Embed Size (px)

Citation preview

In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making any investment decision based on this

research, the reader needs to consider, with or without assistance of an adviser, whether the advice is appropriate to their particular investment needs, objectives and financial circumstances.

Please see disclaimer.

The manganese industry worldwide

– trends and opportunities

IMnI’s 39th Annual Conference

Istanbul – 6th June 2013

Duncan Hobbs

+44 20 3037 4497

– 2 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 3 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 4 –

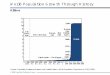

Mn market overview – most ore is used to produce

Mn ferroalloys for the steel industry

Mn ore BF ironmaking1

Mn ferroalloys Slag losses

SiMn2 MLC FeMn HC FeMn Non-steel uses

EMM EMD

~1%

88%

~20%

~80%

60% 12% 28%

~2%

9% ~2%

Stainless steel (200 series)

Non-ferrous metals, mainly

Al, Cu (10%-15% of total)

Batteries, electronics and

welding (10%-15% of total)

Dry-cell batteries

Chemicals (KMnO4, MnCl2),

including fertilisers (MnSO4)

Ceramics, glass and some

metal output (zinc, uranium)

Low carbon surface critical

flat steel products

Long steel products

Non-surface critical flat

products (sheet and plate)

Surface critical flat steel

products (sheet and plate)

Some long products

Examples

Foundry products, mainly

from cast iron

Primarily using HC FeMn;

limited use of other alloys

Examples

Automotive body sheet

Some flat stainless steels

Examples

Construction steels

Unexposed car parts

Examples

Consumer appliances

API3 tube and pipe; rails

Source: CPM, K.Fowkes, Hatch, Macquarie Research, June 2013. Note: 2012 data, basis Mn units. 1. Some Mn ore is charged directly in blast furnace ironmaking, mainly in

Japan and Korea. 2. Some SiMn is used to produce MC FeMn by silicothermic reduction, mainly in China. 3. American Petroleum Institute

– 5 –

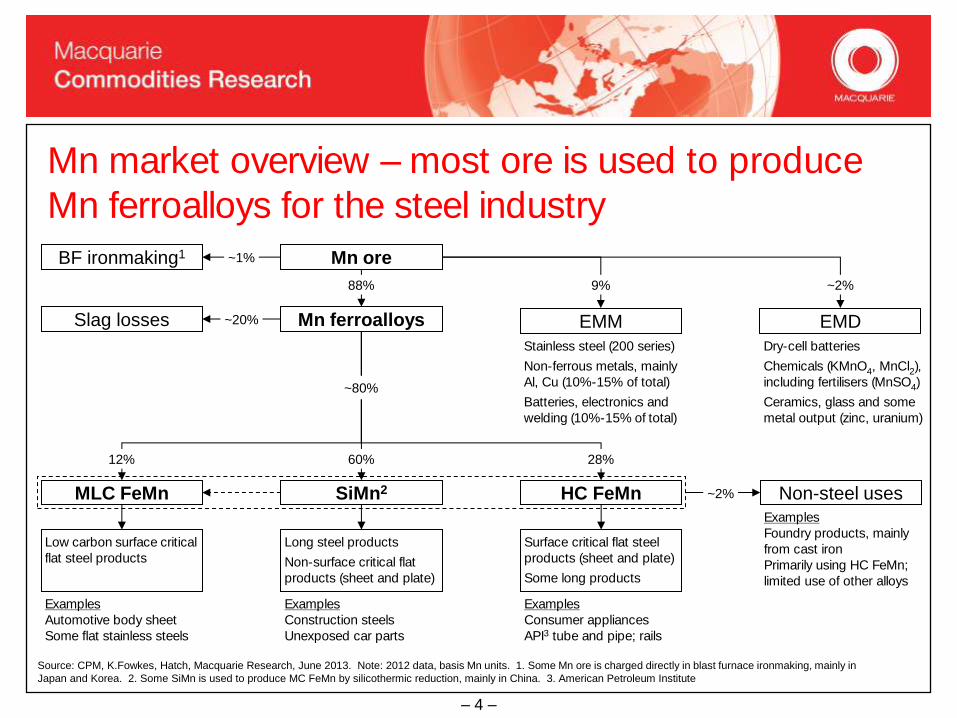

China drives world crude steel output to new records.

Ex-Asia production still below pre-crisis peaks

Global crude steel production

0

250

500

750

1,000

1,250

1,500

1,750

2000

2002

2004

2006

2008

2010

2012

m t

on

nes a

nn

ualised

World

China

0

25

50

75

100

125

150

2000

2002

2004

2006

2008

2010

2012

Ind

ices 2

007 =

100

China

Other

Asia

ROW

N.Am

Europe

Source: Worldsteel, Macquarie Research, June 2013. Note: Pre-GFC trend lines basis Jan 2000 – Jun 2008

– 6 –

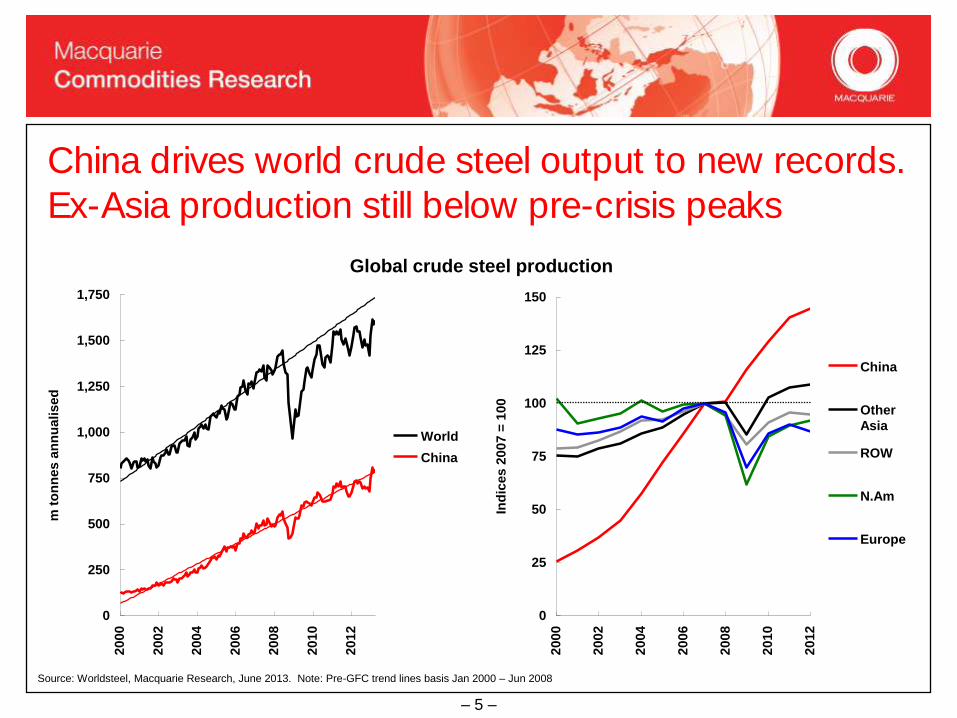

Long term there is still substantial potential for growth

in steel demand built on urbanisation

Population and urbanisation levels in 2010

Germany

Korea

Russia

Brazil

UKUSA

Indonesia

Pakistan

Bangladesh

China

49%

India

31%

Australia

Nigeria

Malaysia

Thailand

Vietnam

Singapore Japan

0%

20%

40%

60%

80%

100%

-250 0 250 500 750 1,000 1,250 1,500

Population, millions

Urb

an

isati

on

rate

-250

Raising China’s

urbanisation rate

to levels similar to

those in developed

Asian or European

countries will involve

moving more than

300m people into

towns and cities

This number is

equal to the entire

population of the

USA today and to

China’s urbanisation

since the early

1990s

Source: UN, Macquarie Research, June 2013. Note: 2010 data. China and India forecasts are for 2030. Size of circles proportional to population in each country

– 7 –

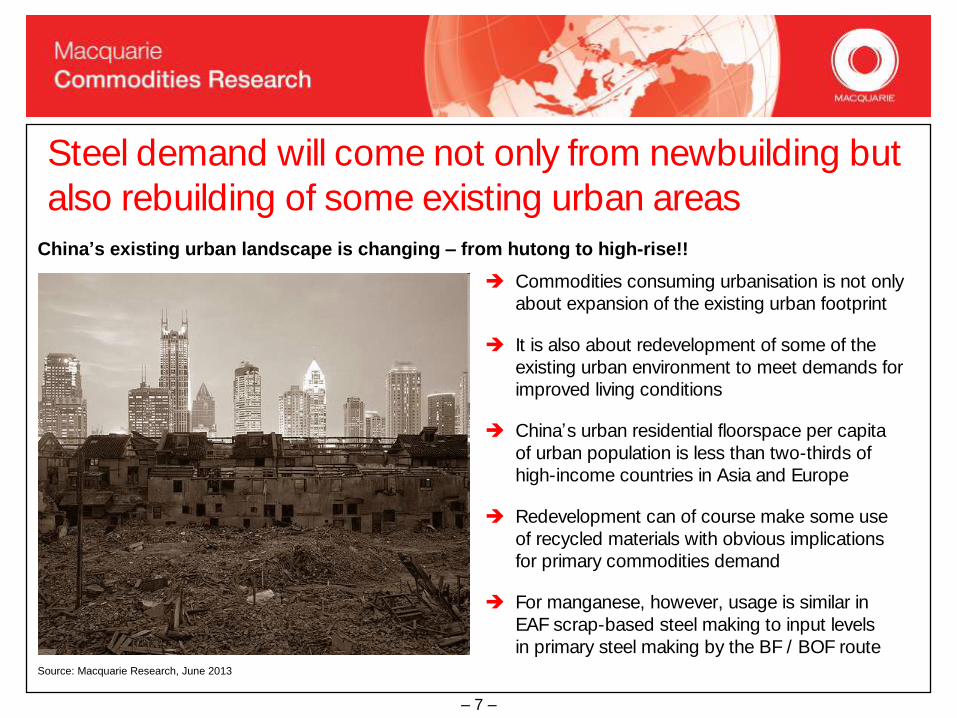

Steel demand will come not only from newbuilding but

also rebuilding of some existing urban areas

China’s existing urban landscape is changing – from hutong to high-rise!!

Commodities consuming urbanisation is not only

about expansion of the existing urban footprint

It is also about redevelopment of some of the

existing urban environment to meet demands for

improved living conditions

China’s urban residential floorspace per capita

of urban population is less than two-thirds of

high-income countries in Asia and Europe

Redevelopment can of course make some use

of recycled materials with obvious implications

for primary commodities demand

For manganese, however, usage is similar in

EAF scrap-based steel making to input levels

in primary steel making by the BF / BOF routeSource: Macquarie Research, June 2013

– 8 –

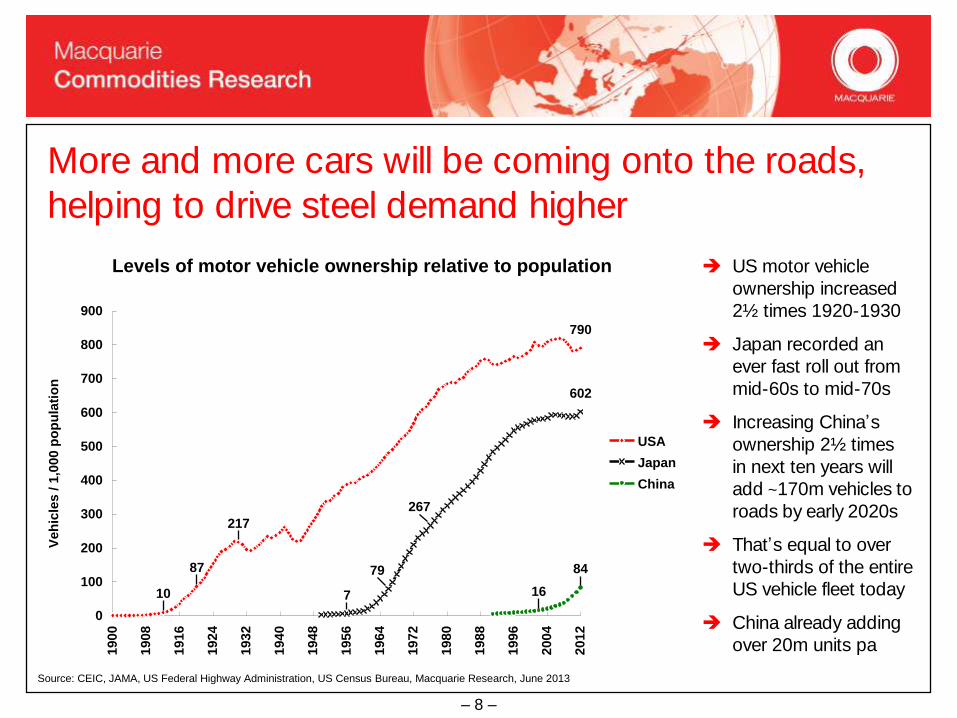

More and more cars will be coming onto the roads,

helping to drive steel demand higher

Levels of motor vehicle ownership relative to population

790

602

84

0

100

200

300

400

500

600

700

800

900

1900

1908

1916

1924

1932

1940

1948

1956

1964

1972

1980

1988

1996

2004

2012

Veh

icle

s / 1

,000 p

op

ula

tio

n

USA

Japan

China

10

87

217

7

79

267

16

84

US motor vehicle

ownership increased

2½ times 1920-1930

Japan recorded an

ever fast roll out from

mid-60s to mid-70s

Increasing China’s

ownership 2½ times

in next ten years will

add ~170m vehicles to

roads by early 2020s

That’s equal to over

two-thirds of the entire

US vehicle fleet today

China already adding

over 20m units pa

Source: CEIC, JAMA, US Federal Highway Administration, US Census Bureau, Macquarie Research, June 2013

– 9 –

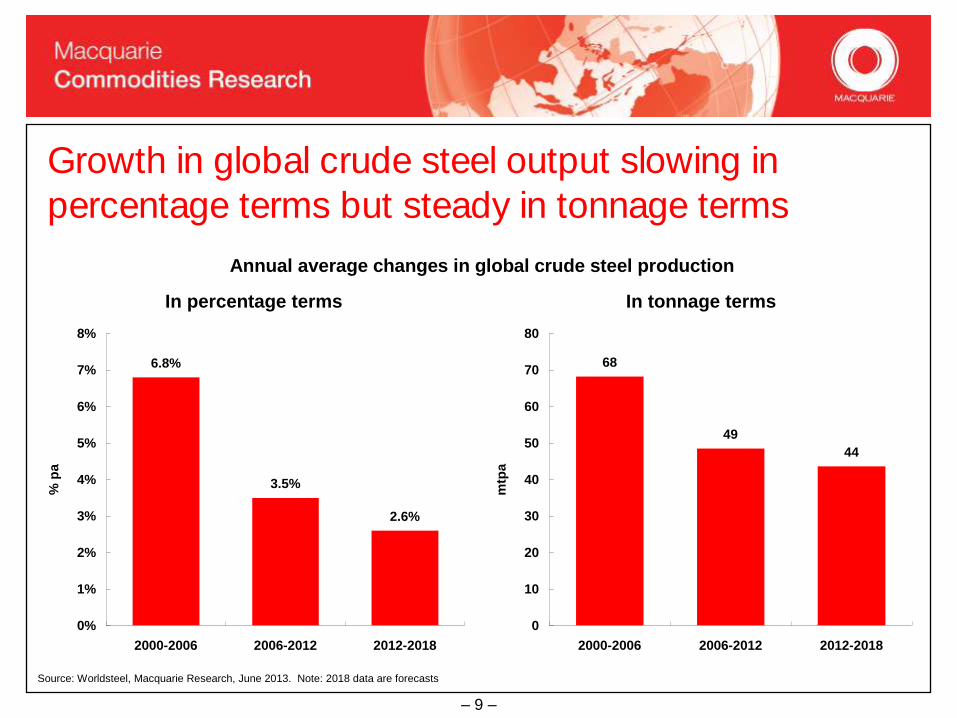

Growth in global crude steel output slowing in

percentage terms but steady in tonnage terms

Annual average changes in global crude steel production

In percentage terms

6.8%

3.5%

2.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2000-2006 2006-2012 2012-2018

% p

a

In tonnage terms

68

49

44

0

10

20

30

40

50

60

70

80

2000-2006 2006-2012 2012-2018

mtp

a

Source: Worldsteel, Macquarie Research, June 2013. Note: 2018 data are forecasts

– 10 –

Future steel production will be shaped by several

factors driving demand and supply

Demand-side drivers

Steel demand in populous developing countries

China, India and others

Emerging consumer class

Urbanisation and infrastructure development

Industrialistion

Scope for substitution into and out of steel

Construction

Automotive

Scope for thrifting in steel-based manufacturing

Lightweighting

Migration of steel-based manufacturing industry

Supply-side drivers

Consolidation of ownership and control

Backward integration into raw materials

De-integration of steelmaking and rolling, which

has advantages and disadvantages

Costs of iron and steelmaking, which vary widely

by country and region

Cost and availability of alternative raw materials

and energy supplies

Environmental and industrial policies

Change in iron and steelmaking technology

Source: Macquarie Research, June 2013

– 11 –

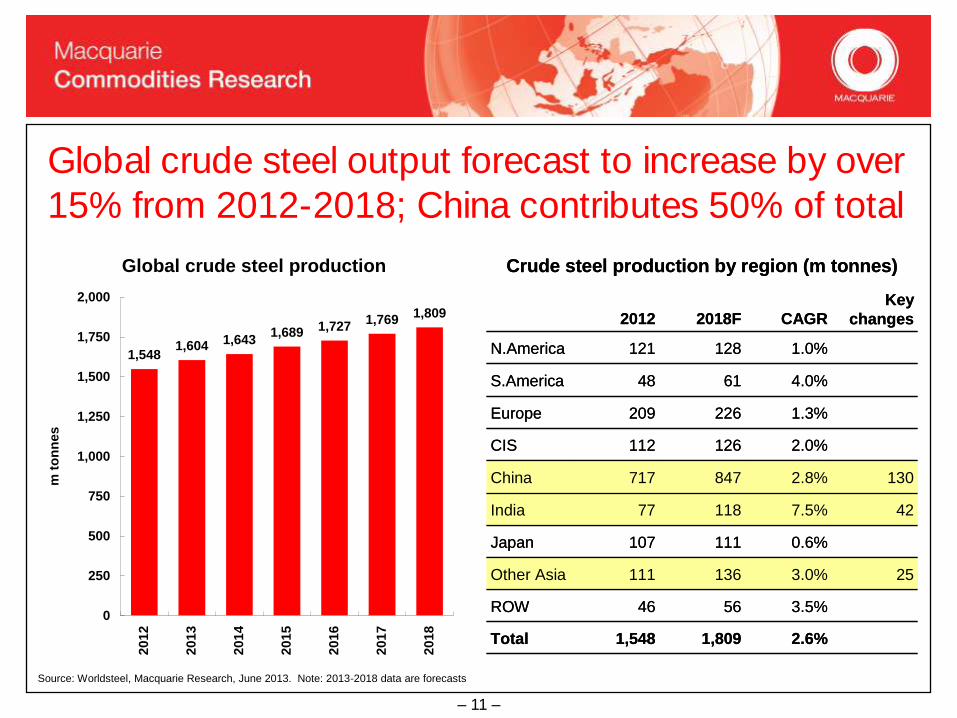

Global crude steel output forecast to increase by over

15% from 2012-2018; China contributes 50% of total

Global crude steel production

1,5481,604 1,643

1,689 1,7271,769

1,809

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2012

2013

2014

2015

2016

2017

2018

m t

on

nes

2.6%1,8091,548Total

3.5%5646ROW

253.0%136111Other Asia

0.6%111107Japan

427.5%11877India

1302.8%847717China

2.0%126112CIS

1.3%226209Europe

4.0%6148S.America

1.0%128121N.America

Key

changesCAGR2018F2012

Crude steel production by region (m tonnes)

2.6%1,8091,548Total

3.5%5646ROW

253.0%136111Other Asia

0.6%111107Japan

427.5%11877India

1302.8%847717China

2.0%126112CIS

1.3%226209Europe

4.0%6148S.America

1.0%128121N.America

Key

changesCAGR2018F2012

Crude steel production by region (m tonnes)

Source: Worldsteel, Macquarie Research, June 2013. Note: 2013-2018 data are forecasts

– 12 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

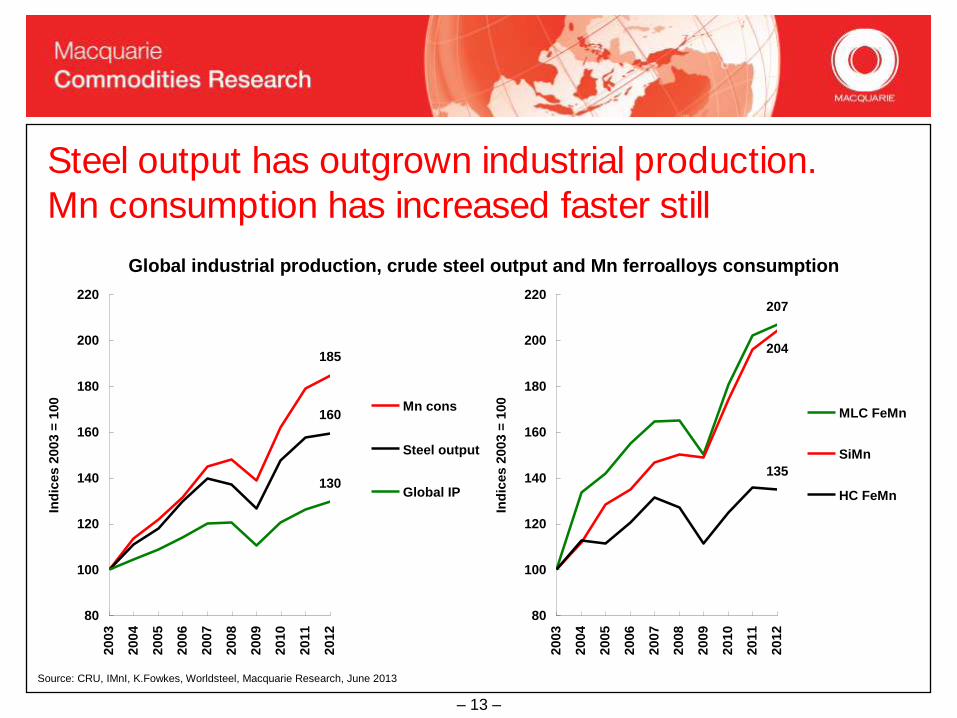

– 13 –

Steel output has outgrown industrial production.

Mn consumption has increased faster still

Global industrial production, crude steel output and Mn ferroalloys consumption

185

160

130

80

100

120

140

160

180

200

220

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ices 2

003 =

100 Mn cons

Steel

output

Global IP

Steel output

207

204

135

80

100

120

140

160

180

200

220

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ices 2

003 =

100

MLC FeMn

SiMn

HC FeMn

Source: CRU, IMnI, K.Fowkes, Worldsteel, Macquarie Research, June 2013

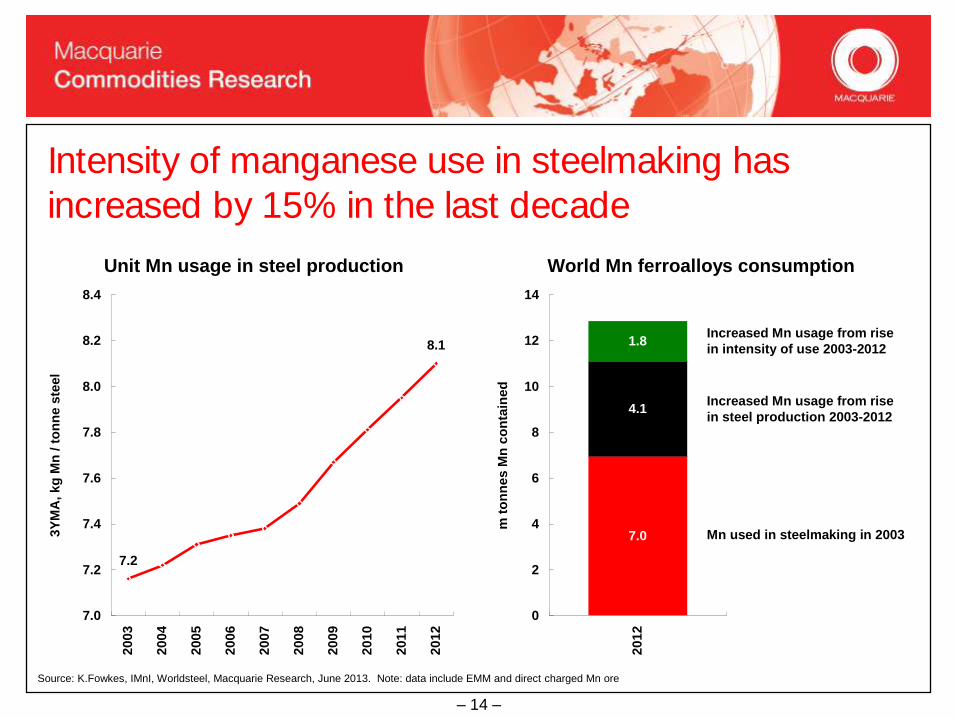

– 14 –

Intensity of manganese use in steelmaking has

increased by 15% in the last decade

Unit Mn usage in steel production

8.1

7.2

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

3Y

MA

, kg

Mn

/ t

on

ne s

teel

World Mn ferroalloys consumption

7.0

4.1

1.8

0

2

4

6

8

10

12

14

2012

m t

on

nes M

n c

on

tain

ed

Mn used in steelmaking in 2003

Increased Mn usage from rise

in steel production 2003-2012

Increased Mn usage from rise

in intensity of use 2003-2012

Source: K.Fowkes, IMnI, Worldsteel, Macquarie Research, June 2013. Note: data include EMM and direct charged Mn ore

– 15 –

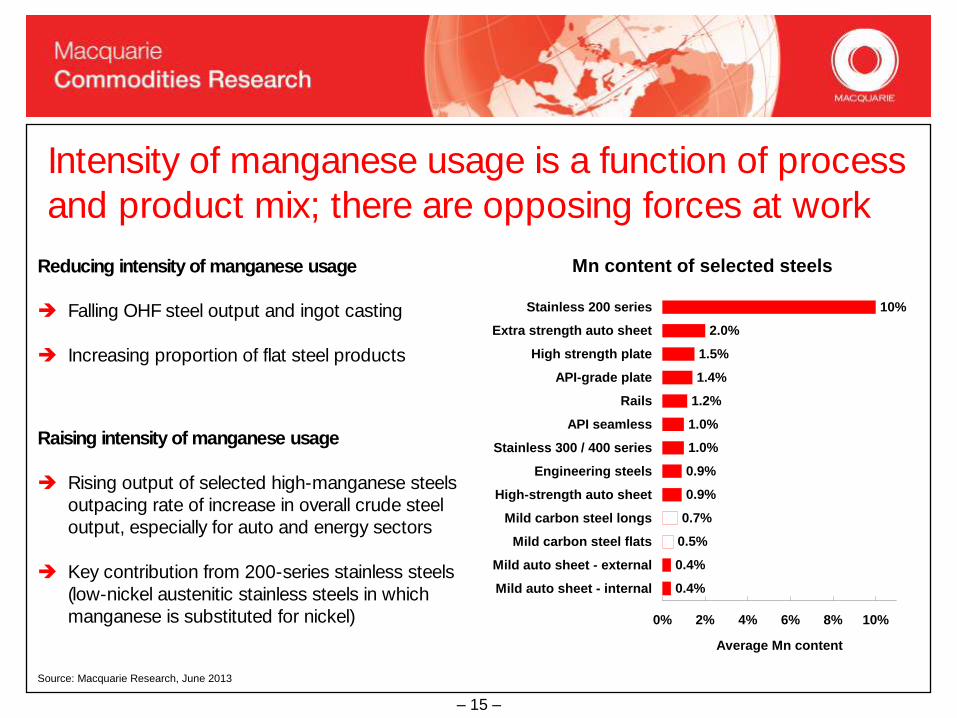

Intensity of manganese usage is a function of process

and product mix; there are opposing forces at work

Reducing intensity of manganese usage

Falling OHF steel output and ingot casting

Increasing proportion of flat steel products

Raising intensity of manganese usage

Rising output of selected high-manganese steels

outpacing rate of increase in overall crude steel

output, especially for auto and energy sectors

Key contribution from 200-series stainless steels

(low-nickel austenitic stainless steels in which

manganese is substituted for nickel)

Source: Macquarie Research, June 2013

Mn content of selected steels

2.0%

1.5%

1.4%

1.2%

1.0%

1.0%

0.9%

0.9%

0.7%

0.5%

0.4%

0.4%

10%

0% 2% 4% 6% 8% 10%

Stainless 200 series

Extra strength auto sheet

High strength plate

API-grade plate

Rails

API seamless

Stainless 300 / 400 series

Engineering steels

High-strength auto sheet

Mild carbon steel longs

Mild carbon steel flats

Mild auto sheet - external

Mild auto sheet - internal

Average Mn content

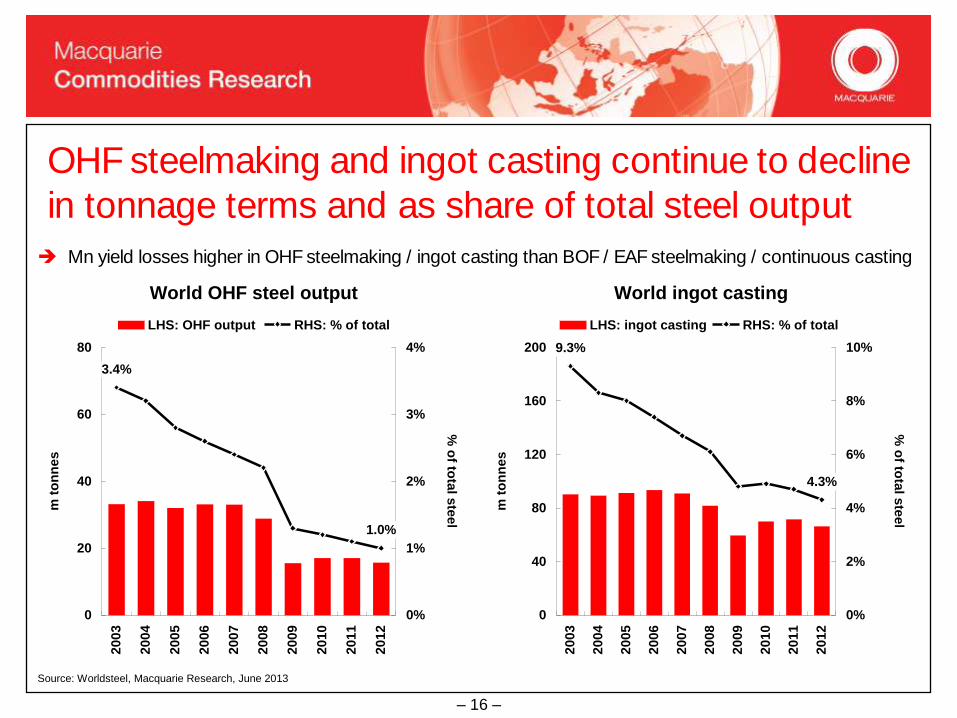

– 16 –

OHF steelmaking and ingot casting continue to decline

in tonnage terms and as share of total steel output

Source: Worldsteel, Macquarie Research, June 2013

Mn yield losses higher in OHF steelmaking / ingot casting than BOF / EAF steelmaking / continuous casting

World OHF steel output

1.0%

3.4%

0

20

40

60

80

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes

0%

1%

2%

3%

4%

% o

f tota

l ste

el

LHS: OHF output RHS: % of total

World ingot casting

4.3%

9.3%

0

40

80

120

160

200

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes

0%

2%

4%

6%

8%

10%

% o

f tota

l ste

el

LHS: ingot casting RHS: % of total

– 17 –

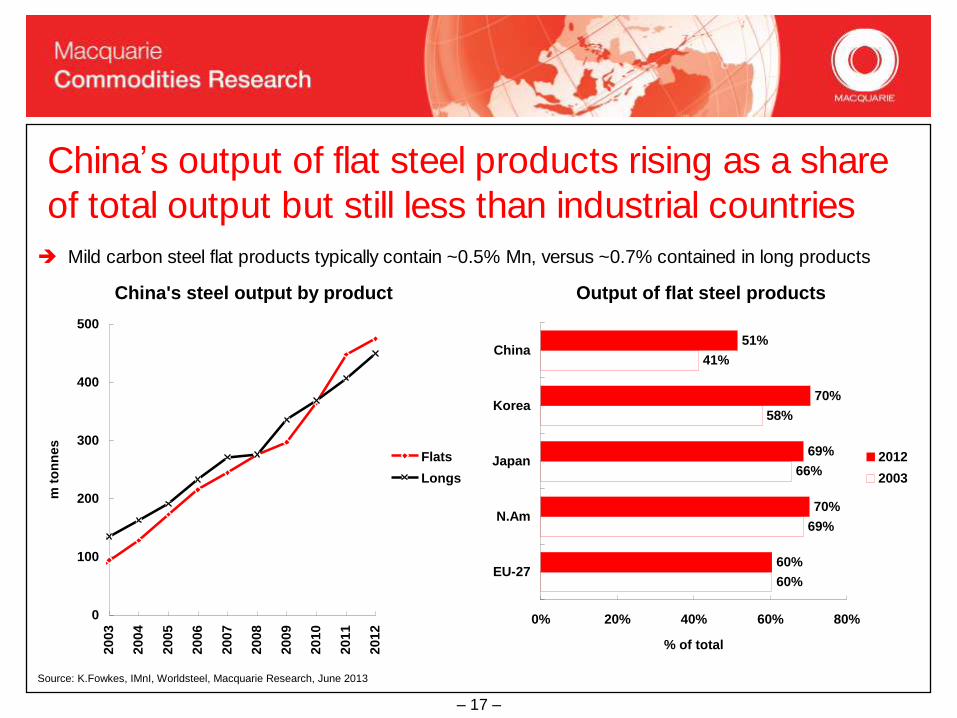

China’s output of flat steel products rising as a share

of total output but still less than industrial countries

Source: K.Fowkes, IMnI, Worldsteel, Macquarie Research, June 2013

Mild carbon steel flat products typically contain ~0.5% Mn, versus ~0.7% contained in long products

China's steel output by product

0

100

200

300

400

500

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes

Flats

Longs

Output of flat steel products

60%

69%

66%

58%

41%

60%

70%

69%

70%

51%

0% 20% 40% 60% 80%

EU-27

N.Am

Japan

Korea

China

% of total

2012

2003

– 18 –

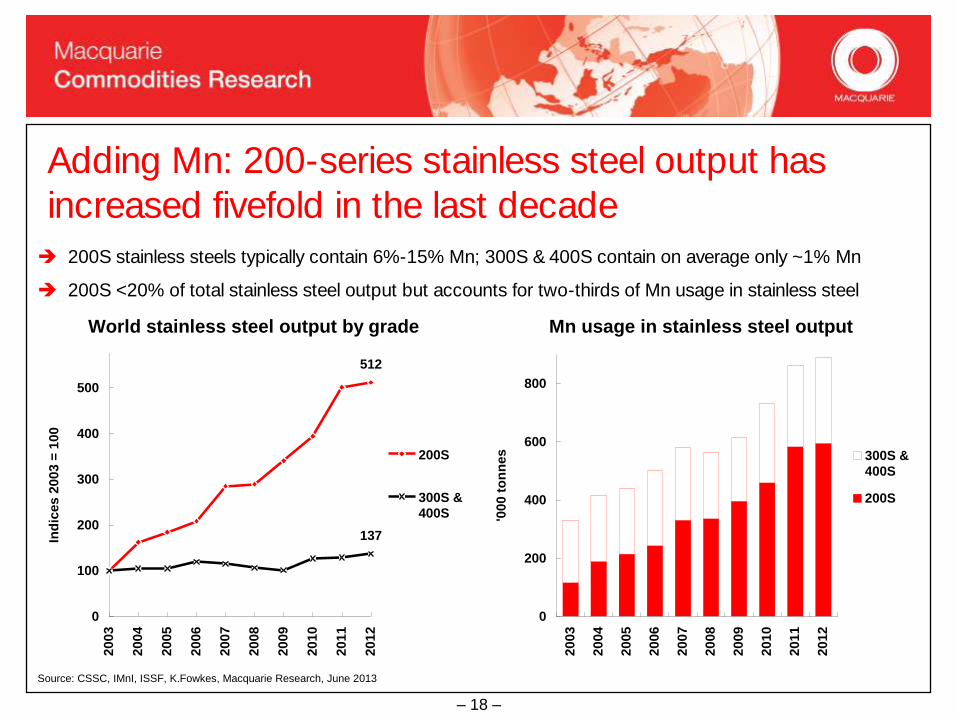

Adding Mn: 200-series stainless steel output has

increased fivefold in the last decade

200S stainless steels typically contain 6%-15% Mn; 300S & 400S contain on average only ~1% Mn

200S <20% of total stainless steel output but accounts for two-thirds of Mn usage in stainless steel

World stainless steel output by grade

512

137

0

100

200

300

400

500

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ices

20

03

= 1

00

200S

300S &

400S

Mn usage in stainless steel output

0

200

400

600

800

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

'00

0 t

on

ne

s 300S &

400S

200S

Source: CSSC, IMnI, ISSF, K.Fowkes, Macquarie Research, June 2013

– 19 –

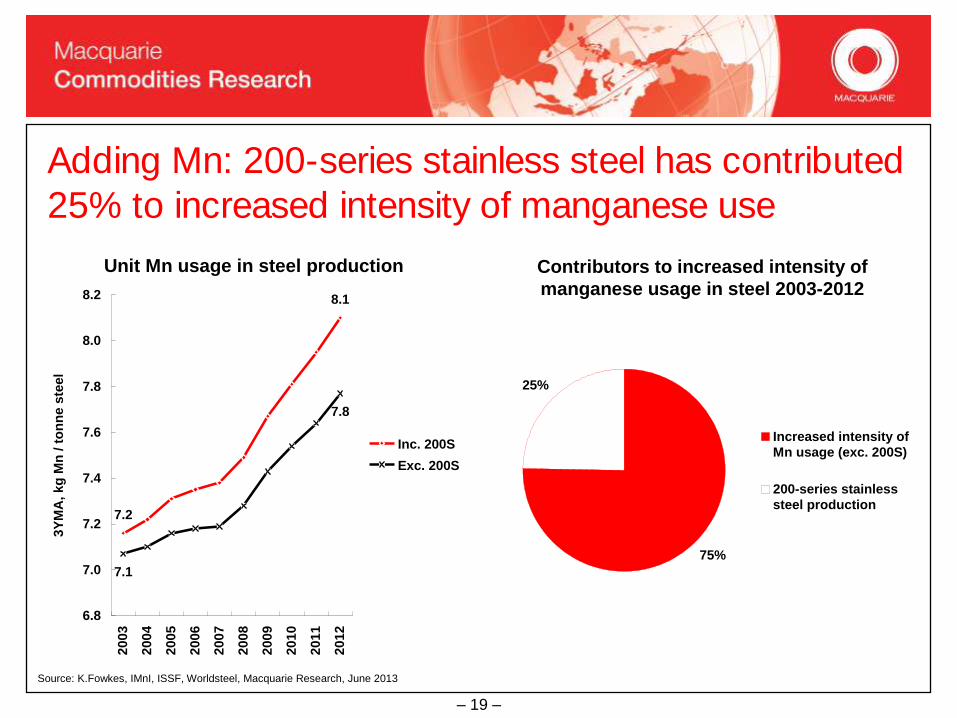

Adding Mn: 200-series stainless steel has contributed

25% to increased intensity of manganese use

Source: K.Fowkes, IMnI, ISSF, Worldsteel, Macquarie Research, June 2013

Unit Mn usage in steel production

7.2

8.1

7.8

7.1

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

3Y

MA

, kg

Mn

/ t

on

ne s

teel

Inc. 200S

Exc. 200S

Title

75%

25%

Increased intensity of

Mn usage (exc. 200S)

200-series stainless

steel production

Contributors to increased intensity of

manganese usage in steel 2003-2012

– 20 –

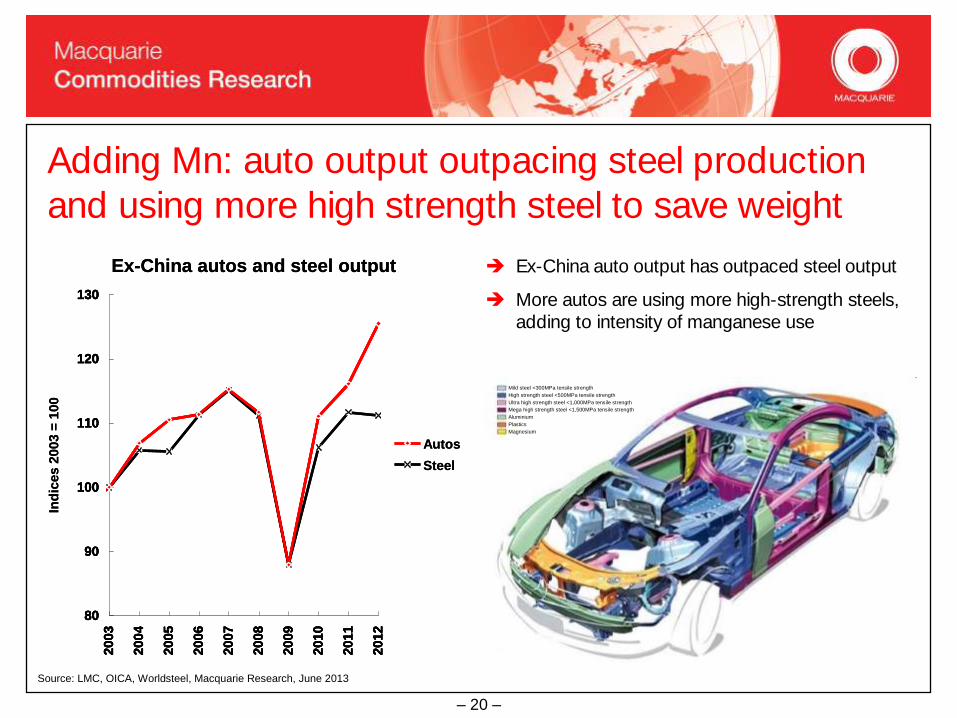

Adding Mn: auto output outpacing steel production

and using more high strength steel to save weight

Ex-China autos and steel output

80

90

100

110

120

130

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ices 2

003 =

100

Autos

Steel

80

90

100

110

120

130

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ex-China autos and steel output

80

90

100

110

120

130

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ices 2

003 =

100

Autos

Steel

80

90

100

110

120

130

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ex-China auto output has outpaced steel output

More autos are using more high-strength steels,

adding to intensity of manganese use

Mild steel <300MPa tensile strength

High strength steel <500MPa tensile strength

Ultra high strength steel <1,000MPa tensile strength

Mega high strength steel <1,500MPa tensile strength

Aluminium

Plastics

Magnesium

Mild steel <300MPa tensile strength

High strength steel <500MPa tensile strength

Ultra high strength steel <1,000MPa tensile strength

Mega high strength steel <1,500MPa tensile strength

Aluminium

Plastics

Magnesium

Source: LMC, OICA, Worldsteel, Macquarie Research, June 2013

– 21 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 22 –

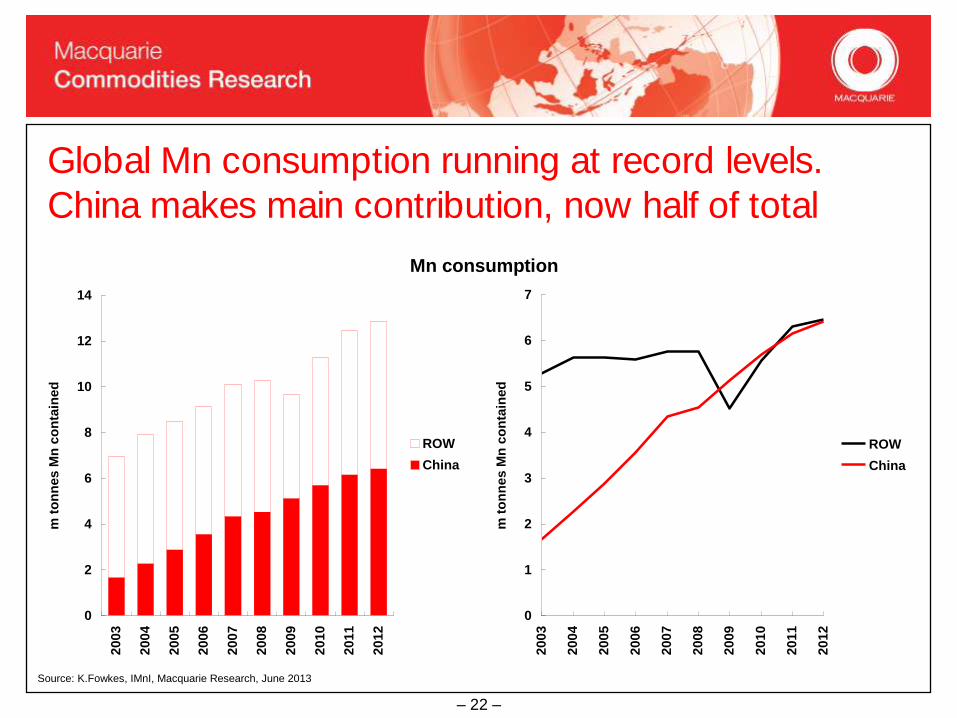

Global Mn consumption running at record levels.

China makes main contribution, now half of total

Mn consumption

0

2

4

6

8

10

12

14

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes M

n c

on

tain

ed

ROW

China

0

1

2

3

4

5

6

7

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes M

n c

on

tain

ed

ROW

China

Source: K.Fowkes, IMnI, Macquarie Research, June 2013

– 23 –

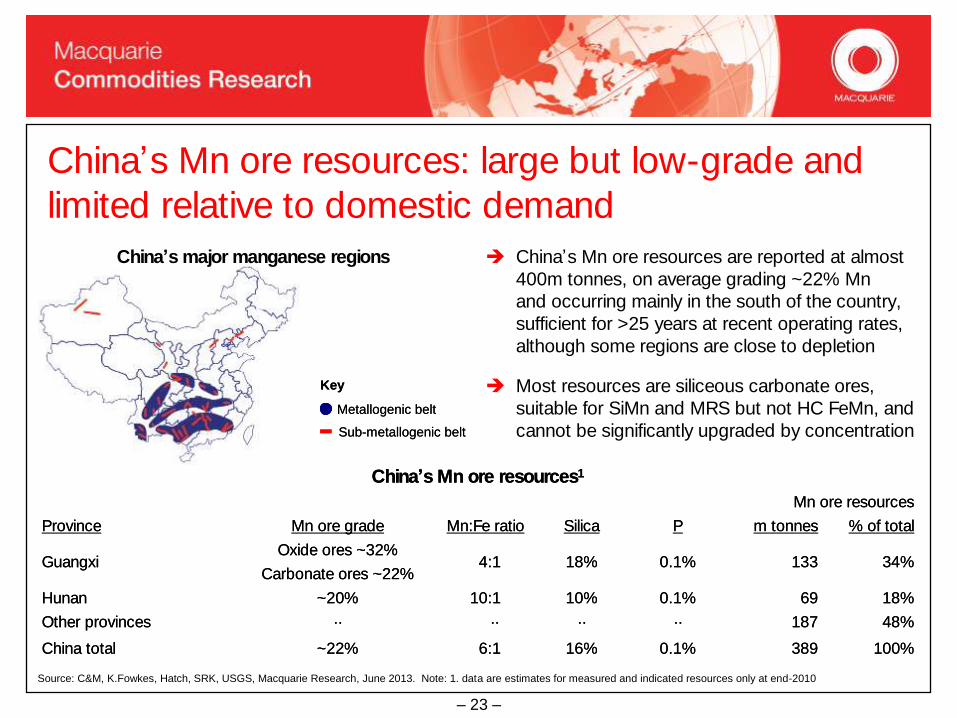

China’s Mn ore resources: large but low-grade and

limited relative to domestic demand

China’s major manganese regions

Key

Metallogenic belt

Sub-metallogenic belt

Key

Metallogenic belt

Sub-metallogenic belt

China’s Mn ore resources are reported at almost

400m tonnes, on average grading ~22% Mn

and occurring mainly in the south of the country,

sufficient for >25 years at recent operating rates,

although some regions are close to depletion

Most resources are siliceous carbonate ores,

suitable for SiMn and MRS but not HC FeMn, and

cannot be significantly upgraded by concentration

Mn ore resources

% of totalm tonnesPSilicaMn:Fe ratioMn ore gradeProvince

100%3890.1%16%06:1~22%China total

48%187········Other provinces

18%690.1%10%10:1~20%Hunan

Carbonate ores ~22%34%1330.1%18%04:1

Oxide ores ~32%Guangxi

China’s Mn ore resources1

Mn ore resources

% of totalm tonnesPSilicaMn:Fe ratioMn ore gradeProvince

100%3890.1%16%06:1~22%China total

48%187········Other provinces

18%690.1%10%10:1~20%Hunan

Carbonate ores ~22%34%1330.1%18%04:1

Oxide ores ~32%Guangxi

China’s Mn ore resources1

Source: C&M, K.Fowkes, Hatch, SRK, USGS, Macquarie Research, June 2013. Note: 1. data are estimates for measured and indicated resources only at end-2010

– 24 –

China’s Mn ore imports have increased fourfold in

last decade; now supply 60% of local consumption

China's Mn ore imports by country

0

2

4

6

8

10

12

14

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes g

ross w

eig

ht

ROW

MMR

BRA

GAB

ZAF

AUS

China's Mn consumption

0%

20%

40%

60%

80%

100%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

3Y

MA

% o

f to

tal, b

asis

Mn

co

nta

ined

Imported

Mn ore

Local mine

output

Source: China Customs, K.Fowkes, IMnI, Macquarie Research, June 2013

– 25 –

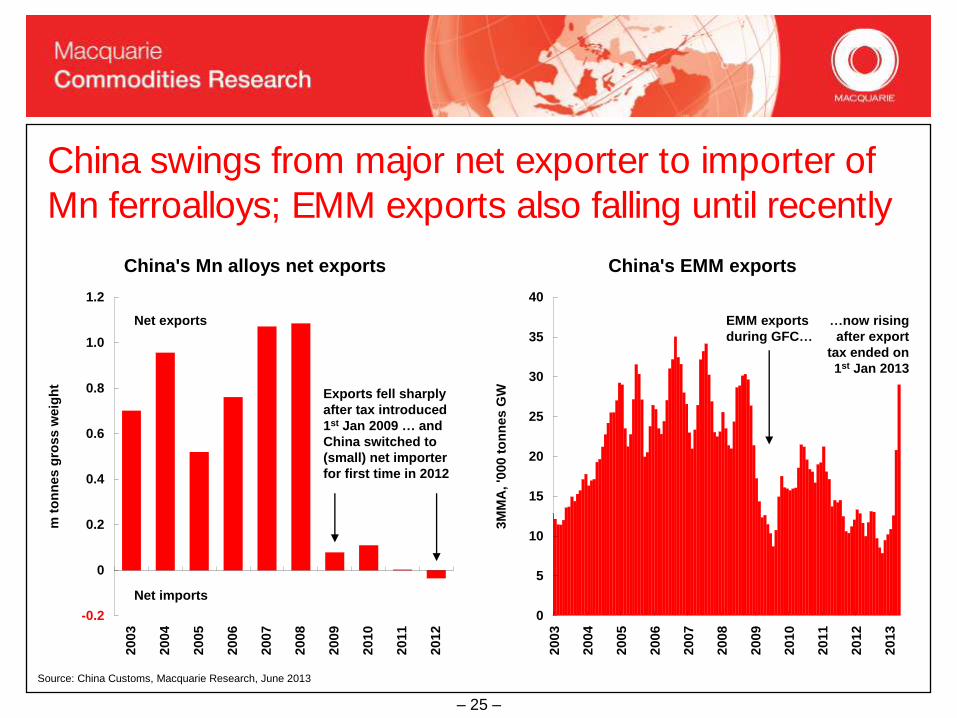

China swings from major net exporter to importer of

Mn ferroalloys; EMM exports also falling until recently

China's Mn alloys net exports

-0.2

0

0.2

0.4

0.6

0.8

1.0

1.2

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes g

ross w

eig

ht

Net exports

Net imports

Exports fell sharply

after tax introduced

1st Jan 2009 … and

China switched to

(small) net importer

for first time in 2012

China's EMM exports

0

5

10

15

20

25

30

35

40

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

3M

MA

, '0

00 t

on

nes G

W

EMM exports

during GFC…

…now rising

after export

tax ended on

1st Jan 2013

Source: China Customs, Macquarie Research, June 2013

– 26 –

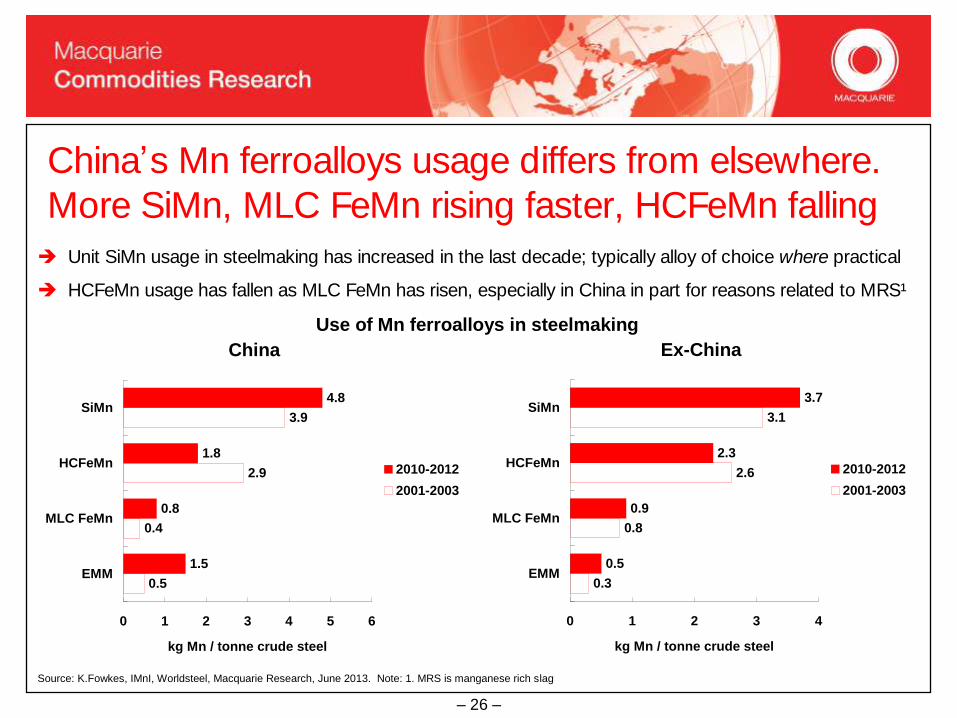

China’s Mn ferroalloys usage differs from elsewhere.

More SiMn, MLC FeMn rising faster, HCFeMn falling

Unit SiMn usage in steelmaking has increased in the last decade; typically alloy of choice where practical

HCFeMn usage has fallen as MLC FeMn has risen, especially in China in part for reasons related to MRS¹

Use of Mn ferroalloys in steelmaking

China

4.8

1.8

0.8

1.5

3.9

2.9

0.4

0.5

0 1 2 3 4 5 6

SiMn

HCFeMn

MLC FeMn

EMM

kg Mn / tonne crude steel

2010-2012

2001-2003

Ex-China

3.7

2.3

0.9

0.5

3.1

2.6

0.8

0.3

0 1 2 3 4

SiMn

HCFeMn

MLC FeMn

EMM

kg Mn / tonne crude steel

2010-2012

2001-2003

Source: K.Fowkes, IMnI, Worldsteel, Macquarie Research, June 2013. Note: 1. MRS is manganese rich slag

– 27 –

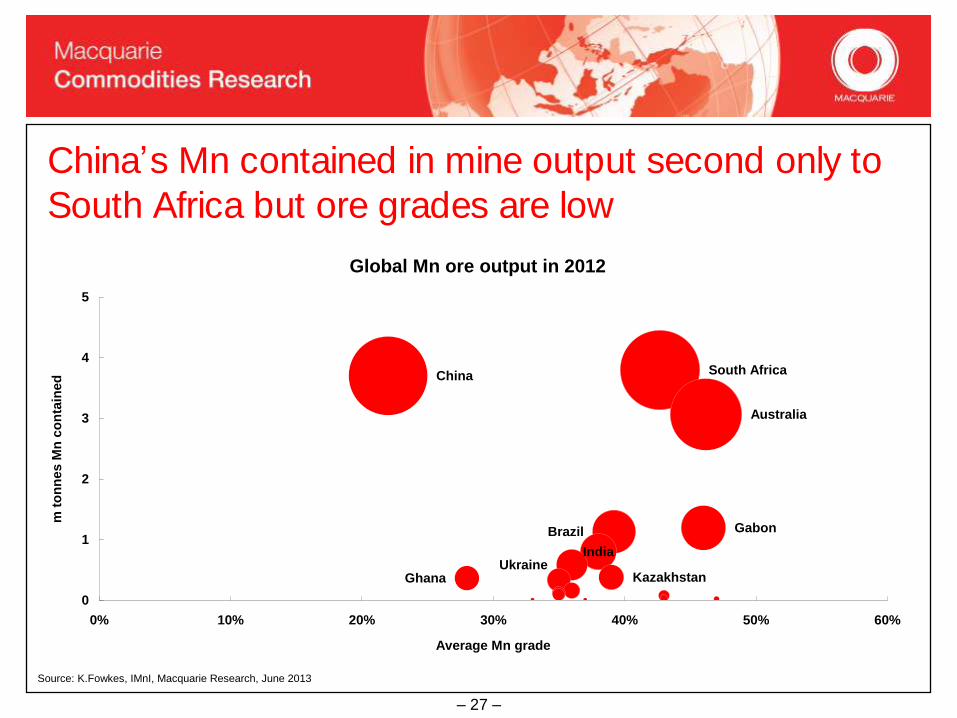

China’s Mn contained in mine output second only to

South Africa but ore grades are low

Global Mn ore output in 2012

KazakhstanUkraine

India

Brazil

Ghana

Gabon

Australia

South AfricaChina

0

1

2

3

4

5

0% 10% 20% 30% 40% 50% 60%

Average Mn grade

m t

on

nes M

n c

on

tain

ed

Source: K.Fowkes, IMnI, Macquarie Research, June 2013

– 28 –

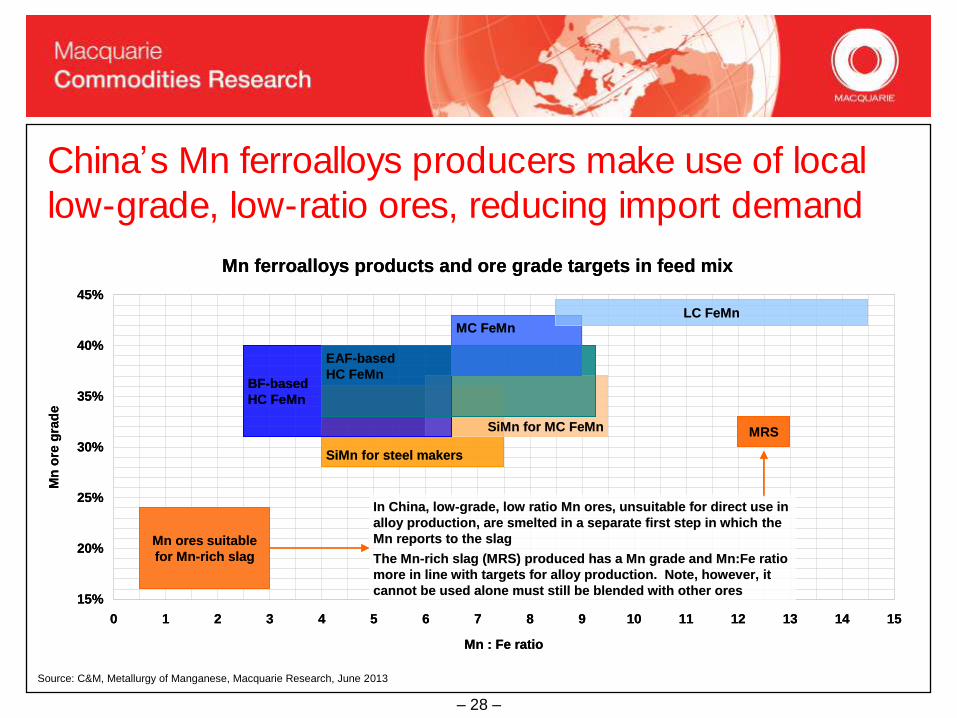

China’s Mn ferroalloys producers make use of local

low-grade, low-ratio ores, reducing import demand

Mn ferroalloys products and ore grade targets in feed mix

15%

20%

25%

30%

35%

40%

45%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Mn : Fe ratio

Mn

ore

gra

de

Mn ores suitable

for Mn-rich slag

SiMn for steel makers

SiMn for MC FeMn

BF-based

HC FeMn

EAF-based

HC FeMn

MC FeMnLC FeMn

MRS

In China, low-grade, low ratio Mn ores, unsuitable for direct use in

alloy production, are smelted in a separate first step in which the

Mn reports to the slag

The Mn-rich slag (MRS) produced has a Mn grade and Mn:Fe ratio

more in line with targets for alloy production. Note, however, it

cannot be used alone must still be blended with other ores

Mn ferroalloys products and ore grade targets in feed mix

15%

20%

25%

30%

35%

40%

45%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Mn : Fe ratio

Mn

ore

gra

de

Mn ores suitable

for Mn-rich slag

SiMn for steel makers

SiMn for MC FeMn

BF-based

HC FeMn

EAF-based

HC FeMn

MC FeMnLC FeMn

MRS

In China, low-grade, low ratio Mn ores, unsuitable for direct use in

alloy production, are smelted in a separate first step in which the

Mn reports to the slag

The Mn-rich slag (MRS) produced has a Mn grade and Mn:Fe ratio

more in line with targets for alloy production. Note, however, it

cannot be used alone must still be blended with other ores

Source: C&M, Metallurgy of Manganese, Macquarie Research, June 2013

– 29 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 30 –

Mn use in steelmaking – a summary

Source: Hatch, K.Fowkes, Macquarie Research, June 2013

Mn has two main uses in modern steelmaking

1. As an alloying agent

Mn increases tensile strength, hardness, toughness, wear resistance and machinability

2. To "fix" residual sulphur

No substitutes and essential in all steelmaking but use reduced by adoption of hot metal

desulphurisation as standard practice today

Mn ferroalloy(s) and amount used are a function of three main factors

1. The aim chemistry of the finished steel product

Mn content allied to carbon and silicon control. Flat steel products typically lower in carbon than

long steel products. Silicon control important in surface critical flat products

2. Steelmaking process and practice, which affect efficiency in achieving aim chemistry

No significant difference between BF / BOF and EAF steelmaking, except where bottom-stirring

used to reduce carbon on tapping in primary steelmaking

3. Cost of alternative alloying additions within constraints of aim chemistry and steel plant design

Configuration of hoppers feeding furnaces

– 31 –

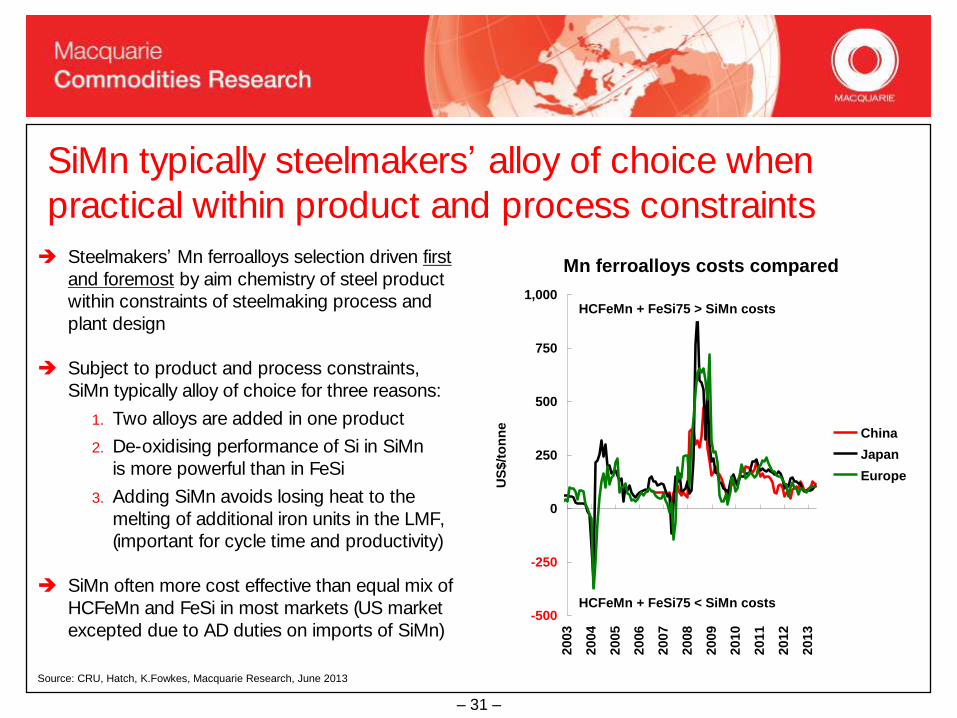

SiMn typically steelmakers’ alloy of choice when

practical within product and process constraints

Steelmakers’ Mn ferroalloys selection driven first

and foremost by aim chemistry of steel product

within constraints of steelmaking process and

plant design

Subject to product and process constraints,

SiMn typically alloy of choice for three reasons:

1. Two alloys are added in one product

2. De-oxidising performance of Si in SiMn

is more powerful than in FeSi

3. Adding SiMn avoids losing heat to the

melting of additional iron units in the LMF,

(important for cycle time and productivity)

SiMn often more cost effective than equal mix of

HCFeMn and FeSi in most markets (US market

excepted due to AD duties on imports of SiMn)

Source: CRU, Hatch, K.Fowkes, Macquarie Research, June 2013

Mn ferroalloys costs compared

-500

-250

0

250

500

750

1,000

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

US

$/t

on

ne

China

Japan

Europe

HCFeMn + FeSi75 > SiMn costs

HCFeMn + FeSi75 < SiMn costs

– 32 –

Future shifts in steel product mix may alter balance of

Mn ferroalloys used by steelmakers

Source: Hatch, K.Fowkes, Macquarie Research, June 2013

Forecasts of an increasing uptake of higher strength, higher manganese steels in certain applications,

especially auto and energy steels, may see steelmakers seek adaptations and / or new products in

Mn ferroalloys

Products that mix better and melt faster with greater consistency in sizing and alloy chemistry.

Melting speed is important for cycle time. Mn recovery from ferroalloy to steel is a function of

steelmaking practice but also alloy quality; consistent recovery reduces risk of “off-spec” steel

Higher Mn grade to reduce volume additions required and resultant drop in steel temperature,

with positive implications for cycle time, productivity and cost control

Lower content of carbon and deleterious residuals, notably hydrogen, nitrogen, phosphorous

In future, steelmakers may consider melting Mn ferroalloys to add in liquid form at tapping and in the

LMF with the advantages this would be easier to add to the liquid steel stream and reduce energy use.

This is already practiced by some stainless and speciality steelmakers

– 33 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 34 –

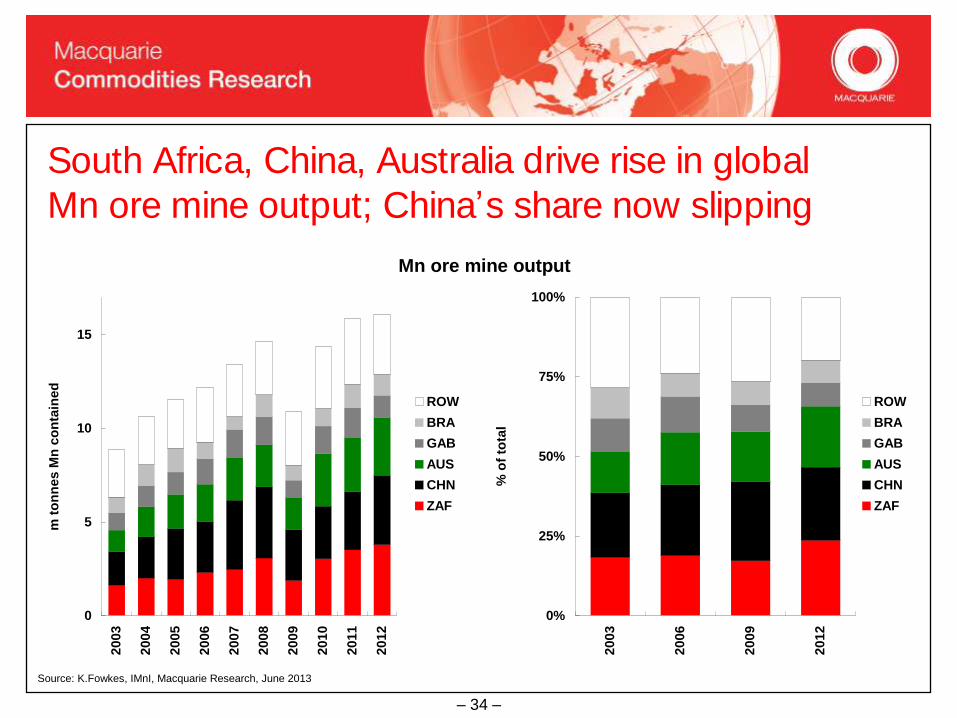

South Africa, China, Australia drive rise in global

Mn ore mine output; China’s share now slipping

Mn ore mine output

0

5

10

15

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

m t

on

nes M

n c

on

tain

ed

ROW

BRA

GAB

AUS

CHN

ZAF

0%

25%

50%

75%

100%

2003

2006

2009

2012

% o

f to

tal

ROW

BRA

GAB

AUS

CHN

ZAF

Source: K.Fowkes, IMnI, Macquarie Research, June 2013

– 35 –

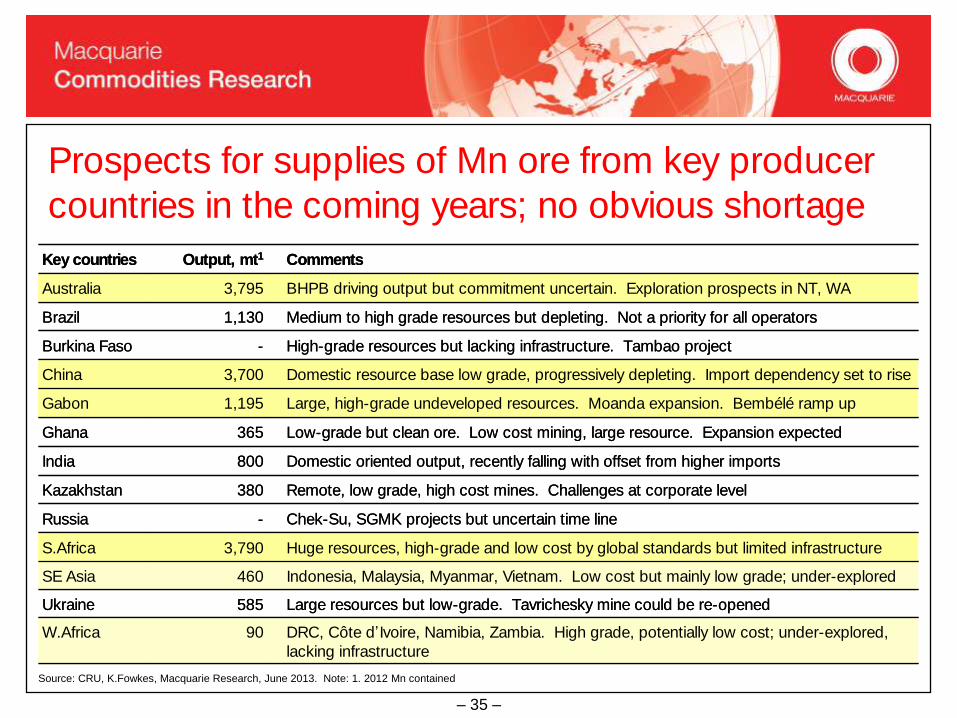

Prospects for supplies of Mn ore from key producer

countries in the coming years; no obvious shortage

Indonesia, Malaysia, Myanmar, Vietnam. Low cost but mainly low grade; under-explored460SE Asia

Low-grade but clean ore. Low cost mining, large resource. Expansion expected365Ghana

Large resources but low-grade. Tavrichesky mine could be re-opened585Ukraine

DRC, Côte d’Ivoire, Namibia, Zambia. High grade, potentially low cost; under-explored,

lacking infrastructure

90W.Africa

Huge resources, high-grade and low cost by global standards but limited infrastructure 3,790S.Africa

Chek-Su, SGMK projects but uncertain time line-Russia

Remote, low grade, high cost mines. Challenges at corporate level380Kazakhstan

Domestic oriented output, recently falling with offset from higher imports800India

Large, high-grade undeveloped resources. Moanda expansion. Bembélé ramp up1,195Gabon

Domestic resource base low grade, progressively depleting. Import dependency set to rise3,700China

High-grade resources but lacking infrastructure. Tambao project-Burkina Faso

Medium to high grade resources but depleting. Not a priority for all operators1,130Brazil

BHPB driving output but commitment uncertain. Exploration prospects in NT, WA3,795Australia

CommentsOutput, mt1Key countries

Indonesia, Malaysia, Myanmar, Vietnam. Low cost but mainly low grade; under-explored460SE Asia

Low-grade but clean ore. Low cost mining, large resource. Expansion expected365Ghana

Large resources but low-grade. Tavrichesky mine could be re-opened585Ukraine

DRC, Côte d’Ivoire, Namibia, Zambia. High grade, potentially low cost; under-explored,

lacking infrastructure

90W.Africa

Huge resources, high-grade and low cost by global standards but limited infrastructure 3,790S.Africa

Chek-Su, SGMK projects but uncertain time line-Russia

Remote, low grade, high cost mines. Challenges at corporate level380Kazakhstan

Domestic oriented output, recently falling with offset from higher imports800India

Large, high-grade undeveloped resources. Moanda expansion. Bembélé ramp up1,195Gabon

Domestic resource base low grade, progressively depleting. Import dependency set to rise3,700China

High-grade resources but lacking infrastructure. Tambao project-Burkina Faso

Medium to high grade resources but depleting. Not a priority for all operators1,130Brazil

BHPB driving output but commitment uncertain. Exploration prospects in NT, WA3,795Australia

CommentsOutput, mt1Key countries

Source: CRU, K.Fowkes, Macquarie Research, June 2013. Note: 1. 2012 Mn contained

– 36 –

S.Africa’s infrastructure for Mn ore exports is limited.

Long lead times to expand (limiting supply meanwhile)

More expensive

Transnet’s preferred option. ZAR2.7bn first phase approved by

TRF CEO in May. Ambitious target to reach 12mtpa by mid-2017.

However, industry worries over cost estimated at ~ZAR11bn.

Local Mn ferroalloys smelter unlikely to be built

10m–16m tpaCoega by rail

Trucking to Richards Bay up to ~15% more expensive than to

Durban. Mn ore exports must compete with (increasing) chrome

ore and iron ore shipments and volumes are falling

~1m tpaRichards Bay by road

BMA terminal is expanding and offers option of container shipping.

Rail access increasing but some road haulage still required and

remains expensive (~US$1.80-1.90/dmtu for "low" grade ore)

3m–4m tpaDurban by rail and road

Transnet is no longer considering allocation of capacity for

Mn ore shipments in the next Sishen–Saldanha Bay rail expansion.

New capacity will not be available before 2016/17 in any case

~13m tpaSaldanha Bay by rail

Previous commitment to discontinue exports through

Port Elizabeth by 2016 now looks unlikely before 2017-18.

Rail allocation among competing producers in the meantime

still to be decided

5.5m tpaPort Elizabeth by rail

Less expensiveLatest statusCapacityRoute

More expensive

Transnet’s preferred option. ZAR2.7bn first phase approved by

TRF CEO in May. Ambitious target to reach 12mtpa by mid-2017.

However, industry worries over cost estimated at ~ZAR11bn.

Local Mn ferroalloys smelter unlikely to be built

10m–16m tpaCoega by rail

Trucking to Richards Bay up to ~15% more expensive than to

Durban. Mn ore exports must compete with (increasing) chrome

ore and iron ore shipments and volumes are falling

~1m tpaRichards Bay by road

BMA terminal is expanding and offers option of container shipping.

Rail access increasing but some road haulage still required and

remains expensive (~US$1.80-1.90/dmtu for "low" grade ore)

3m–4m tpaDurban by rail and road

Transnet is no longer considering allocation of capacity for

Mn ore shipments in the next Sishen–Saldanha Bay rail expansion.

New capacity will not be available before 2016/17 in any case

~13m tpaSaldanha Bay by rail

Previous commitment to discontinue exports through

Port Elizabeth by 2016 now looks unlikely before 2017-18.

Rail allocation among competing producers in the meantime

still to be decided

5.5m tpaPort Elizabeth by rail

Less expensiveLatest statusCapacityRoute

Source: Assmang, Macquarie Research, June 2013

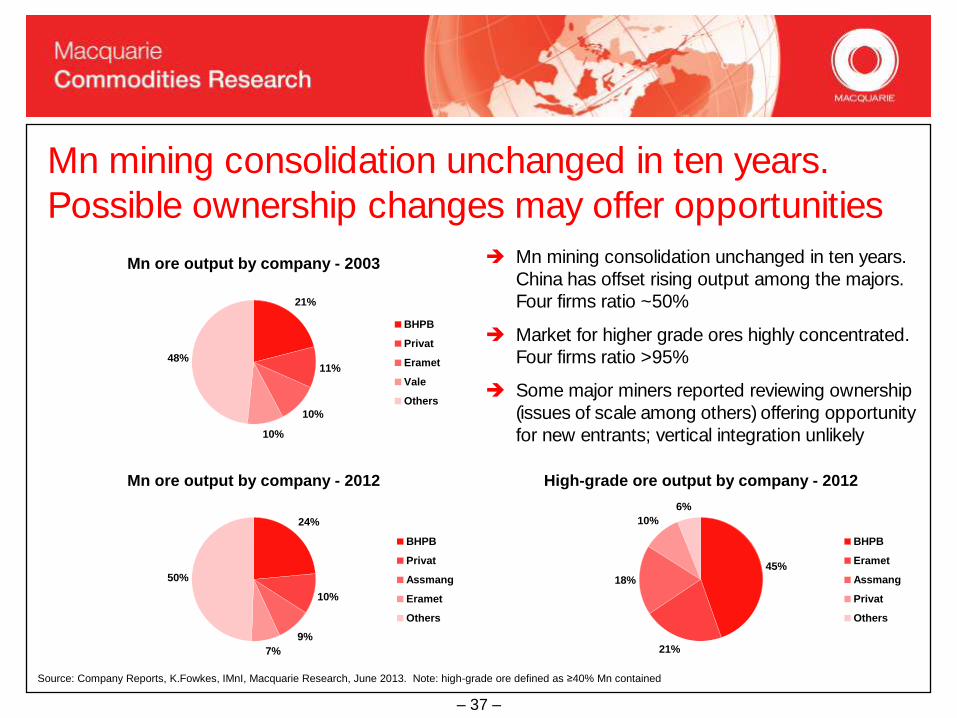

– 37 –

Source: Company Reports, K.Fowkes, IMnI, Macquarie Research, June 2013. Note: high-grade ore defined as ≥40% Mn contained

Mn mining consolidation unchanged in ten years.

Possible ownership changes may offer opportunities

Mn ore output by company - 2003

21%

11%

10%

10%

48%

BHPB

Privat

Eramet

Vale

Others

Mn ore output by company - 2012

24%

10%

9%

7%

50%

BHPB

Privat

Assmang

Eramet

Others

Mn mining consolidation unchanged in ten years.

China has offset rising output among the majors.

Four firms ratio ~50%

Market for higher grade ores highly concentrated.

Four firms ratio >95%

Some major miners reported reviewing ownership

(issues of scale among others) offering opportunity

for new entrants; vertical integration unlikely

High-grade ore output by company - 2012

45%

21%

18%

10%

6%

BHPB

Eramet

Assmang

Privat

Others

– 38 –

The manganese industry worldwide

– trends and opportunities

Global steel production and future prospects

Intensity of manganese usage in steelmaking

China’s role as manganese consumer and producer

Selection and use of manganese ferroalloys in steelmaking

Manganese ore supply

Summary and conclusions

– 39 –

The manganese industry worldwide

– trends and opportunities

Summary and conclusions

Global steel output running at record levels. Prospects for further increases promising

driven by urbanisation and additions to auto fleet, especially in China

Intensity of manganese use in steelmaking has been rising and likely to continue albeit at

probably more moderate rate (scope for further efficiency gains reduced)

Don’t doubt demand side potential for manganese!!

China likely to remain world’s largest consumer of manganese for many years yet and

import dependence likely to increase with local resources relatively limited

Steelmakers demands of Mn ferroalloys likely to continue changing but with

SiMn remaining alloy of choice subject to product / process constraints

Sufficient supply in prospect to meet demand into second half of decade, despite

South African infrastructure constraints. Longer term expansion with care

– 40 –

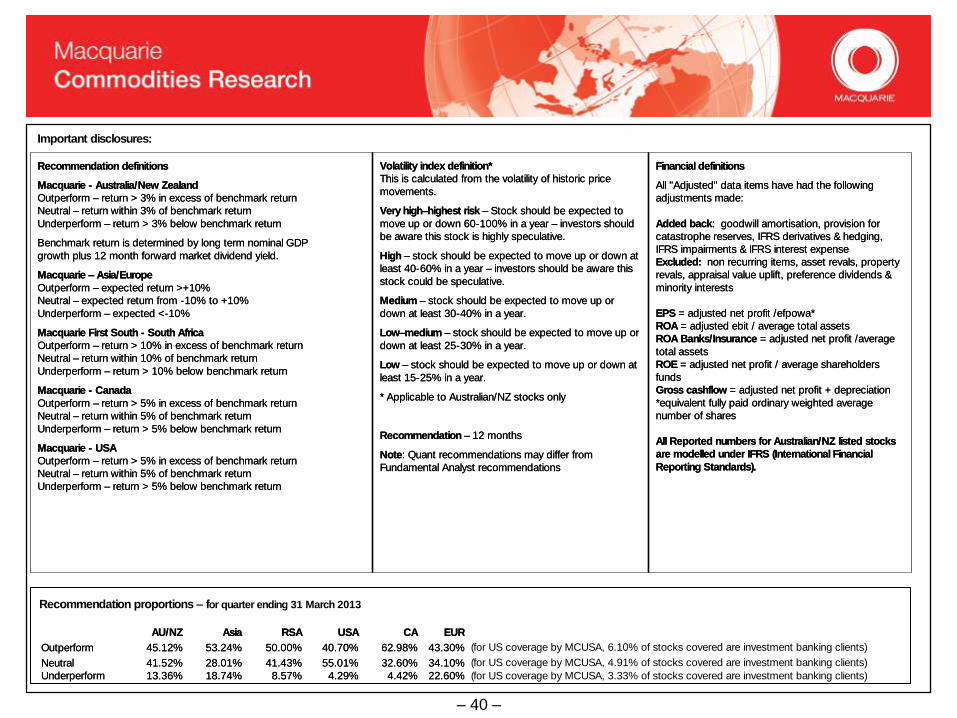

Important disclosures:

Financial definitions

All "Adjusted" data items have had the following

adjustments made:

Added back: goodwill amortisation, provision for

catastrophe reserves, IFRS derivatives & hedging,

IFRS impairments & IFRS interest expense

Excluded: non recurring items, asset revals, property

revals, appraisal value uplift, preference dividends &

minority interests

EPS = adjusted net profit /efpowa*

ROA = adjusted ebit / average total assets

ROA Banks/Insurance = adjusted net profit /average

total assets

ROE = adjusted net profit / average shareholders

funds

Gross cashflow = adjusted net profit + depreciation

*equivalent fully paid ordinary weighted average

number of shares

All Reported numbers for Australian/NZ listed stocks

are modelled under IFRS (International Financial

Reporting Standards).

Volatility index definition*

This is calculated from the volatility of historic price

movements.

Very high–highest risk – Stock should be expected to

move up or down 60-100% in a year – investors should

be aware this stock is highly speculative.

High – stock should be expected to move up or down at

least 40-60% in a year – investors should be aware this

stock could be speculative.

Medium – stock should be expected to move up or

down at least 30-40% in a year.

Low–medium – stock should be expected to move up or

down at least 25-30% in a year.

Low – stock should be expected to move up or down at

least 15-25% in a year.

* Applicable to Australian/NZ stocks only

Recommendation – 12 months

Note: Quant recommendations may differ from

Fundamental Analyst recommendations

Recommendation definitions

Macquarie - Australia/New Zealand

Outperform – return > 3% in excess of benchmark return

Neutral – return within 3% of benchmark return

Underperform – return > 3% below benchmark return

Benchmark return is determined by long term nominal GDP

growth plus 12 month forward market dividend yield.

Macquarie – Asia/Europe

Outperform – expected return >+10%

Neutral – expected return from -10% to +10%

Underperform – expected <-10%

Macquarie First South - South Africa

Outperform – return > 10% in excess of benchmark return

Neutral – return within 10% of benchmark return

Underperform – return > 10% below benchmark return

Macquarie - Canada

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Macquarie - USA

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Financial definitions

All "Adjusted" data items have had the following

adjustments made:

Added back: goodwill amortisation, provision for

catastrophe reserves, IFRS derivatives & hedging,

IFRS impairments & IFRS interest expense

Excluded: non recurring items, asset revals, property

revals, appraisal value uplift, preference dividends &

minority interests

EPS = adjusted net profit /efpowa*

ROA = adjusted ebit / average total assets

ROA Banks/Insurance = adjusted net profit /average

total assets

ROE = adjusted net profit / average shareholders

funds

Gross cashflow = adjusted net profit + depreciation

*equivalent fully paid ordinary weighted average

number of shares

All Reported numbers for Australian/NZ listed stocks

are modelled under IFRS (International Financial

Reporting Standards).

Volatility index definition*

This is calculated from the volatility of historic price

movements.

Very high–highest risk – Stock should be expected to

move up or down 60-100% in a year – investors should

be aware this stock is highly speculative.

High – stock should be expected to move up or down at

least 40-60% in a year – investors should be aware this

stock could be speculative.

Medium – stock should be expected to move up or

down at least 30-40% in a year.

Low–medium – stock should be expected to move up or

down at least 25-30% in a year.

Low – stock should be expected to move up or down at

least 15-25% in a year.

* Applicable to Australian/NZ stocks only

Recommendation – 12 months

Note: Quant recommendations may differ from

Fundamental Analyst recommendations

Recommendation definitions

Macquarie - Australia/New Zealand

Outperform – return > 3% in excess of benchmark return

Neutral – return within 3% of benchmark return

Underperform – return > 3% below benchmark return

Benchmark return is determined by long term nominal GDP

growth plus 12 month forward market dividend yield.

Macquarie – Asia/Europe

Outperform – expected return >+10%

Neutral – expected return from -10% to +10%

Underperform – expected <-10%

Macquarie First South - South Africa

Outperform – return > 10% in excess of benchmark return

Neutral – return within 10% of benchmark return

Underperform – return > 10% below benchmark return

Macquarie - Canada

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Macquarie - USA

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

22.60%

34.10%

43.30%

EUR

(for US coverage by MCUSA, 3.33% of stocks covered are investment banking clients)

(for US coverage by MCUSA, 4.91% of stocks covered are investment banking clients)

(for US coverage by MCUSA, 6.10% of stocks covered are investment banking clients)

4.42%

32.60%

62.98%

CA

4.29%8.57%18.74%13.36%Underperform

55.01%41.43%28.01%41.52%Neutral

40.70%50.00%53.24%45.12%Outperform

USARSAAsiaAU/NZ

22.60%

34.10%

43.30%

EUR

(for US coverage by MCUSA, 3.33% of stocks covered are investment banking clients)

(for US coverage by MCUSA, 4.91% of stocks covered are investment banking clients)

(for US coverage by MCUSA, 6.10% of stocks covered are investment banking clients)

4.42%

32.60%

62.98%

CA

4.29%8.57%18.74%13.36%Underperform

55.01%41.43%28.01%41.52%Neutral

40.70%50.00%53.24%45.12%Outperform

USARSAAsiaAU/NZ

Recommendation proportions – for quarter ending 31 March 2013

– 41 –

Company Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst Certification:

The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the

analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the

preparation of this research receives compensation based on overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related

entities (the Macquarie Group) and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie

Capital (USA) Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; and Macquarie

First South Securities (Pty) Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and

Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their

obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide

assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the

obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale

clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use

or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee

the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts

policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including the FSA Rules) which sets

out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or

product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or

particular needs. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice

is appropriate in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can

and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments,

such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on

information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no

obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any

liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients

should contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise.

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities

Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared,

approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal

Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports

issued by Macquarie Capital Markets Canada Ltd in the United States and sent to US persons. Any person wishing to effect transactions in the securities described in the

reports issued by Macquarie Capital Markets Canada Ltd should do so with Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie

– 42 –

Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and

distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Services Authority (No. 193905). Germany: In Germany, research is

issued and distributed by Macquarie Capital (Europe) Ltd, Niederlassung Deutschland, which is authorised and regulated in the United Kingdom by the Financial Services

Authority (No. 193905). France: In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated in the United Kingdom

by the Financial Services Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital Securities Ltd,

which is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited Shanghai Representative Office

only engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie

Capital Securities Ltd. Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc.,

Osaka Securities Exchange Co. Ltd. (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association and

Financial Futures Association of Japan and Japan Securities Investment Advisers Association). India: In India, research is issued and distributed by Macquarie Capital

Securities (India) Pty Ltd., 92, Level 9, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051, India, which is a SEBI registered Stock

Broker having membership with National Stock Exchange of India Limited (INB231246738) and Bombay Stock Exchange Limited (INB011246734). Malaysia: In Malaysia,

research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 463469-W) which is a Participating Organisation of

Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: Information on securities/instruments that are

traded in Taiwan is distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion

of the report may be reproduced or quoted by the press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a

solicitation to buy or sell any security or product. Thailand: In Thailand, research is issued and distributed by Macquarie Securities (Thailand) Ltd, a licensed securities

company that is authorized by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange member no. 28 of the Stock

Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy

of the Securities and Exchange Commission of Thailand. Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai

Listed Companies but this Report can be accessed at: http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated,

research is prepared, issued and distributed by Macquarie Securities Korea Limited , which is regulated by the Financial Supervisory Services. Information on analysts in

MSKL is disclosed at http://dis.kofia.or.kr/fs/dis2/fundMgr/DISFundMgrAnalystPop.jsp?companyCd2=A03053&pageDiv=02. South Africa: In South Africa, research is

issued and distributed by Macquarie First South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by

Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and

Futures Act to deal in securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital

Securities (Singapore) Pte Ltd is exempt from complying with sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by

Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie First South Securities (Pty) Limited and Macquarie Capital (USA) Inc. represent and

warrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States, research is issued and distributed by

Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each

research report prepared by one of its non-US affiliates when the research report is distributed in the United States by Macquarie Capital (USA) Inc. Macquarie Capital

(USA) Inc.’s affiliate’s analysts are not registered as research analysts with FINRA, may not be associated persons of Macquarie Capital (USA) Inc., and therefore may not

be subject to FINRA rule restrictions on communications with a subject company, public appearances, and trading securities held by a research analyst account. Any

persons receiving this report directly from Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie

Capital (USA) Inc. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures, or

contact your registered representative at 1-888-MAC-STOCK, or write to the Supervisory Analysts, Research Department, Macquarie Securities, 125 W.55th Street, New

York, NY 10019.

© Macquarie Group