Embed Size (px)

Citation preview

The Hull, the Feasible Set, and the Risk Surface A Review of the Portfolio Modelling Infrastructure in R/Rmetrics

Diethelm Würtz

g /

Institute for Theoretical Physics ETH ZurichInstitute for Theoretical Physics ETH ZurichCurriculum for Computational Science ETH Zurich

Finance Online & Rmetrics Association Zurich

UseR! Gaithersburg, July 2010

Joint work withYohan Chalabi, William Chen, Christine Dong, Andrew Ellis,

Sebastian Pérez Saaibi, David Scott, Stefan Theussl

www.itp.phys.ethz.ch | www.rmetrics.org | www.finance.ch

Overview

Part I Rmetrics and Our Visions

Part II Portfolio Analysis with R/Rmetricsy /

Part III New DirectionsPart III New Directions

2

Part I

Who is Rmetrics and what are our Visions ?

Rmetrics is a non profit taking Association under Swiss law working in the public interest in the field of measuring and analyzing risks in finance and related fields

W t Ed ti l d T hi Pl tf• We operate an Educational and Teaching Platform• We offer an R Code Archive and a Public Tools Platform• We started to Build a Public Stability and Risk Data BaseWe started to Build a Public Stability and Risk Data Base

about 50 packages and 25 developers on r‐forge

3

Vision No 1: An Open Educational and Teaching PlatformAn Open Educational and Teaching Platform

Rmetrics Open Source Teaching Platform and Community

• Software Packages Serving as Code Archive• Datafeeds for Public Available Data on the WebDatafeeds for Public Available Data on the Web• High Quality Documentation R/Rmetrics eBooks• Support Student Internships for Training at ETHZ• Support Student Internships for Training at ETHZ• Rmetrics Meielisalp Summer School• Rmetrics Meielisalp User and Developer Workshop• Rmetrics Meielisalp User and Developer Workshop

4

Vision No 2: An Open Code ArchiveAn Open Code Archive

Why we Maintain an R Code Archive

• We need a platform which provides algorithms and software tools to measure and control the risk andsoftware tools to measure and control the risk andunstabilities of financial investments.

• We need more graphical tools which allow for better views on the performance risk attributions andviews on the performance, risk attributions and stability of financial investments.

5

Vision No 3: An Open Stability and Risk Data PlatformAn Open Stability and Risk Data Platform

Why we Create a Stability and Risk Data Platform

• Financial stability and risk data are in the public interest.

• We need an independent data base and platform which allows to make investments more transparentwhich allows to make investments more transparent and reproducible for everybody.

• We believe it is time to start with such a project, feelfree to join us.j

6

Part II

Portfolio Design with R/Rmetrics• What is a Financial Portfolio?What is a Financial Portfolio?• Portfolio Objectives and Constraints• Rmetrics Portfolio Solver Interfaces

ExamplesAb l t d R l ti Ri k Obj ti• Absolute and Relative Risk Objectives

• Covariance Matrix Estimation• Extreme Risk MeasuresExtreme Risk Measures• Estimation Risk/Problems

7

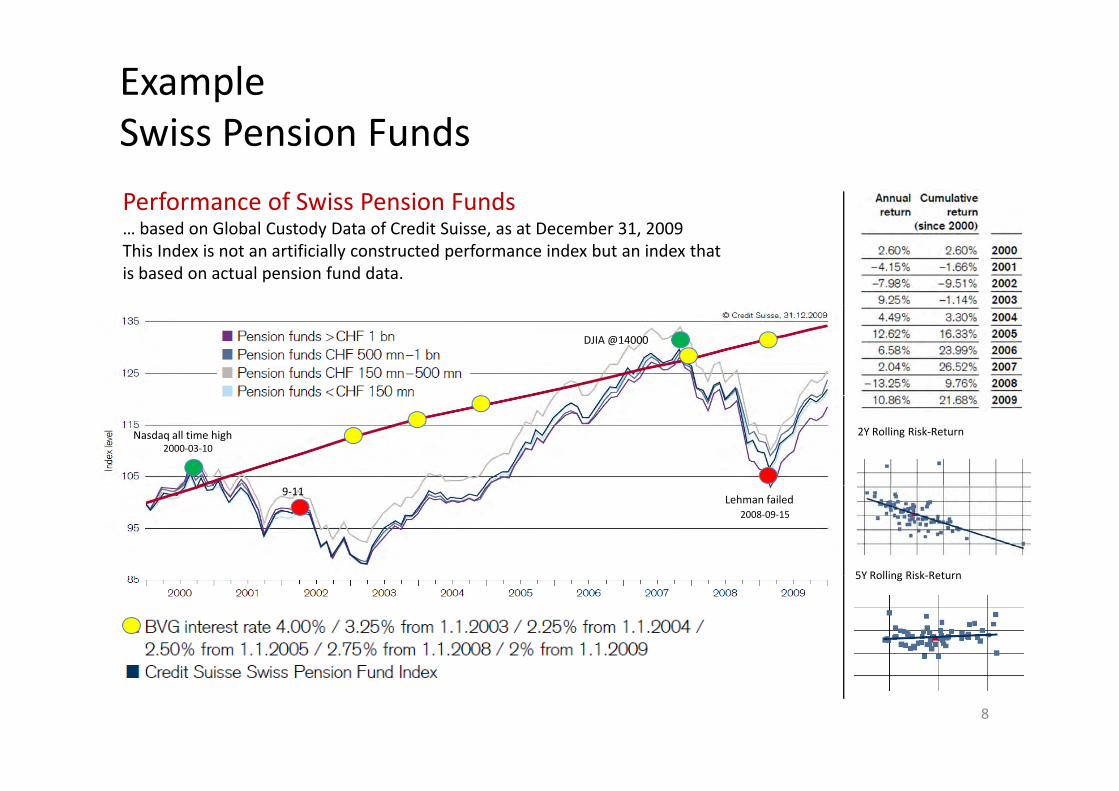

ExampleSwiss Pension FundsSwiss Pension FundsPerformance of Swiss Pension Funds

ExampleSwiss Pension Fund Portfolio

… based on Global Custody Data of Credit Suisse, as at December 31, 2009This Index is not an artificially constructed performance index but an index that is based on actual pension fund data.

DJIA @14000

Nasdaq all time high2000‐03‐10

2Y Rolling Risk‐Return

Lehman failed9‐11

2008‐09‐15

5Y Rolling Risk Return5Y Rolling Risk‐Return

8

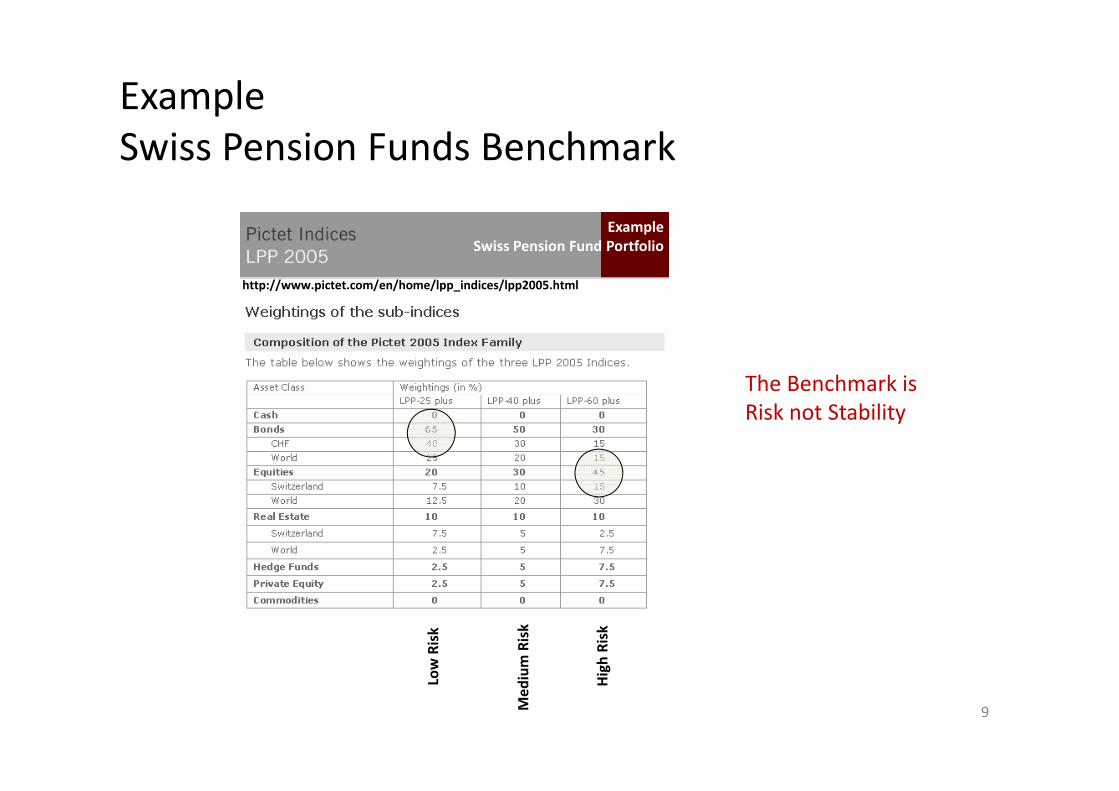

ExampleSwiss Pension Funds Benchmark

ExampleSwiss Pension Fund Portfolio

http://www.pictet.com/en/home/lpp_indices/lpp2005.html

The Benchmark is Risk not Stability

w Risk

m Risk

h Risk

9

Low

Med

ium

Hig

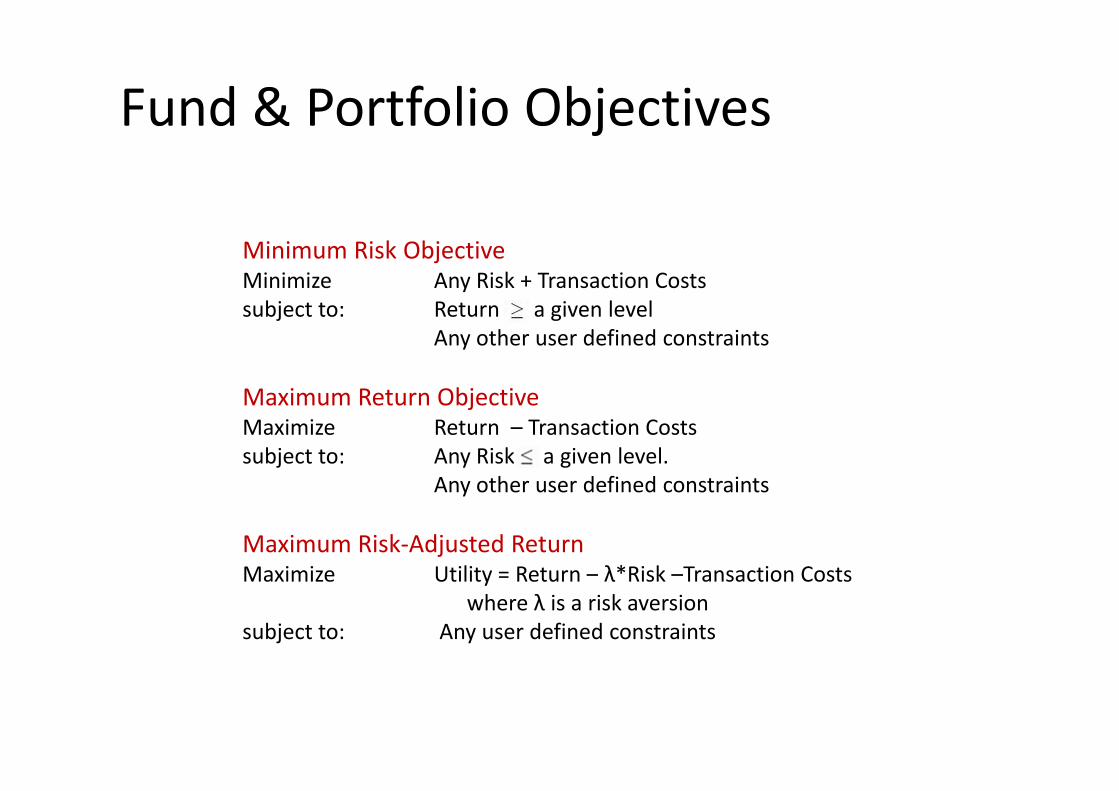

Fund & Portfolio Objectivesj

Minimum Risk ObjectiveMinimize Any Risk + Transaction Costssubject to Return > a given levelsubject to: Return > a given level

Any other user defined constraints

Maximum Return ObjectiveMaximum Return ObjectiveMaximize Return – Transaction Costssubject to: Any Risk < a given level.

Any other user defined constraintsAny other user defined constraints

Maximum Risk‐Adjusted ReturnMaximize Utility = Return – λ*Risk –Transaction CostsMaximize Utility = Return – λ Risk –Transaction Costs

where λ is a risk aversionsubject to: Any user defined constraints

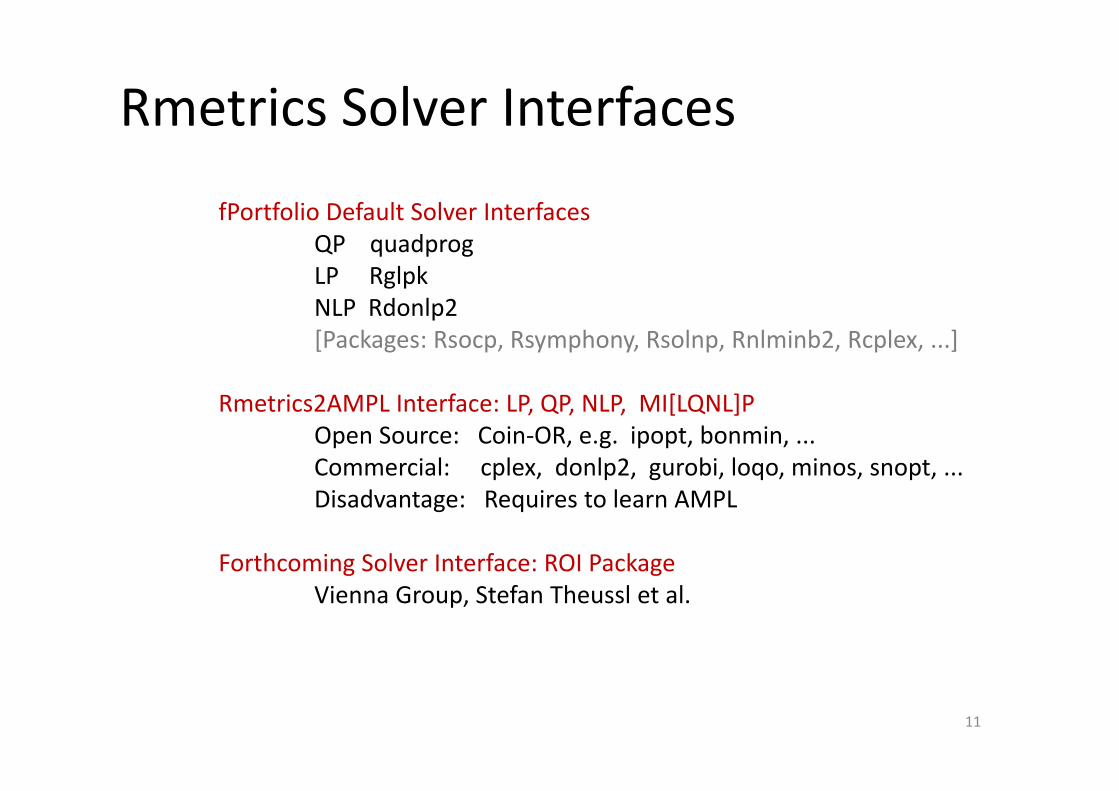

Rmetrics Solver Interfaces

fPortfolio Default Solver InterfacesfPortfolio Default Solver Interfaces QP quadprogLP Rglpk NLP Rdonlp2NLP Rdonlp2 [Packages: Rsocp, Rsymphony, Rsolnp, Rnlminb2, Rcplex, ...]

R i 2AMPL I f LP QP NLP MI[LQNL]PRmetrics2AMPL Interface: LP, QP, NLP, MI[LQNL]POpen Source: Coin‐OR, e.g. ipopt, bonmin, ... Commercial: cplex, donlp2, gurobi, loqo, minos, snopt, ...Disadvantage: Requires to learn AMPL

Forthcoming Solver Interface: ROI Package g gVienna Group, Stefan Theussl et al.

11

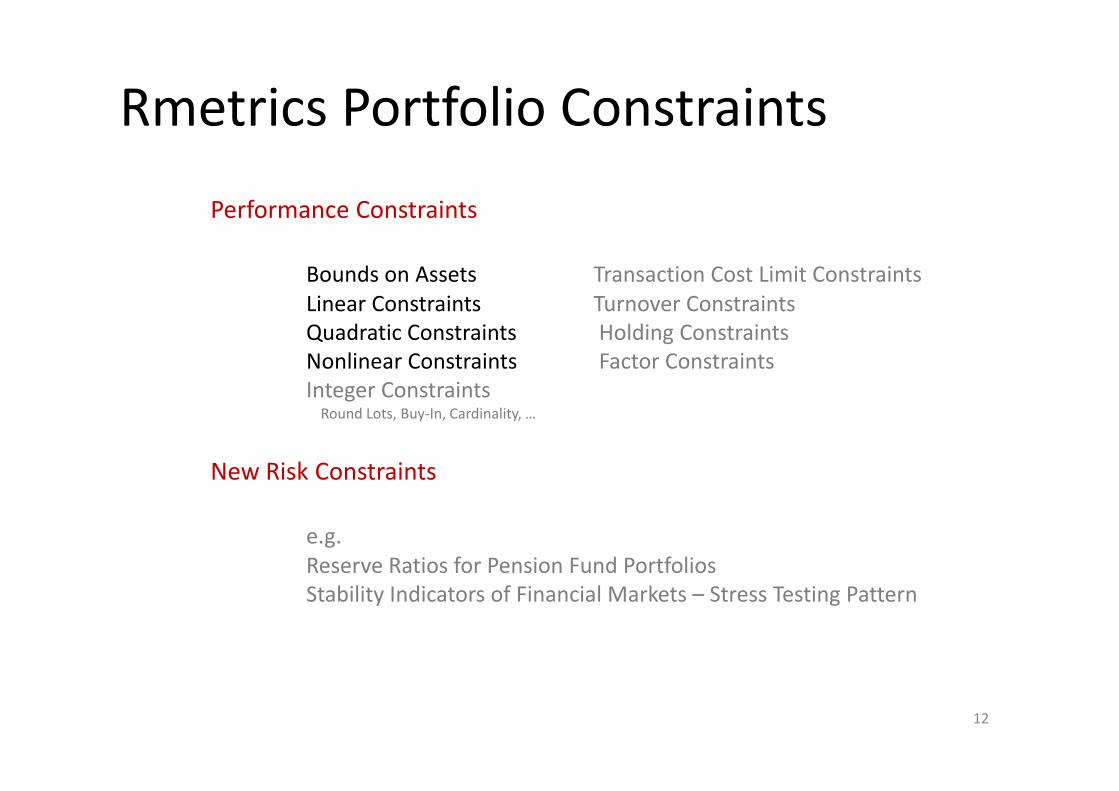

Rmetrics Portfolio Constraints

Performance ConstraintsPerformance Constraints

Bounds on Assets Transaction Cost Limit ConstraintsLinear Constraints Turnover ConstraintsLinear Constraints Turnover Constraints Quadratic Constraints Holding ConstraintsNonlinear Constraints Factor ConstraintsInteger ConstraintsInteger ConstraintsRound Lots, Buy‐In, Cardinality, …

New Risk Constraints

e.g. Reserve Ratios for Pension Fund PortfoliosStability Indicators of Financial Markets – Stress Testing Pattern

12

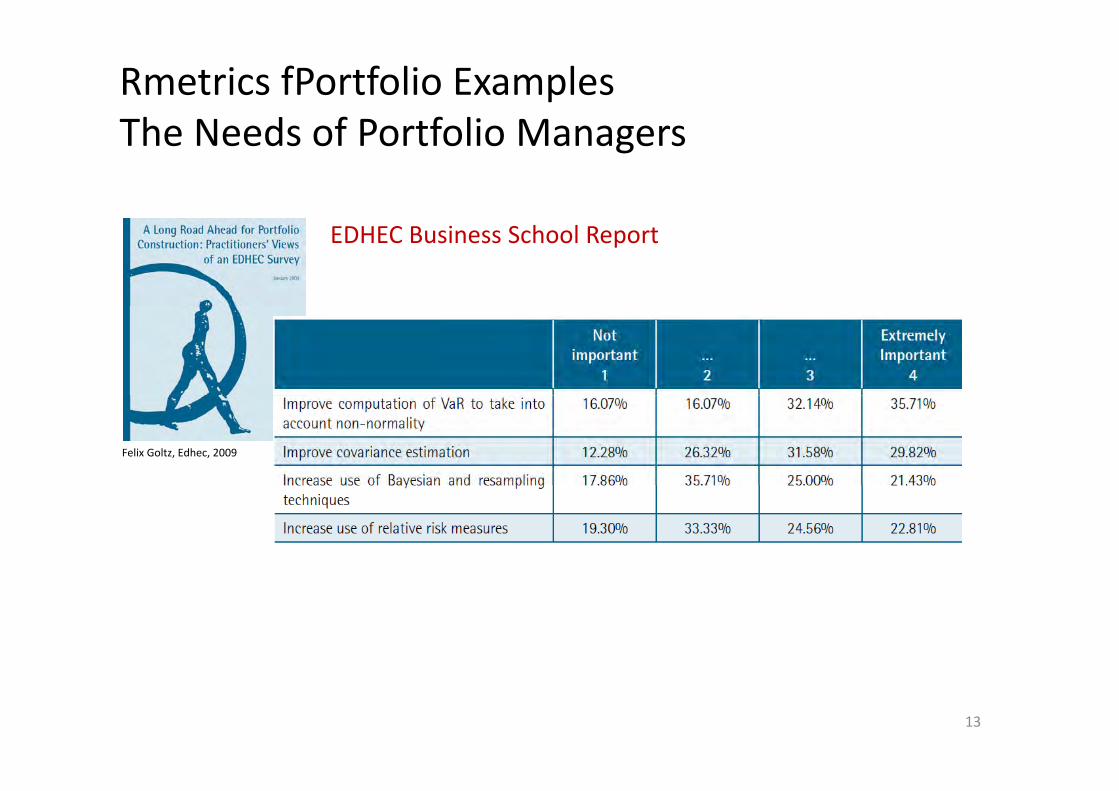

Rmetrics fPortfolio ExamplesThe Needs of Portfolio ManagersThe Needs of Portfolio Managers

EDHEC Business School Report

Felix Goltz, Edhec, 2009

13

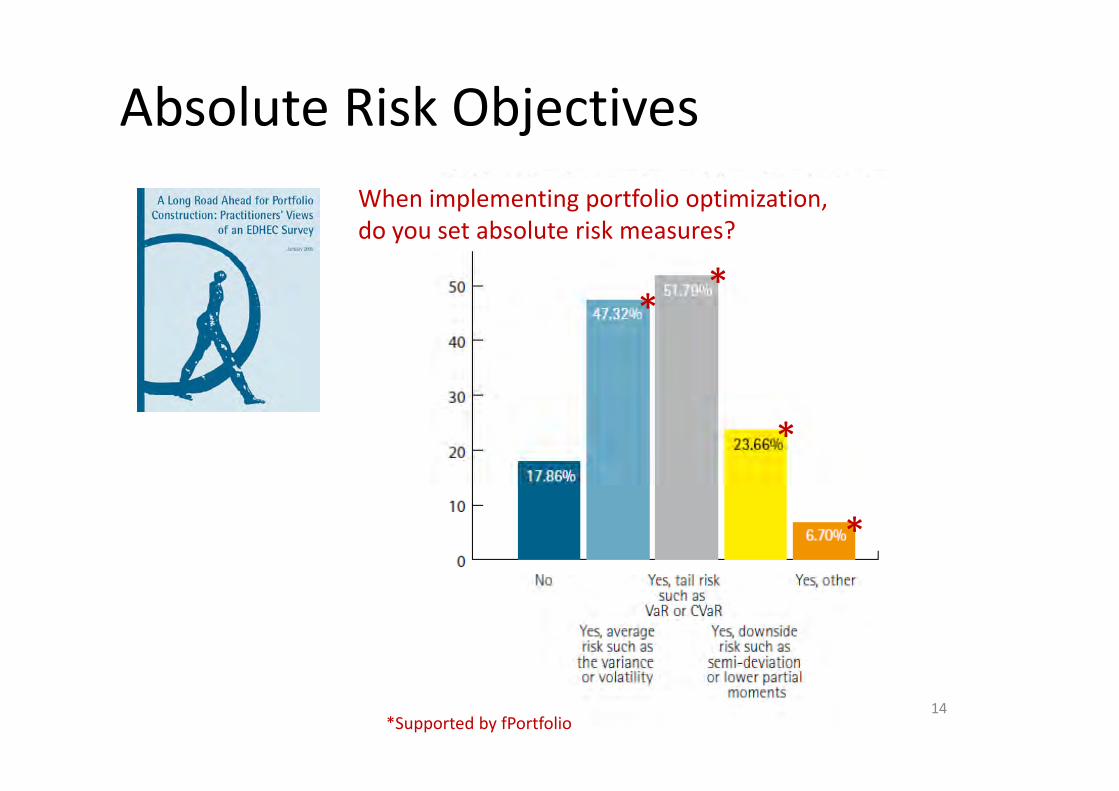

Absolute Risk ObjectivesjWhen implementing portfolio optimization,

* *do you set absolute risk measures?

*

*

*

14*Supported by fPortfolio

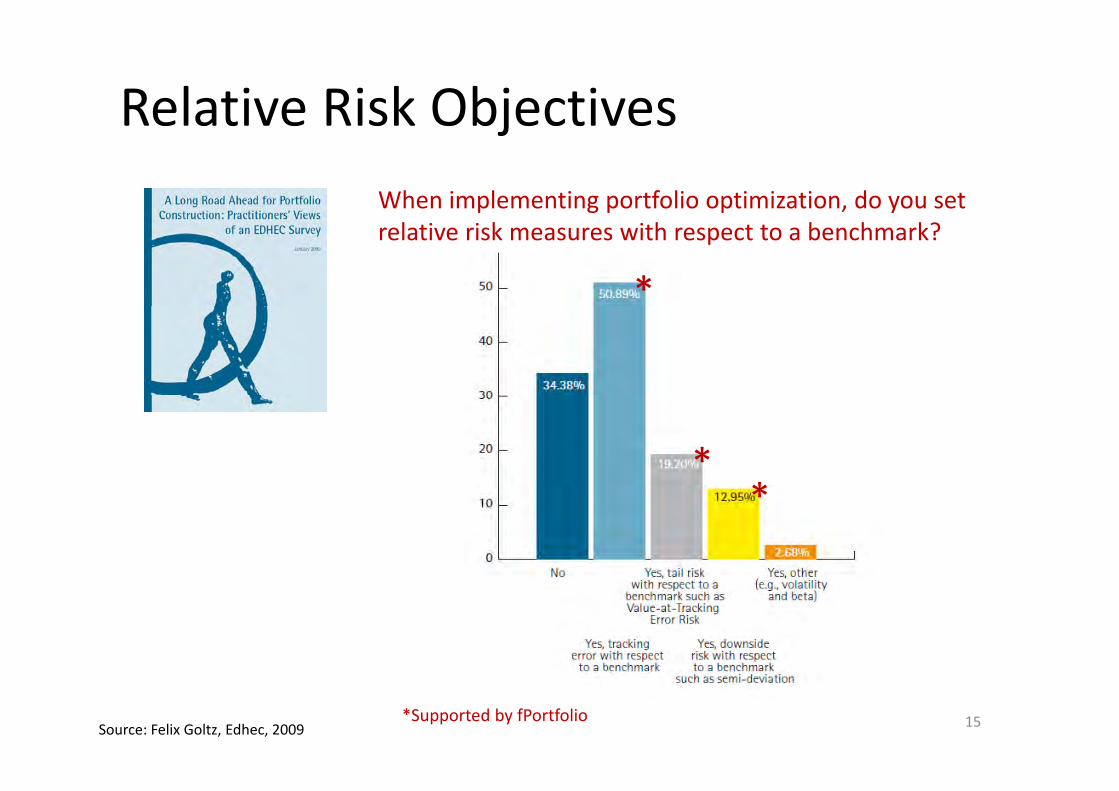

Relative Risk ObjectivesjWhen implementing portfolio optimization, do you set

*relative risk measures with respect to a benchmark?

***

15Source: Felix Goltz, Edhec, 2009 *Supported by fPortfolio

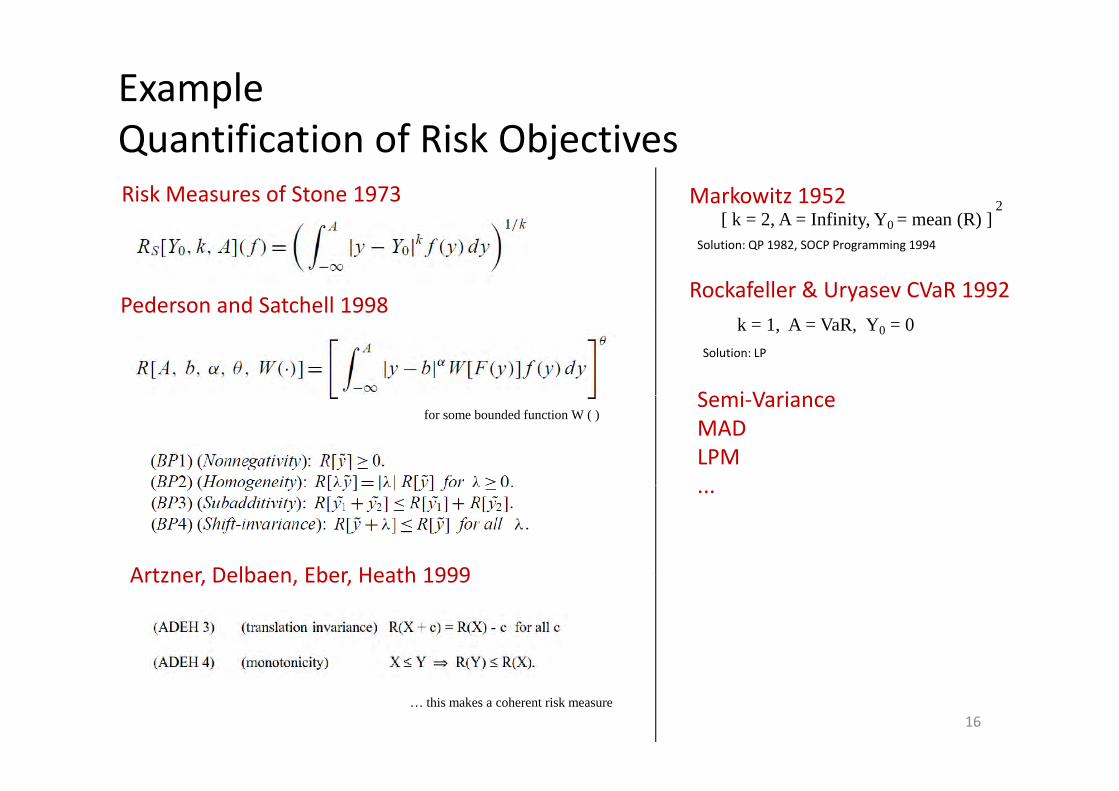

ExampleQ ifi i f Ri k Obj iQuantification of Risk ObjectivesRisk Measures of Stone 1973

[ k 2 A I fi it Y (R) ]2Markowitz 1952

Pederson and Satchell 1998Rockafeller & Uryasev CVaR 1992

[ k = 2, A = Infinity, Y0 = mean (R) ]Solution: QP 1982, SOCP Programming 1994

Pederson and Satchell 1998k = 1, A = VaR, Y0 = 0

Solution: LP

Semi Variancefor some bounded function W ( )

Semi‐VarianceMADLPM

Artzner Delbaen Eber Heath 1999

...

Artzner, Delbaen, Eber, Heath 1999

16… this makes a coherent risk measure

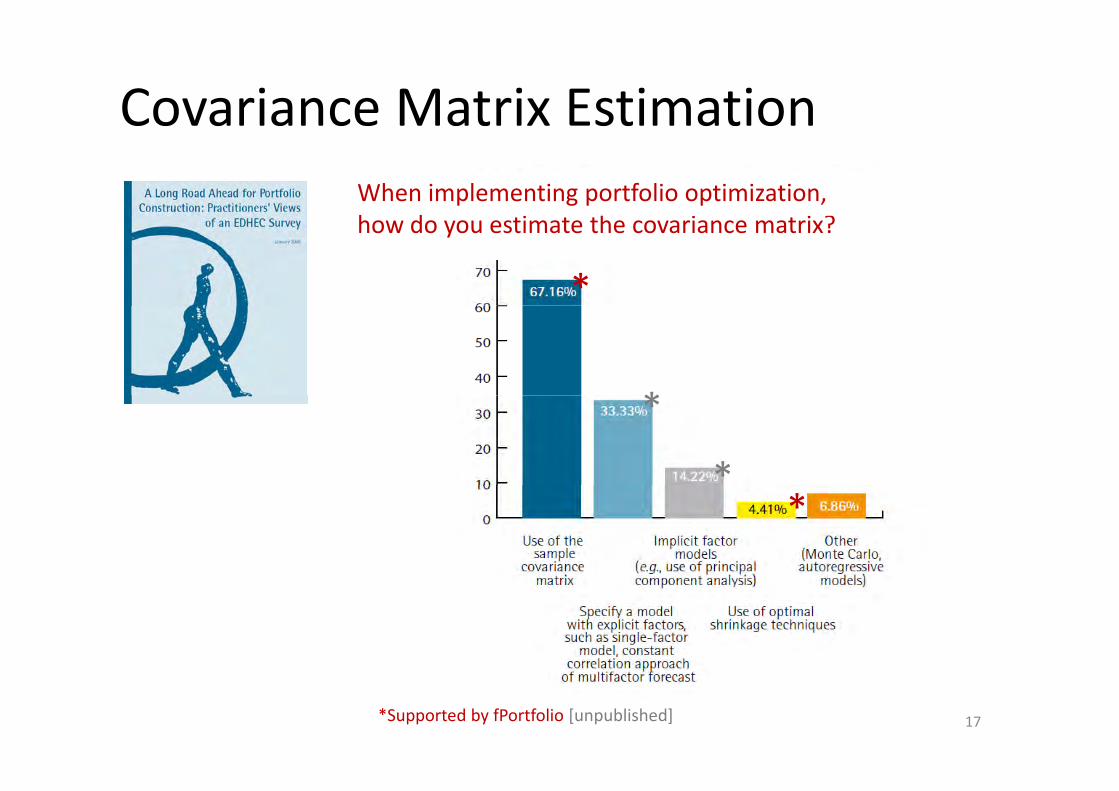

Covariance Matrix EstimationWhen implementing portfolio optimization, h d i h i i ?

*

how do you estimate the covariance matrix?

**

**

17*Supported by fPortfolio [unpublished]

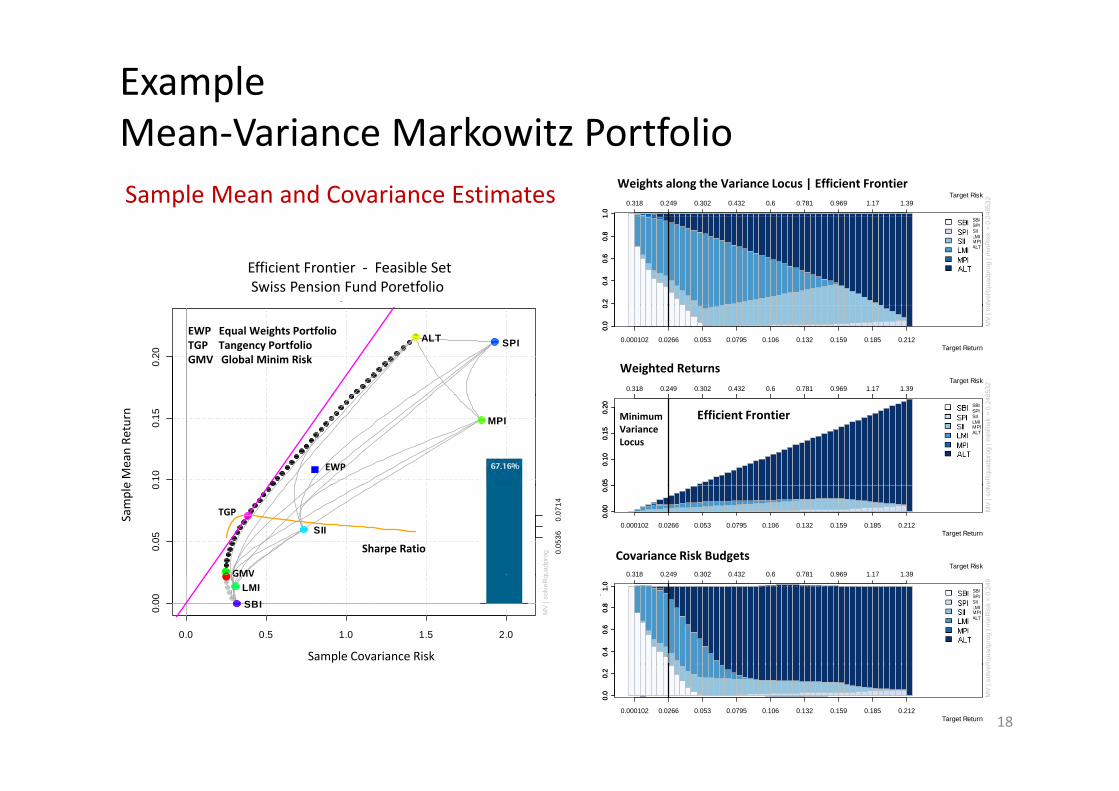

ExampleMean Variance Markowitz PortfolioMean‐Variance Markowitz Portfolio

1.0

1.0

0.318 0.249 0.302 0.432 0.6 0.781 0.969 1.17 1.39Target Risk

ht 2485

32

WeightsWeights along the Variance Locus | Efficient FrontierSample Mean and Covariance Estimates

Efficient FrontierMV Portfolio | mean-Stdev View

0.2

0.4

0.6

0.8

1

SBISPISIILMIMPIALT

0.2

0.4

0.6

0.8

1W

eigh

olve

Rqu

adpr

og |

min

Ris

k =

0.2

Efficient Frontier ‐ Feasible SetSwiss Pension Fund Poretfolio

0.20

SPIALT

0.0

00.

00

0.000102 0.0266 0.053 0.0795 0.106 0.132 0.159 0.185 0.212Target Return

MV

| so

0.318 0.249 0.302 0.432 0.6 0.781 0.969 1.17 1.39Target Risk

8532

Weighted Returns

EWP Equal Weights PortfolioTGP Tangency PortfolioGMV Global Minim Risk

Weighted Returns

0.10

0.15

et R

etur

n[m

ean] MPI

050.

100.

150.

20 SBISPISIILMIMPIALT

050.

100.

150.

20W

eigh

ted

Ret

urn

veR

quad

prog

| m

inR

isk

= 0.

248

EWP

MinimumVarianceLocus

Efficient Frontier

e Mean Re

turn

0.05

0

uadp

rog

Targ

e

0.05

36

0.0

714

SII

0.00

0.0

0.00

0.0

0.000102 0.0266 0.053 0.0795 0.106 0.132 0.159 0.185 0.212Target Return

MV

| sol

v

0 318 0 249 0 302 0 432 0 6 0 781 0 969 1 17 1 39Target RiskCov Risk Budgets

TGP

Sharpe Ratio

GMV

Covariance Risk Budgets

Sample

0.0 0.5 1.0 1.5 2.0

0.00

MV

| sol

veR

q

Target Risk[Cov]

SBILMI

0.4

0.6

0.8

1.0

SBISPISIILMIMPIALT

0.4

0.6

0.8

1.0

0.318 0.249 0.302 0.432 0.6 0.781 0.969 1.17 1.39

Cov

Ris

k Bu

dget

s

Rqu

adpr

og |

min

Ris

k =

0.24

9

GMV

Sample Covariance Risk

0.0

0.2

0.0

0.2

0.000102 0.0266 0.053 0.0795 0.106 0.132 0.159 0.185 0.212Target Return

MV

| sol

veR

18

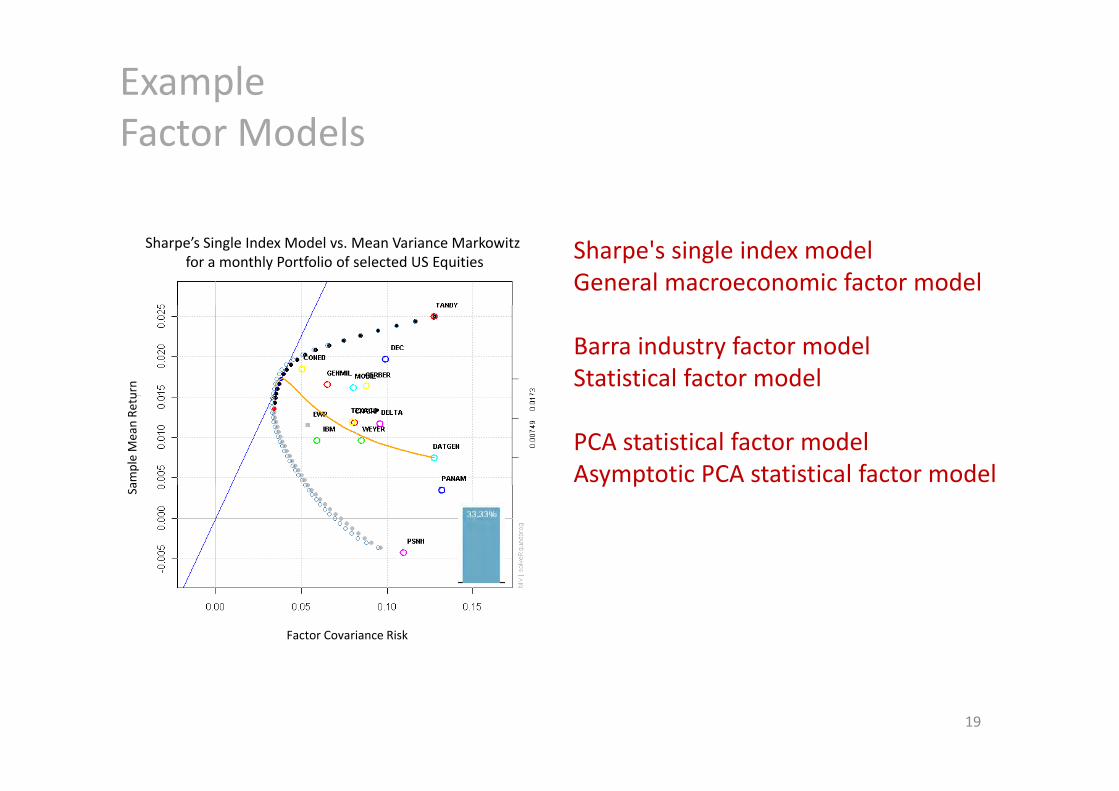

ExampleFactor ModelsFactor Models

Sharpe's single index model General macroeconomic factor model

Sharpe’s Single Index Model vs. Mean Variance Markowitz for a monthly Portfolio of selected US Equities

Barra industry factor model Statistical factor model

urn

PCA statistical factor model Asymptotic PCA statistical factor model am

ple Mean Re

tu

y p

Sa

Factor Covariance Risk

19

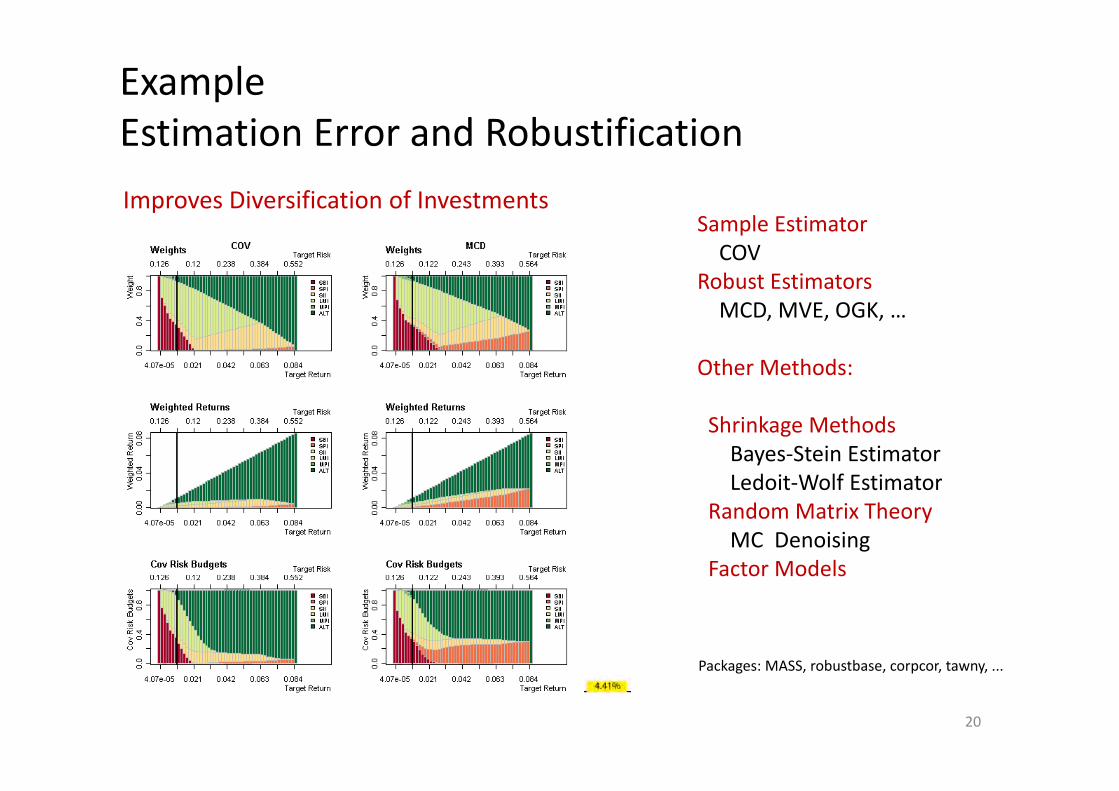

ExampleEstimation Error and RobustificationEstimation Error and Robustification

S l iImproves Diversification of Investments

Sample EstimatorCOV

Robust EstimatorsMCD MVE OGKMCD, MVE, OGK, …

Other Methods:

Shrinkage MethodsBayes‐Stein EstimatorLedoit‐Wolf EstimatorLedoit Wolf Estimator

Random Matrix TheoryMC Denoising

Factor ModelsFactor Models

Packages: MASS robustbase corpcor tawny

20

Packages: MASS, robustbase, corpcor, tawny, ...

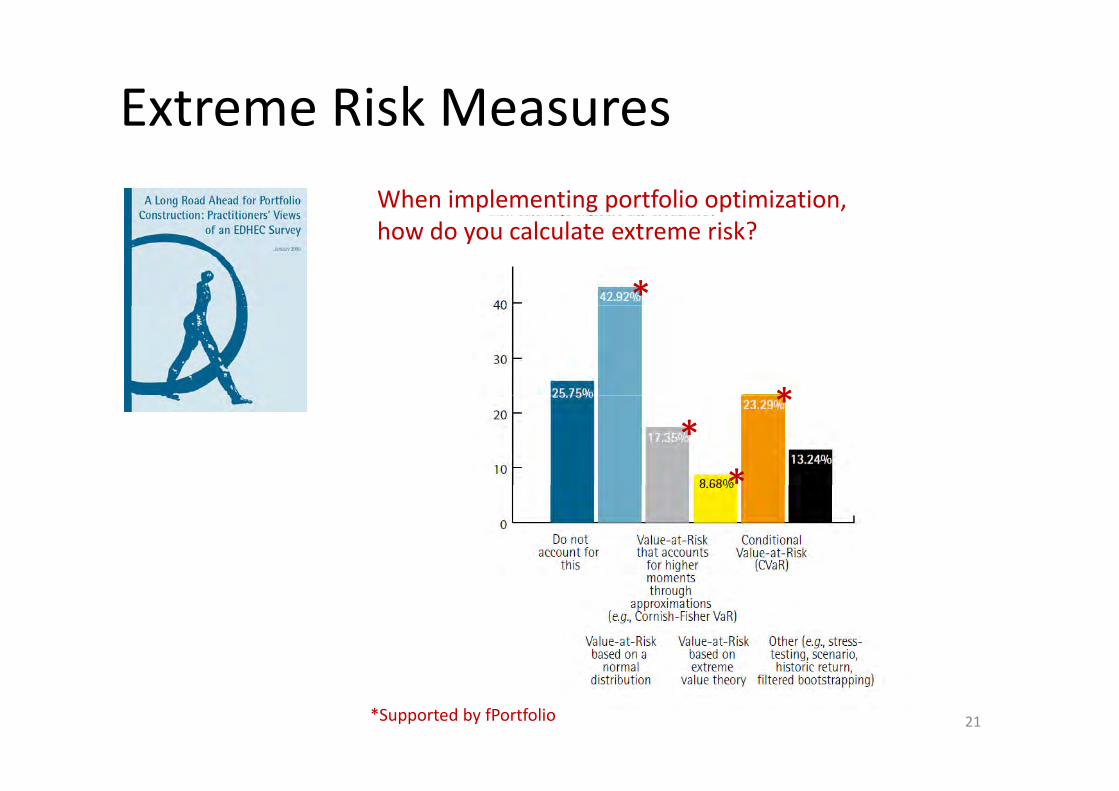

Extreme Risk MeasuresWhen implementing portfolio optimization,

*

how do you calculate extreme risk?

**

*

*

21*Supported by fPortfolio

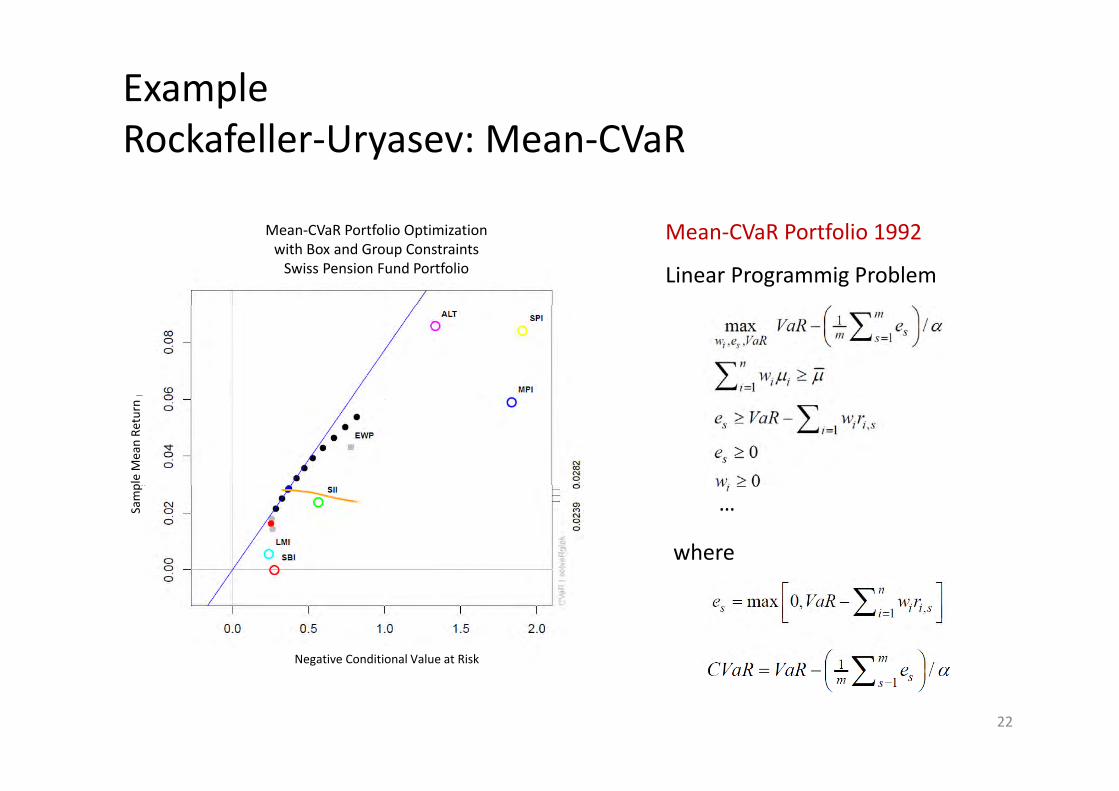

ExampleR k f ll U M CV RRockafeller‐Uryasev: Mean‐CVaR

Mean‐CVaR Portfolio 1992

Linear Programmig Problem

Mean‐CVaR Portfolio Optimizationwith Box and Group Constraints Swiss Pension Fund Portfolio

ple Mean Re

turn

where

…Samp

Negative Conditional Value at Risk

22

g

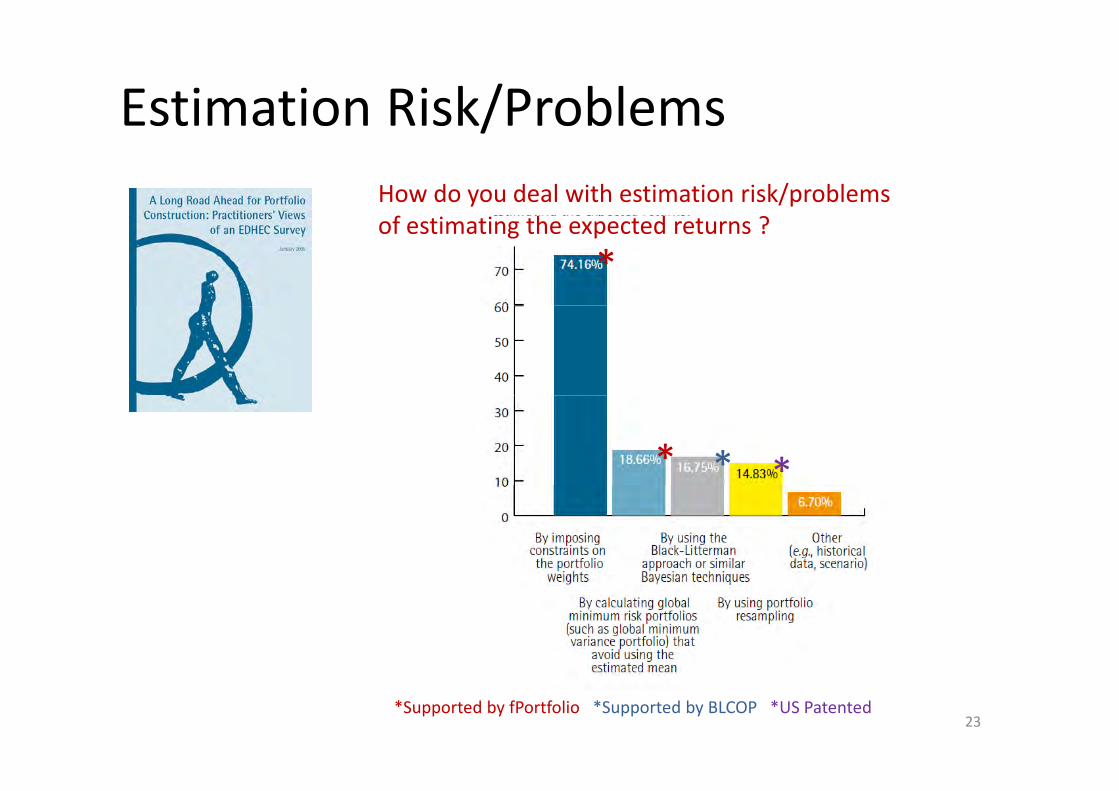

Estimation Risk/Problems/How do you deal with estimation risk/problemsf h d ?

*of estimating the expected returns ?

* **

23*Supported by fPortfolio *Supported by BLCOP *US Patented

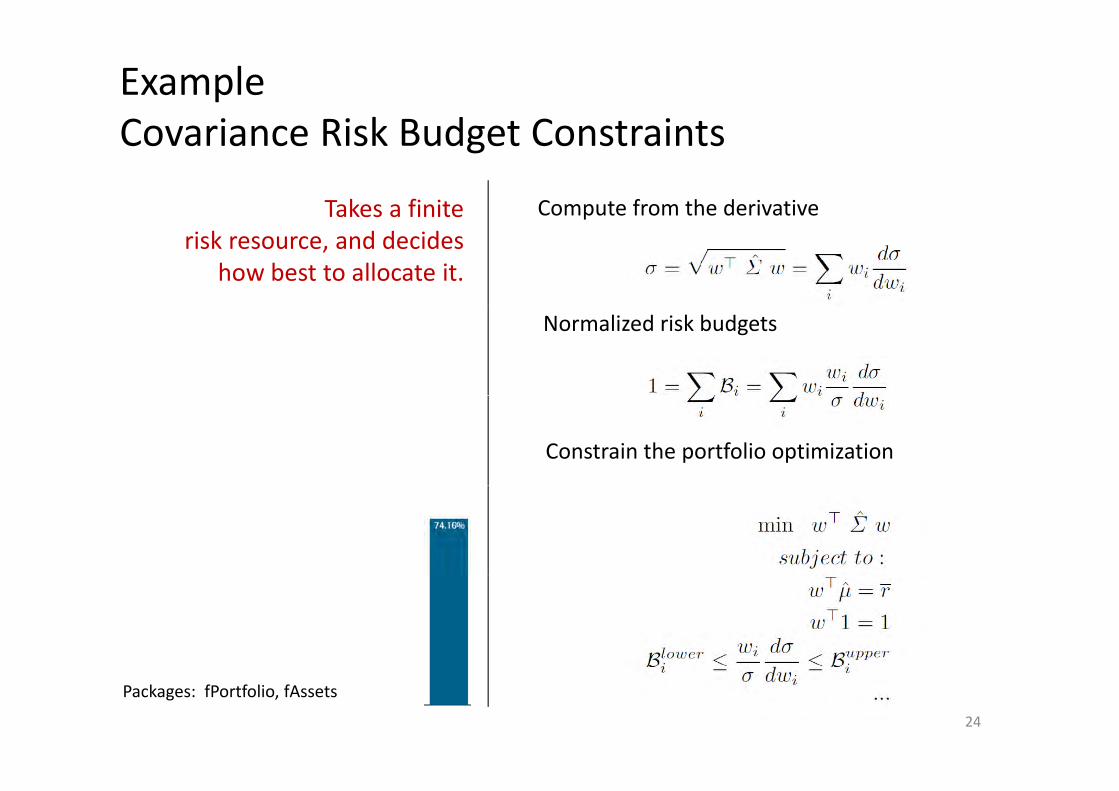

ExampleCovariance Risk Budget ConstraintsCovariance Risk Budget Constraints

Takes a finite Compute from the derivativeTakes a finite risk resource, and decides

how best to allocate it.

p

Normalized risk budgets

Constrain the portfolio optimization

24

Packages: fPortfolio, fAssets

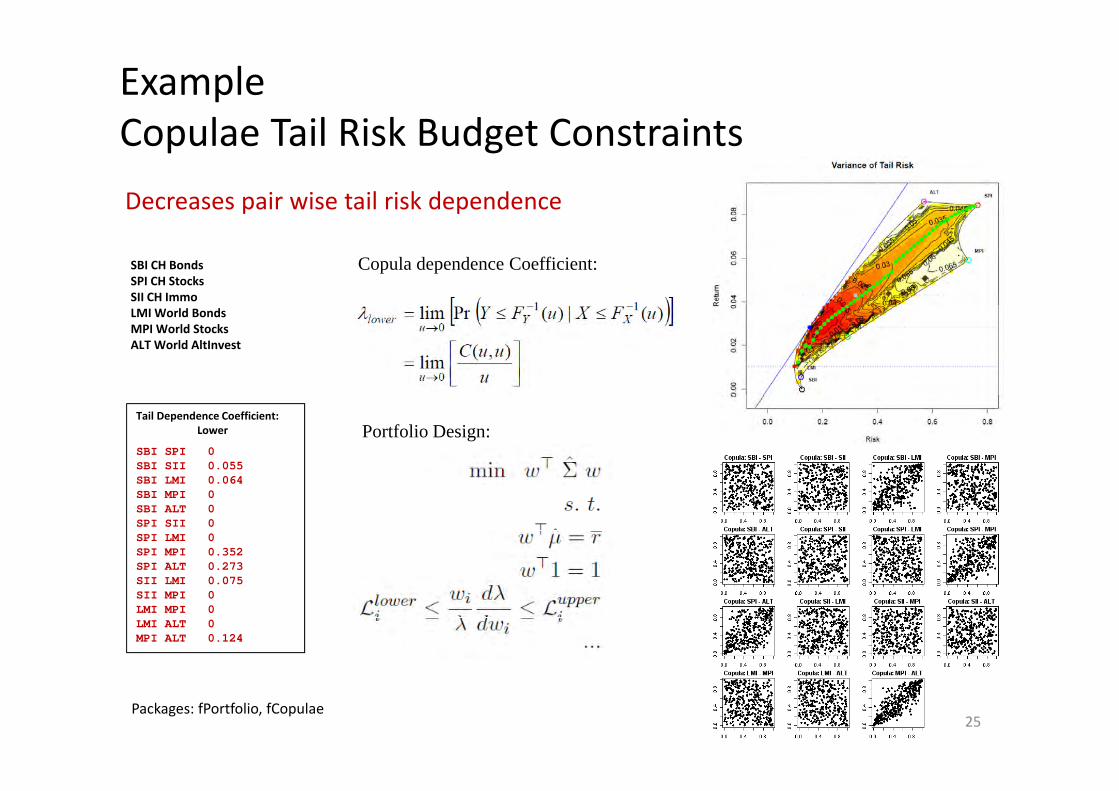

ExampleCopulae Tail Risk Budget ConstraintsCopulae Tail Risk Budget ConstraintsDecreases pair wise tail risk dependence

SBI CH BondsSPI CH StocksSII CH Immo

Copula dependence Coefficient:

LMI World BondsMPI World StocksALT World AltInvest

Tail Dependence Coefficient:Lower

SBI SPI 0 SBI SII 0.055 SBI LMI 0.064

Portfolio Design:

SBI MPI 0 SBI ALT 0 SPI SII 0 SPI LMI 0 SPI MPI 0.352 SPI ALT 0.273 SII LMI 0.075 SII MPI 0 LMI MPI 0 LMI ALT 0 MPI ALT 0.124

25Packages: fPortfolio, fCopulae

Part III

New Directions

• Portfolio Risk Surfaces & Risk Profile Lines• Rastered Motion Risk Surfaces• Portfolio Shape Pictograms• Stability Measures

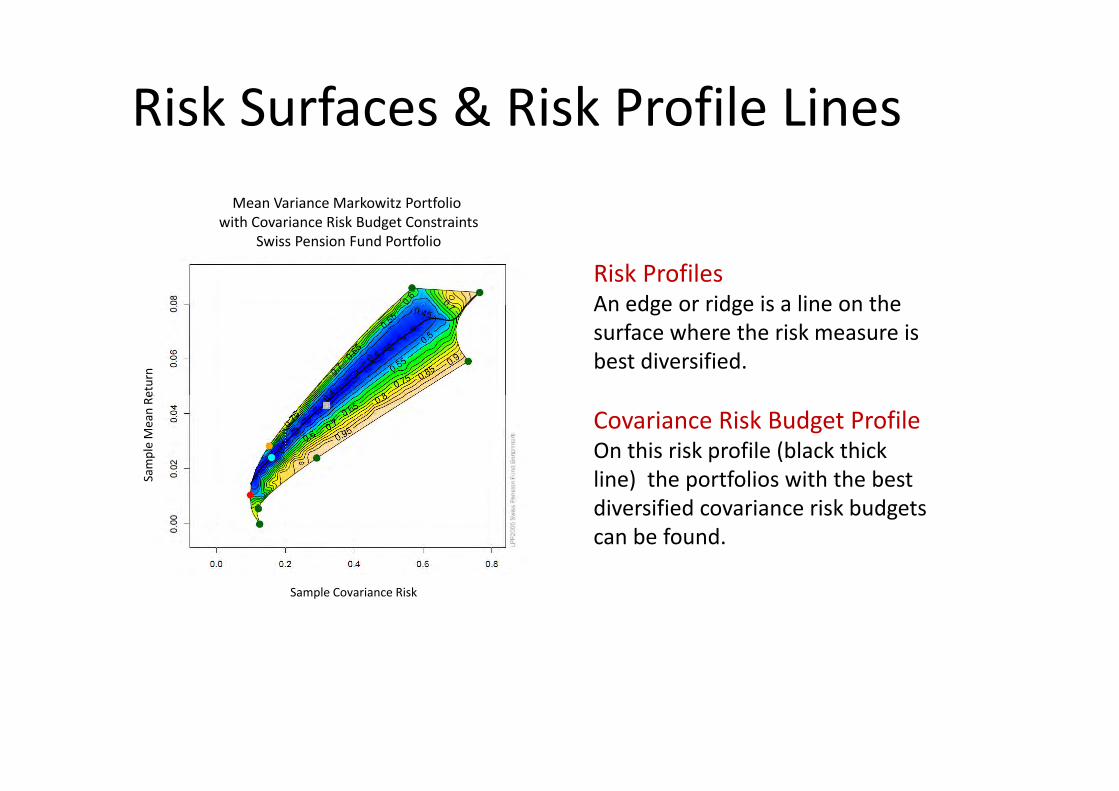

Risk Surfaces & Risk Profile Lines Mean Variance Markowitz Portfolio

Risk ProfilesAn edge or ridge is a line on the

with Covariance Risk Budget ConstraintsSwiss Pension Fund Portfolio

An edge or ridge is a line on the surface where the risk measure is best diversified.

eturn

Covariance Risk Budget ProfileOn this risk profile (black thick line) the portfolios with the bestSa

mple Mean Re

line) the portfolios with the best diversified covariance risk budgets can be found.

Sample Covariance Risk

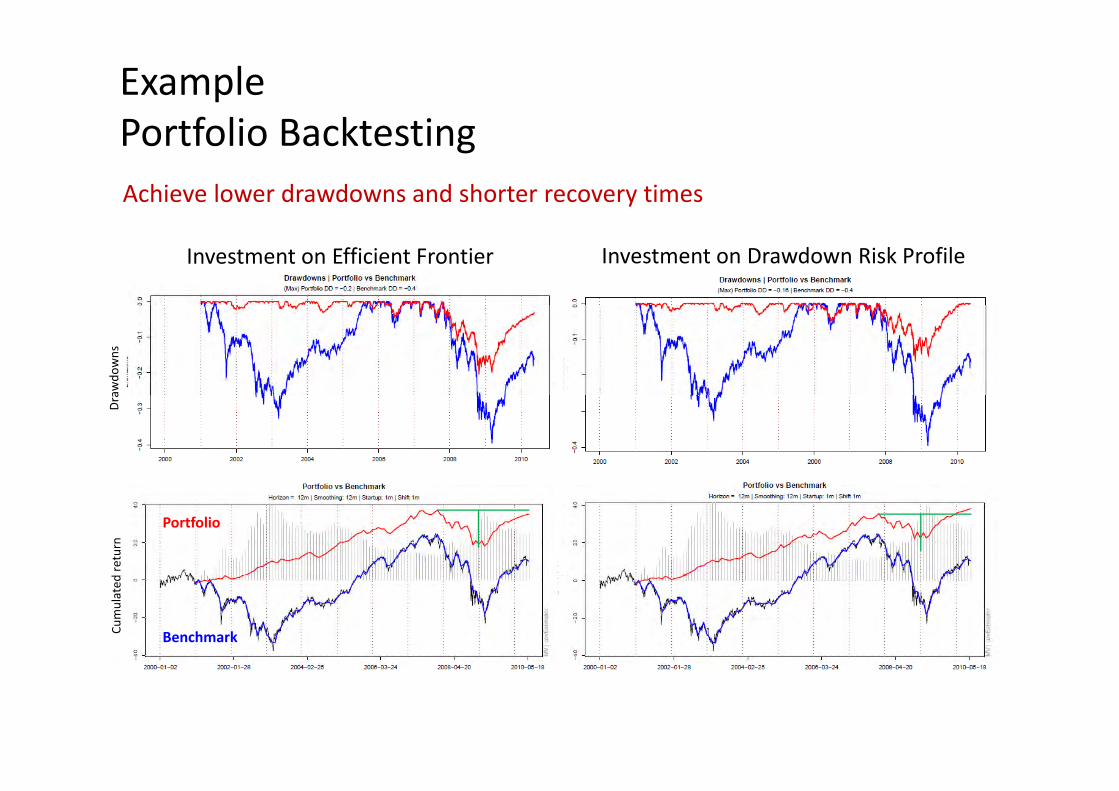

ExampleInvestments along Risk ProfilesInvestments along Risk Profiles

A simple Efficient Frontier Strategy

Smoothly rebalance the investments from the tangency portfolioSmoothly rebalance the investments from the tangency portfolio if it exists, otherwise invest in the global minimum risk portfolio.

Alternative Risk Profile Line StrategyAlternative Risk Profile Line Strategy

Instead investing on the efficient frontier, we now invest in better risk diversified portfolios with the same return but now on pthe ridge frontier.

Remark: These portfolios have higher total risks, but are better diversified

Package: fPortfolioBacktesting28

ExamplePortfolio BacktestingPortfolio BacktestingAchieve lower drawdowns and shorter recovery times

Investment on Efficient Frontier Investment on Drawdown Risk Profile

awdo

wns

Dra

return

Portfolio

Cumulated

Benchmark

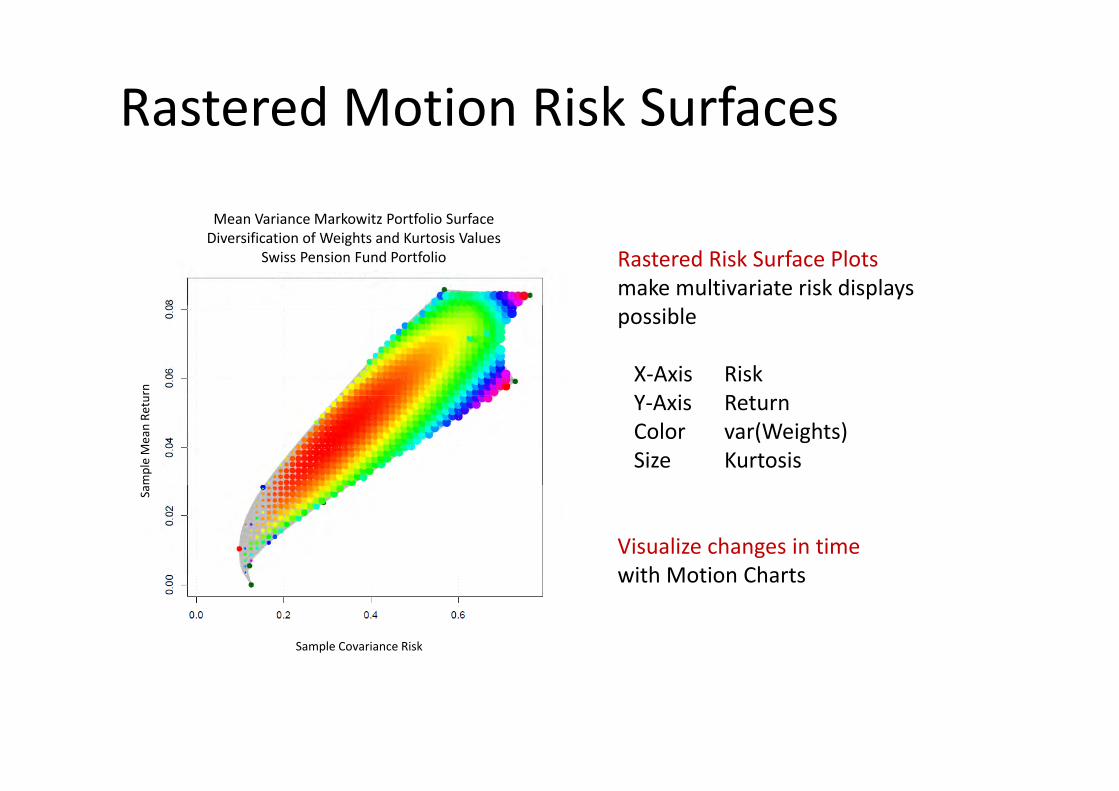

Rastered Motion Risk Surfaces

M V i M k it P tf li S f

Rastered Risk Surface Plots make multivariate risk displays

Mean Variance Markowitz Portfolio SurfaceDiversification of Weights and Kurtosis Values

Swiss Pension Fund Portfolio

possible

X‐Axis RiskY A i Rrn Y‐Axis ReturnColor var(Weights)Size Kurtosis

mple Mean Re

tu

Visualize changes in timewith Motion Charts

Sa

with Motion Charts

Sample Covariance Risk

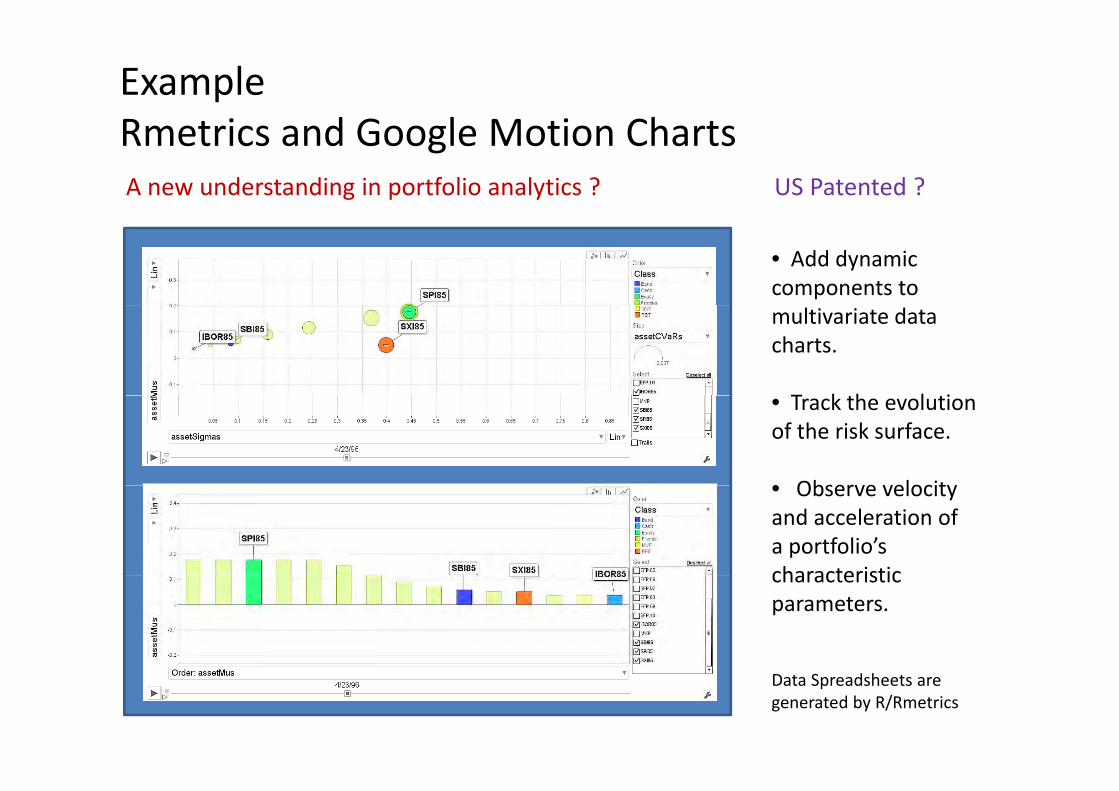

ExampleRmetrics and Google Motion ChartsRmetrics and Google Motion ChartsA new understanding in portfolio analytics ? US Patented ?

• Add dynamic components tomultivariate data charts.

T k h l i• Track the evolution of the risk surface.

• Observe velocity• Observe velocity and acceleration of a portfolio’s characteristiccharacteristic parameters.

Data Spreadsheets are generated by R/Rmetrics

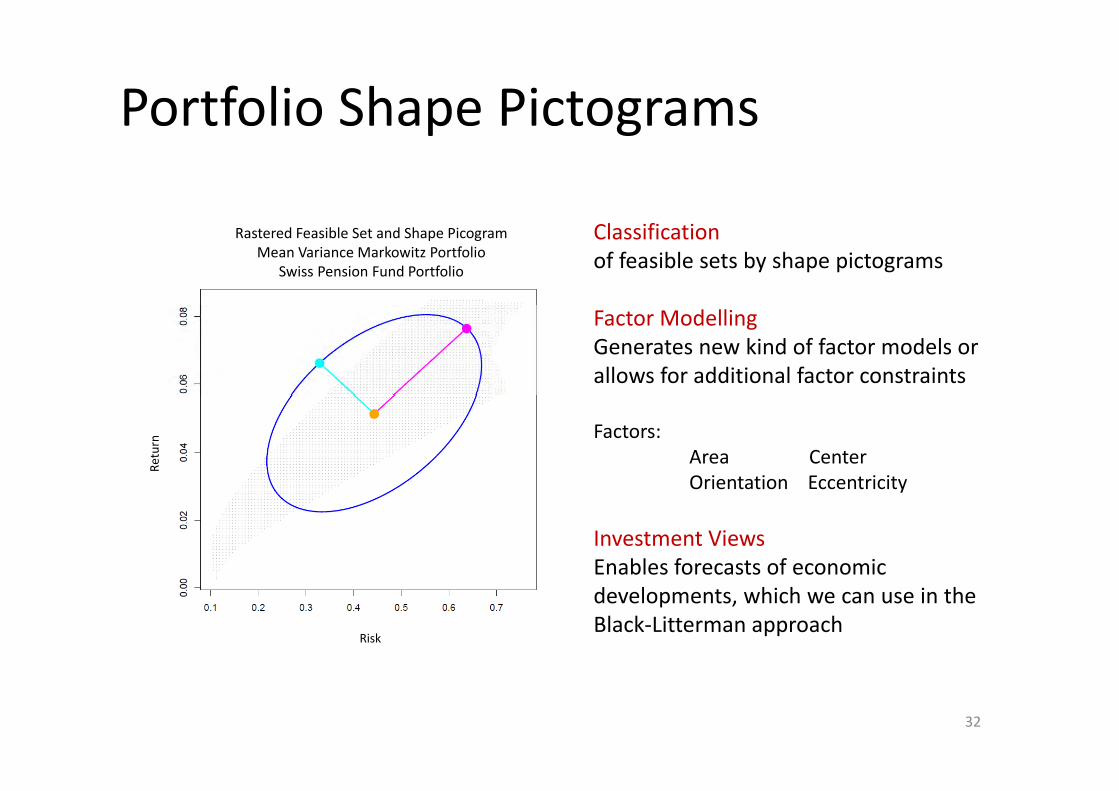

Portfolio Shape Pictogramsp g

Classification of feasible sets by shape pictograms

Rastered Feasible Set and Shape PicogramMean Variance Markowitz Portfolio

Swiss Pension Fund Portfolio

Factor ModellingGenerates new kind of factor models or allows for additional factor constraints

Factors:Area CenterOrientation Eccentricity

Return

Orientation Eccentricity

Investment ViewsEnables forecasts of economic developments, which we can use in the Black‐Litterman approach

Risk

32

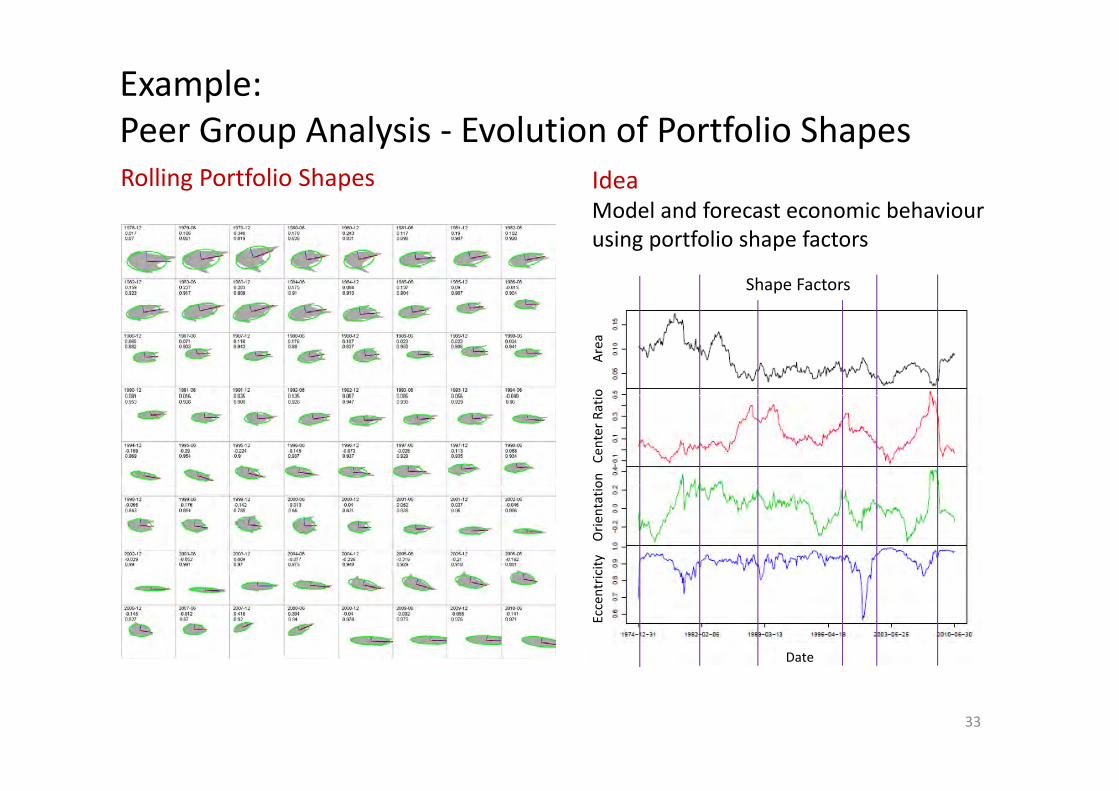

Example:Peer Group Analysis Evolution of Portfolio ShapesPeer Group Analysis ‐ Evolution of Portfolio Shapes

IdeaModel and forecast economic behaviour

Rolling Portfolio ShapesModel and forecast economic behaviourusing portfolio shape factors

Shape Factors

o Area

on Ce

nter

Ratio

city Orie

ntatio

Date

Eccentri

33

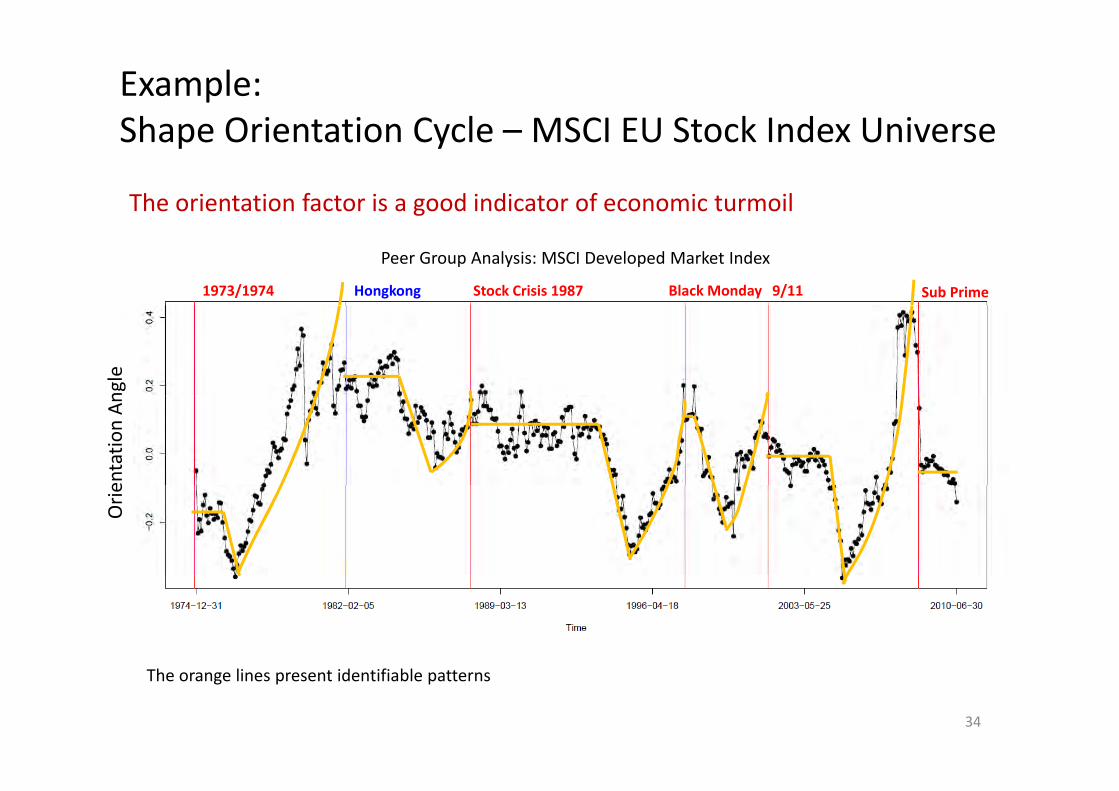

Example:Shape Orientation Cycle MSCI EU Stock Index UniverseShape Orientation Cycle – MSCI EU Stock Index Universe

The orientation factor is a good indicator of economic turmoil

Peer Group Analysis: MSCI Developed Market Index

Hongkong Sub Prime9/11Black MondayStock Crisis 19871973/1974

ngle

entatio

n An

Orie

34

The orange lines present identifiable patterns

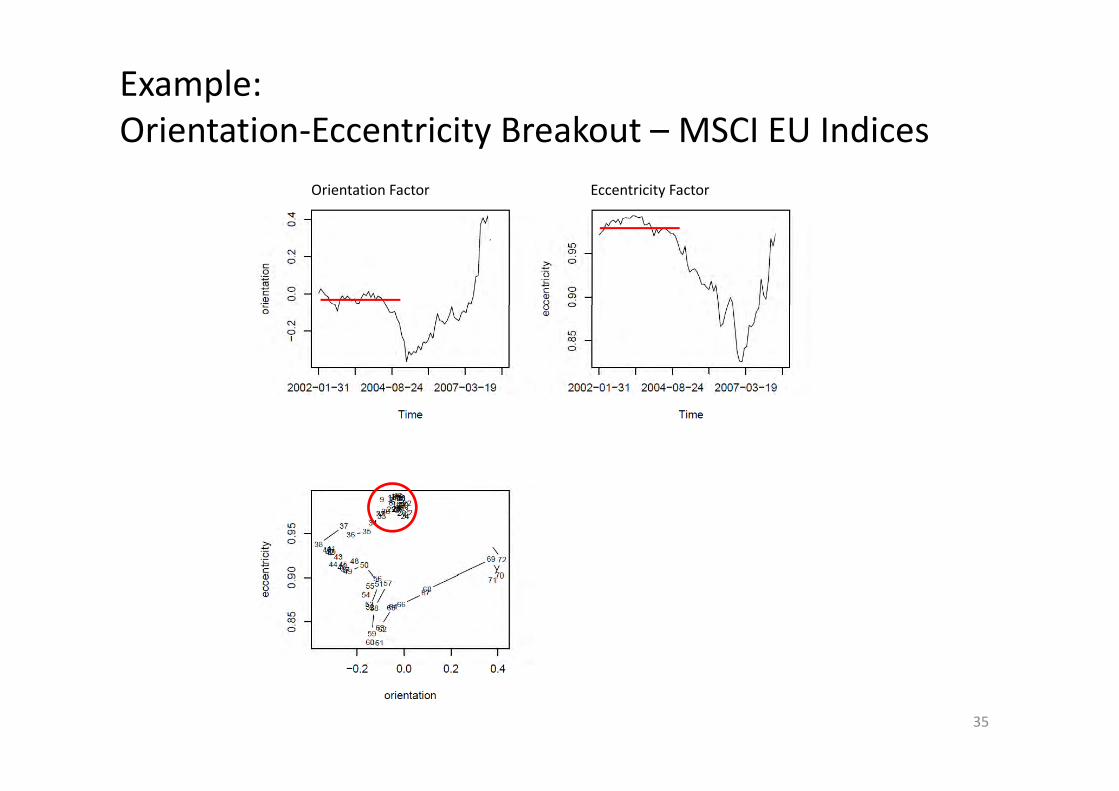

Example:Orientation Eccentricity Breakout MSCI EU IndicesOrientation‐Eccentricity Breakout – MSCI EU Indices

Orientation Factor Eccentricity Factor

35

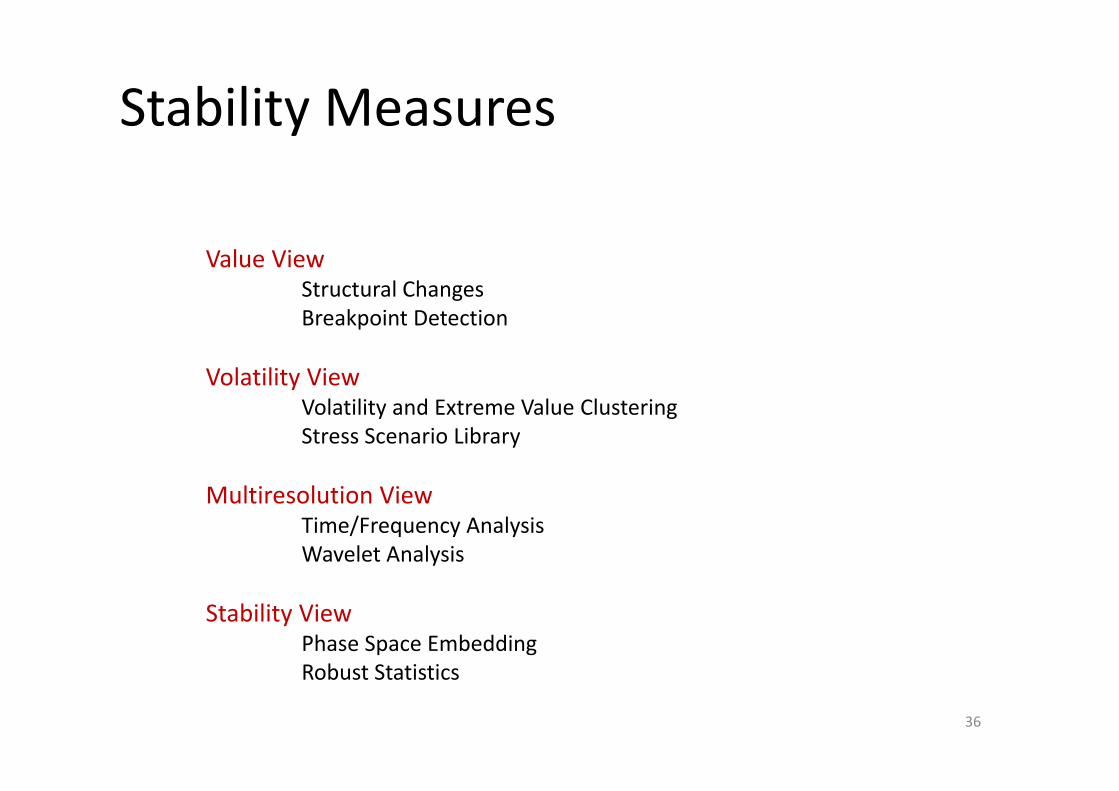

Stability Measuresy

Value ViewStructural Changes Breakpoint Detection

Volatility ViewVolatility and Extreme Value ClusteringStress Scenario Library

l lMultiresolution ViewTime/Frequency AnalysisWavelet Analysis

Stability ViewPhase Space EmbeddingR b S i i

36

Robust Statistics

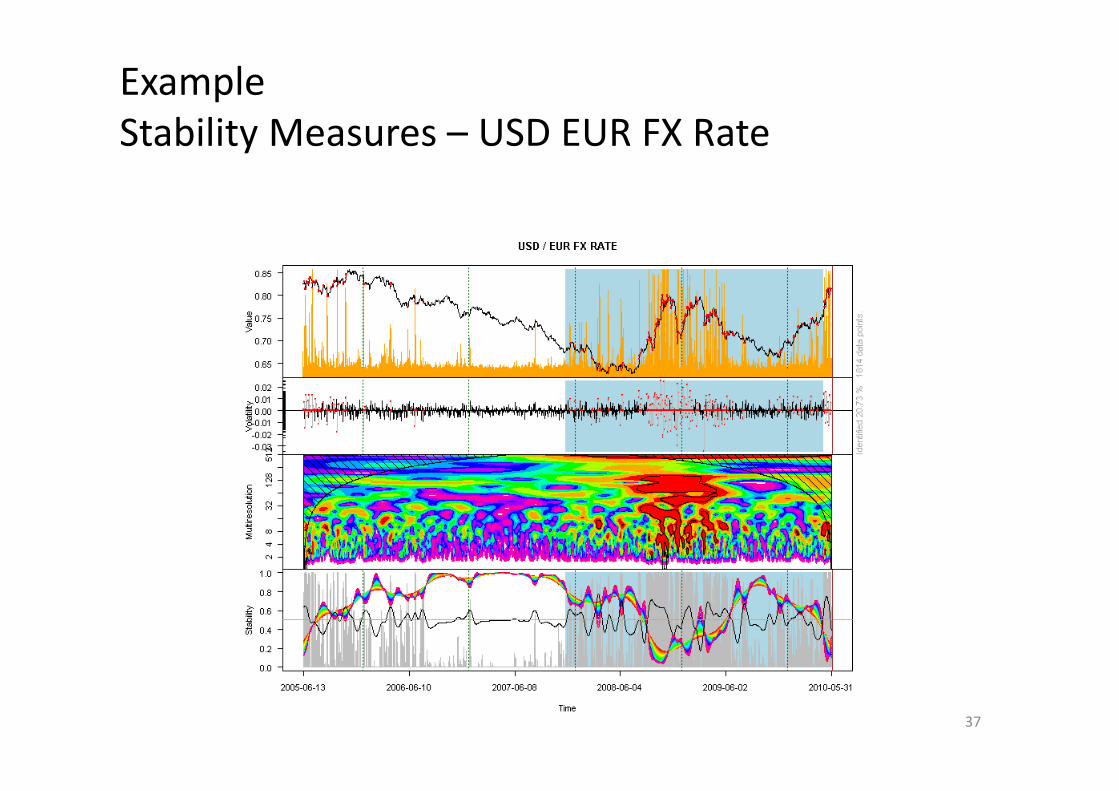

ExampleStability Measures USD EUR FX RateStability Measures – USD EUR FX Rate

37

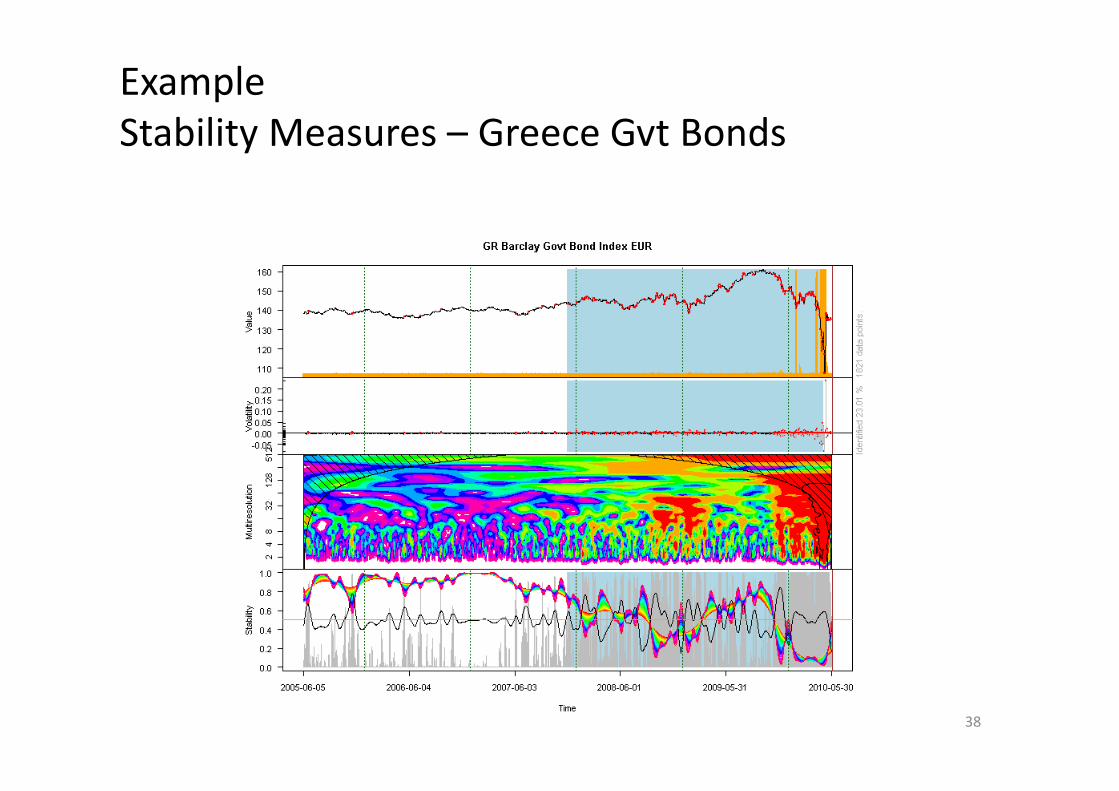

ExampleStability Measures Greece Gvt BondsStability Measures – Greece Gvt Bonds

38

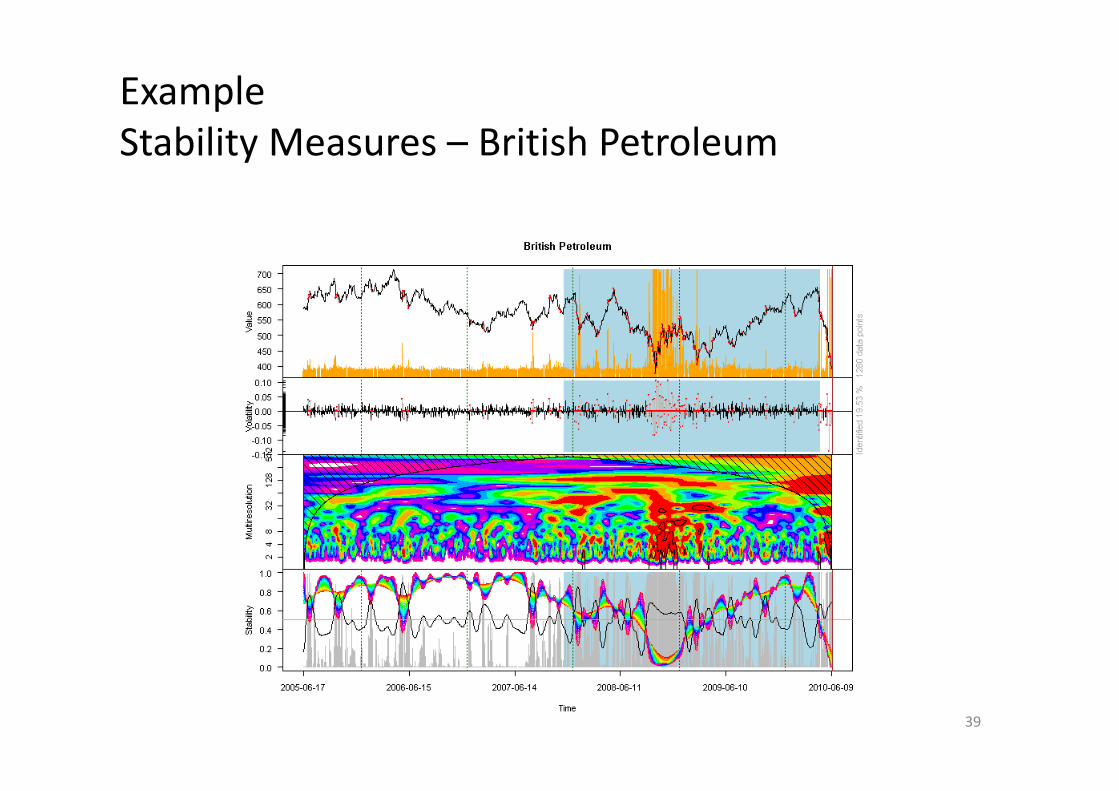

ExampleStability Measures – British Petroleum

39

Our ProposalfStability as New Peer Group & Portfolio Objectives

ObjectiveMaximize Stability

Subject to:jReturn ConstraintsRisk ConstraintsStress Resistance ConstraintsStress Resistance Constraints

40

www.rmetrics.orgwww.ethz.chJoint work with:

Yohan Chalabi

h h h

Yohan ChalabiWilliam ChenChristine DongA d Elli

Thank [email protected] Ellis

Sebastian Pérez SaaibiDavid Scott Thank YouStefan Theussl

![Optimizing for Aesthetically Pleasing Quadrotor Camera Motion · gradient descent and penalizing distance between possible solutions and the feasible hull. Like [Liu et al. 2006],](https://img.pdfslide.us/doc/110x75/5f721644d6702a6f5649e700/optimizing-for-aesthetically-pleasing-quadrotor-camera-motion-gradient-descent-and.jpg)