Embed Size (px)

Citation preview

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

1

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty pharmacy:The topic that won’t stop growing.

2

Grant Knowles, PharmD, CSP

VP, Business Development

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty pharmacy

An undeniable and growing proportion of healthcare spend.

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Defining

4

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

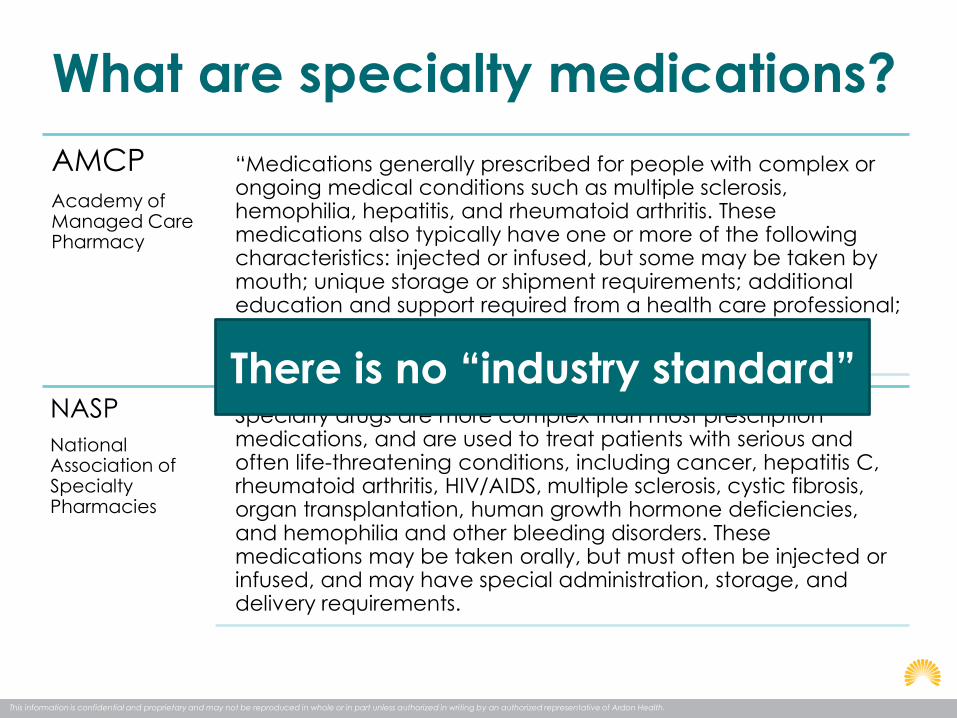

What are specialty medications?

AMCPAcademy of Managed Care Pharmacy

“Medications generally prescribed for people with complex or ongoing medical conditions such as multiple sclerosis, hemophilia, hepatitis, and rheumatoid arthritis. These medications also typically have one or more of the following characteristics: injected or infused, but some may be taken by mouth; unique storage or shipment requirements; additional education and support required from a health care professional; usually not stocked at retail pharmacies.”

NASP

National Association of Specialty Pharmacies

Specialty drugs are more complex than most prescription medications, and are used to treat patients with serious and often life-threatening conditions, including cancer, hepatitis C, rheumatoid arthritis, HIV/AIDS, multiple sclerosis, cystic fibrosis, organ transplantation, human growth hormone deficiencies, and hemophilia and other bleeding disorders. These medications may be taken orally, but must often be injected or infused, and may have special administration, storage, and delivery requirements.

There is no “industry standard”

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty medications

High cost

$1,000-$40,000 per

Rx

Complex admin

Injection, infusion, complex

oral regimen

Unique monitoring

efficacy

concerns,

side-effect,REMS*

Specific climate needs

Specific storage or shipment protocol

Require additional

patient education

“high-touch” disease states,

adherence

Require 24/7

clinical support

High side-effects,

adherence assistance

Drugs not available in retail settings

LDD±

1. *REMS – Risk Evaluation and Mitigation Strategies

2. ± LDD – Limited Distribution Drugs

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

How payers define specialty

43%

66%

67%

73%

71%

81%

85%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Requires patient admin training

Indicated for disease already classified as specialty

Limited distribution

Requires specialty handling

Treats orphan disease

Requiring special monitoring

High cost

1. From 91 payers with over 124 million lives

2. EMD Serono Injectable Digest (10th Edition).

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Traits of specialty medications

1. EvaluatePharma. World Preview 2015-2020.

2. IMS - Medicines Use and Spending Shifts – April, 2015

3. Milliman: Commercial Specialty Medication Research: 2016 Benchmark Projections

7 out of the top 10 medications

in 2014

9 out of the top 10 prescription

in 2020

$7,000 -$400,000

treatment year

28 times more costly than

non-specialty

Increase in price by 6%-20% annually

Patients have a 10X PMPM

99%

1%

UTILIZATION

Traditional Drugs Specialty Drugs

67%

33%

SPEND

Traditional Drugs Specialty Drugs

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

How payers define high cost

14%

40%

29%

17%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

<$600 $600-$800 $1000-1200 >$1,200

1. From 91 payers with over 124 million lives

2. EMD Serono Injectable Digest (10th Edition).

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Past & Future

10

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Healthcare spending(past and future)

11

1. CMS. National Health Expenditure Projections 2014-2024. Accessed April, 2016

0%

2%

4%

6%

8%

10%

12%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Bill

ion

s

National Health Expenditures (NHE) % NHE Growth

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Healthcare & Prescription spending(past and future)

12

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Bill

ion

s

National Health Expenditures (NHE) Prescription Drug Expenditures (PDE) % PDE of NHE

1. CMS. National Health Expenditure Projections 2014-2024. Accessed April, 2016

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Prescription spending(past and future)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$0

$100

$200

$300

$400

$500

$600

Bill

ion

s

Prescription Drug Expenditures (PDE) % PDE Growth

13

1. CMS. National Health Expenditure Projections 2014-2024. Accessed April, 2016

Branded

Blockbusters

Patent Cliff

Specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Limited generic relief

14

2010-2013

0-2%

2014-15

9-15%

2016+

6-8%Trend line

Rx spend

Generic & Biosimilar saving

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Towering trends

1. Drug Trend Report 2014 & 2015 – Express Script

2. IMS: Medicines Use and Spending in the U.S.

-0.5% -0.1%

22.6%

17.7%

9.0%

6.4%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2015 Estimate 2015 Actual

Traditional Specialty Overall

Purchase

cost

Includes after

purchase

discounts

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Towering trends

1. Drug Trend Report 2014 & 2015 – Express Script

2. IMS: Medicines Use and Spending in the U.S.: April 2016

-0.5% -0.1%

22.6%

17.7%

9.0%

6.4%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2015 Estimate 2015 Actual

Traditional Specialty Overall

MSRP

IMS 2015 Trend

Gross - 12.2%

Net - 8.5%

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Estimated specialty spend

$55 $151

$400

$1,700

$ in Billion

2005 2015 2020 2030

1. IMS - Medicines Use and Spending Shifts – April, 2016

2. PCMA - Pharmaceutical Care Management Association

3. UnitedHealth Center: The growth of specialty pharmacy

4. Milliman: Commercial Specialty Medication Research: 2016 Benchmark Projections

Farther reaching estimations diminish in accuracy

NASH (Nonalcoholic

Steatohepatitis)

Alzheimer’s disease

Muscular dystrophy

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Estimated spend distribution

1. IMS - Medicines Use and Spending Shifts – April, 2015

2. Drug Trend Report 2014 & 2015 – Express Script

81.0%

67.3% 62.3%50.0%

19.0%

32.7% 37.7%50.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2014 2015 2018-2020

Traditional Drugs Specialty Drugs

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

81.0%

67.3% 62.3%50.0%

19.0%

32.7% 37.7%50.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2014 2015 2018-2020

Traditional Drugs Specialty Drugs

Estimated spend distribution

1. IMS - Medicines Use and Spending Shifts – April, 2015

2. Drug Trend Report 2014 & 2015 – Express Script

3. Milliman: Commercial Specialty Medication Research: 2016 Benchmark Projections

2016 Estimates:

• Specialty will be 58% of medical drugs spend

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Cost of Hepatitis C. therapy

21

1. Forbes: For Hepatitis C Drugs, U.S. Prices Are Cheaper Than In Europe. Accessed 4/12/16

2. WSJ: What the ‘Shocking’ Gilead Discounts on its Hepatitis C Drugs Will Mean. Accessed 4/12/16

$53,760

$53,312

$60,480

$55,000

$54,541.67

$67,000

$84,000

$83,300

$94,500

Sovaldi

Viekira Pak

Harvoni

US - Purchase UK/Germany US - after purchase discount estimate

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Why so special?

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Why so special?

• Treatment & cures for conditions that may have had none

• Serious benefits and serious potential for side effects

• Shifting therapies to patient administered

• More home, less hospital

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Improved efficacy

+90%, 5-year survival

for CML

1. Cancer.Net: Leukemia – Chronic Myeloid – CML: Statistics

2. CML = chronic myeloid leukemia

Prior

Therapy

for CML

Gleevec

30%, 5-year survival

for CML

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Acute become chronic

1. Adapted from the Cancer Treatment & Survivorship. Facts & Figures: 2014-2015

26%

35%

41%

26% 27%

23%21%

35%

32%

37%

27%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Cancer survivor increase by 2024

$4.4M more survivors

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Hepatitis C therapies

26

48

24

12

28%

66%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

2002 2011 2014-2015

Weeks on Therapy Cure Rate (SVR for Genotype 1)

1. HCSP Fact Sheet: A Brief History of Hepatitis

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Where’s the

generics? Trick question, there aren’t any…

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Biosimilars

Must demonstrate safety, purity, and potency with:

Types

• Biosimilars, 2 approved.

• Interchangeables, 0 approved

28

1. FDA.gov: Information on Biosimilars

Analytical testing

BioassaysAnimal studies

Human clinical studies

Per FDA, “Biosimilars are highly similar to the reference product they were compared to, but have allowable differences because they are made from living organisms. Biosimilars also have no clinically meaningful differences in terms of safety, purity, and potency from the reference product.”

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Size & Complexity – Small molecule drugs & biologics

1. http://www.fda.gov/Drugs/DrugSafety/PostmarketDrugSafetyInformationforPatientsandProviders/ucm220037.htm

Siz

eC

om

ple

xity

Aspirin21 atoms

Small Molecule Drug Large Molecule Drug

Bike~21 lbs..

hGh~3000 atoms

Car~3000 lbs.

Large Biologic

IgG Antibody~25,000 atoms

Business Jet~30,000 lbs. (without fuel)

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Size & Complexity – Small molecule drugs & biologics

1. http://www.fda.gov/Drugs/DrugSafety/PostmarketDrugSafetyInformationforPatientsandProviders/ucm220037.htm

Siz

eC

om

ple

xity

Aspirin21 atoms

Small Molecule Drug Large Molecule Drug

Bike~21 lbs..

hGh~3000 atoms

Car~3000 lbs.

Large Biologic

IgG Antibody~25,000 atoms

Business Jet~30,000 lbs. (without fuel)

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Market impact - biosimilars

Potential $44.2 billion reduction in spending from 2014 to 2024

New competition

• Reference product (brand) will not go away

• Interchangeable >5 years away

• 10-35% savings

Slow market entry

• Generic approvals take 30-48 months

• Two biosimilars have been approved in the last 2 years.

Biosimilar approved

• Zarxio to compete with Neupogen

• Inflectra to compete with Remicade

311. The Cost Savings Potential of Biosimilar Drugs in the United States. RAND Corporation

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Focus

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

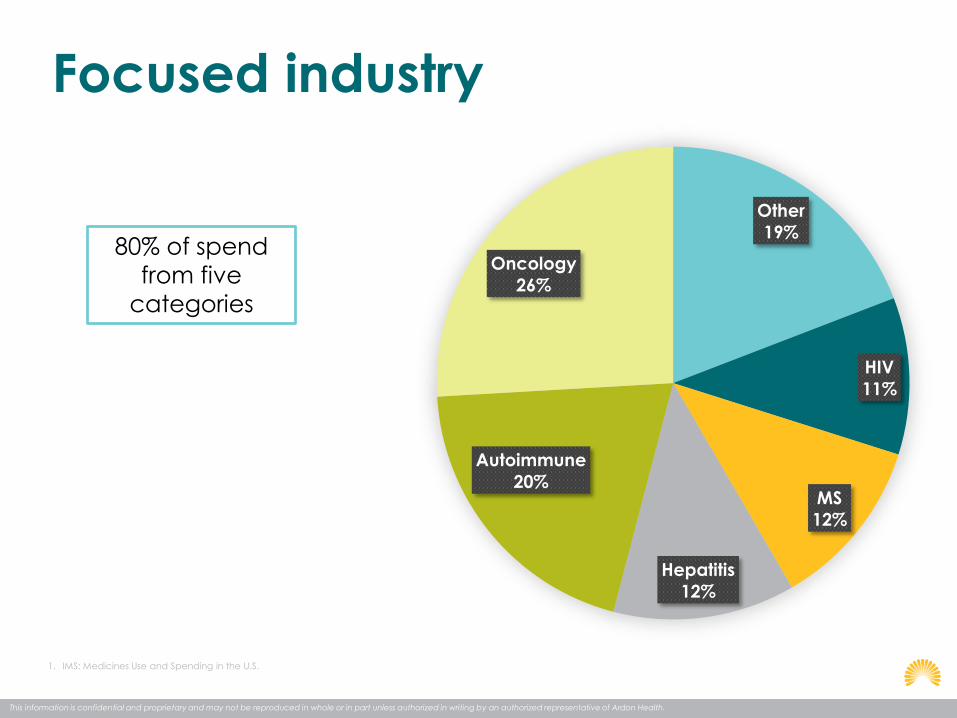

Focused industry

1. IMS: Medicines Use and Spending in the U.S.

Other

19%

HIV

11%

MS

12%

Hepatitis

12%

Autoimmune

20%

Oncology

26%

80% of spend

from five

categories

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty pipeline

1. Pharmaceutical Research and Manufacturers of America.

2. FDA: CDER’s New Molecular Entities and New Therapeutic Biological Products. Accessed April 2016

3. EvaluatePharma. World Preview 2015-2020..

4. IMS - Medicines Use and Spending Shifts – April, 2016

2012-2015: over 50% of FDA approvals

were specialty

Oncology, autoimmune, & viral

hepatitis are expected to lead

Manufacturer R&D is estimated at $493B

2015: FDA approved 19 oncology drugs at

+$8K a prescription

630 products in phase II or higher, 37% are

for specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

FDA new drug approvals

35

22 2218

23 24

1217

21

9

24 27

6 78

810

14

18

22

19

2727

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Traditional Specialty

1. Adaption from PWC Behind the number, 2016. Slide 5

2. FDA: CDER’s New Molecular Entities and New Therapeutic Biological Products. Accessed April 2016

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Fueling the growth

TrendNovel mechanisms

Improved efficacy

Larger patient

populations

Expanding drug

indications

Large pipeline of new drugs

Price increases

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Fueling the growth

TrendNovel mechanisms

Improved efficacy

Larger patient

populations

Expanding drug

indications

Large pipeline of new drugs

Price increases

Price

increase

expected to

account for

10-12% of trends

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty

Pharmacies

38

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty, Pharmacy?

US population

~320 million

~0.9/RX /patient/month

Specialty RX’s are ~1%

# of US pharmacies

~67,000

Typical retail

pharmacy dispenses:

~1,075 RX/week

~11 specialty Rx/week

Specialty pharmacy dispense:

~500-5000 specialty RX/week

Specialization

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

The 1%

40

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

The 1% is our 100% focus

41

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Expertise

• Appropriate to start?

• Appropriate to continue?

• Drug interactions?

Right medication

• Initiation of therapy?

• Continuation of therapy?

Right dose

• Is it being taken?

• What is the frequency?

Right time

Specialty medication can make up 80% or more of a patient’s health care spend.

Multiple Sclerosis therapies can reduce other healthcare spending (ER, hospital, etc.) by 18%.

1. Milliman. Multiple Sclerosis: New Perspective on the Patient Journey

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

High-touch advantages

43

Eligibility verification

Benefit issue resolution

Coordination of benefits

PA assistancePA

recertification (30 days)

<1 business day Rx transfer

<1 business day new patient

contact

Financial assistance enrollment

Support program

connection

Website injection

training videos

Health history check

Drug utilization review

Medication reconciliation

Comprehensive business

continuity

Transition override

coordination

Effectiveness review

Clinical programs

24/7/365 pharmacist call

line

Therapy education

Preemptive refill coordination

Multiple patient outreach & MD coordination

Adherence management

Side effect management

Provider & RX coordination

Same-day delivery options

Next-day delivery

Email package tracking

Ancillary supplies for free

Overuse reviewMedication

replacement coordination

E-prescribingPerson-to-

person contact

Experienced specialty

pharmacists

Same-day delivery

opportunities

Bilingual customer service

Translation capabilities for

>200 languages

36-hour validated coolers

Saturday delivery options

Shipment monitoring &

extraction

Summer packing

Winter packingState-of-the-art

call center

Dedicated to the positive impact of every patient with every interaction

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

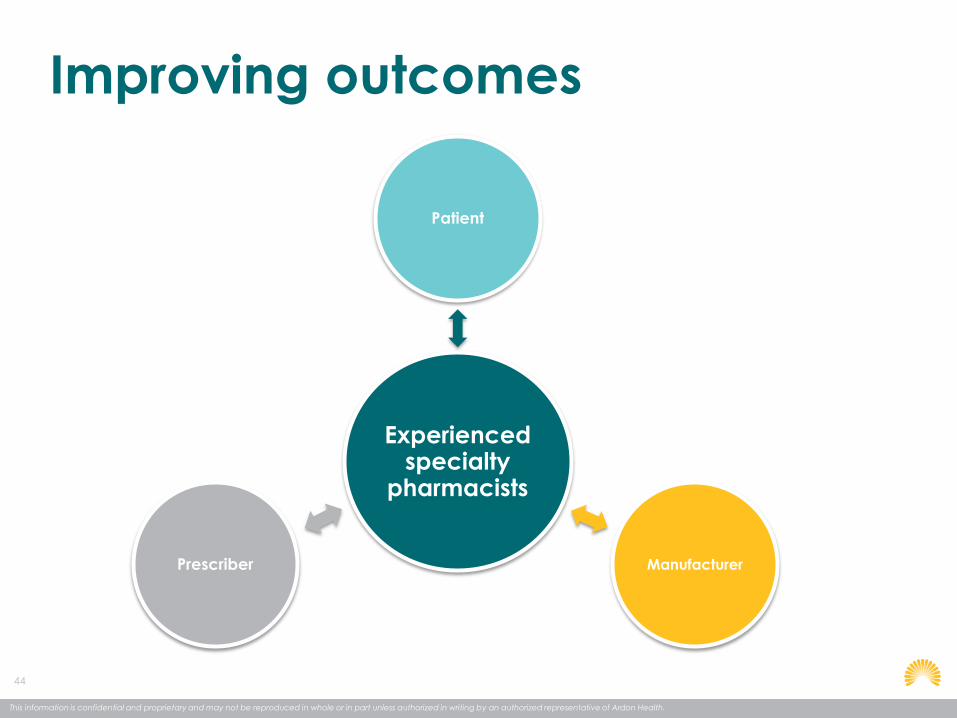

Improving outcomes

44

Experienced specialty

pharmacists

Patient

ManufacturerPrescriber

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Improving outcomes

45

Experienced specialty

pharmacists

Patient

ManufacturerPrescriber

Side effects

Adherence

Administration

Stability

Drug interactions

Side effects

Adherence

Drug interactions

Dose confirmation

Length of therapy

Effectiveness

Side effects

Malfunctions

Stability

Drug replacement

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Improving access

46

87% of fills were connected

with assistance

Median

patient paid:

$5.00

Average obtained:

$138.45

Average patient paid: $22.47

2015 financial assistance

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

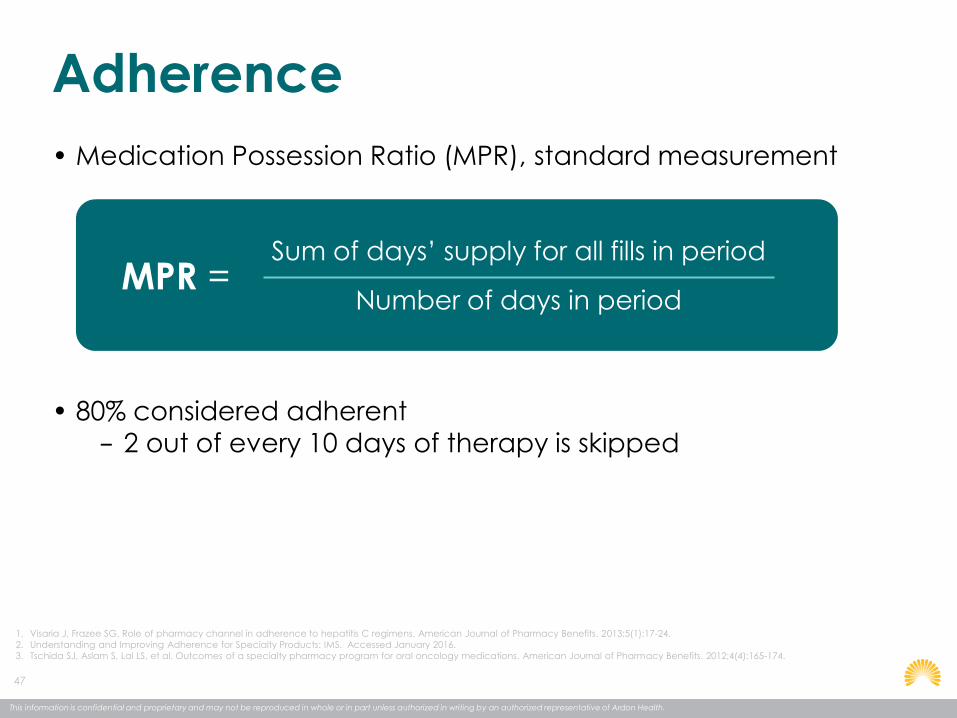

Adherence

47

• Medication Possession Ratio (MPR), standard measurement

• 80% considered adherent− 2 out of every 10 days of therapy is skipped

1. Visaria J, Frazee SG. Role of pharmacy channel in adherence to hepatitis C regimens. American Journal of Pharmacy Benefits. 2013;5(1):17-24.

2. Understanding and Improving Adherence for Specialty Products: IMS. Accessed January 2016.

3. Tschida SJ, Aslam S, Lal LS, et al. Outcomes of a specialty pharmacy program for oral oncology medications. American Journal of Pharmacy Benefits. 2012;4(4):165-174.

MPR = Sum of days’ supply for all fills in period

Number of days in period

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Improving adherence

48

• Case studies show pharmacies achieve MPR of

− Retail: 75-82%

− Specialty: 85-90%

1. Visaria J, Frazee SG. Role of pharmacy channel in adherence to hepatitis C regimens. American Journal of Pharmacy Benefits. 2013;5(1):17-24.

2. Understanding and Improving Adherence for Specialty Products: IMS. Accessed January 2016.

3. Tschida SJ, Aslam S, Lal LS, et al. Outcomes of a specialty pharmacy program for oral oncology medications. American Journal of Pharmacy Benefits. 2012;4(4):165-174.

4. IMS: Avoidable Costs in U.S. Healthcare. June 2013

Ardon maintained a

92% MPR in 2015Non-adherence:

A $105B problem

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Improving adherence

49

• Case studies show pharmacies achieve MPR of

− Retail: 75-82%

− Specialty: 85-90%

1. Visaria J, Frazee SG. Role of pharmacy channel in adherence to hepatitis C regimens. American Journal of Pharmacy Benefits. 2013;5(1):17-24.

2. Understanding and Improving Adherence for Specialty Products: IMS. Accessed January 2016.

3. Tschida SJ, Aslam S, Lal LS, et al. Outcomes of a specialty pharmacy program for oral oncology medications. American Journal of Pharmacy Benefits. 2012;4(4):165-174.

4. Yermakov S, Davis M, Calnan M, et al. Impact of increasing adherence to disease-modifying therapies on healthcare resources utilization and direct medical and indirect work loss costs for

patient with multiple sclerosis. J Med Econ. 2015;18(9):711-720

Ardon maintained a

92% MPR in 2015

10% increase in adherence for MS:

Reduction in ER visits:

9-19%

Reduction in work loss

days:

3-8%

Reduction in direct/

indirect cost:

3-5%

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Managing

specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

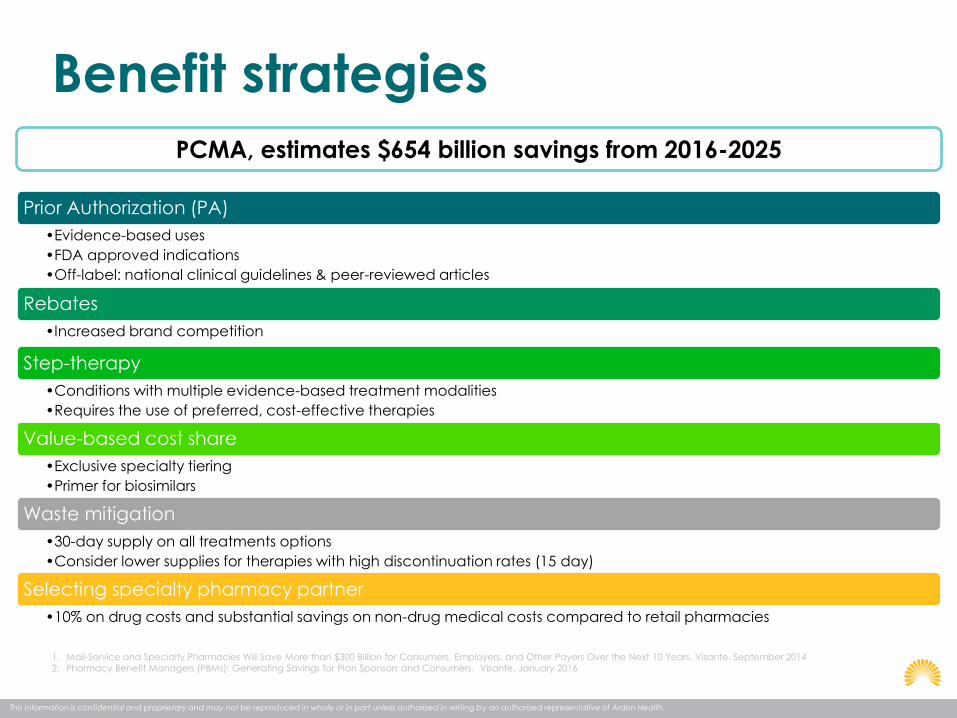

Benefit strategies

Prior Authorization (PA)

•Evidence-based uses

•FDA approved indications

•Off-label: national clinical guidelines & peer-reviewed articles

Rebates

•Increased brand competition

Step-therapy

•Conditions with multiple evidence-based treatment modalities

•Requires the use of preferred, cost-effective therapies

Value-based cost share

•Exclusive specialty tiering

•Primer for biosimilars

Waste mitigation

•30-day supply on all treatments options

•Consider lower supplies for therapies with high discontinuation rates (15 day)

Selecting specialty pharmacy partner

•10% on drug costs and substantial savings on non-drug medical costs compared to retail pharmacies

1. Mail-Service and Specialty Pharmacies Will Save More than $300 Billion for Consumers, Employers, and Other Payers Over the Next 10 Years. Visante. September 2014

2. Pharmacy Benefit Managers (PBMs): Generating Savings for Plan Sponsors and Consumers. Visante. January 2016

PCMA, estimates $654 billion savings from 2016-2025

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

52