Embed Size (px)

Citation preview

CIRCULAR DATED 23 FEBRUARY 2008

THIS CIRCULAR IS ISSUED BY THE STRAITS TRADING COMPANY LIMITED. THIS CIRCULAR ISIMPORTANT AS IT CONTAINS THE RECOMMENDATIONS OF THE INDEPENDENT DIRECTORS OFTHE STRAITS TRADING COMPANY LIMITED AND THE ADVICE OF CIMB-GK SECURITIES PTE.LTD. IN RELATION TO THE FINAL TCPL OFFER (AS DEFINED HEREIN) AND THE REVISED KTIPLOFFER (AS DEFINED HEREIN). THIS CIRCULAR REQUIRES YOUR IMMEDIATE ATTENTION ANDYOU SHOULD READ IT CAREFULLY.

If you are in any doubt in relation to this Circular or as to the action you should take, you should consultyour stockbroker, bank manager, solicitor, accountant or other professional adviser immediately.

If you have sold or transferred all your issued ordinary shares in the capital of The Straits TradingCompany Limited, you should immediately forward this Circular to the purchaser or to the bank,stockbroker or agent through whom you effected the sale for onward transmission to the purchaser.

The Singapore Exchange Securities Trading Limited assumes no responsibility for the correctness of anyof the statements made, reports contained or opinions expressed in this Circular.

THE STRAITS TRADING COMPANY LIMITED(Incorporated in Singapore)

(Company Registration Number: 188700008D)

CIRCULAR TO SHAREHOLDERS

in relation to

THE FINAL TCPL OFFER AND THE REVISED KTIPL OFFER

Independent Financial Adviser to the Independent Directors of The Straits Trading Company Limited

CIMB-GK SECURITIES PTE. LTD.(Incorporated in the Republic of Singapore)

(Company Registration Number: 198701621D)

SHAREHOLDERS SHOULD NOTE THAT THE SECOND PRICE REVISION ANNOUNCEMENT ON THETCPL OFFER STATES THAT ACCEPTANCES SHOULD BE RECEIVED BY THE CLOSE OF THEFINAL TCPL OFFER AT 5.30 P.M. ON 6 MARCH 2008 AND THAT TCPL DOES NOT INTEND TOEXTEND THE FINAL TCPL OFFER BEYOND 5.30 P.M. ON 6 MARCH 2008 EXCEPT WHERE THEFINAL TCPL OFFER BECOMES UNCONDITIONAL AS TO ACCEPTANCES OR WHERE TCPLINCURS A MANDATORY OFFER OBLIGATION UNDER RULE 14 OF THE CODE DURING THEOFFER PERIOD THROUGH THE ACQUISITION OF SHARES (OTHER THAN PURSUANT TOACCEPTANCES OF THE FINAL TCPL OFFER).

SHAREHOLDERS WHO WISH TO ACCEPT THE FINAL TCPL OFFER MUST DO SO BY 5.30 P.M. ON6 MARCH 2008.

SHAREHOLDERS SHOULD NOTE THAT THE KTIPL OFFER DOCUMENT STATES THATACCEPTANCES SHOULD BE RECEIVED BY THE CLOSE OF THE REVISED KTIPL OFFER AT 5.30P.M. ON 13 MARCH 2008, OR SUCH LATER DATE(S) AS MAY BE ANNOUNCED FROM TIME TOTIME BY OR ON BEHALF OF KTIPL.

SHAREHOLDERS WHO WISH TO ACCEPT THE REVISED KTIPL OFFER MUST DO SO BY 5.30 P.M.ON 13 MARCH 2008, OR SUCH LATER DATE(S) AS MAY BE ANNOUNCED FROM TIME TO TIME BYOR ON BEHALF OF KTIPL.

DEFINITIONS .................................................................................................................................... 1

LETTER TO SHAREHOLDERS

1. INTRODUCTION ...................................................................................................................... 7

2. THE FINAL TCPL OFFER ...................................................................................................... 7

3. THE REVISED KTIPL OFFER ................................................................................................ 8

4. RATIONALE FOR THE KTIPL OFFER AND KTIPL’S FUTURE PLANS FOR THE COMPANY .............................................................................................................................. 10

5. LISTING STATUS AND COMPULSORY ACQUISITION ........................................................ 10

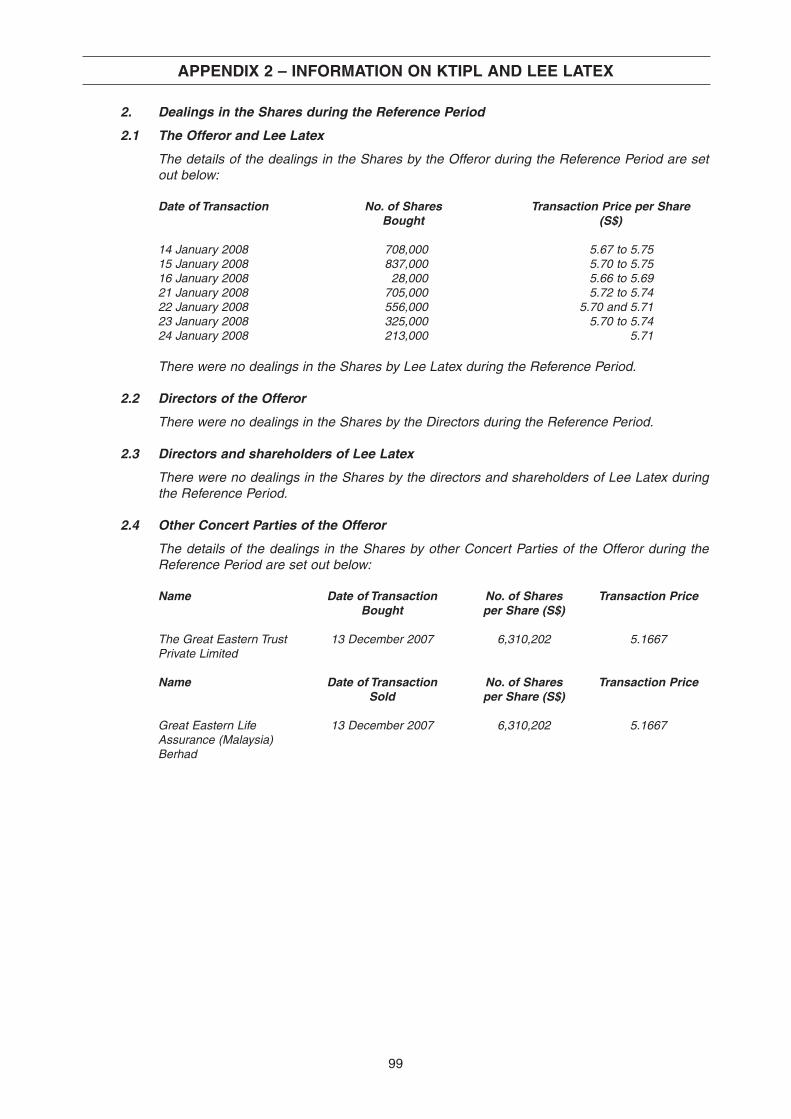

6. INFORMATION ON KTIPL AND LEE LATEX ........................................................................ 11

7. IRREVOCABLE UNDERTAKINGS.......................................................................................... 11

8. ADVICE OF THE IFA .............................................................................................................. 12

9. INDEPENDENT DIRECTORS’ RECOMMENDATIONS .......................................................... 15

10. OVERSEAS SHAREHOLDERS .............................................................................................. 15

11. CPFIS INVESTORS ................................................................................................................ 16

12. ACTION TO BE TAKEN BY SHAREHOLDERS ...................................................................... 16

13. RESPONSIBILITY STATEMENT ............................................................................................ 17

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED ........................................................................................................ 18

APPENDIX 1 - GENERAL INFORMATION .................................................................................. 74

APPENDIX 2 - INFORMATION ON KTIPL AND LEE LATEX ...................................................... 83

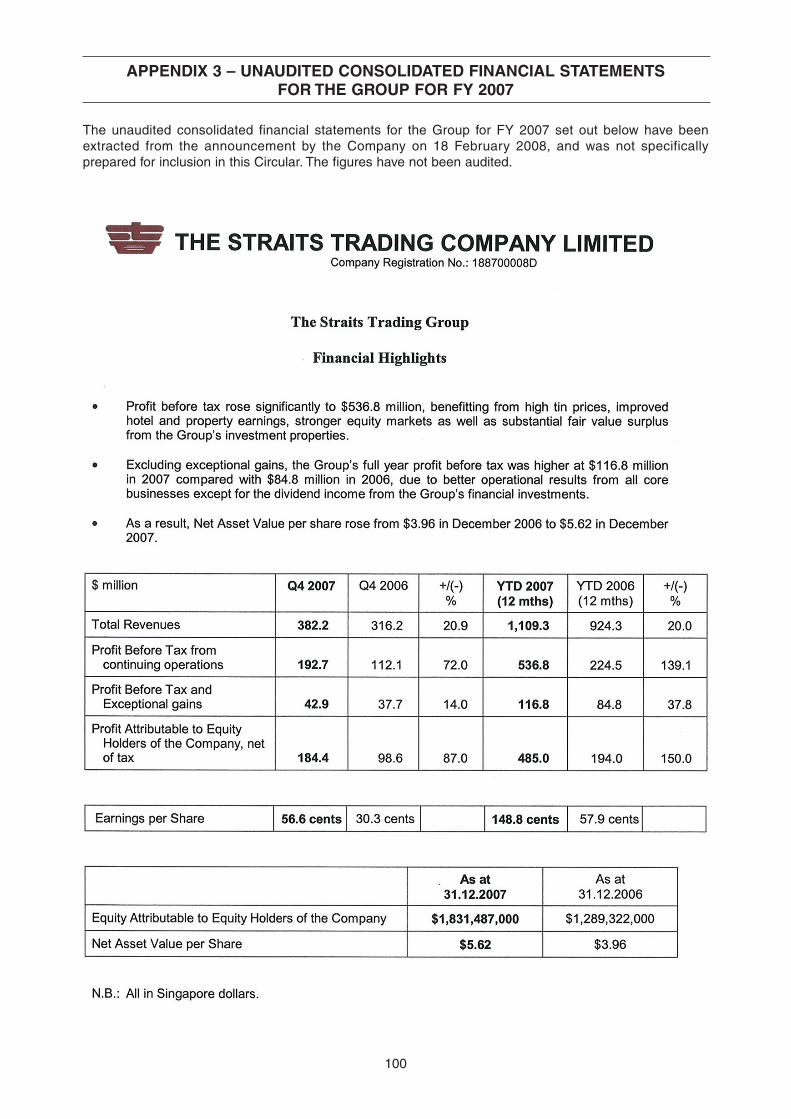

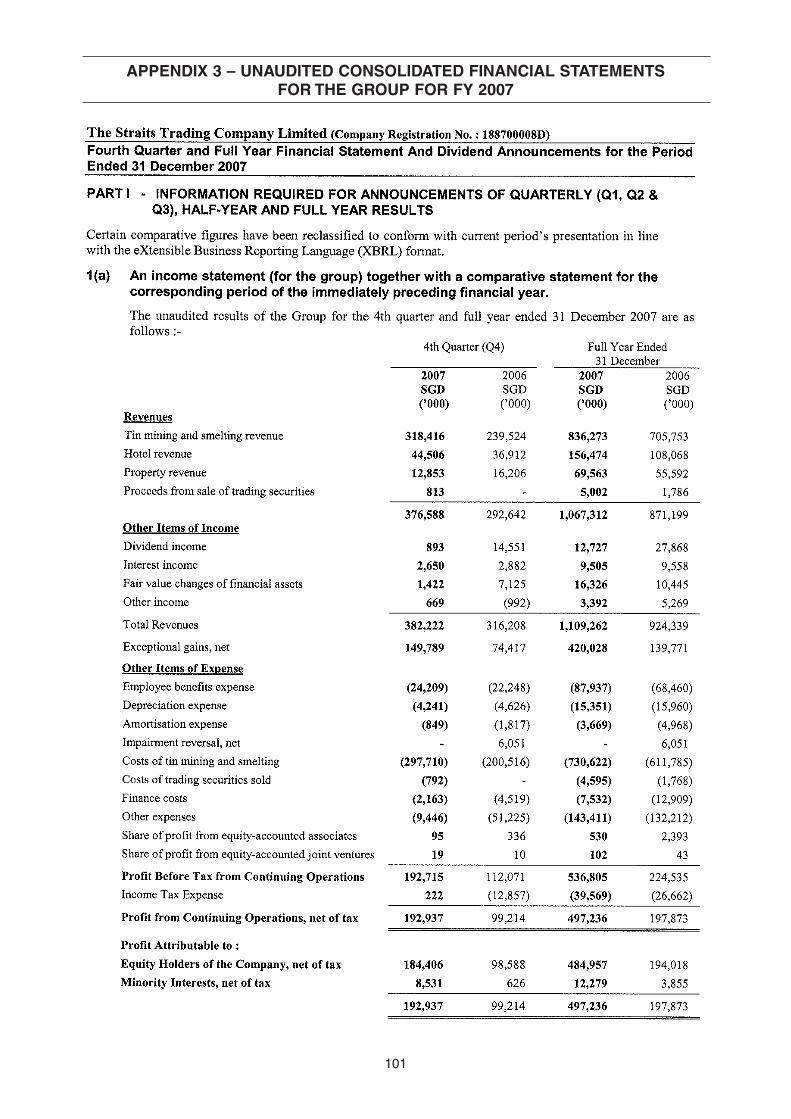

APPENDIX 3 - UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR THE GROUP FOR FY 2007 ........................................................................................................ 100

CONTENTS

1

Except where the context otherwise requires, the following definitions apply throughout this Circular:

“Act” : Companies Act, Chapter 50 of Singapore

“Annual Report” : The annual report of the Company

“Auditors” or “Ernst & Young” : Ernst & Young, the auditors of the Company

“CDP” : The Central Depository (Pte) Limited

“CPF” : Central Provident Fund

“CPF Agent Banks” : Agent banks included under CPFIS

“CPFIS” : Central Provident Fund Investment Scheme

“CPFIS Investors” : Investors who have purchased Shares using their monies pursuantto the CPFIS

“Circular” : This circular to Shareholders dated 23 February 2008 from theCompany containing the recommendations of the IndependentDirectors and the advice of the IFA to the Independent Directors inrelation to the Final TCPL Offer and the Revised KTIPL Offer

“Code” : The Singapore Code on Take-overs and Mergers

“Company” or “STC” : The Straits Trading Company Limited

“Concert Parties” : Parties acting or presumed to be acting in concert with KTIPL inconnection with the KTIPL Offer

“Concert Party Group” : (i) The directors of KTIPL;

(ii) Lee Latex and its directors and shareholders; and

(iii) certain presumed concert parties of KTIPL, namely,

(a) Selat (Pte) Limited, Island Investment Company(Private) Limited, Lee Plantations (Pte) Ltd, LeeFoundation, Lee Rubber Company (Pte) Limited andSingapore Investments (Pte) Limited (beingcompanies within the Lee Family Companies);

(b) OCBC Bank and its wholly-owned subsidiaries; and

(c) GEH and its wholly-owned subsidiaries

“Condition” : Shall have the meaning ascribed to it in paragraph 3.4 of theCompany’s Letter to Shareholders in this Circular

“Credit Suisse” : Credit Suisse (Singapore) Limited

“Directors” : The directors of the Company as at the Latest Practicable Date

“DTZ” : DTZ Debenham Tie Leung (SEA) Pte Ltd

DEFINITIONS

2

“FAs” : Credit Suisse and OCBC Bank, the financial advisers to KTIPL

“Final TCPL Offer” : The final voluntary conditional cash offer by SCB, for and on behalfof TCPL, to acquire all the TCPL Offer Shares on the terms andsubject to the conditions set out in the Final TCPL Offer Letter, theTCPL Offer Document, the TCPL FAA and the TCPL FAT

“Final TCPL Offer Letter” : The letter from TCPL dated 18 February 2008 issued by SCB, forand on behalf of TCPL, to Shareholders, setting out, inter alia, therevisions to the Revised TCPL Offer

“Final TCPL Offer Price” : Shall have the meaning ascribed to it in paragraph 2.1 of theCompany’s Letter to Shareholders in this Circular

“FY” : Financial year ended or ending 31 December

“GEH” : Great Eastern Holdings Limited

“GEH Group” : GEH and its subsidiaries

“Group” or “STC Group” : The Company and its subsidiaries

“IFA” or “CIMB-GK” : CIMB-GK Securities Pte. Ltd., the independent financial adviser tothe Independent Directors

“Independent Directors” : The directors of the Company who consider themselves to beindependent for the purpose of making recommendations toShareholders in respect of the TCPL Offer and the KTIPL Offer,namely, Mr Tang I-Fang, Professor Lim Chong Yah, Mr MichaelHwang, Mr Norman Ip Ka Cheung, Mr Razman Ariffin and MrGerard Ee Hock Kim

“JLL” : Jones Lang LaSalle Hotels

“KTIPL” : Knowledge Two Investment Pte Ltd, a wholly-owned subsidiary ofLee Latex

“KTIPL FAA” : Form of Acceptance and Authorisation for the KTIPL Offer

“KTIPL FAT” : Form of Acceptance and Transfer for the KTIPL Offer

“KTIPL Offer” : The mandatory conditional cash offer by the FAs, for and on behalfof KTIPL, for all the KTIPL Offer Shares on the terms and subjectto the conditions set out in the KTIPL Offer Document, the KTIPLFAA and the KTIPL FAT

“KTIPL Offer Announcement” : Announcement of KTIPL’s intention to make the KTIPL Offer whichwas released on the KTIPL Offer Announcement Date

“KTIPL Offer Announcement : 24 January 2008, being the date on which the KTIPL OfferDate” Announcement was made

“KTIPL Offer Closing Date” : 5.30 p.m. (Singapore time) on 13 March 2008 or such later date(s)as may be announced from time to time by or on behalf of KTIPL,being the last day and time for the lodgement of acceptances forthe Revised KTIPL Offer

DEFINITIONS

3

“KTIPL Offer Document” : The document dated 12 February 2008 issued by the FAs, for andon behalf of KTIPL, in respect of the KTIPL Offer

“KTIPL Offer Price” : S$5.76 in cash for each KTIPL Offer Share

“KTIPL Offer Shares” : All the issued Shares other than those already owned or agreed tobe acquired by KTIPL and the Lee Family Companies

“Latest Practicable Date” : 20 February 2008, being the latest practicable date prior to theprinting of this Circular

“Lee Family” : Messrs Lee Seng Gee, Lee Seng Tee and Lee Seng Wee and theirimmediate family members

“Lee Family Companies” : The intermediate companies through which the Lee Family directlyor indirectly has interests in Lee Latex

“Lee Latex” : Lee Latex (Pte) Limited

“Listing Manual” : The SGX-ST Listing Manual

“Market Day” : A day on which the SGX-ST is open for the trading of securities

“MSC” : Malaysia Smelting Corporation Berhad, a subsidiary of theCompany

“MYR” : Malaysian Ringgit, being the lawful currency of Malaysia

“OCBC Bank” : Oversea-Chinese Banking Corporation Limited, a substantialshareholder of the Company

“OCBC Bank Malaysia” : OCBC Bank (Malaysia) Berhad, a subsidiary of OCBC Bank

“OCBC Group” : OCBC Bank and its subsidiaries

“Offers to OCBC Bank and : Shall have the meaning ascribed to it in paragraph 2.4 of theGEH Announcement” Company’s Letter to Shareholders in this Circular

“Overseas Shareholder” : Shall have the meaning ascribed to it in paragraph 10.1 of theCompany’s Letter to Shareholders in this Circular

“Properties” : The properties of the Group which are the subject of the ValuationReports, as set out in Appendix 8 to the TCPL Offeree Circular

“Relevant Directors” : Shall have the meaning ascribed to it in paragraph 9.1 of theCompany’s Letter to Shareholders in this Circular

“Revised KTIPL Offer” : The revised mandatory conditional cash offer by the FAs, for andon behalf of KTIPL, to acquire all the KTIPL Offer Shares on theterms and subject to the conditions set out in the Revised KTIPLOffer Letter, the KTIPL Offer Document, the KTIPL FAA and theKTIPL FAT

DEFINITIONS

4

“Revised KTIPL Offer : Announcement of KTIPL’s intention to revise the KTIPL Offer whichAnnouncement” was released on 14 February 2008, setting out, inter alia, the

revisions to the KTIPL Offer as set out in the KTIPL OfferDocument

“Revised KTIPL Offer Letter” : The letter from KTIPL which will be despatched to Shareholderssetting out, inter alia, the revisions to the KTIPL Offer as set out inthe KTIPL Offer Document

“Revised KTIPL Offer Price” : Shall have the meaning ascribed to it in paragraph 1.4 of theCompany’s Letter to Shareholders in this Circular

“Revised TCPL Offer” : The revised voluntary conditional cash offer by SCB, for and onbehalf of TCPL, to acquire all the TCPL Offer Shares on the termsand subject to the conditions set out in the Revised TCPL OfferLetter, the TCPL Offer Document, the TCPL FAA and the TCPLFAT

“Revised TCPL Offer Letter” : The letter from TCPL dated 2 February 2008 issued by SCB, forand on behalf of TCPL, to Shareholders, setting out, inter alia, therevisions to the TCPL Offer

“Revised TCPL Offer Price” : S$6.50 in cash for each TCPL Offer Share

“SCB” : Standard Chartered Bank, the financial adviser to TCPL

“Second Price Revision : Announcement of TCPL’s intention to revise the Revised TCPL Announcement on the Offer Price which was released on 18 February 2008, setting out, TCPL Offer” inter alia, the Final TCPL Offer Price and TCPL Offer Closing Date

“SGX-ST” : Singapore Exchange Securities Trading Limited

“Shareholders” : Persons who are registered as holders of Shares in the Register ofMembers of the Company and Depositors who have Sharesentered against their names in the Depository Register

“Shares” : Issued ordinary shares in the capital of the Company

“SIC” : The Securities Industry Council of Singapore

“STASB” or “STAR(M)” : Straits Trading Amalgamated Resources Sendirian Berhad, awholly-owned subsidiary of the Company

“STC Distribution” : Shall have the meaning ascribed to it in paragraph 3.3 of theCompany’s Letter to Shareholders in this Circular

“TCPL” : The Cairns Pte. Ltd.

“TCPL FAA” : Form of Acceptance and Authorisation for the TCPL Offer.

“TCPL FAT” : Form of Acceptance and Transfer for the TCPL Offer.

“TCPL Offer” : The voluntary conditional cash offer by SCB, for and on behalf ofTCPL, to acquire all the TCPL Offer Shares on the terms andsubject to the conditions set out in the TCPL Offer Document, theTCPL FAA and the TCPL FAT

DEFINITIONS

5

“TCPL Offer Closing Date” : Shall have the meaning ascribed to it in paragraph 2.2 of theCompany’s Letter to Shareholders in this Circular

“TCPL Offeree Circular” : The circular to Shareholders dated 3 February 2008 from theCompany containing the recommendations of the IndependentDirectors and the advice of the IFA to the Independent Directors inrelation to the Revised TCPL Offer

“TCPL Offer Document” : The document dated 23 January 2008 issued by SCB, for and onbehalf of TCPL, in respect of the TCPL Offer

“TCPL Offer Price” : S$5.70 in cash for each TCPL Offer Share

“TCPL Offer Shares” : All the Shares in issue that are not already owned, controlled, oragreed to be acquired by TCPL

“S$” or “$” and “cents” : Singapore dollars and cents respectively, being the lawful currencyof Singapore

“Valuation Reports” : The valuation reports dated 28 January 2008, 29 January 2008and 1 February 2008 and the valuation certificates of theProperties from the Valuers setting out, inter alia, their valuation ofthe Properties which were reproduced in Appendix 8 to the TCPLOfferee Circular

“Valuers” : DTZ, JLL and WTW, the valuers appointed by the Company, inconnection with the TCPL Offer and the KTIPL Offer, to value theProperties and to issue the Valuation Reports on these Properties

“WTW” : CH Williams Talhar & Wong Sdn Bhd

“%” or “per cent.” : Per centum or percentage

Unless otherwise defined, the term “acting in concert” shall have the meaning ascribed to it in the Code.

The terms “Depositor”, “Depository Register” and “substantial shareholder” shall have the meaningsascribed to them respectively in the Act.

The headings in this Circular are inserted for convenience only and shall be ignored in construing thisCircular.

Any discrepancies in the tables in this Circular between the listed amounts and the totals thereof are dueto rounding.

Words importing the singular shall, where applicable, include the plural and vice versa. Words importingthe masculine gender shall, where applicable, include the feminine and neuter genders and vice versa.References to persons shall, where applicable, include corporations.

Any reference in this Circular to any enactment is a reference to that enactment as for the time beingamended or re-enacted. Any word defined under the Act, the Code, the Listing Manual or any statutorymodification thereof and not otherwise defined in this Circular shall, where applicable, have the samemeaning assigned to it under the Act, the Code, the Listing Manual or any statutory modification thereof,as the case may be, unless the context otherwise requires.

Any reference to a time of day and date in this Circular is made by reference to Singapore time and daterespectively unless otherwise stated.

DEFINITIONS

All statements other than statements of historical facts included in this Circular are or may be forward-looking statements. Forward-looking statements include but are not limited to those using words such as“expect”, “anticipate”, “believe”, “intend”, “project”, “plan”, “strategy”, “forecast” and similar expressions orfuture or conditional verbs such as “will”, “would”, “should”, “could”, “may” and “might”. These statementsreflect the Company’s current expectations, beliefs, hopes, intentions or strategies regarding the futureand assumptions in light of currently available information. Such forward-looking statements are notguarantees of future performance or events and involve known and unknown risks and uncertainties.Accordingly, actual results may differ materially from those described in such forward-looking statements.Shareholders and investors should not place undue reliance on such forward-looking statements, andneither the Company nor CIMB-GK undertakes any obligation to update publicly or revise any forward-looking statements, subject to compliance with all applicable laws and regulations and/or rules of theSGX-ST and/or any other regulatory or supervisory body or agency.

6

DEFINITIONS

7

THE STRAITS TRADING COMPANY LIMITED(Incorporated in Singapore)

(Company Registration Number: 188700008D)

Directors Registered Address

Mr Bobby Chin Yoke Choong (Chairman) 18 Cross Street #15-01Mr Tang I-Fang Singapore 048423Mr Michael Wong Pakshong Professor Lim Chong Yah Mr Michael Hwang Tan Sri Dato’ Dr Lin See-Yan Mr Norman Ip Ka Cheung (President & Chief Executive Officer)Mr Razman Ariffin Mr Gerard Ee Hock Kim

23 February 2008

To: The Shareholders of The Straits Trading Company Limited

Dear Sir/Madam

THE FINAL TCPL OFFER AND THE REVISED KTIPL OFFER

1. INTRODUCTION

1.1 TCPL Offer. On 6 January 2008, SCB announced, for and on behalf of TCPL, that TCPL intends tomake the TCPL Offer at the TCPL Offer Price.

1.2 KTIPL Offer. On 24 January 2008, OCBC Bank announced, for and on behalf of KTIPL, that KTIPLintends to make the KTIPL Offer at the KTIPL Offer Price.

1.3 Revised TCPL Offer. On 28 January 2008, SCB announced, for and on behalf of TCPL, that TCPLwas revising its offer price from the TCPL Offer Price to the Revised TCPL Offer Price.

1.4 Revised KTIPL Offer. On 14 February 2008, the FAs announced, for and on behalf of KTIPL, thatKTIPL is revising its offer price from the KTIPL Offer Price to S$6.55 in cash for each KTIPL OfferShare (the “Revised KTIPL Offer Price”). Details of the Revised KTIPL Offer are set out inparagraph 3 below.

1.5 KTIPL Offer Document and Revised KTIPL Offer Letter. Shareholders should by now havereceived a copy of the KTIPL Offer Document issued by the FAs, for and on behalf of KTIPL,setting out, inter alia, the terms and conditions of the KTIPL Offer. The principal terms andconditions of the KTIPL Offer are set out on pages 8 to 11 of the KTIPL Offer Document.Shareholders are advised to read the terms and conditions contained therein carefully.

The Revised KTIPL Offer Announcement states that the Revised KTIPL Offer Letter will bedespatched to Shareholders as soon as practicable.

2 THE FINAL TCPL OFFER.

2.1 Final TCPL Offer Price. On 18 February 2008, SCB announced, for and on behalf of TCPL, thatTCPL is revising its offer price again from the Revised TCPL Offer Price to S$6.70 in cash for eachTCPL Offer Share (the “Final TCPL Offer Price”). Save as disclosed in the Second Price RevisionAnnouncement on the TCPL Offer, all the other terms and conditions of the TCPL Offer as set outin the TCPL Offer Document remain unchanged.

LETTER TO SHAREHOLDERS

8

2.2 TCPL Offer Closing Date. As announced in the Second Price Revision Announcement on theTCPL Offer, TCPL does not intend to further revise the Final TCPL Offer Price and the Final TCPLOffer will remain open for acceptances until 5.30 p.m. (Singapore time) on 6 March 2008 (the“TCPL Offer Closing Date”).

The Second Price Revision Announcement on the TCPL Offer also states that TCPL does notintend to extend the Final TCPL Offer beyond 5.30 p.m. (Singapore time) on the TCPL OfferClosing Date except where the Final TCPL Offer becomes unconditional as to acceptances orwhere TCPL incurs a mandatory offer obligation under Rule 14 of the Code during the offer periodthrough the acquisition of Shares (other than pursuant to acceptances of the Final TCPL Offer).

2.3 Final TCPL Offer Letter. Shareholders should by now have received a copy of the Final TCPLOffer Letter issued by SCB, for and on behalf of TCPL, setting out, inter alia, the revisions to theRevised TCPL Offer.

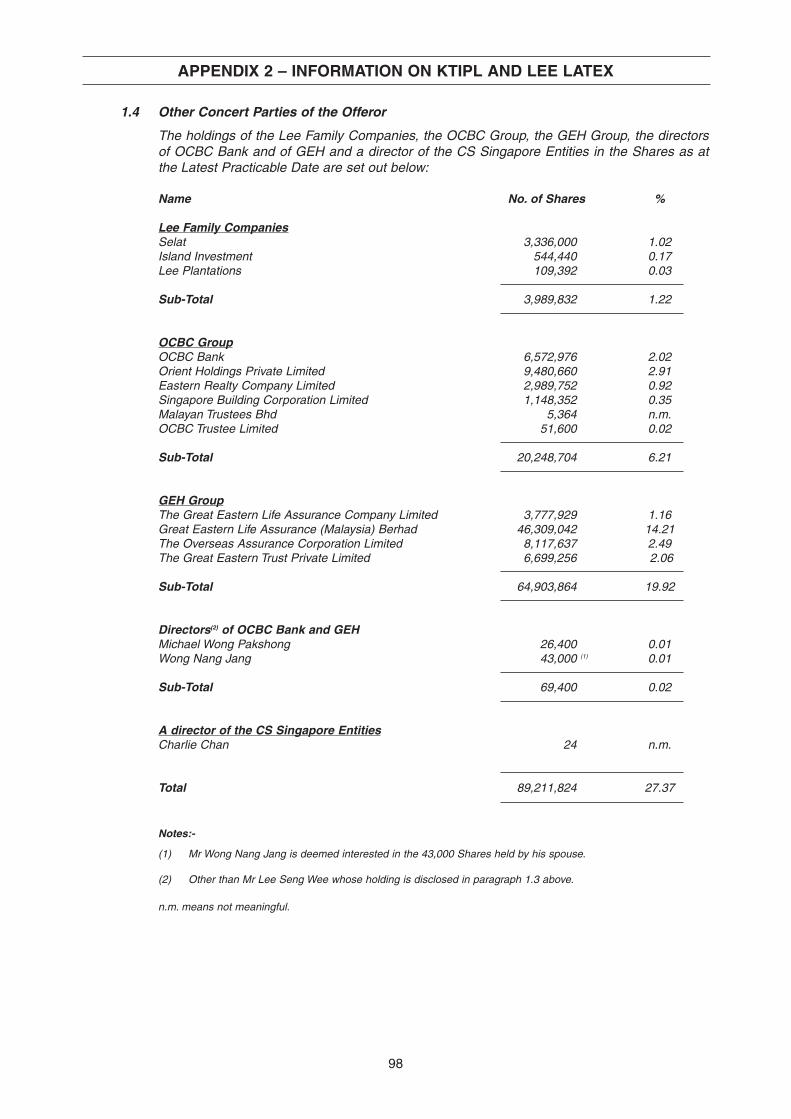

2.4 Offers to OCBC Bank and GEH. On 18 February 2008, SCB also announced that it had alsoissued, for and on behalf of TCPL, a letter of offer to each of OCBC Bank and GEH to purchase, atthe Final TCPL Offer Price, all the 20,248,704 Shares held by the OCBC Group (excluding theGEH Group) representing approximately 6.21 per cent. of all the issued Shares, and all the64,903,864 Shares held by the GEH Group, including the Shares held by the participating funds ofGreat Eastern Life Assurance Company Limited and Great Eastern Life Assurance (Malaysia)Berhad, representing approximately 19.92 per cent. of all the issued Shares (the “Offers to OCBCBank and GEH Announcement”)1.

The offers to OCBC Bank and GEH are unconditional and will expire at 5.00 p.m. (Singapore time)on 6 March 2008 if they are not accepted by OCBC Bank and/or GEH. The same announcementalso states that should OCBC Bank and GEH accept the offers, TCPL and parties acting in concertwith it shall then own, control or have agreed to acquire not less than 162,205,896 Shares,representing 49.77 per cent. of all the issued Shares. TCPL shall then convert the TCPL Offer intoa mandatory offer for the TCPL Offer Shares in accordance with the provisions of the Code.

2.5 Circular. The purpose of this Circular is to provide Shareholders with relevant informationpertaining to the Group and to set out the recommendations of the Independent Directors and theadvice of the IFA to the Independent Directors with regard to the Final TCPL Offer and the RevisedKTIPL Offer.

3. THE REVISED KTIPL OFFER

3.1 Consideration. As set out in the Revised KTIPL Offer Announcement, KTIPL will make theRevised KTIPL Offer on the following basis:

For each KTIPL Offer Share : S$6.55 in cash

Shareholders should note that the Final TCPL Offer Price of S$6.70 in cash for each TCPLOffer Share is S$0.15 higher than the Revised KTIPL Offer Price of S$6.55 in cash for eachKTIPL Offer Share.

3.2 Other Terms. According to the Revised KTIPL Offer Announcement, save for the revision of theKTIPL Offer Price as disclosed in the Revised KTIPL Offer Announcement, all the other terms andconditions of the KTIPL Offer as set out in the KTIPL Offer Document remain unchanged.

LETTER TO SHAREHOLDERS

1 The figures set out in paragraph 2.4 of the Company’s Letter to Shareholders in this Circular are based on the information setout in the Offers to OCBC Bank and GEH Announcement.

9

3.3 No Encumbrances. The KTIPL Offer Shares are to be acquired fully paid and free from all claims,charges, equities, liens, pledges and other encumbrances and together with all rights, benefits,entitlements and advantages attached thereto as at the KTIPL Offer Announcement Date andthereafter attaching thereto, including the right to all dividends, rights and other distributions (if any)declared, made or paid thereon on or after the KTIPL Offer Announcement Date (including anydividends that may be declared, made or paid thereon in respect of FY 2007).

Without prejudice to the generality of the foregoing, the Revised KTIPL Offer Price has beendetermined on the basis that the KTIPL Offer Shares will be acquired with the right to receive anydividends, other distributions or return of capital that may be declared, made or paid by STC on theKTIPL Offer Shares on or after the KTIPL Offer Announcement Date (the “STC Distribution”).

In the event any STC Distribution has been paid by STC to a Shareholder who accepts orhas accepted the Revised KTIPL Offer, the Revised KTIPL Offer Price payable to suchaccepting Shareholder shall be reduced by the amount which is equal to the STCDistribution paid by STC to such accepting Shareholder.

Accordingly, if any STC Distribution is declared, made or paid by STC on or after the KTIPL OfferAnnouncement Date and the settlement date in respect of the KTIPL Offer Shares acceptedpursuant to the Revised KTIPL Offer falls after the books closure date for the determination ofentitlements to the STC Distribution, the amount of the STC Distribution in respect of such KTIPLOffer Shares will be deducted from the Revised KTIPL Offer Price payable for such KTIPL OfferShares, as KTIPL will not have received the STC Distribution in respect of those KTIPL OfferShares from STC.

3.4 Condition. In the KTIPL Offer Document, it was stated that the KTIPL Offer will be conditionalupon KTIPL having received, by the close of the KTIPL Offer, valid acceptances in respect of suchnumber of KTIPL Offer Shares which, when taken together with the Shares owned or agreed to beacquired by KTIPL and its Concert Parties including the Concert Party Group (either before orduring the KTIPL Offer and pursuant to the KTIPL Offer or otherwise), will result in KTIPL and itsConcert Parties, including the Concert Party Group, holding such number of Shares carrying morethan 50 per cent. of the voting rights attributable to the issued Shares as at the close of the KTIPLOffer (the “Condition”).

The KTIPL Offer is unconditional in all other respects.

3.5 Warranty. According to the KTIPL Offer Document, acceptance of the KTIPL Offer will be deemedto constitute an unconditional and irrevocable warranty by the accepting Shareholder that eachKTIPL Offer Share in respect of which the KTIPL Offer is accepted is sold by the acceptingShareholder, as or on behalf of the beneficial owner, fully paid and free from all claims, charges,equities, liens, pledges and other encumbrances and together with all rights, benefits, entitlementsand advantages attached thereto as at the KTIPL Offer Announcement Date and thereafterattaching thereto, including the right to all dividends, rights and other distributions (if any) declared,made or paid thereon on or after the KTIPL Offer Announcement Date (including any dividends thatmay be declared, made or paid thereon in respect of FY 2007).

3.6 Details of the KTIPL Offer. Further details of the KTIPL Offer are set out in pages 8 to 11 of theKTIPL Offer Document and Appendix 1 to the KTIPL Offer Document including details on (a) theduration of the KTIPL Offer; (b) the procedures for acceptance of the KTIPL Offer; (c) therequirements relating to announcements of the level of acceptances of the KTIPL Offer; and (d) theright of withdrawal of acceptances.

A copy each of the KTIPL Offer Announcement, the KTIPL Offer Document and the Revised KTIPLOffer Announcement is available on the website of the SGX-ST at www.sgx.com.

3.7 KTIPL Offer Closing Date. Shareholders should note that the Revised KTIPL Offer will close at5.30 p.m. (Singapore time) on 13 March 2008 or such later date(s) as may be announced fromtime to time by or on behalf of KTIPL.

LETTER TO SHAREHOLDERS

10

4. RATIONALE FOR THE KTIPL OFFER AND KTIPL’S FUTURE PLANS FOR THE COMPANY

The full text of the rationale for the KTIPL Offer and KTIPL’s intentions relating to the Company hasbeen extracted from the KTIPL Offer Document and is set out in italics below. Unless otherwisedefined, all terms and expressions used in the extract below shall have the same meanings asthose defined in the KTIPL Offer Document. Shareholders are advised to read the extract belowcarefully.

“5.1 Rationale for the Offer

The Lee Family has had shareholding interests in STC for many years. The Offeror(together with the GEH Group and the OCBC Group) has effective control of STC as theycontrol the largest single block of Shares. The Offer is being made in response to theCairns Offer with the objective of maintaining or consolidating effective control of STC.

5.2 The Offeror’s Intentions relating to STC

It is the intention of the Offeror that STC will continue to develop and grow its existingbusinesses. Depending on the outcome of the Offer and the resultant shareholding of theOfferor in STC following the close of the Offer, the Offeror (if appropriate together with itsConcert Parties) intends to seek representation on the board of directors of STC.

In addition, after the close of the Offer, if the Offeror (together with the GEH Group and theOCBC Group) continues to control the largest single block of Shares, the Offeror intends topropose to STC to engage a financial adviser to conduct a study on the financialperformance of STC and to recommend possible steps to take to further unlock value inSTC for the benefit of Shareholders. In this connection, the Offeror supports the policy ofthe STC board as stated on page 83 of STC’s circular to Shareholders dated 3 February2008 in relation to the Cairns Offer, which is reproduced as follows:

“With a clear focus on shareholders’ value, the Group will continue to review its businessstrategy and prioritise the allocation of funds to enhance shareholders’ value and togenerate higher return to shareholders in the long term”.

Save as disclosed above, the Offeror has no immediate plans for any major changesrelating to the existing business of the STC Group (including redeployment of fixed assets)or the employment of the existing employees of the STC Group, other than in the ordinarycourse of business.”

5. LISTING STATUS AND COMPULSORY ACQUISITION

The KTIPL Offer Document also sets out the intentions of KTIPL relating to the listing status of theCompany as follows:

“7. COMPULSORY ACQUISITION AND LISTING STATUS

Pursuant to Section 215(1) of the Act, if the Offeror receives valid acceptances pursuant tothe Offer in respect of not less than 90% of the Offer Shares (other than those already heldby the Offeror, its related corporations or their respective nominees as at the date of theOffer and excluding any Shares held as treasury shares), the Offeror would have the rightto compulsorily acquire all the Offer Shares not acquired by the Offeror pursuant to theOffer.

Shareholders who have not accepted the Offer have the right under and subject to Section215(3) of the Act, to require the Offeror to acquire their Shares in the event that the Offeroror its nominees acquire, pursuant to the Offer, such number of Shares which, together withthe Shares held by the Offeror, its related corporations or their respective nominees,comprise 90% or more of the total number of issued Shares (excluding treasury shares).Shareholders who have not accepted the Offer and who wish to exercise such right areadvised to seek their own independent legal advice.

LETTER TO SHAREHOLDERS

11

Pursuant to Rule 1105 of the Listing Manual, upon an announcement by the Offeror thatacceptances have been received pursuant to the Offer that bring the holdings owned by theOfferor and its Concert Parties to above 90% of the total number of issued Sharesexcluding treasury shares, the SGX-ST may suspend the listing of the Shares on the SGX-ST until such time it is satisfied that at least 10% of the total number of issued Sharesexcluding treasury shares are held by at least 500 Shareholders who are members of thepublic. Rule 1303(1) of the Listing Manual provides that if the Offeror succeeds in garneringacceptances exceeding 90% of the total number of issued Shares excluding treasuryshares, thus causing the percentage of the total number of issued Shares excludingtreasury shares held in public hands to fall below 10%, the SGX-ST will suspend trading ofthe Shares only at the close of the Offer.

In addition, under Rule 724 of the Listing Manual, if the percentage of the total number ofissued Shares excluding treasury shares held in public hands falls below 10%, STC must,as soon as practicable, announce that fact and the SGX-ST may suspend the trading of allthe Shares. Rule 725 of the Listing Manual states that the SGX-ST may allow STC a periodof three months, or such longer period as the SGX-ST may agree, to raise the percentageof Shares in public hands to at least 10%, failing which STC may be delisted from the SGX-ST.

It is the present intention of the Offeror to maintain the listing status of STC on theSGX-ST. However, in the event SGX-ST suspends the listing of the Shares on theSGX-ST in the above circumstances or in the event that the Offeror receivesacceptances in respect of not less than 90% of the Offer Shares (other than thosealready held by the Offeror, its related corporations or their respective nominees asat the date of the Offer and excluding Shares held as treasury shares), the Offerorwill reassess its position in respect of its shareholdings in STC.”

6. INFORMATION ON KTIPL AND LEE LATEX

Paragraph 3 of the KTIPL Offer Document sets out information on KTIPL and Lee Latex, asfollows:

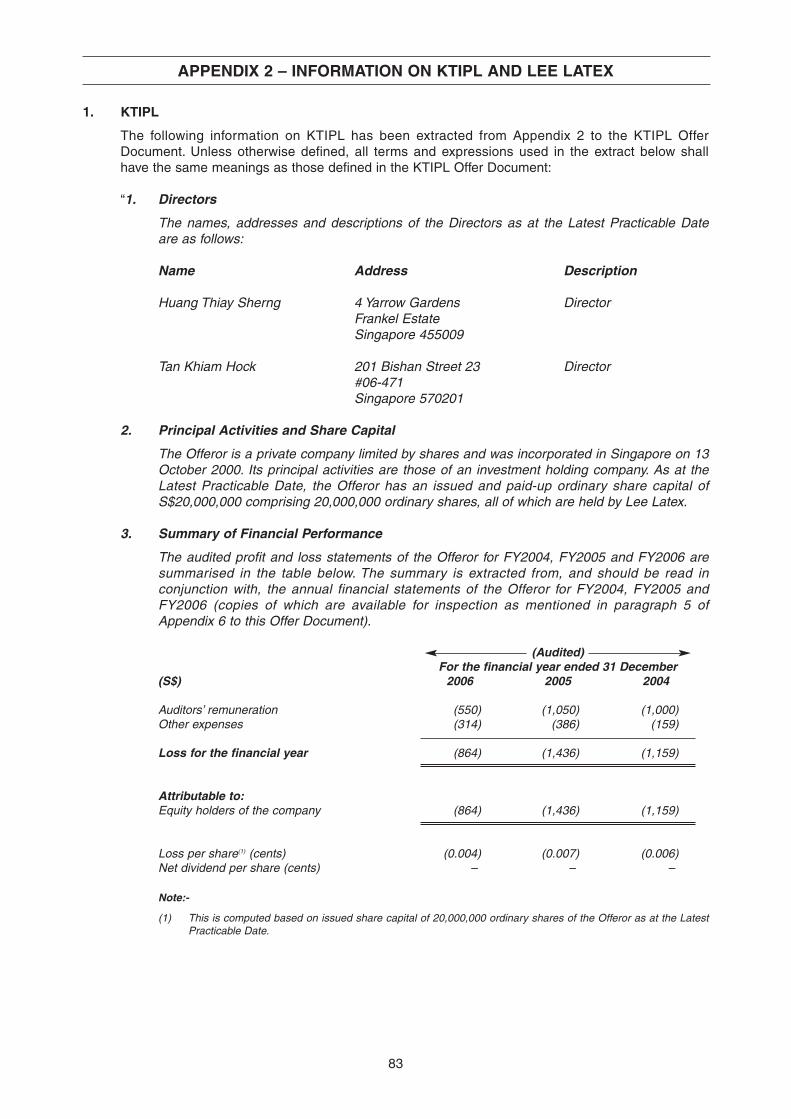

“3.1 The Offeror. The Offeror is a company incorporated in Singapore on 13 October 2000. Itsprincipal activities are those of an investment holding company. As at the Latest PracticableDate, the Offeror has an issued and paid-up ordinary share capital of S$20,000,000comprising 20,000,000 ordinary shares, all of which are held by Lee Latex. The Offeror is adirect wholly-owned subsidiary of Lee Latex. As at the Latest Practicable Date, theDirectors are Messrs Huang Thiay Sherng and Tan Khiam Hock.

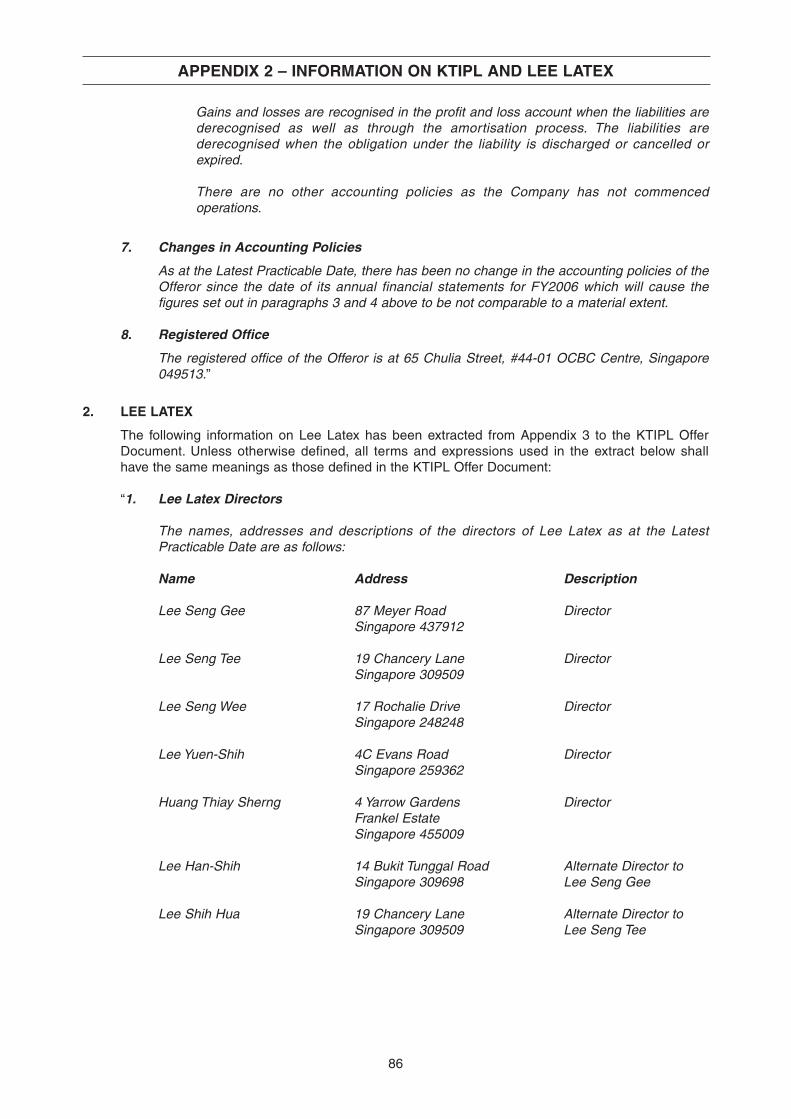

3.2 Lee Latex. Lee Latex is a company incorporated in Singapore on 10 June 1947. Itsprincipal activity is that of investment holding. As at the Latest Practicable Date, Lee Latexhas an issued and paid-up share capital of S$30,000,000 comprising 30,000 ordinaryshares. As at the Latest Practicable Date, the directors of Lee Latex are Messrs Lee SengWee, Lee Seng Gee, Lee Seng Tee, Lee Yuen-Shih, Lee Han-Shih (alternate to Lee SengGee), Lee Shih Hua (alternate to Lee Seng Tee) and Huang Thiay Sherng.

3.3 Additional Information. Additional information on the Offeror and Lee Latex is set out inAppendix 2 and Appendix 3 to this Offer Document, respectively.”

7. IRREVOCABLE UNDERTAKINGS

The KTIPL Offer Document states that as at 11 February 2008, neither KTIPL nor its ConcertParties have received any irrevocable undertaking from any holder of KTIPL Offer Shares to acceptor reject the KTIPL Offer.

LETTER TO SHAREHOLDERS

12

8. ADVICE OF THE IFA

8.1 IFA. CIMB-GK has been appointed as the independent financial adviser to advise the IndependentDirectors in respect of the TCPL Offer and the KTIPL Offer. Shareholders should consider carefullythe recommendations of the Independent Directors and the advice of CIMB-GK to the IndependentDirectors before deciding whether to accept or reject the Final TCPL Offer or the Revised KTIPLOffer, as the case may be. The advice of CIMB-GK is set out in its letter dated 23 February 2008,which is set out on pages 18 to 73 of this Circular (the “IFA Letter”).

8.2 Key Factors Taken into Consideration by CIMB-GK. Unless otherwise defined or the contextotherwise requires, all capitalised terms below shall have the same meanings as defined in the IFALetter.

In arriving at its advice, CIMB-GK has relied on the following key considerations (an extract ofwhich is set out below and which should be read in conjunction with, and in the context of, the fulltext of the IFA Letter):

“8. SUMMARY OF ANALYSIS

In arriving at our advice on the Revised KTIPL Offer and the Final TPL Offer, we have reliedon the following key considerations (which should be read in conjunction with, and in thecontext of, the full text of this letter):

(a) the Revised KTIPL Offer Price and the Final TCPL Offer Price falls within the rangeof the estimated sum-of-parts valuation of each Share.

(b) The Revised KTIPL Offer Price represents a premium of approximately 17.0% overthe unaudited book NTA per Share as at 31 December 2007 but is at a discount ofapproximately 0.6% to the Revalued NTA per Share as at 31 December 2007. TheFinal TCPL Offer Price represents a premium of approximately 19.6% over theunaudited book NTA per Share as at 31 December 2007 and at a premium ofapproximately 1.7% to the Revalued NTA per Share as at 31 December 2007.

(c) The ex-cash Revised KTIPL Offer Price represents a premium of approximately20.9% over the ex-cash book NTA per Share as at 31 December 2007 but is at adiscount of approximately 0.7% to the ex-cash Revalued NTA per Share as at 31December 2007. The ex-cash Final TCPL Offer Price represents a premium ofapproximately 24.2% over the ex-cash book NTA per Share as at 31 December 2007and is at a premium of approximately 2.0% over the ex-cash Revalued NTA perShare as at 31 December 2007.

(d) The Revised KTIPL Offer Price and the Final TCPL Offer Price are at a premiumover the VWAP of the Shares for all historical periods during the three years prior tothe TCPL Offer Announcement Date. As at the Latest Practicable Date, the Sharesare trading above the Revised KTIPL Offer Price but are trading at the Final TCPLOffer Price.

(e) It is highly likely that the market price of the Shares has been supported by theOffers and purchases by KTIPL, TCPL or their respective concert parties since theTCPL Offer Announcement Date. As the Shares have been trading at or about theFinal TCPL Offer Price since the Second Price Revision Announcement on the TCPLOffer, there is no assurance that the market price and the trading volume of theShares will be maintained at the level prevailing as at the Latest Practicable Dateafter the closing dates of the Offers.

LETTER TO SHAREHOLDERS

13

(f) The market price premia to the last transacted price, the 1-month VWAP and the 3-month VWAP prior to the TCPL Offer Announcement Date implied in the RevisedKTIPL Offer Price and the Final TCPL Offer Price are above the correspondingmedian and mean premia in both the successful privatisation and non-privatisationTake-over Transactions while the P/NTA ratios of the Group implied in the RevisedKTIPL Offer Price and the Final TCPL Offer Price are below the mean but equal tothe median P/NTA ratios of the successful non-privatisation Take-over Transactions.

(g) The net dividend yield of the Company implied in the Revised KTIPL Offer Price andthe Final TCPL Offer Price is lower than the net dividend yields (in respect of theirlast financial year) of almost all of the Alternative Companies and that of the STI ETF.

(h) As at the Latest Practicable Date, neither KTIPL nor TCPL and their respectiveconcert parties possess statutory control of the Company. Both the Revised KTIPLOffer and the Final TCPL Offer have not become unconditional as at the LatestPracticable Date.

(i) It is the present intention of each of KTIPL and TCPL to maintain the listing status ofthe Company on the SGX-ST. There is however no assurance that KTIPL or TCPLwill preserve the listing status of the Company on the SGX-ST if free float is lessthan 10 per cent. or that they will not exercise the right of compulsory acquisitionunder Section 215(1) of the Act.

(j) The Final TCPL Offer Price of S$6.70 for each Share is S$0.15 higher than theRevised KTIPL Offer Price of S$6.55 for each Share.

(k) It is stated in the Second Price Revision Announcement on the TCPL Offer thatTCPL does not intend to further revise the Final TCPL Offer Price. The Final TCPLOffer will close at 5.30 p.m. on 6 March 2008 and TCPL has stated that it does notintend to extend the Final TCPL Offer beyond 5.30 p.m. on the Final Closing Dateexcept where the Final TCPL Offer becomes unconditional as to acceptances orwhere TCPL incurs a mandatory offer obligation under Rule 14 of the Code duringthe offer period through the acquisition of the Shares (other than pursuant toacceptances of the Final TCPL Offer). The Revised KTIPL Offer will close at 5.30p.m. on 13 March 2008 or such later date(s) as may be announced from time to timeby or on behalf of KTIPL.

In summary, based on our analysis set out above and after having considered carefully theinformation available to us, the existence of competing bids for statutory control of theCompany and based on the monetary, industry, market, economic and other relevantconditions prevailing as at the Latest Practicable Date, we are of the view that both theRevised KTIPL Offer Price and the Final TCPL Offer Price are, on balance, reasonable butnot compelling.”

LETTER TO SHAREHOLDERS

14

8.3 Advice of CIMB-GK. Unless otherwise defined or the context otherwise requires, all capitalisedterms below shall have the same meanings as defined in the IFA Letter.

After carefully considering all available information and based on CIMB-GK’s assessment of thefinancial terms of the Final TCPL Offer and the Revised KTIPL Offer, CIMB-GK has advised theIndependent Directors to make the following recommendations to Shareholders in relation to theFinal TCPL Offer and the Revised KTIPL Offer:

“9. CIMB-GK’S ADVICE ON THE OFFERS

After carefully considering all available information and based on our assessment of thefinancial terms of the Revised KTIPL Offer and the Final TCPL Offer, we advise theIndependent Directors to make the following recommendations to Shareholders in relation tothe Revised KTIPL Offer and the Final TCPL Offer:

“Shareholders who hold a long-term view of their investments in the Shares and/or whoare confident and optimistic about their equity investments in the Company and theprospects of the Group may wish to REJECT both the Revised KTIPL Offer and the FinalTCPL Offer.

Shareholders who hold a short-term view of their investments in the Shares and whowish to realise their holdings in the Shares in the near term and/or who are not preparedto accept the uncertainties facing the future prospects of the Group or the risk that noneof the Offers will become unconditional may wish to SELL their Shares on the openmarket if they can obtain a price at about or higher than the Final TCPL Offer Price (afterdeducting all related expenses) by doing so as there is currently no certainty that eitherof the Offers will become unconditional. Shareholders should note that as at the LatestPracticable Date, the Shares are trading at the Final TCPL Offer Price. In the event thatShareholders (in particular, those with significant holdings) are unable to sell theirShares on the open market at a price at about or higher than the Final TCPL Offer Price,they should REJECT the Revised KTIPL Offer but may wish to ACCEPT the Final TCPLOffer but should be aware that there is currently no certainty that the Final TCPL Offerwill become unconditional. Further, such Shareholders may wish to consider acceptingthe Final TCPL Offer at a later time so as to be able to take into account anyannouncements and/or documents relevant to their consideration of the Offers whichmay be released or published by or on behalf of the Company, TCPL and/or KTIPL afterthe Latest Practicable Date. The Final TCPL Offer will close at 5.30 p.m. on 6 March2008 and TCPL has stated that it does not intend to extend the Final TCPL Offer beyond5.30 p.m. on the Final Closing Date except where the Final TCPL Offer becomesunconditional as to acceptances or where TCPL incurs a mandatory offer obligationunder Rule 14 of the Code during the offer period through the acquisition of the Shares(other than pursuant to acceptances of the Final TCPL Offer). The Revised KTIPL Offerwill close at 5.30 p.m. on 13 March 2008 or such later date(s) as may be announcedfrom time to time by or on behalf of KTIPL.

Shareholders should note that (i) there is currently no indication as to whether there maybe a further enhancement or revision of the Revised KTIPL Offer following the SecondPrice Revision Announcement on the TCPL Offer; and (ii) there is no assurance that thetrading volumes and market prices of the Shares will be maintained at current levelsprevailing as at the Latest Practicable Date.”

Shareholders should read the extracts in paragraphs 8.2 and 8.3 above in conjunction with, and inthe context of the full text of the IFA Letter which is set out on pages 18 to 73 of this Circular.

LETTER TO SHAREHOLDERS

15

9. INDEPENDENT DIRECTORS’ RECOMMENDATIONS

9.1 Exemptions by SIC. In its letter dated 31 January 2008, the SIC has ruled that the followingdirectors of the Company, namely Mr Bobby Chin Yoke Choong, Mr Michael Wong Pakshong andTan Sri Dato Dr Lin See-Yan (the “Relevant Directors”) are exempt from the requirement to makerecommendations on the TCPL Offer and the KTIPL Offer as they face irreconcilable conflicts ofinterest being directors of parties acting in concert with KTIPL. Nevertheless, the RelevantDirectors will still accept responsibility for the accuracy of the facts stated or opinions expressed indocuments and advertisements issued by, or on behalf of, the Company in connection with theTCPL Offer and the KTIPL Offer.

9.2 Recommendations of Independent Directors. The Independent Directors, having consideredcarefully the terms of the Final TCPL Offer and the Revised KTIPL Offer and the advice given byCIMB-GK, concur with the advice of CIMB-GK in respect of the Final TCPL Offer and the RevisedKTIPL Offer. Accordingly, the Independent Directors’ recommendations in respect of the Final TCPLOffer and the Revised KTIPL Offer are as set out in paragraph 8.3 above.

Shareholders are advised to read the IFA Letter set out on pages 18 to 73 of this Circularcarefully.

9.3 No Regard to Specific Objectives. In making their recommendations, the Independent Directorshave not had regard to the specific objectives, financial situation, tax status, risk profiles or uniqueneeds and constraints of any individual Shareholder. Accordingly, the Independent Directorsrecommend that any individual Shareholder who may require advice in the context of his specificinvestment portfolio should consult his stockbroker, bank manager, solicitor, accountant, tax adviseror other professional adviser immediately.

10. OVERSEAS SHAREHOLDERS

10.1 Overseas Shareholders. Based on the KTIPL Offer Document, the availability of the RevisedKTIPL Offer to Shareholders whose addresses are outside Singapore, as shown in the Register ofMembers of STC or in the records of CDP (as the case may be) (each, an “OverseasShareholder”) may be affected by the laws of the relevant overseas jurisdictions. Accordingly,Overseas Shareholders should inform themselves about and observe any applicable legalrequirements.

It is the responsibility of Overseas Shareholders who wish to accept the Revised KTIPL Offer tosatisfy themselves as to the full observance of the laws of the relevant jurisdiction, including theobtaining of any governmental or other consent which may be required, or compliance with othernecessary formalities or legal requirements and the payment of any taxes, imposts, duties or otherrequisite payments due in such jurisdiction. Such Overseas Shareholders shall be liable for anysuch taxes, imposts, duties or other requisite payments payable and KTIPL, its relatedcorporations, the FAs, CDP and any person acting on their behalf shall be fully indemnified andheld harmless by such Overseas Shareholders for any such taxes, imposts, duties or otherrequisite payments as KTIPL, its related corporations, the FAs, CDP and/or any person acting ontheir behalf may be required to pay. In accepting the Revised KTIPL Offer, each OverseasShareholder represents and warrants to KTIPL and the FAs that he is in full observance of the lawsof the relevant jurisdiction in that connection and that he is in full compliance with all necessaryformalities or legal requirements.

LETTER TO SHAREHOLDERS

If you are in doubt about your position, you should consult your professional adviser in therelevant jurisdiction.

KTIPL and the FAs each reserve the right not to treat an acceptance or purported acceptance ofthe Revised KTIPL Offer in or from any overseas jurisdiction and/or in respect of an OverseasShareholder as valid. Overseas Shareholders accepting the Revised KTIPL Offer should note that ifthey have, in the KTIPL FAT, provided addresses in overseas jurisdictions for the receipt ofremittances of payment by KTIPL, such acceptances may be rejected.

10.2 Copies of KTIPL Offer Document. Where there are potential restrictions on sending the KTIPLOffer Document, the KTIPL FAA and the KTIPL FAT to any overseas jurisdiction, KTIPL and theFAs each reserve the right not to send the KTIPL Offer Document, the KTIPL FAA and the KTIPLFAT to any overseas jurisdiction. Subject to compliance with applicable laws, any affected OverseasShareholder may, nonetheless, attend in person and obtain copies of the KTIPL Offer Document,the KTIPL FAA or the KTIPL FAT, as the case may be, and any related documents during normalbusiness hours and up to the KTIPL Offer Closing Date, from Knowledge Two Investment Pte Ltdc/o Tricor Barbinder Share Registration Services (a division of Tricor Singapore Pte. Ltd.) at 8Cross Street, #11-00, PWC Building, Singapore 048424 or CDP at 4 Shenton Way, #02-01 SGXCentre 2, Singapore 068807, as the case may be. Alternatively, an Overseas Shareholder may,subject to compliance with applicable laws, write in to Tricor Barbinder Share Registration Servicesat the above-stated address to request that the KTIPL Offer Document, the KTIPL FAA or theKTIPL FAT, as the case may be, and any related documents be sent to an address in Singapore byordinary post at his own risk (up to three Market Days prior to the KTIPL Offer Closing Date). Forthe avoidance of doubt, the Revised KTIPL Offer is made to all Shareholders (for all KTIPL OfferShares) including those to whom the KTIPL Offer Document may not be despatched.

10.3 Notice. KTIPL and the FAs each reserve the right to notify any matter, including the fact that theRevised KTIPL Offer has been made, to any or all Shareholders (including Overseas Shareholders)by announcement to the SGX-ST or paid advertisement in a daily newspaper published orcirculated in Singapore, in which case, such notice shall be deemed to have been sufficiently givennotwithstanding any failure by any Shareholder to receive or see such announcement oradvertisement.

11. CPFIS INVESTORS

According to the KTIPL Offer Document, CPFIS Investors should receive further information onhow to accept the Revised KTIPL Offer from their CPF Agent Banks shortly. CPFIS Investors areadvised to consult their respective CPF Agent Banks should they require further information, and ifthey are in any doubt as to the action they should take, CPFIS Investors should seek independentprofessional advice. CPFIS Investors who wish to accept the Revised KTIPL Offer are to reply totheir respective CPF Agent Banks accordingly by the deadline stated in the letter from theirrespective CPF Agent Banks. Subject to the Revised KTIPL Offer becoming or being declaredunconditional in accordance with its terms, CPFIS Investors who accept the Revised KTIPL Offerwill receive the Revised KTIPL Offer Price payable in respect of their KTIPL Offer Shares in theirCPF investment accounts.

12. ACTION TO BE TAKEN BY SHAREHOLDERS

Shareholders who do not wish to accept the Final TCPL Offer need not take any further action inrespect of the TCPL Offer Document, the TCPL FAA and/or the TCPL FAT which have been sent tothem.

Shareholders who wish to accept the Final TCPL Offer must do so not later than 5.30 p.m. on 6March 2008. The Directors would like to draw the attention of Shareholders who wish to accept theFinal TCPL Offer to the “Procedures for Acceptance” as set out on pages 19 to 23 of the TCPLOffer Document.

16

LETTER TO SHAREHOLDERS

Acceptances should be completed and returned as soon as possible and, in any event, so as to bereceived by CDP (in respect of the TCPL FAA) or the share registrar of the Company (in respect ofthe TCPL FAT), as the case may be, not later than 5.30 p.m. on 6 March 2008.

Shareholders who do not wish to accept the Revised KTIPL Offer need not take any further actionin respect of the KTIPL Offer Document, the KTIPL FAA and/or the KTIPL FAT which have beensent to them.

Shareholders who wish to accept the Revised KTIPL Offer must do so not later than 5.30 p.m. on13 March 2008, or such later date(s) as may be announced from time to time by or on behalf ofKTIPL. The Directors would like to draw the attention of Shareholders who wish to accept theRevised KTIPL Offer to “Additional Terms of the Offer” as set out in Appendix 1 to the KTIPL OfferDocument.

Acceptances should be completed and returned as soon as possible and, in any event, so as to bereceived by CDP (in respect of the KTIPL FAA) or the share registrar of the Company (in respect ofthe KTIPL FAT), as the case may be, not later than 5.30 p.m. on 13 March 2008, or such laterdate(s) as may be announced from time to time by or on behalf of KTIPL.

13. RESPONSIBILITY STATEMENT

The Directors of the Company (including any who may have delegated detailed supervision of thisCircular) have taken all reasonable care to ensure that the facts stated and all opinions expressedin this Circular are fair and accurate and that no material facts have been omitted from this Circular,and they jointly and severally accept responsibility accordingly. Where any information has beenextracted or reproduced from published or publicly available sources, the sole responsibility of theDirectors of the Company has been to ensure through reasonable enquiries that such informationis accurately extracted from such sources or, as the case may be, reflected or reproduced in thisCircular.

In respect of the IFA Letter, the sole responsibility of the Directors has been to ensure that the factsstated therein with respect to the Group are fair and accurate.

Yours faithfullyFor and on behalf of the Board of Directors ofTHE STRAITS TRADING COMPANY LIMITED

Norman Ip Ka CheungPresident and Chief Executive Officer

17

LETTER TO SHAREHOLDERS

18

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

CIMB-GK SECURITIES PTE. LTD.(Incorporated in the Republic of Singapore)

(Company Registration Number: 198701621D)

50 Raffles Place #19-00Singapore Land Tower

Singapore 048623

23 February 2008

To: The Independent DirectorsThe Straits Trading Company Limited18 Cross Street #15-01Singapore 048423

Dear Sirs,

MANDATORY CONDITIONAL CASH OFFER BY CREDIT SUISSE (SINGAPORE) LIMITED ANDOVERSEA-CHINESE BANKING CORPORATION LIMITED FOR AND ON BEHALF OF KNOWLEDGETWO INVESTMENT PTE LTD FOR THE STRAITS TRADING COMPANY LIMITED

VOLUNTARY CONDITIONAL CASH OFFER BY STANDARD CHARTERED BANK FOR AND ONBEHALF OF THE CAIRNS PTE. LTD. FOR THE STRAITS TRADING COMPANY LIMITED

1. INTRODUCTION

On 6 January 2008 (the “TCPL Offer Announcement Date”), Standard Chartered Bank (“SCB”)announced (the “TCPL Offer Announcement”), for and on behalf of The Cairns Pte. Ltd. (“TCPL”),that TCPL intends to make a voluntary conditional cash offer (the “TCPL Offer”) for all the issuedordinary shares (“Shares”) in the capital of The Straits Trading Company Limited (“STC” or the“Company”), other than those already owned, controlled or agreed to be acquired by TCPL (“TCPLOffer Shares”), at a price of S$5.70 for each TCPL Offer Share.

On 24 January 2008 (the “KTIPL Offer Announcement Date”), Oversea-Chinese BankingCorporation Limited (“OCBC Bank”) announced (the “KTIPL Offer Announcement”), for and onbehalf of Knowledge Two Investment Pte Ltd (“KTIPL”), a wholly-owned subsidiary of Lee Latex(Pte) Limited (“Lee Latex”), that KTIPL intends to make a mandatory conditional cash offer (the“KTIPL Offer”) for all the Shares other than those already owned or agreed to be acquired byKTIPL and the intermediate companies (“Lee Family Companies”) through which Messrs Lee Seng Gee, Lee Seng Tee and Lee Seng Wee and their immediate family members hold theirinterests in Lee Latex (“KTIPL Offer Shares”), at a price of S$5.76 for each KTIPL Offer Share(the “KTIPL Offer Price”).

On 28 January 2008 (the “Revised TCPL Offer Announcement Date”), SCB announced (the“Revised TCPL Offer Announcement”), for and on behalf of TCPL, that TCPL is revising the offerprice to S$6.50 (the “Revised TCPL Offer Price”) for each TCPL Offer Share (the “Revised TCPLOffer”).

On the same date, SCB also issued, for and on behalf of TCPL, a letter of offer to each of OCBCBank and Great Eastern Holdings Limited (“GEH”) to purchase, at the Revised TCPL Offer Price,all the 20,248,704 Shares held by OCBC Bank and its subsidiaries (excluding the GEH Group (asdefined hereinafter)) (“OCBC Group”) representing approximately 6.21 per cent. of all the issued

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

19

Shares, and all the 64,903,864 Shares held by GEH and its subsidiaries (“GEH Group”)representing approximately 19.92 per cent. of all the issued Shares. The announcement also statedthat the offers to OCBC Bank and GEH are unconditional and would expire at 5.30 p.m. on 22February 2008 if they were not accepted by OCBC Bank and/or GEH and should OCBC Bank andGEH have accepted the offers, TCPL and parties acting in concert with it would then own, controlor have agreed to acquire not less than 162,058,845 Shares, representing 49.73 per cent. of all theissued Shares. TCPL would then convert the Revised TCPL Offer into a mandatory conditionalcash offer for the Shares in accordance with the provisions of The Singapore Code on Take-oversand Mergers (the “Code”).

On 14 February 2008 (the “Revised KTIPL Offer Announcement Date”), Credit Suisse(Singapore) Limited (“Credit Suisse”) and OCBC Bank announced (the “Revised KTIPL OfferAnnouncement”), for and on behalf of KTIPL, that KTIPL is revising the offer price to S$6.55 (the“Revised KTIPL Offer Price”) for each KTIPL Offer Share (the “Revised KTIPL Offer”).

On 15 February 2008, OCBC Group (excluding the GEH Group) announced that, having regard toits own considerations, it has decided that it does not intend to accept either the Revised TCPLOffer or the Revised KTIPL Offer in respect of its 6.21 per cent. of all the issued Shares.

On 18 February 2008 (the “Second Price Revision Announcement Date on the TCPL Offer”),SCB announced (the “Second Price Revision Announcement on the TCPL Offer”), for and onbehalf of TCPL, that TCPL is revising the offer price to S$6.70 (the “Final TCPL Offer Price”) foreach TCPL Offer Share (the “Final TCPL Offer”). It is also stated in the Second Price RevisionAnnouncement on the TCPL Offer that TCPL does not intend to further revise the Final TCPL OfferPrice.

On 18 February 2008, SCB also announced that it had also issued, for and on behalf of TCPL, aletter of offer to each of OCBC Bank and GEH to purchase, at the Final TCPL Offer Price, all the20,248,704 Shares held by the OCBC Group (excluding the GEH Group) representingapproximately 6.21 per cent. of all the issued Shares, and all the 64,903,864 Shares held by theGEH Group, including the Shares held by the participating funds of Great Eastern Life AssuranceCompany Limited and Great Eastern Life Assurance (Malaysia) Berhad, representingapproximately 19.92 per cent. of all the issued Shares.

The offers to OCBC Bank and GEH are unconditional and will expire at 5.00 p.m. (Singapore time)on 6 March 2008 if they are not accepted by OCBC Bank and/or GEH. The same announcementalso states that should OCBC Bank and GEH accept the offers, TCPL and parties acting in concertwith it shall then own, control or have agreed to acquire not less than 162,205,896 Shares,representing 49.77 per cent. of all the issued Shares. TCPL shall then convert the TCPL Offer intoa mandatory offer for the TCPL Offer Shares in accordance with the provisions of the Code.

Shareholders should by now have received the offer document containing the terms and conditionsof the KTIPL Offer (the “KTIPL Offer Document”).

CIMB-GK Securities Pte. Ltd. has been appointed as the independent financial adviser to thedirectors of the Company who are deemed to be independent (“Independent Directors”) for thepurpose of rendering a recommendation to the shareholders of the Company (“Shareholders”) inconnection with the offers made by TCPL and KTIPL (collectively, the “Offers”).

This letter sets out, inter alia, our evaluation of the financial terms of the Offers and our advicethereon. It forms part of the circular dated 23 February 2008 and issued by the Company,providing, inter alia, details of the KTIPL Offer, the Revised KTIPL Offer and the Final TCPL Offerand the recommendation of the Independent Directors in respect of the Revised KTIPL Offer andthe Final TCPL Offer (the “Circular”). Unless otherwise defined or the context otherwise requires,all terms defined in the Circular shall have the same meanings herein.

2. TERMS OF REFERENCE

We have been appointed to advise the Independent Directors on the financial terms of the Offersand whether Shareholders should accept or reject the Offers, pursuant to Rules 7.1 and 24.1(b) ofthe Code. We have confined our evaluation to the financial terms of the Offers and our terms ofreference do not require us to evaluate or comment on the commercial risks and/or commercialmerits of the Offers or the future prospects of the Company and its subsidiaries (the “Group”) orany of its associated or joint venture companies and we have not made such evaluation orcomment. However, we may draw upon the views of the Directors and/or the management of theCompany or make such comments in respect thereof (to the extent deemed necessary orappropriate by us) in arriving at our opinion as set out in this letter. We have not been requested,and we do not express any opinion on the relative merits of the Offers as compared to any otheralternative transaction. We have not been requested or authorised to solicit, and we have notsolicited, any indications of interest from any third party with respect to the Shares.

We have held discussions with the Directors and the management of the Company and haveexamined publicly available information collated by us as well as information, both written andverbal, provided to us by the Directors, the management of the Company and the Company’s otherprofessional advisers. We have not independently verified such information, whether written orverbal, and accordingly we cannot and do not warrant or make any representation (whetherexpress or implied) regarding, or accept any responsibility for, the accuracy, completeness oradequacy of such information. However, we have made such enquiries and exercised our judgmentas we deem necessary on such information and have found no reason to doubt the reliability of theinformation.

We have relied upon the assurances of the Directors (including those who may have delegatedsupervision of the Circular) that they have taken all reasonable care to ensure that the facts statedand opinions expressed by them or the Company in the Circular are true, complete and accurate inall material respects. The Directors have confirmed to us, that to the best of their knowledge andbelief, all material information relating to the Group, its associated or joint venture companies andthe Offers have been disclosed to us, that such information is true, complete and accurate in allmaterial respects and that there are no other material facts and circumstances the omission ofwhich would make any statement in the Circular inaccurate, incomplete or misleading in anymaterial respect. The Directors have jointly and severally accepted such responsibility accordingly.

We have not made any independent evaluation or appraisal of the assets and liabilities (includingwithout limitation, real property) of the Group or any of its associated or joint venture companiesand we have not been furnished with any such evaluation or appraisal, except for the letters andvaluation certificates from the Valuers appointed by the Company in connection with the Offers setout in Appendix 8 to the TCPL Offeree Circular in which we have placed sole reliance on for suchasset appraisal. With respect to such letters and valuation certificates, we are not experts in theevaluation or appraisal of the assets concerned and we have not made any independentverification of the contents of these letters and valuation certificates.

Our opinion is based upon market, economic, industry, monetary and other conditions prevailing on20 February 2008 (the “Latest Practicable Date”), as well as the information made available to usas at the Latest Practicable Date. Such conditions may change significantly over a short period oftime. Accordingly, we do not express any opinion or view on the future prospects, financialperformance and/or financial position of the Group, its associated or joint venture companies.Shareholders should take note of any announcement and/or documents relevant to theirconsideration of the Offers which may be released or published by or on behalf of the Company,TCPL and/or KTIPL after the Latest Practicable Date.

20

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

21

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

In rendering our advice, we have not had regard to the specific investment objectives, financialsituation, tax position, risk profile or particular needs and constraints of any individual Shareholder.As each Shareholder would have different investment objectives and profiles, any Shareholder whomay require specific advice in the context of his specific investment objectives or portfolio shouldconsult his stockbroker, bank manager, solicitor, accountant, tax adviser or other professionaladviser immediately.

The Company has been separately advised in the preparation of the Circular (other than thisletter). We were not involved in and have not provided any advice in the preparation, review andverification of the Circular (other than this letter). Accordingly, we take no responsibility for, andexpress no views (express or implied) on, the contents of the Circular (other than this letter).

3. THE REVISED KTIPL OFFER

Shareholders should by now have received a copy of the KTIPL Offer Document dated 12 February 2008 issued by Credit Suisse and OCBC Bank, for and on behalf of KTIPL. TheRevised KTIPL Offer Announcement states that KTIPL will shortly despatch the Revised KTIPLOffer Letter to Shareholders relating to the Revised KTIPL Offer.

According to the Revised KTIPL Offer Announcement, save for the Revised KTIPL Offer Price, allthe other terms and conditions of the KTIPL Offer as set out in the KTIPL Offer Document remainunchanged.

3.1 Revised KTIPL Offer Price

For and on behalf of KTIPL, Credit Suisse and OCBC are making the Revised KTIPL Offer toacquire all the KTIPL Offer Shares on the following basis:

For each KTIPL Offer Share : S$6.55 in cash

3.2 No Encumbrances

The KTIPL Offer Shares are to be acquired:

(i) fully paid;

(ii) free from all claims, charges, equities, liens, pledges, and other encumbrances; and

(iii) together with all rights, benefits, entitlements and advantages attached thereto as at theKTIPL Offer Announcement Date and thereafter attaching thereto, including the right to alldividends, rights and other distributions (if any) declared, made or paid thereon on or afterthe KTIPL Offer Announcement Date (including any dividends that may be declared, madeor paid thereon in respect of the financial year ended 31 December 2007).

Without prejudice to the generality of the foregoing, the Revised KTIPL Offer Price has beendetermined on the basis that the KTIPL Offer Shares will be acquired with the right to receive anydividends, other distributions or return of capital that may be declared, made or paid by STC on theKTIPL Offer Shares on or after the KTIPL Offer Announcement Date (“STC Distribution”). In theevent any STC Distribution has been paid by STC to a Shareholder who accepts the KTIPL Offer,the Revised KTIPL Offer Price payable to such accepting Shareholder shall be reduced by anamount which is equal to the STC Distribution paid by STC to such accepting Shareholder.Accordingly, if any STC Distribution is declared, made or paid by STC on or after the KTIPL OfferAnnouncement Date and the settlement date in respect of the KTIPL Offer Shares acceptedpursuant to the Revised KTIPL Offer falls after the books closure date for the determination ofentitlements to the STC Distribution, the amount of the STC Distribution in respect of such KTIPLOffer Shares will be deducted from the Revised KTIPL Offer Price payable for such KTIPL OfferShares, as KTIPL will not receive the STC Distribution in respect of those KTIPL Offer Shares fromSTC.

22

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

3.3 Conditions of the Revised KTIPL Offer

In the KTIPL Offer Document, it was stated that the KTIPL Offer will be conditional upon KTIPLhaving received, by the close of the KTIPL Offer, valid acceptances in respect of such number ofKTIPL Offer Shares which, when taken together with the Shares owned or agreed to be acquiredby KTIPL and parties acting in concert with it (either before or during the KTIPL Offer and pursuantto the KTIPL Offer or otherwise), will result in KTIPL and parties acting in concert with it, includingsuch relevant persons, holding such number of Shares carrying more than 50 per cent. of thevoting rights attributable to the issued Shares in the capital of STC as at the close of the KTIPLOffer.

The KTIPL Offer will be unconditional in all other respects.

3.4 Closing Date of the Revised KTIPL Offer

Shareholders should note that the Revised KTIPL Offer will close at 5.30 p.m. on 13 March2008 or such later date(s) as may be announced from time to time by or on behalf of KTIPL.

3.5 Information on KTIPL

KTIPL is a private company limited by shares and was incorporated in Singapore on 13 October2000. Its principal activities are those of an investment holding company. As at the KTIPL OfferAnnouncement Date, KTIPL has an issued and paid-up ordinary share capital of S$20,000,000comprising 20,000,000 ordinary shares, all of which are held by Lee Latex. KTIPL is a directwholly-owned subsidiary of Lee Latex. As at the KTIPL Offer Announcement Date, the directors ofKTIPL are Messrs Huang Thiay Sherng and Tan Khiam Hock.

Lee Latex is a company incorporated in Singapore on 10 June 1947. Its principal activity is that ofinvestment holding. As at the KTIPL Offer Announcement Date, Lee Latex has an issued and paid-up share capital of S$30,000,000 comprising 30,000 ordinary shares. As at the KTIPL OfferAnnouncement Date, the directors of Lee Latex are Messrs Lee Seng Wee, Lee Seng Gee, LeeSeng Tee, Lee Yuen-Shih, Lee Han-Shih (alternate to Lee Seng Gee), Lee Shih Hua (alternate toLee Seng Tee) and Huang Thiay Sherng.

3.6 Rationale for the KTIPL Offer and KTIPL’s Future Plans for STC

The full text of the rationale for the KTIPL Offer and KTIPL’s future plans for STC are stated inSection 5 of the KTIPL Offer Document. Excerpts of the relevant sections are reproduced in italicsbelow.

“The Lee Family has had shareholding interests in STC for many years. The Offeror (together withthe GEH Group and the OCBC Group) has effective control of STC as they control the largestsingle block of Shares. The Offer is being made in response to the Cairns Offer with the objectiveof maintaining or consolidating effective control of STC.”

“It is the intention of the Offeror that STC will continue to develop and grow its existing businesses.Depending on the outcome of the Offer and the resultant shareholding of the Offeror in STCfollowing the close of the Offer, the Offeror (if appropriate together with its Concert Parties) intendsto seek representation on the board of directors of STC.

In addition, after the close of the Offer, if the Offeror (together with the GEH Group and the OCBCGroup) continues to control the largest single block of Shares, the Offeror intends to propose toSTC to engage a financial adviser to conduct a study on the financial performance of STC and torecommend possible steps to take to further unlock value in STC for the benefit of Shareholders. Inthis connection, the Offeror supports the policy of the STC board as stated on page 83 of STC’scircular to Shareholders dated 3 February 2008 in relation to the Cairns Offer, which is reproducedas follows:

23

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

“With a clear focus on shareholders’ value, the Group will continue to review its business strategyand prioritise the allocation of funds to enhance shareholders’ value and to generate higher returnto shareholders in the long term”.

Save as disclosed above, the Offeror has no immediate plans for any major changes relating to theexisting business of the STC Group (including redeployment of fixed assets) or the employment ofthe existing employees of the STC Group, other than in the ordinary course of business.”

The KTIPL Offer Document also sets out the intentions of KTIPL in relation to the listing status ofthe Company as follows:

“It is the present intention of the Offeror to maintain the listing status of STC on the SGX-ST.However, in the event SGX-ST suspends the listing of the Shares on the SGX-ST in the abovecircumstances or in the event that the Offeror receives acceptances in respect of not less than 90%of the Offer Shares (other than those already held by the Offeror, its related corporations or theirrespective nominees as at the date of the Offer and excluding Shares held as treasury shares), theOfferor will reassess its position in respect of its shareholdings in STC.”

Based on the above, we would like to draw your attention to the following:

(i) The Lee Family has had shareholding interests in STC for many years. KTIPL (togetherwith GEH Group and the OCBC Group) has effective control of STC as they control thelargest single block of Shares. As at the Latest Practicable Date, KTIPL and its concertparties own, control or have agreed to acquire an aggregate of 108,927,956 Shares,representing approximately 33.4 per cent. of the total number of issued Shares.

(ii) KTIPL has stated its intention that STC will continue to develop and grow its existingbusinesses. However, KTIPL has also stated its intention to seek representation on theboard of directors of STC depending on the outcome of the Offer and the resultantshareholding of KTIPL and its concert parties in STC following the close of the RevisedKTIPL Offer.

(iii) KTIPL has also stated its intention, if it (together with the GEH Group and the OCBCGroup) continues to control the largest single block of Shares, to propose to STC to engagea financial adviser to conduct a study on the financial performance of the Company and torecommend possible steps to take to further unlock value in STC for the benefit ofShareholders. OCBC has also in its announcement dated 15 February 2008 stated that itintends to, if it together with the GEH Group and the Lee Family Companies continue tohave effective control of the Company, make a formal request to the board of the Companyto appoint, after the close of the offer, a financial adviser to conduct a study and makerecommendations to the Company’s board on possible ways to unlock value and enhanceShareholders’ value.

(iv) KTIPL has stated that it is its present intention to maintain the listing status of the Companyon the SGX-ST. However, in the event that free float falls below 10 per cent. and trading inthe Shares is suspended or in the event that KTIPL is entitled to exercise the right ofcompulsory acquisition pursuant to Section 215(1) of the Act, KTIPL will reassess itsposition in respect of its shareholdings in the Company. Accordingly, there is no assurancethat KTIPL will preserve the listing status of the Company on the SGX-ST if free float isless than 10 per cent. or that it will not exercise the right of compulsory acquisition underSection 215(1) of the Act.

24

LETTER FROM CIMB-GK TO THE INDEPENDENT DIRECTORS OF THE STRAITS TRADING COMPANY LIMITED

4. THE FINAL TCPL OFFER

Shareholders should by now have received a copy of the TCPL Offer Document dated 25 January2008 and the Final TCPL Offer Letter dated 18 February 2008 issued by SCB, for and on behalf ofTCPL.

According to the Second Price Revision Announcement on the TCPL Offer, save as disclosed inthe Second Price Revision Announcement on the TCPL Offer, all the other terms and conditions ofthe TCPL Offer as set out in the TCPL Offer Document remain unchanged.

4.1 Final TCPL Offer Price

For and on behalf of TCPL, SCB is making the Final TCPL Offer to acquire all the TCPL OfferShares on the following basis:

For each TCPL Offer Share : S$6.70 in cash

It is stated in the Second Price Revision Announcement on the TCPL Offer that TCPL does notintend to further revise the Final TCPL Offer Price.

4.2 No Encumbrances

The TCPL Offer Shares are to be acquired:

(i) fully paid;

(ii) free from all liens, equities, mortgages, charges, encumbrances, rights of pre-emption andother third party rights and interests of any nature whatsoever; and