Embed Size (px)

Citation preview

The Time Traveller Scenarios: SOUTH AFRICA’S NEXT 10 YEARS

Produced by the

SOUTH AFRICA’S GROWTH OUTLOOK Expect low growth levels driven by hostile domestic policy and a difficult global growth environment

-2

-1

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2004 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

South Africa’s GDP growth

GLOBAL GROWTH Global growth is set to average just over 3% in 2015 driven in large part by growth in developing economies

0

1

2

3

4

5

6

2012 2013 2014 2015 2016 2017

Global economic outlook World High income Developing economies

0

10

20

30

40

50

60

Share of global PP adj GDP by region Share of global GDP (PPP)

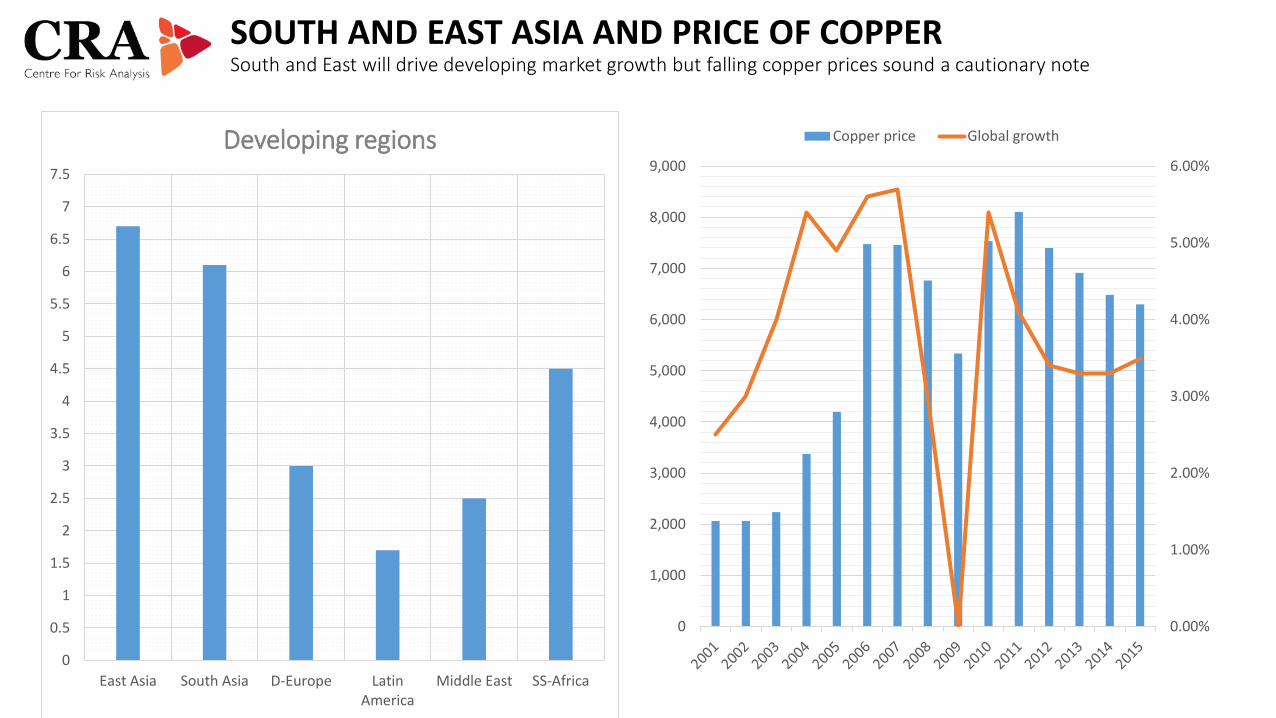

SOUTH AND EAST ASIA AND PRICE OF COPPER South and East will drive developing market growth but falling copper prices sound a cautionary note

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Copper price Global growth

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

7

7.5

East Asia South Asia D-Europe LatinAmerica

Middle East SS-Africa

Developing regions

CHINA, THE EU, AND SA’S EXPORTS World Bank forecasts anticipate China slowing with significant implications for South Africa’s exports

-2

-1

0

1

2

3

4

5

6

7

8

9

China Euro-area

Growth rates key economies

2012 2013 2014 2015

0 50 100 150 200 250

C H I N A / H K / J

E U

U S A

A F R I C A

R E S T O F T H E W O R L D

SOUTH AFRICA’S EXPORT PARTNERS (RBN)

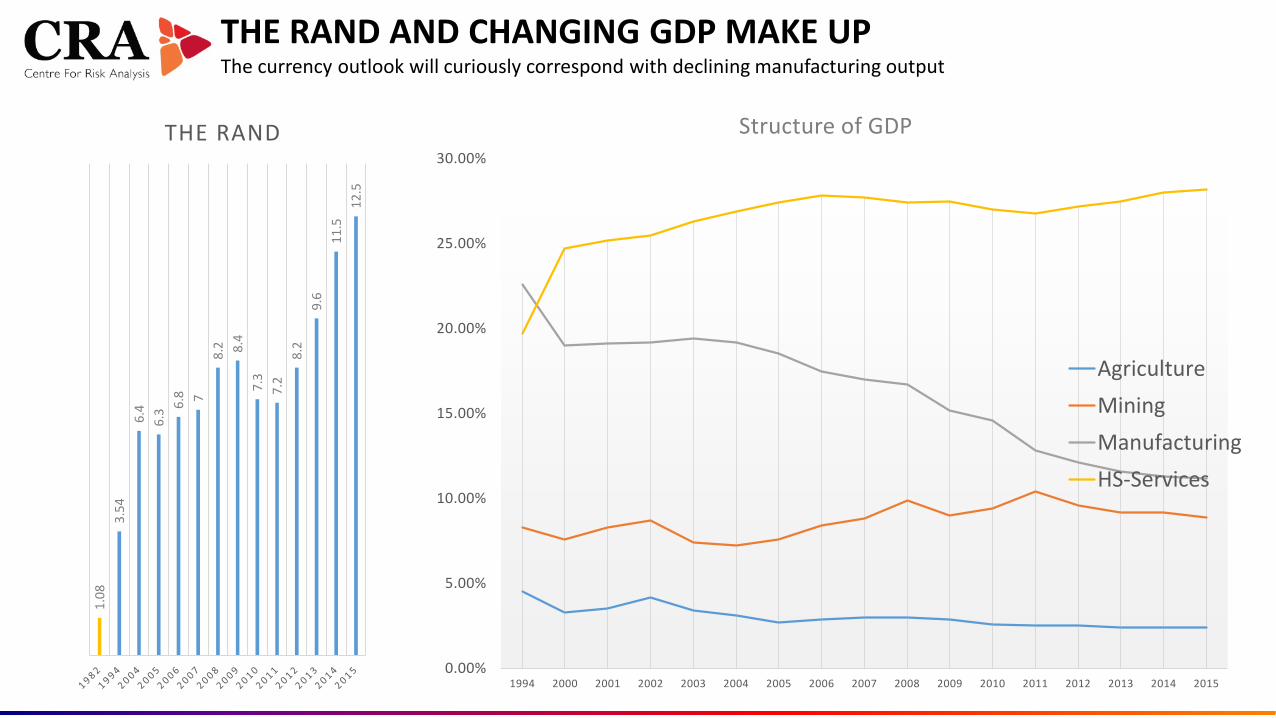

THE RAND The outlook is for further currency weakness

1.08

3.54

6.4

6.3 6.

8 7

8.2 8.4

7.3

7.2

8.2

9.6

11.5

12.5

15

20

1 9 8 2 1 9 9 4 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 2 0 2 0 2 4

THE RAND

THE RAND AND CHANGING GDP MAKE UP The currency outlook will curiously correspond with declining manufacturing output

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

1994 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Structure of GDP

AgricultureMiningManufacturingHS-Services

1.08

3.

54

6.4

6.3 6.

8 7 8.

2 8.4

7.3

7.2

8.2

9.6

11.5

12

.5

THE RAND

TAXPAYERS AND GOVERNMENT FINANCES Weak economic growth will dampen tax base expansion as government finances come under further strain

0

10

20

30

40

50

60

-6

-5.5

-5

-4.5

-4

-3.5

-3

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Budget deficit and government debt Budget deficit Debt/GDP

0

10000000

20000000

30000000

40000000

50000000

60000000

Population Adults 20+ Employed On welfare Registeredtaxpayers

Liable forreturns

Taxpayers

ELECTRICITY SUPPLY AND INFRASTRCUTURE Electricity supply constraints are placing growth estimates of over 3% of GDP in doubt

0

10000

20000

30000

40000

50000

60000 19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

20

18

2019

20

20

2021

20

22

2023

20

24

Available capacity Installed capacity (MW) Demand at 1% growth Demand at 3% growth

and… any significant

further breakdown in existing power

infrastructure will force growth

forecasts to be revised

downwards

LABOUR MARKETS We anticipate sustained high levels of joblessness centred around young people

0 10 20 30 40 50 60

15-24

25-34

35-44

45-54

55-64

Official unemployment rate by age group

0

10000000

20000000

30000000

40000000

50000000

60000000

Population Of workingage

Employed Unemployed Not lookingfor work

Jobs and unemployment 2001 2014

0.7

1.8

GLOBAL YOUTH GLOBAL UNEMPLOYED

YOUTH

Global picture

9

8

3

1

4

JOBS AND GROWTH We expect GDP growth to remain key determinant of broader joblessness rate

-2

-1

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Growth and unemployment

Unemployment rate GDP growth

INCOMES, ASSETS, AND THE MIDDLE CLASS The risk is that middle class size is overstated with 12% spending over R10 000 a month

African, 12040000

White, 1380000 African, 665000 White, 859000

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

African Coloured Indian White

Household monthly expenditure

Total R0-R2499 R2500-R9999 R10000+

African, 479000 Coloured, 176000

Indian, 67000 White, 419000

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

African Coloured Indian White

Households and home loans

Homeloans Households

African R10 000

= 5.5%

SCHOOLS AND EDUCATION Despite half of children now completing their school education quality remains very poor

0

10

20

30

40

50

60

70

Grade 1 Grade 2 Grade 3 Grade 4 Grade 5 Grade 6 Grade 9 Matricmathspass at

50%

Numeracy rates and matric maths

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1955 1965 1975 1985 1995 2005 2015 Numberin 2015cohort

Black African matric passes

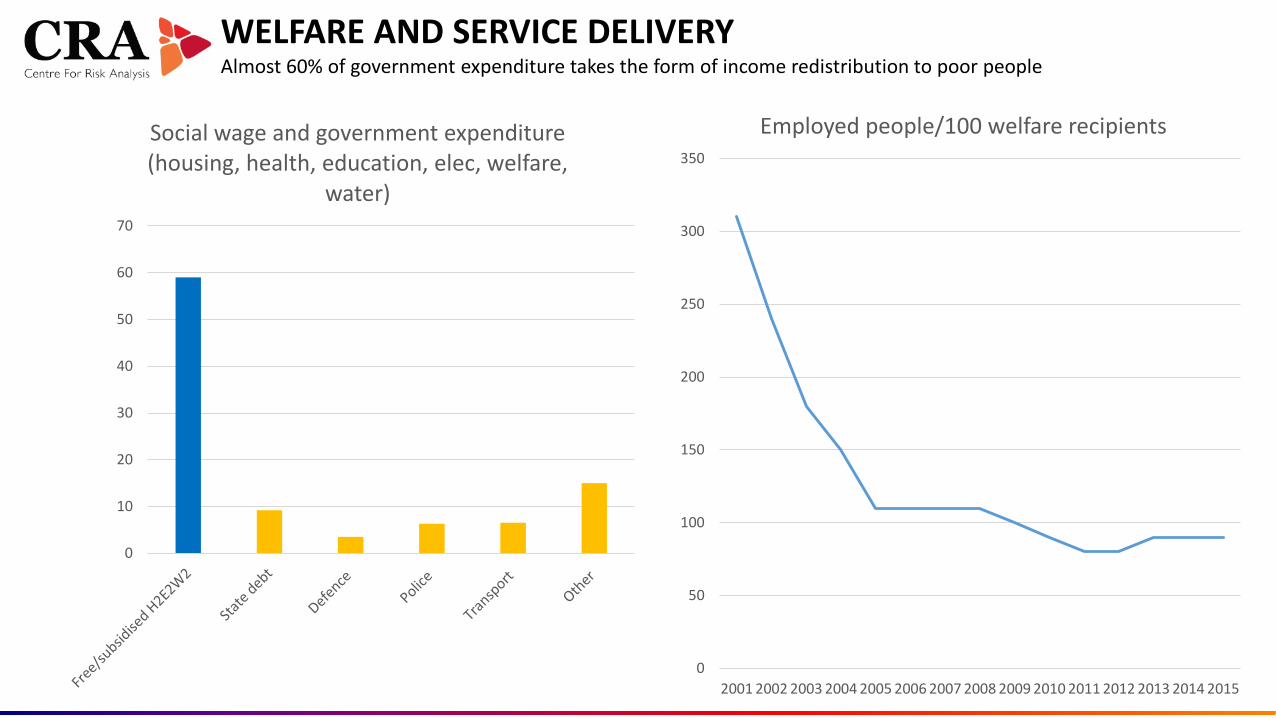

WELFARE AND SERVICE DELIVERY Almost 60% of government expenditure takes the form of income redistribution to poor people

0

50

100

150

200

250

300

350

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Employed people/100 welfare recipients

0

10

20

30

40

50

60

70

Social wage and government expenditure (housing, health, education, elec, welfare,

water)

CRIME AND SECURITY Expectation is that high violent crime levels will continue to overwhelm the justice system

250000

260000

270000

280000

290000

300000

310000

320000

330000

340000

0

5000

10000

15000

20000

25000

30000

35000

40000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Robbers and convicts Armed residential/business robbery All criminal convictions

0

10

20

30

40

50

60

70

80

Murder rate

POLLS AND SOCIAL ATTITUDES Anti-government sentiment is rising

Government performs well?

72% YES

2000

54% 2014

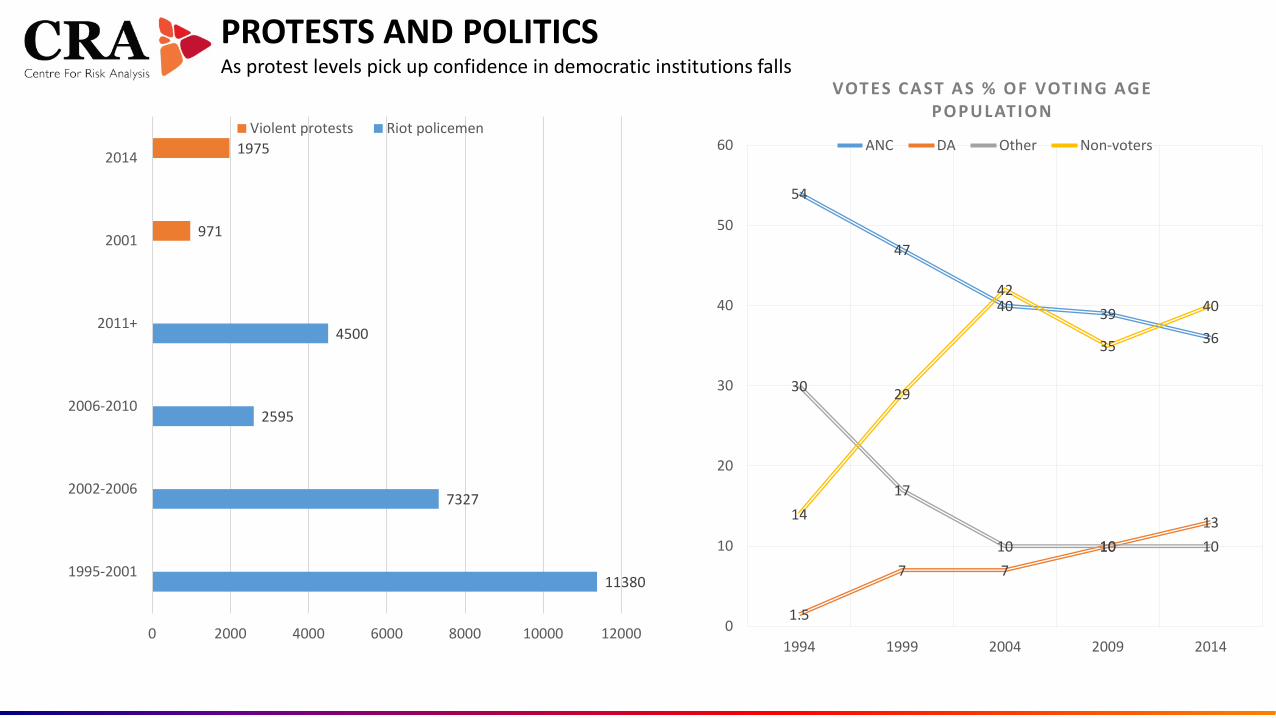

PROTESTS AND POLITICS As protest levels pick up confidence in democratic institutions falls

11380

7327

2595

4500

971

1975

0 2000 4000 6000 8000 10000 12000

1995-2001

2002-2006

2006-2010

2011+

2001

2014

Violent protests Riot policemen

54

47

40 39 36

1.5

7 7 10

13

30

17

10 10 10

14

29

42

35

40

0

10

20

30

40

50

60

1994 1999 2004 2009 2014

VOTES CAST AS % OF VOTING AG E POPULATION

ANC DA Other Non-voters

SCENARIOS AND PROBABILITIES: 2024 On current trends a Toll Road/Rocky Road hybrid is the scenario of greatest probability

NARROW ROAD forced market

friendly reforms

TOLL ROAD policy confusion amidst vibrant

institutions

ROCKY ROAD socialism amidst

crumbling democratic institutions

WIDE ROAD popular mandate for

market reforms

Market driven economic reform

Erosion of democratic institutions

Free open society under rule of law

Socialist “development state”

LEADING INDICATORS OF CHANGE The following leading indicators will cause us to consider upping to ‘most probable’ of any of the other three scenarios Economic upsurge of South Africa’s major export partners coinciding with sustained

long term uptick in global commodity demand Increases in foreign interest rates coinciding with high levels of sustained capital outflows

out of South Africa Evidence of reckless short term borrowing on the part of the South African government A period of sharp rand weakening – especially in an environment of rising oil prices Fundamental reforms on labour and then empowerment policy by the South African

government Evidence of the likely significant loss of autonomy of key democratic institutions including

the media, civil society, the judiciary and quasi-state democratic institutions such as the Public Protector and the Independent Electoral Commission

Likely successful attempts to vest property rights in the State Evidence of large scale institutional instability within the African National Congress Sustained sharp increases in violent anti-government protest actions

Frans Cronje: [email protected] Media desk: [email protected] Web: www.irr.org.za