Embed Size (px)

Citation preview

The Impact of the Affordable Care Act on Safety Net

Providers and their Patients: Opportunities for Outreach

and Education

What We’ll Cover

• Expansion of Health Insurance Coverage

• Application and Eligibility • Consumer Assistance Resources• What Providers Can do to Help • Resources for Consumers and

Providers

Expansion of Insurance Coverage

Many uninsured patients will become eligible for affordable health care coverage beginning in 2014.

The Affordable Care Act:• Strengthens private insurance for consumers.• Creates a Marketplace in each state where individuals

and small businesses can shop for insurance.• Provides financial help for many people to better afford

insurance through the Marketplace.• Gives states the opportunity to expand Medicaid coverage

to low-income adults.

Health Insurance Marketplace

• Every state will have a Marketplace (aka Exchange) where individuals and small businesses can shop for and purchase private health insurance.

• All options will be in one place, with clear language and apples-to-apples comparisons about prices and benefits.

• Plans offered through the Marketplace are called Qualified Health Plans (QHPs).

Enrollment starts October 1, 2013 Coverage starts January 1, 2014

Enrollment starts October 1, 2013 Coverage begins as early as January 1, 2014

Advantages of the Marketplace

• Helps enhance competition in the health insurance market.

• Increases Affordability through premium tax credits, cost sharing reductions, or public insurance programs.

• Ensures Quality through QHPs that must meet basic standards, including quality standards, consumer protections, and access to an adequate range of clinicians.

• Makes Costs Clear by providing information about prices and benefits in simple terms consumers can understand, so they don’t have to guess about costs.

Marketplace Establishment

Source: Kaiser Family Foundation. Status of State Health Insurance Exchange Decision, as of July 1, 2013, available at http://kff.org/health-reform/state-indicator/state-decisions-for-creating-health-insurance-exchanges-and-expanding-medicaid/#

State-Based (SBM):16 States & DC are setting up & managing their own Marketplaces.

State Partnership (SPM): 7 States are working in partnership with the federal government.

Federally-Facilitated (FFM): In 27 States the federal government is setting up the Marketplace.

Help to Pay for Qualified Health Plan Costs

• 90% of the uninsured will qualify for some form of financial assistance based on family income and size.

• Eligible persons can get premium tax credits and/or purchase plans with lower cost-sharing (e.g., co-pays and deductibles).

% of Federal Poverty Level (FPL)

Individuals household income*

Family of 4 household income*– Discounted Premiums– 100-400%– $11,490 - $45,960 – $23,550 - $94,200– Reduced Cost-sharing– 100-250%– $11,490 - $28,725 – $23,550-$58,875

% of Federal Poverty Level (FPL)

Individuals household income*

Family of 4 household income*

Premium Tax Credits 100-400% $11,490 -

$45,960 $23,550 - $94,200

Reduced Cost-sharing 100-250% $11,490 -

$28,725 $23,550-$58,875

*Based on 2013 Federal Poverty Guidelines

Medicaid Expansion

• States have the option to expand Medicaid eligibility to adults ages 19-64 with incomes up to 133% of the Federal Poverty Level (FPL)*.

• One streamlined application for Medicaid and Marketplace private health plans.

• Shifts to simplified way of calculating income (MAGI) to determine Medicaid/CHIP eligibility.

• 100% federal funding for newly Medicaid eligible 2014-2016 phased down to 90% by 2020.

• States have no deadline to decide if they are going to expand.

* ($15,282/year for an individual, $31,322/year for a family of 4)

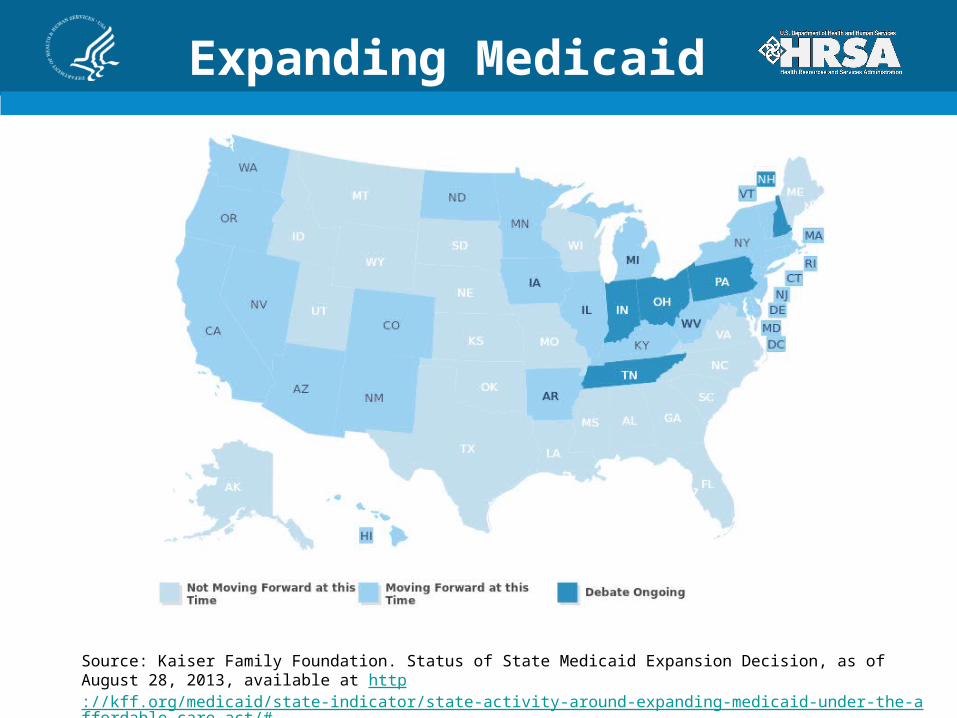

Expanding Medicaid

Source: Kaiser Family Foundation. Status of State Medicaid Expansion Decision, as of August 28, 2013, available at http://kff.org/medicaid/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/#

What If a State Does Not Expand Medicaid?

• Individuals whose income is more than 100% of the federal poverty level* will be able to buy health insurance in the Marketplace and may be eligible for subsidies to help pay for coverage.

• Individuals whose income is less than 100% of the federal poverty level* will be able to get insurance in the Marketplace, but are not eligible for financial assistance.– These individuals may be able to get an exemption from having to pay

a fee for not having health insurance coverage.

• Even if a state is not expanding Medicaid, individuals should apply for coverage to see if they qualify.

• Find out if your state is expanding Medicaid at HealthCare.gov.

* $11,500 per year as a single person (about $23,500 for a family of 4

Eligibility Cheat Sheet

Income level% FPL

Eligible :

For Medicaid?

To purchase insurance through Market-places?

For insurance purchased through the Marketplace:

Premium Tax

Credits

Reduced cost-

sharing

0 to 100%

Currently eligible people will generally remain eligible.

Individuals with incomes up to 138% FPL will be able to enroll in

Medicaid in states that implement Medicaid expansion

YesNo (Exception:

legal immigrants)

100% - 138% Yes

Yes*138% - 250%

Generally not (although some States cover some individuals)

Yes

250% - 400% No Yes Yes* No

Above 400% No Yes No No

Not lawfully present

No (except emergency Medicaid) No No No

* unless eligible for other minimum essential coverage as defined in IRC 5000A(f)

Outreach and EnrollmentNational Snapshot

• 41 million eligible uninsured• 17.8 million 18-35 years old

– 58% male– 26% Latino– 18% African American

• CBO projects 7 million to enroll in Marketplaces in 2013-2014.

• HHS has primary responsibility for outreach in 29 states

• Poverty Level

• 20% have not graduated High School

• 3.8 million rely on Spanish

• One million rely on some other language

< 138% 139-400% 400%+

54%

38%

8%

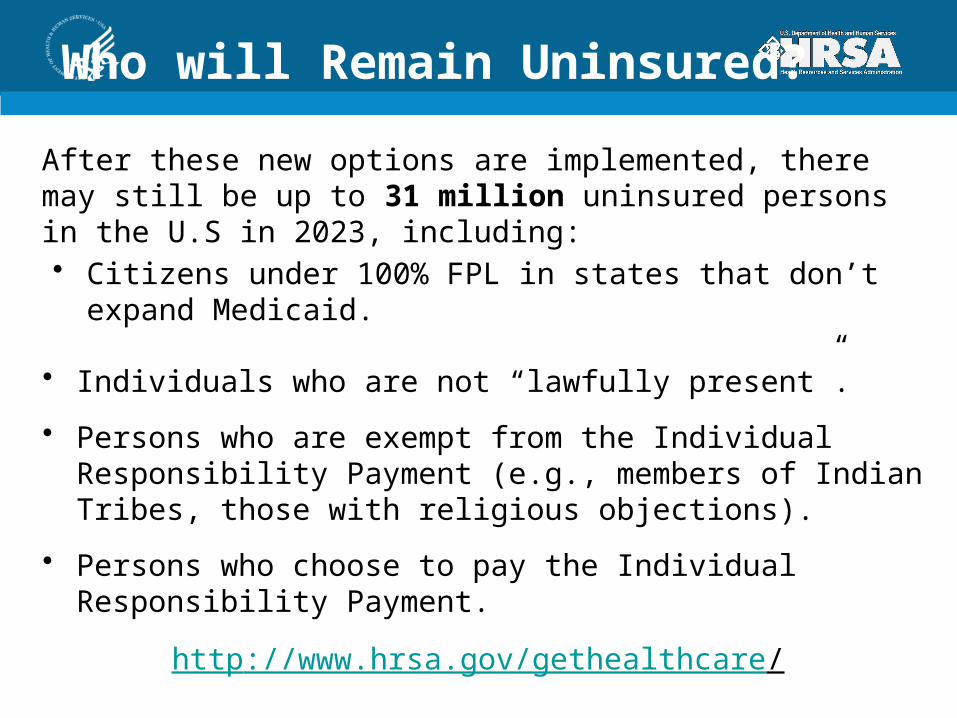

Who will Remain Uninsured?

After these new options are implemented, there may still be up to 31 million uninsured persons in the U.S in 2023, including:• Citizens under 100% FPL in states that don’t expand

Medicaid.

• Individuals who are not “lawfully present”.

• Persons who are exempt from the Individual Responsibility Payment (e.g., members of Indian Tribes, those with religious objections).

• Persons who choose to pay the Individual Responsibility Payment.

http://www.hrsa.gov/gethealthcare/

Application and Eligibility

One streamlined application to apply for Medicaid, the Children’s Health Insurance Program (CHIP), the new Health Insurance

Marketplace, and tax credits that will help pay for premiums in the Marketplace.

Submit single,

streamlined

application to the Marketpla

ce

Verify and

determine eligibility

• Online• Phone• Mail• In Person

Supported by Data Services Hub

Eligible for Marketplace or Medicaid/CHIP

Enroll (Marketplace)

Enroll (Medicaid/CHIP)

Timelines for Enrolling

• Initial Open Enrollment starts October 1, 2013 and ends March 31, 2014 with QHP coverage effective as early as January 1, 2014.

• Annual Open Enrollment: October 15, 20xx-December 7, 20xx• Special Enrollment Periods available. • Medicaid enrollment will continue to occur throughout the year.

Enrollment Assistance

Call 24x7Support for 150 Languages

In Person

Medicaid/CHIPOnline/phone/in person

WrittenApplications inEnglish/SpanishNotices & letters

PlansPayment online/phoneOngoing customer serviceMobile

24x7Email & text updates

Online24x7WebchatEnglish/Spanish siteUser Account AssistanceAPI available for other sitesSyndicated content

In-Person Consumer Assistance Framework

Two categories of in-person consumer assistance are available:

• Marketplace Assisters

• Marketplace Educators

Marketplace Assisters

Assisters

•Navigators•In-person Assisters

•SBM (optional)•Consumer SPM (required)

•Certified Application Counselors (CACs)

•Agents/Brokers

•Call Center Representatives

Listed on www.HealthCare.gov in Local Help & Customer Service

Referrals

• Navigator Grant program sponsored by each Marketplace to provide consumer assistance.

• Navigators have a number of responsibilities including, but not limited to: – Maintaining expertise in eligibility, enrollment, and program

specifications and conduct public education activities.– Providing accurate and impartial information about QHPs and

other health programs such as Medicaid and CHIP.– Facilitating selection of a QHP.– Providing information in a manner that is culturally and

linguistically appropriate and accessible for people with disabilities.

• Navigators must be trained and certified.

Navigator Program

• Transitional program to supplement Navigators.– Optional for State-based Marketplace.– Required for State- Partnership Marketplace.

• In-Person Assisters perform generally same functions as Navigators.– In most cases, have similar role and responsibilities.

• In-Person Assisters have comprehensive training and certification requirements similar to Navigator program.

In-Person Assisters

• CACs provide assistance in every Marketplace. – Educate consumers about insurance affordability

programs and coverage options.– Help consumers apply for coverage through the

Marketplace.– Have more limited role than other assisters.

• Do not receive federal Marketplace grant money– May receive other private, state, or federal funding

Certified Application Counselors (CAC)

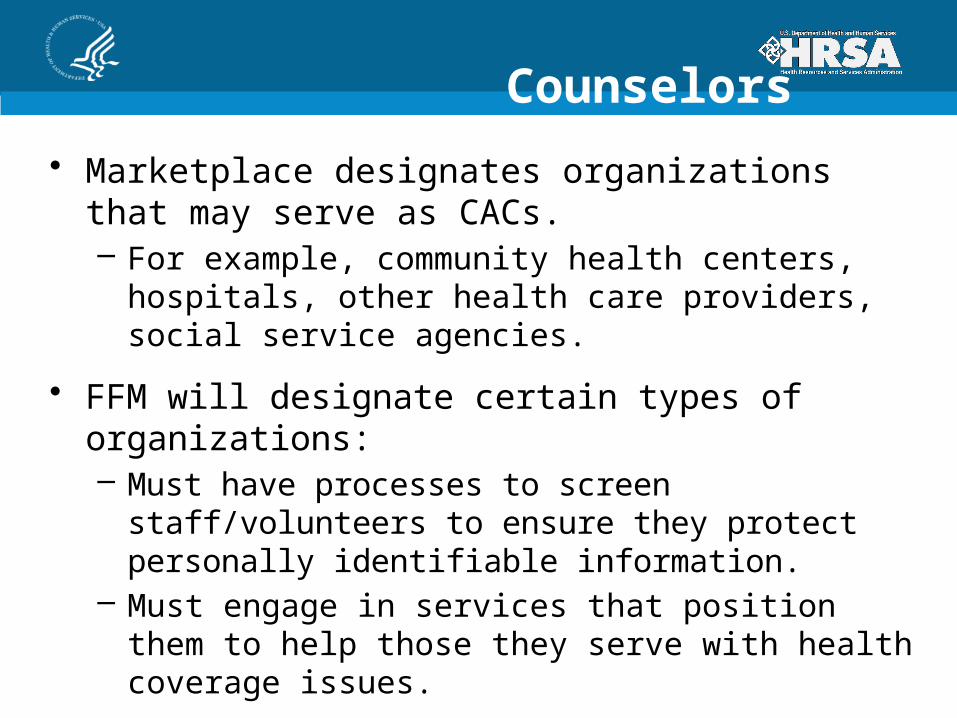

Certified Application Counselors

(CAC)• Marketplace designates organizations that may serve

as CACs.– For example, community health centers, hospitals, other

health care providers, social service agencies.

• FFM will designate certain types of organizations:– Must have processes to screen staff/volunteers to ensure

they protect personally identifiable information.– Must engage in services that position them to help those

they serve with health coverage issues.

• State-based Marketplace may follow FFM guidance for designating organizations or establish own processes.

• May apply to be a designated organization for FFM or SPM:

http://marketplace.cms.gov/help-us/cac-apply.html

• CAC Training is available at:– Link to CAC training:

https://marketplace.medicarelearningnetworklms.com – Link to CAC training content:

http://marketplace.cms.gov/training/get-training.html

CAC Application & Training

Marketplace Educators

Educators

•Partners & Stakeholders

•Local government branches & employees

•School administration & staff

Then Direct to Customer Service

Website

Call Center

Assister

Aren’t displayed in Find Local Help tool and aren’t consumer referral

points – educators refer consumers

Champions for Coverage

• A new way to recognize organizations who are engaged in outreach and education efforts.

• Organizations can fill out an online form on marketplace.cms.gov/help-us/champion.html to become publically recognized as a “Champion.”

• Outreach activities can include: Sending emails to their networks about the Marketplace. Posting the HealthCare.gov widget on their website. Recording and sending out PSAs about the Marketplace. Hanging posters and/or giving out fact sheets and brochures about the

Marketplace. Hosting a conference call, webinar, or another educational event about

the Marketplace.

Recap: Marketplace Consumer Assistance

State-Based Marketplace

Partnership Marketplace

Federally-Facilitated

Marketplace

Navigators Yes Yes Yes

In-Person Assisters

Only if state elects to

Yes No

Certified Application Counselors

Yes Yes Yes

Educators Yes Yes Yes

What Providers Can Do

1. Educate patients: • What the options are: Many individuals who stand to

benefit under the expansion are not aware of their options.• How insurance works: Many newly-eligible individuals

would benefit from education on how insurance works (e.g., how cost-sharing works, what a provider network is).

2. Sign up to be a Champion for Coverage.

3. Partner with local organizations that provide application assistance to:• Offer on-site application assistance.• Develop a plan for referring patients to assistors.

What Providers Can Do

4. Assist patients with applying for and enrolling in health coverage:

• Apply to be a Certified Application Counselor.• Accessing the eligibility and enrollment system

(ideally through computer kiosks; also accessible via the phone or mail.)

• Working their way through the application.• Understanding and evaluating factors they should

consider when selecting a plan. For example:• Does it cover the Rx I need? • Does it include the provider(s) I want to see?

Healthcare.gov

• Healthcare.gov is where consumers can go to:– Learn about their health insurance options; – Get accurate information on different plans; – Apply for and enroll in coverage; and/or– Get directed to the Marketplace in their state.

• Assisters will be listed on the site so consumers can find local help.

• Twitter: @HealthCareGov• Facebook.com/Healthcare.gov

Marketplace.cms.gov

Get the latest resources to help people apply, enroll, and get coverage in 2014

• 1-800-318-2596 (TTY 1-855-889-4325)– Assistance available 24/7– English, Spanish, and 150 languages

• June – September– Call Center will provide general information to consumers

and employees of SHOP employers. • Starting in October

– Call Center will help with eligibility, enrollment, and referrals.

• State-based Marketplaces will have their own call center and consumers will be referred as appropriate

National Marketplace Call Center

• HRSA Affordable Care Act Website– www.hrsa.gov/affordablecareact

• Provider Marketplace Toolkit– www.hrsa.gov/affordablecareact/toolkit.html

• HIV/AIDS Bureau Affordable Care Act Website– http://hab.hrsa.gov/affordablecareact

HRSA Resources

Key Points to Remember

• The Marketplace is a new way to find and buy health insurance.

• Consumers in all 50 states will have better health insurance choices when open enrollment begins on Oct. 1, 2013.

• There is financial help for working families and other people with limited income.

• There is assistance available to help consumers get the best coverage for their needs through HealthCare.gov, the call center, and in-person assistance.

Q&A