Embed Size (px)

Citation preview

MA

Y 2

00

2

IS

SU

E 1

ww

w.b

rid

ge

po

int-

ca

pit

al.

co

m

Investment minefield or utopia?Europe’s healthcare industry under the microscope

Death to the Italian ratHow buy and build turned France’s Eurogestion into Italy’s number one rat catcher

Making fat boys slim Diet for an entrepreneur

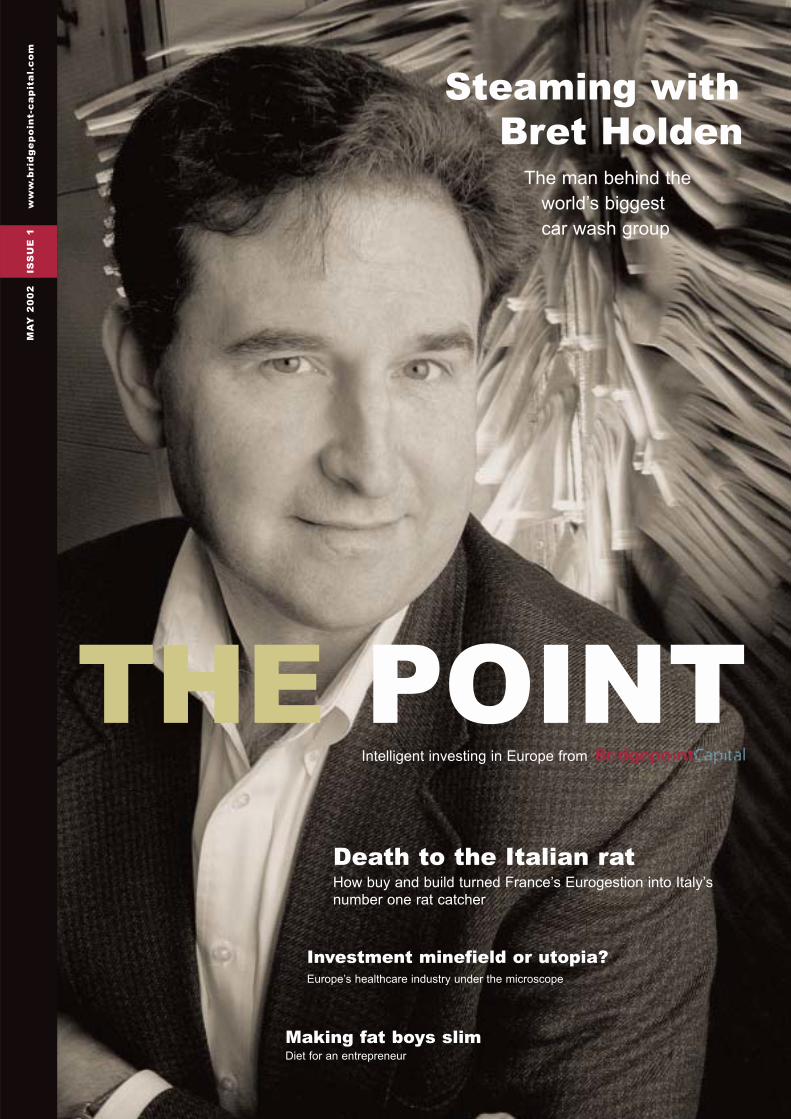

Steaming withBret Holden

The man behind the world’s biggest car wash group

THE POINTIntelligent investing in Europe from

Intelligent private equity investing in Europe

• Focus on Europe’s middle market companies

• 25 year track record of buying and selling businesses

• Over €4bn under management

• Offices in France, Germany, Italy, Spain, UK and Nordic region

EDITORIAL

What’s The Point?

The Point is our way of showingthe people who matter most to us –our investors, our managementteams, the intermediary communitywe work with and of course, ourown team - what it means to be aBridgepoint-backed investment.

Not that Bridgepoint itself needsany introduction. Our aim is to useThe Point to shine a light on the middle market and thecompanies within it as well as to provide intelligent insightinto one of the most dynamic sectors in Europe.

Typically, we invest in middle market companies because anumber of characteristics will have already drawn us to them.It goes without saying that the management of the companyitself will be impressive - both with their knowledge of theirsector and with their vision for their business. Witness BretHolden, chief executive of IMO Car Wash Group, a companyBridgepoint backed in 1998. The car wash sector and vision?Think again and read Amanda Hall’s profile of the man andhis views on what you do with over 800 car wash sitesacross Europe.

The sector in which our companies operate will also becapable of development, either through organic growth orconsolidation. In each issue of The Point, we’ll be looking atwhich sectors to watch. In this issue it’s healthcare, a marketwell known to Bridgepoint and one which frequentlymakes the headlines wherever you are in Europe. PaulDurman takes us through what he describes as ‘a near-perfectinvestment opportunity’.

And what about the businesses themselves? Bridgepointcompanies will be growing either domestically or be capableof transformation into an international operation. Recogniseyour own business in this? Catherine Wheatley explainsexactly what we mean when she explores the ‘buy and build’strategies of several Bridgepoint companies - NordiskParkering, the car park operator in Scandinavia, France’sEurogestion, the pest control group, Plastimo, the marinerecreational equipment manufacturer, Alcontrol, the Dutchanalytical services company and the UK’s specialistequipment hire company Longville Group.

All of these reasons may go some way to explaining whythis market is attracting the attention of investors fromaround the world - investors who are constantly looking forreasons to allocate their sought-after funds in areas with themost promise. I hope that like them, you too will begin to seewhy Europe’s middle market is the place to be.

William Jackson is chief executive of Bridgepoint Capital

THE POINT 3

THE POINT CONTENTS

MAY 2002 ISSUE 1 www.bridgepoint-capital.com

Published by: Bladonmore Publishing Ltd www.bladonmore.com

Publisher: Richard Rivlin

Editor: Amanda Hall

Design: Create Services

Photography: Tom Stockill

The views expressed in The Point are not necessarily those of Bridgepoint Capital

Eurogestion p9 Longville Group p10 Alcontrol Laboratories p10 Nordisk Parkering p10 Plastimo p11 IMO Group p12 Nestor Healthcare p16 Healthcall p16 Alliance Medical p16

Rhoen Klinikum p17 Synergy Healthcare p17 Match Group p18 myCFO p20 Coutts p20 C Hoare & Co p20 Centre for Nutritional Medicine p21

Companies in this issue

News 4From Stockholm to Madrid:Bridgepoint funds, acquisitions,exits, people

Rat Catcher 9How buy and build turned Pierre-VincentDebatte’s Eurogestion into Italy’s numberone pest business. By Catherine Wheatley

Face to Face 12Amanda Hall talks to Bret Holden,ceo of IMO Group on cleaning up atthe car wash

Market View 15Nick Lockley reports from Germany on the state of the privateequity business

European Healthcare 16Investment opportunities under the microscope. By Paul Durman

Making the Most 20The Point guide to smarter living. Luke Johnson in Madrid. And making fat boys slim

Bottom Line 22Richard Rivlin on how UK tax changesare boosting entrepreneurial Britain

Bridgepoint Capitalhas raised more than €1.7bn forits latest fund and could end up with closer to €2bn atformal closing in May.

The firm originally set out to raise €1.6bn butincreased interest from investors has pushed thistarget higher.

The new fund, which has an investment period ofup to five years, will target pan European mid-marketbuyout opportunities.

New investors from Europe and North America andAsia have been told that the money is earmarked fortransactions with a value up to €400m, with equityinvestments of between €15m and €100m.

The mid-market is a competitive arena, but the newfund will give Bridgepoint the opportunity to consolidateits position as a leading investor in this field over thecoming years.

The fund has already signed off its first three deals;the €206m buy out and de-listing of UK manufacturerand distributor of ethnic and speciality foods WTFoods, and the €176m growth capital/equity releasetransaction in Virgin Active, the health and fitness business;and the €67m buy out of UK specialist hire companyHydrex Group.

Bridgepoint’s new fund is likely to increase thecompetitive stakes among mid-market equity providers.William Jackson, chief executive, believes that raising thisfund in the current market vindicates the company’s

Nordisk Parkering, the biggest privately ownedcar park operator in the Nordic zone, has acquiredScanpark AS, the fourth largest parking manager inthe region.

Bridgepoint acquired Nordisk Parkering in July lastyear with a plan to grow the business organically andthrough selective acquisition. The combined group isnow the Nordic market leader and the numbertwo in the Norwegian market.

Founded in 1997, Scanpark was owned by itsmanagement team led by managing directorHans Sa lomonsen a long wi th founder andmarket ing director Torr Foss. Following theacquisition Salomonsen and Foss remain withthe company - both have reinvested in the business.

Graham Oldroyd, Bridgepoint’s director responsible

for investments in the Nordic region says: “Scanparkis the fastest growing car park operator in Norwaywith a management team that will fit well with thatof Nordisk Parkering. Combining both businesseswill also result in significant cost and operationalsynergies as wel l as improving Nordisk’sgeographic coverage.”

Around two thirds of Scanpark’s revenues comefrom car park management and a third fromparking enforcement.

Oldroyd adds: “This deal is strategically very impor-tant as it will enhance our ability to win new contractsand will give us bigger operational coverage. Carpark landlords want to know their chosen supplier isa substantial player with a good track record.”See Spotlight on Nordic Region, p7

strong reputation with its investors.Jackson says: “The European mid-market is emerging

as a place where investors want to be. This is clearfrom the number of new investors attracted to thefund who are making allocations with a privateequity firm that has a proven middle marketinvestment strategy.”

The latest fund follows Bridgepoint’s €1.6bn FirstEuropean Private Equity Fund which closed in April1999 and which has made 65 investments over the pastthree years.

Leading placement agents Helix Associates andJerome P Greene & Associates advised Bridgepoint onthe raising of funds.

Graham Dewhirst, Bridgepoint’s head of investorrelations, says: “We haveclosed initially at €1.7bn.We will close the fund onMay 3rd with around€1.9bn set against a€1.6bn target.

“By modern standards,given that a number offunds have not madetheir targets, to come inahead of ours, and withinthe time frame is verypleasing.”

4 THE POINT

Dewhirst: ahead of target

NEWS

Sto

ck

ho

lm t

o M

ad

rid

Nordisk Parkering acquires Norway’s Scanpark

New fund targets pan European buyouts

EXPRESS

When a company de-lists from a stock exchange andbecomes private again it is a serious business. Now itlooks like the recent spate of UK public-to-privates,as they are called, or PTPs could well be set to estab-lish themselves on the private equity scene in Europe.

Looking at the UK market where, since 1996, over84 PTPs worth more than €1.8bn have been completedwith the majority backed by private equity, PTPsappear to be a permanent fixture.

Bridgepoint itself has completed 11 PTPs duringthis time, including the most recent €206m de-listingof WT Foods, the manufacturer and distributorof ethnic foods, and the €371m PTP of Norcros, thebuilding materials and adhesives group. Why did thesetransactions become popular?

Many of the companies taken private during themid-late 90s were smaller company stocks, typicallycapitalised at under€800m, and in mostcases operating in sectorsout of favour with theCity, such as engineer-ing and manufacturing.

A de-listing, withbacking from afinancial buyer, enabledthese firms to raiseadditional capital forexpansion, to exploreacquisition opportunitiesand to incentivise agreater number of themanagement teamthrough equity participation in the business. This waymanagement could see a re tur n for the i r equityas opposed to a declining share price.

Although the rate of PTPs in the UK has started toslow since 1999 (when it peaked with 46 PTPs in thatyear), it still remains a viable form of funding for UKquoted companies.

And in continental Europe, PTPs are on theincrease: since 1996, there have been 54 worth€10.5bn with the highest proportion of these inFrance (18) followed by Germany (9). However, theoverall size of PTPs in Germany has considerablyexceeded that of France with PTPs worth €1.2bncompleted in Germany between 1991 and 2001compared to €543m in France.

Many smaller and mid-cap continental Europeancompanies are suffering a similar fate to that of theirUK counterparts: some operate in ‘unloved’ sectors,notably in German manufacturing and automotives,many have seen their share price decline or stagnate,many are unable to raise further capital for growthfrom existing shareholders and it is clear that they donot have the economies of scale for expansion asa single entity.

Despite certain obstacles to PTPs in continentalEurope – notably rules governing the market forcorporate control that need to be liberalised to makePTP practice more accessible – it looks like moreEuropean companies will turn to PTPs as a sensibleway to fund the expansion of their business.

And while there will be differences between the variousEuropean financial markets, the companies in questionwill have one thing in common – managementteams keen to explore ways of growing their business.

THE POINT 5

NEWS

PTPs mean businessExit Birmingham Airport

Branson sells to Bridgepoint Sir Richard Bransonhas sold a majoritystake in his health andfitness clubs businessVirgin Active toBridgepoint Capitalfor €65.28m plus afurther €20.8m tofund future growth.

The deal, valued at€176m, sees Bridgepointtake a 55 per cent stakein the company whileVirgin remains a size-able minority shareholder with 36.6 percent. The company’s managementowns 7.9 per cent of the shares withHeller Financial, the senior debtprovider, holding 0.5 per cent.

Virgin Active is to use theBridgepoint investment to fund aglobal expansion of its business.Currently the group owns nine clubs inthe UK and 76 in South Africa where itis the clear market leader.

The planned expansion will see a roll-out of eight more clubs in the UK,including three in London this year, anddevelopment of the Virgin Active brandin Europe, North America and Asia.

Frank Reed, Virgin Active chief exec-utive says: “Since Richard and Virginbacked us in developing Virgin Active’sunique health and leisure concept in 1998,we have taken the market by storm withan unbeatable combination of qualityclubs and a value-for-money offer whichhas already attracted over 350,000members in the UK and South Africa.

“This deal will allow us to roll out theconcept around the rest of the UKand the world.”

The Virgin transaction marks thesecond time that Bridgepoint hasbacked Reed and his finance directorMatthew Bucknall. In 1994 the firminvested £27.2m in a management buy-out of Living Well Health and Leisure,the fitness business run by Reed. LivingWell was sold to Stakis in 1996.

The following year Reed left Stakisand was recruited by Branson initially

Macquarie Airports Group, a private equity airport investment fund, hasbought Bridgepoint’s 24 per cent stake in Birmingham International Airport for €134.4m.

The sale marks the exit for an investment first made by Bridgepoint inFebruary 1997 when it invested alongside Aer Rianta and gives MacquarieAirports Group a substantial shareholding in one of Britain’s key regional airports.

Anthony Kahn, Macquarie Airports chairman says: “We are committed tobeing a long-term shareholder in the airport and the investment signalsour continued confidence in the long-term growth of the aviation sector. Welook forward to working alongside fellow shareholders Aer Rianta and thedistrict councils together with the management and employees in support-ing the continued successful development of the airport and the Midlands.”

Andrew Burgess, who coordinated the sale for Bridgepoint, reports that thefirm achieved a ‘very healthy return’ on its initial investment.

as a research consultant and laterto launch his Virgin-brandedhealth clubs business.

In 1996, Bridgepoint also made a€78.8m growth capital investmentin Holmes Place, now a listed company.

Rob Moores, Bridgepoint directorexplains: “We made three times ourmoney on Living Well. Via an intro-duction from Frank, we then met themanagement at Holmes Place. Thisis a sector we know and like.”

Virgin Active is positioned atwhat Moores describes as the“affordable end”of the health clubmarket selling full membershipsfor €64 a month.

The clubs are bigger than manybranded health clubs – typicallythey are between 50,000 and60,000 square feet – and have adistinct family focus.

Moores adds: “We’ve followedthis business from the drawingboard through to its first clubs andon to its roll-out because of therelationship we’ve had with itsmanagement. In some respect it’s aslightly earlier stage investmentthan we would normally make butwe have a high level of comfortwith the individuals involved.”

“It looks like

more European

companies will

turn to PTPs as

a sensible way

to fund the

expansion of

their business”

Healthy alliance: (L-R) Moores, Bucknall and Reed plan global expansion

“This deal will allow usto roll out the conceptaround the rest of theUK and the world”

The Canada Pension Plan InvestmentBoard has become the latest institutionalinvestor to earmark a percentage of itsholdings for private equity investment.

It has chosen to back Bridgepoint’slatest fund to gain exposure to mid-marketEuropean buyout deals.

A growing number of experiencedinvestors are deciding to back alternativeassets such as hedge funds and privateequity funds.

News of Canada Pension PlanInvestment Board’s commitment hashelped Bridgepoint beat its original targetof a €1.6bn fund.

The investment by the State PensionFund is an endorsement of the Europeanprivate equity market and is likely toencourage other North American fundsto invest in the region.

CPPIB made its decision to invest inBridgepoint’s fund on the strength ofthe firm’s track record in buildingbusinesses and creating long-termshareholder value.

Graham Dewhirst, Bridgepoint’s head ofinvestor relations says: “Our aim is to applyour pan-European infrastructure andresources to invest in domestic businessesthat can be transformed into internationalgroups, particularly through buy andbuild opportunities.

“In this way, we are able to release latentvalue in the middle market businesseswe buy.”

An unusual cross-border deal involvingthe sale of a private equity backed Germandata storage company to Finland Post wascompleted earlier this quarter, nearly fouryears after the business was first boughtout from a listed UK company.

Eurocom Depora, a German specialistdata storage and output products provider,bought originally by Bridgepoint’s UKoffice from Microgen for €17m has beensold to Finland Post, the Finnish nationalpostal operator for an undisclosed sum.Over the lifespan of the investment,Bridgepoint offices in Germany andScandinavia were also involved in developingthe Eurocom business.

The deal is the second transactionbetween Bridgepoint and Finland Post.The Finns had already bought the CapellaGroup of Sweden from Bridgepoint inAugust 2001.

Eurocom Depora, currently employs200 people, operating mainly in andaround Frankfurt and Duisburg. Its servicerange, principally to the insurance andfinance sectors, comprises microfilming,electronic management and filing of massinformation, retrieval systems anddocument management and printingservices. The business, which was foundedin 1970, had sales in 2001 of €21.1m.

According to Finland Post, the combinedgroup will be able to offer major interna-tional organisations, such as financial

institutions and industrial groups, end-to-end services that utilise cutting-edgetechnology, all the way from the receptionand processing of electronic data toprinting and filing services.

Analysts are expecting the nationalpostal companies across Europe to developnew products and services in a bid tocounter the competitive pressures frominternet and email services.

Niche businesses like Eurocom thathave developed innovative communicationsand data storage products will becomeincreasingly attractive as possible acquisi-tion targets for the state owned operators.

Deal triggers for middle market buyoutsWhere do deals come from? It's a question everyone involved in the private equity business

needs answered. The two charts below show the number and value of buy outs by deal source

done during 2001 in western Europe that fall into the €30m-400m bracket.

6 THE POINT

NEWS

Canadians backnew fund

Finland Post lands Eurocom

Family private

50

40

30

20

10

0

Public to private

Institutional parent

Local parent

45

15

27

49

Number of deals by source

Family private

7000

6000

5000

4000

3000

2000

1000

0

Public to private

Institutional parent

Local parent

31862896

3632

5731

Value of deals by source

€ millions

Source: Initiative Europe

Data storage: key to postal services

Spotlight on...

Alan Payne, director of BridgepointCapital responsible for the Hydrex dealadds: “The growth of the UK railmarket and Hydrex’s market leadingposition were key attractions in thisinvestment. Hydrex is the only realnational player in its market and iskeen to grow the company further.Our investment will allow the companyto continue this growth, augmentedby a selective acquisition programme.”

Bridgepoint is already an investor inthe Midlands-based Longville Group,another specialist hire firm that is theworld’s number one pump hire businessand number two in chiller hire.

Payne says: “This transactiondemonstrates Bridgepoint’s continuingcommitment to invest in qualitybus inesses despite the economicslowdown.

“We are already aware of theopportunities within the specialisthire market through our investment inLongville Group. Hydrex has manyqualities we look for in an investmentand adds to our track record ofimplementing buy-and-build strategiesfor progressive companies.”

Nordic Market

Becoming an expert on theNordic car park market isprobably not somethingGraham Oldroyd would haveput in his career plan when hestarted out in the privateequity world.

But today, as head ofBridgepoint’s business in theNordic region – a market thatcovers Denmark, Finland,Norway and Sweden – wherethe company’s biggest invest-ment is Nordisk Parkering,one of the area’s biggest car park operators, Oldroydis a genuine authority on the subject.

He is the man who orchestrated Nordisk’s firstacquisition, that of Scanpark AS, a privately heldNorwegian business.

Oldroyd knows perhaps better than anyone whyBridgepoint’s decision to start investing in the regionin 1995 and to open a Stockholm office last year hasproved a smart move.

“The Nordic market represents about eight tonine per cent of European private equitytransactions above €10m,” he says.

“The economies are well developed and have ahighly educated workforce with the highest percent-age of graduates in the world. Mainstream Europeanaccounting standards are well established, English isthe main business language and there’s a prettystrong work ethic.”

For Oldroyd, the emphasis on high-quality goodsand services is also important. “The small size ofdomestic populations forces most companies to beexport oriented.

“There’s an appreciation of the importance ofquality and value-added because if exportinggoods is critical to your business, you’ve got tooffer something someone wants to buy,” he explains.

As well as Nordisk Parkering, Bridgepoint’sprimary investments in the region are Huurre, a coldstore manufacturing company, and Aura, a businessmaking long-life industrial lighting products.

Major investments which the company has exitedinclude Toolex Alpha, a Stockholm business makingCD pressing equipment which is now quoted on thelocal exchange and produced an IRR of 351 per cent,and Semcon, an engineering and IT consultancybusiness also now a quoted company and one thatdelivered an IRR of 183 per cent.

“The region’s four countries have distincteconomies,” Oldroyd explains.

“Norway, for instance, is an oil economy whileDenmark is a strong trading nation, a mercantileculture that does not have a big manufacturing base.

“Companies will often have a strong domesticmarket and may be selling to one of the othercountries in the region,” says Oldroyd.

“When you invest in these companies you oftenhave the chance to take them pan-Nordic whichin turn makes them attractive to internationalplayers looking to get in to the region.”

While the Nordic area held up well in theaftermath of September 11, the downturn in worldstock market values has affected the businessof investing.

“We are experiencing some problems of priceexpectation,” he says. “But if you can find a willingseller, this is a good time to buy.”

IMO acquires TomanIMO Car Wash Group, Europe’s biggestindependent car wash business, hasacquired the Toman Group, a German business and one-time sister company ofIMO, from Harpen AG, a subsidiary ofGerman giant RWE. The combinedbusiness now has 800 car wash sitesacross Europe.

See interview with Bret Holden, IMO chief executive, p12

Post arrives for CapellaCapella Group AB, the Swedish data

services outsourcing business, acquired by Bridgepoint and management inOctober 1998 has been sold to FinlandPost for an undisclosed amount.

Financial Sponsor awardThe European Venture Capital Journal has named Bridgepoint Capital its Mid-Market Financial Sponsor of the Yearfor 2001. The award, judged by industryspecialists and EVCJ writers, followsBridgepoint's success last year whenit was named Mid-Market House of the Year.

WT de-listsWT Foods, one of the UK’s leading manufacturers and distributors of ethnicand speciality foods, has been de-listed in a €206m management buy out withbacking from Bridgepoint Capital. Guy Weldon of Bridgepoint says:“De-listing the company will give the business a longer investment horizon andthe resources it needs to play a full role inthe expected consolidation of the ethnicand oriental food sector.”

Bridgepoint has increased its exposureto the booming equipment hire business inthe UK with a €24m investment in theBristol-based Hydrex Group, a companyspecialising in the supply of heavyequipment and operators to the rail andconstruction industries.

The deal sees Bridgepoint become themajority stakeholder in Hydrex by buyingout existing shareholders 3i and BrianDavies, the firm’s founder who started thecompany 17 years ago. The company’sexecutive management who own a stake inthe group remain at the helm.

Hydrex has grown rapidly over the pastthree years as a result of increased publicsector spending on infrastructure and thedevelopment of the rail industry.Bridgepoint’s €24m investment will beused to expand the company’s fleet and tomake acquisitions. Andrew Simcox, chiefexecutive of Hydrex believes theinvestment will allow the company toexpand all three of its divisions: rail,industrial services and construction.

“Our markets are showing strong growthand the Bridgepoint investment gives usthe firepower to keep pace with theavailable opportunities,” he says.

THE POINT 7

NEWS

“I’m on the train.”

E M P T Y D E S K

Bridgepoint takes Hydrex stake

NEWS by Amanda Hall and Richard Rivlin

Oldroyd: region's expert

After ten years with one of France’s leadingpest control businesses, Eurogestiondirector Pierre-Vincent Debatte was bothexcited and nervous when the opportunityarose last year to acquire his chief Italianrival Libco.

Since November 1999 Debatte and hiscolleagues had bought seven French firmsand a further five Australian companieswhen Bridgepoint Capital backed their€75m management buy-out. But Libco,with a turnover more than ten times largerthan any of their previous purchases, was amuch bigger challenge.

The deal would give Eurogestion adominant position in Italy ahead ofglobal competitor Rentokil, but it wouldalso bring management obstacles andfinancial pressures.

“There was a debate about whether weshould pay a higher multiple for Libcothan Bridgepoint paid for Eurogestion. Weargued that we might risk losing valueon the group. But ultimately the strategyis to increase the multiple you can sellthe group for, so we went ahead. It’schanged the look of the entire company,”Debatte explains.

Now, after a three-year programmeof acquisitions and reorganisation,

Eurogestion is itself being eyed by com-petitors keen to acquire the flourishingbusiness. In that time, the French group’sturnover, at €130m, has increased substan-tially. Like other buy-and-builds, each newpurchase has been funded either fromcashflow or mezzanine finance rather thanby new share capital, so the original stake-holders take profits on any deal.

“Our strength is identifying, buying andmerging new businesses into the existingcompany,” says Debatte. “A sale will beproof of our success.”

For Bridgepoint, buying and buildingcompanies like Eurogestion has become akey part of its investment strategy over thelast three years. It is an active, hands-onapproach to creating value that maximisesreturns by building market leaders in keygeographic territories. The resultantbusinesses frequently make attractiveacquisitions for international players.

Around a quarter of the companiesacquired by Bridgepoint’s latest fund arewhat the company calls “serious buy-and-build candidates”, and around 10 per centof its cash is earmarked for adding toexisting investments.

Typically, directors at Bridgepoint-owned companies will spend up to fiveyears engineering a bigger and occasionallydominant market position across Europeor around the world in a bid to improveearnings and increase values.

Since the late 1990s such expansion hasadded expertise, improved best practiceand delivered straightforward scaleeconomies to many Bridgepoint companies.The strategy is a response to a tough mar-ket for successful exits and a recognitionthat truly successful companies are unlikelyto operate in only one country.Acquiring big players is the obvious route

to dominance, and a mixture of luck andjudgement has allowed Eurogestion topick off not one, but two domestic marketleaders over the past two years. As well asacquiring 40 Italian exterminating outlets(everything from rats to cockroaches),Debatte and his colleagues have alsosnapped up the pest control subsidiary ofGroupe Suez, giving the company a

THE POINT 9

Buy and build is an integral

part of the Bridgepoint

investment strategy

which aims to create value by

building market leaders. From

rat catchers to laboratories,

Catherine Wheatley

examines how the

strategy works

“Ultimately the strategy

is to increase the

multiple you can sell

the group for”

Eurogestion’s Pierre-Vincent Debatte: “Buy and build has changed the look of the entire company.”

FEATURE: BUY AND BUILD

Gunning for growth

FEATURE: BUY AND BUILD

dominant position in Belgium.Other companies are building in tinier

increments by picking off smaller rivalsand filling in gaps in an existing portfolio.

For example, British equipment hirecompany Longville Group, which suppliedmachinery for the construction of theMillennium Dome, has made five smallishacquisitions in the UK and America sinceSeptember 1999 when Bridgepoint backedan €128m management buy-in. The largestdeal, at just €13.2m, added Chicago-basedchiller-hire company Nu-Temp to a portfolioof businesses that lease equipment whichcan pump water, generate power andcontrol temperature.

Straightforward organic growth is alsopart of the package at many Bridgepointcompanies. Anglo-Dutch group AlcontrolLaboratories, which conducts safety testson a range of environmental samples fromfood to soil to drinking water, has recentlybuilt two new labs in the UK following a€112.7m MBO in December 2000.

Certain sectors lend themselves betterto a buy-and-build strategy. Functions thatbigger companies are outsourcing - laborato-ry testing or equipment hire - offer clearopportunities. At the beginning of the

year, for example, the Dutch governmentpassed a law allowing food producers tooutsource tests for BSE and other diseasesto private labs. And in the UK, water andpower utilities are being given greater free-dom to appoint outside contractors.

“There’s massive scope for developmentbecause outsourcing is becoming morecommon in the construction, petrochemicaland pharmaceutical industries where wework,” says Eric Hook, Longville’s chiefexecutive. “We can also add a huge amount ofvalue because we have specialist knowledge.”

Markets where new investors aredeterred by barriers to entry such as a highskills-base or a dominant position are alsopopular. Scandinavian car-parking businessNordisk Parkering, which Bridgepointacquired in a €107m secondary buy outlast June, is particularly strong in Swedenbecause of the country’s unusual propertyleasing regulations. Under Swedish law,

car-park tenants have the right to renew alease in perpetuity and the market rent isset not by the highest bidder but by anarbitration panel.

Nordisk Parkering already owns just lessthan half the market across the country – astake it has no intention of giving up. “It’sa very strong protection,” says chief execu-tive Mats Kullman. “Even if a competitoroffers a higher rent the landlord can’tthrow us out.”

Like other Bridgepoint-backed companies,Nordisk Parkering is picking up substantialcontracts for work that is being out-

10 THE POINT

“There's massive

scope for development

because outsourcing

is becoming more

common” Alcontrol's Gerard Baalhuis: “A more efficient, production driven approach.”

sourced. In Sweden more than 50 per centof the market for car-parking spaces andattendants is still controlled by the cityauthorities, but much of the work is beingcontracted out to private operators. As aconsequence, the company’s earnings rose25 per cent last year from turnover thatwas up around 15 per cent.

It is those types of mid-market companiesin which Bridgepoint specialises which areparticularly suited to the buy-and-buildapproach. Many underdeveloped GermanMittelstamp businesses, for example, havestrong growth prospects. Other sectors -particularly manufacturing -- are packedwith middle-ranking businesses that areripe for consolidation.

Before investing, Bridgepoint is clearabout the buy-and-build potential of acompany, and often the chosen strategy isone the management has been pursuingfor some time.

At Alcontrol, chief executive Gerard

Baalhuis had already purchased twoSwedish labs and a Dutch competitorbefore Bridgepoint invested and while thefirm was still owned by UK water companyKelda (formerly Yorkshire Water.)

“That was one of the reasons we wereinterested in Bridgepoint,” he explains.

The strategy devised by Baalhuis andBridgepoint is to take laboratories thathave traditionally been run by researchscientists and introduce a more efficient,production-driven approach.

Now, using special software, customerscan place an electronic order with a lab

while a courier is dispatched to pick up therelevant samples. The programme allowsclients to input all the data on the size andtype of sample directly into Alcontrol’sfiles so there are fewer copying errors.Information can be sifted and experimentsprepared before the material has evenreached Alcontrol’s premises. As a result,the average time to process a sample hasbeen cut from seven to three days.

“Exporting our know-how will be verybeneficial,” says Baalhuis, who has madethree further acquisitions since the MBO.“That’s how we increase value forBridgepoint and its shareholders – andthat’s why buy-and-build works for us.”

Transferring existing expertise to newlyacquired companies is part of the buy-and-build process, but sometimes buying inknowledge is just as important. In France,Eurogestion’s acquisition of Paris-basedSen Hygiene, which deals with commercialclients, added a new dimension to the

FEATURE: BUY AND BUILD

company’s predominantly residential pest-control services.Another purchase, of Lyon-based group ATB, brought with itnew capabilities in termite eradication.

Clearly, bringing a high degree of experience under onecorporate roof delivers distinct market advantages. Longville,the equipment hire company, is starting to take its specialistknowledge of draining water from construction sites tocountries where such skills are entirely absent.

“It’s not an easy activity for others to get into. Now, we havethe largest hire fleet of pumping equipment in the world andwe bring a huge amount of value added in terms ofapp l ica tion knowledge,” says Eric Hook.

Finding the right acquisition targets is one of the chiefchallenges facing many buy-and-build companies. Bridgepointitself has a substantial network of offices and many morecontacts through which it can source potential deals, but for themanagers involved, detailed market knowledge is animportant prerequisite.

Retiring owners of French and German family businesses areoften attracted by the promise of being part of a bigger firm intheir sector - especially if the company driving the buy-and-build strategy and its private equity backers have a good marketreputation. And managers in bigger businesses are often drawn

by the prospect of working within a reinvigorated group wheretheir experience can be vital.

Sometimes, however, suitable acquisitions are simply notavailable. “There are target companies but the list is limited andthere are high expectations on price,” admits Alcontrol’sBaalhuis, who is currently eyeing three businesses in the UKand the Netherlands.

Nordisk Parkering’s Kullman tells a similar story: “Theproblem is that there’s not that much to acquire.”

Bringing together different corporate and national culturescan be another challenge and one that is vital to grasp formanagement teams. In many cases, teaching subsidiarycompanies new skills or approaches will play a vital part inbuilding value. Alcontrol’s laboratory software and its efficientapproach to research are exported to all its new purchases,while Nordisk Parkering’s acquisitions use the parentcompany’s highly-developed financial and administra-tion system.

Most managers know well in advance what remedial actionwill be required at a newly acquired business. “It’s part of thedue diligence process to gather data so that we know whattraining is needed and what changes to employment packagesare required,” says Eurogestion’s Debatte.

At most of the companies involved it will be a couple of yearsbefore the strategy’s outcome can truly be measured. But onthe current evidence, company values are building nicely.

Catherine Wheatley is a freelance business journalist

Tony Le Saffre has plotted a course to substantial growthsince July 1999 when Bridgepoint backed his €37m managementbuy-out of French marine-equipment manufacturer Plastimo.

Over the past three years the company has acquired a broadspread of new businesses including UK life-jacket maker XMand French bow-thruster business Max Power in deals thathelped double turnover and boost group profits by 12 per centin the year to April 2001.

Plastimo’s aim is to build a pan-European brand that willbenefit from scale and distribution economies as well as name-recognition in a highly-fragmented market. Smaller companiesbrought under the Plastimo umbrella are now able to exporttheir goods to around 90 companies across the continentthrough a 50-strong sales team, and the brand name appears ona huge range of products from wet-weather gear to anchors.

“We want to builda logical patchworka l l o w i n g u s t oc a p ture as muchexposure in the shopsas possible. If youstart getting bigger,the synergies begintrickling in naturally,”managing director LeSaffre says.

The company,which manufacturesaround 6,500 lines, isalready the onlyinternational one ofits kind in Europeand Le Saffre believesPlastimo will betough to overtake.Over the next cou-ple of years he willfocus on stream-lining production,distribution and warehousing in a bid to increase his priceadvantage over competitors.

“We can offer discounts that others can’t but it’s a defensiveposition and we have to be careful of specialists,” he says.

Finding acquisition targets requires both smart thinking andsubstantial market knowledge, he admits. A number of targetshave been created and run by entrepreneurs who are close toretirement - including one recent acquisition in Denmarkwhere the proprietor was 76.

“We work in a very fragmented market so we have tried tothink strategically and identify product lines that have highpotential growth,” he explains. “Rather than expectingcompanies to knock on our door we draw up a shopping list,and generally the response has been good.”

One of the chief challenges Plastimo has faced is exportingthe corporate culture to new countries and companies. Thecompany already has subsidiaries in at least ten Europeannations as well as operations in the USA. “We have to learn tobe multi-cultural,” Le Saffre says. “We have to prove we aregood at taking care of cultures and languages and individuals.”

THE POINT 11

“There are target companies

but the list is limited and

there are high expectations

on price”

Making waves: yachting supremo Grant Daltonsports Plastimo gear

Plotting a course

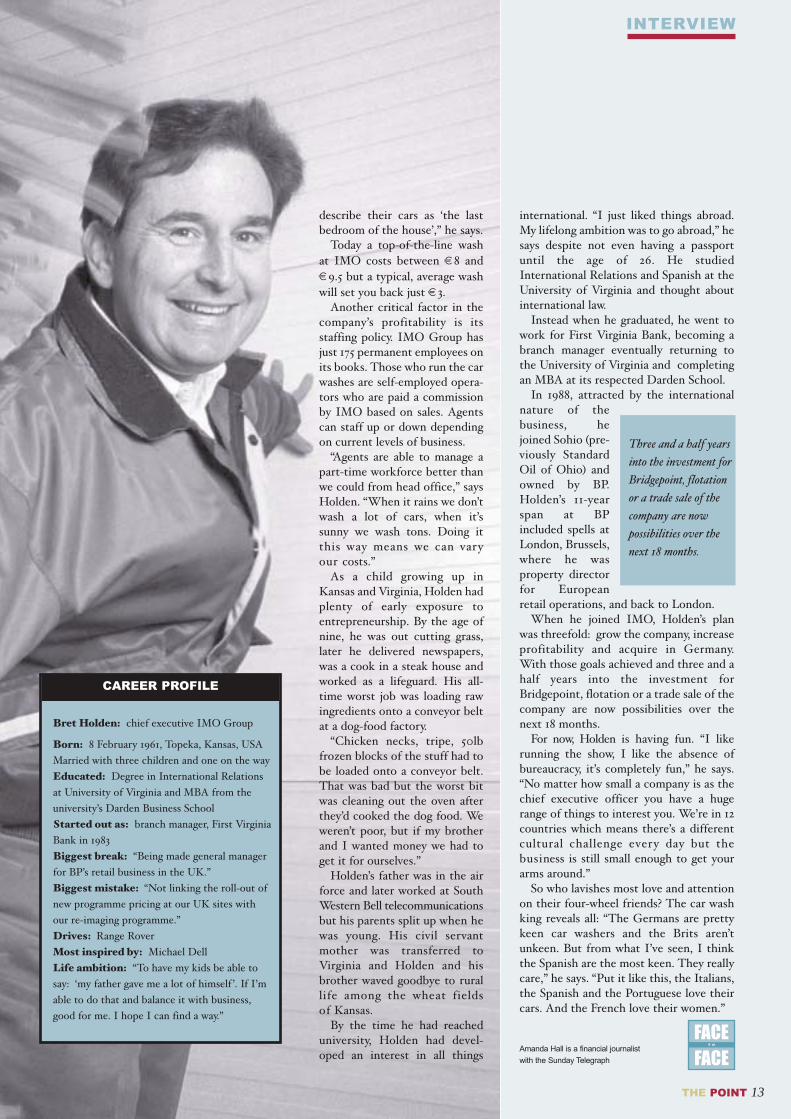

Between now and the end of thissentence, Bret Holden, a tall, dark,41-year-old American MBA, born inKansas and raised in Virginia, will havewashed five cars. That’s about one everysecond. Or, if you prefer, 30m cars acrossEurope in the space of a year.

Holden is Europe’s car wash king. Aschief executive of IMO Group, the world’sbiggest independent car wash businesswith a small headquarters in HighWycombe to the west of London, he is aman who prays for hot, dry summers andcold, frosty winters with plenty of grit onthe roads. He is also a man who sends hismanagement team off to wash cars to keepthem in touch.

“You really want to know what I firstthought when I was approached to runthis business?” he asks in an Americanaccent diluted by 11 years spent in Europe.“Why would I want to go run a crappy carwash company?”

That was back in 1999 when Holden wasworking for BP Amoco, the UK oil giantat its London headquarters where he wasresponsible for strategy and planning ofthe group’s downstream operations. As aformer general manager of BP’s retailoperations in the UK with a turnover ofaround €7bn and 5,000 employees, he washardly likely to leap at a head-hunter’soffer to go and run a car wash business.

“It was Mike Smith, a colleague at BPand now our chief operating officer atIMO who said: ‘Wait a minute, let’s put aplan together’,” Holden explains.

“We looked at the business, its meritsand what could go wrong and couldn’t findmuch. The internet couldn’t wash your carso we were safe from that; the companywas already the biggest in Europe eventhough they had never spent a penny onmarketing; there was a need in the market-place but very little competition; and it

had a low cost structure.“So we modelled a plan of the business

to see where it could go, stressed it from anumber of different angles and still wecouldn’t see how it couldn’t be a winner.”

Holden took the job, driven by a desireto do something new after those 11 years atBP, and to do it in an area he knew well.

And judging by the financialperformance of the business, it has proveda wise move for Holden, who holds a 4.5per cent stake in the company, and forshareholder Bridgepoint Capital whichowns the majority of the stock.

When the boy from BP joined thecompany in 1999, IMO had 412 sites inEurope and generated earnings beforeinterest, tax and depreciation of €21.6m.For the year to December 2001, earningsrose to €30.4m. In January this yearHolden acquired his German rival, TomanGroup for €130m, a deal that has takensite numbers up to 800. Toman waspreviously part of the IMO Group butwas split off in 1990 in its ownmanagement buyout.

How has Holden driven profitability atthe business? By restructuring washprogrammes to include more profitable‘extras’ and by refurbishing and rebrandingsites - some under the ARC name - tomake them more appealing, especially towomen concerned about safety.

“Extra options tend to be very profitablebut lots of sites weren’t selling all theoptions. So we bundled programmestogether. That workedbecause people liketo treat their carsreally well - in theUK, for instance, 30-40 per cent of cus-tomers always wantthe ‘top wash’ andin Germany they

12 THE POINT

Amanda Hall meets

Bret Holden,

the all American boy

who is cleaning up

in the European

car wash market

INTERVIEW

Awash with success

“I like running

the show, I like

the absence of

bureaucracy, it’s

completely fun”

“In Germany theydescribe their carsas ‘the last bedroom of thehouse’.”

FACEFACE

T O

describe their cars as ‘the lastbedroom of the house’,” he says.

Today a top-of-the-line washat IMO costs between €8 and€9.5 but a typical, average washwill set you back just €3.

Another critical factor in thecompany’s profitability is itsstaffing policy. IMO Group hasjust 175 permanent employees onits books. Those who run the carwashes are self-employed opera-tors who are paid a commissionby IMO based on sales. Agentscan staff up or down dependingon current levels of business.

“Agents are able to manage apart-time workforce better thanwe could from head office,” saysHolden. “When it rains we don’twash a lot of cars, when it’ssunny we wash tons. Doing itthis way means we can varyour costs.”

As a child growing up inKansas and Virginia, Holden hadplenty of early exposure toentrepreneurship. By the age ofnine, he was out cutting grass,later he delivered newspapers,was a cook in a steak house andworked as a lifeguard. His all-time worst job was loading rawingredients onto a conveyor beltat a dog-food factory.

“Chicken necks, tripe, 50lbfrozen blocks of the stuff had tobe loaded onto a conveyor belt.That was bad but the worst bitwas cleaning out the oven afterthey’d cooked the dog food. Weweren’t poor, but if my brotherand I wanted money we had toget it for ourselves.”

Holden’s father was in the airforce and later worked at SouthWestern Bell telecommunicationsbut his parents split up when hewas young. His civil servantmother was transferred toVirginia and Holden and hisbrother waved goodbye to rurallife among the wheat fieldsof Kansas.

By the time he had reacheduniversity, Holden had devel-oped an interest in all things

international. “I just liked things abroad.My lifelong ambition was to go abroad,” hesays despite not even having a passportuntil the age of 26. He studiedInternational Relations and Spanish at theUniversity of Virginia and thought aboutinternational law.

Instead when he graduated, he went towork for First Virginia Bank, becoming abranch manager eventually returning tothe University of Virginia and completingan MBA at its respected Darden School.

In 1988, attracted by the internationalnature of thebusiness, hejoined Sohio (pre-viously StandardOil of Ohio) andowned by BP.Holden’s 11-yearspan at BPincluded spells atLondon, Brussels,where he wasproperty directorfor Europeanretail operations, and back to London.

When he joined IMO, Holden’s planwas threefold: grow the company, increaseprofitability and acquire in Germany.With those goals achieved and three and ahalf years into the investment forBridgepoint, flotation or a trade sale of thecompany are now possibilities over thenext 18 months.

For now, Holden is having fun. “I likerunning the show, I like the absence ofbureaucracy, it’s completely fun,” he says.“No matter how small a company is as thechief executive officer you have a hugerange of things to interest you. We’re in 12countries which means there’s a differentcultural challenge every day but thebusiness is still small enough to get yourarms around.”

So who lavishes most love and attentionon their four-wheel friends? The car washking reveals all: “The Germans are prettykeen car washers and the Brits aren’tunkeen. But from what I’ve seen, I thinkthe Spanish are the most keen. They reallycare,” he says. “Put it like this, the Italians,the Spanish and the Portuguese love theircars. And the French love their women.”

Amanda Hall is a financial journalist

with the Sunday Telegraph

THE POINT 13

INTERVIEW

Three and a half yearsinto the investment forBridgepoint, flotationor a trade sale of thecompany are now possibilities over thenext 18 months.

CAREER PROFILE

Bret Holden: chief executive IMO Group

Born: 8 February 1961, Topeka, Kansas, USAMarried with three children and one on the wayEducated: Degree in International Relationsat University of Virginia and MBA from the university’s Darden Business SchoolStarted out as: branch manager, First VirginiaBank in 1983Biggest break: “Being made general managerfor BP’s retail business in the UK.”Biggest mistake: “Not linking the roll-out ofnew programme pricing at our UK sites withour re-imaging programme.”Drives: Range RoverMost inspired by: Michael DellLife ambition: “To have my kids be able tosay: ‘my father gave me a lot of himself ’. If I’mable to do that and balance it with business,good for me. I hope I can find a way.”

FACEFACE

T O

In the first months of 2002 it is onceagain steady-as-she-goes for Germany’sprivate equity market. The incoming taxreforms have not triggered a flurry ofdeals. The mass restructuring of Germany’scross-holdings has, as expected, nothappened overnight. The deals are notfalling from the trees into the laps of thebuyout houses.

Few private equity managers were pre-dicting a storm of deals on the back of thenew tax changes that came into effect atthe start of the year. The reforms targetedthe banks and large corporates and weredesigned to allow the unravelling of cross-holdings in a zero-rated capital gains taxenvironment.

They heralded a move to a more AngloSaxon style of capitalism away from theprotectionism of fortress Europe. It wouldforce corporates to focus on the creationof shareholder value through the sale ofminority interests in other companies.

When the tax changes were firstannounced, the share prices of the banksand corporates with assets to offloadsoared and many thought this would bethe key to unlock the world’s third-largest economy.

Initially the assumption was that itwould provide rich pickings for the privateequity community. It still may. But firstthere needs to be a systematic consolida-tion of the minority industrial holdings.Banks like Dresdner are quietly offloadingtheir industrial portfolios, bolstering2001’s miserable results. The private equityteams can then move to dismantle thecorporates. It is, however, still some way off.

Wolfgang Lenoir, responsible forBridgepoint’s German operations, based inFrankfurt says:

“I think the quiet start is due to a num-ber of things, something to do with the taxreform, something to do with September11 and the Mittelstand’s reluctance to sell inthe new price environment.”

According to the German VentureCapital Association (BVK), the German

private equity industry invested €4.4bnlast year. However once new members ofthe industry association were stripped outthe numbers fell back to pre-bubble1999 levels.

Holger Frommann, managing director ofthe BVK, says the like-for-like number iscloser to €3.1bn. The deals have fallenback across all stages, though buyouts roseas a proportion of the total.

Part of the problem continues to be therebasing of vendor expectations - explainingto sellers that the gravy train of ever-risingstock markets has left the station. A neweconomic environment is here to stay and,

for private equity to make a return, so arethe new prices. Germany’s Mittelstand,however, has shaken its head and retired tothe golf course.

As one consultant says: “Mittelstandfamily firms are very hierarchical andparochial. There are probably some750,000 Mittelstand companies. A tenth,or 75,000, of them are said to be facingsevere succession problems. The childrendo not want anything to do with the par-ents’ business and the incumbent has aningrained distrust of outsiders and cannotgrasp why his business is worth less nowthan twelve months ago. You cannot win.”

Some private equity firms have all butturned their back on the 75,000-strongopportunity among the Mittelstand firms.The 6,000 or so corporate orphans thatpeople the business landscape are unloved

by their corporate parents. Others havealtogether turned their back on Germanyfor the time being. Lenoir explains:“People are being more realistic and the hypeabout the anticipated market has calmed.”

According to Alfred Herda, partner atlaw firm Clifford Chance Puender, youwould need a crystal ball to divine the truecauses behind the private equity market’slack of dramatic growth.

He even points to the tax reforms as apossible inhibition. Vendors are not con-vinced that the regime will hold good oncethe new government takes control afterelections later this year.

So far the realwinners, thebusiest players inGermany’s privateequity market forseveral years - andthe start to 2002has been noexception - are theheadhunters andrecruitment spe-cialists. The passingenthusiasms of thebanks’ captivefunds - and thecompetitive envi-ronment - haveensured fluidity tothe country’s pri-vate equity jobmarket. For everyr e t r e n c h m e n tback to London, anew office hasopened. It is a

mark of the market’s immaturity.Deal flow may be slow but for the com-

mitted there is still a strong, if fiercelycontested pipeline. Lenoir says: “In themiddle market, depending how you defineit, there are 20 deals per annum, maybe asmany as 40.”

Despite the competition, Lenoir isnevertheless optimistic about the potentialof rich pickings by the second half of theyear. Herda cautions that in Germanyhopes have too often been taken forexpectations. “The market is picking up,but not as fast as was hoped. It could dobetter, but that is always the case inGermany,” he says.

Like a clever but recalcitrant schoolboy,Germany has yet to fulfil its early promise.Another term beckons. Must try harder.Nick Lockley is Frankfurt correspondent for Financial News

THE POINT 15

Restructuring of Germany’s

cross-holdings has not ignited

the anticipated explosion in

deals for the buy out houses.

But there are signs that the

market is beginning to move

Nick Lockley reports

VIEW

Market VIEWGermany

“To describe the European healthcare industry is to sketch theoutline of a near-perfect investment opportunity.

It is an enormous, diverse and growing market. It is subject toconstant technological change that necessitates heavy newinvestment. The bulk of the cost falls to government which mustgive the highest priority to health spending as a condition ofpolitical survival. And the need for structural reform andfor cost containment ensures plenty of new opportunities forentrepreneurial private firms.

The demand for healthcare services is literally inexhaustible.Sickness will always be with us. And the advance of medicalscience is steadily extending the list of treatable conditionsand diseases.

The economic soil is so fertile that Justin Jewitt, chief executiveof Nestor Healthcare, the UK’s largest independent providerof nurses and other medical personnel, can afford towelcome competition.

“It’s such a big market,” he says. “We need more people in it todevelop it with good ideas, good innovations and good services tomake people feel comfortable (with private provision). Otherwise,when people think independent healthcare, they think BUPA.”

In stock market terms, by far the largest private sectorbusinesses involved in healthcare provision are the pharmaceuti-cal companies. A strong tradition in medical science, particularlyin Britain, Germany and Switzerland, has given rise to Europeangiants such as Aventis, AstraZenecea, GlaxoSmithKline,Novartis and Roche.

However, from a private equity perspective, the scale and costof modern pharmaceutical development is too great to offer muchin the way of useful investment opportunities. It is estimated thatit can cost in excess of €600m to bring a successful drug tomarket these days.

Backing a biotechnology start-up might be more manageablefinancially but such investments are extremely high-risk and arebest left to specialists.

Rob Moores, head of healthcare investments at BridgepointCapital, says: “If it is at an early stage, it does not fit ourinvestment criteria. What we are looking for is an establishedbusiness with a profit stream and cash flow.”

Fortunately, there is a multitude of opportunities outside drugdevelopment. Expenditure on drugs accounts for only a smallproportion of healthcare budgets. The bulk of the money is spenton caring for patients and providing the back up services thatallow doctors and nurses to perform their duties effectively. In theUK, for example, two-thirds of the €108bn spent on healthcare in2000 went on pay.

Nestor is a good example of a substantial public company thathas grown strongly through helping the NHS to meet its person-nel requirements. The company, which owns the long-establishedBNA nursing agency, recently reported a 39 per cent improvementin operating profits to €41.2m on the back of a 37 per centincrease in sales.

Nestor’s growth is being supported bylast year’s acquisition of Healthcall, acompany it bought from Bridgepoint.Healthcall, a public company untilBridgepoint took it private in a €105mdeal in February 1998, provides out-of-hours cover for general practitioners.Jewitt says Healthcall provides cover formore than a quarter of Britain’s 38,000GPs, dealing with more than 6 millioncalls a year.

Another big market exists in supplyingmedical equipment and devices.

Development timetables are muchshorter than in the pharmaceuticalindustry, helping to make this sector moresuitable for private equity investment.

Again, Bridgepoint’s portfolio providesan example in the form of AllianceMedical, a company that supplies hospitals

16 THE POINT

Enormous, diverse and growing - the

European healthcare market with its

need for reform and cost containment

ensures plenty of new markets for

entrepreneurial private firms

Paul Durman examines the best

investment opportunities

Testing times in the National Health Service: Laboratories are

FEATURE

Se

cto

r w

atc

h HealthCare

with imaging equipment and the staff tooperate it.

A good example of a company thatcombines both medical equipment andmedical services is Fresenius Medical Care,a German quoted business that is theworld leader in kidney care. The companymakes dialysis machines and related prod-ucts and, through its international networkof 1,375 clinics, provides treatment to morethan 100,000 patients with chronic kidneyfailure. As an acquisitive company, Freseniuscould also provide a potential exit forprivate equity investments in its sector.

In future, healthcare companies are likelyto become increasingly specialised, focusingon a single area of disease. An emphasis ondiagnostic related groups, as they arecalled, is now driving the development ofthe German healthcare system. This pro-vides opportunities for companies such asRhoen-Klinikum, the German hospitalsgroup that is spearheading an increasedreliance on the private sector.

Paul Saper, director at LCSInternational, a firm of healthcareconsultants, says there are also openingsfor venture capital in less wealthyEuropean countries, such as Poland.

“Companies are trying to look aftertheir staff, to help them attract the rightcalibre of people. The quality of care is sobad (in Poland) that there’s a market forprivate sector providers.”

Richard Steeves could be forgiven forwalking with a spring in his step. Afteryears of struggling under the weight of toomuch debt, Synergy Healthcare - a businesshe has run for the past ten years - is finallystarting to move more freely.

After raising over €12m from a flotationon the Alternative Investment Market lastyear, Steeves has the resources to expandSynergy more rapidly. The company is aclassic outsourcing play, taking care ofhospitals’ laundry and sterilising surgicalinstruments.

Since flotation, Synergy has picked upover €30m of contracts. It has recruited asales and marketing team and, most impor-tantly of all, it has pulled off its biggestacquisition, buying Hays Clinical Servicesthis spring for over €19m.

The business, part of the Hays BusinessServices group, is Synergy’s largest com-petitor in the field of sterile services,managing the supply of instruments forseven NHS trusts. The deal means that 60per cent of Synergy’s business now comesfrom its more profitable sterile servicesoperation. Pre-deal the mix was 70:30 infavour of laundry.

Synergy - which is not a Bridgepointinvestment - is a microcosm of thehistory of outsourcing in the NHS and aclassic example of entrepreneurship in thehealthcare market. Its origins lie in a firmcalled Sterile Theatre Services, which inthe late 1980s tried to build a businesssupplying operating theatres with surgicalgowns and drapes. The Aids scare hadheightened concerns about the risks ofcross-infection during surgery.

Steeves says: “It was a good idea but theNHS was not ready for it.” The companystruggled and collapsed into receivershipin 1991.

The business was rescued by AndrewFitton, who had been running Braithwaite,a pump hire business that has since becomeAndrews Sykes. Steeves started out as aconsultant with LEK Consulting, workedwith Fitton as Braithwaite’s corporatedevelopment manager and was made chiefexecutive of Synergy in 1992 when he wasstill only 30.

Initially, Steeves concentrated on pro-moting the use of “barrier” gowns anddrapes - those made of a breathable butliquid-proof fabric that offers significantadvantages over the traditional cotton. Buthe soon realised this was only part ofa bigger opportunity.

He says: “In 1994 and 1995, we tooka decision to concentrate on providing a

THE POINT 17

a prime example of the need for consolidation

FEATURE

growing num-ber of servicesto the NHS.TheGovernmentwas encourag-ing hospitals too u t s o u r c en o n - c l i n i c a la c t i v i t i e s .That expandedthe number ofmarkets withinthe NHS thatwe could oper-ate in.”

The key movescame in 1996when Synergybought the area laundry from the DerbyHealth Authority. At the same time, SouthDerbyshire Acute Hospitals NHS Trust haddecided to seek a private company to takeover the running of the sterile services unitat the Derby Royal Infirmary andappointed Synergy.

The business installed a new but signifi-cantly smaller clean room and today suppliesthe trust’s 15 operating theatres with about30,000 instruments a year. It has alsointroduced bar-code tracking software toallow it to trace the usage of an individualinstrument and improve service quality.

The linen services side of the businesswas expanded and renamed after the acqui-sition of Healthtex in 1999 and the firm isalso moving into disposing of clinical wasteafter buying another small business fromthe receivers at the end of 2000.

Steeves says: “We go to 130 hospitalsevery day now. We have the ability to offerother services to that network.”

He says the common theme is thatSynergy’s activities are aimed at minimisingthe risk of hospital-acquired infection. AHouse of Commons report two years agofound that nine per cent of patients pick upan infection while in hospital. Steeves says15-20 per cent of these - or up to 20,000 ayear - could be avoided simply by adheringto existing best practice.

He adds that the study found as many asa third of NHS sterile units failed to meetacceptable standards. This has promptedthe Government to commit £200m totackle the problem.

The company is rapidly emerging as aleader in a market that is still immature.Synergy and other private sector companiesmanage only three per cent of the 320sterile services departments within theNHS. The outsourcing of laundry is moreadvanced but there are still about 40NHS laundries.

This is a niche market but one thatoffers good opportunities to a specialistsuch as Synergy. “We are completely andutterly focused on the health service,”says Steeves.

Synergy Healthcare

Synergy's story is aclassic example ofentrepreneurship in thehealthcare market

HealthCare

At the same time helping health servicesmeet their staffing requirements lookslikely to remain a strong business for yearsto come. More doctors, nurses and othercarers will be needed to keep with anageing and ailing population.

Richard Jarvis, an analyst with NomuraInternational, says: “The baby boomers arehitting 60 and getting all the problems ofelderly patients, such as prostate cancer.The growing prosperity of Europe as awhole is driving the expectations ofindividuals as patients. People are notprepared to put up with their symptoms orlong stays in hospital.”

Wealthier, better-educated and better-informed patients will not be prepared towait around for treatment. Increasingly,patients will want to be treated in thehome or at their local surgery or clinic.Governments will seek to encourage thistrend to avoid the “hotel costs” of keepingpatients in hospital.

These changing demands will test allEurope’s health systems, not least inattracting staff. In the UK this plays intothe hands of the likes of Nestor and BNA,adept at filling gaps in the NHS staffingroster from the ranks of nurses on itsbooks who are only able to work a fewextra hours each week.

Bridgepoint is also involved in thissector through its investment in MatchGroup, the agency nursing business thatused to form the core of SinclairMontrose, the listed healthcare companytaken private in 1999.

Match is close to becoming a €320m ayear business, and is the clear number twoin the market behind BNA. Moores sayshe hopes Match will be ready to return tothe stock market by the end of next year.

The NHS is trying to curtail its spendingon agency nurses by establishing its owninternal flexible staffing service. However,Jewitt believes NHS Professionals willinevitably be hampered by the salary,overtime and pension costs of full-timeemployees.

“They’re beginning to understand someof the logistical issues they’ve got,” he says.“They’re gaining a greater appreciation ofthe need for outsourcing rather than theneed to maintain it themselves.”

The growth of outsourcing of non-clinicaloperations should provide a rich opportu-nity for private equity investors. SynergyHealthcare is taking advantage of thesteady realisation by hospitals that they nolonger need to run their own laundry services.(See panel p17). It is also taking over the

running of the sterile services units thatclean and supply the instruments andlinen used in operating theatres. AndBridgepoint’s own portfolio provides anexample in the form of Alliance Medical,a company that supplies hospitals withimaging equipment and the staff tooperate it.

Moores believes pathology laboratories,which analyse blood and urine samples, areanother area crying out for consolidation.He says: “Every big hospital has its ownpath lab which is sub-optimal in termsof value for money. I suspect standardsvary enormously between good labs andbad labs.

“There’s no reason on earth why thatcould not be outsourced. The economiesof scale must be enormous.”

Saper says that the Europe-wide rise in

healthcare spending is being driven by therising cost of drugs and by advances inmedical devices. One example of the latteris the growth in the use of stents, theminiature metal scaffolds that are usedto support and hold open damagedblood vessels.

The introduction of stents, which areinserted with the aid of a catheter, hasgreatly reduced the need for open-heartsurgery. The next advance will be thearrival of so-called drug delivery stents,which are coated with a drug to counterrestenosis, the narrowing of the artery thatsometimes occurs in response to the presenceof the stent. The drug delivery stent

market is forecast to be worth nearly €5bnby 2005.

Keyhole surgery is another potentiallypromising area. Less traumatic surgerydramatically reduces the amount of timepatients need to spend in hospital, whichhas the welcome benefit of significantlycutting the cost of an operation. Therecould be opportunities here for privateequity firms, such as in backing firmsdeveloping the tools needed to carry outminimally invasive surgery.

Saper says another big opportunity liesin introducing information technology tothe provision of healthcare. For instancein the UK, only 1.5 per cent of healthspending is on IT, compared to 6 per centin the US.

Moreover, health spending on IT massivelytrails IT spending in other government

departments and in other areas of theeconomy.

Working with a health service as acustomer is not without its challenges andfrustrations. Purchasing decisions areoften slow to arrive, subject to politicalinfluence and driven by criteria that are notalways obvious to private sector managers.Healthcare firms need to stay nimble toensure they are not inadvertently trampledunderfoot because of sudden changes ofpolicy by the healthcare elephants. Asever, good management remains the key toa successful investment.Paul Durman is a business reporter for the Sunday Times

18 THE POINT

Cash injection: Analysts are identifying opportunities to back firms developing next generation tools

FEATURE

20 THE POINT

MAKING THE MOST

Smart MoneyHigh net-worth?Richard Rivlin looks at how best tohandle your money

Doing it Thoughts from the top

When Jim Clark, the Silicon Valley billionaire and Netscape founderrealised he was employing a full-time staff of advisors just to manage hismoney, he knew there had to be a better way to do things.

True to his entrepreneurial routes, Clark set up myCFO, an on-linewealth advisory business whose board and customers include some of thebiggest and wealthiest names in business, John Doerr of Kleiner Perkins,John Chambers of Cisco and Jim Barksdale former chief executive atNetscape all bank at myCFO and sit on its board.

Sadly for Europe’s growing community of high net-worth individuals,myCFO has yet to expand outside the US. But Clark’s original frustrationat managing his finances is certainly not a US phenomenon. Unless you doit right, managing the money you have made can become a costly andtime-consuming business. So how do you avoid it?

Historically in Europe, individuals used private banks, stockbrokers andinvestment advisers. Today a new breed of wealth managers inside a rangeof financial institutions - high street banks like Abbey National, globalbanks like UBS, specialist private banks like C Hoare & Co - offer all ofthese services.

Coutts, (perhaps the most famous name in private banking), segmentsits clients into nine different groups. Tim Pethybridge, who runs thedivision representing senior executives, believes the onus is on deliveringproducts and services that work for people receiving ever more complexremuneration packages including bonuses, share option schemes and carryarrangements for private equity executives.

The Coutts’ offer is effectively a personal bank manager with whomcustomers can have as deep or shallow a relationship as they wish. As wellas traditional retail banking services, its products include access to privateequity and hedge fund products.

Says Pethybridge: “We are the UK’s largest hedge fund provider withmore than £3bn of our clients’ assets in hedge funds.” He also recommendsthat up to 20 per cent of a client’s assets should be in alternative assets.

“Life is about understandingyourself and making a few good friends and maybe, if you’re lucky, grabbing that Arcamedian lever and changing the world just a bit.”

Larry Ellison,

founder Oracle Corporation

“I ask everyone to wake up terrified every morning, theirsheets drenched in sweat.Because we should be afraid ofour competitors, we should beafraid of our customers. I wakeup every morning thinkingabout how we can keepimproving the customer experience and that’s fun.”

Jeff Bezoz,founder Amazon

“Never forgetting it’s allabout our customers. Our approach has to be innovative and personal.Customer service has to be our competitive advantage. We have to talkplainly and personally toour customers - no excuses or arguments.”

Marjorie Scardino, chief executive Pearson

“Go to a beach and sit there forthree whole weeks? Only themost secure can do that. I lasthalf an hour. I wanna go hit agolf ball and see what my scoreis, I wanna go play a hockeygame and try score a goal. I’minsecure, I’m insecure. I’vegotta prove to me I just didokay, that I haven’t lost it.”

Scott McNealy, co-founder Sun Microsystems

“Many people dream ofsuccess. To me success canonly be achieved through repeated failure and introspection. In fact, success represents one per cent of your work which results from the 99 per cent that is called failure.”

Soichiro Honda, founder Honda Corporation

“There are those who are interested in investing and others who wantto hold on to what they have. We try and understand their personalwishes and then make judgements together on what are the best productsfor them,” he explains.

Alexander Hoare, chief executive of C Hoare & Co, one of Europe’soldest private banks, predicts that over the coming years the demand formore and more specialist information on individual products is likely todrive the banks into building closer relationships with a smaller number ofproduct providers like hedge fund or tax planning specialists.

Hoare says: “Our ten thousand clientswant us to remain small and not be offer-ing just our own brand products. We alignourselves with the clients and externalexpertise to get the best products for them.”

This proprietary approach contrastswith Coutts’ service and is based upona be l i e f that the bes t productschange constantly and are produced byspecialist providers.

But if all that sounds too much like hardwork, you might prefer to consider a ‘one-size-fits-all’ approach of the wealthmanagement divisions of the global banksoffering their own brand products. UBSWarburg, Dresdner Private Bank andInvestec each gives details on its website of

discretionary services and investment funds. As one offshore tax exile explains: “The best do not have one single

advisor. They pick and choose from different fields. I might use one bankfor my accounts and another for their alternative assets but I doubt if anysignificant private investors would rely on just one relationship.”

Further details are available from the following websites:

www.barclaysprivatebanking.co.uk www.hoaresbank.co.ukwww.coutts.com www.investecprivatebank.co.ukwww.dresdnerprivatebanking.co.uk www.mycfo.com

“Our clients want us toremain small and not beoffering just our ownbrand products. We align ourselves withthem, and with externalexpertise to get the bestproducts.”

Alexander Hoare, chief executive C Hoare & Co

THE POINT guide

€SM

Health & fitness

High achiever’s diet

by Amanda Hall HF

THE POINT 21

MAKING THE MOST

Top Table MadridLuke Johnson gets a taste of Barcelona - in Madrid

La Fonda, Lascarga 11, Salamanca, 28001 Madrid, Spain

Why recommend a Catalanrestaurant in the middle of aCastilian city? Because the cuisine of Barcelona

is very good, and they do it wellat La Fonda. The restaurant islocated in the newer part ofSpain’s capital city, to thenorth-east of the centre, in abarrio called Salamanca. It’s anelegant district organised into agrid system of streets, and full ofsmart designer shops plus the oddposh place to eat or drink.

La Fonda has an understatedentrance and a cosy feel, with thewood-fired oven and grill of the kitchen in full view as you enter. Ourhotel had cocked-up the booking, but the greeter sorted out the upsetwithout a murmur.

Service throughout our meal was excellent. Staff speak English butwill try their best with your Spanish if you prefer. Most of the customersseemed to be locals, with a smattering of tourists. The atmosphere isfriendly but not too boisterous or noisy, since the restaurant is dividedinto sections of a few tables each.

Our dishes were almost all first-class. I ate escalivada, a classic starterof roasted peppers, onions and aubergines; my companion had adelicious warm spinach salad with pine nuts, ham and raisins. For maincourses we had salt-grilled veal and roasted cod with white beans. Bothwere cooked to perfection and beautifully served. We drank anexcellent house Rioja and several bottles of the very salty CatalanVichy mineral water.

The only disappointment was the crema Catalana for pudding. It wastoo runny; the fruit salad was, however, delicious. The bill for the entireaffair came to around €75 (about £25 each). By London standards it wastremendous value for a classy meal - by Madrid standards I suspect it wasexpensive but not outrageous.

The toilets were remarkable for their complimentary combs andtoothbrushes. Clearly, La Fonda’s customers like to be well groomed.

La Fonda operates such a short trading session that I rather wonderedif it makes money: it serves dinner from 9:30pm to midnight, with theusual mad lunch session from 1.30 to 4pm. Of course Madrileños eat late,so the place is quiet until an hour before closing in the evening. I suggestyou book since they only have one sitting.

When in Salamanca, be sure to visit a disused theatre nearby, calledTeatriz, at 15, Calle de Hermosilla. The renovation into a restaurant, barand discotheque was supervised by designer Phillipe Stark some yearsago, and the result is stunning. There is a handsome bar in the old foyer,or a fine marble bar on the stage itself. There are even private diningrooms in the stalls. It caters to an upmarket crowd of good-lookingthirty-somethings. I suggest you dine at La Fonda and stroll up the roadto Teatriz for a nightcap - but don’t bother going before midnight.

Luke Johnson is Chairman of Signature Restaurants

Heard of FBS? It is a syndrome prevalent amongst high achievingbusiness types. What is FBS all about? In a word, fat. In three,Fat B**t**d Syndrome.

And Dr Adam Carey has encountered more FBS than most. Carey runsthe Centre for Nutritional medicine, a private business in London’sHarley Street that specialises in helping high achievers eatfor performance.

“If you plot a businessman’s age against his weight on a chart,on average you’ll see he will put on about a stone every ten years,” saysCarey who also works with England’s rugby union squad andstars like Angelina Jolie.

“With that weight gain, they notice impaired performance, theystruggle to get through meetings and late nights, everything is harderthan it used to be. Few will admit it but they also suffer sexually. Mostguys have put their lives into business, sacrificing family, lifestyle anddiet - they are making buckets of money but end up miserable.”

The principle underlying Carey’s advice is that of body compositionand its impact on physical and mentalperformance.

“We focus on bringing people intoa normal body fat range which isbetween 15 and 20 per cent of bodymass. But because most see them-selves as above average, once they getthere, they’ll often set themselveshigher goals and aim to get body fatdown to an athletic 10 to 15 per cent,”he says.

How does Carey and his team bringabout what can be a staggering trans-formation? British serial entrepreneurDavid Steene reduced his weight by almost eight stone in a year.