Embed Size (px)

Citation preview

Dr. Tom Vanden Borre Ius Commune ConferenceSenior Research Fellow KUL Maastricht, 29 November 2013(Institute for Energy and Environmental Law)

The global gas revolution vslocal policy response

Agenda

I. Natural gas revolution

III. Policy developments EU and in BE

IV. Conclusion

II. Europe is paying the bill

Parts I and II summarise the presentation of Mr. M. Alverà, Senior Executive Vice President – Midstream – eni, at the European Autumn Gas Conference, Brussels, 12 November 2013

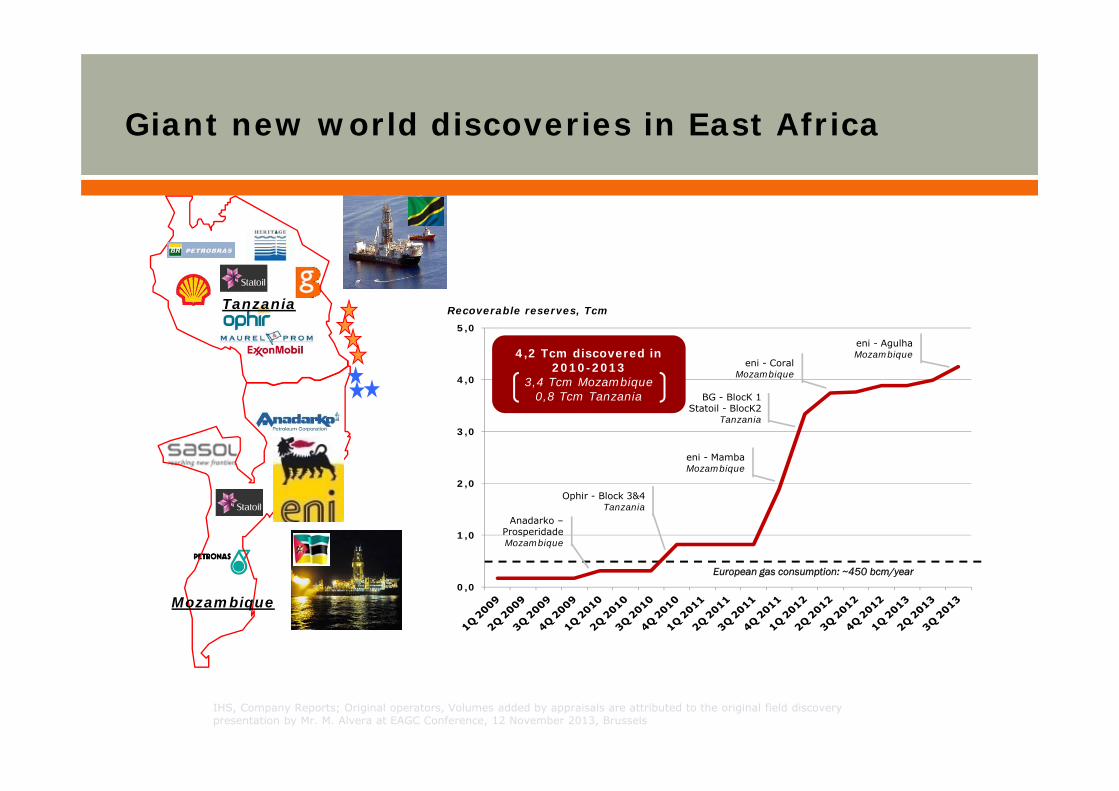

Tanzania

Mozambique

Giant new world discoveries in East Africa

IHS, Company Reports; Original operators, Volumes added by appraisals are attributed to the original field discoverypresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

European gas consumption: ~450 bcm/year0,0

1,0

2,0

3,0

4,0

5,0

Anadarko –ProsperidadeMozambique

Ophir - Block 3&4Tanzania

eni - MambaMozambique

BG - BlocK 1Statoil - BlocK2

Tanzania

eni - CoralMozambique

eni - AgulhaMozambique

Recoverable reserves, Tcm

4,2 Tcm discovered in 2010-2013

3,4 Tcm Mozambique0,8 Tcm Tanzania

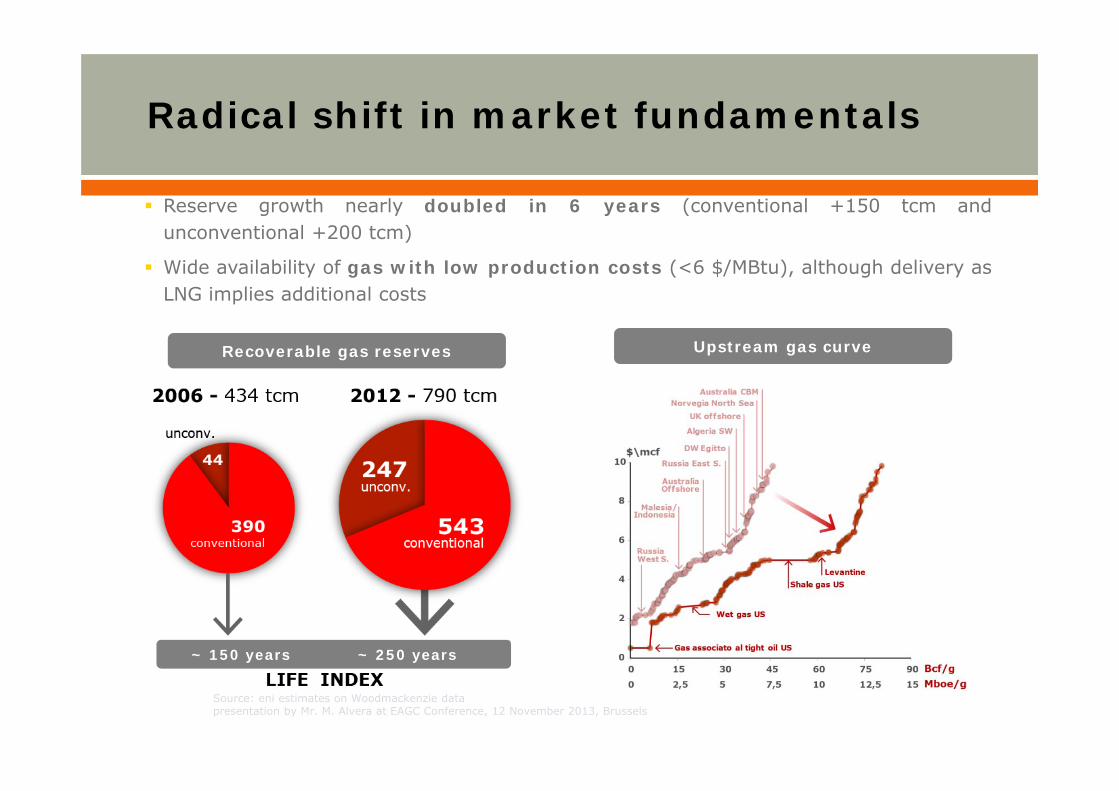

Reserve growth nearly doubled in 6 years (conventional +150 tcm andunconventional +200 tcm)

Wide availability of gas with low production costs (<6 $/MBtu), although delivery asLNG implies additional costs

Recoverable gas reserves Upstream gas curve

~ 150 years ~ 250 years

Source: eni estimates on Woodmackenzie datapresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

Radical shift in market fundamentals

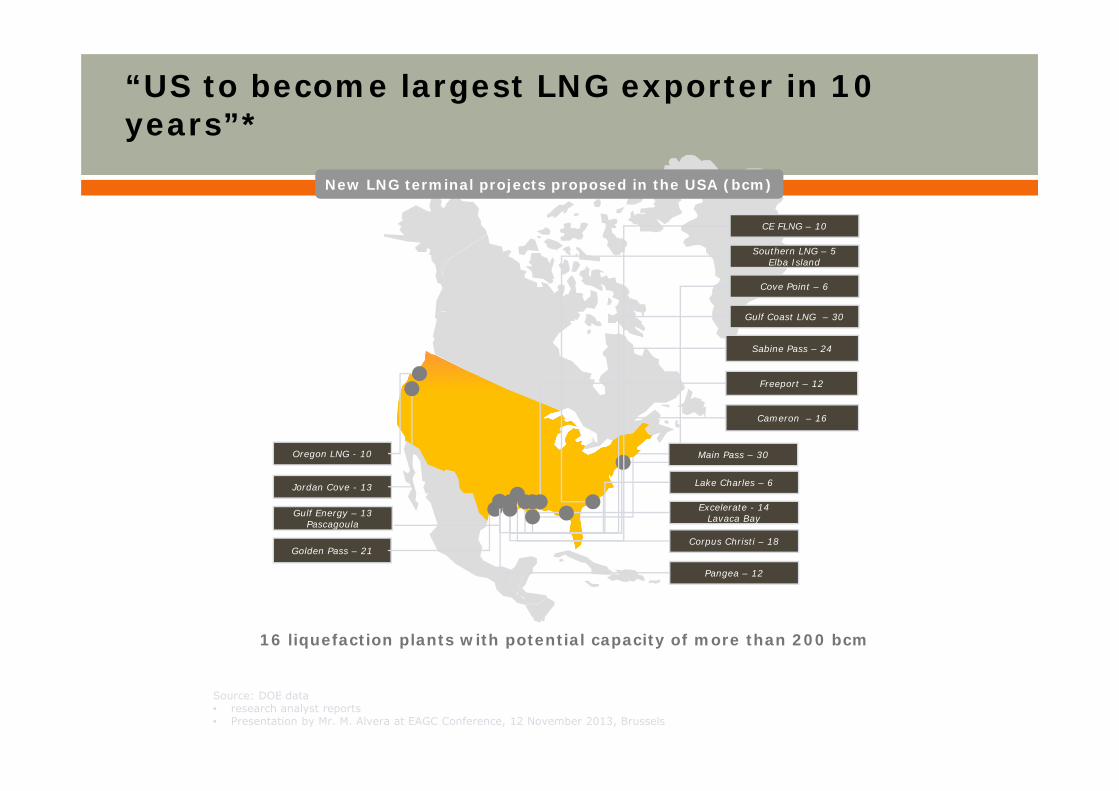

Corpus Christi – 18

Cove Point – 6

Freeport – 12

Cameron – 16

Excelerate - 14Lavaca Bay

Lake Charles – 6

Sabine Pass – 24

Golden Pass – 21

Southern LNG – 5Elba Island

Gulf Energy – 13Pascagoula

Oregon LNG - 10

Jordan Cove - 13

CE FLNG – 10

Gulf Coast LNG – 30

Pangea – 12

Main Pass – 30

New LNG terminal projects proposed in the USA (bcm)

“US to become largest LNG exporter in 10 years”*

16 liquefaction plants with potential capacity of more than 200 bcm

Source: DOE data • research analyst reports• Presentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

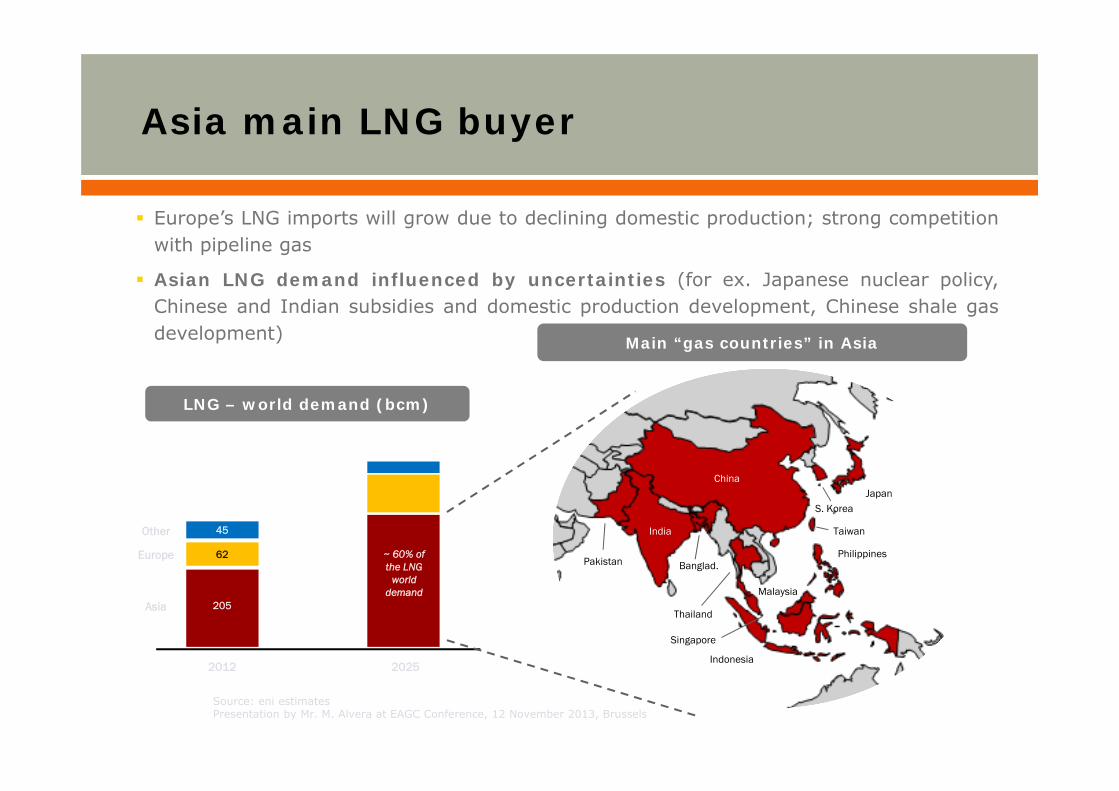

Europe’s LNG imports will grow due to declining domestic production; strong competitionwith pipeline gas

Asian LNG demand influenced by uncertainties (for ex. Japanese nuclear policy,Chinese and Indian subsidies and domestic production development, Chinese shale gasdevelopment)

LNG – world demand (bcm)

Asia main LNG buyer

Asia 205

62

45

Europe

Other

2012 2025

~ 60% of the LNG

world demand

China

India

Philippines

Malaysia

Indonesia

Thailand

JapanS. Korea

Banglad.Pakistan

Singapore

Taiwan

Main “gas countries” in Asia

Source: eni estimatesPresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

Agenda

I. Natural gas revolution

III. Policy developments EU and in BE

IV. Conclusion

II. Europe is paying the bill

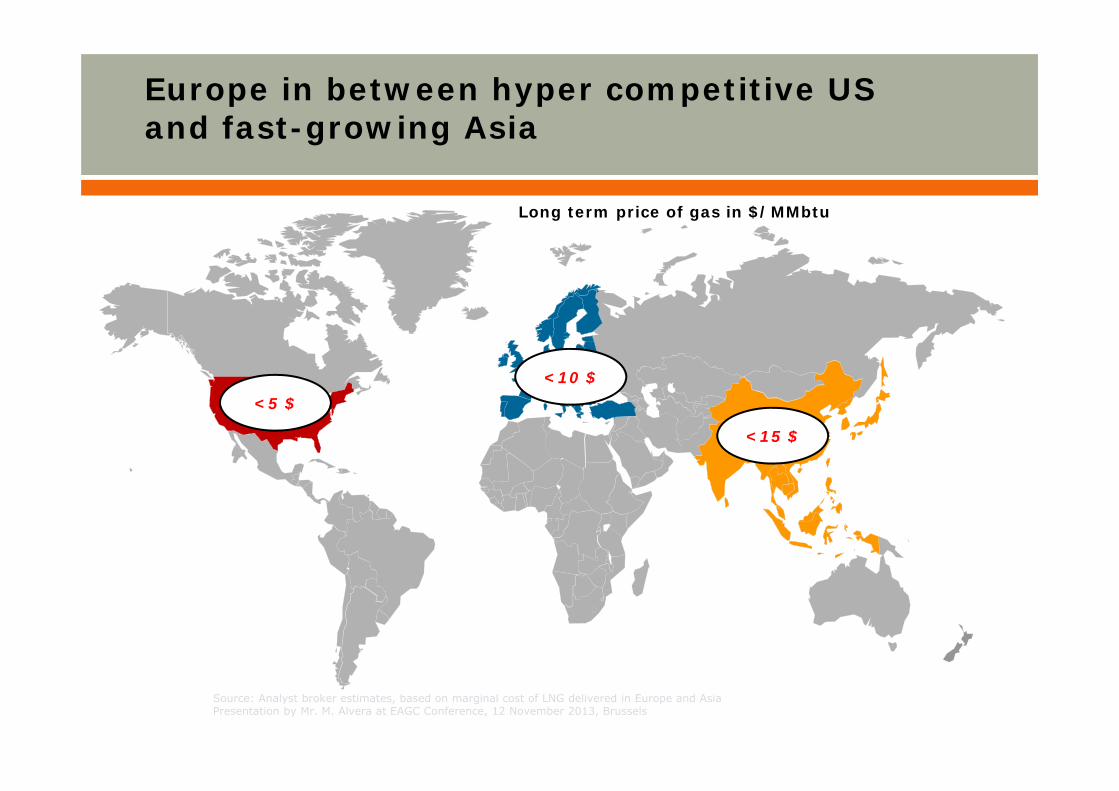

Long term price of gas in $/MMbtu

Source: Analyst broker estimates, based on marginal cost of LNG delivered in Europe and AsiaPresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

<5 $<10 $

<15 $

Europe in between hyper competitive US and fast-growing Asia

Source: Analyst broker estimates, analyst reportsPresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

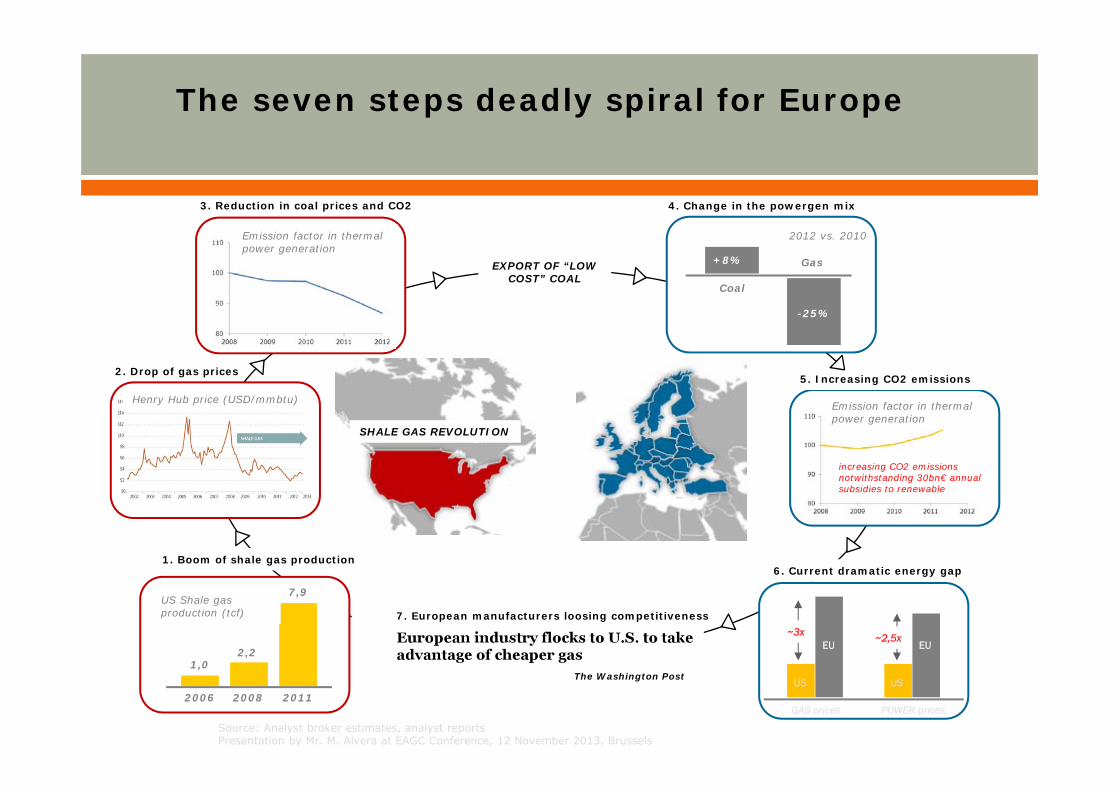

SHALE GAS REVOLUTION

2006 2008 2011

1,02,2

7,9US Shale gas production (tcf)

1. Boom of shale gas production

Henry Hub price (USD/mmbtu)

2. Drop of gas prices

Emission factor in thermal power generation

3. Reduction in coal prices and CO2

5. Increasing CO2 emissions

Emission factor in thermal power generation

increasing CO2 emissionsnotwithstanding 30bn€ annual subsidies to renewable

EXPORT OF “LOW COST” COAL

The Washington Post

POWER pricesGAS prices

US US

~3x ~2,5xEU EU

6. Current dramatic energy gap

4. Change in the powergen mix

+8%

Coal

Gas

-25%

2012 vs. 2010

7. European manufacturers loosing competitiveness

The seven steps deadly spiral for Europe

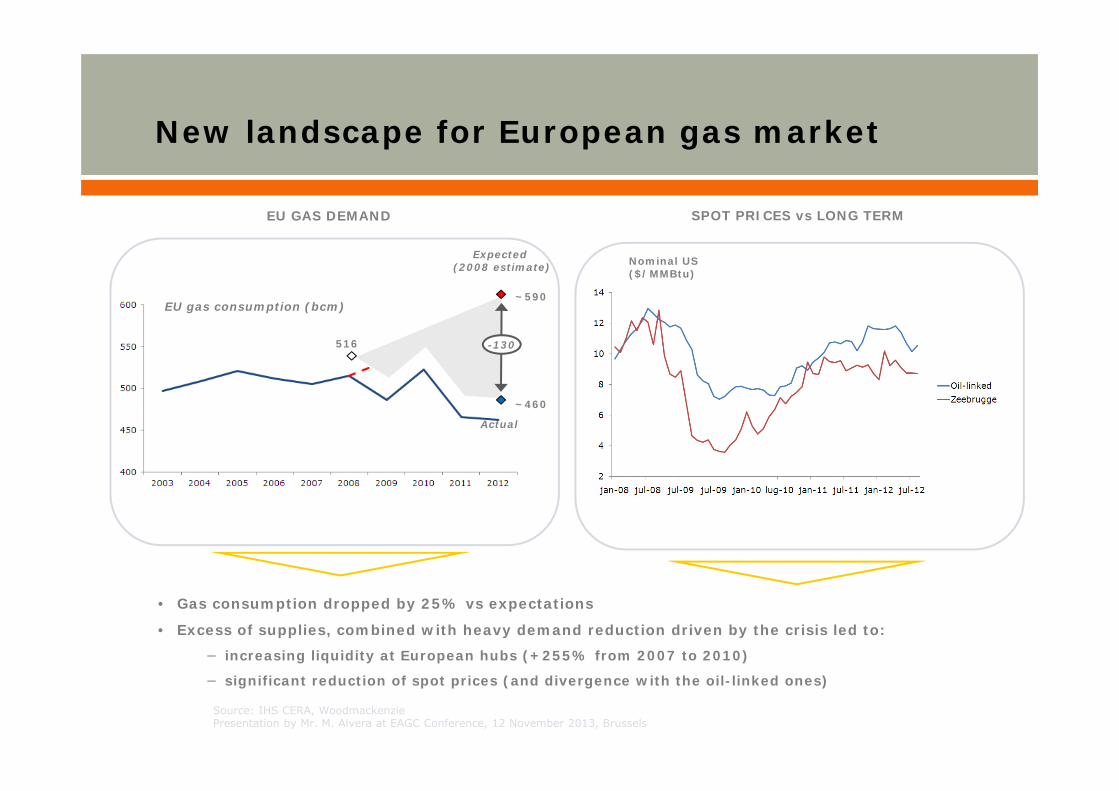

New landscape for European gas market

Nominal US ($/MMBtu)

EU GAS DEMAND SPOT PRICES vs LONG TERM

• Gas consumption dropped by 25% vs expectations

• Excess of supplies, combined with heavy demand reduction driven by the crisis led to:

− increasing liquidity at European hubs (+255% from 2007 to 2010)

− significant reduction of spot prices (and divergence with the oil-linked ones)

Source: IHS CERA, WoodmackenziePresentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

~590

~460

516 -130

Expected (2008 estimate)

Actual

EU gas consumption (bcm)

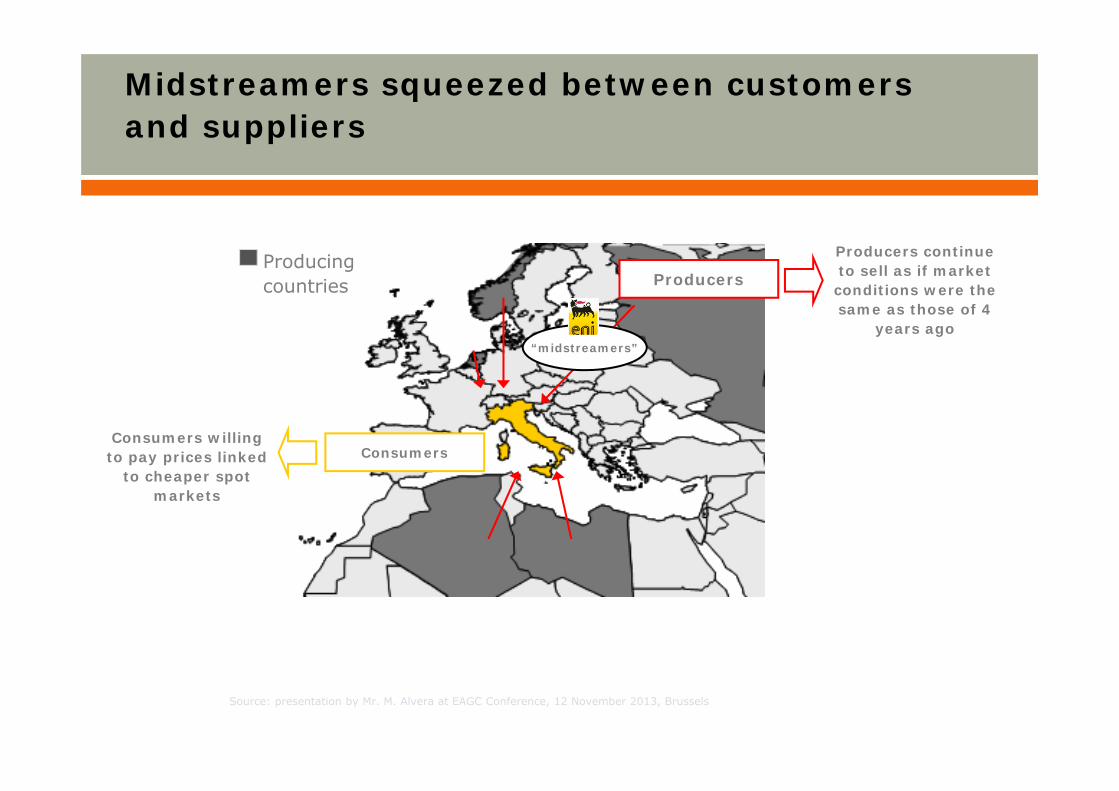

Midstreamers squeezed between customersand suppliers

Producers

Consumers

“midstreamers”

Consumers willing to pay prices linked

to cheaper spot markets

Producers continue to sell as if market conditions were the same as those of 4

years ago

Producing countries

Source: presentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

Agenda

I. Natural gas revolution

III. Policy developments EU and in BE

IV. Conclusion

II. Europe is paying the bill

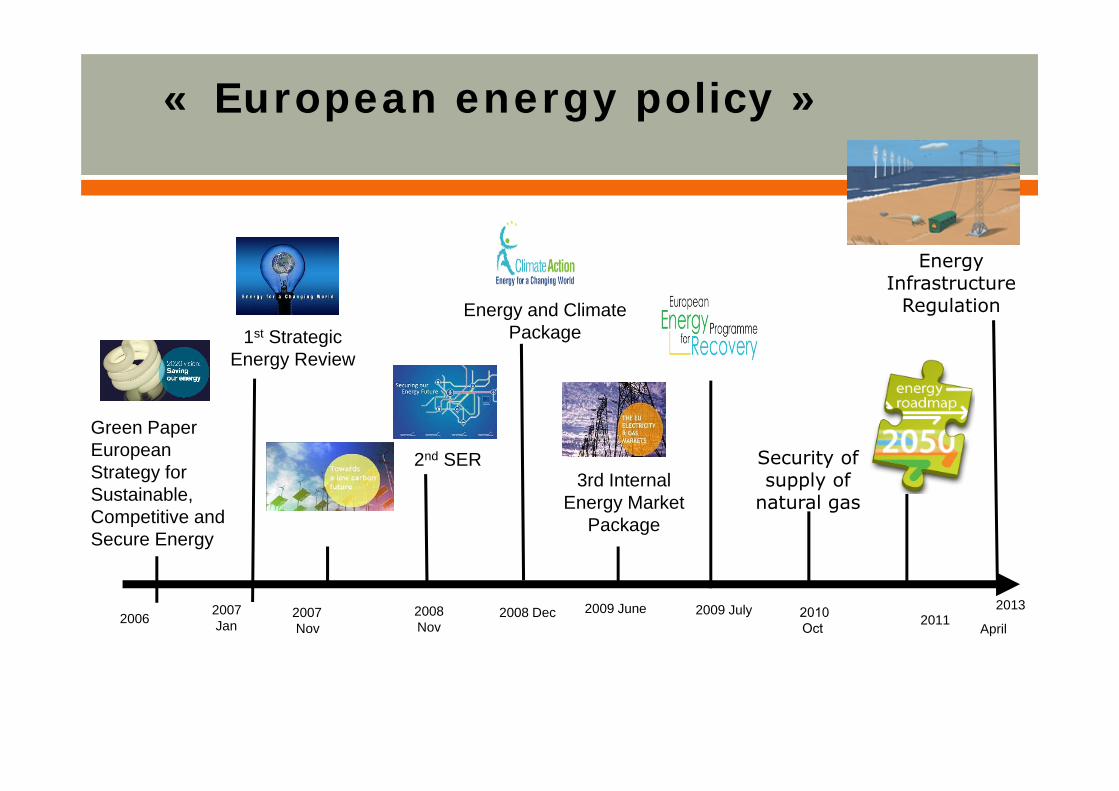

2007Jan

2008Nov 2011

2009 June

3rd Internal Energy Market

Package

Energy and Climate Package

2nd SER

2008 Dec2006

1st Strategic Energy Review

Green Paper European Strategy for Sustainable, Competitive and Secure Energy

2009 July

« European energy policy »

2007Nov

2010Oct

Security of supply of

natural gas

2013

April

Energy Infrastructure

Regulation

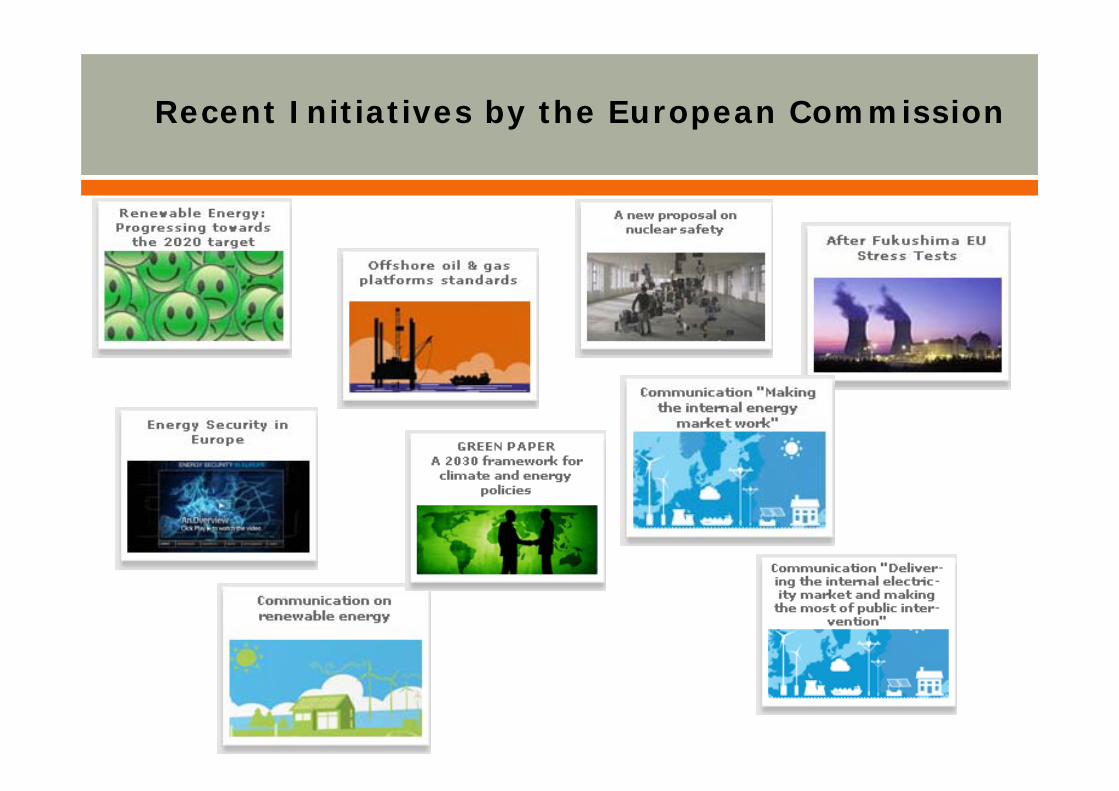

Recent Initiatives by the European Commission

In times of crisis, tendency to focus on prices of end consumerso Wallonia wants to introduce system of “free KwH” for householdso Flanders (and federal level): Prohibition to take margins on green

certificates• Flemish rule annulled by Constitutional Court

o Federal level: Since April 2012: price regulation scheme inspired by Dutch model “vangnetregulering”

• Variable energy prices can only be indexed every quarter• Limitation of use of indexation parameters

• Gas: no oil linked parameters

Production: Plan Wathelet wants to address security of supplyo Nuclear phase-out as of 2025o Support mechanisms for existing and new gas fired power plants given

lack of investments in gas fired power plants

Some highlights of recent Belgian energy policy

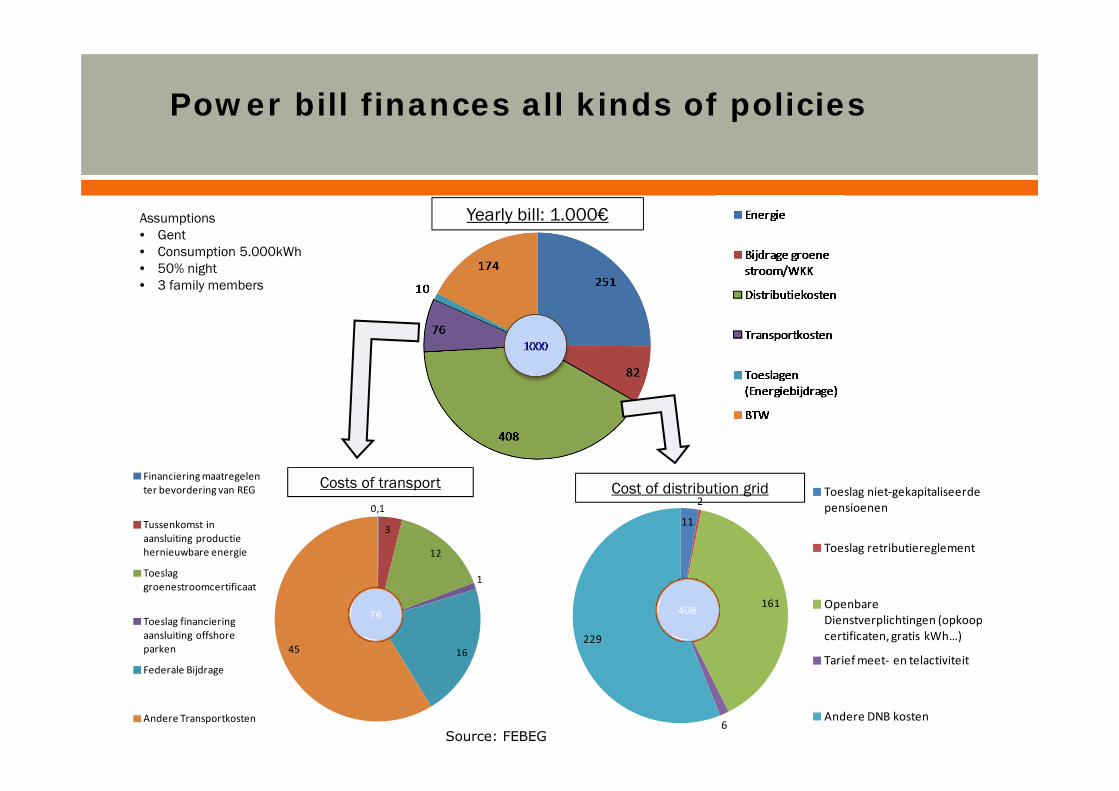

0,1

3

12

1

1645

11

2

161

6

229

408

Cost of distribution gridCosts of transportFinanciering maatregelen ter bevordering van REG

Tussenkomst in aansluiting productie hernieuwbare energie

Toeslag groenestroomcertificaat

Toeslag financiering aansluiting offshore parken

Federale Bijdrage

Andere Transportkosten

76

Yearly bill: 1.000€

Toeslag niet‐gekapitaliseerde pensioenen

Toeslag retributiereglement

Openbare Dienstverplichtingen (opkoop certificaten, gratis kWh…)

Tarief meet‐ en telactiviteit

Andere DNB kosten

Assumptions• Gent• Consumption 5.000kWh• 50% night• 3 family members

Power bill finances all kinds of policies

Source: FEBEG

Off-shore windmill parks in Belgiumo 15,7 billion € in next 20 yearso 800 million € per year

Income for operators: o 1/3 power priceo Rest: certificates

• Do not depend on market price

Someone will have to pay forthis

17

The cost of wind

Agenda

I. Natural gas revolution

III. Policy developments EU and in BE

IV. Conclusion

II. Europe is paying the bill

19

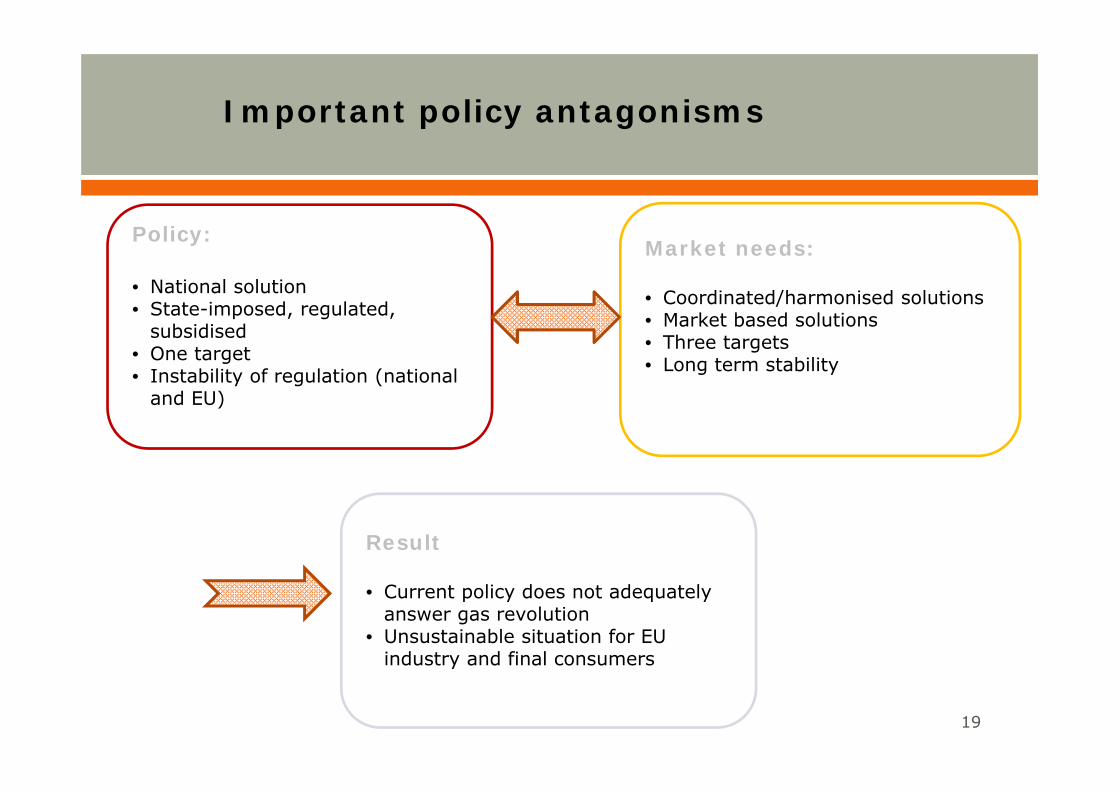

Policy:

• National solution• State-imposed, regulated,

subsidised• One target• Instability of regulation (national

and EU)

Market needs:

• Coordinated/harmonised solutions• Market based solutions• Three targets• Long term stability

Result

• Current policy does not adequatelyanswer gas revolution

• Unsustainable situation for EU industry and final consumers

Important policy antagonisms

What Europe should do

1. European should pursue extraction of its indigenous potential

2. Actively engage neighbouring producing countries to redefine an

energy alliance based on low predictable prices and growing

consumption of natural gas

3. Limit the revival of coal in order to achieve environmental targets

and invest in R&D for new renewable technology, limiting older-

generation renewable subsidies to improve competitiveness

20

Source: presentation by Mr. M. Alvera at EAGC Conference, 12 November 2013, Brussels

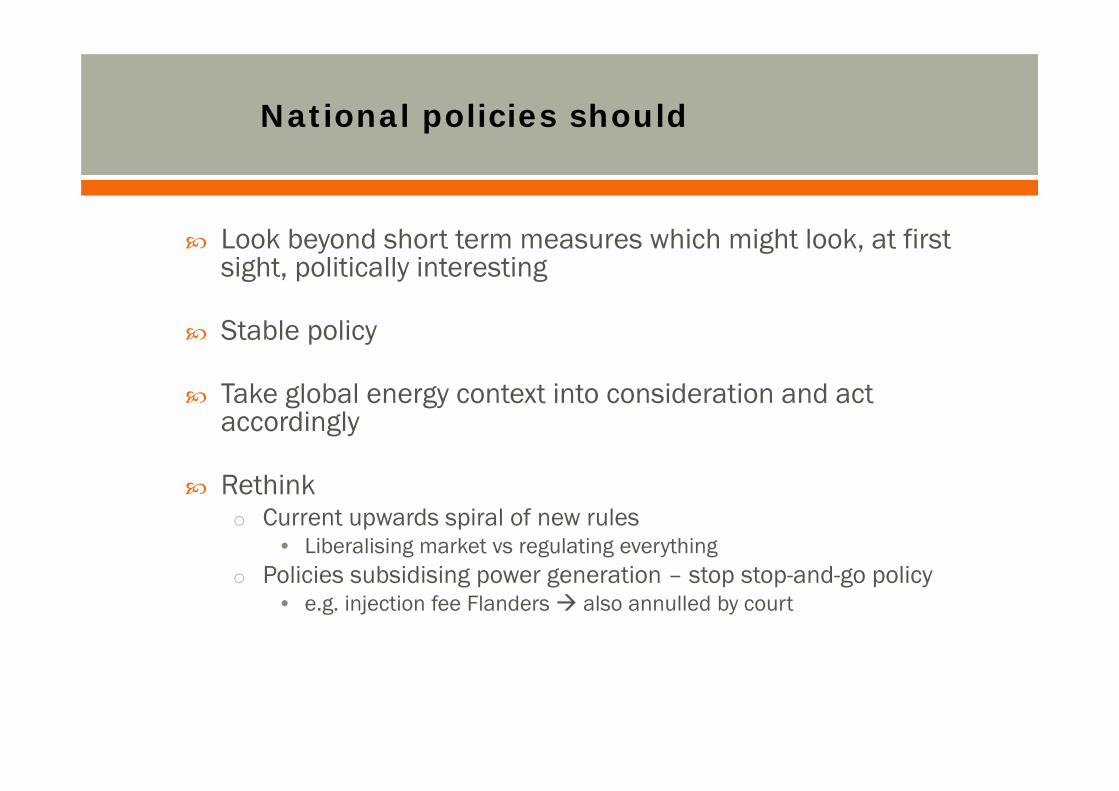

Look beyond short term measures which might look, at first sight, politically interesting

Stable policy

Take global energy context into consideration and act accordingly

Rethink o Current upwards spiral of new rules

• Liberalising market vs regulating everythingo Policies subsidising power generation – stop stop-and-go policy

• e.g. injection fee Flanders also annulled by court

National policies should