Embed Size (px)

Citation preview

Thomas Idzorek, CFA Head of Investment Methodology and

Economic Research,

Investment Management group, Morningstar

#MICEU @MorningstarInc

©2015 Morningstar, Inc. All rights reserved.

Tom Idzorek, CFA Head of Investment Methodologies and Investment Research, Investment Management group, Morningstar

For professional use only.

Not for use with the public.

New Dimensions of Popularity

3 For financial professional use only. Not for public distribution.

.

Classic Efficient Market CAPM

More Risk Equals More Return

Dimensions of Popularity ROGER G. IBBOTSON AND THOMAS M. IDZOREK

4

Understanding Returns – the Role of Popularity Popularity

In the short run, the market is a voting machine but in the long run, it is a weighing machine. –Benjamin Graham

“The Essays of Warren Buffett” (2003).

5

Which Investment would you prefer to purchase? Investment A – Speculative

Investment B – Safe

6

Which company/stock would you prefer to purchase? Company A – Fast Growth (Revenue, Earnings, etc.) Company B – Slow Growth (Revenue, Earnings, etc.)

7

Which company/stock would you prefer to purchase? Company A – Powerful Brand Company B – Weak Brand

8

Which company/stock would you prefer to purchase? Company A – Outstanding Reputation Company B – Bad Reputation

9

Which company/stock would you prefer to purchase? Company A – High Investment Capacity Company B – Low Investment Capacity

No answers yet.

What does efficient market theory

tell us (about the answers)…

Efficient Market Theory

Investors are…

gPerfect Decision Makers (Optimizers)

gFree of Biases (or Feelings)

Sheldon Cooper

“Big Bang Theory”

MVO Optimizer

Inputs

Ex

pected R

eturn

MVO Efficient Frontier

Individual Assets

Standard Deviation

Classic Modern Portfolio Theory

Mean-Variance Optimization

►Capital Market Assumption

►Expected Returns

►Standard Deviations (Risks)

►Correlations

Ex

pected R

etu

rn

Emerging Markets

International Developed

Bonds

TIPS

Cash

Standard Deviation

Private Equity

Commodities

Small Cap

Large Cap

This is a graphical representation; plot points are not necessarily meaningful.

Classic Modern Portfolio Theory

More Risk Equals More Return

For Illustration Only

Ex

pected R

etu

rn

Emerging Markets

International Developed

Bonds

TIPS

Cash

Standard Deviation

Private Equity

Commodities

Small Cap

Large Cap

This is a graphical representation; plot points are not necessarily meaningful.

Classic Modern Portfolio Theory

More Risk Equals More Return

For Illustration Only

Ex

pected R

etu

rn

Beta

This is a graphical representation; plot points are not necessarily meaningful.

Classic Efficient Market CAPM

More Risk Equals More Return

For Illustration Only

E[Ri]=𝑟𝑓+βi,mkt(MarketPremium)

…and what does history tell us about

the return of major asset classes…

17

Stocks, Bonds, Bills, and Inflation 1926–2015 Ibbotson® SBBI®

0.10

1

10

100

1K

$100k

1926 1936 1946 1956 1966 1976 1986 1996 2006

Source: Morningstar

$26,641

$4,677

$21

$13

$109

Returns shown are hypothetical; indices are unmanaged and not available for direct investment. Assumes

reinvestment of all capital gains and dividends and does not account for transactions costs or taxes. Past

performance is not indicative of future results.

Small stocks

Large stocks

Government bonds

Treasury bills

Inflation

12.0

10.0

5.6

3.4

2.9

Compound annual return %

10K

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

US – Major Asset Classes

Risk (Standard Deviation) and Return – 1926 to 2015

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=98%

T-Bills

Long-Term Gov. Bonds

Large Cap Stocks

Small Cap Stocks

Source: Author calculations using data from Morningstar Direct

Com

pou

nd A

nn

ual R

etu

rn

Beta

US – Major Asset Classes

Risk (Beta) and Return – 1926 to 2015

For Illustration Only

5%

10%

1.0 2.0 2.5 0.5 1.5

R-square=99%

T-Bills

Long-Term Gov. Bonds

Large Cap Stocks

Small Cap Stocks

Source: Author calculations using data from Morningstar Direct

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

United Kingdom – Major Asset Classes

Risk (Standard Deviation) and Return – 1900 to 2015

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=92%

Bills Bonds

UK Stocks

Source: Author calculations using Dimson, Marsh, Stanton data from Morningstar Direct

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

Netherlands – Major Asset Classes

Risk (Standard Deviation) and Return – 1900 to 2015

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=99%

Bills

Bonds

Netherlands Stocks

Source: Author calculations using Dimson, Marsh, Stanton data from Morningstar Direct

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

18 Countries (Bills, Bonds, and Stocks) from

Dimson, Marsh, and Stanton

Risk (Standard Deviation) and Return – 1900 to 2015

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=85%

Source: Author calculations using Dimson, Marsh, Stanton data from Morningstar Direct

The risk and return paradigm is working

pretty well for asset classes.

Now let’s look at different

characteristics within equities…

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

US – Fama-French Size and Value Indexes

Risk (Standard Deviation) and Return – 1926 to 2013

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=27%

FF Large Growth FF Small Growth

FF Large Value

FF Small Value

Source: Author calculations using data from Ken French’s web site.

Com

pou

nd A

nn

ual R

etu

rn

Standard Deviation

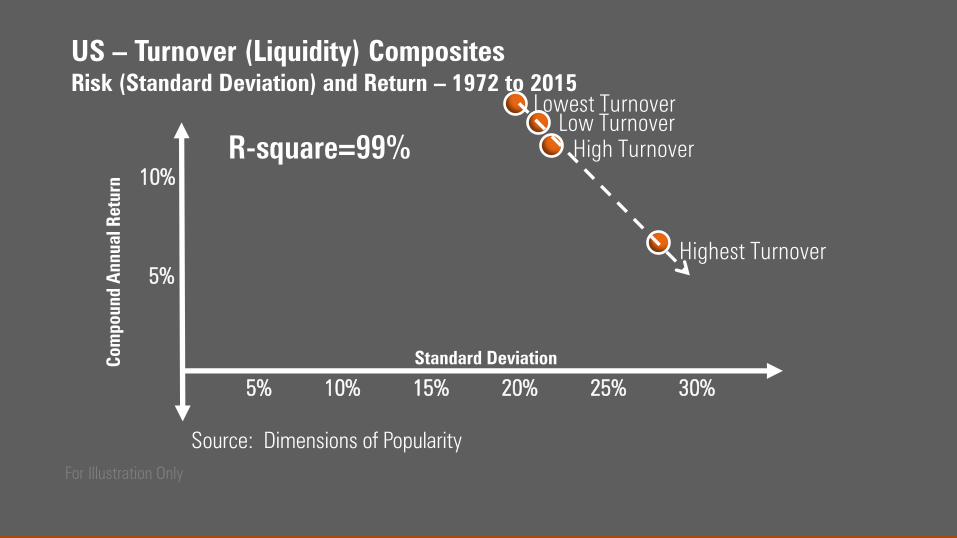

US – Turnover (Liquidity) Composites

Risk (Standard Deviation) and Return – 1972 to 2015

For Illustration Only

5%

10%

10% 20% 30% 5% 15% 25%

R-square=99%

Lowest Turnover

Highest Turnover

Low Turnover

High Turnover

Source: Dimensions of Popularity

26

Traditional Risk-Return Relationship is Broken Beta, volatility, size, value, liquidity, and momentum quartiles Ibbotson and Kim [2015]

For illustrative purposes only.

…a new theory is needed.

Introducing the Theory of Popularity…

28

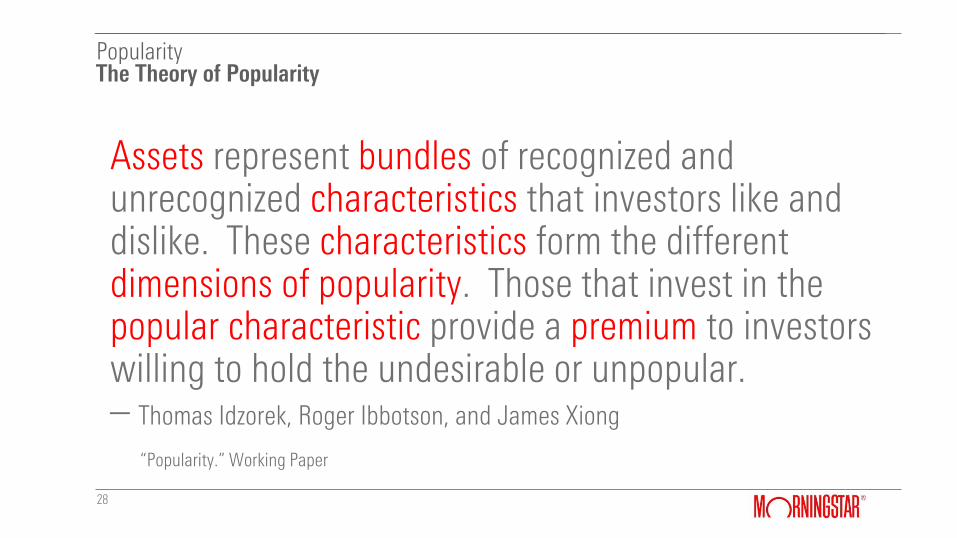

The Theory of Popularity Popularity

Assets represent bundles of recognized and unrecognized characteristics that investors like and dislike. These characteristics form the different dimensions of popularity. Those that invest in the popular characteristic provide a premium to investors willing to hold the undesirable or unpopular. – Thomas Idzorek, Roger Ibbotson, and James Xiong

“Popularity.” Working Paper

29

The Precursor to the Theory of Popularity Popularity

30

Popularity is a Naturally Occurring Phenomenon Popularity

We believe that most of the best-known market premiums and anomalies can be explained by an intuitive and naturally occurring (social or behavioral) phenomenon observed in countless settings: popularity. – Roger Ibbotson and Thomas Idzorek

“The Dimension of Popularity,” Journal of Portfolio Management, 40th Anniversary Edition

31

Example: High School Students Popularity

32

Example: High School Students Popularity

Popularity can decrease… …or increase…

33

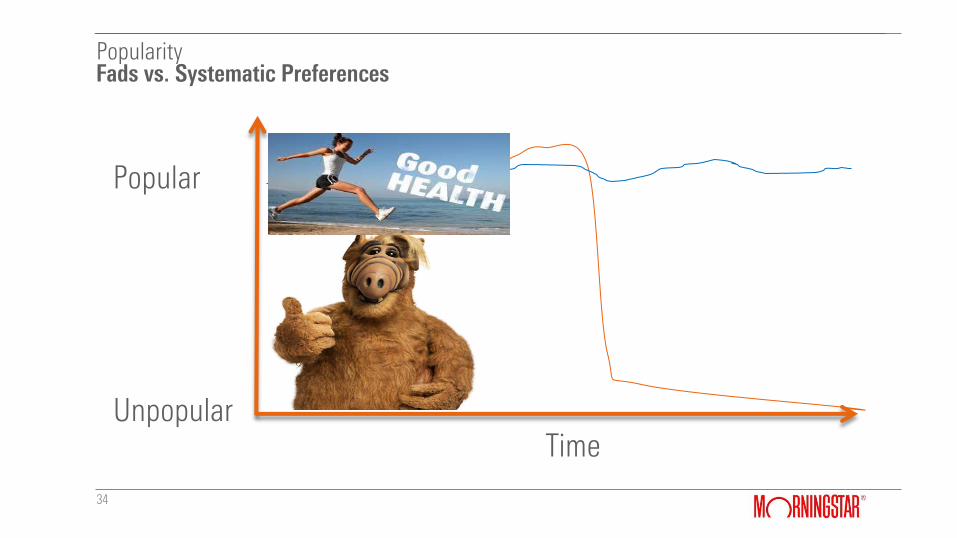

Fads vs. Systematic Preferences Popularity

Some aspects of popularity are systematic, or more or less permanent (for example, modern society seems to prefer thin to fat or tall to short). Other aspects of popularity may be transitory or exist only as fads (for example, mullets, or Mohawk hairstyles).

– Roger Ibbotson and Thomas Idzorek

“The Dimension of Popularity,” Journal of Portfolio Management, 40th Anniversary Edition

34

Fads vs. Systematic Preferences Popularity

Popular

Unpopular Time

35

Natural Re-ordering of Relative Popularity Popularity

…within any given category there is a natural ordering in which some constituents are more popular and others are less popular.

– Roger Ibbotson and Thomas Idzorek

“The Dimension of Popularity,” Journal of Portfolio Management, 40th Anniversary Edition

36

Re-Ordering of Relative Popularity Popularity

37

Theory and Returns Popularity

Traditional Efficient Market View… More Risk = More Return Popularity View… Unpopular characteristics = More Return

Well-Know Premiums and Anomalies

38

Popularity

gEquity Premium (Williams [1938], Ibbotson and Sinquefield [1976])

gLow Volatility / Low Beta (Haugen and Haines [1972])

gValue premium (Graham and Dodd [1934], Basu [1977])

gSize premium (Banz [1981])

gMomentum (Jegedesh, Narasimham, and Titman [1993], Carhart [1997]

gFixed Income Liquidity (Amihud and Mendelson [1991]

gStock Liquidity (Amihud and Mendelson [1986], Ibbotson et al. [2013])

gLiquidity in Funds (Idzorek, Xiong, and Ibbotson [2012])

Popularity Based Explanations for well-known Premiums

39

Popularity

g Equity Premium – Stocks are riskier than safe assets. The outsized equity premium puzzle could be explained by the

democratization of equity investing (creation of mutual funds & ETFs, lower trading costs, online trading, etc.) causing

more and more investors to diversify away from safe assets.

g Low Volatility / Low Beta – Within equities related to the theory of leverage aversion and / or active managers hoping

to outperform market cap benchmarks makes high volatility / high beta stocks too popular relative low vol / low beta

stocks. Migration within dimension creates premium.

gValue premium – Value stocks are often out of favor (unpopular), less well known, and / or operating in less

glamorous, slower growth industries. Migration within dimension creates premium.

g Size premium – By definition small capitalization stocks are less popular and have lower “capacity” than large

capitalization stocks. Migration within dimension creates premium.

gMomentum – Rapid, short-term increases and decreases along one or more dimensions of popularity.

g Fixed Income Liquidity – Investors prefer higher liquidity creating visible discount and thus return premium.

g Stock Liquidity – Investor prefer higher liquidity. Migration within dimension creates premium.

A Better Theory

40

Popularity

Premium Consistent With Traditional Risk-Return Trade-off

Consistent With Theory of Popularity

Equity Premium

Low Vol / Low Beta

Value Premium

Size Premium

Momentum

Fixed Income Liquidity

Equity Liquidity (Turnover)

Equity Liquidity (Amihud)

‘Sin’ Stocks

?

41

New Evidence Supporting the Theory of Popularity

New Evidence Supporting the Theory of Popularity

42

Popularity: Alternative Dimensions of Popularity

gBrand Power

/Theory: High Reputation = High Popularity

gCompetitive Sustainable Advantage

/Theory: Competitive Sustainable Advantage = High Popularity

gFirm Reputation

/Theory: Larger Population = High Popularity

43

Alternative Dimensions of Popularity Brand Power/Value: Interbrand’s Annual Best Global Brands Report Jan. 2001 – April 2015

For illustrative purposes only. Source: Idzorek, Thomas, James Xiong, and Roger Ibbotson. “Popularity.” Working Paper.

Q1 - Lowest Brand Value

Q4-Highest Brand Value

Geo. Mean 12.39% 7.30%

Std. Dev. 17.97% 18.14%

Sharpe 0.52 0.24

Historically, buying the unpopular dimension outperformed.

$5.44 Q1

$2.78 Q4

$1.00

2001 2004 2007 2010 2013 2016

44

Morningstar Economic Moat

45

Alternative Dimensions of Popularity Sustainable Competitive Advantage: Morningstar MOAT® June 2004 – July 2015

For illustrative purposes only. Source: Idzorek, Thomas, James Xiong, and Roger Ibbotson. “Alternative Dimensions of Popularity.” Working Paper. August 2015.

Q1-Lowest Moat Q4-Highest Moat

Geo. Mean 16.1% 11.6%

Std. Dev. 24.6% 15.9%

Sharpe 0.53 0.54

$7.01 Q1

$4.19 Q4

$1.00

2004 2006 2008 2010 2012 2014

Historically, buying the unpopular dimension outperformed.

46

Company Reputation: Harris Poll Reputation Quotient®

March 2001 – July 2015

Alternative Dimensions of Popularity

For illustrative purposes only. Source: Idzorek, Thomas, James Xiong, and Roger Ibbotson. “Popularity.” Working Paper.

Q1-Lowest Reputation

Q4-Highest Reputation

Geo. Mean 14.5% 7.5%

Std. Dev. 21.2% 16.4%

Sharpe 0.54 0.27

2001 2004 2007 2010 2013 2016

$8.01 Q1

$3.03 Q4

$1.00 Historically, buying the unpopular dimension outperformed.

A Better Theory—New Evidence

47

Popularity

Premium Consistent With Traditional Risk-Return Trade-off

Consistent With Theory of Popularity

Brand Power

Competitive Advantage

Company Reputation

48

Great Companies may not be Great Investments Popularity at Work

1. We tend to over pay for great companies (characteristics) and are penalized with lower relative returns.

2. We tend underpay for bad companies (characteristics) and

are rewarded with high relative return

49

Efficient Market Theory, Behavior Theory, or a Unifying Theory?

Classical Finance vs. Behavioral Finance

50

Popularity

Classical Finance Behavioral Finance

Rational Irrational

Efficient Capital Markets (Fair Pricing) Mispricing

Premiums Anomalies

51

A Unifying Theory Popularity

The natural movement along a popularity dimension is the fundamental factor driving many of the most common market premiums and anomalies. This movement along the different dimension of popularity serves as a unifying explanation that elegantly links size, valuation, liquidity, low volatility, and momentum.

Is Theory of Popularity an Efficient Markets or Behavioral Finance Theory?

52

Popularity

gAs an Efficient Markets Theory…

/Investors not only care about risk/volatility as in the classical efficient markets theory

/Also care about liquidity, taxes, information costs, management, distress, etc.

/In equilibrium, investor who are averse to stocks with undesirable characteristics provide premiums to those who are willing to hold those unpopular stocks .

Is Theory of Popularity an Efficient Markets or Behavioral Finance Theory?

53

Popularity

gAs a Behavioral Theory…

/Investors who are overly confident may go after the most popular stocks and end up driving the price too high.

/This provides premiums for investors who hold unpopular stocks.

gIn both theories…

/Those who hold popular stocks are willing losers.

/The winners hold the unpopular stocks.

54

Conclusions Popularity

1. “Good” companies aren't as good as we think and “Bad” companies aren’t as bad as we think – price matters!

2. Unpopular characteristics = More Return

3. Theory of Popularity seems to explain all of the premiums & anomalies

55

Disclosure

©2016 Morningstar Investment Management LLC. All rights reserved. For information and/or illustrative purposes only. Not for public distribution. Morningstar Investment Management LLC is a registered investment adviser and subsidiary of Morningstar, Inc. The information contained in this presentation is the proprietary material of Morningstar Investment Management LLC. Reproduction, transcription or other use by any means, in whole or in part, without the prior written consent of Morningstar Investment Management LLC, is prohibited. The Morningstar name and logo are registered trademarks of Morningstar, Inc. Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results.

References – Page 1

57

Popularity

g Asness, C.S., A. Frazzini, and L.H. Pedersen. “Leverage Aversion and Risk Parity.” Financial Analysts Journal, Vol. 58, No. 1 (2012), pp. 47-59.

g Amihud, Yakov. 2002. “Illiquidity and Stock Returns: Cross-Section and Time-Series Effects,” Journal of Financial Markets, vol. 5, no.1 (January): 31-56.

g Baker, Nardin L. and Robert A. Haugen. 2012. “Low Risk Stocks Outperform within all Observable Markets of the World,” www.lowvolatilitystocks.com, April.

g Baker, M., B. Bradley, and J. Wurgler. 2011. “Benchmarks as Limits to Arbitrage: Understanding the Low-Volatility Anomaly.” Financial Analysts Journal, 67, pp. 40-54.

g Basu, Sanjoy. 1977. “Investment Performance of Common Stocks in Relation to their Price-Earnings Ratios: A Test of the Efficient Market Hypothesis” Journal of Finance (September).

g Bawa, V., and E. Lindenberg. 1977. “Capital Market Equilibrium in a Mean-Lower Partial Moment Framework.” Journal of Financial Economics, 5, pp. 189-200.

g Carhart, M. M. (1997). “On Persistence in Mutual Fund Performance.” Journal of Finance 52: 57–82.

g Fama, Eugene F. 1970. “Efficient Capital Markets: A Review of Theory and Empirical Work." Journal of Finance, May, 25:383-417.

g Fama, Eugene F. and Kenneth R French. 1992. “The Cross-Section of Expected Stock Returns,” Journal of Finance 47 (June): 427–465.

g Fama, Eugene F. and Kenneth French. 1996. “Multifactor Explanations of Asset Pricing Anomalies.” Journal of Finance 51: 55–84.

g Fama, Eugene F. and Kenneth R French. “Migration.” Financial Analysts Journal, Vol. 37, No. 3 (2007), pp. 48-57.

g Harris Poll 2015. “The Harris Poll RQ® 2015 Summary Report.” http://www.harrisinteractive.com/vault/2015%20RQ%20Media%20Release%20Report_020415.pdf Dated February 2015 and downloaded on June 4, 2015.

g Haugen, Robert A. and A. James Heins. 1972 “On the Evidence Supporting the Existence of Risk Premiums in the Capital Market.”Unpublished Working Paper

g

References – Page 2

58

Popularity

g Haugen, Robert A. and A. James Heins. “Risk and the Rate of Return on Financial Assets: Some Old Wine in New Bottles.” Journal of Financial and Quantitative Analysis. 1975

g Haugen, Robert and Nardin Baker (1991), “The Efficient Market Inefficiency of Capitalization-Weighted Stock Portfolios”, Journal of Portfolio Management, vol. 17, No.1, pp. 35–40

g Ibbotson, Roger G., and Thomas M. Idzorek. “Dimensions of Popularity.” Journal of Portfolio Management, Special 40th Anniversary Edition, 2014, pp. 68-74.

g Ibbotson, Roger G., Larry B. Siegel., and J.J. Diermeier. “The Demand for Capital Market Returns: A New Equilibrium Theory.” Financial Analysts Journal, January/February 1984.

g Idzorek, Thomas M. “Popularity Drives Returns.” Morningstar Magazine, 2015, pp. XX – XX.

g Idzorek, Thomas M., James X. Xiong, and Roger G. Ibbotson. “The Liquidity Style of Mutual Funds.” Financial Analysts Journal, November/December 2012, pp. 38-53.

g Kraus, A., and R. Litzenberger.1976. “Skewness Preference and the Valuation of Risk Assets.” Journal of Finance, 31, pp. 1085-1100.

g Lakonishok, Josef, Andrea Shleifer, and Robert W. Vishny. 1994. “Contrarian Investment, Extrapolation, and Risk.” Journal of Finance, December 1994.

Join the conversation: #MICEU