Embed Size (px)

Citation preview

ההסתדרות הציונית העולמית

The World Zionist Organization

THE OFFICE OF THE COMPTROLLER

ANNUAL REPORT

for 2014

to

THE 37th

ZIONIST CONGRESS

Jerusalem, October 2015

The Office of the Comptroller:

14 Hillel St., P.O.B. 7063, Jerusalem 9107001

Tel: 972-2-6204500 Fax: 972-2-6204545

Delegates to the 37th

Zionist Congress,

I am honored to submit to the 37th Zionist Congress a Report on the

activities of the Office of the Comptroller for the year 2014 and since the

36th

Zionist Congress.

The volume includes reports that were discussed at the Subcommittee for

Control of the Zionist General Council Standing Committee for Budget and

Finance.

According to the Statutes of the Comptroller and the Control Office (18b),

the Chairman of the Zionist Executive should prepare a response to the

individual reports submitted by the Comptroller. Such a response has not

been received for each of the individual reports included in this volume.

The Comptroller's recommendations should be thoroughly reviewed by the

controlled bodies and implemented thereafter in order to improve ways of

management, use of human resources, and funds allocated to them.

I would like to thank the Chairperson of the Control Subcommittee and the

members of the Subcommittee for their assistance in pursuing the

implementation of my recommendations, as well as the Controlled bodies

for their cooperation. Thanks go also to my staff for their thorough work.

Asaf Sela

Comptroller

Jerusalem, October 2015

2

Message of the Chairperson of the Subcommittee for Control

The World Zionist Organization

Standing Committee for Budget and Finance

1. The Comptroller of the National Institutions examines the activities

of the World Zionist Organization. Since the 36th

Zionist Congress

and following the election of the present Chairman of the World

Zionist Organization, the Comptroller and his staff have been

working to provide the members of the Subcommittee for Control

and the World Zionist Organization with reports that include

findings and recommendations for discussion and conclusion with

the reviewed entities.

2. The Subcommittee for Control regards the work of the Comptroller

and his staff as an important auxiliary tool for proper management

of the various institutions and organizations and emphasizes this

stand in its meetings.

Also, the Subcommittee, together with the Comptroller and in

coordination with the reviewed bodies, follows up on the

implementation of the recommendations specified in the

Comptroller's reports.

3. In view of the last two years' experience, I recommended to the

Chairman of the World Zionist Organization that it is appropriate to

grant an independent status to the Subcommittee for Control of the

Standing Committee for Budget and Finance. I was informed that a

resolution on the matter was approved at the XXXVI/5 Zionist

General Council, in February 2015. This decision constitutes

recognition of the importance of the work of the Comptroller and its

stature in facilitating proper management of the reviewed entities.

4. The Subcommittee expresses its appreciation of the thorough on

going work of the Comptroller and his staff in conducting the

examinations and preparing the reports, while constantly aspiring to

improve the activities of the World Zionist Organization.

5. I thank the members of the Subcommittee for Control for their

cooperation. Upon completion of our term, I would like to thank all

those involved in this important endeavor and wish success to those

who will follow us and serve on the independent Control Committee.

Baruch Levy, Ph.D.

October 2015

Table of Contents

Activities of the Office of the Comptroller during the Period

Covered by the Report ........................................................................... 11

List of Reports Prepared in the Years 2005–2015 ............................ 15

Comptroller's Reports:

The Zionist Federation in South Africa ............................................. 19

Objectives ............................................................................................... 21

Method and Scope .................................................................................. 21

Background ............................................................................................ 21

Support of Activities in South Africa ..................................................... 25

The World Zionist Organization Office in France ............................ 31

Objectives ............................................................................................... 33

Method and Scope .................................................................................. 33

Background ............................................................................................ 33

Legal Status ............................................................................................ 35

Budget .................................................................................................... 36

Finances .................................................................................................. 39

Banks ...................................................................................................... 43

Activities ................................................................................................ 46

Personnel and Reimbursement ............................................................... 51

T.L. Culture for Israel Ltd. ................................................................. 53

Introduction ............................................................................................ 55

WZO and the Ministry of Culture and Sport ......................................... 56

WZO and the Company ......................................................................... 58

Company Structure and Institutions ....................................................... 60

Company Operations .............................................................................. 63

Personnel ................................................................................................ 65

Budget and Finances (Company) ........................................................... 67

Income from Ministry of Culture ........................................................... 68

Activity and Program Expenses ............................................................. 68

General and Administrative Expenses ................................................... 70

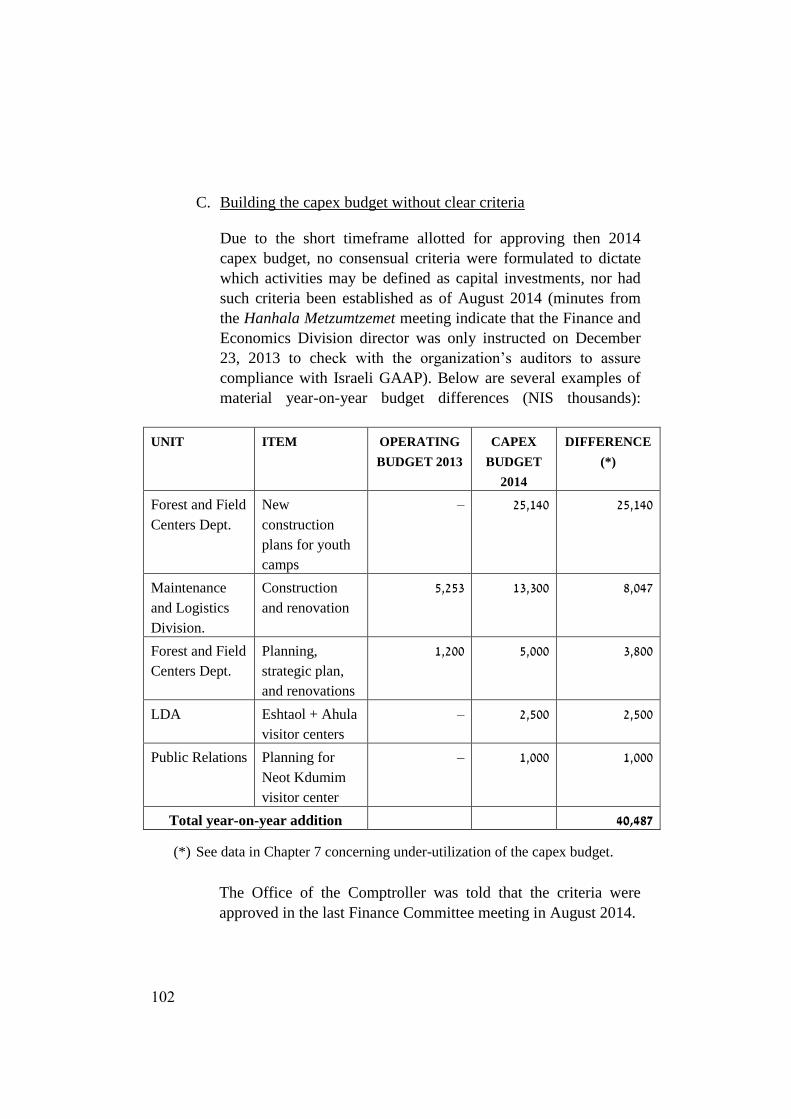

Keren Kayemeth LeIsrael – Budget Preparation ............................. 73

Introduction ............................................................................................ 75

Background ............................................................................................ 78

Budget Preparation ................................................................................. 87

Assumptions in Preparing the Operating Activities Budget .................. 92

Budget Re-allocation .............................................................................. 95

Operating and Capital Expenditures Budget Approval Process ............ 98

Capital Expenditures Budget – Actual Performance ............................. 104

Fixed Costs Budget ................................................................................ 107

Keren Kayemeth LeIsrael – Spokesperson Unit ............................... 115

Introduction ............................................................................................ 117

Background ............................................................................................ 119

Budget Performance in 2014 .................................................................. 123

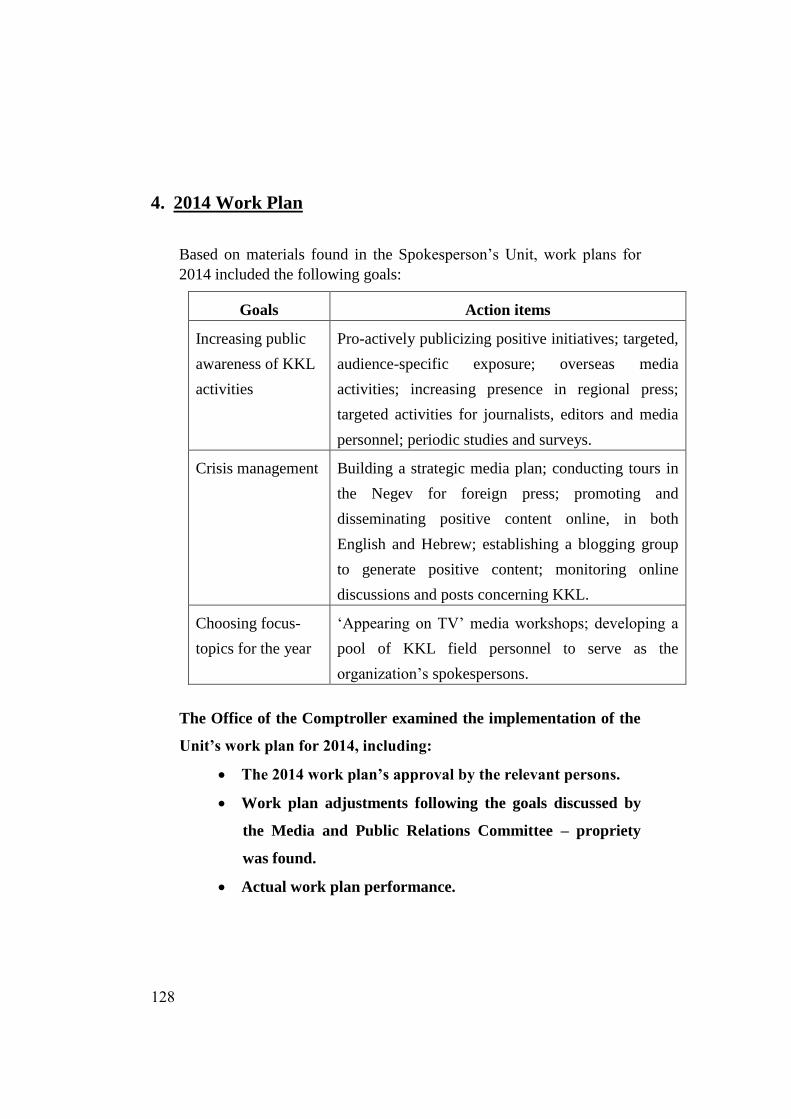

2014 Work Plan ..................................................................................... 128

Service Provider Contracts ..................................................................... 132

Overseas Communications Activities .................................................... 139

Procedures .............................................................................................. 149

Keren Kayemeth LeIsrael – Joint Programs with Organizations ... 153

Introduction ............................................................................................ 153

Budget .................................................................................................... 156

Decision-Making Process ...................................................................... 158

Budget Approval .................................................................................... 163

Contracts between KKL-JNF and the Organizations ............................. 165

Monitoring Compliance with the Organizations

Commitments towards KKL-JNF ................................................. 171

Reporting on the Utilization of KKL-JNF Funds .................................. 172

Transferring KKL-JNF Funds to Organizations .................................... 173

Funding for WZO Organizations ........................................................... 174

Fiscal Conduct ........................................................................................ 199

Summary ................................................................................................ 205

Keren Hayesod – Property Management ........................................... 207

Introduction ............................................................................................ 209

Background ............................................................................................ 212

Ongoing Property Management ............................................................. 215

Disposal of Properties ............................................................................ 233

Procedures .............................................................................................. 235

Identifying and Reclaiming Properties .................................................. 237

American Zionist Commonwealth Inc. Lands ....................................... 238

Statutes of the Comptroller and the Control Office,

The World Zionist Organization ........................................................ 243

Activities of the Office of the Comptroller

During the Period Covered by the Report

12

13

Activities of the Office of the Comptroller

During the Period Covered by the Report

Functions of the Comptroller

The authority of the Comptroller of the Word Zionist Organization is drawn

from Article 60 of the WZO Constitution, which determines the independent

status and main functions of the Comptroller. Detailed provisions on the

functions and mode of operation of the Comptroller can be found in the

Statutes of the Comptroller and the Control Office, as passed at the Zionist

General Council, (brought below, in the last section of this book).

It is the Comptroller's task to conduct an independent review of the WZO

departments, the National Funds and other bodies, as defined in Clause 10

of the Statutes, in order to ascertain whether they operate within the

desirable norms of legality, budgetary discipline, financial accountability,

administrative propriety and efficiency, and moral integrity. The Office of

the Comptroller also deals with complaints from the public concerning the

bodies coming under its purview.

The control findings, together with the Responses of the Chairman of the

Executive, are debated in the Standing Committee for Budget and Finance

of the Zionist General Council, which has set up a special sub-committee for

this purpose. The individual reports included in this Report to the 37th

Zionist Congress, have been debated in the sub-committee, yet without the

Responses to the Chairman of the Executive, that have not been submitted.

The WZO Comptroller, who is elected according to the Constitution by the

Zionist Congress, may also serve as Comptroller of the Jewish Agency, if so

elected by the Board of Governors of the Agency. This linkage of roles has

existed in practice for many years.

14

One Office of the Comptroller –

Several Entities Under Purview

It is important to stress that the Office of the Comptroller functions as one

unit controlling the gamut of activities of the National Institutions. Thus it

achieves flexibility in placing control teams in the various controlled entities

and creates a possibility of implementing lessons drawn from control of one

entity to the other.

Reports of the Office of the Comptroller

Following the Comptroller's Report to the 36th

Zionist Congress of June

2010 which reviewed the control activities since the 35th

Zionist Congress

convened in June 2006, Annual Reports were submitted to the Zionist

General Council in June 2012, November 2013 and February 2015.

Annual Reports were also submitted to the Jewish Agency Board of

Governors in June 2010, June 2011, June 2012, November 2013, June 2014

and June 2015.

51

Reports Prepared by the Office of the Comptroller

of The World Zionist Organization

in the Years 2005–2015

Arranged according to the year of publication

The World Zionist Organization

2005 The 34th

Zionist Congress

2005 Allocation to the World Zionist Unions

2005 The Zionist Federation in France

2006 The Department for Zionist Activity

2006 The Hagshamah Department – Payments to the Hagshamah

Movements

2006 Center for Religious Affairs in the Diaspora

2007 Allocations for Reform and Conservative Religious Services

2007 The Human Resources Division

2008 Herzl Center – Museum and Zionist College

2008 The Central Zionist Archive

2010 The Finance Department

2010 Short Term Shlichut at the World Zionist Organization

2010 The Zionist Council in Israel

2012 The 36th

Zionist Congress

2012 The World Zionist Unions – Use of WZO Allocation

2012 The Building at 17 Kaplan Street, Tel-Aviv

2012 Department for Diaspora Activities, Herzl Museum

2012 The Unit for Zionist Shlichut - The Shlichim Set up

51

2013 The Hagshamah Movements – Use of WZO Allocation

2013 The Zionist Council in Israel

2013 Center for Religious Affairs in the Diaspora

2013 The Human Resources Division

Feb. 2015 The Unit for Morim Shlichim in the Diaspora

Feb. 2015 Habayta – Aliyah Promotion Unit

Oct. 2015 The Zionist Federation in South Africa

Oct. 2015 The WZO Office in France

Oct. 2025 Tarbut LeIsrael Ltd.

Keren Kayemeth LeIsrael

2005 Water Reservoirs

2006 Maintenance Division

2006 The Ben Shemesh Land Policy and Land Use Research Institute

2007 Land Development Authority, Land Reclamation Projects and

Roads

2008 Hemnuta Co. Ltd. – The Process of Letting Properties and

Handling the Maintenance Costs

2008 Land Development Authority – Forestry Division, Fire Prevention

2008 Land Development Authority – Arrangements with Land Bed

Haulage Contractor in the Southern District

2010 Communications and Public Relations Division

2010 The Shaar Hagay Khan (Carvansary)

2010 The Resources Development Division – Contribution Funded

Projects

2012 Voluntary Retirement in 2009

2012 The Education & Youth Division

51

2013 Forest Contractors

2013 Short Term Shlichut

Feb. 2015 Salaries and Human Resources

Feb. 2015 Investment Management

Oct. 2015 Budget Building

Oct. 2015 Spokesperson Unit

Oct. 2015 Joint Programs with Third-Party Organizations

Keren Hayesod

2006 Missions and International Events Unit

2007 Human Resources and Emissaries Administration

2008 Legacies and Funds

2010 Short Term Shlichut

2012 Procurements and Contracts

2012 High Priority Projects

2013 Payment Security

2013 Salaries and Human Resources

Feb. 2015 Cash Management

Oct. 2015 Property Management

51

Jewish Agency and Zionist Federation

Activities in South Africa

02

02

02

Jewish Agency and Zionist Federation

Activities in South Africa

1. Objectives

Checking propriety of the following:

1.1 The Israel Center’s finances.

1.2 Administration of the World Zionist Organization’s funds in

South Africa.

2. Method and Scope

The audit was conducted in June 2013 in Johannesburg, at the offices

of the Israel Center, the South Africa Zionist Federation (SAZF), and

Beyachad. The audit also included meetings with relevant persons and

gathering of data, at the Jewish Agency's and World Zionist

Organization’s headquarters in Jerusalem.

3. Background

3.1 South Africa has undergone profound political, social, and

economic changes in the past twenty years. In 2013, South

Africa had a population of about 50 million. The fall of the

apartheid regime in the early 1990s led to the first multi-

racial democratic elections in the country, held in 1994.

Years of apartheid rule had left the nation’s wealth in the

hands of a small social elite, and had led to economic decline,

with 50% of the population living below the poverty line and

00

00

unemployment ranging from 25% to 40% according to some

reports. 1 The official unemployment rate is 28%.

Among other things, the country is coping with public health

problems (epidemics, disease, and a lack of medical

infrastructure), crime, and failing education, especially in the

city of Johannesburg.

3.2 There are approximately 70,000 Jews living in South Africa,

of which approximately 45,000 reside in Johannesburg,

15,000 in Cape Town, and the rest in Durban, Pretoria, and

Port Elizabeth.

According to Jewish Agency data, approximately 85% of the

youths in South Africa go to Jewish schools, most of which

are associated with the Orthodox community. The Jewish

community is traditional in its religious views, and Jewish

organizations such as Chevra Kadisha play an important role

in the structure of the local community.

3.3 Jewish youths have a hard time finding employment in the

various service industries, due to affirmative action favoring

Blacks. Business owners must also comply with various

affirmative action laws, which undermine productivity and

competitiveness.

Limits and quotas imposed on Jews due to affirmative action

are also felt in academic institutions.

Traditional anti-Semitism is quite rare. However, there is

ever-increasing hostility toward Israel, which is superseding

classical anti-Semitism.

1 http://www.themarker.com/news

02

3.4 The Jewish community is known for its strong and extremely

positive ties to Israel. Support of Israel bridges geographic

locations and religious views. Israel is a dominant issue on

the community’s agenda, with SAZF and Israel Center events

attended by many thousands of people throughout the year.

The community invests significant resources in maintaining

its ties with Israel, through a variety of channels.

3.5 In the first years of the new millennium, Jewish organizations

in Johannesburg, including the Jewish Agency, the SAZF, the

local Keren HaYesod (IUA) campaign, WIZO, and others,

joined together to establish an umbrella organization known

as Beyachad.

Beyachad, a local entity, provides each of its member

organizations administrative and logistical services, from a

shared building. These services include: building security and

maintenance, rent, and financial administration services.

Beyachad's finance department manages funds and provides

accounting services for all member organizations, through

Beyachad’s accountant, while keeping the financial data for

each organization separate. Thus, each organization operates

through its own personnel and organs, and remains

administratively independent.

The fact that the organizations’ offices are all located in the

same building allows for easy and immediate contact

between organizations and their personnel, which fosters

collaboration.

In addition to the use of office space, the building hosts

events and activities for the member organizations.

02

02

3.6 In 2002, the Israel Center was established. The Israel Center

carries out the Jewish Agency's and the SAZF’s operations in

South Africa. As such, the Israel Center is the most

significant organization dealing with the local Jewish

community's needs on issues such as Jewish/Zionist identity,

and the Jewish Agency's core themes.

3.7 When the Israel Center opened in Johannesburg, the various

Jewish/Zionist organizations in South Africa started

operating under a single roof, receiving financial and

infrastructure services from Beyachad. The building

administered by Beyachad provides office space for

personnel, and also hosts activities and events.

As aforesaid, Beyachad provides member organizations

financial services through its accounting department and an

accountant which serves as finance director for each

organization, including the local Keren HaYesod (IUA-

IUCF) Campaign, SAZF, the Jewish Agency, etc. The

various organizations using the building pay Beyachad for its

management services, accounting services, and infrastructure.

3.8 The work carried out by the various organizations through

Beyachad is carried out in full cooperation with the local

community.

The Israel Center is regarded as an integral part of the local

community. The Israel Center and the Jewish Agency’s

representative enjoy a great deal of freedom in their actions.

The Israel Center oversees all Aliya-related matters, the Masa

program, the youth movements, Partnership Together (P2G),

short-term programs in Israel such as Encounter, and liaises

with the local Jewish Agency office consisting of community

shlichim, and youth movement shlichim.

02

4. Support of Activities in South Africa

4.1 Budgetary support from the World Zionist Organization

The World Zionist Organization supports and finances the

Jewish community’s activities through the SAZF and the

Israel Center in South Africa. This funding supports the day-

to-day activities and special events, and covers part of the

shlichim’s expenses.

Support includes an allocation by the World Zionist

Organization’s Executive, by the Department for Zionist

Activities in the Diaspora, and by the Unit for Religious

Affairs in the Diaspora. The Zorim Tzionut project receives

more than half of all funds provided by the World Zionist

Organization for activities in South Africa. The project is

primarily funded by the Ministry of Education which has

ownership of the project and credits the World Zionist

Organization for the project’s expenses. The project is also

supported by the youth movements.

02

02

The following table details the World Zionist Organization’s

financial support of the SAZF and the Israel Center (the

aforementioned budgets do not include shlichim-related costs

in the Israel Center and SAZF):

2012 (USD) 2013 (USD)

Budget Expenditure Budget Expenditure

A World Zionist

Organization

Budget

060666 190995 100666 100666

B Transfer to the

Israel Center

500666 500666 050666 060,02

Zorim Tzionut

(operating

expenses and

shlichim salaries)

523,49 773075 50,3559 5003527

Ben-Ami (Zorim

Tzionut)

23409 53554 2 2

Zionist Calendar

(Zorim Tzionut)

053224 5,3224 43497 43275

C Total for Zorim

Tzionut

500001, 900001 5200,10 52501,0

Total Support 590001, 5000020 0600,10 0600019

After the World Zionist Organization’s support is determined

(Section A), instructions are issued to the local IUA

campaign (in Johannesburg) which transfers the funds to the

SAZF. Keren HaYesod then charges the World Zionist

Organization for the transfer.

02

Transfer of funds for Sections B and C are effected by bank

transfer from the World Zionist Organization's headquarters

in Jerusalem.

Fund transfers to the SAZF are composed of a fixed

component and a variable component. The variable

component depends on receipt of reports from the SAZF and

supporting documents for the expenses.

The Office of the Comptroller found that the

Department for Zionist Activities in the Diaspora

receives reports and supporting documents for

expenses in connection with the Zorim Tzionut

project and for support for the Israel Center’s

operations. Propriety was found.

The Office of the Comptroller found that data are not

received from the SAZF concerning the

implementation of the work plan. Thus, the World

Zionist Organization cannot implement proper

supervision and control over the utilization of the

funds it provides the SAZF (referring to Section A in

the table).

Support for activities in South Africa includes, as

aforesaid, several components, and they are presented

under separate budget items. The Office of the

Comptroller found that there is no single database

which could present management a full picture of all

support for activities in South Africa.

4.2 The SAZF’s Operations

The SAZF has a work plan which includes activities and

projects involving the Jewish community. Activities are

02

04

usually carried out in cooperation with the Israel Center, with

the help of the Center’s professional staff.

The SAZF’s work plan lists the projects and activities

planned for each month, including their composition.

According to the understanding between the organizations,

the Jewish Agency, through the Israel Center, handles issues

such as Aliya, Masa programs, or other youth programs such

as Encounter. The SAZF is active in special events (holidays,

Yom Hazikaron, Yom Ha’atzmaut, Yom Yerushalaim,

conferences, etc.), and shares in the funding of joint projects

with the Israel Center. Furthermore, the SAZF covers part of

the costs for the youth movement shlichim (Netzer, Beitar,

and Habonim Dror/ Zorim Tzionut in Johannesburg and Cape

Town).

The SAZF’s management meets every month to coordinate

decisions for the coming month.

A review of the minutes from the meetings which took place

in May and March 2013, found that in each meeting, the

minutes from the previous month’s meeting were approved.

Meetings were attended by the SAZF's management and the

director of the Israel Center. In addition, updates were made

concerning key events and upcoming projects.

The reviewed minutes also included highlights from the

discussions in the SAZF’s education committees. The Israel

Center's director also reported on planned activities.

02

4.3 The SAZF’s budget

The SAZF’s budget for 2012–2013 was as follows:

Annual Revenues (ZAR)

0650 0652

Grant for operating activities –

IUA

2395,3222 237203490

Educational programs – IUA – 5223222

Yom Ha’atzmaut grant – IUA 0403222 0923222

Youth movement grant – IUA 2,23222 2,23222

Regional grant – IUA 5,93222 5,93222

Additional grant – IUA – 5023222

Local grants 0923222 –

Special income for Yom

Ha’atzmaut

– 2573222

Revenues from local activities ,223,54 ,293922

Total 10950099,

(0900550)$

00006029,

(0060666)$

As detailed in Section 11.1 above, each year the World

Zionist Organization provides the SAZF with budgetary

support (Section A in the above table).

The SAZF’s budget bears no mention of the World Zionist

Organization’s support, which is included in the local IUA's

transfers to the SAZF.

22

,2

Recommendations:

a. To prepare a comprehensive budget that will present

all allocation of funds for activities in South Africa,

both for the SAZF and to the Israel Center, including

sub-items, according to the various activities and the

utilization of these resources.

b. To supervise the utilization of funds transferred by

the World Zionist Organization to the SAZF, based on

implementation reports of the SAZF’s work plan.

April 2014

13

World Zionist Organization

Office in France

13

11

Word Zionist Organization

Office in France

1. Objectives

To check propriety of the following:

1.1 Fiscal management in the World Zionist Organization’s

(“WZO”) office in France.

1.2 The office’s activities in France.

2. Method and Scope

The audit was conducted in WZO’s office in France in June 2014. The

audit also included meetings with relevant persons and data gathering

in WZO’s headquarters in Jerusalem.

3. Background

3.1 The Jewish community in France is estimated at half a million

Jews with hundreds of thousands more entitled to make Aliyah.

In the last 60 years, there has been an increase in the number of

Jews attending Jewish schools, which are mostly associated with

the conservative Jewish community. Today, 30,000 children

attend these schools, about one third of Jewish children in this

age group. Almost all these schools are public and supported by

the French government, with the French Education Ministry

enforcing uniform requirements for general subjects.

3.2 Recently, hundreds of thousands of people in France have

started sympathizing with anti-Semitic messages. This follows a

sixty-year grace period where anti-Semitic discourse was

considered taboo. Blatant anti-Semites have started breaking the

13

bounds of Holocaust denial and advocate the right to anti-Jewish

discourse. French comedian Dieudonne, who identifies with

Nazi ideology, has more than 600,000 followers on Facebook.

His online videos have been watched more than 23 million

times.

3.3 Recent years have seen a rise in the popularity of reactionary

right-wing parties. These parties preach nationalism, sometimes

ranging into anti-Semitism and xenophobia.

3.4 There are several umbrella-organizations working together in

the Jewish community in France:

Fond Social Juif Unifie – The main organization for

education, welfare and fundraising in the Jewish

community.

CRIF – Conseil Representatif des Institutions – The

council of Jewish communities, representing the

communities before the French government.

Consistoire Central Israelite de France – The executive

body for Jewish religious institutions in France.

3.5 Towards the end of 2012, WZO decided to open regional offices

to better achieve its vision and goals. The office in France was

established to achieve these goals, and especially in promoting

Aliyah.

As part of its Aliyah-promoting activities, the WZO executive

decided to encourage Aliyah to settlements. An agreement was

accordingly signed between WZO and the Settlement Division

which was granted a special government budget for this matter.

Activities are carried out through the Unit for Promoting Aliyah

and supervised by the Office of the Chairman of the Zionist

Executive.

13

WZO’s office in France is situated in Paris. The office employs

local employees, along with a head shaliach. In addition to its

main branch in Paris, the office also operates in additional cities

across France.

Findings and Recommendations

4. Legal Status

Since 2012, WZO has operated a local office in Paris, which carries

out Zionist activities throughout France. WZO’s representative

conducts these activities together with his staff, from an office located

in a rented office building where additional Jewish/Zionist

organizations are based.

The office sought to formalize its legal status in France, and register

as a non-profit organization. To this end, the office prepared draft

articles for an NPO, which were then submitted to the Jerusalem

headquarters for approval.

Since the start of its operations, WZO’s Paris office has enlisted the

aid of the Jewish Agency, whose Paris office is a registered non-

profit. The WZO office uses the Jewish Agency’s office to conduct

financial transactions such as rental payments, insurance, etc.

As of the audit date, no progress had been made in formalizing the

legal standing of WZO’s office. The NPO’s articles of association had

not been approved, no constituent documents had been established,

and thus, the office was not registered in France and its legal standing

has yet to be formalized.

The legal standing of WZO’s office in France, and implications of

its legal standing, should be reviewed together with the legal

counsel.

13

5. Budget

WZO has offices around the world which carry out its vision and

goals. Activities in France are carried out through the following

budgets:

1. The Department for Zionist Activities in the Diaspora.

2. The Unit for Promoting Aliyah.

3. The Department for Activities in Israel and Countering Anti-

Semitism.

4. The Zorim Tzionut Project (funded by the Ministry of

Education and operated by WZO).

5. Additional budgets (Unit for Teaching Shlichut in the

Diaspora, Promoting Zionist Identity, etc.)

13

Budget and expenditure details (as of November 2014):

2013 (USD) 2014 (USD) No. Budget Expenditure Budget Expenditure

(Balance)

1 Section 708.50.38 – Promoting Aliyah

Seminars 000111 031 300,11 ,89

Fairs 0,0111 0101,1 000011 330,30

Prep visits and missions 080911 080080 – 109

Misc. 80911 30780 010111 –

Total – Promoting

Aliyah

000666 (166%)

490693 (85%)

580666 (166%)

480843 (33%)

3 Section 713 – WZO Office Salary 0090339 0000110 03107,1 ,0017,

Office 900111 1773, 710811 9,0801

Activities 1,0111 380807 900111 000010

Total – Section 713 3300448 (166%)

3350196 (94%)

3890896 (166%)

1000691 (03%)

1+3

Total – WZO Office and

Promoting Aliyah

4140448 (166%)

3000353 (58%)

4330896 (166%)

3610034 (85%)

4 Section 701 – Jewish Federation Current budget 190111 190111 300911 0800,7

Activities – – 390111 10003

4 Total – Section 701 080666 (166%)

080666 (166%)

000866 (166%)

330436 (40%)

3 Sections 920-921 – Zorim Tzionut Zorim 300011 090890 970011 3,0700

Hebrew – – 300111 30130

8 Section 702 – Dpt. for Activities in Israel and Countering Anti-Semitism Countering Anti-

Semitism

100911 0,0,11 – –

0 Section 701.03.00.102 – Zionist Identity Project 00911 00911 – –

0 Section 930.00.38 – Teachers Unit Teachers conf. – – 00111 00009

4-0 Total – Federation and

Projects

1060366 1040383 1800066 050416

1-0 Total budget 3040848 (166%)

3460840 (91%)

8610396 (166%)

3090944 (83%)

13

The data indicate:

5.1 WZO budgets both the Paris office and the Zionist

Federation. Funds are transferred separately to these two

organizations, according to their individual plans for projects

and expenses. Each organization manages its budget

separately.

5.2 The WZO office’s budget grew in 2014, as compared to

2013, even though the 2013 budget was not fully utilized. Of

particular note – the budget for promoting Aliyah was not

fully utilized.

ERP system data from November 2014 indicate that the

budget for promoting Aliyah will again not be fully utilized

in fiscal 2014, even though these activities were among the

cornerstones for establishing the Paris office.

5.3 Fixed costs (salaries, infrastructure) account for a material

portion of the overall budget.

5.4 WZO allocates about half a million USD annually to the

office and the Federation, but does not manage to generate

activities matching its budget investments.

5.5 As aforesaid, WZO, through various budgetary channels,

allocates funds to the office and the Federation, to support

activities. WZO’s headquarters in Jerusalem does not have a

supervisory staff position responsible for overall oversight of

WZO’s budget allocations to the various organizations in

France.

Recommendations:

a) To examine the reasons for budget under-, particularly as

concerns activities.

13

b) To manage WZO’s budget in France as a single unit,

consolidating the various budgets and expenses for the various

activities under one table (such as the one above). This will

enable better management and supervision of WZO’s various

activities in France.

6. Finances

6.1 As aforesaid, WZO’s office operates from rented space in

Paris and is responsible for paying its suppliers. The Finance

Department in WZO’s headquarters has sent the Paris office

a finance procedure to establish clear responsibilities and key

workflows.

Lacking an office treasurer, the procedure instructs the office

manager on the following responsibilities:

Budget management

Cash flow management

Supervision over bank accounts

Supervision and control over financial transactions,

including liaising with the Finance Department in

Jerusalem.

Supervision over procurement

Concerning payments, the procedure states that the office

manager must obtain prior approval from the Jerusalem

headquarters for non-current expenses or any expense over

EUR 1,000.

6.2 There are three payment options:

Direct payment by the headquarters in Jerusalem

34

Payment through the Jewish Agency’s NPO (Paris

office)

Direct payment by WZO’s Paris office.

6.3 In practice, the office’s operating expenses are paid as

follows:

In general, payment from a French bank account is

made after prior approval by the Office of the

Chairman of the Zionist Executive and the Finance

Department in Jerusalem.

After the office manager pays for an operating

expense, he asks the Office of the Chairman of the

Zionist Executive and the Finance Department in

Jerusalem to approve reimbursement through the

bank account in Paris.

Direct payment to a supplier by the Finance

Department in Jerusalem and approval by the Office

of the Chairman of the Zionist Executive.

The following expenses are paid through the Jewish

Agency’s Paris office: mobile phone, office

insurance, landline, and participation in joint

activities.

6.4 Procedure

The finance procedure does not provide for the following:

Opening and closing bank accounts, including how to

transfer funds for activities from the office manager’s

bank account.

33

Transfers and recordkeeping for funds transferred

from the Jewish Agency office to suppliers providing

goods and services to the WZO office.

Periodic financial reporting by the Paris office

manager to the Jerusalem headquarters.

The controls which the Finance Department in

Jerusalem must implement over fiscal management in

the Paris office.

6.5 Budgetary controls

WZO’s Finance Department manages the Paris office’s

budget by typing in revenue and expense data, based on the

amounts approved by the headquarters and actual transfers.

Documentation for payments made by the Jewish Agency

(according to agreements and understandings approved by

the headquarters) is also submitted to the Finance

Department, and data are entered in the ERP system.

Based on these data entries, an ongoing budget performance

report is generated for the Paris office. This report details

budgetary items and relevant activities.

6.6 Expense documentation and fiscal controls in the Paris office

Expenses are approved as aforesaid by either the Office of

the Chairman or the Finance Department in Jerusalem. The

Paris office does not have an ERP system to manage its

finances, and all office expenses are recorded by the office

manager in an internal MS Excel file.

33

For internal auditing purposes, the office prepares a

consolidated monthly expense report listing all revenues and

expenses.

Each report specifies the opening start-of-month bank

balance and the end-of-month closing balance. This allows

the office manager to stay on top of the office’s cash flow

while presenting inflow and outflow data.

The Office of the Comptroller examined the following

documents/reports:

Expenses statement for November 2013.

Current expenses for December 2013.

January – March 2014.

April 2014.

6.6.1 All the above documents included opening and

closing bank balances based on bank statements.

Propriety was found.

6.6.2 All documents matched the consolidated expense

statement, as recorded in the office manager’s Excel

file. Propriety was found.

6.6.3 All documents matched the invoices received for the

office’s activities. Propriety was found.

6.6.4..All expenses recorded on the examined documents

were approved in advance by the Jerusalem

headquarters. Propriety was found.

The Office of the Comptroller recommends supplementing the

procedure with the missing provisions as aforesaid.

31

7. Banks

7.1 Lacking a treasurer, the office manager is directly

responsible for managing WZO’s Paris office’s finance. This

includes paying suppliers (fixed and variable costs), expense

reimbursements, and salary payments.

7.2 The Paris office does not have a bank account, as it is not

registered as an NPO or other legal entity.

7.3 Cash outflows and inflows are made, as aforesaid, through

three channels:

a) Directly through the Jerusalem headquarters.

b) Through the Jewish Agency office in Paris.

c) Payment through the office manager’s personal bank

accounts in Paris.

The office manager has a personal bank account (“Personal

Account A”), and another account (“WZO/Personal Account

B”) used for WZO-related activities.

7.4 As these are personal accounts, the office manager is the sole

authorized signatory in both.

7.5 The office manager’s salary is transferred to Personal

Account A.

7.6 Funds are transferred to WZO/Personal Account B for

outgoing payments to suppliers.

7.7 The Jerusalem headquarters does not transfer a fixed amount

each month to WZO/Personal Account B. Transfers are only

made following specific requests.

33

Thus, lacking a payable balance in WZO/Personal Account

B, the office manager uses Personal Account A to pay for

such expenses as travel, refreshments or activity-related

expenses (supplier payments). Payment is made in cash or

using the office manager’s personal credit card, and invoices

are receipts are kept for expenses.

7.8 Once a month, the office manager prepares a revenues and

expenses report, with the help of the accounts manager, who

examines fund transfers, recordkeeping and documentation

(invoices and bank statements).

7.9 Based on this monthly report, the office manager requests

reimbursement from the Jerusalem headquarters for amounts

paid out of Personal Account A.

7.10 Subject to approval of such expenses by the headquarters in

Jerusalem, funds are then transferred from Jerusalem to

WZO/Personal Account B, and from there back to Personal

Account A.

7.11 Bank statements for WZO/Personal Account B are not

examined by the Finance Department in Jerusalem, as an

additional control to that applied by the accounts manager.

7.12 Under the current system, there is no control over the

personal bank account used to pay for the office’s activities.

Transfers to a personal bank account for office activities may

present a risk due to anti-money laundering legislation.

7.13 It is noted that, in all its examinations, the Office of the

Comptroller found proper documentation (invoices and

receipts) and expenses were approved by the headquarters in

Jerusalem.

33

7.14 Upon opening his bank accounts in Paris, the office manager

was issued a credit card, bearing his name. The card was

given to the account owner as a benefit for a period of two

years and has not been used since its issue (the bank account

is charged annual card management fees).

The card was issued without approval by the Finance

Department in Jerusalem. Following the Office of the

Comptroller’s audit, the office manager stated that the card

has been cancelled and returned to the bank.

Recommendations:

a) To consider, together with the Legal Counsel, whether to open

a commercial bank account for the Paris office, with two

authorized signatories. Consideration should also be given to

the risk involved in conducting the Paris office’s activities

through two personal bank accounts.

b) To supervise, through the WZO Finance Department in

Jerusalem, transactions in WZO/Personal Account B.

Response of the WZO Paris Office Manager

Lacking a registered NPO using a formal fiscal management system,

and in order to carry out activities, the office manager was forced to

open a personal account in his name, called Simcha Felber WZO. The

Finance Department in Jerusalem was notified of the plan to open this

account and approved it accordingly

The account is managed (again – for lack of a better alternative) as an

NPO account for all intents and purposes. Payments are only made in

reimbursement and following approval by both the Office of the

Chairman and the Finance Department.

33

8. Activities

The office in France conducts activities geared toward the following:

Promoting Aliyah

Supporting local Zionist movements

Jewish-Zionist education in schools and Hebrew studies

Forming settlement-bound Aliyah groups

Activities are carried out in collaboration with the Jewish Agency,

KKL-JNF, the Zionist Federation in France, the Klitah Ministry,

additional organizations, or independently.

Activities include the following:

8.1 Planning and reporting

The office manager has prepared a work plan for

WZO’s office in France for both 2013 and 2014. The

plan was prepared together with WZO’s headquarters

in Jerusalem.

The office manager has provided the organization’s

management, the organization’s CFO, and the

accounts manager in the Paris office reports on the

six-month work plan. Data is derived from the annual

work plan.

The office manager keeps records of ongoing

activities, and submits monthly summary reports to

WZO’s management.

8.2 Database

One of the office’s main goals is to operate throughout

France to promote Aliyah among eligible individuals.

33

The Office of the Comptroller’s examination of the Paris

office’s activities in 2013 and in the first six months of 2014

found that fairs and conferences had been organized for the

Jewish community in France. The office took part in these

activities together with other Jewish organizations, including

the Jewish Agency.

The Office of the Comptroller’s examinations found that, in

all the above activities, no record was kept of participants’

names. Thus, it was not possible to:

establish a database of participants/prospective

candidates.

conduct follow-up activities

assess the scope and efficacy of these activities.

8.3 Key Activities

Key activities in which the office took part, and WZO’s share

in the costs, were as follows:

0103

Aliyah fairs, usually conducted together with the

Jewish Agency. For example: Israel Fair, share in

costs – USD 3,714; and Aliyah Promotion Fair, share

in cost – USD 3,398.

0100

Israel Today and Tomorrow, conducted together with

KKL-JNF – USD 6,773.

France Fair, conducted together with the Jewish

Agency – USD 8,284.

33

Paris Fair – USD 3,294.

ICUBE Fair in Marseilles – EUR 1,208.

Israeli Independence Day celebration.

Ulpan Olim in Marseilles, participation of USD 1,000

(out of a total cost of EUR 7,000).

Ulpan Gar’in Bouglogne – EUR 1,400 (out of a total

cost of EUR 3,500).

8.4 Collaboration with the Jewish Agency

General

Examination of WZO’s Aliyah-promoting activities found

that the Paris office conducts Aliyah-promoting activities as

detailed in Section 8.3 above. These include Aliyah fairs, as

well as other Zionism-oriented activities.

The Jewish Agency is responsible for the actual Aliyah

process, and for granting eligibility to make Aliyah. Over the

past year, the Jewish Agency’s Paris office has increased its

Aliyah-related activities in the Jewish community. The

Jewish Agency has a dedicated staff for handling Aliyah-

related matters. The staff employs an IT system in managing

these activities, including a database of Aliyah candidates,

actions taken with each candidate, and records of documents

received for Aliyah and eligibility purposes.

The Office of the Comptroller found that meetings

are occasionally held between the WZO and Jewish

Agency representatives. However, joint meetings

have not been established as formal operating

procedure.

33

The Office of the Comptroller found that data is not

shared across the Jewish Agency and WZO IT

systems.

After examining Aliyah-related, the Office of the

Comptroller found the same activities conducted by both the

WZO and Jewish Agency offices, without formal

coordination.

As the Jewish Agency is the leading organization in France

for Aliyah-related matters, it does not seem that the WZO

office in France plans its activities as an auxiliary

organization assisting the major organization conducting

Aliyah activities.

Response of WZO’s Representative in France:

WZO’s purpose in France is clear, and was made clear to the

Jewish Agency representatives: to draw as many Jews as

possible to the Jewish Agency’s offices, to initiate Aliyah

proceedings. This purpose was established uniformly by the

WZO Executive for all countries.

The WZO Executive made promoting Aliyah a major goal

after the Jewish Agency stopped promoting Aliyah in the

Diaspora, including in France, in 2010.

8.5 Ashkelon

As part of the work plan, a meeting took place in 2013

between city hall representatives from Ashkelon with the

WZO representative in France and the director of the Unit for

Promoting Aliyah. The goal of this meeting was to offer an

attractive destination to Aliyah candidates from France.

Thus, secondary issues were specified for further

clarification, ranging from municipal Aliyah benefits, to

informational material, appointing a POC for WZO, etc.

34

There was no actual follow-up to the meeting, and none of

the secondary issues were seen through, so that the city could

be presented to Aliyah candidates.

Response of the WZO Representative in France:

WZO is not responsible for the delay. In 2013, municipal

elections were held which prevented the municipality from

pursuing the matter. After these elections, a WZO delegation

met with the new mayor and his team.

8.6 Settlement Groups

Under WZO’s agreement with the Settlement Division, a

work plan was drafted as aforesaid. The work plan specified

that the Paris office is responsible, among other things, for

establishing ‘settlement groups’.

An examination conducted in June 2014 could not find that

such settlement groups had been established.

Furthermore, it is not possible to know how many olim (if

any) reached the settlements through plans implemented by

the Paris office to date, nor to which settlements they moved,

or if they stayed in these settlements or relocated.

Upon inquiry with the representative, the Office of the

Comptroller found that actions have been taken to establish

three community-based Aliyah groups:

Boulogne, destined for Modi’in

Creteil, destined for Netanya or Kfar Yona

Eretz Moledet, destined for Be’er Ganim (Hof

Ashkelon Regional Council)

33

These community-based Aliyah groups have not yet reached

the point of making Aliyah.

The Office of the Comptroller recommends examining the reasons

for the partial implementation of pre-determined activities. The

Office of the Comptroller further recommends establishing

criteria for assessing the efficacy of Aliyah-promoting activities.

9. Personnel and Reimbursement

The representative assumed his position in France on October 14,

2012. The representative has recruited a team which assists in daily

duties, comprising the following:

Secretary – local employee.

A Department for Diaspora Activities employee (Zorim

Tzionut activities), since 2014.

Accounts manager.

9.1 The accounts manager formerly served as treasurer for the

Jewish Agency Paris office. Today, lacking a treasurer in

WZO’s Paris office, the accounts manager examines and

supervises records of office inflows and outflows.

9.2 These examinations are made in the Paris office at least once

a month. The accounts manager conducts additional

examinations in the Paris office, as applicable and as

instructed by the representative.

9.3 The accounts manager is paid a total of EUR 600 a month.

This amount is transferred directly to his bank account from

the WZO bank account in Jerusalem.

33

This expense is not recorded in the Paris office’s expense

statements. Furthermore, no pay slip is issued for the

accounts manager, nor is an invoice received for this

expense.

In effect, the Paris office does not document in any way the

services rendered by the accounts manager or the fact that he

is employed by the office.

By working in the above method, the Paris office is exposed

to risk from the French tax authorities.

9.4 Representation fees

The representative in Paris is paid a total of EUR 210 a

month. Propriety was found.

9.5 Petty cash

The Paris office does not maintain a petty cash account, and

all reimbursements are recorded and paid as detailed in

Section 6 above. Propriety was found.

9.6 Rental fees

The Office of the Comptroller examined rental payments

made to the representative and the Department for Zionist

Activities employee in the first half of 2014. The

examination found these payments to be properly made.

The issue of payment to the accounts manager and

compliant record-keeping in WZO’s Paris office must be

addressed.

January 2015

T.L. Culture for Israel Ltd.

45

44

T.L. Culture for Israel Ltd.

Introduction

T.L. Culture for Israel Ltd. (“the Company”) was established by the World

Zionist Organization (“WZO”) on April 18, 2010, and began operations on

June 1, 2010.

The Company is a wholly-owned WZO subsidiary. On December 5, 2010,

the Company was registered as a private community interest company under

the Companies Law (Amendment 6), 2007, and the Trusts Law, 1979.

The Company’s main goals as set forth in its constituent documents are to

promote cultural activities in outlying areas, put on shows and events

supported by the Ministry of Culture and Sports in outlying areas, and

increasing access to cultural activities for under-privileged and special-focus

populations, which do not commonly participate in cultural activities.

To achieve these goals, the Company consults townships on cultural

matters, organizes and implements numerous cultural and arts-focused

projects in such diverse fields as: music, dance, theater, literature, cinema,

and the plastic arts.

As aforesaid, these projects seek to curate and reinforce a high-quality local

cultural-artistic repertoire and present it to the general public, with special

emphasis on supporting equal cultural opportunity in outlying areas, in the

Arab sector, and along the border. The Company serves as an operational

arm, leveraging and channeling the local authorities’ cultural administration

budgets.

Activities are carried out with the help of Ministry of Culture and Sports

(“Ministry”) budgets, as well as budgets provided by local authorities

seeking to conduct such projects.

45

At the time of the audit, in the first half of 2015, the Company operated in

202 towns throughout the country, among both Jewish and Arab

populations.

Support for a given project is determined based on several Ministry-

established criteria, according to the town’s geographic region, the number

of residents, distance from the country’s center, and the socio-economic

profile of the given population.

In 2013, the Company’s activities totaled NIS 65 million, of which NIS 18

million came from Ministry budgets, and the remainder coming from local

authority budgets.

In 2014, the Company’s activities totaled NIS 85 million, of which NIS 20

million came from Ministry budgets, about NIS 3 million from Mifal

HaPayis (Israel Lottery), and the remaining coming from local authority

budgets.

In 2015, the Company’s budget was set at NIS 94 million, of which NIS 25

million came from Ministry budgets, and the rest coming from local

authority budgets.

The audit was conducted in the first half of 2015, and focused mainly on

2013, 2014, and 2015.

The audit was based on meetings with relevant employees in WZO and the

Company, examining relevant work flows, procedures, documents, and

entries in the Company’s and WZO’s ERP systems.

WZO and the Ministry of Culture and Sport

WZO’s work with the Ministry is based on an agreement initially signed on

March 23, 2010, for spreading cultural activities from the central region to

the outlying areas of the country.

45

To carry out these activities, WZO established Culture for Israel Ltd. on

April 18, 2010, and the Company began operations on June 1, 2010.

On March 23, 2011, the Ministry and WZO signed an agreement concerning

the project, aimed, as aforesaid, at promoting cultural activities in outlying

areas.

After about one year of operation, WZO was required to submit to a tender.

The Ministry’s Tenders Committee subsequently chose WZO through a

public tender (712012) on November 28, 2011.

WZO’s agreement with the Ministry allows the parties to extend it for 10

years. The agreement is extended annually.

The Office of the Comptroller found that the agreement was extended

through December 31, 2015. Furthermore, the Ministry signed an expansion

of the agreement to a total value of NIS 25 million.

The Office of the Comptroller examined the agreements and expansions,

and found them to be in proper order, duly signed, and effective through

December 31, 2015, as aforesaid.

Under WZO’s said agreement with the Ministry, the latter transfers WZO

funds subsidizing the Company’s operations. These amounts are deposited

in WZO’s general account, and not in a separate account.

The Office of the Comptroller recommends that the subsidies WZO

receives from the Ministry, supporting the Company’s operations, be

deposited in a separate account, to facilitate supervision and control

over the utilization of Ministry funds by the company.

The director of WZO’s Finance Department stated that he

does not accept the Office of the Comptroller’s

recommendation that subsidies received by WZO from the

Ministry be held in a separate account.

45

WZO and the Company

As aforesaid, WZO established the Company as a wholly-owned subsidiary

on April 18, 2010, in order to carry out those goals set forth in WZO’s

agreement with the Ministry:

- Promoting cultural activities in outlying areas, including

producing shows by Ministry-supported cultural institutions in

outlying towns.

- Increasing access to cultural activities for under-privileged

populations and special-focus communities which do not

commonly participate in cultural activities in the country’s

center.

As aforesaid, the Company began operations on June 1, 2010.

The Office of the Comptroller notes that no agreement was signed between

WZO and the Company.

The Office of the Comptroller believes WZO should sign an agreement

with the Company regulating the parties’ interaction. Despite the

Company being a wholly-owned WZO subsidiary, the Company still

constitutes a separate, independent legal entity. It is thus necessary to

ensure, among other things, that WZO’s ties to the Company would not

cause WZO to incur such debt as may be assumed by the Company.

The director of WZO’s Finance Department stated that the

recommendation is accepted and that the contract will be

prepared by WZO’s Legal Counsel.

The Office of the Comptroller found that WZO provides the Company with

several services, such as: communications, computers, accounting services,

handling the Company’s employees’ employment contracts, and legal

services.

45

The Office of the Comptroller further found that WZO has signed the lease

for the Company’s offices. In practice, WZO pays the rental fees, and then

charges them back from the Company.

Upon inquiry as to why WZO has signed the lease instead of the Company,

the Office of the Comptroller was told this was required by the landlord, as

the Company was newly-established when the lease was signed, and had not

yet begun operations.

The Office of the Comptroller believes the lease should be between the

Company and the landlord, and not between WZO and the landlord.

The Company is a separate legal entity, which has been operating for

five years, and should be responsible for its contract with the owner of

its office space.

As aforesaid, the Company reimburses WZO for rental fees. In practice,

WZO offsets these fees from the Ministry’s subsidies for the Company’s

operations.

The Office of the Comptroller examined if WZO’s credit and debit accounts

in the Company’s ledgers match with those of the Company in WZO’s

ledgers. In 2013, these accounts matched fully.

In the period starting January 1, 2014 and until the time of the audit on

February 9, 2015, various mismatches were found in expenses such as

telephone costs, bank fees, Ministry of Justice fees, guarantee fees, etc.

These mismatches, to a total amount of NIS 220,000 were due to sums not

yet recorded in the Company’s ledgers, which had already been recorded by

WZO, as detailed below.

The Office of the Comptroller notes that the Company pays WZO NIS

180,000 annually for various services. This amount is based on part-time

position calculations for legal services which WZO provides the Company.

56

As aforesaid, lacking a formal agreement between WZO and the Company,

it is not possible to examine and verify the contractual terms between the

parties.

Furthermore, upon inquiry, the Office of the Comptroller was told that final

reconciliation of accounts is made when preparing the annual financial

statements. At the time of the audit in June 2015, audited financial

statements were not yet available for 2014.

The Office of the Comptroller believes that accounts and entries in the

Company’s and WZO’s ledgers should be reconciled monthly.

Company Structure and Institutions

As aforesaid, the Company is a wholly-owned WZO subsidiary. At the time

of the audit, the Company had 11 board members (including the chairman),

representing WZO, local authorities, and the public.

The Company has four committees, as follows:

- Executive Committee, comprising nine members who convene

quarterly, receive reports, and approve various plans.

- Internal Audit Committee

- Repertoire Committee

- Pricing Committee

The Office of the Comptroller reviewed minutes from the Company’s

general meetings in the past three years. According to these minutes, the

general meeting convened to approve the Company’s financial statements.

There were no other matters on the agenda. The minutes were duly dated

and signed.

56

The Office of the Comptroller notes that, according to the Companies Law

(154 B), a company auditor must be appointed in each annual general

meeting.

Minutes from the Company’s general meeting indicate that the

Company did not appoint an auditor as required by law.

Following repeated requests, the Office of the Comptroller received six

minutes from Company management meetings, held every three-four

months between June 2013 and early 2015. The minutes from one of these

six meetings was not dated, and four minutes were not signed.

The Office of the Comptroller recommends that minutes be kept for

Company management meetings, and that these be duly dated and

signed.

The director of WZO’s Finance Department and the

Company accepted the Office of the Comptroller’s

recommendation. The Company will make sure that minutes

are duly signed.

The Company’s general meeting appointed an audit committee as required

by law for community interest companies. Among its first actions, the

Committee appointed an internal auditor for the Company. The same CPAs

firm has served as the Company’s internal auditor since it was first

established in 2010.

Minutes from management and general meetings indicate that reappointing

the internal auditor, who has been serving in this position for five years, was

not discussed.

The Office of the Comptroller believes there is room to periodically

review the Company’s engagement with its internal auditor, as common

for contracts with suppliers, even if this is not strictly required by law.

56

The director of WZO’s Finance Department and the

Company accepted the Office of the Comptroller’s

recommendation to periodically renew the contract with the

Company’s internal auditor.

The Office of the Comptroller reviewed minutes from an Audit Committee

meeting which took place in June 2013. No additional minutes were

received. It is unclear whether the Committee had any additional meetings

or if this was the only time the Audit Committee convened in the

Company’s five years of operation.

In the Company’s five years of operations, the internal auditor submitted

only two audit reports: one for 2011 (submitted on December 18, 2012)

concerning “leading projects” in the Company; and the other for 2014

(submitted on April 28, 2015), concerning “salary payments to Company

employees”.

The reports are detailed and cite data as required. They also include

Company responses.

The Office of the Comptroller notes that according to the Companies Law

345(i)(b), “The internal auditor will provide the board of directors a

proposal for an annual work plan…” The Office of the Comptroller found

that no annual work plan was submitted to the board for approval, as

required.

The Office of the Comptroller believes preparing two audit reports over

a five year period is insufficient. The Company should comply with

statutory requirements and submit annual audit plans, and increase

internal auditing activities.

The Company stated in response that it will make sure to

prepare annual audit plans and will increase internal auditing

activities.

56

Company Operations

As aforesaid, the Company operates in 202 towns, providing consultancy

and organization services, and operating cultural activities and special

projects.

The commissioning process begins with the local authority (municipalities

and townships) contacting the Company in writing, specifying the various

shows and cultural activities it wishes to order.

The Company’s website lists the shows and cultural activities offered,

including all details and conditions for ordering. The website also details

prices and subsidy conditions for each activity or show.

As aforesaid, entitlement and subsidies are dictated by the towns’

classification by group, according to distance from the country’s center, the

socio-economic profile of its residents, the number of residents, etc. Criteria

are specific and well-defined. Information is detailed and easily accessible.

As aforesaid, the criteria and subsidy brackets used by the Company are

dictated by the Ministry.

The Local Authorities use Company-employed coordinators, who consult

them in selecting shows. After selecting the desired activity or show, the

local authority signs a contract with the Company. The contract specifies all

the applicable terms and details for the order.

One of the main and most important conditions is a commitment to pay for

the shows in advance.

The Office of the Comptroller examined order work flows in contracts with

20 local authorities. Propriety was found, and work flows complied with the

applicable procedures.

The Office of the Comptroller found that according to section 13 to the

contract, authorities are to provide the Company with ‘show feedback’

55

forms. These forms should include details on the show and the authority’s

level of satisfaction.

The Office of the Comptroller found that the Company does not ensure

that authorities submit their show feedback forms, with only some

authorities submitting these forms.

The Office of the Comptroller recommends that compliance with this

section be maintained, as it provides the Company an important

managerial and supervisory tool.

The Company stated in response that changes were made to the

agreement, so that feedback on shows is provided over the

phone, without need to send in a written form.

The Company has a database of Ministry-approved organizations providing

shows and events. These organizations do not require additional approval by

the Company. The Company’s database also includes shows and events by

organizations not approved by the Ministry, but rather by the Company’s

Repertoire Committee.

The Company’s Repertoire Committee comprises relevant professionals.

Upon inquiry, the Office of the Comptroller was told that no written criteria

are used to guide the Committee in its decisions, and shows are

approved/rejected solely based on the Committee members’ professional-

artistic assessment.

The Repertoire Committee coordinator receives a written opinion from the

Committee members, which includes detailed explanations. Shows and

events approved by the Committee are included in the Company’s database.

Even though decisions do not require additional Ministry approval, the

Ministry may veto inclusion of a show/event in the Company’s database.

Ministry interventions in the Company’s activities are subject to approval

by the Ministry’s legal counsel.

54

Once a year, the Company conducts ‘showcase’ days for cultural

coordinators from local authorities. Participants are given explanations,

lectures, and information on the various cultural activities.

In 2014, the ‘showcase’ was held on April 8, 2014, in the Suzanne Dellal

Center. The event was attended by 350 cultural coordinators from various

local authorities. The event cost a total of NIS 48,000.

The Office of the Comptroller examined the Company’s budget and

expenditure for the event. Propriety was found.

In 2015, the ‘showcase’ event took place on May 5, 2015, under a similar

format and budget as the previous year’s event.

Personnel

The Company has 14 employees, as follows:

- CEO

- 3 accounting personnel

- 4 department directors

- 5 town coordinators (including a coordinator for Arab

townships)

- secretary

11 of these employees hold full-time positions, while 3 hold part-time

positions.

The Company also receives accounting and pricing consultancy services.

The Office of the Comptroller examined the employment contracts for all

employees. All agreements were duly signed prior to employees starting

work, and are effective for an indefinite period of time. The Office of the

55

Comptroller notes that the Company does not have employees sign any

changes in their employment terms.

The Office of the Comptroller recommends that employees sign on

changes in the terms of their employment.

The Company stated in response that it adopts the Office of

the Comptroller’s recommendation.

The Company also has a WZO-appointed accountant, who provides the

Company with services but is not a Company employee. In other words, the

accountant reports to WZO. The agreement with the accountant is based on

his agreement with WZO, signed April 25, 2010.

The Office of the Comptroller notes that there is no written documentation

of the agreement’s extension.

The Office of the Comptroller recommends extending the accountant's

agreement, with the parties affirming its extension in writing.

Under the agreement, the accountant submits an invoice to WZO every

month for services rendered to the Company. WZO pays the cost stated on

the invoice, and is reimbursed by the Company.

The employment agreements with all the employees were drafted by the

Jewish Agency’s Legal Department, using a uniform format.

As aforesaid, the Company’s internal auditor prepared a report on salaries in

2014. The Company’s management is working to rectify the flaws identified

in the report.

55

Budget and Finances (Company)

The following table presents financial data, in NIS, concerning the

Company’s operations as presented in its audited financial statements for

2012 and 2013. Data for 2014 and 2015 are based on the Company’s

ledgers, as audited financial statements were not yet available at the time of

the audit, in June 2015.

2102* 2102* 2102** 1-5/2015**

Revenues:

From Ministry of

Culture

005,225222

0052,25222

005,,55222

0250005222

From local authorities

,550,55,52

6556605050

0550025222

0255005222

Total Revenues ,18,,58,01 9,82098252 0980,08111 2180258111

Expenses:

Activities and

programs

Administrative and

general

505,055000

056665020

00550655,,

05,,05506

5050555222

05,025222

0255055222

5205222

Total Expenses ,081228225 9,822989,0 0285508111 208,908111

Surplus operating

expenses (income)

05,5005

(0,55000)

(056025222)

5005222

Finance expenses

(income)

(,05250) (05,65) 0,5222 (,5222)

Surplus expenses

(income) for the year

0228520

(0908221)

(0825,8111)

0058111

* From audited financial statements.

** From Company accounting ledgers, as of May 2015.