-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

1/11

1

Section I. Macro

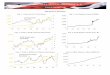

$0$200$400$600$800

$1,000$1,200$1,400

$1,600$1,800$2,000

2000 2002 2004 2006 2008 2010 2012-5%-4%-3%-2%-1%0%1%2%

3%4%5%Fig.1. Gold and US Real Rates

US Real RatesGold Price

Source: Bloomberg

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

1995 1999 2003 2007 2011

Fig.2. Fed Balance Sheet ($B)

Source: Bloomberg

-3%

-2%

-1%

0%

1%

2%

3%

4%

2000 2002 2004 2006 2008 2010 2012 0

200

400

600

800

1,000

1,200

1,400

1,600 Fig.3. Gold and ECB Real Rates

GoldECB Real Rates

Source: Bloomberg

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1999 2003 2007 2011

Fig.4 . ECB Balance Sheet ( B)

Source: Bloomberg

0

2,000

4,000

6,000

8,00010,000

12,000

14,000

2000 2002 2004 2006 2008 2010 2012-5%-4%-3%-2%-1%0%1%2%

3%4%5%Fig.5. Gold and PBC Real Rates

PBC Real RatesGold

Source: Bloomberg

0

5,000

10,000

15,000

20,00025,000

30,000

35,000

2003 2005 2007 2009 2011 2013

Fig.6. PBC Balance Sheet (CNY B)

Source: Bloomberg

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

2/11

2

Section I. Macro

$4

$6

$8

$10

$12

$14

$16

2006 2007 2008 2009 2010 2011 2012 2013

Fig.7 . The Biggest 6 Central Bank Balance SheetsUS, UK, Japan,

China, EU & Switzerland (US$T)

Source: Bloomberg

-5%

0%

5%

10%15%

20%

25%

1970 1980 1990 2000 2010

Fig.9. US M1 YoY%

Source: Bloomberg

0%

5%

10%

15%

1970 1980 1990 2000 2010

Fig.10. US M2 YoY%

Source: Bloomberg

0%

5%

10%

15%

20%

1999 2001 2003 2005 2007 2009 2011 2013

Fig.11. ECB M1 YoY %

Source: Bloomberg

0%

2%

4%

6%

8%10%

12%

1999 2001 2003 2005 2007 2009 2011 2013

Fig.12. ECB M2 YoY %

Source: Bloomberg

0%5%

10%15%20%25%30%35%40%

1996 2000 2004 2008 2012

Fig.13. PBC M1 YoY %

Source: Bloomberg

0%

5%

10%

15%

20%

25%

30%

35%

1996 2000 2004 2008 2012

Fig.14. PBC M2 YoY %

Source: Bloomberg

$0

$10

$20

$30

$40

$50

1999 2003 2007 2011$0

$500

$1,000

$1,500

$2,000

h o u s a n

d s

Fig.8. Gold and M2 (US$B; Fed, ECB, PBC)

Gold

M2

Source: Bloomberg

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

3/11

3

Section I. Macro

Fig.15 . Inflation

US Euro Area ChinaHeadline CPI 1.2 0.9 3.0

Core CPI 1.7 0.9 n/a

Shadowstats 8.8 n/a n/a

0%

5%

10%

15%

20%

25%

2013200920052001199719931989

Fig.20. Interest Expense as % of TotalGovernment Outlays

Source: Bloomberg; US Treasury

$13

$14

$15

$16

$17

$18

2011 2012 2013 201

Fig.18. The Debt Ceiling ($T)

Total Federal Debt

Debt Ceiling Limit

Source: Bloomberg

Source: Bloomberg, Shadow Government Statistics. As of

11/30/2013

2.0%

2.5%3.0%

3.5%4.0%

4.5%5.0%

5.5%6.0%

6.5%7.0%

2000 2002 2004 2006 2008 2010 2012

Fig.19. Average Annual Interest Rate on USDebt

Source: US Treasury, Meridian Macro.

$0

$5

$10

$15

$20

$25

1940 1950 1960 1970 1980 1990 2000 2010

Fig.16. US National Debt ($T)

Source: TreasuryDirect.gov, USDebtClock.org

120%

170%

220%

270%

320%

370%

1947 1957 1967 1977 1987 1997 2007

Fig.17. US Debt as % of GDP

Source: Bloomberg

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

4/11

4

Section I. Macro

-$20

$20

$60

$100

$140

$180

$220

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Fig.23. China Net Purchases Long-Term US Securities(annual

US$B)

Source: US Treasury; MacroMavens, LLC

-$100

$400

$900

$1,400

$1,900

2005 2006 2007 2008 2009 2010 2011 2012 2013

Fig.21. Global Forex Accumulation(US$B, 12 month sum)

Source: Bloomberg; MacroMavens, LLC

-$100

$100

$300

$500

$700

1978 1983 1988 1993 1998 2003 2008 2013

Fig.22. Net Purchases of US Treasury Notes and Bonds by All

ForeignCountries (US$B, 12 month sum)

Source: US Treasury; MacroMavens, LLC

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

5/11

5

Section II. Gold

19.6%21.8%

3.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1934 1982 3Q2013

Fig.25. Market Cap of Above Ground Gold as % of Total US

FinancialAssets

Source: Federal Reserve, World Gold Council

0

40

80

Oct-03 Oct-05 Oct-07 Oct-09 Oct-11 Oct-13

M i l l i o n s o

f O u n c e s

Fig.26. Gold Held by ETFs

All ETFS

SPDR Trust

Source: Bloomberg, Company Filings.

Fig.24. Gold Supply and Demand (tonnes) 2002 2003 2004 2005 2006

2007 2008 2009 2010 2011 2012 3Q13

Supply

Mine production 2,591 2,592 2,478 2,550 2,481 2,476 2,409 2,584

2,739 2,827 2,848 2,188

Old gold scrap 835 944 829 886 1,107 956 1,217 1,672 1,723 1,669

1,626 1,047

Traditional supply 3,426 3,536 3,307 3,436 3,588 3,432 3,626

4,257 4,463 4,495 4,473 3,235Net producer hedging (412) (279) (445)

(86) (373) (444) (349) (252) (108) 10 (20) (39)

Official sector sales 545 617 497 662 367 484 236 30 - - - -

Total supply 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034

4,355 4,505 4,453 3,196

Demand

Jewellery 2,680 2,522 2,673 2,707 2,283 2,405 2,187 1,760 2,017

1,972 1,908 1,645

Other 360 385 416 431 458 462 436 373 466 453 428 309

Total fabrication 3,040 2,907 3,089 3,138 2,741 2,867 2,623

2,134 2,483 2,425 2,336 1,954

Bar & coin retail investment 373 314 396 412 421 446 649 743

1,205 1,519 1,256 1,252

Official sector purchases - - - - - - - - 77 457 535 297

ETFs & similar 3 39 133 208 260 253 321 617 382 185 279

(697)Implied net investment 143 614 (259) 254 160 (94) (80) 541 207

(81) 47 390

Total demand 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034

4,355 4,505 4,453 3,196Source: World Gold Council

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

6/11

6

Section II. Gold

InvestmentAdviser,19.80%

Broker, 9.90%

PrivateBanking, 3.10%

Pension Fund,0.40%

Hedge Fund,5.80%Mutual Fund,

3.20%

InsuranceCompany,

0.20%

Non-Institutional,

60.70%

Fig.27. SPDR Gold Trust Ownership by Type

Source: FactSet

00 01 02 03 04 05 06 07 08 09 10 11 12 3Q13

-600-500-400-300-200

-1000

100200300400500600 Fig.29. Central Banks Net Purchases

(tonnes)

Source: World Gold Council

29,500

30,000

30,500

31,000

31,500

32,000

32,50033,000

33,500

34,000

3/00 3/02 3/04 3/06 3/08 3/10 3/12

Fig.30. Central Banks Holdings of Gold(tonnes)

Source: World Gold Council

Fig.28. Notable Transaction in October 2013

Country Tonnes TransactionKazakhstan 2.4 PurchaseAzerbaijan 2.0

Purchase

Turkey 13.0 AdditionSource: World Gold Council

8%

9%

10%

11%

12%

13%

14%

3/00 3/02 3/04 3/06 3/08 3/10 3/12

Fig.31. Gold as % of Total Reserves

Source: World Gold Council

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

7/11

7

Section II. Gold

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013

Fig.32 . Web searches for "Gold Bubble"

Source: GoogleTrends

0

20

40

60

80

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Fig.33. Web searches for "Gold Investment"

Source: GoogleTrends

$0$200$400$600$800$1,000$1,200$1,400$1,600

$1,800$2,000

0

20

40

6080

100

2006 2007 2008 2009 2010 2011 2012 2013

Fig.34 . Bernstein's Daily Sentiment Index

DSIGold

Source Bloomberg, Bernstein's DSI

$400$600$800$1,000$1,200$1,400$1,600$1,800$2,000

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013

Fig.35. Market Vane Bullish Consensus

Market VaneGold

Source Bloomberg, Market Vane

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

8/11

8

Section II. Gold

$0$200$400$600$800$1,000$1,200$1,400

$1,600$1,800$2,000

800

1000

1200

1400

1600

1800

2000

2006 2008 2010 2012

Fig.36. Comex Gold Futures Open Interest(tonnes)

Open Interest

Gold

Source: Bloomberg

-20%

80%

180%

280%

380%

480%

2000 2002 2004 2006 2008 2010 2012

Fig.37. Gold vs ContinuousCommodity Index

CCI Index

Gold

Source: Bloomberg

$500

$700

$900

$1,100

$1,300

$1,500$1,700

$1,900

0%

20%

40%

60%

80%

100%

7/10 7/11 7/12 7/13

Fig.39. Commercial Net Shorts as % of TotalOpen Interest

Net Short/Open InterestGold

Source: Bloomberg; The McClellan Market Report

More Net Short

Less Net Short

$0

$500

$1,000

$1,500

$2,000

-1,000

-800

-600

-400

-200

0

200

400

600

800

1,000

2006 2007 2008 2009 2010 2011 2012 2013

Fig.38. Comex Gold Futures Activity (tonnes)Net Large

SpeculatorsNet Hedgers/CommercialsGold

Source: CFTC

0

1020

30

40

5060

70

8090

0

1

2

3

4

5

6

2003 2005 2007 2009 2011 2013

M i l l i o n s o

f O u n c e s

Fig. 40 . Registered COMEX Gold Stocks vs.Owners per Ounce

Registered Stocks

Owners per Ounce

Source: Bloomberg

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

9/11

9

Section III. Gold Mining Equities

0%

10%

20%

30%

40%

50%

60%

70%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Fig.41. XAU and HUI as a Ratio of Gold

HUI/GoldXAU/Gold

Source: FactSet

-$3,000

-$2,000

-$1,000

$0

$1,000

$2,000

$3,000

$4,000

1 H 0 7

2 H 0 7

1 H 0 8

2 H 0 8

1 H 0 9

2 H 0 9

1 H 1 0

2 H 1 0

1 H 1 1

2 H 1 1

1 H 1 2

2 H 1 2

1 H 1 3

Fig.42. Net Fund Flows For Lipper's EquityPrecious Metals Fund

Universe ($M)

Source: Morningstar2H13 - as of 11/30/13

$0

$2$4

$6

$8

$10

$12

$14

$16

5/06 5/07 5/08 5/09 5/10 5/11 5/12 5/13

Fig.43. Market Cap of Van Eck Gold EquityETFs ($B)

Source: FactSet

0

50

100

150

200

250

300

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

00 01 02 03 04 05 06 07 08 09 10 11 12 13

Fig.44. Equity Capital Issued by Gold Miners

$B of Equty Issued

# of Transactions

Source: RBC Capital Markets

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

10/11

-

8/13/2019 Tocqueville Gold Monitor 4Q 2013

11/11

11

Section III. Gold Mining Equities

Source: BMO Capital Markets

Source: BMO Capital Markets

Fig.49. Gold Price Discounted by Market ($/Oz)

Fig.50. NAV Premiums Senior & Intermediate Producers

(N.A.)

Source: ScotiabankSource: Scotiabank

Fig.51. P/CF Universe of Coverage AverageFig.52. Adjusted Market

Cap per Oz of Resource

Divided by Gold Price