Embed Size (px)

Citation preview

The Knowledge Based Bio-Economy (KBBE) in Europe: Achievements and Challenges Full report

14 September 2010

© iS

tock

© iS

tock

© V

IB

© B

ayer

A4_1.indd 1 26/08/10 14:25

The Knowledge Based Bio-Economy (KBBE) in Europe: Achievements and Challenges

Full report

14 September 2010

-2-

Study prepared and coordinated by

Clever Consult BVBA (Belgium) - www.cleverconsult.eu

Experts involved in this study Johan Albrecht

Ghent University, Belgium

Dirk Carrez

EuropaBio, Belgium

Patrick Cunningham Chief Scientific Advisor to the Irish Government,

Ireland

Lorenza Daroda National Agency for New Technologies, Energy and Sustainable Economic Development, Italy

Roberta Mancia CIAA, Belgium

László Máthé WWF International, UK

Achim Raschka, Michael Carus, Stephan Piotrowski

nova-Institut, Germany

DISCLAIMER

The views expressed in this publication do not necessarily reflect the position of

the Belgian Presidency or the European Commission.

The contributors do not necessarily endorse the full content of the report.

-3-

Table of Contents 1 Summary ....................................................................................................................... 5

2 Introduction .................................................................................................................. 13

2.1 The Knowledge-Based Bio-Economy (KBBE) ............................................................... 13

2.2 The economic importance of the KBBE....................................................................... 13

2.3 The main global challenges ...................................................................................... 14

3 The KBBE from 2005 to 2010: major achievements .......................................................... 18

3.1 The KBBE in EU research: building on European strengths and knowledge ..................... 18

3.1.1 Introduction ............................................................................................ 18

3.1.2 The EU Framework Programmes ................................................................ 18

3.1.3 ERA-NETs ............................................................................................... 19

3.1.4 European Technology Platforms (ETPs) ...................................................... 19

3.1.5 EU Expert Groups .................................................................................... 20

3.2 Feedstock for food, feed, fuel and products ................................................................ 20

3.2.1 The feedstock situation in Europe .............................................................. 21

3.2.2 Availability of arable land ......................................................................... 24

3.2.3 Research on feedstocks optimisation .......................................................... 26

3.3 Livestock: from farm to fork ..................................................................................... 29

3.3.1 The importance for the EU economy .......................................................... 29

3.3.2 The role of the Technology Platforms ......................................................... 29

3.4 Innovative food production ...................................................................................... 29

3.4.1 The food industry in Europe ...................................................................... 29

3.4.2 Research and innovation .......................................................................... 30

3.4.3 EU policies .............................................................................................. 34

3.5 Innovative bio-based products ................................................................................. 36

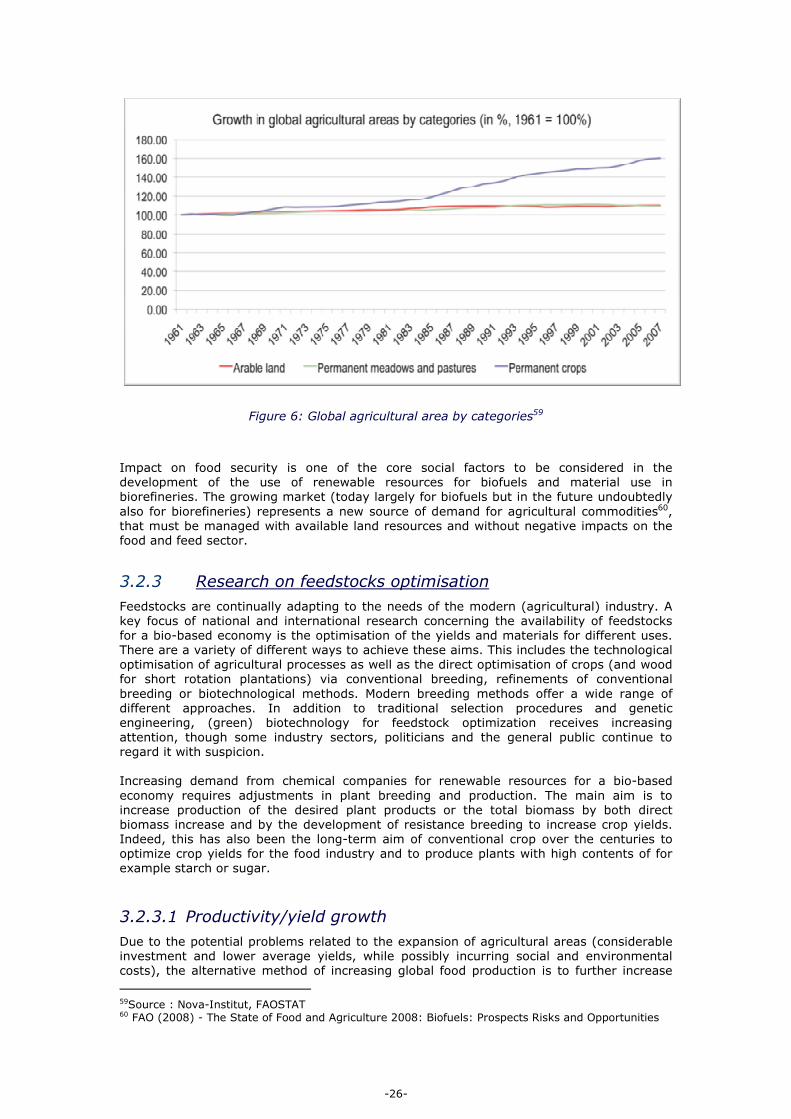

3.5.1 The development of a bio-based economy .................................................. 36

3.5.2 Research and innovation .......................................................................... 37

3.5.3 Regulations and policies as drivers for innovation ........................................ 42

3.6 Sustainability aspects of the KBBE ............................................................................ 43

4 The KBBE towards 2020: main challenges and needs ......................................................... 46

4.1 Towards an more integrated approach of the KBBE in 2020 ......................................... 46

4.2 Sustainable feedstock production for food and non-food .............................................. 46

4.2.1 Food versus Non-Food - Only Non-Food crops for industrial use? ................... 46

4.2.2 Competition biomass for energy versus industrial material use ...................... 47

4.2.3 Research, breeding technologies and green biotechnology ............................ 47

4.3 Livestock: from breeding to cloning? ......................................................................... 49

4.3.1 Research and innovation .......................................................................... 49

4.3.2 Cloned animals for food: between ethics and food safety .............................. 49

4.4 Innovative food production for a growing population ................................................... 50

4.4.1 Research and innovation: prevention of diseases and promotion of health ...... 50

4.4.2 Policies stimulating innovation and securing food supply ............................... 51

4.5 Innovative bio-based products in a sustainable bio-based economy .............................. 53

4.5.1 Major trends and opportunities .................................................................. 53

4.5.2 Research and innovation .......................................................................... 53

4.5.3 Dedicated policies for biobased products .................................................... 55

4.6 Policies for a sustainable KBBE ................................................................................. 58

-4-

5 Main recommendations................................................................................................... 59

5.1 Need for an integrated policy for the KBBE ................................................................. 59

5.2 Research and innovation .......................................................................................... 59

5.2.1 More public funding for research ............................................................... 59

5.2.2 Support for specific technologies ............................................................... 59

5.2.3 Better integration of the different research areas ......................................... 60

5.2.4 Better coordination between Academia and Industry .................................... 60

5.2.5 Clusters and public–private partnerships, essential to stimulate innovation ..... 61

5.2.6 Public support for the development of demonstration projects ....................... 61

5.3 Towards economic-sustainable and innovative SMEs ................................................... 61

5.4 Communication and education .................................................................................. 62

5.5 A strong EU common policy for agriculture: the new CAP (post 2013) ........................... 62

5.6 Support reconversion towards low-carbon renewable-based production systems ............. 63

5.7 Policies stimulating the market for KBBE products....................................................... 64

5.8 Science based sustainability criteria .......................................................................... 64

6 Conclusions................................................................................................................... 66

-5-

1 SUMMARY

The European Knowledge Based Bio-Economy (KBBE)

The increasing demand for a sustainable supply of food, raw materials and fuels, together with recent scientific progress, is the major economic driving force behind growth of the Knowledge Based Bio-economy (KBBE) in Europe over the last few decades. The bio-economy – the sustainable production and conversion of biomass, for a range of food, health, fibre and industrial products and energy, where renewable biomass encompasses any biological material to be used as raw material - can play an important role in both creating economic growth, and in formulating effective responses to pressing global challenges. In this way it contributes to a smarter, more sustainable and inclusive economy. It is estimated that the European bio-economy currently has an approximate market size of over 2 trillion Euro, employing around 21.5 million people, with prospects for further growth looking more than promising. In addition to being economically favourable, the KBBE can help to meet the most urgent global challenges improving public well-being in general. Areas that it can benefit include social and demographic development and its impact on agriculture, the growing pressure on water, the threat of climate change, the limited resources of fossil fuel, the need for sustainable development, the impact of changes in lifestyles and eating habits, the demand for safer and healthier foods and the prevention of epizootic and zoonotic diseases.

Major achievements

When the European Commission developed the concept of the KBBE, it was with the aim of developing the European bio-economy so that it could compete on a global level and build on European strengths. These included excellence in science, technology and industry to deliver innovation, world leadership in food technologies and products and animal breeding technologies, and having a strong chemical and manufacturing industry base. Over the last five years, within the Commission, research and innovation have provided the main supporting policies for the KBBE. To support this initiative, 9 KBBE specific European Technology Platforms (ETP) were set up, and research in the area of the KBBE has been promoted and financed through the Commission’s Framework Programme 7 and several Member State initiatives. As these ETPs developed, they started to communicate and work together on issues of mutual interest, such as identifying synergies in their Strategic Research Agendas (SRAs). The European Commission set up regular meetings with representatives from the KBBE ETPs and invited experts to discuss policy-related issues together. Today the 9 ETPs active in the KBBE sector are joining forces in the BECOTEPS project, funded by the European Commission’s Seventh Framework Programme. The objectives of the BECOTEPS project are to achieve closer and more coordinated collaboration between the KBBE ETPs and to develop recommendations for better interaction between the KBBE ETP stakeholders along the product chains. They also focus on the sustainability issue regarding multidisciplinary research, innovation and policy issues, and the goal to encourage dialogue between European and national, public and private and research and innovation initiatives. At EU level, research in the KBBE area has also strengthened by the implementation of several ERA-Nets. The ERA-NETs aim to reduce the fragmentation of the European Research Area (ERA) by improving the coherence and coordination of national and regional research programmes. In addition to ERA-NETs and ETPs, a third category of pan-European KBBE-related networks consists of European Commission expert groups. These include the Advisory Group on Food, Agriculture and Biotechnologies, the KBBE-Net, the KBBE National Contact Point, and the EU Standing Committee for Agriculture Research.

-6-

The current and future availability of biomass feedstock for food, feed, energy and industrial material use in Europe as well as the question of the available land for food and non-food crops still remains a contentious issue in need of in depth analysis. The impact on food security is one of the core social factors to be considered in the development of the use of renewable resources for biofuels and material use in biorefineries. The growing market (today largely focussed on the production of biofuels but in the future undoubtedly also for biorefineries) represents a new source of demand for agricultural commodities. This demand must be managed appropriately with respect to available land resources and without associated negative impacts on the food and feed sector. Feedstocks are continually adapting to the needs of the modern (agricultural) industry. A key focus of national and international research concerning the availability of feedstocks for a bio-based economy is the optimisation of the yields and materials for different uses. This includes the technological optimisation of agricultural processes as well as the direct optimisation of crops (and wood for short rotation plantations) via conventional breeding, refinements of conventional breeding or biotechnological methods. Today, modern breeding methods offer a wide range of different approaches. In addition to traditional selection procedures and genetic engineering, (green) biotechnology for feedstock optimization receives increasing attention, though some industry sectors, politicians and the general public continue to regard this technology with suspicion. This appears to remain a Europe-specific problem whilst emerging economies such as China, Brazil and India are embracing these techniques as promising and important technology advances for their nations. The potential of this technology is also demonstrated by the fact that in 2009 more than 134 million ha of arable land were planted with transgenic crops by 14 million farmers worldwide. A second focus is the optimization of the plant ingredients such as through a change of the starch molecule for technical uses of the potato or the change in composition of fatty acids in rapeseed, sunflower or crambe oils. Nutritional improvements of a large range of food products and the development of novel food products and processes, including food packaging technologies are important drivers in realising ambitions for healthy food and healthy lifestyles. Additionally improvements in this area are necessary for minimising the environmental impacts of agriculture by reducing green house gas emissions and energy and water consumption whilst contributing to a more sustainable eco-friendly economy. These research topics tackle some of our key societal challenges such as how to feed almost 9 billon people by 2050 and how to manage the demands of a population that is shifting its food preferences towards a greater consumption of meat. Achievements in the food sector in terms of promoting research and market development include the launch of diversified research programmes (from basic to applied research, research infrastructures, training and support to SMEs), reinforcing cooperation and better exploiting research results. They have also involved boosting competitiveness through the active participation of relevant industrial partners in European technology platforms, and integrating strategically focused, trans-national research that will deliver innovative processes, products and tools in line with the needs and expectations of the consumer. Since 2006, 36 National Technology Platforms (NTPs) have been established under the umbrella of the ETP Food for Life. The National Food Platforms play a key role in conveying the programme of the ETP to the national industry, especially to SMEs and the research community. In addition, actors within the food supply chain are united together under the European Food Sustainable Consumption and Production (SCP) Round Table initiative in order to face current and future sustainability challenges. In the area of bio-based products, Europe has become the leading region for the development and production of enzymes. Because enzymes play a crucial role for applications in many other industrial sectors, this sector represents significant potential for the EU in terms of escalating global leadership in the area of biobased products and processes. On the other hand, the United States and Brazil are the world leaders in the production of biofuels (mainly bioethanol). Another established sector is the production of biochemicals which find applications in the pharmaceutical industry, the food and feed industry, the production of detergents and cosmetics, and many other sectors. In the

-7-

chemical industry, an important step in increasing the share of biobased chemicals is the creation of biotechnological platform intermediates based on the use of renewable carbon sources. Furthermore, although the production of bio-based polymers and plastics are technologies still in their infancy, this industry has been characterised by an annual grow rate of almost 50% due to new synergies and collaborations. In Europe, there is also a growing focus on biorefineries. These use biological matter (as opposed to petroleum or other fossil sources) to produce transportation fuels, chemicals, and heat and power. Because they combine and integrate the technologies necessary to convert renewable raw materials into industrial intermediates and final products, they can straddle the whole value chain. The European Commission has funded several projects under FP6 and FP7 analysing the biorefinery research situation in the European Union. At the beginning of 2010, they then launched three large collaborative projects addressing the entire value chain. Aspects included in these projects were the production of biomass, logistics, intermediary processing steps and conversion into end-products with the feasibility of techniques shown at pilot scale. Moving forward, the Commission will fund the programmes with 52 million Euro over a period of 4 years. 81 partners from universities, research institutes and industry in 20 countries will invest an additional €28 million. In addition, at member state level, we see an increasing number of biorefinery oriented research programmes. More than 300 research projects have been identified in Europe (at EU, national and regional levels), with a total budget of around 1.2 billion Euro, of which more than 808 million Euro comes from public funding. There is a clear need for a coordinated technology development covering different technologies and parts of the value chain including feedstock development, product development, production optimization and innovative application development. Cooperation in cluster structures rather than in single-company partnerships is significantly accelerating the development of processes and their penetration into the industry. Towards the end of 2009, the European Commission published an action plan on Key Enabling Technologies (KET), which included industrial biotechnology. The purpose is to develop an action plan with measures to remove obstacles hindering further development and to fully exploit the results of research. These measures include a focus on demo projects and better coordination of the activities between EU and Member States for example through joint calls or joint programming. SusChem’s European Innovation project - BIOCHEM - was selected at the beginning of 2010 for funding by the European Commission under its INNOVA scheme. BIOCHEM will define and promote bio-based product opportunities in the chemical sector, and will also facilitate and help finance new bio-based business ideas to proof-of-concept, including facilitating access for organizations to European test facilities. Specific policies for the development of biobased products are more extensive for bioenergy, including for liquid biofuel use and solid biomass applications, than for biochemicals or biomaterials. Worldwide, many governments support their emerging biofuel industries far more than other KBBE sectors through subsidies, mandates, adjustments to fuel taxes and incentives for the use of flexi-fuel vehicles. In Europe, the Renewable Energy Directive of 2009 is calling for a mandatory target of a 20% share of renewable energies in the EU's energy mix by 2020. In addition, by the same date, each Member State must ensure that 10% of total terrestrial transport, such as road transport and train fuel, comes from ‘renewable energy’, defined to include biofuels and biogas, as well as hydrogen and electricity. Furthermore, in order to stimulate the use of so-called second generation energy sources, biofuels from waste, residues, non food cellulosic material, and lignocellulosic material will count twice towards achieving the renewable energy transport target. Although Europe plays a leading role in research and science, it is less successful in converting the science-based findings into commercially valuable products. This is why the Commission has developed a so-called demand-based innovation policy, the Lead Market Initiative (LMI). One of the areas that this policy focuses on is that of bio-based products. An Ad-hoc Advisory group has developed a series of concrete recommendations and actions, ranging from improving the implementation of the present targets for bio-based products to standardisation, labelling and certification in order to ensure the quality and consumer information on the new products.

-8-

In Europe, sustainability it is an important driver for many of our policies, and several of the demand-side regulations include sustainability aspects such as 'green' public procurement. But sustainability is not solely about greenhouse gas emissions reductions or climate change, it also concerns waste reduction, minimizing energy consumption and efficient use of resources. Because of the interdependencies between processes involved in growing, harvesting, manufacturing, distributing and disposing of a product, sustainability requires a life cycle analysis encompassing the whole value chain. This includes the production of biomass, evaluating land use, consumption of water, energy, pesticides and fertilizers and the production and use of the final products. Currently, national and international efforts to develop more comprehensive, systems-oriented sustainability frameworks for bio-based products are under development.

Main challenges

Over the next 10 years we can expect a shift in practice from a sectoral approach towards a more integrated approach of the KBBE. In the case of a sustainable feedstock production, for food and non-food applications, significant challenges remain to be solved for the future. In Europe, in particular, there needs to be a concise strategy to satisfy the demands of a range of stakeholders for the use for food, feed, fuel and materials. On this basis, “food versus non-food” debates and the biomass competition between energy and material still needs to be resolved. Other challenges concerning the feedstock needed for different applications include the growing demands for food, fuels and materials in the context of an expanding worldwide human population. In addition, the adaptation and optimisation of existing feedstocks for the given land that can be used for agriculture are a key focus. In this field, in particular, the use of advanced breeding technologies and green biotechnology should be discussed and evaluated in the context of new challenges concerning global warming, pressure on natural resources and sustainable agriculture. Gene transfer between species has now been a reality in plant breeding and selection for two decades. In addition, it has been achieved technically in animal species as diverse as goats, pigs and fish. The debate on the public acceptability of these techniques in food animals has already begun in the United States, and is likely to be even more contentious in Europe. In parallel, the cloning of animals is also now technically feasible, though it is still far from becoming commercially viable. Genetic modification (GM) technologies, already applied in over 130 million ha of crops worldwide, have met strong opposition from European consumers. Issues of public acceptability are therefore likely to be increasingly important as GM and related technologies, such as (animal) cloning, continue to develop. Changes in both population demographics and life span demand that European public health policies focus on healthy ageing, which not only includes the prevention of diseases but also on delaying the deterioration of health status. However, the area of research in health, food and diet-related diseases is both complex and fragmented. At the same time, there are a number of pressing challenges on a European-scale that can only be tackled through a combination of public policy development, academic research and industry developments in European Member States and Associated Countries. Future efforts should include prevention of chronic diseases through promoting collaborative research and sharing data and results on health impacts of nutrition and lifestyle. They should also incorporate effective interventions, and the creation of a coherent long term, public health research programme on diet related diseases from molecular to population levels by integrating systems including biology, genetics, nutrition, epidemiology and social sciences. In addition, industry finds it difficult to seek authorisation for novel food products, because of the lengthy procedures and the uncertainty of the outcome. The cost factor discourages many from patenting food products or new processing techniques, in particular SMEs. Although the total amount of agricultural output will have to increase over the coming decades, climate change is expected to have a profound and increasing impact on food production through factors such as rising temperatures, altered rainfall patterns and more frequent extreme events. Moreover, this challenge of delivering food security in the

-9-

context of climate change also means that it is necessary to find innovative ways of increasing efficiency and reducing waste throughout the food chain in order to make the most of the resources and raw materials available. Another important contribution of the food sector could be the reduction of food losses by introducing modern collection, processing, storage and transportation methods. The development of innovative bio-based products is R&D intensive, and increasing investments in certain technologies will be a major challenge. Although industrial biotechnology has been identified as a key enabling technology, only 2% of biotech R&D went towards developing industrial biotechnology in 2003. This is incongruous with OECD predictions that industrial biotechnology will contribute up to 39% of the biotech industry’s gross value added (GVA) by 2030. In addition, member states of the International Energy Agency (IEA) spent 13 times less on R&D in bioenergy (including biofuels) than the amount spent on nuclear fission and fusion R&D and 4 times less than was spent on R&D into fossil fuels. Furthermore, research activities in the EU concerning lignocellulosic bio-ethanol and second generation biofuels in general, are modest when compared with the massive efforts of the U.S. and Brazilian governments. The initial construction of bio-refinery pilot and demonstration plants is not only a costly undertaking but it also involves bringing together market actors along a new and highly complex value chain. Countries like the US, Brazil, China and others are increasing investment into research, technology development and innovation, and are supporting large scale demonstrators in which many European companies already participate. In addition, producing chemicals through bio-chemical routes is currently still more expensive when compared with traditional production routes. It should also be taken into account that existing production facilities for chemical syntheses cannot be converted to biotechnological production without massive new investments. In contrast to biofuels, there is currently no European policy framework to support bio-based materials. As a result, these products suffer from a lack of tax incentives or other supporting regulations. Other demand-driven policies focus on the sustainability agenda (including green public procurement) and are often implemented as a mix of public procurement procedures, legislation and direct financial incentives which is a complex matter in Europe. However, such policy frameworks have been successfully developed in other parts of the world. Addressing sustainability issues through all segments of the value chain of bio-based products (from biomass production to end-use) in a fair, evidence-based regulatory framework, is a major challenge for biofuels and other bio-based products. In doing so, the sector has to demonstrate that it possesses sustainability credentials in order to gain a strong “license to operate” from governments and consumers, especially if supporting policies have to be developed. Unfortunately the lack of widely-accepted schemes to assess and confirm sustainability is a significant barrier to consumer and government confidence.

Main recommendations

1. Need for an integrated policy for the KBBE

To achieve a competitive KBBE, broad approaches, such as creating and maintaining markets for environmentally sustainable products, funding basic and applied research, and investing in multi-purpose infrastructure and education, will need to be combined with shorter term policies. These include measures such as the application of biotechnology to improve plant and animal varieties, improving access to technologies for use in a wider range of plants, fostering public dialogue, increasing support for the adoption and use of internationally accepted standards for life cycle analysis together with other incentives designed to reward environmentally sustainable technologies.

2. Research and innovation

In order to make a swifter more efficient shift towards more integrated and sustainable production and processing systems, the level of R&D funding in the bio-economy

-10-

should be increased through multidisciplinary research programmes at both national and European level. In addition, cooperation between private and public sectors should be a focus for further improvement. Building competence networks between industry and academia could also help to overcome the competence hurdle and knowledge gap that currently exist between these two stakeholder groups. In addition, better interdisciplinary and collaborative research would lead to valuable new business activities. Special attention should also be placed on specific key areas, such as the development of efficient and robust enzymes particularly for the conversion of lignocellulosic material. This should enable conversion from a variety of feedstock, synthetic biology and metabolic pathway engineering and the combination of technologies such as biochemical and chemical processes as well as applications derived from agricultural and industrial biotechnology. In addition, specific research is needed to improve feedstock yield and/or the composition of biomass involving both plant genomics and new breeding programmes, also incorporating further research into efficient crop rotation, land management and land-use change issues. Integration of the individual KBBE sectors should support pre-competitive research covering the entire value chain – from feedstock to end-product – as this will help to stimulate innovation and encourage the uptake of its results by the industrial partners involved. In the longer term, we expect not only closer integration of the different sectors of the KBBE, but also between different research areas across food as well as non-food commercial applications. One of industry’s remaining major challenges is to translate research to products, including the development of new product applications. Setting up public-private partnerships would result in a pooling of resources, thus allowing more ambitious goals to be set in terms of reducing the time-to-market. This would also enable industry to adopt longer-term investment plans in the field of the bio-economy, taking into account the market perspective. Stimulating the construction of demonstrators via public-private partnerships is one of the most important measures that can be taken in the development of the bio-economy, as they are able to close a critical gap between scientific feasibility and industrial application. They dramatically reduce the risk of introducing new technology on an industrial scale and therefore make a biorefinery venture much less risky for investors.

3. Towards economic-sustainable and innovative SMEs

Spin-offs and high-tech SMEs are key for technology and knowledge development, and investing in research and innovation is the only way for these enterprises to survive. It is of critical importance to the success of these SMEs, and hence to the innovation potential of the sector as a whole, to improve their access to finance. However, without larger scale validation, it remains very hard for SMEs to attract the large industrial partners or other private investors that they need to become sustainable. Developing grants for “Proof of Concept” studies could help partially overcome this problem. One of the weaknesses of the many SMEs in the more “traditional” sectors (such as agriculture, forestry, aquaculture, food sector) is that many of them do not have the in-house technical skills to take up the results of innovation. Supporting tech transfer or stimulating SMEs to participate in “open innovation” programmes could therefore be a way to overcome this problem.

4. Communication and education

To facilitate smooth long-term development and implementation of the different technologies of the KBBE, a strategy for communication and stakeholder involvement is necessary. This would not only help to raise awareness of the technologies but would help ensure that longer term objectives are fixed to provide solutions that reflect societies real needs.

-11-

It is of critical importance for the bio-economy to have a multi- and interdisciplinary work force, in order to ensure that it keeps up-to-date with new knowledge and techniques. There is therefore a need for multidisciplinary education, good international training programmes and efficient lifelong learning. In addition, due to a gap in education, biotechnology and chemistry are still too often perceived as “competing technologies” instead of as being complementary.

5. A strong EU common policy for agriculture: the new CAP (post 2013)

It is essential that the new CAP promotes sustainable and competitive agricultural production, and ensures balanced access to raw materials for the food and feed sectors, as well as for industrial applications, without disrupting food supply. The new CAP should ensure the possibility to maintain a competitive supply of raw materials that meets EU standards, notably in the areas of safety, environmental sustainability, and animal welfare. The CAP should also address situations of extreme price volatility, acting as a safety net in order to secure supply by preventing crisis situations and remedying temporary market imbalances. Absolute coherence is needed across all the policy areas driving supply, including food safety, innovation and new technologies, trade, development, the environment, animal welfare, and consumer and public policies. Horizontal policy coherence should result in reduced raw material market disruptions and should also contribute to ensuring competitive EU agriculture. In order to stimulate the development of local biorefineries and to support rural development, it is important to develop and maintain a reliable upstream supply chain. This should be capable of mobilising a sufficient level of feedstock for conversion without being achieved at the expense of food and land use. For this reason, it is also important to invest in local and regional infrastructures and in logistical capabilities to allow all biomass, including agricultural, forestry and waste-based raw material, to be utilized.

6. Support reconversion towards low-carbon renewable-based production

systems

Investments required for building a new bio-industrial facility - especially if it competes with the conventional one - might be a significant barrier to the development of the KBBE. For SMEs, such an investment might represent an even more difficult hurdle to overcome. Governments aiming to support biorefineries for reasons of environmental sustainability, energy security and innovation leadership will therefore need to support market growth, and carefully regulate the industrialization process in order to stimulate and encourage private sector investments.

7. Policies stimulating the market for KBBE products

Decision makers can help provide the necessary motivation by implementing a regulatory framework of incentive based and demand stimulating policies. Mandates, subsidies and incentives are provided by governments all over the world to stimulate the demand of sustainable bio-based products. The European Commission’s Lead Market Initiative for bio-based products represents a good example of such a scheme and moving forward, this should be further developed and build upon. In the future, a similar initiative could be developed for the food sector or for the KBBE as a whole.

8. Science based sustainability criteria

Sustainability criteria addressing the different KBBE sectors should aim to measurably reduce the key impacts associated with feedstock production, consumption and use. In addition, implementation of measures involve the active participation of all stakeholders involved in the supply chain. Recent developments in the biofuel sector in the EU will make it possible to use private standards to prove compliance with sustainability requirements. While some schemes have ambitious sustainability criteria going beyond the minimum EU requirements, most of these only address a fraction of the overall concerns. Wider sustainability concerns will need to be addressed by governments in partnership with the private sectors. In addition, feedstock producing

-12-

countries - especially in the global South - will need significant technical and financial support to implement adequate safeguards.

-13-

2 INTRODUCTION

2.1 The Knowledge Based Bio-Economy (KBBE)

The ability to innovate has increasingly determined the success and competitive strength of our industry. But even in a global economy where mainly high technological industries have been thriving, a large part of our prosperity is still directly derived from basic natural, biological resources, as they are the raw materials for the majority of the products on which we depend on a day to day basis. Although they are the basis of the oldest economic activities, new technologies such as and life sciences and biotechnology are now transforming them into one of the newest, at the frontier of the emerging knowledge-based economy. The recent scientific and technological progress has opened up a vast array of new possible applications and products in a wide range of fields, and will soon yield immense health, societal and economic rewards. Scientists have mapped the entire human genome and those of a rapidly increasing number of animals, plants and micro-organisms. The growing knowledge of the molecular mechanics of organisms is paving the way for new agricultural products and practices, biodegradable materials as well as emission-reducing biofuels. Advanced biotechnology is creating new possibilities in terms of tailor-made foods targeted at specific consumer needs and tastes. In addition, industrial biotechnology is breaking new ground in understanding microbial biodiversity and bio-processes that could lead to valuable bio-products and bio-materials. All this has cleared the way for the emergence of a successful so-called Knowledge-Based Bioeconomy (KBBE) in Europe. The KBBE can be concisely defined1 as “life sciences and biotechnology knowledge converging with other technologies to transform into new, sustainable, eco-efficient and competitive products”. The ‘bioeconomy’ encompasses all industries and economic sectors that produce, manage, or otherwise exploit biological resources (e.g. agriculture, food, forestry, fisheries and the industries based upon). Recently the 9 European Technology Platforms involved in the Becoteps2 project developed a common definition for the KBBE:

The bio-economy is the sustainable production and conversion of biomass, for a

range of food, health, fibre and industrial products and energy. Renewable

biomass encompasses any biological material to be used as raw material.

2.2 The economic importance of the KBBE

The increasing demand for a sustainable supply of food, raw materials and fuels, together with the scientific progress, is the major economic driving force behind growth of the KBBE, which has been significant over the last few decades. Innovation is believed to be the best way to increase productivity and competitiveness, and at the same time to improve our quality of life, secure sustainable food production and protect the environment. The KBBE is basically occupied with both aspects, as life sciences and biotechnology help us to live in a healthier and more sustainable fashion by finding more environmentally friendly production methods. The sector can thus play an important role in both creating economic growth, and in formulating effective responses to pressing global challenges. In this way it contributes to a more competitive and sustainable economy - for the benefit of all. It is estimated that the European bio-economy has currently an approximate market size of over 2 trillion Euro, employing around 21.5 million people, and the prospects for further growth are more than promising. For a variety of reasons it is expected that in the next decade significant changes will take place in this field. There is growing pressure on

1 Cologne paper (2007) - En route to the knowledge-based bio-economy. 2 http://www.becoteps.org/

-14-

European companies to diversify their portfolio of products. As an example, some of the largest pulp and paper producers, mainly in Northern-Europe, are conducting cutting-edge research in the field of biofuels and biomaterials.

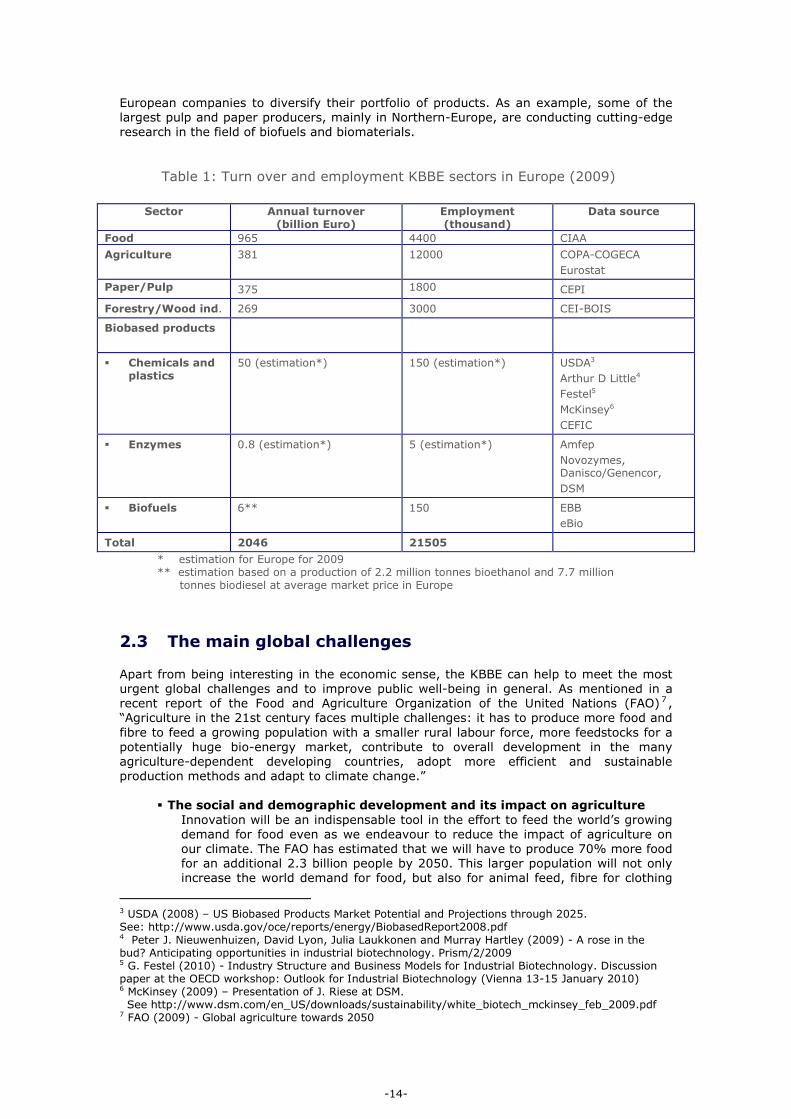

Table 1: Turn over and employment KBBE sectors in Europe (2009)

Sector Annual turnover

(billion Euro) Employment (thousand)

Data source

Food 965 4400 CIAA

Agriculture 381 12000 COPA-COGECA

Eurostat

Paper/Pulp 375 1800 CEPI

Forestry/Wood ind. 269 3000 CEI-BOIS

Biobased products

� Chemicals and plastics

50 (estimation*)

150 (estimation*) USDA3

Arthur D Little4

Festel5

McKinsey6

CEFIC

� Enzymes 0.8 (estimation*)

5 (estimation*)

Amfep

Novozymes, Danisco/Genencor,

DSM

� Biofuels 6** 150 EBB

eBio

Total 2046 21505

* estimation for Europe for 2009 ** estimation based on a production of 2.2 million tonnes bioethanol and 7.7 million tonnes biodiesel at average market price in Europe

2.3 The main global challenges

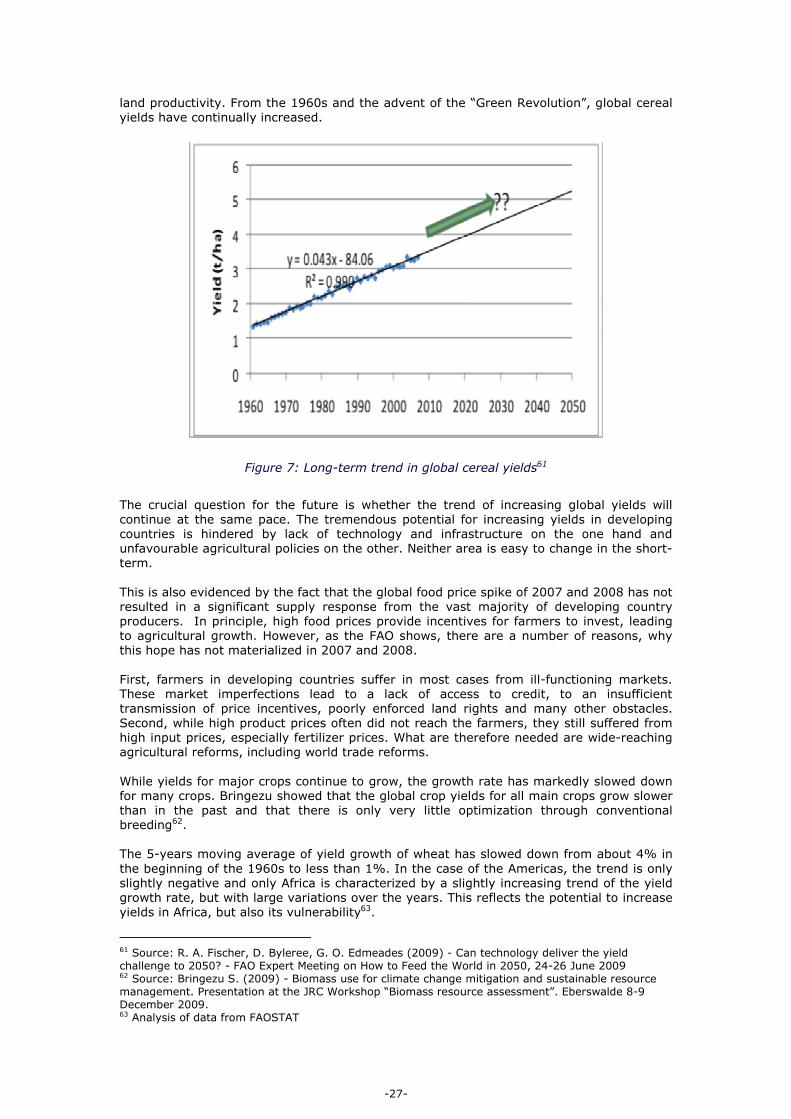

Apart from being interesting in the economic sense, the KBBE can help to meet the most urgent global challenges and to improve public well-being in general. As mentioned in a recent report of the Food and Agriculture Organization of the United Nations (FAO) 7 , “Agriculture in the 21st century faces multiple challenges: it has to produce more food and fibre to feed a growing population with a smaller rural labour force, more feedstocks for a potentially huge bio-energy market, contribute to overall development in the many agriculture-dependent developing countries, adopt more efficient and sustainable production methods and adapt to climate change.”

� The social and demographic development and its impact on agriculture Innovation will be an indispensable tool in the effort to feed the world’s growing demand for food even as we endeavour to reduce the impact of agriculture on our climate. The FAO has estimated that we will have to produce 70% more food for an additional 2.3 billion people by 2050. This larger population will not only increase the world demand for food, but also for animal feed, fibre for clothing

3 USDA (2008) – US Biobased Products Market Potential and Projections through 2025. See: http://www.usda.gov/oce/reports/energy/BiobasedReport2008.pdf 4 Peter J. Nieuwenhuizen, David Lyon, Julia Laukkonen and Murray Hartley (2009) - A rose in the bud? Anticipating opportunities in industrial biotechnology. Prism/2/2009 5 G. Festel (2010) - Industry Structure and Business Models for Industrial Biotechnology. Discussion paper at the OECD workshop: Outlook for Industrial Biotechnology (Vienna 13-15 January 2010) 6 McKinsey (2009) – Presentation of J. Riese at DSM. See http://www.dsm.com/en_US/downloads/sustainability/white_biotech_mckinsey_feb_2009.pdf 7 FAO (2009) - Global agriculture towards 2050

-15-

and housing, clean water and energy. Due to growing world demand for meat, grains and fuels, the average prices of food, feed and energy commodities are likely to remain volatile or could even rise significantly8. An important increase in agricultural production is needed to fulfill the growing demand for food and raw material for industrial use. In addition this should be achieved in a sustainable way, e.g. by avoiding losses, recycling where possible, maximising use of agricultural waste, conserving biodiversity, etc. Management practices in forestry and agriculture will have to be continuously aligned with biodiversity and climate change mitigation targets. The challenge is undoubtedly significant, especially if we consider some of the key limitations. For example, at the moment approximately 30% of the Earth’s area is used for agriculture and grazing. But this represents 55% of the habitable area9. So a growing population will not only increase demand for food, fuel and fibre but will also reduce the area where the production of these can take place.

� The pressure on water Agriculture is the largest consumer of freshwater by far – about 70% of all freshwater withdrawals go to irrigated agriculture10 and nearly 60% is wasted. Water scarcity will limit food production and supply, putting pressure on food prices and increasing countries’ dependence on food imports. Combining this with the potential for droughts caused by climate change, we may see many more people located on land under water stress in the future. Water shortage could drive the development of a KBBE that reduces water consumption.

• Need to reverse current trends Growing demand for food, fibre and fuel has contributed to the conversion of approximately 2.2 million hectares / year of new agricultural land. A significant share of this comes from converting natural forests and grasslands. Agriculture is responsible for at least 55% of habitat loss in the last few decades. Improving management practices and increasing the efficiency, both in the production but also in the processing and consumption of the commodities will have a significant influence on how we will satisfy the forecasted growth in demand. The potential to improve management practices and reduce impacts are significant. For example 70-90% of farmers loose more carbon/year than put back and 25-40% of greenhouse gases that contribute to climate change are related to agriculture11. Forestry management practices are equally important. Demand for one of the most versatile renewable material continues to grow. This can lead to unsustainable intensification of forest management in currently managed forests and expansion of harvesting into areas with natural forests. Responsible forest management can however have positive impacts on biodiversity, livelihoods and contribute to climate change mitigation.

� The threat of climate change

Climate change could adversely affect water supplies and agricultural productivity. The need to cut CO2 emissions to avoid dangerous climate change has made the transition from conventional fossil fuels to alternative and renewable resources a priority for everyone. UNEP (2010)12 notes that “doubling of wealth leads to 80% higher CO2 emissions”. The KBBE can encourage the development of new biological processes and the use of agricultural waste streams and renewable raw materials derived from plants, crops and trees to produce biobased fuel, materials and chemicals that have the potential to enhance quality of life while reducing negative environmental impact and thus reducing our ecological footprint. While climate change mitigation is one of the main drivers, we should not forget that climate change will also have a

8 OECD (2009) – The bioeconomy to 2030: designing a policy agenda OECD-FAO (2010) - Agricultural Outlook 2010-2019 9 Clay (2004) – World Agriculture and the Environment: A Commodity-By-Commodity Guide To Impacts And Practices 10 Third United Nations World Water Development Report (2009) - Water in a changing world 11 Clay (2004) – World Agriculture and the Environment: A Commodity-By-Commodity Guide To Impacts And Practices 12 UNEP (2010) - Environmental Impacts of Consumption and Production

-16-

significant impact on productivity, yields, water and land availability. The development of the KBBE will likely mean the need for significant amounts of biomass. While yields in forest for example might increase in parts of the world such as Northern-Europe, the factors destabilizing forest ecosystems (insect attacks, changing weather conditions) will have growing impacts. In agriculture, IFPRI 13 notes that yields especially in the developing countries will likely decrease, and South-Asia will be especially hard hit.

� Limited resources of fossil fuel and energy security

A challenge of equal order is the anticipated increased demand for services delivered through fossil fuels and energy in the next decades while fossil fuel reserves, particularly oil and gas, will continue to decline. The global demand for fossil fuels is expected to increase by over 44% from 2006 to 203014, and this will not only lead to a further increase in GHG emissions but also to higher energy prices. Expert analysis15 shows that it is possible to decarbonize the energy sector by 2050 by massively investing in renewable energy and energy efficiency.

� The need for sustainable development

All major facets of European society and economic activity are being challenged to demonstrate their sustainability. Consumers are more and more conscious about the impacts of their consumption and companies want to show the progress they make. In most countries, household consumption, over the life cycle of the products and services, accounts for more than 60% of all impacts of consumption16. The KBBE can contribute to a more sustainable society, not only because it leads to an economy no longer wholly dependent on fossil fuels for energy and industrial raw materials with the potential to reduce greenhouse gas emissions, but also by generating less waste, by a lower energy consumption and by using less water17. In addition, the KBBE provides also for the established industries the opportunity for further growth in a sustainable way.

� Fast technological development Technological development has progressed rapidly and will further boost the applications of the KBBE. Growing knowledge, bioinformatics, and the strong interaction of engineering sciences with life sciences will open avenues to new products and applications. Biotransformation will be a key technology in several industrial sectors, and the genetically engineered modification of microorganisms results in new sustainable processes.

� Changes in lifestyles and eating habits

Economic development and the movement from an industrial economy to a service-based economy has brought new employment patterns and has changed consumer eating habits impacting on food consumption. While a quarter of the world’s population does not have enough food, over 40% of the world’s grain harvest is fed to livestock. Predominantly meat-based diets, characteristic to most OECD countries, are very inefficient. Farming animals for meat and dairy requires huge inputs of land and water for growing animal feed - on average, 6kg of plant protein is required to produce just 1kg of meat protein18. Transition to a lower meat rich diet will potentially reduce climate change mitigation costs by 50%19. Consumers demand “easy” food choice, “ready to eat” and “heat to eat” as meals are increasingly consumed away from home switching habits from domestic to out-of-home lifestyle and diets 20 . These changes require the

13 IPFRI (2009) - Climate change: Impact on agriculture and costs of adaptation. See: http://www.ifpri.org/publication/climate-change-impact-agriculture-and-costs-adaptation 14 OECD (2009) – The bioeconomy to 2030: designing a policy agenda 15 Ecofys (2010) - Energy Unlimited (to be published). 16 UNEP (2010) - Environmental Impacts of Consumption and Production 17 JRC (2007) - Consequences, Opportunities and Challenges of Modern Biotechnology for Europe 18 WWF-UK (2010) - http://www.wwf.org.uk/what_we_do/changing_the_way_we_live/food/ 19 Stehfest et al. (2009) – Climate benefits of changing diet. Climatic Change 95, pp 83–102. See http://tier-im-fokus.ch/wp-content/uploads/2009/06/stehfest09.pdf 20 ETP Food for Life (2007) - Strategic Research Agenda 2007-2020. See: http://etp.ciaa.be/asp/documents/docs.asp?cat=Documents

-17-

continuous development of innovative packaging able to guarantee that food remains healthy, tasty and convenient which still remain crucial factors for consumers, but also to satisfy the enjoyment of food and its accessibility (i.e. ease of container-opening for children and the elderly).

� The demand for safer, healthier and higher quality foods Although manufactured foods are safer than ever, excessive food intake, in conjunction with a decrease in physical activity has led to an increase of life style-related diseases such as obesity, diabetes, coronary and heart-related diseases in European society meaning that health and well being issues represent an increasingly significant concern for consumers. Food and drinks are necessary for the development, wellbeing and health of European citizens21 . Therefore there is a need to provide not only quality, tasty and safe food but also varied, wholesome, functional, nutritious diets focusing on healthy ageing, prevention of diseases and delaying the deterioration of health status.

� Control and prevention of epizootic and zoonotic diseases22 In the last fifty years, the situation in animal disease in Europe has been transformed. First, major diseases which were formerly of great importance (such as Foot & Mouth Disease or Classical Swine Fever) have been eradicated. Secondly, the major zoonoses (tuberculosis, brucellosis) are in the final stages of eradication. These eradication programmes, which required decades of dedicated and coordinated effort, have been very expensive, but have brought major economic benefits. At the same time, their very absence leaves the populations very vulnerable to major consequences of accidental reintroduction. This was illustrated in the case of the Foot & Mouth disease outbreak in the UK in 2001 which was brought under control at a cost estimated at 13 billion Euro. Continued controls and vigilance are therefore necessary. Changes in husbandry practices, generally involving intensification, together with development of effective drugs has eliminated much of the losses formerly due to various species of parasites in the different animal species. Increasingly intensive production systems, and stresses related to higher animal performance, require higher levels of management. In some cases a combination of these factors has facilitated the spread of the diseases BVD (Bovine Viral Diarrhea) and IVR in cattle, and influenza in pigs. Finally, the experience of BSE (Mad Cow Disease) has shown how unprepared Europe was for a devastating and totally new disease. The BSE experience is estimated to have imposed a permanent additional cost of 3 billion Euro per annum on the European beef production industry. Because of its demonstrated link to nvCJD (new variant Creutzfeldt-Jakob Disease) in humans, it has led to the creation of new food safety authorities on a permanent basis for the EU and in each European country. Finally, the extensive actions required in the face of potential threat from avian and swine virus sources illustrates the scale of the potential dangers faced in an increasingly integrated global food chain. These emerging threats are likely to continue. Experience has shown that, overall, new diseases have been detected at the rate of about one per year for the past thirty years. For the future, much of the emphasis will need to be on improved surveillance, detection, anticipation of diseases and practices in the animal sector which can have an impact on human health. Production and processing methods can adversely affect the incidence of food borne illness attributable to Salmonella, Listeria or E-coli. The development of antibiotic resistance as a result of widespread use of antibiotics in production systems is a problem which is not yet fully under control.

21 Commission White Paper on nutrition, overweight and obesity-related health issues (2007). See: http://register.consilium.europa.eu/pdf/en/07/st15/st15612.en07.pdf 22 Based on: P. Cunningham (2003) – “After BSE – A Future for the European Livestock Sector”. European Association for Animal Production, Publication No. 108, 2003

-18-

3 THE KBBE FROM 2005 TO 2010: MAJOR ACHIEVEMENTS

3.1 The KBBE in EU research: building on European strengths and knowledge

3.1.1 Introduction

In 2004, the European Commission (DG Research) developed the concept of the Knowledge-Based Bio-Economy or KBBE. The idea behind it was that the European bioeconomy cannot compete on a global level by delivering only basic agricultural commodities, but needs to build on European strengths such as excellence in science, technology and industry to deliver innovation, world leadership in food technologies and products and animal breeding technologies, and having a strong chemical and manufacturing industry base. Several European Technology Platforms (ETP) were set up, and research in the area of the KBBE has been promoted and financed via the Commission’s Framework Programme 7 and several Member State initiatives. In September 2005, the Commission also organised the first KBBE stakeholder conference in Brussels23.

3.1.2 The EU Framework Programmes

3.1.2.1 Sixth Framework Programme (FP6)

Under FP6 (2002-2006), KBBE-related research was covered mainly through the Specific Programme "Integrating and Strengthening the European Research Area", Thematic Priority 5 (‘Food Quality and Safety’). This thematic priority accounted for 6.1% of the FP6 budget allocated to thematic research and for 4.2% of the overall FP6 budget (excluding EURATOM). It addressed the complete food chain, from farmer to consumer, and consisted of eight scientific areas (Epidemiology of food-related diseases and allergies; Impact of food on health; Traceability’ processes all along the production chain; Methods of analysis, detection and control; Safer and more environmentally friendly production methods and technologies and healthier foodstuffs; Impact of animal feed on health; Environmental health risks; The total food chain). Over the four years of the programme, the Food Quality and Safety priority spent 751 million Euro across 181 projects involving 3034 participants.

3.1.2.2 Seventh Framework Programme (FP7)

Under FP7 (2007-2013), KBBE-related issues are covered through the Specific Programme ‘Cooperation’, which constitutes the core of FP7, representing two thirds of the overall budget. It fosters collaborative research across Europe and other partner countries through projects by transnational consortia of industry and academia. Research is carried out in ten key thematic areas. The second key thematic area is ‘Food, agriculture and fisheries, and biotechnology24’, to which 1.9 billion Euro of funding has been allocated. This thematic area is built around three major activities:

• Sustainable production and management of biological resources from land, forest and aquatic environments

• Fork to farm: food (including seafood), health and well-being • Life sciences, biotechnology and biochemistry for sustainable non-food products

and processes

23 EU Conference report (2005) – New perspectives on the Knowledge-based Bio-economy 24 http://cordis.europa.eu/fp7/kbbe/

-19-

3.1.3 ERA-NETs

At EU level, research in the KBBE area is strengthened by the implementation of several ERA-Nets. The objective of the ERA-NET scheme is to develop and strengthen the coordination of public research programmes conducted at national or regional level. It provides a framework to network and mutually open national or regional research programmes, leading to concrete cooperation such as the development and implementation of joint programmes or activities. The ERA-NET scheme is expected to reduce the fragmentation of the European Research Area (ERA) by improving the coherence and coordination of national and regional research programmes. Some of the ERA-Nets with a clear link to the KBBE are: ERA-PG25 (Plant Genomics), ERASysBio26 (Systems Biology), EuroTrans-Bio27 (European Network of Transnational Collaborative RTD for SME Projects in the Field of Biotechnology), ERA-IB 28 (Industrial Biotechnology), WoodWisdom-Net 29 (wood material science and engineering), SAFEFOODERA 30 (food safety research programming), Marifish 31 (marine fisheries science and fisheries management), EMIDA32 (Emerging and Major Infectious Diseases of Livestock).

3.1.4 European Technology Platforms (ETPs)

The concept of European Technology Platforms (ETPs) was developed by the European Commission starting in 2003, with the first ETPs emerging in 2004. The aim of ETPs is to contribute to European competitiveness, boost research performance, concentrate efforts and address fragmentation across Europe. ETPs are characterised by addressing challenging issues for growth, embodying major technological advances in the medium to long term, creating community added-value, involving high research intensity and requiring a European approach. In the KBBE area, nine ETPs have emerged since then: Plants for the Future33, Food for Life34, Sustainable Chemistry35, Sustainable Farm Animal Breeding and Reproduction36, Forest-based Sector37, Biofuels38, Agricultural Engineering39, Aquaculture Technology and Innovation40, and Global Animal Health41. As these ETPs developed, they started to communicate and work together on issues of mutual interest, such as identifying synergies in their Strategic Research Agendas (SRAs). The European Commission started regular meetings with representatives from the KBBE ETPs and invited experts to discuss policy-related issues together. Today the 9 ETPs active in the KBBE sector are joining forces in BECOTEPS42, a Coordination and Support Action (CSA) funded by the European Commission’s Seventh Framework Programme. The main objectives of the BECOTEPS project are:

• To achieve closer and more coordinated collaboration between the KBBE ETPs

• To develop recommendations for better interaction between the KBBE ETP stakeholders along the product chains and the sustainability issue regarding multidisciplinary research, innovation and policy issues

25 http://www.erapg.org 26 http://www.erasysbio.net 27 http://www.eurotransbio.eu 28 http://www.era-ib.net 29 http://www.woodwisdom.net 30 http://www.safefoodera.net 31 http://www.marifish.net 32 http://www.emida-era.net 33 http://www.plantetp.org 34 http://etp.ciaa.be 35 http://www.suschem.org 36 http://www.fabretp.org 37 http://www.forestplatform.org 38 http://www.biofuelstp.eu 39 http://www.manufuture.org 40 http://www.eatip.eu 41 http://www.ifahsec.org 42 http://www.becoteps.org

-20-

• To encourage discussions between European and national, public and private, research and innovation initiatives.

3.1.5 EU Expert Groups

In addition to ERA-NETs and ETPs, a third category of pan-European KBBE-related networks consists of European Commission expert groups. The expert groups the most related to the KBBE are:

• The Advisory Group on Food, Agriculture and Biotechnologies: it’s mission is to give advice to the Commission services in the field of food, agriculture and biotechnology research and help to stimulate, if possible, the corresponding European research communities.

• The KBBE-Net: an expert Group of officials from Member States on the Knowledge Based Bio-Economy, coordinated by DG Research, supporting the Commission and the Member States to achieve a coordinated effort in the development and implementation of a research policy for a KBBE.

• The KBBE National Contact Point: the mission of this expert Group is to assist potential applicants for EC funding, to disseminate information on calls and policy initiatives, to raise awareness, to give feedback to the EC, etc.

• The EU Standing Committee for Agriculture Research: the Standing Committee on Agricultural Research (SCAR)43 was initially managed by DG AGRI and advised the Commission in the field of the coordination of research in agriculture. Since 2005 the “renewed” SCAR is managed by DG RTD, and looks beyond the narrow aspects of research relating to production. Today SCAR addresses the major sectors within the concept of a ‘Knowledge Based Bio-Economy’ (e.g. animal health and welfare; consumer issues relating to the quality, safety and security of food production and supply; issues of consumer behaviour towards food, nutrition, retailing and market; issues related to developments in non-traditional and non-food areas of agriculture activity including forestry).

3.2 Feedstock for food, feed, fuel and products

The aim of this section is to analyse how the productivity of biomass from agriculture, forestry and organic waste streams has increased over recent years and how research and innovation has also improved the performance of crops especially those with higher yields using lower amounts of fertilisers and water. In addition to this the European feedstock situation should be compared to the rest of the world and there is a need to analyse what has been done to make agriculture more sustainable. In this part of study we use the term feedstock to mean “biomass” according to the definition of the FAO from 2004: “Biomass means material of biological origin excluding material embedded in geological

formations and transformed to fossil.44”

The use of biomass (Renewable Raw Materials or RRM) as a feedstock for the production of fuels, materials, chemicals and other biobased products can save fossil resources and reduce negative impacts on the environment. In particular, green house gas emissions could be reduced by bio-based products providing substitutes for products based on crude oil. It can also support the agricultural and forestry sectors and lead to innovations in, for example, biomaterials or biobased chemicals. For the chemical industry – other than for

43 http://ec.europa.eu/research/agriculture/scar/index_en.html 44 FAO (2004) – UBET: Unified Bioenergy Terminology. See http://www.fao.org/docrep/007/j4504e/j4504e00.htm

-21-

fuels and energy - RRM are the only current alternative source of carbon to crude oil for the production of chemical products45. In view of these opportunities a KBBE is widely needed and wanted in Europe. This leads to several needs especially with regards to the need for feedstock because if the bio-based industry is to achieve its potential the supply of feedstock is a key issue to be addressed (see 4.2).

3.2.1 The feedstock situation in Europe

The current and future amount of biomass feedstock for food, feed, energy and industrial material use in Europe as well as the question of the available land for food and non-food crops is a contentious issue and remains an area in need of in depth analysis. Although many studies, assessments and scenarios on biomass potentials in Europe as a whole and for different countries already exist their conclusions differ widely.

Figure 1: Assessment for recent biomass supply, use and future demand in Europe46

The FP7 project “Biomass Energy Europe” (BEE), focusing on the energy use and future demands of bioenergy, analyses several recent studies on biomass resources in a meta analysis for their “Status of Biomass Resource Assessments”47. The aim of this project is to harmonize the existing biomass resource availability assessments for Europe to improve the consistency, accuracy and reliability of the assessments. The project analyzed the results of 57 different data sources including 30 key studies and 9 further studies on three different types of biomass for the bio-based industry:

45 Jering A., Günther J., Raschka A., Carus M., Piotrowski S., Scholz L. (2010) - Use of renewable raw materials with special emphasis on chemical industry. ETC/SCP report 1/2010, European Environmental Agency. 46 Jossart J.-M. (2009) - Development of the bioenergy sector. Presentation at the JRC Workshop “Biomass resource assessment”, Eberswalde 8-9 December 2009. 47 First results are published in: Rettenmaier N., Reinhardt G., Schorb A., Köppen S., von Falkenstein E. et al. (2008) - Status of Biomass Resource Assessments, Version 1. IFEU and BEE project, Heidelberg. Despite this there are different presentations available on the topic, e.g. Dees M., Rettenmaier N. (2009) - Overview of European studies of biomass resource assessment. Presentation at the JRC Workshop “Biomass resource assessment”, Eberswalde 8-9 December 2009.

-22-

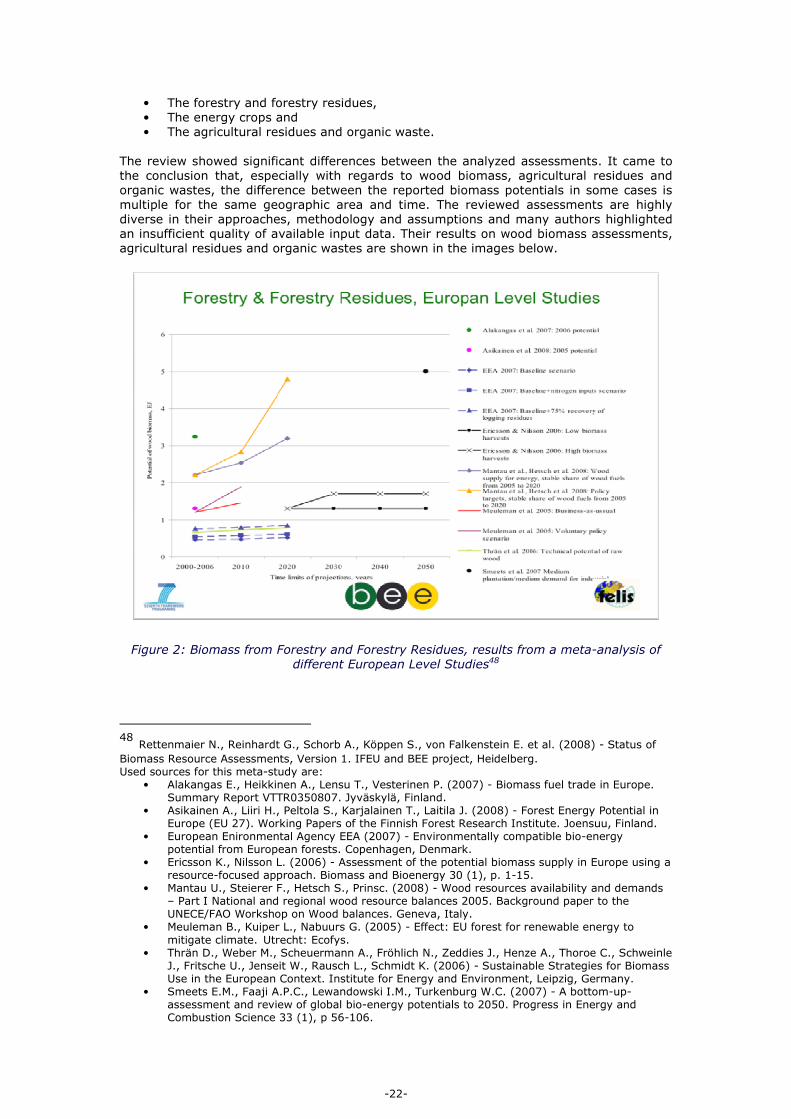

• The forestry and forestry residues, • The energy crops and • The agricultural residues and organic waste.

The review showed significant differences between the analyzed assessments. It came to the conclusion that, especially with regards to wood biomass, agricultural residues and organic wastes, the difference between the reported biomass potentials in some cases is multiple for the same geographic area and time. The reviewed assessments are highly diverse in their approaches, methodology and assumptions and many authors highlighted an insufficient quality of available input data. Their results on wood biomass assessments, agricultural residues and organic wastes are shown in the images below.

Figure 2: Biomass from Forestry and Forestry Residues, results from a meta-analysis of

different European Level Studies48

48 Rettenmaier N., Reinhardt G., Schorb A., Köppen S., von Falkenstein E. et al. (2008) - Status of

Biomass Resource Assessments, Version 1. IFEU and BEE project, Heidelberg. Used sources for this meta-study are:

• Alakangas E., Heikkinen A., Lensu T., Vesterinen P. (2007) - Biomass fuel trade in Europe. Summary Report VTTR0350807. Jyväskylä, Finland.

• Asikainen A., Liiri H., Peltola S., Karjalainen T., Laitila J. (2008) - Forest Energy Potential in Europe (EU 27). Working Papers of the Finnish Forest Research Institute. Joensuu, Finland.

• European Enironmental Agency EEA (2007) - Environmentally compatible bio-energy potential from European forests. Copenhagen, Denmark.

• Ericsson K., Nilsson L. (2006) - Assessment of the potential biomass supply in Europe using a resource-focused approach. Biomass and Bioenergy 30 (1), p. 1-15.

• Mantau U., Steierer F., Hetsch S., Prinsc. (2008) - Wood resources availability and demands – Part I National and regional wood resource balances 2005. Background paper to the UNECE/FAO Workshop on Wood balances. Geneva, Italy.

• Meuleman B., Kuiper L., Nabuurs G. (2005) - Effect: EU forest for renewable energy to mitigate climate. Utrecht: Ecofys.

• Thrän D., Weber M., Scheuermann A., Fröhlich N., Zeddies J., Henze A., Thoroe C., Schweinle J., Fritsche U., Jenseit W., Rausch L., Schmidt K. (2006) - Sustainable Strategies for Biomass Use in the European Context. Institute for Energy and Environment, Leipzig, Germany.

• Smeets E.M., Faaji A.P.C., Lewandowski I.M., Turkenburg W.C. (2007) - A bottom-up-assessment and review of global bio-energy potentials to 2050. Progress in Energy and Combustion Science 33 (1), p 56-106.

-23-

Figure 3: Biomass from agricultural residues and organic wastes, results from a Meta-

analysis of different European Level Studies 49

49 Rettenmaier N., Reinhardt G., Schorb A., Köppen S., von Falkenstein E. et al. (2008) - Status of Biomass Resource Assessments, Version 1. IFEU and BEE project, Heidelberg Used sources for this meta-study are:

• Ericsson K., Nilsson L. (2006) - Assessment of the potential biomass supply in Europe using a resource-focused approach. Biomass and Bioenergy 30 (1), p. 1-15.

• Siemons R. Vis M., van den Berg D., Mc Chesney I., Whiteley M., Nikolaou N. (2004) - Bio-energy’s role in the EU Energy market, a view of developments until 2020. BTG Report, Enschede, the Netherlands.

• De Noord M., Beurskens L.W.M, de Vries H.-J. (2004) - Potentials and costs for renewable electricity generation, a data overview (Chapter 6). ECN Report, Petten, the Netherlands.

• Krause H., Oettel E. (2007) - REDUBAR: Investigations targeted to the creation of legislative instruments and the reduction of administrative barriers for the use of biogas for heating, cooling and power generation. Project report, DBI Gas- und Umwelttechnik GmbH, Leipzig, Germany.

• Edwards R.A.H., Suri A., T.A. Huld, J.F. Dallemand (2005) - GIS-based assessment of cereal straw energy resource in the European Union. Proceedings of the 14th European Biomass Conference & Exhibition. Biomass for Energy, Industry and Climate Protection, 17-21 October 2005, Paris, France.

• DeWit M.P., Faaji A.P.C. (2008) - Biomass Recourses Potential and related Costs. Assessment of the EU-27, Switzerland, Norway and Ukraine. REFUEL Report, Utrecht University, The Netherlands.

• Ganko E., Kunikowski G., Pisarek M., Rutkowska-Filipczak M., Gumeniuk A., Wróbel A. (2008) - Biomass resources and potential assessment. Final report WP 5.1 of RENEW project, Institute for Fuels and Renergable Energy, Warsaw.

• Nikolaou A., Remrowa M., Jeliazkow I. (2003) - Biomass availability in Europe. Final report CRES, BTG, ESD, Athens, Greece.

• Thrän D., Weber M., Scheuermann A., Fröhlich N., Zeddies J., Henze A., Thoroe C., Schweinle J., Fritsche U., Jenseit W., Rausch L., Schmidt K. (2006) - Sustainable Strategies for Biomass Use in the European Context. Institute for Energy and Environment, Leipzig, Germany.

-24-

Currently, the data available on the industrial material use of biomass as feedstock in the EU is limited in both its availability and accuracy. Furthermore on a national level there are only a few studies, mainly for Germany, France, the Netherlands and Great Britain, concerning the material use of forestry and agricultural feedstocks and demands. Thanks to a study on the industrial material use in Germany by the nova-institute a good database on the uses of RRM in German industry is available50. In addition, the national Non-Food Crops Centre (NNFCC) and Arthur D. Little Limited produced a market analysis of key renewable materials and product sectors for Great Britain51 and Bewa provided a study on the current and prospective markets for industrial bioproducts in France, excluding wood and pulp, textiles and health products52. For the Netherlands Nowicki et al. published a state-of-the-art assessment on the bio-based economy focusing on the market value of bio-based products53. Additionally, data is available for certain industries such as the pulp and paper industry from CEPI or the wood industry as a whole for certain periods. As a whole the feedstock assessments for industrial material use must be the same as in the bioenergy feedstocks discussed above because all available feedstocks and land can be used for the energy production as well as for bio-based products. One problematic area in the calculation of industrial material use is evaluation on the basis of energy units (Joules) as opposed to mass units (tons) as it is difficult to compare these two measurements.

3.2.2 Availability of arable land

According to a recent FAO study using longer term population and income projections, global food production needs to increase by more than 40% by 2030 and by 70% by 2050 compared to average 2005-07 levels54. Increased food production will either result from increased yields or from area expansion. Theoretically, according to the OECD/FAO Agricultural Outlook55, some 1.6 billion ha could be added to the current 1.4 billion ha of cropland. These 1.6 billion ha are referred to as the Net Land Balance (NLB), which is the additional available area for crop production after excluding areas allocated to either forests, urban areas or protected areas. Yet, historically expansion of arable land area has been slow, and bringing more marginal land into production could involve considerable investment and lower average yields, while possibly incurring social and environmental costs56. Over half of this NLB is located in Africa and in Latin America. These regions account for most of the available land that has the highest suitability class for rain-fed crop production. Also historically, expansion of arable land has since the 1960s mainly taken place in Africa and Asia while it has continually declined in Europe. However, in practice bringing the additionally available land into production is in many cases hindered by insufficient infrastructure, lack of capital and poor transmission of price incentives to farmers.