Embed Size (px)

Citation preview

Rodrigo Echeverri

DEPARTMENT HEAD - REGIONAL MARKETING

PT ADARO INDONESIA

The Future of Indonesia in the Asian Coal Market

Disclaimer

2

These materials have been prepared by PT Adaro Energy (the “Company”) and have not been

independently verified. No representation or warranty, expressed or implied, is made and no reliance

should be placed on the accuracy, fairness or completeness of the information presented or contained in

these materials. The Company or any of its affiliates, advisers or representatives accepts no liability

whatsoever for any loss howsoever arising from any information presented or contained in these materials.

The information presented or contained in these materials is subject to change without notice and its

accuracy is not guaranteed.

These materials contain statements that constitute forward-looking statements. These statements include

descriptions regarding the intent, belief or current expectations of the Company or its officers with respect

to the consolidated results of operations and financial condition of the Company. These statements can be

recognized by the use of words such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or words

of similar meaning. Such forward-looking statements are not guarantees of future performance and

involve risks and uncertainties, and actual results may differ from those in the forward-looking statements

as a result of various factors and assumptions. The Company has no obligation and does not undertake to

revise forward-looking statements to reflect future events or circumstances.

These materials are for information purposes only and do not constitute or form part of an offer,

solicitation or invitation of any offer to buy or subscribe for any securities of the Company, in any

jurisdiction, nor should it or any part of it form the basis of, or be relied upon in any connection with, any

contract, commitment or investment decision whatsoever. Any decision to purchase or subscribe for any

securities of the Company should be made after seeking appropriate professional advice.

The Future of Indonesia in the Asian Coal Market

Presentation Outline

3

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

The Future of Indonesia in the Asian Coal Market

Presentation Outline

4

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

China and Indonesia Coal Trade: 2008

Growing Together

Source: McCloskey, 2014, Ministry Energy and Mineral Resources, 2014, Indonesia Coal Mining Association, 2014

CHINA EXPORTS

CHINA

INDONESIA EXPORTS

INDONESIA

CHINA IMPORTS

(In Million Tonnes)

• In 2008, China imported almost as much as it exported

• The main International supplier to the Chinese market was Vietnam

• Indonesian lower-CV coals were not technically accepted by many power plants in China

• The main market for Indonesian coal was Northeast Asia

• The Indonesian Domestic Coal market was 49 million tonnes

3

China and Indonesia Coal Trade: 2013

Growing Together

6

(In Million Tonnes)

CHINA CHINA EXPORTS

INDONESIA EXPORTS

CHINA IMPORTS

INDONESIA

• By 2013, China had become the biggest coal importer in the world

• Indonesia became the biggest coal exporter in the world – by far

• Most power plants along the cost of China adapted to use Indonesian low-CV coals

• Indonesia became the biggest source of imported coal for China and India

• The Indonesian Domestic Coal market had grown to approximately 78 million tonnes

Source: McCloskey, 2014, Ministry Energy and Mineral Resources, 2014, Indonesia Coal Mining Association, 2014

The Future of Indonesia in the Asian Coal Market

Presentation Outline

7

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

China Coastal Demand

Domestic and Imported Coal in Coastal China

8 Source: WoodMackenzie, Coal Market Service, 2013

• Since 2008, imports have steadily gained market share in China

• The success of imports in the Chinese coastal market is due to their favorable delivered cost compared to coals mined in Shanxi, Shaanxi and Inner Mongolia

• Other origins have resorted to sell ‘off-Spec coals’ to the Chinese market to be able to compete with domestic Chinese coals and Indonesian coals

• Before 2014, due to infrastructure constraints, Chinese coal supply did not grow at the same pace as demand

China Production

Switching Basins in China

9

Source: China Coal Resource, 2014; WoodMackenzie, Coal Market Service, 2013

• Before year 2000, coastal Chinese power plants were designed mainly for coals from old mines in Shanxi and Shaanxi province (typically 5000-5500 kcal/kg NAR

• However, low mining costs and significant resources have motivated the development of mega-mines in Inner Mongolia.

• To support this development, the Chinese government decided to develop new railway links to connect the coal producing regions to coastal ports

• The CV of coals from Inner Mongolia is typically 4000-4800 NAR – similar to the CV of Indonesian coal

The Transition to Lower CV

Driven by the Chinese Domestic Market

10 Source: WoodMackenzie, Coal Market Service, 2013

• Due to the change in the mix of basins supplying the Chinese domestic coal market the CV of domestic coal is dropping

• Power plants built in the last 10 years have taken this into account for the design CV of the boilers

• This trend has made Chinese demand converge in CV preference with Indonesian coals

• However, most of the environmental attributes of Indonesian coals are better than domestic Chinese coals (NOx, SOx, trace elements, ash)

China Coastal Demand

Comparison of Coal Logistics in China and Indonesia

11

Shanxi

Qinhuangdao

Guangzhou

South Kalimantan

Domestic Coal arrives in 8-9 Days

Imported Coal arrives in 7-8 Days

• For southern China, the domestic coal logistics chain is not very different from Indonesia

• Coal from the main coal producing regions in China is transported by either rail or truck to the ports in the Bohai area

• Then, the coal is moved in small coastal vessels to the main demand centers in Guangdong, Fujian, Jiangsu, Shanghai, Zhejiang and Shandong

• From Indonesia, most of the coal is barged within one day to an ocean anchorage and then transported by sea-going vessel to South China

The Growing Role of Imports

Comparison of Logistics of Indonesia vs Others

12

Shanxi

Qinhuangdao

Guangzhou

South Kalimantan

8 D

ays

Australia South Africa

• Australian and South African coals need to be transported much farther than Indonesian coal in order to reach the demand centers in the south of China

• This logistics disadvantage will remain crucial in the future, making coal imports from those origins only “arbitrage coals”

• Indonesia, on the other hand, has secured a place as a base supplier in spite of price movements

China Coastal Demand

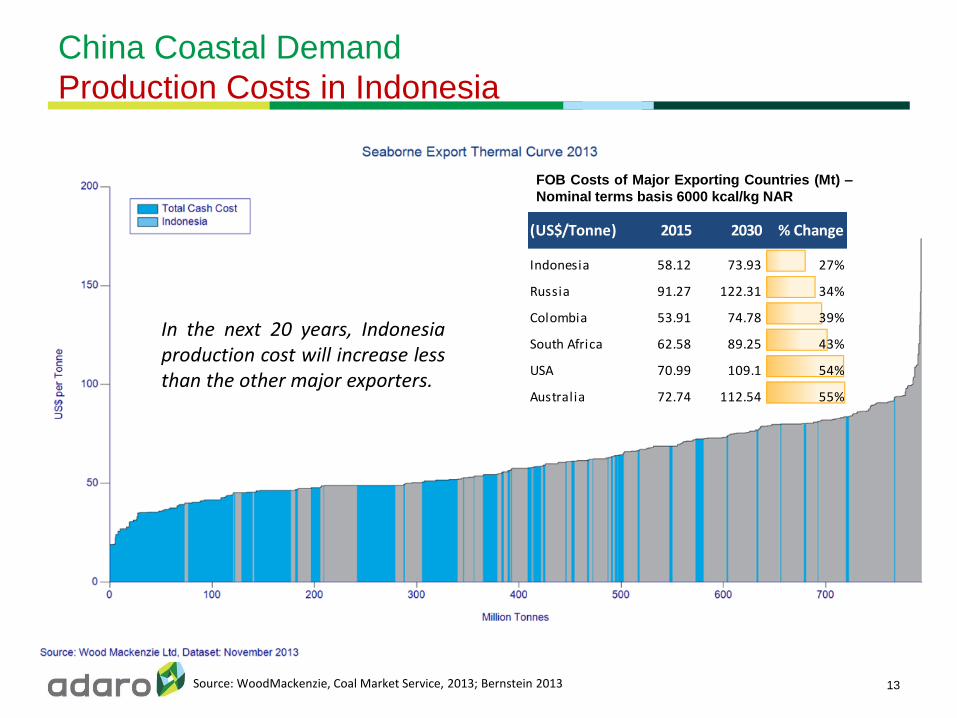

Production Costs in Indonesia

13

Seaborne Export Thermal Curve 2012

Source: WoodMackenzie, Coal Market Service, 2013; Bernstein 2013

FOB Costs of Major Exporting Countries (Mt) –

Nominal terms basis 6000 kcal/kg NAR

(US$/Tonne) 2015 2030 % Change

Indonesia 58.12 73.93 27%

Russia 91.27 122.31 34%

Colombia 53.91 74.78 39%

South Africa 62.58 89.25 43%

USA 70.99 109.1 54%

Australia 72.74 112.54 55%

In the next 20 years, Indonesia production cost will increase less than the other major exporters.

The Future of Indonesia in the Asian Coal Market

Presentation Outline

14

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

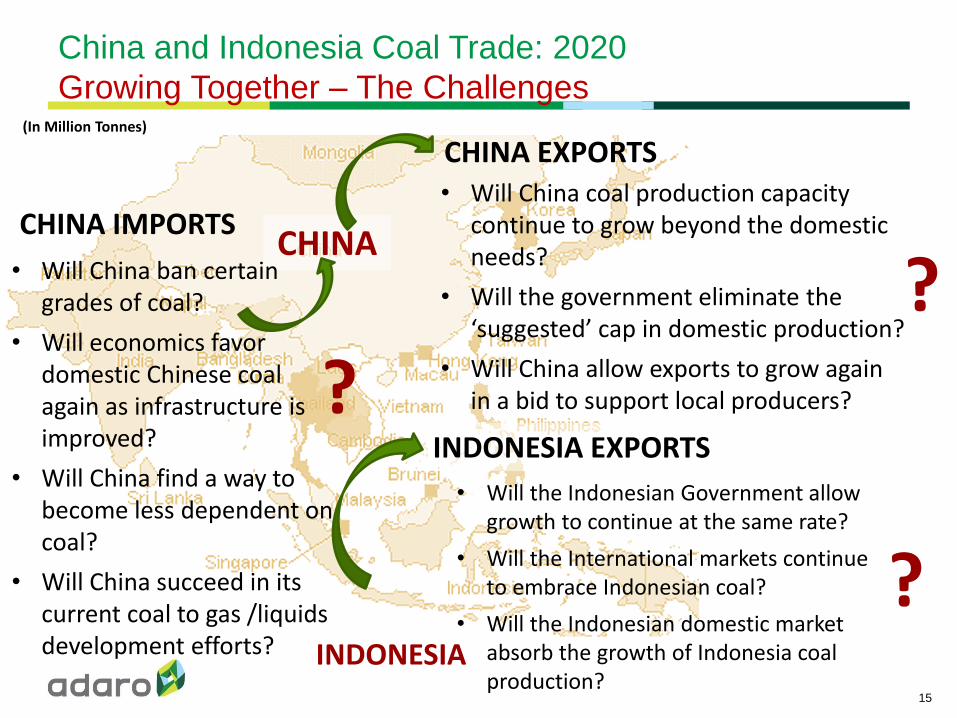

China and Indonesia Coal Trade: 2020

Growing Together – The Challenges

15

CHINA EXPORTS

INDONESIA EXPORTS

INDONESIA

?

• Will China coal production capacity continue to grow beyond the domestic needs?

• Will the government eliminate the ‘suggested’ cap in domestic production?

• Will China allow exports to grow again in a bid to support local producers?

(In Million Tonnes)

• Will the Indonesian Government allow growth to continue at the same rate?

• Will the International markets continue to embrace Indonesian coal?

• Will the Indonesian domestic market absorb the growth of Indonesia coal production?

?

?

CHINA CHINA IMPORTS

• Will China ban certain grades of coal?

• Will economics favor domestic Chinese coal again as infrastructure is improved?

• Will China find a way to become less dependent on coal?

• Will China succeed in its current coal to gas /liquids development efforts?

16

China Coal Market Projections

Fuel Mix - WoodMackenzie and IEA

Source: WoodMackenzie, Coal Market Service, 2013

• In spite of using different sets of assumptions, both IEA and WoodMackenzie project similar growth electricity capacity in China

• Both models coincide in predicting limited development in Nuclear Energy in China

• Also, gas is a consensus point, highlighting the challenge in accessing domestic shale deposits and the limited potential

• A big unknown is to what extend China will be successful in its conversion of coal to liquids and gas

China Coal Market Projections

Coal Demand Models for China

17

Source: WoodMackenzie, Coal Market Service, 2013

• WoodMackenzie projects that coal demand in China will grow by over one billion tonnes by 2020

• The IEA ‘New Policies’ model provides a forecast which assumes many political and technical challenges can be overcome

• However, even in IEA New Policies scenario, coal demand in China continues to grow steadily into 2020.

• Hence, the range of forecasts for the additional supply needed is very wide: 300 to 1000 million tonnes of new production required by 2020

• Forecasting where the coal is going to come from is an even bigger challenge

• However, in all cases Coal will remain the main alternative and growth will continue at a strong rate

18 Source: WoodMackenzie, Coal Market Service, 2013

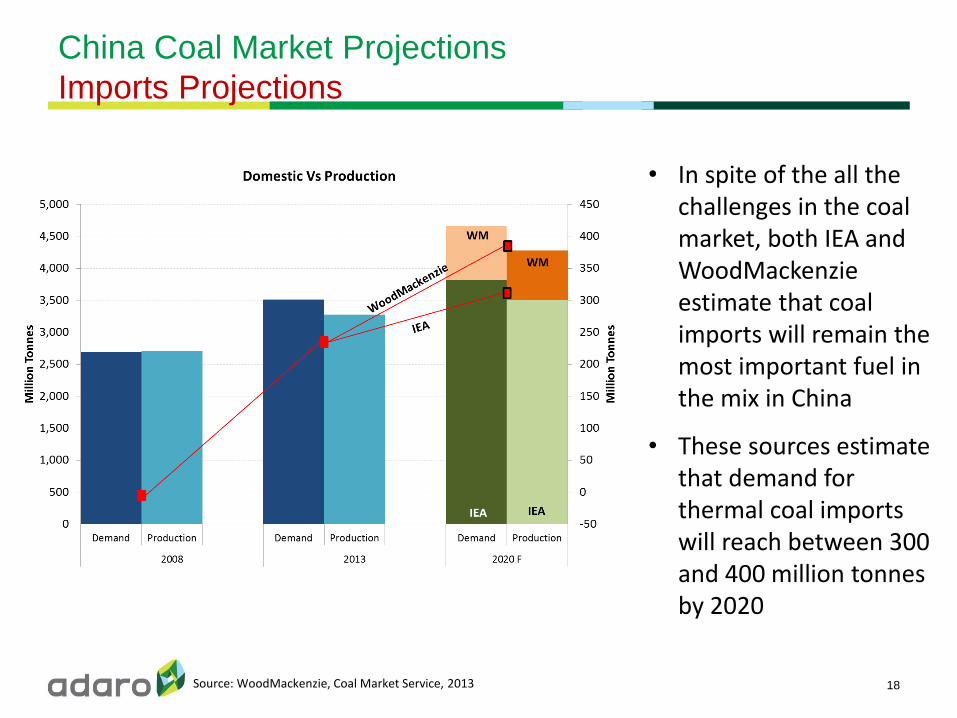

China Coal Market Projections

Imports Projections

• In spite of the all the challenges in the coal market, both IEA and WoodMackenzie estimate that coal imports will remain the most important fuel in the mix in China

• These sources estimate that demand for thermal coal imports will reach between 300 and 400 million tonnes by 2020

The Future of Indonesia in the Asian Coal Market

Presentation Outline

19

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

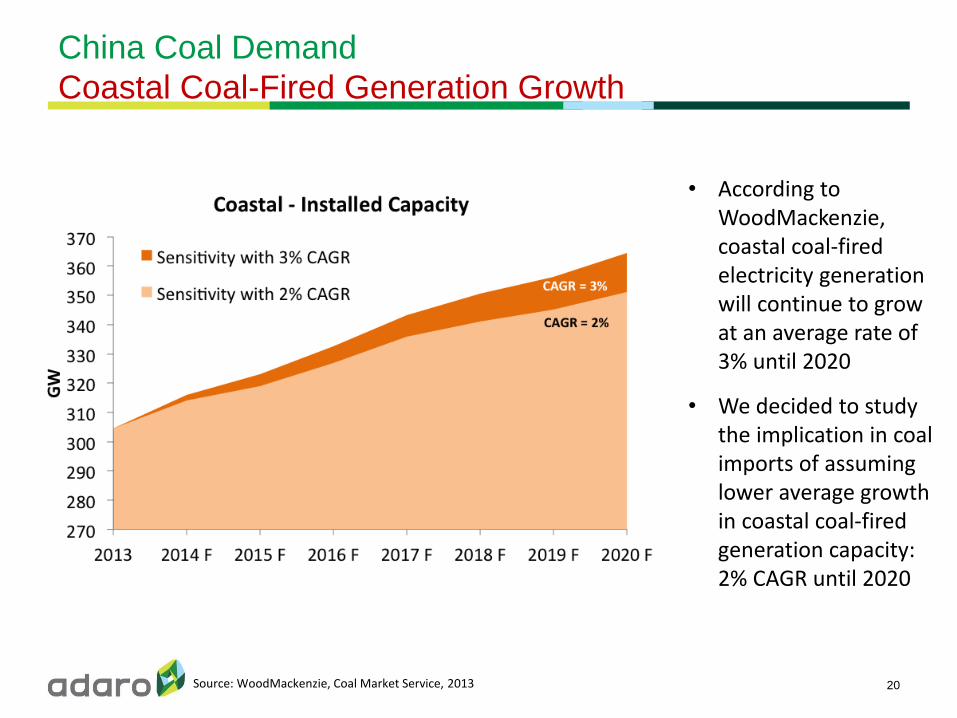

China Coal Demand

Coastal Coal-Fired Generation Growth

20 Source: WoodMackenzie, Coal Market Service, 2013

• According to WoodMackenzie, coastal coal-fired electricity generation will continue to grow at an average rate of 3% until 2020

• We decided to study the implication in coal imports of assuming lower average growth in coastal coal-fired generation capacity: 2% CAGR until 2020

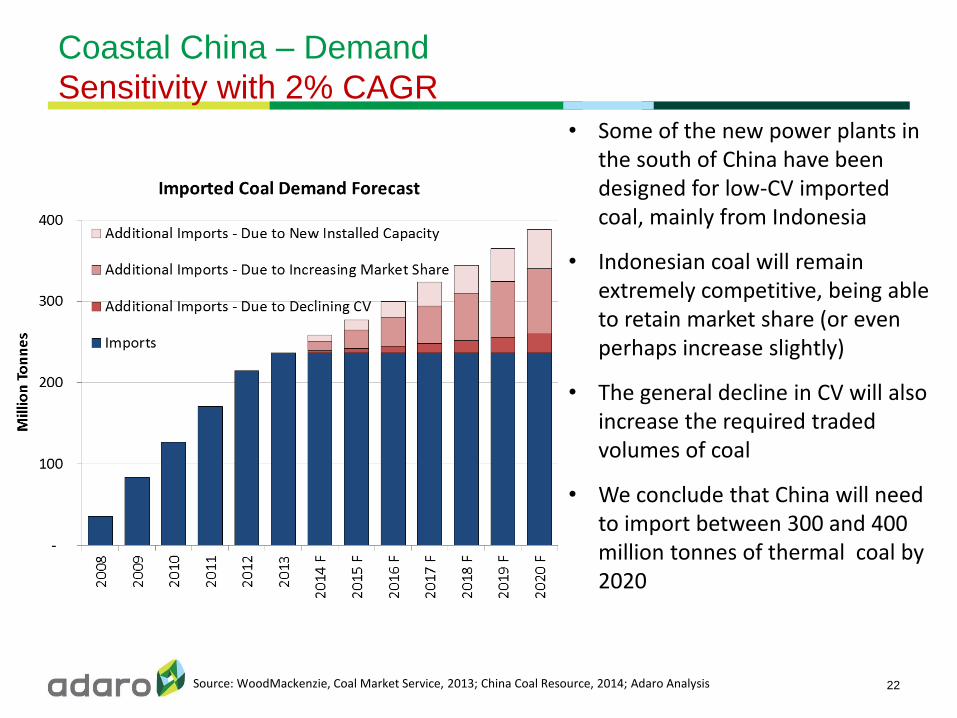

Coastal China – Demand

Sensitivity with 2% CAGR

21 Source: WoodMackenzie, Coal Market Service, 2013; China Coal Resource, 2014; Adaro Analysis

• Using 2% average growth on coal-fired capacity, we can see that –all other factors being equal-, coastal coal demand will grow over 100 million tonnes

• However, it is important to also consider that the average CV is declining significantly – this will also increase volume

Coastal China – Demand

Sensitivity with 2% CAGR

22 Source: WoodMackenzie, Coal Market Service, 2013; China Coal Resource, 2014; Adaro Analysis

• Some of the new power plants in the south of China have been designed for low-CV imported coal, mainly from Indonesia

• Indonesian coal will remain extremely competitive, being able to retain market share (or even perhaps increase slightly)

• The general decline in CV will also increase the required traded volumes of coal

• We conclude that China will need to import between 300 and 400 million tonnes of thermal coal by 2020

The Future of Indonesia in the Asian Coal Market

Presentation Outline

23

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

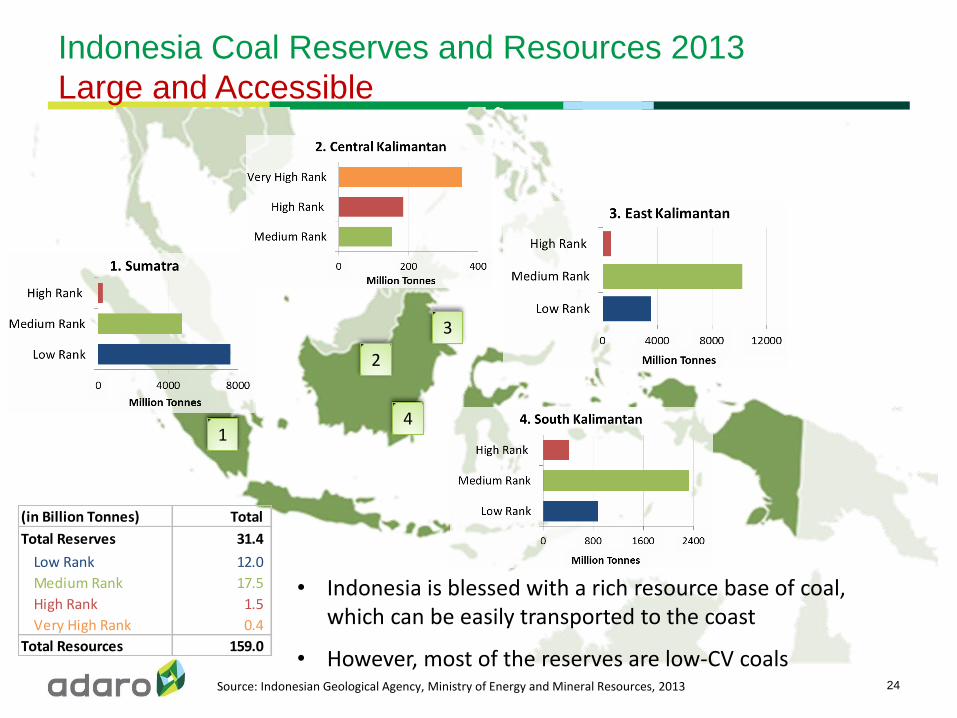

Indonesia Coal Reserves and Resources 2013

Large and Accessible

24

1

2

3

4

Source: Indonesian Geological Agency, Ministry of Energy and Mineral Resources, 2013

(in Billion Tonnes) Total

Total Reserves 31.4

Low Rank 12.0

Medium Rank 17.5

High Rank 1.5

Very High Rank 0.4

Total Resources 159.0

• Indonesia is blessed with a rich resource base of coal, which can be easily transported to the coast

• However, most of the reserves are low-CV coals

Indonesia Production

Potential Plateau in two years?

25 Source: WoodMackenzie, Coal Supply Service, 2013

• However, the mines currently operating might plateau in 2-3 years, requiring the development of new projects

• Market support will be required for the ‘Probable’ and ‘Possible’ projects to come online

• Current market conditions do not support further project development

The Future of Indonesia in the Asian Coal Market

Presentation Outline

26

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

27

Source: WoodMackenzie, Coal Market Service 2013

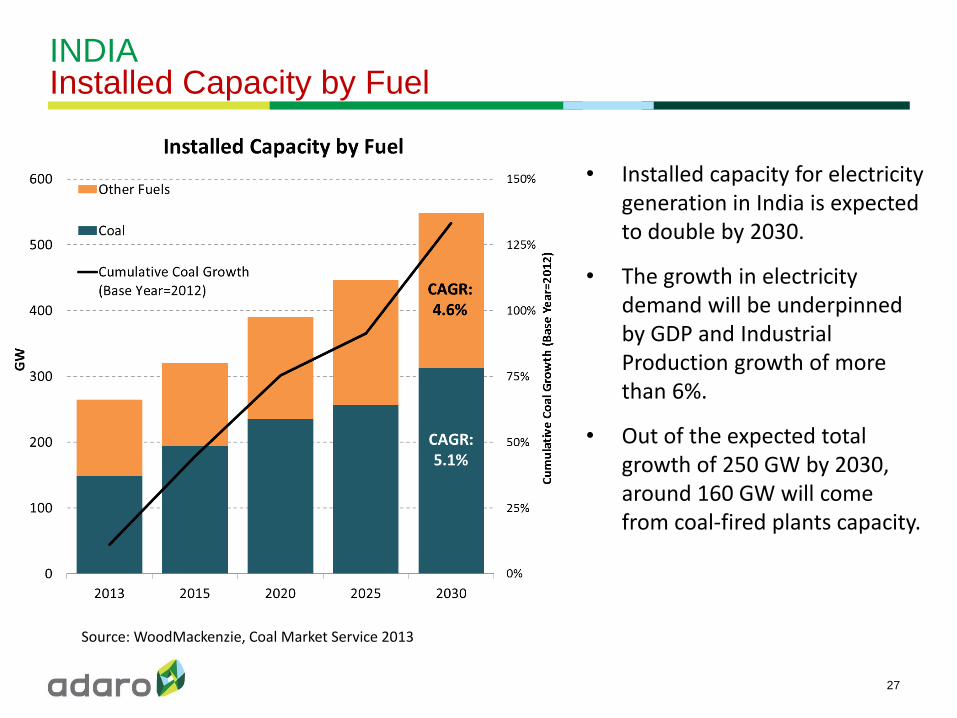

• Installed capacity for electricity generation in India is expected to double by 2030.

• The growth in electricity demand will be underpinned by GDP and Industrial Production growth of more than 6%.

• Out of the expected total growth of 250 GW by 2030, around 160 GW will come from coal-fired plants capacity.

INDIA Installed Capacity by Fuel

28

Source: WoodMackenzie, Coal Market Service 2013

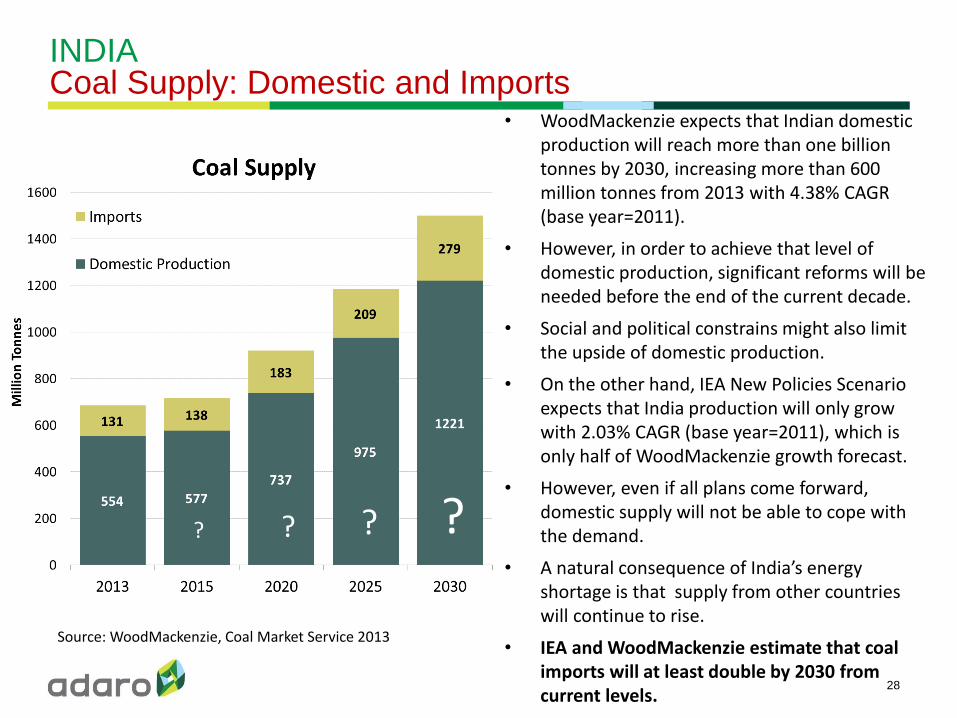

• WoodMackenzie expects that Indian domestic production will reach more than one billion tonnes by 2030, increasing more than 600 million tonnes from 2013 with 4.38% CAGR (base year=2011).

• However, in order to achieve that level of domestic production, significant reforms will be needed before the end of the current decade.

• Social and political constrains might also limit the upside of domestic production.

• On the other hand, IEA New Policies Scenario expects that India production will only grow with 2.03% CAGR (base year=2011), which is only half of WoodMackenzie growth forecast.

• However, even if all plans come forward, domestic supply will not be able to cope with the demand.

• A natural consequence of India’s energy shortage is that supply from other countries will continue to rise.

• IEA and WoodMackenzie estimate that coal imports will at least double by 2030 from current levels.

INDIA Coal Supply: Domestic and Imports

? ? ? ?

29

Source: WoodMackenzie, Coal Market Service 2013

• Low CV coals will remain the preferred choice in India for the next 20 years. The majority of low-rank coal imports will be fulfilled by Indonesia.

• India will need to compete with other major importers, such as China and Southeast Asian countries, to be able to procure Indonesian low-CV coals.

• In the next decade, Indonesian low-rank coals will not be sufficient to fulfill the increasing demand in India.

• Imports of Higher-CV, higher-cost coals will be needed in India. This will be a supporting factor for coal prices in the long-term.

INDIA Coal Imports by Grade

30 Source: WoodMackenzie Energy Market Service, 2013; Adaro Analysis

Vietnam

Thailand

Indonesia

Myanmar

Philippines

Cambodia

Imports

Domestic

Malaysia

SOUTHEAST ASIA COAL REQUIREMENTS FOR ELECTRICITY Coal Demand by Country

• Southeast Asia is expected to remain one of the fastest-growing regions in the world well into the next decade

• Access to gas and other resources is and will continue to be limited

• The only country capable of producing enough coal to support the demands of the region is Indonesia

31 Source: WoodMackenzie Energy Market Service, 2013; Adaro Analysis

Imports

Domestic (Indonesia)

Domestic (Ex-Indonesia)

Total 212 MT

Total 361 MT

• Southeast Asian countries (other than Indonesia) will need to import more than 130 million tonnes of coal by 2020

• Indonesian domestic demand will continue to grow at a steady rate, reaching over 130 million tonnes by 2020

• Domestic production in other ASEAN countries is not expected to grow significantly

SOUTHEAST ASIA COAL REQUIREMENTS FOR ELECTRICITY Coal Demand by Country

The Future of Indonesia in the Asian Coal Market

Presentation Outline

32

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

33 Source: WoodMackenzie Energy Market Service, 2013; Adaro Analysis

SUMMARY Too much demand for Indonesian coal?

China Demand

India Demand

Southeast Asia Demand (excl. Indonesia)

Indonesia Domestic Demand

Operating Mines

Highly Probable Projects

Probable Projects

Possible Projects

Indonesia Production by Status

China, India, Indonesia, and SEA Demand

Indonesian Coal Availability is Limited

TOTAL 961 MT

TOTAL 817 MT

TOTAL 580 MT TOTAL

~450MT

The Future of Indonesia in the Asian Coal Market

Presentation Outline

34

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

35

South Kalimantan

80 Km haul road

230 Km barging

Domestic supply

• The second largest coal producer in Indonesia

• Integrated, reliable coal supplier

Our Model – Introduction to Adaro Pit-to-Port Integration

Adaro Indonesia (AI)

Coal mining, S Kalimantan

Balangan

Coal mining, S Kalimantan

Mustika Indah Permai (MIP)

Coal mining, S Sumatra

Bukit Enim Energi (BEE)

Coal mining, S Sumatra

IndoMet Coal

Project (IMC), BHP JV

Coal mining, C Kalimantan

Bhakti Energi

Persada (BEP)

Coal mining, E Kalimantan

100%

75%

75%

61%

25%

10.2%

Saptaindra

Sejati (SIS)

Coal mining and

hauling contractor

Jasapower

Indonesia (JPI)

Overburden crusher

and conveyor

operator

100%

100%

100%

100%

51.2%

100%

Makmur Sejahtera

Wisesa (MSW)

2x30MW mine-

mouth power plant

operation in

S Kalimantan

Bhimasena Power

2x1000MW power

plant operator in

Central Java

South Kalimantan

Power Project

2x100MW power

plant operator in

S Kalimantan

100%

34%

65%

Maritim Barito

Perkasa (MBP)

Coal barging and

shiploading operator Harapan Bahtera

Internusa (HBI)

Third-party barging

and shiploading Sarana Daya

Mandiri (SDM)

Channel dredging

contractor Indonesia Bulk

Terminal (IBT)

Coal and fuel terminal

Our Model – Introduction to Adaro Pit-to-Power Integration

PT Adaro Energy

Adaro Mining Assets (ATA)

Adaro Mining Services

Adaro Logistics

Adaro Power

*Simplified Corporate Structure

36

ENVIROCOAL SPECIFICATIONS

Unit E5000 E4000

Typical Typical

Calorific Value NAR 4,600 kcal/kg 3,700 kcal/kg

Total Moisture ARB 28% - 30.0% 38.0% - 40.0%

Ash ADB 2% - 3% 3% - 4%

Sulphur ADB 0.15% - 0.25% 0.15% - 0.25%

Volatile Matter ADB 40.0% 40.0%

HGI - 45 65

Ash Fusion Temperature (reducing atmosphere)

Initial deformation

deg. C 1,150 1,150

37

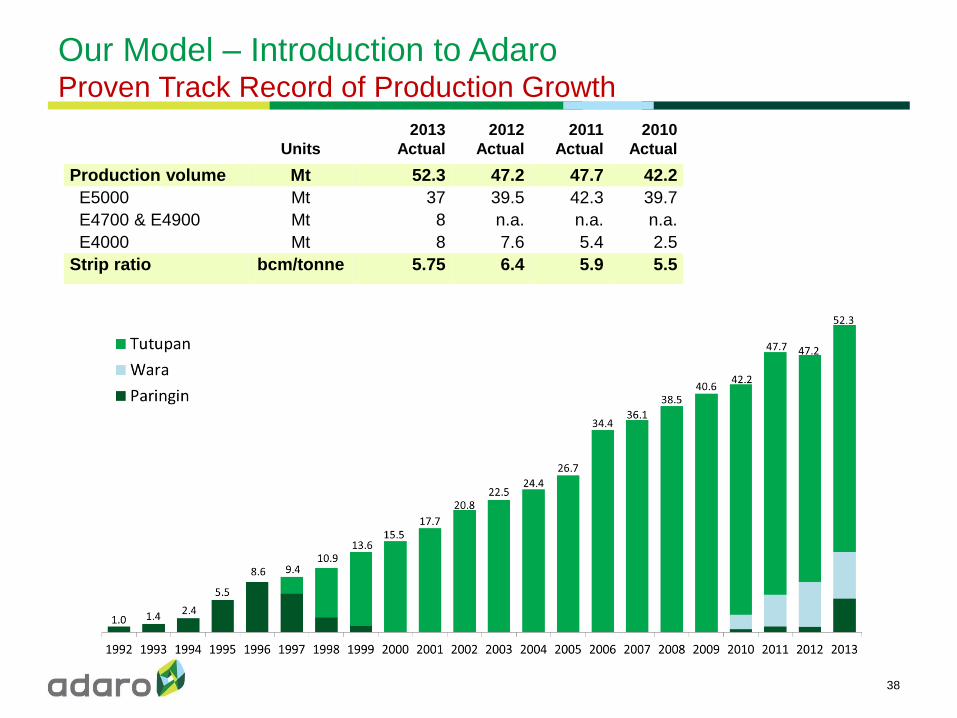

Our Model – Introduction to Adaro Focus on Two Product Ranges

Units

2013

Actual

2012

Actual

2011

Actual

2010

Actual

Production volume Mt 52.3 47.2 47.7 42.2

E5000 Mt 37 39.5 42.3 39.7

E4700 & E4900 Mt 8 n.a. n.a. n.a.

E4000 Mt 8 7.6 5.4 2.5

Strip ratio bcm/tonne 5.75 6.4 5.9 5.5

38

Our Model – Introduction to Adaro Proven Track Record of Production Growth

The Future of Indonesia in the Asian Coal Market

Presentation Outline

39

• CHINA IMPORTS GROWTH HISTORY AND PROJECTIONS

• CHINA AND INDONESIA – GROWING TOGETHER • THE GROWING ROLE OF IMPORTS • COAL DEMAND FORECASTS FOR CHINA • CHINA – A GROWTH SENSITIVITY

• PROJECTION FOR INDONESIAN COAL SUPPLY

• PROJECTIONS FOR SUPPLY AND DEMAND IN EMERGING ASIAN COUNTRIES

• INDIA AND SOUTHEAST ASIA • THE WHOLE GROWTH PICTURE

• INTRODUCTION TO ADARO

• CONCLUSIONS

• A lot of uncertainty in China power growth and energy mix – extremely difficult to predict as not only economics, but also regulations play a role

• Indonesian coal production will peak in two years if the market does not support the development of new projects

• Additionally, there is the potential that the Indonesian government might limit production

• Southeast Asia and India will will continue to need Indonesian coal – these regions are likely to become the main destination for Indonesian exports in the near future

40

The Future of Indonesia in the Asian Coal Market

Presentation Conclusions

ADARO WILL CONTINUE TO DELIVER

POSITIVE ENERGY TO THE ASIAN MARKET

41

The Future of Indonesia in the Asian Coal Market

Presentation Conclusions