Embed Size (px)

Citation preview

TMB Bank Plc.

To be the most advocated bank in Thailand

Investor Presentation - TMB 5-Year Plan

Contents

➢ Aspiration & Strategy

➢ TMB Journey

➢ TMB 5-Year Plan

➢ Make THE Difference Story

Appendix

2018 Financial Targets

2

TMB Aspiration & Strategy

Ripple out Make THE Difference philosophy

3

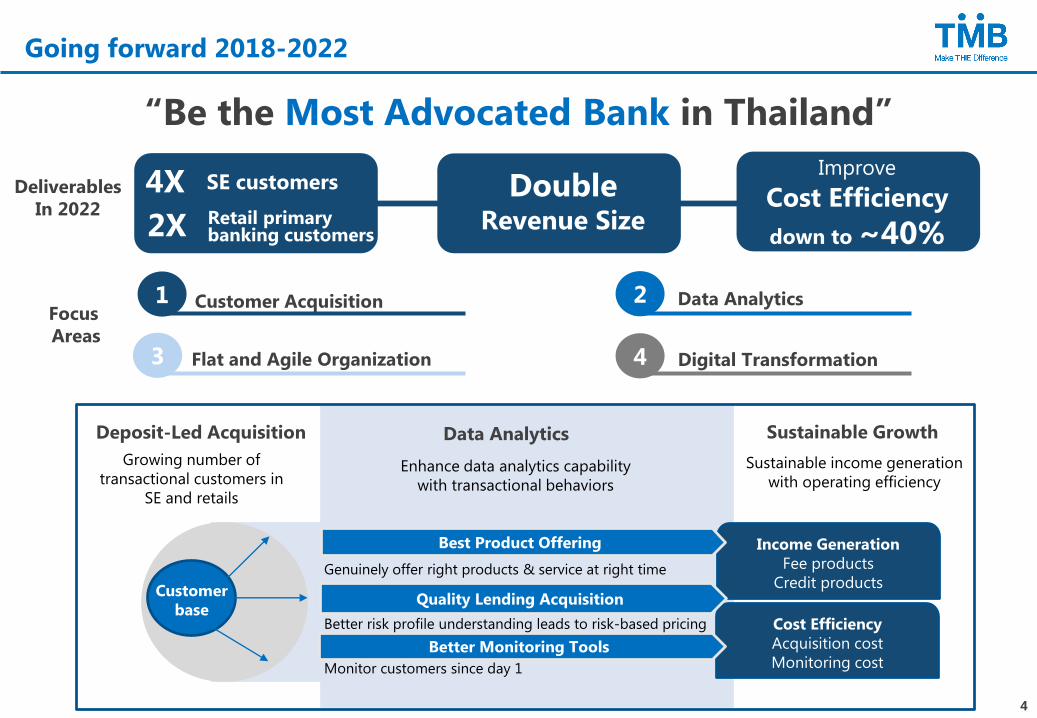

Going forward 2018-2022

Deposit-Led Acquisition

Enhance data analytics capability

with transactional behaviors

Growing number of

transactional customers in

SE and retails

Data Analytics

Income Generation

Fee products

Credit products

Cost Efficiency

Acquisition cost

Monitoring cost

Quality Lending Acquisition

Best Product Offering

Better Monitoring Tools

Sustainable Growth

Customer

base

Genuinely offer right products & service at right time

Better risk profile understanding leads to risk-based pricing

Monitor customers since day 1

Sustainable income generation

with operating efficiency

“Be the Most Advocated Bank in Thailand”

1 Data Analytics2Customer Acquisition

Flat and Agile Organization3 4 Digital Transformation

Focus

Areas

4X DoubleRevenue Size

Improve

Cost Efficiency

down to ~40% 2X

SE customers

Retail primary banking customers

Deliverables

In 2022

4

More diversified deposit base through SE and Retail

20%

20%

60%

22%

8%

70%

Deposit by Segments

F20222017

SE

Retail

Large Corporate

611 bn

F20222017

Deposit by Products

Non

-

Trxn

55%

Trxn

45%

Non

-

Trxn

60%

Trxn

40%

611 bn

Acquire SE

Operating Account

➢ Unique transactional excellence by “SME One Bank,

the awarded winning “SME Product of the Year

2017” would allow us to acquire new customers

and grow deposit volume

➢ With superior retail transactional deposit, TMB will

continue to acquire new customers through more

primary banking benefits

▪ Uplift banking experience to fit with customers’

lifestyle with TMB WoW

TMB All Free

Acquire Retail

Transactional Account

TMB WOW

Going forward, TMB will continue to build stable

deposit base by growing more diversified retail

as well as SE deposits

5

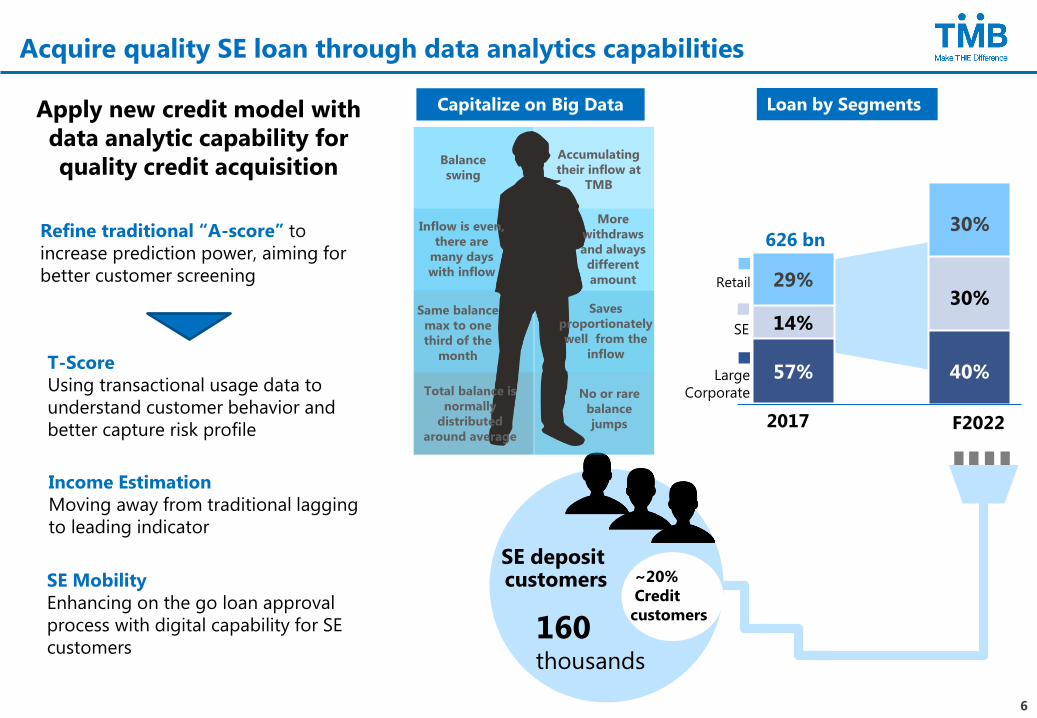

Acquire quality SE loan through data analytics capabilities

Apply new credit model with

data analytic capability for

quality credit acquisition

Loan by Segments

F20222017

SE

Large

Corporate

Retail

626 bn30%

30%

40%

29%

14%

57%

160thousands

SE deposit customers ~20%

Credit

customers

Capitalize on Big Data

T-Score

Using transactional usage data to

understand customer behavior and

better capture risk profile

Income Estimation

Moving away from traditional lagging

to leading indicator

SE Mobility

Enhancing on the go loan approval

process with digital capability for SE

customers

Refine traditional “A-score” to

increase prediction power, aiming for

better customer screening

Accumulating

their inflow at

TMB

Balance

swing

More

withdraws

and always

different

amount

Inflow is even,

there are

many days

with inflow

Saves

proportionately

well from the

inflow

Same balance

max to one

third of the

month

Total balance is

normally

distributed

around average

No or rare

balance

jumps

6

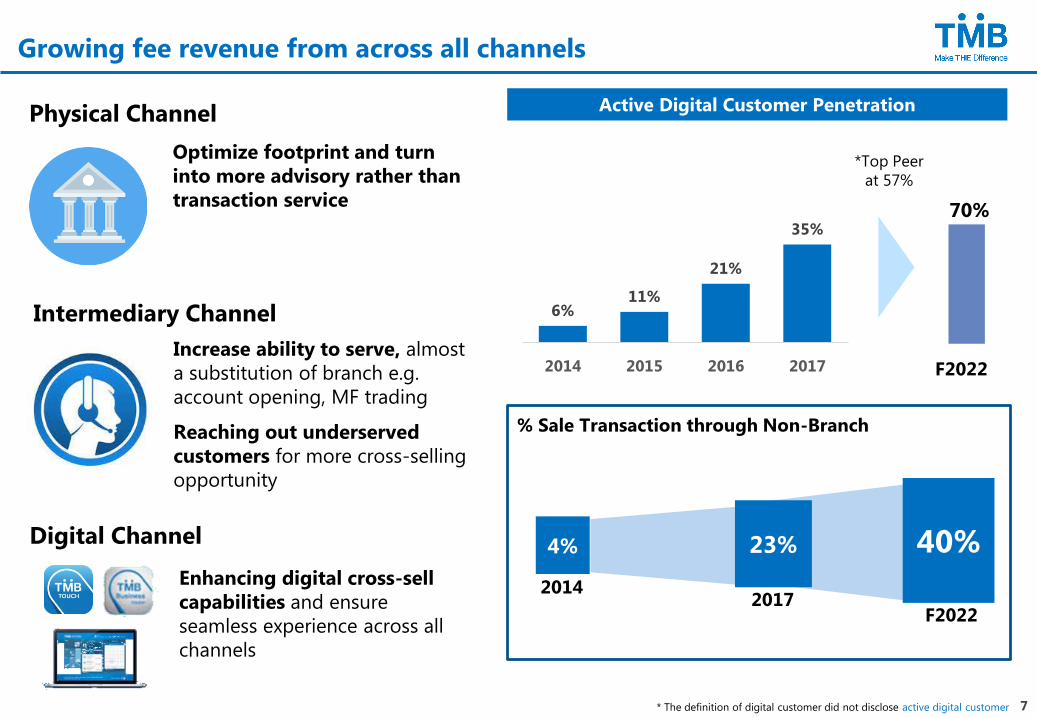

Growing fee revenue from across all channels

Active Digital Customer Penetration

70%

% Sale Transaction through Non-Branch

4% 40%

F2022

*Top Peer

at 57%

Optimize footprint and turn

into more advisory rather than

transaction service

Increase ability to serve, almost

a substitution of branch e.g.

account opening, MF trading

Reaching out underserved

customers for more cross-selling

opportunity

Physical Channel

Intermediary Channel

Digital Channel 23%

20142017

F2022

Enhancing digital cross-sell

capabilities and ensure

seamless experience across all

channels

6%11%

21%

35%

2014 2015 2016 2017

* The definition of digital customer did not disclose active digital customer 7

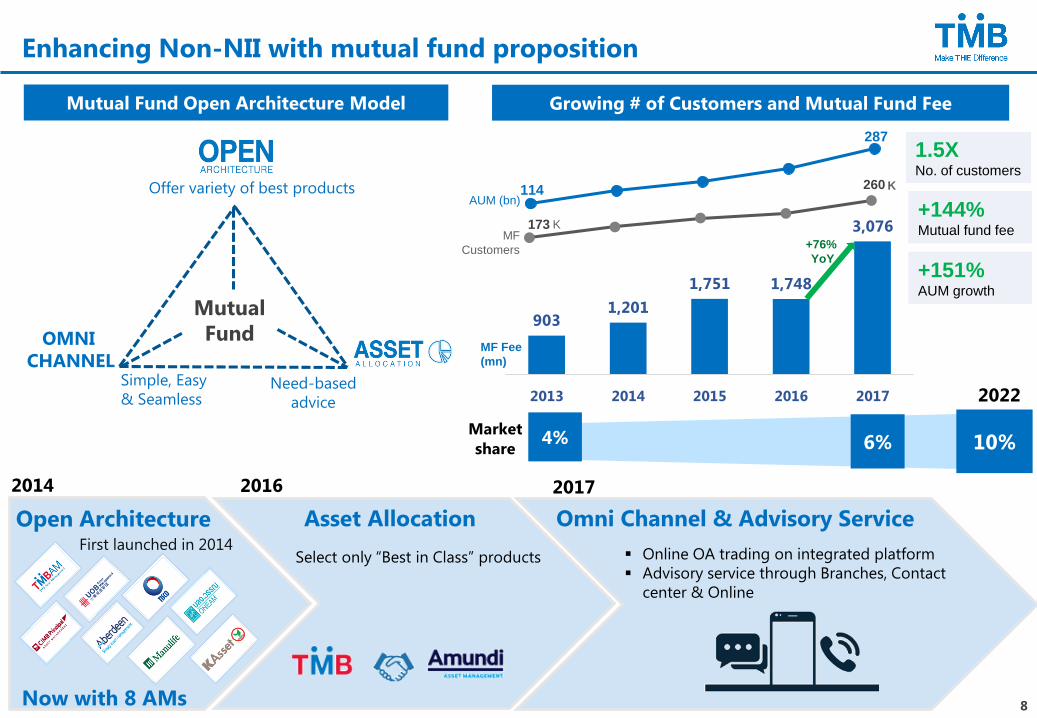

Enhancing Non-NII with mutual fund proposition

Market

share

Growing # of Customers and Mutual Fund Fee

4% 6% 10%

Open Architecture

2022

2014 2016 2017

Asset Allocation

Select only “Best in Class” productsFirst launched in 2014

Omni Channel & Advisory Service

▪ Online OA trading on integrated platform

▪ Advisory service through Branches, Contact

center & Online

Mutual Fund Open Architecture Model

OMNI

CHANNEL

Offer variety of best products

Need-based

advice

Simple, Easy

& Seamless

Now with 8 AMs

Mutual

Fund

1.5XNo. of customers

+144% Mutual fund fee 173

260

9031,201

1,751 1,748

3,076

2013 2014 2015 2016 2017

+76%

YoY

MF Fee

(mn)

AUM (bn)

MF

Customers

+151% AUM growth

K

K114

287

8

Strategic

Collaboration

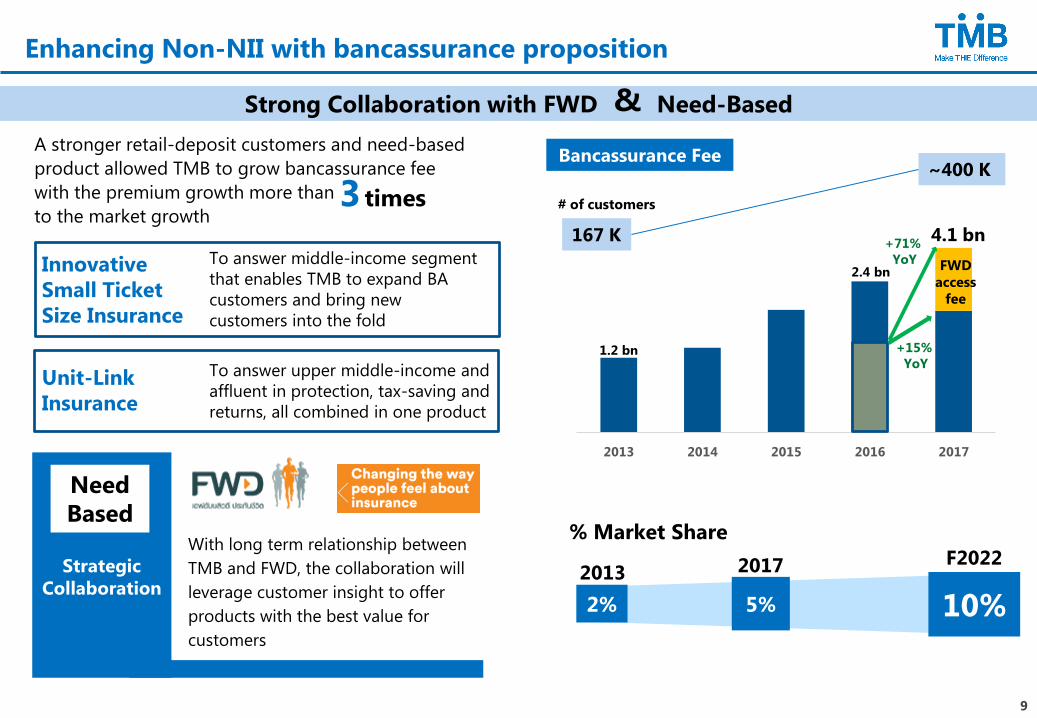

Enhancing Non-NII with bancassurance proposition

A stronger retail-deposit customers and need-based

product allowed TMB to grow bancassurance fee

with the premium growth more than

to the market growth

% Market Share

5% 10%

2017 F2022

2%

2013

With long term relationship between

TMB and FWD, the collaboration will

leverage customer insight to offer

products with the best value for

customers

Strong Collaboration with FWD Need-Based&

3 times

Need

Based

Innovative

Small Ticket

Size Insurance

To answer middle-income segment

that enables TMB to expand BA

customers and bring new

customers into the fold

Unit-Link

Insurance

To answer upper middle-income and

affluent in protection, tax-saving and

returns, all combined in one product

1.2 bn

2013 2014 2015 2016 2017

+15%

YoY

+71%

YoY

4.1 bn

Bancassurance Fee

FWD

access

fee

167 K

~400 K

# of customers

2.4 bn

9

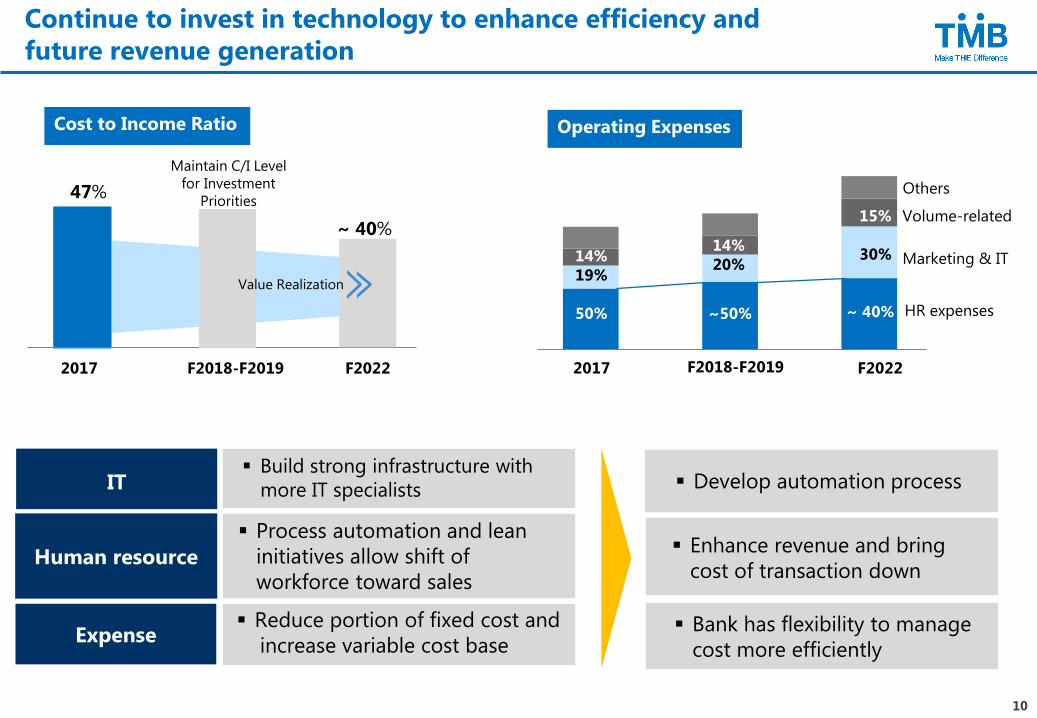

Continue to invest in technology to enhance efficiency and

future revenue generation

F2018-F2019 F2022

Maintain C/I Level

for Investment

Priorities

Cost to Income Ratio

~ 40%

47%

2017

IT▪ Build strong infrastructure with

more IT specialists ▪ Develop automation process

Human resource

▪ Process automation and lean

initiatives allow shift of

workforce toward sales

F2018-F2019 F20222017

HR expenses

Marketing & IT

Others

Operating Expenses

14%

19%

50%

14%

20%

~50%

15%

30%

~ 40%

Expense▪ Reduce portion of fixed cost and

increase variable cost base▪ Bank has flexibility to manage

cost more efficiently

Value Realization

▪ Enhance revenue and bring

cost of transaction down

Volume-related

10

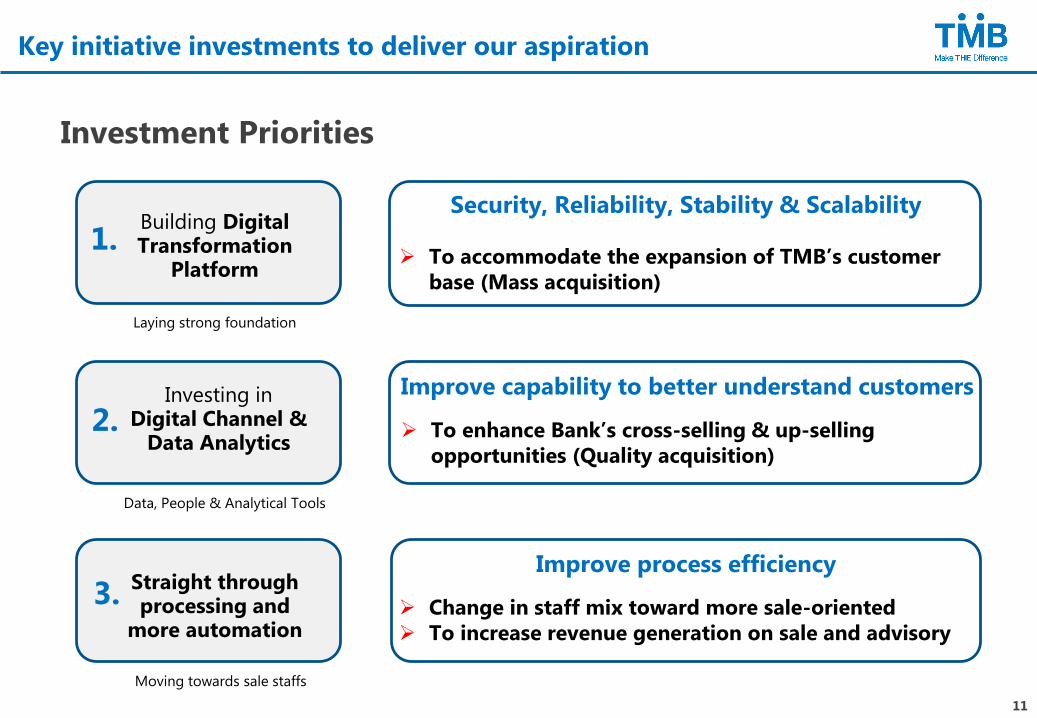

Key initiative investments to deliver our aspiration

Investment Priorities

Building Digital Transformation

Platform

1.

Investing in Digital Channel &

Data Analytics2.

3. Straight through processing and

more automation

Moving towards sale staffs

Data, People & Analytical Tools

Laying strong foundation

➢ To accommodate the expansion of TMB’s customer

base (Mass acquisition)

➢ To enhance Bank’s cross-selling & up-selling

opportunities (Quality acquisition)

Improve capability to better understand customers

Improve process efficiency

Security, Reliability, Stability & Scalability

➢ Change in staff mix toward more sale-oriented

➢ To increase revenue generation on sale and advisory

11

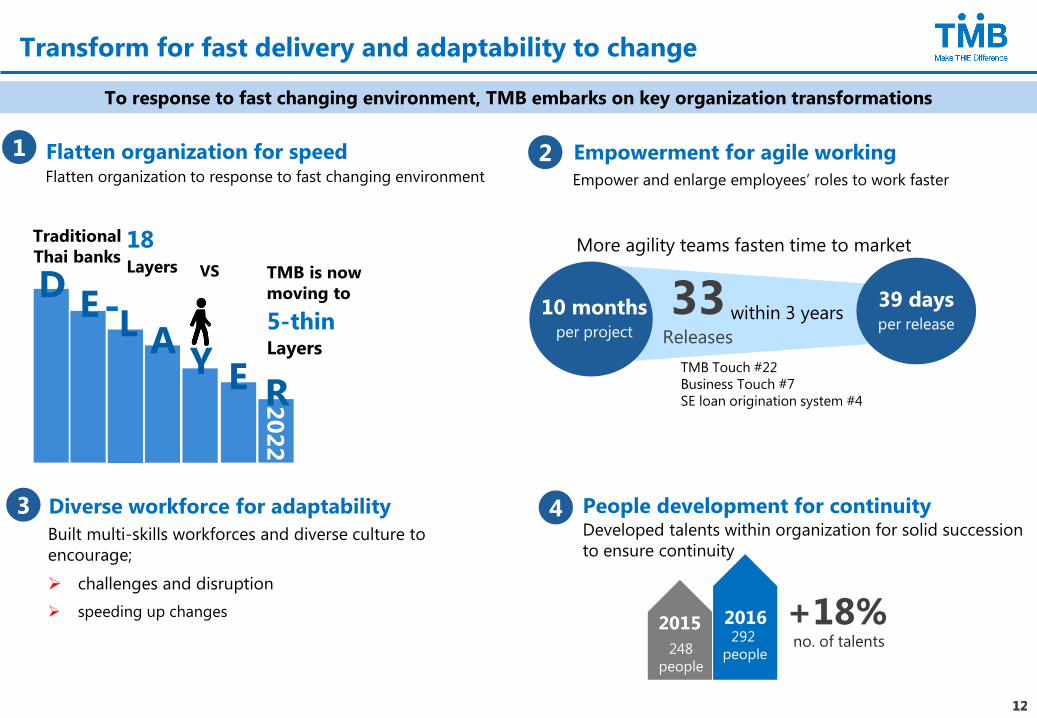

Transform for fast delivery and adaptability to change

Traditional

Thai banks18 Layers

5-thinLayers

39 days per release

10 monthsper project

Flatten organization for speed

33Releases

within 3 years

To response to fast changing environment, TMB embarks on key organization transformations

Built multi-skills workforces and diverse culture to

encourage;

➢ challenges and disruption

➢ speeding up changes

Developed talents within organization for solid succession

to ensure continuity

292

people

DE

L AY E

20

22

R

no. of talents

TMB Touch #22

Business Touch #7

SE loan origination system #4

Empowerment for agile working

VS

Diverse workforce for adaptability

More agility teams fasten time to market

People development for continuity

+18%2016292

people

2015

248

people

1 2

3 4

TMB is now

moving to

-

Empower and enlarge employees’ roles to work fasterFlatten organization to response to fast changing environment

1212

TMB’S TRANSFORMATION JOURNEY

Grow customer base

Improve income generation both NII and Non-NII

Lower cost to income through lean initiatives

Grow quality profit

Strengthen financial position and capital base

13

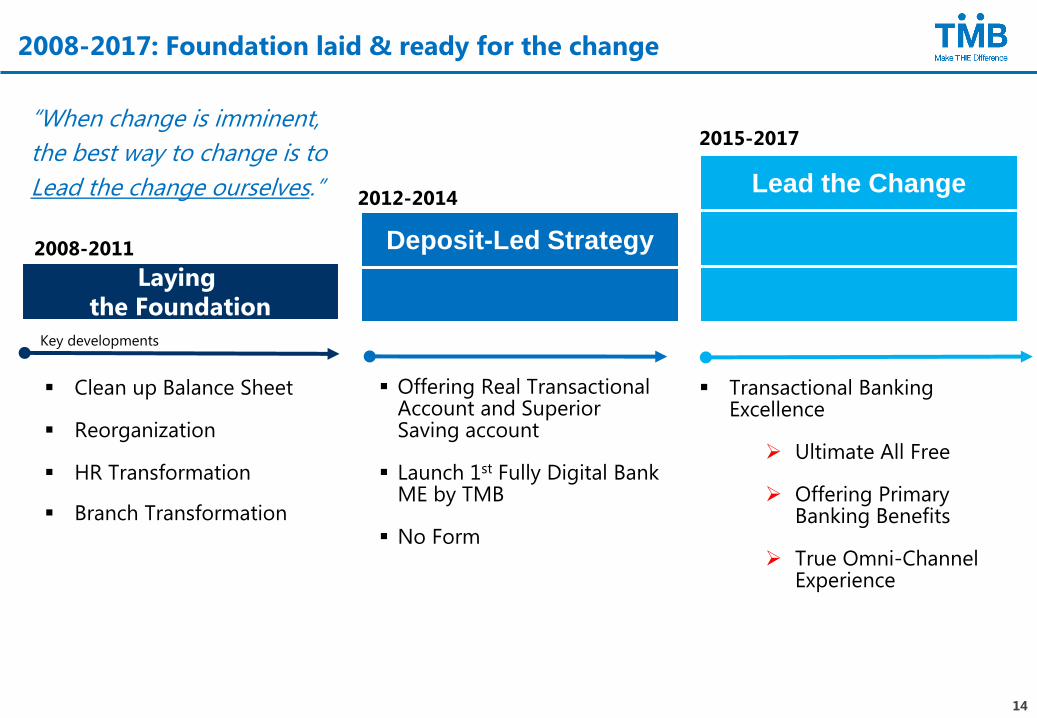

2008-2017: Foundation laid & ready for the change

2008-2011 Deposit-Led Strategy

Lead the Change

Laying the Foundation

2012-2014

2015-2017

▪ Offering Real Transactional Account and Superior Saving account

▪ Launch 1st Fully Digital Bank ME by TMB

▪ No Form

▪ Transactional Banking Excellence

➢ Ultimate All Free

➢ Offering Primary Banking Benefits

➢ True Omni-Channel Experience

Key developments

“When change is imminent,

the best way to change is to

Lead the change ourselves.”

▪ Clean up Balance Sheet

▪ Reorganization

▪ HR Transformation

▪ Branch Transformation

14

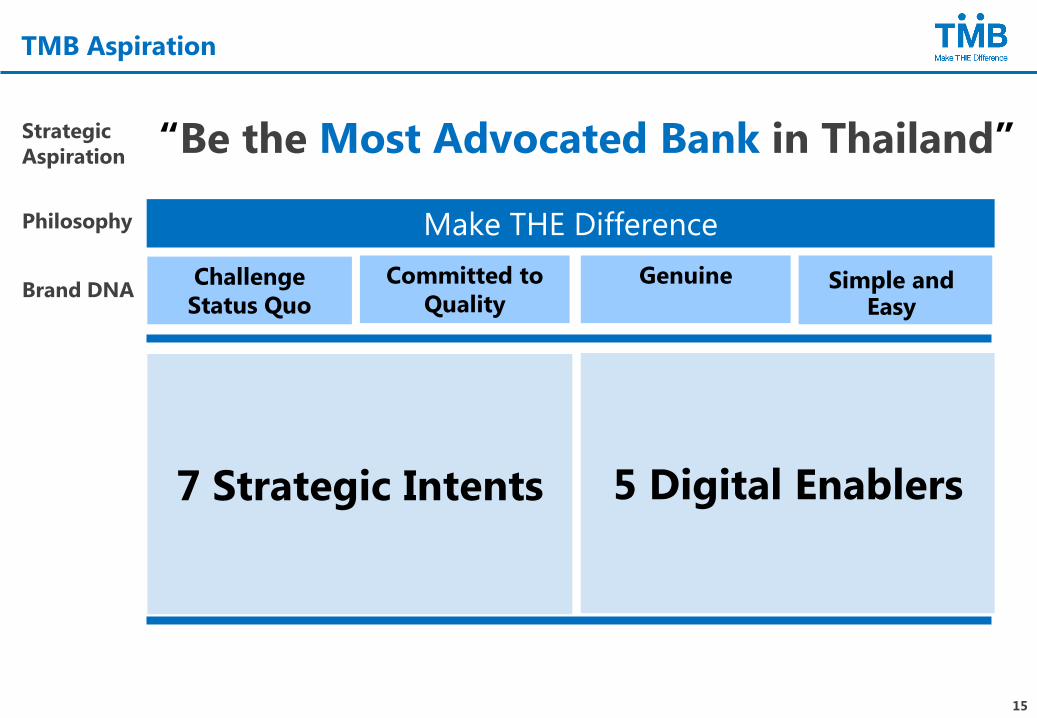

TMB Aspiration

“Be the Most Advocated Bank in Thailand”

Challenge

Status Quo

Committed to

Quality

GenuineBrand DNA

Make THE DifferencePhilosophy

Strategic

Aspiration

7 Strategic Intents

Simple and Easy

5 Digital Enablers

15

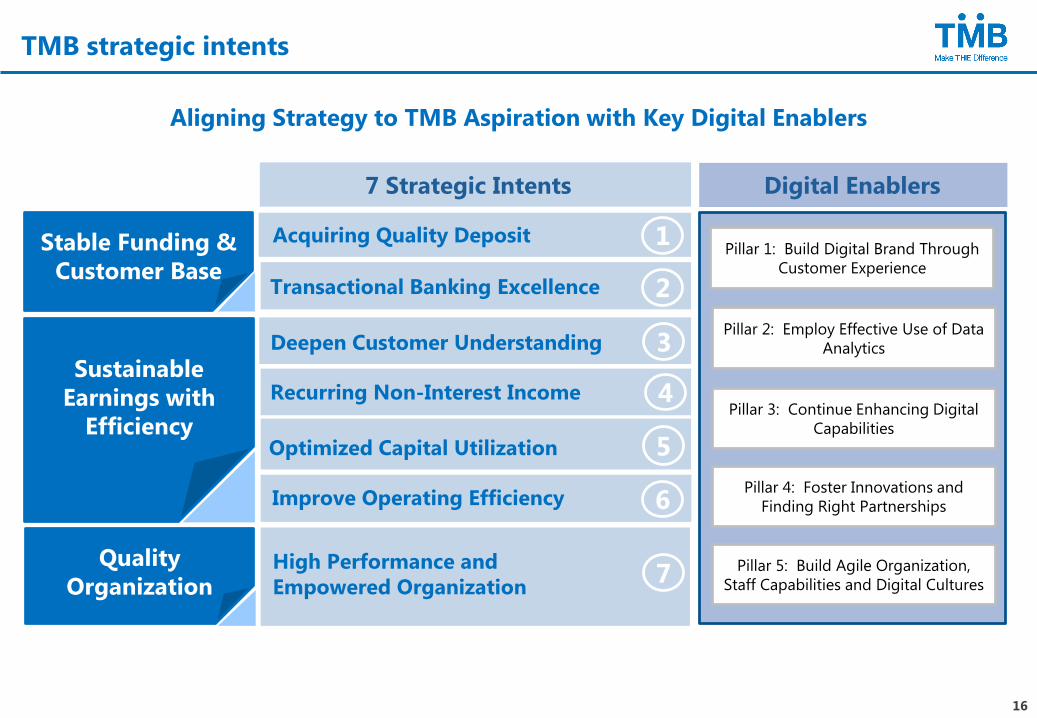

TMB strategic intents

Acquiring Quality DepositPillar 1: Build Digital Brand Through

Customer Experience

Stable Funding &

Customer BaseTransactional Banking Excellence

Sustainable

Earnings with

Efficiency

Recurring Non-Interest Income

Optimized Capital Utilization

Improve Operating Efficiency

Quality

Organization

7 Strategic Intents

Deepen Customer Understanding

High Performance and

Empowered Organization

1

2

3

4

5

6

7

Digital Enablers

Pillar 2: Employ Effective Use of Data

Analytics

Pillar 3: Continue Enhancing Digital

Capabilities

Pillar 4: Foster Innovations and

Finding Right Partnerships

Pillar 5: Build Agile Organization,

Staff Capabilities and Digital Cultures

Aligning Strategy to TMB Aspiration with Key Digital Enablers

16

4

1619

3840

50

2009 2010 2011 2012 2013 2014 2015 2016 9M17

2009 2010 2011 2012 2013 2014 2015 2016 9M17

Growing customer base and optimize deposit mix

1.64% 1.36%

1.85%

1.30%

4 Big-banks TMB

Growing quality deposit

CASA

50%

TD

50%

Trxn

Non

Trxn

Deposit by Product & Cost of deposit

# New All Free Deposit Accounts

Avg new account per month

(‘000 accounts)

Trxn

Non

Trxn 65%

86%

2.2 mnno. of

customers

2nd Lowest

CoD

TMB challenges market

status quo by forgoing

cross regional and other

hidden fees since 2012

➢ Through our superior products, TMB could acquire

customer base at accelerated pace from better value

proposition products that genuinely offered to

customers

➢ Deposit structured has shifted toward retail base,

creating more stable funding source with less

concentration from large depositors

➢ Replacing traditional deposit products with

Transactional and Non-Transactional deposit, cost of

deposit has improved and now on par with peers

2017

20172009 2010 2011 2012 2013 2014 2015 2016 9M17

611 bn

Deposit by Segment

408 bn

Retail

60%

Retail

70%

201717

2009 2010 2011 2012 2013 2014 2015 2016 9M17

20%

27%

53%

316 bn

626 bn

6.3%

5.26%

4.6% 5.14%

2009 2010 2011 2012 2013 2014 2015 2016 9M17

4 Big-banks TMB

Large corporate

Retail

SME

Performing Loan by Segment

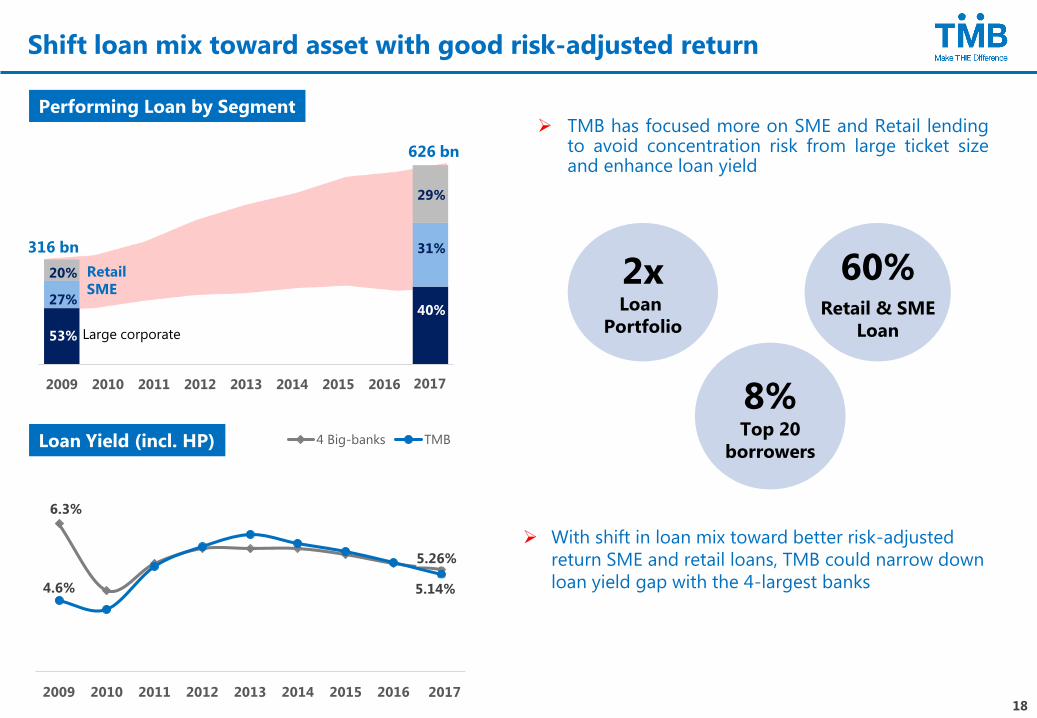

Shift loan mix toward asset with good risk-adjusted return

29%

31%

40%

2xLoan

Portfolio

60%Retail & SME

Loan

Loan Yield (incl. HP)

➢ TMB has focused more on SME and Retail lending to avoid concentration risk from large ticket size and enhance loan yield

➢ With shift in loan mix toward better risk-adjusted

return SME and retail loans, TMB could narrow down

loan yield gap with the 4-largest banks

8%Top 20

borrowers

2017

201718

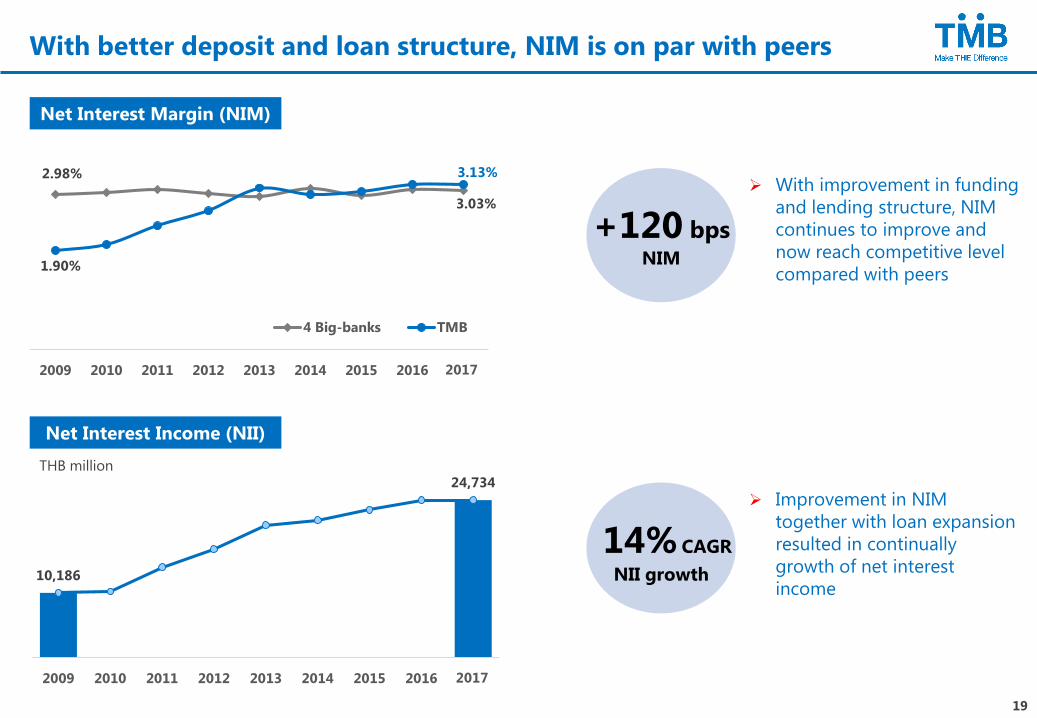

With better deposit and loan structure, NIM is on par with peers

2.98%

3.03%

1.90%

3.13%

2009 2010 2011 2012 2013 2014 2015 2016 9M17

4 Big-banks TMB

10,186

24,734

2009 2010 2011 2012 2013 2014 2015 2016

THB million

Net Interest Income (NII)

+120 bpsNIM

14% CAGR

NII growth

Net Interest Margin (NIM)

➢ With improvement in funding

and lending structure, NIM

continues to improve and

now reach competitive level

compared with peers

➢ Improvement in NIM

together with loan expansion

resulted in continually

growth of net interest

income

2017

2017

19

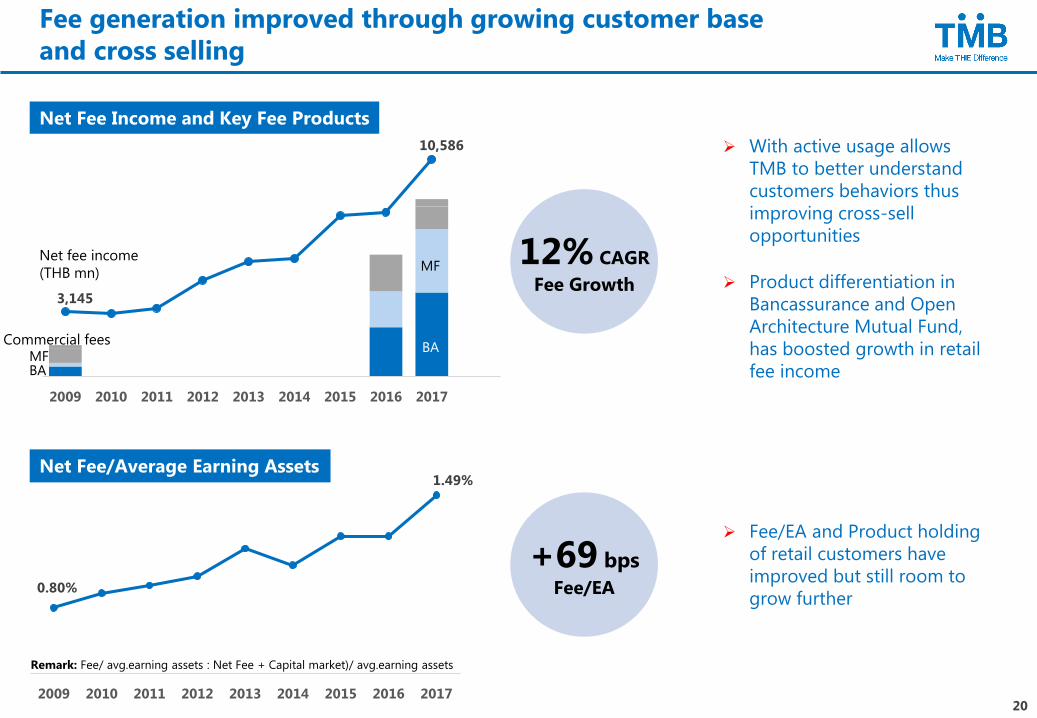

Fee generation improved through growing customer base

and cross selling

3,145

10,586

2009 2010 2011 2012 2013 2014 2015 2016 2017

BAMF

Commercial fees

Net Fee Income and Key Fee Products

Net fee income

(THB mn)

0.80%

1.49%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Net Fee/Average Earning Assets

Remark: Fee/ avg.earning assets : Net Fee + Capital market)/ avg.earning assets

MF

BA

12% CAGR

Fee Growth

+69 bps

Fee/EA

➢ With active usage allows

TMB to better understand

customers behaviors thus

improving cross-sell

opportunities

➢ Product differentiation in

Bancassurance and Open

Architecture Mutual Fund,

has boosted growth in retail

fee income

➢ Fee/EA and Product holding

of retail customers have

improved but still room to

grow further

20

2,361 2,054

2009 2010 2011 2012 2013 2014 2015 2016 2017

-25 pptC/I ratio

+57%digital

customers

482431

2009 2010 2011 2012 2013 2014 2015 2016 9M17

431 1,120

2.0 mn

2.5 mn

2011 2017

➢ Enhancing digital self-service solution delivers a variety

of personalized preference to support digital trends

▪ Online Mutual Fund Trading

▪ TMB So GoooD (TMB installment program)

▪ Online account opening, card issuance and cancellation

➢ With lean initiatives and channel optimization, TMB was

able to achieved cost to income ratio at 46% level

Branches

ATMs

No. of Active Retail & Digital Customers

TMB

72%

47%

2009 2010 2011 2012 2013 2014 2015 2016 2017

35%25%

Improving efficiency through lean initiatives and digital capabilities

Active customers

Active

digital customers

+24%

+70%

Cost to Income RatioOptimize no. of Physical Channels and Location

VSAvg. 4 Big banks

+280-51

Note: Digital Customers TMB Direct and TMB Touch)

-307

21

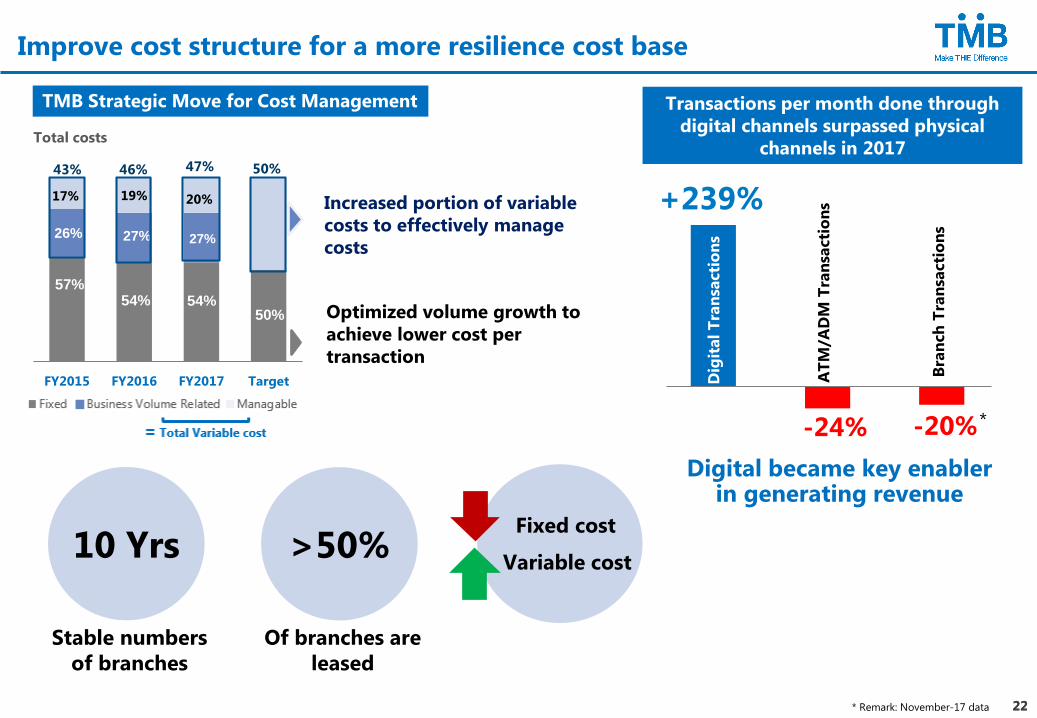

Improve cost structure for a more resilience cost base

TMB Strategic Move for Cost Management

Optimized volume growth to

achieve lower cost per

transaction

Increased portion of variable

costs to effectively manage

costs

FY2015 FY2016 FY2017 Target

Total costs

57%

26%

54%

27%

54%

27%

50%

17% 19% 20%

43% 46% 47% 50%

Transactions per month done through

digital channels surpassed physical

channels in 2017

Digital became key enabler in generating revenue

Dig

ital T

ran

sacti

on

s

+239%

Bra

nch

Tra

nsa

cti

on

s

AT

M/A

DM

Tra

nsa

cti

on

s

-24% -20%

10 Yrs

Stable numbers

of branches

>50%

Of branches are

leased

Fixed cost

Variable cost

*

* Remark: November-17 data 2222

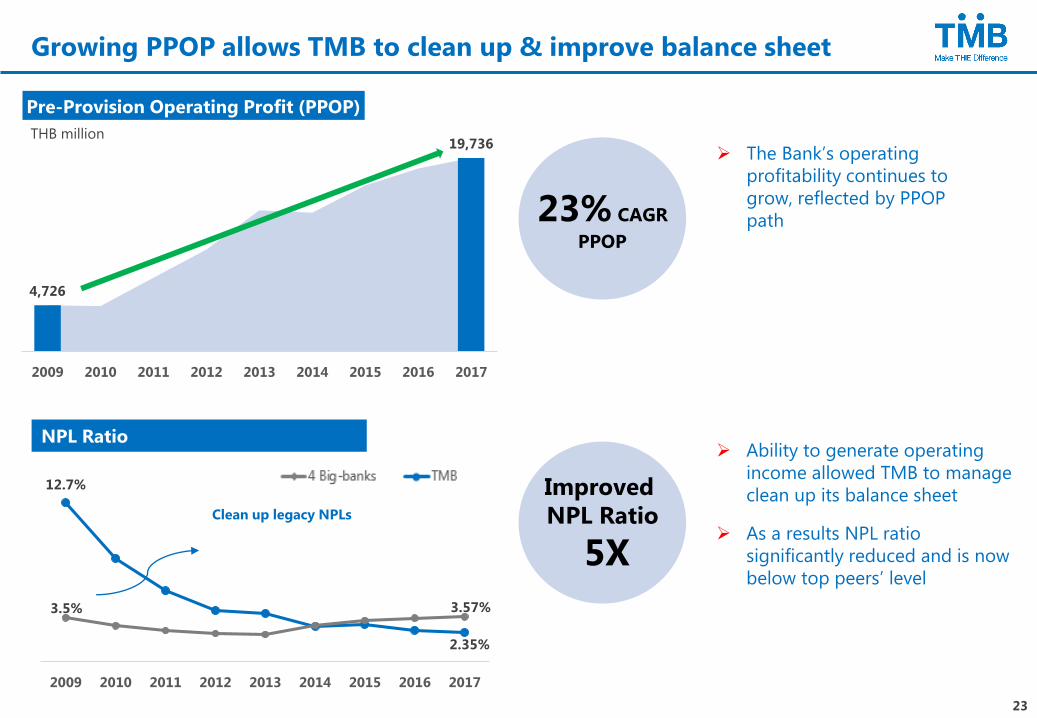

4,726

19,736

2009 2010 2011 2012 2013 2014 2015 2016 2017

Pre-Provision Operating Profit (PPOP)

THB million

12.7%

2.35%

3.5% 3.57%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Growing PPOP allows TMB to clean up & improve balance sheet

➢ The Bank’s operating

profitability continues to

grow, reflected by PPOP

path

NPL Ratio

Clean up legacy NPLs

➢ Ability to generate operating

income allowed TMB to manage

clean up its balance sheet

➢ As a results NPL ratio

significantly reduced and is now

below top peers’ level

23% CAGR

PPOP

Improved

NPL Ratio

5X

23

12.6%

9.2%

4.3%

10.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017

4 Big-banks TMB

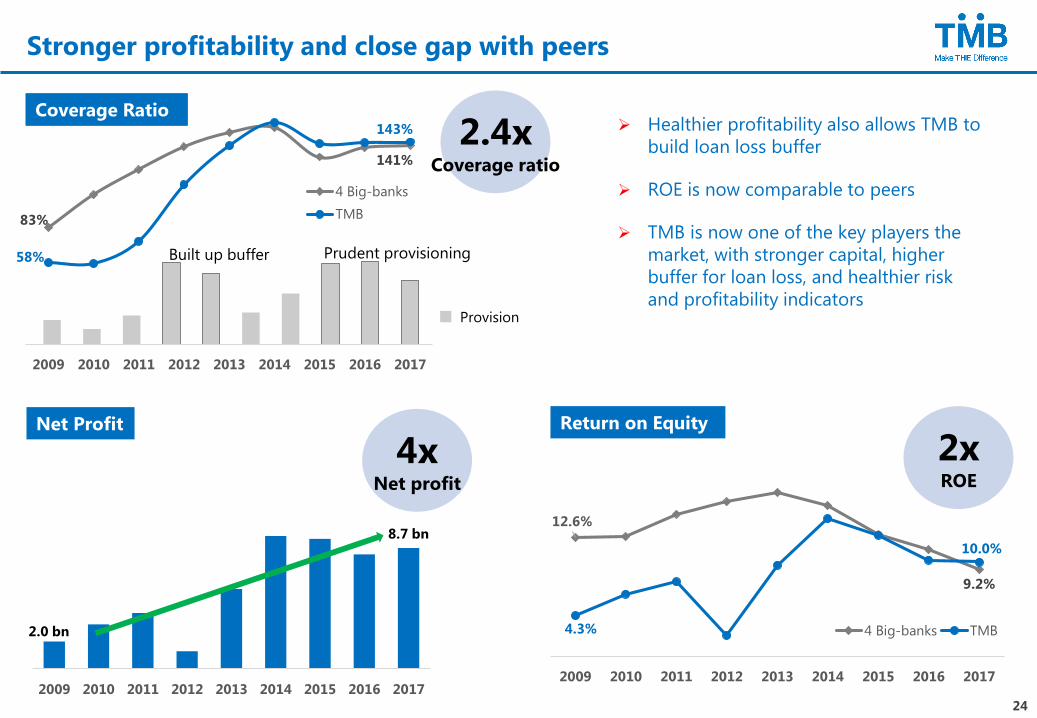

Stronger profitability and close gap with peers

2.0 bn

8.7 bn

2009 2010 2011 2012 2013 2014 2015 2016 2017

➢ Healthier profitability also allows TMB to

build loan loss buffer

➢ ROE is now comparable to peers

➢ TMB is now one of the key players the

market, with stronger capital, higher

buffer for loan loss, and healthier risk

and profitability indicators

Net Profit

Coverage Ratio

Return on Equity

4xNet profit

2.4xCoverage ratio

2xROE

Coverage Ratio

Built up buffer Prudent provisioning

Provision

83%

141%

58%

143%

2009 2010 2011 2012 2013 2014 2015 2016 2017

4 Big-banks

TMB

24

-100000

0

100000

200000

300000

400000

500000

600000

0

20000

40000

60000

80000

100000

120000

140000

2009 2010 2011 2012 2013 2014 2015 2016 2017

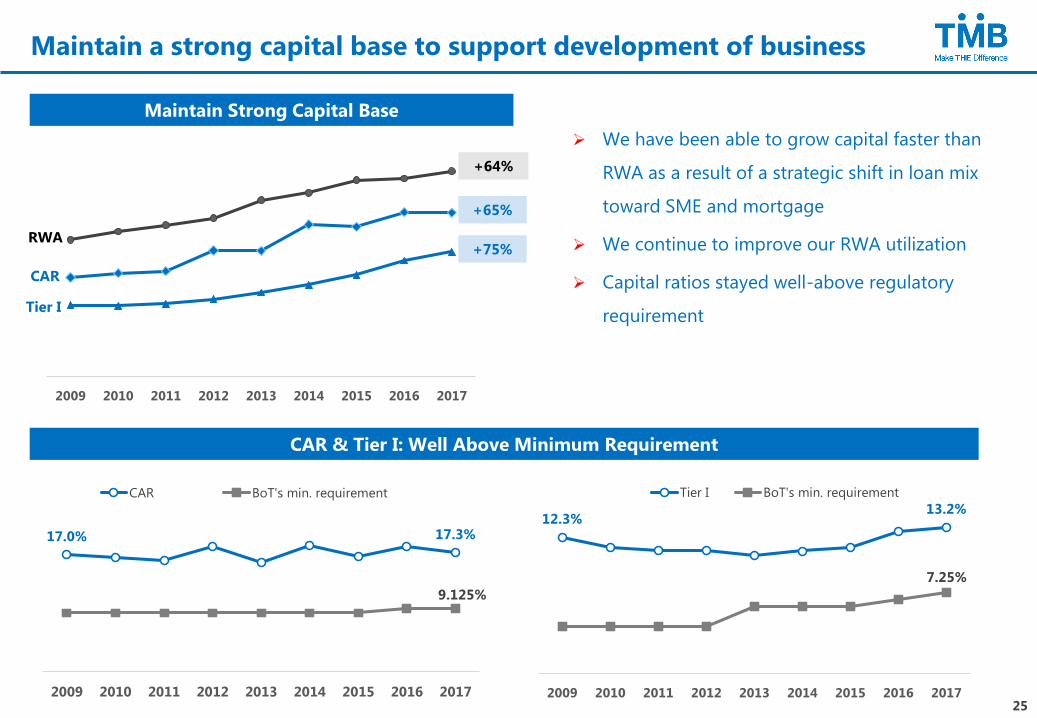

Maintain a strong capital base to support development of business

➢ We have been able to grow capital faster than

RWA as a result of a strategic shift in loan mix

toward SME and mortgage

➢ We continue to improve our RWA utilization

➢ Capital ratios stayed well-above regulatory

requirement

17.0% 17.3%

9.125%

2009 2010 2011 2012 2013 2014 2015 2016 2017

CAR BoT's min. requirement

12.3%13.2%

7.25%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Tier I BoT's min. requirement

Maintain Strong Capital Base

RWA

CAR

Tier I

+75%

+65%

+64%

CAR & Tier I: Well Above Minimum Requirement

25

WE MAKE THE DIFFERENCE

People

Customers

Society

26

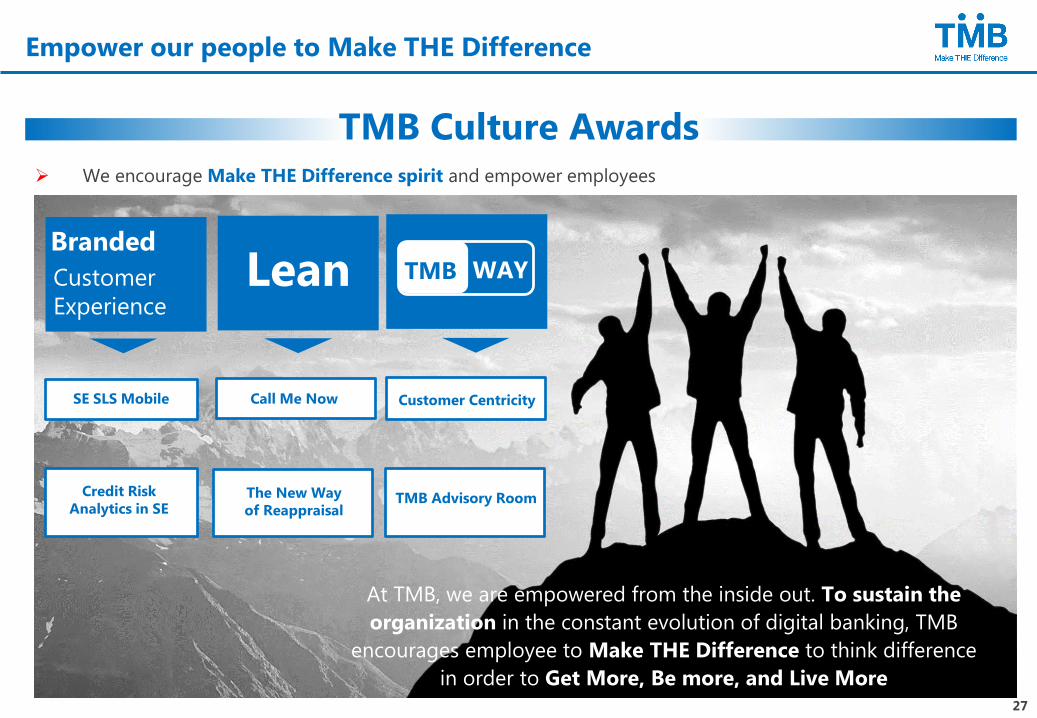

Empower our people to Make THE Difference

TMB Culture Awards➢ We encourage Make THE Difference spirit and empower employees

Branded

Customer

Experience

Lean TMB WAY

At TMB, we are empowered from the inside out. To sustain the

organization in the constant evolution of digital banking, TMB

encourages employee to Make THE Difference to think difference

in order to Get More, Be more, and Live More

SE SLS Mobile

Credit Risk

Analytics in SEThe New Way

of Reappraisal

Call Me Now Customer Centricity

TMB Advisory Room

27

We offer financial products & services

available to customers and banking

industry that promote sustainable

development

Make THE Difference to our customers

Simple & EasyNeed-Based Bank

I.

II.

MAXIMIZE YOUR LIFE THROUGH PRODUCTS AND SERVICES THAT MAKE THE DIFFERENCE

Superior

Insurance

Products

III.

15/9 Life Insurance

Unit-Link

Superior

Transactional

Products

TMB All Free

SME One BankSuperior

Investment

Products

No Fixed

ME by TMB

OA

▪ Open Architecture with 8 Fund House

▪ Online Trading

▪ Advisory Service

Business TouchTMB Touch

Superior

Lending

Products

IV.

Mortgage

SME

28

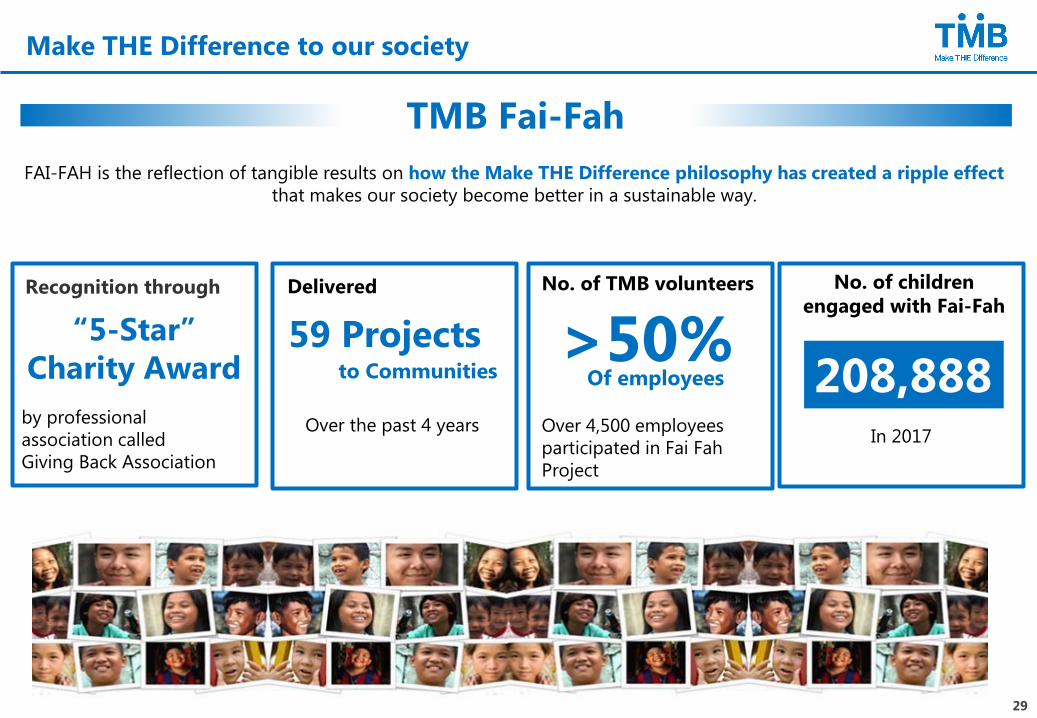

Make THE Difference to our society

TMB Fai-Fah

>50% Delivered

Over the past 4 years

Recognition through

Over 4,500 employees

participated in Fai Fah

Project

No. of TMB volunteers

to Communities Of employees

“5-Star”

Charity Award

by professional

association called

Giving Back Association

208,888

No. of children

engaged with Fai-Fah

59 Projects

In 2017

FAI-FAH is the reflection of tangible results on how the Make THE Difference philosophy has created a ripple effect

that makes our society become better in a sustainable way.

29

APPENDIX

30

2018 Financial Targets

Key ratios 2017 Target Actual 2017 2018 Target

Performing loan growth 8-10% 8.7% 8-10%

Deposit growth 5-7% 2.1% 10-12%

Net interest margin (NIM) 3.1%-3.2% 3.13% 3.05%-3.15%

Net fee income growth 20-30% 32% 15%-20%

Cost to income ratio 45%-47% 47% 45%-47%

NPL ratio 2.3%-2.5% 2.35% 2.3%-2.5%

Coverage ratio 140-150% 143% 140%-150%

Credit cost (annualized) 140-150 bps 139 bps 135-145 bps

31

TMB Bank Public Company Limited

3000 Phahonyothin Road

Chatuchak Bangkok

10900

TMB Website : www.tmbbank.com

IR Webpage : www.tmbbank.com/ir

Important Disclaimer

This presentation contains some information from other sources, that TMB Bank Public Company Limited does not make any representations regarding the

use, validity, accuracy, or reliability of, or the results of the use of information, data but not limited to, all text, and images (“the Content”) on this

presentation. Some content may contain forward looking statements, that based on management’s view upon the information currently available to us.

These statement are subject to certain risks and uncertainties that could cause the actual results materially differed from what had been previously stated.

The materials in this presentation shall not, and are not intended to, constitute or contain an offer to sell or the solicitation of an offer to buy, any securities

of TMB Bank Public Company Limited.

![TMB Bank Plc. · Analysts & Investors Presentation. July 2009 [2] 2Q09 results review](https://img.pdfslide.us/doc/110x75/5f4bf2267c11ae244b2a3039/tmb-bank-plc-analysts-investors-presentation-july-2009-2-2q09-results.jpg)