Embed Size (px)

Citation preview

n I July 1981 (.,I

Station Bulletin No. 337

THE ROLE OF TRANSPORTATION

IN INTERNATIONAL AGRICULTURAL TRADE

Department of Agricultural Economics Agricultural Experiment Station

Purdue University West Lafayette, Indiana

,

*

THE ROLE OF TRANSPORTATION IN

INTERNATIONAL AGRICULTURAL TRADE

by

* James K. Binkley and Mary E. Revelt

Assistant Professor, Department of Agricultural Economics, Purdue University and Economist, Foreign Agriculture Service, U.S.D.A. This research was partially supported by the U.S.D.A. under contract 801-15-46. The authors wish to thank Robert Boynton, Lance McKinzie, Jerry Sharples, and Robert Thompson for helpful comments.

It is the policy of the Agricultural Experiment Station of Purdue University that all persons shall have equal opportunity and access to Its programs and facilities without regard to race, religion, color, sex or national origin .

SUMMARY

This paper examines the role of ocean transportation in international trade, primarily from the point of view of trade researchers. The basic premise is that there are many situations where transportation cannot be treated as simply a wedge which increases the price of imported and/or exported goods by a constant amount.

The first part of the paper is concerned with providing descriptive information about international shipping markets. Information is provided which shows that transport rates can vary significantly over different routes at a given point in time, and, perhaps of greater importance, can fluctuate greatly over the same route and across routes through time.

The balance of the paper is involved with examining some specific issues wherein factors identified previously are of possible importance. These include international price variability, comparative advantage, international market power, and international trade modeling.

TABLE OF CONTENTS

Introduction. • 0 •

The Ocean Transport Industry.

Cost Factors in Bulk Shipping • U.S. Cargo Preference Laws.

The Quantitative Importance of International Shipping Costs: Macro and Micro Considerations.

Variability in Ocean Freight Rates. The Short Run Supply of Shipping.

Possible Effects of Rate Variability. Price Stabilization and Welfare • . Comparative Advantage and Price Variability . • Market Power in International Grain . . • . Implications of Rate Variability for Trade Modeling

Conclusions .

Bibliography.

LIST OF TABLES

TABLE

1. World Seaborne Grain Trade, Selected Years.

2. World Seaborne Trade, 1964-74 .

PAGE

1

2

4 7

10

15 16

21 21 26 27 28

30

31

PAGE

1

3

3. Liner, Bulk Carrier, and Tanker Exports of U.S. Grain 3

4. Reported Voyage Fixtures for Grain -First Quarter 1975 .....•...

5. Size Distribution of Vessels Employed in the Grain

5

Trade, Various Years. • . • . . . . . 6

6. Comparison of Ship Costs, Grain Trade, New Orleans-Rotterdam, 1977 . . . . . • . . 7

7. Tonnage Shipped in U.S. Vessels Under P.L. 480, and Average Freight Rate Differential 1967-1976 . 8

8. Average Rates to Soviet Black Sea Ports, 1972-76, by Flag of Registry • . • . • • . • . 9

LIST OF TABLES (Continued)

TABLE

9. Ocean Rates and Rates as a Percentage of Kansas City Wheat Prices, Various Routes,

PAGE

1972-76. • . . . • • . . • . . . . . . . . 11

10. Monthly Percentage Changes in Norwegian Shipping News Dry Cargo Freight Index, 1973-74. . . . . 19

11. Quarterly Percentage Changes in Norwegian Shipping News Dry Cargo Freight Index and Average Grain Rates from U.S. Gulf and U.S. East Coast to Europe 19

12. Bulk Shipping Statistics, 1972-75 .• 20

LIST OF FIGURES

FIGURE PAGE

1. Supply and Demand for Ocean Shipping ••.•... 18

2. Effects of Shifting Demand on Price with Constant Freight Rates . . . . . . . . . . . . . . 22

3. Effects of Shifting Demand on Price with Variable Freight Rates . . . . . . . . . . . 23

. .

Introduction

An extensive body of literature exists on the 'subject of international trade and its effect on the welfare of an individual country and the world as a whole. Much emphasis has been placed upon the issues of what goods a country will trade and at what prices, and how national and international well-being are affected. Additional effort has been devoted to the analysis of the effects of institutional barriers on free trade with particular emphasis on the effects of tariffs, import and export taxes and subsidies, quotas, etc. With the escalation in trade in the past decade has come a corresponding increase in the volume of research dealing with these issues. Even with this increasing interest in trade problems, there remains one aspect of trade which continues to receive very limited attention. This aspect is transportation. While the underlying importance of transportation to trade is not questioned, in the majority of trade research transport is generally treated (explicitly or implicitly) as if it were nonexistent. Transportation seems to be viewed as playing a catalytic role, necessary for the process but of no inherent interest in itself.

It is fairly obvious that, broadly speaking, changes in transport can have marked effects on the nature of agricultural trade. The development of the international grain trade has closely paralleled the development of seaborne transport. The expansion of this trade in the seventeenth and eighteenth centuries came about after the introduction of large sailing ships. North considers this as one of the primary factors that permitted U.S . wheat to compete in European markets after the 1870's. Malenbaum points out that lower inland transport costs and reduced ocean freight charges enabled Canada, Australia, and Argentina to become major grain exporters in the 1890's. It was not until the advent of steamships that trade began to even approach existing levels. In the last fifteen years, seaborn grain trade has more than doubled (see Table 1), and many observers expect continued increases in the volume of trade on international markets. The movement of such vast quantities of grain clearly requires an effective international transportation system.

Table 1: World Seaborne Grain Trade, Selected Years (million metric tons)

YEAR TRADE VALUE

1965 82

1970 89

1975 137

Source: Bulk Systems International.

1976 146

1977 147

1978 169

1979 175

The question to be investigated herein is the degree to which the usual practice of taking transportation for granted when analyzing international trade issues is valid. As will be argued below, there appear to be cases in which ignoring transportation is at best questionable, and in which the effects of transport should be considered, at least to some extent. For some problems, this might involve explicit incorporation of the transport sector into the analysis. For others, it might only entail a qualitative assessment of possible effects on policies and analytical

-2-

results that might arise due to transportation. Even for cases where ignoring transport is fully justified, an analyst requires some awareness of international transport markets before he can legitimately conclude that a particular problem is in fact such a case.

A major purpose of this paper is to increase awareness of the operation of international transport markets. Specifically, the aim is (1) to provide information to trade analysts concerning the nature and operation of international transport markets and (2) \<Jhenever possible, to link this information to existing knowledge about important factors affecting international agricultural trade. The information provided herein is thus of value to researchers both to the extent that it can be used to refine trade models (e.g., in incorporating a transport sector) and in indicating what types of transport effects might be relevant to analysis of a given trade problem, and the likely consequences of ignoring these effects. Given this purpose, the paper is primarily expository, drawing upon previous work in trade and transportation and presenting data descriptive of the characteristics of bulk ocean shipping .

The Ocean Transport Industry

Ocean shipping can be roughly divided into two essentially separate markets involving two different commodity groups: that carried by liners and that carried by tramp ships and bulk vessels. Liners specialize in general cargo (especially manufactured goods) in relatively small lots, follow regular schedules, and have varying degrees of fixed rates. They are subject to some regulations by various countries, but the primary source of regulation, at least with respect to rates, is shipping cartels formed by liner companies. A firm need not be a member of a cartel in order to participate in the liner business, but most are.

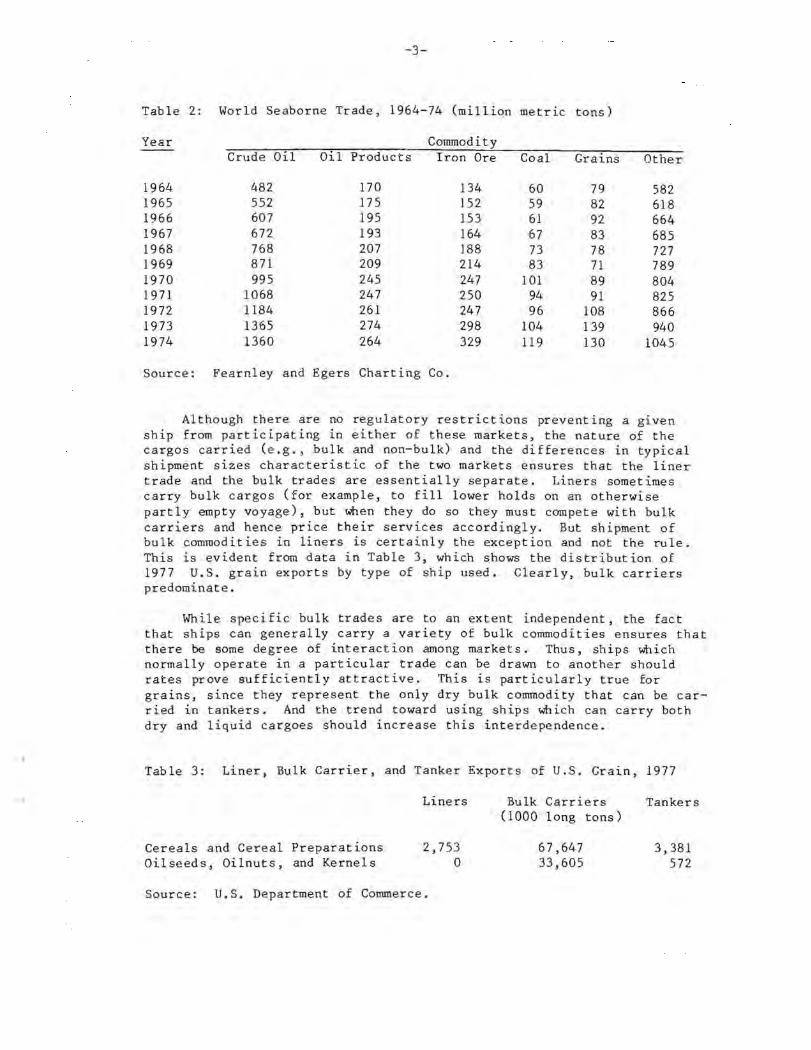

The second major market , that involving tramp ships and large bulk carriers, is that for carriage of basic commodities in bulk, typically in full shiploads , It is dominated by a few major commodities: oil and oil products , coal, iron ore, and grains, including soybeans. Shipment of these commodities comprises well over half of all seaborne trade. This is indicated by Table 2, showing trade for the period 1969-74. Bulk commodities clearly predominate, especially considering that much of the "other" category includes such commodities as bauxite, phosphate rock, and sugar~

A variety of ships participate in the bulk trades, ranging from aging tramp steamers to mammoth carriers capable of handling cargoes exceeding several hundred thousand tons. Although many bulk carriers are specialized, most can carry any bulk commodity. The major exception is tankers, which are confined to liquid bulk cargoes and grains, However, there has been a recent trend toward use of vessels specifically designed for carrying either liquid or dry bulk commodities. Other ships are designed to be able to carry both manufactured goods and bulk commodities, the most outstanding example being car carriers, which are active in the grain and coal trades.

-3-

Table 2 : World Seaborne Trade, 1964-74 (milliqn metric tons)

Year Commodity Crude Oil Oil Products Iron Ore Coal Grains Other

1964 482 170 134 60 79 582 1965 552 175 152 59 82 618 1966 607 195 153 61 92 664 1967 672 193 164 67 83 685 1968 768 207 188 73 78 727 1969 871 209 214 83 71 789 1970 995 245 247 101 89 804 1971 1068 247 250 94 91 825 1972 1184 261 247 96 108 866 1973 1365 274 298 104 139 940 1974 1360 264 329 119 130 1045

Source: Fearnley and Egers Charting Co.

Although there are no regulatory restrictions preventing a given ship from participating in either of these markets, the nature of the cargos carried (e.g ., bulk and non-bulk) and the difference s in typical shipment sizes characteristic of the two markets ensures that the liner trade and the bulk trades are essentially separate. Liners sometimes carry bulk cargos (for example, to fill lower holds on an otherwise partly empty voyage), but when they do so they must compete with bulk carriers and hence price their services accordingly. But shipment of bulk commodities in liners is certainly the exception and not the rule. This is evident from data in Table 3, which shows the distribution of 1977 u.S. grain exports by type of ship used. Clearly, bulk carriers predominate.

While specific bulk trades are to an extent independent, the fact that ships can generally carry a variety of bulk commodities ensures that there be some degree of interaction among markets. Thus, ships which normally operate in a particular trade can be drawn to another should rates prove sufficiently attractive. This is particularly true for grains, since they represent the only dry bulk commodity that can be carried in tankers. And the trend toward using ships which can carry both dry and liquid cargoes should increase this interdependence.

Table 3: Liner, Bulk Carrier, and Tanker Exports of U.S. Grain, 1977

Liners Bulk Carriers Tankers (1000 long tons)

Cereals and Cereal Preparations 2,753 67,647 3,381 Oilseeds, Oilnuts, and Kernel s 0 33,605 572

Source: U.S. Department of Commerce.

-4-

The market for bulk ocean shipping, at least on the supply side, is characterized by a high degree of competition. Not only is entry unrestricted, but there is no market dominance by any shipping firm. While some vessels are shipper-owned (especially in the oil trade), most are chartered by shippers, either for a set period of time or for a given number of voyages (most commonly one). Rates for either type of charter are determined by bargaining between shippers and vessel owners, either directly or through brokers.

The fact that there is no market power on the supply side ensures that rates charged will tend to reflect costs in the long run. (Short run effects are discussed below.) In the grain trade, this tendency may be enhanced by the fact that a large portion of chartering is conducted by a small number of shippers, the major international grain houses. As an illustration of their dominant role in grain shipping markets, Table 4 presents data on grain chartering activity for the first quarter of 1975. Nearly one half of the reported charters for that period were made by the five major grain companies. The domination of trade by these firms, who are large enough to operate their own vessels (and do so to some extent), precludes the possibility of rates exeeding costs for an extended period.

Cost Factors in Bulk Shipping

Technological changes in ocean transportation have resulted in declining real costs, at least until the mid-1970's. The primary development has been a trend toward the use of larger ships, whose at-sea operating costs are lower than those for smaller vessels. Since the efficient use of such ships requires well developed ports and a fairly reliable volume of cargo, this trend has been less prevalent in grain trading than in that for other commodities, since international grain movements are relatively volatile and involve many ports with deficient facilities. For example, in 1974,78% of iron ore shipments and 55% of coal shipments involved vessels larger than 40,000 DWT, but only 16% of grain movements involved ships of that size. l Recently, however, perhaps due to the fact that some major port areas have been upgrading their facilities, the use of large ships for grain transportation has been increasing significantly, a trend which is quite evident from the data in Table 5. This trend has largely been confined to major trading routes, such as the U.S. Gulf to Rotterdam, where the use of large vessels has become the norm. Elsewhere smaller bulk carriers (20 - 30,000 DWT) have tended to predominate, especially for shipments originating from South Africa, Australia, and Argentina. However, both Argentina and Australia have recently placed increased emphasis on port development. The Kiwana terminal in Western Australia is now capable of handling 100,000 DWT vessels. Argentina is completing facilities with similar capabilities at Punta Medanos.

Such developments as these may contribute to further reductions in the costs of seaborne grain carriage. However, any reductions in costs

1 DWT stands for "dead weight tonnage," which represents the weight required to sink a vessel to its summer load line.

Table 4: Reported Voyage Fixtures for Grain - First Quarter 1975 (number of shipments and thousand metric tons)

Destination Northwest Mediterranean Near East

Europe Sea Charterer

Bunge 13 427.8 4 83.0 -- 83.0 Continental Grain 12 370.7 19 421.6 2 62.5 Cook 15 502.5 4 102.3 -- --Dreyfus 14 367.4 14 296.3 3 63.8 Tradax (Cargill) 34 853.6 13 357.0 4 85.3

TOTAL 88 2,522.0 52 1,260.3 9 211.6

Government Agencies -- -- 7 188.5 29 714.0 Other Charterers 65 2,024.6 40 802.9 2 36.8 Not Specified 13 442.0 13 261.0 6 235.0

TOTAL 66 4,988.6 112 2,512.6 46 1,197.4

Source: H.P. Drewry, Limited.

Far East

-- 100.7 6 9 159.0 4 I 24.8 3 2 88.0 4

10 244.5 2

29 617 .0 19

20 462.3 2 22 502.7 9 10 184.9 10

79 1,766.9 40

South America

82.3 28 84.5 44 32.9 23 65.3 37 30.8 63

295.8 195

25.0 58 152.3 138 150.6 52

623.7 443

Total

693.8 1,098.3

662.5 880.8

1,571.2

4,906.6

1,389.8 3,519.3 1,273.5

11 ,089. 2

I V1 ,

-6-

Table 5: Size Distribution of Vessels Employed in the Grain Trade, Various Years (Percents)

1965 1970 1975 1976

Less than 25 , 000 DWT 95 62 34 26 25 - 40,000 DWT 4 27 35 35 40 - 60,000 Dwr 1 10 15 18 80 - 100,000 DWT 1 7 11 More than 100,000 Dwi 7 8

Source: Cargo Systems .

due to economiCS of scale must be balanced against rising costs due to increased fuel prices . Should these continue to escalate, it is doubtful that the real cost of international transport and hence its importance as a component of delivered cost will be any lower in the future than it is at the present day.

The particular costs associated with operating a vessel can be divided into three categories: ownership costs, in-port costs, and atsea costs. The major components of these cost categories are as follows:

Ownership costs: depreciation and interest, crew wages, insurance, stores and supplies, in-port fuel, administration and miscellaneous expenses.

In-port costs: pilotage, tuggage, tonnage taxes, pier and dock charges, fresh water, shoreside power.

At-sea costs: fuel, crew maintenance.

A further cost involved with ocean shipping is the cost of loading and unloading. These, along with other port expenses, can be quite substantial, approximately as large as at-sea costs. (See Binkley and Harrer and references therein.)

To provide an indication of the relative importance of some major cost categories in determining the overall costs of vessel operation, Table 6 presents estimated costs for shipping grain from the U.S. Gulf to Rotterdam via three types of ships (circa 1977). In the table, "voyage costs" are those costs specifically attributable to the voyage and which would not be incurred if the ship remained inactive. The other costs are those that would be incurred by an idle, fully-manned vessel. Two aspects of this information are noteworthy. One is the generally lower costs incurred by larger vessels, particularly with respect to capital costs and voyage costs (primarily fuel). The second is the effect of ship registry on costs. The Liberian vessel has very low crew costs, partly a reflection of lower manning requirements per ton for larger vessels, but also a result of the lack of restrictions on crew wages and nationalities imposed by Liberia (a so-called "flag of convenience"

-7-

country).2 On the other hand, crew costs and capital costs are quite high for the U.S. vessel. This reflects restrictions imposed on vessels registered in the U.S., restrictions which have necessitated that U.S. ships be subsidized in order to remain in business. Since one of the primary means of this subsidization involves export grain movements they warrant further discussion here.

Table 6: Comparison of Ship Costs, Grain Trade, New Orleans - Rotterdam, 1977 (cost 1n dollars per cargo ton)

SHIP TYPE 44,500 DWT 29,000 DWT 30,000 DWT Liberian Greek U.S.

Cost Component Cost % Cost % Cost %

Manning .80 12.3 1.86 14.6 4.58 26.8 Provisions .22 3.3 1.14 8.9 .99 5.8 Maintenance and Repair .65 10.0 .94 7.4 .86 5.0 Insurance .27 4.1 .58 4.6 1. 52 8.9 Miscellaneous .37 5.7 .59 4.6 .44 2.6 Capital 1.15 17.6 3.33 26.1 5.07 29.7

---

Operating and Capital 3.46 53.0 8.44 66.2 13.46 78.8 Voyage Costs 3.06 47.0 4.30 33.8 3.62 21.2 --- ---

6.52 100.0 12.74 100.0 17.08 100.0

Source: John Binkley, "Competitiveness of U.S. Flag Merchant Marine".

U.S. Cargo Preference Laws

With few exceptions, ships registered under the U.S. Flag are required to be constructed in the United States and to be operated by crews who are U.S. citizens. This greatly increases costs for such ships, since ship construction costs in the U.S. are significantly above those in other countries, and wages for U.S. seamen are the highest in the world. The reason for this policy is to ensure the existence of a fleet of merchant ships should they ever be required for defense purposes and to maintain domestic ship building capability. Since these vessels are faced with higher costs than are ships flying foreign flags, they must be subsidized if they are to continue to operate.

A major means of providing a subsidy to U.S. flag bulk carriers is a requirement that 50 percent of P.L. 480 grain shipments be carried by

2 "Flag of convenience" refers to registration in an "open registry" country. Such countries permit registration of vessels owned by citizens of other countries. They generally impose fewer regulations on ship operation. In addition, this form of registry permits tax advantages in some cases. Open registry is currently permitted by Liberia, Panama, Cyprus, Singapore, Lebanon, Bahamas, and Oman.

-8-

U.S. flag carriers, unless insufficient shipping capacity of this type IS

available. In Table 7 appear the annual tonnages shipped in u.s. flag vessels under the P.L. 4·80 program for the period 1967 to 1976, along with the average rate differential per ton. The rate differential is the difference between the rate paid for chartering the U.S. ship and the rate that would have been paid to charter an equivalent foreignregistered vessel. These are calculated by the U.S. Maritime Administration. The quantity shipped has been trending downward, reflecting the decline. in P.L. 480 sales in recent years. As can be seen, the magnitude of the differential is quite large, generally in excess of average freight rates for grain shipments in foreign vessels from U.S. ports for this period. Actually, the differentials presented are deceptively large. A disproportionate share of P.L . 480 grain shipments involved bagged grain, which, since it is more difficult to handle than bulk grains, moves at considerably higher rates. In an analysis of rates for bulk grain, Binkley and Harrer estimated the rate differential to be about $11 per ton, based on 1976 rates. Interestingly enough, this is very close to the cost difference between the U.S. and Liberian vessels in Table 6.

Table 7: Tonnage Shipped in U.S. Vessels Under P.L. 480, and Average Freight Rate Differential, 1967-1976.

Tonnage (thousands) Differential per Ton

1967 4,317 $18.80 1968 3,527 19.62 1969 3,310 19.24 1970 3,632 15.80 1971 3,044 13.17 1972 3,097 22.93 1973 1,700 33.29 1974 683 15.37 1975 1,492 13.87 1976 2,617 22.54

Source: The American ShipEer.

It is commonly believed that cargo preference laws, by raising transport costs of U.S. grain exports, operate to reduce foreign demand. For example, Johnson, Grennes, and Thursby have stated that:

The U.S. Government has pursued several policies that have raised shipping costs paid by exporters of U.S. wheat ... . These include the promotion of shipping cartels or conferences that collude to set monopoly freight rates and cargo preference laws that require exporters to use higher cost U.S. ships when cheaper transport is available. An increase in shipping cost lowers the price received by U.S. sellers relative to the price p~id by foreign importers. In this respect, it acts as an export tax' or a currency revaluation (p. 620).

-9-

This statement is revealing in that it illustrates the overall lack of information regarding international transportation on the part of researchers in international trade. First of all, as was noted above, cartels are only formed by liner companies, which are of no consequence in the grain trade. Secondly, the manner in which cargo preference laws are administered causes them to have no impact on effective freight rates paid by importers and exporters. It is true that whoever charters a U.S. flag vessel for a P . L. 480 grain shipment must generally pay a higher rate than if a foreign flag vessel were used. However, the USDA reimburses the difference in these rates to the shipper, based on the freight rate differentials calculated by the U.S. Maritime Administration. In effect, then, the freight rate differential is paid by U.S. taxpayers and not by shippers, and thus there will be no deleterious effect on export demand due to higher freight rates .

An additional transport policy that could potentially affect U.S. grain exports involves grain sales agreements with the Soviet Union. A requirement in the 1972 agreement was that at least one third of shipments be carried in U. S. flag vessels, with no reimbursement of the freight rate differential. In principle, this represents a higher cost to Soviet purchasers and hence it should dampen their demand. However, in practice this does not appear to have been the case, for rates charged by U.S. ships involved in these movements have been very similar to rates charged by foreign vessels. That this is the case can be seen from data presented in Table 8. The reason for this is not clear; in view of the fact that the requirement that U.S. ships be used was considered an important part of the trade agreement, the lack of any large rate differences is surprising.

Table 8: Average Rates to Soviet Black Sea Ports, 1972-76, by Flag of Registry (number of observations in parentheses; rates in dollars per long ton).

Year

1972

1973

1974

1975

1976

U. S. Gulf U.S. Flag

22 .46 (1)

12.51 (52)

12.94 (22)

16.77 (12)

16.28 (73)

Foreign Flag

(0)

(0)

15.90 (2)

14.20 (34)

15.05 (12 )

From: U.S. East Coast

U. S. Flag

12.87 (59)

24.08 (0)

18.37 (8)

12.61 (6)

10.06 (32)

Foreign Flag

13.41 (10)

(0)

12.40 (5)

9.53 (7)

10.56 (7)

Source: Calculated from Maritime Research, Inc.

-10-

The Quantitative Importance of International Shipping Costs: Macro and Micro Considerations

Other things the same, the greater the proportion of transport costs 1n the delivered price of a good, the more significant is transportation 1n determining the good's pr.oduction and marketing patterns . In the present context, a reasonab Ie measure of this is the transport cost rate t, defined as {cif value - fob value)/fob value. As an approximation to this, in Tab Ie 9 are presented rat ios of the average reported trip charter rate for all grains to the average Kansas City wheat price for some important trade routes for various years (the rates are also presented).3 These are only meant as rough indicators of t . The Kansas City price is lower than the fob port price, leading to an overestimate of t, and charter rates include cargo handling costs to varying degrees. If handling costs are considered part of transport costs, then t may be underestimated; if they are not, then t is further overestimated. 4

These considerations aside, the data in Table 9 suggest a rather large variation in the importance of transport across trading routes and among years. Overall, the data suggest that transport accounts for somewhere between five and fifteen percent of delivered grain prices, depending upon the route and time period in que s tion. For trade in all commodities, the United Nations has estimated a rate of 11%; Geraci and Prewo estimated it to be 12.8%. Thus, the transport cost rate for grain appears to be comparab Ie to that for all seaborne trade, and typically less than that for domestic movements. This may be one reason why domestic grain transportation has received much more attention than oceanborne grain transport.

These data suggest that transportation costs are not a dominant factor in the international grain trade , in the sense that possible changes in aggregate transport costs would be unlikely to bring about large changes in trade volumes. For example, with perfectly elastic supply, under which a change in transport cost would be fully translated into a change in price, even a doubling of these costs would only tend to increase price by something on the order of between five and ten percent. It should be pointed out, however, that, ceteris paribus , the effect of a transport cost change will be greater than that for most inputs, since the only viable substitution possibility for transportation is home production.

In general, then, if interest is only on aggregate levels of international grain movement (the macro case), ignoring transportation is unlikely to do a great deal of violence to reality. Thus, for example, a

3 The price 1S for No . 1 hard red winter wheat, which 1S viewed as a representative grain price.

4 Binkley and Harrer have estimated that including loading in rates increases them by about $2.90/ton; in their sample, rates including both loading and unloading were increased by about $ll/ton. Of the routes in Table 9, only those from the U.S. North Pa~ific involve a large percentage of shipments which include cargo handl1ng costs.

Table 9: Ocean Rates and Rates as a Percentage of Kansas City Wheat Prices, Various Routes, 1972-76 (Rates in Dollars pe r Long Ton)

Year Route 1972 1973 1974 1975 1976 Average

Rate % Rate % Rate % Rate % Rate % Rate %

U.S. Gulf - Europe 4.31 5.1 12.45 6.9 11 .17 7. 0 6.08 4.0 6.12 5.9 8.03 5.8

Great Lakes - Europe 8.98 10.6 21.18 11.8 23.12 14.4 14.67 9.6 16.45 15.9 16.88 12.5

U.S. East Coast - Europe 4.34 5.1 12 . 94 7.2 14.19 8.9 5.78 3. 8 6.17 5,9 8.68 6.2

U. S. North Pacific - Japan 7.74 9.2 16 . 12 8. 9 27.23 12 . 0 11.92 7.8 14.74 14.2 15.55 11.4

U.S. Gulf - Japan 5.94 7.0 15.34 8. 5 23.95 15 . 0 11.41 7.5 10.98 10.6 13 . 52 9.7

Brazil - Europe 7.67 9.1 19.73 10.9 26.22 16.4 10.68 7. 0 12.79 12.3 15.42 11. 2

Australia - Japan 9.82 11.6 15.21 8.4 22.28 13.9 11. 7 3 7.7 12.15 11.7 14.24 10.6

Source: Calculated from Maritime Research, Inc., and U.S. Dept . of Agriculture.

I ...... ...... I

-12-

simple non-spatial price equilibrium trade model, based on the existence of one world market clearing price, may be a useful approach to the study of many aggregate trade problems. Although such models completely ignore transport costs, this may not be a serious omission. However, much international trade analysis is not as concerned with overall trade levels as with patterns of trade and the effects of specific trade policies, which generally involve only a subset of possible trading partners (the micro case). From this viewpoint, the most interesting aspect of the data in Table 9 is its variability, both with respect to routes and time. The latter affects international price variability, a matter taken up below. The variation among routes is important because it affects the competition among exporters.

In the theory underlying agricultural trade between two countries, the addition of transport costs causes upward shifts in export supply or import demand schedules. The above discussion suggests that these shifts are modest, causing little difference relative to the case of ignoring spatial separation. However, in a multi-country context, with differing transport costs among sets of potential trading partners and/or differing elasticities of supply, this may no longer be the case. A change in transport costs that affects only a subset of trading routes, even if only a modest change, can potentially have perceptible impacts on trading patterns. In contrast to the case for transportation as a whole, there are generally very good substitutes for transport between an importer and anyone exporter in the form of transport from other exporters. Thus, a transport cost change can induce an importer to change its source of supply or perhaps exact more favorable prices from existing suppliers. This could lead to a change in u.s. export prices and/or export quantities.

Differing transport rates among traders have effects similar to different tariff structures. Hence raising or lowering transport costs between two countries can be viewed as (say) the imposition or removal by an importer of a tariff on imports from a particular exporter. The effect of tariff changes on the pattern of trade among traders and changes in this pattern has been a topic of interest to trade analysts, but very little interest has been displayed in similar effects arising from transportation. In this light, a study by Sampson and Yeats is pertinent. In assessing the relative importance of tariffs and transport costs on actual and potential exports from Australia, they found that the overall effect of transport and insurance costs, while varying greatly across products, poses as significant a barrier to trade as at least two or three times the current level of tariffs. An earlier study by Finger and Yeats of imports into the United States arrived at similar conclusions.

Binkley and Harrer have shown that, through improved shipping technology, the possibility exists for a reduction in existing freight costs differences between a given importer and competing exporters. Thus, for example, South America could, through transport improvements, improve its position vis-a-vis the United States in supplying the European market. The major consequences of such a development for the United States would most probably involve lower export prices than it would otherwise receive. But it also could lead to a loss of markets.

-13-

In order to examine this issue further, consider the following simple three country trading model, with two exporters supplying a single importer:

Ql ct l + ct2

(P - T ) 1 (1)

Q2 81 + 82 (P - T2) ( 2)

Q3 8 1 + 8P 2 (3)

Ql Q3 - Q 2 (4)

Q and Q2

are quantities supplied by exporters 1 and 2 and Q3

is quanti~y demanded by the importer. P is the global price, and Tl and T2 are the transport costs from the first and second exporter, respectl. vely, to the importer.

This model can be used to examine the effect of a change in transport costs on the countries involved. Suppose Tl changes. Totally differentiating the system with respect to Tl yields

dQl dP - ct 2 dTl dT dT l ct 2 dT dTl

1 1

(1' )

dQ2 dP dTl

82 dT dTl 1

(2' )

dQ3 dP dT

l 8 2 dT dTl

1

(3' )

dQl dQ 3 dQ2 -dT dT dTl - -dT dT l 1 1

dTl

1

(4' )

Subtituting (3 ') into (4 t) yields 3 equations in 3 unknowns. In matrix form, these are

1 0 -ct2

dQl

dTl

-ct2

0 1 -8 2

dQ2 dT

l 0 dTl dTl

dP 1 1 -8 2 dT

l 0

-14-

These can be solved to obtain

dQl a2

(82 - 8 2)

dT1

IT

dQ2 82a

2 dT

1 IT

dP -a2 dT

1 IT

where IT = (82 - 82 - a 2). Since a2 and 82 are both positive and 02 is negative, IT is negative and dQl/dT1 is positive. Thus, should exporter 1 lower its transport cost, it will increase its exports, its competition will reduce exports, price will fall, and total trade will expand.

What is of interest here is that the effect on the two exporters is independent of existing market shares and only depends upon their elasticities of export supply. In particular, examination of the above derivatives indicates that as 82 and a2 increase (i.e., the elasticity of supply of either or both of the exporters becomes large) the responsiveness of exports from the two countries increases. If exporter 1 lowers its freight rate, the greater will be its increase in exports, and the greater will be the decrease for exporter 2, the larger are the supply elasticities.

Of possibly greater interest is the effect on world price. Analysis of the derivative of price with respect to T1 shows that the price change will be greater the more elastic is the supply of exporter 1 relative to that of exporter 2.4

This analysis has some relevance for the competitive position of a major exporter like the U.S. Although the U.S. is the dominant supplier on international grain markets, a number of other countries also consistently export wheat, corn, and/or soybeans. If one of these implemented a transport improvement, resulting in a lowering of its transport costs, this would have effects on both U.S. exports and export price received, irrespective of existing market shares. The effect on price could be especially important, since it will be greater the more elastic is the

4 For an analysis similar to that presented here, see Laing.

-15-

supply of the smaller exporter relative to the U.S. It may well be the case that the long run export supply functions of some (relatively) minor producers, who have yet to use their resources and to fully implement technology to the extent true of the United States, are more elastic than that of the U.S, especially if there are large potentials for improvements in yields. In addition, as a producer expands exports, its unit transport costs will tend to fall as scale economies are realized. 6 This implies a non-vertical shift in long run export supply, in the manner of a reverse ad valorem tariff, leading to a more elastic curve.

As an example, consider the case of Brazil. In 1976, the rate to Europe from Brazil was approximately 16 cents a bushel higher than the rate from the U.S. Gulf (Table 9). Binkley and Harrer have estimated that only about five percent of this difference is attributable to distance, with the balance reflecting differing port and vessel efficiency. This suggests that much of the difference could be eliminated. If threefourths of it were, and, if due to the supply elasticities involved, half of that were reflected in a reduction in U.S. price, price would fall by six cents per bushel, or about two percent for three dollar corn. As a point of comparison, Thompson, in a "worst case" analysis, estimated that a four-fold increase in Brazilian corn exports would have generated an 8.4 percent U.S. export price reduction in 1975.

Of course the above is mostly conjecture, and does not include possible realignments among trading partners. On the other hand, it does not take into account possible reductions in U.S. exports. But it does provide some indication of how transport improvements by one supplier can affect other exporters. Given the possibilities for production expansion along with the adoption of improved transport technology by some "less important" grain exporters, the effects of possible transport changes on export prices and trade patterns may not be trivial .

Variability in Ocean Freight Rates

The data in Table 9 indicate that ocean freight rates for grain are quite variable over time, probably at least as variable (on a percentage basis) as grain prices in the U.S. There are thus two sources of price variability to importers: that caused by shifting demand and supply for grain, and that arising due to volatility in transport markets. The former is undoubtedly the more important, but transport does serve to inject further instability into these markets. Since one of the primary justifications for trade policies is the elimination of price instability or at least to shield the policy-making country from its effects, freight rate variability is of potential importance in various policy contexts. As an example, agricultural economists have devoted much effort to examining welfare effects of price stabilization on international markets. In this process, variability in freight rates has gone unrecognized. Nor has it been pointed out that transportation can playa role in determining how price instability is translated into effects on importers and exporters.

6 The effects of scale economies have been suggested above. For a fuller discussion, see Kendall and Binkley and Harrer.

-16-

The importance of transport's role for this and related issues depends critically on the nature of transport supply, especially short run supply . Apparently, this is thought to be infinitely elastic, for transport costs , When considered, are viewed as constant. However, this is a very dubious assumption, at best applying only to a portion of the supply function .

rae Short Run Supply of Shipping

The market for ocean shipping of bulk commodities is among the most unstable of markets , This is primarily due to the volatility of demand for the commodities transported and the short run inelasticity of the supply of shipping services over certain ranges. It is the latter that is of interest here ,

When a particular segment of the shipping market is at normal capacity, expansion can occur in three ways: deliveries of new vessels, more intensive use of existing vessels, and entry of capacity from other shipping markets. Concerning the first, this bears little relation to short term events in shipping markets, since it takes at least tvlO years from the time an order is placed until a ship is delivered. Thus, new deliveries are as likely to be made during periods of excess capacity as When they are needed, and thus will augment short run supply only by chance. 7

More intensive use of vessel capacity, while in principal a means to expand short run supply , is unlikely to make a significant contribution. This is due to the vast escalation in costs encountered: the major means of increased vessel utilization is through increased speed, but fuel consumption rises exponentially with speed.

The third type of short run increases in shipping capacity, the attraction of vessels from other markets, does in fact occur, as noted earlier. However, any significant response can not be immediate,

7 Indeed , if there is cyclic behavior in freight markets, new deliveries may be more likely to occur during inactive periods. H.P. Drewry, Ltd., has noted that :

"When profitability is eroded by a weak market, contracting activity (for new vessels) comes to an abrupt halt, even though this may be the most favorable time to order new tonnage. Similarly, at times of high freight rates, shipowners seem to believe that the boom times will last forever" (p. 65).

Zannetos has extensively examined the role of expectations in creating instability in tankship markets and underscored the importance of short run supply inelasticities:

" ... tankship . .. markets are much more complicated than those described by the classical cobweb theorem of the cattle and hog cycles. Ships are not as perishable as cattle, hogs, or wheat, so the production cycle does not fully determine the duration of the price cycle" (p. 9).

-17-

primarily due to existing contractual arrangements, costs of converting from hauling one commodity to another, and so on. In addition, this source of supply expansion presupposes the existence of slack capacity in other markets (relative to the market in question).

For these reasons, if the capacity in a given market is at or near full utilization, an abrupt increase in demand is likely to, in the very short run, only increase rates, with some supply response over time through attraction of capacity from other sources. By the time any genuinely new capacity generated by the price increase becomes available on the market, the demand increase is as likely as not to have dissipated.

The upper portion of the short run supply function is therefore extremely inelastic. The converse is the case along the lower portion. When rates are insufficient to cover variable costs, vessels are often "tied up"--idled in ports . While, due to expectations of rate recovery, ships sometimes continue to operate at rates below costs, sustained periods of low rates result in extensive tie-ups. Since vessels have different per unit variable costs, the practice of idling ships at rates below these costs makes for nearly perfectly elastic supply at rates approximating the variable costs of less efficient ships. Thus, the supply function is elastic over only a portion of its range.

Thus, the general shape of the short run supply curve for ocean shipping is as presented in Figure 1. Given this supply function, a shift in demand from DO to D1 would have no effect on rates, while a shift to D2 would bring about a dramatic change. If demand shifted further to D3' rates would rise substantially, with little or no increase in supply. The location of point B, where the change from elastic to inelastic occurs, relative to demand is a major factor in rate volatility. Zannetos estimated an aggregate short run supply function for the tanker market and found that B occurs at about 95% of capacity. He found that beyond that point, a 1.66% increase in transport demand would increase rates by 83%. Since dry bulk shipping markets are qualitatively similar to those for oil, they have similar potential volatility.8

As an illustration of the short term variability of ocean freight rates, consider the two years 1973-74. For this period, monthly percentage changes in the Norwegian Shi~ping News (NSN) dry cargo trip charter index are presented in Table 10. As can be seen, there are often large rate fluctuations from month to month, in a fashion similar to grain prices themselves.

The data in Table 10 are strong evidence that short run equilibrium transport supply is often not on an elastic portion of the curve.

8 Charles River Associates has estimated a dry cargo supply function similar to that of Zannetos.

9 The Norwegian Shipping News Index ~s based on actual rates on all major dry bulk commodities on a worldwide basis. It is the standard index used in the shipping industry.

-18-

p

Q

Figure 1. Supply and Demand for Ocean Shipping.

-19-

Table 10; Monthly Percentage Changes in Norwegian Shipping News Dry Cargo Freight Index, 1973-74.

Percentage Change Month 1973 1974

January 16.8 -2.4 February 5.5 -7.5 March 4.9 12.7 April 12.8 -4.9 May 6.5 .5 June 2.2 -3.5 July -2.8 -9.3 August 7.5 -.9 September 18.1 .6 October 31.9 2.0 November -8.0 -1.2 December 8.5 -6.3

Source: Calculated from Norwegian Shipping News.

Furthermore, the NSN index applies to all bulk commodities on a worldwide basis. It thus is likely to mask rate fluctuations that might be encountered for a specific commodity and/or for a specific route, since rate increases for one market may be counterbalanced by rate decreases in another. The more specific a shipping market (in terms of commodities involved and location) the more inelastic will short run supply tend to be. This is due to the time it takes for one market to react to changes in another, as in, for example, ships transporting one commodity to switch to another. That rates are more variable in particular markets is apparent from comparing changes in the NSN index to those for grain rates on specific routes. This is done in Table 11 for two routes, u.S. Gulf to Rotterdam and U.S. East Coast to Rotterdam, for quarterly changes for a

Table 11; Quarterly Percentage Changes in Norwegian Shipping News Dry Cargo Freight Index and Average Grain Rates from u.S. Gulf and U.S. East Coast to Europe.

Percent Change Year Quarter NSN U.S. Gulf - Europe U.S. East Coast - Europe

1977 1 -3.3 -5.4 -9.5 1977 2 .1 -.8 -14.7 1977 3 3.1 28.8 28.4 1977 4 -.8 -6.9 .7 1978 1 5.0 24.8 6.0 1978 2 -1.0 -1.4 50.9 1978 3 5.7 31.1 -8.1 1978 4 2.0 7.0 19.9 1979 1 11. 9 50.7 35.3 1979 2 16.8 14.0 -11.4

Source; Calculated from Norwegian Shipping News and FATUS.

r

-20-

period in the late 1970's. It is obvious that the specific rates are more variable. Furthermore, the short-term behavior of rates over the two routes is not parallel. This suggests that in the very short run, demand fluctuations on a particular route may bring little if any supply response and only serve to change rates: costs are likely to be sensitive to quantities shipped.

In the longer run, ocean freight markets are interrelated. Some evidence of this is provided by data in Table 12, which is descriptive of international shipping for 1972-75. In the first column are the annual average rates from the U.S. Gulf to Europe, while column 2 has total seaborne grain trade. Assuming that changes in the grain trade from the Gulf paralleled those for the world as a whole, and supposing no shifts in supply of shipping capacity between 1972 and 1973, the rate and quantity changes suggest a supply elasticity of .15, which is indeed inelastic. However, the total supply of dry bulk shipping capacity was not constant (column 4), and there was a movement along this function due to a reduction in idle vessels (column 5).10 On the other hand, other

Table 12 : Bulk Shipping Statistics, 1972-1975.

Average World Grain Rate, Seaborne U.S. Gulf Grain

Year Rotterdama Tradeb

0) (2)

1972 4.31 108 1973 12.45 139 1974 11.17 130 1975 6.08 132

a Dollars per long ton. b Million metric tons. c Thousand dead weight tons.

World Dry Dry Bulk Bulk Tradeb FleetC

(3) (4 )

1317 69300 1481 78600 1623 88000 1537 96300

Dry Cargo Tankers Tonnage in Grain Tied Upc TradingC

(5) (6)

1620 579 520 750 440 3175

8500 2263

Source: Rates: Table 9; all others from Fearnley and Eggers, Ltd.

dry bulk trade also increased (column 3), thus reducing capacity available to grain shippers. Although the grain trade declined between 1973 and 1974, and due to declining oil trade, tanker participation in this trade increased (column 6) rates remained fairly steady, primarily due to a large increase in non-grain trading. However, grain rates fell sharply between 1974 and 1975, even though trade was virtually unchanged. This was primarily due to the continued increase in capacity coupled with declining trade in other commodities. The overall depressed state of seaborne trade in 1975 brought about a marked rise in idle tonnage.

10 The data in column 4 overstate capacity increases, s~nce it includes only vessels of greater than 10,000 DWT. Since this period was characterized by increasing vessel sizes, part of the growth represents replacement of smaller with larger vessels.

-21-

It should be pointed out that throughout this period there was a large escalation in fuel pricees, which undoubtedly contributed to some rate increases. It is likely that a substantial part of the difference between rates in 1972 and 1975 reflects fuel cost changes. However, the high rates in 1973 and 1974 were undoubtedly primarily due to demand pressures.

The data 1n Table 12 illustrate the dependence of rates in one market on events in another. The strong interdependence between markets makes it clear that knowledge of the magnitude of the grain trade is 1n itself insufficient for determining the level of grain rates, a fact manifest in the data presented. Transport creates a linkage with trade in other commodities. Through this linkage, the supply of shipping capacity to the grain trade may be increased or decreased, which can augment or dampen the inherent rate variability in grain shipping at any point in time. By the same token, grain shipping in one part of the world is affected by grain shipping elsewhere, as well as by transport markets for other commodities. Thus, the short run supply function of shipping capacity in anyone market is constantly subjected to shifts due to events 1n other markets. The net effect is a great deal of rate variability.

possible Effects of Rate Variability

Price Stabilization and Welfare

From the above discussion, it 1S apparent that the conventional V1ew that the effect of transport costs is to bring about a vertical shift in (say) the excess supply function, while perhaps valid in the very long run, is only an approximation (and a poor one) of the effect of transport for a shorter time period. This has rather important implications for assessing the effects of price instability on importers and exporters. Under the conventional view, the presence of transport affects only the level of price and not its variability. Consider Figure 2, which depicts two excess supply curves, one ~ith and one without transport costs. Price variation, introduced through a shifting excess demand function, 1S obviously the same in either case. (This would be only approximately true if excess supply and/or excess demand were non-linear.) The only effect of transport is to lower export prices, raise import prices, and reduce the level of trade.

This is not the case if transport supply takes the form described above. Figure 3 is similar to Figure 2, except that ES2 represents the superimposition of a transport supply function such as that from Figure 1 on the exporter's exces~ supply, ES1. With no transport costs, price varies between Po and PO. With ~ransport costs, the price to the importer varies between PI and PI, which is always greater than the,no transport case; for the exporter, the variation is between PE and PE , which is always less.

For the situation depicted, where instability arises due to shifts in excess demand, Hueth and Schmitz have shown that, ignoring transport, producers and consumers in the exporting country gain (in a welfare sense) from price instability, as do consumers in the importing country,

-22-

P

ES + T

ES

Q

Figure 2. Effects of Shifting Demand on Price with Constant Freight Rates.

-23-

p

pI I ---~------______ _

Q

Figure 3. Effects of Shifting Demand on Price with Variable Freight Rates.

-24-

while the producers in the importing country lose. The world as a whole loses from instability. Since the gains or losses vary directly with instability, the inelastic supply of shipping will tend to increase the social loss from instability. This follows since exporter price variation is reduced (and hence so are welfare gains from destabilization in the exporting country) and importer price variation is increased (thus increasing net welfare losses). Therefore, the nature of transport markets gives importers a greater stake in stabilization and exporters a smaller stake in destabilization; hence from a global perspective the gains from price stabilization are increased.

Following the arguments of Hueth and Schmitz, an analogous result applies when instability arises due to shifts in the excess supply function. Then the gainer from instability (the importer) gains less because import price variability is reduced, while the loser (the exporter) loses more because his price variability is increased. In addition, work by Just, ~~. has shown that with non-linear supply and demand curves, any gains from instability may be smaller than under linear functions. Hence, it is conceivable that in some cases the effect of transport may be sufficient to eliminate the benefits of instability to individual traders.

A caveat may be appropriate at this point. It can be argued that, since grain accounts for approximately 15 percent of dry bulk trade, it is unlikely that freight rates would respond to an expansion in agricultural trade as depicted in Figure 3. For illustrative purposes, the role of transport is somewhat exaggerated in the figure. However, it is quite possible that the type of response suggested by the figure can occur. Zannetos has found this to be the case for tanker markets, which are characterized by behavior similar to that for dry cargo. Also, referring to Table la, we see that in late 1973 there was a marked increase in the NSN dry cargo freight index, primarily due to an expansion in grain trading at that time. This suggests that increased grain trade can exert an effect on rates out of proportion to its averag percentage of total bulk trade. This is simply a result of the inelasticity of the transport supply function. Finally, the disturbances on world grain markets that engender price variability by their nature occur in the relatively short run. Even a modest short run increase in demand for imported grain and thus for grain shipping is likely to have an adverse effect on rates (from the shipper's perspective), since at any point in time there may be little slack capacity available, and rates must rise in order to draw vessels from other uses.

It has been contended that the best way to alleviate problems associated with price variability, at least from a global standpoint, is to remove all policies discouraging free trade. Such arguments have considerable merit, but they ignore negative transport effects. Tariffs, trade agreements, levies, and other trade restrictions tend to stabilize quantities traded and hence world prices must absorb a disproportionate share of the shocks incurred on grain markets. Under free trade, quantity becomes more variable, since it plays a larger role in restoring equilibrium after a disturbance occurs. But with more variability in quantity traded comes more variation in transport costs and, consequently, in price (as compared to the case of constant transport costs). Thus,

-25-

although free trade might tend to reduce variability in delivered prices, the reduction will be smaller than would be true if transport were not a factor. In addition, as has been pointed out above and elsewhere (e.g., Bulk Systems International), more stability in quantities of grain shipped would permit an expansion in the use of large vessels, which would tend to result in lower average rates. Thus, from the standpoint of transport, free trade may not be an unmitigated blessing.

Consider the example of buffer stocks. By eliminating fluctuations in imports and exports, buffer stocks would lead to more stable trade flows between countries. This would tend to lower average transport costs by eliminating large fluctuations in vessel capacity requirements, while at the same time alleviating the undesirable effects of transportinduced price variation. Such considerations have been ignored in comparisons of buffer stocks policies to free trade. For example, Bigman and Reulinger used constant transport costs in their simulations examining such policies. They concluded that to reduce instability, free trade was preferable to holding stocks. However, the assumption of constant transport costs is clearly questionable. Ignoring the true nature of transport markets leads to an overestimate of the benefits of free trade.

Of course, the practical relevance of the above considerations depends upon whether problems with transport are translated into "sufficiently large" effects on grain prices. Returning to Table 9, and using the U.S. Gulf to Europe as an example , we might suppose the 1976 rate of $6.10/long ton to be a reasonable estimate of the long run equilibriu~ rate for then prevailing levels of cost (a figure close to the : cost for the most efficient ship in Table 6). Given this supposition, the 1972 rate was about five cents lower per bushel than the norm while that in 1973-74 was about fifteen cents above it. It is difficult to say whether this sort of variability is large enough to be of serious concern. It does not appear so small as to warrant total disregard, at least in all cases. l1

As Cochrane has recently argued, the entire question of welfare gains and losses associated with price instability may be nothing more than an academic exercise, with no practical relevance. After all, the really important question relative to unstable international grain markets is probably not the garnering of marginal welfare gains but the ability of a nation to provide food for its people at a non-prohibitive price in cases of serious production shortfalls, either domestic or external. In light of this, the question of getting grain to where it's needed, when it's needed, and with reasonable dispatch, may be the most important issue. For this transport is of obvious significance, particularly the nature of its supply. Thus, for example, any analysis of optimal quantities and locations of international food reserves which ignored the characteristics of transport markets presented above would be inviting erroneous conclusions.

11 For Brazil, the corresponding procedure yields prices 11 cents below and 30 cents above the norm.

-26-

Comparative Advantage and Price Variability

The primary determinants of comparative advantage are relative production costs and relative marketing costs, with the major component of the latter being transportation. In a preceding section it was argued that there is a realistic potential for changes in comparative advantage among world agricultural producers arising due to transport changes. However, the argument can be made that the major observable impact of such changes may be on prices received by exporters. First of all, as noted above, even relatively large changes in transport costs may be translated into only small changes in landed prices. Correspondingly, large changes in relative transport costs will generally only bring about small changes in relative landed prices from different sources. Under a stable long run equilibrium situation, such changes could cause significant shifts in marketing patterns. However, stability has not been characteristic of world grain markets in recent times, and fluctuating prices make it difficult to discern small price differences. More importantly, buyers turn their attention to the price uncertainties of the market. In an unstable market such as that for grain, variations in price can be as important to buyers as price levels.

Jabara and Thompson have recently argued that under conditions of international price uncertainty, a risk averse importer will produce more of a good which it also imports than would be true without the uncertainty. As they state, this "may indeed by consistent with a broad concept of comparative advantage which recognizes that risk has a subjective cost" (p. 197). A logical extension of this argument is that, ceteris paribus, such an importer, when it does enter international markets, will choose that supplier whose exports are subject to the least price variation. Thus, ignoring any differences in f.o.b. price variation, an importer would prefer an exporter with relatively stable transport rates, a fact which might reduce the effect of different rate levels. On the other hand, rate variability can accentuate differences in average rates. Even if highly variable, rates are unlikely to £all very much below costs, but they can deviate substantially above them. This gives fluctuations an upward bias.

Again referring to Table 9, it is apparent that rates on some routes are subject to larger fluctuations than are rates on others. Perhaps of more importance, when rates rise, they appear to rise by about the same percentage on all routes, causing larger fluctuations for high cost shippers and worsening their position during periods of active trade. For example, assuming equal f.o.b. prices, Brazil's position relative to the U.S. in terms of price c.i.f. Europe was worse in 1973 than in 1972: the differential increased from about $3.50 to over $7.00. From the standpoint of comparative advantage, rate variability may be a more important factor than any differences in average rates that might exist in the absence of variability, both due to the "subjective cost" of variability itself and the tendency for fluctuations to at least temporarily magnify differences In rate levels.

It can be argued that since large rate changes are usually aSSOCIated with periods of intense trade activity, a sellers' market exists, and importers are not in a position to be very sensitive to either the

-27-

level or variability of transport costs. This may have some validity. However, it can also be argued that importers seeking long term contracts with exporters (in order to insure stable supplies at reasonably stable prices) may be sensitive to such differences. Even though a contract may shield the buyer from f.o.b. price variation, it will generally not provide protection from changes in transport rates

2 unless providers of

transportation are parties to such agreements. 1

Market Power in International Grain

One group for whom there would seem to be clear gains from price instability is the transport sector itself. If rates are as likely to deviate above a norm as below, then the transport supply function in Figure 3 would yield welfare gains to shipowners. Given the ease of entry into shipping, such gains are not likely to persist. The implication, therefore, is that the normal rate is below cost and that the occasional increases far in excess of this rate are simply remuneration for peaking capacity.13

On the other hand, market power is likely to exist in international grain trading, due to its domination by a few major firms. A casual reading of Morgan's Merchants of Grain makes it evident that a major asset of these firms is superior access to market information, information not available to small traders or even governments. When combined with control of marketing services in inelastic supply (such as transportation), this permits the exploitation of gains due to instability. For example, with prior warning of a market upturn, ships can be chartered for future delivery of grain on a c.i.f. basis. Thus, one would expect major grain firms to resist moves toward stabilizing grain markets. In this context, it is pertinent to note the contention by McCalla and Schmitz that control of the U.S. grain trade by private exporting companies has hindered the formation of long term cont,acts with importers. Such arrangements would undoubtedly reduce long run transport costs through reducing variability in shipments and therefore lead to increased price stability.

Carter and Schmitz have advanced the hypothesis that major importers such as Europe and Japan wield monopsony power in world grain markets. To the extent that this hypothesis has validity (and they provide some empirical support), the elasticity of the marginal cost of importing curve assumes greater importance. The significance of transport costs is

12 Although, as noted above, less variation in quantity traded (which might result from contracts) is likely to lead to lower transport costs. In addition, contracts could permit traders to procure vessels on a long term charter basis, thus eliminating transport price variability.

13 In an examination of tanker rates for the period 1950-1974, Hawdon found pronounced peaks, but of short duration. In only 9 of the 24 years were rates above the average for the entire period. Also, the average length of a peak period was 1.8 years, compared to 3.75 years for a trough period.

-28-

magnified, for inelastic transport supply causes rates to have a disproportionate impact on marginal cost of imports as trade expands. With full or near-full utilization of shipping capacity, an increase in trade raises rates on all shipments, not just on the marginal unit, and a buyer with monopsony power will be more hesitant to expand purchases than he would be if transport were not a factor. This is true a fortiori for expansion of purchases from a single supplier, since thls is likely to increase demand for shipping on a particular trading route, and consequently also increase freight rates on that route.

Potential market power effects can be illustrated via some approximate calculations. Suppose Japan, which accounts for about 15% of world seaborne grain and soybean imports, increased its purchases by 5%, leading to a .75% increase in world trade. If ocean freight rates were to respond as they did in 1972-73, when a 29% increase in trade induced a 143% increase in rates, rates would rise by about 3.7%. Assuming Japan currently imports 25 million tons of grain and soybeans, and supposing an average freight rate for Japanese imports of $15 per ton, the import expansion would increase Japan's freight bill on existing imports by nearly $14 million. In effect, this would increase the price of the 1.25 million tons of new imports (5% of 25 million) by over $11 a ton (as compared to no freight rate increases), perhaps a rise sufficient to dampen the demand increase.

This example is, of course, only an approximation. In addition, it is based on a sudden, non-sustained demand increase. If Japan permanently increased its demand, the initial effect may approximate that outlined above. However, eventually the shipping system would adjust to the new level of trade, and the ensuing stability would lead to lower rates. But the example does illustrate how market power can endow transport with more significance than it otherwise would have. It also suggests a reason why a major importer may prefer to do its buying through a government agency rather than through private firms, since the former permits a greater control over import variation.

Implications of Rate Variability for Trade Modeling

The above discussion has concentrated on the implications of rate variability in the analysis of specific trade issues. This variability may also have more general effects relevant for the formulation of trade models. For example, spatial equilibrium trade models often do not replicate existing patterns of trade. There are two likely reasons for this. One is that the matrix of rates used in such a model may not be selected with sufficient care--if a particular year is chosen and actual rates for that year are used, it is quite possible that it is not representat ive of a "typical" year. Indeed, given the variabi Ii ty inherent in rates, it is not obvious what a "typical" year is. If one adopts a long run viewpoint it would be preferable to employ actual costs incurred (i.e., net of rents). However, the determination of these costs is a difficult undertaking, especially since these costs can vary significantly by ports.

-29-

Secondly, traders may react to rate variability as well as to rate levels. However, spatial equilibrium models only incorporate the latter. In addition, rates used in such models are constant, that is, they are invariant with respect to quantity shipped, regardless of the length of time in question. From the above discussion, it is clear that there are many actual situations where this is not appropriate. This suggests that, in analyses where the spatial dimension is of particular interest, it may be necessary to endogenize transport rates so that the relationship between trade and transport is more realistically modeled. This may, of course, be somewhat difficult, but given continuing advances in computer methodology, more complex and realistic models are increasingly possible.

The nature of transport markets introduces similar problems into non-spatial equilibrium models . For example, such models often utilize price linkage equations as a means to equalize price among importers and exporters, with transport costs between countries serving as the link. The same problems associated with choice of a given set of rates that apply to spatial models also apply for non-spatial models" Similarly, this type of non-spatial model is based on the assumption that the price linkages are constant and do not vary with trade. The fluctuations in actual transport rates undoubtedly seriously distort these linkages: while in the long run price differences among traders undoubtedly reflect transport costs, in the short run this relationship may hold only approximately at best. This would suggest that models employing price linkage equations should employ equations that determine the required freight rates endogenously .

An additional area of trade modeling in which consideration of transport is of possible importance involves estimating the demand function facing a given exporter. Specifically, it involves the choice of what price is to be used. If the price actually paid by the importer is used (i.e., the cif price), then there is no problem. If the price at the point of export is employed (i.e., the fob price), then there will be no problem as long as the difference between the two prices is constant. If it is not, use of the fob price is not appropriate. For example, if price is rising due to increased demand and transport markets have no slack capacity, freight rates will rise. Thus, the cif price will rise more than the fob price. Ignoring the effect of transport would lead to ascribing the full effect on demand to the effect of the change in fob price, and in this case , lead to an overestimate of price elasticity. Given that transport rates are not constant, one should either use cif prices in demand estimation or explicitly include transport in the demand function. Indeed, depending upon the scope of the model in question, the transport market may need to be directly incorporated, in order to account for feedback effects between demand and supply of transport and the markets for the commodities being shipped .

In general, then, international trade modelers need to recognize that ocean transport rates for grain are neither exogenous nor constant. Ideally, analytical models employed by trade researchers should explicitly include an endogenous transport sector. Of course this may not be an easy task, since, although data on international transport rates is available, it is not generally in a readily usable form. But models that

-30-

ignore transport, either by omitting it or by treating it 1n a cavalier fashion, should be recognized as being incomplete. Depending upon the purpose of the analysis, this may have important effects on the conclusions obtained. At a minimum, analysts need to be able to assess the likely nature and magnitude of such effects.

Conclusions

This paper has at tempted to provide informat io'n on how the international grain transportation system operates, to point out important characteristics of that system, and to indicate some cases where these are likely to be of importance to international trade modelers. One thing should be clear from the information herein: the effect of transportation goes beyond simply driving a wedge between export and import prices. This wedge is of obvious importance to trade, since its magnitude is one of the most important factors determining trade patterns on international markets. As such, it is clear that transport-induced price level differences need to be accounted for in most international trade analysis. And indeed they generally have been, from the familiar vertical shifting of excess supply and demand curves in theoretical analyses to the use of transport costs in many spatial and non-spatial trade model s.

However, a major argument of this paper is that treating transport costs simply as a differential between export and import prices is, at least in many contexts, incomplete. For a variety of reasons, transport rates are quite variable, and this variability can have important effects on grain trade patterns and quantities and on various policies implemented by importers and exporters. Indeed, it is quite likely that transport rate variability is of greater relevance to trade researchers than are transport levels. Although international transport rates for grains are not inconsequential, they (on average) do not comprise a major portion of delivered grain prices. While differences in cost levels between competing traders can be of a sufficient magnitude to have effects on trade patterns, it seems likely that rate instability is of greater importance. On the one hand it serves to obscure rate level differences; on the other it generates effects with generally undesirable consequences. Certainly there is no ~ priori reason why these effects should be ignored, at least in every case. Yet this is what has been done previously.

The most important conclusion that is, hopefully, obvious from this paper is that international transport markets can be complex and need not by any means be exogenous to international grain markets. The extent to which this needs to be considered by trade analysts depends upon the types of problems under study. It is not argued here that transport must always be considered. Rather, the main point is that the opposite practice of in effect assuming that transport is nugatory, a practice followed either explicitly or implicitly by many trade researchers, is certainly to be questioned. In addition, it is hoped that the information in this paper suggests that international agricultural transportation may be a topic worthy of research in its own right.

-31-

BIBLIOGRAPHY

Bigman, David and Schlomo Reutlinger, "Food Price and Supply Stabilization: National Buffer Stocks and Trade Policies," American Journal of Agricultural Economics, November, 1979.

Binkley, James K. and Bruce Harrer, "Major Determinants of Ocean Freight Rates for Grain: An Econometric Analysis," American Journal of Agricultural Economics, February, 1981.

Binkley, John A, "The Competitiveness of the U.S. Flag Merchant Marine," Simat, Helliesen, and Eichner, Washington, D.C., December, 1978.

Carter, Colin and Andrew Schmitz, "Import Tariffs and Price Formation ~n the World Wheat Market," American Journal of Agricultural Economics, August, 1979.

Charles River Associates, Inc., Forecasting Ocean Freight Shipping Rates, Cambridge, 1974.

Cochrane, Willard W., "Some Nonconformist Thoughts on Welfare Economics and Commodity Stabilization Policy," American Journal of Agricultural Economics, August, 1980.

"Farmers Want $91,000,000 Maritime Subsidy Now Buried in USDA Budget Freed for Farm Price Support Program," American Shipper, March, 1979.

Fearnley and Egers, Ltd., Annual 1975, Oslo, 1976.

Finger, J.M. and A.J. Yeats, "Effective Protection by Transportation Costs and Tariffs: A Comparison of Magnitudes," Quarterly Journal of Economics, February, 1976.

Geraci, Vincent J. and Wilfried Prewo, "Bilateral Trade Flows and Transport Costs," Review of Economics and Statistics, 59, 1977.

"Grain and Derivatives -- Trade with Uncertain Constraints," Bulk Systems International, April, 1980.

"Grain -- Erratic Trade Hampers Port Development," Cargo Systems, June, 1978.

H.P. Drewry, Ltd., Types and Sizes of Ships for Grain Trading, London, 1975.

Hawdon, D., "Tanker Freight Rates ~n the Short and Long Run," Appl ied Economics 10, 1978.

Hueth, Darrell, and Andrew Schmitz, "Internat ional Trade in Intermediate and Final Goods: Some Welfare Implications of Destabilized Prices," Quarterly Journal of Economics, August, 1972.

-32-

Jabara, Cathy, and Robert L. Thompson, "Comparative Advantage and Price Uncertainty," American Journal of Agricultural Economics, May, 1980.

Johnson, Paul R., Thomas Grennes, and Marie Thursby, "Devaluation, Foreign Trade Controls, and Domestic Wheat Prices," American Journal of Agricultural Economics, November, 1977.