Embed Size (px)

Citation preview

PwC

The New Basel AccordBanks’ current state of readiness

A European perspective

14 May 2002 – Istanbul

Charles IlakoPartner, Head of EMEA Regulatory Practice (Europe)

Charles IlakoPartner, Head of EMEA Regulatory Practice (Europe)

PwC

Issues Considered

• Overall context

• Basel Timeframe

• Basel Project Lifecycle

• Strategic implications

• Banks’ preparedness

• General observations• Credit risk• Operational risk• Project management

• Our Diagnostic approach

• Conclusions

PwC

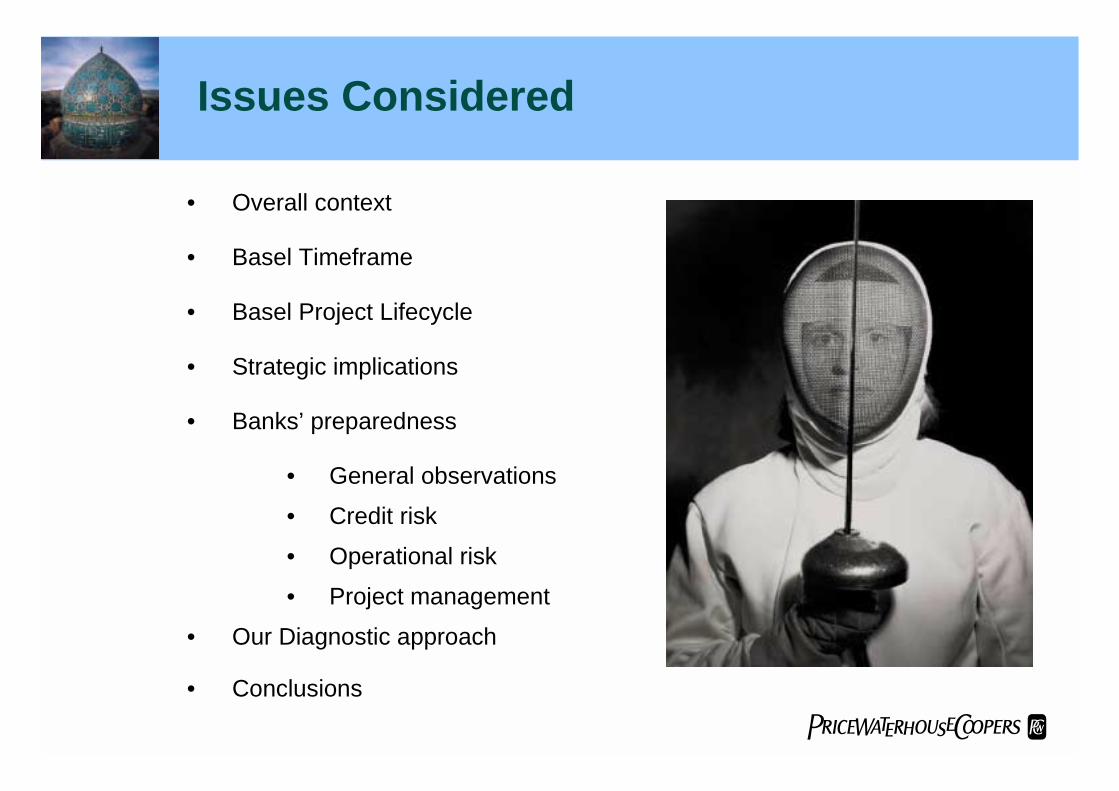

Market feedback on the Basel Accordproposals

“Disclosure will provide alot more data - will it

provide more meaningfulinformation?”

“Lots of losers inthis - difficult to see

the winners.”

“Calibration mustbe right”

“Meeting thequalitative criteriawill prove to be thebiggest challenge.”

“Disclosure-prescriptiveness,

volume, and detail ofthe proposals fiercelycriticised. Concerns

regardinginconsistency with

IAS”

“a significantchallenge to

supervisors’ skill sets”

PwC

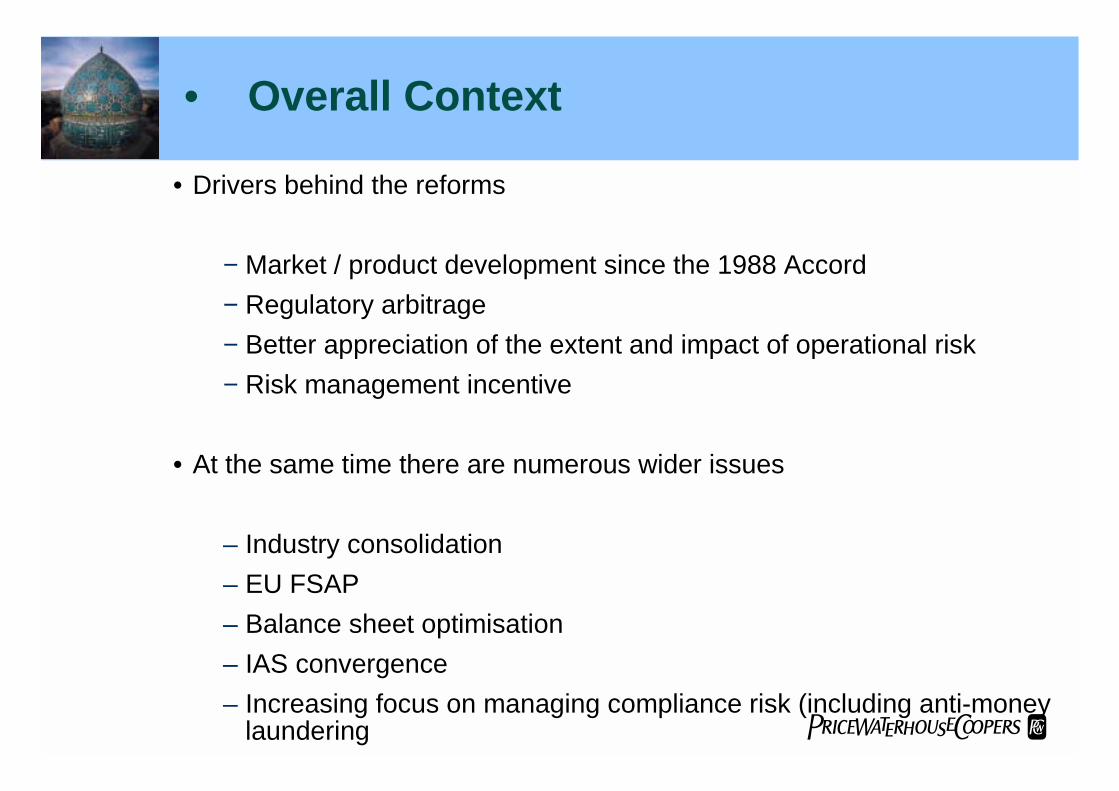

• Drivers behind the reforms

− Market / product development since the 1988 Accord− Regulatory arbitrage− Better appreciation of the extent and impact of operational risk− Risk management incentive

• At the same time there are numerous wider issues

– Industry consolidation– EU FSAP– Balance sheet optimisation– IAS convergence– Increasing focus on managing compliance risk (including anti-money

laundering

• Overall Context

PwC

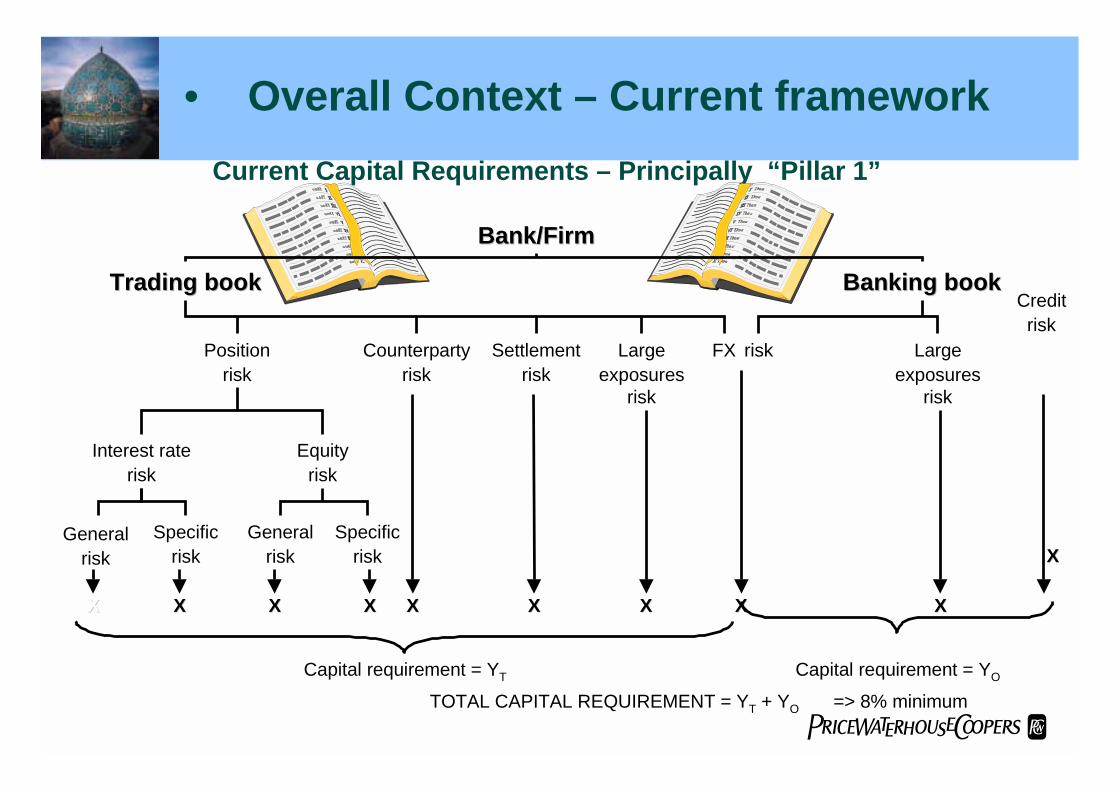

Current Capital Requirements – Principally “Pillar 1”

Bank/FirmBank/Firm

Trading bookTrading book Banking bookBanking book

Positionrisk

Counterpartyrisk

Settlementrisk

Largeexposures

risk

FX Largeexposures

risk

Creditrisk

Interest raterisk

Equityrisk

Generalrisk

Specificrisk

Generalrisk

Specificrisk

risk

XX XX XX XX XX XX XX XX XX

XX

Capital requirement = YT Capital requirement = YO

TOTAL CAPITAL REQUIREMENT = YT + YO => 8% minimum

• Overall Context – Current framework

PwC

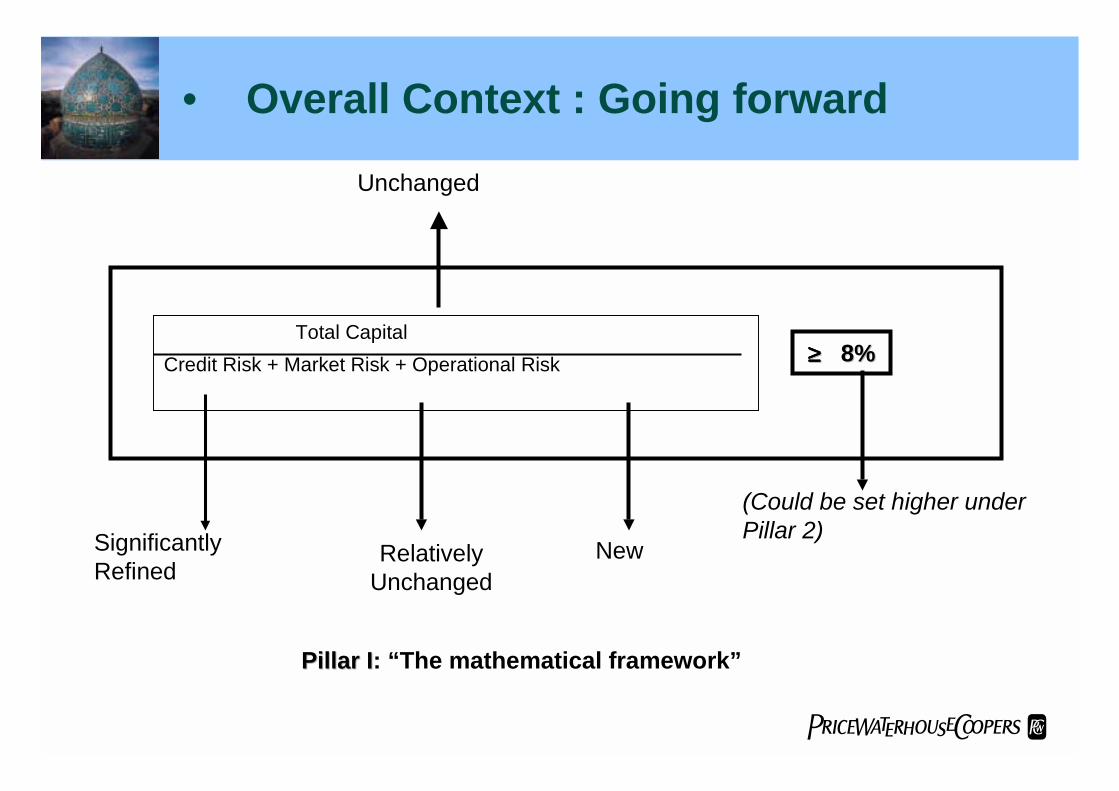

• Overall Context : Going forward

Unchanged

(Could be set higher underPillar 2)

Total CapitalCredit Risk + Market Risk + Operational Risk ≥≥≥≥≥≥≥≥ 8% 8%

SignificantlyRefined

NewRelativelyUnchanged

Pillar IPillar I: “The mathematical framework”

PwC

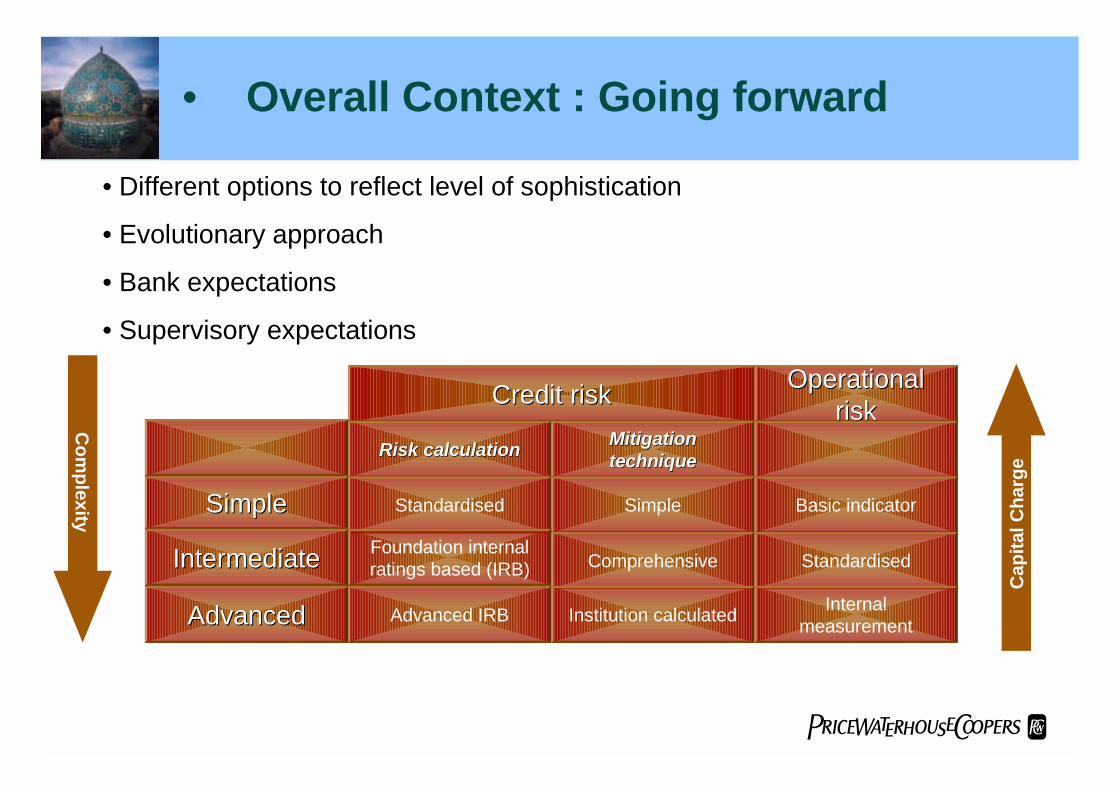

Credit riskCredit risk

Risk calculationRisk calculation MitigationMitigationtechniquetechnique

OperationalOperationalriskrisk

Standardised Simple Basic indicatorSimpleSimpleFoundation internalratings based (IRB) Comprehensive StandardisedIntermediateIntermediate

Advanced IRB Institution calculated InternalmeasurementAdvancedAdvanced

• Different options to reflect level of sophistication

• Evolutionary approach

• Bank expectations

• Supervisory expectations

Com

plexityC

apita

l Cha

rge

• Overall Context : Going forward

PwC

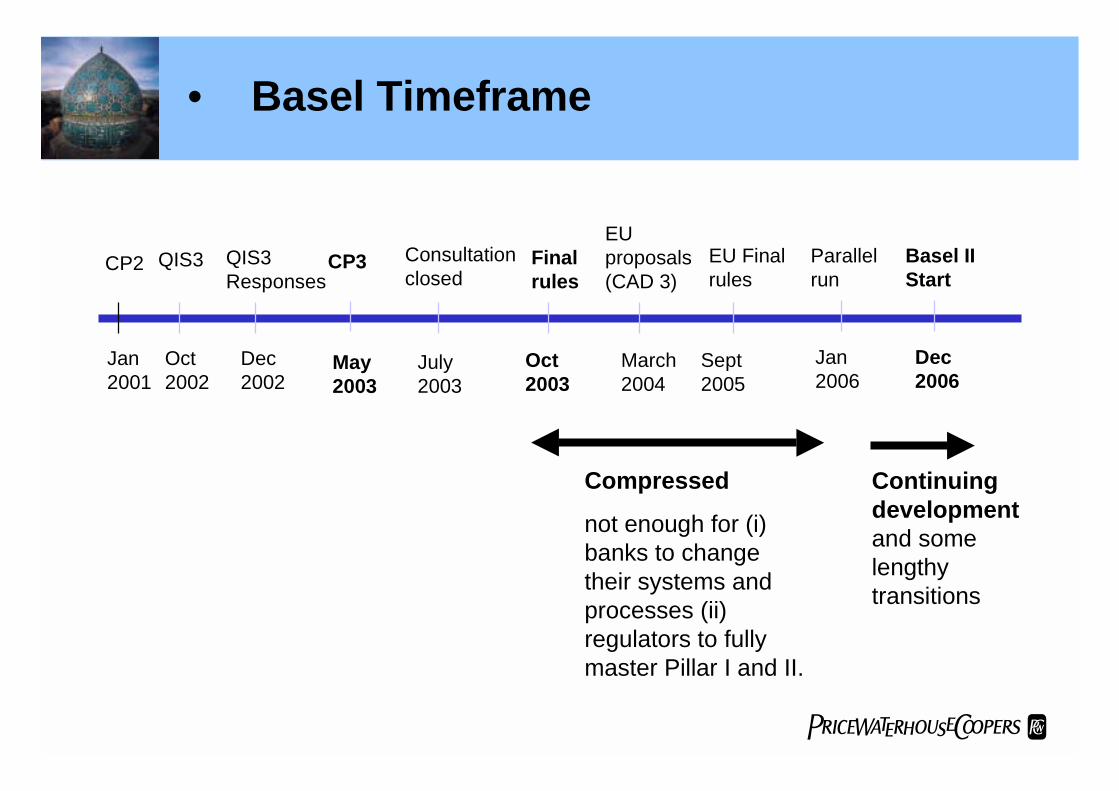

Oct2002

July2003

Jan2006

CP2 Consultationclosed

Compressed

not enough for (i)banks to changetheir systems andprocesses (ii)regulators to fullymaster Pillar I and II.

Continuingdevelopmentand somelengthytransitions

CP3

May2003

• Basel Timeframe

Jan2001

QIS3 QIS3Responses

Dec2002

Oct2003

Finalrules

EUproposals(CAD 3)

March2004

EU Finalrules

Sept2005

Parallelrun

Basel IIStart

Dec2006

PwC

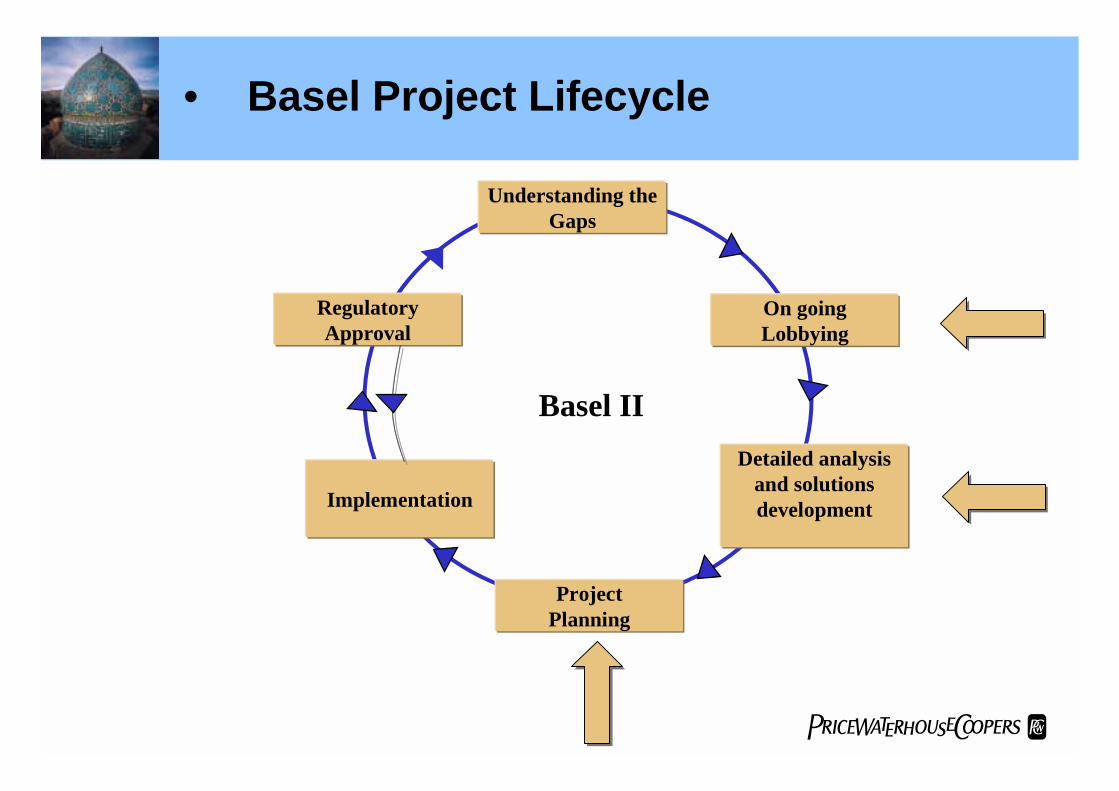

Understanding theGaps

On goingLobbying

Detailed analysisand solutionsdevelopment

ProjectPlanning

Implementation

RegulatoryApproval

Basel II

• Basel Project Lifecycle

PwC

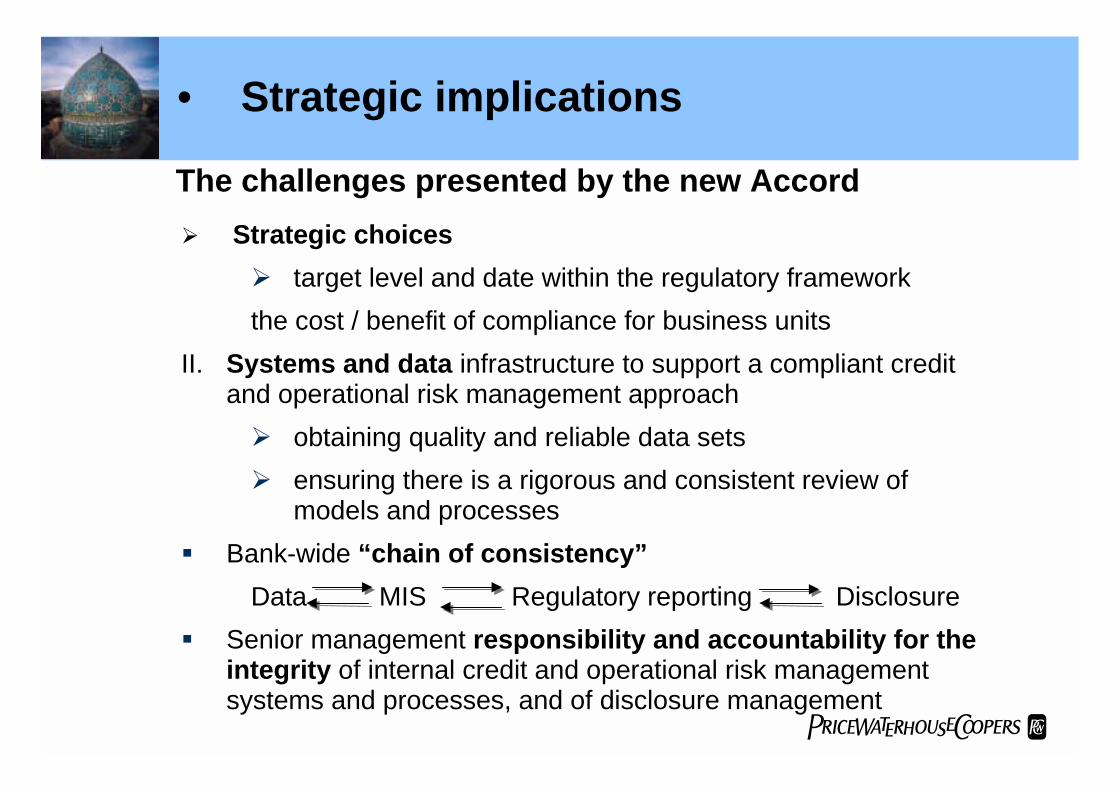

The challenges presented by the new Accord! Strategic choices

! target level and date within the regulatory frameworkthe cost / benefit of compliance for business units

II. Systems and data infrastructure to support a compliant creditand operational risk management approach! obtaining quality and reliable data sets! ensuring there is a rigorous and consistent review of

models and processes" Bank-wide “chain of consistency”

Data MIS Regulatory reporting Disclosure" Senior management responsibility and accountability for the

integrity of internal credit and operational risk managementsystems and processes, and of disclosure management

• Strategic implications

PwC

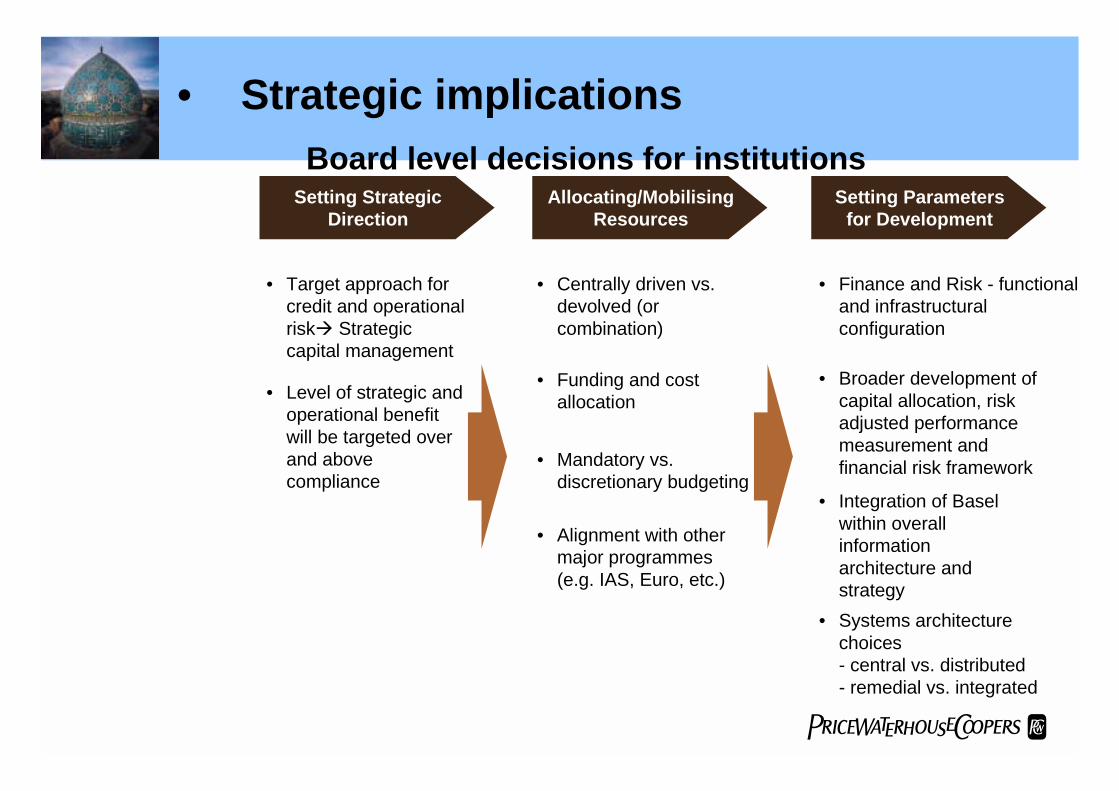

Board level decisions for institutionsSetting Parameters

for DevelopmentSetting Strategic

DirectionAllocating/Mobilising

Resources

• Broader development ofcapital allocation, riskadjusted performancemeasurement andfinancial risk framework

• Integration of Baselwithin overallinformationarchitecture andstrategy

• Systems architecturechoices- central vs. distributed- remedial vs. integrated

• Finance and Risk - functionaland infrastructuralconfiguration

• Target approach forcredit and operationalrisk# Strategiccapital management

• Level of strategic andoperational benefitwill be targeted overand abovecompliance

• Funding and costallocation

• Mandatory vs.discretionary budgeting

• Centrally driven vs.devolved (orcombination)

• Alignment with othermajor programmes(e.g. IAS, Euro, etc.)

• Strategic implications

PwC

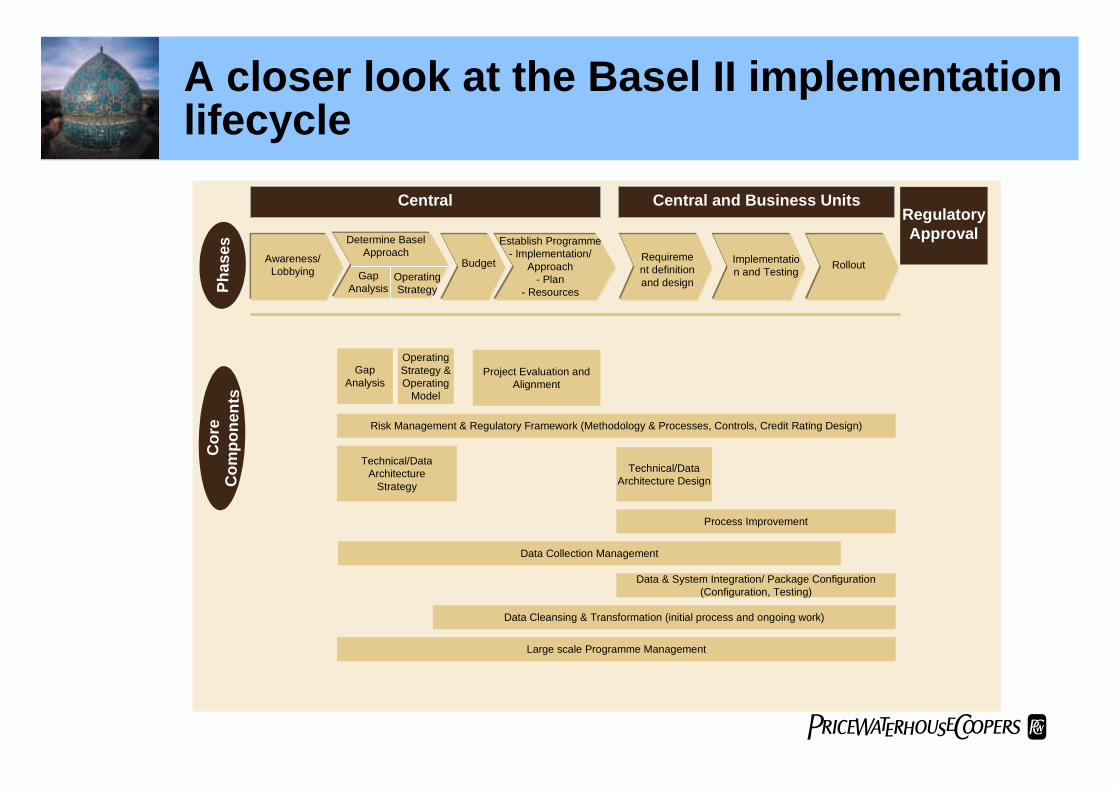

A closer look at the Basel II implementationlifecycle

Project Evaluation andAlignment

Process Improvement

Technical/DataArchitecture Design

Data & System Integration/ Package Configuration(Configuration, Testing)

Data Cleansing & Transformation (initial process and ongoing work)

Technical/DataArchitecture

Strategy

Risk Management & Regulatory Framework (Methodology & Processes, Controls, Credit Rating Design)

Large scale Programme Management

Data Collection Management

GapAnalysis

OperatingStrategy &Operating

Model

Phas

es

Awareness/Lobbying Rollout

Cor

eC

ompo

nent

sEstablish Programme

- Implementation/Approach

- Plan- Resources

Requirement definitionand design

Budget Implementation and Testing

Central Central and Business UnitsRegulatoryApprovalDetermine Basel

Approach

GapAnalysis

OperatingStrategy

PwC

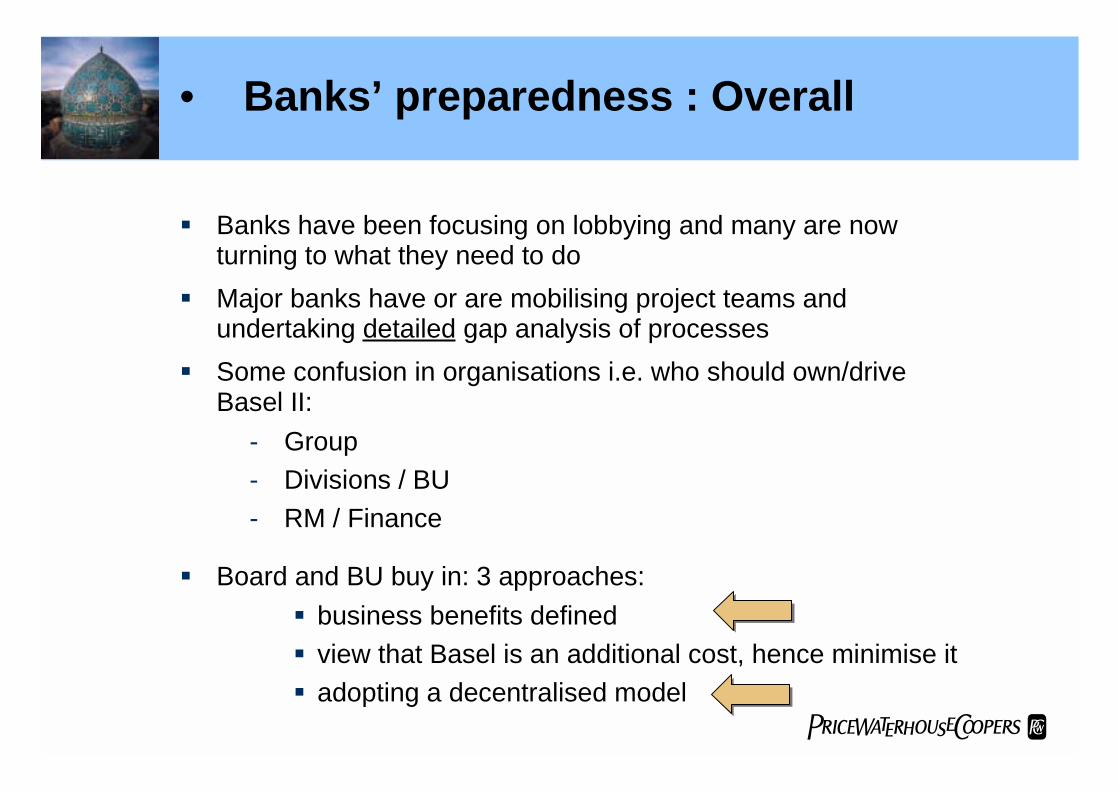

" Banks have been focusing on lobbying and many are nowturning to what they need to do

" Major banks have or are mobilising project teams andundertaking detailed gap analysis of processes

" Some confusion in organisations i.e. who should own/driveBasel II:

- Group- Divisions / BU- RM / Finance

" Board and BU buy in: 3 approaches:" business benefits defined" view that Basel is an additional cost, hence minimise it" adopting a decentralised model

• Banks’ preparedness : Overall

PwC

" Budgeting: primarily step-by-step" Efforts underway to determine the “net cost / benefit”" Operational risk requirements have become somewhat clearer

which is aiding decision making

• Banks’ preparedness : Overall

PwC

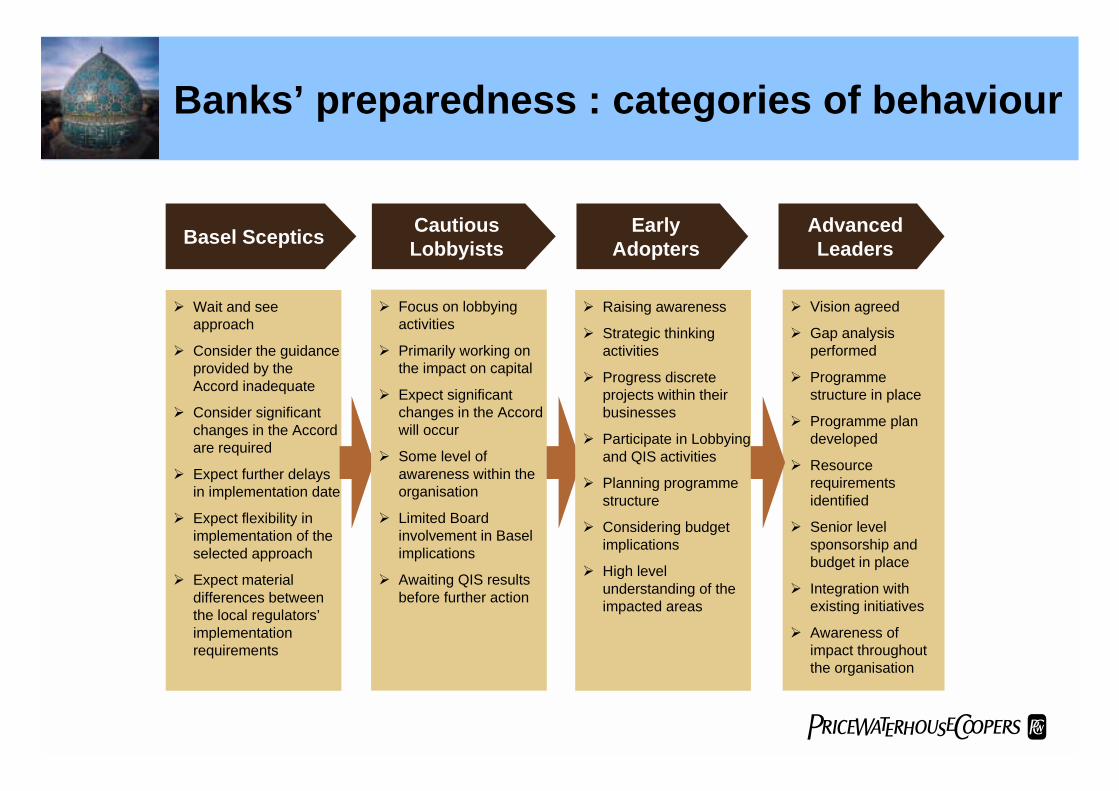

AdvancedLeaders

! Vision agreed

! Gap analysisperformed

! Programmestructure in place

! Programme plandeveloped

! Resourcerequirementsidentified

! Senior levelsponsorship andbudget in place

! Integration withexisting initiatives

! Awareness ofimpact throughoutthe organisation

Basel Sceptics

! Wait and seeapproach

! Consider the guidanceprovided by theAccord inadequate

! Consider significantchanges in the Accordare required

! Expect further delaysin implementation date

! Expect flexibility inimplementation of theselected approach

! Expect materialdifferences betweenthe local regulators’implementationrequirements

CautiousLobbyists

! Focus on lobbyingactivities

! Primarily working onthe impact on capital

! Expect significantchanges in the Accordwill occur

! Some level ofawareness within theorganisation

! Limited Boardinvolvement in Baselimplications

! Awaiting QIS resultsbefore further action

EarlyAdopters

! Raising awareness

! Strategic thinkingactivities

! Progress discreteprojects within theirbusinesses

! Participate in Lobbyingand QIS activities

! Planning programmestructure

! Considering budgetimplications

! High levelunderstanding of theimpacted areas

Banks’ preparedness : categories of behaviour

PwC

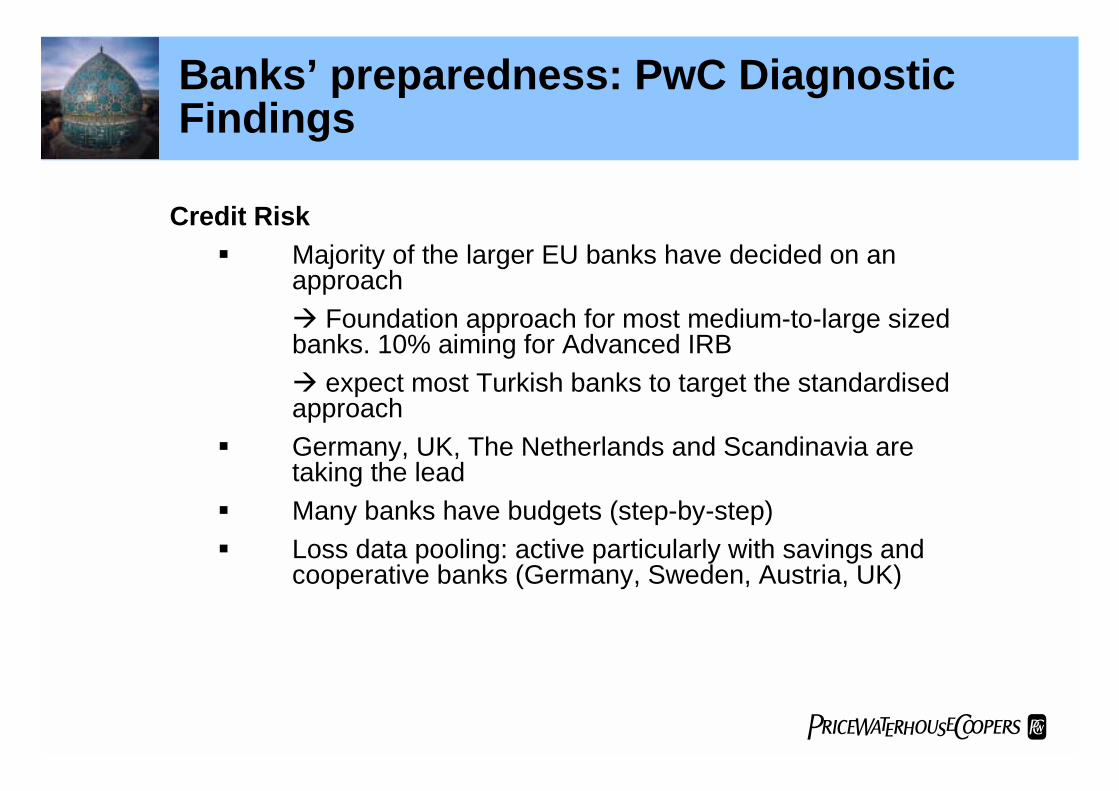

Banks’ preparedness: PwC DiagnosticFindings

Credit Risk" Majority of the larger EU banks have decided on an

approach# Foundation approach for most medium-to-large sizedbanks. 10% aiming for Advanced IRB# expect most Turkish banks to target the standardisedapproach

" Germany, UK, The Netherlands and Scandinavia aretaking the lead

" Many banks have budgets (step-by-step)" Loss data pooling: active particularly with savings and

cooperative banks (Germany, Sweden, Austria, UK)

PwC

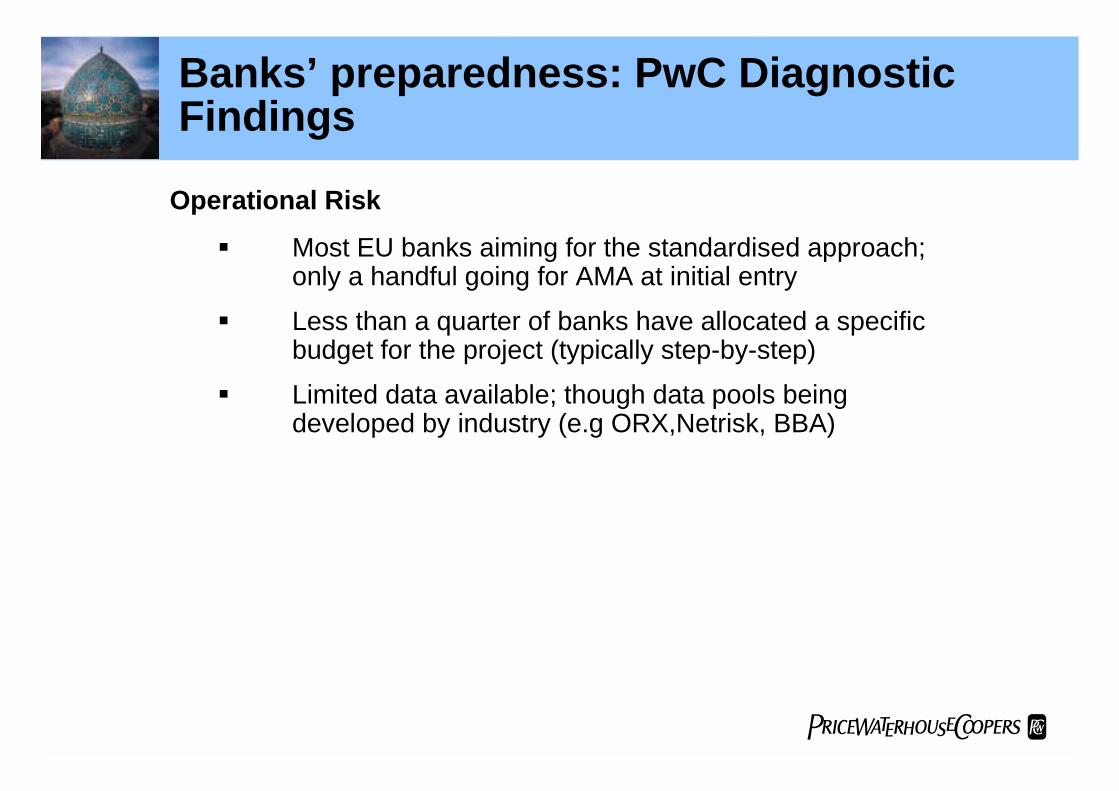

Banks’ preparedness: PwC DiagnosticFindings

Operational Risk" Most EU banks aiming for the standardised approach;

only a handful going for AMA at initial entry" Less than a quarter of banks have allocated a specific

budget for the project (typically step-by-step)" Limited data available; though data pools being

developed by industry (e.g ORX,Netrisk, BBA)

PwC

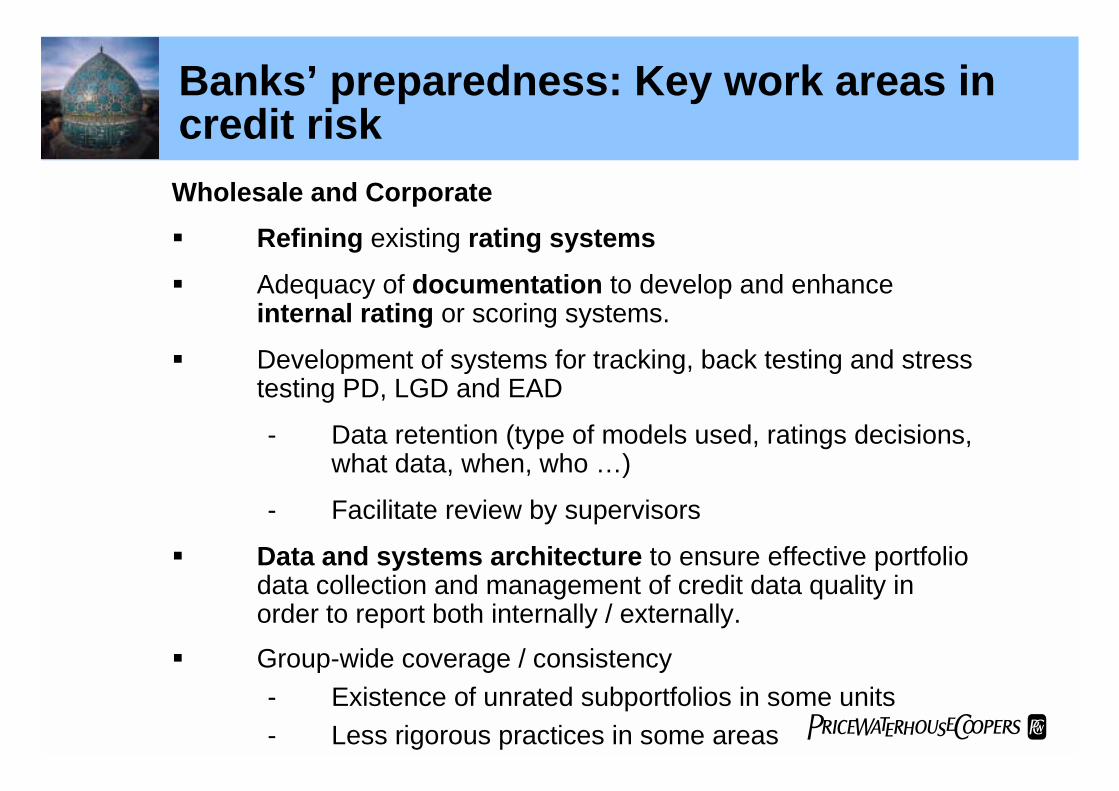

Banks’ preparedness: Key work areas incredit riskWholesale and Corporate" Refining existing rating systems" Adequacy of documentation to develop and enhance

internal rating or scoring systems.

" Development of systems for tracking, back testing and stresstesting PD, LGD and EAD

- Data retention (type of models used, ratings decisions,what data, when, who …)

- Facilitate review by supervisors

" Data and systems architecture to ensure effective portfoliodata collection and management of credit data quality inorder to report both internally / externally.

" Group-wide coverage / consistency- Existence of unrated subportfolios in some units- Less rigorous practices in some areas

PwC

Banks’ preparedness: Other creditrisk issues

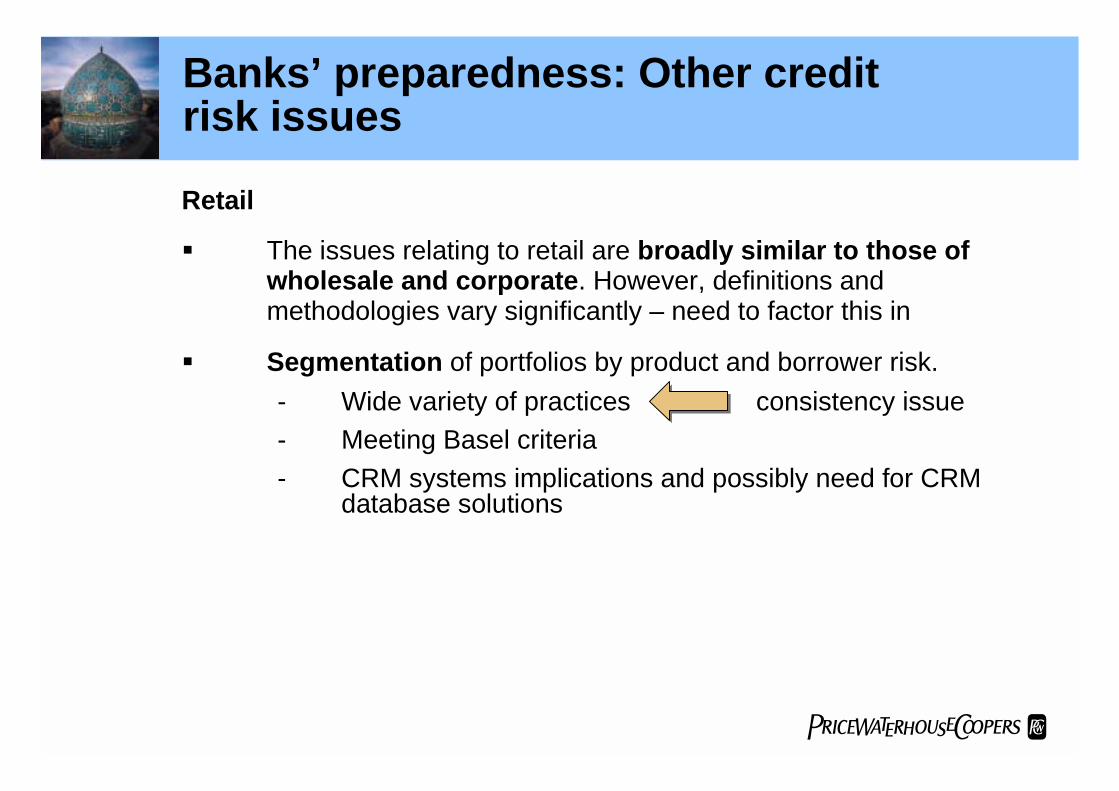

Retail

" The issues relating to retail are broadly similar to those ofwholesale and corporate. However, definitions andmethodologies vary significantly – need to factor this in

" Segmentation of portfolios by product and borrower risk.- Wide variety of practices consistency issue- Meeting Basel criteria- CRM systems implications and possibly need for CRM

database solutions

PwC

Banks’ preparedness: Other creditrisk issues" Formal process (inc. documentation) for Board to approve

credit risk strategy and policy; demonstration that credit riskappetite and policy meets Basel standard

" Review and changes to legal documentation regardingcollateral and guarantees (enforceability, value)

" Assessment of skills gaps and development needs in creditand internal audit:- Credit risk practices- Rating systems- Governance- CRM

" Typical internal deadlines# Rating systems by end of year# Data systems by end 2003# Workable capital calculations by end 2004

PwC

Banks’ preparedness: Key workareas in operational risk

" Determining long-term loss data collection and reportingsolution and developing the processes.- Internal sources- Data pooling- Analysis and interpretation of data

" Capturing of Exposure Indicator information (grossincome) in order to calculate the operational risk capitalcharge.

" Formal process (e.g training) by which the skill sets ofoperational risk and internal audit personnel are improvedand kept up to date.

PwC

Banks’ preparedness: Shortcomingsand gaps" There are a number of common problem areas in respect of credit

and operational risk:

!Possibly too much focus on the capital numbers at expense ofprocesses

!Firms not bringing together credit risk, operational risk, capitalmodelling and reporting capabilities to best effect. Silo mentalityresulting in business benefits being undermined and duplicationof effort

!Defining and establishing an adequate risk managementframework (including policies & procedures, governance, roles &responsibilities)

- Basel compliant- Providing a Basel base for E Capital

!Determining the appropriate organisational structure for riskmanagement

!Setting risk appetite / risk tolerance

PwC

Banks’ preparedness: Shortcomingsand gaps

! Ensuring that information for disclosure requirements isappropriately supported by audit trails.

! Data MI Regulatory reporting Disclosure! Process upgrade led by Finance and involving RM and

Corporate Communications

PwC

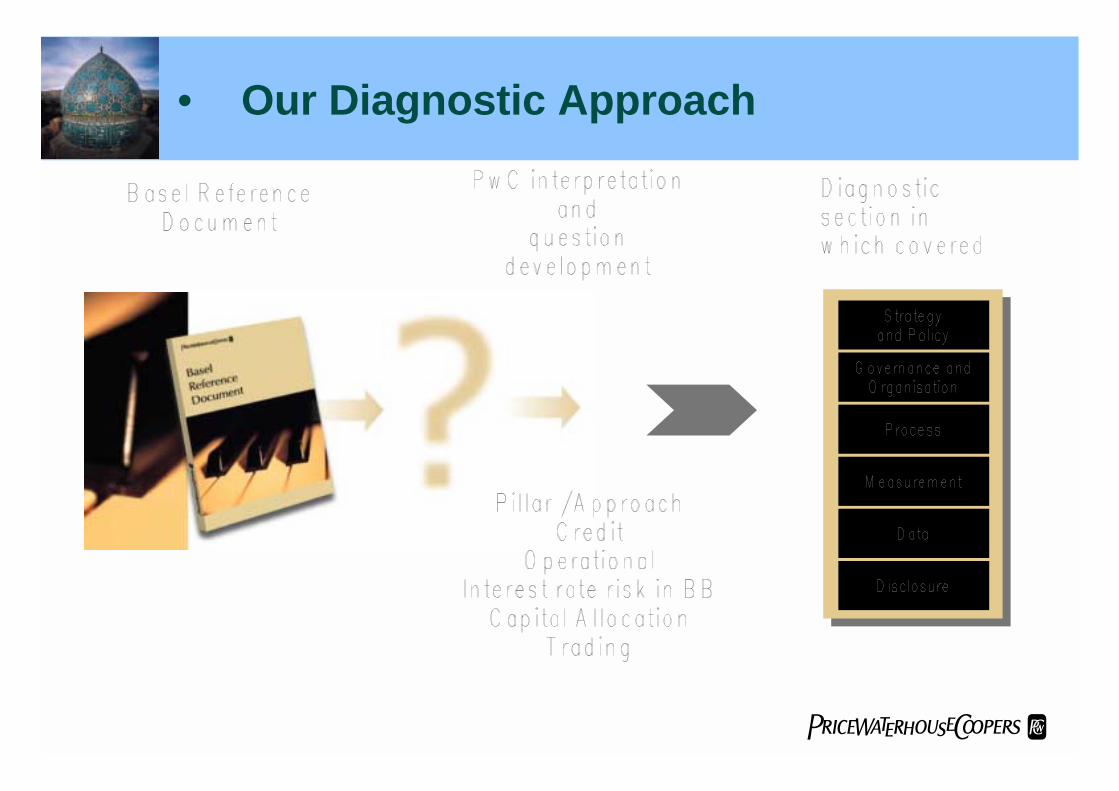

• Our Diagnostic Approach

PwC

Our approach: Six key risk areas

Credit and Operational R

isk

Level 1

Level 2

Level 3

• Our Diagnostic Approach

PwC

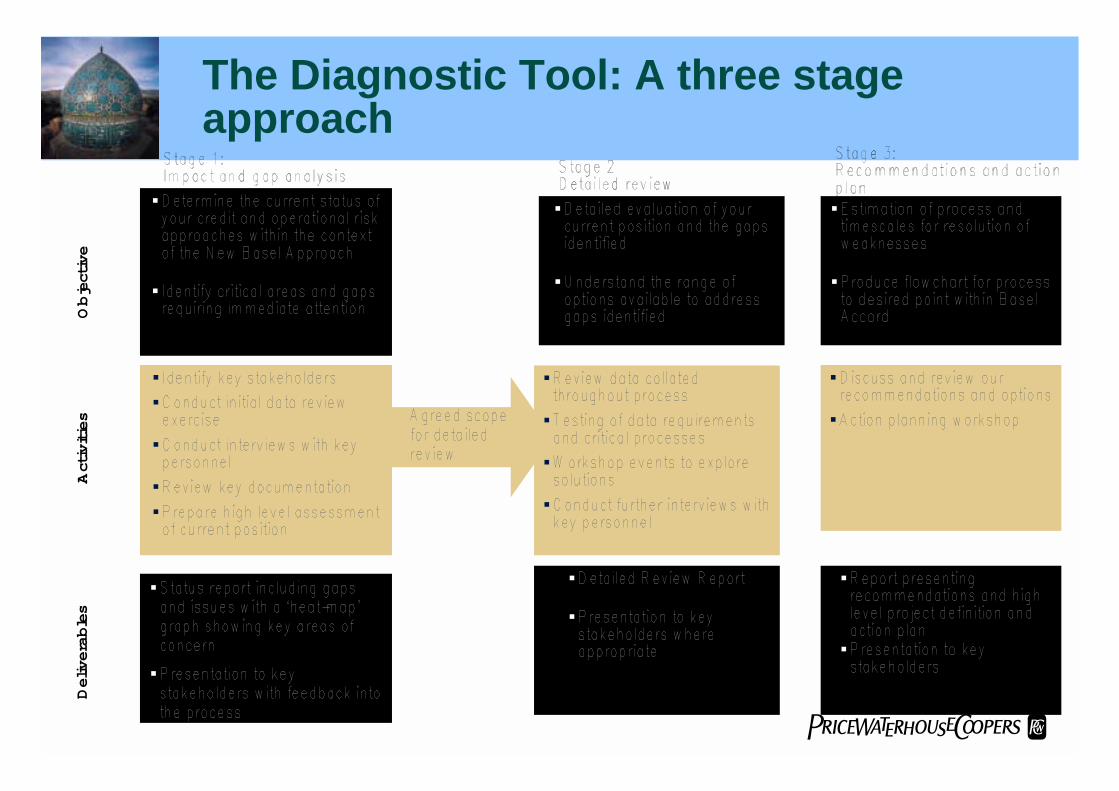

The Diagnostic Tool: A three stageapproach

"

"

"

"

"

"

"

"

"

"

"

"

Objective

"

"

"

"

"

"

"

"

"

Activities

Deliverables

"

"

PwC

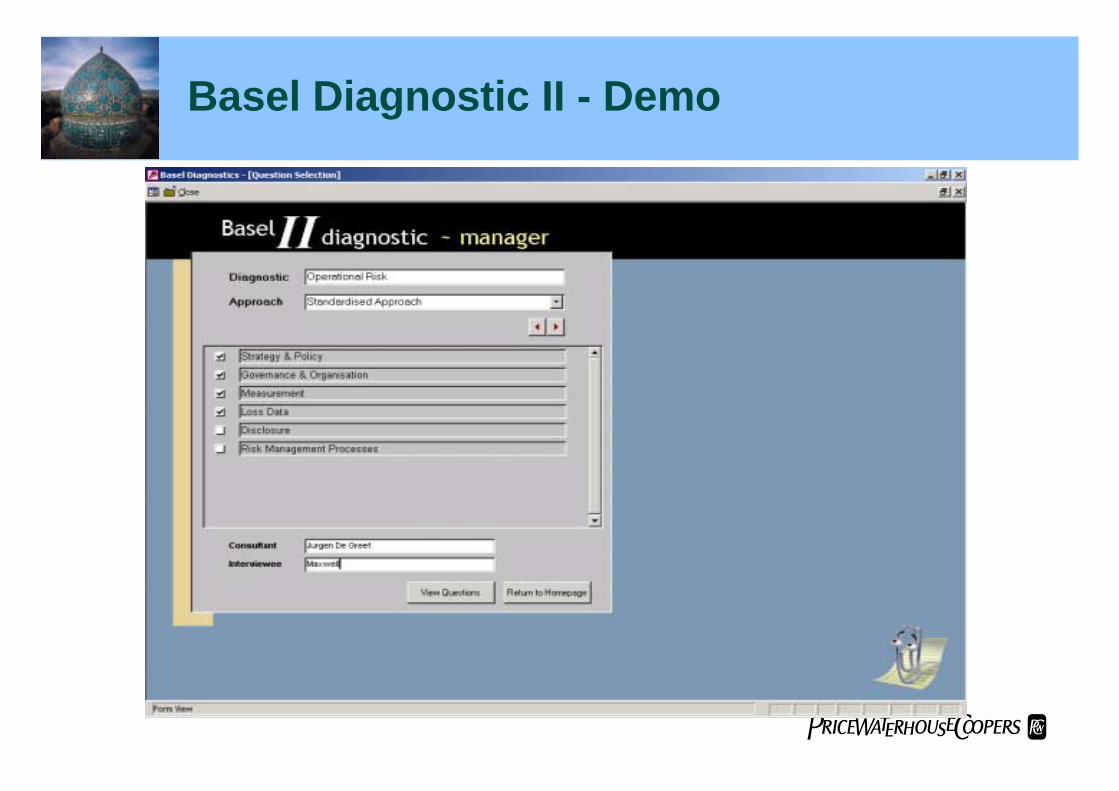

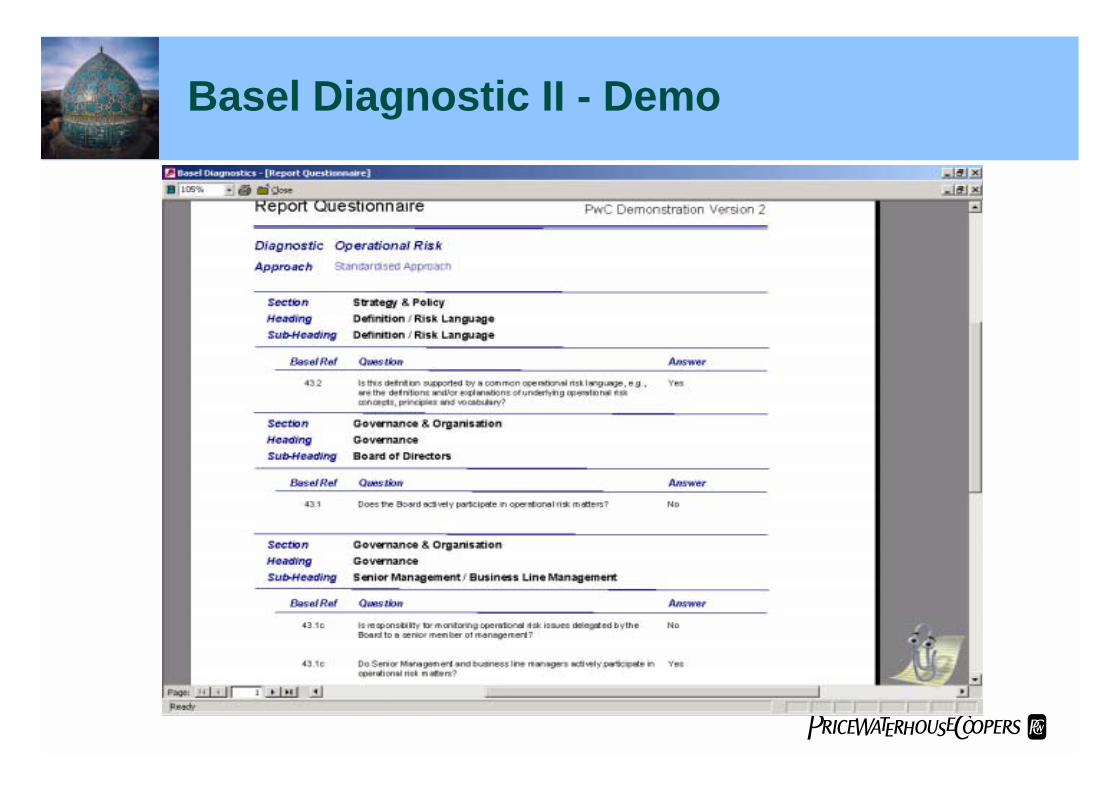

Basel Diagnostic II - Demo

PwC

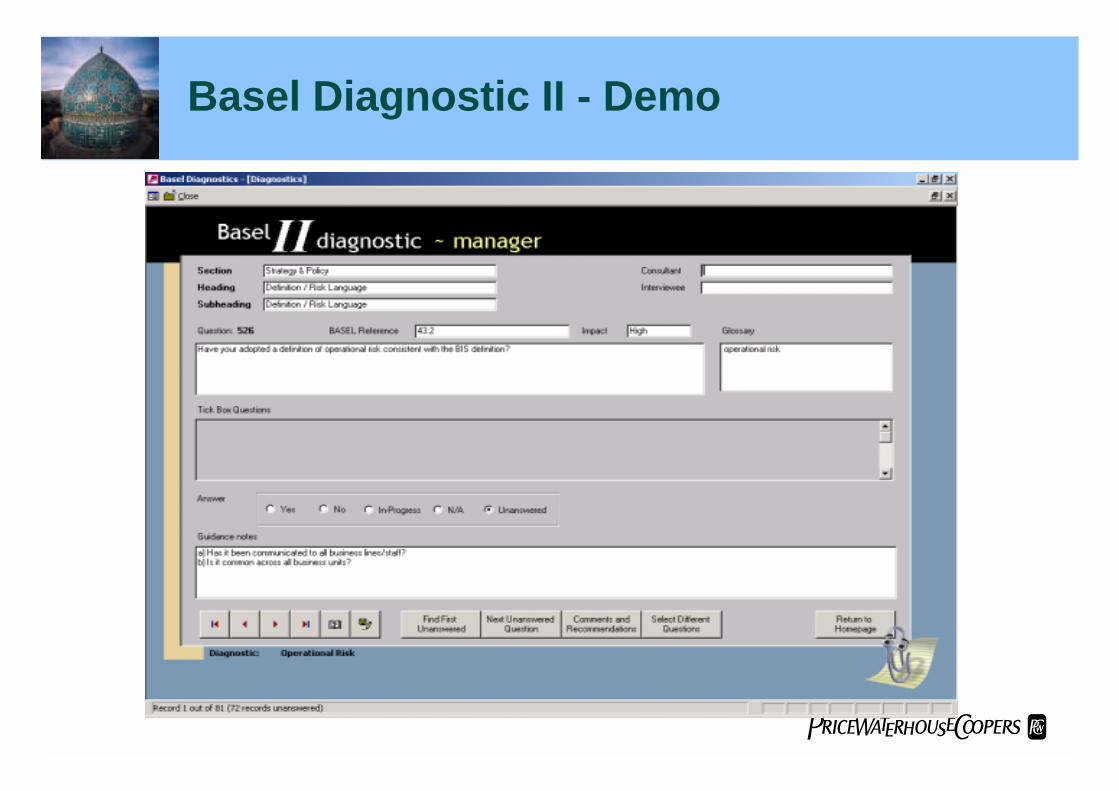

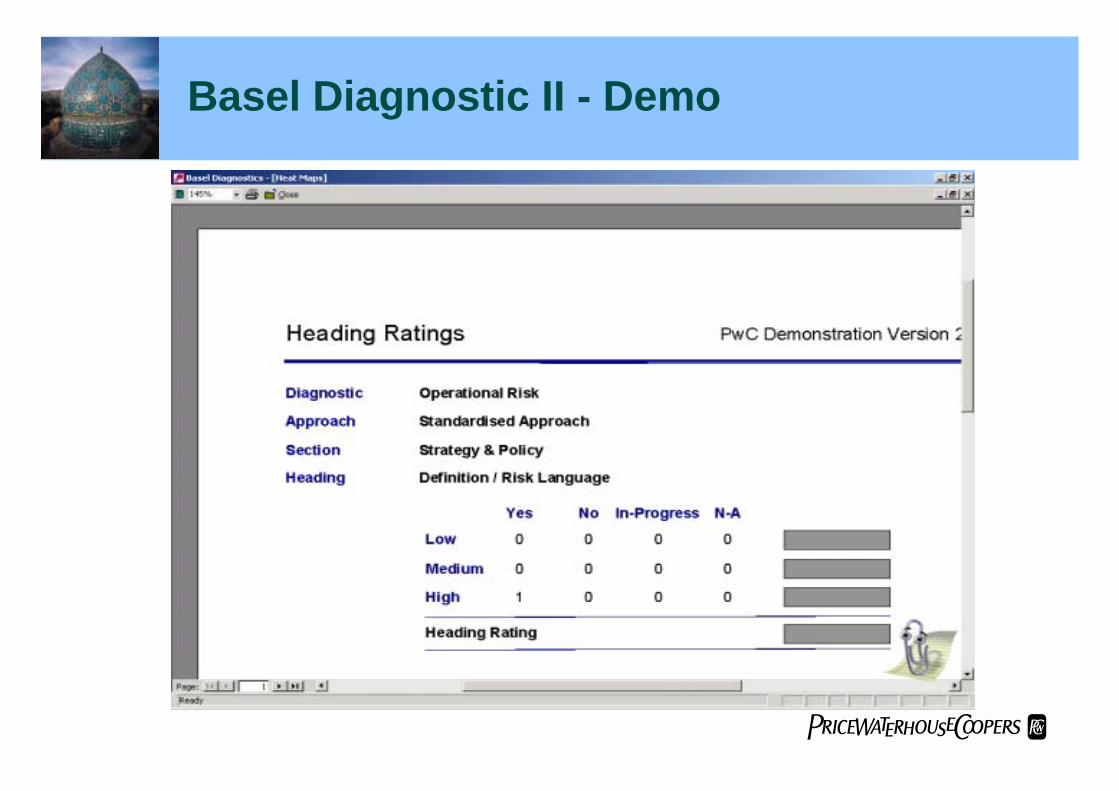

Basel Diagnostic II - Demo

PwC

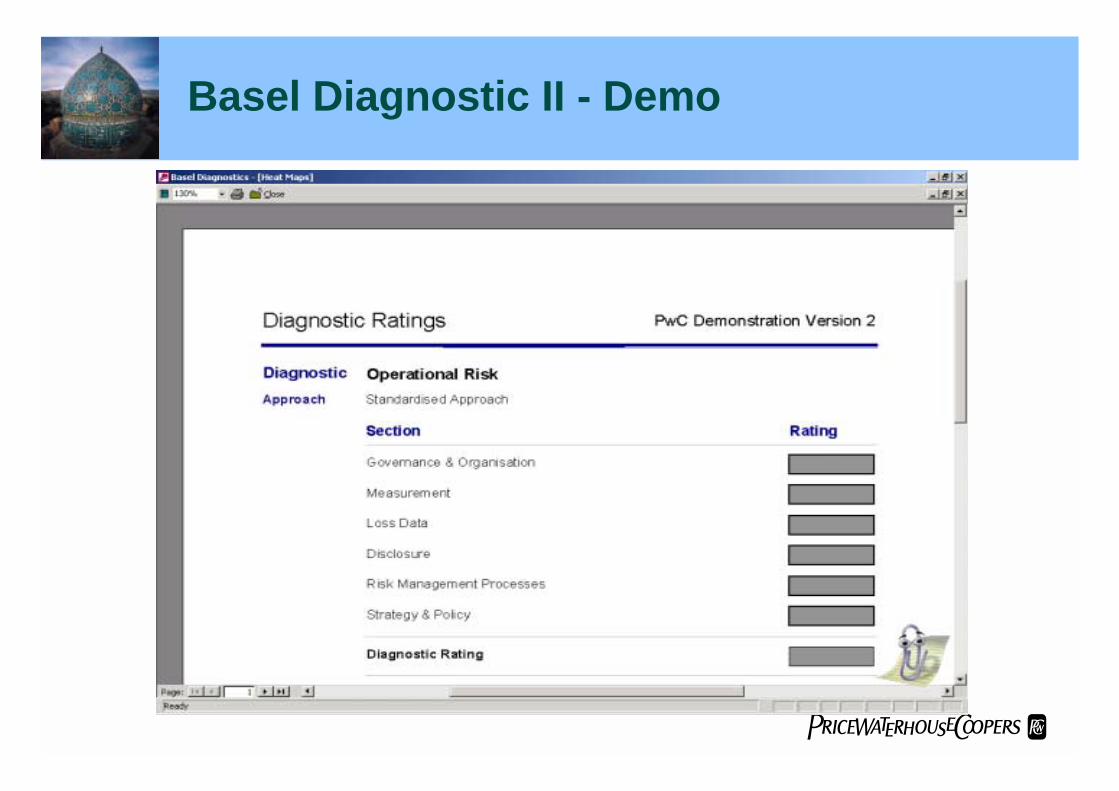

Basel Diagnostic II - Demo

PwC

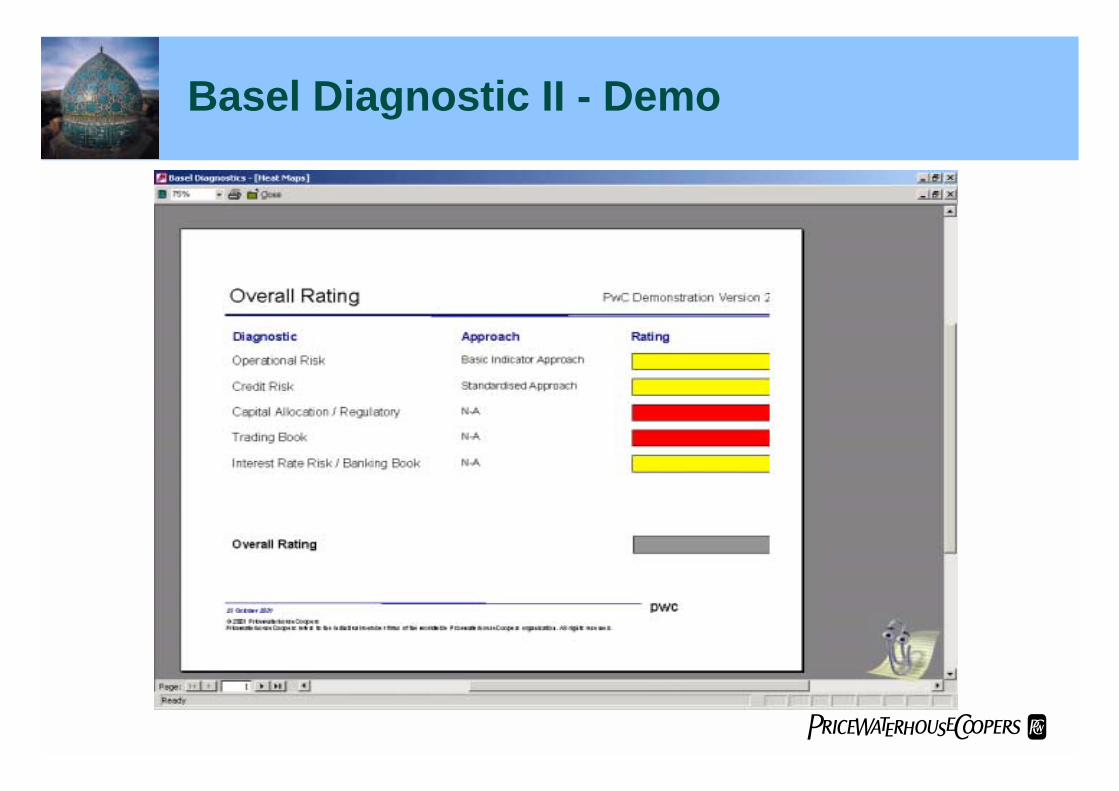

Basel Diagnostic II - Demo

PwC

Basel Diagnostic II - Demo

PwC

Basel Diagnostic II - Demo

PwC

" A group of large and medium sized EU banks firmly on track" Vital that banks use the additional time wisely" Boards should be actively engaged

• Conclusion