Embed Size (px)

Citation preview

CONTENTS

President Conner's Remarks 1The Nineteenth Annual Meeting 6The New Directors 8Past President Ebert's Remarks 9The Twenty-Second Bond Attorneys' Workshop 12Actions by the Board of Directors

on September 24, 1997 (Susan Weeks) 14Actions by the Board of Directors

on September 25, 1997 (Howard Zucker) 15Actions by the Board of Directors

on November 6 and 7, 1997 (Howard Zucker) 17Washington Saga (Amy K. Dunbar) 18Committee on Securities Law and Disclosure Files Comments

on Proposed MSRB Rule on Selection of Underwriter's Counsel 21Shared Tax Observations (Sharon Stanton White) 24Invitation for Comments on NYC Bar's Proposed Pay-to-Play Rule 28The ABA Task Force on Lawyer Contributions:

A Preview of the Issues (Fredric A. Weber) 33Exposure Draft: Joint Recommendations for Communicating

With the Beneficial Owners of Defaulted Municipal Securities 43Ethical and Malpractice Implications of Representing the Client

in an IRS Audit Where Your Firm Did the Underlying Work(William Freivogel) 51

Liabilities and Professional Responsibilities 52Proposed Amendments to Chapter 9 May Be Unnecessary

and Could Be Counter-Productive (James E. Spiotto) 70Legal Assistants' Corner (Ann L. Atkinson) 80Software Review: Federal Taxation of Municipal Bonds

(Richard H. Nicholls) 81Voice from the Past (Manly W. Mumford) 83Bond Dogs 84Remembering Barry Mann (Henry S. (Hank) Klaiman) 86Editor's Notes 87Quarterly Limericks 88

Volume 18, No. 4 December 1, 1997

The Quarterly Newsletter of the National Association of Bond Lawyers ("NABL") is published on or about March 1, June 1, September 1 and December 1 of each year, fordistribution by first class mail solely to members and associate members of the Association. Membership information may be obtained by writing to Patricia F. Appelhans,Executive Director, NABL, 1761 S. Naperville Road, Suite 105, Wheaton, Illinois 60187, or by calling 630/690-1135. ©NABL, 1997.

The Quarterly Newsletter December 1, 1997

Because opinions with respect to the interpretation of state and federal laws relating to municipal obligations frequentlydiffer, the National Association of Bond Lawyers ("NABL") has given the authors who contribute to The QuarterlyNewsletter, and its editor, the opportunity to express their individual legal interpretations, opinions, and positions. Theseinterpretations, opinions, and positions, whether explicit or implicit, are not intended to reflect any position of NABL or thelaw firms, branches of government, or organizations with which the authors and editor are associated, unless they have beenspecifically adopted by such organizations. For educational purposes, the authors and editor may employ hyperbole or offersuggested interpretations for the purpose of stimulating discussion. Neither the authors, the editor, or NABL can takeresponsibility as to the completeness and accuracy of the materials contained herein; accordingly, readers are encouragedto conduct independent research of original sources of authority. The Quarterly Newsletter is not intended to provide legaladvice or counsel as to any particular situation. Errors or omissions should be called to the editor's attention.

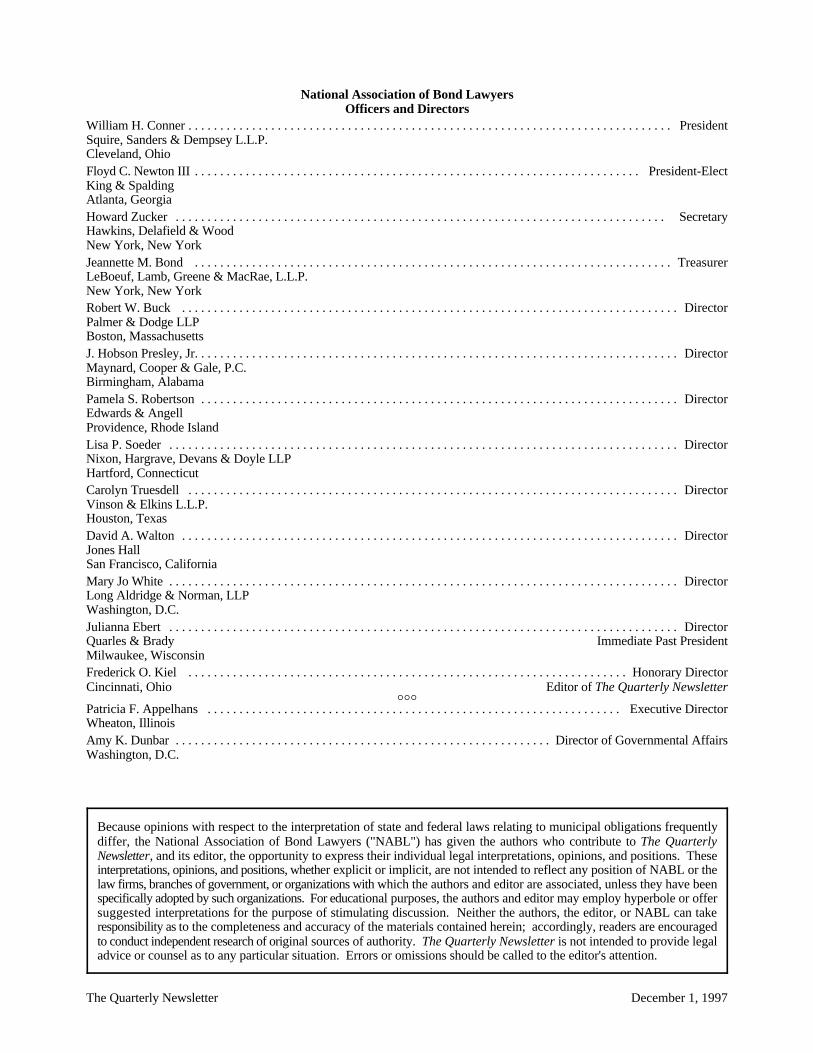

National Association of Bond LawyersOfficers and Directors

William H. Conner . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . PresidentSquire, Sanders & Dempsey L.L.P.Cleveland, OhioFloyd C. Newton III . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . President-ElectKing & SpaldingAtlanta, GeorgiaHoward Zucker . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SecretaryHawkins, Delafield & WoodNew York, New YorkJeannette M. Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . TreasurerLeBoeuf, Lamb, Greene & MacRae, L.L.P.New York, New YorkRobert W. Buck . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorPalmer & Dodge LLPBoston, MassachusettsJ. Hobson Presley, Jr. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorMaynard, Cooper & Gale, P.C.Birmingham, AlabamaPamela S. Robertson . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorEdwards & AngellProvidence, Rhode IslandLisa P. Soeder . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorNixon, Hargrave, Devans & Doyle LLPHartford, ConnecticutCarolyn Truesdell . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorVinson & Elkins L.L.P.Houston, TexasDavid A. Walton . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorJones HallSan Francisco, CaliforniaMary Jo White . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorLong Aldridge & Norman, LLPWashington, D.C.Julianna Ebert . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . DirectorQuarles & Brady Immediate Past PresidentMilwaukee, WisconsinFrederick O. Kiel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Honorary DirectorCincinnati, Ohio Editor of The Quarterly Newsletter

NNNPatricia F. Appelhans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Executive DirectorWheaton, IllinoisAmy K. Dunbar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Director of Governmental AffairsWashington, D.C.

The Quarterly Newsletter December 1, 1997

PRESIDENT CONNER'S REMARKS

Editor's Note: The following remarks were deliv-ered by President William H. Conner at the an-nual meeting of the Association on September 24,1997.

Ladies and gentlemen, I am privileged andhonored to have this opportunity to serve as Presi-dent of your Association over the next twelvemonths. I follow a very distinguished line ofhardworking, extremely capable, highly dedicatedand motivated individuals who have served aspresident of the Association. I will aspire toemulate them and their accomplishments, with thehope that this time next year, you will concludethat I have succeeded and was worthy of the honorof leading this Association.

As my first official act as President, I wouldlike to thank Julie Ebert for her tireless, energeticand capable service as President these past twelvemonths. Congratulations and thanks, Julie, for ajob very well done. Please join me in giving Juliea rousing hand.

When I first began preparation of these re-marks, I went back and reread the speeches mypredecessors had made upon assuming the presi-dency, looking for themes and ideas. What do yousay in the precious few minutes at the end of theannual meeting that concludes the first day of thisreturn of bond lawyers to Capistrano and thecommencement of the cocktail and dinner hour?I am sure many in this room, and certainly all ofthose absent members busy networking elsewhere,would cheer if I followed the example WallyMcBride set two years ago of delivering no re-marks whatever on this occasion. Wally's decisioncame after a tense 90 minutes of the first and onlycontested election — but not coincidentally thebest attended annual meeting — in NABL history.Fortunately for the Association, but unfortunatelyfor you, no such act of leadership is called fortonight.

One of the most striking things about readingthe remarks of past presidents was to be remindedonce again of the developments that concerned usin years past:

• The newly enacted Tax Reform Act of1986, the ink on which was barely dry bythe date of the 1986 Workshop and annualmeeting: how would we cope with thatmassive reform legislation thatfundamentally altered the tax laws appli-cable to tax-exempt bonds and introducedrebate to all of public finance?

• The collapse of WPPSS, the investigationsthat followed and the rising pressure onthe SEC and Congress to do somethingabout secondary market disclosure in thecontext of governmental bonds

• The rise in litigation involving bond law-yers

• The constitutional limits of Congress'power to restrict the federal tax exemptionof State and local governmental obliga-tions

• The increasing politicization in the selec-tion of bond counsel

• The commencement of an active auditprogram by the Internal Revenue Serviceto enforce the tax-exempt bond provisionsof the Internal Revenue Code

• The advent of secondary market disclosurefor state and local government obligations

• And, of course, political contributions, ofwhich I will say more later.

All of these concerns seemed so daunting at thetime. But the world did not end over any of them.The public finance industry survived these con-cerns and today remains healthy and vital to thehealth and well-being of state and local govern-ments. If there is a lesson in this recent history, itis that nothing stays the same for very long.Change is the norm. The challenge for all of usand for NABL is to master that change — toconstructively guide and influence that inexorablechange as much as we can so that the publicfinance industry remains healthy and vibrant andthe role of bond counsel remains essential,challenging and intellectually stimulating.

The Quarterly Newsletter 2 December 1, 1997

One of the issues from the past remains very In the three and a half years since the adoptionmuch with us. Four years ago, the issue of politi- of the NABL Statement, the issue has not beencal contributions by bond lawyers first surfaced. resolved. In fact, the rhetoric surrounding pay-to-President Neil Arkuss characterized the contro- play has steadily increased and, of late, has becomeversy over political contributions in 1993 as "the quite shrill. This is due almost entirely to themost prominent apple" of the apples and oranges narrowly focused crusade of Arthur Levitt, the— thus mixing apples and oranges as Neil occa- chairman of the Securities and Exchange Commis-sionally does. He meant of course that the issue of sion, to effectively prohibit political contributionspolitical contributions by public finance lawyers by municipal finance lawyers. Of late, the presswas then the most prominent among the apples and has joined the fray with a steady stream of articlesoranges on the tree that were ready to drop in our and editorials, all of which accept as fact that thecollective lap. Neil did not equivocate on the practice of making political contributions solely tomatter in his annual meeting remarks: "The use of get business exists in the bond counsel industry andpolitical contributions to obtain underwriting, bond all of which call on lawyers, the SEC, state barcounsel or other professional engagements from associations and/or the ABA to take affirmativestate and local governments is an abuse. The steps to end the practice.integrity of the government process and the inter-ests of taxpayers and ratepayers demand that it bedealt with."

The NABL Board under Neil's leadership did this land that it exists, particularly among munici-what it could. A task force on political contribu- pal finance lawyers. That perception, that appear-tions was established under the leadership of ance of impropriety, by itself is enough to compelHoward Zucker, who tonight begins yet another the legal profession in general and municipalyear of service to the Association as Secretary. finance lawyers in particular to try to come to gripsSome of the best and brightest in our profession with the matter and deal with it effectively.served on that task force. Three months later, afterintensive discussion and deliberation, the task forcesubmitted its report to the Board. That reportbecame the foundation for the "Statement ofProfessional Principles with Respect to PoliticalContributions" adopted by the Board in February,1994. With that statement, NABL became the firstpublic finance group to take a position on what hascome to be known as "pay-to-play."

The key point of the NABL Statement was as dump." I did not make these up. All of thesefollows: "No lawyer should make any Political terms have appeared in media reports over the lastContribution for the purpose of retaining or obtain- six months characterizing the legal practice ining municipal finance engagements," either directly municipal finance. How does it feel to have la-or indirectly. Further, bond counsel should be bored in the vineyards thinking you are making fineselected on the basis of their professional quali- wine, only to be told by the media that you arefications and expertise. The Statement noted the wallowing in a "cesspool of corruption," an "au-integral role that lawyers play in the political thentic garbage dump?" It's not good!process and stated that municipal finance lawyersshould not be penalized in their right, in commonwith other individuals, to make contributions toindividual political candidates. And finally, theStatement endorsed meaningful disclosure ofpolitical contributions by lawyers.

It is no longer relevant to question whetherpay-to-play in fact exists in the legal profession.There is clearly a widespread perception across

While the widespread perception that pay-to-play exists is not confined to municipal financeprofessionals, you would not realize that fromreading the media reports and the editorials aboutpay-to-play. Bond lawyers are always mentioned.Often they are the only professionals mentioned.The words are harsh — "sleazy practice," "sleazepit," "racket," "corrupt," "commercial bribery,""cesspool of corruption," "authentic garbage

Some have accused NABL of "behaving like aflock of ostrich[es];" of failing to exert aggressiveleadership; of whining instead of leading thecrusade. But NABL is limited in what it can do.NABL is a voluntary trade association whosepurpose is to educate, advise and comment onmatters affecting state and local obligations. It is

The Quarterly Newsletter 3 December 1, 1997

not a regulatory agency with the power and author- parties that seem to wind up supporting candidates.ity to make rules binding on lawyers or even bond The New York Times in April ran a lengthy story onlawyers. NABL can do little more than try to the continued high level of indirect giving byinfluence events when the right path is clear and investment bankers, taking full advantage of thesubject to little debate. It can hardly take an loopholes in G-37. There have been stories onaggressive position on an issue over which its contributions by "consultants" retained to drum upmembers are hopelessly divided and as to which business, prompting a proposed new rule by thethe right path is far from clear. MSRB to close that loophole. Recently, stories

Part of the problem is that the term "pay-to-play" is a clever and catchy pejorative term that isapplied to conduct that is not so easily classified.Without question, making political contributionsfor the purpose of obtaining or retaining govern-ment work is wrong and probably unlawful in all50 states. It does not follow, however, that allpolitical contributions by bond lawyers are for thepurpose of obtaining or retaining government workand therefore must be per se wrong and unlawful.Yet that is essentially what Chairman Levitt and thechorus echoing his views have charged. Focusingon the bond lawyers is like shining the flashlight atthe tail of the dog rather than at its head to see if itis snarling.

The root of the problem is not the lawyers, butthat government officials must run for office. Thatis expensive and is becoming more so, it seems,with each election. In short, it takes money to runfor office. Lots of it! Politicians can hardly befaulted for trying to raise money from whomeverthey can, whether they be lawyers, bankers, doc-tors, engineers, Buddhist nuns, Taiwanese orwhatever. They are merely following the advice ofF. Scott Fitzgerald: "Don't marry for money. Gowhere the money is and marry for love."

The perception of pay-to-play originates not somuch with the contributors as with the habitelected officials seem to have of awardinggovernment work to their contributors. What canbe done about that? The MSRB's much heraldedRule G-37 is widely trumpeted as havingeffectively banned pay-to-play among municipalsecurities dealers. Rule G-37 generally prohibitsdealers from engaging in municipal securitiesbusiness with an issuer within two years after anycontribution to an elected official of such issuer bythe dealer or any municipal finance professionalassociated with that dealer. But has it? Scarcely aweek goes by that the media does not report a storyon soft dollar contributions by dealers to political

have appeared suggesting a link between politicalcontributions and the retention of money managersto invest the billions socked away in public pensionfunds.

And the perception of pay-to-play amonglawyers is certainly not confined to bond lawyers.Two weeks ago, USA Today carried an editorialcolumn describing the fact that the handful ofprivate attorneys hired by the states to negotiate amassive settlement with the tobacco industry forwhat are potentially enormous contingency fees arelargely the same attorneys who bankrolled statepolitical campaigns of the officials who retainedthem. I could go on and on.

All of this would seem to suggest to any saneobserver that the way we finance politicalcampaigns is the root of the problem and thatbroad-based campaign reform to deal with theperceived link between political contributions andthe awarding of government business to those whocontribute is needed. Sane perhaps — but notrealistic. One can easily surmise from watchingCongress and state legislatures kick around thefootball of campaign reform that the objective ofsuch efforts is not so much to score points, but tokeep the ball in motion so as to be able to say thatthe problem is being addressed. Broadbasedcampaign reform is not likely to happen in ourlifetimes, for a very obvious reason. Legislatorswho must raise large sums of money to campaignfor office are understandably loath to enacteffective restrictions on the flow of campaigncontributions.

Ah, but the legal profession cannot just sit backand do nothing, since awarding government con-tracts to campaign contributors at least gives theappearance of impropriety, even though it may beperfectly legal and not the least bit corrupt. Theappearance of impropriety must be avoided bylawyers, according to the ethical rules that governus all. And, of course, SEC Chairman Levitt is

The Quarterly Newsletter 4 December 1, 1997

determined to do something about the matter Pursuant to that direction, ABA Presidentinsofar as municipal bond lawyers are concerned. Jerome Shestack has formed a twelve-memberNot the legal profession as a whole mind you; not task force that holds its first meeting next week.industry, commerce or the professions as a whole. Former President Julie Ebert has been asked toJust municipal finance professionals, since only serve on that task force and she has agreed to dothey affect the "market" over which the SEC stands so, along with two other public finance lawyers,as guardian. one of whom served on the NABL political contri-

When NABL adopted its Statement on Politi-cal Contributions in 1994, it pledged to participatewith issuers, broker-dealer associations and otherorganizations to pursue certain areas for furtheraction in the context of political contributions.NABL recognized then what Chairman Levittrecently observed: "the only way to end pay-to-playis through collective action." Perhaps, the oppor-tunity for collective action has arrived. On August6, the American Bar Association House of Dele-gates overwhelmingly approved Revised Resolu-tion 10D. That Resolution, first, "condemns theconduct of lawyers making political campaigncontributions to, and soliciting political campaigncontributions for, public officials in return forbeing considered eligible by public agencies to per-form professional services, including municipalfinance engagements;" second, calls on bar associ-ations, lawyer disciplinary agencies and the judi-ciary to enforce applicable ethical rules to prohibitthis conduct; third, condemns the conduct ofpublic officials considering as eligible for engage-ment only those lawyers who make political cam-paign contributions to, or solicit political campaigncontributions for, public officials; and fourth, callsupon legislative bodies, judicial rule-makingagencies, bar associations, lawyer disciplinaryagencies and public agencies to enact or adopt andenforce laws, rules and regulations that will dis-courage the conduct condemned in the Resolution.The NABL Board supported Revised Resolution Fortunately, no other bar association in the10D since it was essentially the same as the NABL country has supported the City Bar proposal and aStatement, broadened as it should be to include all number of associations have rejected it. Bondlawyers. lawyers must not be sacrificed on the altar of pay-

Revised Resolution 10D calls upon the presi-dent of the ABA to appoint a task force to reviewthe issues related to political campaign contribu-tions by lawyers, consider effective solutionsthereto, and submit recommendations to the ABAHouse of Delegates for consideration at its August1998 meeting.

butions task force in 1993/1994. It is an awesomeresponsibility that the task force undertakes, and adaunting task for Julie and the other municipalfinance professionals on the task force. Once thedeep complexities of the political contributionsproblem have been fully explored and are com-pletely understood, the temptation among lawyerprofessionals outside municipal finance may be tooffer up restrictions solely on bond lawyers as asacrificial lamb, in the hope and expectation thatChairman Levitt will be satisfied and content todeclare victory in his campaign to end pay-to-playamong bond lawyers and will move on to otherregulatory matters. We have already seen anexample of that temptation. A committee of theNew York City Bar Association, apparently lackinga single bond lawyer among its members, hasproposed for adoption in New York State a rulethat would prohibit law firms from doing financework for governments if the firm or any memberor employee thereof has contributed, directly orindirectly, within the prior two years to an electedofficial in a position to influence the award of thatwork. One cannot help but wonder if that proposalmay have been motivated less by the moralistichigh ground it claims than by the desire to nip thekudzu vine banning political contributions by alllawyers before it spreads out of control. The CityBar proposal is to be considered by the New YorkAdministrative Board of the Courts on October 7.

to-play. If political contributions are a problem forthe legal profession, it is a problem among alllawyers, not just bond lawyers. Hopefully, theABA task force will prove to be an enlightenedgroup that fully understands the reality of politicalcontributions, but is nonetheless capable of craftinga broad solution that deals fairly with the problemof pay-to-play and the appearance of improprietyamong the legal profession as a whole and not just

The Quarterly Newsletter 5 December 1, 1997

one small segment thereof: a solution that, if it with the tax laws, the disclosure obligations andmust prohibit doing business with governments to the myriad other puzzles that we must solve daily.whose elected officials you have contributed, as Those who would legislate and regulate us all toothe New York City Bar Association has proposed, often lack that experience and the sobering educa-applies across the board to all lawyers and to all tion that it provides. If we do not participate in thework involving governments, not just bond lawyers efforts of your Association to deal with the issuesand not just municipal finance work. Any solution affecting public finance, we risk the enactment ofthat focuses alone on bond lawyers, and not on the changes that, however well-intentioned, couldlegal profession as a whole, is patently unfair and fundamentally alter our role as bond counsel. Getis likely to produce only one certain result: the involved!separation of bond lawyers from their multi-prac-tice firms into numerous bond law boutiques.

The issue of pay-to-play is a serious one. Asthe work of the task force proceeds, those presentand former NABL board members who have beenclosely involved in NABL's deliberations con-cerning pay-to-play over the past four or five yearsare being asked to assist Julie in any way she findshelpful. I am sure that she would welcome yourthoughts and ideas on this subject as well. Ignor-ing the problem, however, is not an idea she wouldwelcome. The profession must confront pay-to-play in all its ramifications and either find aneffective broad-based solution or recognize thatpay-to-play is something that the legal professioncannot deal with on its own and try to refocus thedebate toward broad-based campaign financereform.

What can we as lawyers do? We must all getinvolved in the debate, not just on pay-to-play buton the other issues of the day that confront theAssociation and its members. In short, more of usmust volunteer to participate in the work of theAssociation and its committees as they work tocarry out the Association's principal goal — toeducate its members and contribute to the well-being of the public finance industry. I ask you togive something back to that unique niche of thelegal profession called bond counsel. You can dothat by volunteering to serve on a committee of theAssociation and by getting involved in committeeprojects. Yes, I know, in this day and age in whichwe are all expected to do more with less, of pres-sure to increase chargeable hours and attract newclients, who has time to get involved? We musttake the time. We simply must not neglect ourprofession or our unique corner of it. We haveexperience in the real world of public finance —we know what it is like in the trenches, dealing

Thank you for your patience, and good eve-ning. This meeting is adjourned.

TRY IT: www.nabl.org

The Quarterly Newsletter 6 December 1, 1997

THE NINETEENTH ANNUAL MEETING

The Nineteenth Annual Meeting of the Na-tional Association of Bond Lawyers was called toorder by President Julianna Ebert at 5:40 p.m.,Central Daylight Time, on September 24, 1997, atthe Downtown Marriott Hotel, in Chicago. Inattendance were all officers and members of theBoard of Directors of the Association, ExecutiveDirector Patricia F. Appelhans, Director ofGovernmental Affairs Amy K. Dunbar and ap-proximately 80 other members of the Association.

President Ebert announced that the first orderof business was a report from Treasurer Floyd C.Newton III. Treasurer Newton announced that thefinancial condition of the Association is sound,noting that the membership of the Association isexpected to reach 3,000 by year-end and that BondAttorneys' Workshop registrations exceed 1,000.Treasurer Newton also said that the Associationcurrently has a fund balance approximately equalto one year's expenses, and that the Board ofDirectors has decided not to raise dues in 1998 butwill continue to monitor seminar expenses in orderto maintain adequate reserves.

President Ebert thanked Treasurer Newton forhis report and spoke about those members, direc-tors, officers and other volunteers as well as thestaff of the Association who had made significantcontributions to the Association during the prioryear. She gave special thanks to NABL’s Commit-tee Chairs and Vice-Chairs and praised their effortsin the past year. Ms. Ebert's remarks are printedinfra.

President Ebert then introduced ImmediatePast President William H. McBride, Chair of the JOB BANK1997 Nominating Committee, who remindedmembers that, in accordance with Article VII ofthe By-Laws of the Association, the NominatingCommittee consisted of five persons, a majority ofwhom were not current directors or officers ofNABL. Mr. McBride then presented the report ofthe 1997 Nominating Committee as previouslycirculated to the membership. He also stated that,pursuant to the By-Laws, because no member ofthe Association had indicated an intention to makeany other nominations, no other nominations

would be accepted. Accordingly, the nominationsof the Nominating Committee were presented foradoption. Upon motion of Immediate Past Presi-dent McBride, seconded by Samuel C. Stone, thenominees of the Nominating Committee wereapproved by unanimous vote of the memberspresent and voting at the meeting and, thereupon,Floyd C. Newton III became President-Elect,Jeannette M. Bond became Treasurer, HowardZucker became Secretary, Carolyn Truesdell andMary Jo White became members of the Board ofDirectors for terms expiring in 2000, and David A.Walton became a member of the Board of Direc-tors for a term expiring in 1998. It was noted thatWilliam H. Conner became President automaticallyupon the election of a new President-Elect and thatJ. Hobson Presley, Jr., would become a member ofthe Board of Directors by virtue of his being thenext Chair of the Bond Attorneys’ Workshop.Julianna Ebert, as Immediate Past President, willcontinue as a director pursuant to Section 5.02 ofthe By-Laws.

President Conner then addressed the mem-bership. His remarks are printed supra.

The meeting was adjourned by PresidentConner at 6:25 p.m., Central Daylight Time.

Susan Weeks

Secretary

NABL

has a

for members and public sector lawyersseeking employment opportunities

with private law firms.

Contact Patricia Appelhansat

630/690-1135

The Quarterly Newsletter 7 December 1, 1997

The

Ass

ocia

tion

's 1

997-

1998

Boa

rd o

f D

irec

tors

and

Exe

cuti

ve S

taff

Seat

ed, l

eft t

o ri

ght:

Pam

ela

S. R

ober

tson

, Pre

side

nt-E

lect

Flo

yd C

. New

ton

III,

Sec

reta

ry H

owar

d Z

ucke

r, P

resi

dent

Will

iam

H. C

onne

r,T

reas

urer

Jea

nnet

te M

. Bon

d, a

nd D

irec

tor

of G

over

nmen

tal A

ffai

rs A

my

K. D

unba

r

Stan

ding

, le

ft to

rig

ht:

Hon

orar

y D

irec

tor

Fred

eric

k O

. Kie

l, R

ober

t W. B

uck,

Dav

id A

. Wal

ton,

Im

med

iate

Pas

t Pre

side

nt J

ulia

nna

Ebe

rt,

Bon

d A

ttorn

eys'

Wor

ksho

p C

hair

J. H

obso

n Pr

esle

y, J

r., M

ary

Jo W

hit

e, L

isa

P. S

oede

r, E

xecu

tive

Dir

ecto

r Pa

tric

ia F

. App

elha

ns, a

nd C

arol

ynT

rues

dell

The Quarterly Newsletter 8 December 1, 1997

THE NEW DIRECTORS

Carolyn Truesdell, a partner in the PublicFinance Section of Vinson & Elkins, L.L.P., Hous-ton, was elected a director of the Association for aterm expiring in 2000. Ms. Truesdell has served asa faculty member for the Fundamentals of Munici-pal Bond Law Seminar for the past five years, andfrom 1986-1988. She has served on the SteeringCommittee for the Bond Attorneys’ Workshop andcurrently serves on the Model Indenture Commit-tee as well as on The Quarterly Newsletter Edito-rial Board.

Ms. Truesdell attended Stanford University andgraduated in 1961 from Case Western ReserveUniversity with a B.A., and from the University ofHouston with a J.D., magna cum laude, in 1975.There she was selected to be a member of theOrder of the Barons. Ms. Truesdell joined Vinson& Elkins after serving as a law clerk to Judge JohnR. Brown, then Chief Judge of the United StatesCourt of Appeals for the Fifth Circuit. Ms.Truesdell practices primarily in the areas ofhousing and industrial development finance asbond counsel, and also represents trustees incorporate and tax-exempt financings.

Mary Jo White, a partner in the firm of Long,Aldridge & Norman, Washington, D.C., waselected a director of the Association for a termexpiring in 2000. She has practiced in publicfinance since 1984. Ms. White has served as bondor underwriter’s counsel in more than 250financings, aggregating approximately $5 billion inprincipal amount. These transactions includegeneral obligation and revenue bond issues, waterand sewer financings, tax increment financings,pooled financings, municipal lease and leasepurchase transactions, credit-enhanced issues and"multi-modal" bond transactions. She has been afrequent lecturer on public finance matters, and isa recognized national expert on disclosure matters.Ms. White has served on the Steering Committeeof the Bond Attorneys’ Workshop and as Chair ofthe Fundamentals of Municipal Bond LawSeminar. She was an Adjunct Professor, Collegeof William and Mary, Marshall Wythe School ofLaw, for the Spring, 1995 term, and created andtaught a course entitled "Municipal Finance andUrban and Economic Development."

From August 1995 to March 1997, Ms. Whitewas an Attorney Fellow, Office of MunicipalSecurities, at the United States Securities andExchange Commission, where she was involved inthe SEC’s activities in all areas of the municipalsecurities industry. While at the SEC, Ms. Whiteworked with the Division of Enforcement onmunicipal securities enforcement matters; theDivisions of Corporation Finance and MarketRegulation on no-action and exemptive reliefunder the federal securities laws; and with theChairman on his prudent investment of publicfunds initiatives. She was appointed the"municipal ombudsman," which involved workingwith the municipal issuer community as well asother municipal market participants.

Ms. White earned her undergraduate degreefrom the University of North Carolina and her lawdegree from the College of William and Mary,where she was a member of the Order of Coif andthe Business Editor of the William and Mary LawReview.

David A. Walton, of Jones Hall, A Profes-sional Law Corporation, San Francisco, waselected a director of the Association for a termexpiring in 1998. He provides tax support and actsas special counsel in the firm's municipal financepractice. In 1989, after five years in private lawpractice, Mr. Walton joined the Internal RevenueService in Washington, D.C., as Counsel to theAssistant Chief Counsel (Domestic) - FinancialInstitutions and Products, specializing in tax-exempt finance and financial products. In June,1990, Mr. Walton joined the United StatesTreasury Department where he served as anAttorney-Advisor in the Office of Tax Policy, alsospecializing in tax-exempt finance.

In 1980, Mr. Walton received a B.S. degree inaccounting from Brigham Young University(summa cum laude) and a J.D. degree, in 1983,from the University of California Hastings Collegeof Law (cum laude). Mr. Walton is licensed as anon-practicing CPA, is a member of the AmericanBar Association - Tax-Exempt Finance Section,and was a member of the Anthony Commission onPublic Finance. During the past three years, Mr.Walton has served as Chair of the Association'sArbitrage and Rebate Committee. From 1993

The Quarterly Newsletter 9 December 1, 1997

NABLhas a

JOB BANKfor members and public sector lawyers

seeking employment opportunitieswith private law firms.

Contact Patricia Appelhansat

630/690-1135

through 1996, Mr. Walton served as a member ofthe Steering Committee of the Bond Attorneys’Workshop. He was a member of the EditorialAdvisory Board of the Public Finance Advisorduring the period of that periodical’s publication,and is currently a member of the EditorialAdvisory Board of the Municipal Finance Journal.

J. Hobson Presley, Jr., a partner withMaynard, Cooper & Gale, P.C., Birmingham,Alabama, has been elected Chair of the BondAttorneys’ Workshop, and will serve as a memberof the Board of Directors during his term asWorkshop Chair. He had previously been amember of the Steering Committee of the BondAttorneys’ Workshop for nine years, and served asSecond Vice-Chair and First Vice-Chair of thatCommittee during the past two years.

In 1972, Mr. Presley received his B.A., magnacum laude, from Birmingham Southern College.In 1975, he received his law degree fromVanderbilt University, where he was Order of theCoif, Student Writing Editor for the VanderbiltLaw Review and a Patrick Wilson Scholar in Law.Mr. Presley has practiced in the area of publicfinance for twenty-one years, and is a frequentspeaker and writer on various aspects of publicfinance.

PAST PRESIDENT EBERT'SREMARKS

Editor's Note: The following remarks weredelivered by outgoing President Julianna Ebert atthe annual meeting of the Association onSeptember 24, 1997.

I am delighted to report that thanks to theefforts of a great number of capable and caringvolunteers, this has been a very productive year forNABL. I am deeply grateful to all of you whohave contributed to the Association's efforts thisyear, and I urge you to continue your commitmentinto the future. While I have tried to thank manyof the active volunteers in The QuarterlyNewsletter, I did want to make a special note ofsome of the contributions again this evening.

The Opinions Committee has revised anddistributed the Model Bond Opinion Report.Special thanks go to Chair and Vice-Chair MichaelBudin and Ed Lucas, Board Advisor HowardZucker, and committee members for all of theirhard work on this project.

The Enforcement Subcommittee of theSecurities Law and Disclosure Committee underthe leadership of John McNally produced athorough discussion and analysis of recent SECenforcement actions which is included in yourworkshop materials. The BondholderCommunication Subcommittee led by MontyHumble is continuing its work to produce amemorandum describing "Recommended Stan-dards for Communicating with the BeneficialOwners of Defaulted Municipal Securities." TheSecurities Law and Disclosure Committee isalso working to finalize comments to be submittedto the MSRB regarding its recently proposed ruleamendments. My special thanks to Chair andVice-Chair Bill Nelson and Walt St. Onge forleading this Committee and overseeing its projectsand to John McNally, Monty Humble, Mary JoWhite, Board Advisor Jack Gardner and the otherswho made significant contributions.

The Professional Responsibility Committeehas worked tirelessly on revisions to the ModelEngagement Letters. An exposure draft of thegovernment obligations letter was published in theJune edition of The Quarterly Newsletter. Thanks

The Quarterly Newsletter 10 December 1, 1997

to active committee members Roy Koegen,Meredith Hathorn, and Mary Anne Braymer, andBoard Advisor Bob Buck for their diligence andpatience in the drafting process. We are lookingforward to the participation of additionalvolunteers and completion of that project in themonths ahead. In addition, the Committee isworking on a revision to the Selection andEvaluation of Bond Counsel and the Role andResponsibilities of Bond Counsel pamphlet. Thework of this committee is extremely valuable, notonly for our members, but for the public whichsometimes misunderstands the function andprofessional responsibilities of bond counsel.

The Section 103 Editorial Board, LindaD'Onofrio, Cliff Gerber, and Kristin Franceschi,not only oversaw revisions and updates to theFederal Taxation of Municipal Bonds, but alsowas instrumental in urging Aspen to produce theCD Rom version which was introduced today. TheEditorial Board worked painstakingly to assure thecontinued high quality of this publication. Ourthanks to them. Thanks, too, to Treasurer FloydNewton, who worked closely with Linda toestablish a better business relationship with Aspen.

Charlie Henck served as Chair, Bill Gehrig asVice-Chair, and Pam Robertson as Board Advisorto the Education Committee which wasresponsible for the production of NABL's threeannual seminars. The reviews this year for allthree seminars were overwhelmingly positive.Charlie and Bill, the seminar chairs and Board, reviewed proofs of each edition; and toAssociation staff did an outstanding job. Our Ric Weber and George Campbell who stood by tothanks to John Cross and Patti Wu, Chair and review any cases requesting or needing amicusVice-Chair of the Tax Seminar; Lauren Mackand Eric Ballou, Chair and Vice-Chair ofFundamentals; and Doug Rollow and MitchRapaport, Chair and Vice-Chair of the Wash-ington Seminar. The expertise and preparation ofthe volunteer faculty, too numerous to mention inthese remarks, are always a key to the success ofthe seminars, and I thank them all.

And as evidenced by the crowds at theregistration desk today, Gigi Benjamin and herVice-Chairs and Steering Committee haveproduced yet another successful Bond Attorneys'Workshop.

The Tax Committees — Arbitrage andRebate (Dave Walton, Chair and Jeremy Spector,Vice-Chair) and General Tax (John Cross, Chairand Larry Carlile, Vice-Chair) — continued anumber of projects, including commenting onproposed regulations on arbitrage restrictions, onRevenue Procedure 96-41 and on the finalregulations on the private activity bond tests. David and John particularly, but also the othermembers of and contributors to those twocommittees and their Board Advisors, Lisa Soederand Jeannette Bond, deserve the warm thanks ofall of us for their efforts. Thanks, too, toPresident-Elect Bill Conner who testified inWashington earlier this year on yield-burningissues.

The Legal Assistants Committee haspublished its "Statement on the Utilization of LegalAssistants in the Public Finance Practice," andcontinues its work on a Legal Assistant'sHandbook. Their efforts have been headed-up byAnn Atkinson, Chair, and Michelle Kelly, nowretired Vice-Chair, with the able assistance ofBoard Advisor Gigi Benjamin. My thanks also toMorrie Knopf and Charles Waters who are leadingthe Form Indenture Committee of theAssociation with the active participation ofImmediate Past President Wally McBride. Thisproject is anticipated to be completed next year.

Thanks are also due to Joe Johnson, DeanPope, Carolyn Truesdell, and Scott Lilienthal,who, as The Quarterly Newsletter Editorial

briefs from the Association. Jim Spiotto and PeterKornman were enlisted to assist with anybankruptcy issues.

Many of the Committee projects and publi-cations were included in editions of The QuarterlyNewsletter this year. I am grateful to HonoraryDirector Fred Kiel for his work as editor of theNewsletter and on other Association publications.He deserves much praise for his efforts on ourbehalf and congratulations on completing 15 yearsas our editor.

The Quarterly Newsletter 11 December 1, 1997

increase professionalism in the municipal financeI would also like to mention the non-Board

members of the Nominating Committee whoprepared the slate of officers and directors that wewill vote on tonight. Helen Atkeson, LindaD'Onofrio, and Bill Nelson were instrumental inthe selections. I believe their thoughtful consid-eration and recommendations will strengthen theBoard and the Association in the future.

the profession and for the clients we serve.Bill Conner was a great help during the year as

President-Elect, and I leave confident that we are As you know, much of this criticism focusesin good hands for next year. Bill, Floyd Newton on the question of political contributions by bondand Susan Weeks, as members of the ExecutiveCommittee, were reliable and thoughtful advisorsthroughout the year.

The loyalty and hard work of Pat Appelhansand her staff in the National office has beenoutstanding. Amy Dunbar in the Washingtonoffice continues to provide us with an essentialWashington perspective and presence. My thanksto both Pat and Amy for all of their efforts thisyear.

Throughout the year, the members of theBoard of Directors have been attentive, con-cerned, dedicated, supportive, and hardworking.My warm thanks to all of you. You are anincredible group of people who have made my jobmuch easier . . . and sometimes even fun! Thankyou for all you have done. I would like to singleout the three retiring Directors, Susan Weeks, JackGardner, and Wally McBride who providedespecially valuable comments and did major workon a number of projects for the Association, notonly during their terms on the Board, but prior toserving on the Board. They have provided manyworthwhile contributions to the Association, and Iknow that they will continue to do so. PastPresidents including Drew Kintzinger, Neil Arkuss,Jane Dickey, and Ric Weber have offered guidanceand encouragement throughout the year.

As busy and productive as the past year hasbeen, it has not been without its challenges. Inspite of the outstanding projects, publications andprograms produced by the remarkably talented anddedicated member volunteers I have justmentioned — projects, publications and programsintended to educate ourselves and others and to

industry — and in spite of the daily efforts of ourmembers to live up to the high standards expectedof bond counsel — there are those who questionthe professionalism and criticize the leadershipefforts of municipal bond lawyers generally and theAssociation specifically. I am disheartened by thisunfair and uninformed criticism. Members of ourAssociation do a tremendous amount of good for

lawyers. In earlier publications (Selection andEvaluation of Bond Counsel (1988)) and(Standards of Practice (1989)), NABL hasadopted affirmative statements regarding thestandards to be followed in selecting lawyers inmunicipal finance transactions. In 1994, theNABL Board of Directors adopted a specificpolicy (Statement of Professional Principles withRespect to Political Contributions) stating thatbond counsel should be selected on the basis ofprofessional qualifications, condemning themaking of political contributions for the purpose ofobtaining or retaining municipal financeengagements, endorsing a role for meaningfuldisclosure, and offering to work with other groupsaddressing the issue.

We now have that opportunity. IncomingABA President Jerome Shestack has appointed aTask Force and included three bond lawyersamong its twelve members — David Cardwell,Jack Williams and me. I am confident that themembers of the Task Force will thoughtfullyconsider all of the issues raised by politicalcontributions by lawyers in crafting recommen-dations to be submitted to the ABA House ofDelegates at its meeting in August, 1998. It is achallenging assignment, and I welcome yourthoughts and suggestions.

As a final thought, I would like to thank mypartners and all the attorneys and staff at Quarles &Brady. During the time I have been activelyinvolved with the Association, they have beenencouraging and understanding. They haveenabled me to maintain my bond practice whileserving the Association. I appreciate all of thesupport they provided me.

The Quarterly Newsletter 12 December 1, 1997

It has been a privilege and an honor to serveyou and the Association over the past year. I lookforward to working with you in the years ahead.Thank you.

[3×5 photo #6]

Bond Attorneys' Workshop ChairVirginia D. Benjamin

Leads off the General Session

THE TWENTY-SECONDBOND ATTORNEYS' WORKSHOP

This year's edition of the Bond Attorneys'Workshop, attended by about one thousand of us(September 24-26), was absolutely scintillating.Hall talk and serious post-mortems tell us that thepanels' faculty members were almost universallywell-prepared, well-spoken, inventive, andreceptive to the life-and-death quaeres posed byattendees. There were the usual scaryadmonitions, and war stories (what does it meanwhen an SEC official nods her head?), but only afew tears.

At the Thursday luncheon, the Association'sBernard P. Friel Medal was presented by formerPresident Harold B. Judell to Joseph H. Johnson,Jr., of Lange, Simpson, Robinson & Somerville,Birmingham, Alabama. Mr. Johnson is a chartermember of the Association with a long history ofservice to the organization. He has served asChairman of its Special Committee on Standardsof Practice (1986-1988), primary author of thatCommittee's reports entitled "The Question ofLawyer Competence and Professionalism" and"Lawyer Proliferation in Public FinanceTransactions," Vice-Chairman of the Committeeon Opinions (1984-1985), member of its Board ofDirectors (1985-1990), Secretary (1986-1987),President-Elect (1987-1988), and President (1988-1989). He currently serves as a member of theEditorial Board of The Quarterly Newsletter.

The Carlson Prize of the Association wasconferred by former Executive Director Rita J.Carlson upon John M. McNally, of Hawkins,Delafield & Wood, Washington, D.C., for his "DueDiligence in the Context of Municipal SecuritiesUnderwritings," which appeared in the March 1,1997, edition of The Quarterly Newsletter.

After the luncheon, attendees were vocifer-ously regaled by members of the song-and-dancetroupe Capitol Steps, who made good musical funof any number of Washingtonians of both parties.We were astonished to see President William H.Conner and 1997-1998 Bond Attorneys' WorkshopCommittee Chair J. Hobson Presley, Jr., on stagefor the troupe's finale.

The Quarterly Newsletter 13 December 1, 1997

[3.1×3 photo #10 - needs cropping]

Joseph H. Johnson, Jr., is Presented withthe Bernard P. Friel Medal by Harold B. Judell

On Thursday morn, the inimitable Charles P.Carlson (co-founder of the Bond Attorneys'Workshop) expostulated on state law develop-ments during the year past, while former presidentRobert Dean Pope sketched out and editorializedupon securities law and lore, and former presidentRichard Chirls lectured on tax law happenings andnon-happenings.

As the co-founder with Chuck, your editor,confessing a certain pride in co-founderhood, iscompelled to conclude that this Bond Attorneys'Workshop was one of the best ever. Notable wasthe proliferation of Federal Express boxes by thehundreds, wherein we could send home our ten-pound bound volumes with no risk of shoulderitis.Notable also were the NABL staff's heroic effortsto deliver (or post) zillions of telephone and faxmessages. Virginia D. Benjamin, the Chair, andExecutive Director Patricia F. Appelhans and herstaff did themselves (and the Association) proud.

[3.1×3 photo #3 - needs cropping]

John M. McNally is Presented withThe Carlson Prize by Rita J. Carlson

Next year, the Palmer House, a Hilton hotel.The folks from the Palmer House handed out about1,000 tote bags to Bond Attorneys' Workshopattendees. (The Ernst & Young people had thepunchbowl full of golf balls.) Other exhibitorswere Bond Case Briefs, The Bond Buyer, Spec-trum Printing (which prints The QuarterlyNewsletter and the Bond Attorneys' Workshopbook), Aspen Law & Business, FSA, the SanDiego Convention and Visitors Bureau in con-junction with Loews Coronado Bay Hotel, whereatthe Tax Seminar will be held next February, andThomson Financial Publishing, which brings us theRed Book.

Some of us toured the Palmer House onSeptember 25, and were treated to high ceilings,spacious vistas, and innumerable portraits of the(very) late Mrs. Palmer. The original PalmerHouse burned in the great Chicago Fire (1871)thirteen days after it was constructed. Mr. Palmerraised $11 million, pretty much on his signature, torebuild. The second incarnation dates in part from1872, with more recent additions, all elegant orfaux-elegant. The staff is wonderful. We thinkyou'll like it. Parenthetically, the first BondAttorneys' Workshops were held at another Hilton,the one near O'Hare.

[3×5 photo #21]

The Quarterly Newsletter 14 December 1, 1997

New Bond Attorneys' Workshop ChairJ. Hobson Presley, Jr.,

Addresses the Thursday Luncheon

ACTIONS BY THEBOARD OF DIRECTORSON SEPTEMBER 24, 1997

The Board of Directors met at the DowntownMarriott Hotel, in Chicago, on September 24,1997. President Julianna Ebert presided. Alsopresent were William H. Conner, President-Elect;Floyd C. Newton III, Treasurer; Susan Weeks,Secretary; Directors Virginia D. Benjamin,Jeannette M. Bond, Robert W. Buck, John M.Gardner, Pamela S. Robertson and Lisa P. Soeder;William H. McBride, Immediate Past President;Honorary Director Frederick O. Kiel; Patricia F.Appelhans, Executive Director; and Amy K.Dunbar, Director of Governmental Affairs.

Report of Treasurer

Treasurer Newton provided an overview of theAssociation's financial results as of August 31,1997, noting that Bond Attorneys' Workshop

revenues and membership dues exceed budgetprojections and that overall expenses are in linewith the 1997 budget. Treasurer Newtonconcluded that the financial position of theAssociation is sound.

Committee Reports

President Ebert then called for Committeereports by Board members.

1. Securities Law and Disclosure

(A) MSRB Rule Comments - DirectorGardner described the progress of the SecuritiesLaw and Disclosure Committee in draftingcomments on the MSRB's recently-proposed ruleamendments relating to the underwriting processand advised that the scope of the comments hadbeen narrowed to the selection of underwriter'scounsel. Following a discussion of the contents ofthe Committee's proposed letter in which Boardmembers offered comments and suggestions,Director Gardner advised the Board of theCommittee's plans to promptly file a revised letterwith the MSRB.

(B) Bondholder Notification - Director ofGovernmental Affairs Dunbar described revisionsto the structure and format of the "best practices"memorandum on bondholder notification. Ms.Dunbar indicated that the memorandum would besubmitted to the respective organizationsparticipating in this project as an exposure draftfollowing additional formatting revisions, editingand resolution of certain differences of opinion.[The exposure draft is printed infra.]

2. Professional Responsibility - Boardmembers offered Director Buck specific commentson the form of governmental bond engagementletter and general guidance on the form of conduitbond engagement letter. President Ebertrecommended that the Committee enlist additionalmembers to provide input on the conduit letter,and Treasurer Newton suggested that theCommittee consider whether additionalcommentary or alternative language should bedeveloped to reflect the situation in which theconduit borrower rather than the issuer is the clientof bond counsel.

The Quarterly Newsletter 15 December 1, 1997

Secretary Weeks then briefed the Board on theformation of a sub-committee to update Selectionand Evaluation of Bond Counsel and the proposed Director of Governmental Affairs Dunbar thentime schedule for this project. President Ebert also gave her report, briefing the Board on (i) an SECreminded Director Buck of the need to update The settlement with Smith Barney in a Dade County,Roles and Responsibilities of Bond Counsel. Florida, derivatives case, (ii) the effort to develop

3. Section 103 Editorial Board - TreasurerNewton described the progress of Aspen, Inc., indeveloping a CD-ROM product relating to FederalTaxation of Municipal Bonds and indicated thatAspen would demonstrate this product at thetechnology session of the Bond Attorneys'Workshop.

4. Education - Upon motion of ImmediatePast President McBride, seconded by DirectorBond, the Board approved the appointment ofLinda Schakel as Vice-Chair of the Tax Seminar.

5. Form Indenture - Immediate Past Presi-dent McBride sought the Board's input on theoutline draft of alternative positions accompanyingthe form indenture before the Board and indicatedthat this material would be discussed at the BondAttorneys' Workshop.

Pay-to-Play Task Force

President Ebert updated the Board on thecomposition of the pay-to-play task force ap-pointed by ABA President Jerome Shestack inaccordance with Resolution 10-B approved by theABA at its August meeting in San Francisco.Board members concurred in President Ebert'sview that she is serving on the task force as therepresentative of NABL, and President Ebertencouraged Board members to provide her inputand guidance. A motion was made by DirectorGardner, seconded by Secretary Weeks andunanimously approved, that the Associationreimburse the expenses of President Ebert inconnection with her service on the task force.

Report of Executive Director

President Ebert then called on ExecutiveDirector Appelhans to give her report, whichincluded an update on membership figures, BondAttorneys' Workshop registrations and exhibitorrevenues. Executive Director Appelhans advisedBoard members that 1998 dues notices would bemailed on October 1, 1997.

Report of Director of Governmental Affairs

a draft joint statement on IRS arbitrageenforcement proposed by certain industry andpublic interest groups, (iii) the status of thereserved portions of the private activity bondregulations, and (iv) a mid-October report of theBankruptcy Commission.

Susan Weeks

Secretary

ACTIONS BY THE BOARD OF DIRECTORS ON SEPTEMBER 25, 1997

The Board of Directors met at 7:30 a.m. onSeptember 25, 1997, at the Downtown ChicagoMarriott, in Chicago. President William H. Connerpresided. Also present were: Floyd C. Newton III,President-Elect; Jeannette M. Bond, Treasurer;Howard Zucker, Secretary; Directors J. HobsonPresley, Jr., Robert W. Buck, Lisa P. Soeder,Pamela S. Robertson, David A. Walton, CarolynTruesdell, and Mary Jo White; Immediate PastPresident, Julianna Ebert; Honorary DirectorFrederick O. Kiel; Patricia F. Appelhans,Executive Director; and Amy K. Dunbar, Directorof Governmental Affairs.

On motion by Treasurer Bond, seconded byDirector Robertson, the Board unanimously votedto appoint Kenneth R. Artin of Cobb, Cole & Bell,Maitland, Florida, to the GovernmentalAccounting Standards Board Advisory Council.

Following a discussion of President Conner'srecommendations for Chair and Vice-Chair andBoard Advisor for each of the Association'sCommittees, it was moved by Honorary DirectorKiel, seconded by Treasurer Bond andunanimously approved that those persons named

The Quarterly Newsletter 16 December 1, 1997

below be appointed to serve as Chair, Vice-Chair, Kristin H.R. FranceschiBoard Advisor or Members, as the case may be, of Valerie Pearsall Robertsthe respective Committees, as follows: Advisor Jeannette M. Bond

Amicus Review The Quarterly Newsletter Committee Chair Fredric A. Weber Members Joseph H. Johnson, Jr. Vice-Chair George E. Campbell Scott R. Lilienthal Advisor Howard Zucker Robert Dean Pope

Arbitrage and Rebate Chair Perry E. Israel Vice-Chair Jeremy A. Spector Advisor Lisa P. Soeder

Bankruptcy Chair James E. Spiotto Harris Bank as a depositary of Association funds, Vice-Chair S. Frank D'Ercole and authorizing the President, Treasurer and Advisor Carolyn Truesdell Executive Director to sign checks and withdraw

Education Chair William L. Gehrig Vice-Chair Lauren K. Mack Advisor Floyd C. Newton III

Form Indenture Chair Morris E. Knopf Committee Chairs would soon need to furnish their Vice-Chair Charles H. Waters, Jr. budgets to Treasurer Bond for inclusion in the Advisor Carolyn Truesdell preliminary 1998 budget.

General Tax Matters Chair John J. Cross, III Vice-Chair Larry L. Carlile Howard Zucker Advisor David A. Walton

Legal Assistants Chair Ann L. Atkinson Vice-Chair Susan M. Parker Advisor J. Hobson Presley, Jr.

Opinions Chair Edwin F. Lucas, III Vice-Chair Virginia D. Benjamin Advisor Pamela S. Robertson

Professional Responsibility Chair Roy J. Koegen Vice-Chair Mae Nan Ellingson Advisor Robert W. Buck

Securities Law and Disclosure Chair William L. Nelson Vice-Chair Walter J. St. Onge III Advisor Mary Jo White

Section 103 Editorial Board Members Clifford M. Gerber

Karen S. Neal Advisor J u l i a n n a E b e r t

Executive Director Appelhans submitted to theBoard for its approval a resolution designating

funds. Upon the motion of Director Truesdell,seconded by Director Presley, the Boardunanimously approved the adoption thereof.

President Conner then reviewed the scheduleof events for the upcoming year and noted that

Secretary

The Quarterly Newsletter 17 December 1, 1997

ACTIONS BY THE BOARD OF DIRECTORS ON NOVEMBER 6 AND 7, 1997

The Board of Directors of the Association metin Savannah, Georgia, on November 6 and 7,1997. President William H. Conner presided.Also present were: Floyd C. Newton III,President-Elect; Howard Zucker, Secretary;Jeannette M. Bond, Treasurer; Directors J.Hobson Presley, Jr., Robert W. Buck, Pamela S.Robertson, Lisa P. Soeder, David A. Walton,Carolyn Truesdell, and Mary Jo White; ImmediatePast President Julianna Ebert; Honorary DirectorFrederick O. Kiel; Patricia F. Appelhans,Executive Director; and Amy K. Dunbar, Directorof Governmental Affairs.

Model Engagement Letters

The President and Director Buck reviewed thehistory of the Model Engagement Letters project,and there ensued a discussion concerning theorganization of the document. The Presidentrequested all Board member comments be sent toDirector Buck and Professional ResponsibilityCommittee Chair Roy J. Koegen prior toDecember 1, 1997. Director Buck expressed hisexpectation of having a revised draft by theFebruary, 1998, Board meeting.

Report of The Treasurer

The President then called on Treasurer Bond togive her financial report, whereupon she providedan overview of the Association's financial results asof October 31, 1997, noting that revenues andexpenses are in line with the 1997 budget. TheTreasurer and Executive Director Appelhans willreview the postage budget and recommend whichAssociation publications and mailings can beshipped at "bulk rate." Director Truesdellrequested that a balance sheet be included in futurefinancial statements.

The Board agreed to hold advertising rates forThe Quarterly Newsletter for 1998 at 1997 levels.Executive Director Appelhans will handleadvertising marketing from the national office.

Upon motion by the Secretary, seconded by thePresident-Elect, the Board voted unanimously to

establish the following seminar registration fees for1998:

Non-Seminar Member Member

Tax $420 $580Fundamentals $395 $545Washington $410 $580 *Bond Attorneys' Workshop $415 $585

* Also, a special rate of $450 forgovernment employees or non-practicing academics

Upon motion by the Treasurer, seconded byDirector Soeder, the preliminary 1998 budget wasapproved unanimously by the Board, with certainadjustments discussed by the Board; the ExecutiveDirector and the Treasurer are to revise itaccordingly and send it to Board members forcomments, with final approval of the changesdelegated to the Executive Committee.

Pay-to-Play

Immediate Past President Ebert will circulatecertain pay-to-play materials which she hasreceived. Upon motion by the Immediate PastPresident, seconded by Director Robertson, theBoard unanimously approved a resolutionauthorizing the President, in his discretion, toexpend an amount not to exceed $3,000 on a jointNABL/ABA Section of State and LocalGovernment Law newsletter on the pay-to-playissue. The Immediate Past President will alsospeak to former Association President Fredric A.Weber about preparing an article about the pay-to-play issue for inclusion in The QuarterlyNewsletter [infra] and, with member input,drafting Association comments on the NYC Bar'sProposed Pay-to-Play Rule.

Committee Reports

The President called for Committee reports.

1. Bankruptcy — Director of GovernmentalAffairs Dunbar gave a report concerning therecently released report of the National BankruptcyCommission. There was discussion of themunicipal portions of the report and discussion ofwhen, if at all, the Association should comment.

The Quarterly Newsletter 18 December 1, 1997

The Secretary observed that this would be an project is being led by former Director Susanappropriate topic for the Washington Seminar. Weeks. Director Buck related that Ms. Weeks

2. Arbitrage and Rebate — Director Soeder ledthis discussion. It was decided to ask thisCommittee and the General Tax Matters Com- 8. Education — The Board approved themittee to work together on certain projects, selection of G. Mark Mamatov, of Bass, Berry &especially giving issuers the right to appeal Sims, PLC, Knoxville, as Vice-Chair of thetechnical advice memoranda, creating an articu- Fundamentals Seminar.lated standard for the issuance of TAMs, devel-oping an alternative dispute resolution process,creating something like a "tax matters partner"concept for tax-exempt debt so that the issuer orconduit borrower will have the right to representthe bondholders, and developing rules relating toasset hedges. It was also decided that on the issueof yield burning, the Association would continue toprovide technical advice but not take a leadingrole.

3. General Tax Matters — Director Walton ledthis discussion. (See also paragraph immediatelyabove.) The Committee is on the lookout for theoutput regulations and expects to provide input assoon as they are released. There was alsodiscussion about two recent private letter rulingsconcerning "residential rental property."

4. Securities Law and Disclosure — DirectorWhite led this discussion. The Board had before itthe bondholder notification report as to whichcomments are due by December 10. It wasdecided to try to update the Association's 15c2-12book in combination with the EnforcementSubcommittee Report and to establish an editorialboard therefor.

5. Section 103 Editorial Board — TreasurerBond acknowledged the very good work done byformer Section 103 Editorial Board Chair Linda L.D'Onofrio in having prepared and distributed theerrata sheets for the most recent edition.

6. Opinions — Director Robertson stated that sheexpected the Committee to have an exposure draftof a model underwriter's counsel opinion report forthe February, 1998, Board meeting but that theBoard would likely not act on a proposed draftprior to the Spring meeting.

7. Professional Responsibility — Director Buckupdated the Board on the status of the revision ofSelection and Evaluation of Bond Counsel. That

suggests the Association's work product be sharedwith GFOA.

Report of the Director of Governmental Affairs

The Director of Governmental Affairs briefedthe Board on, among other things, the followingmatters: the Output Facility Regulations, ListServeand Web Page issues, $150 Million Cap issues, andcooperation with ALAS.

Report of the Executive Director

The Executive Director briefed the Board onthe following matters, among others: membership(3,016 as compared to last year's 2,961); duesinvoicing and renewals; Bond Attorneys'Workshop (958 attendees); 1998 Tax Seminarplanning; and scheduled Fundamentals Seminarand Washington Seminar meetings.

Howard Zucker

Secretary

The Quarterly Newsletter 19 December 1, 1997

WASHINGTON SAGA

Congress has left town, but not without doingsome damage on its way to adjournment. SenatorMurkowski introduced S.1483 and S.1513,identical bills required by parliamentary floorprocedure, relating to the tax treatment of bondsused to finance electric output facilities. Itseffective date is November 8, 1997, for sales ofoutput affected by the amendments of the bill.Sharon White has provided analysis of the bill inher “Shared Tax Observations” column herein. Ifyou would like copies of either the bills or thereport she refers to, please contact our office. It isfair to say that our world is a little safer now thatCongress is gone. If Treasury decides to issue theoutput regulations in the face of the implicit threatsprovided by the Joint Committee Report andSenator Murkowski’s legislation, it will be easierfor them to do so with Congress not in session.That being said, it was certainly intended that theReport and the legislation discourage the Treasuryfrom releasing the long-awaited regulations.Unfortunately, it appears that we have reverted tothe era when members of Congress, knowing thatbond counsel may be discouraged from renderingclean opinions on transactions, use immediateeffective dates to try to block the issuance ofbonds.

$150 Million Cap on 501(c)(3) Bonds

Now that the cap on the issuance of new bondsfor new capital expenditures for non-hospital501(c)(3) bonds has been lifted, interpretivequestions are arising. The Joint Committee onTaxation will be providing a “Blue Book” on thelegislation enacted this summer and we can expectthat there may be interpretive guidance therein.NABL will be working with other members of thepublic finance and 501(c)(3) community to seekappropriate guidance from Treasury, the IRS, andthe Joint Committee. You should feel free tocontact John Cross, Larry Carlile, or me with yourconcerns or post them in the Tax Law section ofthe NABL web page.

NABL Web Page

The web subcommittee of the EducationCommittee is working on redesigning the web pageto make it more user-friendly and to provide more

useful content. We will also be developing anexpanded use of e-mail that will in some waysreplace the public chat groups on the page. Wewill be sending you information about this inDecember. We hope to be able to provide moretimely and substantive information to NABLmembers in this fashion. You should be thinkingabout how much or little you would like to bereceiving from NABL via e-mail, e.g., mailings,legislative alerts, etc.

1998

I expect 1998 to be a very busy year inWashington. In an election year, members will belooking to “bring home the bacon” to prove totheir constituents that they should be reelected.The first order of business will be to restructure theIRS. This is bound to have some impact on thebond community, although most of what isimmediately being described does not affect us. Iexpect the focus to broaden some next year,especially if tax restructuring becomes a genuineissue prior to enactment of the IRS restructuringlegislation. There are signs that the White Housemay be interested in engaging in a dialogue withCongress about fundamental tax law changes. I’mnot holding my breath that any real structuralchanges can be enacted since there are so manyplayers with such differing views on the answers.However, in true Clinton fashion, it appears that

The Quarterly Newsletter 20 December 1, 1997

Try NABL's home page on the Web:www.nabl.org

the White House may be planning to co-opt bonds by private entities for infrastructure projects.another Republican agenda item. Also, the National Bankruptcy Commission has re-

More importantly for the bond community, Iexpect there to be a genuine effort to enactlegislation to increase the private activity bondvolume cap. I think we have finally reached thecritical mass required to develop the political clout The other major area of action next year willto achieve an effort of that sort. The public interest be enforcement by the IRS and SEC. We cangroups laid the ground work this year with the expect to see both agencies bringing forth actionsintroduction by Mrs. Kennelly (D-CT) and Mr. in yield burning and other areas. The SEC usuallyHoughton (R-NY) of H.R. 979 and by Mr. takes up to two years to bring a case and they areD’Amato (R-NY) and Mr. Breaux (D-LA) of approaching that timeframe. The public interestS.1251. These identical bills would immediately groups continue to press the Administration andreturn the state volume caps to the greater of $75 Treasury for relief from the tenets of Rev. Proc.per capita or $250,000,000 and provide an annual 96-41, so some response from the Treasury iscost-of-living adjustment. You can find these bills expected in 1998.through links generated in the State and GeneralLaw Section of our web page, or directly throughthe Government Printing Office’s Access web site(www.access. gpo.gov/congress). You can alsocall our office for copies.

Next year I would expect that there will be working Monday through Thursday, being flexiblesignificant effort made to enlist as many cospon- for Friday events. Laura Butera, my assistant, willsors for these bills as possible, so that when the tax be available on Fridays. She handles requests forbill is put together there will be adequate support legislation, documents, and web postings, so don’tto include the volume cap increase. The be reluctant to call. We wish you Happy HolidaysRepublicans have said that they want to pursue a and a wonderful 1998. Stay tuned for more newstax bill that will do away with the estate tax and from the Nation’s Capitol . . .marriage penalty, and restructure the IRS. Thiswill provide the vehicle for a larger expecteddebate over whether Congress should be spendingthe anticipated budget surplus or buying down thenational debt. Once the level of the surplus isestablished, the debate will be framed. Because itis an election year, unless they end up with a veryclean, minimalist bill, we can expect items likevolume cap increase to have an opportunity to beenacted.

The other issues on which we can expect to seeaction next year are electric utility restructuringand reauthorization of the Intermodal SurfaceTransportation Efficiency Act (ISTEA). Each ofthese will potentially have bond-related provisions.As mentioned above, once Congress and theAdministration determine and then coalesce behindtheir respective policies in energy restructuring, theimpact on tax-exempt finance will be clearer.ISTEA reauthorization probably will contain somedemonstration programs permitting the issuance of

leased its report to Congress and next year will beconsidering bankruptcy reform. Look at JimSpiotto’s column herein for a full description of thereport's proposals in the Chapter 9 arena.

I hope 1998 will be a happy and healthy yearfor you. Thanks to the NABL Board’s willingnessto be family friendly, I am looking forward toworking a four-day week so I can spend a littlemore time with my daughter, Emily. I will be

Amy K. Dunbar

Director of Governmental Affairs

November 14, 1997

The Quarterly Newsletter 21 December 1, 1997

COMMITTEE ON SECURITIESLAW AND DISCLOSURE FILESCOMMENTS ON PROPOSEDMSRB RULE ON SELECTION OFUNDERWRITER'S COUNSEL

Editor's Note: The following comment letter wasfiled by the Association's Committee on SecuritiesLaw and Disclosure on October 2, 1997.

Ernesto A. LanzaAssistant General CounselMunicipal Securities Rulemaking Board1150 18th Street, N.W.Suite 400Washington, D.C. 20036

Municipal Securities Rulemaking BoardRequest for Comment on Board

"Review of Underwriting Process"

Dear Mr. Lanza:

This letter is submitted on behalf of the Com-mittee on Securities Law and Disclosure of theNational Association of Bond Lawyers ("NABL")in response to the request of the MunicipalSecurities Rulemaking Board (the "MSRB" or the"Board") for comments on its "Review ofUnderwriting Process," published on May 20, 1997(the "Review").

NABL was incorporated as an Illinois non-profit corporation on February 5, 1979, for thepurposes of educating its members and others inthe law relating to state and municipal bonds andother obligations, providing a forum for theexchange of ideas as to law and practice, im-proving the state of the art in this field of law,providing advice and comment at the federal, stateand local levels with respect to existing orproposed legislation, regulations, rulings and otheractions affecting state and municipal obligations,and providing advice and comment with regard tostate and municipal obligations in proceedingsbefore courts and administrative bodies throughbriefs and memoranda as a friend of the court oragency. Currently, NABL has approximately3,000 members who actively participate in someaspect of public or private municipal financepractice. They include bond counsel, underwriter's

counsel, municipal attorneys, issuer's counsel,corporate counsel, trustee's counsel, and defensecounsel in securities and tax-related proceedings.

We share the view of the Chairman of theBoard, Roger G. Hayes, that ". . . all of us -- under-writers, issuers, counsel, and financial advisors --have a responsibility to see that the underwriting ofa new issue is efficient and above reproach." We1

applaud the Board's commitment to ". . .strengthen further the integrity of the process andprotect investors." We share the Board's concernabout the integrity of the municipal securitiesunderwriting process and therefore we are pleasedto respond to your request for comments on theReview specifically with respect to issuer selectionof underwriter's counsel and disclosure regardingsuch selection. As discussed below, we believethat there is sufficient existing guidance regardingselection of underwriter's counsel and that this isnot an appropriate matter for rulemaking.

We believe that the starting point for anydiscussion regarding selection of counsel isrecognition of the importance of participation bycompetent counsel. The American Bar Associa-tion has spoken on competency of counsel in itsModel Rules of Professional Conduct. ModelRule 1.1 provides that "[a] lawyer shall providecompetent representation to a client. Competentrepresentation requires the legal knowledge, skill,thoroughness, and preparation reasonablynecessary for the representation."2

NABL has long endorsed the need forcompetent and qualified attorneys in the variouscounsel roles in municipal securities transactions.The role of bond counsel developed over 100 yearsago as a result of investor concerns. As NABL haspreviously stated, "[t]he premise underlying [thebond counsel] arrangement was that bond counselwould . . . exercise objectivity and acquire theexpertise required to provide assurance of thevalidity of the bonds. . . . [The opinion of bondcounsel] ordinarily is required by both issuers andinvestors." NABL has stated in its Selection and3