Embed Size (px)

DESCRIPTION

An Underwriting Newsletter by First American Title

Citation preview

An Underwriting Newsletter by First American Title

GET TO KNOW

KEN JANNENVP, CORPORATE SENIOR UNDERWRITING COUNSEL

THE PROPERTY PROFESSOR

SHORT SALES

CLOSING CORNER

ACRONYMS

WHAT YOU NEED TO KNOW

POWERS OF ATTORNEY

UNDERWRITING

RAPID RESPONSE TEAM

Volume II December 2015/January 2016

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

The information contained in this document was prepared by First American Title Insurance Company (“FATICO”) for informational purposes only and does not constitute legal advice. FATICO is not a law firm and this information is not intended to be legal advice. Readers should not act upon this without seeking advice from professional advisers. First American Title Insurance Company makes no express or implied warranty respecting the information presented and assumes no responsibility for errors or omissions. First American, the eagle logo, First American Title, and firstam.com are registered trademarks or trademarks of First American Financial Corporation and/or its affiliates.

First American Title | The Florida Legal Eagle2233 Lee Road, Suite 202, Winter Park, FL 32789407.691.5295

EXECUTIVE EDITORS: Len PrescottAlan McCallTrish LadanChip Koval

EDITORS: JoJo GroveAdrianna La Kam

I t is with great pleasure that we bring to you the second edition of The Florida Legal Eagle. We hope you enjoy this publication, but more

importantly, we hope it provides value and that it makes it into your collection of reference materials.

Among the broad range of topics in this edition, you will find a spotlight on someone already very familiar to many in Florida: Kenneth Jannen, Corporate Senior Underwriting Counsel and member of our home office staff. Ken is a 30-plus year veteran of the title insurance industry in Florida, a past president of the Florida Land Title Association and the 1992 recipient of its prestigious Raymond O. Denham Memorial Award for leadership and outstanding service to the industry. Ken has already created a legendary and lasting legacy and we are very grateful that he continues to be a terrific underwriter, leader, and mentor for our team. We are pleased to highlight our appreciation of him in this edition as he reminds us all to “pay it forward.”

As we finish up what has proven to be an often challenging but very successful year, our underwriting team is focused on continuing and improving our pursuit of excellence and innovations that will make the most impact on our customers and our company. Our Underwriting Performance Goals for 2016 have three areas of primary focus: 1) underwriting response time; 2) relationship with our customers; and 3) brand identity. The Rapid Response Team and this newsletter are two new initiatives to help accomplish these goals. Our commitment to you is that our team will never stop learning and finding ways to make a positive impact. In the process, we will take inspiration from Ken Jannen’s: “Make some friends!”

On behalf of all of us at First American Title, thank you for being an extension of our family. We wish you a very successful end of year and look forward to seeing where we can go together in 2016!

All the Best,

FROM THE EDITOR’S DESK

PAGE TITLE

3 Executive Spotlight: Ken Jannen

4 The Property Professor: Short Sales

5 Underwriting Q&A: Powers of Attorney

6 Case Law Updates

7 Closing Corner: Acronyms

9 Revisiting the Common Law Unities of Title in Survivorship Estates

11 Underwriting Spotlight: Charles (Chip) Koval

12 Rapid Response Team / Legal and Industry Updates

13 Florida Statewide Underwriters

IN THIS ISSUE:

We Want Your Insight!Your insight is valued by the Florida underwriting team. If you would like to contribute to the Florida Underwriting Newsletter, or if you have any comments or suggestions for topics you would like to see in our newsletter, please submit your ideas to one of our Underwriting Associates, Adrianna La Kam at [email protected] or JoJo Grove at [email protected]. We look forward to hearing from you!

Len PrescottVP, Florida State Counsel

Q WHAT WAS YOUR FIRST JOB IN THE TITLE INSURANCE INDUSTRY?

A I was in my second year at New York Law School and had just switched from daytime attendance to night law school. I was looking for a full-time job and there was an index card on the school bulletin board to call New York Abstract for a position. The company, an agency, had just been bought by First American Title. I started with scheduling closings and reviewing documents that came in from the closers prior to recording. I gained experience searching, examining, closing, and spent some time as a sales representative. I also met my wife Kathy there!

Q WHAT ATTRIBUTES DO YOU THINK AN EFFECTIVE UNDERWRITER SHOULD POSSESS?

A You don’t have to be a lawyer to be an effective underwriter, but you have to have a real interest in the law and how it works. I’ve heard it said that claims handlers should not transition into underwriting because they will be too conservative; but a practical knowledge of claims, how they arise, what the issues are and how the legal system works is valuable. You also have to like law and digging for the facts. If you don’t have the facts, you don’t know what the risks and opportunities are. As to the law, every day it seems that I find some legal nugget that is useful and interesting. I love WESTLAW®, an interactive computer-assisted legal research site, and I love getting into the court files in PACER (Public Access to Court Electronic Records) when I’m working on a bankruptcy or federal receivership. Finally, you have to enjoy helping people solve problems. It’s not enough to spot an issue; you have to come up with a solution, whether it’s a way to clear up the problem or to approach it from the question of what kind of coverage is appropriate.

Q DID YOU EXPERIENCE ANY MAJOR SETBACKS DURING YOUR PATH TO YOUR CURRENT POSITION?

A No. As a matter of fact, First American Title opened up some wonderful opportunities for me and I was fortunate to have great mentors.

Q WHAT ADVICE WOULD YOU GIVE TO OUR FLORIDA UNDERWRITERS?

A The better you become at your job, the better the Company will become. We have great underwriters in Florida, beginning with Alan McCall and Len Prescott. Learn from them and reach out into areas of the industry with which you are unfamiliar, even if you are uncomfortable at first. Find good mentors, and when your turn comes, mentor others. I find that I learn a lot from the younger underwriters and they inspire and energize me to learn more. Make some friends!

KEN JANNENVP, CORPORATE SENIOR UNDERWRITING COUNSEL, HOME OFFICE STAFF

Executive Spotlight Executive Spotlight

FROM OUR HOME TO YOURS

Happy Holidays!Thank you to our employees and agents for your continued support and loyalty.

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 3

Dear Property Professor,

We closed a sale for one of our best customers, Big Bank, who was providing financing for the purchase of a beachfront house from an underwater seller. The property already had two mortgages to pay off—a first mortgage to McMansion Mortgage Company and a second mortgage to Overreach Community Bank. The outstanding balances exceeded the sales price and not by just a little, either.

But, here’s the thing. This order was placed by a company called Maddog Consulting (Maddog), who negotiated the short sale for a cute older couple named Pappy and Happy Trails. They were buying the house

for their son and daughter-in-law. Maddog gave us written payoffs from both McMansion and Overreach. After we wired the discounted payoffs to both of them, we disbursed big service fees to Maddog. The consultant who worked with them was so helpful, friendly and easy to work with; we never had to speak with anyone at either McMansion or Overreach. I wish every transaction was like this.

This morning, we received a call from Chris at McMansion Mortgage asking us why we had wired funds to them “by mistake” (his words). When I mentioned Maddog Consulting, Chris said he had never heard of them. After checking with his boss, Chris called back to say his company had not authorized the short

sale and was not aware of any closing.After providing Chris with the name and phone number of the person we had been speaking with at Maddog, I am hopeful he can straighten this out for us. I am sure it is a misunderstanding. It has been two weeks, however, and still no word. We are also having trouble getting in touch with the buyers.

We were wondering if this might be some sort of scam. Should we issue the policy or raise an exception to the two mortgages?

Thanks,

– Befuddled in Brevard

Dear Befuddled,

It is possible that Maddog might have been up to something. I hope Maddog had the authority to negotiate and provide the short sale payoff from both lenders. If not, neither McMansion nor Overreach may have any legal obligation to satisfy or release their mortgages. The correct thing to do at this point is to file a claim with the title insurance underwriter and let the claims department get to the bottom of it before doing anything else.

Preserve all the emails, correspondence, file notes, documents and other materials in the file. You should be prepared to provide this information to the title insurance underwriter. Please be

particularly careful to send them the written authority, if any, from McMansion and Overreach instructing you to accept the payoffs. I would also preserve the record of your direct telephone calls to the lenders in order to verify the payoffs and think about putting your errors and omissions insurer on notice to preserve any coverage you might have.

This case is a strong reminder to be wary of the authority of those claiming to be agents for others, whatever the issue, especially when it comes to short sales. Even when dealing directly with a mortgage company or bank, it is wise to be skeptical of the authority of an employee who agrees to a reduced payoff. It is critical to get everything

in writing, especially from a lender making a concession or providing a discount in the payoff. The authority of an agent, such as Maddog, should be obtained in writing and scrutinized carefully. In addition, it is a good idea to have a procedure to follow up with the principal, such as a lender, seller or other party by email and telephone.

Please be prepared to cooperate fully with the claims department as they investigate this matter.

Thanks, Befuddled. It is always good to hear from you.

– Property Professor

The Property Professor:

SHORT SALESBy: Alan McCallVP, Southeast Region Underwriting Counsel, Daytona Beach, FL

Page 4First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016

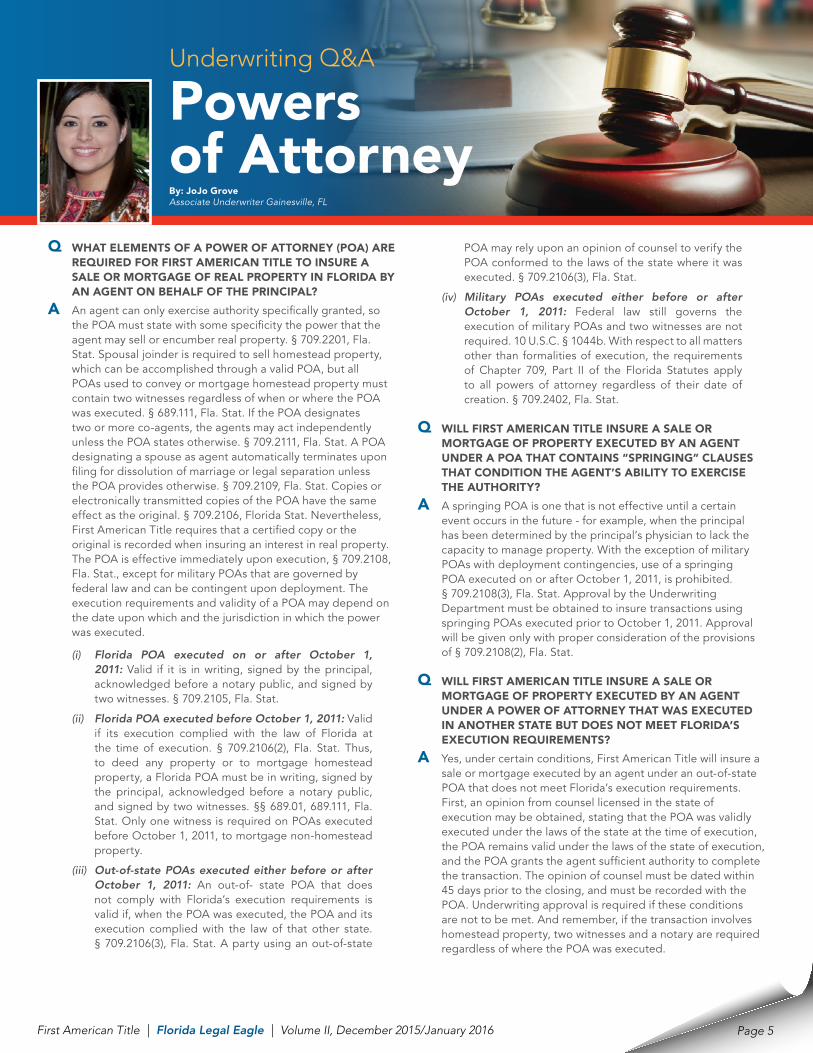

Q WHAT ELEMENTS OF A POWER OF ATTORNEY (POA) ARE REQUIRED FOR FIRST AMERICAN TITLE TO INSURE A SALE OR MORTGAGE OF REAL PROPERTY IN FLORIDA BY AN AGENT ON BEHALF OF THE PRINCIPAL?

A An agent can only exercise authority specifically granted, so the POA must state with some specificity the power that the agent may sell or encumber real property. § 709.2201, Fla. Stat. Spousal joinder is required to sell homestead property, which can be accomplished through a valid POA, but all POAs used to convey or mortgage homestead property must contain two witnesses regardless of when or where the POA was executed. § 689.111, Fla. Stat. If the POA designates two or more co-agents, the agents may act independently unless the POA states otherwise. § 709.2111, Fla. Stat. A POA designating a spouse as agent automatically terminates upon filing for dissolution of marriage or legal separation unless the POA provides otherwise. § 709.2109, Fla. Stat. Copies or electronically transmitted copies of the POA have the same effect as the original. § 709.2106, Florida Stat. Nevertheless, First American Title requires that a certified copy or the original is recorded when insuring an interest in real property. The POA is effective immediately upon execution, § 709.2108, Fla. Stat., except for military POAs that are governed by federal law and can be contingent upon deployment. The execution requirements and validity of a POA may depend on the date upon which and the jurisdiction in which the power was executed.

(i) Florida POA executed on or after October 1, 2011: Valid if it is in writing, signed by the principal, acknowledged before a notary public, and signed by two witnesses. § 709.2105, Fla. Stat.

(ii) Florida POA executed before October 1, 2011: Valid if its execution complied with the law of Florida at the time of execution. § 709.2106(2), Fla. Stat. Thus, to deed any property or to mortgage homestead property, a Florida POA must be in writing, signed by the principal, acknowledged before a notary public, and signed by two witnesses. §§ 689.01, 689.111, Fla. Stat. Only one witness is required on POAs executed before October 1, 2011, to mortgage non-homestead property.

(iii) Out-of-state POAs executed either before or after October 1, 2011: An out-of- state POA that does not comply with Florida’s execution requirements is valid if, when the POA was executed, the POA and its execution complied with the law of that other state. § 709.2106(3), Fla. Stat. A party using an out-of-state

POA may rely upon an opinion of counsel to verify the POA conformed to the laws of the state where it was executed. § 709.2106(3), Fla. Stat.

(iv) Military POAs executed either before or after October 1, 2011: Federal law still governs the execution of military POAs and two witnesses are not required. 10 U.S.C. § 1044b. With respect to all matters other than formalities of execution, the requirements of Chapter 709, Part II of the Florida Statutes apply to all powers of attorney regardless of their date of creation. § 709.2402, Fla. Stat.

Q WILL FIRST AMERICAN TITLE INSURE A SALE OR MORTGAGE OF PROPERTY EXECUTED BY AN AGENT UNDER A POA THAT CONTAINS “SPRINGING” CLAUSES THAT CONDITION THE AGENT’S ABILITY TO EXERCISE THE AUTHORITY?

A A springing POA is one that is not effective until a certain event occurs in the future - for example, when the principal has been determined by the principal’s physician to lack the capacity to manage property. With the exception of military POAs with deployment contingencies, use of a springing POA executed on or after October 1, 2011, is prohibited. § 709.2108(3), Fla. Stat. Approval by the Underwriting Department must be obtained to insure transactions using springing POAs executed prior to October 1, 2011. Approval will be given only with proper consideration of the provisions of § 709.2108(2), Fla. Stat.

Q WILL FIRST AMERICAN TITLE INSURE A SALE OR MORTGAGE OF PROPERTY EXECUTED BY AN AGENT UNDER A POWER OF ATTORNEY THAT WAS EXECUTED IN ANOTHER STATE BUT DOES NOT MEET FLORIDA’S EXECUTION REQUIREMENTS?

A Yes, under certain conditions, First American Title will insure a sale or mortgage executed by an agent under an out-of-state POA that does not meet Florida’s execution requirements. First, an opinion from counsel licensed in the state of execution may be obtained, stating that the POA was validly executed under the laws of the state at the time of execution, the POA remains valid under the laws of the state of execution, and the POA grants the agent sufficient authority to complete the transaction. The opinion of counsel must be dated within 45 days prior to the closing, and must be recorded with the POA. Underwriting approval is required if these conditions are not to be met. And remember, if the transaction involves homestead property, two witnesses and a notary are required regardless of where the POA was executed.

Underwriting Q&A

Powers of AttorneyBy: JoJo GroveAssociate Underwriter Gainesville, FL

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 5

Underwriting Q&A

Powers of AttorneyQ WILL FIRST AMERICAN TITLE INSURE A SALE OR

MORTGAGE OF PROPERTY EXECUTED BY A SUCCESSOR ATTORNEY-IN-FACT?

A Yes, a principal may designate one or more successor attorneys-in-fact if the original attorney-in-fact resigns, dies, becomes incapacitated or declines to serve. § 709.2111(2), Fla. Stat. Where a successor attorney-in-fact will execute the instrument, the Company will require the resignation of the previous attorney(s)-in-fact be recorded. If the resignation is not in recordable format, it may be recorded as an attachment to an affidavit acceptable to the Company. Additionally, unless the POA provides otherwise, the successor attorney-in-fact has the same authority granted to the original attorney in fact. § 709.2111(2), Fla. Stat.

Q WILL FIRST AMERICAN TITLE INSURE A GIFT OF PROPERTY EXECUTED BY A SUCCESSOR ATTORNEY-IN-FACT?

A Underwriting approval is required to insure transactions involving a gift made using a POA. An attorney-in-fact has fiduciary duties to the principal and must act in good faith in a manner that is not contrary to the principal’s best interests. § 709.2114, Fla. Stat. Gifts using a POA are permissible where a principal specifically enumerates and initials a gift of real property in the POA. § 709.2202, Fla. Stat. But title agents must be wary of POAs used to convey or gift the principal’s property to attorneys-in-fact or any of their family members or related entities. § 709.2116(5), Fla. Stat.

Lis pendensIn an action relating to sale of commercial space in condominium building, potential purchaser who was the assignee of the condominium association’s right of first refusal filed their Lis Pendens in accordance with section 48.23, Florida Statutes because right of first refusal was duly recorded. 100 Lincoln Rd SB, LLC v. Daxan 26(FL), LLC, 3D15-1941, 2015 WL 6499331 (Fla. 3d DCA 2015).

Eminent domain Attorney’s fees – “[W]hen a condemning authority engages in tactics that cause excessive litigation, the trial court shall utilize section 73.092(2) to calculate a reasonable attorney’s fee, but only for those hours incurred in defending against the excessive litigation or that portion that is considered to be in response to or caused by the excessive tactics. The remainder of the fee shall be calculated pursuant to the benefits achieved formula delineated in section 73.092(1). The two amounts added together shall be the total fee.” Joseph B. Doerr Trust v. Cent. Florida Expressway Auth., No. SC14-1007, 2015 WL 6748858, at *7 (Fla. Nov. 5, 2015).

Mortgage foreclosure Conditions precedent – Default notice does not need to strictly comply with the provisions of the mortgage. “[T]he lender’s

default notice to the borrower must only substantially comply with the conditions precedent set forth in the mortgage.” Bank of New York Mellon v. Nunez, No. 3D15-83, 2015 WL 6735856, at *2 (Fla. Dist. Ct. App. Nov. 4, 2015).

Homestead exemption – Summary judgment in favor of the mortgagee was improper where “genuine issue of material fact exist[ed] as to whether the homeowner established the subject property as her homestead prior to the Bank’s mortgage.” Vera v. Wells Fargo Bank, N.A., No. 4D14-2672, 2015 WL 6735342, at * 3 (Fla. Dist. Ct. App. Nov. 4, 2015).

Standing – The trial court erred in denying defendants’ motion to dismiss foreclosure complaint where substituted plaintiff failed to establish that the original plaintiff had standing “at inception of the suit.” Dickson v. Roseville Properties, LLC, No. 2D14-1137, 2015 WL 6777155, at *3 (Fla. Dist. Ct. App. Nov. 6, 2015).

Standing – Trial court erred in entering judgment of foreclosure where substituted plaintiff failed to prove that the initial plaintiff was entitled to enforce the note on the date initial complaint was filed. Seidler v. Wells Fargo Bank, N.A., 1D14-2569, 2015 WL 7008174, at *3 (Fla. 1st DCA 2015).

Real property Railroads – A group of owners of land abutting a railroad brought suit against the government claiming the following: (1) that the conveyances for a railroad right-of-way to a recreational trail, pursuant to the National Trails System Act Amendments of 1983, granted only an easement for the railroad rather than fee simple title; (2) the abandonment of the railroad right-of-way entitled the landowners to claim the land free of the easements; and (3) the conversion of the land to a public recreational trail constituted a taking. The United States Court of Federal Claims entered judgment in favor of the government, and, therefore, held the landowners were not entitled to compensation. The Court of Appeals for the Federal Circuit certified a question of Florida law for the Supreme Court to answer. The Supreme Court held: (1) as provided under Fla. Rev. Stat. 2241, railroads may hold fee simple title to land acquired for the purpose of building railroad tracks; (2) no policy in Florida limits the railroad’s interest in the property, regardless of the language of the deeds; and (3) the railroad’s occupancy on the property prior to execution of deed would not affect the quality of the railroad’s property interest conveyed under later-executed deeds. Rogers v. United States, No. SC14-1465, 2015 WL 6749915 (Fla. Nov. 5, 2015).

CASE LAW UPDATES

Page 6First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016

Acronyms have become commonplace in our real estate settlement services industry. In fact, acronyms have come so far that there are acronyms of acronyms! One of the newest is TRID, an acronym for TILA-RESPA Integrated Disclosure. Some acronyms are part of an industry group or association, such as ALTA, FLTA, NAHB, DOI, DFR or RPPTL; sometimes an acronym may describe certain standards.

Do you feel like you are drowning in alphabet soup? Are you ALTA Best Practice Certified? Did you order your CPL from the ASC? Is your E&O up to date? Did you file a UCC or prepare your POA? There are so many acronyms that it can be confusing and certainly overwhelming. As a tool for our agents and employees, First American Title has created the table below with the industry’s most commonly used acronyms and their meanings. CLICK HERE for a downloadable version.

1031 1031 Exchange

ABA American Bankers Association or American Bar Association

ACREL American College of Real Estate Lawyers

AIR Assignment Information Report

ALFN American Legal & Financial Network

ALTA American Land Title Association

APN Assessor's Parcel Number

APR Annual Percentage Rate

ARM Adjustable Rate Mortgage

ASC Agency Service Center

BPO Broker Price Opinion or Business Process Outsourcing

BPOSG BPO Standards and Guidelines

CBA Consumer Banker Association

CC&Rs Covenants, Conditions and Restrictions

CCC Closing Cost Calculator

CFPB Consumer Financial Protection Bureau

CLE Continuing Legal Education

CLI Certified Legal Intern

CLTV Combined Loan to Value

COA Community Association

CPL Closing Protection Letter

DFAST Dodd-Frank Act Stress Testing

DFR Department of Federal Regulation

DFS Department of Financial Services

DIL Deed In Lieu

DOI Department of Insurance

E&O Errors and Omissions Insurance

ECOA Equal Credit Opportunity Act (Regulation B)

EULA End User License Agreement

FACC First American Comprehensive Calculator

FAEC First American Exchange Company

FAEG First American Energy Group

FAF First American Financial Corporation stock symbol

FASS First American Signature Services

FAST First American Settlement Transactions

FATCO First American Title Company

FCL Foreclosure

FDIC Federal Deposit Insurance Corporation

FHA Federal Housing Administration

FHFA Federal Housing Finance Agency

FHLMC Federal Home Loan Mortgage Corporation (“Freddie Mac”)

FLTA Florida Land Title Association

FNMA Federal National Mortgage Association (“Fannie Mae”)

FRA Federal Railroad Administration

Acronyms Closing Corner:

By: Stefanie LollisEscrow Branch ManagerWinter Park, FL

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 7

FRBAR /FARBAR Florida Realtors/Florida Bar

FRM Fixed Rate Mortgage

FTC Federal Trade Commission

GFE Good Faith Estimate

GLBA Gramm-Leach-Bliley Act (Privacy)

GNMA Government National Mortgage Association (Ginnie Mae)

GSE Government Sponsored Entity

HAMP Home Affordable Modification Program

HARP Home Affordable Refinance Program

HELOC Home Equity Line of Credit

HMDA Home Mortgage Disclosure Act

HOA Home Owners Association

HOEPA Home Ownership and Equity Protection Act

HUD Department of Housing and Urban Development

ILSA orILSFDA Interstate Land Sales Full Disclosure Act of 1968

IMD Integrated Mortgage Disclosures

LOC Letter of Credit

LTV Loan to Value

MACReport Market Analysis and Condition Report

MBA Mortgage Bankers Association®

MBS Mortgage Backed Securities

MERS Mortgage Electronic Registration System

MISMO® Mortgage Industry Standards Maintenance Organization

MLS Multiple Listing Service

MRTA Marketable Record Title Act

NAHB National Association of Home Builders

NAR National Association of Realtors®

NCS National Commercial Services

NNA® National Notary Association

NOD Notice of Default

NOS Notice of Sale

NPPI Non-Public Personal Information

OCC Office of the Comptroller of the Currency

O&E Ownership and Encumbrance Report

OFAC Office of Foreign Assets Control

OIR Office of Insurance Regulation

PDR Printed Disclosure Report

PID Positive Identification

PMI Private Mortgage Insurance

POA Power of Attorney

POC Paid Outside of Closing

PTFA Protecting Tenants at Foreclosure Act

REA Reciprocal Easement Agreement

REIT Real Estate Investment Trust

REO Real Estate Owned

RESPA Real Estate Settlement Procedures Act

ROE Return on Equity

ROI Return on Investment

RPIR Real Property Information Report

RPPTL Real Property Probate & Trust Section of the Florida Bar

SCRA Service Members' Civil Relief Act

SDN Specially Designated Nationals

SMDU Servicing Management Default Utility (Fannie Mae)

SNDA Subordination, Non-Disturbance, and Attornment Agreement

STB Surface Transportation Board

TFB The Florida Bar

TILA Truth in Lending Act (Regulation Z)

TRID TILA-RESPA Integrated Disclosures

TSR Title Search Report

UCC Uniform Commercial Code

UDAP Unfair and Deceptive Acts and Practices

UETA Uniform Electronic Transactions Act

UPB Unpaid Principal Balance

UPL Unauthorized Practice of Law

USC United States Code

UTA United Trustee Association

VA Veterans Administration

Acronyms Closing Corner:

Page 8First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016

A father purchases land and in the deed he provides the property will be held with his son and daughter-in-law as a joint tenants with right of survivorship. The father expressly provides that he holds a two-third

interest in the property, while his son and daughter-in-law hold a one-third interest in the property. Did the father, son, and daughter-in-law properly take title as joint tenants with right of survivorship?

Under the traditional common law principals and Florida jurisprudence, such a transfer of title as joints tenants with right of survivorship would be invalid because one of the four requisite unities of title is not present. Specifically, the unity of interest is not present because the tenants do not own, or have rights, to an identical and equal portion of the real property. A recent decision issued by the Second District Court of Appeals, however, creates a wrinkle in this long standing principle.

Simon v. Koplin, 159 So. 3d 281 (Fla. 2d DCA 2015)

In Simon v. Koplin, the personal representative of the estate challenged the probate court’s order dismissing with prejudice the petition to determine homestead status of the real property2. The personal representative argued that the probate court misapplied Section 689.15, Florida Statutes, in concluding that the property passed as joint tenants with right of survivorship because the necessary unities of title—namely, the unity of interest— was absent in the transaction3. The deed provided as follows:

This Indenture made this 15th day of May, 2013, between Ronald S. Simon, Trustee of the J & E Simon Trust, whose post office address is 9301 Vittoria Court, Fort Myers, Florida 33912, of the County of Lee, State of Florida, grantor, and Joseph O. Simon, an unmarried widower, as to an undivided two-thirds (2/3) interest, whose post office address is 14380 Riva Del Lago Drive # 1101, Fort Myers, Florida 33907, and Joanne Koplin and Kent Koplin, husband and wife, a married woman, as to an undivided one-third (1/3) interest, as joint tenants with full rights of survivorship, whose post office address is 2419 Riverwoods Drive, Riverwoods, IL 60015, grantee[.]4

The Second District Court of Appeals held that in accordance with Section 689.15, Florida Statutes, because the instrument conveying the property expressly provided that the parties were to take title as joint tenants with right of survivorship, the survivorship estate was properly formed.5

Following the holding in Simon, the issue presented to real property practitioners and title agents is how does this holding affect, and most importantly comport with, previous Florida case law?

Unities of Title

Under Section 689.15, Florida Statutes, in order for land owners to vest title as joint tenants with right of survivorship, the instrument creating the estate must expressly provide for the right of survivorship interest. Following the enactment of Section 689.15, Florida Statues, the Florida Supreme Court held that “four coexisting unities are necessary and requisite to the creation and continuance of a joint tenancy; namely, unity of interest, unity of title, unity of time, and unity of possession.”6 Accordingly, in order for joint tenants to create a survivorship estate, the real property interests “must be identical, the interests must have originated in the identical conveyance, and the interests must have commenced simultaneously.”7 If one of the joint tenants acts in a manner which would destroy any of the necessary unities of title, such an act would sever the joint tenancy and extinguish the right of survivorship interest.8

Cases Disregarding the Common Law Unities of Title

In the case of Winchester v. Wells, 265 F.2d 405 (5th Cir. 1959), the Fifth Circuit held, “[w]hatever impediment, if any, may have existed under the common law rules of real property to the effectuating of the intent of the parties to the deed here questioned, such impediment has been removed by the Florida Legislature in enacting Section 689.15.”9

Despite the holding in Winchester, the Florida Supreme Court has expressly disapproved of the proposition that Section 689.15, Florida Statutes, abrogated the unities of title requirement. In LaPierre v. Kalergis, 251 So. 2d 885 (Fla. 1st DCA 1971), the First District Court of Appeals held:

It is to be noted that Section 689.15, supra, only abolished the Common law doctrine of the right of survivorship among joint tenants. Such doctrine

Revisiting the Common Law Unities of Title in Survivorship Estates

By: Adrianna La KamUnderwriting Associate

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 9

required, among other matters, that for such an estate to come into being, there must be in the grantees unity of interest, title, time and possession. The Legislature of Florida, by enactment of Section 689.15, supra, brushed away all such restraints.10

The Florida Supreme Court granted certiorari to specifically address the above quoted assertion by the First District Court of Appeals. The Florida Supreme Court held,

The quoted language from the opinion of the District Court cannot stand. Certiorari is therefore granted without oral argument and so much of the opinion below as purports to abolish the necessity of the four unities in the creation of a joint tenancy in realty is expressly disapproved.11

While it appears clear from the Florida Supreme Court the four unities of title must be present at the time the property is conveyed, the District Court of Appeals in Simon attempted to distinguish the holding in LaPierre. In one sentence, the court determined,

The Supreme Court in LaPierre clarified that the unities of possession, interest, title, and time are required to create a true joint tenancy. [] However, LaPierre has no bearing on this case as the right of survivorship here does not depend on the nature of the tenancy but on the express provision in the deed.12

One concern with the holding in Simon is that the deed in question in LaPierre did not merely depend on the nature of the tenancy. The deed in LaPierre contained an expressed provision which granted title as joint tenants with right of survivorship.13 Given the fact the LaPierre decision pertained to a deed with an expressed provision granting survivorship rights under a joint tenancy, it would appear the Florida Supreme Court granted certiorari to specifically reiterate that, along with the expressed provision required in the instrument conveying title under section 689.15, Florida Statutes, the four unities of title must also be present to create a survivorship estate.

Implication of Simon v. Koplin

Real property practitioners should be cognizant of the Simon case. As exemplified in Simon, one area in which this issue may arise is during a probate proceeding. This is because one of the main advantages of holding property as joint tenants with right of survivorship is that property passes outside of the probate estate and transfers automatically to the surviving joint tenant(s) upon the decedent’s death.14

Although the Simon case distinguished its holding from the holding in LaPierre, the court still acknowledged the formal unity of title requirements. Provided the case law holding that the four unities are necessary for the creation of a survivorship estate, it is conceivable that under a similar set of facts another district court within the state may rule differently. If the court were to determine property was not sufficiently titled as joint tenancy with right of survivorship, the property owners would thereafter hold title as tenants in common. Any property interest held by the decedent would then have to be distributed through probate. Litigating these property disputes is a costly endeavor and should be avoided.

Conclusion

Real estate practitioners should continue advising their clients that in order to vest title as joint tenants with right of survivorship, both the expressed provision requirement as specified under Section 689.15, Florida Statutes, and all four unities of title must be present at the time of conveyance. If the property owners are adamant on dividing their real property rights in unequal shares, practitioners should thoroughly advise the property owners of the risks associated with such a transfer, namely that a court may find that the transfer does not create a joint tenancy with right of survivorship.

Litigation may ensue if title deficiencies occur on account of the practitioner not properly advising their clients during the transfer. Practitioners do not want to be in the position of defending the property owner’s title interest. As always, if an issue arises regarding a deficiency in one of the unities of title, please contact our Underwriting Department for further assistance.

1 See Beal Bank, SSB v. Almand & Associates, 780 So. 2d 45 (Fla. 2001); Kozacik v. Kozacik, 157 Fla. 597, 26 So. 2d 659 (1946); Sitomer v. Orlan, 660 So. 2d 1111 (Fla. Dist. Ct. App. 4th Dist. 1995); LaPierre v. Kalergis, 257 So. 2d 33 (Fla. 1971); Kuebler v. Kuebler, 131 So. 2d 211 (Fla. Dist. Ct. App. 2d Dist. 1961).

2 Simon, 159 So. at 281.3 Id.4 Id. at 282.5 Id. at 282.

6 Kozacik v. Kozacik, 157 Fla. 597, 601, 26 So. 2d 659, 661 (1946).

7 Beal Bank, SSB v. Almand & Associates, 780 So. 2d 45, 53 (Fla. 2001).

8 See Crockett v. Crockett, 708 So. 2d 329, 331 (Fla. Dist. Ct. App. 1998).

9 Wells, 265 F.2d at 408.10 LaPierre, 251 So. 2d at 887.11 LaPierre v. Kalergis, 257 So. 2d 33, 34 (Fla. 1971)

(emphasis added).

12 Simon, 159 So. 3d at 282-83 (internal citation omitted).

13 LaPierre, 251 So. 2d at 886 (“‘Note’ Pursuant to Section 689.15 Florida Statutes (F.S.A.), provision is hereby and in this instrument expressly made for the right of survivorship between the grantees.”).

14 See generally, Jennifer L. Griffin & Deborah Packer Goodall, Important Preliminary Administration Issues, PPC FL-CLE 1-1.

Revisiting the Common Law Unities of Title in Survivorship Estates

Page 10First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016

Q IN WHAT AREA OF LAW DID YOU PRACTICE PRIOR TO COMING TO FIRST AMERICAN TITLE?

A I started my legal career with a large law firm in Palm Beach County where my private practice focused on commercial and residential real property and health law. Over time, I became increasingly involved as counsel for two community hospitals. I enjoyed the diverse challenges and responsibilities so much, I eventually accepted a position as in-house counsel with Boca Raton Community Hospital. It was a great experience that required sharp legal analysis within the context of a very complex business operation. I took a similar position with a not-for-profit hospital in Ormond Beach, and then served as deputy general counsel for Shands Healthcare in Gainesville.

Q WHAT MADE YOU WANT TO WORK IN THE TITLE INSURANCE INDUSTRY?

A I have always enjoyed my real estate practice and have had the opportunity to work on some very interesting title questions. I like to understand the background of transactions, the title issues that come up, and to find ways to solve problems so transactions can close. Title work is similar to my health law experience in that I deal with a wide range of issues. I really enjoy the variety! I also enjoy learning about the history of the properties we deal with and seeing how their ownership and use have changed over time.

Q WHAT BROUGHT YOU TO FIRST AMERICAN TITLE?

A I had left Shands and was working with an agent of First American Title, Dell Graham, PA, in Gainesville. I was not looking to make a change. While on vacation, Jennifer Bloodworth left a phone message saying that she needed to speak with me. I was an agent for First American Title, and when senior underwriting counsel called... I worried about whether I had done something wrong. When we connected, I was relieved and surprised when Jennifer said First American Title was interested in discussing the possibility of giving me a job! They were looking to hire an Underwriting Counsel in Gainesville that had the appropriate real property background and familiarity with the area to continue the development of strong relationships and service to agents. Len Prescott and Jen met with me; I was hooked by their vision for the opportunity and their enthusiasm for what they do. I did my homework on the Company and accepted their offer. I started in May 2015, and so far the position has been exactly what they said it would be.

Q TELL US ABOUT THE EMPLOYEE CULTURE IN THE GAINESVILLE OFFICE.

A The atmosphere in Gainesville is very positive. Everyone has a great deal of experience and knowledge, and we work very well together. I especially appreciate the fact that everyone stands by their commitments and provides the same level of service regardless of the value of the transaction. I have felt very comfortable and supported by the folks in the office and underwriting counsel around the state. We also have the advantage of working very closely with the Ocala office, which also has a very talented and experienced staff.

Underwriting Spotlight:

Charles (Chip) KovalUnderwriting Counsel, Gainesville, FL

Chip Koval joined the First American Title team in May 2015, as Underwriting Counsel for North Central Florida, with an office in Gainesville. Chip brings over twenty-five years of legal experience to his position with the Florida Underwriting Department. While at First American Title, Chip has become a subject matter expert for the Florida underwriting team in the areas of code enforcement liens, POAs and Oil, Gas & Minerals. With his vast experience managing complex business transactions and his keen ability to discern and solve problems, Chip has already proven to be an invaluable asset to the Florida underwriting team.

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 11

In response to our customers’ needs, First American Title has established, within our Florida Underwriting Department, a Rapid Response Team. We recognize that there are times when

our agents’ customers have a need for a quick response to keep their deals moving towards a successful closing. We received feedback that there are times when time pressures are urgent and our agents have been unable to reach their preferred underwriting staff member quickly enough; so we have formed our Rapid Response Team to better serve our agents.

The idea was originated by Ken MacKay, SVP, Eastern Division, and was fueled by feedback from and collaboration with our employees. The Rapid Response Team is overseen by Greg Blomeley and includes Florida State Underwriting Counsels Bill Boyce, Chip Koval and Wade Wallace. There is an expectation that other underwriters will be added in the future. This is the first time that First American Title has offered this type of platform and we believe combining new technology with our knowledgeable, approachable, and responsive underwriters will make this new initiative a huge success.

The Rapid Response Team is primarily designed to respond to issues involving residential transactions, as well as commercial transactions with liability up to $5 million. The team has established a general email address so our agents won’t have to remember or look for specific names.

The e-mail address is [email protected] and the Team phone number is 866.728.5207.

All underwriters on the Rapid Response Team have access to this email address and phone number. Being able to utilize this communication method will save time and eliminate the need to make multiple telephone calls or send multiple emails if your preferred underwriter is unavailable. The quality and responsiveness of this focused team will increase our speed of service and allow us to provide timely underwriting support and assistance to our loyal and valued agents!

RAPID RESPONSE TEAM

Team Members

Greg BlomeleyVP, UnderwriterWinter Park, FL

Bill BoyceUnderwriting CounselTampa Bay, FL

Charles (Chip) KovalUnderwriting CounselGainesville, FL

Wade WallaceUnderwriting CounselEstero, FL

By: Greg BlomeleyVP, Underwriter, Winter Park, FL

LEGAL NEWS AND INDUSTRY UPDATES

Monthly Foreclosure Jump Highest in 4 YearsBy: Daily Real Estate News | November 12, 2015Foreclosure filings – including default notices, scheduled auctions, and bank repossessions, rose 6 percent in October month-over-month, led by a 12 percent monthly jump in foreclosure starts.

Real Estate Shell Companies Scheme to Defraud Owners Out of Their HomesBy: Stephanie Saul, The New York Times | November 7, 2015Attention lately has focused on the growing use of shell companies to buy prized real estate in Manhattan and other glittering destinations for global wealth. But the stealthy practice of deed theft illustrates another way that limited liability company law used to create such entities has been twisted and stretched to conceal the ownership of real estate.

Home-Loan Borrowers Bypass the BanksBy: Anya Martin, The Wall Street Journal November 4, 2015Almost half of home-purchase loans now come from independent mortgage companies, which say they can offer faster, cheaper loans.

TRID Costing Clients More Than Just TimeBy: Justin da Rosa, Mortgage Professional America | November 11, 2015 TRID is forcing clients to lock in rates for longer periods of time, due to the increased need for longer closings.

The Long Decline in American Church Construction May Soon EndBy: Carla Vianna, Miami Today News | October 30, 2015America’s 13-year church-building slump may soon come to an end.

U.S. Supreme Court Won’t Hear Appeal on Mortgage RatingsBy: Associated Press | November 2, 2015The Supreme Court won’t hear an appeal from shareholders who claim the Standard & Poor’s ratings firm made false statements about its ratings of risky mortgage investments that helped trigger the financial crisis.

In Mortgages, Here We Go Again? Not Quite By: Joe Light, The Wall Street Journal | November 2, 2015Homes over the past few months have sold at their quickest pace since 2007. But despite low mortgage rates and government efforts to expand mortgage access, borrowers with anything but strong credit scores are still relatively absent, according to a report released Monday.

26,000 Condos in Pipeline for Downtown MiamiBy: Ben Leubsdorf, The Wall Street Journal | November 1, 2016Miami’s potential condo pipeline grew by 738 units this past quarter compared to last, now promising to inflate the greater downtown market by 26,000 new units.

Lenders Worry About Accuracy in Complying with HMDA RuleBy: Andy Peters, National Mortgage News | October 30, 2015Accurately capturing mortgage data to meet new federal regulators is a top challenge for banks and credit unions, according to Wolters Kluwer Financial Services.

Page 12First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

www.firstam.comFirst American Title Insurance Company makes no express or implied warranty respecting the information presented and assumes no responsibility for errors or omissions. First American, the eagle logo, First American Title, and firstam.com are registered trademarks or trademarks of First American Financial Corporation and/or its affiliates.

AMD: 12/2015

FLORIDA STATEWIDEU N D E R W R I T E R S

Represents locations of FL underwriters

REGIONAL AND STATE UNDERWRITING COUNSEL TEAM

REGIONAL AND STATE UNDERWRITING COUNSEL TEAM

FLORIDA STATEWIDE U N D E R W R I T E R S

Represents locations of FL underwriters

First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016 Page 13

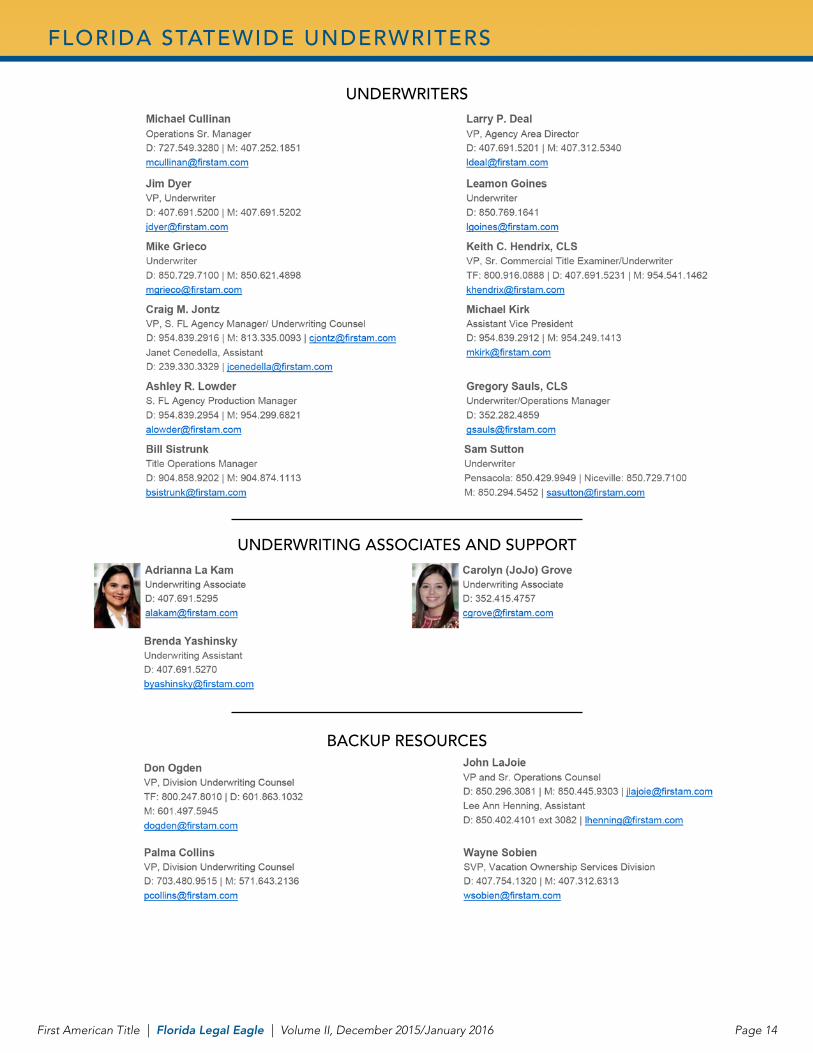

FLORIDA STATEWIDE UNDERWRITERS

UNDERWRITERS

UNDERWRITING ASSOCIATES AND SUPPORT

BACKUP RESOURCES

Page 14First American Title | Florida Legal Eagle | Volume II, December 2015/January 2016