Embed Size (px)

Citation preview

The Spitzer Inquiries

AASCIF

Policyholder Services & Law Committee Conference

October 3-4, 2005

Kiawah Island, South Carolina

Presented by: Curtis Larsen, Montana State FundPresented by: Curtis Larsen, Montana State Fund Cora Butler, Missouri Employers’ MutualCora Butler, Missouri Employers’ Mutual Stephen Marks, Kentucky Employers’ MutualStephen Marks, Kentucky Employers’ Mutual

TOPICS

Distribution Methods Compensation MethodsSpitzer’s Inquiry and ResultsOther Inquiries and ResultsIndustry ResponsesLegislative Responses

INSURANCE DISTRIBUTION AND COMPENSATION

METHODS

Presented by: Steve Marks, Kentucky Employers’ Mutual Insurance Company

INSURANCE DISTRIBUTION METHODS

Independent Agency System

Independent contractors free to represent multiple insurance companies Independent Agent

• Represent multiple unrelated insurance companies. The agent decides which company to recommend for a specific client

• Agent of the insurance companies

• Own the expirations and can switch business among insurers they represent

• Compensated by insurance companies

INSURANCE DISTRIBUTION METHODS

Managing General Agents (MGA’s)

Wholesale insurance intermediary that stands between the insurer and agents who sell directly to the consumer

Provide underwriting and administrative services on behalf of the insurer they represent

Exact duties vary depending upon the contracts with the insurers they represent

Compensated by insurance companies

INSURANCE DISTRIBUTION METHODS

Brokers Work on behalf of the insurance buyer to identify

their insurance needs and find an insurance company that will meet their needs Insurance Brokers

• Closely resemble Independent Agents, place insurance with many different companies

• Agent of the insurance buyer

• Own the expirations and can switch business among insurers

• Compensated by insurance buyer and sometimes by insurance companies

INSURANCE DISTRIBUTION METHODS

Excess and Surplus Lines Brokers

Resemble MGA’s in that they usually do business primarily with other brokers and agents and not directly with consumers

Surplus lines brokers are specially licensed by the state to place business with insurers not licensed by that state

INSURANCE DISTRIBUTION METHODS

Exclusive Agency SystemIndependent contractors restricted by contract

to represent a single insurance company or group of insurance companies under similar management

• Agent of the insurance company

• Ownership of expiration is usually retained by insurance company. Limited ownership may exist while contract is in force but agent does not have the option of selling the expiration to anyone other than the insurer

• Compensated by insurance company

INSURANCE DISTRIBUTION METHODS

Direct Writer System/Direct Response System

Sales agents are employees of the insurance companies they represent • Services offered to prospective policyholders by mass

media, internet, telephone, mail, and face-to-face contact

• Represent a single insurance company or group of insurance companies

• Ownership of expirations is retained by the insurance company

• Compensated by the insurance company

INSURANCE DISTRIBUTION METHODS

Combination Systems

Mixed system consisting of two or more distribution methods

Compensation Methods

Fixed Commission

A fixed percentage of premiums

• Agent’s primary source of compensation • Varies by company and line of business• May be different for new and renewal

business

Compensation Methods

Variable Commission

Additional commission that may be paid by the insurance company to the agent or broker based on established factors such as volume and quality of business. Variable commission is sometimes also called contingent commission, profit-sharing commission, bonus commission, or steering commission.

Compensation Methods

Types of Variable Commission

Contingent Commission/Bonus Commission

A commission that will be paid to an agent or broker contingent upon specific characteristics of their book of business with a carrier

• The most common factors used in determining are total premium volume, increase in premium volume over a set period of time, and profitability

Compensation Methods

Profit Sharing Commission A commission that will be paid to an agent or broker

contingent upon a carrier’s profitability and the profitability of the agent or broker’s book of business with a carrier

• The carrier may require a minimum premium volume before an agent or broker is eligible

Compensation Methods

Steering Commission A commission that will be paid to an agent or broker

based on an increase in the volume of business that agent or broker places with a carrier

• Retention of current policyholders and total premium volume with a carrier may be factors in determining eligibility and commission percentage

Compensation Methods

Gifts/Prizes Similar to variable commissions except items of

value are substituted in place of monetary compensation. Trips are a common form of gifts

• The most common factors used in determining are increase in premium volume over a set period of time, total premium volume, and profitability

Compensation Methods

Fees

Payment made by the insurance buyer to a broker to identify insurance needs and find an insurance company that will meet their needs

Compensation Methods

Salary

Fixed compensation for services, paid to a person on a regular basis

Compensation Methods

Bonuses

Similar to variable commission for those being compensated by salary

• Increase in premium volume over a set period of time and profitability may be factors in determining eligibility

Compensation Methods

Other Forms of Compensation

Forgivable or reduced interest loans

Advertising

Favorable term lease agreements

Use of hardware and software

Compensation by Distribution Methods

Independent Agency System

Fixed Commission

Variable Commission (contingent commission, bonus commission, or profit sharing commission)

Gifts

Compensation by Distribution Methods

Brokers

Fees

Variable Commission (contingent commission, bonus commission, or profit sharing commission)

Gifts

Compensation by Distribution Methods

Exclusive Agency System

Fixed Commission

Variable Commission (contingent commission, bonus commission, or profit sharing commission)

Salary

Gifts

Compensation by Distribution Methods

Direct Writer System/Direct Response System

Salary

Bonus

Gifts

RECENT LEGAL ACTIONS INVOLVING AGENTS AND

BROKERS:

Presented by: Curtis Larsen, Montana State Fund

INVESTIGATIONS AND CHARGES BY NEW YORK ATTORNEY GENERAL

Involve large brokers (not agents) with big market clout – Marsh, Aon, Willis

Brokers received fees from many sources, including customers, carriers and reinsurers

MARSH’S ARRANGEMENTS WITH CUSTOMERS AND CARRIERS

Placement Service Agreements (“PSAs”) and Market Service Agreements (“MSAs”) with carriers

Received fee from customer and commissions from carrier

Elements of contingent commission

•Growth

•Retention

•Profitability

ELEMENTS OF CHARGES

Bid-rigging – obtaining phony quotes (artificially high) from carriers to justify placements with other carriers

Steering – placing customers’ insurance coverage with preferred carriers

Tying – combining retail placements with reinsurance

Contingent Commissions – undisclosed profit or volume-related commissions or fees from carriers

Conflicts of Interest – Brokers purportedly placing their own financial interests above customers’ interests: Placing business with carrier that offered best contingent commissions

Related Party Transactions

•Brokers’ creation of and investment in off-shore carriers

•Steering business to these related companies

SUMMARY OF QUESTIONED PRACTICESPractice Pro/Con Comment

Contingent Commissions

Benefits of Practice(industry supporters)

Encourage good risk management prior to underwriting (profit-related commissions). Support long-term relationships between brokers, clients and insurers

Form of Alleged Abuse (industry critics)

Bid-rigging. Failure to seek/obtain best terms for client

Scale of Abuse(industry supporters)

The action of a few individuals within a few firms; not systemic

Scale of Alleged Abuse(industry critics)

Very widespread and influential: “these hidden payments drive the insurance business as a whole” (Spitzer Senate testimony)

Source: Conning Research & Consulting, Inc., Prospects for Agents and Brokers (2005), p.25

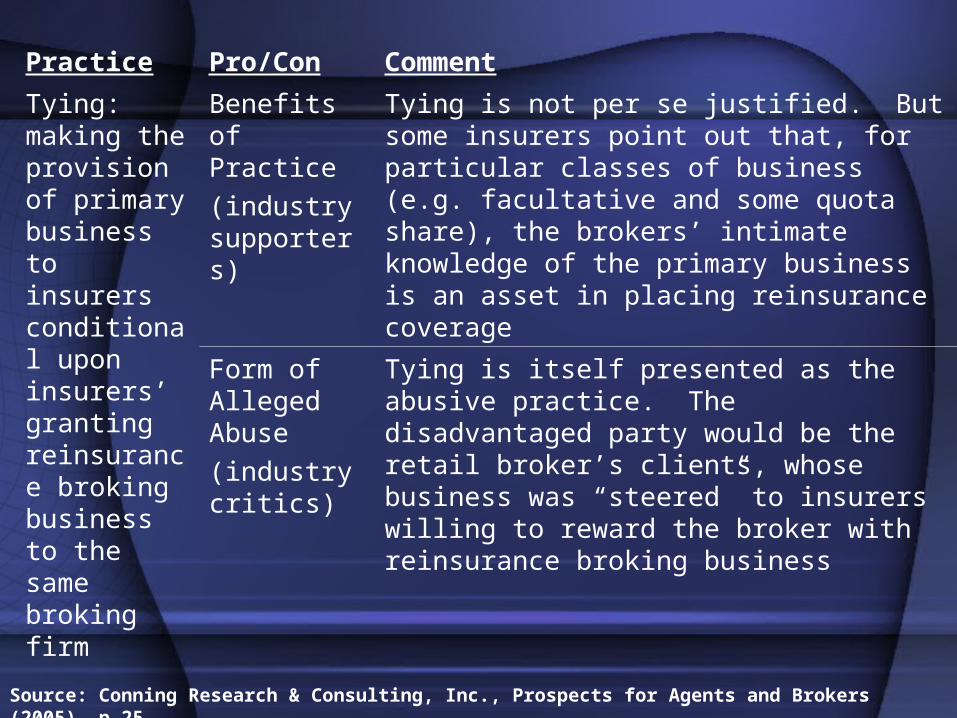

Practice Pro/Con Comment

Tying: making the provision of primary business to insurers conditional upon insurers’ granting reinsurance broking business to the same broking firm

Benefits of Practice(industry supporters)

Tying is not per se justified. But some insurers point out that, for particular classes of business (e.g. facultative and some quota share), the brokers’ intimate knowledge of the primary business is an asset in placing reinsurance coverage

Form of Alleged Abuse (industry critics)

Tying is itself presented as the abusive practice. The disadvantaged party would be the retail broker’s clients, whose business was “steered” to insurers willing to reward the broker with reinsurance broking business

Source: Conning Research & Consulting, Inc., Prospects for Agents and Brokers (2005), p.25

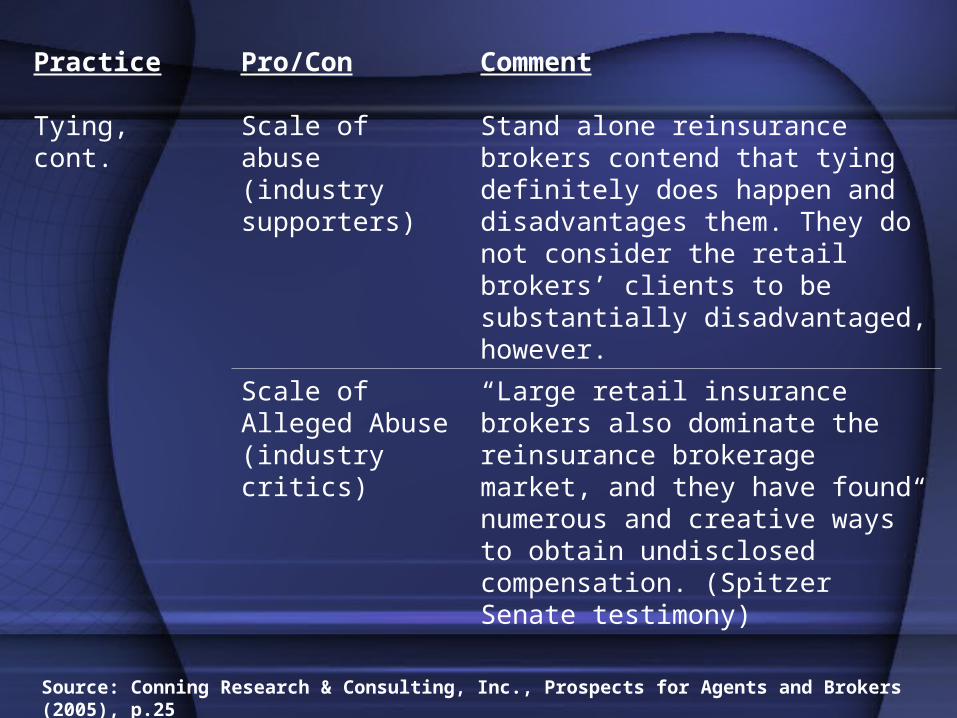

Practice Pro/Con Comment

Tying, cont. Scale of abuse (industry supporters)

Stand alone reinsurance brokers contend that tying definitely does happen and disadvantages them. They do not consider the retail brokers’ clients to be substantially disadvantaged, however.

Scale of Alleged Abuse (industry critics)

“Large retail insurance brokers also dominate the reinsurance brokerage market, and they have found numerous and creative ways” to obtain undisclosed compensation. (Spitzer Senate testimony)

Source: Conning Research & Consulting, Inc., Prospects for Agents and Brokers (2005), p.25

Practice Pro/Con Comment

Broker investments in insurance companies

Benefits of Practice (industry supporters)

Creation of new insurance capacity at times of acute capacity shortage. Marsh in particular played a major role in the creation of the Bermuda market in this way

Form of Alleged Abuse (industry critics)

Related-party transactions, under which business is steered to insurance companies in which brokers have invested, in preference to other insurers

Scale of Abuse (industry supporters)

Not regarded as significant. The companies offer fresh capacity for lines hard to place elsewhere. Unlikely therefore that broker favoritism disadvantaged clients

Scale of Alleged Abuse (industry critics)

Not specified but “huge transfer of insurance capital and underwriting activity” offshore is cited, and brokers are said to either own in part or operate “many of these offshore entities.” (Spitzer Senate testimony)

Source: Conning Research & Consulting, Inc., Prospects for Agents and Brokers (2005), p.25

Insured Primary Insurer

Primary Broker Reinsurance Broker

Reinsurer

1

2 3 4

1 Contingent commissions paid by insurer

2 Reinsurance brokerage obtained through “tying” of direct and reinsurance business

3 Contingent commissions paid by reinsurer

4 Return on broker’s ownership stake in reinsurerPremiums

Commissions

Potential Undisclosed Broker Income Streams Identified by Eliot Spitzer

Conning Research & Consulting, Inc., Prospects for Agents and Brokers (2005), p.16

SPITZER’S RESULTSMarsh

Agreed to refunds of $850 million

Gave up contingent commissions ($800 million/year)

Criminal charges and guilty pleas - both Marsh and carrier employees who engaged in bid-rigging

Management Changes

Aon

Agreed to refunds of $190 million

Willis

Agreed to give up contingent commissions

Agreed to refunds of $51 million

Others – e.g., Gallagher: $27 million – Ill. AG; Hilb, Royal & Hobbs Co.: $30 million – Conn. AG

ONGOING INVESTIGATIONS AND ACTIONS

Criminal charges pending against broker and carrier employees

At least 16 guilty pleas from broker and carrier employees

Eight former Marsh execs indicted by Spitzer in September

NAIC’s multi-state regulatory agreement with Marsh

OTHER STATE INVESTIGATIONS

•CaliforniaAG Investigations

Commissioner Garamendi v. Universal Life Resources

•ConnecticutSubpoena to at least 42 carriers and brokers

Spitzer-style lawsuit by AG against Marsh

•Other States’ InvestigationsAlabama, D.C., Florida, Georgia, Illinois, Massachusetts, Minnesota, New Jersey, North Carolina, Ohio and Oregon

•Letters of Inquiry to Carriers and Brokers

PRIVATE LITIGATION

•CaliforniaIn Re Insurance Broker Commission Litigation

Alleging contingent commissions illegal

RICO lawsuit

•FloridaSmall business lawsuit against 20 insurers

•MassachusettsClass action a la Spitzer complaint against Marsh and insurers

•More private litigation to come(?)

DELIVERY OF INSURANCE PRODUCT (OR SERVICE)

Independent Agents•Work for several carriers

•Agent of the carrier, not the policyholder

•Actions and knowledge of Agent imputed to carrier

•Do policyholders understand that the insurance agent is agent of the carrier?

•Could agent be agent of both carrier and customer?

•Commissions paid by carrier

•Written appointment agreement with carrier (or not)

DELIVERY OF INSURANCE PRODUCT (OR SERVICE)

(Continued)• Brokers

Retained and paid by the customer (maybe)Broker is agent of the customer, not the carrierCompensation may come from both the customer

and the carrier – commission or fee.

• Producers In some states’ licensing laws, both brokers and

agents may be termed producersNAIC’s Model “Producer” Licensing Act –

comprehensive licensing scheme that blurs the line between agents and brokers

DUTIES OF AGENTS-BROKERS

Tension between servicing customer and financial interests of broker or agent

Agent may be in a conflict situation

May be agent of both under some circumstances

May owe duties to both customer and carrier

3 Couch on Insurance 3d, Chapter 45 (1997)

Deonier & Associates v. The Paul Revere Life Ins. Co., 9 P.3d 622 (Mont.2000)

DUTIES OF AGENTS-BROKERS (continued)Quote from Testimony of Gregory Serio, New York

Superintendent of Insurance to New York State Assembly Standing Committee on Insurance:

“The principle of uberrimae fidei and its translation, “of the utmost good faith,” has long been used to characterize the core duty accompanying an insurance contract. Encompassed within this duty is a basic obligation on insureds to deal with insurers openly and honestly. The industry depends on this principle to ensure that a consumer discloses all material facts about risk of loss and failure to do so, either through misrepresentation or concealment of material facts, generally renders an insurance contract voidable under New York law. Material facts are those that had they been revealed by the consumer would have either prevented the insurer from issuing a policy or prompted the insurer to issue such policy at a higher premium. This same duty of dealing fairly and honestly, with full disclosure, is also owed by the industry to its clients. Would consumers have accepted the insurance contract, at the price paid, had they been fully informed about the material facts pertaining to producer compensation arrangements that may have influenced the recommendation for placement? It is highly unlikely that a consumer would have accepted any placement where such placement was driven by any factor other than the best interests of the customer.

State statutory licensing standards: Montana, for example

•33-17-1001. Suspension, revocation, or refusal of license. (1) The commissioner may suspend, revoke, refuse to renew, or refuse to issue an insurance producer's license, adjuster license, or consultant license, may levy a civil penalty in accordance with 33-1-317, or may choose any combination of actions when an insurance producer, adjuster, consultant, or applicant for those licenses has: ….

(f) in the conduct of the affairs under the license, used fraudulent, coercive, or dishonest practices or the licensee or applicant is incompetent, untrustworthy, financially irresponsible, or a source of injury and loss to the public; (g) misrepresented the terms of an actual or proposed insurance contract or application for insurance; (h) been found guilty of an unfair trade practice or fraud prohibited by Title 33, chapter 18;

•Unfair trade practicesMisrepresentation of benefits, advantages, conditions or terms of insurance policy (MCA § 33-18-202)

Twisting – misrepresentation or incomplete comparison of terms, conditions or benefits contained in a policy

•Other legal dutiesGood faith and fair dealing

Fiduciary duties (trust relationship): a fiduciary cannot place its own interests ahead of those with whom the fiduciary holds a special relationship

Brokers or agents may have fiduciary duties. See e.g. MCA, 33-17-1102 (Producer is a fiduciary re premium)

Attempts to expand fiduciary duties are of great concern to the industry

BROKERS-AGENTS DUTIES/IMPLICATIONS FOR CARRIERS

Producer should not place business merely with carrier that provides best compensation package

Best value for customer

•Not always the lowest price

•Value of long-term relationship

How does producer show it has produced best value for customer?

OTHER AGENT COMPENSATION ISSUESNegotiating commissions

Unfair discrimination or rebating 33-18-210. Unfair discrimination and rebates prohibited -- property, casualty, and surety insurances. (1) A title, property, casualty, or surety insurer or an employee, representative, or insurance producer of an insurer may not, as an inducement to purchase insurance or after insurance has been effected, pay, allow, or give or offer to pay, allow, or give, directly or indirectly, a: (a) rebate, discount, abatement, credit, or reduction of the premium named in the insurance policy; (b) special favor or advantage in the dividends or other benefits to accrue on the policy; or (c) valuable consideration or inducement not specified in the policy, except to the extent provided for in an applicable filing with the commissioner as provided by law

(2) An insured named in a policy or an employee of the insured may not knowingly receive or accept, directly or indirectly, a: (a) rebate, discount, abatement, credit, or reduction of premium; (b) special favor or advantage; or (c) valuable consideration or inducement (3) An insurer may not make or permit unfair discrimination in the premium or rates charged for insurance, in the dividends or other benefits payable on insurance, or in any other of the terms and conditions of the insurance either between insureds or property having like insuring or risk characteristics or between insureds because of race, color, creed, religion, or national origin

MCA 33-18-210 continued

Net pricing – Rebating problem

Commission not included in premium calculations for the policy. Each producer working with a State Fund policyholder would then be required to negotiate and receive a fee or commission directly from the policyholder, or

Producers would add on their commission to State Fund net of commission quote-- commonly known as a negotiated commission price.

CONSEQUENCES FOR PARTIES TO INSURANCE CONTRACTAgents

•Greater transparency/disclosure to customers

•Decline of incentive plans

•Greater cost of doing business

•Pressure to shop around for customer

Customers

•More informed

•Perhaps higher prices

Carriers

•More churning of business (?)

•Lower costs in commissions

More regulation

THE INSURANCE INDUSTRY AND REGULATORS RESPOND

Presented by: Cora Butler, Missouri Employers Mutual Insurance Company

The Council of Insurance Agents & Brokers (CIAB)

Recommendations Made By CIAB to the President of the

National Association of Insurance Commissioners:

• Transparency and Disclosure Prior disclosure of contingent compensation arrangements

where advice is offered by producer directly to a client

• Coordination of State Inquiries Uniform and coordinated inquiries by state regulators

• Recognition of Legitimate Compensation Practices

Proper and legal method of compensating brokers for additional services provided by brokers to carrier

• Uniformity Commercial insurance is a national (and global business)

making uniformity crucial to carriers

Industry Response

Independent Insurance Agents&Brokers of America (IIABA)

• “I don’t think the consuming public has a problem with the way we are compensated” Thomas Grau, President of IIABA speaking at the annual conference September 2005

Incentive-based fees paid to brokers did not lead to bid-rigging and price-fixing

Allegations of kickbacks and steering of insurance contracts in return for profitable contingent commissions have proven to be isolated circumstances

IIABA (Big “I”), contd.

• Big “I” Board Adopts Policy on Insurance Company Disclosure“. . . wide range of divergent company requirements would disrupt the way in

which agents and brokers do business . . .” Robert Rusbuldt, IIABA CEO

• Recommendations For Insurer Disclosure Notifications:

Insurance policy was placed by independent insurance agent not an employee of the company

Company believes the use of independent insurance agents and brokers is an efficient and effective way to distribute its policies

Agent or broker placing the policy may receive commission for that placement

If applicable, the agent or broker may be eligible to receive additional compensation

Any questions about the nature of the compensation should be directed to the agent or broker

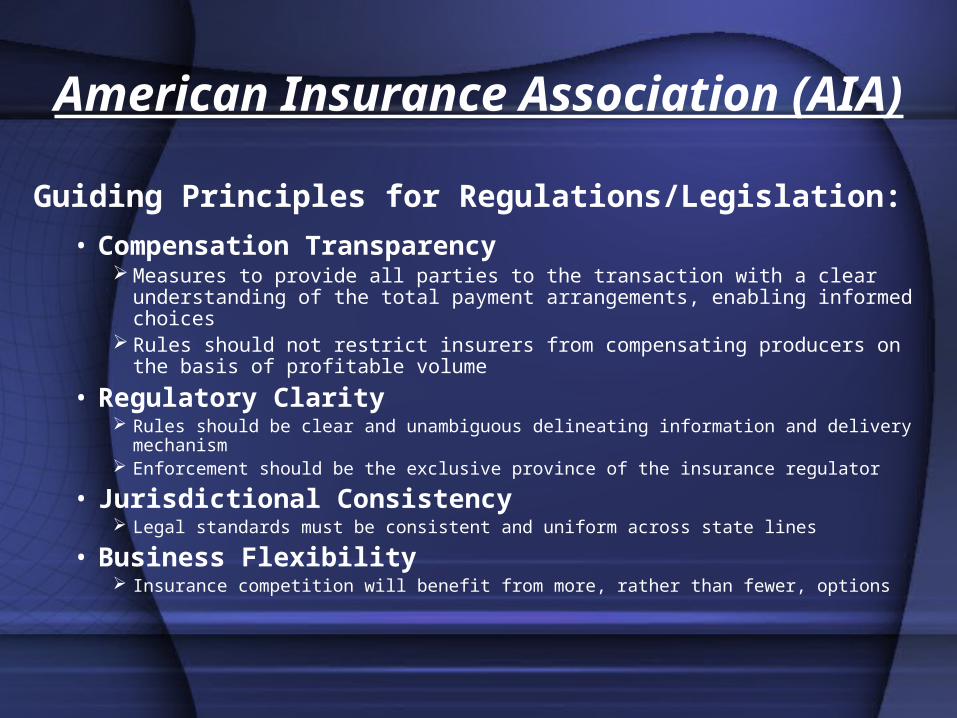

American Insurance Association (AIA)

Guiding Principles for Regulations/Legislation:

• Compensation Transparency Measures to provide all parties to the transaction with a clear

understanding of the total payment arrangements, enabling informed choices

Rules should not restrict insurers from compensating producers on the basis of profitable volume

• Regulatory Clarity Rules should be clear and unambiguous delineating information and delivery

mechanism Enforcement should be the exclusive province of the insurance regulator

• Jurisdictional Consistency Legal standards must be consistent and uniform across state lines

• Business Flexibility Insurance competition will benefit from more, rather than fewer, options

National Regulatory Response

Federal

Department of Labor Advisory Opinion 2005 – 02A

ERISA pension and welfare plans:

• Insurers to disclose all commissions and fees paid to producers whether directly or indirectly attributable to contract

Persistency and profitability bonuses

Prizes and other forms of compensation

Must be disclosed on form 5500, schedule A (insurance information)

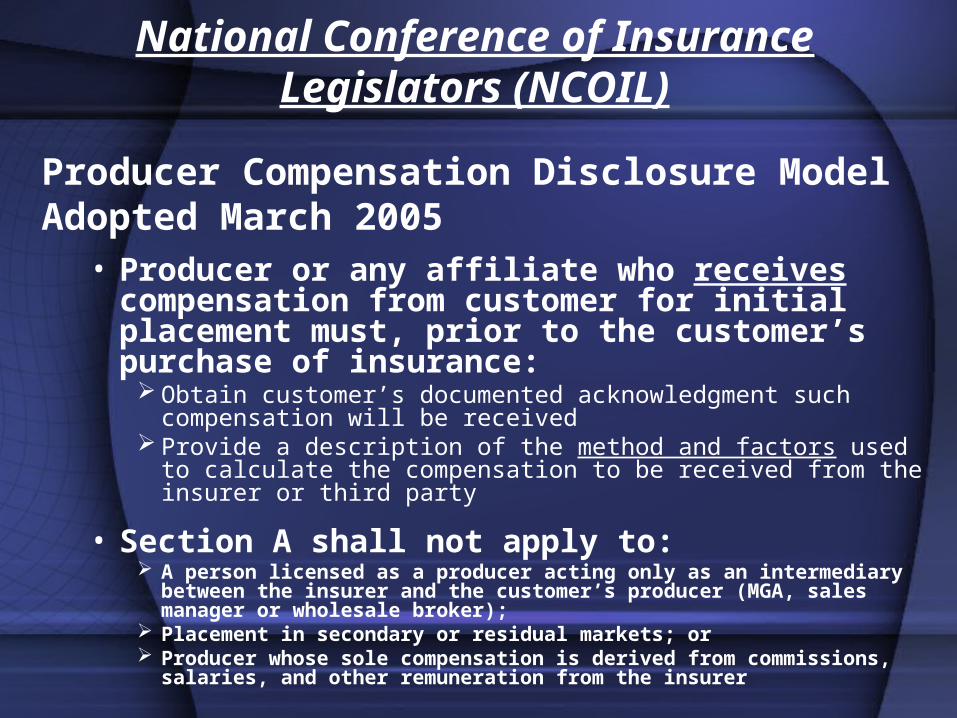

National Conference of Insurance Legislators (NCOIL)

Producer Compensation Disclosure Model Adopted March 2005

• Producer or any affiliate who receives compensation from customer for initial placement must, prior to the customer’s purchase of insurance:

Obtain customer’s documented acknowledgment such compensation will be received

Provide a description of the method and factors used to calculate the compensation to be received from the insurer or third party

• Section A shall not apply to: A person licensed as a producer acting only as an intermediary

between the insurer and the customer’s producer (MGA, sales manager or wholesale broker);

Placement in secondary or residual markets; or Producer whose sole compensation is derived from commissions,

salaries, and other remuneration from the insurer

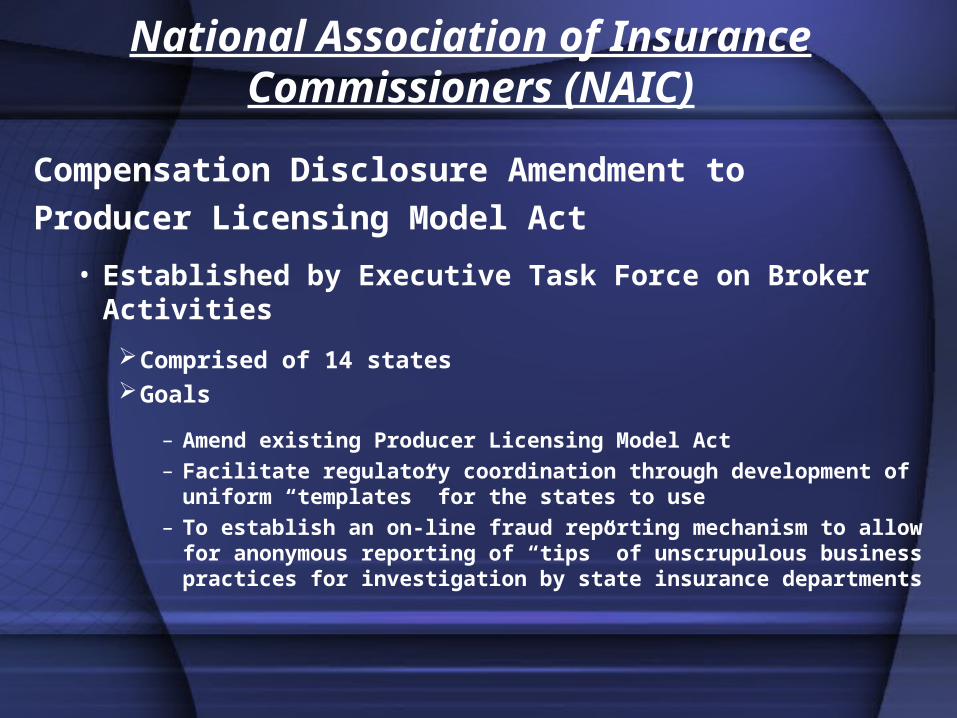

National Association of Insurance Commissioners (NAIC)

Compensation Disclosure Amendment to Producer Licensing Model Act

• Established by Executive Task Force on Broker Activities

Comprised of 14 statesGoals

– Amend existing Producer Licensing Model Act– Facilitate regulatory coordination through development of

uniform “templates” for the states to use– To establish an on-line fraud reporting mechanism to

allow for anonymous reporting of “tips” of unscrupulous business practices for investigation by state insurance departments

NAIC, contd.

Compensation Disclosure Amendment to the Producer Licensing Model Act Adopted December 29, 2004

Subsection A (1)• Any insurance producer or affiliate receives compensation from the customer for the

placement of insurance or represents the customer with respect to placement, shall not accept or receive compensation from insurer or other third party unless, prior to purchase:

Customer’s documented acknowledgment of compensation obtained Amount of compensation from insurer or third party is disclosed to customer If amount unknown the specific method of calculation should be disclosed and, if

possible, a reasonable estimate of the amount

Subsection A (1) not to apply to insurance producer who• Does not receive compensation from customer for the placement; and• In connection with that placement represents an insurer has appointed the producer; and• Discloses to the customer prior to purchase that:

Producer will receive compensation from an insurer in connection with that placement; or

In connection with the placement the producer represents the insurer and that the producer may provide services to the customer for the insurer

NAIC, contd.

Subsection B“Customer” is not

• Participant or beneficiary in employee benefit plan• Covered by group or blanket insurance policy or

group annuity contract sold, solicited or negotiated by the insurance producer or affiliate

Subsection C• Section does not apply to producer who acts only

as an intermediary between insurer and customer’s producer (MGA, sales manager, or wholesale broker; or

• Reinsurance intermediary

NAIC, contd.

• NAIC considers policy renewal to be placement of insurance

Customer is evaluating options in the purchase of insurance

• NAIC does not consider modifications of existing policy to be placement

Customer is not evaluating options in the purchase of insurance

NAIC, contd.

NAIC producer documentation guidance

• Producer should be able to establish that:

The required information was conveyed to the customer on a specific date

The customer indicated consent regarding the described compensation to be received by the producer or affiliate

– Technology may be employed to document consent

State Regulatory Response

Arkansas

Producer Licensing Model Act Amended to create more transparency for

consumers through better disclosure

•Applies to all producers Source of compensation for placement of insurance

Producer represents insurer and is providing service on behalf of insurer

Disclosure may be made verbally (written preferred)

Where producer compensated by affiliate or third party the source of compensation to be disclosed and the relationship explained

Source: September 2005 Property Casualty Insurers Association of America

California

• Proposed Regulation Producer (agent or broker) to disclose whether producer

will seek quote from one insurer or more than one insurer

Whether acting on behalf of the insurer or the client (accepting a fee from client is conclusively deemed to be acting on behalf of client)

Reveal amount of compensation if the client purchases insurance with any insurer recommended by producer

If compensation cannot be reasonably known at the time of disclosure, may disclose the method of calculation

Source: September 2005 Property Casualty Insurers Association of America

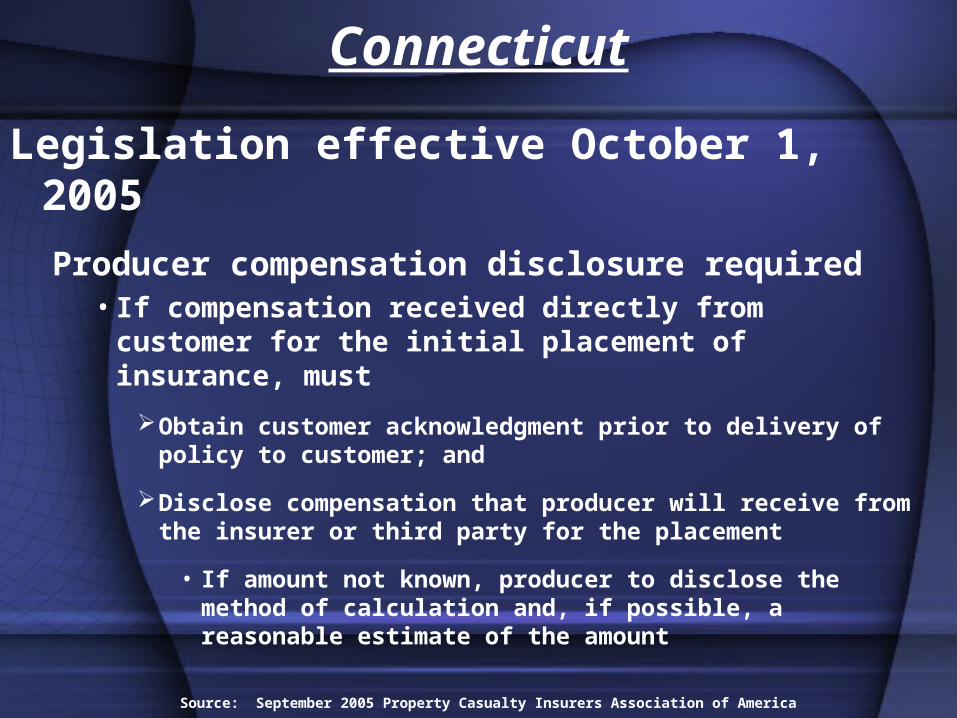

Connecticut

Legislation effective October 1, 2005

Producer compensation disclosure required • If compensation received directly from customer

for the initial placement of insurance, must

Obtain customer acknowledgment prior to delivery of policy to customer; and

Disclose compensation that producer will receive from the insurer or third party for the placement

• If amount not known, producer to disclose the method of calculation and, if possible, a reasonable estimate of the amount

Source: September 2005 Property Casualty Insurers Association of America

North Carolina

Department of Insurance sought changes to NC law based on NAIC Model

•Legislation introduced in the House (Broker Compensation Transparency)

Passed the House but not heard in the Senate

Anticipate additional debate next May

Source: September 2005 Property Casualty Insurers Association of America

Texas

Legislation effective September 1, 2005Amends Texas Insurance Code

• Provides that if agent receives compensation from a customer for the placement or renewal of an insurance product, other than an application fee, service fee or inspection fee, the agent may not accept or receive compensation from insurer or third party, unless prior to customer’s purchase

Agent has obtained customer’s documented acknowledgment that compensation will be received by the agent; and

Provided a description of the method and factors used to compute the compensation to be received from insurer or third party

Source: September 2005 Property Casualty Insurers Association of America

Rhode Island

Legislation effective January 1, 2006Amend the Rhode Island Producer Licensing

Act

• Where insurance producer or affiliate of producer receives compensation from the customer for the placement of insurance, neither the producer or affiliate shall accept or receive compensation from insurer or affiliate of insurer unless prior to customer’s purchase the producer has:

Obtained the customer’s documented acknowledgment that such compensation will be received by the producer or affiliate; and

Provided a description of the method and factors used to calculate the compensation

Source: September 2005 Property Casualty Insurers Association of America

Nevada

Final Regulation Adopted• Applies to brokers only

• Minimal disclosureDisclose all details of compensation and

all quotes

Source: September 2005 Property Casualty Insurers Association of America

Oregon

Final Rule Adopted• Similar to NCOIL Model

Applies to compensated producers no language with regard to representation

Source: September 2005 Property Casualty Insurers of America

New York

• Legislation Introduced (4 Bills)

Producers to avoid excessive self dealing, conflict of interest and excessive compensation

Disclose all compensation and its nature on form developed by Dept. of Ins.

Failure to disclose violation of fiduciary duty Duty to exercise reasonable care

Failure to provide best terms and what could reasonably be believed to be best quote violation of fiduciary duty

Incentive and profit sharing commission permitted if based on profit, volume, growth and retention; such arrangements to be filed annually with the state

Source: September 2005 Property Casualty Insurers of America

Summary

Living in Interesting Times

Living In Interesting Times

• Transparency Is Essential

Hilb Rogal & Hobbs Co. (HRH)• Most recent major brokerage settlement over compensation

practicesConnecticut Attorney General charged unlawful:

Implemented a “carrier consolidation” program designed to steer clients to select group of carriers

Moved blocks of clients to favored insurance carriers Placed clients in “producer captive” insurance carriers of which

HRH owned all or part without disclosing the ownership interest to clients

Entered into undisclosed fee arrangements whereby insurers paid undisclosed compensation to HRH for placement of business

Steered clients to favored insurance carriers to qualify for larger bonuses and contingent commissions

Paid improper premium rebates to clients in return for client retaining HRH as its broker

Provided preferred insurers with first looks on books of business that HRH wished to move to preferred carriers

Living in Interesting Times

Settlement Agreement TermsMonetary Relief

• Thirty Million to be distributed to certain brokerage clients Business Reforms

• Within 60 days of execution of Agreement HRH to undertake reforms related to insurance placements, renewal and servicing when acting as broker:

• HRH acting pursuant to written contract with client can accept

Fee Paid by Client Specified Commission to be Paid by Insurer Where allowed by law, a combination of both

• HRH to Accept No Compensation or Compensation of Any Type, Unless and Until a written Contract Signed by Each Client

Fully Discloses to the Client in Plain, Unambiguous Written Language the Commission or Other Compensation in Either Dollars or Percentage Amounts; and

The Client Consents in Writing

Living In Interesting Times

•HRH Not to Accept or Request, Directly or Indirectly Anything of Material Value From an Insurer Including, but not limited to, money, credit, loans, stock, forgiveness or principal or interest, vacations, prizes, gifts or the payment of employee salaries or expenses except as previously noted

•Contingent Compensation not allowed for brokerage

Contingent upon placing a particular number or dollar value Achieving a particular level of growth in number or dollar value Meeting a particular rate of retention on renewal business Placing or keeping sufficient business to achieve a measure of

profitability (loss ratio or other similar measure) Providing any preferential treatment in the placement process (first or last

looks, rights of first refusal, limiting number of quotes)

Living in Interesting Times

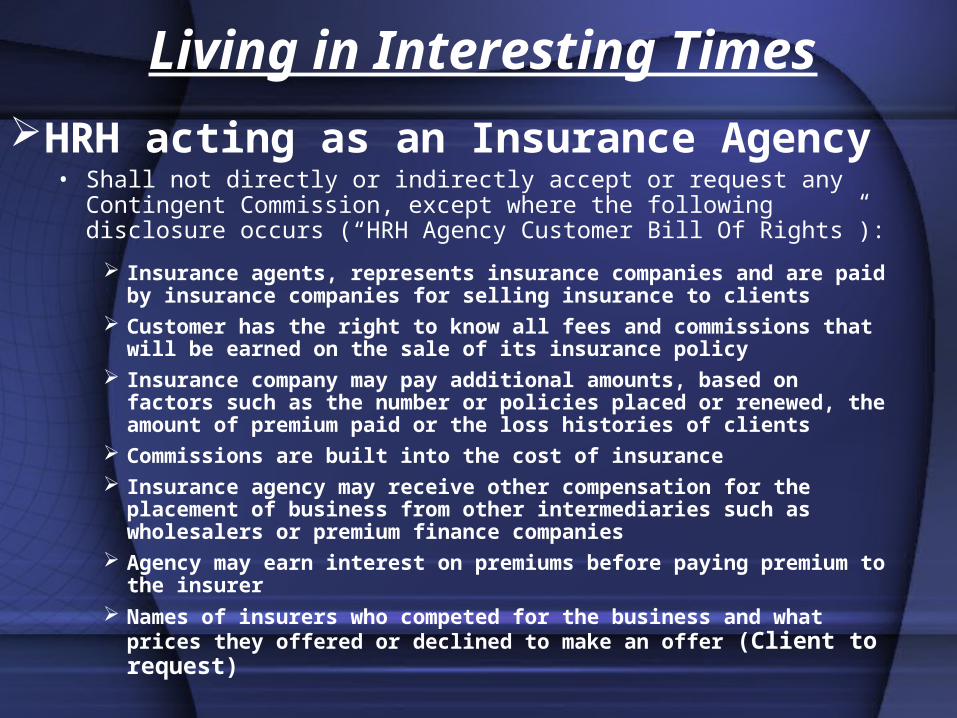

HRH acting as an Insurance Agency• Shall not directly or indirectly accept or request any Contingent

Commission, except where the following disclosure occurs (“HRH Agency Customer Bill Of Rights”):

Insurance agents, represents insurance companies and are paid by insurance companies for selling insurance to clients

Customer has the right to know all fees and commissions that will be earned on the sale of its insurance policy

Insurance company may pay additional amounts, based on factors such as the number or policies placed or renewed, the amount of premium paid or the loss histories of clients

Commissions are built into the cost of insurance Insurance agency may receive other compensation for the placement of

business from other intermediaries such as wholesalers or premium finance companies

Agency may earn interest on premiums before paying premium to the insurer

Names of insurers who competed for the business and what prices they offered or declined to make an offer (Client to request)

Living in Interesting Times

• Reality

Client’s prefer not to pay out of pocket

95% of producer compensation paid by insurer

Flexibility and experimentation in producer compensation may be necessary to achieve business goals

![2006 EAST END BEACH RESTORATION PROJECT KIAWAH … · Coastal Science & Engineering (CSE) March 2011 – Year 4 Annual Monitoring Report [2258] 5. Kiawah Island, South Carolina. The](https://img.pdfslide.us/doc/110x75/5f9ec6937149d12d897451d8/2006-east-end-beach-restoration-project-kiawah-coastal-science-engineering.jpg)

![Policyholder: 1[ABC Company]](https://img.pdfslide.us/doc/110x75/61fb14eb2e268c58cd59ef53/policyholder-1abc-company.jpg)