Embed Size (px)

Citation preview

The Politics and Impact of PPACA on Brokers and

Employers

Janet Trautwein, CEO

National Association of Health Underwriters

The New Political Dynamics• Changes to Congress– Factors to Consider:• Very conservative Republican base in the House• Desire to repeal rather than fix

• Election Results—Changes to States– New Governors– Impact of Tea Party– Desire to wait on Supreme Court– Decision to do nothing

The Unintended Consequences• Dependents to Age 26 and lifetime and annual limits– Popular but at a cost – waivers required on limits

• Medical Loss Ratios– Devastating to Brokers

• Grandfathered plan issues– Very few employers can meet grandfathering requirements

• Pre-existing conditions limitations for children– Child only coverage unavailable in many states

• Restrictions on OTC medications– Encourages use of more expensive medications and

physician visits

Limited Benefits Plan Waivers• These plans typically offered to part-time

employees or others that may not have access to or be able to afford other coverage.

• Initial waivers were granted in September 2010 if it could be demonstrated that it would cause a significant number of people to lose access to any coverage prior to 2014.

• The initial waivers were granted for one year.

Current Status• On June 17, 2011, CMS issued a notice that plans that

had received waivers already could extend their waiver through 2013.

• The waiver extension request must be submitted by September 22, 2011.

• Any plan offered prior to September 23, 2010 that intends to file an initial waiver must file by September 22, 2011.

• The guidance also includes new disclosure requirements regarding communication to plan participants.

Status of MLR

• HR 1206 now has 107 bipartisan cosponsors• Senate legislation to be introduced soon• NAIC broker task force has endorsed HR 1206• Further NAIC action expected by September• NCOIL (National Conference of State

Legislators) has also endorsed HR 1206

Key Health Care Reform Bills 112th Congress

• Overall Repeal – H.R. 2 – Cantor (R-VA) – Repealing the Job

Killing Health Care Law Act– S. 192 – DeMint (R-SC) – Repealing the Job

Killing Health Care Law Act

• Health Insurance Tax– H.R. 1370 – Boustany (R-LA) – Health insurance

tax repeal

Key Health Care Reform Bills 112th Congress

• Employer Mandate Repeal– H.R. 1744 – Boustany (R-LA) – American Job

Protection Act– S. 20 – Hatch (R-UT) – American Job Protection

Act

• Individual Mandate Repeal– S. 19 – Hatch (R-UT) – American Liberty

Restoration Act

Key Health Care Reform Bills 112th Congress

• Medical Malpractice Reform– H.R. 5 – Gingrey (R-GA) – Help Efficient,

Accessible, Low-cost, Timely Healthcare (HEALTH) Act

– S. 1099 – Blunt (R-MO) – Help Efficient, Accessible, Low-cost, Timely Healthcare (HEALTH) Act

Key Health Care Reform Bills 112th Congress

• FSA Over-the-Counter– H.R. 1004 – Boustany (R-LA) – Medical FSA

Improvement Act

• HSA Reform– S. 1098 – Hatch (R-UT) – Family and Retirement

Health Investment Act– H.R. 2010 – Paulsen (R-MN) – Family and

Retirement Health Investment Act

Key Health Care Reform Bills 112th Congress

• MLR Repeal–H.R. 1206 – Rogers (R-MI) – Access to

Professional Health Insurance Advisors Act–H.R. 2077 – Price (R-GA) – MLR Repeal

Act

PPACA Requirements in 2014

PPACA in 2014 – Individual Mandate

• Requires all American citizens and legal residents to purchase qualified health insurance coverage

• Legal challenges to the constitutionality of this requirement will take this case to the Supreme Court.

• In 2014, those without insurance will pay the greater of $95 or 1% off household income that exceeds personal exemption for that year

• Starting in 2016, the penalties rise, to the greater of $695 or 2.5% of income. These penalties apply to EACH family member without coverage

PPACA in 2014 – Individual Mandate

• Exemptions to individual mandate for:– financial hardship– religious objections (see for reference IRC Sec. 1402 (g)

(1))– American Indians– those without coverage for less than three months– undocumented immigrants, incarcerated individuals– those for whom the lowest cost plan option exceeds 8% of

an individual’s income, and those with incomes below the tax filing threshold

Current Status of Individual Mandate

• On June 29, 2011, the U.S. Court of Appeals for the 6th Circuit ruled that the individual mandate is constitutional. This ruling affirms an October 2010 U.S. District Court decision.

• Two other U.S. Courts of Appeal (4th and 11th Circuits) have decisions pending.

• The June 29th ruling moves the process one step closer to Supreme Court review.

• Meanwhile, the Republican majority in the House continues to push for repeal of the provision.

PPACA in 2014• Coverage must be offered on a guarantee issue

basis in all markets and be guarantee renewable

• Rates are restricted to 3 to 1 for age and no health status

• Exclusions based on preexisting conditions would be prohibited in all markets

• Redefines small group coverage as 1-100 employees.

PPACA in 2014• Creates sliding-scale tax credits for non-Medicaid

eligible individuals with incomes up to 400% of FPL to buy coverage through the exchange

• The requirement that the subsidies are only available through the exchange is significant

• It is a particular threat to employer plans due to other provisions that allow employees to opt out of employer sponsored coverage

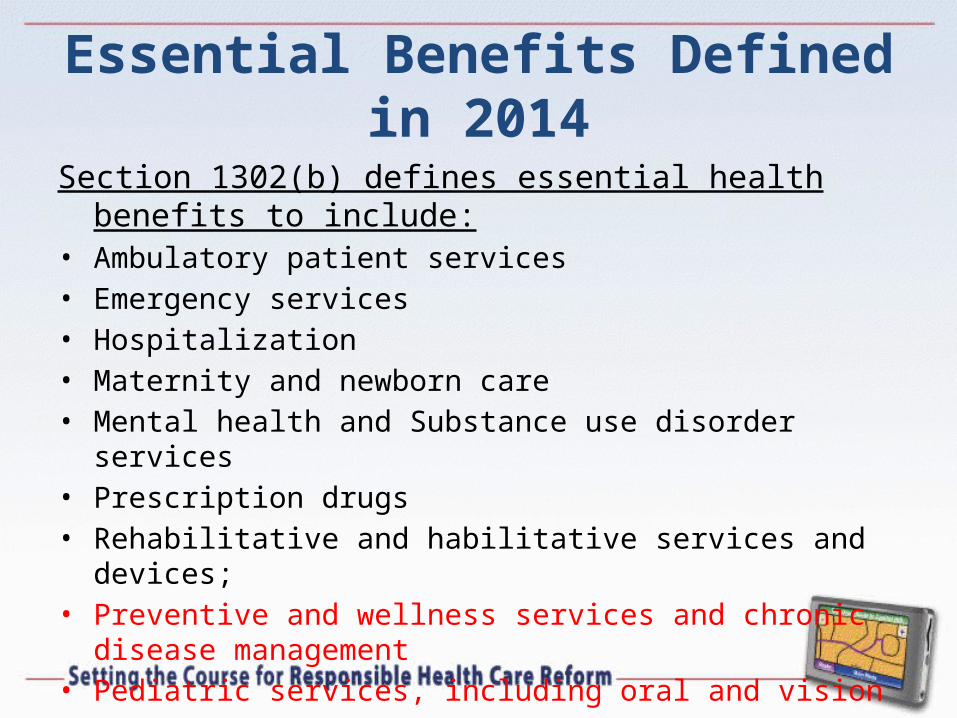

Essential Benefits Defined in 2014

Section 1302(b) defines essential health benefits to include:• Ambulatory patient services• Emergency services• Hospitalization• Maternity and newborn care• Mental health and Substance use disorder services• Prescription drugs • Rehabilitative and habilitative services and devices; • Preventive and wellness services and chronic disease management• Pediatric services, including oral and vision care

Institute of Medicine Recommendations on Preventive Care for Women

– Screening for gestational diabetes– Human Papilloma virus DNA testing– Annual counseling and screening on STDs & HIV– FDA approved contraceptives, sterilization

procedures, and counseling– Lactation support and equipment rental– Screening and counseling for domestic violence– At least one well-woman preventive visit annually

Health Insurance Exchanges

Health Insurance Exchanges

• The establishment of health insurance exchanges is one of the most significant and far-reaching aspects of the private health insurance reforms contained in the federal Patient Protection and Affordable Care Act (PPACA).

• Decisions state and federal policymakers will be making over the next few years regarding design will be critical.

©2010 Steptoe & Johnson LLP

Exchanges - 2014

A web portal

“marketplace” for health

insurance

A web portal

“marketplace” for health

insurance

Federal Government• Sets criteria for plan participation and purchaser eligibility • Provides subsidies for individuals • Manages state Exchange if a state

fails to

Individuals No subsidies for ones offered

employer-based coverage, unless that coverage is “unaffordable” or doesn’t meet quality test

Small Businesses Groups of up to 100

employees, can buy unsubsidized coverage through the Exchange

States• Each sets up own Exchange

structure and governance• Will be involved in premium

rate reviews; can approve/reject as provided under state law

Grandfathered, self-insured and

large fully insured plans not eligible

to participate

Exchanges—Who Has AccessPurchaser Types of Coverage

Individual Coverage

Group Coverage

Income-Eligible Subsidized Coverage

Individuals without access to employer coverage (U.S citizens and legal residents only)Individuals whose employer coverage doesn’t meet the affordability or quality testsIndividuals previously covered by the Pre-existing Condition Insurance PlanSmall employers and their employees

Congress and Congressional Staff

Groups With No Access and the Potentially Uninsured

Purchaser No Exchange Access Potentially Uninsured

Any size employer who wants to maintain a grandfathered planEmployer with more than 100 employees (by 2017 states could allow)Any size employer who wants to offer a self-funded productPeople of all income levels who have qualified group coverage that meets the affordability and quality tests People eligible for Medicaid/S-CHIP but not enrolledPeople the choose to ignore the individual mandate/pay penaltyIndividuals who are not U.S. Citizens or Legal Residents

Exchanges – Inside and Outside Markets• Congress specifically provided that individual

and group health insurance markets are to exist outside of the exchanges.

• The law specifies that “grandfathered” plans will continue to exist outside the exchange.

• Other plans are also permitted to exist outside of the exchange, and from experience in Massachusetts and Utah, some individuals and businesses will continue to purchase coverage there.

Employers and Exchanges• Making sure exchanges provide a benefit for employers and do

not in any way undermine the ability or willingness of employers to provide coverage is a top priority.

• Although PPACA allows the state the option of expanding the exchange to serve as a potential coverage option for larger groups beginning January 1, 2017, this could result in unintended consequences. – The large employers that would be attracted to the exchange

would be those with an older and sicker employee population that would benefit from the exchange’s modified community rating structure.

– This would increase the cost of coverage for other participants.

Questions Employers Are Asking• Will the exchanges really save us money ? • How will tax credits /subsidies or vouchers be

administered and tracked back to employers?• What is considered in determining “household” or

family income to determine if coverage “unaffordable” ?

• Exchanges are a somewhat new idea – and we are hearing problems with the Massachusetts exchange – what if they fail?

• Can we as a country afford all these new subsidies?

Current Status

• On July 11, HHS released a proposed rule on establishment of Exchanges.

• The rule includes the minimum requirements for carriers to offer qualified plans in an Exchange

• It also includes the requirements employers must meet to participate in the SHOP exchange.

Current Status• The proposed rule theoretically gives states

more flexibility in implementing Exchanges.• The rule indicates that a state may receive

“conditional approval” if they are making progress even if they can’t demonstrate full operational status by January 1, 2013.

• The regulations also allow states to develop to partner with the federal government and use the systems being developed there.

Current Status• The regulation does not address:– premium subsidies– the process for receiving an exemption from the

individual mandate– The definition of essential health benefits– Quality standards for Exchanges and QHPs

• Comments on this proposed rule are due by September 28, 2011.

• The remaining items are expected to be addressed by June of 2012.

Other Newly Released Regulations and Developments

• Proposed Rule on Reinsurance and Risk Adjustment

• Proposed Rule on Cooperatives• OPM Request for Information on Multi-State

Plans• Pre-existing conditions plan now using agents

after low initial enrollments in the program.

Employer Responsibilities

Employer Responsibilities• Employer must count all full-time employees and

part-time employees – on a full-time equivalent basis – in determining if they have 50 or more employees– Certain seasonal workers are not counted in determining if

employer has 50 workers– Full-time = 30 or more hours per week, determined on a

monthly basis• The definition of full-time employee is a major topic

of discussion on Capitol Hill

• Penalties assessed for “no coverage” or coverage that is not “affordable”

No Coverage• If an employer fails to provide its full-time employees

(and their dependents) the opportunity to enroll in “minimum essential coverage,” and

• One or more full-time employees enrolls for coverage in an exchange and qualifies for a premium tax credit or cost-sharing reduction, then

• Employer penalty = $2,000 for each of its full-time employees in the workforce

Unaffordable Coverage• If employer offers its full-time employees (and their dependents)

the opportunity to enroll in minimum essential coverage, and• One or more full-time employees enrolls for coverage in an

exchange and qualifies for a premium tax credit or cost sharing reduction because– The employee’s share of the premium exceed 9.5% of

income, or– The actuarial value of the coverage was less than 60%, then

• Employer penalty = $3,000 for each full-time employee who receives a tax credit or cost-sharing reduction

Summary of Potential Employer Penalties under PPACA, Cong. Research Service May 14, 2010

Some Good News!

• The provision on free-choice vouchers was removed in the budget act agreement.• The requirement that businesses issue

1099’s for vendor payments exceeding $600 has been repealed.

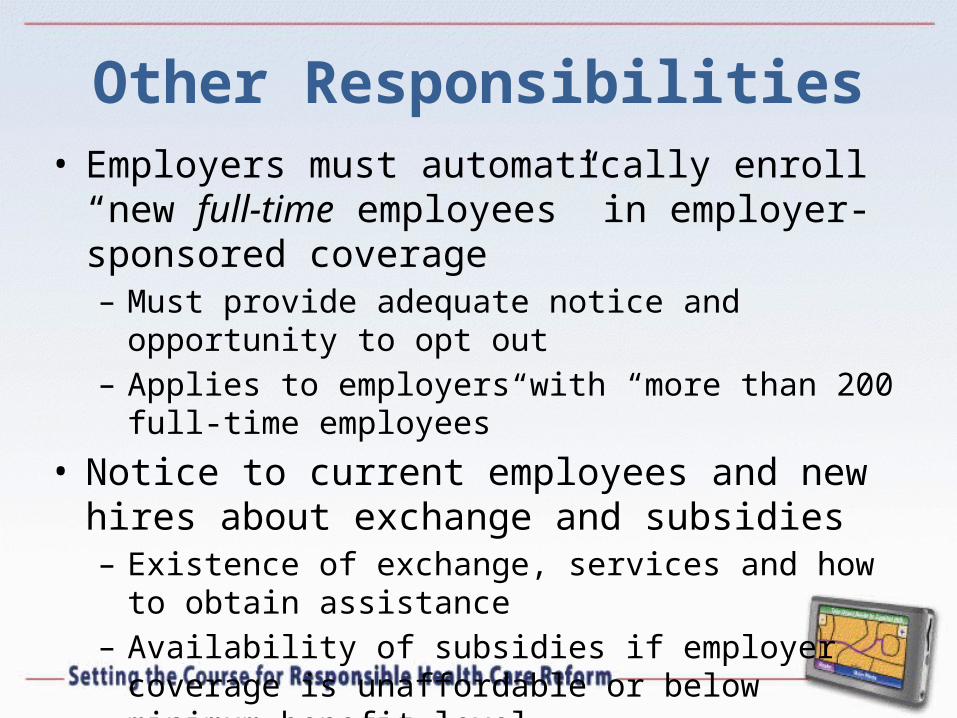

Other Responsibilities• Employers must automatically enroll “new full-time

employees” in employer-sponsored coverage– Must provide adequate notice and opportunity to opt out– Applies to employers with “more than 200 full-time

employees”

• Notice to current employees and new hires about exchange and subsidies– Existence of exchange, services and how to obtain

assistance– Availability of subsidies if employer coverage is

unaffordable or below minimum benefit level.

More Employer Responsibilities• New rules are out relative to the reporting on

W-2s the value of employer provided health insurance

• A new four-page summary of benefits must be provided to employees beginning in 2012

• Completion of form 5500 will become more complex

• New requirements on claims and appeals will be in place

More Employer Responsibilities

• Tracking and notification of number of months employees covered by minimum required coverage.

• A variety of new reporting requirements for self-funded plans must be provided to the government and employees.

Summaries and Related Requirements

• Effective for plan years beginning on or after March 23, 2012, both insured and self-funded plans will be required to provide new summaries of benefits before and after enrollment.

• Failure to provide required information will result in a fine of not more than $1,000 per enrollee.

• HHS guidance for this provision was due on March 23, 2011. However, as of July 21, 2011, guidance has not been issued.

What is Included in this Section• A glossary of standard medical and insurance terms• A four-page Benefit Summary describing plan

benefits, cost sharing and limitations• A “Coverage Facts Label” with an example of costs

based on the specific plan’s benefits for three conditions: maternity, breast cancer treatment and diabetes management

• Online availability of Certificates, SPDs and policies• Notification of material modifications at least 60 days

before their effective date

Pending or Watch Listed• 105(h) non-discrimination rules• Accountable Care Organizations• Specific process of auto-enrollment• Information Sharing for Subsidies• Class Act• MLR and Essential Benefits on Ex-Pats• Medicare Secondary Payer and potential expansion of

employer ESRD responsibility

Employer Decisions• How to budget for increased plan costs• What will the new compliance costs be?• Can I afford to continue to offer coverage to

employees?• What are the implications if I drop coverage

for employees?• What is my communication strategy?

Moving forward• MLR is our top immediate priority• Exchanges are critical• Business friendly initiatives to keep employers

engaged in providing health plans• Focus on real issues – the cost of health care• Press initiatives• Broker role in the spotlight• NAHU visibility is high• Grassroots efforts• HUPAC