Embed Size (px)

Citation preview

5th Russia & CIS Petrochemicals Technology Conference & Exhibition25-26 September, 2006, Moscow

Sergey Yaremenko,MRC – Market Report Company

The Russian market of basic polymers:what capacities are essential to satisfy demand?

AgendaAgenda

•• Market is processors!Market is processors!

•• Example Example 1. 1. PVC marketPVC market

•• Example 2Example 2. . PS marketPS market

•• What do we expect from HDPE, LLDPE, PP What do we expect from HDPE, LLDPE, PP markets?markets?

Market is processorsMarket is processors!!

• Oil and naphtha – excellent correlation (prices go simultaneously)

Source: CMAI

• Oil and polymers – good correlation (prices go with short lag)

• Oil and integral margin of polymer production– NO correlation

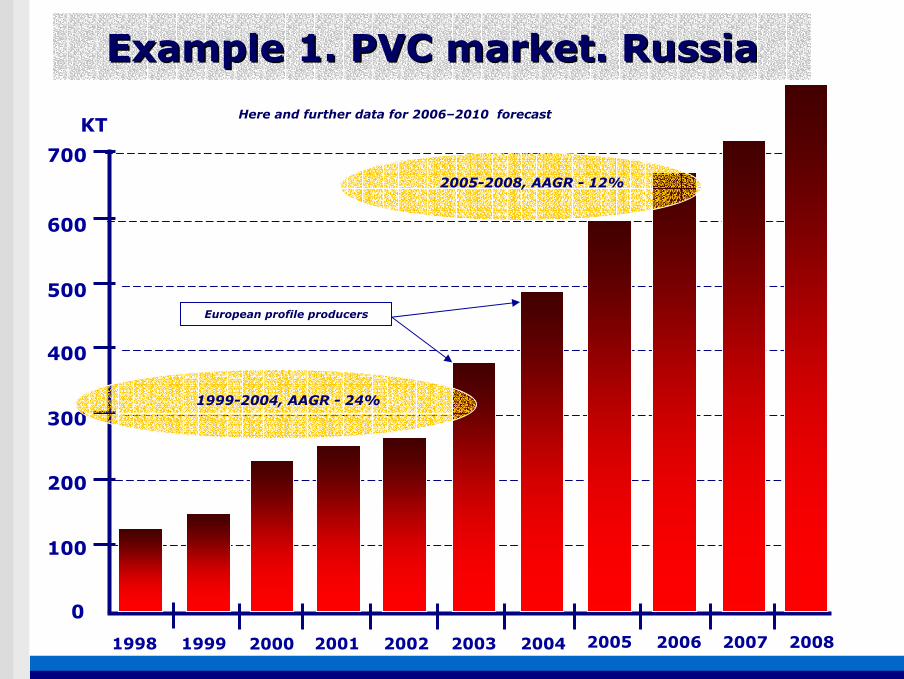

ExampleExample 1. 1. PVC marketPVC market. . RussiaRussia

100

200

300

400

500

600

0

KT

2000 2001 2002 2003 2004 2005 2006 2007 2008

700

1998 1999

1999-2004, AAGR - 24%

2005-2008, AAGR - 12%

European profile producers

Here and further data for 2006–2010 forecast

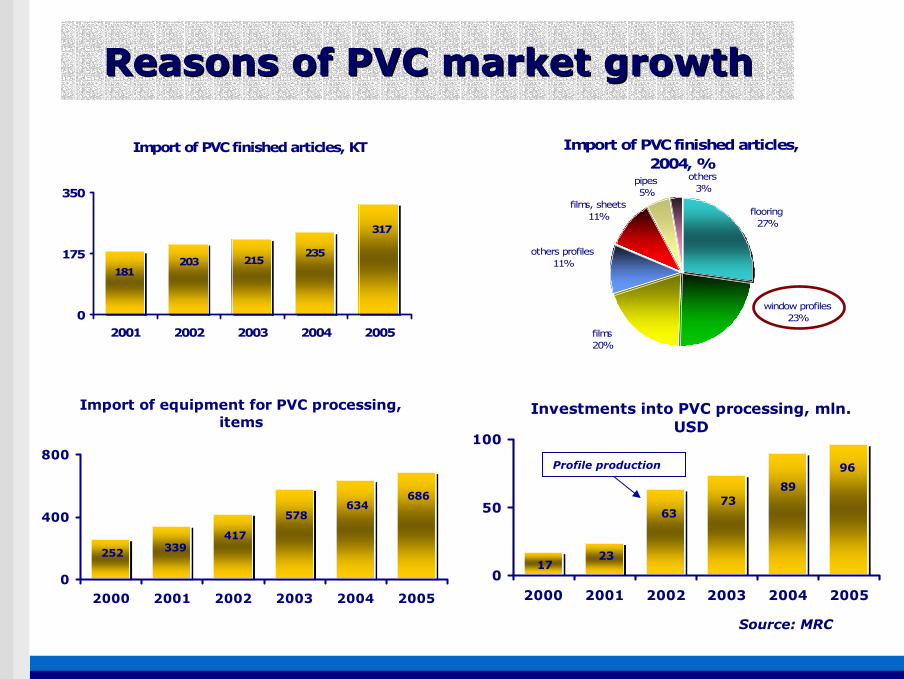

Import of equipment for PVC processing, items

252 339417

686634

578

0

400

800

2000 2001 2002 2003 2004 2005

Investments into PVC processing, mln. USD

89

96

7363

2317

0

50

100

2000 2001 2002 2003 2004 2005

Reasons of PVC market growthReasons of PVC market growth

Import of PVC finished articles, KT

181203 215

235

317

0

175

350

2001 2002 2003 2004 2005

Import of PVC finished articles, 2004, %

flooring27%

films20%

window profiles23%

others profiles11%

films, sheets11%

pipes5%

others3%

Profile production

Source: MRC

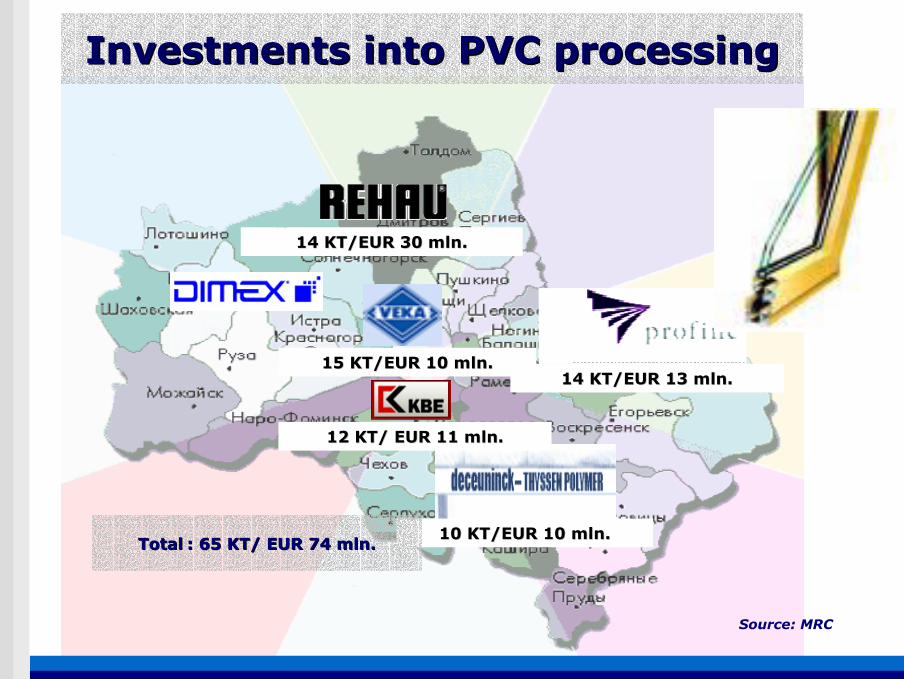

Investments into PVC processingInvestments into PVC processing

14 KT/EUR 30 mln14 KT/EUR 30 mln..

15 KT/EUR 10 mln15 KT/EUR 10 mln..14 KT/EUR 13 mln14 KT/EUR 13 mln..

12 KT/ EUR 11 mln12 KT/ EUR 11 mln..

10 KT/EUR 1010 KT/EUR 10 mlnmln..TotalTotal : 65 KT/ EUR 74 mln: 65 KT/ EUR 74 mln..

Source: MRC

Construction per capita, 2004, m2

2,8

4,2

3,2

1,3

0,6

0,20,3

0

1

2

3

4

5

Poland Hungary CzechRep

Romania Bulgaria Russia Ukraine

PVC consumption per capita, MT

8,0

10,0

7,5

1,8 1,8 2,0

3,4

0

2

4

6

8

10

Poland Hungary CzechRep

Romania Bulgaria Russia Ukraine

Russia and C&EE countriesRussia and C&EE countries

PVC prof iles consumption per 1000 housing, MT

0

4

8

12

16

Poland

Czech R

ep

UK

Lithuania

Ireland

Turkey

Belgium

Slovenia

Latvia

Estonia

Austria

Slovakia

Hungary

Germ

any

France

Russia

Profiles consumption in Europe, 2003

Others21%

UK21%

Poland12%

Russia6%

Germany16%

Turkey11%

Czech Rep3%

France10%

Source: MRC

C&EEC&EE: : PVC consumption, PVC consumption, КТКТ

C&EE 803

Slovakia26

Lithuania15

Estonia3

Ex-Yugoslavia71

Czech Rep55

Poland376

Turkey588

Hungary110

Ukraine61

Bulgaria16 Romania

45

Russia448

Belorus23

0

2

4

6

8

10

12

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Market increase, 99-04,%

PVC per capita, kg

2004: 2004: PVC consumption per capita isPVC consumption per capita is 4,4,66 kgkg

in the worldin the world 5,5,66 kgkg

in Chinain China 44,,4 kg4 kg

in Russiain Russia 3,2 3,2 kgkg

Source: Harriman Chemsult, MRC

Poland462

Hungary116

Czech Rep60

Romania89

Bulgaria19

Ukraine142

Belorus38

Estonia5

43Slovakia Ex-Yugoslavia

55

C&EE1 033

Russia839

Turkey862

Lithuania26

0

3

6

9

12

15

0% 5% 10% 15% 20%

Market increase, 05-10,%

PVC per capita, kg

2010: 2010: PVC consumption per capita PVC consumption per capita -- 6,6,33 kgkg

in the worldin the world 77,,00 kgkg

in Chinain China 66,,77 kgkg

in Western Europein Western Europe 14,5 14,5 kgkg

in Russiain Russia 5,9 5,9 kgkg

Source: Harriman Chemsult, MRC

C&EEC&EE: : PVC consumption, PVC consumption, КТКТ

0

100

200

300

400

500

600

700

800

900

1000

1100

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Domestic PVC Imported PVC Imported goods from PVC

Capacities300 КТ

Bashchim? LUKoil -Neftechem? Sibmanagement? Sibur? + 300 КТ

100 КТ

Additional impulsefor processors

200 КТ

КТ

* PVC capacities utilization in 2005 - 98%

* Current additional margin of PVC producer - 150 USD

Source: MRC

PVCPVC--SS. . Market development till 2012Market development till 2012

PVC-S prices

884

837

767808

894915

875 865840

975 974 973956 963 967 963

920925

695709723

986966949

1230121512201190

700

800

900

1 000

1 100

1 200

1 300

1 400

1 500

Jan.05 Feb.05 Mar.05 Apr.05 May 05 Jun.05 Jul.05 Aug.05 Sep.05 Oct.05 Nov.05 Dec.05 Jan.06 Feb.06

FOB NWE, USD/ MT average ICIS-LOR/ Platts Domestic market, Russia, including duty without VAT, USD/MT

PVC in Russia: shortage timesPVC in Russia: shortage times

+USD 200 !!!

Source: MRC

LDPE consumption and prices

0

200

400

600

800

2000 2001 2002 2003 2004 2005 2006 2007 2008

KT

0

600

1200USD

PS consumption and prices

0

150

300

2000 2001 2002 2003 2004 2005 2006 2007 2008

KT

0

700

1400USD

PP consumption and prices

0

200

400

600

800

2000 2001 2002 2003 2004 2005 2006 2007 2008

KT

0

650

1300USD

HDPE consumption and prices

0

200

400

600

800

2000 2001 2002 2003 2004 2005 2006 2007 2008

KT

0

650

1300

USD

ExampleExample 22. . PS marketPS market

+ USD 41*

* Russia: domestic prices without VAT in 1H2006 compared to prices in Western Europe (CMAI)

** GPPS prices in Russia and Western Europe

+ USD 151*

+ USD 94* - USD 10**

Source: MRC

0

100

200

300

400

500

2002 2003 2004 2005 2006 2007 2008 2009 2010

Domestic PS PS export PS import

Capacities

PS:PS: market development till 20market development till 201010

120 КТ

+100 КТ

60 КТ

КТ

* PS capacities utilization in 2005 - 60%

* PS producers don’t get the additional margin

+50 КТ

Styrovit? + 50 КТ?

Consumption

Salavat? + 70 КТ?

Source: MRC

Import of equipment for PS processing, items

73 89

152

190

165169

0

100

200

2000 2001 2002 2003 2004 2005

Investments into equipment for PS processing, mln. USD

23

3034

21

480

25

50

2000 2001 2002 2003 2004 2005

Investments into PS processingInvestments into PS processing

Investments into PS processing, 2005, %

EPS sheets28%

sheet extrusion

32%

IM11%

films4%

others25%

- Containers: Huhtamaki CIS, Aktiv-Greiner, Оmsk Chemical Company

- New investments into BOPS: Alkopack, Marta

- Market needs freon stable brands (Stinol, Atlant, Nord - 50 КТ)

- EPS/XPS sheets: Penoplex, Dow

Source: MRC

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010

Domestic HDPE HDPE export HDPE import

Capacities

HDPEHDPE: : market development till 20market development till 201010

160 КТ

Kazanorgsyntez + 170 Кт ?

10 КТ

КТ

* HDPE capacities utilization in 2005 - 95%

* Current additional margin of HDPE producers is about 100 USD

SIBUR, Nizhnekamskneftechem + 240 Кт ?

Consumption

Salavat + 120 Кт ?

Source: MRC

0

100

200

300

2002 2003 2004 2005 2006 2007 2008 2009 2010

Domestic LLDPE LLDPE export LLDPE import

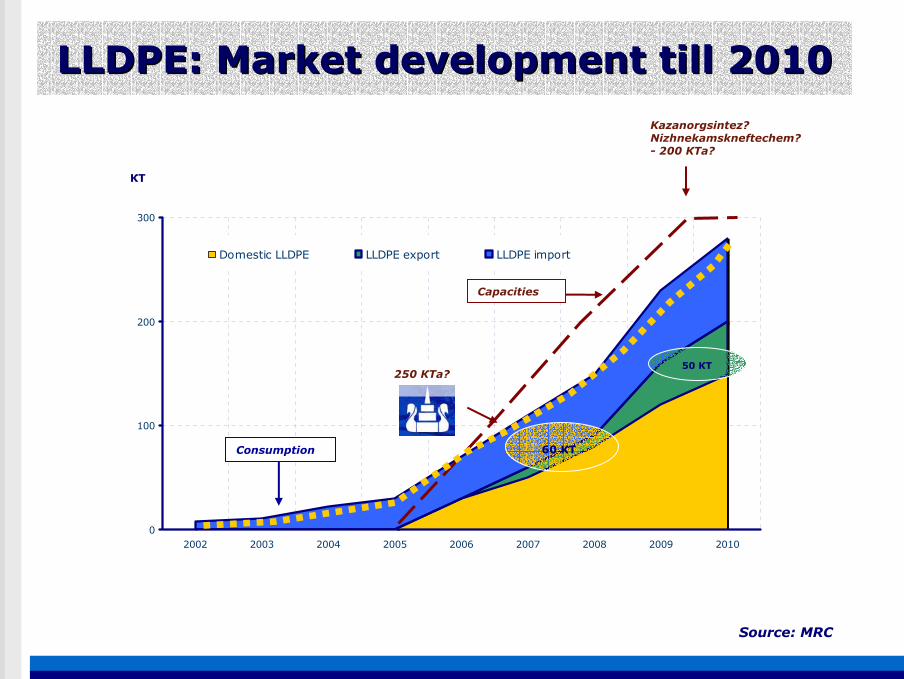

LLDPELLDPE: : Market development till 20Market development till 201010

60 КТ

250 КТа?50 КТ

КТ

Kazanorgsintez? Nizhnekamskneftechem? - 200 КТа?

Consumption

Capacities

Source: MRC

Import of equipment for PE processing, items

280 263

539

305

176172

0

300

600

2000 2001 2002 2003 2004 2005

Investments into equipment for PE processing, mln. USD

35

76

382723

140

50

100

2000 2001 2002 2003 2004 2005

Investments into PE processingInvestments into PE processing

- Pipes: Eurotrubplast (Russia, Ukraine, Belarus), Kazanorgsintez

Investments into PE processing, 2005 , %

Coatings2%

IM16%

EBM13%

Films22%

Pipes24%

Others23%

- LLDPE -Ukraine: Khekro, Vozko, Plastmodern, Ukrplastic, (almost 25 КТ)

- Films: DPО Plastic, Polimer, Uralplastic, Multiflex, stretch – Regent, Papirus

- ЕВМ: WBD (Lianozovskiy МC, Sibirskoe moloko, Plant of children milk products), Suzdalskiy МP, Procter and Gamble Novomoskovsk, Mib-lising

- Pipes: KWH. Who is next? – Pipelife, Wavin, Uponor?

Source: MRC

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010

Domestic PP PP export PP import

Capacities

PPPP: : market development till 20market development till 201010

+180 КТ

60 КТ

КТ

* PP capacities utilization in 2005 - 95% * Additional margin of PP producers is about USD 100

+120 КТ

Titan? Тomsk? Tobolsk? +300 КТ?

Consumption

130 КТ

Source: MRC

Import of equipment for PP processing, items

75 90 65

281

237

750

200

400

2000 2001 2002 2003 2004 2005

Investments into equipment for PP processing, mln. USD

28

105

6101710

0

60

120

2000 2001 2002 2003 2004 2005

Investments into PP processingInvestments into PP processing

Investments into PP processing, 2005 , %

BOPP-films49%

IM15%

Bags, filaments5%

Pipes3%

Sheet extrusion

6%

Other films6%

Others16%

- Ukraine: BOPP-films (Ukrplastic, Chemosvit), IM (Aleana, Atem, Ista, Office-mebel)

- Pipes: Plastikor, Stroypolimer, Plastika-Tyumen, Pereval

- Filaments, bags: Aleko, Chimpack, Isratek, МНМ

- BOPP - films: Novatek, Grinn, Bepack, Roseuroplast, Biaksplen (130 КТ)

- IM: Plastic, AvtoVAZ, Polad, Technoplast, Euromoulding, Berikap

Source: MRC

Sergey Yaremenko, Managing Director, Market Report Company

[email protected]; www.mrcchemical.com

Moscow +7 495 543 91 94; Kiev +38 044 240 82 35

Thank you for your timeThank you for your time!!