Embed Size (px)

Citation preview

The future of the vehicleExploring the future of mobility and implications for the aftermarket

Neal GanguliAutomotive Supplier Consulting LeaderDeloitte Consulting LLP

Copyright © 2017 Deloitte Development LLC. All rights reserved. 1

What does the Future of Mobility means for vehicles and content?

What are the implications for aftermarket players?

Our journey today

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 2

The future of mobilityDeloitte’s view on future automotive archetypes and impact on Automotive Industry players

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 3

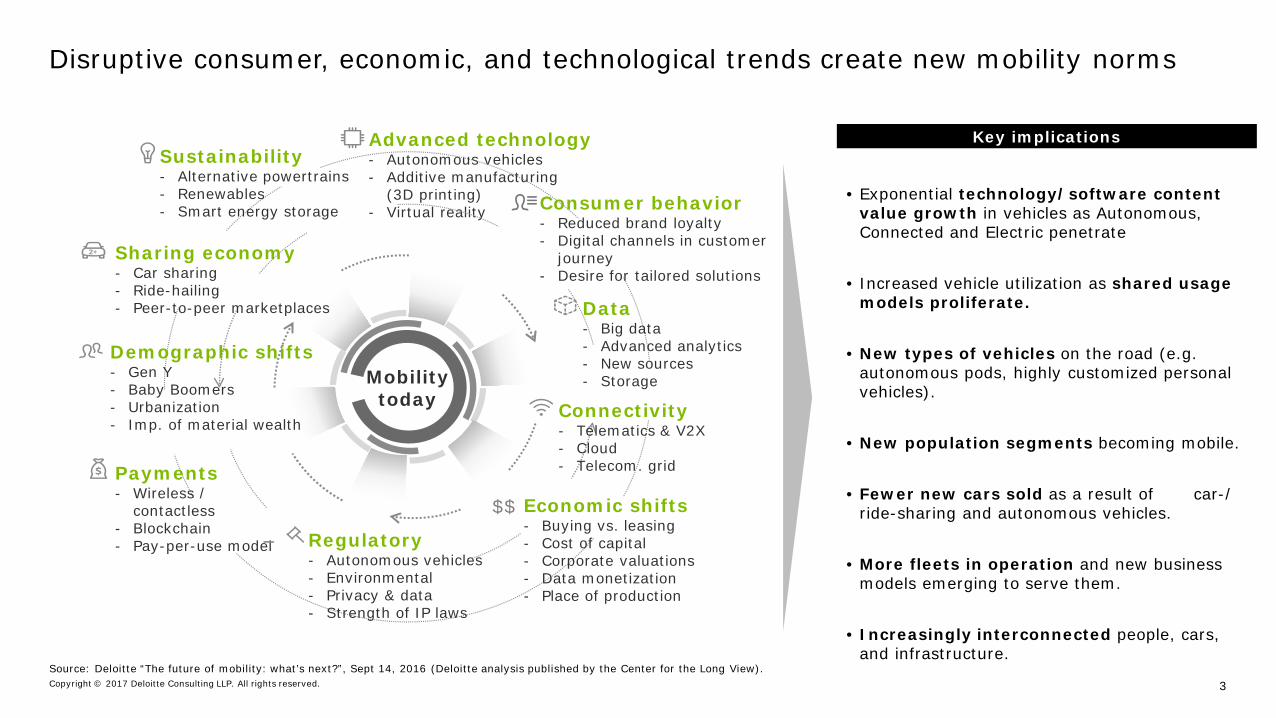

Disruptive consumer, economic, and technological trends create new mobility norms

Source: Deloitte “The future of mobility: what’s next?”, Sept 14, 2016 (Deloitte analysis published by the Center for the Long View).

• Exponential technology/software content value growth in vehicles as Autonomous, Connected and Electric penetrate

• Increased vehicle utilization as shared usage models proliferate.

• New types of vehicles on the road (e.g. autonomous pods, highly customized personal vehicles).

• New population segments becoming mobile.

• Fewer new cars sold as a result of car-/ ride-sharing and autonomous vehicles.

• More fleets in operation and new business models emerging to serve them.

• Increasingly interconnected people, cars, and infrastructure.

Advanced technology- Autonomous vehicles- Additive manufacturing

(3D printing) - Virtual reality

Mobility today

Data- Big data- Advanced analytics- New sources- Storage

Connectivity- Telematics & V2X- Cloud- Telecom. grid

Sustainability- Alternative powertrains- Renewables- Smart energy storage

Payments- Wireless /

contactless- Blockchain- Pay-per-use model

Demographic shifts- Gen Y- Baby Boomers- Urbanization- Imp. of material wealth

Sharing economy- Car sharing- Ride-hailing- Peer-to-peer marketplaces

Regulatory- Autonomous vehicles- Environmental- Privacy & data- Strength of IP laws

Economic shifts- Buying vs. leasing- Cost of capital- Corporate valuations- Data monetization- Place of production

$$

Consumer behavior- Reduced brand loyalty- Digital channels in customer

journey- Desire for tailored solutions

Key implications

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 4

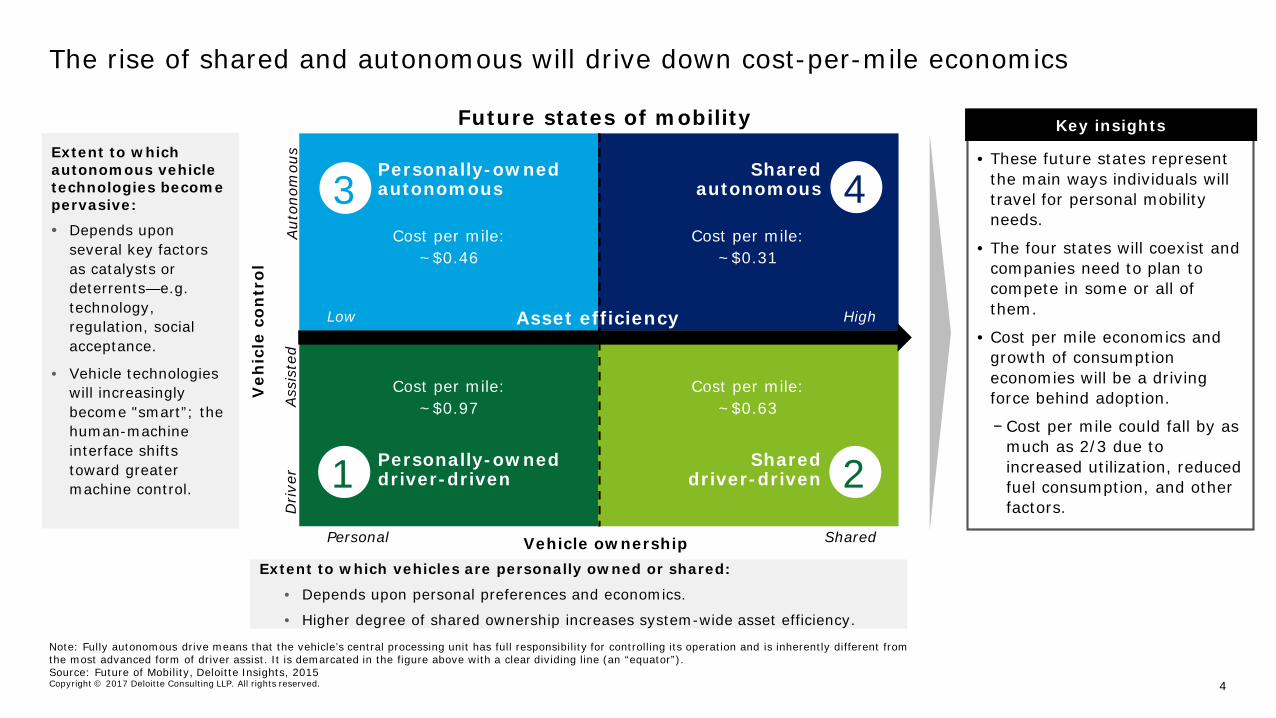

The rise of shared and autonomous will drive down cost-per-mile economics

Extent to which autonomous vehicle technologies become pervasive:

• Depends upon several key factors as catalysts or deterrents—e.g. technology, regulation, social acceptance.

• Vehicle technologies will increasingly become "smart”; the human-machine interface shifts toward greater machine control.

Extent to which vehicles are personally owned or shared:

• Depends upon personal preferences and economics.

• Higher degree of shared ownership increases system-wide asset efficiency.

Personal Shared

Aut

onom

ous

Drive

r

Future states of mobility

Vehicle ownership

Veh

icle

con

trol

Shared autonomous

Shareddriver-driven

Personally-owned autonomous

Personally-owned driver-driven1 2

3 4

Asset efficiencyLow High

Ass

iste

d

Note: Fully autonomous drive means that the vehicle’s central processing unit has full responsibility for controlling its operation and is inherently different from the most advanced form of driver assist. It is demarcated in the figure above with a clear dividing line (an “equator”). Source: Future of Mobility, Deloitte Insights, 2015

• These future states represent the main ways individuals will travel for personal mobility needs.

• The four states will coexist and companies need to plan to compete in some or all of them.

• Cost per mile economics and growth of consumption economies will be a driving force behind adoption.

− Cost per mile could fall by as much as 2/3 due to increased utilization, reduced fuel consumption, and other factors.

Cost per mile:~$0.46

Cost per mile:~$0.31

Cost per mile:~$0.97

Cost per mile:~$0.63

Key insights

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 5

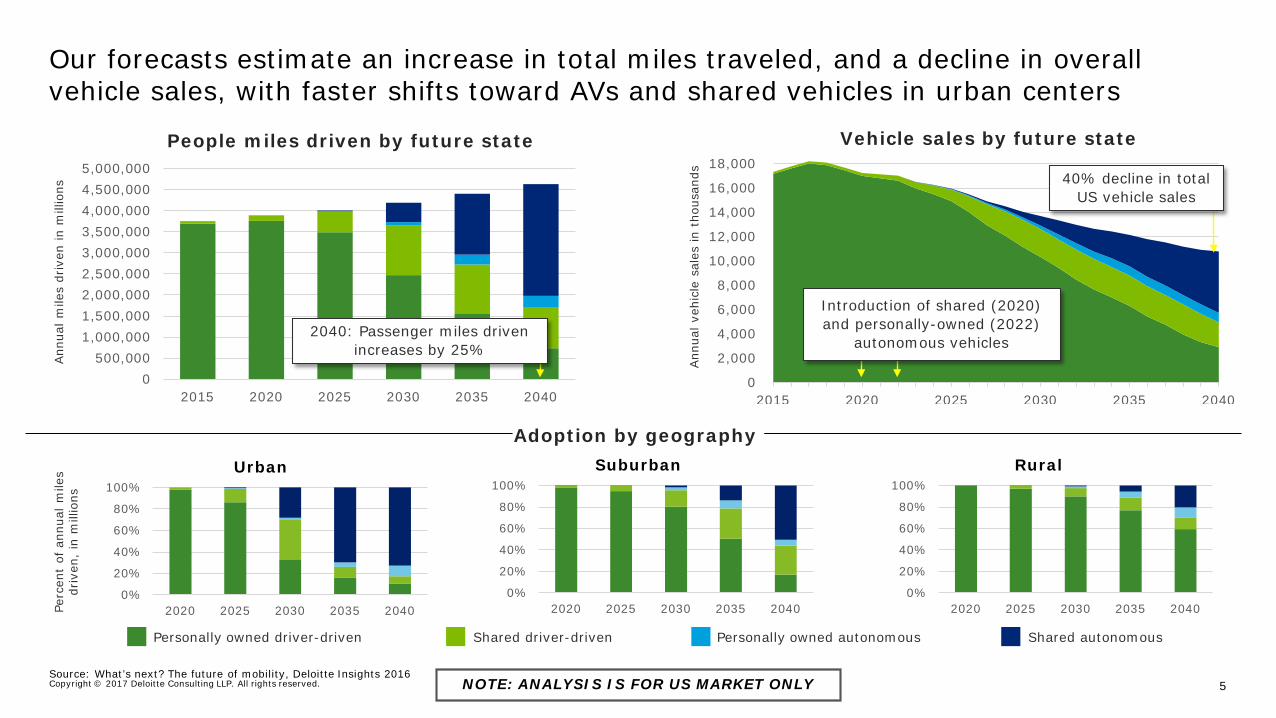

Our forecasts estimate an increase in total miles traveled, and a decline in overall vehicle sales, with faster shifts toward AVs and shared vehicles in urban centers

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2015 2020 2025 2030 2035 2040

Vehicle sales by future state

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,0004,000,0004,500,0005,000,000

2015 2020 2025 2030 2035 2040

People miles driven by future state

Personally owned driver-driven Shared driver-driven Personally owned autonomous Shared autonomous

Introduction of shared (2020) and personally-owned (2022)

autonomous vehicles2040: Passenger miles driven

increases by 25%

Urban Suburban Rural

Perc

ent

of a

nnua

l m

iles

driv

en,

in m

illio

nsAnn

ual m

iles

driv

en in

mill

ions

Ann

ual v

ehic

le s

ales

in t

hous

ands

Adoption by geography

40% decline in total US vehicle sales

0%

20%

40%

60%

80%

100%

2020 2025 2030 2035 20400%

20%

40%

60%

80%

100%

2020 2025 2030 2035 20400%

20%

40%

60%

80%

100%

2020 2025 2030 2035 2040

Source: What’s next? The future of mobility, Deloitte Insights 2016NOTE: ANALYSIS IS FOR US MARKET ONLY

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 6

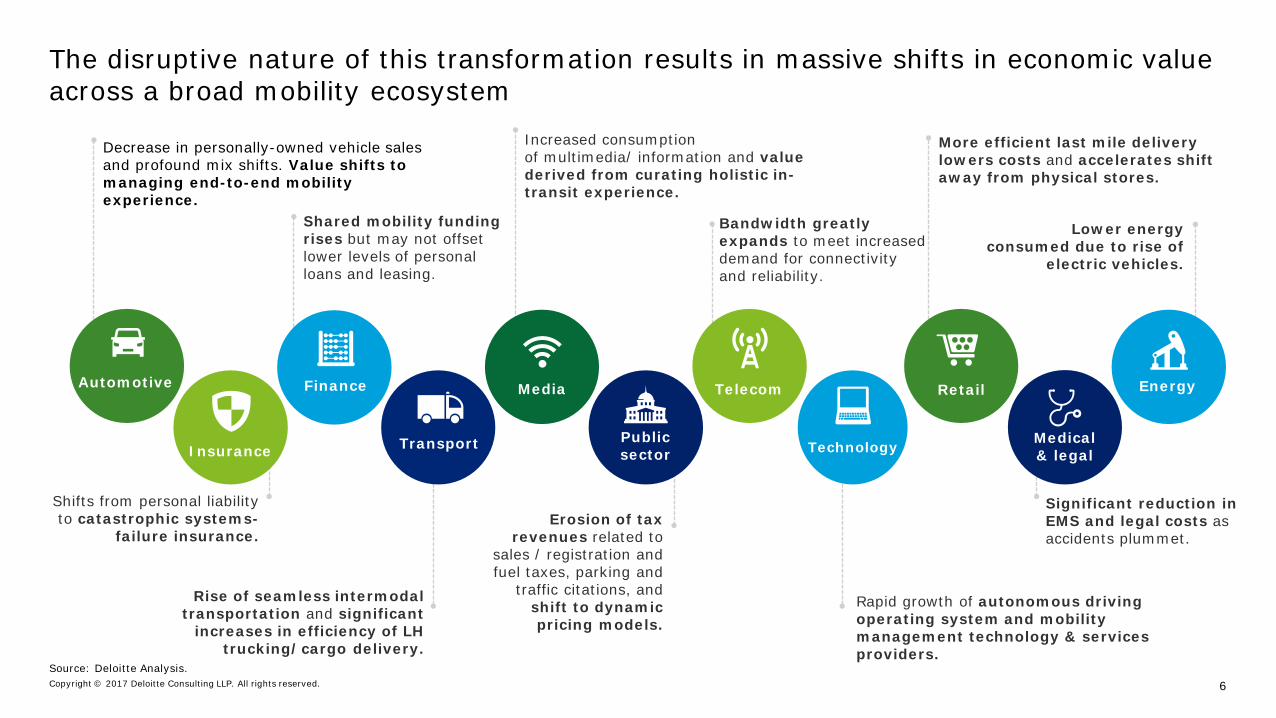

The disruptive nature of this transformation results in massive shifts in economic value across a broad mobility ecosystem

Increased consumption of multimedia/ information and value derived from curating holistic in-transit experience.

Decrease in personally-owned vehicle sales and profound mix shifts. Value shifts to managing end-to-end mobility experience.

Shared mobility funding rises but may not offset lower levels of personal loans and leasing.

Rapid growth of autonomous driving operating system and mobility management technology & servicesproviders.

Shifts from personal liability to catastrophic systems-

failure insurance.

Lower energy consumed due to rise of

electric vehicles.

Erosion of tax revenues related to

sales / registration and fuel taxes, parking and

traffic citations, and shift to dynamic pricing models.

More efficient last mile delivery lowers costs and accelerates shift away from physical stores.

Bandwidth greatly expands to meet increased demand for connectivity and reliability.

Significant reduction in EMS and legal costs as accidents plummet.

Rise of seamless intermodal transportation and significant

increases in efficiency of LH trucking/cargo delivery.

EnergyFinance

TransportInsurance

TelecomAutomotive Retail

Publicsector

Medical& legalTechnology

Media

Source: Deloitte Analysis.

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 7

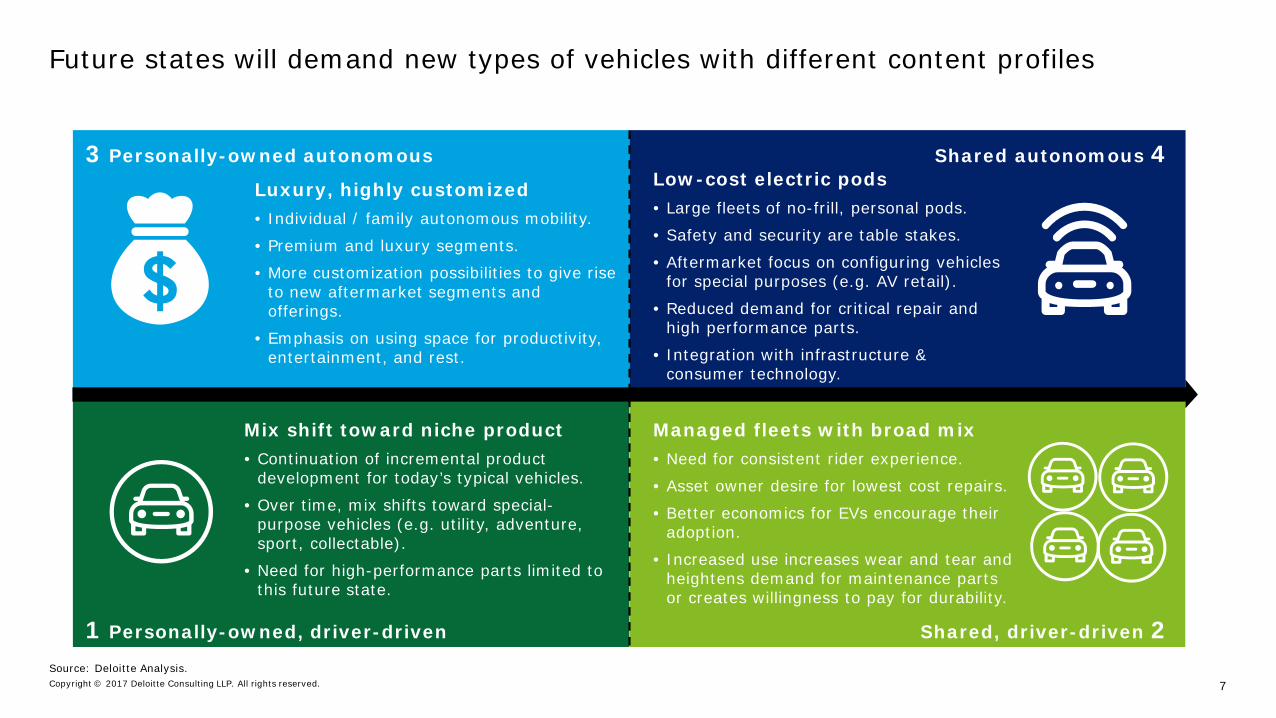

Future states will demand new types of vehicles with different content profiles

Luxury, highly customized• Individual / family autonomous mobility.

• Premium and luxury segments.

• More customization possibilities to give rise to new aftermarket segments and offerings.

• Emphasis on using space for productivity, entertainment, and rest.

Mix shift toward niche product• Continuation of incremental product

development for today’s typical vehicles.

• Over time, mix shifts toward special-purpose vehicles (e.g. utility, adventure, sport, collectable).

• Need for high-performance parts limited to this future state.

Shared autonomous 4

Shared, driver-driven 2

3 Personally-owned autonomous

1 Personally-owned, driver-driven

Low-cost electric pods• Large fleets of no-frill, personal pods.

• Safety and security are table stakes.

• Aftermarket focus on configuring vehicles for special purposes (e.g. AV retail).

• Reduced demand for critical repair and high performance parts.

• Integration with infrastructure & consumer technology.

Managed fleets with broad mix• Need for consistent rider experience.

• Asset owner desire for lowest cost repairs.

• Better economics for EVs encourage their adoption.

• Increased use increases wear and tear and heightens demand for maintenance parts or creates willingness to pay for durability.

Source: Deloitte Analysis.

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 8

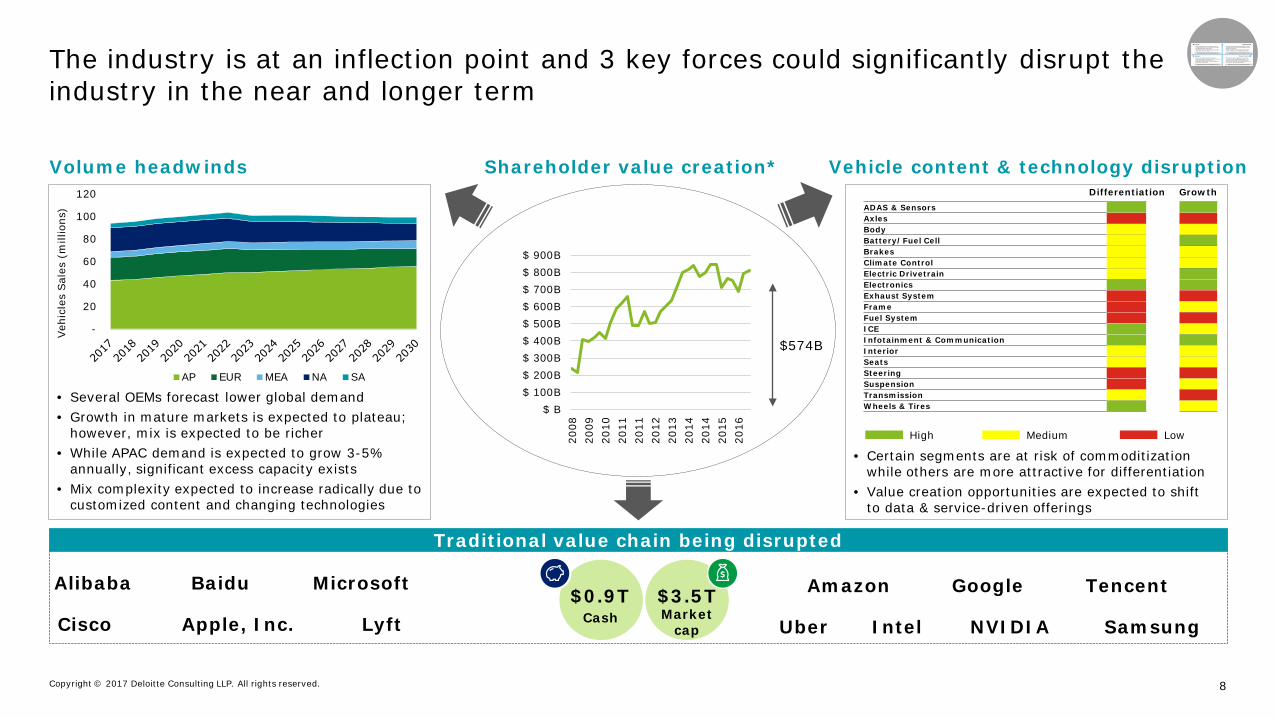

The industry is at an inflection point and 3 key forces could significantly disrupt the industry in the near and longer term

Volume headwinds Shareholder value creation*

• Several OEMs forecast lower global demand• Growth in mature markets is expected to plateau;

however, mix is expected to be richer• While APAC demand is expected to grow 3-5%

annually, significant excess capacity exists• Mix complexity expected to increase radically due to

customized content and changing technologies

GrowthDifferentiation

$ B$ 100B$ 200B$ 300B$ 400B$ 500B$ 600B$ 700B$ 800B$ 900B

2008

2009

2010

2011

2011

2012

2013

2014

2014

2015

2016

Vehicle content & technology disruption

Traditional value chain being disrupted

$0.9TCash

$3.5TMarket

cap

$574B -

20

40

60

80

100

120

Vehi

cles

Sal

es (

mill

ions

)

AP EUR MEA NA SA

• Certain segments are at risk of commoditization while others are more attractive for differentiation

• Value creation opportunities are expected to shift to data & service-driven offerings

ADAS & SensorsAxlesBodyBattery/Fuel CellBrakesClimate ControlElectric DrivetrainElectronicsExhaust SystemFrameFuel SystemICEInfotainment & CommunicationInteriorSeatsSteeringSuspensionTransmissionWheels & Tires

Alibaba

Cisco

Baidu Microsoft

LyftApple, Inc. Uber Intel

GoogleAmazon

NVIDIA Samsung

Tencent

LowMediumHigh

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 9

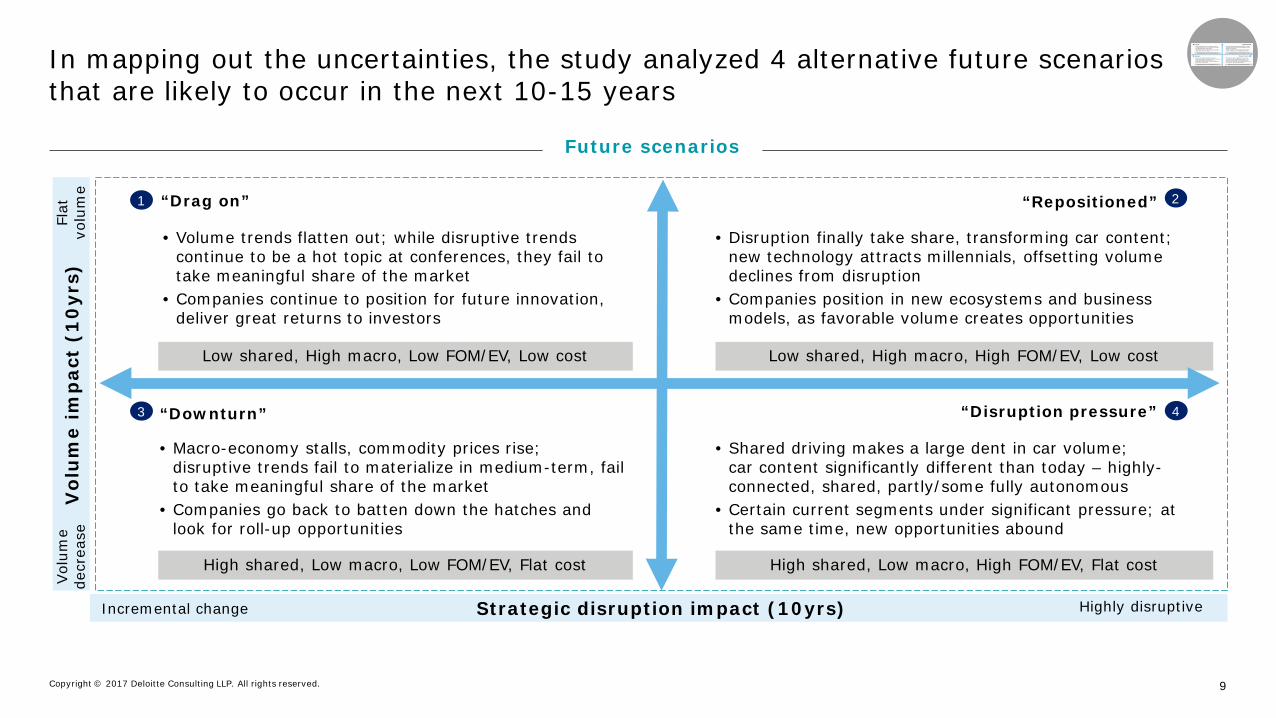

In mapping out the uncertainties, the study analyzed 4 alternative future scenarios that are likely to occur in the next 10-15 years

Vol

um

e im

pac

t (1

0yr

s)

Strategic disruption impact (10yrs)

“Repositioned” 2

Flat

vo

lum

eVol

ume

decr

ease

Highly disruptive

• Volume trends flatten out; while disruptive trends continue to be a hot topic at conferences, they fail to take meaningful share of the market

• Companies continue to position for future innovation, deliver great returns to investors

“Drag on”1

• Disruption finally take share, transforming car content; new technology attracts millennials, offsetting volume declines from disruption

• Companies position in new ecosystems and business models, as favorable volume creates opportunities

• Macro-economy stalls, commodity prices rise; disruptive trends fail to materialize in medium-term, fail to take meaningful share of the market

• Companies go back to batten down the hatches and look for roll-up opportunities

“Downturn”

• Shared driving makes a large dent in car volume; car content significantly different than today – highly-connected, shared, partly/some fully autonomous

• Certain current segments under significant pressure; at the same time, new opportunities abound

3

Low shared, High macro, Low FOM/EV, Low cost Low shared, High macro, High FOM/EV, Low cost

High shared, Low macro, Low FOM/EV, Flat cost

“Disruption pressure” 4

High shared, Low macro, High FOM/EV, Flat cost

Future scenarios

Incremental change

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 10

$17 $26 $24 $32 $35

$51 $42 $46 $49

$13 $83

$138 $20

$38 $143

$104 $105

$249 $242

-27%-3%5%

-15%-4%

-27%-5%

-11%4%

415%12%

-26%551%254%

-6%29%34%

-20%-5%

$12 $25 $25 $27 $34 $37 $40 $41 $52 $69

$93 $102

$132 $133 $133 $135 $141

$199 $230

Fuel system

Suspension

Climate control

Steering

Brakes

Exhaust system

Axles

Frame

Wheels & tires

Electric drivetrain

Seats

Transmission

ADAS & sensors

Battery / Fuel cell

Interior

Electronics

Infotainment & communication

ICE

Body

Total segment revenue expected to grow from 2017-2030

-200 B

-100 B

B

100 B

200 B

300 B

400 B

500 B

600 B

Risk Afermarket/Service

Traditionalcontent/Volume

AEV content/Volume

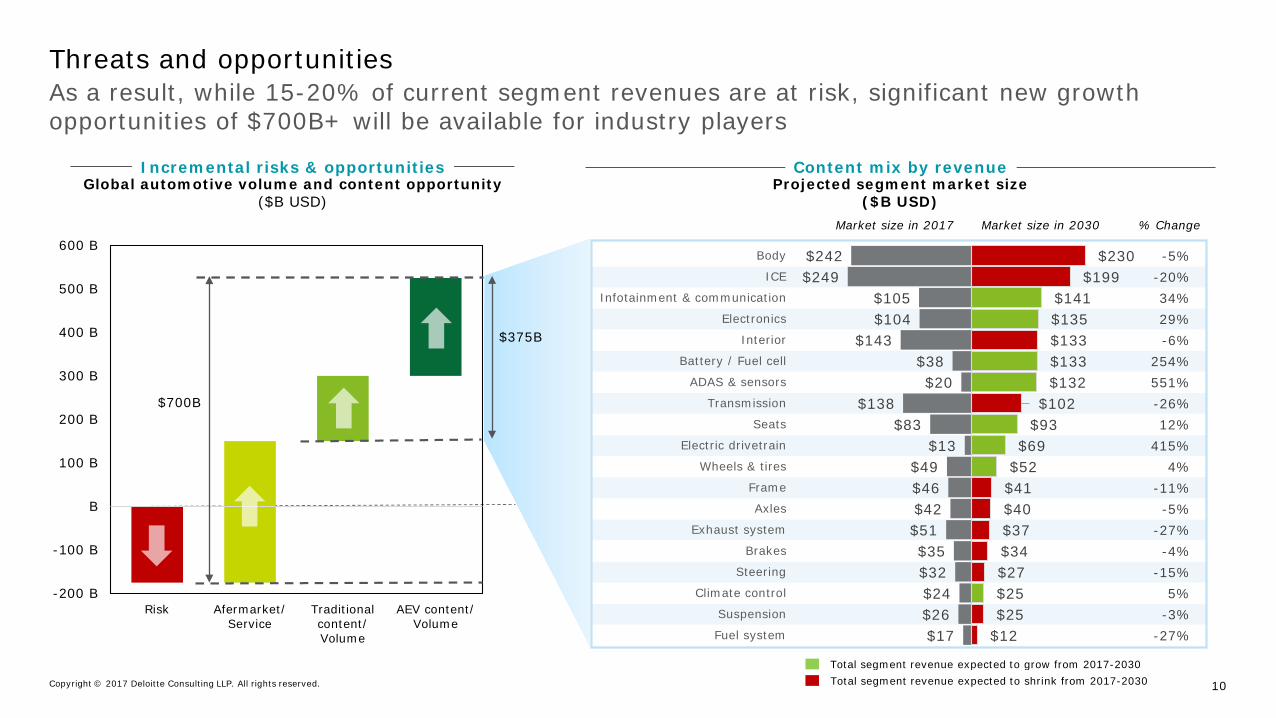

Incremental risks & opportunities Content mix by revenueGlobal automotive volume and content opportunity

($B USD)Projected segment market size

($B USD)

Total segment revenue expected to shrink from 2017-2030

Market size in 2017 Market size in 2030

$375B

$700B

% Change

As a result, while 15-20% of current segment revenues are at risk, significant new growth opportunities of $700B+ will be available for industry players

Threats and opportunities

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 11

ADAS & sensors

Infotainment & communication

ElectronicsElectric

drivetrain

Battery / Fuel Cell

ICE

Wheels & tires

Seats

Body

Interior

Transmission

Climate control

Brakes

Frame

Steering

Exhaust system

Fuel system

Suspension

Axles

1.6

2.1

2.6

3.1

3.6

4.1

4.6

1.4 1.9 2.4 2.9 3.4 3.9 4.4 4.9

Gro

wth

po

ten

tial

Ability to differentiate

Median differentiation Score

Median growth score

Overall attractiveness varies across product segments, with several facing significant risk of commoditization/decline

Observations

• Suppliers, OEMs as well as non-traditional suppliers and high tech players vying for competitive position in attractive segments

• Attractive segments’ traditional value chain is being challenged, as the technology disruption occurs – e.g., tier leapfrogging may challenge the traditional linear model

• Suppliers with product portfolio in middle-ground segments are shifting focus to more profitable segments and enhanced value propositions

• Players in segments with higher risk and asset intensity may begin to consolidate further and/or become potential acquisition targets

Attractive

Risky

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 12

$17 $26 $24 $32 $35

$51 $42 $46 $49

$13 $83

$138 $20

$38 $143

$104 $105

$249 $242

-27%-3%5%

-15%-4%

-27%-5%

-11%4%

415%12%

-26%551%254%

-6%29%34%

-20%-5%

$12 $25 $25 $27 $34 $37 $40 $41 $52 $69

$93 $102

$132 $133 $133 $135 $141

$199 $230

Fuel system

Suspension

Climate control

Steering

Brakes

Exhaust system

Axles

Frame

Wheels & tires

Electric drivetrain

Seats

Transmission

ADAS & sensors

Battery / Fuel cell

Interior

Electronics

Infotainment & communication

ICE

Body

Incremental risks & opportunities Content mix by revenue

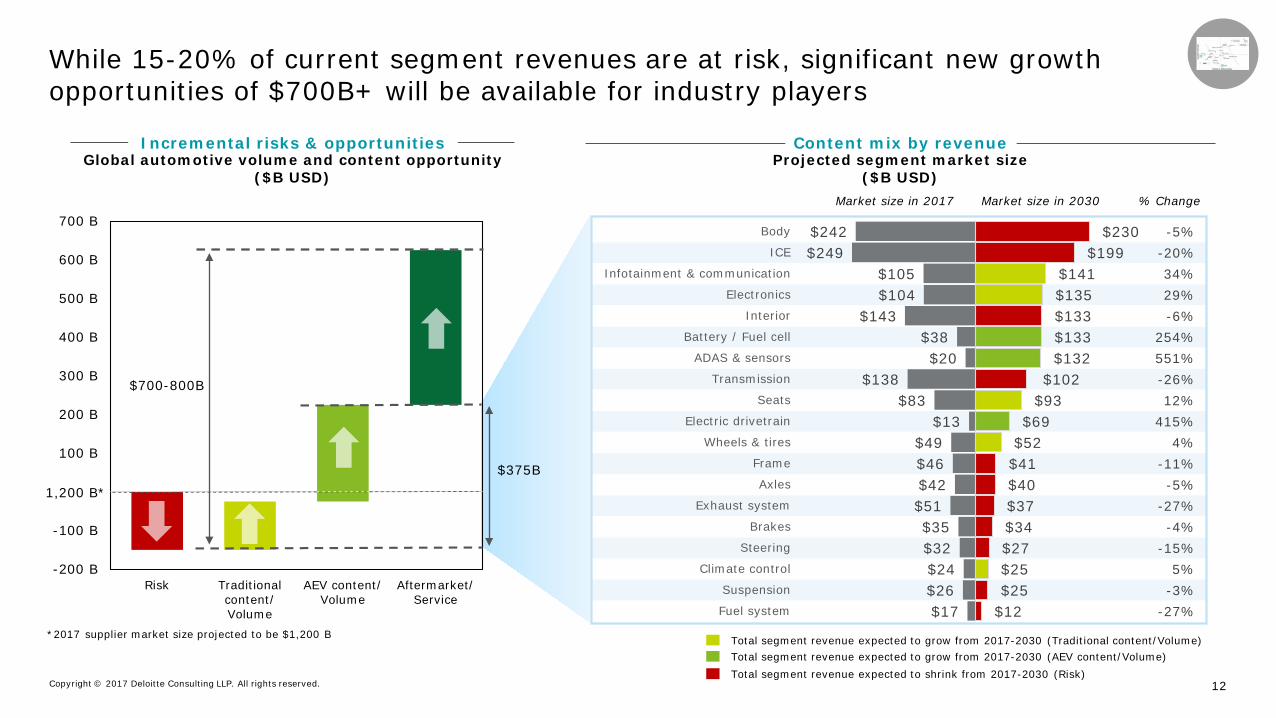

While 15-20% of current segment revenues are at risk, significant new growth opportunities of $700B+ will be available for industry players

Global automotive volume and content opportunity ($B USD)

Projected segment market size ($B USD)

Total segment revenue expected to grow from 2017-2030 (AEV content/Volume)

Market size in 2017 Market size in 2030 % Change

$375B

Total segment revenue expected to shrink from 2017-2030 (Risk)

Total segment revenue expected to grow from 2017-2030 (Traditional content/Volume)

-200 B

-100 B

B

100 B

200 B

300 B

400 B

500 B

600 B

700 B

Risk Traditionalcontent/Volume

AEV content/Volume

Aftermarket/Service

$700-800B

1,200 B*

*2017 supplier market size projected to be $1,200 B

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 13

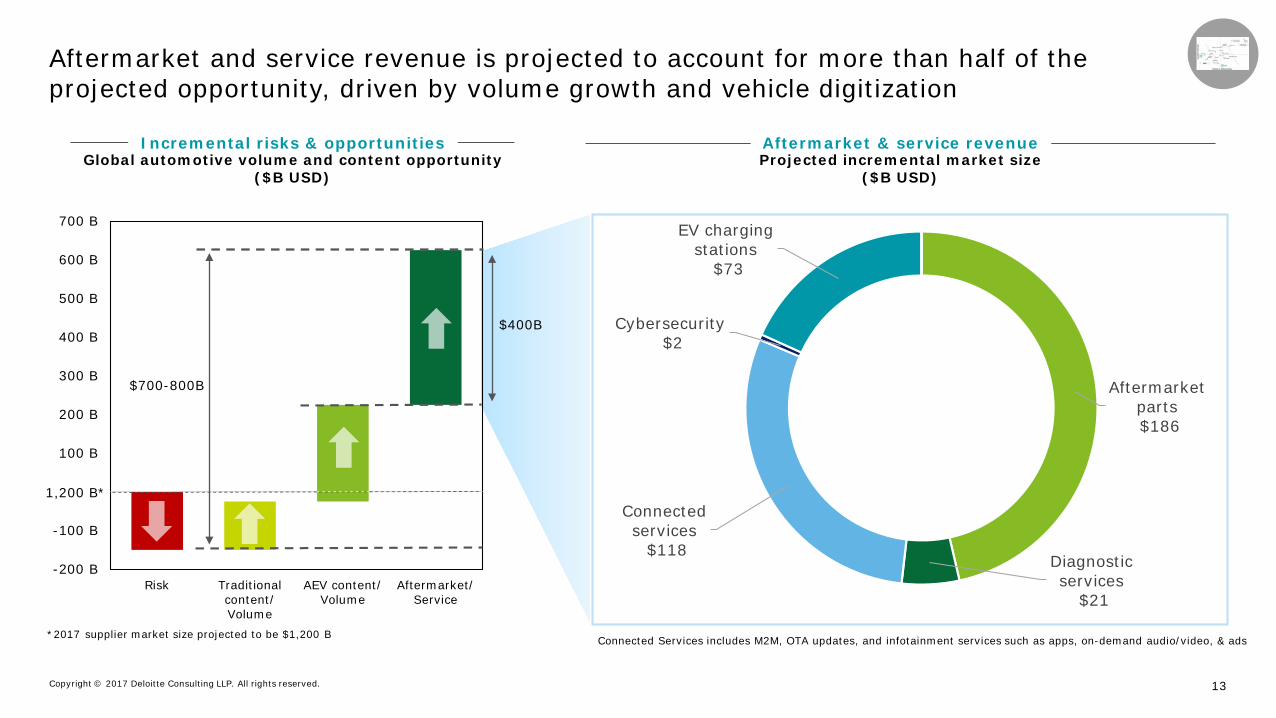

-200 B

-100 B

B

100 B

200 B

300 B

400 B

500 B

600 B

700 B

Risk Traditionalcontent/Volume

AEV content/Volume

Aftermarket/Service

Incremental risks & opportunities Aftermarket & service revenue

Aftermarket and service revenue is projected to account for more than half of the projected opportunity, driven by volume growth and vehicle digitization

Global automotive volume and content opportunity ($B USD)

Projected incremental market size ($B USD)

$400B

$700-800B Aftermarket parts$186

Diagnostic services

$21

Connected services

$118

Cybersecurity$2

EV charging stations

$73

Connected Services includes M2M, OTA updates, and infotainment services such as apps, on-demand audio/video, & ads*2017 supplier market size projected to be $1,200 B

1,200 B*

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 14

Implications for automotive aftermarketTrends shaping the aftermarket industryPotential considerations for aftermarket players

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 15

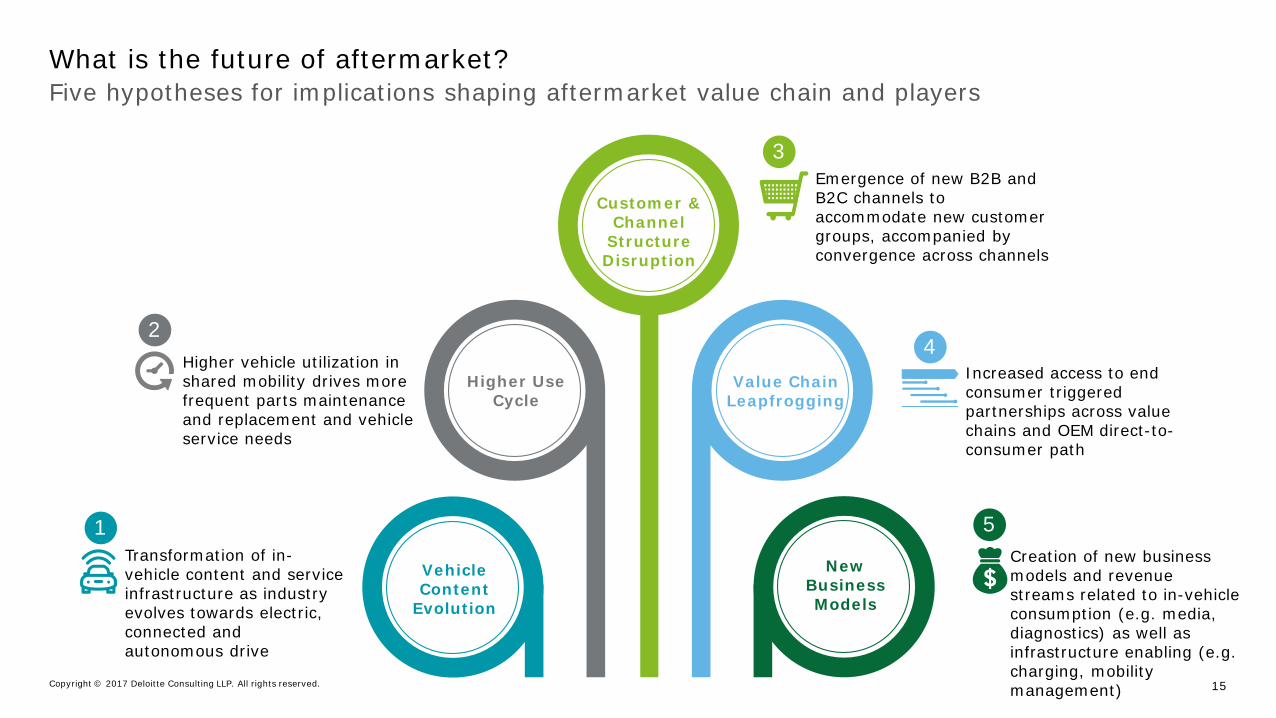

Five hypotheses for implications shaping aftermarket value chain and playersWhat is the future of aftermarket?

Customer & Channel

Structure Disruption

Value Chain Leapfrogging

Higher Use Cycle

Vehicle Content

Evolution

New Business Models

Higher vehicle utilization in shared mobility drives more frequent parts maintenance and replacement and vehicle service needs

Transformation of in-vehicle content and service infrastructure as industry evolves towards electric, connected and autonomous drive

Emergence of new B2B and B2C channels to accommodate new customer groups, accompanied by convergence across channels

Increased access to end consumer triggered partnerships across value chains and OEM direct-to-consumer path

Creation of new business models and revenue streams related to in-vehicle consumption (e.g. media, diagnostics) as well as infrastructure enabling (e.g. charging, mobility management)

3

4

5

2

1

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 16

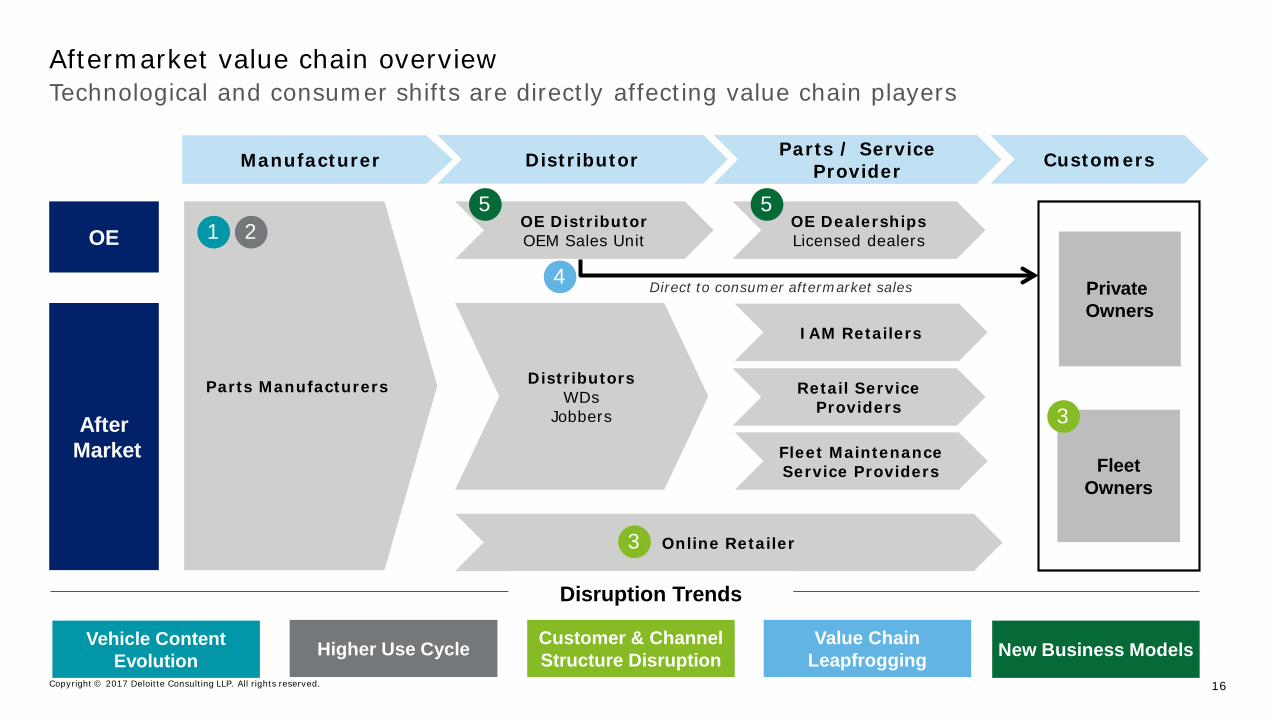

Technological and consumer shifts are directly affecting value chain playersAftermarket value chain overview

Parts Manufacturers

OE DistributorOEM Sales UnitOE

AfterMarket

Direct to consumer aftermarket sales

DistributorsWDs

Jobbers

Online Retailer

OE DealershipsLicensed dealers

IAM Retailers

Retail Service Providers

Fleet Maintenance Service Providers

Private Owners

FleetOwners

3

3

4

1 25 5

DistributorManufacturer Parts / Service Provider Customers

Disruption Trends

Vehicle Content Evolution Higher Use Cycle Customer & Channel

Structure DisruptionValue Chain

Leapfrogging New Business Models

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 17

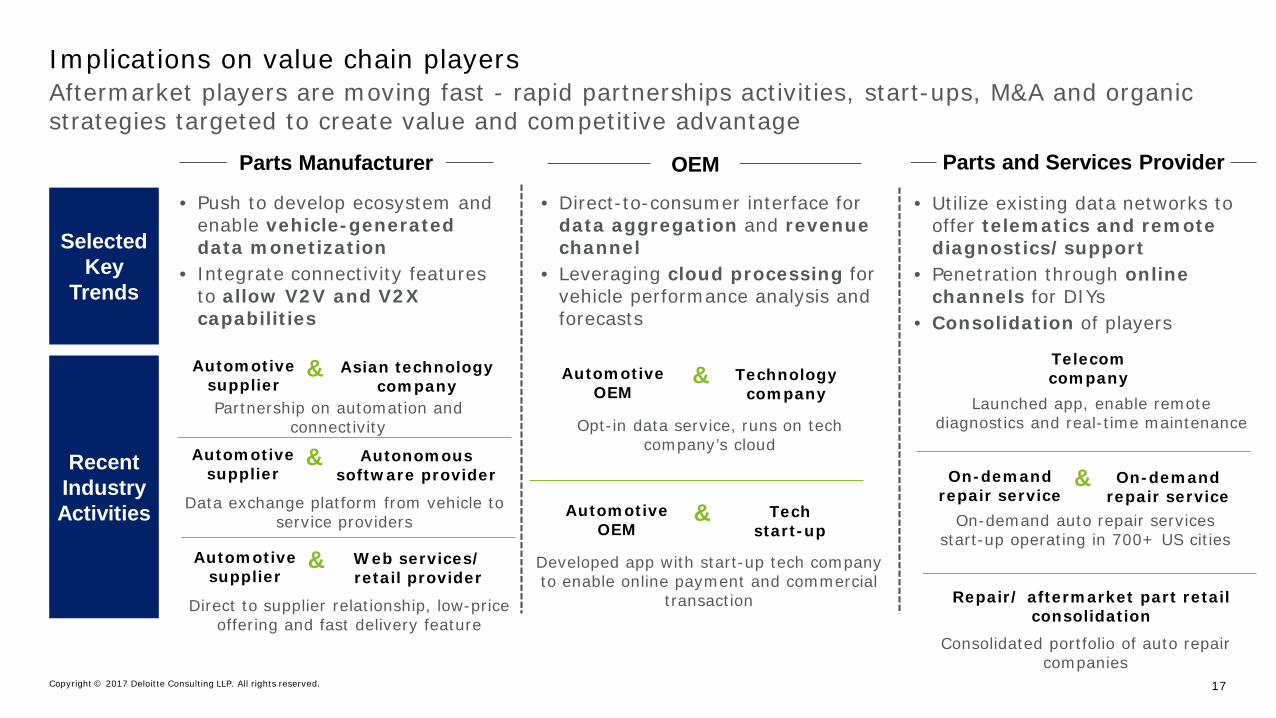

Aftermarket players are moving fast - rapid partnerships activities, start-ups, M&A and organic strategies targeted to create value and competitive advantage

Implications on value chain players

Selected Key

Trends

Recent Industry Activities

OEM

Opt-in data service, runs on tech company’s cloud

Developed app with start-up tech company to enable online payment and commercial

transaction

Data exchange platform from vehicle to service providers

Launched app, enable remote diagnostics and real-time maintenance

Direct to supplier relationship, low-price offering and fast delivery feature

• Push to develop ecosystem and enable vehicle-generated data monetization

• Integrate connectivity features to allow V2V and V2X capabilities

• Direct-to-consumer interface for data aggregation and revenue channel

• Leveraging cloud processing for vehicle performance analysis and forecasts

• Utilize existing data networks to offer telematics and remote diagnostics/support

• Penetration through online channels for DIYs

• Consolidation of players

Parts Manufacturer Parts and Services Provider

On-demand auto repair services start-up operating in 700+ US cities

Consolidated portfolio of auto repair companies

Partnership on automation and connectivity

Automotive supplier

Asian technology company

&

Automotive supplier

Autonomous software provider

&

Automotive supplier

Web services/ retail provider

&

Automotive OEM

Technology company

&

Automotive OEM

Techstart-up

&

Telecomcompany

On-demandrepair service

On-demandrepair service

&

Repair/ aftermarket part retail consolidation

Copyright © 2017 Deloitte Consulting LLP. All rights reserved. 18

Executing the right strategies helps our clients mitigate risks and capture value from new opportunities

Transforming disruption into opportunities

Cost and Asset Efficiency • Core business profitability• Cost & asset efficiency and

profitability transparency• Material cost efficiency• Digital supply chainOrganization, talent, and

operating model• IP- and service-centric business

models• Partnership and contracting

models• Talent requirements• Capability building

Portfolio optimization and technology roadmap• Portfolio strategy and analytics• Scenario planning to optimize portfolio

performance• Product and technology strategy and

roadmap

M&A/Divestiture strategies and transaction execution• Growth and/or consolidation strategies • Capability identification and acquisition• Due diligence and transaction advisory• Integration execution

Service offerings and new business models• Innovation strategy and agenda• Approach and process to new offering

development• Niche creation in new mobility ecosystem

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2017 Deloitte Development LLC. All rights reserved.36 USC 220506