Steven J. Willis 2006 11

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

© Steven J. Willis 2006 12

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

© Steven J. Willis 2006 13

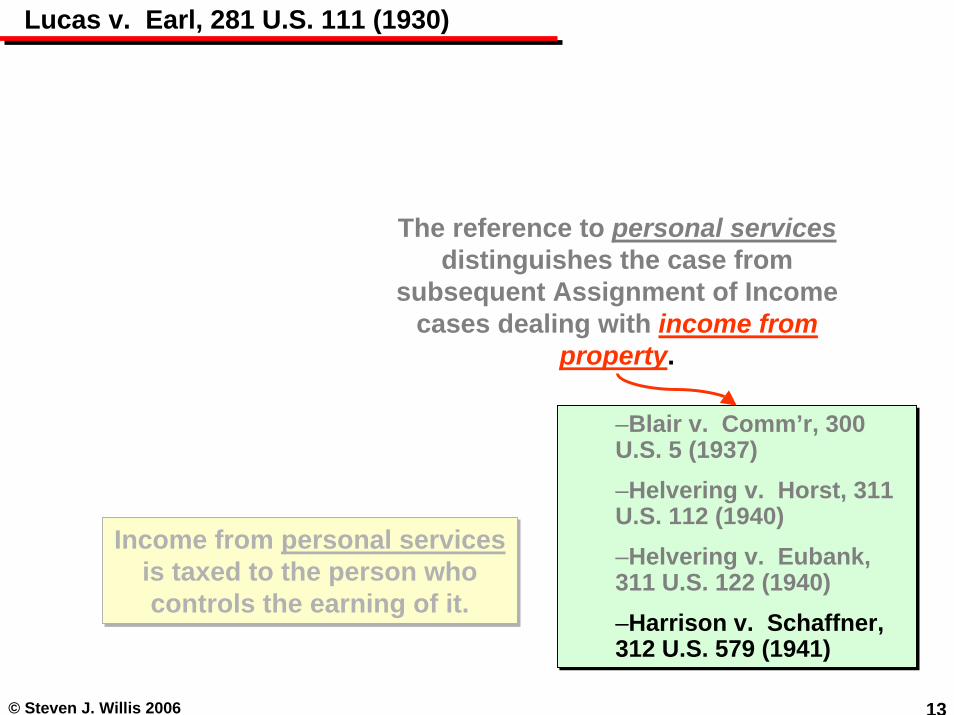

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

© Steven J. Willis 2006 14

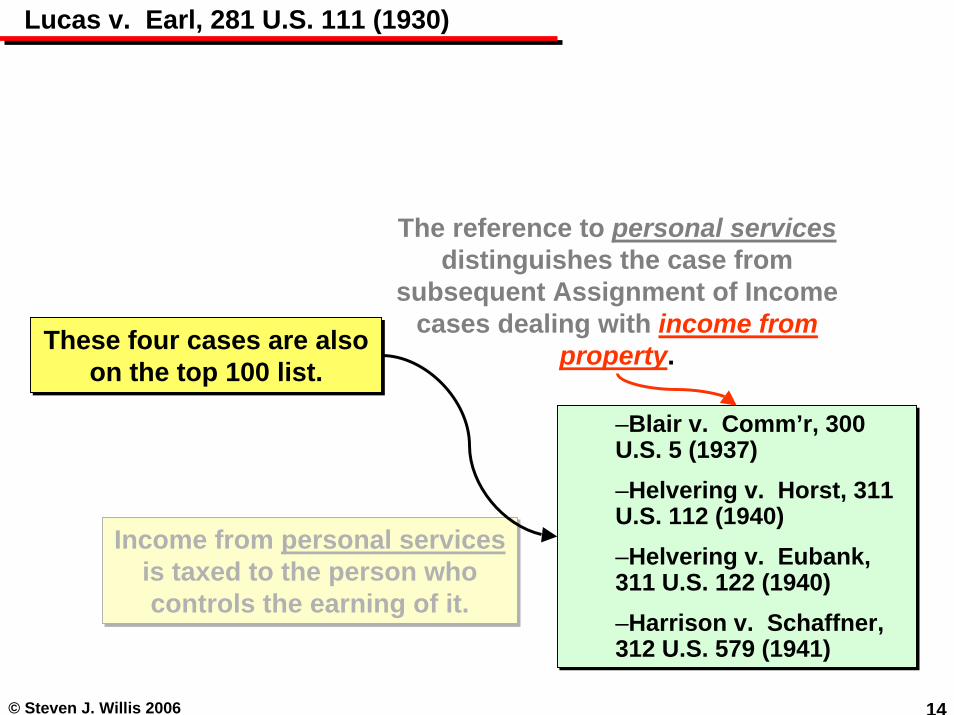

Lucas v. Earl, 281 U.S. 111 (1930)

The reference to personal servicesdistinguishes the case from

subsequent Assignment of Income cases dealing with income from

property.

Income from personal servicesis taxed to the person who controls the earning of it.

Income from personal servicesis taxed to the person who controls the earning of it.

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

–Blair v. Comm’r, 300 U.S. 5 (1937)–Helvering v. Horst, 311 U.S. 112 (1940)–Helvering v. Eubank, 311 U.S. 122 (1940)–Harrison v. Schaffner, 312 U.S. 579 (1941)

These four cases are also on the top 100 list.

These four cases are also on the top 100 list.

© Steven J. Willis 2006 15

Lucas v. Earl, 281 U.S. 111 (1930)

• To summarize:

– When you hear of Lucas v. Earl you must think of:

– You should also associate the case with transactional accountingand the notion that every year stands alone.

• Ideally, you would also associate the case with– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

© Steven J. Willis 2006 16

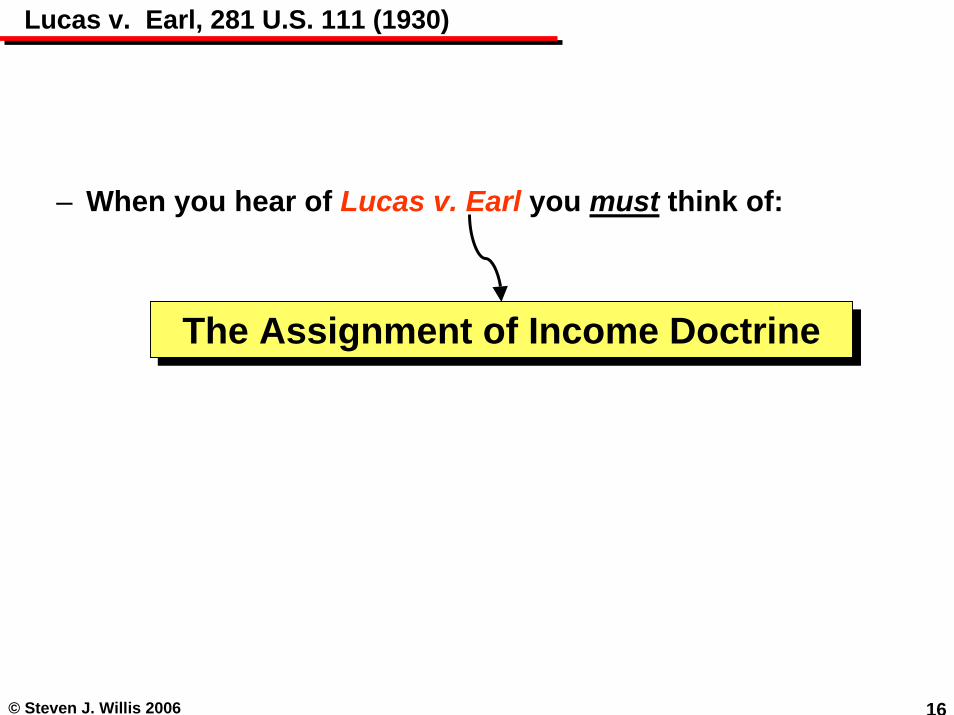

Lucas v. Earl, 281 U.S. 111 (1930)

• To summarize:

– When you hear of Lucas v. Earl you must think of:

– You should also associate the case with transactional accountingand the notion that every year stands alone.

• Ideally, you would also associate the case with– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

© Steven J. Willis 2006 17

Lucas v. Earl, 281 U.S. 111 (1930)

• To summarize:

– When you hear of Lucas v. Earl you must think of:

– You should also associate the case with transactional accountingand the notion that every year stands alone.

• Ideally, you would also associate the case with– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

Ideally, you will recall it deals with

income from services.

Ideally, you will recall it deals with

income from services.

© Steven J. Willis 2006 18

Lucas v. Earl, 281 U.S. 111 (1930)

• To summarize:

– When you hear of Lucas v. Earl you must think of:

– You should also associate the case with transactional accountingand the notion that every year stands alone.

• Ideally, you would also associate the case with– Burnet v. Sanford & Brooks, 282 U.S. 359 (1931) – U.S. v. Lewis, 340 U.S. 590 (1951).

The Assignment of Income DoctrineThe Assignment of Income Doctrine

Ideally, you will recall it deals with

income from services.

Ideally, you will recall it deals with

income from services.

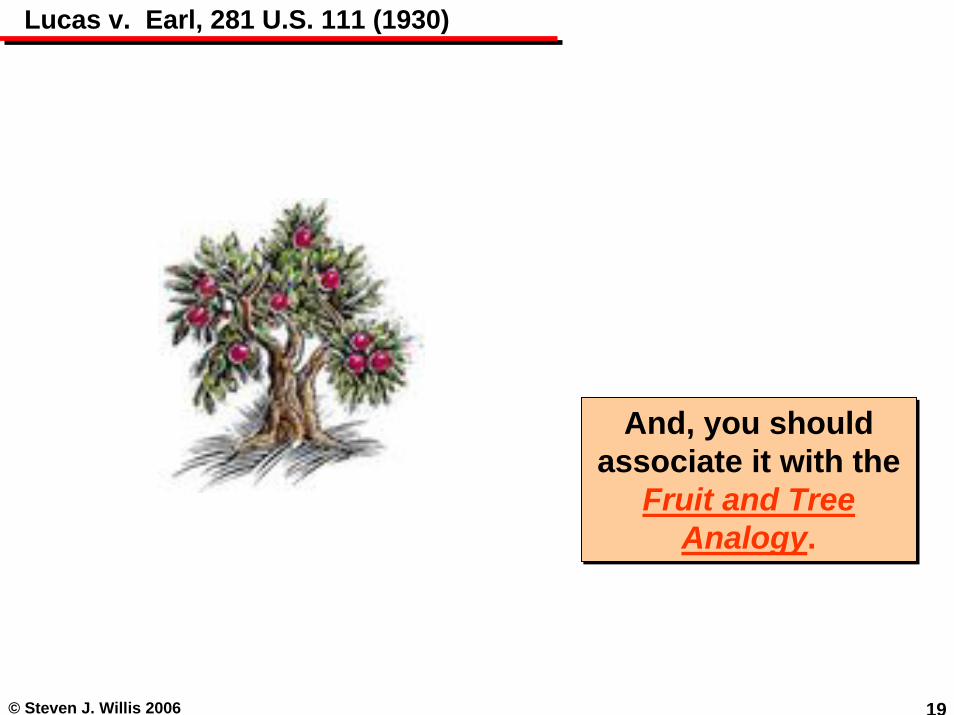

And, you should associate it with the

Fruit and Tree Analogy.

And, you should associate it with the

Fruit and Tree Analogy.

© Steven J. Willis 2006 19

Lucas v. Earl, 281 U.S. 111 (1930)

And, you should associate it with the

Fruit and Tree Analogy.

And, you should associate it with the

Fruit and Tree Analogy.

© Steven J. Willis 2006 20

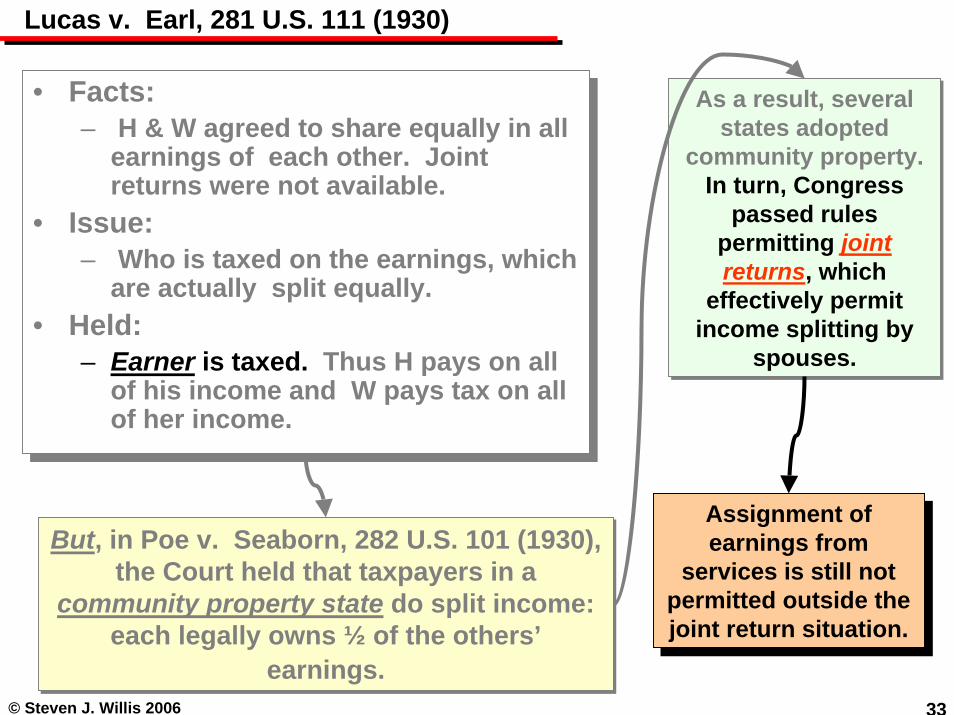

Lucas v. Earl, 281 U.S. 111 (1930)

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on his income and W pays tax on hers.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on his income and W pays tax on hers.

© Steven J. Willis 2006 21

Lucas v. Earl, 281 U.S. 111 (1930)

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally?• Held:

– Earner is taxed. Thus H pays on his income and W pays tax on hers.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally?• Held:

– Earner is taxed. Thus H pays on his income and W pays tax on hers.

© Steven J. Willis 2006 22

Lucas v. Earl, 281 U.S. 111 (1930)

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

© Steven J. Willis 2006 23

Lucas v. Earl, 281 U.S. 111 (1930)

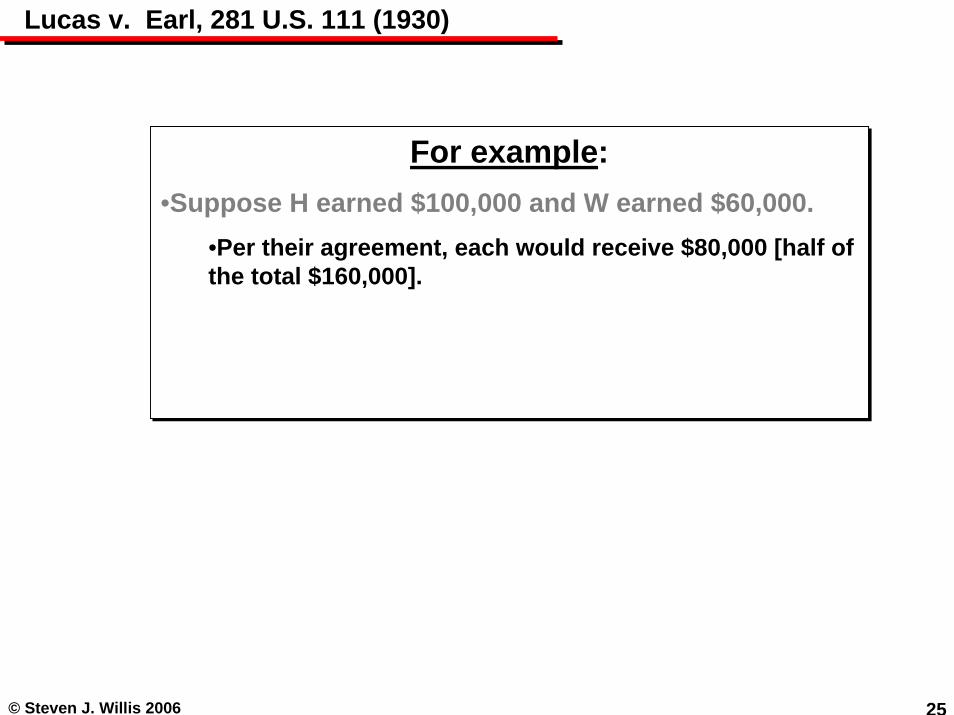

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

© Steven J. Willis 2006 24

Lucas v. Earl, 281 U.S. 111 (1930)

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

© Steven J. Willis 2006 25

Lucas v. Earl, 281 U.S. 111 (1930)

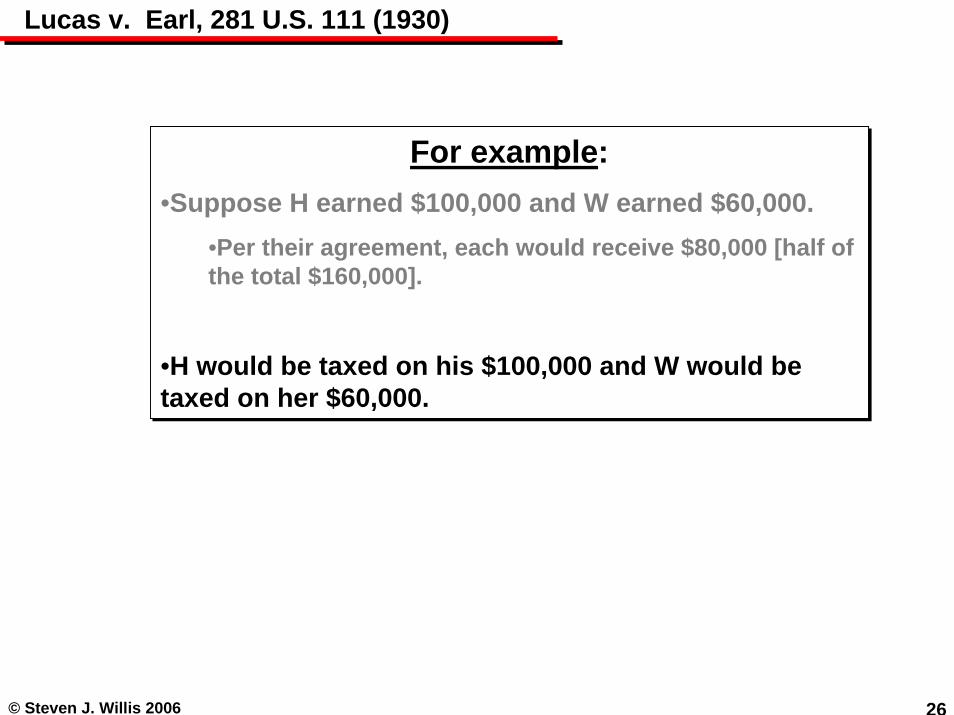

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

© Steven J. Willis 2006 26

Lucas v. Earl, 281 U.S. 111 (1930)

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

© Steven J. Willis 2006 27

Lucas v. Earl, 281 U.S. 111 (1930)

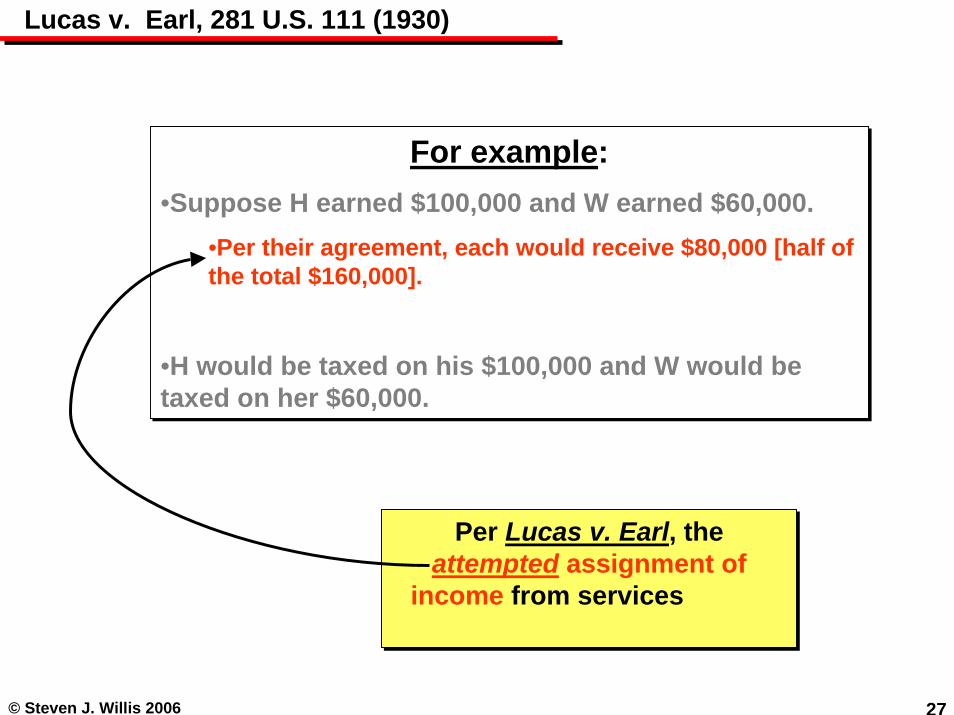

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

Per Lucas v. Earl, the attempted assignment of

income from services would not be successful.

Per Lucas v. Earl, the attempted assignment of

income from services would not be successful.

© Steven J. Willis 2006 28

Lucas v. Earl, 281 U.S. 111 (1930)

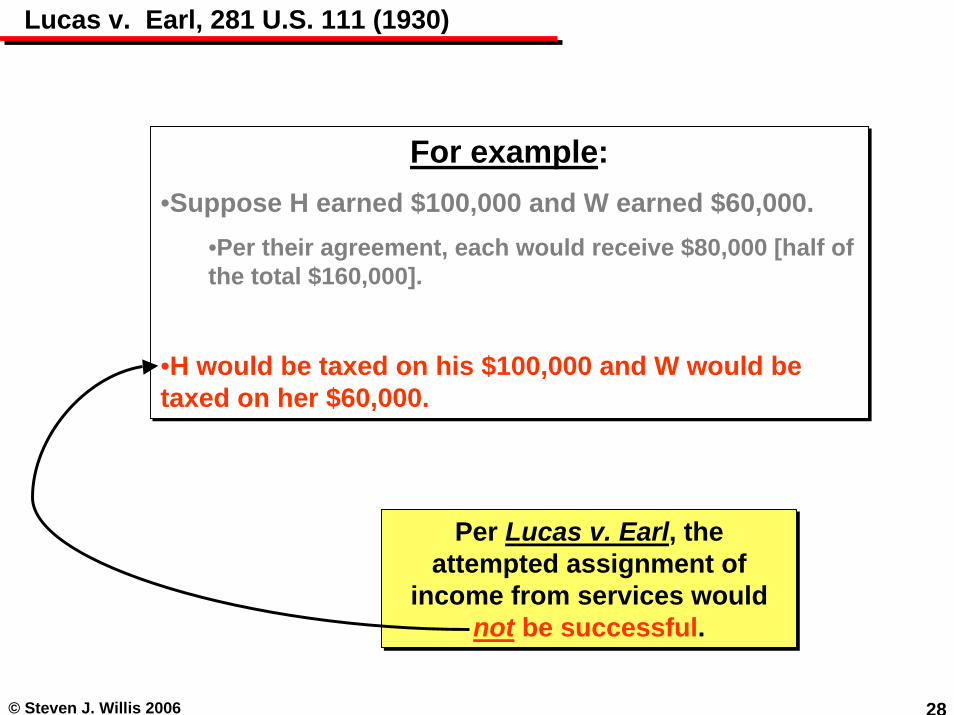

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

For example:•Suppose H earned $100,000 and W earned $60,000.

•Per their agreement, each would receive $80,000 [half of the total $160,000].

•H would be taxed on his $100,000 and W would be taxed on her $60,000.

Per Lucas v. Earl, the attempted assignment of

income from services would not be successful.

Per Lucas v. Earl, the attempted assignment of

income from services would not be successful.

© Steven J. Willis 2006 29

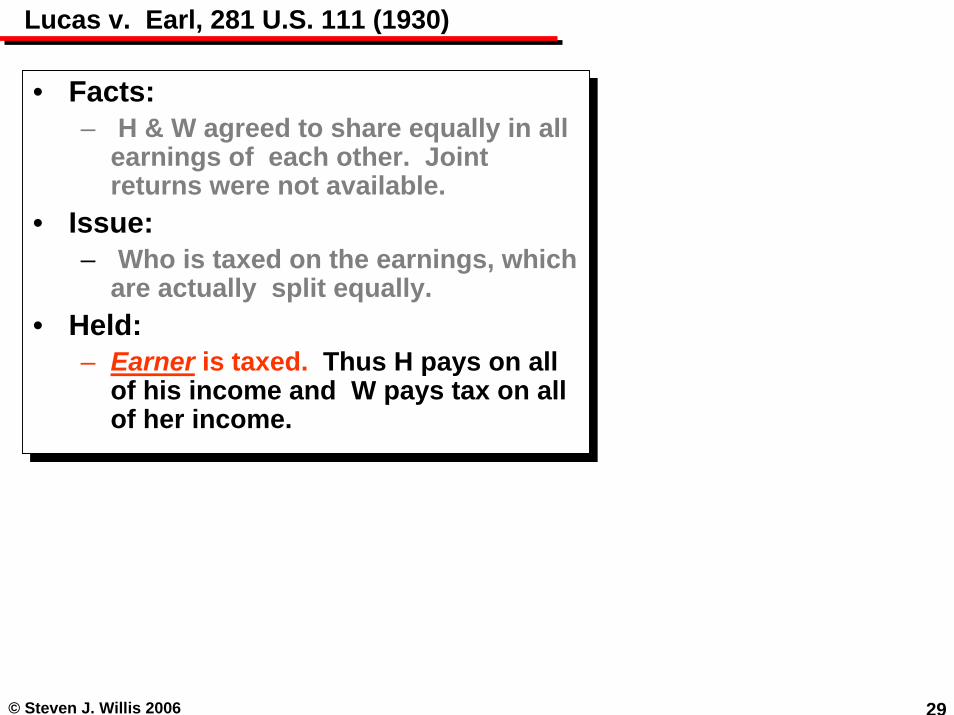

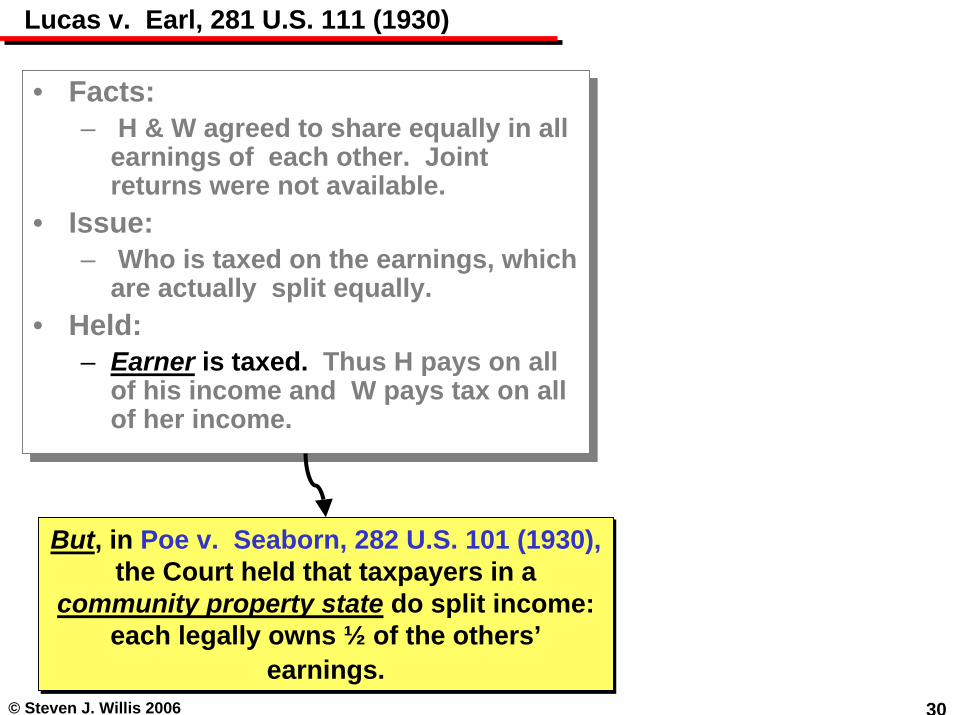

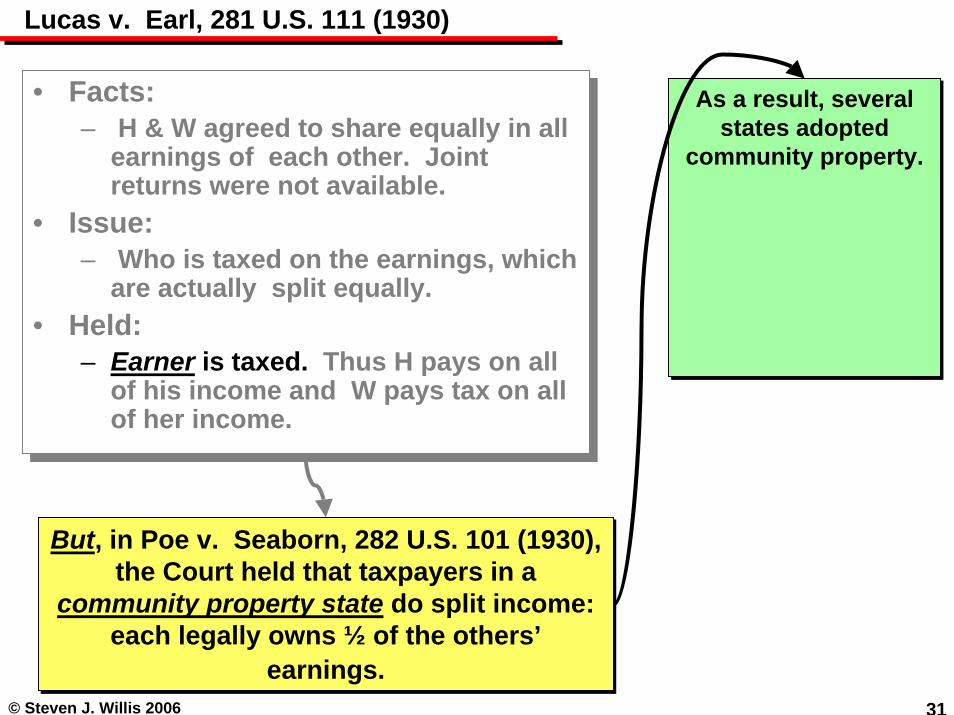

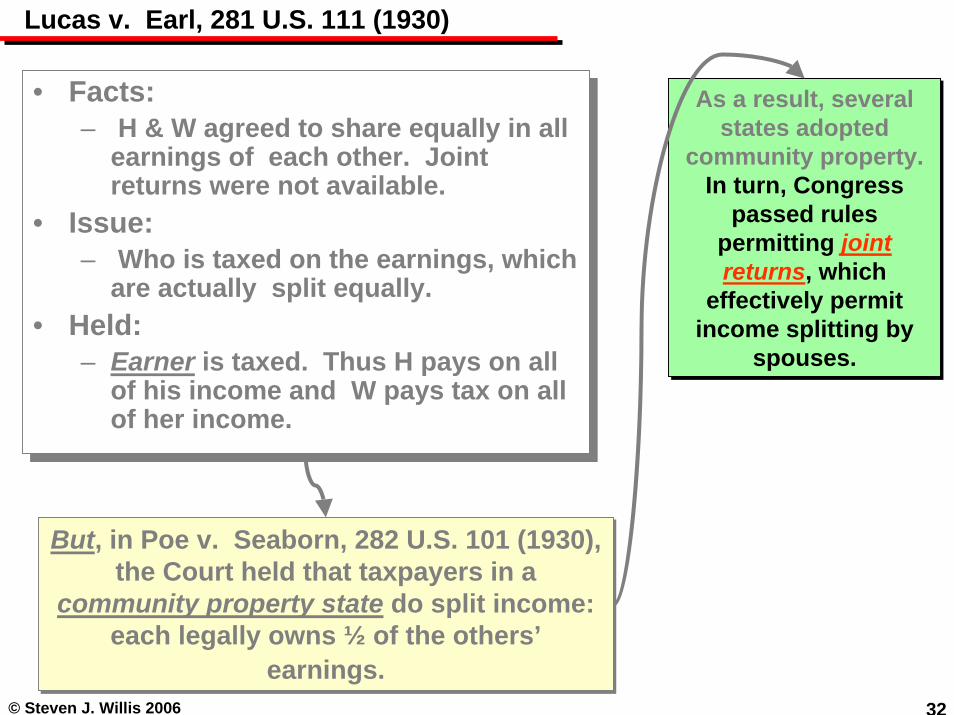

Lucas v. Earl, 281 U.S. 111 (1930)

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

© Steven J. Willis 2006 30

Lucas v. Earl, 281 U.S. 111 (1930)

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

© Steven J. Willis 2006 31

Lucas v. Earl, 281 U.S. 111 (1930)

As a result, several states adopted

community property. In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

As a result, several states adopted

community property. In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

But, in Poe v. Seaborn, 282 U.S. 101 (1930),the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

But, in Poe v. Seaborn, 282 U.S. 101 (1930),the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

© Steven J. Willis 2006 32

Lucas v. Earl, 281 U.S. 111 (1930)

As a result, several states adopted

community property.In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

As a result, several states adopted

community property.In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

© Steven J. Willis 2006 33

Lucas v. Earl, 281 U.S. 111 (1930)

As a result, several states adopted

community property.In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

As a result, several states adopted

community property.In turn, Congress

passed rules permitting joint returns, which

effectively permit income splitting by

spouses.

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

But, in Poe v. Seaborn, 282 U.S. 101 (1930), the Court held that taxpayers in a

community property state do split income: each legally owns ½ of the others’

earnings.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

• Facts: – H & W agreed to share equally in all

earnings of each other. Joint returns were not available.

• Issue:– Who is taxed on the earnings, which

are actually split equally.• Held:

– Earner is taxed. Thus H pays on all of his income and W pays tax on all of her income.

Assignment of earnings from

services is still not permitted outside the joint return situation.

Assignment of earnings from

services is still not permitted outside the joint return situation.

© Steven J. Willis 2006 34

Lucas v. Earl, 281 U.S. 111 (1930)

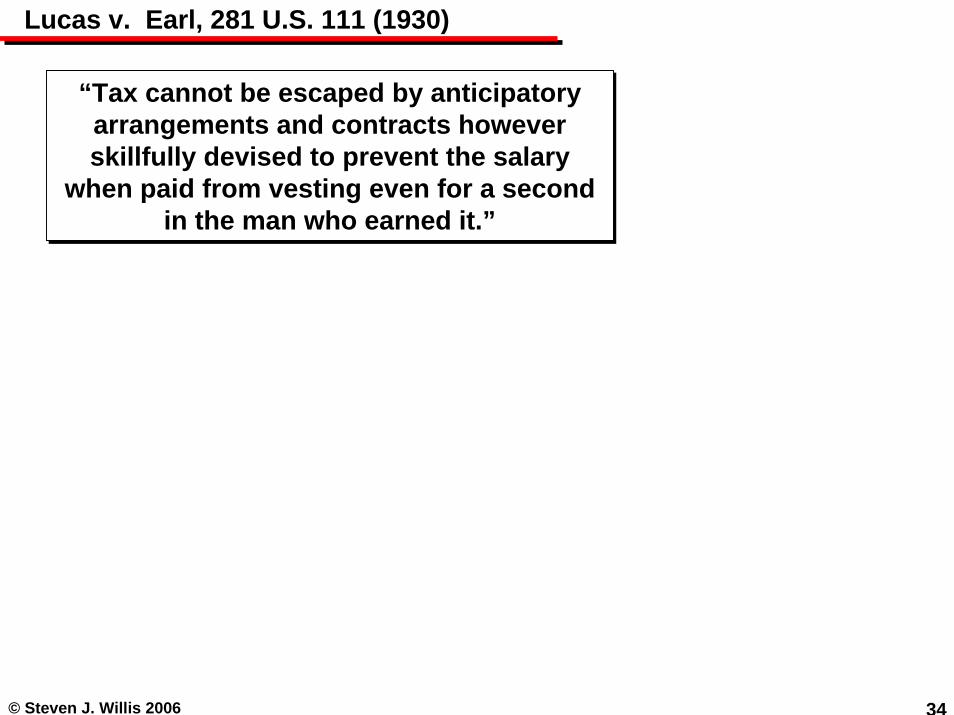

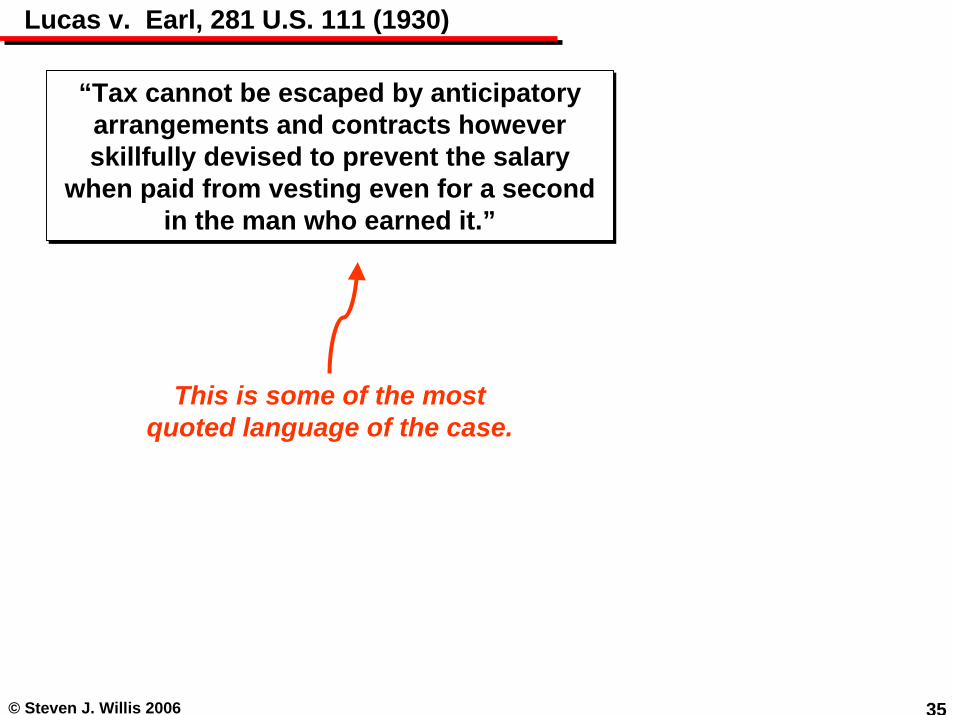

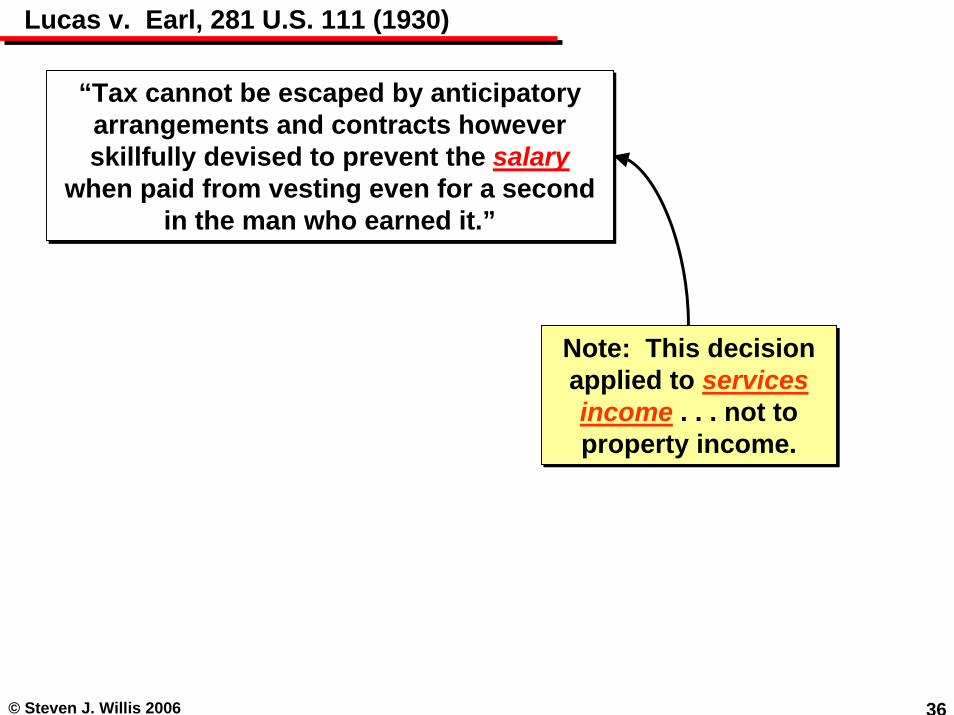

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

© Steven J. Willis 2006 35

Lucas v. Earl, 281 U.S. 111 (1930)

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

This is some of the most quoted language of the case.

© Steven J. Willis 2006 36

Lucas v. Earl, 281 U.S. 111 (1930)

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

Note: This decision applied to services income . . . not to property income.

Note: This decision applied to services income . . . not to property income.

© Steven J. Willis 2006 37

Lucas v. Earl, 281 U.S. 111 (1930)

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

© Steven J. Willis 2006 38

Lucas v. Earl, 281 U.S. 111 (1930)

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

© Steven J. Willis 2006 39

Lucas v. Earl, 281 U.S. 111 (1930)

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

“Tax cannot be escaped by anticipatory arrangements and contracts however skillfully devised to prevent the salary

when paid from vesting even for a second in the man who earned it.”

This is the other often quoted language.

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

The Court disapproved of schemes by which “fruits

are attributed to a different tree from that on which they

grew.”

© Steven J. Willis 2006 40

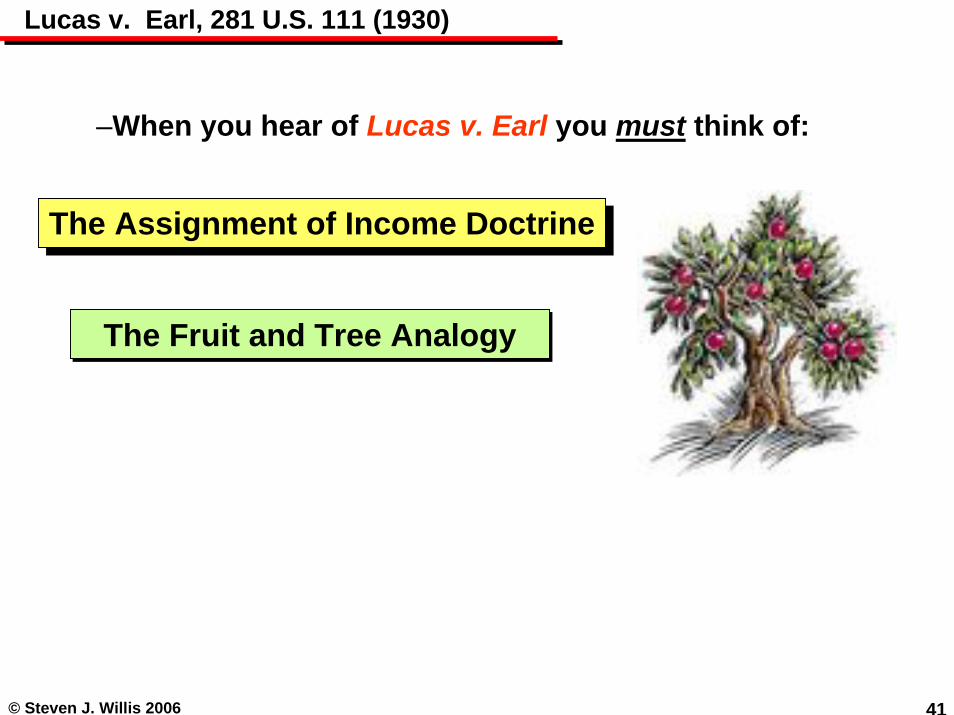

Lucas v. Earl, 281 U.S. 111 (1930)

–When you hear of Lucas v. Earl you must think of:

The Assignment of Income DoctrineThe Assignment of Income Doctrine

© Steven J. Willis 2006 41

Lucas v. Earl, 281 U.S. 111 (1930)

–When you hear of Lucas v. Earl you must think of:

The Assignment of Income DoctrineThe Assignment of Income Doctrine

The Fruit and Tree AnalogyThe Fruit and Tree Analogy

![State v. Lucas - Supreme Court of Ohio€¦ · · 2009-01-06[Cite as State v. Lucas, 2009-Ohio-19.] COURT OF APPEALS STARK COUNTY, OHIO FIFTH APPELLATE DISTRICT STATE OF OHIO](https://img.pdfslide.us/doc/110x75/5ac24a8f7f8b9aca388e1408/state-v-lucas-supreme-court-of-ohio-2009-01-06cite-as-state-v-lucas-2009-ohio-19.jpg)