Embed Size (px)

Citation preview

Giovanni GomezRegional Coordinator of Outreach

The Affordable Care Act:Illinois Health Insurance

Marketplace

What is the Affordable Care Act?

Signed into law on March 23, 2010 by President Obama.

Includes provision for states to create Health Insurance Marketplaces for individuals, families, and small employers to purchase affordable plans

Consumers can sign up starting Oct. 1, 2013 Coverage starts Jan. 1, 2014

What does the ACA do now?

Extend dependent eligibility to age 26Children with pre-existing conditions cannot

be denied coverageElimination of lifetime limits on coveragePreventive care coveredImplementation of 80/20 rule that requires

insurance companies spend at least 80% of premiums on health care

What does the ACA do in 2014?

Equal premium rates for men and womenNo one can be denied because of a pre-

existing conditionThe extension of MedicaidThe establishment of the Marketplace

You may qualify for assistance to help with health care premiums and lower your out-of-pocket costs

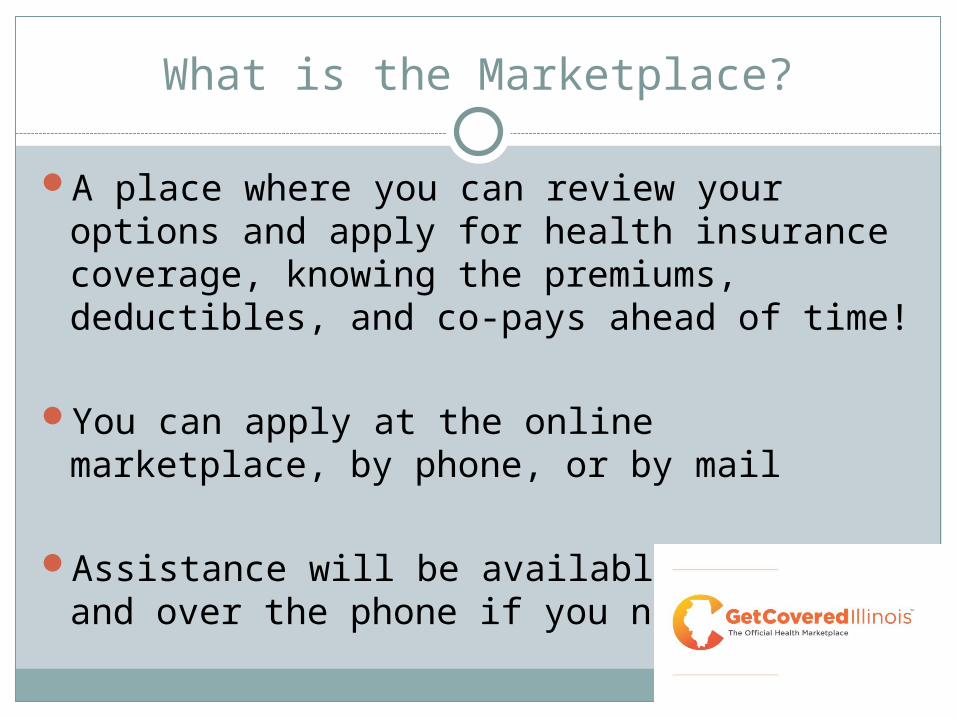

What is the Marketplace?

A place where you can review your options and apply for health insurance coverage, knowing the premiums, deductibles, and co-pays ahead of time!

You can apply at the online marketplace, by phone, or by mail

Assistance will be available in-person and over the phone if you need it.

How will it work?

One Application ProcessThe Marketplace and ABE

Eligibility for Individuals

U.S. Citizen;U.S. National;Or otherwise lawfully present during the

intended enrollment period.

Not incarceratedResident of Illinois

Who is Eligible for Tax Credits?

Individuals and families with income between 100% to 400% FPL Must be US citizens or lawfully present in the US Must not be eligible for other “minimum essential

coverage” If your offered insurance at work and it fills all the

requirements

Lawfully residing immigrants with incomes below 100% FPL who are not eligible for Medicaid because of their immigration status

Who is Eligible for Tax Credits?

FPL

400%

300%

200%

100%

300%

200%

133%

Marketplace

Children(All Kids)

Pregnant Women

Parents People w/ Disabilities

Adults w/o Children

Unsubsidized

SubsidizedPremiums on sliding

scale.

Marketplace Plans

Must include Essential Health Benefits: Ambulatory patient services Emergency services Hospitalization Maternity and newborn care Mental health and substance use disorder services Prescription drugs Rehabilitative and habilitative services and devices Laboratory services Preventive and wellness services including chronic

disease management Pediatric services including oral and vision care

Marketplace Plans

Medaled plans: Medal level signifies actuarial value, not content, of

plan Platinum Gold Silver Benchmark Plan Bronze

Catastrophic coverage will be available to people under 30 and those who qualify for the individual exemption.

Example: Single Individual

John 24 years old Income of $22, 980 (200%FPL) Expected Contribution: 6.3% or $1,448

Plans Covering John Gold: $5,200 Silver Plan: $5,000 Benchmark Plan Bronze: $4,800

Premium Credits $5,000 - $1,448= $3,552

*These are not official prices*

$1,448

$3,552

$3,552

$3,552$3,552

$1,648

$1,848

$1,248

Eligibility for Individuals

You could get a break on costs: Consumers between 100% and 400% FPL are eligible for

tax subsidies that are applied to premiums.

Consumers between 100%-250% FPL can receive cost-sharing reductions. Must be enrolled in a silver plan from the marketplace Must be eligible for the tax credit

Both are on a sliding scale. Consumers also receive a cap on out-of-pocket spending.

Eligibility for Individuals

Those who receive employer-provided insurance that meets ACA standards of value and affordability can apply for coverage on the Marketplace, but they are not eligible for tax subsidies.

Who Can Help You Through The Process?

The IL Assistor Program The In-person Counselor program (IPCs) & Navigators No Wrong Door Policy

Certified Application Counselors (CACs)

They will help you every step of the way.