Embed Size (px)

Citation preview

1

A BUSINESS IMPROVEMENT DISTRICT FOR ABERYSTWYTH FEASIBILITY STUDY REPORT

Date: 28/7/2014

Themeans: to change places for the better.

2

TABLE OF CONTENTS

................... Page

Executive Summary 5

1.0 INTRODUCTION & METHODOLOGY 7

1.1 The Project Brief 7

1.2 Background 7

1.3 Methodology 8

1.3.1 Business consultation: scoping and feasibility 8

2.0 RESULTS OF THE BUSINESS INTERVIEWS 9

2.1 Sample 9

2.2 Business Health 11

2.3 Top issues for business in Aberystwyth 12

2.3.1 Parking 12

2.3..2 Vacancy rates 12

2.3.3 Levels of marketing and promotion 13

2.4 Improvements to the town centre 13

2.4.1 Parking 13

2.4.2 Increase promotional activity 14

2.4.3 Improved interactions with the council 14

2.5 Reactions to concept of a BID for Aberystwyth 14

2.5.1 Targeting spending 15

3.0 CHARACTERISTICS OF ABERYSTWYTH’S CENTRAL AREAS 17

3.1. Area Description 17

3.2 Options for the BID area 18

4.0 POTENTIAL BID LEVY OUTTURN 25

4.1 The Average UK BID and Aberystwyth 25

4.2 Potential levy income 26

4.3 Levy rates by BID area 27

4.4 Top ten hereditaments and potential levy payers 28

5.0 CONCLUSIONS AND RECOMMENDATIONS FOR PHASE TWO 29

3

5.1 Suggested themes for a BID programme 30

5.2 Recommendations and next steps 31

5.3 .3 Timescale for ballot 34

APPENDIX (SEE SEPARATE DOCUMENT)

4

Table of figures

Figure 1: Graph 1, breakdown of businesses by type 9

Figure 2: Graph 2, nature/type of business 10

Figure 3: Graph 3, further breakdown by nature/type of businesses 10

Figure 4: Graph 4, business performance 11

Figure 5: Graph 5, business optimism 11

Figure 6: Graph 6, issues in Aberystwyth town centre 12

Figure 7: Graph 7, Improvements to Aberystwyth 13

Figure 8: Graph 8, BID support 15

Figure 9: Image 1, focus of a BID in Aberystwyth word cloud 16

Figure 10: Map 1, Options for the BID area 18

Figure 11: Map 2, Options for Zone 1 19

Figure 12: Map 3, Options for Zone 2 20

Figure 13: Map 4, Options for Zone 3 21

Figure 14: Map 5, Options for Zone 4 22

Figure 15: Map 4, Options for Zone 5 23

Figure 16: Map 5, Options for Zone 6 24

Figure 17: Image 2, the means average BID model 25

Figure 18: Table 1, BID levy outturn by zone 26

Figure 19: Table 2, BID levy outturn by zone with £5,000 threshold 26

Figure 20: Table 3, options for BID area 28

Figure 21: Table 4, top 10 hereditaments with BID levy 28

Figure 22: Table 6, for/against a BID ballot 31

Figure 23: Timescale for a BID ballot (summary) 34

5

The means was initially commissioned by Ceredigion County Council, to complete a scoping study in support of the

Welsh Government BID funding application in November 2013. This was followed by a further commission, in April

2014, to carry out a feasibility study into the development of a BID in Aberystwyth. In total, 86 businesses were inter-

viewed across the centre along with 150 informal consultations, including those based on Alexandra Place, Baker

Street, Bridge Street, Cambrian Place, Chalybeate Street, Eastgate Street, Great Darkgate Street, Llys y Brenin, Marine

Terrace, Market Street, North Parade, Owain Glyndwr Square, Park Avenue, Pier Street, Portland Road, Terrace Road

and Upper Portland Street. These surveys aimed to test business reactions to the concept of a BID and capture issues

in the town centre and the best ways to tackle them.

Overall, the survey results demonstrated that business health in the town centre was relatively good. For example, a

significant number of businesses reported that their turnover had grown over the past 12 months.

The results also highlighted the following key points:

A significant number of businesses identified parking, vacant premises, marketing and promotions, and

business networking opportunities as being the most important issues.

In terms of measures for improving the area, the majority of businesses identified providing easier and cheap-

er parking, increasing the promotional activity, improving the interactions with the council, and an increased availa-

bility of public toilets as key areas for action.

When asked directly about their views about the BID concept in principle, 79% of respondents were posi-

tive and 13% were unsure. Only 8% were against the concept.

Based on the above evidence, this report therefore concludes that Aberystwyth town centre should move toward a

BID ballot in 2015.

The report recommends that the BID programme be based around four key themes:

Accessibility

Marketing, promotions and events

Advocacy and enhanced engagement with public authorities

EXECUTIVE SUMMARY

6

7

1.1 The project brief

The means was commissioned by Ceredigion County Council, to complete a feasibility study into the development of a BID

in Aberystwyth town centre, following a successful application to Welsh Government for BID funding in April 2014.

This study represents a significant step in the work to explore the option of a BID in Aberystwyth, and to ascertain

whether a BID would be an effective mechanism to address current issues and build towards a brighter future for the

town centre.

1.2 Background

The birth of modern-day Aberystwyth followed the extension of the Cambrian railway line from Machynlleth to the

town, and the subsequent connection to Cardigan which prompted the development of the local railway station. Aber-

ystwyth quickly became a Victorian tourist attraction, recognised widely as the “Biarritz of Wales”.

Development and expansion of the town continued, with the fishing, silver and lead mining industries providing stimulus

for its economic growth. In 1872, Aberystwyth was elected as the site for the first University of Wales, and in 1907 the

National Library of Wales was established in the town by Royal Charter. The library was officially opened in 1937 by King

George VI.

Since the collapse of the mining industries, and the growth in overseas travel as a result of increases in personal afflu-

ence, Aberystwyth has become increasingly dependent on the University as an economic stimulus. One of the largest

employers in the town, the institution also brings an influx of over 11,000 students per year (2012), almost doubling the

resident population. These incoming students provide an invaluable (although seasonal) source of income to the busi-

nesses in town, which are predominantly services oriented. Following the 2008 global recession and a considerable de-

mise in the intake of students, the sheltered economy of Aberystwyth is struggling, and is in need of a boost.

1.0 Introduction & methodology

Aberystwyth is a seaside town located near

the confluence of the Ystwyth and Rheidol

rivers in Cardigan Bay, on the west coast of

Wales.

Covering an area of 433 hectares, Aberyst-

wyth has a population of 13,040 (Census

2011). For more information on the de-

mographics of Aberystwyth, see Appendix B.

8

Despite this recent decline, the essence of the town as an attractive seaside resort remains, and it’s unique identity sees visi-

tors return year after year. With the promise of significant commercial investment over the coming years and a strong net-

work of independent businesses already present in the town, the potential for Aberystwyth’s revival is clear.

1.3 Methodology

The feasibility study focused on gathering opinions on issues that were important to businesses in the Aberystwyth town

centre area and views on measures to improve trading conditions. The study also aimed to raise awareness and gauge levels

of support among businesses for a Business Improvement District.

1.3.1 Business consultation: scoping & feasibility

An initial visioning event held at The Richmond Hotel on the 11th November 2013 highlighted concerns from a small number

of businesses regarding the proposed process and an impromptu vote was held regarding the decision to progress the study.

Following agreement to proceed, the means adopted a cautious approach to consultations; introducing an additional phase

involving informal discussions with the businesses around the BID concept and the opportunity available to them.

The business consultation was conducted in both feasibility and scoping phases where interviews took place on a face-to face

basis at individual business premises. Where possible the most senior member of staff was interviewed, which in most cases

was the store manager/ owner or a company director. During the interview, whilst being asked questions to determine busi-

ness issues and trends, the concept of a BID was introduced/ discussed. A full list of the businesses consulted as well as a

copy of the questionnaire used can be found in the appendices. The result of the business interviews can be found in Section

2.

9

2.1 The sample

The means conducted a total of 88 interviews over a six month period, which aimed to gather a cross section of businesses

views. These were in addition to 150 informal consultations carried out in the preliminary phase as discussed above. The

interviews were designed to ascertain;

1) The nature of the business and its current health

2) The individual’s view of the key issues facing Aberystwyth town centre and possible measures to improve trading con-

ditions

3) Reaction to the idea in principle of a Business Improvement District.

Consultation with businesses across Aberystwyth was on the whole relatively easy; face-to-face discussions were initiated,

largely on a ‘drop in’ basis, and senior decisions makers (managers or owners) were generally on hand and willing to partici-

pate in the survey. This was also usually the case with chain or franchise organisations, although some managers felt they

were not empowered to engage in the discussion, and diverted questions to head office. It was more difficult to apply the

‘drop in’ approach to office-based businesses; in these cases contact was made via telephone or email in the first instance.

Business interviews covered different business types and a spread of sectors, shown as follows:

Figure 1

2.0 Results of the business interviews

Gra

ph

1: Bre

ak

do

wn

of b

usin

esse

s by

typ

e

10

Figure 2

The different industries covered in the research were grouped into four basic sectors to help simplify comparisons.

Retail: Non Food Retail, Food (butchers etc.), convenience stores, Fashion Retail and Newsagents.

Hospitality: Restaurants, hotels, bars, cafes and pubs.

Services: Community Facilities, Motor Trade, Leisure, Other Services and Professional Services (estate agents, banks

etc.).

Other: includes charities, housing associations and libraries.

Figure 3

Gra

ph

2: B

rea

kd

ow

n o

f bu

sine

sses b

y se

ctor

Gra

ph

3: Bre

ak

do

wn

of b

usin

ess b

y se

ctor

11

2.2 Business Health

The survey include two questions in order to determine business health; businesses were queried on their levels of growth/

decline over the last 12 months, and what plans the business had for the next year.

Figure 4

Over three quarters of businesses interviewed indicated that operations would remain the same over the next 12 months.

Whilst only 16% indicated that they had plans to expand operations, none of the businesses interviewed highlighted an inten-

tion to reduce the size of their business over the same period. Of the 6% who predicted they would leave the centre in the

next 12 months the majority identified high business rates and rents as the root cause.

Figure 5

Gra

ph

5: Bu

sine

ss op

timism

Gra

ph

4: B

usin

ess p

erfo

rma

nce

12

In response to the question on business performance over the previous 12 months a fifth of those interviewed indicated a de-

cline in operations. Almost half of businesses identified their performance as stable, whilst 35% of interviewees had noticed an

improvement in business performance over that period.

2.3 Top issues for businesses in Aberystwyth

Businesses were presented with a list of issues and asked whether they believed them to be a significant issue, minor issue or

not a problem.

Gra

ph

6: M

ain

issue

s in A

be

rystw

yth

tow

n ce

ntre

Figure 6

2.3.1 Parking

A familiar issue in many urban areas, both the cost and availability of parking were identified as a primary issues within the

town. 80% of respondents indicated that parking was a ‘big issue’ for them and for their customers, as part of a wider discus-

sion around issues of accessibility in Aberystwyth. Conversations largely centred around the lack of long-stay parking within a

convenient distance of the town centre, highlighting the availability of short stay parking at the Rheidol and Ystwyth retail

parks. Interviewees commented that, although long-stay parking was available at car parks outside the primary retail area,

the walking distance into town was off-putting for visitors.

2.3.2 Vacancy Rates

Over 50% of respondents identified vacant units within the town centre as a key issue, although many noted that the situation

had improved over the course of the previous six months. For many, the occupation of these units presented concerns as they

observed an increasing number of charity shops, meanwhile use spaces – particurlarly art galleries within primary retail areas –

and mobile phone shops as detrimental to Aberystwyth’s retail offering. Within the wider conversation around vacancy and

retail in the town, a large number of respondents indicated that a more concerted effort should be made to ensure that the

‘right’ businesses were encouraged to take on these properties. Respondents indicated a need to diversify the retail make-up

of the town, and to encourage companies of commercial interest – for example popular clothing outlets – to take up occupa-

tion in the town.

13

2.3.3 Levels of marketing and promotion

A lack of effective marketing and promotion of the town was highlighted by over 90% of businesses as a core issue, with inter-

viewees as key issues, with 80% stating it was a big issue. Many respondents were frustrated by the limited promotion of

events within the town, to the point where businesses themselves were unaware of such attractions. They also highlighted a

need to enhance Aberystwyth’s offering – both as a retail destination and as a seaside town – in order to attract visitors into

the area. It was noted by many that the town was ‘losing out’ on a significant amount of trade due to its weak retail offering in

comparison other towns of size within the wider area. Interviewees reflected - both from a personal and observed perspective

- that shoppers were more likely to travel to locations such as Shrewsbury, Birmingham, Cardiff and Swansea because of what

was available.

2.4 Improvements to the town centre

Once the issues in the town centre had been discussed, respondents were asked to consider what impact possible improve-

ments might have on the area. They were asked to determine whether they felt each would add ‘a lot’ of value, ‘a little’, or

‘not at all’, before being given an opportunity to suggest other improvements they considered would benefit the area.

Gra

ph

7: Me

asu

res to

imp

rove

Ab

ery

stwy

th to

wn

cen

tre

Figure 7

2.4.1 Parking

Of the possibilities discussed, improvements to parking services were identified by respondents as having the most significant

benefit to the town. 85% highlighted that improvements to the parking facilities in town would help matters ‘a lot’. This was

largely in relation to availability and, as mentioned above, particularly in terms of duration. Most reflected that an increase in

the availability of long-stay parking within the town centre area would impact on footfall within the town. It is worth noting

that whilst many expressed this opinion as their own, others highlighted that this was more an issue of perception- specifically

visitor perception – and that there was an adequate offering car parking spaces. Instead, they highlighted the convenience, or

apparent lack thereof, of those car parks available, which are located a short walking distance from the town centre.

14

2.4.2 Increase promotional activity

Reflective of the issues raised, over 90% of those interviewed indicated that an increase in promotional activity, including mar-

keting and events, would benefit the town, with over 70% suggesting it would help ‘a lot’. Many businesses were frustrated by

what they saw as inadequate attempts to promote the town; respondents highlighted various events and promotions that had

taken place but had lacked significant advertising and were therefore ineffective in attracting visitors to the town. One hotel-

ier, for example, expressed frustration that his awareness of events in the town was prompted by his guests, and not the other

way around. It should also be noted, however, that several participants indicated that an increase in promotional activity

would have little impact until issues regarding the infrastructure and retail offering of the town were addressed.

2.4.3 Improved interactions with the council

Over 90% of those interviewed highlighted that improved interactions with the council would be of benefit, with 65% indicated

that it would help ‘a lot’. These comments were largely in response to a wider frustration regarding what many perceived as a

disconnection between the town and the council, particularly in terms of business interests. Although much of this discussion

was focused on high business rates and a seeming lack of support for local businesses, many also expressed concerns with re-

gard to proposed developments in the town, especially with regard to parking services.

2.4.4 Increased availability of public toilets

78% of businesses suggested that an increase in the availability of public toilets would improve the centre either ‘a lot’ or ‘a

little’. Respondents indicated that, whilst services were available, their absence within the centre itself was an issue, particu-

larly for elderly visitors or those with young children. On the latter point, many also highlighted a lack of baby changing facili-

ties within the town.

The concept of a BID was tested in the survey, and was described to the interviewees was as follows:

There are four distinctive things about a BID:

1. A BID is set up by a democratic ballot of all businesses in the proposed BID area

2. If the ballot is successful, the businesses pay a levy usually based on the current rateable value

of their property to create a pot of money which they get to spend as they see fit.

3. A BID management board will be set up and run by the BID

4. BID services have to be in addition to the services provided by the council. The BID’s services

cannot be used to subsidise council services.

2.5 Reactions to concept of a BID for Aberystwyth

15

Gra

ph

9: R

ea

ction

to th

e B

ID co

nce

pt

Figure 8

Despite some resistance to the concept at the initial visioning event, respondents were extremely positive in response to this

question, with 79% of those interviewed identifying the BID as a good idea in principle. The majority highlighted an urgent need

to drive change in Aberystwyth, and were enthusiastic about the opportunity presented. 13% of respondents expressed a de-

sire for more information and remained undecided, whilst only 8% of businesses were firmly against the concept in principle.

Of those who were against the many highlighted a distrust for such collaborative approaches to regeneration and development,

citing previous experiences with town-wide initiatives as evidence for their concerns. Others reflected that any further cost to

their business, which they perceived as already very high, was unwelcome.

2.5.1 Targeting spending

Following a discussion on the concept of the BID, and the types of measures undertaken by other towns, respondents were

asked to consider what services and improvements an Aberystwyth BID could should prioritise should one be formed in the

town centre.

The word cloud below highlights responses to this question regarding targeted spending; the size of the word is an indication

of its frequency as a response. The most popular suggestions were parking, promotions, marketing, networking, events, and

attracting new businesses into the town.

16

What should the focus of a BID in Aberystwyth be?

Figure 9

17

3.0 Characteristics of Aberystwyth’s central areas

3.1 Area description

For the purposes of the feasibility study, Aberystwyth was divided up into the following main areas:

Zone 1 - The Town Centre Core: The primary commercial area in the town, this zone covers Great Darkgate Street and Ter-

race road as the main retail areas, along with several subsidiary streets including Chalybeate Street, Bridge Street and

Pier Street. The majority of the town’s retail offering is within this zone. Notably, it contains a high number of inde-

pendent and local businesses, compared to the other retail zones (Zone 3 and Zone 5) which are predominantly occu-

pied by nationals and franchises. Within this area there is also a concentration of professional services – for example

solicitors and financial advisors – many of whom are located on Eastgate Street, or on other subsidiary streets. There

are a large number of cafes within this zone, and a number of public houses and restaurants. The majority of vacant

units within the town are to be found in this zone, which many respondents attribute to the higher level of rates for

properties in this area. There are a number of planned retail developments within this zone, including the introduc-

tion of a Tesco Express on Terrace Road and, notably, a Starbucks at the upper end of Great Darkgate Street.

Zone 2 – This area covers Victoria Terrace on the seafront and North Road as its primary streets. Zone 2 is notable for its

reduced retail offering, and the higher concentration of office based businesses. There are a number of hotels within

this area, particularly along Victoria Terrace. The town hall building is located in this zone. Zone 2 acts as the north-

ern periphery of the town centre core, bordered by Constitution Hill at its northernmost point; its easterly border is

the point at which Northgate Street becomes Penglais Hill. Northgate Street is host to a number of independent busi-

nesses from a range of different industries, including a food takeaway and a furniture shop.

Zone 3 – This area is primarily comprised of Alexandra Place, and the Rheidol and Ystwyth retail parks. On this basis it is

identified as the secondary retail area. In contrast to the retail core, Zone 3 contains predominantly national or fran-

chise retailers in large scale properties. Both retail parks are mixed use, hosting food, household and fashion retailers

amongst others. There are also a number professional services located in this zone, including the council and Welsh

Assembly Government offices, as well as a select number of food outlets, and a hotel. This area also contains the site

of the proposed Mill Street development.

Zone 4 – Bordered by the sea front on two sides, Zone 4 has a significantly reduced retail offering. Comprising New Prom-

enade, Quay Street and King Street amongst others, there are a scattering of businesses across the area, many of

which are office based or linked to the university. This Zone is peripheral to the town centre.

Zone 5 – Centred around the lower end of Park Avenue, the most prominent feature of this area is the Parc y Llyn retail

park; a mixed use area, the park contains a large Morrisons supermarket, as well as number of stores selling small

and large household goods. Parc y Llyn is divided by the Park Avenue carriageway, with those stores on the north-

eastern side of the road being a later addition. These include Next, McDonalds, and a large garden centre. This zone

18

Zone 6 – More sparsely occupated than the other zones, still this area contains three of the key employers and stake-

holders in the town. Stretching up Penglais Hill, Zone 6 hosts Bronglais Hospital, the National Library, and Aberyst-

wyth University.

3.2 Aberystwyth Town Centre – Options for the BID Area

Zone Area

1 Town centre core: Great Darkgate Street, Terrace Road, Chalybeate Street, Bridge

Street, Pier Street, etc.

2 Victoria Terrace, North Road, Northgate Street

3 Alexandra Place, Rheidol and Ystwyth retail parks

4 New Promenade, Quay Street, King Street, etc.

5 Parc y Llyn retail park – Morrisons, Halfords, McDonalds, Next, etc.

6 Bronglais Hospital, National Library, Aberystwyth University

Figure 10

19

Figure 11

Total Rateable Value of all commercial property £ 7,710,960

Income from a levy set at

1% 1.25% 1.50%

£ 77,109.60 £96,387 £115,664.40

No of businesses = 423

If a £5,000 threshold was applied

Total Rateable Value of commercial property £ 7,504,100

Income from a levy set at

1% 1.25% 1.50%

£75, 504.10 £93,801.25 £112,561.50

No of businesses = 346

Zone 1 – Town Centre Core

20

Figure 12

Total Rateable Value of all commercial property £ 643,965

Income from a levy set at

1% 1.25% 1.50%

£6,439.65 £8,049.56 £9,659.48

No of businesses = 47

If a £5,000 threshold was applied

Total Rateable Value of commercial property £ 566,800

Income from a levy set at

1% 1.25% 1.50%

£5,668.00 £7,085.00 £8,502.00

No of businesses = 33

Zone 2 - Victoria Terrace, North Road, Northgate Street

21

Zone 3 - Alexandra Place, Rheidol and Ystwyth retail parks

Figure 13

Total Rateable Value of all commercial property £3,371,675

Income from a Levy set at

1% 1.25% 1.50%

£33,716.75 £42,145.94 £50,575.13

No of businesses = 43

If a £5,000 threshold was applied

Total Rateable Value of commercial property £3,320,250

Income from a levy set at

1% 1.25% 1.50%

£33,202.50 £41,403.13 £49,803.75

No of businesses = 40

22

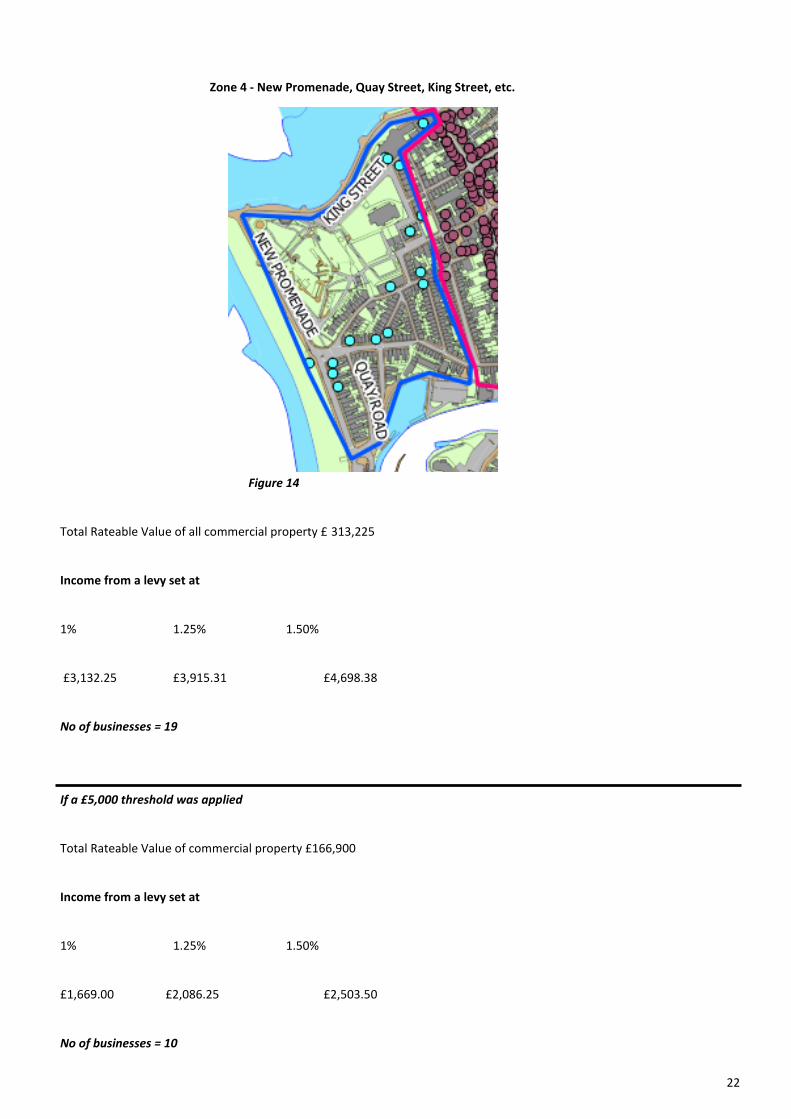

Zone 4 - New Promenade, Quay Street, King Street, etc.

Figure 14

Total Rateable Value of all commercial property £ 313,225

Income from a levy set at

1% 1.25% 1.50%

£3,132.25 £3,915.31 £4,698.38

No of businesses = 19

If a £5,000 threshold was applied

Total Rateable Value of commercial property £166,900

Income from a levy set at

1% 1.25% 1.50%

£1,669.00 £2,086.25 £2,503.50

No of businesses = 10

23

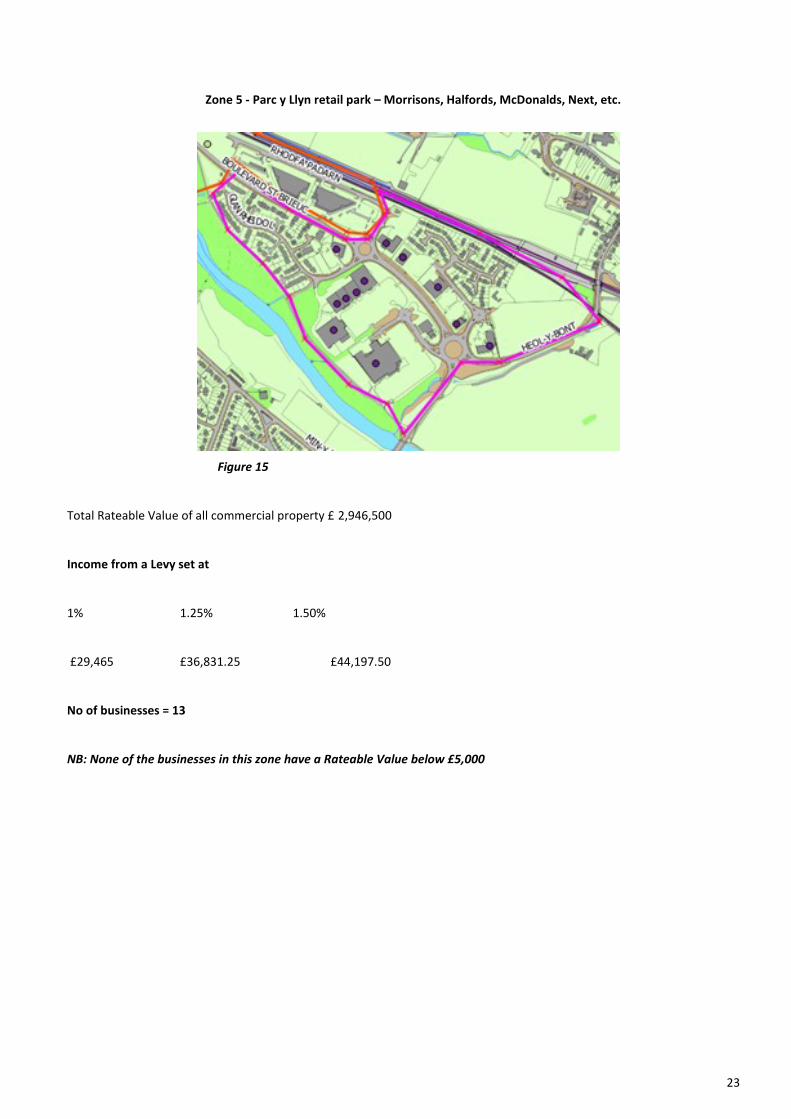

Zone 5 - Parc y Llyn retail park – Morrisons, Halfords, McDonalds, Next, etc.

Figure 15

Total Rateable Value of all commercial property £ 2,946,500

Income from a Levy set at

1% 1.25% 1.50%

£29,465 £36,831.25 £44,197.50

No of businesses = 13

NB: None of the businesses in this zone have a Rateable Value below £5,000

24

Zone 6 – Bronglais Hospital, National Library of Wales, Aberystwyth University

Figure 16

Total Rateable Value of all commercial property £ 2,906,600

Income from a Levy set at

1% 1.25% 1.50%

£29,066.00 £36,332.50 £43,599.00

No of businesses = 7

NB: None of the businesses in this zone have a Rateable Value below £5,000

25

4.0 Potential BID levy outturn

4.1 The UK Average BID & Aberystwyth

According to the 2013 National BIDs Survey, produced by British BIDs, the outturn raised by the smallest annual levy income is

£22,400 at London’s New Addington BID. The largest annual levy income is £2,814,000 at London’s New West End Company.

The means maintains a model of the UK Average BID. At the 20th June the model shows the following outcomes. This illustrates

that the average BID levy in the UK is 1.4% and average levy outturn is £363,000:

It is proposed that Aberystwyth will

follow the UK average with a levy rate

between 1 and 1.5%. This will raise an

annual total levy income lower than

the UK average which, dependent on

the levy percent, threshold and zones,

will collect in the region of £162,000-

250,000 per annum.

Figure 17

26

4.2 Potential levy income

The tables below set out the potential levy income for Aberystwyth town centre when different levy rates and rateable value

thresholds are applied. In most BID areas some form of threshold is applied, partly to ensure that the costs of collecting the

levy from smaller businesses does not exceed the levy they pay, but also to keep the number of BID businesses down to a level

with which the BID board and team can reasonably communicate. The ratings threshold in Merthyr Tydfil, for example, was set

at £5,000.

Table 1: BID LEVY OUTTURN BY ZONE – No threshold

Number of businesses: 553

Figure 18

Zone Total Levy at 1% Total Levy at 1.25% Total Levy at 1.5% Total RV

Zone 1 £77,109.60 £96,387.00 £115,664.40 £7,710,960

Zone 2 £6,439.65 £8,049.56 £9,659.48 £643,965

Zone 3 £33,716.75 £42,145.94 £50,575.13 £3,371,675

Zone 4 £3,132.25 £3,915.31 £4,698.38 £313,225

Zone 5 £29,465.00 £36,831.25 £44,197.50 £2,946,500

Zone 6 £29,066.00 £36,332.50 £43,599.00 £2,906,600

Total £178,929.25 £223,661.56 £268,393.89 £17,892,925.00

Zone Total Levy at 1% Total Levy at 1.25% Total Levy at 1.5% Total RV

Zone 1 £75,041 £94,380.13 £112,561.50 £ 7,504,100

Zone 2 £5,668 £7,085 £8,502 £ 566,800

Zone 3 £33,202.50 £41,403.13 £49,803.75 £3,320,250

Zone 4 £1,669 £2,086.25 £2,503.50 £ 166,900

Zone 5 £29,465 £36,831.25 £44,197.50 £2,946,500

Zone 6 £29,066 £36,332.50 £43,599 £2,906,600

Total £174,111.50 £179,371.76 £243,242.25 £17,411,150.00

Number of businesses: 449

Figure 19

27

4.3 Levy rates by BID area

Whilst decisions regarding levy rate and threshold are paramount, the demarcation of boundaries is also essential and particu-

larly relevant to this question.

In a UK context, BIDs are primarily associated with town centres, the boundaries of which are often clear, although fluid; tradi-

tional infrastructure offers natural boundaries. In a small town context this can spatially reflect a fairly limited district, as ser-

vices and businesses are condensed into the core region. A measure of this is certainly visible in Aberystwyth, with the town

centre core containing 77% of all hereditaments.

That said, our experience elsewhere has shown us that a wider focus of such initiatives is on commercial districts. It is CBDs

(central business districts), for example, that are the focus of BIDs in the urban areas of Cape Town and Johannesburg, South

Africa, and across various locations in the USA and Canada. Distinct from the primarily retail presentations of a small town

centre, an interpretation of commercial interests within a district enables us to adopt a wider focus and a more ambitious pro-

gramme.

The unique relationship between Aberystwyth town centre and its University encourages consideration in this context; the

growth, successes – and more recently, failures – of Aberystwyth University are to some degree reflected in those of the town

centre businesses. Although spatially disconnected there are clear arguments for the inclusion of the University within the BID

zone.

Whilst the impact of this on the total levy outcome (according to the tables above) is large, when mandatory charitable relief

(as is received by the institution on non-domestic rates) is taken into account, the contribution is significantly reduced. BID

legislation leaves decisions of relief, threshold and so on down to the BID itself, therefore considerations must be as to a rea-

sonable and effective contribution from the University should the boundary be drawn to include them.

An additional factor that requires consideration in formulating the BID proposition in Aberystwyth is the the number and scale

of hereditaments that are occupied by the public sector. Depending on where the BID boundary is drawn, a large proportion of

the levy income will be drawn from public bodies or organisations (see table 4 for financial breakdown of these contribu-

tions). Whilst this is not unique to Aberystwyth, the significant investment by these organisations must be recognised, howev-

er the essential, defining feature of a BID—i.e. that it is business-led and commercially focussed— must not be lost. Appropri-

ate governance structures and procedures, and a clear articulation of the strategic roles of each organisation within the BID—

highlighting the cooperative roles of both private and public bodies— will be essential. For further discussion on this see sec-

tion 5.1: Recommendations.

The definition of the BID area could involve any combination of the zones identified above, but should consider the relative

contribution and value each makes to the town, and not simply in a monetary sense.

The following table sets out the potential levy outturn in the case of the eleven different options – each with a £5,000 rateable

value threshold:

28

Option Total Heriditaments Total Levy at 1% Total Levy at

1.25%

Total Levy at 1.5%

Option 1 - All Zones 447 £162,624.60 £179,371.76 £243,242.25

Option 2 - Zones 1 & 2 379 £80,709.00 £101,465.13 £121,063.50

Option 3 - Zones 1 & 3 386 £108,243.50 £135,783.26 £162,365.25

Option 4 - Zones 1, 3 & 5 399 £137,708.50 £172,614.51 £206,562.75

Option 5 - Zones 1, 2 & 3 419 £113,911.50 £142,868.26 £170,867.25

Option 6 - Zones 1, 2, 3 & 4 429 £115,580.50 £144,954.51 £173,370.75

Option 7 - Zones 1, 2, 3 & 5 432 £143,376.50 £179,699.51 £215,064.75

Option 8 - Zones 1, 2, 3 & 6 426 £142,977.50 £179,200.76 £214,466.25

Option 9 - Zones 1, 2, 3, 5 & 6 439 £172,442.50 £216,032.01 £258,663.75

Option 10 - Zones 1, 2, 3, 4 & 5 442 £145,045.50 £181,785.76 £217,568.25

Option 11 - Zones 1, 2, 3, 4 & 6 436 £144,646.50 £181,287.01 £216,969.75

Figure 20

The British Retail Consortium has stated that ‘any levy in excess of 1% of rateable value will be extremely unlikely to deliver

comparable benefits and is therefore unjustified’. Our experience, and the national average (1.4%), show, however, that a

slightly higher levy rate is often recognised as necessary in order to provide an effective (and ambitious) programme of ser-

vices. In considering a spatially wider commercial district, as some of the options listed above reflect, a higher levy rate would

enable the provision of servicing that wider area.

In considering the operational conditions in Aberystwyth, and the potential benefits from undertaking an ambitious pro-

gramme of services, we would recommend a levy rate of 1.25%-1.5% be considered by the BID board.

Whilst we are not currently proposing that a ‘cap’ on higher levy payers should be applied, the possibility should not be dis-

counted as negotiations regarding the inclusion of large occupiers are still ongoing, and compromise is essential in cooperative

initiatives.

4.4 Top ten hereditaments and potential levy payers

The top ten hereditaments across all zones are as follows:

Table 4: TOP TEN HEREDITAMENTS WITH BID LEVY

Figure 21

Business Levy contribution at

1%

Levy contribution at

1.25%

Levy contribution at

1.5%

ABERYSTWYTH UNIVERSITY £15,300.00 £19,125.00 £22,950.00

MORRISONS SUPERMARKET £12,900.00 £16,125.00 £19,350.00

NATIONAL LIBRARY OF WALES £7,750.00 £9,687.50 £11,625.00

CEREDIGION COUNTY COUNCIL £6,250.00 £7,812.50 £9,375.00

WELSH GOVERNMENT OFFICES £5,700.00 £7,125.00 £8,550.00

BRONGLAIS HOSPITAL £4,250.00 £5,312.50 £6,375.00

B&Q £3,175.00 £3,968.75 £4,762.50

MATALAN £3,075.00 £3,843.75 £4,612.50

NEXT £2,775.00 £3,468.75 £4,162.50

CO-OP £2,700.00 £3,375.00 £4,050.00

Table 3: BID LEVY OUTTURN BY OPTION – HEREDITAMENTS ABOVE £5,000 RV THRESHOLD

29

5.0 Conclusions

Since the 19th century Aberystwyth has been a service-oriented town. With the decline of its mining and fishing industries, it

has become primarily a seaside resort, and an educational and administrative centre. Its lack of self-sufficient industry has

created the context for a system of dependence, in which transient and seasonal trade are the primary source of income for

the majority of its businesses. Take note, for instance, of the prevalence of pubs and clubs in the town; over 50 such establish-

ments exist, which is above the number required to cater to the resident population. On the whole, the fortunes of many of

the businesses ebb and flow with the seasons, catering for the students in term-time and the tourists during the summer

months. Whilst there is of course a continuing, year-round clientele to be drawn from the university staff and their families,

and also from those at the National Library and the hospital, their contribution is not enough in itself to sustain the town. Alt-

hough presented as a stimulus for growth in the town, the more recent construction of Welsh Government offices has not, it is

said, significantly impacted on town centre trade.

The dangers of over-dependency on the university have been illustrated over the past two or three years, in which the univer-

sity has experienced a decline in applications and consequently in its student intake. Coupling this with the development of

out of town student villages, local businesses are experiencing a softness in what was once considered a fairly secure trading

environment. This is no more evident than in the student rental market in the town, the stagnation of which has been well

publicised in recent months. The university expects the decline in numbers to be a temporary one, and plans to return the stu-

dent population to its 2012 level by the end of the decade. Nevertheless, it brings a realisation of the need for the town centre

economy to develop commercial strategies which are more broadly based and balanced.

Alongside these issues exist the problems of the town itself, and particularly its retail infrastructure. As many businesses in the

town note, it is not only the student market that is stagnating. A lack of popular commercial enterprises, particularly fashion

retailing, has left Aberystwyth struggling to compete with other areas with a more attractive retail offer. This impacts on the

resident trade as more and more potential customers travel long distances to reach towns and cities that meet their retail ex-

pectations. The increasing number of vacant premises in the town, and the concurrent growth in charity, mobile phone and

betting shops is causing concern amongst business owners that this trade will be lost for good.

Despite these difficulties, the town has a unique character and a strong independent retail offering that holds out the promise

of a revival. Many visitors and tourists return time and time again, and a significant number of students take up permanent

residence in the town once their studies are completed. Whilst in other towns in Wales the economic decline is more evident,

Aberystwyth retains many of its appealing qualities. In order that this remains the case, and that further trade is not diverted

elsewhere, Aberystwyth town centre must evaluate its wider offering, so that through enhancement and promotion of its ex-

isting attractions, as well as development and regeneration of those areas in which it is lacking, it can strive towards a self-

sufficient future working cooperatively with the institutions it supports.

5.0 Conclusions and recommendations for phase two

30

5.1.1 Suggested themes for Core and extended BID programme

The results of the survey, as reported in Section 2, suggest that the following services would be of value as part of the BID pro-

gramme.

1 Enhancing accessibility in and around the town Focusing on access and gateways into the centre, this theme reflects the primary concerns revealed during the business con-

sultations. This could include initiatives such as:

Working with the local authority to develop an effective parking strategy in order to provide better access to

long-stay parking within the town centre, and to approach issues regarding delivery and collection access for

businesses

Developing a strategy to strengthen connections between the town and university, and to connect the town

with the Parc y Llyn retail park

Enhancing gateways

Improvements to signage highlighting services and facilities available in the town

Enhancing the pedestrian experience in the town, particularly with regard to pedestrian routes, in order to

increase footfall in less visited areas.

2 Marketing, promotions and events

Working closely with existing public and private bodies currently engaged in these activities to maximize their

impact

Collaborative advertising for businesses within the town; particularly for local businesses lacking the re-

sources of national organisations

The development of a loyalty scheme within the town with sufficient appeal for residents, students and em-

ployees

Organising events, for example a food festival, to enhance the local offering and attract vistors into the town;

a focus out of season events to counteract the loss of trade from seasonal visitors and students

3 Advocacy and enhanced engagement with public authorities

Establishing a responsive network through which businesses can communicate effectively with the local au-

thority

31

Collaborative approach to regeneration and development of the town, and the integration of a ‘business voice’

into these proceedings

4 Business support

Development of a support strategy for small and local businesses in order to generate growth

Develop a strategy to attract new commercial enterprises into the area in order to diversify the existing retail

offering

Collective purchasing of services such as electricity and waste collection to reduce overhead costs

Provide access to training and support facilities for business owners and staff

Provide opportunities for business networking focused on action and the development of new opportunities

5.2 Recommendations and next steps

5.2.1 Recommendations

Recommendation 1:

Considering the results of the survey and all activities to date, the means recommend that the Aberystwyth BID steering group

progress towards a BID ballot.

Figure 22

FOR a BID ballot AGAINST a BID ballot

There is significant support for

the BID concept within the town,

with 79% of businesses in favour

in principle

There is the potential for strong

leadership from the BID Steering

Group, and the possibility of pos-

itive collaboration with Menter

Aberystwyth and good support

from the Local Authority.

There are a number of planned

retail and physical developments

and regeneration efforts taking

place in the town, which the in-

troduction of a BID programme

would complement – especially

in terms of marketing and acces-

sibility.

For the majority, the BID levy

amounts to a relatively small sum

for individual businesses and

should be portrayed as such.

Given the number of businesses

and the new developments, the

BID levy out-turn will support a

significant BID provision

There are a number of small busi-

nesses who, in the current cli-

mate, may feel unable to contrib-

ute funds into the BID levy.

Whilst their influence over many

of their costs – for instance non-

domestic rates and rents – may

be constrained they have the

power to impact the BID levy.

The application of a threshold

may, however, counteract this.

For the national organisations in

the town the voting decision will

likely be made outside of the

local area.

The services required within the

town present a definite challenge

for the BID in terms of delivery

and success.

32

Recommendation 2:

Findings from this report should be communicated with businesses in the town, as an opportunity for further engagement and

discussion regarding the BID concept, and in order to secure further participation in the BID steering group.

Further efforts should be made to engage with larger stakeholders – for example the University and the Hospital – with whom

contact has so far been limited. Discussions around the report and the proposed zones and levy outturns will enable an assess-

ment of support from these organisations, and therefore an indication of how best to proceed.

Recommendation 3:

Governance

The unique feature of BIDs is of course that they are business led, and commercial and economic interests should be forefront.

This must therefore be reflected in the approach to governance, and in the proposed strategy and business plan. Whilst BIDs

must acknowledge the social, cultural and civic context of the area, their activities must retain this business focus.

In order to do so, it is essential to address the integrated interests of the public and private bodies in the town, and to under-

take measures in order to ensure that initiatives and collaborative and complementary, without obscuring these commercial

obligations.

As indicated in the survey results, many businesses within the town would like to see their relationships with the council

improved. The same applies, to a lesser extent, to other major stakeholding organisations currently driving change in

the area, for example the university. A sensitive approach to the advocacy and governance of the BID could go some

way to repairing this relationship and furthering future collaborations between the public and private stakeholders in

Depending on the outcome of the boundary, a significant proportion of the levy could be from public bodies; the council

and Welsh Government Offices, the University, The National Library and the hospital to name a few.

Current activities for regeneration of the town, and its marketing and promotion, are largely undertaken by a number of

these public bodies, including the community regeneration organisation Menter Aberystwyth. Collaboration and coop-

eration with these organisations and initiatives will be paramount to the BIDs success. Resources are too scarce to coun-

tenance duplication of effort.

In order that BID is able to address the primary concern of the majority of businesses, namely the issues surrounding

parking services in the town, there must be an atmosphere of trust and openness developed with the County Council.

Mutual understanding of the constraints an opportunities that confront the BID and the council will be a pre-requisite to

any re-evaluation of existing policies and strategies.

The prospect of a BID being established in Aberystwyth coincides with progress on another significant development.

Plans for the Mill Street Car Park development include significant new retail attractors. These will undoubtedly change

the way that Aberystwyth is perceived as a retail centre and will broaden the customer appeal. In addition to the

33

development's draw, there are other advantages for the centre. The County Council has ring-fenced up to

£250,000 from the development proceeds to help improve the performance and footfall of the town centre. This would

be used to enhance and act as match funding for BID eligible projects and schemes over the first five-year term. Negotiai-

tions with the local authority will take place to determine how this additional, significant investment can best be cap-

tured and profiled in the BID Proposal that the businesses will be invited to vote on.

It is therefore essential that the governance framework undertaken should ensure both a strategic lead from the businesses

whilst engaging public authorities in the development and delivery of projects and services. Without such an approach the BID

may become tarred as yet another ‘talking shop’ without the capacity to enact necessary changes.

Recommendation 4:

It is recommended that the BID boundary and the potential zones be analysed and assessed by the BID steering group, and

decided upon at a later date. The group in Aberystwyth is still in its infancy and any decisions on this matter would as yet be

premature.

The means have developed a feasibility matrix which will enable the Aberystwyth BID steering group to effectively assess the

sustainability, viability, marketability and ‘doability’ of each of the proposed zones, and to arrive at an appropriate decision

regarding the boundary. From our analysis to date it is apparent that there a number of viable options in the ways zones could

be combined.

Recommendation 5:

It is recommended that the levy rate between 1.25%-1.5% of rateable value is discussed with the BID steering group and large

levy payers, and informally tested with the constituency.

Despite the recommendations from the BRC we consider a higher levy to be justifiable in Aberystwyth, given the relatively low

rateable values and in order to provide an ambitious programme of services that tackle the big issues facing the town.

Recommendation 6:

It is recommended that the threshold for the levy be set at a rateable value of £5,000, and that the decision regarding a ‘cap’

be postponed until detailed discussions with a small number of the largest hereditaments and undertaken. In order to maxim-

ise the potential of the BID the possibility should not be discounted at this stage.

With regard to the threshold, setting it at £5,000 has a positive, downward impact on the number of hereditaments included

without significant impact on the overall levy outturn. Note that two of the four proposed zones do not contain any heredita-

ments with a rateable value below this threshold.

34

5.2.2 Next steps

A more detailed timetable for the BID campaign can be found in the appendices, but can be summarised as follows:

Table 14: TIMESCALE FOR BID BALLOT (SUMMARY)

Figure 23

Timescale Stage

BID Start Date 1st October 2015

Billing Period & Company set up August 2015

Ballot Period July 2015

BID Proposal Published/BID event April 2015

Initiation of pilot projects, illustrating what the BID

can achieve

September 2014 -July 2015

BID Business Plan signed off End February 2015

BID Campaign begins October 2014

Introductory BID leaflet published and website

upgraded

September 2014

Recommendation 7:

It is recommended that an intensive BID campaign be delivered that includes a series of ‘pilot projects’. In essence, action is

more effective than words, and the opportunity to demonstrate the possibilities of what a BID might do in advance of the

ballot has proved invaluable in securing support. Discussions have already begun with the steering group as to possible pi-

lots, and a proposal is being developed for a collaborative marketing campaign.

Similarly, essential to a successful BID campaign is an ongoing and continued face-to-face presence in the town, and the ma-

jority of businesses should be approached in this manner as part of the campaign. It is recommended that a CRM database

be developed and all businesses within the proposed area offered a meeting at their premises.

35

The means: to change places for the better.

www.themeans.co.uk

Swyddfa Cymru Unit 3, West End Yard, 21-25 West End, Llanelli, Sir Gâr / Carmarthenshire,

SA15 3DN London Office

81 Southwark Street, London, SE1 0HX Phone / Ffôn: +44 (0)20 7261 1010 Phone / Ffôn: +44 (0)1554 780170

36