Embed Size (px)

Citation preview

Appendices

The retailisation of non-harmonised investment funds in the European Union(ETD/2007/IM/G4/95)

Prepared for European Commission DG Internal Market and Services

October 2008

PWC

2

APPENDICES

APPENDIX A: Foreign exchange rates used ........................................................................ 6

APPENDIX B: Non-UCITS assets under management by asset class in the 9 countriesunder scope in 2006.................................................................................... 7

APPENDIX C: Regulatory frameworks................................................................................ 8

APPENDIX D: Taxation frameworks ................................................................................. 15

Appendix D1: Belgium................................................................................ 15

Appendix D2: France................................................................................... 19

Appendix D3: Germany............................................................................... 23

Appendix D4: Ireland .................................................................................. 29

Appendix D5: Italy ...................................................................................... 32

Appendix D6: Luxembourg......................................................................... 37

Appendix D7: Poland .................................................................................. 40

Appendix D8: Spain .................................................................................... 42

Appendix D9: United Kingdom .................................................................. 45

APPENDIX E: Market Survey............................................................................................ 50

APPENDIX E1: Participants’ profile .......................................................... 50

APPENDIX E2: Investor base split............................................................. 56

APPENDIX E3: Distribution channel ......................................................... 62

APPENDIX E4: Market dynamics .............................................................. 68

APPENDIX F: Questionnaire for fund managers ............................................................... 76

APPENDIX G: Questionnaire for distributors .................................................................. 121

3

TABLE OF TABLES

Table 32 – Foreign exchange rates ........................................................................................ 6

Table 33 – Non-UCITS funds assets under management (in EUR m) in the 9 countriesunder scope at the end of 2006 ................................................................... 7

Table 34 – Minimum Investment threshold in France .......................................................... 9

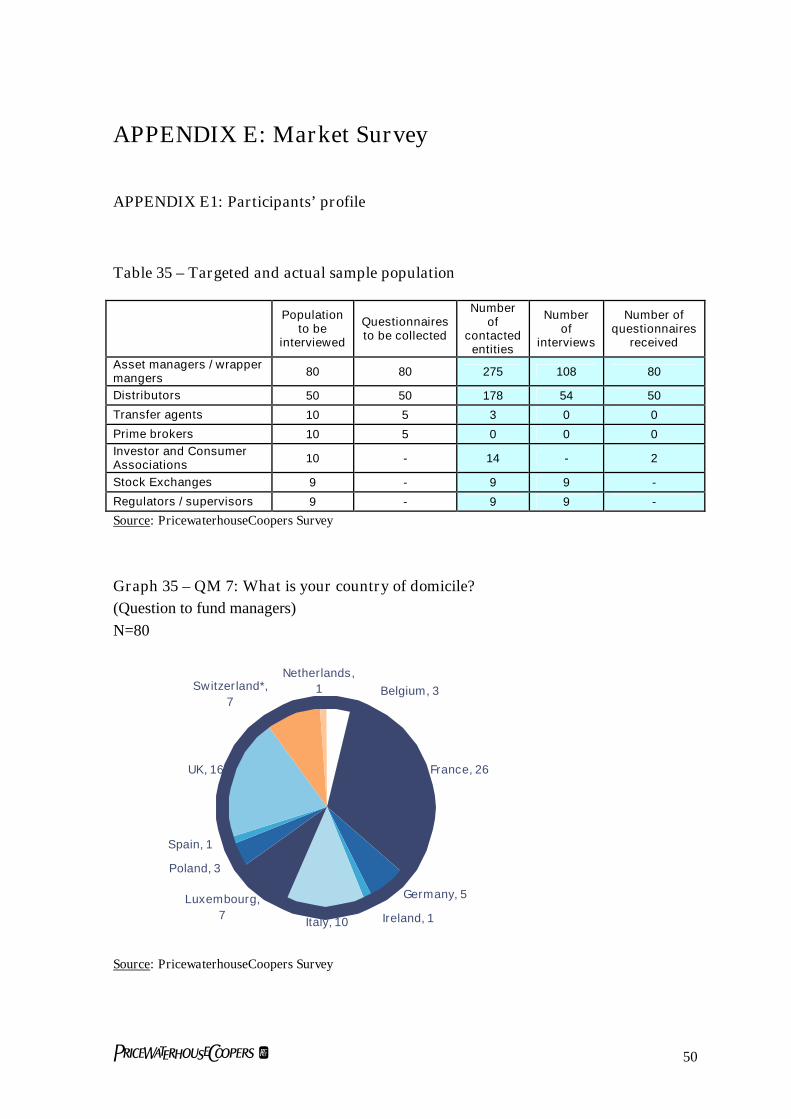

Table 35 – Targeted and actual sample population ............................................................. 50

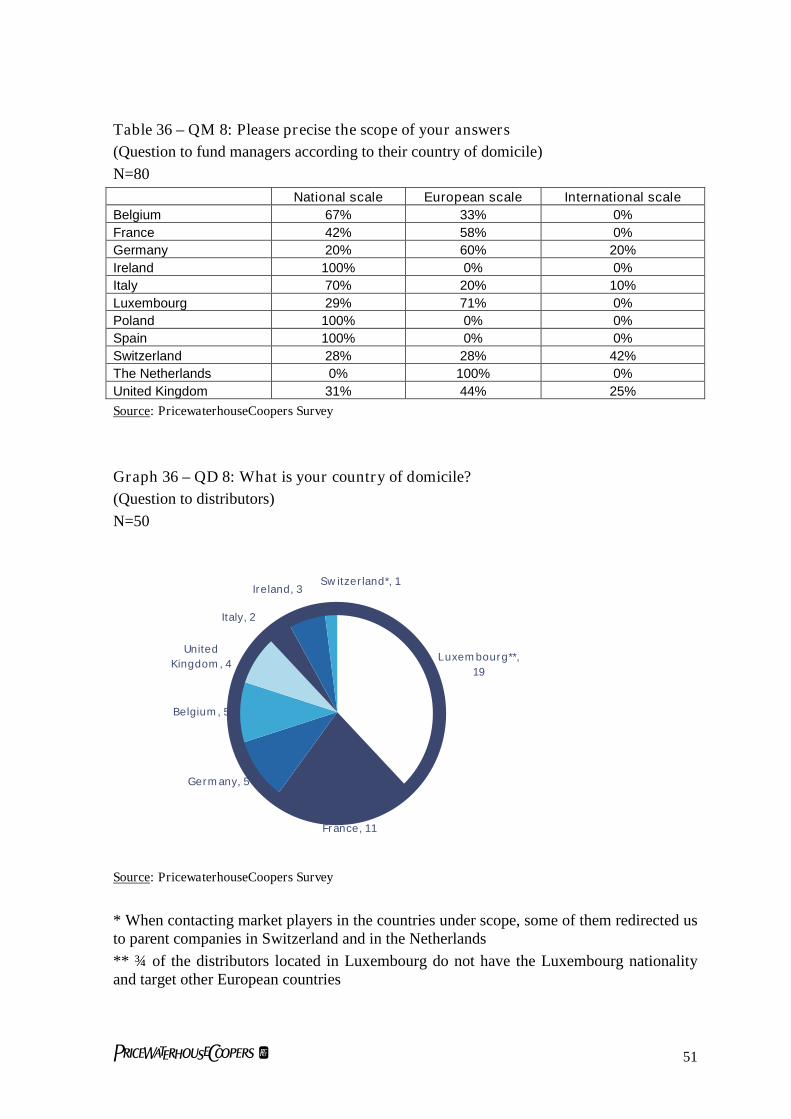

Table 36 – QM 8: Please precise the scope of your answers .............................................. 51

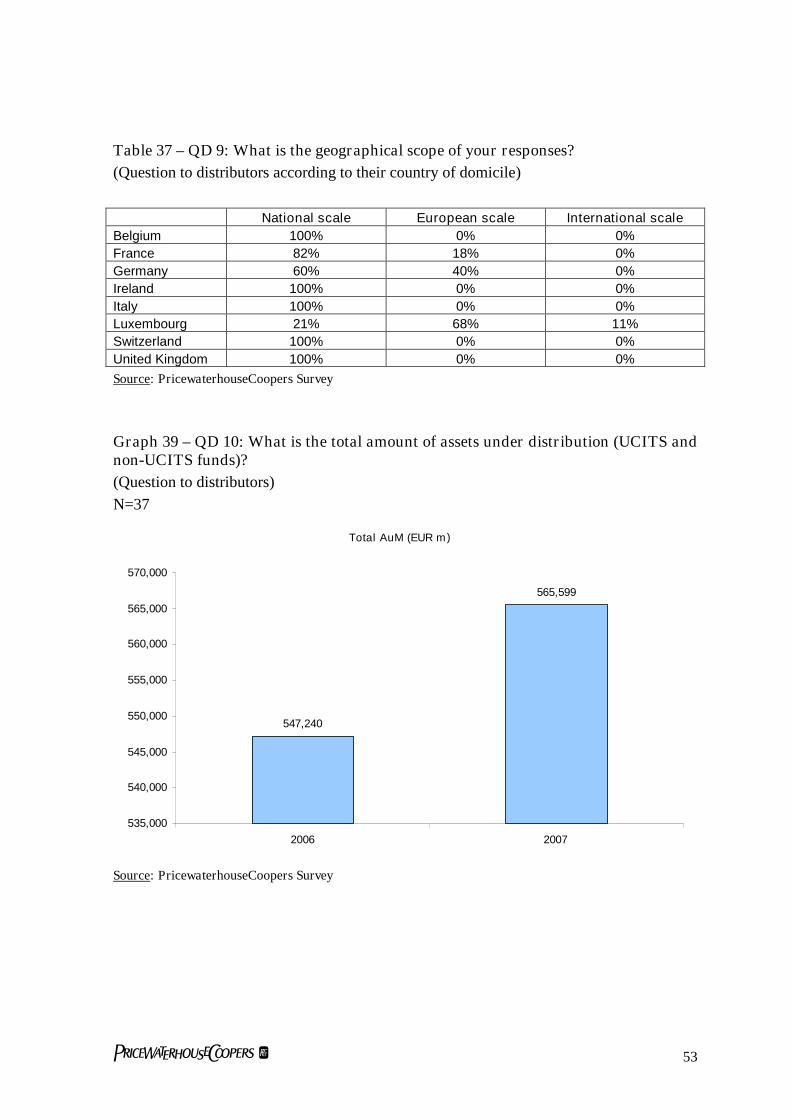

Table 37 – QD 9: What is the geographical scope of your responses? ............................... 53

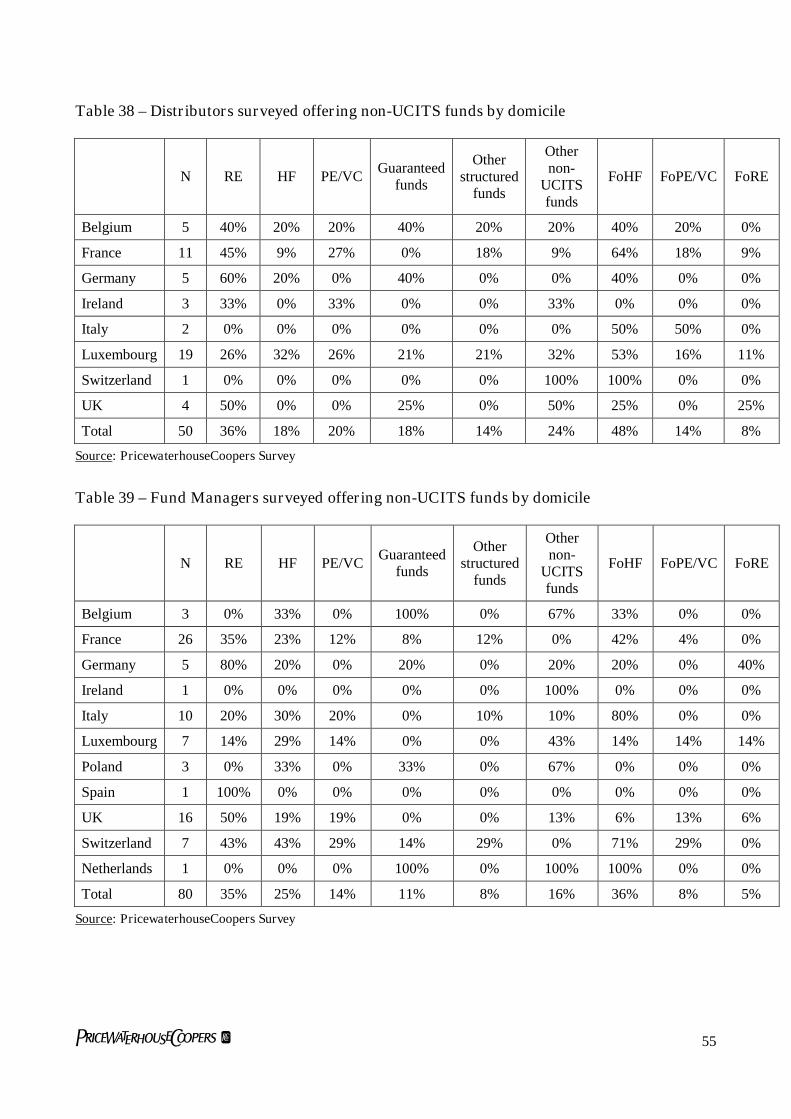

Table 38 – Distributors surveyed offering non-UCITS funds by domicile ......................... 55

Table 39 – Fund Managers surveyed offering non-UCITS funds by domicile ................... 55

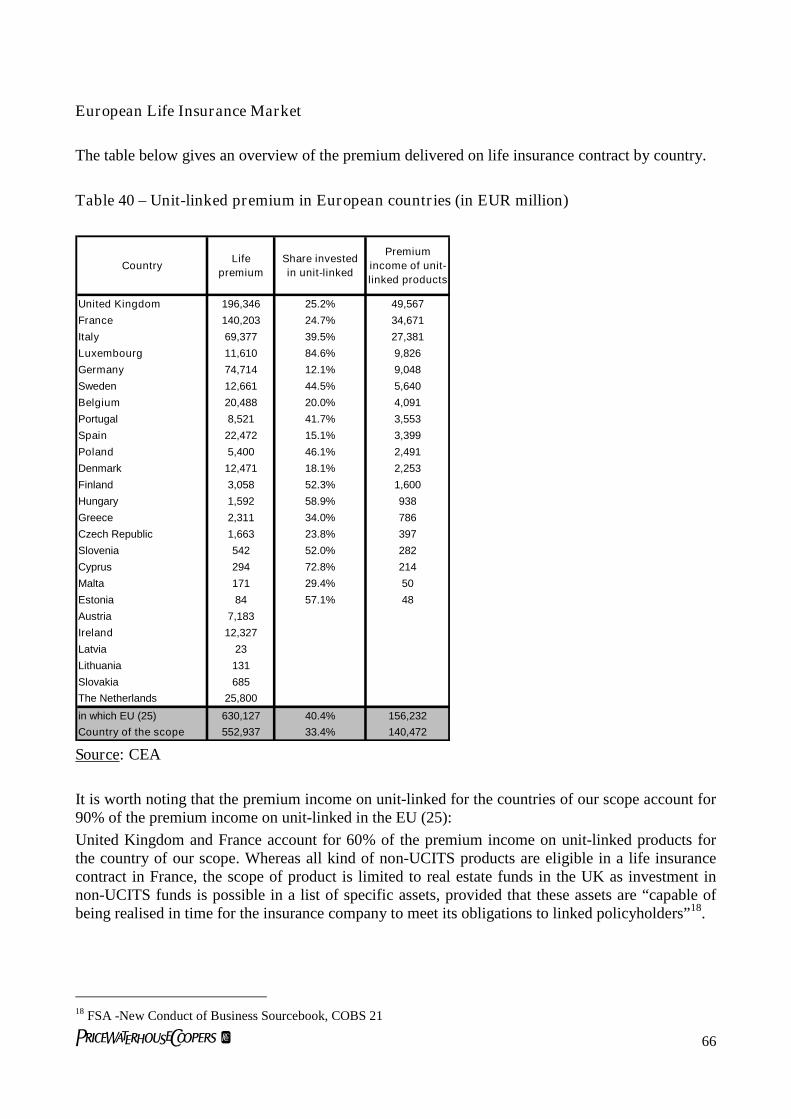

Table 40 – Unit-linked premium in European countries (in EUR million)......................... 66

4

TABLE OF GRAPHS

Graph 35 – QM 7: What is your country of domicile? 50

Graph 36 – QD 8: What is your country of domicile? 51

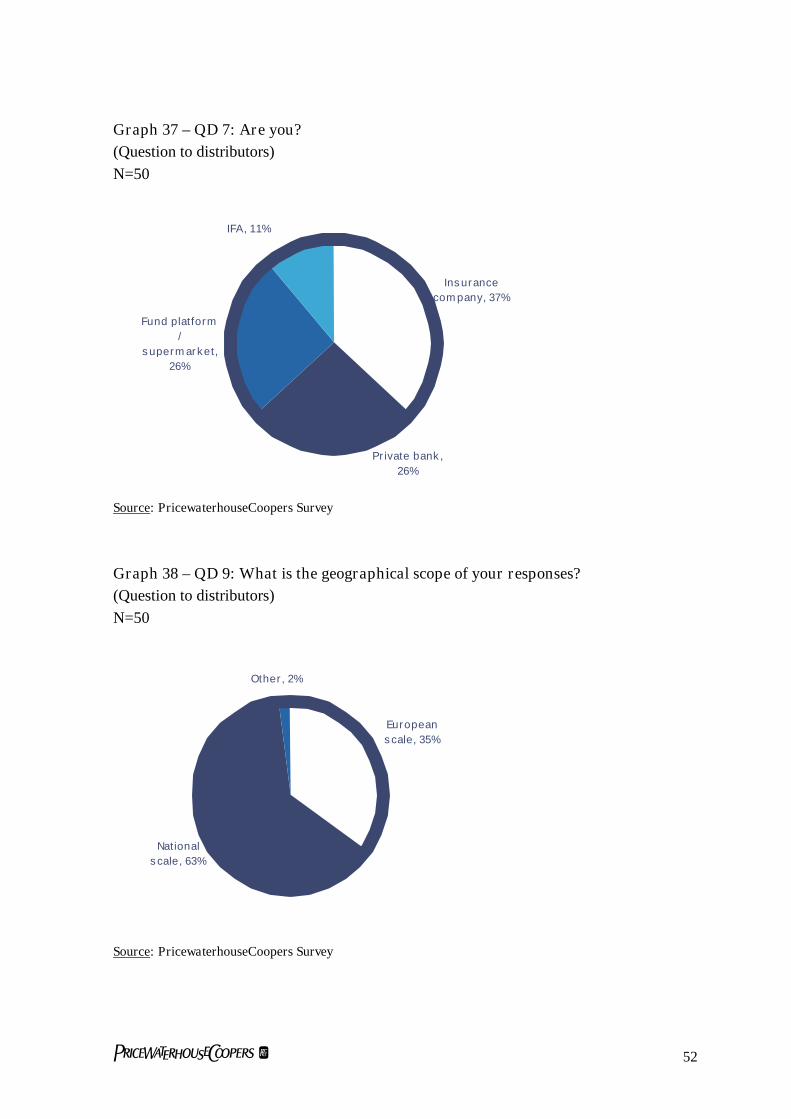

Graph 37 – QD 7: Are you? 52

Graph 38 – QD 9: What is the geographical scope of your responses? 52

Graph 39 – QD 10: What is the total amount of assets under distribution (UCITS and non-UCITS funds)? 53

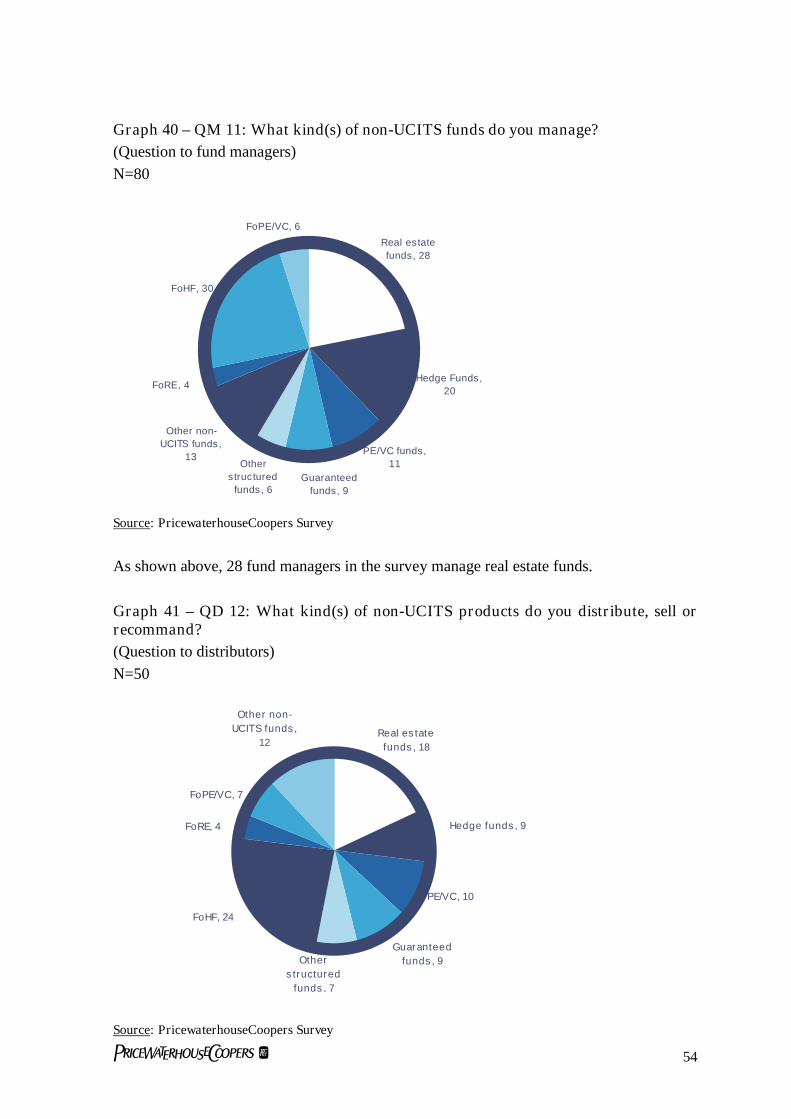

Graph 40 – QM 11: What kind(s) of non-UCITS funds do you manage? 54

Graph 41 – QD 12: What kind(s) of non-UCITS products do you distribute, sell orrecommand? 54

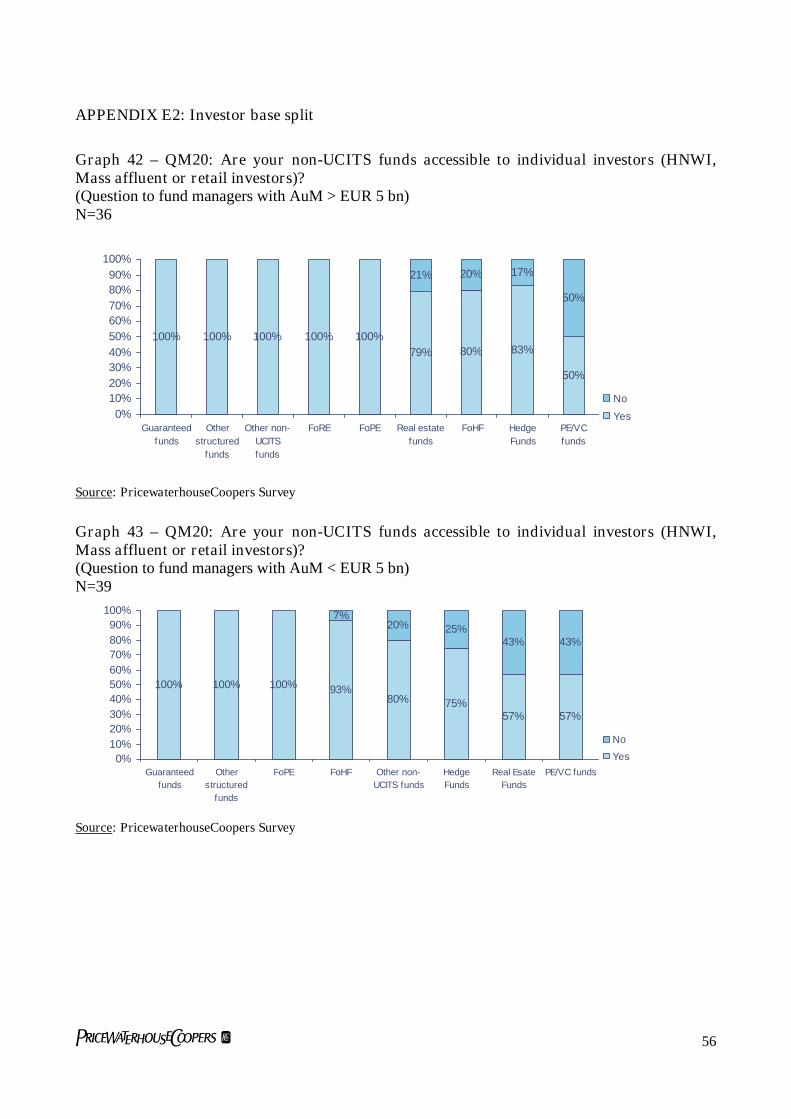

Graph 42 – QM20: Are your non-UCITS funds accessible to individual investors (HNWI,Mass affluent or retail investors)? 56

Graph 43 – QM20: Are your non-UCITS funds accessible to individual investors (HNWI,Mass affluent or retail investors)? 56

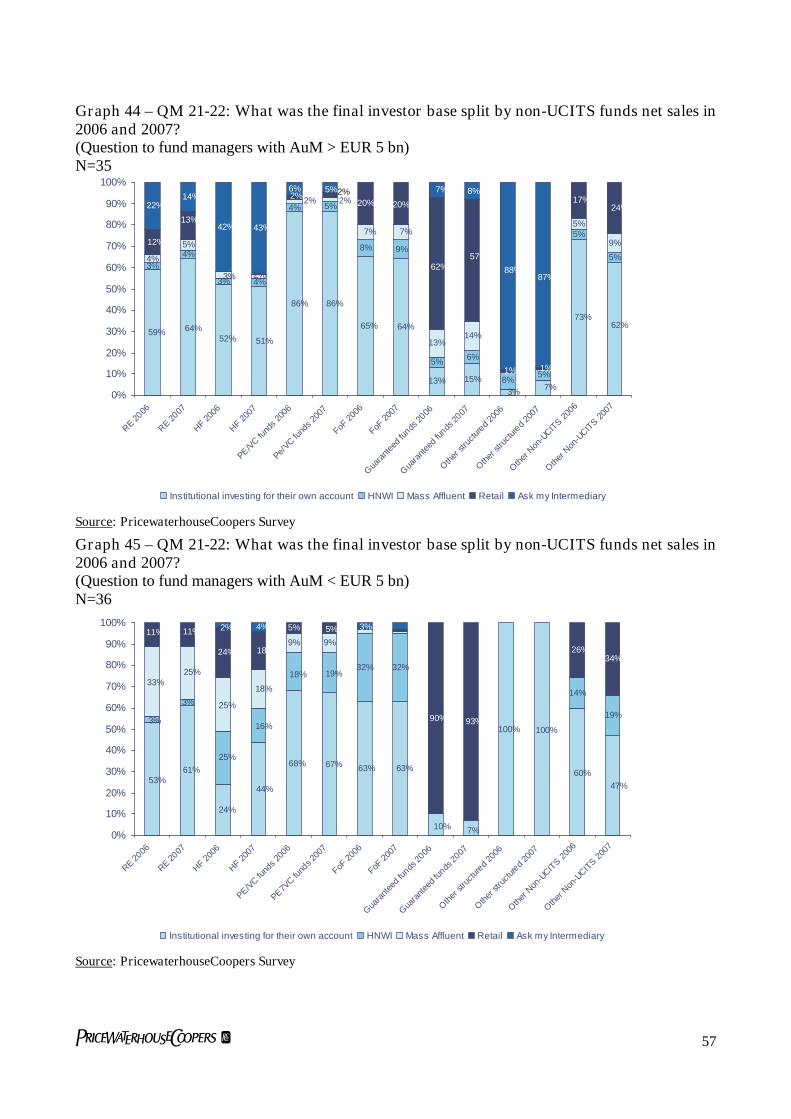

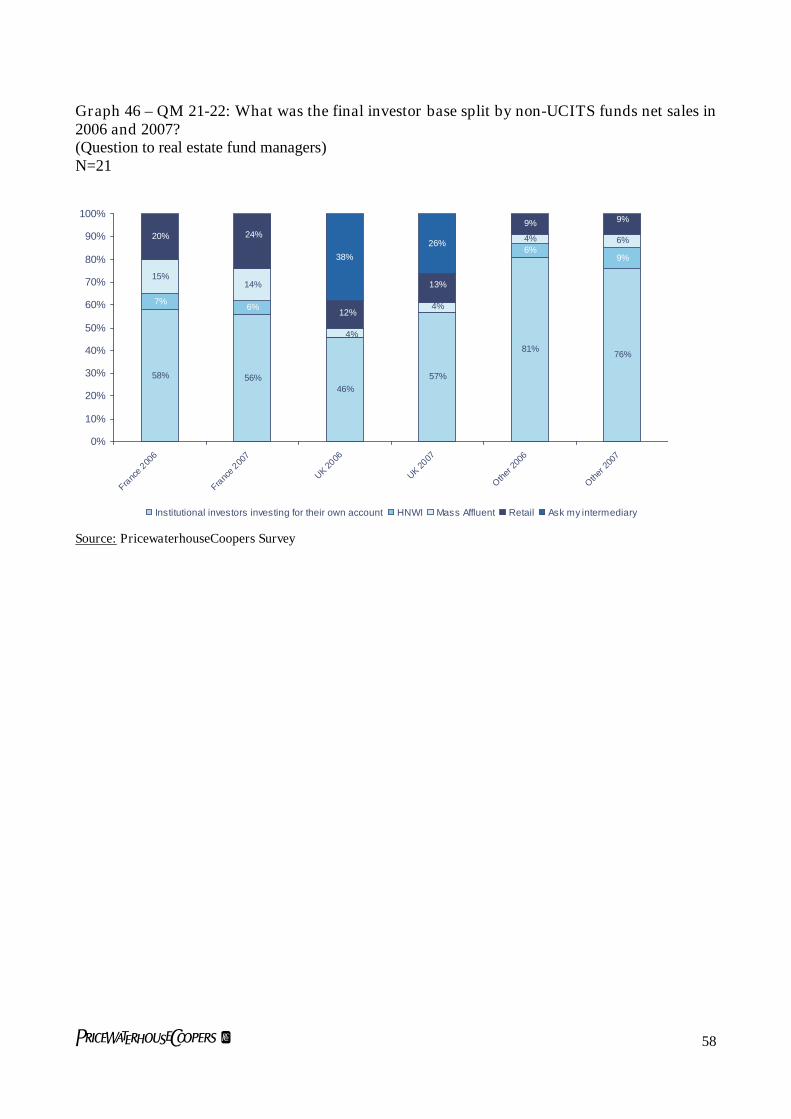

Graph 44 – QM 21-22: What was the final investor base split by non-UCITS funds netsales in 2006 and 2007? 57

Graph 45 – QM 21-22: What was the final investor base split by non-UCITS funds netsales in 2006 and 2007? 57

Graph 46 – QM 21-22: What was the final investor base split by non-UCITS funds netsales in 2006 and 2007? 58

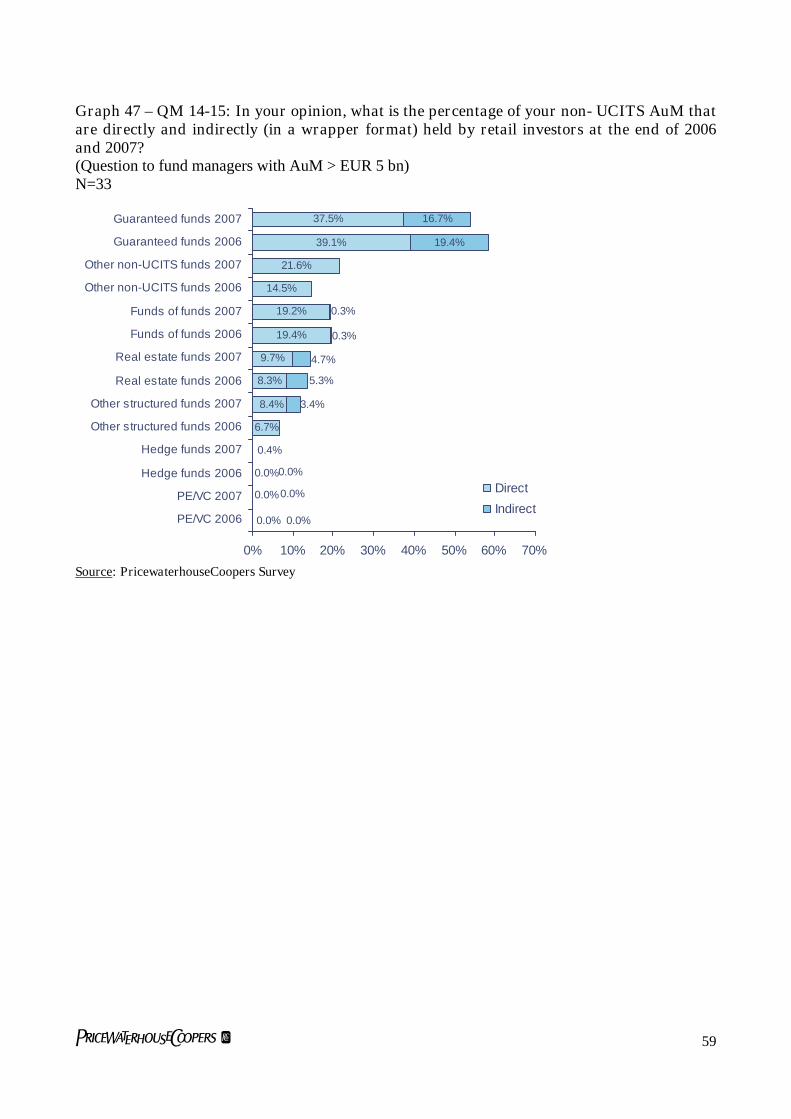

Graph 47 – QM 14-15: In your opinion, what is the percentage of your non- UCITS AuMthat are directly and indirectly (in a wrapper format) held by retail investors at the end of2006 and 2007? 59

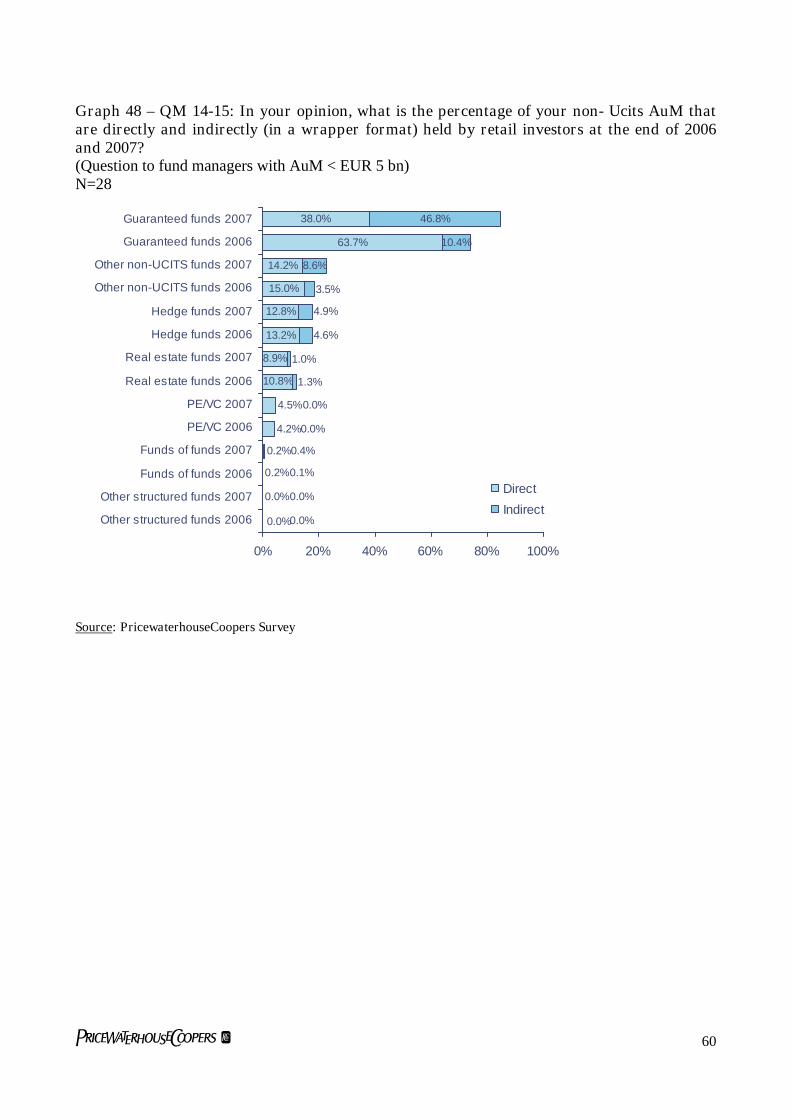

Graph 48 – QM 14-15: In your opinion, what is the percentage of your non- Ucits AuMthat are directly and indirectly (in a wrapper format) held by retail investors at the end of2006 and 2007? 60

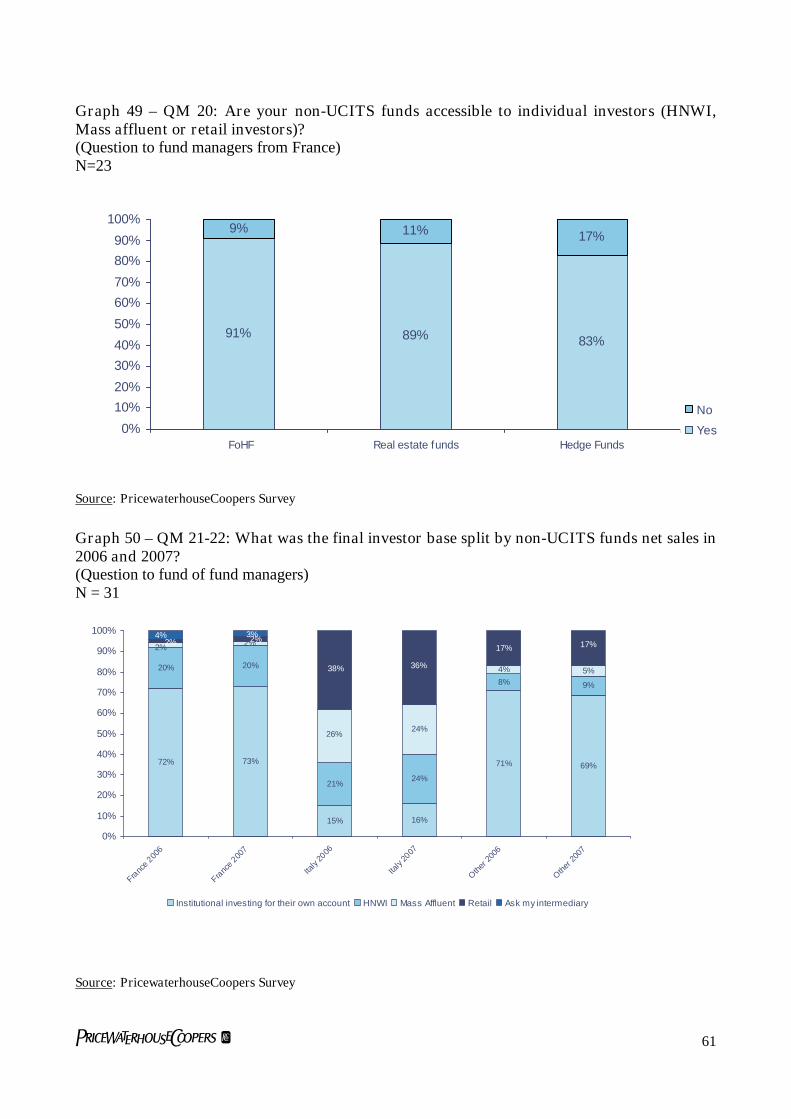

Graph 49 – QM 20: Are your non-UCITS funds accessible to individual investors (HNWI,Mass affluent or retail investors)? 61

Graph 50 – QM 21-22: What was the final investor base split by non-UCITS funds netsales in 2006 and 2007? 61

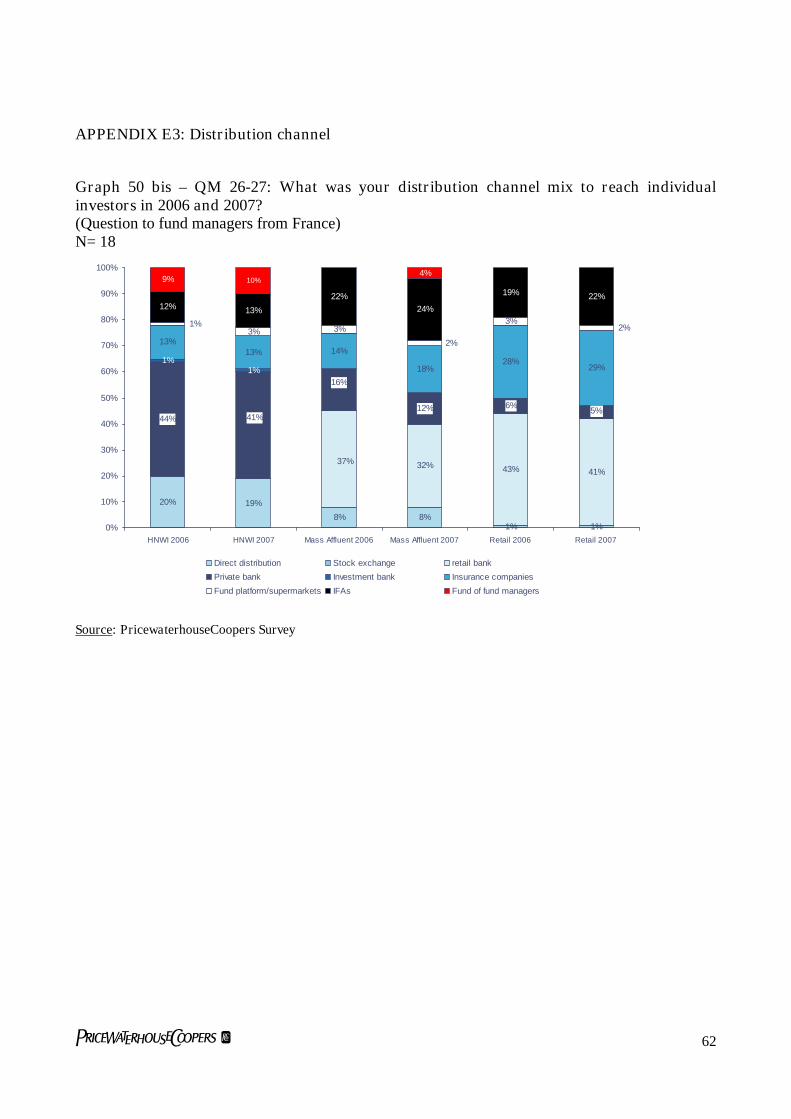

Graph 50 bis – QM 26-27: What was your distribution channel mix to reach individualinvestors in 2006 and 2007? 62

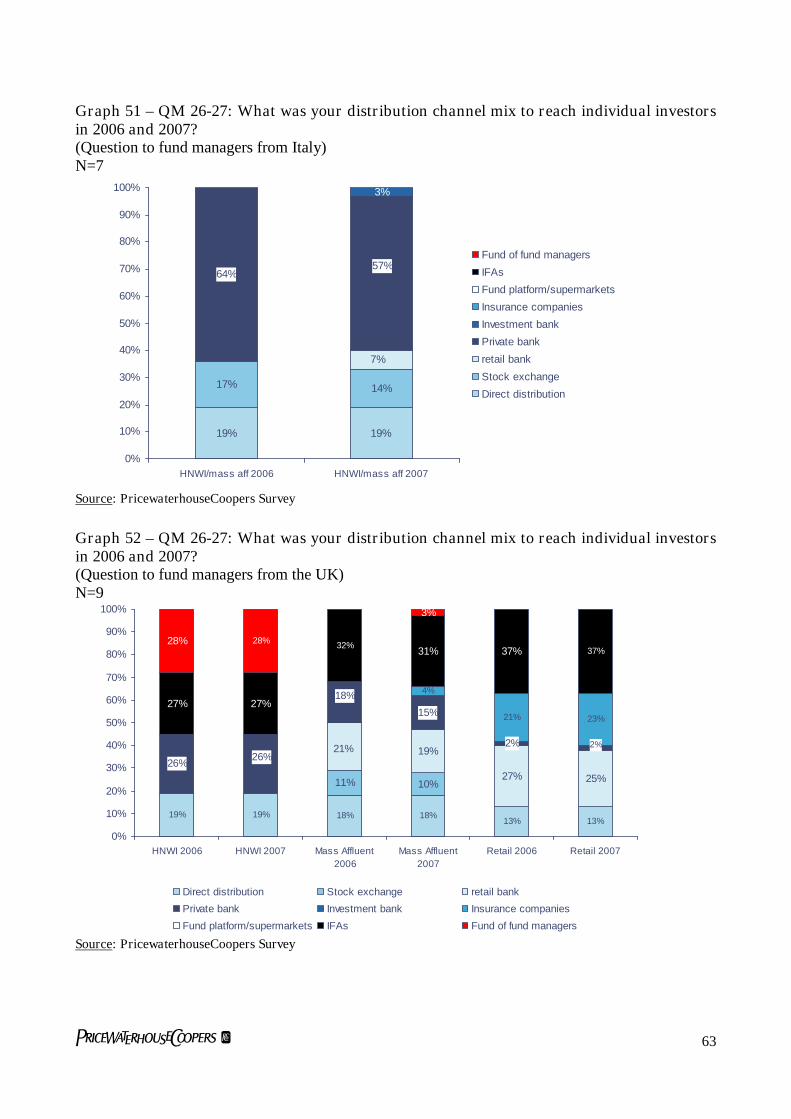

Graph 51 – QM 26-27: What was your distribution channel mix to reach individualinvestors in 2006 and 2007? 63

Graph 52 – QM 26-27: What was your distribution channel mix to reach individualinvestors in 2006 and 2007? 63

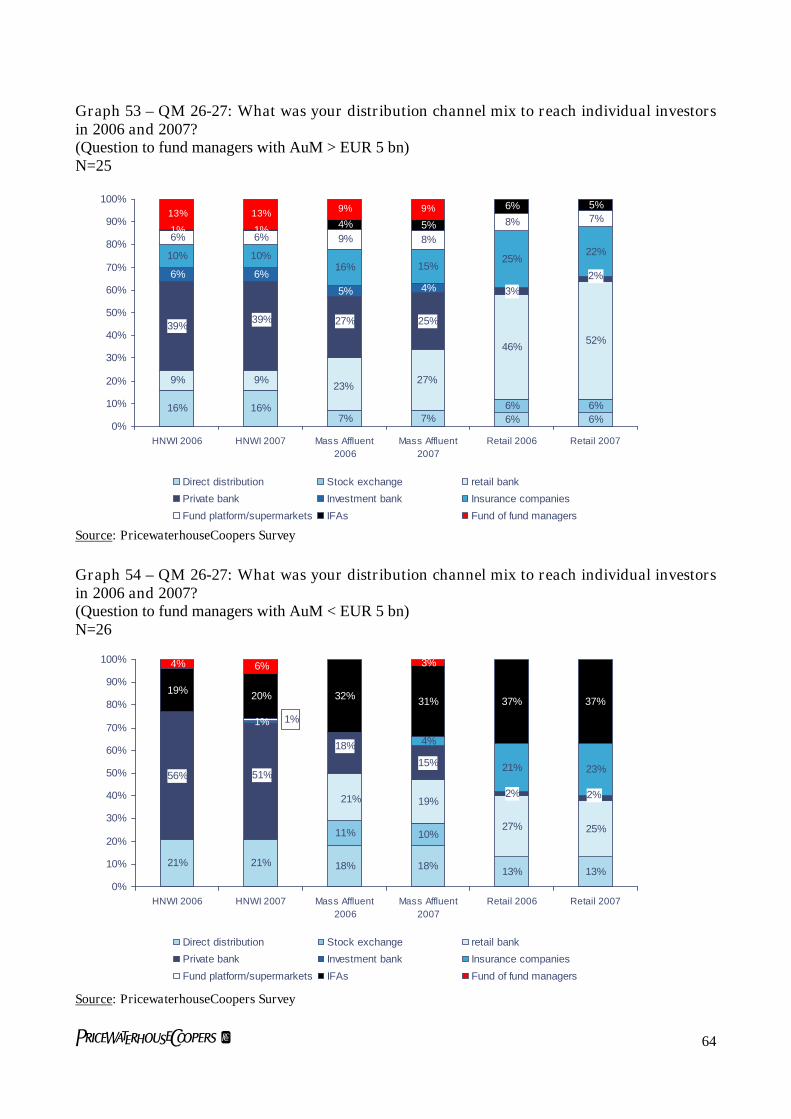

Graph 53 – QM 26-27: What was your distribution channel mix to reach individualinvestors in 2006 and 2007? 64

5

Graph 54 – QM 26-27: What was your distribution channel mix to reach individualinvestors in 2006 and 2007? 64

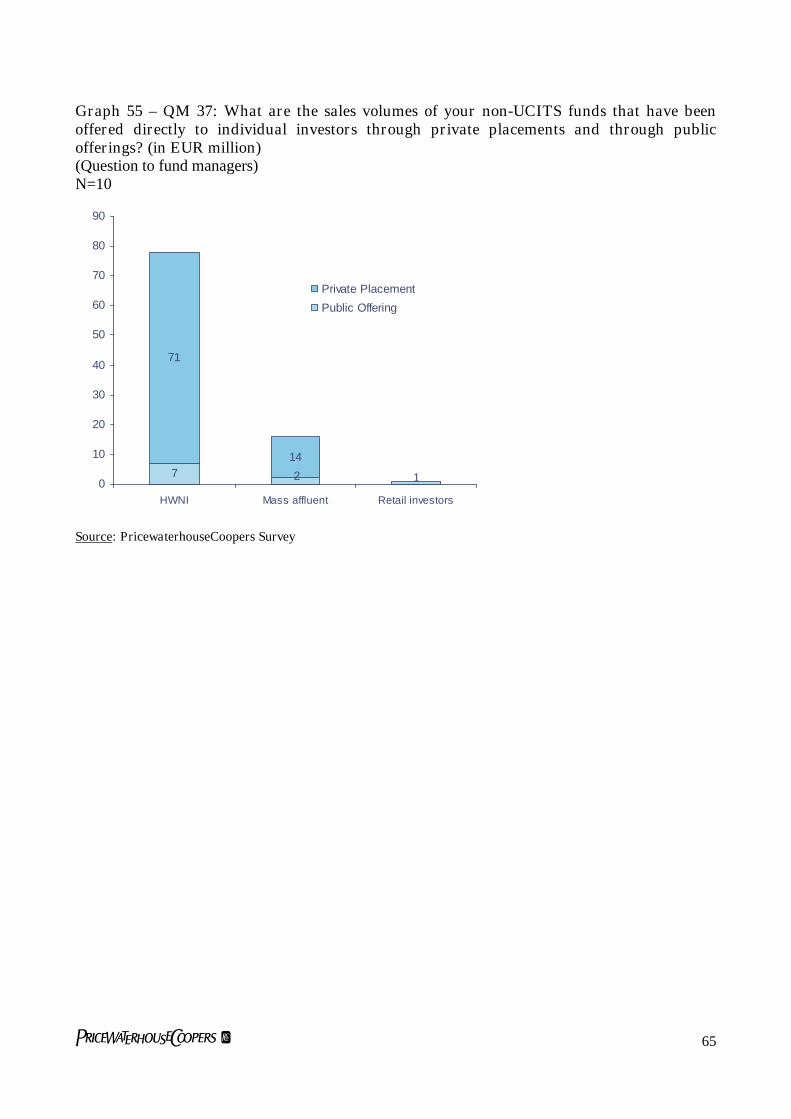

Graph 55 – QM 37: What are the sales volumes of your non-UCITS funds that have beenoffered directly to individual investors through private placements and through publicofferings? (in EUR million) 65

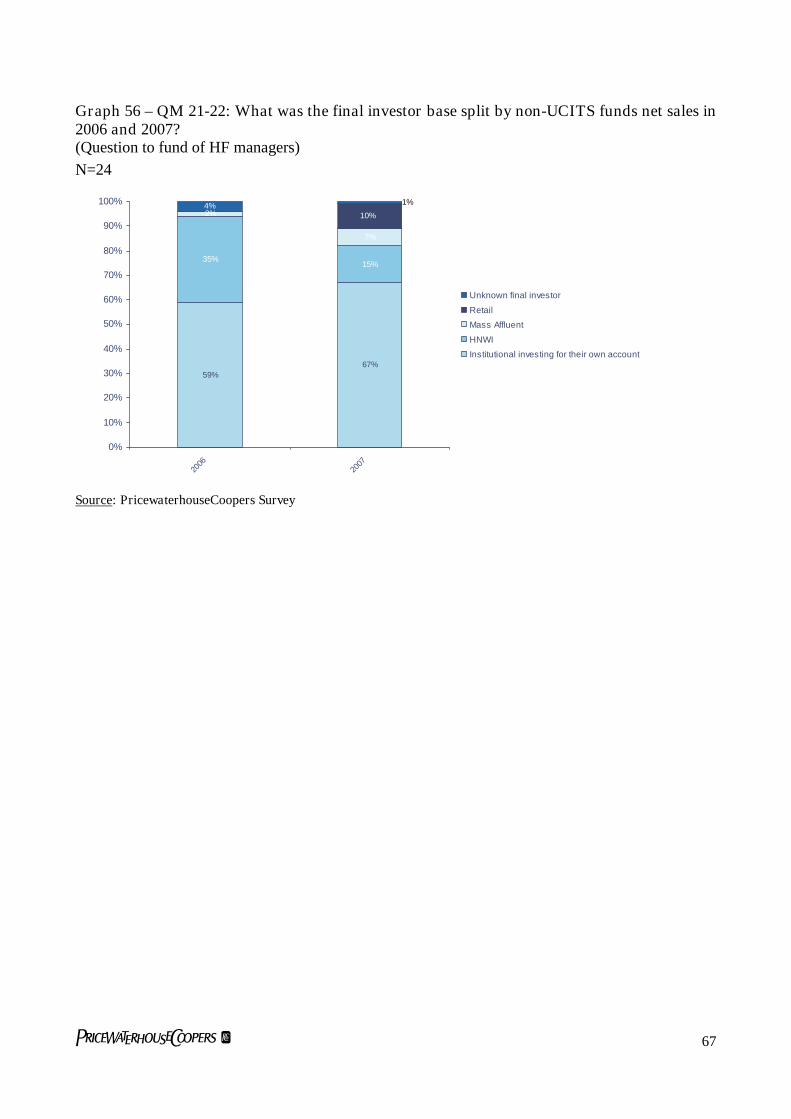

Graph 56 – QM 21-22: What was the final investor base split by non-UCITS funds netsales in 2006 and 2007? 67

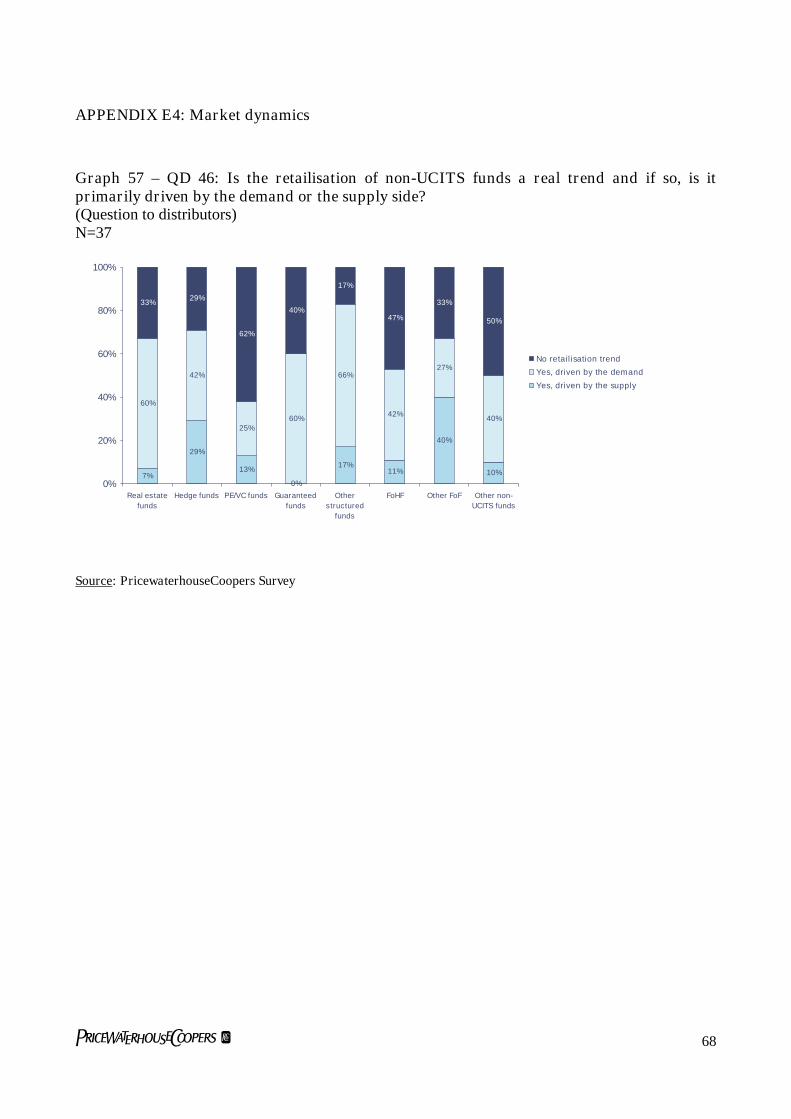

Graph 57 – QD 46: Is the retailisation of non-UCITS funds a real trend and if so, is itprimarily driven by the demand or the supply side? 68

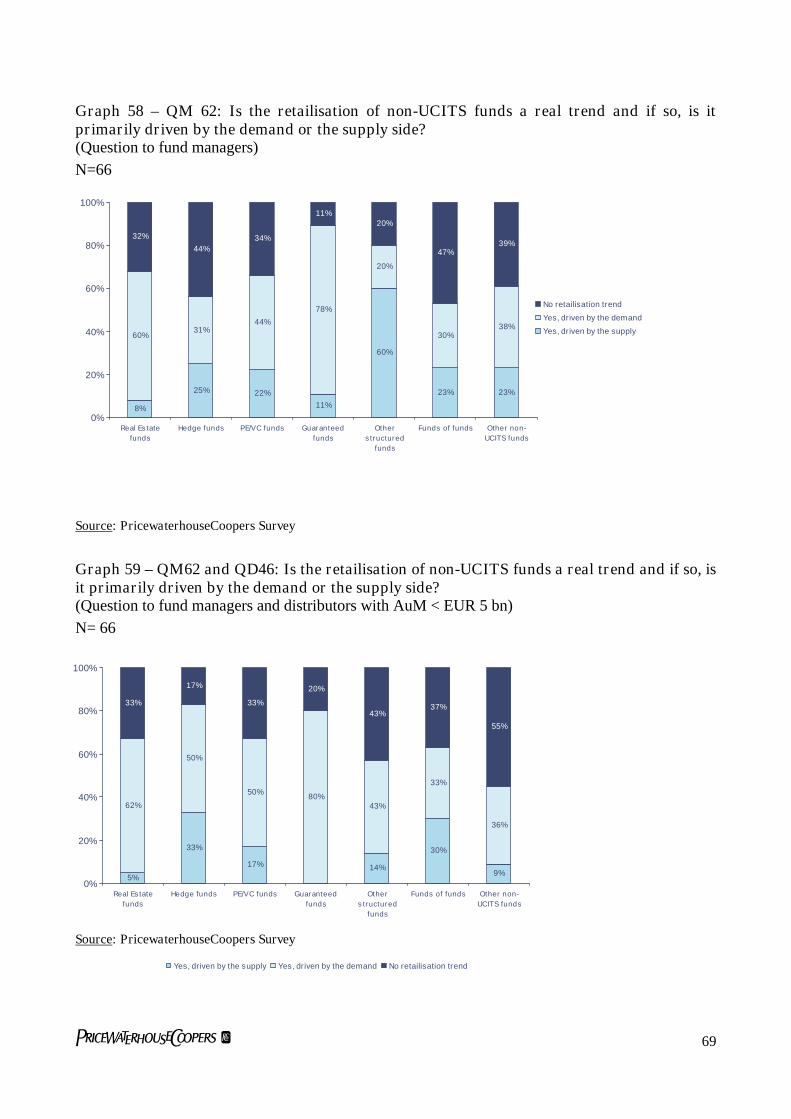

Graph 58 – QM 62: Is the retailisation of non-UCITS funds a real trend and if so, is itprimarily driven by the demand or the supply side? 69

Graph 59 – QM62 and QD46: Is the retailisation of non-UCITS funds a real trend and ifso, is it primarily driven by the demand or the supply side? 69

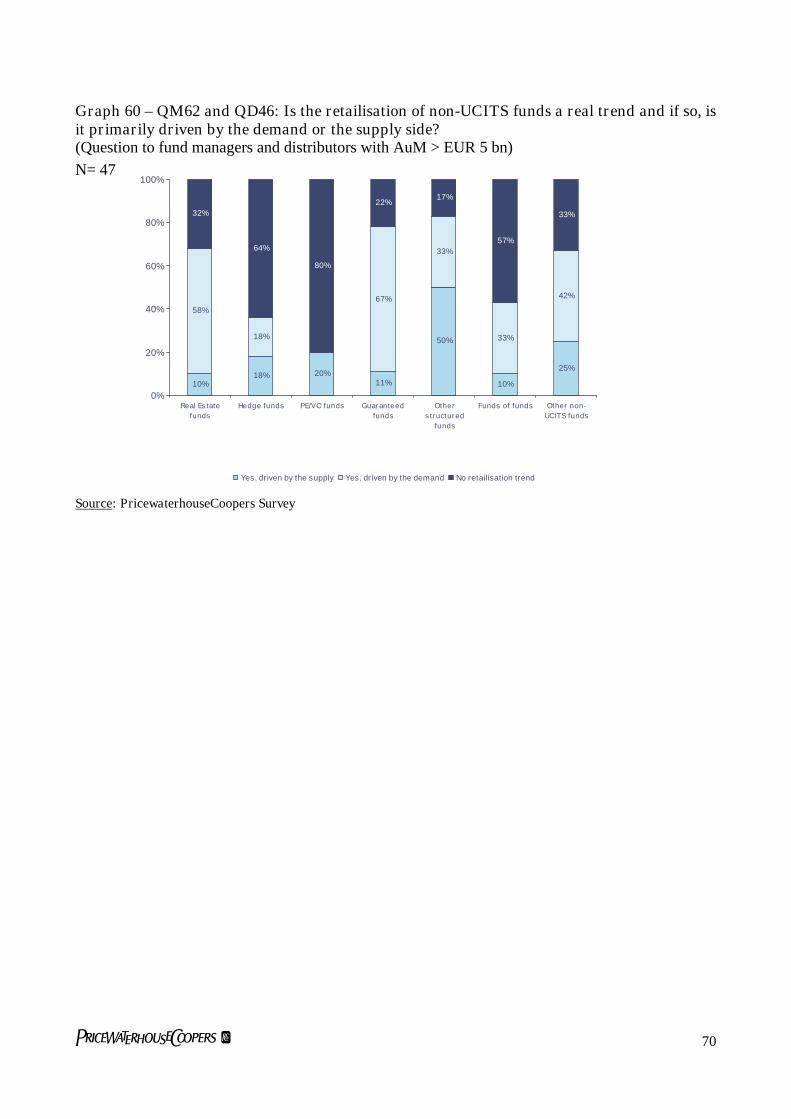

Graph 60 – QM62 and QD46: Is the retailisation of non-UCITS funds a real trend and ifso, is it primarily driven by the demand or the supply side? 70

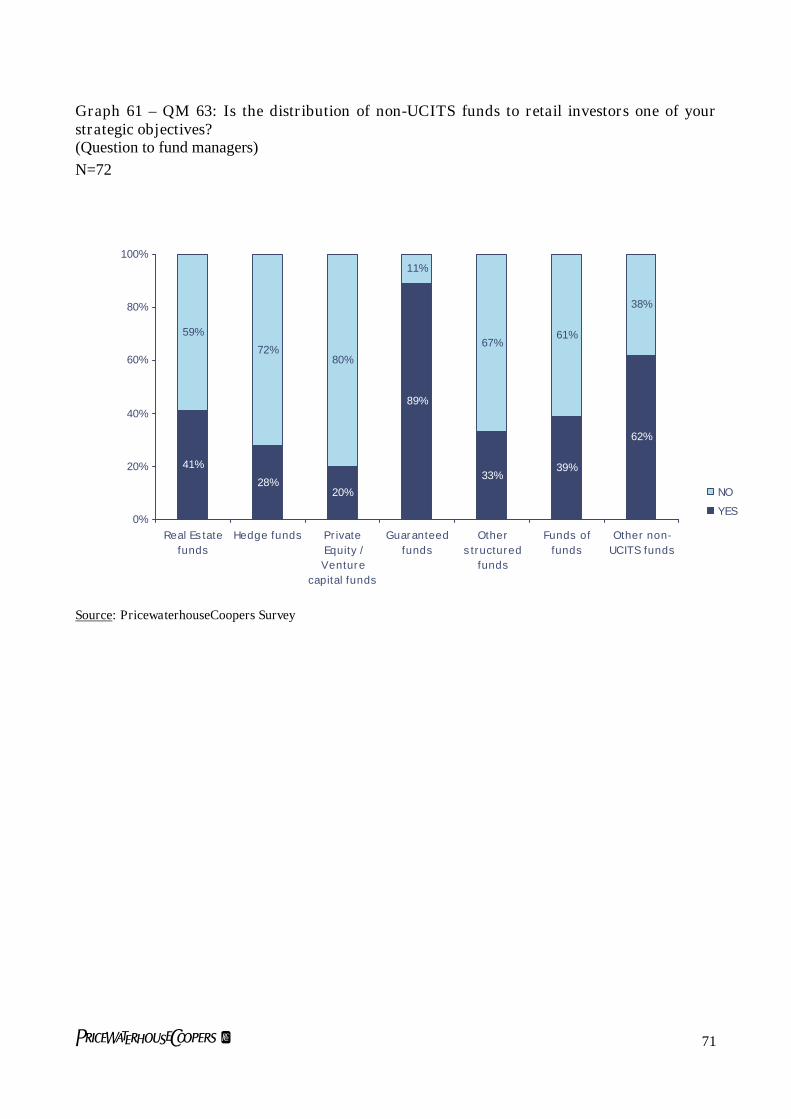

Graph 61 – QM 63: Is the distribution of non-UCITS funds to retail investors one of yourstrategic objectives? 71

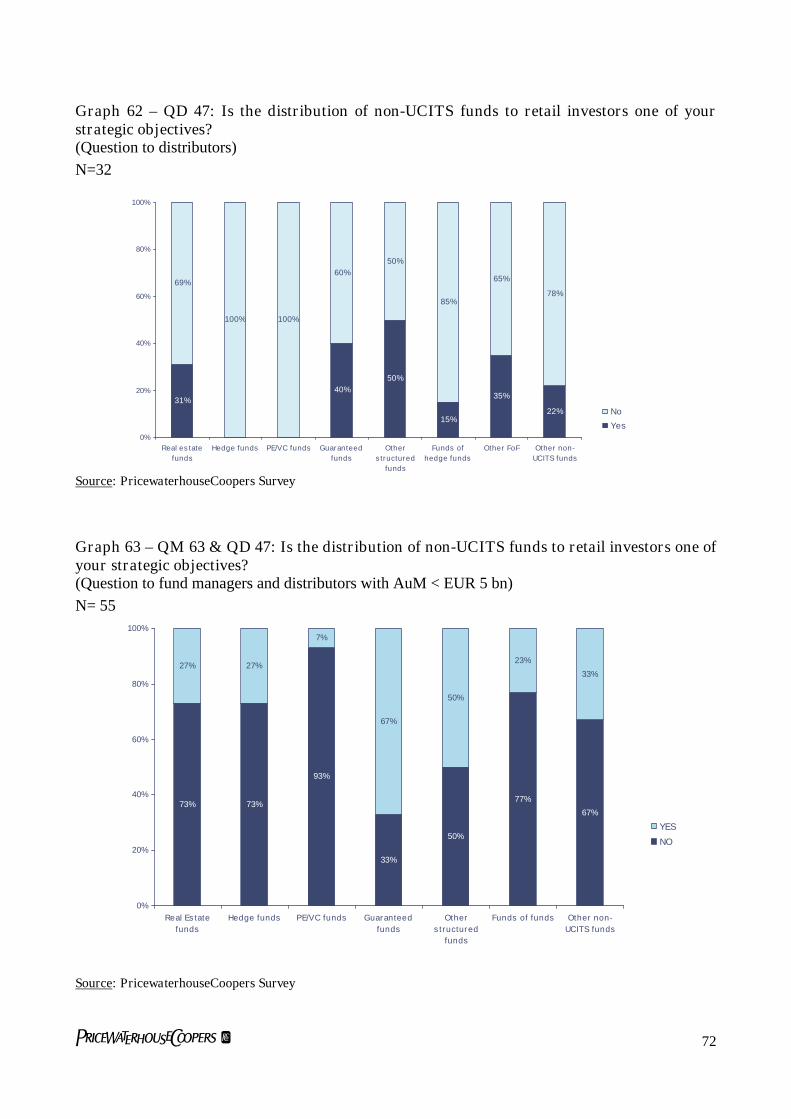

Graph 62 – QD 47: Is the distribution of non-UCITS funds to retail investors one of yourstrategic objectives? 72

Graph 63 – QM 63 & QD 47: Is the distribution of non-UCITS funds to retail investors oneof your strategic objectives? 72

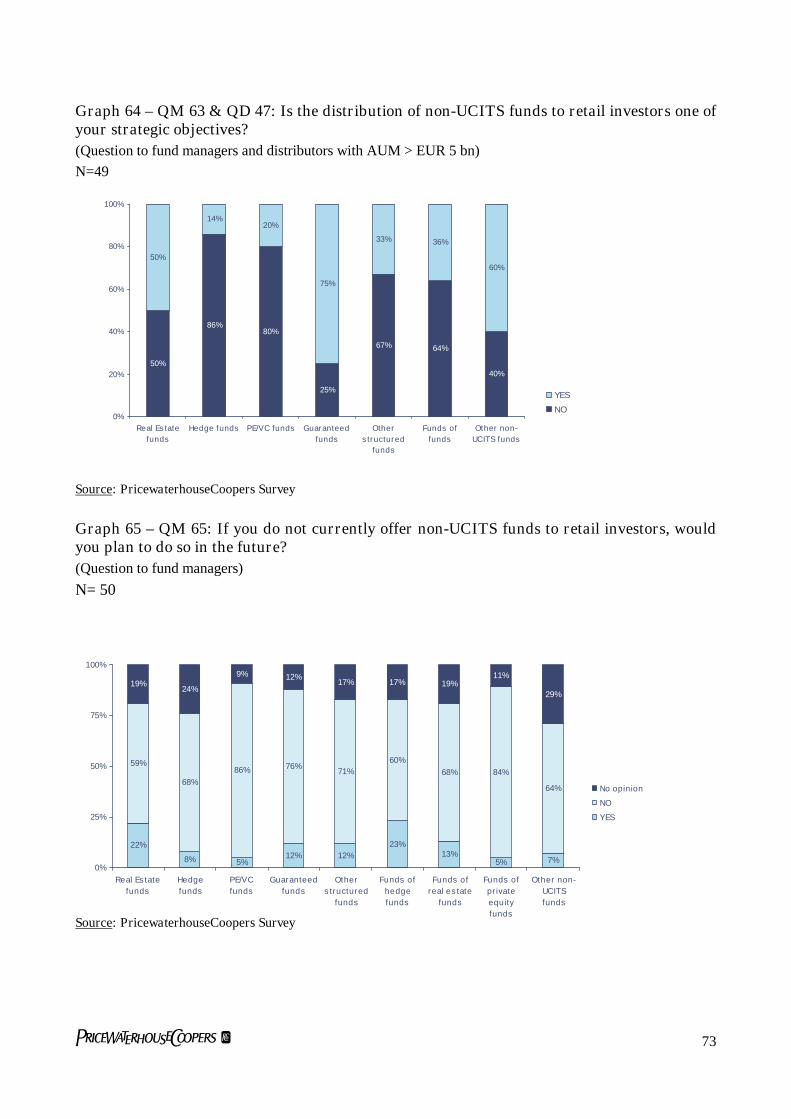

Graph 64 – QM 63 & QD 47: Is the distribution of non-UCITS funds to retail investors oneof your strategic objectives? 73

Graph 65 – QM 65: If you do not currently offer non-UCITS funds to retail investors,would you plan to do so in the future? 73

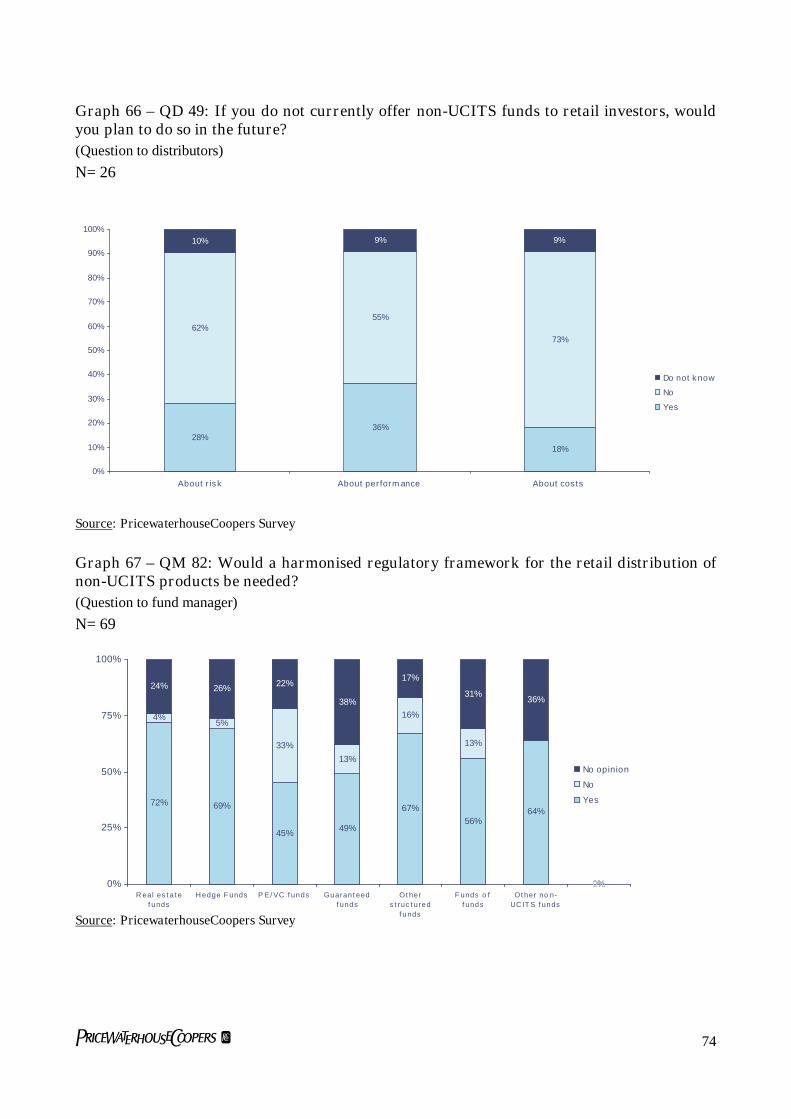

Graph 66 – QD 49: If you do not currently offer non-UCITS funds to retail investors,would you plan to do so in the future? 74

Graph 67 – QM 82: Would a harmonised regulatory framework for the retail distribution ofnon-UCITS products be needed? 74

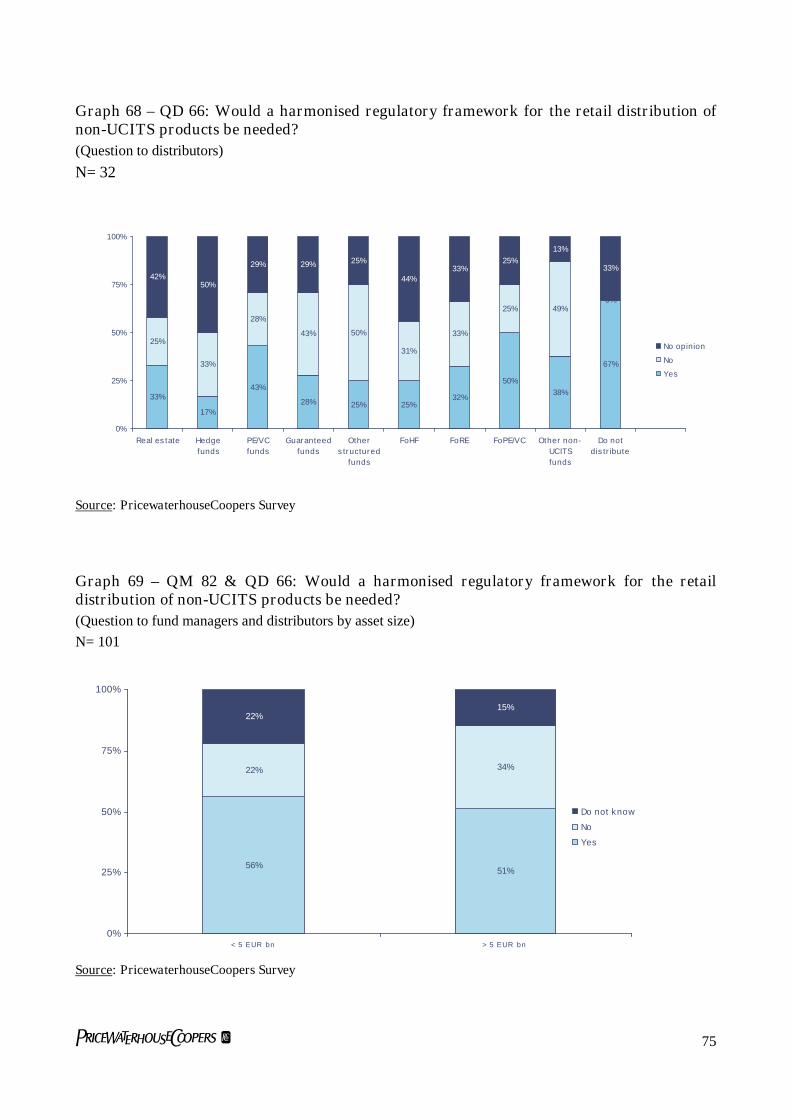

Graph 68 – QD 66: Would a harmonised regulatory framework for the retail distribution ofnon-UCITS products be needed? 75

Graph 69 – QM 82 & QD 66: Would a harmonised regulatory framework for the retaildistribution of non-UCITS products be needed? 75

6

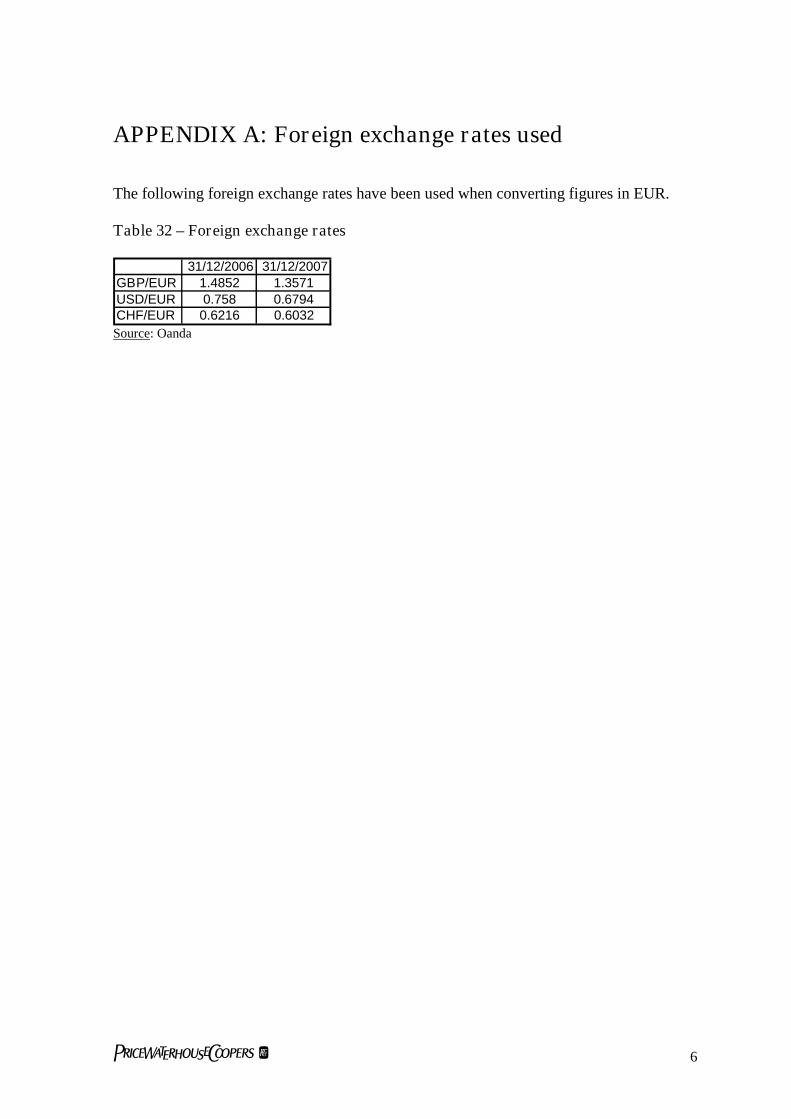

APPENDIX A: Foreign exchange rates used

The following foreign exchange rates have been used when converting figures in EUR.

Table 32 – Foreign exchange rates

31/12/2006 31/12/2007GBP/EUR 1.4852 1.3571USD/EUR 0.758 0.6794CHF/EUR 0.6216 0.6032

Source: Oanda

7

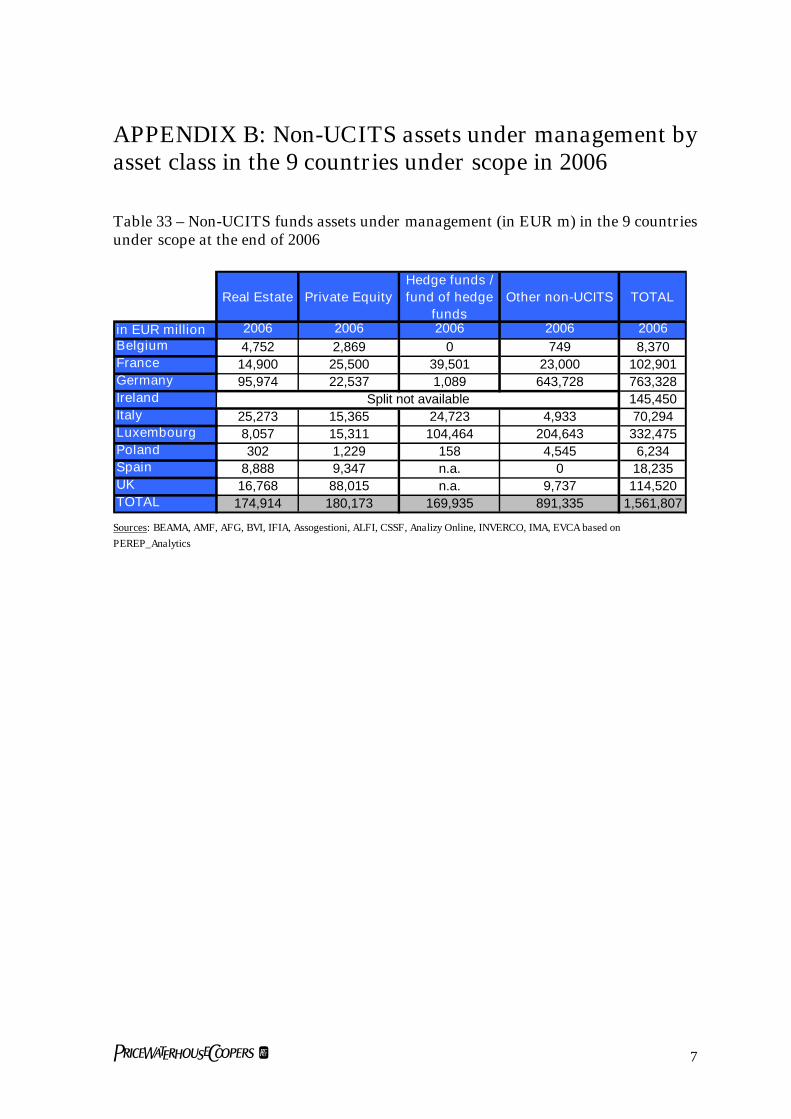

APPENDIX B: Non-UCITS assets under management byasset class in the 9 countries under scope in 2006

Table 33 – Non-UCITS funds assets under management (in EUR m) in the 9 countriesunder scope at the end of 2006

Real Estate Private Equity

Hedge funds /

fund of hedge

funds

Other non-UCITS TOTAL

in EUR million 2006 2006 2006 2006 2006

Belgium 4,752 2,869 0 749 8,370France 14,900 25,500 39,501 23,000 102,901Germany 95,974 22,537 1,089 643,728 763,328Ireland 145,450Italy 25,273 15,365 24,723 4,933 70,294Luxembourg 8,057 15,311 104,464 204,643 332,475Poland 302 1,229 158 4,545 6,234Spain 8,888 9,347 n.a. 0 18,235UK 16,768 88,015 n.a. 9,737 114,520TOTAL 174,914 180,173 169,935 891,335 1,561,807

Split not available

Sources: BEAMA, AMF, AFG, BVI, IFIA, Assogestioni, ALFI, CSSF, Analizy Online, INVERCO, IMA, EVCA based on

PEREP_Analytics

8

APPENDIX C: Regulatory frameworks

9

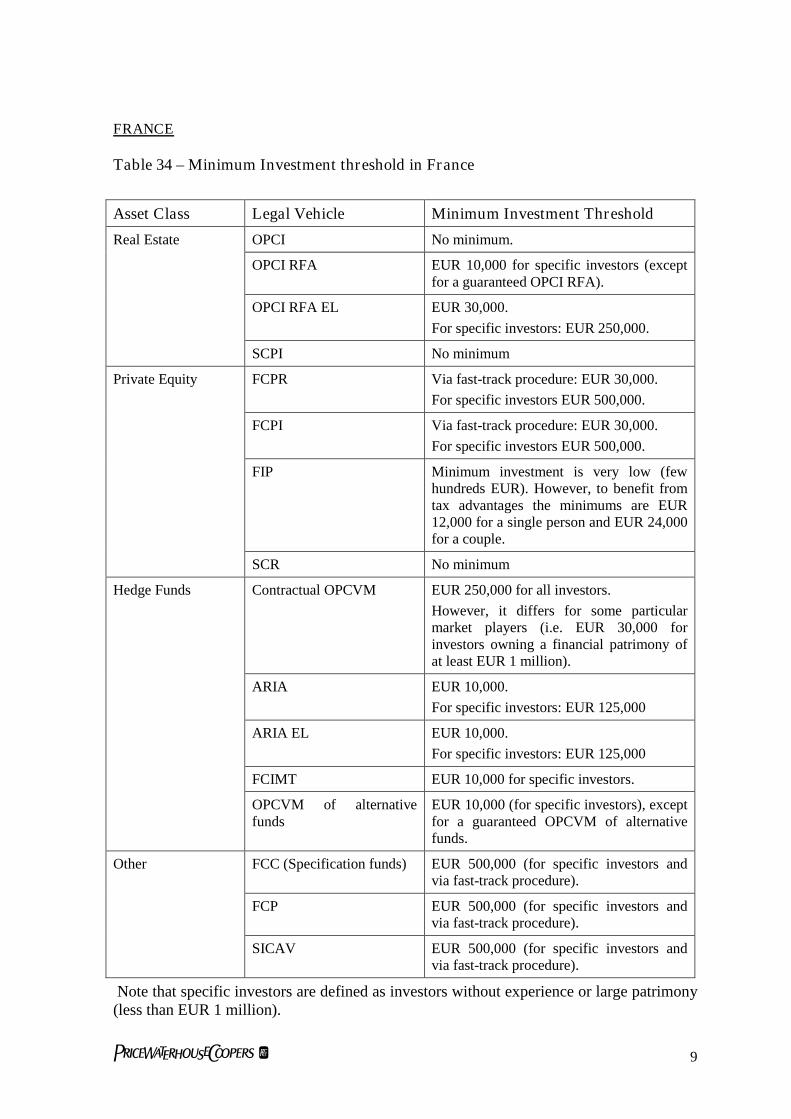

FRANCE

Table 34 – Minimum Investment threshold in France

Note that specific investors are defined as investors without experience or large patrimony(less than EUR 1 million).

Asset Class Legal Vehicle Minimum Investment Threshold

OPCI No minimum.

OPCI RFA EUR 10,000 for specific investors (exceptfor a guaranteed OPCI RFA).

OPCI RFA EL EUR 30,000.

For specific investors: EUR 250,000.

Real Estate

SCPI No minimum

FCPR Via fast-track procedure: EUR 30,000.

For specific investors EUR 500,000.

FCPI Via fast-track procedure: EUR 30,000.

For specific investors EUR 500,000.

FIP Minimum investment is very low (fewhundreds EUR). However, to benefit fromtax advantages the minimums are EUR12,000 for a single person and EUR 24,000for a couple.

Private Equity

SCR No minimum

Contractual OPCVM EUR 250,000 for all investors.

However, it differs for some particularmarket players (i.e. EUR 30,000 forinvestors owning a financial patrimony ofat least EUR 1 million).

ARIA EUR 10,000.

For specific investors: EUR 125,000

ARIA EL EUR 10,000.

For specific investors: EUR 125,000

FCIMT EUR 10,000 for specific investors.

Hedge Funds

OPCVM of alternativefunds

EUR 10,000 (for specific investors), exceptfor a guaranteed OPCVM of alternativefunds.

FCC (Specification funds) EUR 500,000 (for specific investors andvia fast-track procedure).

FCP EUR 500,000 (for specific investors andvia fast-track procedure).

Other

SICAV EUR 500,000 (for specific investors andvia fast-track procedure).

10

ITALY

Procedure for the issuing of the authorization

i) Application for the authorization

An application that includes the following information must be submitted for review:

- details of the applicant company;- name of the fund whose units are intended to be offered in Italy;- name of the subject entitled for the payments, name of the subjects appointed for

the distribution in Italy of the fund units, (if different);- full details of the person who executes the application and his/her powers;- a list of the documents attached to the application.

ii) Documentation to be provided

a) documentation related to the domestic regulatory supervision, which consist in adeclaration of the domestic supervision authority stating that:

- the fund and the management company are subject to the supervision authority andthe management company has an adequate corporate governance, administrativeand accounting structure; it must illustrate all the controls done towards themanaging company and toward the specific product;

- the fund currently offers its units in its home country;- the fund is compliant with its domestic provision related to the set-up of a

secondary seat in Italy, if the fund intends to set it up (it is not mandatory);- the managers of the fund hold the eligibility requirement foreseen by the Italian

legislation.

b) documentation related to the disclosure of information to the public, consisting ofthe following:

- a copy of the fund by-laws, or a copy of the by-laws of the investment company;- the latest offering circular (Prospectus) and the further offering documentation sent

to the domestic supervision authority, with a declaration of the same authority thatsuch documentation is the latest received for approval (should it be subject toapproval);

- the latest financial statements, if public;- detailed information as to the way of disclosing to the public all the costs related to

the units.

c) documentation related to the operating pattern, consisting of the following:

- a report on the operating pattern which the fund intends to adopt to offer its unitsand to ensure proper exercise of financial rights to its unitholders;

- a copy of the agreement with the subject appointed for the payments, with thesubject who is entitled to offer and distribute the units in Italy;

11

- if a secondary seat is registered in Italy, with the task of dealing with the public, ithas to be provided its number of registration in the company register;

- a copy of the agreement with the Italian intermediary entitled to deal with thepublic (if existing);

- a list of the managers of the Italian secondary seat with a declaration of the powersto act on behalf of the company.

- the same documentation required by the Italian law proving that the eligibilityrequirement for fund managers are met.

d) other documentation, consisting of:

- an explanatory report about the operating pattern of the fund (as described further);- a document containing a brief description of the business plan of the fund.

After submission of the above mentioned documentation, Bank of Italy, after consultationwith Consob, is entitled to issue the authorization. The Bank of Italy will issue theauthorization within four months upon the receiving of the application. The term issuspended in the event the documentation provided is lacking of any relevant requirement;in this case Bank of Italy is entitled to ask for completions and the fund is informed of thesuspension of the above mentioned term.

iii) Operating pattern of the foreign non-UCITS fund

In order to issue the authorization, Bank of Italy – after consultation with Consob- isentitled to assess whether the operating pattern of the foreign fund matches the relevantpattern foreseen for domestic funds.

To allow this evaluation, the applicant fund must send an explanation report (see previousd) in which the following aspects are illustrated:

A- the features of the product offered:- the fund business plan and the associated risks;- type of investors to which the offer is addressed, both in its home country and in

Italy;- modality of participation to the fund, especially with reference to the issue and

redemption of the units;- the fund type, closed or open ended;- the legal structure of the fund;- the prudential investment rules;- the information given to the members;

B- the depositary:- the existence of a depositary to whom is entrusted the custody of the asset of the

fund. This subject must grant the same level of investor protection foreseen byItalian law.

12

iv) Documentation and information to be provided to the public

The fund must keep publicly, both by the subject which is entitled for the offer and for thepayments, the following elements:

- the value of the single units of the quota/shares of the fund;- the information to be disclosed under its domestic law;- supplementary accounting information;- if the fund works under an operating agreement, the call notice of the meeting of

the members and the resolution adopted.

The foreign fund must furthermore publish, in at least one National daily-paper, the mostimportant above-mentioned information.

v) Operating pattern in Italy

Intermediation in the payments

In order to grant the exercise of the financial rights of the Italian members of the fund, andthe disclosure of the information above mentioned, the fund and the depositary must enterinto an agreement with one or several Italian banks (subject entitled for the payments), inorder to perform the intermediary activity in the payments connected to the participation tothe fund.

Relations with the investors

The relations between the Italian investors and the foreign seat of the fund are kept by apurposely appointed subject (the subject entitled for the payments, the secondary seat inItaly, an investment management company SGR, etc.)

In the event the units of the fund are only offered to qualified investors, Bancad’Italia shall authorize operative patterns different from the above-mentioned.

The appointed subject must:

- manage the activity of subscription and the request of redemption, received fromthe subject entitled for the placement;

- ensure the respect of the procedure given by the rules of the fund;- manage the relation with the investors providing periodic statements to the single

investors;- give to the member the certificate representative of the units, if foreseen;- keep the relation with the customers, included the managing of their claims;- care about the publication on the press of the above mentioned information.

Placement of the fund

The fund must enter into an agreement with he subjects appointed for the placement of theunits in Italy, these subjects must bind themselves to:

- send to the fund, the request of subscription, redemption and turning;- deposit by the subject entitled for the payments, the payments means related to the

subscription.

13

IRELAND

Foreign schemes are not authorized by the Financial Regulator but must seek approval toinward market to retail investors and must comply with the provisions as listed withinFinancial Regulator’s notices for non-UCITS funds, in particular, NU19 & NU 9.

Foreign funds as outlined above seeking to market their units in Ireland must adhere to theconditions as listed under NU 19, the Financial Regulator’s non-UCITS Notices. CISwhich propose to market their units in Ireland must be authorised by a supervisoryauthority set up in order to ensure the protection of unit holders and which, in the opinionof the Financial Regulator, provides a similar level of investor protection to that providedunder Irish laws, regulations and conditions governing Irish CIS.

In addition to a review of the manager/ custodial functions, the Financial Regulator willalso undertake an assessment of the foreign fund’s investment objective, policies and riskspreading provisions to make a determination on its equivalency to an Irish CIS. ForeignCIS are compared to the detailed rules for domestic retail CIS and similarly professionalCIS to Irish professional CIS.

It is not uncommon for foreign funds seeking to inward market to be asked to complete thedomestic fund authorisation documentation with a view to measuring the specificdifferences between the domestic regulatory requirements and the foreign fund’sinvestment objectives. Any differences arising are reviewed on a case-by-case basis andimpact to the level of investor protection duly assessed to ensure this does not deviate fromthe standard set for domestic funds.

Under NU 19, a CIS situated in another jurisdiction which proposes to market its units inIreland must make application to the Financial Regulator in writing, enclosing thefollowing information and documentation:

- the full name of the CIS.- the full name and address of the operator.- the full name and address of any supervisory authority or authorities to which theoperator is subject in the state in which the operator is established.- the full name and address of the depositary or custodian.- the jurisdiction in which the fund is authorised.- details of the arrangements for the marketing of units in Ireland.- the full name and address of the establishment in Ireland (hereafter “facilities agent”)where facilities will be maintained where:

(i) unit holders can obtain payment of dividends and redemption or repurchase proceeds

(ii) they can obtain copies of the instrument(s) constituting the CIS, the prospectus, theannual and half-yearly reports can be examined, free of charge, and copies obtained ifrequired; and

(iii) complaints can be made for forwarding to the head office of the operator.

- a statement or certificate from the supervisory authority of the CIS confirming that it isauthorised.- a certified copy of the fund rules or instruments of incorporation.- the prospectus and any amendments thereto.

14

- the latest annual report and any subsequent half-yearly report.- a copy of any other document affecting the rights of unit holders in the CIS.- confirmation from the facilities agent that he/she has agreed to act for the CIS.

Documentation submitted to the Financial Regulator must be in English or Irish or must beaccompanied with a translation in English or Irish. Marketing of units in Ireland may nottake place until the CIS receives a letter of approval from the Financial Regulator.

The following statement must be included in a prominent position in each copy of theCIS’s prospectus and in any marketing material distributed in Ireland for the purposes ofpromoting the CIS:

The prospectus of the CIS must provide the following information for Irish investors:

- details of the facilities agent and the maintained facilities;- provisions of Irish tax laws, if applicable;- details of the places where issue and repurchase prices can be obtained or are

published;- the minimum subscription requirement in the case of schemes which market solely

to professional investors.

CIS marketing their units in Ireland must comply with the provisions of the Code ofAdvertising Standards for Ireland. Schemes marketing their units in Ireland must complywith the provisions of the Code of Advertising Standards for Ireland. The code is availablefrom the Advertising Standards Authority for Ireland, 35/39 Shelbourne Road, Dublin 4.The standards are also outlined in the Financial Regulator’s Non-UCITS Notices, NU 9,under “Advertising”.

CIS marketing their units in Ireland must comply with the law, regulations andadministrative provisions in force in Ireland. (Financial Regulator’s Notices, relevantcompany law, advertising standards and the Regulator’s administrative provisions).

The annual and half-yearly reports issued by CIS marketing their units in Ireland must besubmitted to the Financial Regulator as soon as they are available.

When a CIS has received approval from the Financial Regulator to market units in Irelandthe name of the CIS and the name and address of the facilities agent will be placed on a listof CIS marketing in Ireland, which will be made available to public on request.

15

APPENDIX D: Taxation frameworks

Appendix D1: Belgium

Taxation of ongoing income

- Non transparent funds:

Domestic funds

Distributions from a domestic opaque fund to a DRI (Domestic Retail Investor) would betreated as dividends subject to WHT at 15%. No further taxation would be suffered by theDRI.

A number of special regimes would apply:

- PRICAF/PRIVAK (i.e. private equity investment company mainly investing innon-quoted companies and growth companies): the portion of dividends distributedto a DRI corresponding to capital gains realised on shares by the PRICAF/PRIVAKwould be exempt from WHT.

- SICAFI/BEVAK (i.e. real estate investment company with fixed capital): dividendsdistributed to a DRI would be exempt from WHT should certain conditions be met(i.e. at the end of the financial year to which the dividends are referred, at least 60%of the immovable goods of the fund should be invested directly or indirectly inimmovable goods located in Belgium and affected to/ intended exclusively forhousing).

Foreign funds

Distribution from a foreign opaque fund to a DRI would be considered as foreign sourcedividends. Domestic WHT would apply on the net-frontier income (i.e. income afterforeign WHT). In principle, the rate for WHT would be 25%. However, municipalsurcharge would be added to these 25% where no WHT would have been retained in theabsence of a Belgian financial intermediary involved in the movable income payment.

A reduced WHT rate of 15% (plus municipal surcharge in absence of Belgian financialintermediary) would be applicable to certain distributions linked to shares issued as fromJanuary 1, 1994, which represent share capital and were subscribed in cash. This ratewould apply on the following:

(i) dividend distributions relating to shares issued in the context of a public offering, or,(ii) dividend of shares which were the object since their issuance:

- of a nominative inscription with the issuer (for nominative shares);- of an uncovered deposit in Belgium, under certain conditions, with a Belgian

financial institution subject to the control of the Belgian Banking, Finance andInsurance Commission (for bearer shares);

16

- of an inscription in an account in Belgium, in the name of its owner, with asettlement entity or an accountholder which is entitled to hold such titles, under theconditions and procedures of application determined by Royal Decree (fordematerialised shares).

- Transparent funds:

Domestic funds

A Belgian WHT would in principle be retained (either by the Belgian debtor or by theBelgian management company of the fund) upon attribution of the underlying income tothe domestic fund. The tax rate would depend on the nature of the underlying income (i.e.25% on dividends except when a reduced rate of 15% or 10% would apply; 15% oninterest; in principle exemption for capital gains). No taxation would be suffered at thelevel of the DRI on distributions to the DRI.

Foreign funds

The application of tax transparency to foreign funds would be, among others1, subject tobreakdown filing requirements2. The breakdown identifies the nature and source of theincome received. Difficulties may however arise to provide the required evidence.

If a breakdown is provided, a Belgian WHT would be levied on the non-Belgian sourceincome (e.g. dividends, interest) only. The Belgian WHT rate on said non-Belgian sourceincome would then depend on the nature of the underlying income (i.e. 25% on dividendsexcept when a reduced rate of 15% or 10% would apply; 15% on interest; in principleexemption for capital gains). Indeed, Belgian source income should have normally alreadysuffered Belgian WHT upon attribution to the foreign fund. This WHT would be collectedby the Belgian financial intermediary. The capital gain component of the coupon couldbenefit from an exemption if satisfactory evidence with respect to the various componentsof the coupon would be provided.

Should this breakdown not be provided, the whole income distributed by the foreign fundwould become taxable as interest. This would entail: (i) a double taxation of Belgiansource income (i.e. as they would have already been subject to Belgian WHT uponattribution to the foreign fund), and (ii) the application of WHT at 25% on foreign sourceincome (which could have been subject to a lower tax rate if a breakdown of the couponhad been provided)3.

1 Whether or not a fund would qualify as a tax transparent entity constitutes a highly technical question whichtraditionally requires a so-called “lex societatis”/ “lex fori” approach. If the vehicle has legal personality from a localcorporate law perspective (“lex societatis”), the Belgian tax authorities would in principle agree to consider it as anopaque vehicle from a Belgian tax perspective. If not, the fund would be considered as tax transparent. If not clearenough, the question should be addressed by determining whether the vehicle presents legal characteristics that, from aBelgian corporate law perspective, are constitutive of legal personality (“lex fori”).Where the “lex societatis” test is not fulfilled, it is of common practice to introduce a ruling request with the Belgian taxauthorities in order to obtain comfort on the tax treatment of the fund.2 A Royal decree detailing the breakdown to be provided is foreseen, albeit not yet published.3 Until publication of the Royal decree (please, refer to note 3), it is unclear whether the former administrative guidelinesstating that a 15% Belgian WHT should be retained, is still applicable.

17

Taxation of capital gains upon disposal of his units/ shares by the DRI

- Transparent and non transparent funds

Capital gains realised by a DRI upon disposal of his units/ shares in a domestic/ foreignfund would, in principle, be tax-exempt4. However, capital gains realised by a DRI with aspeculative aim could be taxable (even if it was considered as outside the exercise of anoccupational activity).

The income paid or attributed by a domestic/ foreign opaque guaranteed fund to a DRI,which is derived from shares upon the partial distribution of their assets or at the occasionof the redemption of their own shares, would be re-characterised as interest, assuming that,on the occasion of the public offer in Belgium of these shares, guarantees (relating to theamount to be reimbursed or the return on the investments) were entered into relating to aperiod equal to or inferior to 8 years.

Other taxes (e.g. net wealth tax, stamp duties)

To the best of our knowledge, as regards to taxes such as net wealth tax, stamp duties, etc,the same tax treatment would apply to DRIs in domestic and in foreign funds.

Cross-border taxation aspects

- Double Tax treaty

DRIs in domestic/ foreign transparent funds may benefit from a Double Tax Treaty(hereafter referred to as “DTT”) concluded between Belgium and the source country (i.e.the country from which the underlying income arises). In practice, this situation rarelyapplies as sufficient information would generally not be available. DTTs as such would notin general be applicable to foreign transparent funds as they would not in most cases beconsidered as Resident within the meaning of the DTT.

DRIs in a foreign opaque fund would only benefit from the provisions of a DTT if thisfund would qualify as resident within the meaning of the DTT. This condition would rarelybe fulfilled.

- Foreign tax relief

DRIs would only benefit from a foreign tax relief if a DTT would provide for such.

4 As regards foreign transparent funds, according to the current practice of the Belgian players based on administrativedoctrine, tax transparency principles are only applicable to distribution of income by such funds, and not torealised/unrealised capital gains/losses on units of such funds. Therefore, in practice, realized capital gains on units offoreign transparent funds are currently tax exempt, although this interpretation of the Belgian tax law is not fully correctfrom a technical point of view. This is currently debated on the Belgian market.

18

- Controlled Foreign Corporations rules

Special consideration should be given to article 344 § 2 of the Belgian income tax code.This article is an anti-abuse of law provision stipulating the following:

“Legal acts of sale, cession or contribution to capital of shares, bonds, receivables,intellectual property rights or sums of money cannot be upheld towards the Belgian taxauthorities if such transfers are made to a non-resident taxpayer who, in the country wherehe is established, is not subject to tax on income or is subject to a tax regime on the incomegenerated by the income transferred that is markedly more favourable than that whichwould have been applied in Belgium on similar income. The taxpayer can refute this legalpresumption by proving that the transaction corresponds with legitimate financial oreconomic needs or that he received consideration for the transfer producing incomesubject to taxation in Belgium which, when compared to the taxation which would haveapplied had the transfer not taken place, may be considered as normal.”

This anti-abuse provision could theoretically apply (even if rarely used in practice), givensome foreign opaque funds are not subject to any income tax in their country of residence(e.g. Luxembourg SICAV).

Wrappers

Commonly used wrappers in Belgium would be unit-linked insurance products,derivatives, structured products.

The tax regime in the hands of the DRI would vary from products to products, and shouldbe analysed on a case-by-case basis.

At first sight, all other things remaining equal, there should not be major differences in thetax treatment at the DRI’s level between wrappers linked to Belgian funds and wrapperslinked to foreign funds.

19

Appendix D2: France

Taxation of ongoing income

- Domestic funds:

In absence of fund distribution, no taxation would be suffered at the DRI level irrespectiveof the fund being considered as tax transparent (as regards to investment in an FCP, theapplication of this differed taxation regime would be subject to the condition that no DRIwould hold more than 10% of the units in the FCP).

FCP and SICAV

Distributions to DRIs from domestic FCP and SICAV would be subject to taxation asincome from securities (“revenus de capitaux mobiliers”). The tax treatment would varydepending on the nature of the income received by the fund. A regime of tax transparencywould thus apply, albeit taxation would occur only on the income received by the DRI (i.e.differed taxation). Regarding DRIs in SICAV, the benefit of the differentiated taxtreatment as per type of income would be subject to conditions.

- Distribution of dividends: DRIs would be subject to tax at their marginal rate ofincome tax (i.e. up to 40%), plus 11% of social contributions (i.e. up to 51%). If theymeet certain conditions, DRIs would be able to benefit from several tax reliefsincluding a tax relief amounting to 40% of the dividend received. As from 2008,DRIs would be able to elect for taxation at a flat rate of 18% plus 11% of socialcontributions (i.e. 29%).

- Distribution of interest: DRIs would be able to elect for taxation at a flat rate of 18%plus 11% of social contributions (i.e. 29%). Otherwise, taxation would be suffered ata marginal rate of personal income tax.

- Distribution of real estate income: DRIs would be subject to the same tax treatmentas applicable for dividend distributions, albeit they would not be able to benefit fromany tax relief.

- Distribution of capital gains: DRIs would be subject to tax at 18% plus 11% of socialcontributions (i.e. 29%) if the annual amount of sales exceeds EUR 25,000.

20

Other funds

- FCPR/ FCPI/ FIP/ SCR: if certain conditions are met, no taxation would occur at thelevel of the DRI on distributions from such a fund. Social contributions at a rate of11% would still be due.

- SCI/ FPI: distributions from such a fund would be taxed in the hands of the DRI asreal estate income (i.e. taxation at progressive rate of personal income tax up to 40%plus 11% of social contributions).

- SIIC/ SPPICAV: DRIs would suffer taxation on distributions from the fund under theregime applicable for dividend distributions. DRIs would be subject to tax at aprogressive rate of income tax up to 40% plus 11% of social contributions (i.e. up to51%) on 60% of the dividends (i.e. among others, tax relief of 40%). As from 2008,DRIs would be able to elect for taxation at a flat rate of 18% plus 11% of socialcontributions (i.e. 29%).

- Foreign funds:

Distributions from foreign funds would be taxed in the hands of the DRI as income fromsecurities (“revenus de capitaux mobiliers”) at a progressive rate of income tax, up to 40%,plus 11% of social contributions (i.e. up to 51%). A specific analysis would remainrequired depending on the vehicle/ country of residence.

Should the fund be considered as tax transparent from a domestic point of view, DRIswould be taxed on an arising basis (i.e. as the income arises to the fund, whetherdistributed or not).

Taxation of capital gains upon disposal of its units/ shares by the DRI

- Domestic funds

- FCP/ SICAV: DRIs holding shares/ units in domestic FCP or SICAV would besubject to tax under the normal regime applicable for capital gains (i.e. 29%including 11% of social contributions) if the annual amount of sales exceeds EUR25,000 for income received as from 2008.

- FCPR/ FCPI/ FIP/ SCR: capital gains realised by the DRI upon disposal of its shares/interest in such a fund would not be subject to taxation (if certain criteria are met).Only social contributions at 11% would be due.

- SCPI/ FPI: DRI would suffer taxation under the normal regime applicable for capitalgains derived from real estate companies (i.e. 27% including 11% of socialcontributions without any tax relief).

- SIIC/ SPPICAV: DRI would suffer taxation under the normal regime applicable forcapital gains (i.e. 29% including 11% of social contributions for income received asfrom 2008, if the annual amount of sales exceeds EUR 25,000).

21

- Foreign funds

DRI would suffer capital gain taxation at progressive rate of personal income tax (up to40% plus 11% of social contributions).

Disposal of shares/ units in foreign FCP/ SICAV may be taxed at the flat rate of 29% if theannual amount of sales exceeds EUR 25,000 (including 11% of social contributions).As regards to the application of this tax treatment, a specific analysis would remainrequired depending on the vehicle/ country of residence.

DRI in foreign funds bearing comparable features than domestic FCPR/ FCPI/ FIP/ SCR/SCPI/ FPI/ SIIC/ SPPICAV would not benefit from the same tax treatment as thatapplicable to DRI in these domestic funds.

Other taxes

Securities held on January 1 may be included in the tax base for the net wealth tax(taxation at a progressive rate up to 1.8%).

DRIs in certain domestic funds (e.g. in a domestic FIP) may benefit from net wealth taxreliefs as regards to their investment in the fund. Investing in a foreign fund would notenable them to benefit from such reliefs.

Cross-border taxation aspects

- DTT

DRIs in domestic transparent funds (e.g. FCPR/ FCPI/ FIP/ SCPI/ FPI/ FCIMT/ ARIA/ARIEL/ SICAV/ FCP) would in principle benefit (from a French perspective) from theapplicable DTT between France and the source country, should transparency of thedomestic fund be recognised by the source country.

DTT would in general be applicable to DRIs in foreign opaque funds should the foreignfunds be considered as tax resident in its country (subject to the provisions of the relevantDTT).

A number of DTTs signed by France contain special provisions related to investmentvehicles.

- Foreign tax relief

DRIs may only benefit from a tax relief for WHT suffered abroad, if a DTT provides forsuch. If no DTT applies, the net income would be taxable in France.

22

- CFC rules

CFC rules may apply if the investor holds more than a 10%-stake in an entity located in atax haven jurisdiction (section 123 bis A of the French tax code would provide for taxationin France of the income/ gain arisen in a tax haven territories, even in absence ofdistribution by the fund).

Wrappers

The most commonly used wrapper would be the “Individual Saving Account” (i.e. PEA).A special regime would be applicable for DRIs investing in PEAs (should certainconditions be met): no taxation would be suffered on income distributed to DRIs. Onlysocial contributions would be due (11%). This regime would be applicable to investmentswithin the EU. UCITS and French non-UCITS funds would be eligible under certainconditions. Foreign non-UCITS funds would not be eligible to this special regime.

23

Appendix D3: Germany

Taxation of ongoing income

Domestic funds

Scope of application of the Investment Tax Act:

For the application of the Investment Tax Act (hereafter refers to as “InvTA”) toregulated domestic funds a legal definition linked to the German Investment Act (InvA) isapplied:

If one of the two following types of investment funds is given, the InvTA is applicable:

1) Investment funds in form of a corporation/joint stock company(« Investmentaktiengesellschaft »):

Investment Stock Corporations are stock corporations investing and managing their fundsin accordance with the InvA (limitation of allowed assets, risk diversification). Theinvestors should have the right to redeem their shares.

2) Contractual type (« Sondervermögen »):

Mutual funds have to be managed by a management company for the accounts of theinvestors, with the management company being a company in the legal form of a stockcorporation or a limited liability company with its seat and head office in the scope of theInvA whose main purpose is the management of investment funds or the management ofinvestment funds and private asset management. Furthermore, the investors should havethe right to redeem their units.

InvTA applicable and reporting requirements fulfilled (transparent fund)

In order to allow investors to benefit from the most advantageous tax regime, certainreporting requirements need to be fulfilled by the investment fund: the tax relevant dataneeds to be published in the German federal gazette (“elektronischer Bundesanzeiger”)within four months after financial year-end of the investment fund. The information mustbe certified by a qualified person (e.g. tax adviser) in the meaning of the German TaxAdvisor Act.

24

Taxation is based on the principle of transparency, i.e. the earnings at fund level are taxedat investor’s level.

a) In case of distributing funds, the earnings are split within their components (interestincome and other income, dividend income, foreign real estate income, capital gainsfrom shares, other capital gains). Distributed capital gains are not taxable in the handsof private investors.

b) In case of capitalizing funds, in the course of a deemed distribution of ordinaryincome at fund’s financial year-end the income is split into its components (interestincome and other income, dividend income, foreign real estate income). Capital gainsare not included in the taxable basis upon capitalization.

The taxation differs for the different types of income components (applicable regime forprivate investors until 31-12-2008):

Dividend income- 50% of dividend income is tax-exempt (deemed distributed income/distributed

income)- 20% domestic withholding tax (WHT) is applied on dividend income in case of

distribution and capitalization. An additional Solidarity Surcharge of 5.5% is appliedon WHT (21.1 % in total). The WHT can be imputed or deducted in the investor’stax return.

Interest income- Interest income is fully taxable (deemed distributed income/distributed income)- 30 % domestic WHT is applied on interest income in case of distribution and

capitalization. An additional Solidarity Surcharge of 5.5% is applied on WHT. TheWHT can be imputed or deducted in the investor’s tax return

Foreign real estate income- Foreign real estate income is tax-exempt as far as a Double Tax Treaty (DTT) is

applicable and allows for exemption- No domestic WHT on foreign real estate income applicable in case of treaty

exemption.

Capital gains- For private investors capital gains are tax-exempt upon distribution. Capital gains are

not included in the taxable basis upon capitalization.- No domestic WHT applicable on capital gains.

Income from transparent target funds falling in the scope of the application of theInvTA- The target fund’s income components (as published according to the requirements of

the InvTA) are included in the related income components at fund level, which ispassed on to investor’s level and received by the investor as one of the income typesmentioned above (full transparency).

- No specific WHT norm applicable.

25

Income from non-transparent target funds falling in the scope of the application ofthe InvTA- The lump sum amount as described below is included in the taxable basis at fund

level and passed on to investor level as fully taxable income.- No specific WHT norm applicable.

InvTA applicable and reporting requirements NOT fulfilled (non-transparent fund)

No split into the different income components. Instead, at investor’s level a lump sumtaxation is applicable according to a specified formula, which refers to the higher amountof:- at least 6 % of the last redemption price in the calendar year or;- 70 % of the increase in market value within the calendar year plus the total

distributions in calendar year.The calculated lump sum amount and distributions received are fully taxable.

Foreign funds

Scope of application of the InvTA

For foreign funds the basis for the application of the InvTA is not a legal definition linkedto the German Investment Act (InvA) as for domestic fund, but the criterion of economicsubstance has to be analysed:

For foreign funds the InvTA is applicable if the following criteria are fulfilled:

- Investments in specific assets mentioned in the InvA- Concept of risk diversification- Common investment of unitholders- As from January 1, 2008 an additional criterion exists:- The investor should have the right to redeem the shares/units held

OR the investor has not the right to redeem the shares held, but the fund is subject toinvestment supervision in the country it is domiciled

The new criterion has an impact on the application of the InvTA:

- Entities qualifying as fund according to the old regime, but not the new one:- Application of InvTA ends at closing of the business year starting before

December 28, 2007- Entities, which did not apply the Investment Tax Act in the past (e.g. non-transparent

funds):- The new regime is applicable as from January 1, 2008

InvTA applicable for and reporting requirements fulfilled (transparent fund)

In case the InvTA is applicable, the taxation is nearly the same as for domestic funds:

26

Dividend income- Same treatment as for domestic funds, but no domestic withholding tax (WHT)

applicable.

Interest income- Same treatment as for domestic funds, but only 30 % WHT plus Solidarity Surcharge

are withheld in case of distribution. The WHT can be imputed or deducted in theinvestor’s tax return

Foreign real estate income- Same treatment as for domestic funds.

Capital gains- Same treatment as for domestic funds.Income from transparent target funds falling within the scope of the application ofthe InvTA- Same treatment as for domestic funds.

Income from non-transparent target funds falling within the scope of the applicationof the InvTA- Same treatment as for domestic funds.

InvTA applicable and reporting requirements NOT fulfilled (non-transparent fund)

Same treatment as for domestic funds.

Taxation of income upon redemption/disposal of units/shares

- Redemption/disposal by the investor (applicable regime until December 31, 2008)

Domestic funds

The taxation of domestic non-UCITS funds depends on the fulfilled publicationrequirements:

a) InvTA applicable and interim profit published

27

The following types of income are taxable upon redemption:

Interest income/Interim profit- The interim profit is the accrued interest income of the fund, which has not yet been

distributed or deemed to be distributed to the investor. The interim profit is calculatedand published together with the redemption price on each net asset value calculationdate. It is usually published in a widely-spread national newspaper.

- Redemption of fund units:The interim profit (included in the fund’s redemption price) is fully taxable andserves as basis for 30 % WHT in Germany. The WHT can be imputed or deducted inthe investor’s tax return.

- Subscription of fund units:The interim profit/interest income included in the fund’s subscription price atpurchase of the fund unit can be deducted as expenses.

Capital gain- Capital gain is only taxable in case the holding period is less than one year.- The taxable capital gain corresponds to the amount of the redemption price after

deduction of included interim profit.

b) InvTA applicable and interim profit NOT published

Interest income- In case the interim profit is not published, a lump sum interim profit is calculated on

a basis of 6 % of the redemption price taking into account the total holding period.The lump sum interim profit is fully taxable and serves as basis for 30 % WHT. TheWHT can be imputed or deducted in the investor’s tax return.

Capital gain- Capital gain is only taxable in case the holding period is less than one year.

Foreign funds

Same treatment as for domestic funds, but related to the interest income for capitalizingforeign funds the ADDI (Accumulated Deemed Distributed Income) is taken into accountadditionally as taxable basis for the WHT of 30 %.

The ADDI has been the Aggregated Deemed Distributed Income since 1993 and no WHTis applied in case of capitalizations of foreign funds. The ADDI is the basis for WHT. It isnot a real additional tax charge, but rather the basis for prepayment of taxes that arecreditable and deductible in the investor’s annual tax return.

Redemption/disposal by the fund

For the redemption of fund units/shares by a regulated non-UCITS fund, the same taxabletreatment as at investor’s level applies, except for capital gains, which are always treated astax exempt income for private investors, irrespective of the holding period.

28

Outlook: Introduction of a Flat Rate Tax as from January 1, 2009

Investment Tax Act is applicable:

Distribution of fund:

Distributed income of the fund (including dividend income) will be taxable at a flat tax rateof 25 %.

Capital gains will be taxable in case of distribution, except for capital gain resulting fromsecurities purchased before January 1, 2009 and capital gains from real estate if the holdingperiod was not less than 10 years.

Foreign rental income is tax-free as long as it is provided for by an applicable Germandouble taxation treaty (DTT).

Capitalization/ Deemed distributions by the fund:

Deemed distributed income by the fund (including dividend income) will be taxable at aflat tax rate of 25 %, except of tax-free foreign rental income according to a DTT.

As per the old regime, capital gains will not be included in the deemed distributed income.

Disposal of fund shares/units:

In case of disposal, capital gains (i.e. amount of capital gain remaining after the deductionof the interim profit and deduction of the deemed distributed income, which was alreadytaxed before), are taxed at a flat tax rate of 25 % if the shares were purchased as fromJanuary 1, 2001.

Furthermore the investor is taxed based on the interim profit.

Other taxes

No specific tax treatment.

Cross-border taxation tax aspects

- The application of Double Tax Treaties has to be checked on a case-by-case basis.- The relief of foreign taxes is granted, as regulated non-UCITS funds for which the

InvTA is applicable are treated as transparent vehicles.CFC rules generally only apply in case the InvTA is not applicable.

29

Appendix D4: Ireland

Taxation of ongoing income

- Non transparent funds

Distributions of domestic funds to Irish investors would be subject to taxation at thestandard rate of income tax (currently 20%) should the distribution be considered as arelevant payment5 made annually or more frequently. If the payment is made lessfrequently than annually, taxation would occur at the standard rate of income tax plus 3%(i.e. 23%). This tax is accounted for by the fund.Distributions made by foreign corporate funds similar in all material respects to domesticregulated funds would be subject to the same tax treatment, where the details of thepayment have been included in the tax return. Otherwise, taxation would occur at themarginal rate of income tax, inclusive of health/ social welfare levies, or, in certain cases,at a 40% capital gains tax rate (this is not the case where the DRI invests in a domesticfund).A less favourable tax treatment could apply when a fund is located in a jurisdiction outsidethe EU/ OECD, which Ireland has no DTT with (e.g. Cayman Islands, Bermuda).

- Transparent funds

DRI’s investing in domestic transparent funds and in foreign regulated LimitedPartnerships would be subject to the same tax treatment as DRIs in domestic corporatefunds.

Foreign contractual funds and foreign unregulated Limited Partnerships would be viewedas tax transparent in Ireland. Investors in such funds would be treated as if they held thefund’s underlying investments directly.

Taxation of income upon disposal of its units/ shares by the DRI

- Non transparent funds

Capital gains realised upon disposal of the DRI’s shares in a domestic fund or in a foreigncorporate fund would be subject to taxation at the standard rate of income tax plus anadditional 3% tax. This 23% tax (20% plus 3%) would be applicable upon disposal ofshares in a foreign fund, where details of the payment have been correctly included in thetax return (otherwise the DRI may be subject to tax at the marginal rate of income tax(41%)). Indeed, as regards to investments in a foreign fund, this tax is accounted for by theinvestor. For investments in domestic funds this tax is accounted for by the fund.

5 A relevant payment is defined in the Taxes Consolidation Act, 1997, as amended as a payment to aunitholder by a collective investment undertaking by reason of rights conferred on the unitholder as a resultof holding a unit in the collective investment undertaking other than a payment made in respect of acancellation, redemption or repurchase of a unit. In essence it generally relates to annual or more frequentincome distributions made from the fund to the unitholder.

30

- Transparent funds

The tax treatment applicable upon disposal of shares in a corporate fund would beapplicable to the disposal of interest in a transparent entity.

- Deemed disposal regime

Finance Act 2006 introduced the concept of a deemed disposal (for units acquired as fromJanuary 1, 2001) whereby an Irish unitholder would be deemed to have disposal of his/herunits held in an investment undertaking every eight years from the date of acquisition ofsuch units. Any exit tax withheld on a deemed disposal would be available as a creditagainst the tax liability due on the ultimate disposal of units. The aim of this legislation isto prevent an indefinite roll-up/ accumulation of monies within the fund. Normally, this taxis accounted for by the fund. If the value of the number of chargeable units in theinvestment undertaking held by Irish resident investors is less than 10% of the value of thetotal units, the investment undertaking does not have to account for the tax (on deemeddisposals only). Unitholders would be required to return the gain directly to the IrishRevenue Commissioners on a self-assessment basis. Similar provisions apply in the case ofoffshore funds. In such cases, the investor would have to account for the tax under self-assessment rules.

Other taxes (e.g. net wealth tax, stamp duties)

From an Irish tax point of view, the same tax treatment would be applicable to DRIsinvesting in domestic and in foreign non-UCITS funds.

Cross-border taxation aspects

- Double Tax Treaty (DTT)

If there is a DTT in place, a refund can be available. It should be noted that funds do nothave the ability to access the DTT between Ireland and certain countries. Whether aparticular fund can access a DTT between Ireland and another country depends on theparticular treaty in question. In practice, the Irish tax authorities would in most casesrecognise foreign funds as qualifying persons under the terms of Irish DTT’s.

In the case of transparent funds, the DRI may be able to access the particular DTT as Irishtax law would look through the fund and recognise the investor as the beneficial owner.

Foreign tax relief

Foreign tax relief would only be available if a DTT provides for it.

31

Wrappers

A common wrapper used would be an Irish life investment/ pension product investing intoa non-UCITS fund. No tax would be suffered at the life company/ pension fund level inrespect of the investment held in the underlying fund. Gains earned by the life company/pension fund from the investment in the underlying fund would not be taxable if they fallwithin the categories of “Exempt Irish Investor” (as set out in the Taxes Consolidation Act,1997, as amended) and have completed a declaration form to that effect. Gains earned bythe DRI in the life company would be liable to exit tax at 23% (standard rate tax plus 3%).

The tax treatment applicable at the level of DRIs is generally less favourable than directinvestment, particularly in the case of double tax relief. It should also be noted that indirectinvestment by an investor through a wrapper may not improve the investor access to thetreaty when compared to direct investment. Another issue to be aware of is that a retailinvestor may be able to invest in a QIF or a PIF if he/ she indirectly invests through awrapper (which in turn invests in a QIF/ PIF). In general, direct investment in a QIF or PIFis not possible for retail investors, as minimum subscriptions must be held by the investor.

There would be no difference in relation to the taxation of DRIs in domestic and foreignnon-UCITS funds from an Irish taxation perspective.

In relation to transparent funds, the Irish CCF (Common Contractual fund) does not applyto individual investors. In respect of foreign contractual funds, Irish tax would apply atinvestor level as the contractual fund would be transparent for tax purposes. All income/gains would be treated as arising to each investor. Where the wrapper is investing in aCCF, the life company/ pension fund may be treated as investing directly in the underlyingassets of the CCF. In practice the life company/ pension fund would have better treatyaccess compared to a fund.

32

Appendix D5: Italy

Taxation of ongoing income

Domestic funds

RE entities (Fondi Immobiliari, SIIQ and SIINQ6):

- RE FUNDS

The proceeds paid by the Italian RE funds to individuals engaged in their private capacityare subject to a definitive 12.5% WHT.

SIIQ and SIINQ

Provided that specific conditions are met, the SIIQ and SIINQ special tax regime providesfor:

- at the SIIQ/SIINQ level, the exemption of the income realized through the real estateletting/leasing activity from the Corporate Income Tax (Ires) and from the RegionalTax on Productive Activities (Irap);

- the obligation to distribute to the shareholders at least 85% of the net profit arisenfrom the exempted real estate letting activity performed by the SIIQ/SIINQ;

- the application of a 20%-WHT (15% WHT in case the profits are related to therentals of housing real estates signed according to art. 2 (3) of the law 431/1998) ondividends distributed to the shareholders related to the activity of the SIIQ/SIINQexempted from Ires and Irap. The WHT is levied as a definitive payment in case theinvestor is an individual in his private capacity.

Non UCITS funds (fondi non armonizzati7)

The proceeds relating to the units held in the domestic Investment funds (open-end andclosed-end) or in a domestic SICAV are not subject to any withholding tax at the momentof the payment to the individual investors.

As a general rule the open-end/ closed-end domestic investment funds and the domesticSICAVs are subject to a 12.5% substitutive tax levied on the accrued day-end portfolioappreciation.

6SIIQ: listed joint stock companies resident in Italy for tax purposes specialized in the real estates letting/leasing activity

which have opted for the SIIQ special tax regime;SIINQ: non-listed joint stock companies resident in Italy specialized in real estates letting/leasing activity which haveopted for the SIINQ special tax regime.7 The Italian tax law does not provide for a specific tax regime applicable to the domestic hedge funds or private equity.Therefore, it must be made reference to the specific tax regime applicable in case of qualification of the Domestic Hedgefund/PE as an (i) open-end domestic investment fund (ii) closed-end domestic investment fund (iii) domestic investmentfund which invest in “substantial shareholdings” or as a (iii) SICAV.

33

Special regime of domestic investment funds investing in “substantial shareholding”8

The proceeds relating to the units held in the domestic investment funds, which invest in“substantial shareholdings”, are not subject to any withholding tax at the moment of thepayment to the individual investors.

Domestic investment funds which invest in “substantial shareholdings” are subject to asubstitutive tax applied on the accrued day-end appreciation. The substitutive tax applies:

- at the rate of 27%, exclusively on the specific part of the NAV appreciation accruedin relation to the capital gains realized by the fund through the disposal of the“substantial shareholding”; and

- at the rate of 12.5%, on the specific part of the NAV appreciation in relation to (i) theother investments (such as the “non substantial shareholding”) and (ii) the dividendsreceived by the fund in relation to the “substantial shareholdings”.

Foreign funds/Entities:

RE entities (Fondi Immobiliari, companies investing in RE)

RE FUNDS

The proceeds paid in respect of direct investment in foreign RE funds’ units placed oroffered in Italy are subject to a 27% Italian definitive WHT.

No specific rules for foreign RE funds offered abroad are provided by the Italian tax lawand no specific clarification have been issued by the Italian tax authorities.

COMPANIES INVESTING IN REAL ESTATE

In case they are characterized as corporations for Italian tax purposes9, the dividendsdistributed in relation to the “non-substantial shareholdings” are subject to a definitive12.5% WHT in case the investors are individuals acting in their private capacity.

The dividends paid to the individuals, acting in their private capacity, in relation to the“substantial shareholdings” held in the Foreign Companies under analysis are subject to aprovisional 12.5% WHT on the 40% of their amount (dividends relating to income yieldedas from 2008 on, are subject to a provisional 12.5% WHT on the 49.72% of their amount).Subsequently, 40% of the dividends on the “substantial shareholdings” (49.72% fordividends relating to income yielded from 2008 on) will be included in the investor’s taxreturn and subject therein to the progressive tax rates (from 23% to 43%) (60% exemptedfrom taxation or 50.28% exempted from taxation for dividends relating to income yieldedfrom 2008 on). The 12.5% provisional WHT is creditable against the personal income tax.

8 The mentioned tax regime applies exclusively in case (i) the number of investors (investing in the mentioned fund) islower than one hundred (100) or (ii) in case the units/quotas held by the “qualified investors” (other than the “individualqualified investors”) exceed 50% of the total amount of the units issued by such funds.

9 The Italian tax authorities have not clarified yet whether the mentioned Foreign Companies investing in RE must bequalified as “foreign corporations” or as “foreign RE funds”.

34

Foreign non-UCITS investment funds, foreign non-UCITS SICAVs10 and foreignhedge funds

At the investor level, there is the taxation of the proceeds as income from capital, subject toordinary taxation at personal income tax rate (progressive rate from 23% to 43%). If anItalian paying agent is involved, a provisional 12.5% WHT must be levied but is creditableagainst personal income tax.

Taxation of capital gains upon disposal of his/her units/ shares by the DRI

- Domestic funds

RE entities (Fondi Immobiliari, SIIQ and SIINQ)

RE FUNDS

Capital gains realized by the investor in his private capacity through the disposal of units ina domestic RE fund are subject to a 12.5% substitutive tax.

SIIQ and SIINQ

Capital gains realized by the investor in his/her private capacity through the disposal of“substantial shareholdings” in a SIIQ/SIINQ are wholly subject to tax under the investor’sself assessment regime (i.e. the investor will specify the capital gains in his tax return and,therein, the mentioned capital gains will be subject to the progressive tax rates).

Capital gains realized by the investor through the disposal of “non-substantialshareholdings”11 in a SIIQ/SINQ are subject to a 12.5% substitutive tax.

Non UCITS funds (fondi non armonizzati)

Capital gains realized by the investor in his/her private capacity through the disposal ofunits in a domestic fund is subject to a 12.5% substitutive part.

Special regime of domestic investment funds investing in “substantial shareholding”

Capital gains realized by the investor in his/her private capacity through the disposal ofunits in a domestic investment fund investing in “substantial shareholding” is subject to a12.5% substitutive tax.

10 The Italian tax law does not provide a specific rule for the qualification of the foreign non-UCITS SICAVs as “foreignnon-UCITS funds” or as “foreign companies”. Also for tax purposes, reference should be made to the “regulatoryqualification” of the SICAVs. The Italian tax authorities have specified, concerning the Participation Exemption regime,that the mentioned regime cannot be applied in relation to the quotas/ units held in domestic SICAVs, because from a taxpoint of view the domestic SICAVs are treated as the domestic Investment funds.11 “Non substantial shareholdings” are those shareholdings that represent voting rights in the shareholders’meeting not higher than 20% and participation in the share capital not exceeding the 25%. For shares incompanies listed on a stock exchange, the mentioned percentages are reduced, respectively to 2% (votingrights in the shareholders’ meeting) and 5% (participation in the share capital).

35

- Foreign funds

RE entities (Fondi Immobiliari, companies investing in RE)

RE FUNDS

Capital gain realized by the investor in his/her private capacity through the disposal ofunits in a foreign real estate fund is subject to a 12.5% substitutive tax.

COMPANIES INVESTING IN REAL ESTATE

In case they are characterized as corporations12, the capital gains realized by individuals,acting in their private capacity, are:

- subject to a 12.5% substitutive tax, in case of “non-substantial shareholdings”; and- subject to the progressive tax rates (from 23% to 43%) in the investor’s tax return for

40% of their amount (or 49.72% of their amount for the capital gains realized fromJanuary 1, 2009 on), in case of “substantial shareholdings”, if case certain conditionsare met.

Foreign non UCITS funds, foreign non-UCITS SICAVs13 and foreign hedge funds

The same substitutive tax of 12.5% applies on capital gains with respect to both foreignnon-UCITS funds and domestic ones.

Other taxes (e.g. net wealth tax, stamp duties)

From an Italian tax point of view, the same tax treatment would be applicable to DRIsinvesting into domestic and into foreign non-UCITS funds.

Cross-border taxation aspects

- DTTConcerning foreign non-UCITS funds, given that they are not often subject to tax in therelating country of residence, as a general rule, they cannot benefit from a DTT. However,a case-by-case analysis should be performed in order to ascertain whether the foreign non-UCITS funds can benefit of the DTTs.With reference to the domestic funds/entities: (i) the SIIQ, the SIINQ and the domestic REfunds can not benefit of the DTTs because the taxation does not apply at theSIIQ/SIINQ/fund level but at the investor level, (ii) on the other hand, the domestic non

12 The Italian tax authorities have not clarified yet whether the mentioned Foreign Companies investing in REmust be qualified as “foreign corporations” or as “foreign RE funds”.13 The Italian tax law does not provide a specific rule for the qualification of the foreign non-UCITS SICAVsas “foreign non-UCITS funds” or as “foreign companies”. Also for tax purposes, reference should be made tothe “regulatory qualification” of the SICAVs. The Italian tax authorities have specified, concerning theParticipation Exemption regime, that the mentioned regime cannot be applied in relation to the quotas/ unitsheld in domestic SICAVs, because from a tax point of view the domestic SICAVs are treated as the domesticInvestment funds.

36

UCITS fund which are taxed at the fund level, in principle, should be entitled to benefitfrom a DTT.

- Foreign tax relief

In case of a withholding tax levied in the State of source on proceeds relating to non-UCITS funds or on dividends relating to “substantial shareholdings” held by the investor ina foreign company investing in real estate (which should be subject to the progressive taxrates in the investor’s tax return), it is possible for the investor to credit it against hispersonal income, applying the specific regime according to the art. 165 of the ItalianConsolidated Income Tax Act. Under this regime, in case the foreign source proceeds/dividends are partially exempted from the investor’s personal income taxable basis, theforeign WHT levied on the proceeds/ dividends, deductible from the personal income tax,must be reduced accordingly. However, it is not usual to apply this mechanism on theWHTs levied on the proceeds paid by foreign non-UCITS funds.

With reference to the units held in domestic non-UCITS funds, the DRI cannot credit orrefund the WHT/ substitutive tax levied on the proceeds and capital gains which generallyapply as definitive taxes.

- Specific tax obligations

Due to the “external monitoring system”, the Italian intermediaries, interposed in thepayment of foreign source proceeds from foreign entities (e.g. non-UCITS funds or foreigncompanies investing in real estate) to the investors, are obliged to report the payment to theItalian tax authorities.Investors, due to the mentioned system must specify in their tax return each transfer ofmoney, shares or securities, exceeding EUR 10.000, executed between Italy and anotherState as well as investments and financial activities, exceeding the EUR 10.000, heldabroad.

Wrappers

As a general rule, in case of indirect investment in the domestic and foreign non-UCITSfunds through “wrappers”, the direct investment will be taxed (i.e. the “wrapper”)according to its specific tax regime.The most commonly used “wrappers” are the profit linked bonds (PLB) with an expirationperiod of at least 18 months, the domestic RE funds (in case the underlying is a foreign REfund), the insurance policies, and the UCITS funds.

37

Appendix D6: Luxembourg

Taxation of ongoing income

- Non transparent funds

Dividends or interest distributed from non-transparent funds (SICAV/F Part II funds orassimilated foreign non-UCITS funds) to retail investors are subject to a progressive taxrate, upon filing the tax return. The maximum marginal rate to which these distributionscan be liable for is currently of 38.95% and an additional 1.4% of social contributions.Partial exemption of income is available, i.e. EUR 1,500 for singles and EUR 3,000 formarried couples.

Distributions made by foreign non-UCITS funds and by domestic non-UCITS fundsreceive the same tax treatment in Luxembourg.

No Luxembourg taxation arises in the absence of any distribution by a SICAV/F or anassimilated foreign fund. In principle, neither the EU Savings Directive, nor the internalLuxembourg withholding tax is applicable on interest payments served by a non-transparent entity.

- Transparent funds

Dividend distributions from transparent funds (FCP Part II funds or assimilated foreignnon-UCITS funds) are, in theory, taxed on 50% of the gross dividend, if the latter isreceived from an EU non-transparent fully taxable company or from a non-transparentfully taxable company located in a State with which Luxembourg entered into a DTT,following the transparency principle. Still, the marginal rate cannot exceed 38.95% and anadditional 1.4% of social contribution.

Interest received from transparent funds is subject to progressive income tax rates in thehands of the investor, with a maximum rate of 38.95% and an additional 1.4% of socialcontribution.

For both, dividends and interest, the tax credit method/ effective rate method (dependingon DTT provisions) is not applied and partial exemptions of income are available(i.e. EUR 1,500 for singles; EUR 3,000 for married couples).

Interest may be subject to withholding tax and a final tax charge in Luxembourg if it ispaid by an EU paying agent on behalf of funds qualifying for the EU Savings Directivewhich are located in an EU country, the latter having opted for the withholding taxmechanism. However, domestic withholding tax on interest is not applicable.

38

Taxation of income upon redemption/ disposal of units/ shares

Upon redemption/ disposal by the investor

- Non transparent fundsIn principle, capital gains realised by the investors may enter one of three distinctclassifications. Speculative income occurs when the redemption/ disposal of the units/shares takes place within 6 months of the acquisition. It is taxed at a progressive incometax rate, with the maximum marginal rate being 38.95%. Extraordinary income, arising if aminimum shareholding of 10% of the fund’s capital is being held for a period exceeding 6months, is taxed at half the marginal income tax rate (i.e. maximum of 19.475%). Finally,income, which is derived form the redemption/ disposal of units/ shares held for more than6 months, but not qualifying as an important shareholding (10% threshold), is taxexempted.

The same taxation treatment applies to capital gains derived from domestic and foreignnon-UCITS funds.

- Transparent funds

Capital gains derived from the redemption/ disposal of units/ shares in a domestic or aforeign transparent fund are treated on an equal basis. They are subject to the same taxationas non-transparent funds, depending on their classification into speculative income,extraordinary income, or exempted income.

Upon redemption/ disposal by the fund

- Non transparent funds

Upon redemption/ disposal by the non-transparent fund itself, whether domestic or foreign,the income will only be subject to tax (dividend/ interest) if the income is effectivelydistributed.

- Transparent funds

In case of redemption/ disposal by the domestic or foreign transparent fund, the derivedincome is in principle treated as in the case of direct investment: taxation is due ondividends, interest, and capital gains.

Other taxes

No net wealth tax (NWT) is levied on income for Luxembourg tax resident individuals asof January 1, 2006. Therefore for DRIs, the same tax treatment applies whether they investin domestic or foreign non-UCITS funds.

39

Cross-border taxation aspects

- Double Tax Treaty (DTT)

Due to their transparency status, FCPs do not qualify for Luxembourg DTT benefits.Nonetheless, investors in an FCP may claim the relevant DTT relief as individuals, if theFCP is regarded as a transparent entity by the country of investment’s tax purposes.SICAV/F could benefit from a certain number of DTTs (26) signed by Luxembourg.In principle, foreign funds do not benefit from the provisions of Luxembourg DTTs, unlessthe funds are assimilated to Luxembourg resident funds.

- Foreign tax relief

No foreign or local tax credits are transferred with respect to the distributions made by aSICAV/F or by any assimilated foreign fund. In principle, and in accordance with thetransparency of an FCP, any tax credit should be transferable.

Wrappers

- Life insurance

Life insurance is a common wrapper used in Luxembourg for domestic or foreignnon-UCITS funds. The tax treatment of foreign non-UCITS funds, eligible for lifeinsurance contracts, is identical as for investments in domestic non-UCITS funds via lifeinsurance.Taxation of life insurance contracts in units occurs upon distribution; a full exemption isgranted when capital is paid out, while a 50% exemption is applicable if a pension isserved under certain conditions. Premiums may be deductible, depending on the situation.

- Fiduciary agreement

One of the most frequent wrappers used in Luxembourg is the fiduciary contract.Foreign non-UCITS funds are eligible for fiduciary contracts. In such a case, theLuxembourg tax treatment is identical for investments into foreign non-UCITS funds anddomestic funds (irrespective of EUSD potential implications). No tax impacts apply tofiduciary agreements; the DRI encounters the same tax treatment for direct and indirectinvestment.

40

Appendix D7: Poland

Taxation of ongoing income

Domestic funds

All domestic funds would be non transparent.

Distributions from domestic funds to DRIs would be treated as capital gains subject to aWHT at 19%. No further taxation would be suffered on distributed income.

Foreign funds

Poland would recognise the tax transparency of a foreign fund based on an analysis madeby the foreign country. Albeit that, taxation would not occur on an arising basis, but on thedistributed income. From a practical standpoint, the same tax treatment would thus applyto foreign transparent and opaque funds.

Distributions from foreign funds to DRIs would be treated as “income from other sources”subject to progressive tax (i.e. 19% to 40%) in the hands of the DRI.

Taxation of capital gains upon disposal of his units/ shares by the DRI

Domestic funds

Capital gains realised by a DRI upon disposal of its participation in a domestic fund (i.e.opaque fund as all domestic funds would be non transparent) would be subject to WHT at19%.

Foreign funds