Embed Size (px)

Citation preview

FEDERAL TAX ALERT PAGE 1 MARCH/APRIL 2013

THE FEDERAL TAX ALERTTHE FEDERAL TAX ALERTFrom the bench

A PUBLICATION OF THE NATIONAL SOCIETY OF TAX PROFESSIONALS MARCH/APRIL 2013A PUBLICATION OF THE NATIONAL SOCIETY OF TAX PROFESSIONALS MARCH/APRIL 2013

RECAP OF THE RTRP LAWSUIT AND SUBSEQUENT RULINGS – ONE YEAR LATER

The future of the Registered Tax Return Preparer (RTRP) program has been in the hands of the court since the ruling in favor of the lawsuit filed on March 13, 2012 by three tax preparers. The lawsuit ques-tioned the right of the IRS to require testing and continuing education for paid tax preparers. Since January 18, 2013 the program has been in limbo pending the outcome of the appeal by the IRS. Following is the timeline of the original legal action and subsequent motions and court rulings.

March 13, 2012: The Insti-tute for Justice, an organization specializing as an advocate for the rights of entrepreneurs, filed a lawsuit (Loving et al v IRS) on behalf of three accoun-tants contesting the authority of the Internal Revenue Service to require licensing of tax return preparers. The attorney from the Institute for Justice, Dan Alban, stated that “Congress never gave the IRS the authority to license tax preparers, and the IRS can’t give itself that power.” The three accountants who brought the lawsuit are Sabrina Loving of Chicago, IL – who has been preparing taxes for the past three years with prior expe-rience as an accountant; John Gambino of Hoboken, NJ – is a Certified Financial Planner and registered investment advisor

who prepares tax returns for his investment clients; and Elmer Kilian of Eagle WI – a retired Korean War veteran who prepares taxes season-ally on a part-time basis. Ms. Loving and Mr. Kilian prepare approximately 100 tax returns a year and Mr. Gambino prepares approximately 50 returns per year.

January 18, 2013: The United States District Court for the District of Columbia rules in favor of the plaintiffs granting permanent injunctive relief. Judge James E. Boasberg stated that Congress had not given the IRS the power or authority to license tax preparers. With the ruling the IRS could not require that tax preparers take an exam or fulfill continuing education requirements. The PTIN (practitioner tax identi-fication number) system was discontinued and all testing was canceled.

January 24, 2013: The IRS filed a motion to suspend the injunction. The basis of the motion was that the IRS had a reasonable likelihood of prevailing on appeal, the IRS would suffer irreparable harm if the injunction was not suspended, that the Plaintiffs would not be harmed by the motion and that suspending the injunction would serve in the best of the public interest.

January 29, 2013: The Plain-tiffs filed an opposition to the IRS Motion to Suspend Injunc-tion Pending Appeal.

February 4, 2013: The Court filed a Memorandum Opinion and Order in which the Court denied the IRS motion to stay the injunction. The Court further modified the original injunction to make it clear that the IRS was not required to shut down the PTIN program or to suspend testing. However, while the injunction against the requirement for testing remained the requirement to obtain a PTIN for all paid tax preparers was reinstated.

February 20, 2013: The Department of Justice, on behalf of the IRS, filed a Notice of Appeal to preserve the IRS’ right to appeal the ruling on Loving, et al v IRS. The Deputy Director of the Return Preparer Office, Preston Benoit, stated that due to the injunction the IRS will neither recognize nor endorse the RTRP designation.

February 26, 2013: The Department of Justice, on behalf of the IRS, filed a Government’s Motion for a Stay Pending Appeal. If upheld, this motion would allow the IRS to reinstate the RTRP program during the appeals process.

March 8, 2013: Loving et al file a Response to Government’s Motion for a stay Pending Appeal asserting that the IRS “fails to allege any imminent irreparable harm”

March 14, 2013: The response from the Plaintiffs reit-erates that the IRS has collected nearly $105 million in user fees while only incurring $54 million in costs. The program still continues to collect fees (continued on page three)

RTRP RECAP – ONE YEAR LATER From the Bench Page 1

IRS CONTINUES TO STRENGTHEN PROCEDURES AGAINST IDENTIFY THEFT In the news Page 3

IRS CONTINUES TO REmIND TAx RETURN PREPARERS OF EITC DUE DILIGENCE RESPONSIBILITIES

PractIce management Page 4

FAILURE TO FILE A PARTNER-SHIP RETURN

From the Penalty Box Page 6

CANCELLATION OF DEBT AND FORm 1099C

From the hotlIne Page 7

CANCELLATION OF DEBT ON RENTAL REAL ESTATE

From the hotlIne corner Page 8

IRA’S – WHAT YOU SHOULD KNOW

et cetera Page 9

HISTORY OF NSTPrememBer when Page 11

CONTENTSFrom the Bench ......................1In the News ..............................3Practice Management ............4From the Penalty Box .............6From the Hotline ....................7From the Hotline Corner ......8Et Cetera ...................................9Remember When ................ 11

FEDERAL TAX ALERT PAGE 2 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 3 MARCH/APRIL 2013

From the eDItorNSTP enters a new day as it launches a new format for the Federal Tax Alert (FTA). The intent of the Founders of NSTP back

in 1985 was to provide a Newsletter to the members which was centered around preparing Federal Income Tax returns and giving advice on how to practice as a professional and serve the client’s needs. A lot has happened in the tax world since 1985 and the Founders could not have imagined that NSTP members would have to not only learn how to prepare returns, but also would be required to understand software applications and learn what computer hardware was needed. Now the Tax Professional scans and attaches documents to electronically filed returns, monitors a website, signs up for Facebook, Twitter, Cloud and Googles for information. As a result, in many cases, today’s Tax Professional finds that they have become “computer dependent” and do not always understand how and why the net result on the computer generated return was reached. One of the objectives of the new format is to bring the understanding back to the how and why. This will be done in many different ways.

The new FTA is a joint effort by a talented team of Tax Professionals and Educators. The FTA will showcase a new, fresh, practical format for Tax Professionals who are in the trenches preparing income tax returns at all levels and providing much needed tax advice to their clients. The following are some of the areas that will be featured in the new format:

• From the Editor(s) - This section will introduce you to the features in the current FTA.

• News Stories - There will be more day to day practical articles which will help you in your daily practice. This version of the FTA includes IRS actions and issues concerning Identity Theft. (See Page 3)

• Hot Topics from the NSTP Hotline - Here members will be kept abreast of the questions, challenges, issues and comments of the members themselves so that everyone can share in what is hot in the real world of tax.

• From the Penalty Box - Periodically the FTA will address one of the many penalties assessed against individual taxpayers and entities and will discuss the purpose of the assessment as well as the positions, if any, that may be able to be taken in order to have the penalty removed. This month’s issue addresses Section 6698 on the Failure to File a Partnership Return. (Page 6)

• Remember When - This will be a section which will include tax trivia, quotes, comics, etc. Our comics will include our own character Mr. Enes T. Pea who will, under different situations, take on the role of a Tax Professional, taxpayer and even an IRS agent.

• Say It in English - In this section a selected IRC Code Section will be broken down so that the Tax Professional will be able to understand what the statute actually says and intends to accomplish. This will provide the tax professional with technical knowledge needed to service the client.

• From the Bench - Here the reader will be given an analysis of Tax Court cases that are practical to the types of issues that our members may come in contact with and will provide the issue(s) of the case, the positions of the IRS and the taxpayer, as well as the ruling by the court and why. It will then address planning issues as to how the Tax Professional can better advise clients on the issues of the case.

• Practice Management Issues - This will be ideas and hints which will aide Tax Professionals in operating their practice. It will address issues such as: client billing, time savers, office procedures, dealing with difficult clients. This FTA includes EITC Due Diligence Responsibilities. (See Page 4).

• Ethics and Circular 230 Issues - This section will provide an analysis of a section inside Circular 230 Regulations and what it means to you as a Tax Professional.

• Letters to the Editor - This area will provide the tax professional an opportunity to comment on topics of the prior FTA.

• NSTP Calendar - This area will be a great addition for those NSTP members who do not use the website on an ongoing basis and will also serve as a great reminder for those that do use it on upcoming seminars, conferences, and special events. See the program announcement for our June Williamsburg Annual Summer Special Topics Workshop and our First Annual “Williamsburg in the West” seminar in Napa Valley California.

• Affinity Partner Showcase - This section will provide a short blurb about the product(s) and/or service(s) offered by one of NSTP’s affinity partners.

• CPE Credits - This section will allow NSTP members to access NSTP’s website which will provide 5 questions needed to achieve 1 CPE credit hour per each FTA issue at a price of only $5.

FEDERAL TAX ALERT PAGE 2 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 3 MARCH/APRIL 2013

The Federal Tax Alert is published 10 times a year by the National Society of Tax Professionals.

Mailing address: The Federal Tax Alert, 11700 NE 95th St., Suite 100 Vancouver, WA 98682. Telephone: 800-367-8130.

Opinions expressed in The Federal Tax Alert are those of the editors and contributors.

(continued from page one) through the PTIN system. The IRS also acknowledges that the fees received from the program can only be used for the costs of the program. The IRS filed a Reply to Appellee’s Motion for a Stay Pending Appeal. The government responded to the Plaintiff ’s argument that there was no harm to the Treasury due to the lack of regulations for tax return preparers. The government’s position is that the public is at harm due to the lack of regulation for tax return preparers.

For a complete copy of the various rulings and motions, go to the NSTP website for links to the court documents. The battle still continues in the courts between Loving, Gambino and Killian versus the IRS.

In the news

IRS Continues to Strengthen

Procedures Against Identity TheftIdentity theft has exploded in the United

States and as a result stopping identity theft and refund fraud is a top priority of the IRS as reported in the Service’s Fact Sheet FS-2013-2 released on January 25, 2013. The Service reports that it has expanded its efforts to better protect taxpayers and help victims during 2013. More than 3,000 IRS employees have been assigned to work on identity theft-related issues which is double the number from 2011.

§7804 provides that unless otherwise prescribed by the Secretary of the Treasury, the Commissioner of the IRS is authorized to employ the number of personnel deemed proper for the authorization and enforce-ment of the Internal Revenue laws and is permitted to issue all necessary directions, instructions, orders and rules to those personnel. As a result of this authority the

Service has trained 35,000 employees who work with taxpayers to recognize identity theft indicators and help the people who are victimized by it. The Service states that it continues to increase its efforts against refund fraud which includes identity theft. FS 2013-2 reports that for 2013 the Service has significantly increased the number and quality of identity theft screening filters that spot fraudulent tax returns before the refunds are issued and states that dozens of filters are now in place. The Service reports that the Criminal Investigation Department (CID) has increased the number of identity-theft investigations by 300%. In the fiscal year 2012, 900 investigations were opened with almost 500 people being indicted with several hundred more investigations started in the 2013 fiscal year beginning October 1, 2012.

As a result of CID’s efforts, the Justice Department’s Tax Division and local U.S. Attorneys, targeted 105 individuals in 23 states as part of a coast-to-coast enforce-ment sweep. As a result, 939 criminal charges were included in 69 indictments. The Service has expanded a pilot program which allows local law enforcement agen-cies in 9 states to obtain tax return data which helps the Service in investigating and pursuing identity thieves and reports that more than 65 individual law enforcement agencies are involved in this effort. These pilot programs are in Alabama, California, Florida, Georgia, New Jersey, New York, Oklahoma, Pennsylvania and Texas. These are the states where the largest percentage of overall identity theft refund threats have been seen by the IRS. The Service continues to expand this effort to other states as needed. §7206 Fraud and False State-ments provides the Service the authority to impose a fine of up to $100,000 and/or up to 3 years of imprisonment for any person who is found guilty of a felony conviction

for submitting a false tax return.

On February 7, 2013 the Service reported in IR-2013-17 that there was a massive sweep in recent weeks which targeted identity theft in 32 states and Puerto Rico and involved 215 cities and surrounding areas. In January 2013 there were actions against 389 identity theft suspects that led to 734 enforcement actions which included indictments, complaints and arrests. CID expanded its efforts to more than 1,460 since October 1, 2012, the beginning of the fiscal year. In the report, Acting Commis-sioner Steven T. Miller stated:

“As tax season begins this year, we want to be clear that there is a heavy price to pay for perpetrators of refund fraud and iden-tity theft. We have aggressively stepped up our efforts to pursue and prevent refund fraud and identity theft, and we will continue to intensely focus on this area. This is part of a much wider effort under way for the 2013 tax season to stop fraud.”

In addition, the Service is working closely with more than 130 financial institutions to identify identity theft fraud schemes and block those refunds from ever being received by the thieves and this program has protected millions of dollars.

In it’s efforts to help the victims of iden-tity theft the Service reports that it has created steps to assist the victims in 3 ways as follows:

• IPPINExpansion

• VictimCaseResolution

• ServiceOptions

•IP PIN Expansion. The IRS continues to expand the number of Identity Protec-tion Personal Identification Numbers (IP PINSs) being issued to victims of identity theft. The IP PIN is a unique identifier

We are confident that you will enjoy the changes made to the FTA and we assure you that we will be bringing you the very best that NSTP has to offer in each and every issue.

Nina Tross, MBA, EA, RTRP

Rod Ervin, RTRP

Paul LaMonaca, CPA, MST

We welcome your letters, comments and suggestions for future articles. Letters can be emailed to [email protected] or paul @ nstp.org

FEDERAL TAX ALERT PAGE 4 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 5 MARCH/APRIL 2013

that shows that a particular taxpayer is the rightful filer of the return. In 2013, the IRS has already issued IP PINs to more than 600,000 taxpayers who have been victim-ized by identity theft. That’s more than twice as many as the previous year. The IP PIN allows these individuals to avoid delays in filing returns and receiving refunds.

• Victim Case Resolution. The IRS continues to assign more employees in resolving victim cases. The Service reports that these are extremely complex cases and they frequently involve multiple issues and multiple tax years. In some cases resolving identity theft becomes more complicated by the fact that sometimes the thieves them-selves call the IRS. The IRS is working hard to streamline its internal process, but states that much more work remains to be done. A typical case can take about 180 days to resolve, and the IRS is working to reduce that time period.

•Service Options. The IRS is providing information in several ways ranging from a special section on IRS.gov devoted to iden-tity theft to a special phone number avail-able for victims to resolve tax issues. The IRS Identity Protection Specialized Unit is available at 1-800-908-4490.

The Service reminds tax professionals and taxpayers that more information is available on IRS.gov, including the Taxpayer Guide to Identity Theft. If a taxpayer has become the victim of identity theft or is a potential victim and would like the IRS to mark

their tax account to identify any question-able activity the Service recommends that the taxpayer submit Form 14039, Identity Theft Affidavit. On page 2 of Form 14039, Section E, the Tax Professional is one of the representatives who is permitted to submit the Affidavit on behalf of the taxpayer. If a Tax Professionals has been issued a CAF number then it must be entered on the form.

When the Service discovers that a taxpay-er’s identity has been stolen, it issues a letter to the victim. The letter is LTR 4674C which will identify the tax year for which the theft has occurred and will inform the victim why the letter has been sent. The letter discusses the following items:

• The Service is aware that someoneattempted to impersonate the taxpayer by using personal information such as a SSN, or ITIN.

•Morethanonetaxreturnwasfiledusingthe personal information.

• Enclosure of IRS Publication 4535,IdentityTheftPreventionandVictimAssis-tance.

• Adjustment of taxpayer’s account toreflect the correct tax return information and that the victim’s records are accurate with the IRS.

•TherewillnotbecontactbytheIRSviae-mail.

•There is an identity theft indicator onthe victim’s account which will remain there for 3 years. It may be extended if there remains to be an indication that someone else is using the data to file a tax return. If the period is extended then the IRS will contact the victim concerning the exten-sion. The identity theft indicator means that any tax return submitted with the taxpayer’s SSN or ITIN will be reviewed in order to prevent someone else from using it to file tax returns. (Note: As a result, the taxpayer’s return is normally processed over a period which is longer than the normal processing period and will cause a delay in issuing the refund.)

Note: The letter also states that disclosure laws prevents the Service from revealing information about the individual using the victim’s SSN or ITIN.

The LTR 4674C also recommends that the taxpayer monitor their other financial matters and if there is any other suspi-

cious or unusual activity the victim should contact:

1. All the associated financial institu-tions.

2. Fraud department of one of the three major credit bureaus as follows:

• Equifax at 800-525-6285 or www.equifax.com

• Experian at 888-397-3742 or www.experian.com

• TransUnion at 800-680-7289 orwww.transunion.com

3. Check their credit report once every 12 months by requesting a credit report from www.annualcreditreport.com, or call 1-877-322-8228 or writing to:

Annual Credit Report Request Service

P.O. Box 105281

Atlanta, GA 30348-5281

4. Report any activity to the local police authority.

5. File a complaint with Federal Trade Commission. Call toll free at 1-877-438-4338, or online at www.ftc.gov/idtheft or by mail to:

Identity Theft Clearinghouse

Federal Trade Commission

600 Pennsylvania Avenue, N.W.

Washington, D.C. 20580

6. Contact local Social Security Admin-istration Office to ensure earnings records are accurate.

If the taxpayer needs to contact the IRS there is a special toll free number at 1-800-829-0922. Also, if there are tax account problems that have not gotten resolved through the normal channels the Service recommends that the taxpayer or representative contact the Taxpayer Advo-cate Service (TAS). TAS has a separate toll free number at 1-877-275-8261.

PractIce management

IRS Continues to Remind Tax Return Preparers of EITC Due Diligence Responsibilities

All during the 2013 filing season the

NOTICETAX HOTLINEMonday & Tuesday

6 AM — 2 PM PST7 AM — 3 PM MST8 AM — 4 PM CST9 PM — 5 PM EST

Wednesday - Friday9 AM — 5 PM PST

10 AM — 6 PM MST11 AM — 7 PM CST12 PM — 8 PM EST

Saturday11AM — 3PM EST

DIRECT LINE360-695-0556

Technical Tax advice provided by NSTP Hotline staff is based upon specific information conveyed by the member. Members should take special care in relying upon recommendations and opinions that reflect the understanding of the Hotline staff member. NSTP and the Hotline staff are not responsible for misapplication of information given. Members are resposible for the utimate verification and application of any information provided by NSTP.

FEDERAL TAX ALERT PAGE 4 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 5 MARCH/APRIL 2013

Service has been receiving tax returns which either did not include updated Form 8867 APaid Preparer’s Earned Income Credit Checklist@ or received an incomplete Form 8867. The new EITC Due Diligence requirements were finalized in December of 2011 after the passage of the United States - Korea Free Trade Implementation Act. This legislation amended §6695(g) which increased the penalty for the failure to perform due diligence from $100 to $500. The purpose was to help curb EITC fraud.

The Form 8867 was expanded to 4 pages and has 4 parts. Part I includes questions addressing eligibility for all taxpayers as to whether or not they qualify for the EITC. Part II addresses the issues pertaining to qualifying children of the taxpayer. Part III addresses those taxpayers with earned income without a Qualifying Child and Part IV focuses on theDueDiligence require-ments. Note that this section of the Form takes up one and one-half pages.

§6695(g) addresses the failure to be dili-gent in determining eligibility for earned income credit and specifically provides that: any person who is a tax return preparer with respect to any return or claim for refund who fails to comply with due diligence requirements imposed by the Secretary by regulations with respect to determining eligibility for, or the amount of, the credit allowable by §32 shall pay a penalty of $500 for each such failure.

As a result of the change in the statute, §1.6695-2(a) of the final regulations has been amended. In addition, the amended regulation now requires that the Form 8867 be included in the tax return. In prior years the form was retained by the tax preparer in the client file. The regulations also changed who the penalty for failure to perform due diligence could be assessed against. Prior to the update only the signing tax return preparer could be assessed the $100 penalty. After the change, the regulation states that the $500 penalty can be assessed against a tax return preparer therefore subjecting any tax return preparer who determines that a taxpayer is eligible for an EITC or deter-mines the amount of the EITC. In addition, the penalty could be assessed against the employers of those preparers. As a result the IRS can assess penalties against a firm if one of the following apply:

• Managementparticipated inor,priorto the time the return was filed, knew of the failure to comply with the due diligence

requirements; or

• The firm establishes appropriatecompliance procedures but disregards those procedures through willfulness, reck-lessness, or gross indifference, including ignoring facts that would lead a person of reasonable prudence and competence to investigate or figure out the employee was not complying.

The IRS states that employers should protect themselves from penalties caused by employees not meeting their EITC due diligence requirements by:

•Reviewingcurrentofficeproceduresinorder to make sure they address all appro-priate EITC due diligence requirements,

• Reviewing firm procedures withemployees to ensure they clearly understand their responsibilities and the expectations of the employer,

•ConductingannualEITCduediligencetraining or instructing staff to complete the online module that the IRS offers to tax preparers,

• Testing employee’s knowledge of bothdue diligence and firm procedures.

The Service also recommends that an employer perform recurring quality review checks on their employees’ work including credit computations, questions they asked clients, documents they reviewed, and the records kept.

InPartIVof thenewForm8867,ques-tion 24 specifically asks the question did you ask the taxpayer any additional questions that are necessary to meet your knowledge requirements. It also specifically states that the preparer should see the instructions before answering. The instructions say:

If a reasonable and well-informed tax return preparer knowledgeable in the law would conclude that any information the taxpayer has given you appears to be incorrect, incomplete, or inconsistent with the taxpayer’s eligibility to claim the EITC, you must ask the taxpayer reason-able questions to get information that is correct, consistent, and complete. You must document the questions you asked and the answers you received. This is how you meet your knowledge requirement. In other words if the preparer has an itch then it should be scratched.

The instructions also state that the preparer should check “does not apply”

on line 24 if you did not need to ask any additional questions because you were not given any information that appeared to be incorrect, inconsistent, or incomplete.

Question 25 asks if the preparer docu-mented the additional questions asked and the client’s answers which the preparer must answer, yes, no or does not apply. The new regulations also stress the importance of document retention and the requirement of keeping a copy of all documents the preparer used to determine the eligibility for and the calculation of the amount of the EITC. While the new requirements do not require the preparer to ask for or review any more documents than under the old rules they are now required to keep a copy of any documents received from the client and relied on in order to determine EITC eligibility or the amount of the EITC. Examples of these documents include but are not limited to:

• Any income documents other thanW-2 forms

• Income or expense documents thatsupport Schedules C or F income including client prepared records of income and expenses

• Interestincomestatements

• SocialSecuritycards

• Guardianshiprecords

• Courtplacementrecords,etc.

The records are required to be retained for three years from the latest of the following dates that apply:

• The due date of the tax return (not including extensions);

•The date the return was filed (if you signed the return and filed it electroni-cally);

•Thedate the return was presented to the taxpayer for signature (if you signed the return and did not file it electronically); or

•Thedate you submitted the EITC part of the return to the preparer who signed the return (if you prepared the EITC portion of the return but another preparer signed the return).

The IRS stresses that the preparer must store the checklist in either paper or elec-tronic format and will need to be produced if audited.

In order to help preparers become familiar with these new rules the IRS created

FEDERAL TAX ALERT PAGE 6 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 7 MARCH/APRIL 2013

a dedicated EITC due diligence webpage and an online EITC due diligence training module that will help preparers avoid the §6695(g) penalty. Also, the Service has created a helpful FAQs on its website at [email protected] to assist preparers and taxpayers. There is a new Publication 4717, Help Your Tax Preparer Get You the EITC You Deserve. For preparers go to the Search Box and enter Due Diligence Training Module which covers technical parts of must do’s and contains scenarios of applying the due diligence requirements. The preparer can complete the course, pass the test and print a certificate of comple-tion and receive a CPE credit. It is avail-able in English and Spanish. Also, the IRS providesafreeDVDcalled“DueDiligence,Give Your Clients their Due, EITC and Due Diligence Made Easy.”

From the Penalty box

IRC §6698 Failure to File a Partnership Return

Many members have told us that they have clients who have received IRS Notice CP162 assessing a penalty under §6698 for the failure to file a partnership return, IRS Form 1065. §6698(a) provides a general rule that if any partnership required to file a return under §6031 fails to file a return at the time prescribed (including exten-sions) or files a return which fails to show the information required under §6031, then the partnership shall be liable for a penalty (not the individual partners). The penalty is imposed for each month (or fraction of a month) the failure continues. The maximum time period is 12 months. §6698(b) provides that the amount of the penalty is $195 per month multiplied by the number of partners in the partnership for each partner who was a partner for any part of the taxable year. §6698(c) specifically states that the penalty is imposed against the partnership.

Note: The penalty rules for the failure to file for a partnership are more stringent than the failure to file penalties for individual taxpayers, corporations, estates and trusts. Those individuals and entities are penalized only for the failure to file a return. They are not subject to a penalty for filing a return which does not report “the information required.”

§6031 provides that every partnership

(as defined under §761(a)) shall prepare a return for each taxable year, stating specifi-cally the items of gross income and deduc-tions allowable and such other information for the purpose of carrying out the provi-sions of the income tax law as the Secretary may prescribe by forms and regulations. The return shall include the names and addresses of the individuals who would be entitled to share in the taxable income if distributed and the amount of the distribu-tive share of each individual.

§6031(b) provides that if the partnership is required to file a return (Form 1065), then the partnership is also required to furnish to each person who is a partner or holds an interest in such partnership as a nominee for another person at any time during the taxable year, the required information pertaining to that partner on a return as required by the regulations. That informa-tion is to be reported on IRS Form Schedule K-1 (Form 1065). It is required to be issued to the partner by April 15, following the close of the tax year.

Historically, no penalty was assessed against the partnership for the failure to file a Form 1065 or for filing a return which failed to show all the proper infor-mation. The 1978 Tax Reform Act added §6698 effective for returns for tax years after 12/31/78. At the time of the enact-ment of §6698, the penalty was only $50 per month for a maximum period of 5 months. Legislation in 2007 increased the $50 to $85 and the 5 months to 12 months effective for returns required to be filed after 12/20/2007, and before 1/1/2009. In subsequent 2008 Legislation the penalty was increased from $85 to $89 per month for the period after 12/31/1008 and prior to 1/1/2010. For tax periods beginning after 12/31/2009 the penalty has been increased to where we are now at $195 per person who was a partner in a partnership at any time during the year for each month or part of a month the return is late or incomplete with a maximum of 12 months.

Example #1: Partnership A fails to file a timely return and there are 3 partners during the taxable year. The penalty imposed under §6698 would be $195 per month for 12 months, equal to $2,340, times the 3 partners totaling $7,020.

Example #2: In a real situation a Limited Liability Company (LLC) with 2 LLC members failed to file a Form 1065 which was given to the managing member to sign

and file before the April 15 due date. The managing member filed the Form 1065 when he found it in his brief case in early December. The return was 8 months late and the IRS sent the LLC a CP162 Notice assessing the penalty for the 8 months at $195 per month times the 2 members totaling $3,120.

While §6031(a) provides that every partnership must make a return for each taxable year including all information that the Secretary may prescribe by forms and regulations, IRS Rev. Proc. 84-35 (1984-1 C.B. 509) cites an exception for the defini-tion of a partnership under §6231(a)(1)(B). §6231 was enacted in the Tax Equity and Fiscal Responsibility Act of 1982 which added §6211 through §6232 to provide that the tax treatment of partnership items must be determined at the partnership level. §6231(a)(1)(A) defines a “partnership” to mean any partnership required to file a return under §6031(a) except as provided in §6231(a)(1)(B) which provides that a “part-nership” does not include a partnership if the partnership has 10 or fewer partners, each of whom is a natural person (other than a nonresident alien) or an estate, and each partner’s share of each partnership item is the same as such partner’s share of every other item. Also for this purpose, a husband and wife, and their estates are treated as one partner.

The Conference Committee Report concerning §6698 states that the penalty will not be imposed if the partnership can show reasonable cause for failure to file a complete or timely return. Smaller part-nerships (those with 10 or fewer partners ) will not be subject to the penalty under this reasonable cause test so long as each partner fully reports his share of the income, deduc-tions and credits of the partnership.

In order for the reasonable cause excep-tion to apply there are required procedures in Rev. Proc. 84-35 that must take place as follows:

• A domestic partnership composed of10 or fewer partners and coming within the exceptions outlined in §6231(a)(1)(B) will be considered to have met the reason-able cause test and will not be subject to the penalty imposed by §6698 for the failure to file a complete or timely partnership return, provided that the partnership, or any of the partners, establishes, if so requested by the Internal Revenue Service, that all partners have fully reported their shares of

FEDERAL TAX ALERT PAGE 6 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 7 MARCH/APRIL 2013

the income, deductions and credits of the partnership on their timely filed income tax returns.

•Partnershipshavingatrustorcorpora-tion as a partner (tier partnerships) and partnerships where each partner’s interest in the capital and profits are not owned in the same proportion, or where all items of income, deductions and credits are not allo-cated in proportion to the pro rata interests, do not come within the exception provi-sions of §6231(a)(1)(B) of the Code and are subject to the penalty imposed by §6698.

Note: The Rev. Proc. states that although a partnership of 10 or fewer partners may not be automatically excepted from the penalty imposed by §6698 of the Code under §3.01, the partnership may show other reasonable cause for failure to file a complete or timely partnership return. (These exceptions are not addressed in this article.)

In determining whether a partner has fully reported the partner’s share of the income, deductions, and credits of the partner-ship, for purposes of §3.01, all the relevant facts and circumstances will be taken into account. In making this determination, the nature and materiality of any error or omission will be considered. For example, although an isolated clerical error normally reflects no more than mere inadvertence, such an error may be of such magnitude that the partner will not be considered to have fully reported. If the error or omission results in a de minimis understatement of the net amount payable with respect to any income tax, then the penalty will not be asserted. However, if the error or omission results in a material understatement of the net amount payable with respect to any income tax, the partner generally will not be considered to have fully reported and the penalty will be applied to the partnership.

Note: Rev. Proc. 84-35 is effective for returns required to be filed after June 22, 1984.

When responding to the CP162 Notice the Tax Professional must specifically state that the taxpayer disagrees with the Service’s assessment of the penalty under §6698 because Rev. Proc. 84-35 provides an exception for domestic partners with 10 or fewer partners and should specify the actual number of partners and the fact that the individual partners did in fact report the results on their own Form 1040 returns. If the IRS accepts the request to

waive the penalty, then the Service will issue a response on LTR 168C which will state that the penalty is being removed and will specifically state that their action is based on the partnership’s statement that it quali-fied for the relief under Rev. Proc. 84-35. It further states that the penalty will be reassessed if the Service later finds out that the partnership does not qualify for relief because of any of the following reasons:

1. Any partner is not a natural person or the estate of a natural person.

2. The partnership has elected to be subject to the rules for consolidated audit procedures under §6221 through §6234.

3. Any partner filed late or failed to report their distributive share of partnership items on their income tax returns (Form 1040).

The relief provision is very helpful where the partners were not aware that there was a partnership filing requirement or aware that a partnership existed for federal income tax purposes.

The CP162 Notice states that payment is due within 21 days of the Notice. If the taxpayer does not respond within the stated period then the Service will issue CP504B which is a certified letter containing a Notice of intent to levy. The taxpayer has 10 days to respond or pay. The Notice specifi-cally states that they will seize the taxpayer’s property and apply it to the amount owed. In addition, interest is also assessed under §6601.

The issue that the tax professional and taxpayer needs to remember is that the IRS assesses the §6698 failure to file penalty against the small partnership before it is known if the criteria for the waiver is met. It would be helpful to the partnership to be alerted to the exception stated in the Rev. Proc. when the CP 162 Notice is sent to the partnership. If the Service disclosed the exception and allowed the partnership to check a box or to sign off on the require-ments of the exception, the relief could be easily attained and resolved with minimum controversy between the Service and the partnership. It seems that the Service is able to collect substantial revenue on the backs of the unknowing of this exception in Rev. Proc. 84-35.

From the hotlIne

CANCELLATION OF DEBT AND FORm 1099C

In these continued times of financial stress and hardship, we are often called upon to report the tax consequences of debt forgive-ness. Lending institutions, under pressure from the federal government, the public, or even their own stockholders, are realizing the hopelessness of gaining full settlements of amounts owed them. When they give up or write off these receivable amounts, they are able to deduct the losses. Accord-ingly, the debtor realizes income equal to the amount of debt forgiven. IRS Publica-tion 4681 provides guidelines to reporting this income. Included in the definition of “Cancelation of Debt Income” are debts that are cancelled, forgiven, or discharged for less than the full amount. Under certain circumstances there are exceptions to taxation of these amounts. These will be discussed later.

This cancellation of debt is reported by the lender on Form 1099C, which is sent to the IRS and the debtor. Except in a few cases, anytime a 1099 Form is received, it MUST be addressed on the return in one way or another. Before we go further, let’s look at the information reported on the 1099C. Besides identifying the debtor and creditor, the following information is important in determining the tax consequences:

Box 1 – Date of identifiable event (this is usually the date the debt was cancelled);

Box 2 – Amount of debt cancelled;

Box 3 – Interest included in box 2 (this may be important on a home mortgage);

Box 4 – Debt description (this will aid in determining where the income is reported);

Box 5 – Was debtor personally liable for the debt? (may not be taxable);

Box 6 – Identifiable event code (Indicates the reason creditor has filed the form); and

Box 7 – Fair market value of the property (Useful if property was foreclosed and no 1099A).

As regards cancellation of debt, there are at least six common situations that need to be addressed:

FEDERAL TAX ALERT PAGE 8 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 9 MARCH/APRIL 2013

1. Nonbusiness debt cancellation – If a credit card debt or open account used for personal expenditures is forgiven, the amount shown in Box 1 will be reported on line 21 for Form 1040.

2. Personal vehicle repossession – If the client had a personal vehicle repossessed and disposed of by the lender during the year, you will need to determine the gain or nondeductible loss on the disposition. The amount of debt forgiven would be reported on line 21 of Form 1040.

3. Principal residence foreclosure or aban-donment – The income may be excluded on Form 982, if certain conditions are met. Also included in this category are loan modifications and “work-out agreements”. This will be discussed later.

4. Cancellation of debt on rental real estate – This may also involve a “short sale” or foreclosure.

5. Cancellation of debt on acquiring busi-ness property.

6. Cancellation of debt on qualified farm indebtedness.

Each of these situations provides you, as the tax professional, different reporting challenges and opportunities. The two most common situations are those involving a personal residence and involving rental real estate. We will address them in sepa-rate articles.

CANCELLATION OF DEBT ON RENTAL REAL ESTATE

In this current economy, even landlords are faced with mortgages they are unable to service. In this article we will address the rules governing taxation in situations where there has been cancellation of debt on rental property. First and foremost we must remember that forgiven debt, either through out and out write-off, or through modification of the debt agreement, is considered income and may be taxable. Under certain circumstances the “income” may be excluded from taxation. We’ll tackle that later. Keep in mind, the terms “cancelled”, “forgiven” and “discharged”, in context of a reduction in amounts owed are interchangeable.

Investment in real estate as a rental has long been a good way to develop equity, through appreciation and by having the debt paid via rents collected on the prop-

erty. Cancellation of debt on rental prop-erty gives rise to additional rental income and is to be reported on Schedule E for that property. The amount shown in box 2 of Form 1099-C is to be included in line 3 of Schedule E for that property. (The general rule is that the income from debt cancel-lation is reported in the same nature as debt related; ie business debt on Schedule C; farm debt on Schedule F; and personal debt on line 21 of Form 1040). This amount in box 2 may represent some or all of the debt that has been cancelled, or is treated as cancelled. Unless the taxpayer meets one of the exceptions or exclusions discussed later, the amount of the debt that has been canceled is considered income.

If the taxpayer has not made payments owed on a loan secured by property, the lender may foreclose on the loan or repos-sess the property. The foreclosure or repos-session is treated as a sale from which the taxpayer may realize gain or loss. This is true even if the property if voluntarily returned to the lender. The amount realized on the “sale” depends on the type of financing. If the borrower is not personally liable to repay the debt even if the value of the property is less than the outstanding debt, it is called “Nonrecourse Debt”. The amount realized is the full amount of the debt canceled by thelender,evenifgreaterthantheFMV.Ifthe borrower is personally liable to pay any amountofthedebtnotsatisfiedbytheFMVof the property, it is called “Recourse Debt”. If the outstanding loan balance was more than the FairMarketValue (FMV) of theproperty and the lender cancels all or part of the remaining loan balance, then there is also cancellation of debt income.

The gain or loss from a foreclosure or repossession is reported in the same way as gain or loss from a normal sale. The sales price for this “deemed sale” depends on whether or not it is “Recourse Debt”. The adjusted basis of the property (cost less accumulated depreciation) is then subtracted to determine if there is a gain or loss. Like the sale or rental property, this transaction is reported on Form 4797. A lender who acquires an interest in a prop-erty in a foreclosure or repossession should send the taxpayer a Form 1099-A (Acquisi-tion or Abandonment of Secured Property) showing the information to calculate the gain or loss. However, if the lender also cancels part of the debt, they must file Form 1099-C, as well. As an alternative, the lender can include the information about

the foreclosure or repossession on Form 1099-C instead of Form 1099-A.

The reporting on Form 4797 depends on whether the transaction results in a gain or loss. If it’s a gain, the reporting begins on page 2 in part III as a §1250 asset. If the transaction results in a loss, it is reported on page 1 as a §1231 asset. Since a §1231 loss is an ordinary loss, it will offset some or all of the income from cancellation of debt. If the two items result in a net loss, it may be suspended as a passive activity loss.

Example: In 2009, Ann purchased a house to use as a rental. She paid $200,000 for the property, putting $20,000 down and borrowed the remainder from her bank as a recourse loan, with the property as secu-rity. By 2012, the house had decreased in value to $160,000, but the loan balance was $175,000. Ann stopped making the mort-gage payments so the bank then foreclosed on the mortgage. After taking deprecia-tion, the adjusted basis of the property was $185,000. The amount Ann realized on the foreclosure was $160,000 (the lower ofFMVor loanbalance). Her§1231 losswas $25,000 (amount realized less adjusted basis). Her cancellation of debt income to be reported on Schedule E is $15,000 (loan balancelessFMV).Sincetheincomeislessthan the loss on the foreclosure, the loss on foreclosure is limited to $15,000 and the remaining loss of $10,000 becomes a suspended passive activity loss.

et cetera

IRA’S – WHAT YOU SHOULD KNOW

Traditional Individual Retirement Accounts (IRAs) have been with us for years and, like the neighbor next door, there is much we have either never learned or have forgotten about them. This is confirmed by many questions posed to the NSTP’s Tax Hotline. Rather than a piece-meal approach, we have decided to undertake a comprehensive review of the “ins and outs” of IRAs. For reference purposes most of this information is contained in PUB 590 or IRC §219 and §408. It is recommended that you include PUB 590 in your professional reference materials.

Your involvement in this area could be

FEDERAL TAX ALERT PAGE 8 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 9 MARCH/APRIL 2013

from the client who is considering some sort of retirement account and is looking to you for guidance. In most cases, however, the client will already be invested in an IRA of some sort. In all probability, the only time you see the client is at tax time. Due diligence would dictate that you be aware of your clients involvement in order to guide them to proper handling of any transac-tions.

First, let’s address the Traditional IRAs (don’t worry Roth fans, your turn is coming). A Traditional IRA can be an “account” or an “annuity”.

•Advantages – The contributions may be fully or partially deductible on the individ-ual’s current tax return. The account grows tax free in that the current earnings and any increase in value avoid taxation until the funds are withdrawn. Under certain circumstances, the contribution can qualify for the “Retirement Saver’s Credit”.

• How – The accounts are set up as a trust or custodial account, in writing, in accordance with IRC §408(a). The “Trustee Custodian” can be a bank, credit union, savings and loan, or other entity approved as a custodian by the Internal Revenue Service. The contributions for current deduction or application must be in cash (this does not apply to rollovers, which retain their character in the hands of the receiving custodian).

Setting up an Individual Retirement Annuity is accomplished by purchasing an annuity or endowment contract from a life insurance company. This contract must be issued in the individual’s name as the owner. Only he or his designated beneficia-ries can receive the benefits. IRC §408(b) requires:

1. The owner’s interest must be non-forfeitable;

2. The owner cannot transfer ownership to anyone else, except the issuer;

3. The premiums must have flexibility to change if the owner’s compensation changes;

4. The total premiums for a year cannot exceed the maximum limit for IRAs;

5. Refunded premiums must be used to pay for future premiums, or to increase the benefits (up to the maximum). This must be accomplished before the end of the year following the year the refund is received.

6. The rules for Required Minimum Distributions must be followed. (To be discussed later).

•Who – The beneficial owner must be an individual, under the age of 70 ½ with earned, taxable compensation (includ-able in AGI) during the year relating to the contribution. It is possible to have a Traditional IRA, while also being covered by another retirement plan. However, the contributions may not have deductibility if the taxpayer (or spouse, if married) are covered by an employer retirement plan.

For married individuals, if both spouses have taxable compensation and otherwise qualify, they may each have their own IRA. There is no provision for a “Joint IRA”. A “Spousal IRA” can be set up if the taxpayers file a joint return, even if the spouse has little or no taxable compensation. The spousal contribution is limited to the smaller of the individual maximum; or the sum of both spouses compensation, less the amount already contributed to the initial IRA for the year.

Example: John, age 53, and Mary, age 49, are married. John earns $40,000 in wages, but Mary is a stay-at-home Mom. For 2012, John contributes $6,000 to an IRA (he is over 50). If John and Mary file a joint return, John may also contribute to a spousal IRA for Mary. The deductible amount of the spousal IRA is limited to the lesser of: $34,000 ($40,000, less $6,000), or $5,000 (Mary is under 50). Their combined deductible IRA contribution for the year would be $11,000 ($6,000 + $5,000).

•How Much – We’ve already tipped you off to the amounts for 2012. The amount, for persons who have not reached age 50 by December 31st, is $5,000. The maximum becomes $6,000 for those whose age is 50 or older on December 31st. NOTE: For 2013, these amounts become $5,500 and $6,500. If the contribution exceeds the maximum, it could be subject to a 6% penalty, which will be addressed later.

•What is Compensation? - Compensa-tion usually means taxable earnings from personal services (working), including the following according to IRC §219(f):

1. Wages and salaries from box 1 of Form W-2, less any amounts shown as non-qualified plans.

2. Self employment income from Sched-ules C or F; or self employment earnings

from a partnership (as shown on 1065 K-1). These amounts must be reduced by the deduction taken on 1040 for one half of self employment tax.

3. Alimony or separate maintenance payments under a divorce or separate main-tenance decree.

4. Non-taxable combat pay as shown as code “Q” in box 12 of Form W-2 of a member of the U.S. Armed Forces.

5. Military differential payments form an employer to employees called to active duty for more than 30 days. These are already included in box 1 of Form W-2.

•What is not Compensation? – These are earnings from situations not involving personal services:

1. Rental income, interest and dividend income or any other earnings from prop-erty.

2. Retirement benefits such as pensions, annuities, or Social Security benefits.

3. Income from pass-through entities such as partnerships which are NOT for personal service participation.

4. Amounts excluded from income as foreign earned income or housing allow-ances.

•Employer Retirement Plan? – The first indication of the coverage by an employer retirement plan is the box in box 13 of Form W-2. If it is checked, the employer has notified the IRS, the employee and now you, that this individual is covered by an employer plan. With respect to Defined Contribution Plans, (401(k); profit-sharing; stock bonus and money purchase pension plans) persons are considered to be covered if amounts are contributed or allocated to their specific account for the plan year that ends with or is included within the indi-vidual’s tax year, even if the individual is not vested in the plan.

The individual is “covered” if he/she is eligible to participate, even if they have declined to participate; did not make a required contribution; or did not perform the minimum service required to accrue a benefit for the year.

Certain individuals are not considered to be covered by a retirement plan:

1. Persons receiving benefits from a previous employer’s plan;

FEDERAL TAX ALERT PAGE 10 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 11 MARCH/APRIL 2013

1. Borrowing money from the IRA;

2. Selling property to the IRA;

3. Receiving unreasonable compensation for managing the IRA;

4. Using it as security for a loan;

5. UsIng it to purchase property for personal use.

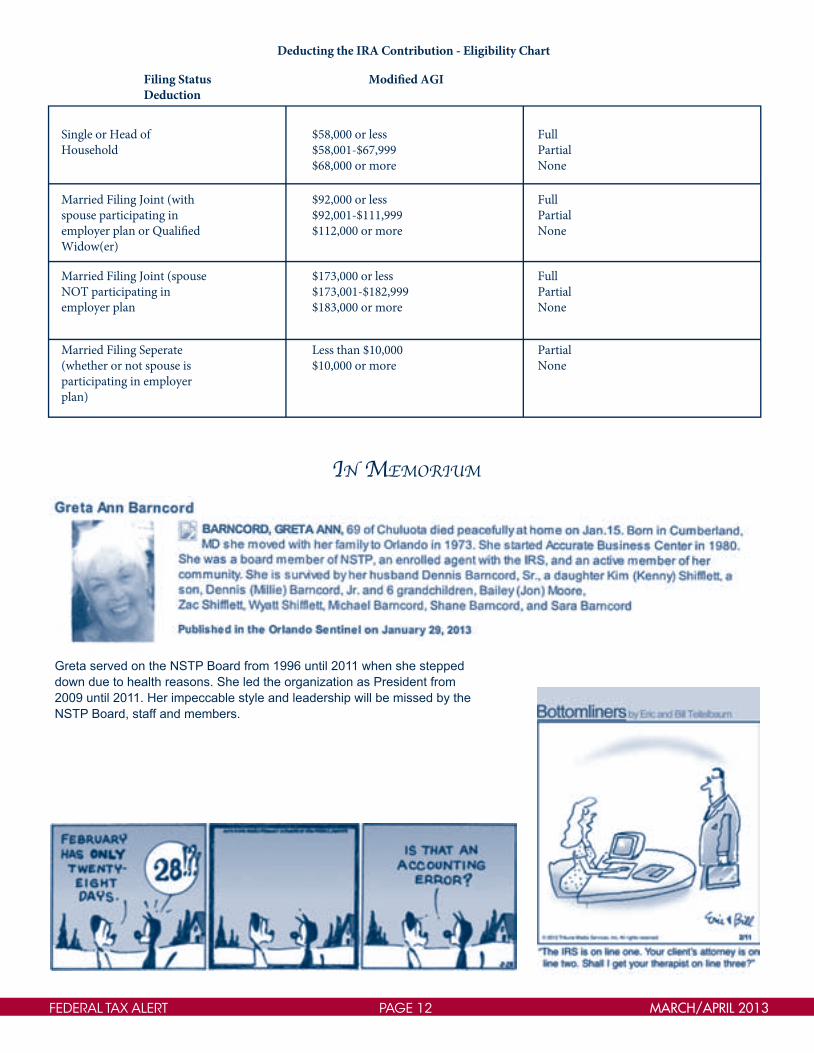

• Deducting the IRA Contributions: The deductibility of the IRA contribution depends on several factors, including the marital status and modified adjusted gross income (MAGI), if there is participation in an employer plan. Depending upon these factors, the contribution may be fully or partially deductible , or non-deductible at all.

Adjusted Gross Income becomes Modi-fied Adjusted Gross Income by NOT including: (see AGI chart on page 12 for deductibility limits)

1. Excluded foreign earned income and housing costs

2. Foreign housing deduction

3. Excluded employer provided adoption assistance

4. Excluded U.S. savings bond interest used for higher education expenses

5. Student loan interest deduction

6. Tuition and fees deduction

7. Domestic production activities deduction

It is important to remember that even if the deduction of a contribution is limited, the taxpayer can still make a maximum allowable contribution. The excess would be considered a non-deductible contribu-tion and would establish basis as we have already discussed.

That’s enough for this month; next we will discuss the “ins and outs” of IRA distri-butions.

Trying to enter the NSTP Members’ Only Section on our website and need to set up a new login or have forgotten your pass-word? You can now click on the “Trouble Signing in” link and follow the instructions to creating a new password.

are $5,000/$6,000 or less (ie they exceeded compensation) the excess can be withdrawn at any time and won’t have to be included in gross income, if they were not deducted. However, the 6% penalty tax will apply for each year the excess contribution remains in the account. If the total contributions exceed the $5,000/$6,000 limits and the excess is not timely withdrawn (by the return due date, including extensions), the entire excess becomes taxable when finally withdrawn, even though no deduction was taken or allowed for that excess.

Unfortunately, if contributions are less than the maximum for a given year, the shortage cannot be corrected by additional contributions after the due date for filing the return (April 15th)

• Non-Deductible Contributions: While there are limits on the deductibility of IRA contributions due to coverage in employer plans, it is still permissible to make “non-deductible” contributions up to the maximum for the year. These non-deductible contributions must be reported on Form 8606. They will establish a basis in future withdrawals, but if not reported on Form 8606, they will be deemed to have been deductible and will be fully taxable when withdrawn.

Example: Loretta is 38 years old and single. In 2012, she was covered by a quali-fied plan at work. Her salary was $65,000, and her modified AGI was $69,500. During 2012, she invested $5,000 in an IRA. Since she was covered by a retirement plan at work and her modified AGI exceeded $68,000, she cannot deduct the $5,000 IRA contribu-tion. She must designate the contribution as non-deductible on Form 8606, and attach it to her return.

Individuals making non-deductible contributions to their Traditional IRA are creating basis in that IRA. The taxability is based on a ratio discussed later when we look at distributions.

• Prohibited Transactions: Now that there is money invested in the Individual Retirement Account, it is important to realize that certain transactions are viola-tions of the trust agreement and are deemed to be distributions to the owner or benefi-ciary. Thus, they must not only be included in income, but penalties for early distribu-tion apply. According to IRC §4975, the following are examples of prohibited trans-actions:

2. Persons covered by Social Security or Railroad Retirement ; (in other words subject to withholding for FICA).

3. Reservists included in a plan only because they are a member of a reserve unit of the armed forces and providing the plan is established by a governmental entity and they did not serve more than 90 days on active duty.

4.Volunteer firefighterswhoparticipatein a governmental plan only because he/she is a volunteer firefighter and the accrued benefits at the beginning of the year will not provide more than $1,800 per year at retirement.

• Excess Contributions – Excess contributions are those made for a tax year that exceed the maximum amount ($5,000/$6,000 for 2012), the individual’s qualified compensation for the year, or if they reached age 70 ½ during the year. A 6% penalty tax applies to the excess contri-bution and is calculated and reported on Form 5329. This form can be filed by itself if the taxpayer is not required to file Form 1040.

If the excess contribution is withdrawn by the due date of the return, including exten-sions, the 6% penalty can be avoided. The taxpayer can also have the excess applied to a current year (if made in the current year) contribution, which would avoid the 6% penalty.

Example: Gordon, age 45, contributes $5,500 to an IRA in December, 2012. He asks you to apply for an extension of time to file. In June, 2013, as you are preparing his return, you notice the excess contri-bution. If Gordon withdraws the excess before October 15, 2013 (the extended due date for the 2012 return) he will avoid the 6% penalty for excess contribution. If the $500 excess earned $29 in interest, it must also be withdrawn and included in Gordon’s income for 2012. In addition, he will be assessed a 10% penalty ($3) on the $29, which is deemed an early distribution (Gordon is under 59 ½ years of age).

If the taxpayer filed his return by the April 15th due date he can still get relief using the 6 month extension period to withdraw excess contributions by filing an amended return (Form 1040X) with the following reference written at the top of the form: “Filed pursuant to Section 301.9100-2”.

If the total IRA contributions for the year

FEDERAL TAX ALERT PAGE 10 MARCH/APRIL 2013 FEDERAL TAX ALERT PAGE 11 MARCH/APRIL 2013

remember when

HISTORY OF NSTPThe National Society of Tax Professionals

has its roots in Oregon when Bill Brown, one of the founding members of the organiza-tion, was on the board of the Oregon Asso-ciation of Tax Consultants (OATC). His vision of a national organization inspired the formation of the National Association of Tax Consultants which was designed to go national representing tax professionals throughout the country. During this time, Bill Brown was also working in the state of Washington to organize the Washington Association of Tax Consultants (WATC) which is a strong state society that continues to this day.

Professionally, Bill Brown was a partner in one of the largest firms in Vancouver,Washington. As a result of his activi-ties with the OATC and the WATC, and subsequent involvement in the start-up of a national organization his practice began to suffer. The practice was sold and a new business venture was launched known as the American Institute of Taxation (AIT). The formation of AIT brought together professionals who would also be key in the formation of the NSTP. John Weber and Rod Larson were tax professionals and additional investors in the AIT while Edward Henderson was introduced to Bill Brown when he was seeking an investment opportunity.

Various roadblocks conspired to derailthe national growth of the NATC. Unable to fulfill the dream of making the NATC a national organization, the AIT board of directors made the decision to assist in the formation of the National Society of Tax Professionals. The initial Board of Directors of the NSTP consisted of: Rod Larson, Pres-ident; Edward Henderson, Secretary; John Weber, Treasurer; and Bill Brown, Susan Girourd and Merlin Pulliam as Directors at Large. The organization contracted with an advertising firm to create a logo and brand for the NSTP. AIT assisted in promoting the NSTP and providing financial support during its fledgling first year. However, AIT began to suffer financially as its most prof-itable seminar, the Enrolled Agents Prep Course, began to face competition from a growing number of EA Prep courses and a dwindling number of entrants into the EA program.

The AIT ceased their funding of the NSTP and it was considered defunct by many in it’s first year of operations. However, after divesting themselves of AIT, both Bill Brown and Ed Henderson made the decision to resurrect what remained of the NSTP. Erik Hansen, an educator, was invited to join the NSTP. He also loaned some much needed capital to the organization and devoted time to teaching at minimal compensation. Jack Weber, a former IRS revenue officer, also became active in the organization.

Finally, at this time, Bylaws were written for the NSTP and adopted at the April 18, 1986 meeting of the Board of Directors. The board members voted in at this meeting were Erik Hansen, President; Jack Weber, Vice President; Ed Henderson, Secretary;and Bill Brown as Director at Large. Bill Brown was also voted in as Executive Director.

With the hard work of Bill Brown and Ed Henderson the organization was building its membership base through their seminar promotions. The two men credit the work and support that was provided by their wives with their ability to conduct successful seminars.

NSTP has always attributed its growth and success due to its ability to attract strong, professional leaders. The Board of Directors has always been, and continues to be, an involved working Board. As part of the Board’s ongoing commitment to the organization, they take on the following key functions:

1. review existing NSTP programs and member benefits,

2. solicit and respond to member comments, suggestions, and challenges,

3. explore new ideas for expanded and improved member benefits,

4. act as liaison with state and federal taxing authorities,

5. represent NSTP at the IRS Tax Forums, and

6. management of the NSTP national office.

Unlike many other industries, the prac-tice of tax preparation is never static. The NSTP is dedicated to providing quality and timely education, vigorous advocacy with the Internal Revenue Service and Congress, and strong support for its members in the success of their tax practices.

In the upcoming months we will look at some of the other areas in which the NSTP history has molded the organization and set the path for our future direction and growth.

NSTP CALENDARFor additional information on the

following seminars, go to our website at NSTP.org for meeting agendas, hotel loca-tions, and registration information.

June 2013:

June 10 – 14, 2013: EA Exam Prep “Boot-camp”,LasVegas

June 26 - 28, 2013: Williamsburg “Special Topics Workshop”

July 2013:

July 8, 2013: NSTP Regional Conference, Orlando

July 9 – 11, 2013: IRS Tax Forum, Orlando

July22–24,2013:NapaValley“Williams-burg in the West”

July 29, 2013: NSTP Regional Confer-ence, Dallas

July 30 – August 1, 2013: IRS Tax Forum, Dallas

August 2013:

August 5 – 9, 2013: EA Exam Prep “Boot-camp”, Chicago

August 13 – 15, 2013: IRS Tax Forum, New Orleans

August 19, 2013: NSTP Regional Confer-ence, Atlanta

August 20 – 22, 2013: IRS Tax Forum, Atlanta

August 27 – 29, 2013: IRS Tax Forum, Washington DC

September 2013:

September 9 – 13, 2013: EA Exam Prep “Bootcamp”, New York City

September 17 – 19, 2013: IRS Tax Forum, San Diego

October 2013:

October 7 – 11, 2013: EA Exam Prep “Bootcamp”, New Orleans

FEDERAL TAX ALERT PAGE 12 MARCH/APRIL 2013

Single or Head ofHousehold

Married Filing Joint (withspouse participating in employer plan or Quali�ed Widow(er)

Married Filing Joint (spouseNOT participating inemployer plan

Married Filing Seperate(whether or not spouse isparticipating in employerplan)

$58,000 or less$58,001-$67,999$68,000 or more

$92,000 or less$92,001-$111,999$112,000 or more

$173,000 or less$173,001-$182,999$183,000 or more

Less than $10,000$10,000 or more

FullPartialNone

FullPartialNone

FullPartialNone

PartialNone

Filing StatusDeduction

Modi�ed AGI

Deducting the IRA Contribution - Eligibility Chart

Greta served on the NSTP Board from 1996 until 2011 when she stepped down due to health reasons. She led the organization as President from 2009 until 2011. Her impeccable style and leadership will be missed by the NSTP Board, staff and members.

In MeMorIuM

⚑ Call for Nominees to the NSTP Board of Directors⚑

Deadline: May 5, 2013The election of two (2) members of the NSTP Board of Directors will take place in July 2013.

NSTP members considering their candidacy for the Board of Directors should be cognizant of thetime commitments which include:

Willingness to dedicate time and efforts to the direction and vision of NSTP asneeded.

A minimum of seven (7) days per year in Board meetings, either in person orwhen held by telephone.

Members of the executive committee (officers of the Board) have additionaltime requirements.

NSTP members considering candidacy for the Board should possess:

Leadership characteristics

Desire to serve the NSTP membership

Vision and desire to promote NSTP

Ability to work with others

Members of the Board of Directors are compensated for travel time and Board meetingattendance.

Candidates should send their intent to run for the NSTP Board of Directors accompanied by abrief bio and statement of goals of no more than 150 words to:

Or by mail to:NSTP 11700 NE 95th Street, Suite 100Vancouver, WA 98682

Letters of intent will be accepted from March 15, 2013 through May 5, 2013. All nominees willhave their nominations acknowledged in writing by NSTP.

NSTP Board members are required not only to abide by the NSTP member code of ethics but theNSTP Board member code of conduct as well. (Please see reverse side for Code of Conduct)

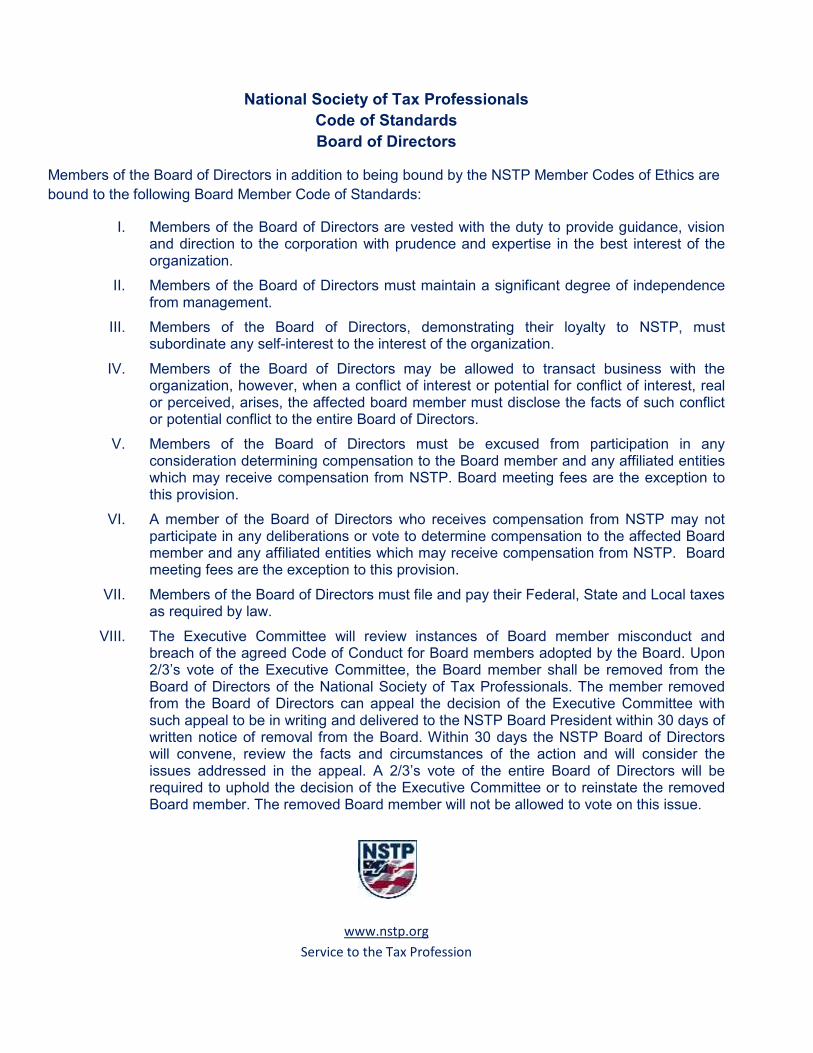

National Society of Tax ProfessionalsCode of StandardsBoard of Directors

Members of the Board of Directors in addition to being bound by the NSTP Member Codes of Ethics arebound to the following Board Member Code of Standards:

I. Members of the Board of Directors are vested with the duty to provide guidance, visionand direction to the corporation with prudence and expertise in the best interest of theorganization.

II. Members of the Board of Directors must maintain a significant degree of independencefrom management.

III. Members of the Board of Directors, demonstrating their loyalty to NSTP, mustsubordinate any self-interest to the interest of the organization.

IV. Members of the Board of Directors may be allowed to transact business with theorganization, however, when a conflict of interest or potential for conflict of interest, realor perceived, arises, the affected board member must disclose the facts of such conflictor potential conflict to the entire Board of Directors.

V. Members of the Board of Directors must be excused from participation in anyconsideration determining compensation to the Board member and any affiliated entitieswhich may receive compensation from NSTP. Board meeting fees are the exception tothis provision.

VI. A member of the Board of Directors who receives compensation from NSTP may notparticipate in any deliberations or vote to determine compensation to the affected Boardmember and any affiliated entities which may receive compensation from NSTP. Boardmeeting fees are the exception to this provision.

VII. Members of the Board of Directors must file and pay their Federal, State and Local taxesas required by law.

VIII. The Executive Committee will review instances of Board member misconduct andbreach of the agreed Code of Conduct for Board members adopted by the Board. Upon2/3’s vote of the Executive Committee, the Board member shall be removed from theBoard of Directors of the National Society of Tax Professionals. The member removedfrom the Board of Directors can appeal the decision of the Executive Committee withsuch appeal to be in writing and delivered to the NSTP Board President within 30 days ofwritten notice of removal from the Board. Within 30 days the NSTP Board of Directorswill convene, review the facts and circumstances of the action and will consider theissues addressed in the appeal. A 2/3’s vote of the entire Board of Directors will berequired to uphold the decision of the Executive Committee or to reinstate the removedBoard member. The removed Board member will not be allowed to vote on this issue.

www.nstp.orgService to the Tax Profession

Announcing NSTP’s

2013 Williamsburg Special Topics

Workshop

June 26–28, 2013Up to 18 CPE Credits Available

The 3rd Annual Ethics Session - Wednesday MorningEthics in 2013 and the Amended Circular 230 Issues

June 26, 2013 9:00am to 10:40am2 CPE Credit Hours

The 5th Annual Executive Session – Wednesday Afternoon"Introduction to the Federal Income Tax Issues of Divorced and Separated

Taxpayers"June 26, 2013 1:00pm to 5:00pm

4 CPE Credit Hours

13th Annual Williamsburg, VA Summer Special Topics Workshop"Introduction to Understanding the Federal Income Tax Issues of the Schedule K-1"

June 27, 2013 8:00am to 12:00pm4 CPE Credit Hours

“Introduction to the Fundamentals of Representing your Client in IRSCollection Issues”

June 27 1:00pm to 5:00pm – June 28th, 2013 8:00am to 12:00pm8 CPE Credit Hours

Where: Holiday Inn Patriot3032 Richmond Road *$74.00 plus 10% state/local tax and $2.00Williamsburg, VA 23185 occupancy tax per room per night757-565-2600 *Rate available from June 21 to July 1, 2013

Hotel cut off date: June 3, 2013

See registration page for pricing information. For additional details or to register onlineplease visit our website at www.nstp.org

National Society of Tax Professionals

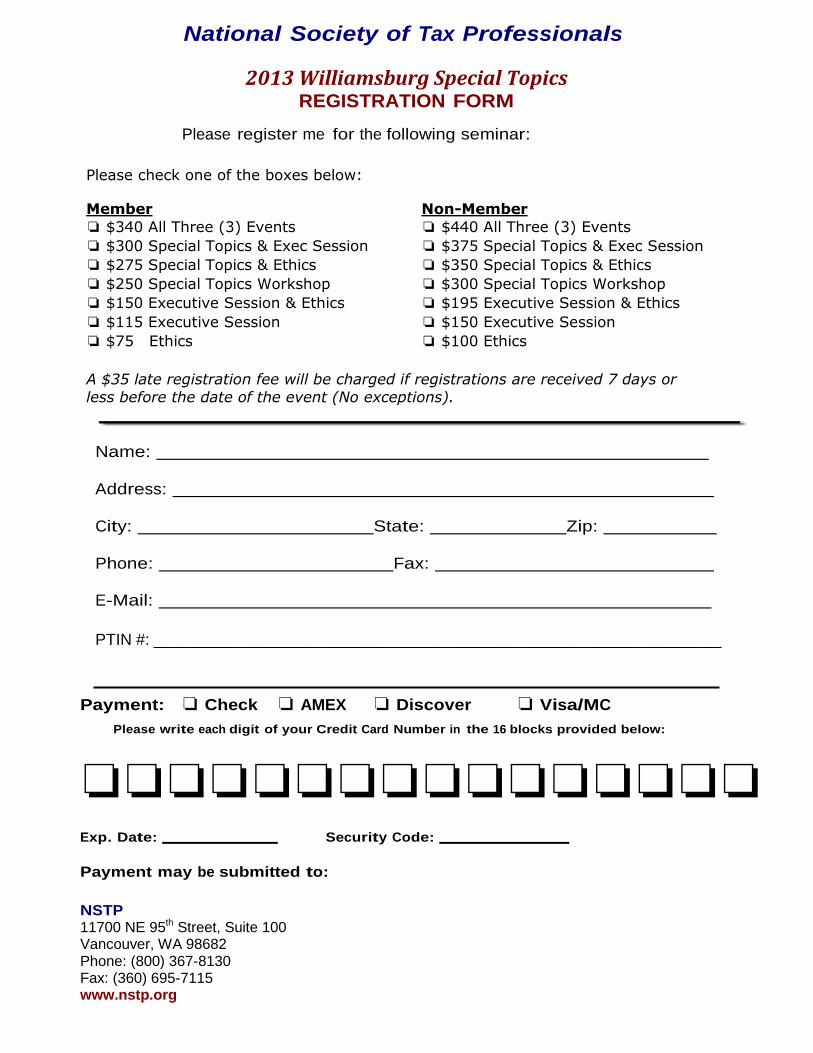

2013 Williamsburg Special Topics REGISTRATION FORM

Please register me for the following seminar:

Please check one of the boxes below: Member Non-Member

❏ $340 All Three (3) Events ❏ $440 All Three (3) Events

❏ $300 Special Topics & Exec Session ❏ $375 Special Topics & Exec Session

❏ $275 Special Topics & Ethics ❏ $350 Special Topics & Ethics

❏ $250 Special Topics Workshop ❏ $300 Special Topics Workshop

❏ $150 Executive Session & Ethics ❏ $195 Executive Session & Ethics

❏ $115 Executive Session ❏ $150 Executive Session

❏ $75 Ethics ❏ $100 Ethics

A $35 late registration fee will be charged if registrations are received 7 days or

less before the date of the event (No exceptions).

Name:

Address:

City: State: Zip:

Phone: Fax:

E-Mail:

PTIN #: ________________________________________________________________

Payment: ❏ Check ❏ AMEX ❏ Discover ❏ Visa/MC

Please write each digit of your Credit Card Number in the 16 blocks provided below:

❏❏❏❏❏❏❏❏❏❏❏❏❏❏❏❏ Exp. Date: Security Code:

Payment may be submitted to: NSTP 11700 NE 95th Street, Suite 100 Vancouver, WA 98682 Phone: (800) 367-8130 Fax: (360) 695-7115 www.nstp.org

Announcing NSTP’s

2013 West Coast Special Topics

Napa, CA

July 22–24, 2013

Up to 18 CPE Credits Available

The 3rd Annual Ethics Session - Monday MorningEthics in 2013 and the Amended Circular 230 Issues

July 22, 2013 9:00am to 10:40am2 CPE Credit Hours

The 5th Annual Executive Session – Monday Afternoon"Introduction to the Federal Income Tax Issues of Divorced and Separated

Taxpayers"July 22, 2013 1:00pm to 5:00pm

4 CPE Credit Hours

Special Topics Workshop"Introduction to Understanding the Federal Income Tax Issues of the Schedule K-1"

July 23, 2013 8:00am to 12:00pm4 CPE Credit Hours

"Introduction to the Fundamentals of Representing Your Client in IRSCollection Issues"

July 23, 2013 1:00pm to 5:00pm – July 24, 2013 8:00am to 12:00pm8 CPE Credit Hours

Where: Embassy Suites Napa Valley1075 California Blvd. *Room Rate: *$179.00 per nightNapa, CA 94559 *Rate available from July 21-23, 20131-800-EMBASSY (1-800-362-2779) Hotel cut off date: June 18, 2013

Group Code: NST or mention National Society of Tax Professionals

See registration page for pricing information. For additional details or to register onlineplease visit our website at www.nstp.org

National Society of Tax Professionals

2013 West Coast Special Topics (Napa Valley) REGISTRATION FORM

Please register me for the following seminar:

Please check one of the boxes below: Member Non-Member

❏ $425 All Three (3) Events ❏ $525 All Three (3) Events

❏ $375 Special Topics & Exec Session ❏ $450 Special Topics & Exec Session

❏ $350 Special Topics & Ethics ❏ $425 Special Topics & Ethics

❏ $300 Special Topics Workshop ❏ $350 Special Topics Workshop

❏ $200 Executive Session & Ethics ❏ $250 Executive Session & Ethics

❏ $150 Executive Session ❏ $185 Executive Session

❏ $75 Ethics ❏ $100 Ethics

A $35 late registration fee will be charged if registrations are received 7 days or

less before the date of the event (No exceptions).

Name:

Address:

City: State: Zip:

Phone: Fax:

E-Mail:

PTIN #: ________________________________________________________________

Payment: ❏ Check ❏ AMEX ❏ Discover ❏ Visa/MC

Please write each digit of your Credit Card Number in the 16 blocks provided below:

❏❏❏❏❏❏❏❏❏❏❏❏❏❏❏❏ Exp. Date: Security Code:

Payment may be submitted to: NSTP 11700 NE 95th Street, Suite 100 Vancouver, WA 98682 Phone: (800) 367-8130 Fax: (360) 695-7115 www.nstp.org