Embed Size (px)

Citation preview

The Potential Entry Defense in Airline Mergers

Andrew Sweeting James Roberts

Duke University

September 2012

PRELIMINARY

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 1 / 45

Introduction

Possible defenses for horizontal mergers between direct competitors inconcentrated markets:

substantial merger-speci�c e¢ ciencies (Horizontal Merger Guidelines2010, Section 10)

probable exit of assets absent a merger (Guidelines 2010, Section 11)

the potential entry defense (Guidelines 2010, Section 9)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 2 / 45

IntroductionPotential Entry Defense

Guidelines, p. 28:

A merger is not likely to enhance market power if entry intothe market is so easy that the merged �rm and its remainingrivals in the market, either unilaterally or collectively, could notpro�tably raise price or otherwise reduce competition comparedto the level that would prevail in the absence of the merger.Entry is that easy if entry would be timely, likely, andsu¢ cient in its magnitude, character, and scope to deter orcounteract the competitive e¤ects of concern.

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 3 / 45

IntroductionOur Contribution

we develop a static model of entry-and-competition to assess thelikelihood and su¢ ciency of post-merger entrythere are two alternative interpretations of the �potential entrydefense�:

1 the existence of potential entrants constrains incumbents evenwithout entry (�contestability�)

2 the existence of potential entrants disciplines incumbents because ananti-competitive merger would induce entry and this will constrainprices

our model only allows us to consider the second interpretationconsistent with post-1992 interpretations of the Guidelines (Baker2003)consistent with the argument that contestability theory �simply doesnot conform to the fact in a de-regulation world consisting of hubairports�.

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 4 / 45

Our Aims

develop and estimate an empirical model of entry and competition

perform merger counterfacuals allowing for endogenous entry

critically we want to allow for selection

i.e., �rms with lower (marginal) costs or better products are more likelyto have entered before the mergerallows us to explain a stylized fact that count of potential entrantsreduces prices (Morrison and Whinston (1987), Kwoka and Shumilkina(2010))

why may selection be important?1 important in determining whether entry is likely and how e¤ective itwill be (example)

2 role in explaining why little post-merger entry is observed in practice

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 5 / 45

Existing Literature on Entry and Mergers

discussion of how ease of entry should be interpreted and measured

Schmalensee (1987)

theoretical analyses of how entry a¤ects the pro�tability and welfareimplications of mergers

Cournot: Spector (2003), Werden and Froeb (1998)Bertrand: Werden and Froeb (1998), Cabral (2003)assume no selection

dynamic games:

Gowrisankaran (1999)Marino and Zabojnik (2006)assume no selection

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 6 / 45

IntroductionOur Conceptual Contribution

Our key conceptual contribution concerns the role of selection in entry :

suppose potential entrants are heterogenous in marginal costs and/orproduct quality

a plausible entry process is likely to select the best �rms into theindustry pre-merger

the remaining potential entrants post-merger will tend to be relativelyweak

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 7 / 45

IntroductionOur Conceptual Contribution

Surprisingly, selection on marginal costs and/or quality has been assumedaway in:

the theoretical literature considering mergers with entry

almost all of the empirical �entry�literature

even though heterogeneity is usually necessary to explain post-entrymarket shares and pricesexceptions: auctions, models with non-structural outcome equations

limited previous empirical research considering mergers and entry(e.g., Collard-Wexler (2011))

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 8 / 45

IntroductionApplication: Airline Mergers

numerous, high-pro�le, on-going

the potential entry defense has been used successfully in airlinemergers

for most routes, there are several non-competing carriers who alreadyserve the endpoints

these are assumed to be well-placed potential entrants

PED was explicitly cited by the Dept of Transportation when itapproved all mergers pre-1989PED has also been explicitly referred to by the Dept of Justicepost-1989the existence of slot constraints has led to approvals conditional on slotdivestitures (e.g., United/Continental, Eastern/Texas Air)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 9 / 45

IntroductionApplication: Airline Mergers

but on the most a¤ected routes, prices rise post-merger and entrydoesn�t happen

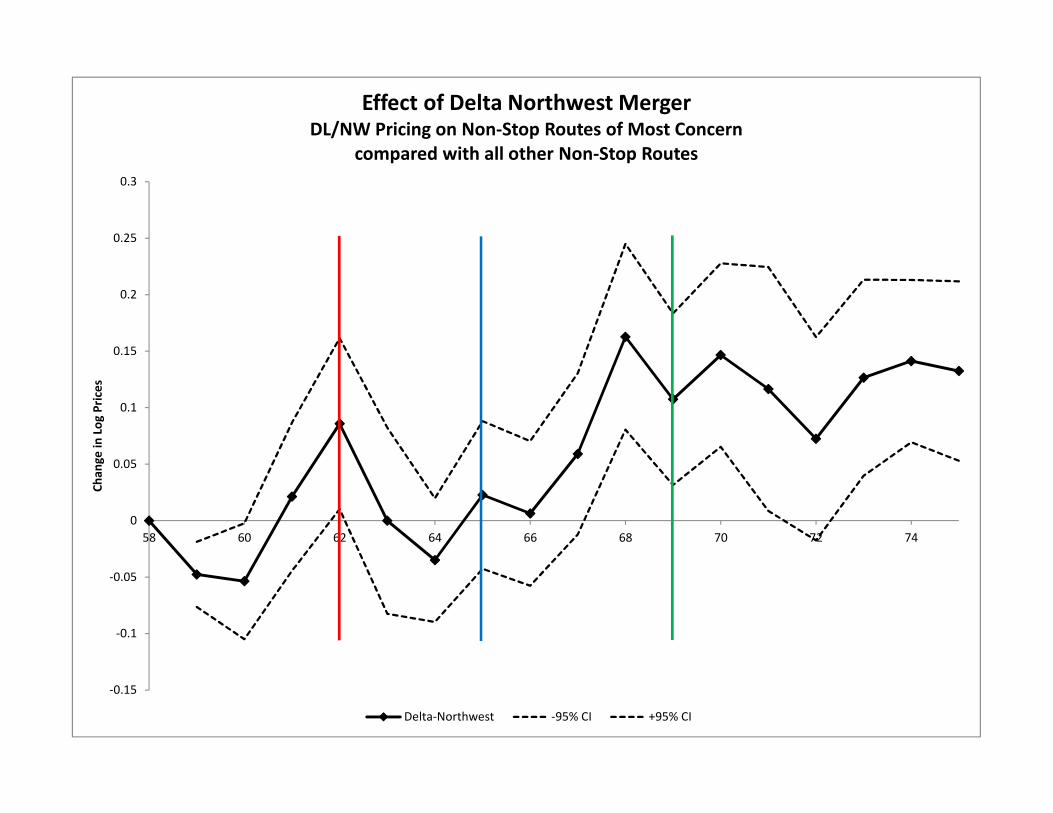

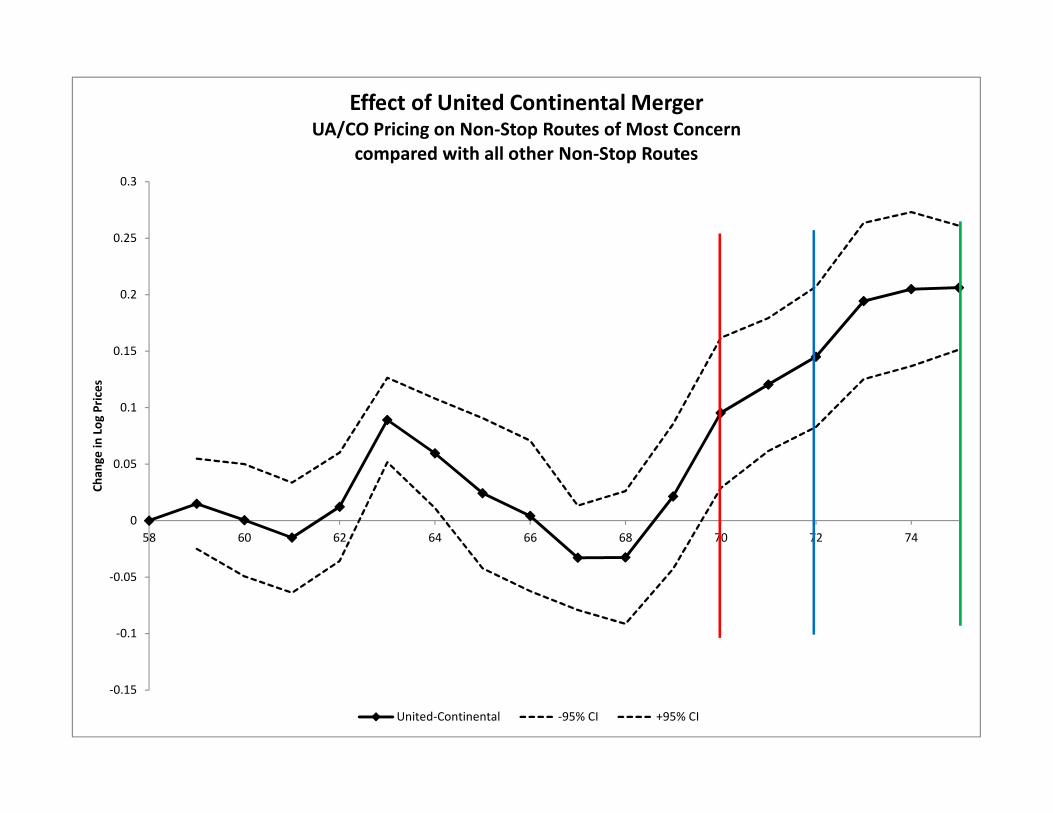

Borenstein (1990), Kim and Singal (1993), Peters (2006): prices rise7-29%new evidence from recent mergers ...

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 10 / 45

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

58 60 62 64 66 68 70 72 74

Chan

ge in

Log

Pric

es

Effect of Delta Northwest MergerDL/NW Pricing on Non-Stop Routes of Most Concern

compared with all other Non-Stop Routes

Delta-Northwest -95% CI +95% CI

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

58 60 62 64 66 68 70 72 74

Chan

ge in

Log

Pric

es

Effect of United Continental MergerUA/CO Pricing on Non-Stop Routes of Most Concern

compared with all other Non-Stop Routes

United-Continental -95% CI +95% CI

IntroductionPotential Entry Defense in Airline Mergers

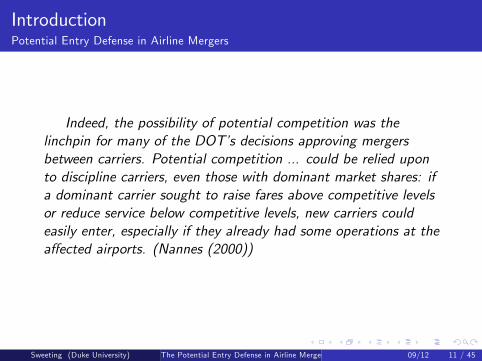

Indeed, the possibility of potential competition was thelinchpin for many of the DOT�s decisions approving mergersbetween carriers. Potential competition ... could be relied uponto discipline carriers, even those with dominant market shares: ifa dominant carrier sought to raise fares above competitive levelsor reduce service below competitive levels, new carriers couldeasily enter, especially if they already had some operations at thea¤ected airports. (Nannes (2000))

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 11 / 45

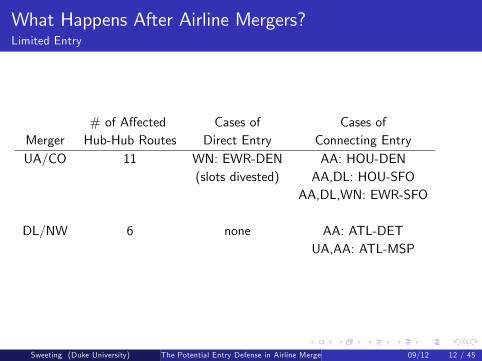

What Happens After Airline Mergers?Limited Entry

# of A¤ected Cases of Cases ofMerger Hub-Hub Routes Direct Entry Connecting EntryUA/CO 11 WN: EWR-DEN AA: HOU-DEN

(slots divested) AA,DL: HOU-SFOAA,DL,WN: EWR-SFO

DL/NW 6 none AA: ATL-DETUA,AA: ATL-MSP

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 12 / 45

Outline for Today�s Talk

1 Literature Review and Our Model2 Data3 Estimation4 Preliminary Results and an Illustrative Counterfactual

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 13 / 45

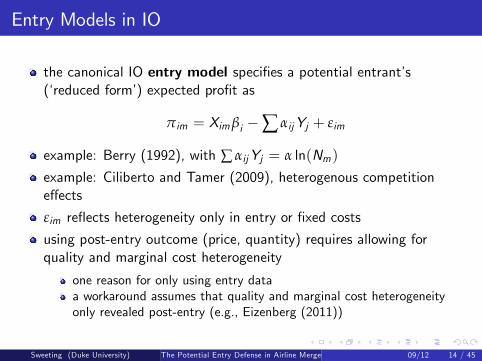

Entry Models in IO

the canonical IO entry model speci�es a potential entrant�s(�reduced form�) expected pro�t as

πim = Ximβi �∑ αijYj + εim

example: Berry (1992), with ∑ αijYj = α ln(Nm)

example: Ciliberto and Tamer (2009), heterogenous competitione¤ects

εim re�ects heterogeneity only in entry or �xed costs

using post-entry outcome (price, quantity) requires allowing forquality and marginal cost heterogeneity

one reason for only using entry dataa workaround assumes that quality and marginal cost heterogeneityonly revealed post-entry (e.g., Eizenberg (2011))

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 14 / 45

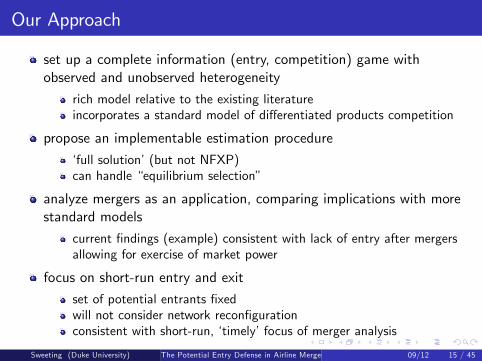

Our Approach

set up a complete information (entry, competition) game withobserved and unobserved heterogeneity

rich model relative to the existing literatureincorporates a standard model of di¤erentiated products competition

propose an implementable estimation procedure

�full solution�(but not NFXP)can handle �equilibrium selection�

analyze mergers as an application, comparing implications with morestandard models

current �ndings (example) consistent with lack of entry after mergersallowing for exercise of market power

focus on short-run entry and exit

set of potential entrants �xedwill not consider network recon�gurationconsistent with short-run, �timely�focus of merger analysis

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 15 / 45

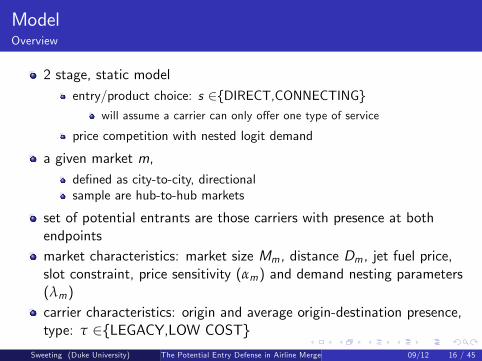

ModelOverview

2 stage, static modelentry/product choice: s 2{DIRECT,CONNECTING}

will assume a carrier can only o¤er one type of service

price competition with nested logit demand

a given market m,de�ned as city-to-city, directionalsample are hub-to-hub markets

set of potential entrants are those carriers with presence at bothendpointsmarket characteristics: market size Mm , distance Dm , jet fuel price,slot constraint, price sensitivity (αm) and demand nesting parameters(λm)carrier characteristics: origin and average origin-destination presence,type: τ 2{LEGACY,LOW COST}

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 16 / 45

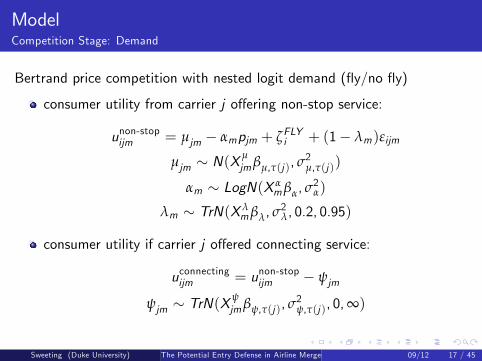

ModelCompetition Stage: Demand

Bertrand price competition with nested logit demand (�y/no �y)

consumer utility from carrier j o¤ering non-stop service:

unon-stopijm = µjm � αmpjm + ζFLYi + (1� λm)εijm

µjm � N(Xµjmβµ,τ(j), σ

2µ,τ(j))

αm � LogN(X αmβα, σ

2α)

λm � TrN(X λmβλ, σ

2λ, 0.2, 0.95)

consumer utility if carrier j o¤ered connecting service:

uconnectingijm = unon-stopijm � ψjm

ψjm � TrN(Xψjmβψ,τ(j), σ

2ψ,τ(j), 0,∞)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 17 / 45

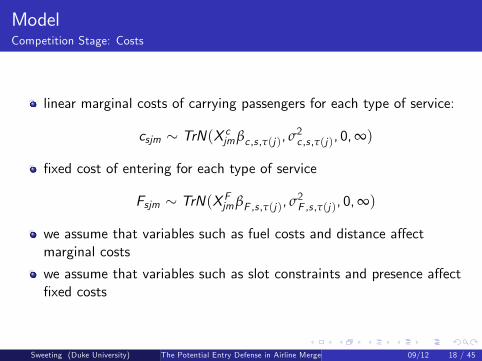

ModelCompetition Stage: Costs

linear marginal costs of carrying passengers for each type of service:

csjm � TrN(X cjmβc ,s ,τ(j), σ2c ,s ,τ(j), 0,∞)

�xed cost of entering for each type of service

Fsjm � TrN(X FjmβF ,s ,τ(j), σ2F ,s ,τ(j), 0,∞)

we assume that variables such as fuel costs and distance a¤ectmarginal costs

we assume that variables such as slot constraints and presence a¤ect�xed costs

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 18 / 45

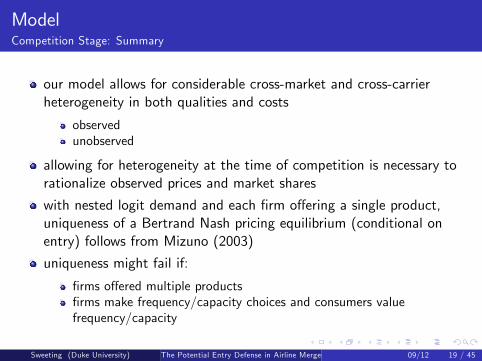

ModelCompetition Stage: Summary

our model allows for considerable cross-market and cross-carrierheterogeneity in both qualities and costs

observedunobserved

allowing for heterogeneity at the time of competition is necessary torationalize observed prices and market shares

with nested logit demand and each �rm o¤ering a single product,uniqueness of a Bertrand Nash pricing equilibrium (conditional onentry) follows from Mizuno (2003)

uniqueness might fail if:

�rms o¤ered multiple products�rms make frequency/capacity choices and consumers valuefrequency/capacity

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 19 / 45

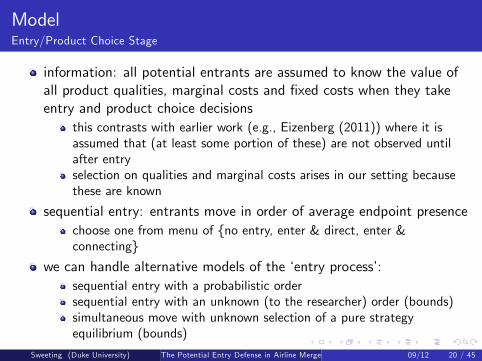

ModelEntry/Product Choice Stage

information: all potential entrants are assumed to know the value ofall product qualities, marginal costs and �xed costs when they takeentry and product choice decisions

this contrasts with earlier work (e.g., Eizenberg (2011)) where it isassumed that (at least some portion of these) are not observed untilafter entryselection on qualities and marginal costs arises in our setting becausethese are known

sequential entry: entrants move in order of average endpoint presencechoose one from menu of {no entry, enter & direct, enter &connecting}

we can handle alternative models of the �entry process�:sequential entry with a probabilistic ordersequential entry with an unknown (to the researcher) order (bounds)simultaneous move with unknown selection of a pure strategyequilibrium (bounds)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 20 / 45

Data

Traditional airline data sources:

DB1B O&D Survey database which is a 10% sample of passengeritineraries

domestic, return tickets with prices less than $50, tickets more than$2000�ticketing carrier�

T100 Flight Segment data

used for calculating presencecarriers �ying non-stop

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 21 / 45

DataSample Markets and Time Period

period: Q2 2004-2008

prior to DL/NW and UA/CO mergers

markets: hub-to-hub markets

focus in recent merger casestypically large, but concentrated with the hub carriers providing mostof the servicewe identify 24 hub cities which serve at least 40 destinations, onecarrier serves at least 20 destinations, and are considered hubs in someother studieswe then exclude hub-hub pairs that are less than 200 miles apart, orbecause unusually many or few people appear to travel

the results today are based on city-city markets

we will try airport-airport markets as well

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 22 / 45

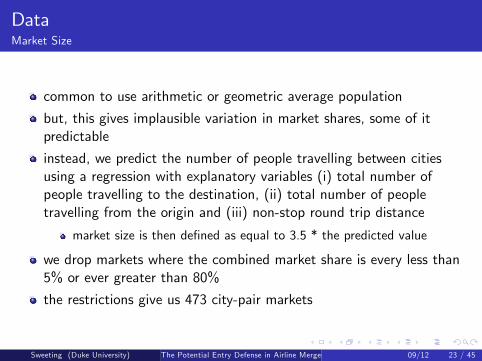

DataMarket Size

common to use arithmetic or geometric average population

but, this gives implausible variation in market shares, some of itpredictable

instead, we predict the number of people travelling between citiesusing a regression with explanatory variables (i) total number ofpeople travelling to the destination, (ii) total number of peopletravelling from the origin and (iii) non-stop round trip distance

market size is then de�ned as equal to 3.5 * the predicted value

we drop markets where the combined market share is every less than5% or ever greater than 80%

the restrictions give us 473 city-pair markets

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 23 / 45

DataCarriers

Our estimation approach can handle up to 9 carriers per market

American (AA), Continental (CO), Delta (DL), Northwest (NW),United (UA), US Airways (US) are named legacy carriers

Southwest (WN) is named low-cost carrier

aggregated �other legacy�

aggregated �other low cost�

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 24 / 45

DataService Type, Prices and Market Shares

a carrier can be counted as an entrant if it carries at least 15 DB1Bpassengers in a quarter

counts as direct if

carries more passengers direct than connectingit o¤ers at least one non-stop �ight

otherwise counts as connecting

price and market shares are calculated using only the type of servicethat we consider entered:

average price of DB1B passengers

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 25 / 45

DataPresence

previous work has shown the importance of airport presence for entrydecisions

we de�ne presence of carrier j in a city y as

# of cities served by j non-stop at least once per day from y# of cities served by anyone non-stop at least once per day from y

varies from being almost zero to 1 (e.g., Continental at Houston)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 26 / 45

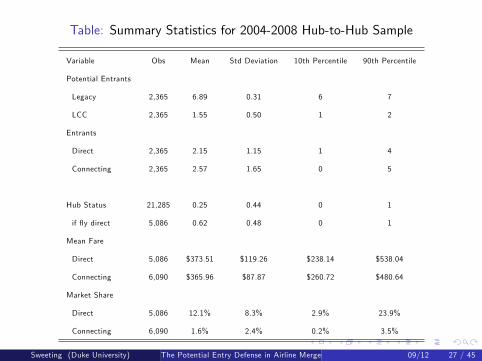

Table: Summary Statistics for 2004-2008 Hub-to-Hub Sample

Variable Obs Mean Std Deviation 10th Percentile 90th Percentile

Potential Entrants

Legacy 2,365 6.89 0.31 6 7

LCC 2,365 1.55 0.50 1 2

Entrants

Direct 2,365 2.15 1.15 1 4

Connecting 2,365 2.57 1.65 0 5

Hub Status 21,285 0.25 0.44 0 1

if �y direct 5,086 0.62 0.48 0 1

Mean Fare

Direct 5,086 $373.51 $119.26 $238.14 $538.04

Connecting 6,090 $365.96 $87.87 $260.72 $480.64

Market Share

Direct 5,086 12.1% 8.3% 2.9% 23.9%

Connecting 6,090 1.6% 2.4% 0.2% 3.5%

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 27 / 45

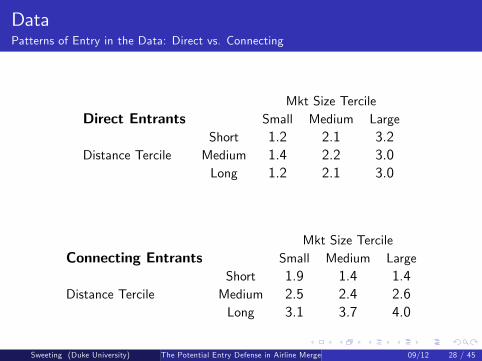

DataPatterns of Entry in the Data: Direct vs. Connecting

Mkt Size TercileDirect Entrants Small Medium Large

Short 1.2 2.1 3.2Distance Tercile Medium 1.4 2.2 3.0

Long 1.2 2.1 3.0

Mkt Size TercileConnecting Entrants Small Medium Large

Short 1.9 1.4 1.4Distance Tercile Medium 2.5 2.4 2.6

Long 3.1 3.7 4.0

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 28 / 45

Estimation

Berry (1992) and Ciliberto and Tamer (2009) estimate by solvingentry games at each guess of the parameters

they don�t have post-entry competitionthey have fewer parametersthey have a binary choiceC&T have only 6 �rms

a nested �xed point approach in our setting (post-entry competition,three choices, nine carriers) won�t work

the non-linearity of second stage outcomes in unobservables makesthe application of two-step methods problematic

we therefore use the Simulated Method of Moments Approach, usingimportance sampling to approximate the simulated moments

suggested by Ackerberg (2009)previously used in our work on second price and �rst price auctions

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 29 / 45

EstimationSimulated Method of Moments with Importance Sampling

the idea is to solve for a large number of games once and thenreweight these solved games during estimation

the parameters we want to estimate are the β and σ (Γ) parametersthat determine the distributions of qualities, price and nestingcoe¢ cients and costs

to take a simple example:

for a set of draws of the {αm ,λm , µjm ,ψjm , csjm ,F

sjm} parameters

(θsim) we can calculate the prices, market shares and entry decisions ofeach carrierif we take a large number of these sets of draws, we can thenapproximate a particular moment by:

E (hm(θ,Xm)jbΓ) � 1S ∑ hm(Xm , θsim)

f (θsim jXm , bΓ)g(θsim jXm)

where g is the importance density from which the draws θsim are taken

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 30 / 45

EstimationSimulated Method of Moments

apart from this di¤erence in how expectations are calculated as theparameters change, implementation is standard, i.e.,

minΓH 0M (Γ)WHM (Γ)

where

HM (Γ) =1M ∑

m[(ym � E (hm(θ,Xm)jbΓ) l(zm)]

and W is a weighting matrix and the zs are instrumentsthe objective function is smooth in the parameters despite thediscreteness of the entry decisionstwo limitations:

requires heterogeneity in all of the structural parametersin practice ability to estimate covariances of the structural parametersis limited

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 31 / 45

EstimationMoments and Instruments

For each carrier we try to form moments based on their entry-typedecision, price and market-share interacted with:

indicators for six market size-distance pairings (S/M/L x short/long)

indicators for high/medium/low presence at the origin

indicators for whether other carriers have above average presence atthe origin

indicator for high/medium/low average presence (across origin anddestination)

indicator for whether origin or destination are slot constrained

fuel price x a dummy for short/long routes

we will add market-speci�c moments to try to identify market �xede¤ects in demand

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 32 / 45

Identi�cationIntuition

the full parametric structure of the model is imposed duringestimationhowever, the arguments for identi�cation would be based on exclusionrestrictions:

for example, the characteristics (e.g., presence) of other carriers willa¤ect their entry decisions and equilibrium pricesfactors, such as slot constraints, that are assumed to a¤ect �xed costs,will also a¤ect entry decisionsmovements in fuel prices (large during our period) could alsopotentially help to identify demand coe¢ cients

the covariance of market shares and prices (conditional onobservables) will play a role in identifying the relative importance ofunobserved heterogeneity in qualities and marginal costs

e.g., positive (negative) covariance suggests more heterogeneity inqualities (marginal costs)

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 33 / 45

Identi�cationIntuition

the level of �xed costs will be identi�ed by the amount of entry

heterogeneity in �xed costs will be identi�ed from how qualities andcosts of entrants vary with market size

if �xed costs are quite similar across carriers, we should only get the�best�entrants in small markets

but, we have only limited variation in the number of potential entrants

an exception is Southwest, which was growing into new hubs duringthe sample

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 34 / 45

EstimationHow Could We Weaken the Sequential Known Order of Entry Assumption?

we can weaken our equilibrium selection assumptionsin particular, we can still use importance sampling to approximatelower and upper bound moments (as in Ciliberto and Tamer (2009)by calculating outcomes for

all possible orders (sequential)all possible pure strategy equilibria (simultaneous)this is computationally quick

in Monte Carlos with a limited number (e.g., 18 parameters) aCT-style approach for searching for bounds also works pretty well

we get tight boundsre�ects the fact that there are rarely more than 3 outcomes that can besupported as equilibriafor the same reason, an estimated probabilistic order of entry gives veryimprecise estimates on the order determining mechanism

the problem is having con�dence in the bounds derived as the numberof parameters increases

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 35 / 45

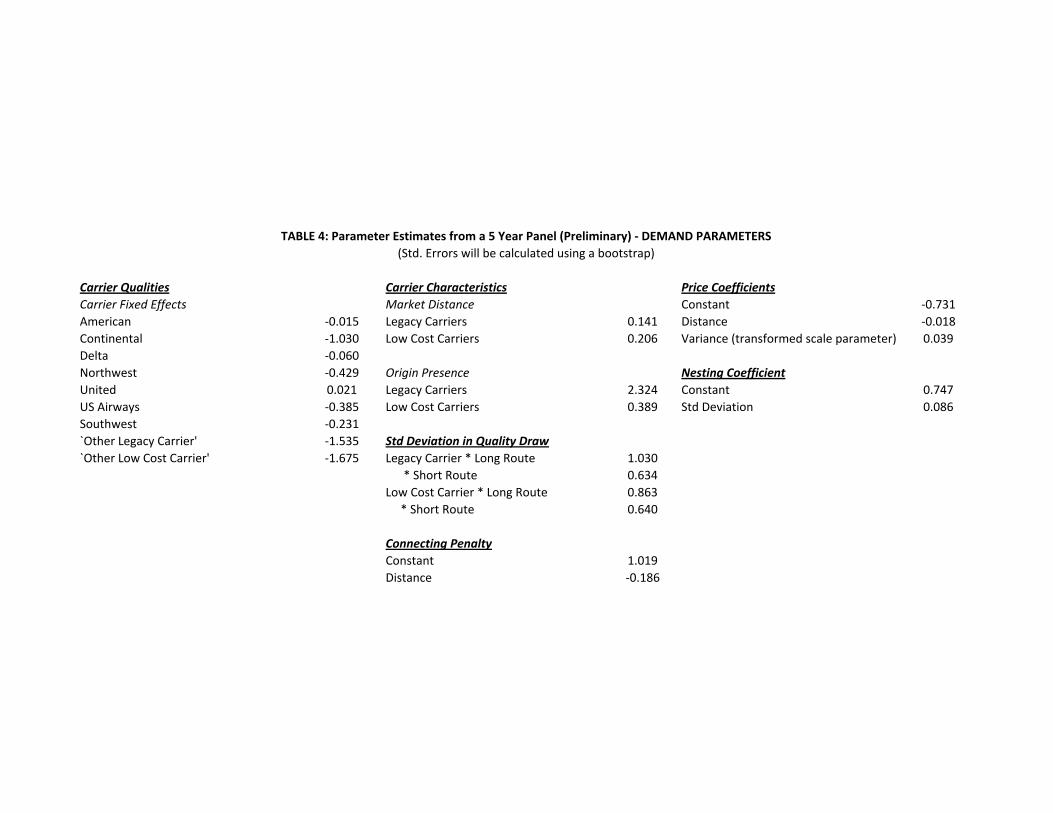

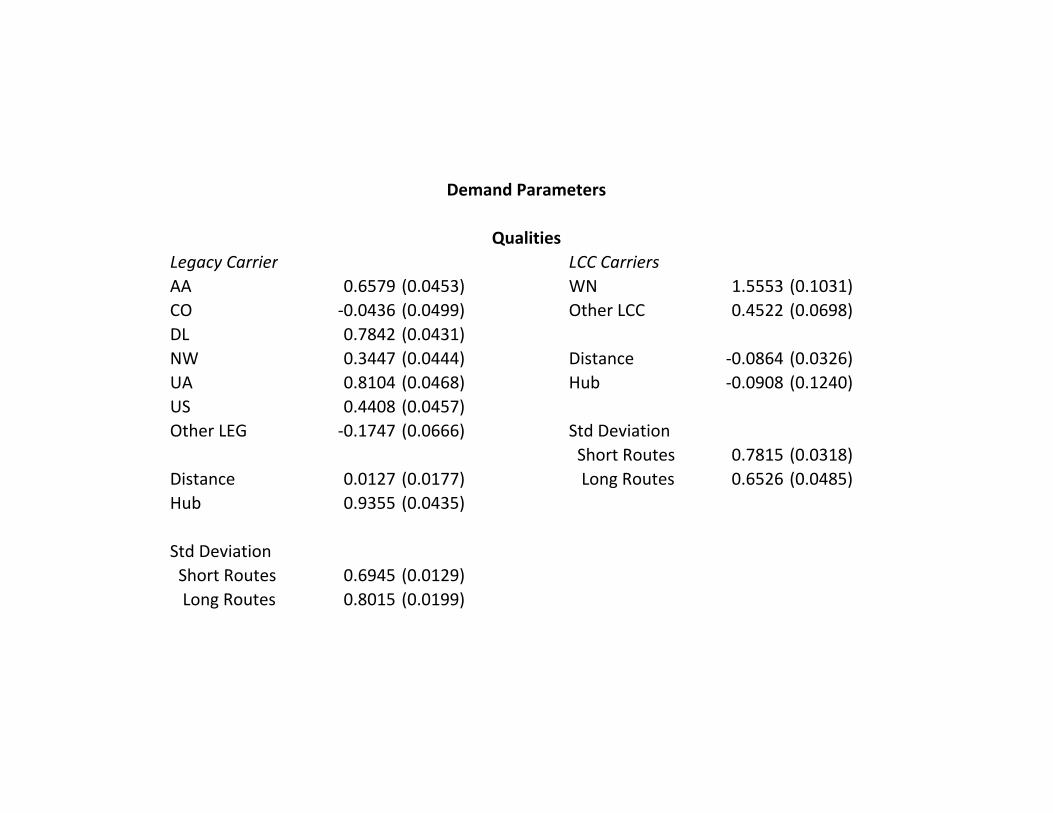

Carrier Qualities Carrier Characteristics Price CoefficientsCarrier Fixed Effects Market Distance Constant -0.731American -0.015 Legacy Carriers 0.141 Distance -0.018Continental -1.030 Low Cost Carriers 0.206 Variance (transformed scale parameter) 0.039Delta -0.060Northwest -0.429 Origin Presence Nesting CoefficientUnited 0.021 Legacy Carriers 2.324 Constant 0.747US Airways -0.385 Low Cost Carriers 0.389 Std Deviation 0.086Southwest -0.231`Other Legacy Carrier' -1.535 Std Deviation in Quality Draw`Other Low Cost Carrier' -1.675 Legacy Carrier * Long Route 1.030

* Short Route 0.634Low Cost Carrier * Long Route 0.863 * Short Route 0.640

Connecting PenaltyConstant 1.019Distance -0.186

TABLE 4: Parameter Estimates from a 5 Year Panel (Preliminary) - DEMAND PARAMETERS(Std. Errors will be calculated using a bootstrap)

Legacy, Direct Service Legacy, Connecting ServiceConstant 2.220 Constant 1.376Distance 0.682 Distance 0.639Jet Fuel Price -0.017 Jet Fuel Price 0.040Std Deviation 0.934 Std Deviation 1.108

Low Cost Carrier, Direct Service Low Cost Carrier, Connecting ServiceConstant 1.260 Constant -0.011Distance 0.974 Distance 1.237Jet Fuel Price -0.182 Jet Fuel Price -0.052Std Deviation 1.035 Std Deviation 1.589

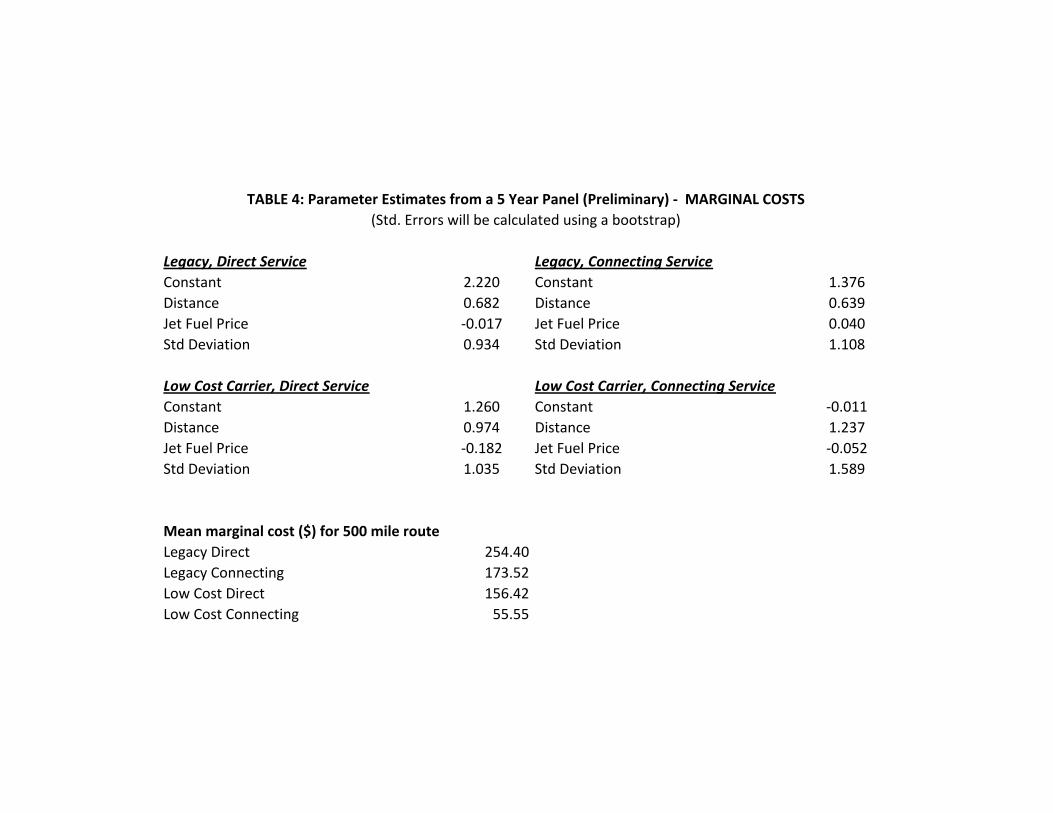

Legacy Direct 254.40Legacy Connecting 173.52Low Cost Direct 156.42Low Cost Connecting 55.55

Mean marginal cost ($) for 500 mile route

TABLE 4: Parameter Estimates from a 5 Year Panel (Preliminary) - MARGINAL COSTS(Std. Errors will be calculated using a bootstrap)

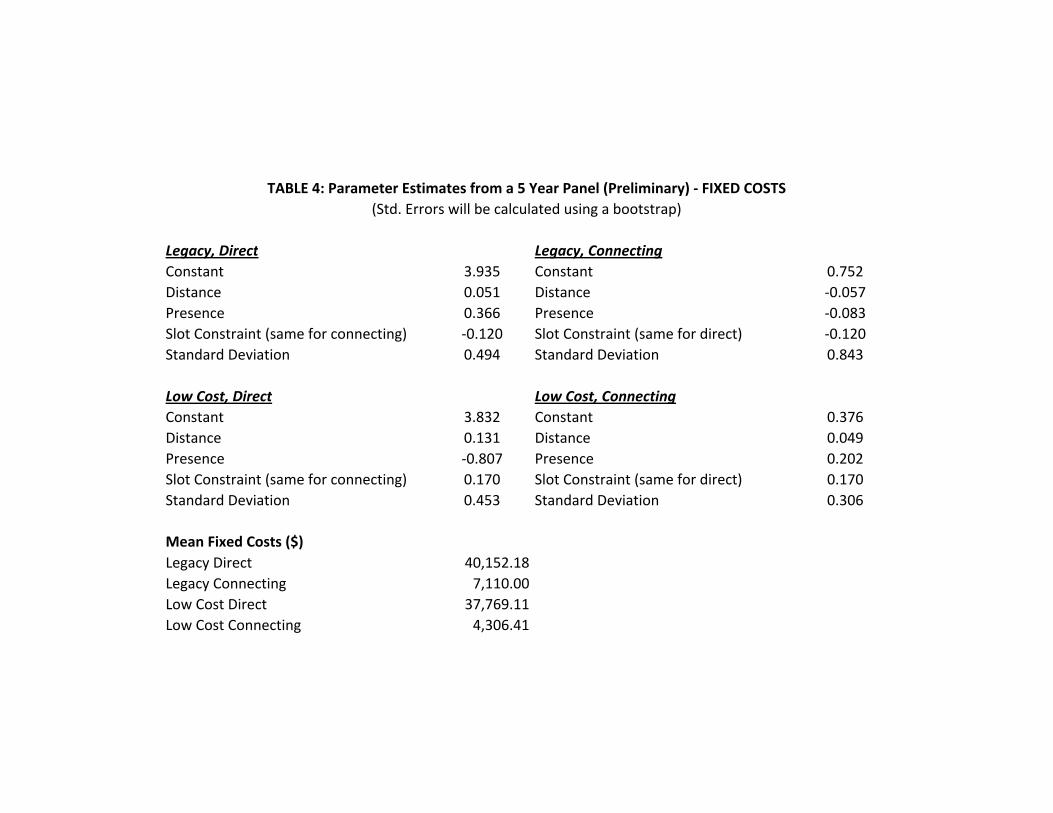

Legacy, Direct Legacy, ConnectingConstant 3.935 Constant 0.752Distance 0.051 Distance -0.057Presence 0.366 Presence -0.083Slot Constraint (same for connecting) -0.120 Slot Constraint (same for direct) -0.120Standard Deviation 0.494 Standard Deviation 0.843

Low Cost, Direct Low Cost, ConnectingConstant 3.832 Constant 0.376Distance 0.131 Distance 0.049Presence -0.807 Presence 0.202Slot Constraint (same for connecting) 0.170 Slot Constraint (same for direct) 0.170Standard Deviation 0.453 Standard Deviation 0.306

Mean Fixed Costs ($)Legacy Direct 40,152.18Legacy Connecting 7,110.00Low Cost Direct 37,769.11Low Cost Connecting 4,306.41

TABLE 4: Parameter Estimates from a 5 Year Panel (Preliminary) - FIXED COSTS(Std. Errors will be calculated using a bootstrap)

Unconditional UnconditionalPotential Entrants Service Type Mean Price No. of Passengers Implied Mean Implied Mean

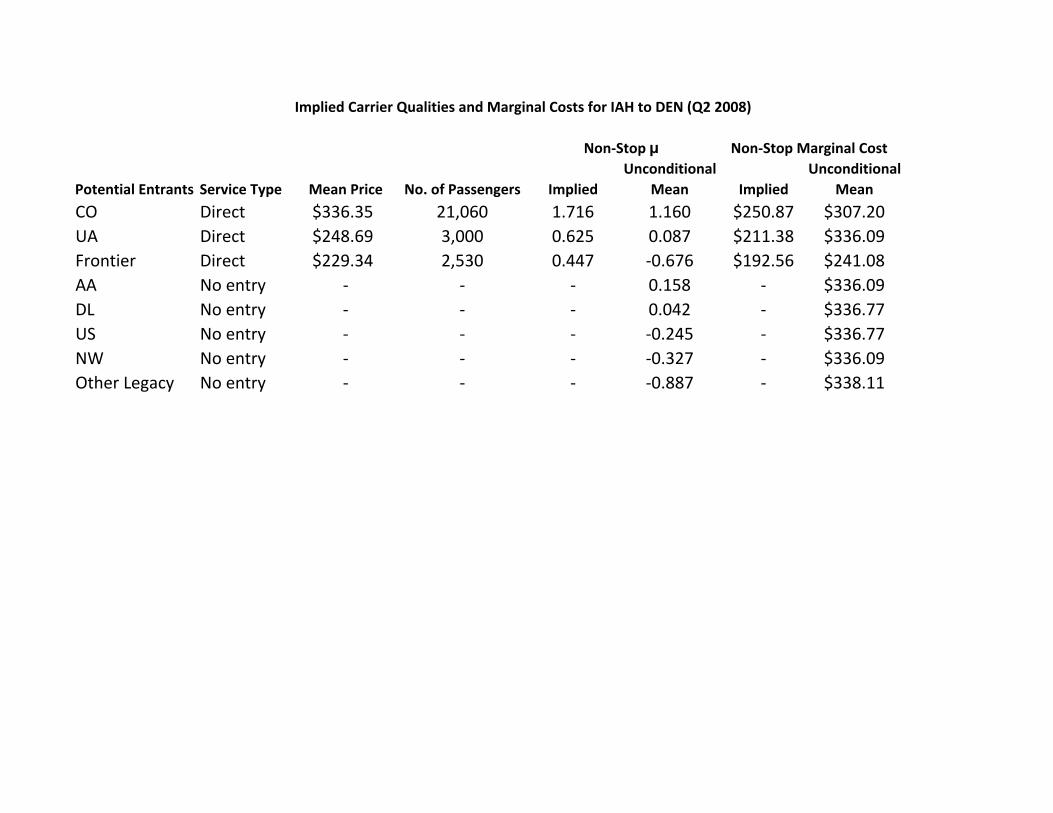

CO Direct $336.35 21,060 1.716 1.160 $250.87 $307.20UA Direct $248.69 3,000 0.625 0.087 $211.38 $336.09Frontier Direct $229.34 2,530 0.447 -0.676 $192.56 $241.08AA No entry - - - 0.158 - $336.09DL No entry - - - 0.042 - $336.77US No entry - - - -0.245 - $336.77NW No entry - - - -0.327 - $336.09Other Legacy No entry - - - -0.887 - $338.11

Implied Carrier Qualities and Marginal Costs for IAH to DEN (Q2 2008)

Non-Stop Marginal CostNon-Stop μ

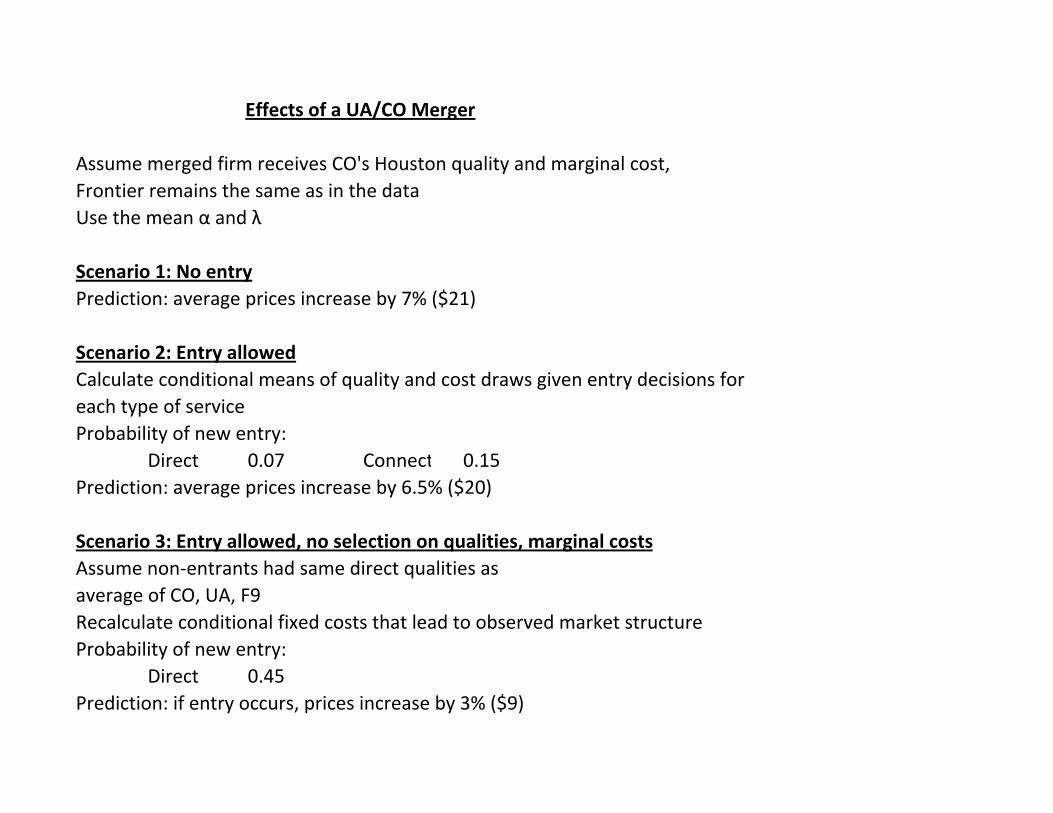

Assume merged firm receives CO's Houston quality and marginal cost, Frontier remains the same as in the dataUse the mean α and λ

Scenario 1: No entryPrediction: average prices increase by 7% ($21)

Scenario 2: Entry allowedCalculate conditional means of quality and cost draws given entry decisions foreach type of serviceProbability of new entry:

Direct 0.07 Connect 0.15Prediction: average prices increase by 6.5% ($20)

Scenario 3: Entry allowed, no selection on qualities, marginal costsAssume non-entrants had same direct qualities asaverage of CO, UA, F9Recalculate conditional fixed costs that lead to observed market structureProbability of new entry:

Direct 0.45Prediction: if entry occurs, prices increase by 3% ($9)

Effects of a UA/CO Merger

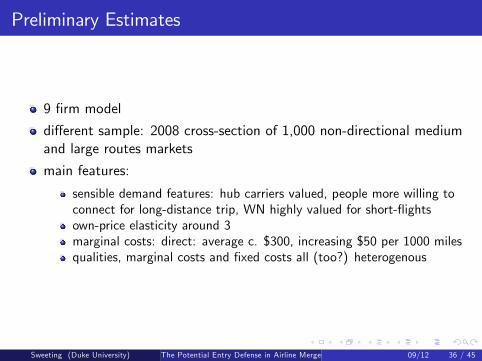

Preliminary Estimates

9 �rm model

di¤erent sample: 2008 cross-section of 1,000 non-directional mediumand large routes markets

main features:

sensible demand features: hub carriers valued, people more willing toconnect for long-distance trip, WN highly valued for short-�ightsown-price elasticity around 3marginal costs: direct: average c. $300, increasing $50 per 1000 milesqualities, marginal costs and �xed costs all (too?) heterogenous

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 36 / 45

Legacy Carrier LCC CarriersAA 0.6579 (0.0453) WN 1.5553 (0.1031)CO -0.0436 (0.0499) Other LCC 0.4522 (0.0698)DL 0.7842 (0.0431)NW 0.3447 (0.0444) Distance -0.0864 (0.0326)UA 0.8104 (0.0468) Hub -0.0908 (0.1240)US 0.4408 (0.0457)Other LEG -0.1747 (0.0666) Std Deviation

Short Routes 0.7815 (0.0318)Distance 0.0127 (0.0177) Long Routes 0.6526 (0.0485)Hub 0.9355 (0.0435)

Std Deviation Short Routes 0.6945 (0.0129) Long Routes 0.8015 (0.0199)

Demand Parameters

Qualities

Price Sensitivity Connecting Penalty (both types)Constant 0.3029 (0.0100) ConstantDistance 0.0879 (0.0055) Distance 1.0153 (0.0190)Variance Std Deviation -0.1653 (0.0084) Short Routes 0.0062 (0.0008) 0.3132 (0.0047) Long Routes 0.0255 (0.0030)

Nesting ParameterMean 0.5339 (0.0072)Std Deviation 0.1343 (0.0068)

Other Demand Parameters

Demand Parameters, Cont.

Legacy Carrier LCC Carriers Legacy Carrier LCC CarriersConstant 2.0966 (0.0508) Constant 1.1289 (0.1109) Constant 3.7276 (0.0378) Constant 4.5748 (0.0932)Distance 0.5566 (0.0246) Distance 0.4708 (0.0428) Distance 0.1223 (0.0158) Distance -0.1836 (0.0394)Hub -0.2506 (0.0664) Hub 0.3934 (0.1029) Hub -0.1168 (0.0394) Hub -0.477 (0.1125)Std Deviation 0.9705 (0.0155) Std Deviation 0.7212 (0.0247) Std Deviation 0.4848 (0.0210) Std Deviati 0.6946 (0.0600)

Legacy Carrier LCC Carriers Legacy Carrier LCC CarriersConstant 1.2205 (0.0403) Constant 1.7031 (0.1374) Constant 0.6718 (0.0220) Constant 0.4815 (0.0367)Distance 0.7669 (0.0180) Distance 0.6847 (0.0505) Distance -0.0714 (0.0063) Distance -0.0501 (0.0094)Hub 0.2004 (0.0458) Hub 0.2162 (0.1553) Std Deviation 0.525 (0.0543) Std Deviati 0.2362 (0.0626)Std Deviation 0.7963 (0.0170) Std Deviation 1.1068 (0.0448)

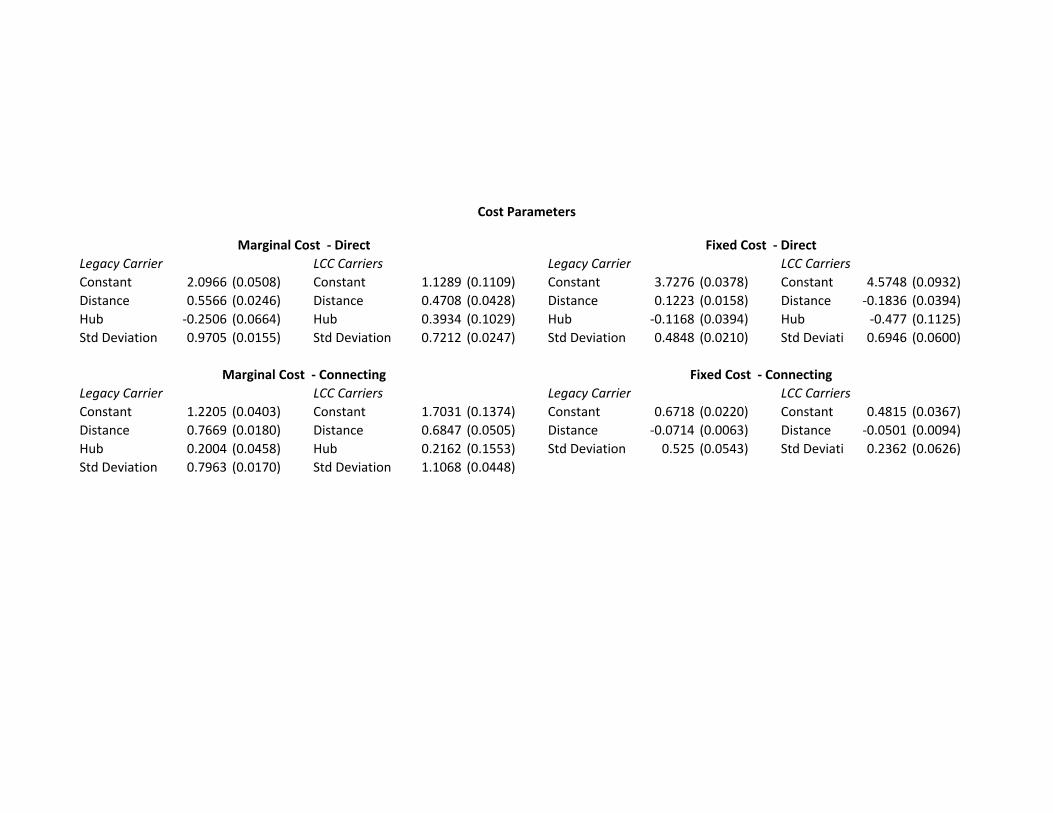

Cost Parameters

Marginal Cost - Direct

Marginal Cost - Connecting

Fixed Cost - Direct

Fixed Cost - Connecting

Illustrative Counterfactual

consider the ATL-DTW market

one of the markets of concern in the DL/NW mergerit actually did experience indirect entry

will use this market to

illustrate selectionperform an analysis of whether a merger is pro�table andwelfare-reducing allowing for entryas an obvious comparison, if one of the merging parties is replaced withan identical new entrant, merger won�t be pro�table (absent synergies)and it won�t a¤ect welfare

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 37 / 45

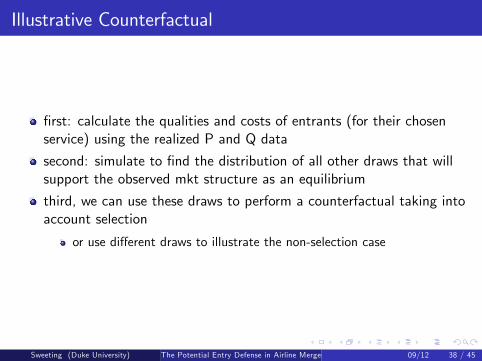

Illustrative Counterfactual

�rst: calculate the qualities and costs of entrants (for their chosenservice) using the realized P and Q data

second: simulate to �nd the distribution of all other draws that willsupport the observed mkt structure as an equilibrium

third, we can use these draws to perform a counterfactual taking intoaccount selection

or use di¤erent draws to illustrate the non-selection case

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 38 / 45

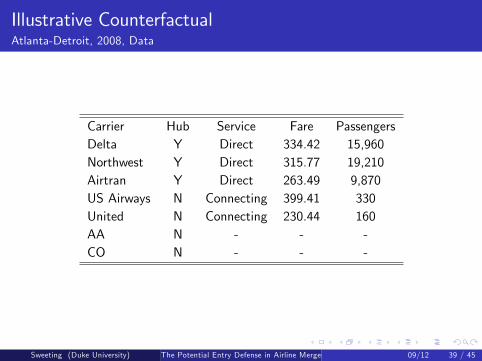

Illustrative CounterfactualAtlanta-Detroit, 2008, Data

Carrier Hub Service Fare PassengersDelta Y Direct 334.42 15,960Northwest Y Direct 315.77 19,210Airtran Y Direct 263.49 9,870US Airways N Connecting 399.41 330United N Connecting 230.44 160AA N - - -CO N - - -

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 39 / 45

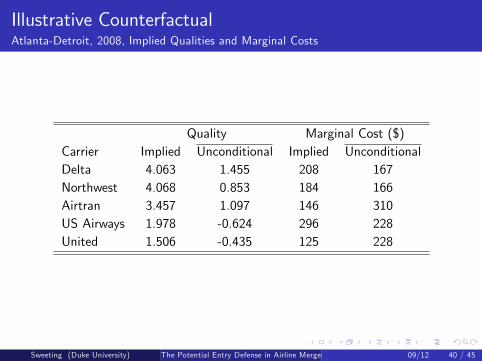

Illustrative CounterfactualAtlanta-Detroit, 2008, Implied Qualities and Marginal Costs

Quality Marginal Cost ($)Carrier Implied Unconditional Implied UnconditionalDelta 4.063 1.455 208 167Northwest 4.068 0.853 184 166Airtran 3.457 1.097 146 310US Airways 1.978 -0.624 296 228United 1.506 -0.435 125 228

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 40 / 45

Illustrative CounterfactualAtlanta-Detroit, 2008, Non-Entrant Qualities and Costs

Direct Quality Direct Marginal Cost ($)Carrier Conditional Unconditional Conditional UnconditionalAmerican 0.51 0.52 207 200Continental -0.47 -0.46 204 200

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 41 / 45

Example CounterfactualAtlanta-Detroit, 2008, DL/NW Merger Simulation

consider a merger of DL and NW

assume they take the average of the pre-merger quality and cost drawsother �rms keep their pre-merger draws

what will be the market structure now? is the merger pro�table?

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 42 / 45

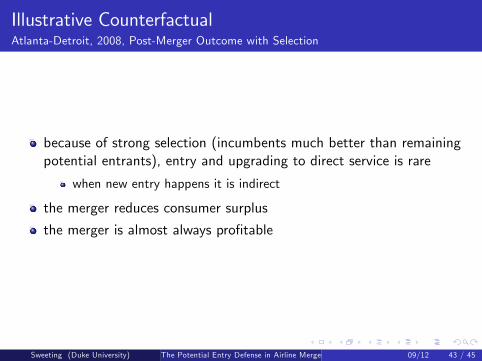

Illustrative CounterfactualAtlanta-Detroit, 2008, Post-Merger Outcome with Selection

because of strong selection (incumbents much better than remainingpotential entrants), entry and upgrading to direct service is rare

when new entry happens it is indirect

the merger reduces consumer surplus

the merger is almost always pro�table

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 43 / 45

Illustrative CounterfactualAtlanta-Detroit, 2008, Post-Merger Outcome without Selection

suppose instead that the potential entrants have quality draws fordirect service like those of the incumbents

entry is now very attractive with or without the mergerif we increase �xed costs of direct service so that won�t enterpre-merger, they will want to enter post-merger

in this case the merger is not pro�table, and the merger may notreduce welfare

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 44 / 45

Conclusions & Insights

acceptance of the �potential entry defense� should require both:

an explanation for why the potential entrants are not in the marketalready

common �xed costs or sunk entry costs may provide this explanation

and an explanation for why the incumbents are in the market ratherthan the potential entrants

�xed costs or sunk entry costs may not provide this explanationshould consider whether marginal costs or qualities drive this selection

we believe that almost any entry process is going to be selective

we develop a highly parametric model to estimate the degree ofselection, and perform counterfactuals

our initial results, and stylized facts in airline mergers, are consistentwith selection

Sweeting (Duke University) The Potential Entry Defense in Airline Mergers 09/12 45 / 45