Embed Size (px)

Citation preview

Lessons from the South: Reflecting on the Shift of Power among the Global Payment Marketplace

Nextgen Payments Forum 20172 February 2017

v1Dr Estelle Brack

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 2

Sommaire

The African banks’ continental expansion strategy

The empowering nature of technology

The challenges for banks

Conclusion

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 3

1. The African banks’ continental expansion strategy

African banks have increased their geographical footprint on the continent and become economically important beyond their home country.

Though pan-African banks seem to have slowed their pace in the past three years, it is mainly to consolidate what they have acquired and to organise new structures before resuming their expansion across the continent.

The banks’ continental expansion strategy was fist fuelled by the need to support corporate clients in their business activities abroad. This is notably the case for the United Bank for Africa (Nigeria), the Standard Bank Group – Stanbic (South Africa) or the Barclays Africa Group – via ABSA (UK and South Africa). Ecobank or the Moroccans (Attijariwafa Bank, BMCE – via Bank of Africa and Banque Centrale Populaire of Morocco – via Banque Atlantique) are aiming for a broader customer base, including mobile money and micro-finance.

The African banking outlook has changed considerably in 30 years…

… and fostered competition on retail banking markets

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 4

1. The African banks’ continental expansion strategy

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 5

2. The empowering nature of technology : the mobile case

One of the greatest examples of the empowering nature of technology has been the meteoric rise of mobile money across Africa. Africa’s mobile money landscape has developed considerably in recent years, with the continent proving to be the perfect breeding ground for transformative mobile payment solutions, most notably seen with the Kenyan launch of M-Pesa in 2007. Mobile money has revolutionised the way financial transactions are made across the continent. For millions of people it has positively transformed their ability to conduct business and their everyday lives.

On average, 33 out 100 adults in SSA have a bank account. 53 out of 100 people have a mobile phone contract in Africa. Around 60% of the 400,000 villages in Africa are covered by telecoms networks, while bank branches are typically present only in large towns.

“The digitisation of banking also provides much greater transparency and an audit trail

throughout more of the economy, from individuals through to the largest

international institutions.“Uzoma Dozie, CEO, Diamond Bank

The dynamism injected into banking competition has, furthermore, led to growth of customer base and to the introduction of digital financial inclusivity solutions

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 6

2. The empowering nature of technology

The success of M-Pesa in Kenya is based on short messages via GSM technology (Global System for Mobile Communication)

The UMTS technology (Universal Mobile Telecommunications System) is progressiveley developed in the cities and promotes a migration to mobile bankingMobile banking provides real-time access to banking services anywhere at any time

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 7

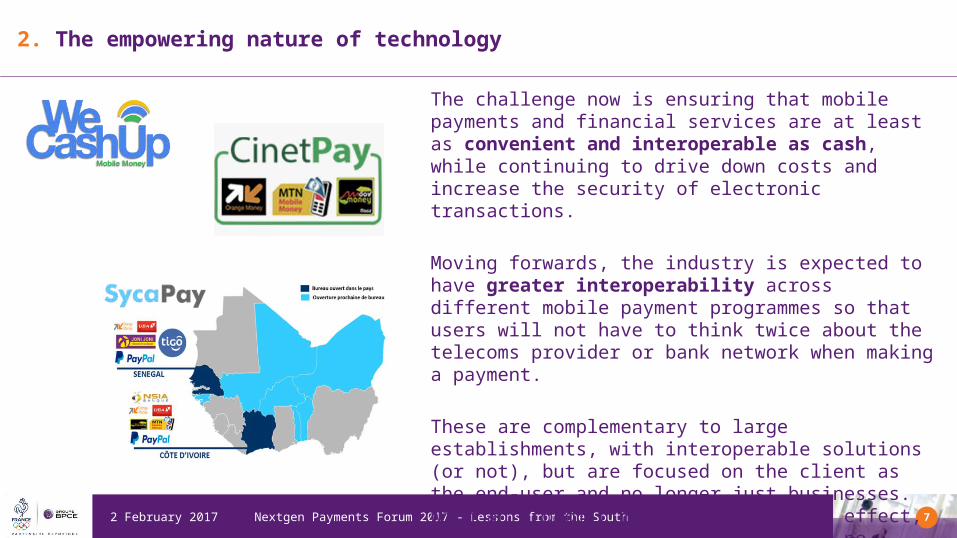

2. The empowering nature of technology

The challenge now is ensuring that mobile payments and financial services are at least as convenient and interoperable as cash, while continuing to drive down costs and increase the security of electronic transactions.

Moving forwards, the industry is expected to have greater interoperability across different mobile payment programmes so that users will not have to think twice about the telecoms provider or bank network when making a payment.

These are complementary to large establishments, with interoperable solutions (or not), but are focused on the client as the end-user and no longer just businesses. With an economic model based on mass effect, much like the digital economy, it is no longer just B to B or B to C, but also H to H, (Human to Human).

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 8

2. The empowering nature of technology

Cash to goods- Mergims in Rwanda- Afrimarket in West Africa- AfricaShop in Senegal

Bank on mobileWala, a digital banking platform is launching on Android to make banking free for everyone in Africa and completely change the way consumer’s access, engage with, and use financial products and services. The Wala platform sits in between banks and customers eliminating many costs thereby creating a more efficient system for everyone.

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 9

2. The empowering nature of technology

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 10

3. Challenges for banks : telcos

Banks often enter the market first by relying on mobile telephone operators’ solutions and have extended their range to distance banking operations. When it comes to the mobile-orientated solutions that are found frequently in Africa, the operator controls the whole value chain from the creation and management of the account through to payment.

But now a new generation of digital financial services is developing for banks to rely on, and they are regaining their place as an intermediary, with services offered without a mobile telephone operator and on the basis of very agile and elaborate à la carte solutions. The solutions supported by InBox, or the TagPay solution, are good examples of this.

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 11

3. Challenges for banks : CBK

The traditional correspondent banking model for cross-border payments has come under acute pressure from customers, regulators and competitors - Customer expectations for real-time, digitally enabled

cross-border payments are growing as domestic retail payments undergo rapid digitization.

- Regulatory compliance is driving up the cost of cross-border payments systems and forcing banks to review their correspondent relations.

- Digital innovators are attracting customers with new solutions and enhanced value propositions that threaten not only to cut banks out of their correspondent banking relationships but also to loosen banks’ ties with end customers, at least where payments-related activities are concerned.

Even leading transaction banks can no longer afford to maintain large international correspondent bank networks and have been closing down less profitable locations.

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 12

3. Challenges for banks : CBK

Nextgen Payments Forum 2017 – Lessons from the South2 February 2017 13

4. Conclusion

Africa combined with payments is an example of the shift of the formal simple flow of influence between countries. From a North – South approach, the countries of the South are sharing same issues and inspire themselves through best practices. They skip some of our evolutions (first generation electronic money) and we share current challenges : how banks adapt to the new environment and multiple stakeholders with basic/simple offers. Countries from the South are able to produce inspiring inputs to our strategic thinking is the North. Our markets are mature and overloaded, our IT systems are highly complex and to big to be able to adapt quickly to all market evolutions. One of them is a priori simple : responding the customers’ needs in a simple and customizable manner. Not only existing needs but also proposing new services, considering different types of usages.

We all share the same challenges : how to cooperate and find the best combination with other stakeholders?

In this complex world, refocusing of the simplicity of our needs as clients and trying to reach a clear vision is key for our industry’s success in the upcoming years.