Embed Size (px)

Citation preview

The perilous journey to Perils Pricing

Thoughts and considerations

© Justin Ho, Insurance Australia Group

This presentation has been prepared for the Actuaries

Institute 2015 General Insurance Half Day Seminar.

The Institute Council wishes it to be understood that

opinions put forward herein are not necessarily those of the

Institute and the Council is not responsible for those

opinions.

Know your perils?

So what perils should we worry about? • Flood • Bushfire

• Earthquake • Storm • Hail • Cyclone/Hurricane/Typhoon

• Storm surge • Tsunami • Landslip/landslides • Volcano • Drought

• Meteor shower? • Solar storms?

Know your perils? (2) Answer: It depends on which geographical region, class of business, layer of CAT RI program

For motor: hail

For home: region specific

• VIC: bushfires/floods

• Nth QLD/WA: cyclone

• NSW: -top layers: earthquake

-lower layers: storms

• SE Asia: Floods, earthquakes

For Commercial Lines:

• Business interruption

Source: 2014 ICA Disaster database revalued

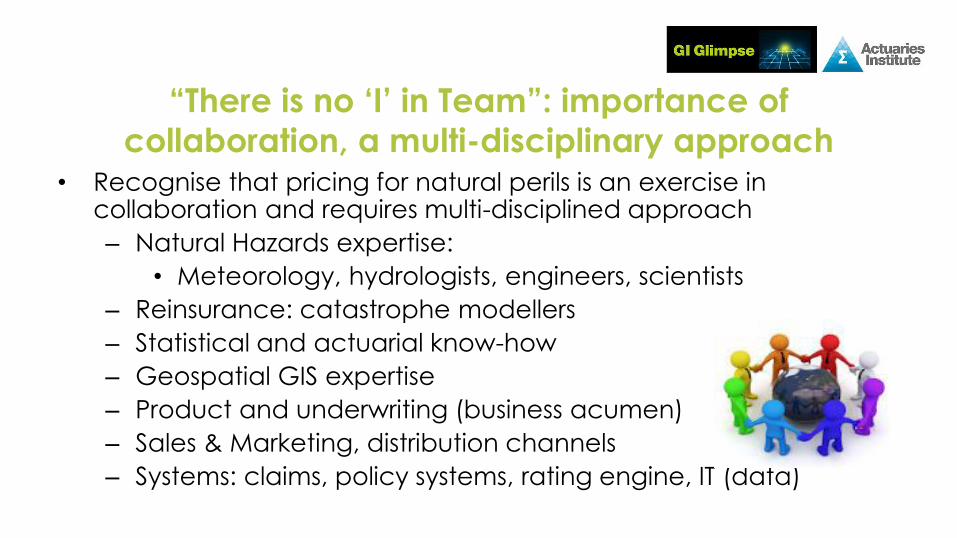

“There is no ‘I’ in Team”: importance of

collaboration, a multi-disciplinary approach • Recognise that pricing for natural perils is an exercise in

collaboration and requires multi-disciplined approach

– Natural Hazards expertise:

• Meteorology, hydrologists, engineers, scientists

– Reinsurance: catastrophe modellers

– Statistical and actuarial know-how

– Geospatial GIS expertise

– Product and underwriting (business acumen)

– Sales & Marketing, distribution channels

– Systems: claims, policy systems, rating engine, IT (data)

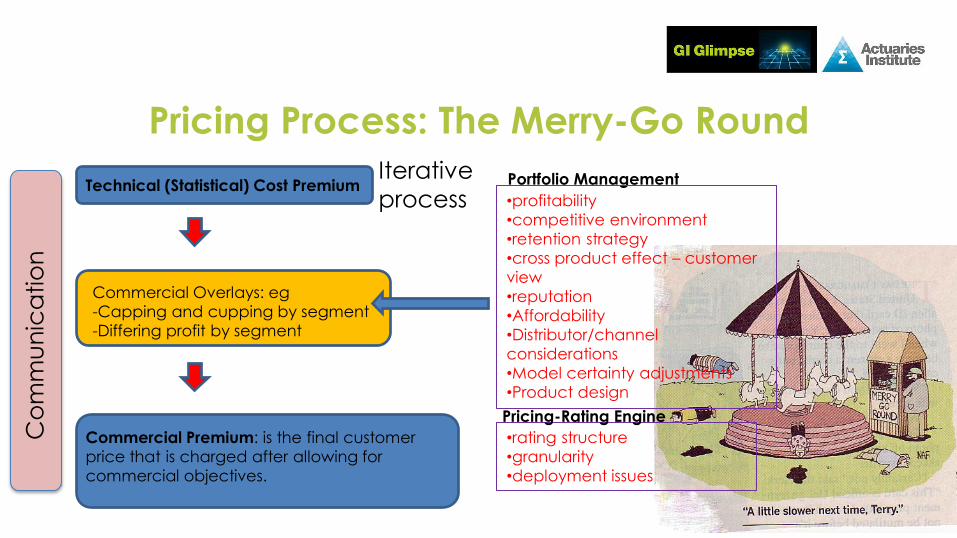

Pricing Process: The Merry-Go Round

Technical (Statistical) Cost Premium

Commercial Overlays: eg

-Capping and cupping by segment

-Differing profit by segment

Commercial Premium: is the final customer

price that is charged after allowing for

commercial objectives.

Portfolio Management

•profitability

•competitive environment

•retention strategy

•cross product effect – customer

view

•reputation

•Affordability

•Distributor/channel

considerations

•Model certainty adjustments

•Product design

•rating structure

•granularity

•deployment issues

Pricing-Rating Engine

Iterative

process

Co

mm

un

ica

tio

n

“Feeding” the model: data

• How good are your data inputs?

– Exposure

• Sum Insured (replacement value?)

– Asset details:

• Risk location and addressing information

• Year of construction. Missing values? Any defaults?

• Construction type

• Other rating factors: occupancy type, roof type, dwelling type etc ->vulnerability

– Policy Details:

• Excess, deductibles, limits,

– External factors:

• Hazard Information: Topography/terrrain, meteorological, seismicity, vegetation

Never enough data but make do with what you can get

Building Attributes: Importance of Building Location

•Flood risk

assessment

resulting in

$100’s to

$1000’s

difference

•Bushfire:

similar

effect

Data: Elevation • Garbage-In Garbage

Out

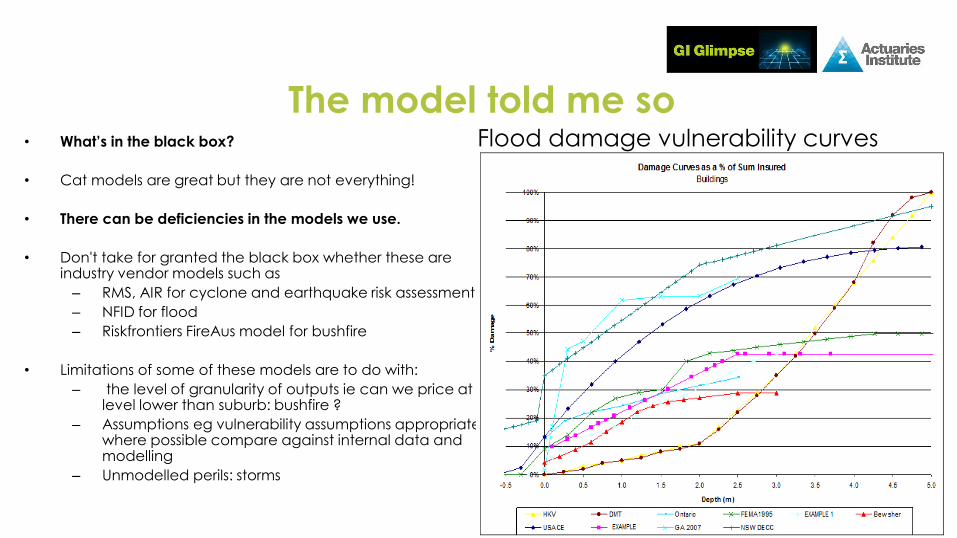

The model told me so • What’s in the black box?

• Cat models are great but they are not everything!

• There can be deficiencies in the models we use.

• Don't take for granted the black box whether these are industry vendor models such as

– RMS, AIR for cyclone and earthquake risk assessment

– NFID for flood

– Riskfrontiers FireAus model for bushfire

• Limitations of some of these models are to do with:

– the level of granularity of outputs ie can we price at level lower than suburb: bushfire ?

– Assumptions eg vulnerability assumptions appropriate. where possible compare against internal data and modelling

– Unmodelled perils: storms

Flood damage vulnerability curves

Earthquake Example

Larger than 6

5 ~ 6

4 ~ 5

Less than 4

Magnitude

Larger than 6

5 ~ 6

4 ~ 5

Less than 4

Magnitude

Circa 1800~ 03 Sept. 2010 03 Sept. 2010 ~ 22 Feb. 2011

Sept. EQ

Feb. EQ Jun. EQ

Greendale Fault

(Seismic Information obtained from GeoNet, GNS, NZ)

Pricing Issues: “we all have issues” • Moving away from community rated to granular risk differentiation

• However this results in affordability issues as removing or reducing the implicit cross subsidies.

• The big conundrum what to do about these large premium changes. – Flood / ceiling / capping strategy of premium amount – Renewal book strategy: caps on premium change, % or $ change – Customer referral process

• Do we take long term or short term view of reinsurance costs. Pricing Vs Reinsurers’ view of risk.

• Cost plus Vs Demand/Supply pricing. Component based basis?

• Dealing with asset location and building attributes

• Optional Vs Mandatory cover

• Dealing with uncertainty: to discount or load? Community rating?

• Competing objectives in the price settling process? -> Commercialised prices may not reflect technical view of risk!

Pricing Considerations: Reputational Risks

Rating Engine: “Breathe deeply”

• Area granularity does your rating engine allow for address level pricing?

• Peril specific pricing: components based pricing, ie each peril is identified or is it some get big mixing

pot..no one know’s how much is allowed for in the commercialised premium for perils and reinsurance

on a per policy level or even portfolio level basis.

• If some of your perils embedded in the base coverage premium then how does this interact with non

perils or discount structures?

• Lack of transparency of the breakdown of perils in commercialised premium introduce cross subsidies or

impossible to perform attribution of the pricing adequacy of the portfolio. Difficulties in backing out old

pricing if wrapped in other factors

• Multiplicative or additive rating structure. Issue of non peril rating factors such as base rate changes or

other factors impacting on the peril component of the premium result in over or under collection of the

peril component of the premium and deviate away from the intended pricing strategy.

“Let’s talk about it”: communication is key

• Internal Stakeholders – Portfolio (Product and underwriting) – Sales and Marketing

– Distributors: ie Agents, Brokers, Call centre and Branch network – Government and Public relations people

• Example of Financial/Customer Impact Analysis:

– Premium Change Distribution Impacts – Distribution of Premiums

– Spilt by Area, Flood Risk, Distribution Channel, Model type – Measures: Number of Policies at Risk, Premiums Values, Sum Insured Vales

• External Stakeholders

– Customers

– Government: local, state, federal – Regulators: APRA, ASIC – Community – Distribution network – ICA, Other insurers

Flood Example:

Figure 1: Area

impacted

•Angry customer disputing premium

•No supporting documentation

•Existing public flood study for the

area

•Indicates the property as high risk ie

ARI < 10

•What would you do? Straight

forward communication to

customer?

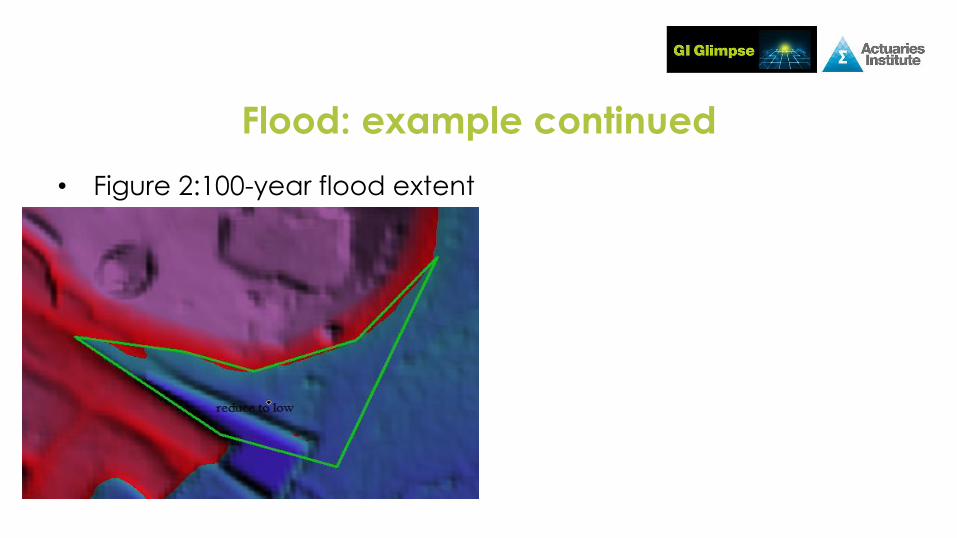

Flood: example continued

• Figure 2:100-year flood extent

Flood example: continued

• Figure 3: 100-year flood extent after filling of land

•Property owner may or maynot

have evidence to prove the land

was elevated eg Section 149

certificate

•But a renter will unlikely be in

position to have this information

unless go to council: fair?

•Based on elevation data the area

was re-rated as low flood risk