Embed Size (px)

Citation preview

The Rankings ~ Slight category changes ~ Five SectorsCONSUMER

Apparel

Retail (+Pharmacies and Dept. Stores)

Personal Care

Luxury (High-end accessories and watches)

Cars

FOOD & DRINK

Beer

Fast Food

Soft Drinks (all non-alcoholic)

FINANCIAL INSTITITIONS

Global Banks

Regional Banks

Insurance

TECHNOLOGY

Technology

Telecoms

COMMODITIES

Oil & Gas

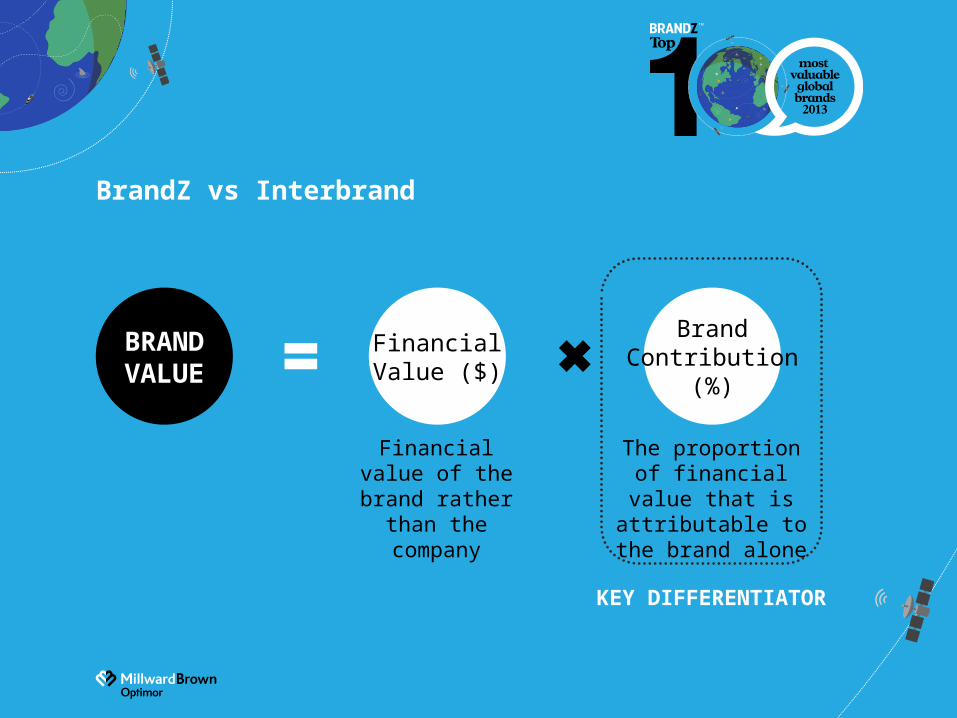

BrandZ vs Interbrand

Financial value of the brand rather than the

company

The proportion of financial value that is

attributable to the brand alone

BRANDVALUE

FinancialValue ($)

BrandContribution

(%)

KEY DIFFERENTIATOR

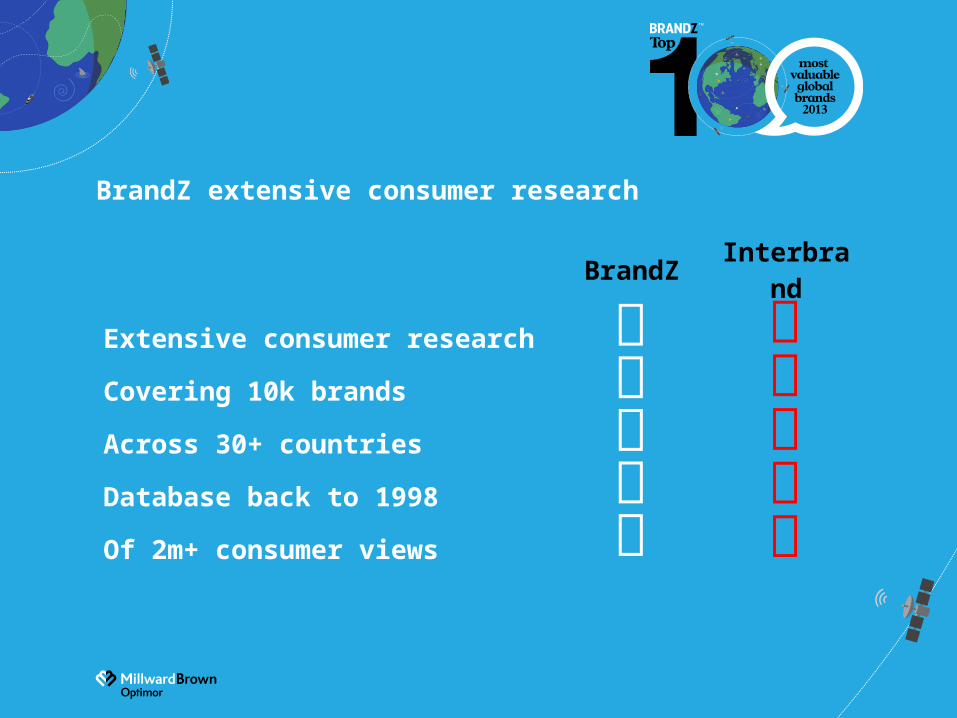

BrandZ extensive consumer research

BrandZ Interbrand

Extensive consumer research

Covering 10k brands

Across 30+ countries

Database back to 1998

Of 2m+ consumer views

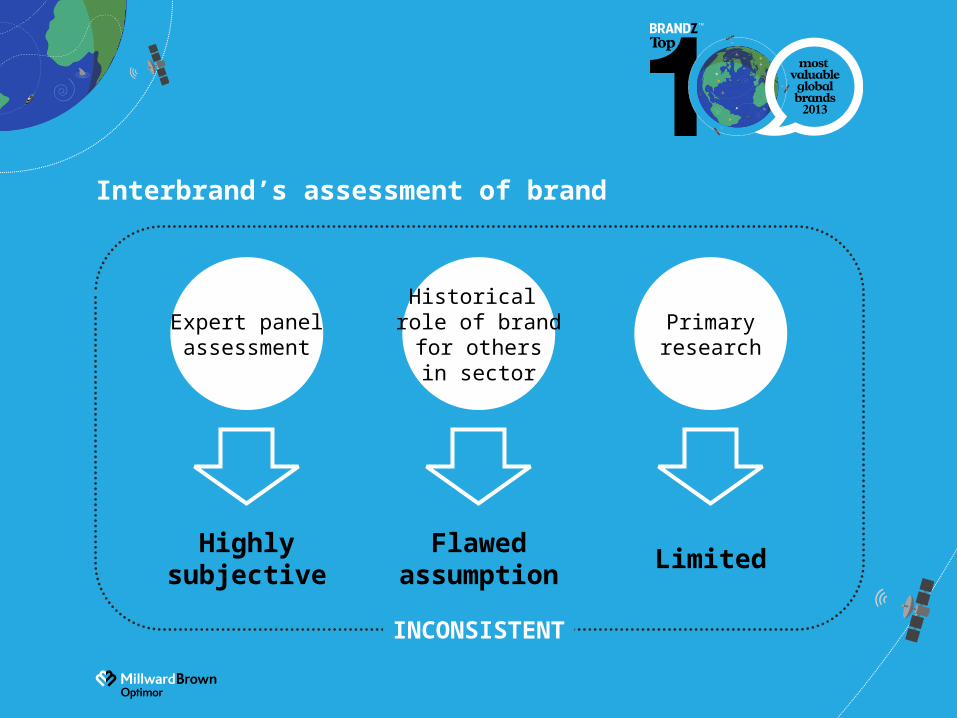

Interbrand’s assessment of brand

Expert panelassessment

Historical role of brand

for othersin sector

Primaryresearch

Highlysubjective LimitedFlawed

assumption

INCONSISTENT

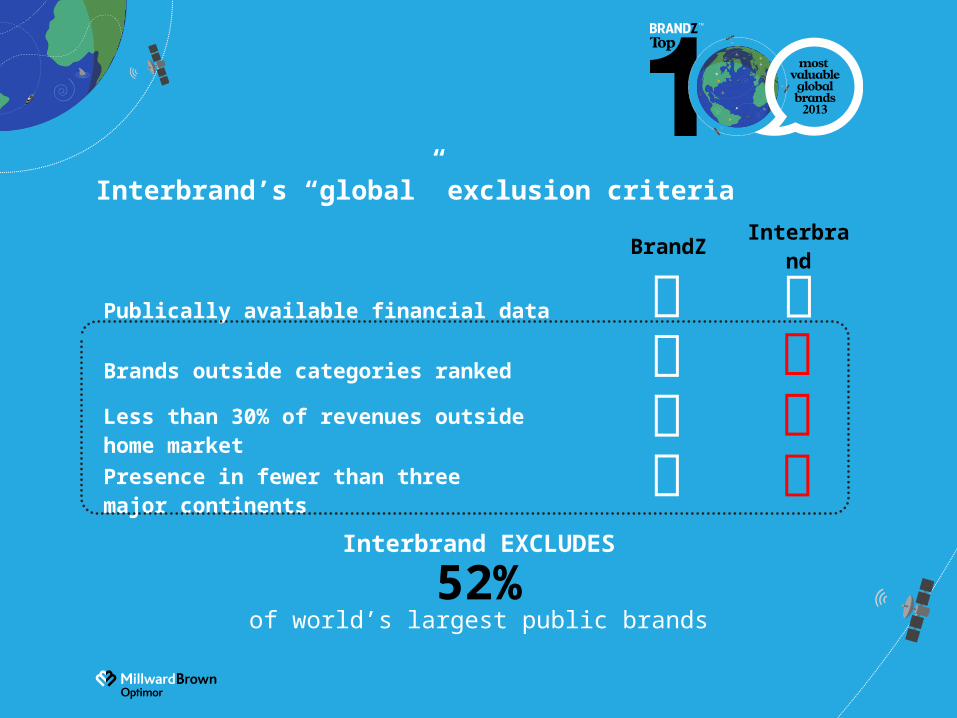

Interbrand’s “global” exclusion criteria

BrandZ Interbrand

Publically available financial data

Brands outside categories ranked

Less than 30% of revenues outside home market

Presence in fewer than three major continents

Interbrand EXCLUDES

52%of world’s largest public brands

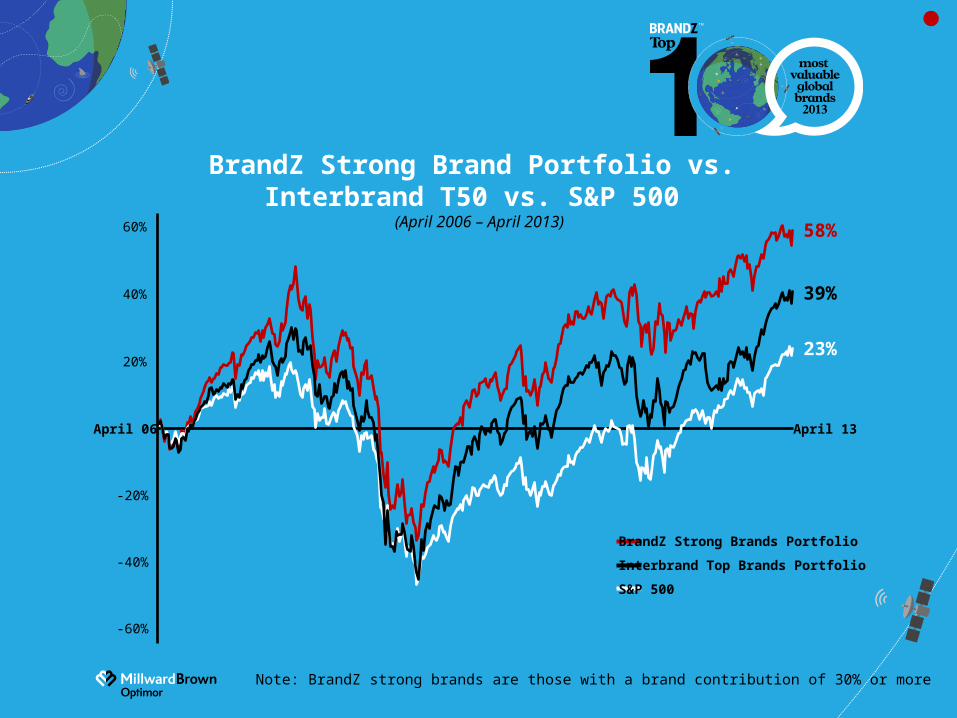

BrandZ Strong Brand Portfolio vs. Interbrand T50 vs. S&P 500

(April 2006 – April 2013)

Note: BrandZ strong brands are those with a brand contribution of 30% or more

April 13April 06

60%

40%

20%

-60%

-40%

-20%

58%

39%

23%

BrandZ Strong Brands Portfolio

Interbrand Top Brands Portfolio

S&P 500

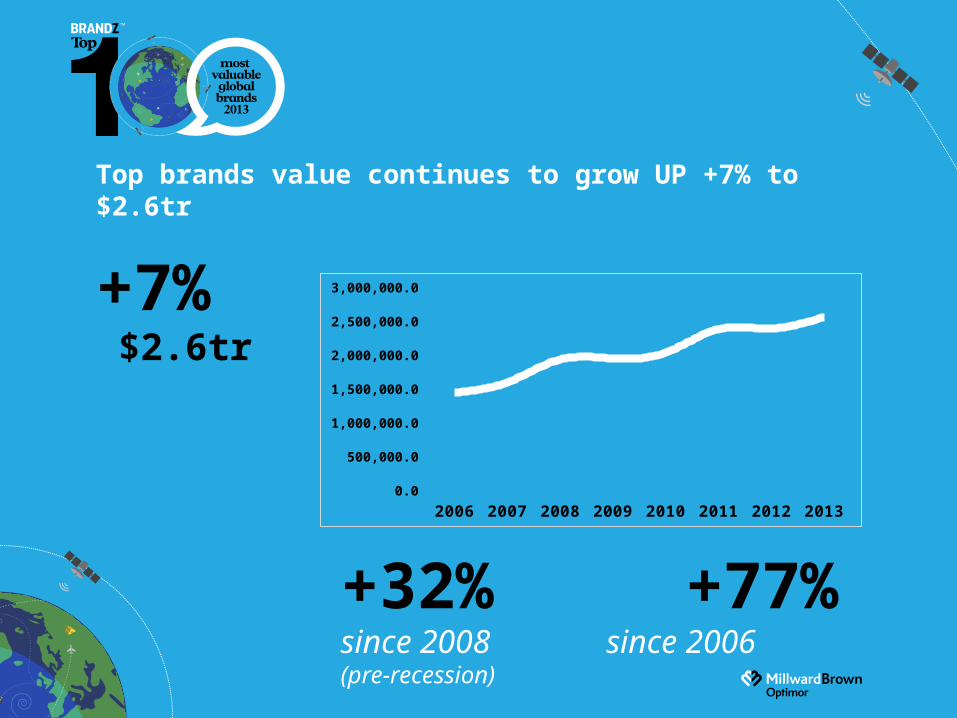

Top brands value continues to grow UP +7% to $2.6tr

+32% +77% since 2008 since 2006(pre-recession)

2006 2007 2008 2009 2010 2011 2012 20130.0

500,000.0

1,000,000.0

1,500,000.0

2,000,000.0

2,500,000.0

3,000,000.0+7% $2.6tr

GROWTH All categories show growth (except Technology, Oil & Gas)

Top brands defy slowdown in Europe/UK.

Asia leads growth, US recovers and LatAm suffers.

FINANCIAL INSTITUTIONS

Banks have bounced back into profit

TECHNOLOGY

Technology continues to dominate and influence

VALUE

Luxury and Value co-exist

GLOBAL IS NOT AUTOMATIC PANACEA

Many regional brands bigger than global competitors

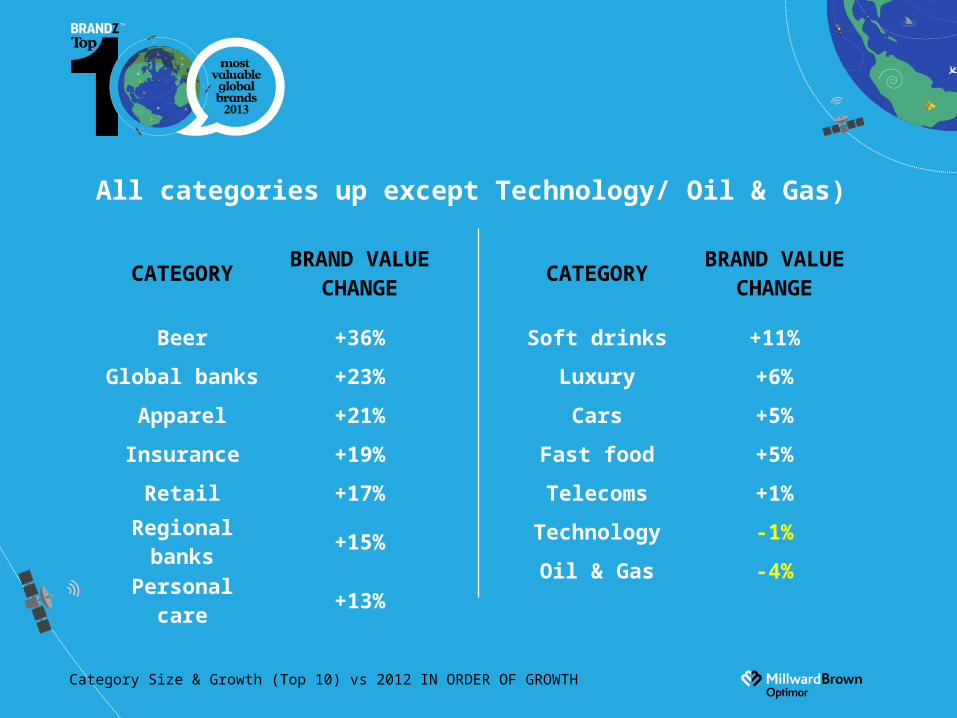

All categories up except Technology/ Oil & Gas)

CATEGORY BRAND VALUE CHANGE

Beer +36%

Global banks +23%

Apparel +21%

Insurance +19%

Retail +17%

Regional banks +15%

Personal care +13%

CATEGORY BRAND VALUE CHANGE

Soft drinks +11%

Luxury +6%

Cars +5%

Fast food +5%

Telecoms +1%

Technology -1%

Oil & Gas -4%

Category Size & Growth (Top 10) vs 2012 IN ORDER OF GROWTH

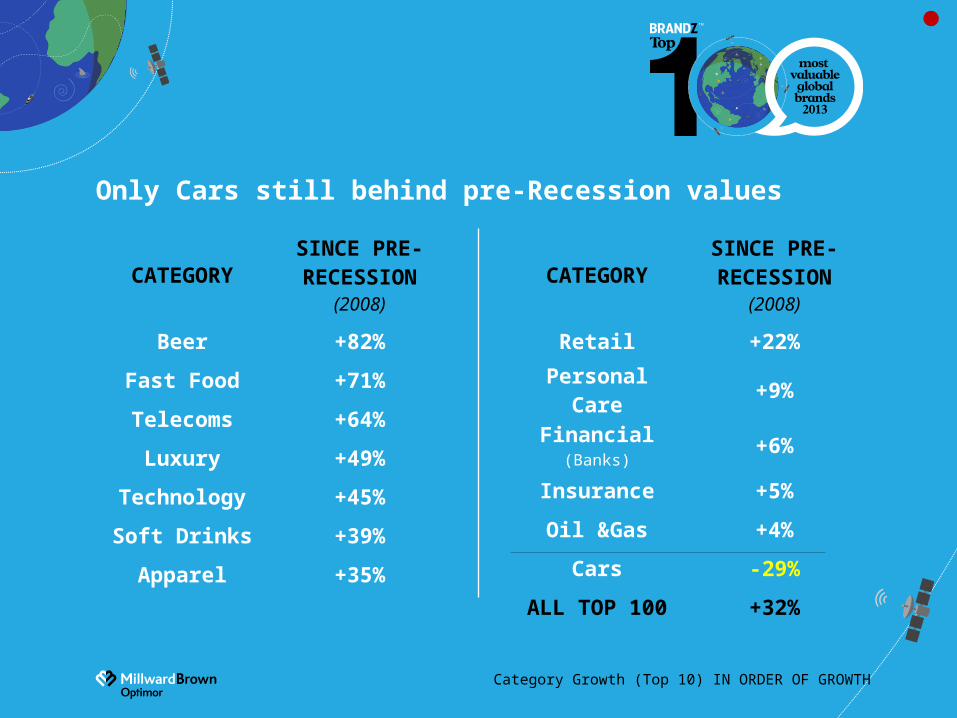

Only Cars still behind pre-Recession values

CATEGORYSINCE PRE-RECESSION

(2008)

Beer +82%

Fast Food +71%

Telecoms +64%

Luxury +49%

Technology +45%

Soft Drinks +39%

Apparel +35%

CATEGORYSINCE PRE-RECESSION

(2008)

Retail +22%

Personal Care +9%

Financial (Banks)

+6%

Insurance +5%

Oil &Gas +4%

Cars -29%

ALL TOP 100 +32%

Category Growth (Top 10) IN ORDER OF GROWTH

Rankings: Top 20 risers from Global and Category Rankings

BRAND BRAND VALUE CHANGE

Prada +63%Brahma +61%

Zara +60%Calvin Klein +52%

Tencent +52%Samsung +51%

Gucci +48%Visa +46%

The Home Depot +43%Disney +40%

BRAND BRAND VALUE CHANGE

eBay +40%Stella Artois +40%

Skol +39%Next +39%Citi +37%

Nivea +36%Heineken +36%

Commonwealth Bank of Australia +36%

Amazon +34%Barclays +34%

Banks back making profits

They may not be popular but they are

valuable infrastructure and can be profitable

exports

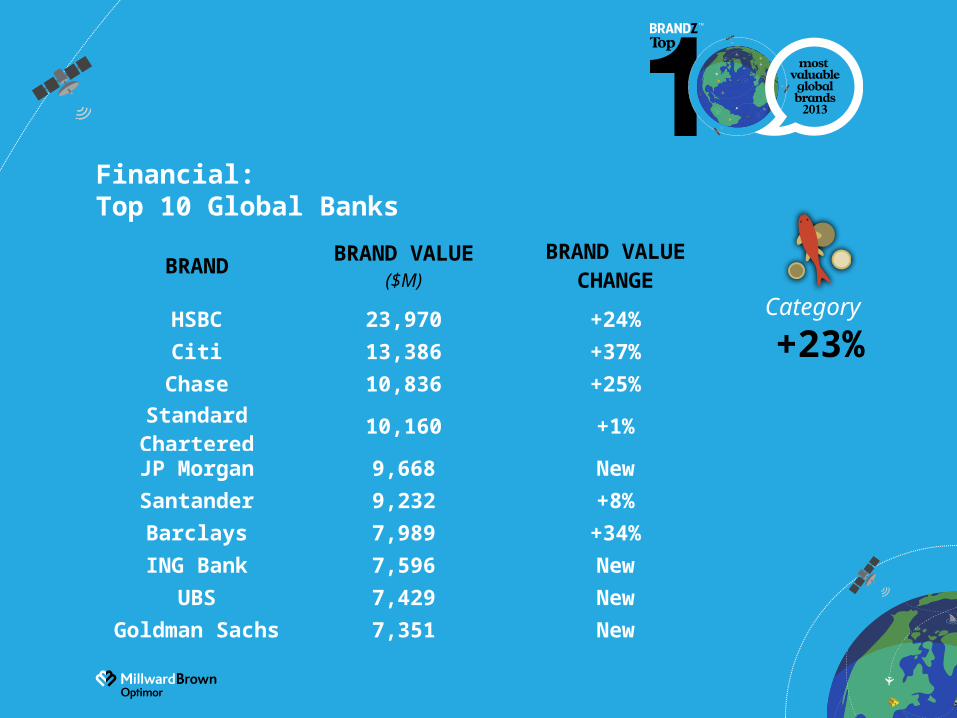

Financial: Top 10 Global Banks

Category

+23%

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

HSBC 23,970 +24%

Citi 13,386 +37%

Chase 10,836 +25%

Standard Chartered 10,160 +1%

JP Morgan 9,668 New

Santander 9,232 +8%

Barclays 7,989 +34%

ING Bank 7,596 New

UBS 7,429 New

Goldman Sachs 7,351 New

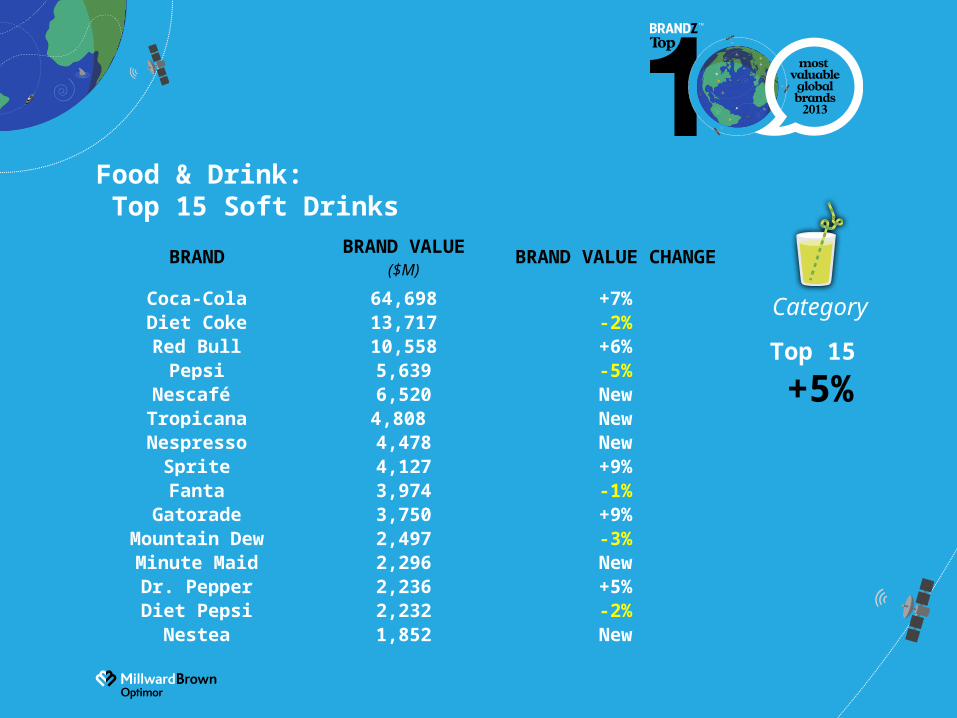

The Soft Drinks ‘share of throat’

increasingly being affected by health

concerns and threatened legislation

Food & Drink: Top 15 Soft Drinks

Category

Top 15

+5%

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Coca-Cola 64,698 +7%Diet Coke 13,717 -2%Red Bull 10,558 +6%

Pepsi 5,639 -5%Nescafé 6,520 New

Tropicana 4,808 NewNespresso 4,478 New

Sprite 4,127 +9%Fanta 3,974 -1%

Gatorade 3,750 +9%Mountain Dew 2,497 -3%Minute Maid 2,296 NewDr. Pepper 2,236 +5%Diet Pepsi 2,232 -2%

Nestea 1,852 New

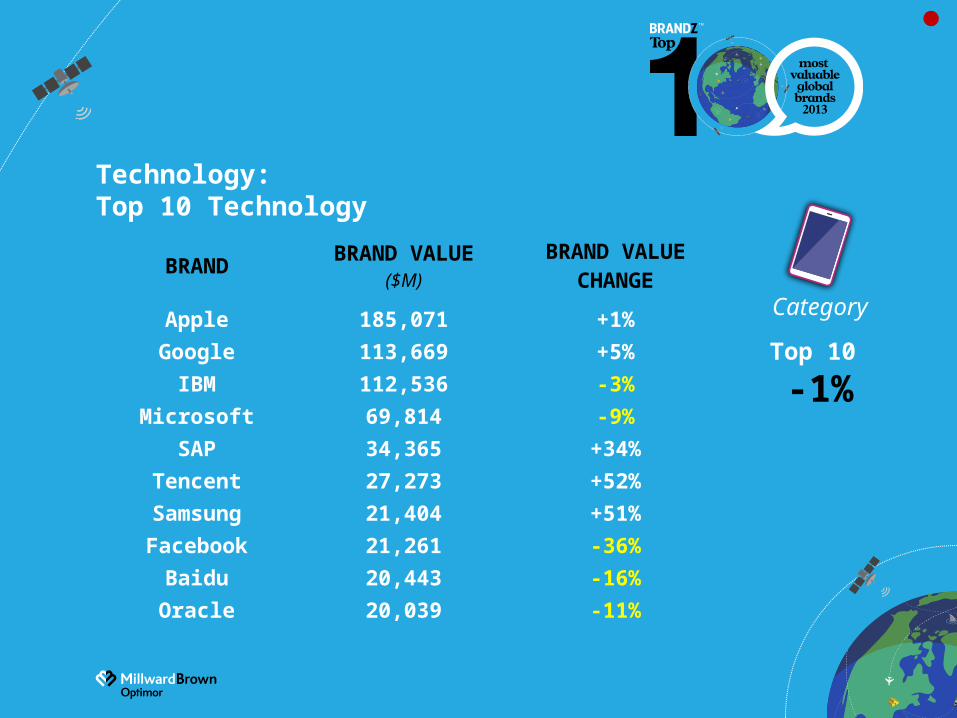

Volatility across Technology

category

A temporary lull in game changing innovations

US still dominates

Technology: Top 10 Technology

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Apple 185,071 +1%

Google 113,669 +5%

IBM 112,536 -3%

Microsoft 69,814 -9%

SAP 34,365 +34%

Tencent 27,273 +52%

Samsung 21,404 +51%

Facebook 21,261 -36%

Baidu 20,443 -16%

Oracle 20,039 -11%

Category

Top 10

-1%

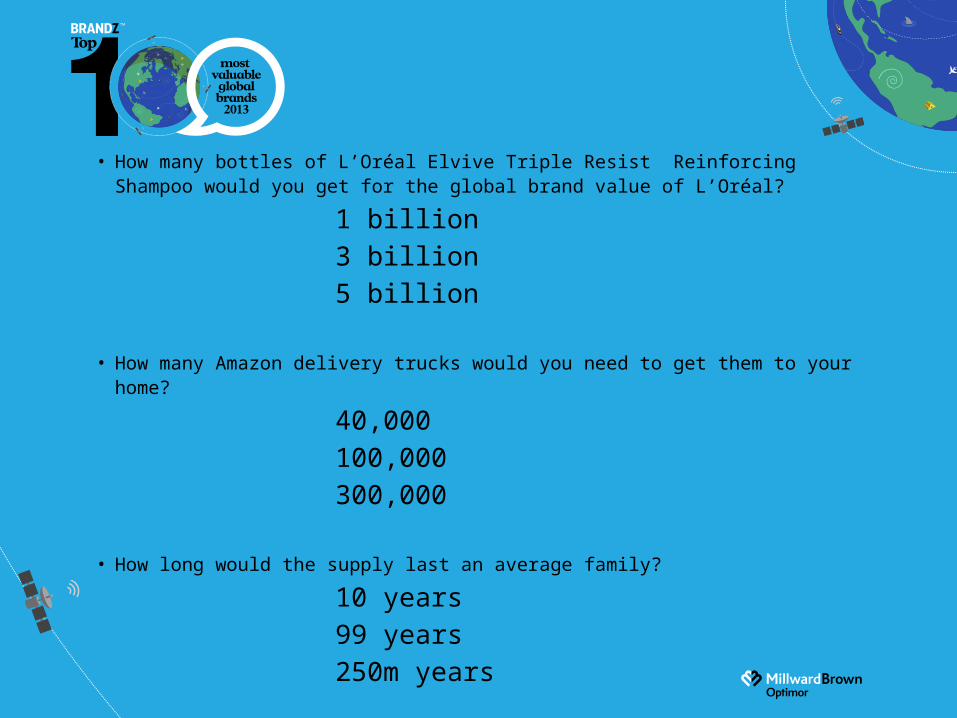

Great T-shirt Giveaway

• How many bottles of L’Oréal Elvive Triple Resist Reinforcing Shampoo would you get for the global brand value of L’Oréal?

1 billion

3 billion

5 billion

• How many Amazon delivery trucks would you need to get them to your home?

40,000

100,000

300,000

• How long would the supply last an average family?

10 years

99 years

250m years

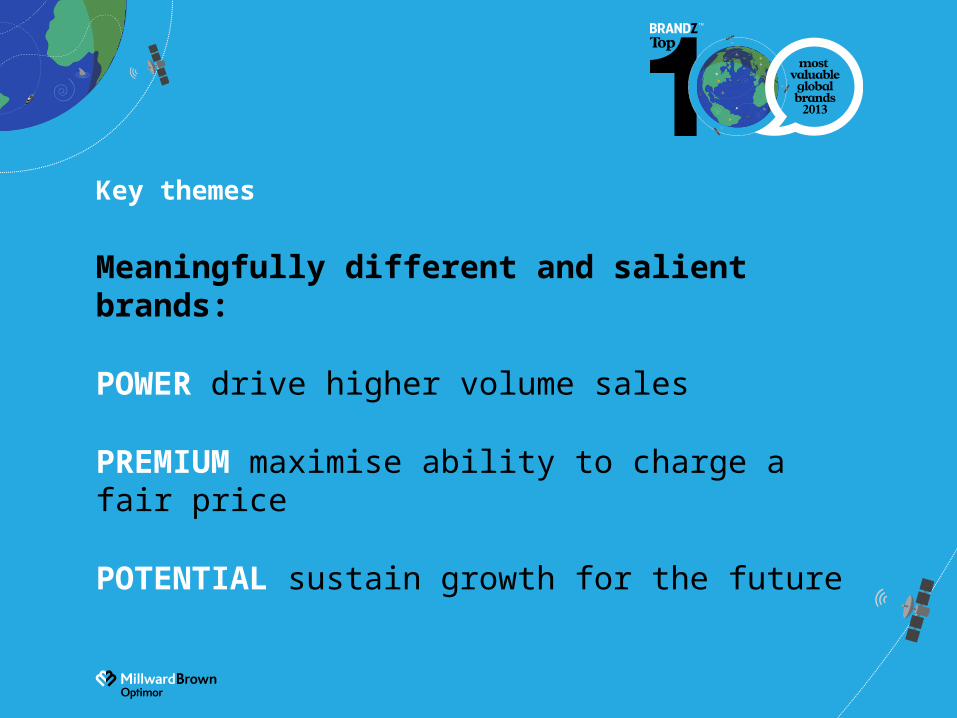

Key themes

Meaningfully different and salient brands:

POWER drive higher volume sales

PREMIUM maximise ability to charge a fair price

POTENTIAL sustain growth for the future

Top 100 Brands

MEANINGFUL 115

DIFFERENT 120

SALIENT 131

Average for all brands 100

Eight Years, Eight Top Risers

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Subway 16,700 +5,798%

Apple 185,071 +1,058%

Amazon 45,700 +664%

Hermès 19,129 +296%

Zara 20,167 +295%

SAP 34,365 +259%

Verizon 53,004 +256%

IBM 112,536 +212%

Up

+425%Top 100 up

+77%

Eight Success Trends

Great Value Proposition

Relevant for today

Harnessing technology

Getting abroad and about

Reputation

Meaningfully Different

Personality

A great branded experience

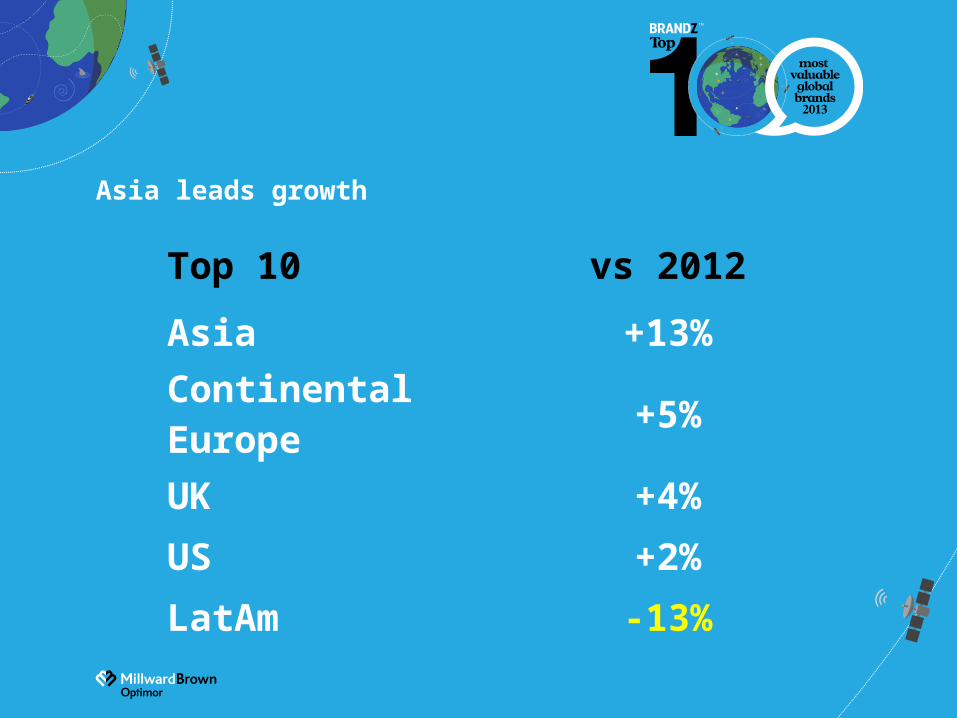

Asia leads growth

Top 10 vs 2012

Asia +13%

Continental Europe +5%

UK +4%

US +2%

LatAm -13%

Rankings: Top 10 Asia

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

China Mobile 55,368 +18%

ICBC 41,115 -1%

Tencent 27,273 +52%China Construction Bank 26,859 +10%

Toyota 24,497 +12%

Samsung 21,404 +51%

Baidu 20,443 -16%Agriculture Bank of China 19,975 +12%

Commonwealth Bank of Australia 17,745 +36%

ANZ 16,565 New

+13%

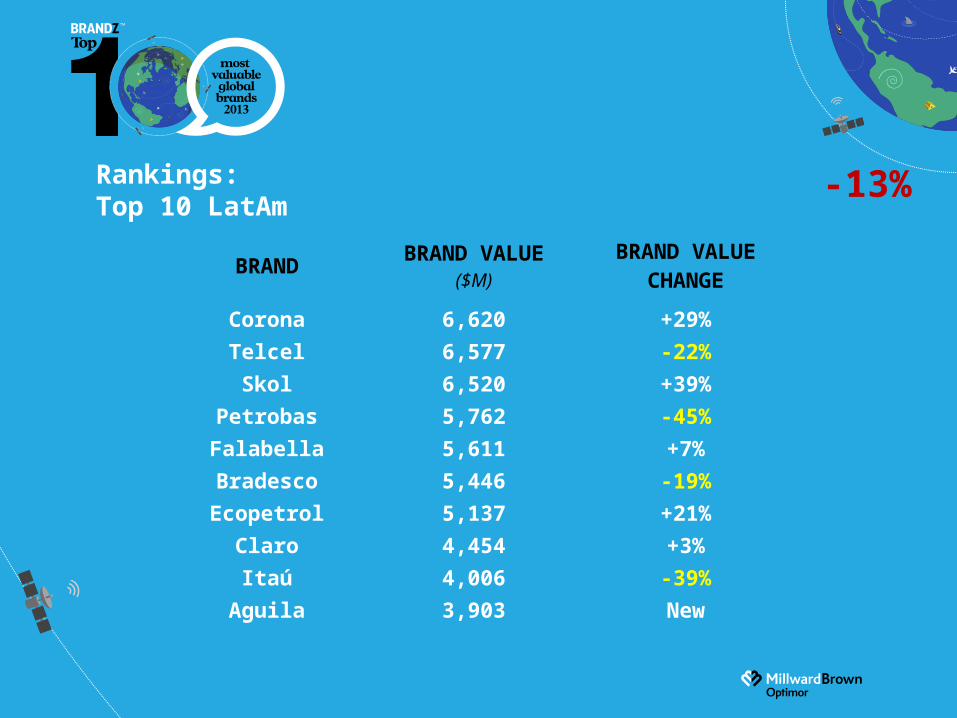

Rankings: Top 10 LatAm

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Corona 6,620 +29%

Telcel 6,577 -22%

Skol 6,520 +39%

Petrobas 5,762 -45%

Falabella 5,611 +7%

Bradesco 5,446 -19%

Ecopetrol 5,137 +21%

Claro 4,454 +3%

Itaú 4,006 -39%

Aguila 3,903 New

-13%

Fast Growing markets: Other

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

ICICI Bank (India) 14,196 +12%

Sberbank (Russia) 12,655 +19%

MTN (Africa) 11,448 +23%

MTS (Russia) 10,633 +11%

Airtel (India) 10,054 -13%

Gazprom (Russia) 6,182 -8%

Lukoil (Russia) 5,011 New

Rankings: Top 10 North America

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Apple 185,071 +1%

Google 113,669 +5%

IBM 112,536 -3%

McDonald’s 90,256 -5%

Coca-Cola 78,415 +6%

AT&T 75,507 +10%

Microsoft 69,814 -9%

Marlboro 69,383 -6%

Visa 56,060 +46%

GE 55,357 +21%

(Canada: RBC 38th, TD 46th, Scotiabank 85th)

+2%

Rankings: Top 10 UK

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Vodafone 39,712 -8%

HSBC 23,970 +24%

Shell 17,678 -1%

Tesco 16,303 -9%

BP 11,520 +11%

Standard Chartered 10,160 +1%

BT 9,531 New

Barclays 7,989 +34%

O2 5,965 -30%

Dove 4,927 +5%

+4%

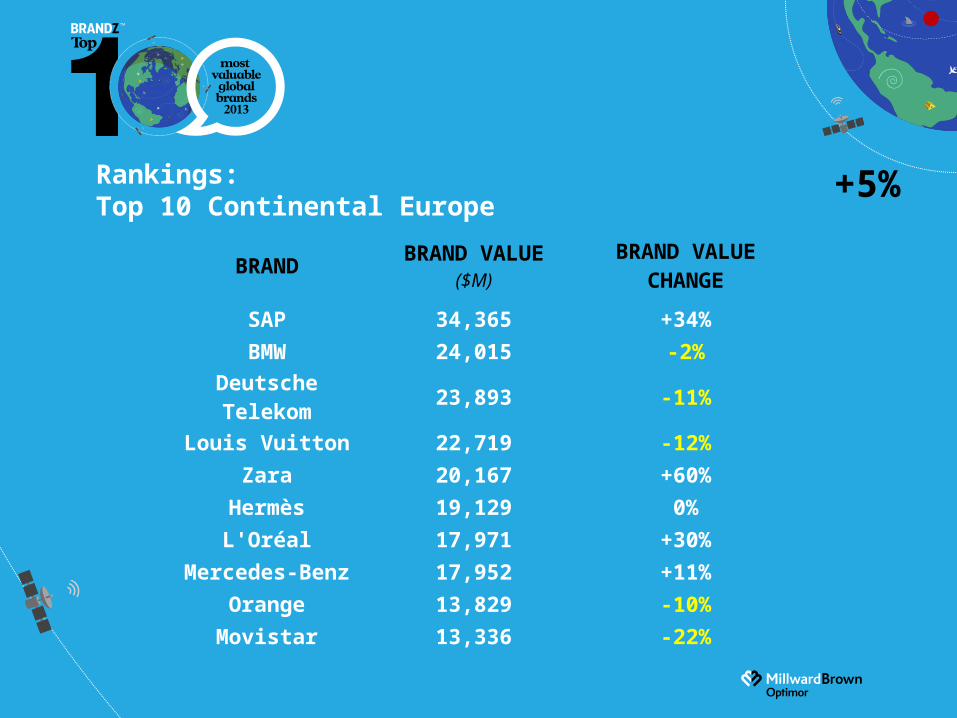

Rankings: Top 10 Continental Europe

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

SAP 34,365 +34%

BMW 24,015 -2%

Deutsche Telekom 23,893 -11%

Louis Vuitton 22,719 -12%

Zara 20,167 +60%

Hermès 19,129 0%

L'Oréal 17,971 +30%

Mercedes-Benz 17,952 +11%

Orange 13,829 -10%

Movistar 13,336 -22%

+5%

BRAND BRAND VALUE($M)

BRAND VALUE

CHANGE

Amazon 45,727 +34%

Walmart 36,220 +5%

The Home Depot 18,488 +43%

eBay 17,749 +40%

Tesco 16,303 -9%

IKEA 12,040 +31%

Target 11,879 +13%

Woolworths 11,039 -

ALDI 8,885 -5%

Lowe’s 7,559 +26%

Consumer: Top 20 Retail 2013

BRAND BRAND VALUE($M)

BRAND VALUE

CHANGE

Carrefour 7,372 -6%

Costco 6,789 +33%

Whole Foods 6,728 -

Walgreens 5,925 -

CVS 5,620 -

Falabella 5,611 +7%

M&S 4,649 +7%

Asda 4,617 +19%

Lidl 4,524 -2%

Coles 4,416 -

Key Take Aways

PURPOSE

CONSUMERS

COMMUNICATION

GROWTH

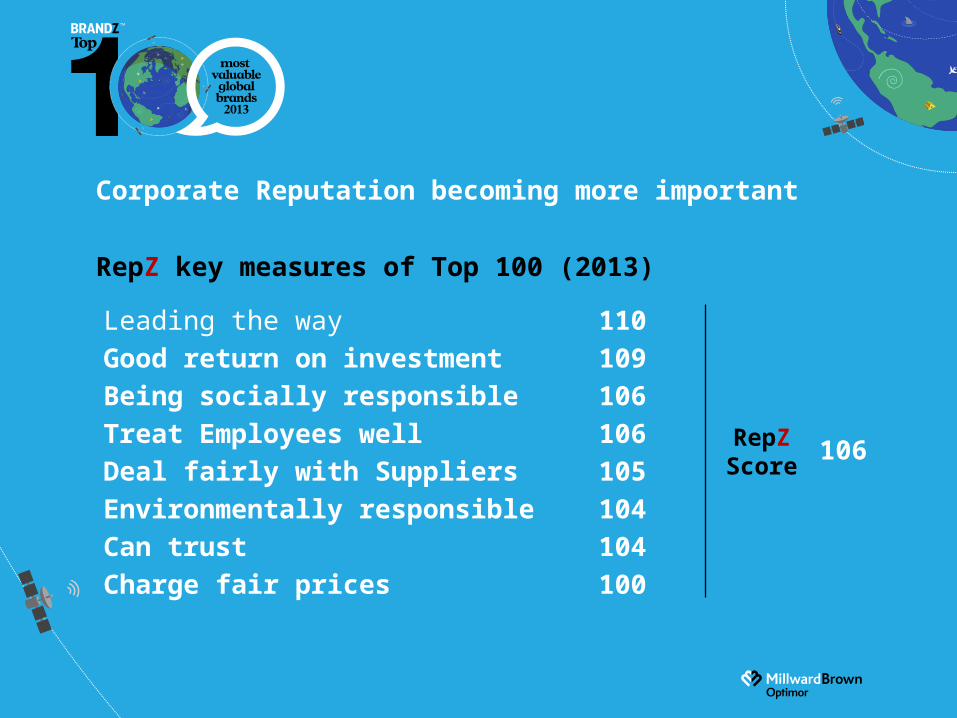

Corporate Reputation becoming more important

RepZ key measures of Top 100 (2013)

Leading the way 110Good return on investment 109Being socially responsible 106Treat Employees well 106Deal fairly with Suppliers 105Environmentally responsible 104Can trust 104Charge fair prices 100

RepZScore

106

Coming soon….