Embed Size (px)

Citation preview

Today’s key challenge in Treasury

Transfer Pricing & Treasury

www.pwc.lu

PwC

Content

The word of the President

Virtual reality of Treasury

Overview - Treasury operations

Intercompany financing

Cash pooling

Guarantees

Documentation requirements

Key Takeaways

PwC’s role

PwC

Key facts and methodology

Want to download the fullreport? Please visit ourwebsite:http://www.pwc.lu/corporate-treasury-solutions

The "virtual reality" of treasury 3

April 2017

The "virtual

reality" of treasury

Treasurersand Chief Financial

Officers

Longand short

questionnaires

+ 220 interviews completed

24 countries

Conduct between July and October

2016

All industries and

areas of service

Financial Transactions •

3

PwC

Key Findings

The "virtual reality" of treasury 4

April 2017

Base Erosion and Profit Shifting (BEPS) will bring tax and treasury closer together

Treasurers need the means to truly make treasury resilient and effective

Treasurers need to take action to safeguard assets with rising cybersecurity threats

True focus on cash flows forecasting may provide a quick return

The agendas of the treasurer and the CFO should be better aligned

Treasury’s scope continues to expand and is now a company-wide process – it no longer operates as a single ‘department’. With treasury processes becoming increasingly virtual, treasurers need to collaborate more with the business, shared services and banks and raise their game in IT security, valuation and financial risk management to succeed in today’s environment.

High on the agenda for treasurers:

Base Erosion and Profit Shifting (BEPS) will bring tax and treasury closer together New fiscal legislation means substance and transfer pricing will take centre stage. This may have a material impact on the location of treasury activities, distribution of decision power and configuration of systems. As a result, treasury will need to work more closely with tax to assess the impact and properly prepare their organisations.

Financial Transactions •

4

Tax paradigm or revolution of the century, but fairness in tax at the price of unending difficulties

Examples: Restriction on interest deduction (interest deductible only if < 30% of EBITDA with threshold of €1m situations in which entities loss-making will no longer be able to deduct interest), Exit Taxation, Switch-over clause, General Anti-Abuse Rule, Hybrid mismatch and extension of “Controlled Foreign Company” rules generating whole wodge of attempts to tax anything that may not have been taxed

New framework: everyone claims its "fair share" of the tax cake

Main idea is to align TAXABLE BASE with VALUE CREATION.

3 main watchwords: (1) Consistency, (2) Substance and (3) Transparency

Treasurers could argue TP rules already existed long before

Some countries already started to question to justify the "fair" TP

Major principle (“choosing the option that costs the least in tax”) has now been called into question

BEPS, became a reality in EU

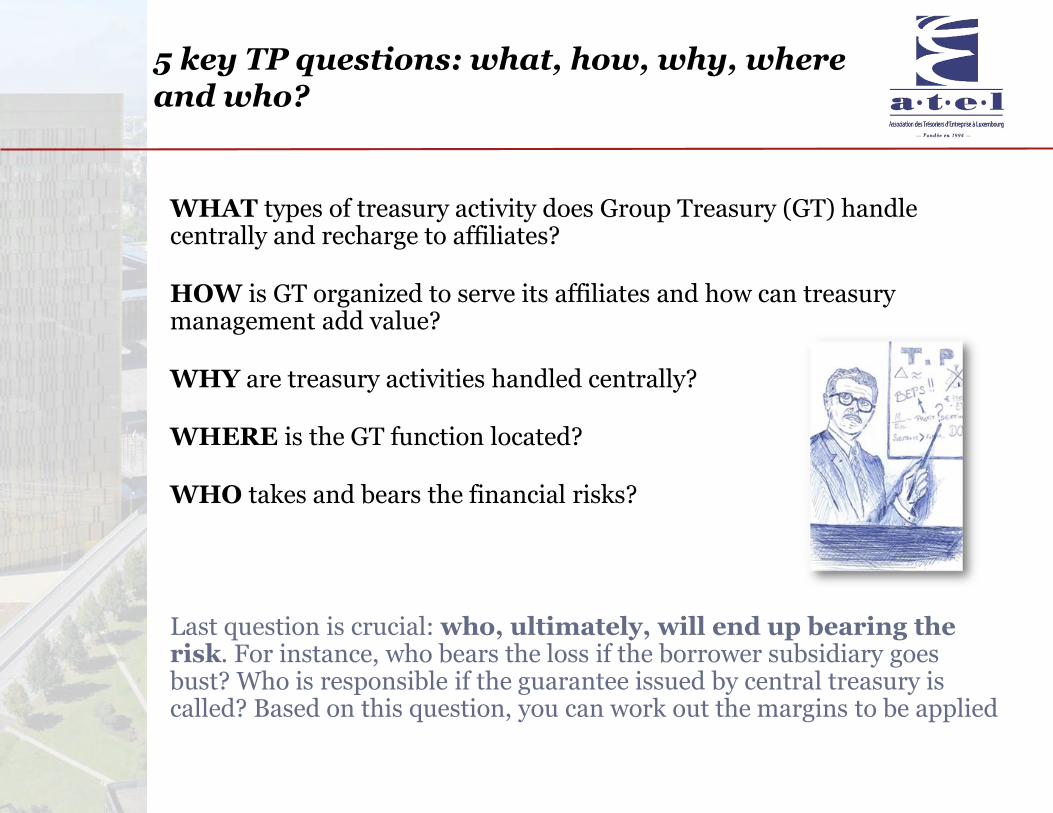

WHAT types of treasury activity does Group Treasury (GT) handle centrally and recharge to affiliates?

HOW is GT organized to serve its affiliates and how can treasury management add value?

WHY are treasury activities handled centrally?

WHERE is the GT function located?

WHO takes and bears the financial risks?

Last question is crucial: who, ultimately, will end up bearing the risk. For instance, who bears the loss if the borrower subsidiary goes bust? Who is responsible if the guarantee issued by central treasury is called? Based on this question, you can work out the margins to be applied

5 key TP questions: what, how, why, where and who?

The 10 TP commandments are…

Be BEPS compliant…

"If you would know the value of money, go try to borrow some“ (French Proverb)

More ironically, we might say: "In business, the lower the price, the bigger the sticker" (even between sub’s of the same group)

PwC

Overview - Treasury operations

TYPICAL TREASURYSERVICES

PROVIDED INTRA-GROUP

Short- term debt management

Long- term debt management

Excess cash management

Working capital management

Hedging (i.e. FX/currency)

External funding optimization

Investment management (i.e. asset acquisition)

Other (ancillary) services

Establishing global

financing in a territory

where substance can

be maintained

More globally and

regionally integrated

business units

Risk management, incl.

acknowledgement of

financial risk

Focus on the

aggregate

business results

PwC

Intercompany financing

Main focus areas

Assess the creditworthiness of the borrowing entities

Define the functional and risk profile of the entities involved

Assess the arm’s length intra-group interest rate - can we rely on the yield curves only?

PwC

Intercompany financing

Interestpayments

Related party financing

ParentCo

SubCos

Rationale forborrowing

Why is the entity borrowing?

What is the borrower’s credit rating?

Based on debt/equity ratios / projections, could the entity borrow?

Do internal / external comparables exist?

Do comparability adjustments need to be performed?

Debtcapacity

Arm’s lengthinterest rate

PwC

Higher

Lower

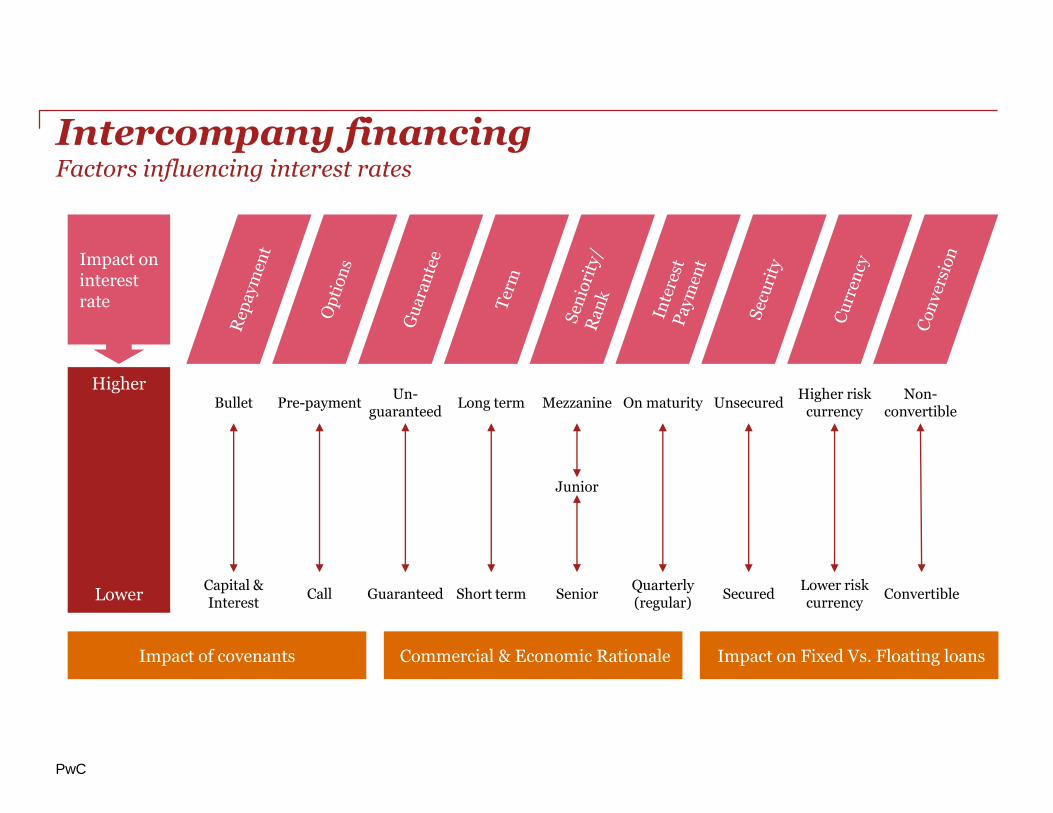

Impact on interest rate

Bullet Pre-paymentUn-

guaranteedLong term Mezzanine On maturity Unsecured

Higher risk currency

Non-convertible

Capital & Interest

Call Guaranteed Short term SeniorQuarterly (regular)

SecuredLower risk currency

Junior

Convertible

Impact of covenants Commercial & Economic Rationale Impact on Fixed Vs. Floating loans

Intercompany financingFactors influencing interest rates

PwC

HigherLowerComplexity

EntityCredit RiskPremium

Country Risk

Premium

Applicable Fees

Ratings per entity

Segmentation into ratings buckets

Combination of ratings and credit limits

Notching only (potentially with credit limits)

Country-specific spreads

Regional segmentation only

Limited consideration of country risk, as exception

Transactional fee benchmarking

Benchmarking for key services only

Cost(plus) based remuneration (service spread)

Key country premia/discounts, with regional segmentation for rest

Technically Strongest Practical and Defensible Subject to adjustmentRisk of

Challenge

Considered as stewardship or immaterial

Intercompany financingInterest rate setting options

PwC

Cash pooling

Main focus areas

Create a netting system used for intercompany payments and receipts

Assess the arm’s length remuneration for the cash pool header

Determine the relative contributions of the various participants

Allocate the cash pool advantages amongst the participants

PwC

SHORT-TERM FUNDING

NEEDS

EXCESS CASH

Reduce the MNE’s total external funding costs

Help manage certain risks such as liquidity or foreign exchange

Help obtaining more favourable borrowing conditions

Management of volatility of the group's liquid cash resources

Decision-making for financing is centralised

Lending Rate Base Rate + Entity Credit Risk Premium

+ Country Risk Premium + Cash Pool Service Fee + Cash Pool Facility Fee

Deposit RateBase Rate - Deposit Rate

Spread - Cash Pool Service Fee

The spread between the two rates

represents the additional

remuneration for the cash pool

leader

Cash poolingFactors influencing cash pooling

PwC

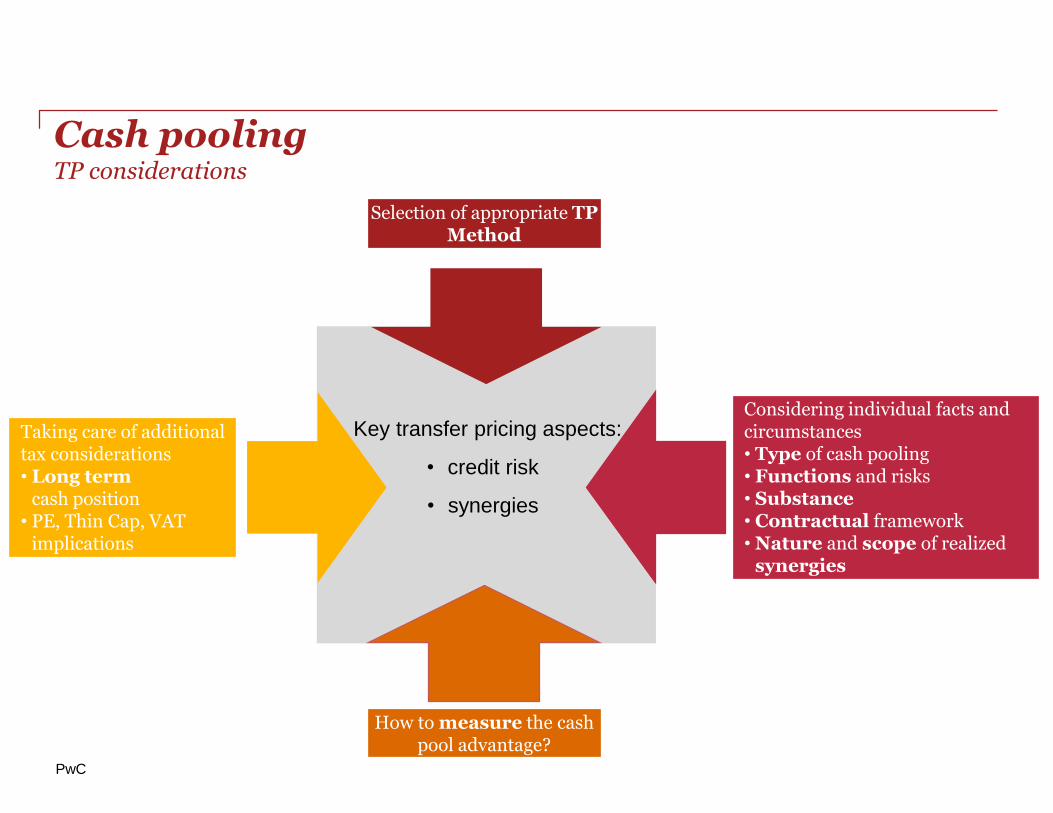

How to measure the cash pool advantage?

Key transfer pricing aspects:

• credit risk

• synergies

Taking care of additional tax considerations• Long term

cash position• PE, Thin Cap, VAT

implications

Selection of appropriate TP Method

Considering individual facts and circumstances• Type of cash pooling• Functions and risks• Substance• Contractual framework• Nature and scope of realized

synergies

Cash poolingTP considerations

PwC

…vs. Notional cash pool

Zero Balanced cash pool…

Cash poolingTypes of cash pools

PwC

Guarantees

Main focus areas

Implicit versus explicit guarantees

Determine the creditworthiness of the borrowing entities

Assess the arm’s length intra-group guarantee fee

PwC

FINANCIAL GUARANTEE

Purpose: reduce risk to lenders

Main benefits: Access to credit borrowing Substitution for capital in the

subsidiary

Cheaper access to credit

The “reliability” of the guarantor is passed to the

related entity…

…decreasing the risks assumed by the third parties

involved…

…resulting in more beneficial terms

and conditions for the transaction

Increase the borrowing capacity of related entities.

Allow the beneficiary to tap resources that it could not access in the absence of a guarantee.

By ensuring fulfilment in case of performance failure, an intercompany guarantee may provide bettercontractual terms also in relation to commercial transactions.

SUPPLY CHAIN GUARANTEE

Purpose: reduce risk to customers of recipient

Main benefits: Secure payment The seller can obtain advance

payment Secured compensation for non-

fulfilment of any important obligations

Guarantees Benefits

PwC

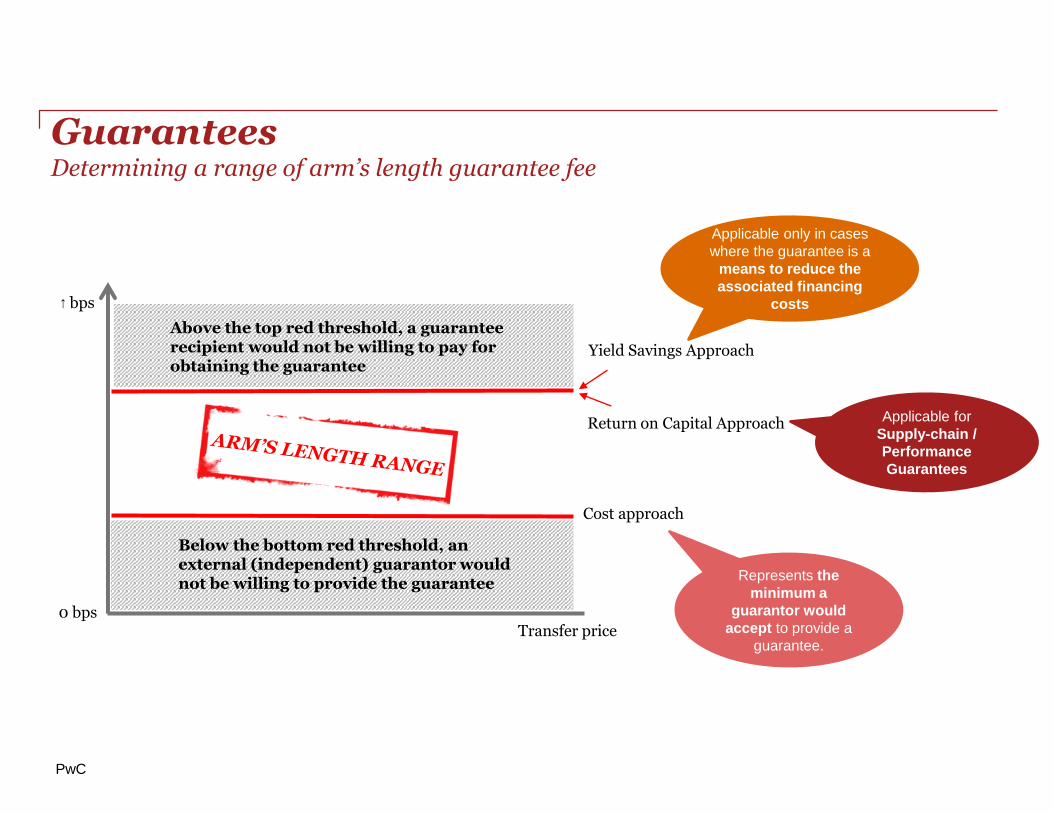

↑ bps

0 bps

Yield Savings Approach

Transfer price

Cost approach

Above the top red threshold, a guarantee recipient would not be willing to pay for obtaining the guarantee

Below the bottom red threshold, an external (independent) guarantor would not be willing to provide the guarantee

Return on Capital Approach

Applicable only in cases

where the guarantee is a

means to reduce the

associated financing

costs

Applicable for

Supply-chain /

Performance

Guarantees

Represents the

minimum a

guarantor would

accept to provide a

guarantee.

Guarantees Determining a range of arm’s length guarantee fee

PwC

Higher

Fees

Lower

Impact on the pricing

High PD High rate Long term High LGD On maturityHigher risk

currency

Low PD Low rate Short term Low LGDQuarterly (regular)

Lower risk currency

Credit quality assessment Terms of the underlying debt / transaction

Guarantees Factors influencing the guarantee pricing

PwC

Documentation requirements

Main focus areas

OECD BEPS – Action 13

Align transfer pricing outcome with value creation

PwC

Provides aggregated financial and tax data by tax jurisdiction to facilitate risk assessments

Complete picture of MNE’s global operations, including analysis of profit drivers, supply chains, intangibles, and financing

Detailed information relating to specific intercompany transactions. Assures compliance with arm’s length principle in material transfer pricing positions impacting a specific jurisdiction

Documentation requirementsOECD Base Erosion and Profit Shifting Action Item 13 - three-tiered approach

PwC

Action 13 - The Masterfile should include:

- “A general description how the group is financed, including important financing arrangements with unrelated parties”

- “The identification of any members of an MNE group that provide a central financing function for the group, including the country under whose laws the entity is organised and the place of effective management of such entities”

- “A general description of the MNE’s general transfer pricing policies related to financial arrangements between associated parties”

What is sufficient substance? Functional analysis

Does this differ for holding and financing activities?

What would best in class look like?

Entity having personnel with ability to evaluate, decline risk, and / or manage risk

Entity having capital to bear such risk

Treasury operations with appropriate substance Acknowledgement of financial risk

Documentation requirementsThe importance of a proper TP documentation

PwC

Identify

• Take an inventory of your intercompany financial transaction

Quantify

• Check the materiality of each transaction

Document

• Have discussion with treasury personnel to understand how these transactions are currently priced and what support may be on file

• Determine whether transfer pricing documentation already in place is current

Evaluate and support your intercompany financial transactionsDo not ignore them!

Documentation requirementsWhere to start?

PwC

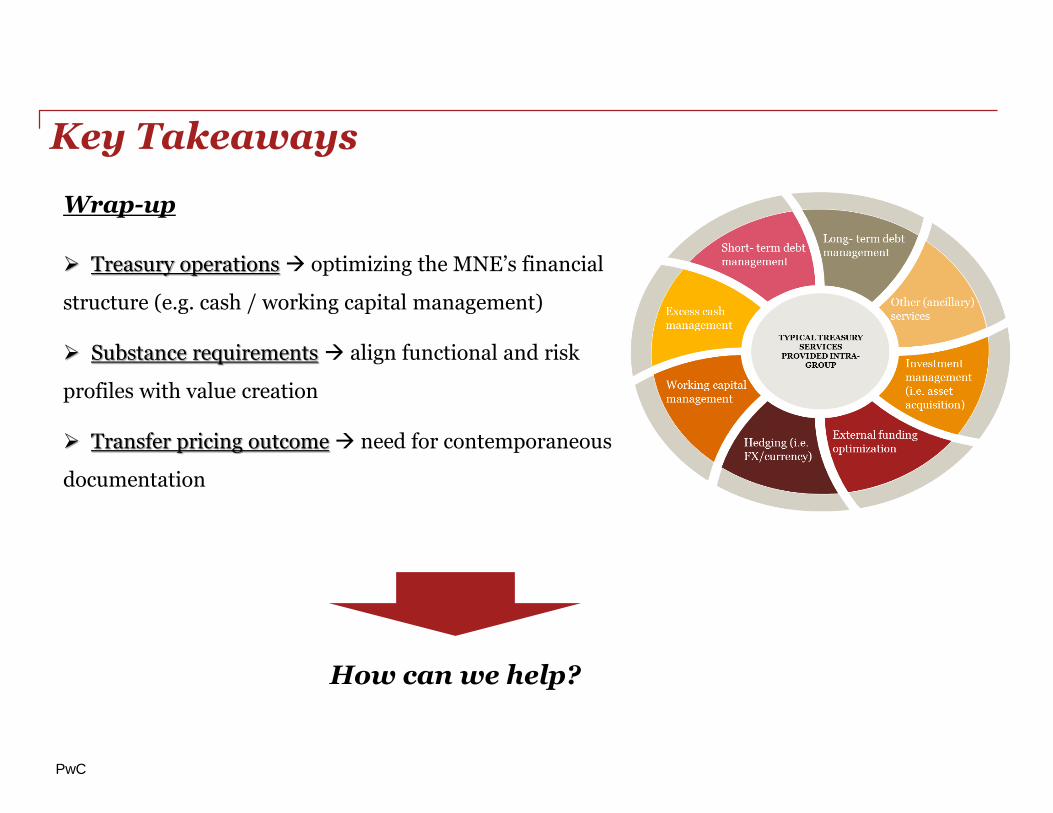

Key Takeaways

Wrap-up

Treasury operations optimizing the MNE’s financial

structure (e.g. cash / working capital management)

Substance requirements align functional and risk

profiles with value creation

Transfer pricing outcome need for contemporaneous

documentation

How can we help?

PwC

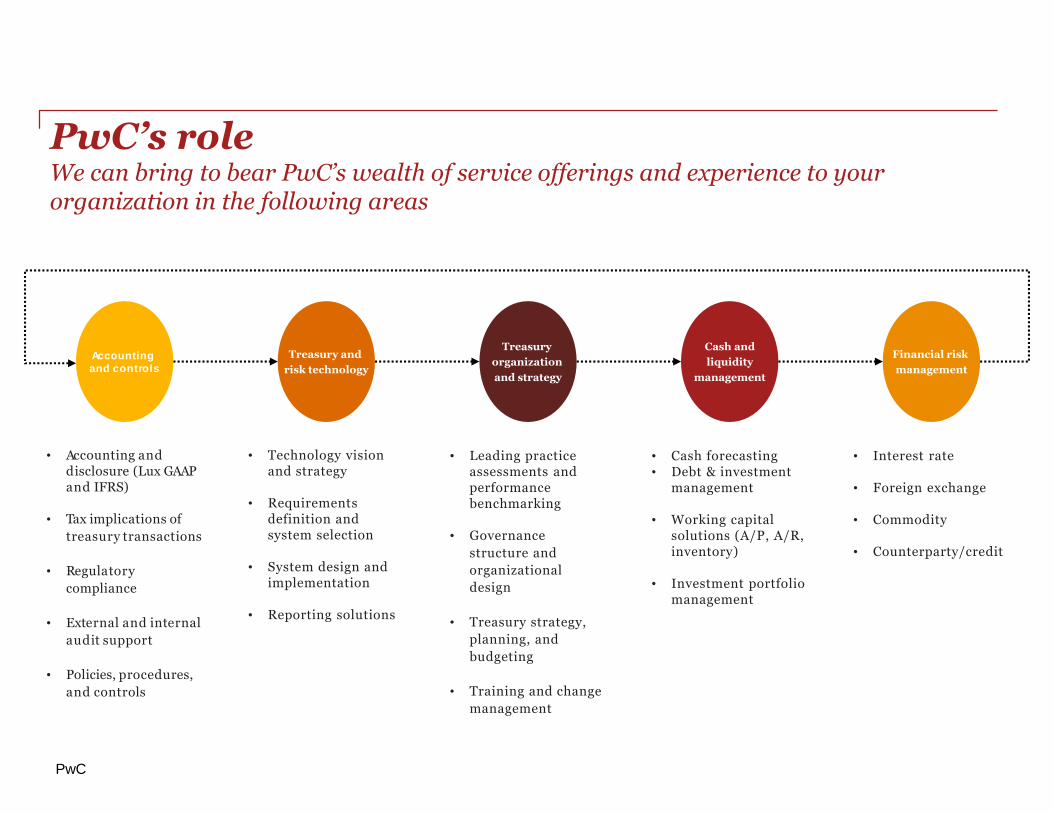

PwC’s roleWe can bring to bear PwC’s wealth of service offerings and experience to your organization in the following areas

Financial risk

management

Treasury and

risk technology

Accounting

and controls

Cash and

liquidity

management

Treasury

organization

and strategy

• Accounting anddisclosure (Lux GAAPand IFRS)

• Tax implications of

treasury transactions

• Regulatory

compliance

• External and internal

audit support

• Policies, procedures,

and controls

• Technology vision and strategy

• Requirements definition and system selection

• System design and implementation

• Reporting solutions

• Leading practice assessments and performance benchmarking

• Governance

structure and

organizational

design

• Treasury strategy,

planning, and

budgeting

• Training and change

management

• Cash forecasting• Debt & investment

management

• Working capital solutions (A/P, A/R, inventory)

• Investment portfolio management

• Interest rate

• Foreign exchange

• Commodity

• Counterparty/credit

PwC

Your contact at PwC Luxembourg

Christophe HillionPartner, Transfer Pricing

Philippe Förster Director, IFRS & Treasury Leader

Thomas CampioneSenior Manager, IFRS & Treasury

PwC

Thank you

© 2017 PricewaterhouseCoopers. All rights reserved. In this document, "PwC" refers to PricewaterhouseCoopers,Société coopérative (address: 2, rue Gerhard Mercator, B.P. 1443, L-1014 Luxembourg) which is a member firm ofPricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.