Embed Size (px)

Citation preview

The Federal Tax alerT [email protected] july / augusT 2017 1

In This IssueIn The newsNews from the IRS .............1

PRACTICe MAnAGeMenTaICPa updates guidelines for TPCs-1 ............................3

When to apply the ‘Cohan rule’ .........................5

FRoM The BenChIrs disregards Court ruling on ‘Placed in service’ ................6

Taxpayer Failed to substantiate sufficient hours to be a real estate Professional ........................10

eTCeTeRAunderstanding who is an employee vs. Independent Contractor .........7

InFoRMATIonTax helpline .........................2NsTP Member Benefits ..........4NsTP Calendar .....................5

NaTIONal sOCIeTy of Tax PrOFessIONals

Federal Tax Alertjuly / august 2017

the

continued on page 8

IRs office of Appeals Pilots Virtual serviceThe Internal Revenue Service Office of Appeals will soon pilot a new web-based virtual conference option for taxpayers and their representatives. This virtual face-to-face option will provide an additional option for taxpayer conferences. The IRS expects it to be especially useful for taxpayers located far from an IRS Appeals office.

Each year, the Office of Appeals hears ap-peals of more than 100,000 taxpayers at-tempting to resolve their tax disputes without going to court. Currently, taxpayers involved in the appeals process can meet with an Ap-peals Officer by phone, in person or virtually through video-conference technology available only at a limited number of IRS offices.

While a phone call works well for most taxpayers, others prefer face-to-face interaction. Appeals’ pilot program will use a secure, web-based screen-sharing platform to connect with taxpayers face-to-face from anywhere they have internet access. Similar to popular screen-sharing programs used on phones and home computers, this technology may also be a way for the IRS to provide greater access, efficiency and flexibility to taxpayers. This web-based model is more convenient and has more features than the existing video-conferencing technology.

“Taxpayers who choose the web-based option will be able to get face-to-face service remotely,” said IRS Chief, Appeals Donna Hansberry. “In the future, the technology may give taxpayers greater options in engaging with Appeals and could allow us the flexibility to serve taxpayers virtually from any location using mobile devices or computers.

“We hope this is one more option to enable IRS employees to provide timely, efficient and effective service to taxpayers,” said Hansberry.

Appeals plans to start the pilot August 1, 2017 and will assess the results, including taxpayer satisfaction with the technology.

The IRS reminds taxpayers that their right to appeal an IRS decision in an independent forum is one of 10 key rights guaranteed to taxpayers under the Taxpayer Bill of Rights. Other rights especially relevant to the appeals process include the right to quality service, the right to pay no more than the correct amount of tax, the right to challenge the IRS’s position and be heard and the right to retain representation.

exam Fee to Increase for special enrollment exam (see)“Enrolled agents” are tax specialists authorized by the IRS to represent taxpayers in tax disputes in many of the same ways as tax attorneys and CPAs. To obtain an “enrolled agent” designation, an applicant must pass an IRS competency examination. In July 2017, the IRS issued a new regulation increasing the user fee applicants must pay to take the examination. Under the new regulation, applicants must pay two fees for each portion of the three-part examination– (1) an $81 fee imposed by the IRS for each portion of the examination, and (2) a $100+ fee for each portion imposed by the contractor retained by the IRS to administer the examination. Combined, applicants will now be required to pay fees of $243 (previous fee was $33) to the IRS and over $300 to the contractor to take all three of the required exams.

During the rulemaking process, the IRS justified the fee increase by reference to its internal cost estimates for the enrolled agent examination. The IRS identified three principal components to the cost estimates— (1) an estimate of the IRS employee time which was devoted to the enrolled agent examination, (2) the direct cost of the employee labor, employee benefits, and a 68% overhead factor, and (3) the cost of conducting background checks on the contractor hired by IRS to administer the examination.

news from the IRs

ReGIsTeR now!

FAll UPdATe seMInARs &

GRAnd eVenTsComing to a city near you!

See the enclosed brochure

for complete schedule and

registration information

EA BOOT CAMP

REgisTRATiON ON

PAgE 12

2 july / augusT 2017 [email protected] The Federal Tax alerT

Technical Tax advice provided by NSTP Helpline staff is based upon specific information conveyed by the member. Members should take special care in relying upon recommendations and opinions that reflect the understanding of the Helpline staff member. NSTP and the Helpline staff are not responsible for misapplication of information given. Members are responsible for the ultimate verification and application of any information provided by NSTP.

NOTICe • TAX helPlIne • dIreCT lINe: 360-695-0556

JAnUARy 16 – JAnUARy 31

Monday–Friday

9:00 aM – 2:00 PM Pst 10:00 aM – 3:00 PM Mst 11:00 aM – 4:00 PM Cst 12:00 PM – 5:00 PM Est

FeBRUARy 1 – APRIl 15

Monday, Tuesday & Thursday

6:00 aM – 2:00 PM Pst 7:00 aM – 3:00 PM Mst 8:00 aM – 4:00 PM Cst 9:00 aM – 5:00 PM Est

February 2 – 5, 2016

wednesday & Friday

9:00 aM – 5:00 PM Pst 10:00 aM – 6:00 PM Mst 11:00 aM – 7:00 PM Cst 12:00 PM – 8:00 PM Est

February 2 – 15, 2016

saturday

8:00 aM – 12:00 PM Pst 9:00 aM – 1:00 PM Mst 10:00 aM – 2:00 PM Cst 11:00 aM – 3:00 PM Est

APRIl 16 – JAnUARy 13

Monday, wednesday & Friday

9:00 aM – 2:00 PM Pst 10:00 aM – 3:00 PM Mst 11:00 aM – 4:00 PM Cst 12:00 PM – 5:00 PM Est

The Federal Tax Alert is published 6 times a year by the National society of tax Professionals.

MAIlInG AddRess: the Federal tax alert 11700 NE 95th st., suite 100 Vancouver, Wa 98682

TelePhone: 800-367-8130

edIToRs:

Paul la Monaca, CPa, [email protected]

Nina tross, MBa, Ea [email protected]

sUBsCRIPTIon seRVICes:

Delta [email protected]

Opinions expressed in The Federal Tax Alert are those of the editors and contributors.

Refer 3 and get One Year FREE!Refer 3 new Full Members to NstP and receive your next year’s dues absolutely FREE! When you refer a new member, make sure they mention your name as their referral so that we can give you credit. When you have referred three new Full Members, you will receive your next year’s membership FREE.

from the edIToRs

when you call the nsTP helPlIne, either you will reach a live person or you will be placed on hold in the queue. The system will disconnect after 5 minutes and you will be prompted to leave a message. within 24-48 hours after submitting your question, a nsTP helPlIne worker will contact you. Please leave your message — yoUR CAll wIll Be ReTURned.

Nina Tross, MBA, EAnina Tross, MBA, eA

Paul La Monaca, CPA, MSTPaul la Monaca, CPA, MsT

So much is happening with the Trump Administration it is difficult to keep up with the proposed changes to the tax code and the Affordable Care Act. However, as tax professionals we must keep in mind that the Affordable Care Act is the law of the land and compliance is based on current law. Your editors are monitoring the ongoing debate and will report once a compromise has been voted on by Congress and signed by the President. Otherwise, in the meantime, it is just conjecture and rumor.

In a recent press conference with Commissioner Koskinen at the Dallas IRS Tax Forum, issues such as the Security Summit, private collection companies, new trends, and the delays in refunds legislated in the PATH Act were discussed.

The IRS is encouraged by the actions undertak-en in reducing the incidence of identity theft and refund fraud. They have seen a substan-tial drop in the number of incidents quoting statistics from the 1st five months of the past three tax filing season. In 2015 the number of incidents was approximately 297,000. 2016 saw a drop to 204,000 incidents and a further drop in the 2017 tax filing season to 107,000 incidents. The public is more aware of the scams and tax fraud and coupled with the IRS efforts to stem refund fraud they are making significant progress in stemming the incidents of individual income tax fraud. Unfortunately, the IRS is now seeing an increase in business related tax fraud and are working to eliminate the incident of corporate tax fraud.

When asked where to file complaints against abusive tactics by the newly retained private collection companies, the response was to file a complaint with the Federal Trade Commission.

While the IRS has been busy shutting down the portals for the criminals perpetuating the tax fraud, the criminals have been busy developing new ways to hack into the federal and state tax systems. One method was to send an email to a company CEO or payroll department

asking them to send the employee year end listing which includes the Form W2 and other personnel information. This scam has been successful with over 200 companies employing thousands of employees. The fraudsters are also using the same tactics to obtain information from mortgage companies and banks.

The IRS will be implementing multi-factor au-thentication for those attempting to access the online services available through IRS.gov. This includes using the cell phone number, email and financial information which is verifiable through the credit reporting agencies. When utilizing the IRS systems for balance dues, installment payments or Offer in Compromise, the taxpayer must use the multi-factor authen-tication to access the taxpayer accounts.

And finally, when questioned on the success of the expedited filing of Forms W2’s and 1099-Misc for nonemployee compensation, Koskinen noted that approximately $50 billion in tax refunds was released on February 16, 2017 and suspicious returns were moved out of the queue for additional review.

Cell phone authentication can now be set up for a family plan or business account by mail. When accessing the online secure system, if the cell phone number is not in your name then authentication can be obtained by mail with a pin issued to access the online services.

The NSTP staff and Board has been busy with the summer series of Destination Education Seminars and the IRS Tax Forums. We will soon be starting up the series of Federal Tax Update Seminars which begin in Cheyenne Wyoming in early November. See the complete schedule in the enclosed circular or on page 11 of the Federal Tax Alert. You can also go online to NSTP.org to see the full schedule of classes, locations and registration information.

And finally, we are thrilled to see you all at the IRS Tax Forums—be sure to stop by and visit as you attend the remaining Forums in Washington, DC, Las Vegas and San Diego.

The Federal Tax alerT [email protected] july / augusT 2017 3

The AICPA Tax Division issues Tax Policy Concept Statements for general information and guidance. They are intended to be used in the development of tax legislation

for the benefit of the public interest. The issues addressed in Tax Policy Concept Statement No. 1, Guiding Principles of Good Tax Policy: A Framework for Evaluating Tax Proposals, recently updated by the AICPA, are intended to recognize the challenges of protecting taxpayer information as we endeavor to keep pace with technical developments and tax administration in a global economy.

To this end two new principles were added: Principle 5, Information Security, and Principle 11, Accountability to Taxpayers. The title of Principle 4 was also changed from Economy in Collection to Effective Tax Administration.

TPCS-1 contains the following 12 Guiding Principles, the first four of which are the maxims of taxation published by the economist Adam Smith in his 1776 work, The Wealth of Nations. The full text of the 12 Guiding Principles can be found on the AICPA website (www.aicpa.org):

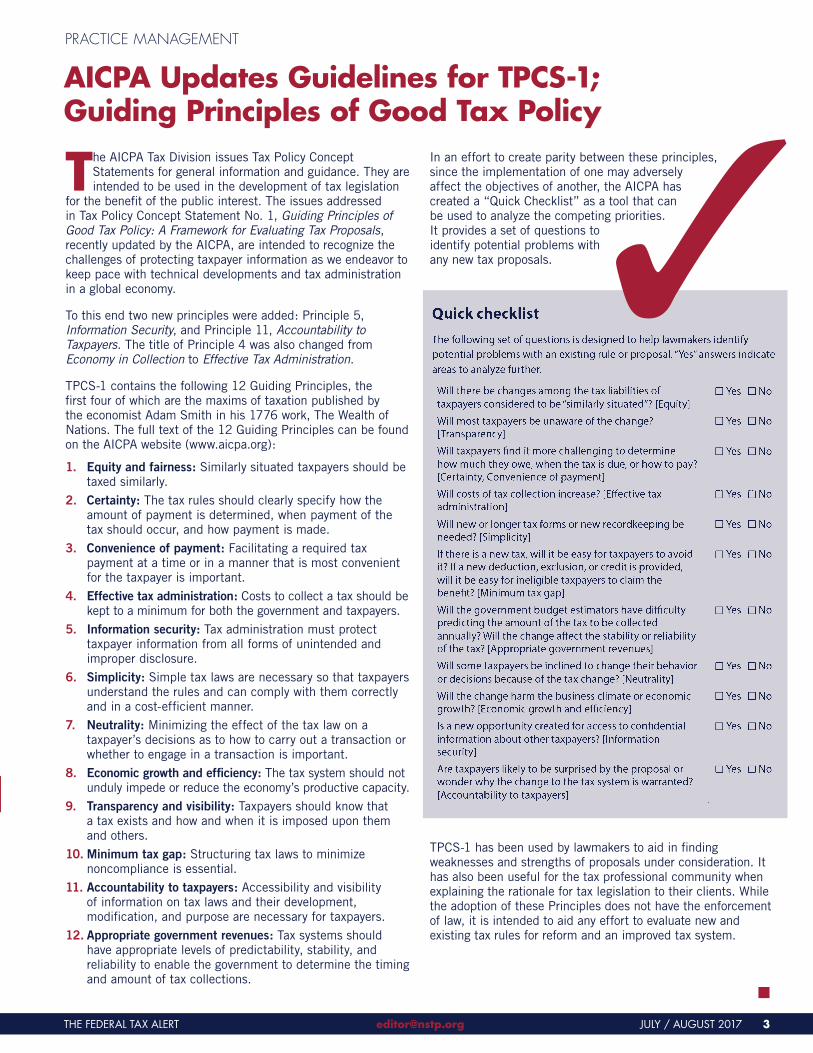

1. Equity and fairness: Similarly situated taxpayers should be taxed similarly.

2. Certainty: The tax rules should clearly specify how the amount of payment is determined, when payment of the tax should occur, and how payment is made.

3. Convenience of payment: Facilitating a required tax payment at a time or in a manner that is most convenient for the taxpayer is important.

4. Effective tax administration: Costs to collect a tax should be kept to a minimum for both the government and taxpayers.

5. Information security: Tax administration must protect taxpayer information from all forms of unintended and improper disclosure.

6. Simplicity: Simple tax laws are necessary so that taxpayers understand the rules and can comply with them correctly and in a cost-efficient manner.

7. Neutrality: Minimizing the effect of the tax law on a taxpayer’s decisions as to how to carry out a transaction or whether to engage in a transaction is important.

8. Economic growth and efficiency: The tax system should not unduly impede or reduce the economy’s productive capacity.

9. Transparency and visibility: Taxpayers should know that a tax exists and how and when it is imposed upon them and others.

10. Minimum tax gap: Structuring tax laws to minimize noncompliance is essential.

11. Accountability to taxpayers: Accessibility and visibility of information on tax laws and their development, modification, and purpose are necessary for taxpayers.

12. Appropriate government revenues: Tax systems should have appropriate levels of predictability, stability, and reliability to enable the government to determine the timing and amount of tax collections.

In an effort to create parity between these principles, since the implementation of one may adversely affect the objectives of another, the AICPA has created a “Quick Checklist” as a tool that can be used to analyze the competing priorities. It provides a set of questions to identify potential problems with any new tax proposals.

TPCS-1 has been used by lawmakers to aid in finding weaknesses and strengths of proposals under consideration. It has also been useful for the tax professional community when explaining the rationale for tax legislation to their clients. While the adoption of these Principles does not have the enforcement of law, it is intended to aid any effort to evaluate new and existing tax rules for reform and an improved tax system.

PrACtICe mANAGemeNt

AICPA Updates Guidelines for TPCs-1; Guiding Principles of Good Tax Policy

n

4 july / augusT 2017 [email protected] The Federal Tax alerT

from the nsTP BoARd PResIdenT

Keith E. Huebel, CPAKeith e. huebel, CPA NSTP President of the Board

• Tax Helpline: our members are never charged a fee for use of the Tax Helpline regardless of the number of times you contact us.

• NSTP Dividend Reward Points: Dividend reward points are earned each time you make a purchase with NSTP whether membership, live events, self-study or materials. Dividend points are automatically deposited into your rewards account and accumulated for you. One dividend point is earned for every dollar spent with NSTP. The dividend points never expire as long as your membership in NSTP continues. Your dividend points can then be “spent” on CPE courses and other educational materials. When you don’t have enough points to qualify to receive your entire course for free, you can purchase the rest of the credits at a specified per credit hour rate. This purchase also earns dividend reward points and your rewards account keeps growing!

• Federal Tax Alert technical newsletter (6 Issues)

• Tax Client Newsletter (3 Issues). Brand with your own logo and send to your customers

• Weekly Update email (52 issues) keeps you current and up-to-date

• Federal Tax Update Seminars across the country at member rate to prepare for the upcoming tax season, including ACA information

• Webinars with CE credits: members get reduced price

• Member rate for Ethics, Special Topics and Executive Session Workshops in Williamsburg, VA and Napa, CA

• NSTP Tax Research Service: member rate for expanded research services. You will be provided with a written report including tax sources, tax code and tax law cites as appropriate

• Professional Liability Insurance at group rates

• Beautiful Membership Certificate (suitable for framing) acknowledging your membership in the National Society of Tax Professionals

Are you Aware of your

nsTP Member Benefits?

First and foremost, on behalf of the Board of Directors and Office Team of NSTP, I’d like to thank everyone who voted this year for the 2018 Board applicants. Some say, “...my vote doesn’t count...”, but this year it surely did. Two of the three Board openings were filled and the third opening resulted in a tie between two applicants. This is the first time in NSTP history a tie resulted. In year’s past, voting has been as narrow as a one or two vote difference. Your vote counts and surely makes a difference. Always vote when asked!

NSTP has established the process for the run-off election and members can go to the Member area at NSTP.org for the bios of the two candidates and the voting instructions. I’m encouraged by the participation already for the run-off voting. Please review NSTP emails, Tax Tidbits or the NSTP website (Member’s Only section—www.NSTP.org) for run-off information, bio’s or voting procedures. Voting closes midnight September 11, 2017. Vote Now! and make your voice heard and count. Positions are effective January 2018 for a three year term. A special THANK YOU is also sent to all those who submitted bio’s to run for the Board of Directors. Your talents and interest in helping steer the NSTP ship for the next three years have certainly been recognized. Please consider furthering your interests by volunteering to participate in one of NSTP’s committees. We want to hear from you: [email protected]. Also, keep your bio’s updated and consider running again next year. Two positions open yearly for each of two years and three positions open the third year. This pattern cycles every three years.

That said, I hope everyone is enjoying their summer and the slower “Tax Season” (April 16 to January 1). Whether you are a part-time tax preparer or a year-round preparer, you need a break to refresh. I encourage each of you to take a breather from the hustle and bustle and relax. Take time for yourself—it does wonders for the body, mind and soul. For those that tied their break time into one or more of the NSTP’s destination seminars this year; Cabo San Lucas, MX in May,

Williamsburg, VA in June or Napa Valley, CA in July, THANK YOU! You returned home relaxed AND you made 2017 one of NSTP’s most successful years. We heard many accolades from the participants and they are still coming in. Relaxing fun times while educating yourselves...and deductible to boot. A WIN WIN!! Book NOW for next year and save. If you are tying-in your break with one of the 2017 IRS National Tax Forums, kudos to you as well. It’s another smart choice. Continuing Education mixed with nice destinations. NSTP speakers present each day at all the IRS Forums and we staff a vendor booth or table all three days

at each Forum location. Please stop by to say Hi!

Before you know it, summer will be history and the Fall season will shine upon us. That means nothing other than September 15th and October 15th deadlines and yes, preparing for Tax Season 2018. Check NSTP’s website for all our Fall 2017 update seminars: www.nstp.org/education. Early-Bird discounts are available now.

I close with one more THANK YOU! It is sent to all those members who signed up for, and reaped the incredible benefits of, NSTP’s “Executive

Membership” program. In May, we celebrated our first anniversary of this great program. The program, participation and benefits are ever-growing. Check it out to be the best tax preparer you can be and at the least cost. Chartered “Executive Memberships” are available only for a little while longer: www.nstp.org/Membership/executive.

NSTP has been serving you since 1985 and will continue to be here to see you successfully through your retirement and the generations to follow. The National Society of Tax Professionals is The Premier Choice for Tax Professionals.

I encourage each of you to take a breather from the hustle and bustle and relax. Take time for yourself—it does wonders for the body, mind and soul.

The Federal Tax alerT [email protected] july / augusT 2017 5

The “Cohan Rule” refers to the deci-sion in the federal court case Cohan

vs. Commissioner, 39 F. 2d 540 (2d Cir. 1930). This case resulted from one of the very first IRS audits. The IRS disal-lowed Cohan’s deductions for business travel citing Internal Revenue Code Sec-tion 162. Under IRC 162 a taxpayer must establish that an expense was (1) paid or incurred for (2) business or profit-orient-ed purposes and (3) the amount spent.

Fred W. Daily explains the situation in his copyrighted article “Getting Audited? Can’t Find All of Your Records? No Problem.”

“The IRS took the position with Mr. Cohan that even if he could convince an auditor that the business expense qualified for a deduction (satisfy num-ber 1 and 2), that he also must be able to fully document the amount spent (number 3). George replied that he was always on the run, and had little time to document many of his expenses. George challenged the IRS stringent re-cord keeping requirements in court. His lawyers argued that the IRS was wrong because even though records were missing, George had presented other credible evidence of the amount of the expenses on which approximations of the true amounts could be made.

George had explained the necessity of the (undocumented) expenses and offered his recollections and approxi-mations of the amounts incurred. The items ran from cab rides and tips to large hotel and restaurant expenses for George and his entourage. The Federal Appeals Court, in an opinion by the aptly named Judge Learned Hand, held that the sums were allowable business expenses. It was unreason-able of the IRS not to allow, at least some of his earnings, not to be based on Cohan’s approximations.”

Another FYI—Judge Learned Hand is the author of the famous quote: “Anyone may arrange his affairs so that

his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one’s taxes. Over and over again the Courts have said that there is nothing sinister in so arranging affairs as to keep taxes as low as possible.

Everyone does it, rich and poor alike and all do right, for nobody owes any public duty to pay more than the law demands.”

What the Cohan ruling says is that since GMC travelled the country to produce and appear in theatrical productions, which was public knowledge via programs and newspaper accounts, it is reasonable and appropriate to assume that he must have incurred certain deductible expenses.

In the production of his plays, Cohan asserted he was obliged to entertain actors, employees, and dramatic critics. He also had to travel a lot, often with his attorney. These expenses amounted to substantial sums, but he had no accounting of these expenses.

At the trial, in 1930, Cohan estimated that he had spent $11,000 during the first six months of 1921; $21,000 be-tween July 1, 1921, and June 13, 1922; and around the same amount for the fol-lowing fiscal year – $55,000 in all. The IRS had refused to allow him to claim any part of this based on the grounds that it was impossible to tell how much he had spent, in the absence of any ac-counting records.

But the 2nd US Circuit Court of Ap-peals questioned how far the refusal of the deductions were justified because it was obvious that Cohan had spent large amounts. In the absence of substantia-tion, the court made reasonable approxi-mations of other deductions. Thus, the “Cohan rule” was born.

Under the Cohan rule if there is no documentation, but other evidence clearly indicates that some deduction should be allowed, the court may come up with its own estimate. As the Fifth Circuit held, “if a qualified expense occurred,...the court should estimate the expenses associated with those activities.” To use the Cohan Rule, the taxpayer must have some sort of basis for using it—whether it is supported by testimony or other independent form of substantiation.

Over the years Congress has, by statute, required more detailed documentation for certain types of expenses in order for a deduction to be allowed—such as business travel and entertainment, business gifts, listed property (autos,

computers, cell phones, and certain entertainment property), and, most recently, charitable contributions.

The Cohan Rule is still alive and well today. It is seen as an antidote to the auditor who says, “no deduction without documentation.” However, acceptance of the Cohan Rule approximations is always discretionary with a court; a taxpayer is not automatically entitled to make an approximation in a tax matter. The IRS must be shown, by oral or written statements or other supporting evidence, a foundation on which a reasonable approximation can be based. And, as a practical matter, when raising Cohan, expect a compromise, rather than a full allowance of the approximated expenses. Never hesitate to bring up the Cohan Rule at any stage of an audit, appeal or court proceeding.

Despite the fact that this “out” exists, the general rule is that it is not to be used as an excuse not to keep good contemporaneous records and maintain detailed documentation of all your business expenses.

PrACtICe mANAGemeNt

For information on NstP classes and events, go to nsTP.org and click ‘Education’.

August 22 – 24, 2017IRs Tax Forum National Harbor (DC), MD

August 27 – 28, 2017The Ugly 1040 • las Vegas, NV

August 29 – 31, 2017IRs Tax Forum • las Vegas, NV

september 12 – 14, 2017IRs Tax Forum • san Diego, Ca

october 23 – 27, 2017eA Boot Camp • las Vegas, NV

May 21 – 25, 2018eA Boot Camp • Nashville, tN

when to Apply the ‘Cohan Rule’Posted by Robert D. Flach, The Wandering Tax Pro, November 17, 2009

n

Register today at nsTP.org

2017 nsTP CAlendAR

6 july / augusT 2017 [email protected] The Federal Tax alerT

In Stine, the United States District Court for the Western District of

Louisiana considered whether a building that was substantially completed but not yet open for business could be considered ’placed in service’ for the purposes of beginning depreciation. The building in question was located in a Gulf Opportunity Zone, an area designated for special tax treatment due to impact by hurricanes Katrina and Rita. Under section 1400N(d)(1)(A), the building would qualify for 50 percent bonus depreciation, but only if the building was deemed to be placed in service prior to December 31, 2008. Though substantially completed with a certificate of occupancy, the store was not yet open to the public.

Stine, LLC is a retail operation that, among other things, sells home building material and supplies. It began construction of two new retail stores in 2007. As of December 31, 2008, both stores had been issued certificates of occupancy which allowed them to receive equipment, shelving, racks and

from the BeNCh

IRs disregards Court Ruling on ‘Placed in service’Stine, LLC v. United States, No. 13-03224, 2015 WL 403146 (W.D. La. Jan. 27, 2015)

merchandise, as well as allowed the appropriate personnel to install and/or stock those items. However, the stores were not yet open for business on December 31, 2008, and the certificates of occupancy did not allow customers to enter the buildings.

In 2005, Congress enacted the “Gulf Opportunity Zone Act of 2005” (GO Zone Act, P.L. 109-135, 12/21/2005), intending, among other provisions tax incentives, to encourage rebuilding of the areas ravaged by Hurricane Katrina (as well as Hurricanes Rita and Wilma). One of these incentives allowed qualifying taxpayers to claim 50% bonus first-year depreciation for “GO Zone property.” This consisted of qualifying types of property (including nonresidential real property or residential rental property) that met the following requirements:

…Substantially all of the use of the property was (a) in the GO Zone and (b) in the active conduct of a trade or business by the taxpayer in the GO Zone.

…The original use of the property in the GO Zone began with the taxpayer after Aug. 27, 2005.

…The property was acquired by the taxpayer after Aug. 27, 2005 and no written binding contract for the acquisition was in effect before Aug. 28, 2005.

…The property, generally, was “placed in service” by the taxpayer before Jan. 1, 2008, or before Jan. 1, 2009 in the case of nonresidential real property and residential rental property, but later deadlines apply to certain property used in highly damaged portions of the GO Zone. (Code Sec. 1400N(d)(2), Code Sec. 1400N(d)(6))

Determining the date property is placed in service for depreciation purposes requires ascertaining from the relevant facts and circumstances: (1) the prop-erty’s specifically assigned function, and (2) when the property is in a condition or state of readiness and availability for

continued on page 7

The Federal Tax alerT [email protected] july / augusT 2017 7

Placed in service continued from page 6

n

etCeterA

A TimeLy Tip from eNNiS T. peA

Understanding who is an employee vs. Independent ContractorTo better determine how to properly classify a worker, consider these three categories: Behavioral Control, Financial Control and Relationship of the Parties.

BEHAVIORAL CONTROL: A worker is an employee when the business has the right to direct and control the work performed by the worker, even if that right is not ex-ercised. Behavioral control categories are:• Type of instructions given, such as

when and where to work, what tools to use or where to purchase supplies and services.

• Degree of instruction, more detailed instructions may indicate that the worker is an employee. Less detailed instructions reflect less control, indicating that the worker is more likely an independent contractor.

the specifically assigned function. (Reg. § 1.167(a)-11(e)(1)) The same framework applies to determine the date property is placed in service for purposes of the in-vestment tax credit under Code Sec. 46. (Reg. § 1.46-3(d)(1)(ii))

The IRS argued that the store, if not open for business, could not be placed in service for the purpose of beginning depreciation. The court refused to accept the use of the opening date to the public as a bright-line rule, acknowledging that in some cases commercial buildings are actually used at a point before they are open to the public. The court further found that case law showed instances when a building was technically open for business and functioning, but not placed into service for the purpose of depreciation until some refurbishments had been completed.

The Stine court concluded by stating its rule: “The building is placed in service when it is substantially complete

meaning in a condition of readiness and availability to perform the function for which it was built—in this instance to house and secure racks, shelving and merchandise.”

According to IRS, the district court erred first by holding that Stine’s intended use for the buildings was to “house and secure racks, shelving and merchandise.” The threshold determination in a placed in service analysis is to identify the specifically assigned function of the property in the context of the taxpayer’s trade or business (Sealy Power, Ltd., (CA 5 1995) 75 AFTR 2d 95-1213; Brown, TC Memo 2013-275), and in this case, Stine intended to use the buildings as retail stores.

Second, the court erred by failing to observe the regulatory requirement that property is placed in service when it is in a condition or state of readiness and availability for its specifically assigned function—i.e., ready and available for

regular operation and income-producing use. (Reg. § 1.46-3(d)(1)(ii); Armstrong World Industries, Inc., TC memo 1991-326; Piggly Wiggly Southern, Inc., (1985) 84 TC 739) IRS cited a number of Tax Court cases and prior IRS guidance involving electric power plants to illustrate the meaning of “regular operational use for income production,” including Rev Rul 76-428, 1976-2 CB 47 and Rev Rul 76-256, 1976-2 CB 46, which set out five factors to determine whether a plant is ready and available for regular operation.

The IRS has issued the Action on Decision (AOD) on page 6 (at left).

Therefore, the IRS will continue to take the position that that a retail store is placed in service for depreciation purposes when the building is ready and available to function as a retail store (the intended use of the building) at which time it is open to the public.

• Evaluation systems to measure the de-tails of how the work is done points to an employee. Evaluation systems measuring just the end result point to either an in-dependent contractor or an employee.

• Training a worker on how to do the job—or periodic or on-going training about procedures and methods—is strong evidence that the worker is an employee. Independent contractors ordinarily use their own methods.

FINANCIAL CONTROL: Does the business have a right to direct or control the financial and business aspects of the worker’s job? Consider:• Significant investment in the equipment

the worker uses in working for someone else.

• Unreimbursed expenses, independent contractors are more likely to incur unreimbursed expenses than employees.

• Opportunity for profit or loss is often an indicator of an independent contractor. If a worker has a significant investment in the tools and equipment used and if the worker has unreimbursed expenses, the worker has a greater opportunity to lose money (i.e., their expenses will exceed their income from the work). Having the possibility of incurring a loss indicates that the worker is an independent contractor.

• Services available to the market. Independent contractors are generally free to seek out business opportunities.

• Method of payment. An employee is generally guaranteed a regular wage amount for an hourly, weekly, or other

period of time even when supplemented by a commission. However, independent contractors are most often paid for the job by a flat fee or agreed upon price for the contract.

RELATIONSHIP: The type of relationship depends upon how the worker and business perceive their interaction with one another. This includes:• Written contracts which describe the

relationship the parties intend to create. Although a contract stating the worker is an employee or an independent contractor is not sufficient to determine the worker’s status.

• Benefits. Businesses providing employee-type benefits, such as insurance, a pension plan, vacation pay or sick pay have employees. Businesses generally do not grant these benefits to independent contractors.

• The permanency of the relationship is important. An expectation that the relationship will continue indefinitely, rather than for a specific project or period, is generally seen as evidence that the intent was to create an employer-employee relationship.

• Services provided which are a key activity of the business. If a worker provides services that are a key aspect of the business, it is more likely that the business will have the right to direct and control his or her activities. For example, if a law firm hires an attorney, it is likely that it will present the attorney’s work as its own and would have the right to control or direct that work. This would indicate an employer-employee relationship.

n

8 july / augusT 2017 [email protected] The Federal Tax alerT

continued on page 9

news from the IRs ...continued from page 1

secure Access: how to Register for Certain online self-help ToolsTo better protect taxpayers, the IRS recently upgraded its identity verification process for certain online self-help tools. The purpose is to prevent taxpayer impersonations and account takeovers by identity thieves. Because the Secure Access Authentication platform is more rigorous, it helps if you prepare to register in advance.

Currently, the Secure Access Authentication process applies to the Get Transcript Online, Get an IP PIN and your tax account tools.

Here’s what new users need to get started:• A readily available email address;• Your Social Security number;• Your filing status and address from

your last-filed tax return;• Your personal account number from a:

credit card, orhome mortgage loan, orhome equity (second mortgage) loan, orhome equity line of credit (HELOC), orcar loan (The IRS does not retain this data)

• A readily available mobile phone. Only U.S-based mobile phones may be used. Your name must be associated with the mobile phone account. Landlines, Skype, Google Voice or similar virtual phones as well as phones associated with pay-as-you-go plans cannot be used;

• If you have a “credit freeze” on your credit records through Equifax, it must be temporarily lifted before you can successfully complete this process.

The card cannot be American Express, a debit card or a corporate card issued in your name by your company or organization.

Because this process involves verification using financial records, there may be a “soft inquiry” placed on your credit report. This notice does not affect your credit score. The IRS does not retain your financial account information.

NoTe: If you have a pay-as-you-go mobile phone or a business/family plan

mobile phone not associated with your name, you may request that we mail an activation code to the address we have on file for you. You still must have a text-enabled, U.S.-based phone to receive a security code text that completes the validation process and allows returning users to access their accounts.

First-time users of any Secure Access-supported tool must:• Submit name and email address to

receive a confirmation code;• Enter the emailed confirmation code;• Provide SSN, date of birth, filing

status and address on the last filed tax return;

• Provide some financial account information for verification such as the last eight digits of their credit card number or car loan number or home mortgage account number or home equity (second mortgage) loan number or home equity line of credit;

• Enter a mobile phone number to receive a six-digit activation code via text message OR request an activation code by mail (see below);

• Enter the activation code sent to mobile phone;

• Create username and password, create a site phrase and select a site image.

First-time users who opt for an Activation Code by Mail must:• Select Activation Code by Mail when

prompted;• Create username and password, create

a site phrase and select a site image;• Allow 5 to 10 days for mail delivery of

the activation code;• Return to the self-help tool and enter

your username and password;• Enter the activation code at the

prompt;• Enter number for any type of text-

enabled phone at the prompt; this may include a pay-as-you-go mobile phone or a business/family plan mobile phone not associated with your name;

• Check phone for a security code text;• Enter the security code text at the

prompt to complete the Secure Access validation process.

Returning users with existing credentials but new to Secure Access must:

• Log in with an existing username and password;

• Submit financial account information for verification, for example, the last eight digits of a credit card number or car loan number or home mortgage account number or home equity (second mortgage) loan account number;

• Submit a mobile phone number to receive an activation code via text OR request an activation code by mail (see above);

• Enter the activation code.

Returning users who previously complet-ed the Secure Access process must:• Log in with an existing username and

password;• Receive a security code text via mobile

phone provided during account set up;• Enter the security code into secure

access.

defend Against RansomwareThe Internal Revenue Service, state tax agencies and the tax industry are warning tax professionals that ransomware attacks are on the rise worldwide as bad actors here and abroad infiltrate computer systems and hold sensitive data hostage.

The IRS is aware of a handful of tax practitioners who have been victimized by ransomware attacks. The Federal Bureau of Investigation recently cautioned that ransomware attacks are a growing and evolving crime threatening the private and public sectors as well as individuals.

Ransomware is a type of malware that infects computers, networks and servers and encrypts (locks) data. Cybercriminals then demand a ransom to release the data. Users generally are unaware that malware has infected their systems until they receive the ransom request.

“Tax professionals face an array of securi-ty issues that could threaten their clients and their business,” IRS Commissioner John Koskinen said. “We urge people to take the time to understand these threats and take the steps to protect themselves. Don’t just assume your computers and systems are safe.”

The 2017 Phishing Trends and Intelligence Report issued annually by Phishlabs named ransomware one of two transformative events of 2016 and called its rapid rise a public epidemic.

The Federal Tax alerT [email protected] july / augusT 2017 9

In May 2017, a ransomware attack dubbed “WannaCry” targeted users who failed to install a critical update to their Microsoft Windows operating system or who were using pirated versions of the operating system. Within a day, criminals held data on 230,000 computers in 150 countries for ransom.

The most common delivery method of this malware is through phishing emails. The emails lure unsuspecting users to either open a link or an attachment. However, the FBI also has warned that ransomware is evolving and cybercriminals can infect computers by other methods, such as a link that redirects users to a website that infects their computer.

Victims should not pay a ransom. Paying it further encourages the criminals. Often the scammers won’t provide the decryp-tion key even after a ransom is paid.

Tips to prevent Ransomware AttacksTax practitioners—as well as businesses, payroll departments, human resource organizations and taxpayers—should talk to an IT security expert and consider these steps to help prepare for and protect against ransomware attacks:

• Make sure employees are aware of ransomware and of their critical roles in protecting the organization’s data.

• For digital devices, ensure that secu-rity patches are installed on operating systems, software and firmware. This step may be made easier through a centralized patch management system.

• Ensure that antivirus and anti-malware solutions are set to automatically update and conduct regular scans.

• Manage the use of privileged accounts—no users should be assigned administrative access unless necessary, and only use administrator accounts when needed.

• Configure computer access controls, including file, directory and network share permissions, appropriately. If

users require read-only information, do not provide them with write-access to those files or directories.

• Disable macro scripts from office files transmitted over e-mail.

• Implement software restriction policies or other controls to prevent programs from executing from com-mon ransomware locations, such as temporary folders supporting popular Internet browsers, compression/de-compression programs.

• Back up data regularly and verify the integrity of those backups.

• Secure backup data. Make sure the backup device isn’t constantly connected to the computers and networks they are backing up. This will ensure the backup data remains unaffected by ransomware attempts.

Victims should immediately report any ransomware attempt or attack to the FBI at the Internet Crime Complaint Center, www.IC3.gov. Tax practitioners who fall victim to a ransomware attack also should contact their local IRS stakeholder liaison.

Hackers, malicious software, rogue employees and hardware loss of theft are all very real risks to your tax business. Should any of these cyber events occur, The Hartford’s new endorsement would help cover damages that typically result. Coverages included are:

n Network Security Wrongful Act n Credit Monitoring and Notification Expenses n Crisis Management Expenses n Cyber Investigation Expenses

Low, Group RatesWhen you choose The Hartford’s E & O coverage, you’ll enjoy group rates thanks to the American Tax Preparers Purchasing Group (ATP). The Hartford has provided coverage for the ATP since 1991 and Target Professional Programs has been the program administrator for over 20 years. This program is available in all states except AK, HI and LA. Full-time or part-time firms with up to 10 professionals are eligible to apply for coverage.

Benefits Highlights n Notary Public Coverage is included at no additional cost n Optional Bookkeeping Coverage is available n The Hartford provides 24/7 claim service and a Risk Management Hotline

Learn More Visit our website at www.TargetProIns.com or contact Shelley Cvek: 331-333-8240 or [email protected]

© 2017 Target Professional Programs is a division of and operates under the licenses of CRC Insurance Services, Inc., CRC of CA Insurance Services, CA Lic No 0778135. No claim to any government works or material copyrighted by third parties. Nothing in this communication constitutes an offer, inducement, or contract of insurance. Financial strength and size ratings can change and should be reevaluated before coverage is bound. This material is for educational use only. It is not meant to be an offer of insurance directly to insureds or business owners. Equal Opportunity Employer – Minority/Female/Disabled/Veteran.

The Hartford is Hartford Financial Services Group, Inc. and its subsidiaries, including issuing companies, Twin City Fire Insurance Company, Hartford Fire Insurance Company, Hartford Life Insurance Company, and Hartford Life and Accident Insurance Company. Its headquarters is in Hartford, CT. Premium indications are a good faith estimate and subject to the full underwriting of all account information. Coverage is not guaranteed. All information herein is as of June 2015. In Texas, insurance is underwritten by Twin City Fire

Network Security, Data Breach and Theft of Data CoverageComplimentary Endorsement to The Hartford’s Tax Preparers E & O Policy

The ATP Program is

endorsed by the NSTP

TARGET PROFESSIONAL PROGRAMSInsurance for Particular Professionals

news from the IRs ...continued from page 8

Victims should NOT pay a ransom.

n

10 july / augusT 2017 [email protected] The Federal Tax alerT

A taxpayer’s attempt to substantiate the number of hours he spent in his real estate business did not

convince the Tax Court that he spent enough hours to be considered a real estate professional for purposes of the passive activity loss (PAL) rules.

In general, under the PAL rules of Code Sec. 469, losses from passive activities may only be used to offset passive activity income. Code Sec. 469(c)(1) provides that a “passive activity” is any activity which involves the conduct of any trade or business, and in which the taxpayer does not materially participate. A taxpayer is treated as materially participating in an activity if he meets at least one of the seven tests in Reg. § 1.469-5T. For example, under one of these tests, an individual will be treated as materially participating in an activity for a tax year if the individual participates in the activity for more than 500 hours during such year. (Reg. § 1.469-5T(a)(1))

In general, under Code Sec. 469(c)(2), a rental activity is per se a passive activity regardless of the taxpayer’s participation in the activity. However, an individual who:

a. Has at least a 10% interest in any rental real estate activity, and

b. Otherwise actively participates in that activity, may offset up to $25,000 of nonpassive income with that portion of the passive activity loss, or of the de-duction equivalent of the passive activ-ity credit, attributable to that activity.

The $25,000 allowance ($12,500 for marrieds filing separately) is reduced (but not below zero) by 50% of the amount by which the taxpayer’s adjusted gross income (AGI) as specially computed exceeds:

i. $100,000 ($50,000 for marrieds filing separately), or

ii. $200,000 ($100,000 for marrieds filing separately) for any portion of the passive activity credit that is attributable to the rehabilitation credit. (Code Sec. 469(i))

In addition, under Code Sec. 469(c)(7), the per se rule for rental activities doesn’t apply to a qualifying real estate professional. A taxpayer qualifies as such for a particular tax year if:

1. More than half of the personal services that he performs during that year are

performed in real property trades or businesses in which he materially participates; and

2. He performs more than 750 hours of services during that tax year in real property trades or businesses in which he materially participates. (Code Sec. 469(c)(7)(B))

In the case of a joint return, the above requirements are satisfied if, and only if, either spouse separately satisfies both requirements. Thus, the couple’s activities cannot be aggregated for purposes of qualification as a real estate professional. (Code Sec. 469(c)(7))

Reg. § 1.469-9(e)(1) states that a taxpayer who qualifies as a real estate professional can treat rental losses as nonpassive, but only if he materially participates. Specifically, the regulation provides that the Code Sec. 469(c)(2) per se rental bar does not apply to any rental real estate activity of a taxpayer for a tax year in which the taxpayer is a qualifying taxpayer (i.e., a real estate professional). Instead, a rental real estate activity of such a qualifying taxpayer is a passive activity under Code Sec. 469 for the tax year unless the taxpayer materially participates in the activity.

Reg. § 1.469-9(e)(3)(i) confirms that even taxpayers who establish real estate professional status must separately show material participation in rental activities (as opposed to other real estate activities) before claiming any rental losses as nonpassive.

The extent of an individual’s participation in an activity may be established by any reasonable means. Contemporaneous daily time reports, logs, or similar documents are not required if the extent of such participation may be established by other reasonable means. Reasonable means include, but are not limited to, the identification of services performed over a period of time and of the approximate number of hours spent performing such services during such period, based on appointment books, calendars, or narrative summaries. (Reg. § 1.469-5T(f)(4)) This reg does not permit a post-event “ballpark guesstimate”. (Bailey, TC Memo. 2001-296TC Memo. 2001-296)

During 2012, Mr. Penley was a full-time employee of HSS, Inc. (HSS). From Janu-ary through September 2012, Mr. Penley

worked as an entry-level field sterilization technician, and from October through December 2012 he worked as a sales ac-count representative. Although Mr. Penley performed many of his duties from his home, he would travel to client sites as needed. These trips could take under half an hour in the case of a local client, or they could on occasion require him to travel several hours throughout Colorado. In all, Mr. Penley spent at least 2,194 hours, including occasional overtime, dur-ing 2012 performing his duties for HSS.

During 2012, Mr. Penley was also actively engaged as a Colorado licensed real estate broker, and he had an active business marketing commercial and residential properties for several clients. He also conducted a rental real estate activity through a subchapter S corporation named Harvey Herbert, Inc. (HHI), which was owned 50% each by him and his wife. During the tax years 2010 - 2012, HHI owned two single-family residential properties in Littleton, Colorado. The Penleys also held a warehouse in Sedalia, Colorado, in a self-directed individual retirement account through a limited liability company, Flying Bee Ranch, LLC. Mr. Penley spent time performing various tasks in the course of managing HHI’s affairs, such as finding tenants, managing the corporation’s finances, and making repairs to the properties.

Mr. Penley, acting through HHI, leased the front unit of the property in Littleton, Colorado (the Sterne property) to a tenant. During 2012, he spent significant time and effort repairing the damage to the rear unit of the Sterne property, performing substantially all of the work on the property with his wife, including installing new flooring, wiring, and plumbing.

From April through August 2012, Mr. Pen-ley spent time performing various regulato-ry and due diligence activities with respect to Evergreen Park property, in Colorado Springs, Colorado, such as negotiating the purchase terms and securing financing. He acquired Evergreen Park on Aug. 15, 2012, and thereafter made frequent trips to make improvements to the property.

Mr. Penley and his wife filed a joint income tax return for 2012, on which they reported $24,092 of total income but zero taxable income. His return included a Schedule E, Supplemental Income and Loss, which reflected a $96,354

from the BeNCh

Taxpayer Failed to substantiate sufficient hours to be a Real estate Professional penley, TC memo. 2017-65TC memo. 2017-65

continued on page 9

The Federal Tax alerT [email protected] july / augusT 2017 11

n

passthrough loss from HHI in two equal parts of $48,177, one for him and his wife, as a nonpassive loss. Mr. Penley claimed that he spent approximately 2,520 hours on his real estate activities during the 2012 tax year, with approximately 1,000 of the claimed hours being related to the rehabilitation of the rear unit of the Sterne property.

On audit, IRS determined that $56,863 of HHI’s reported loss for 2012 was a passive loss from real estate activities and that Mr. Penley did not qualify as a real estate professional under Code Sec. 469(c)(7). After making additional adjustments, IRS determined that the taxpayer’s income for the 2012 tax year exceeded the phaseout threshold of Code Sec. 469(i) and disallowed his deduction for the passive real estate loss in full.

The Tax Court found that the taxpayer failed to demonstrate that he was a real estate professional for 2012. The Court concluded that, on the record before it, Mr. Penley hadn’t sufficiently substantiated his claim that he spent more time during 2012 in his real estate activities than in his employment with HSS, as required by Code Sec. 469(c)(7)(B)(i).

Mr. Penley’s primary substantiation at trial for the hours he worked during 2012 was a monthly calendar. The calendar indicated the property where he worked on a particular day and contained a brief description of the work performed, an estimate of the number of hours worked, and the number of miles driven to and from the property

The Tax Court found that the taxpayer’s calendar record was untrustworthy and greatly exaggerated the time he spent on his real estate activities. Generally, Mr. Penley claimed to have worked on his real estate activities 10-14 hours on each Saturday and Sunday during 2012 and an additional 4-6 hours most weekdays, in addition to another full-time job. For Mr. Penley to have worked 2,520 hours on his real estate activities, as he claimed, he would have had to work a total 4,714 hours (i.e., 2,194 for HHS plus 2,520 on his real estate activities) in 2012. That meant that if he worked every day, he would have needed to have averaged 12.88 total hours per day (i.e., 4,712 ÷ 366 = 12.88).

Further, the Court noted that virtually all of the entries were rounded to the nearest hour or half-hour, did not specify a start or end time for the work, included the time spent driving to and from the property, and did not separate out any time for meals or other breaks. The Tax Court determined that the taxpayer’s calendar did not fall within the regulation’s “any reasonable means” of substantiation. While corroborating evidence, such as credit card statements, phone bills, and emails relating to the purchase of Evergreen Park demonstrated meaningful real estate activity by the taxpayer during 2012, the Tax Court found that the taxpayer did not provide the Court with a sufficient explanation to reconcile this documentary evidence of his activities with the large blocks of time (often 4 hours to 14 hours) shown on the calendar.

COURSE DESCRIPTION: An in-depth study of federal tax law and tax updates for 2017 as related to federal taxes. Covered topics will include 2017 tax return preparation, new tax laws and recent developments. Participants will receive a textbook with detailed information, examples and selected draft IRS forms.

LEARNINg OBJECTIVES: After completing this program, participants will be able to differentiate federal tax law changes from the previous year, identify updated forms and rule changes and apply rules of federal tax law to preparing tax returns.

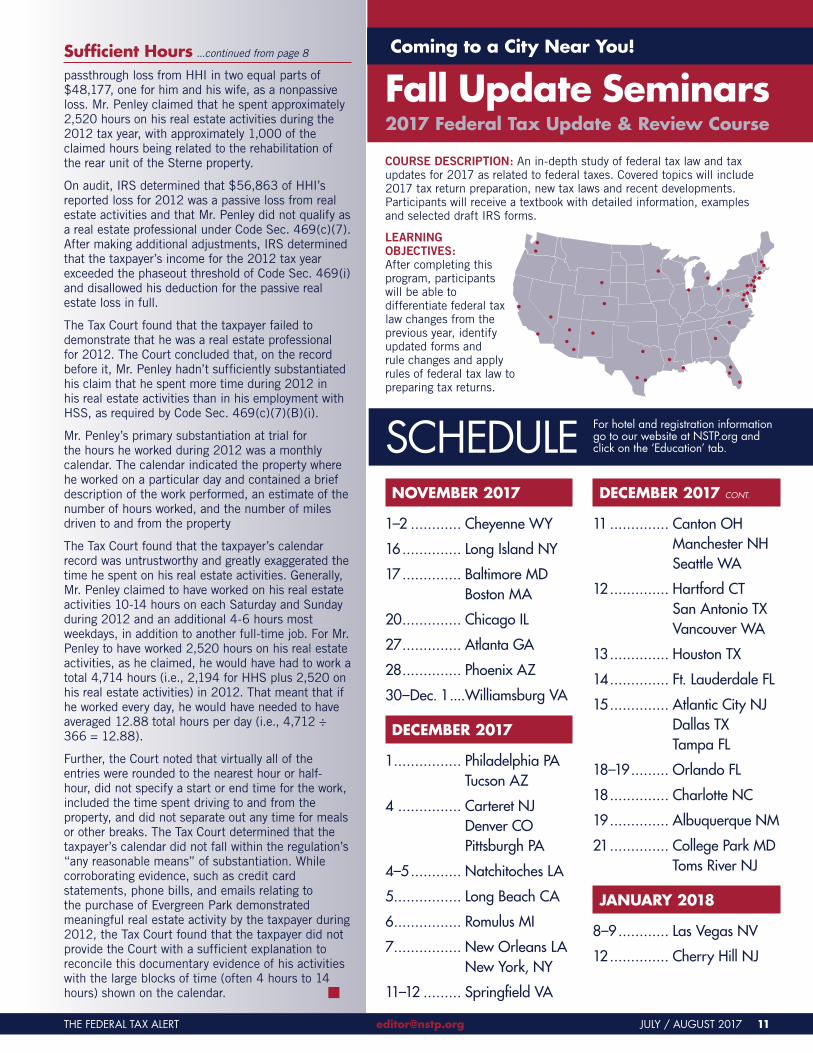

noVeMBeR 2017

1–2 ............ Cheyenne Wy

16 .............. long Island Ny

17 .............. Baltimore MD Boston Ma

20 .............. Chicago Il

27 .............. atlanta ga

28 .............. Phoenix aZ

30–Dec. 1 ....Williamsburg Va

deCeMBeR 2017

1................ Philadelphia Pa tucson aZ

4 ............... Carteret Nj Denver CO Pittsburgh Pa

4–5 ............ Natchitoches la

5................ long Beach Ca

6................ Romulus MI

7................ New Orleans la New york, Ny

11–12 ......... springfield Va

deCeMBeR 2017 coNT.

11 .............. Canton OH Manchester NH seattle Wa

12 .............. Hartford Ct san antonio tX Vancouver Wa

13 .............. Houston tX

14 .............. Ft. lauderdale Fl

15 .............. atlantic City Nj Dallas tX tampa Fl

18–19 ......... Orlando Fl

18 .............. Charlotte NC

19 .............. albuquerque NM

21 .............. College Park MD toms River Nj

JAnUARy 2018

8–9 ............ las Vegas NV

12 .............. Cherry Hill Nj

For hotel and registration information go to our website at NsTP.org and click on the ‘education’ tab.sChedule

Coming to a City near you!

2017 Federal Tax Update & Review CourseFall Update seminars

sufficient hours ...continued from page 8

12 july / augusT 2017 [email protected] The Federal Tax alerT

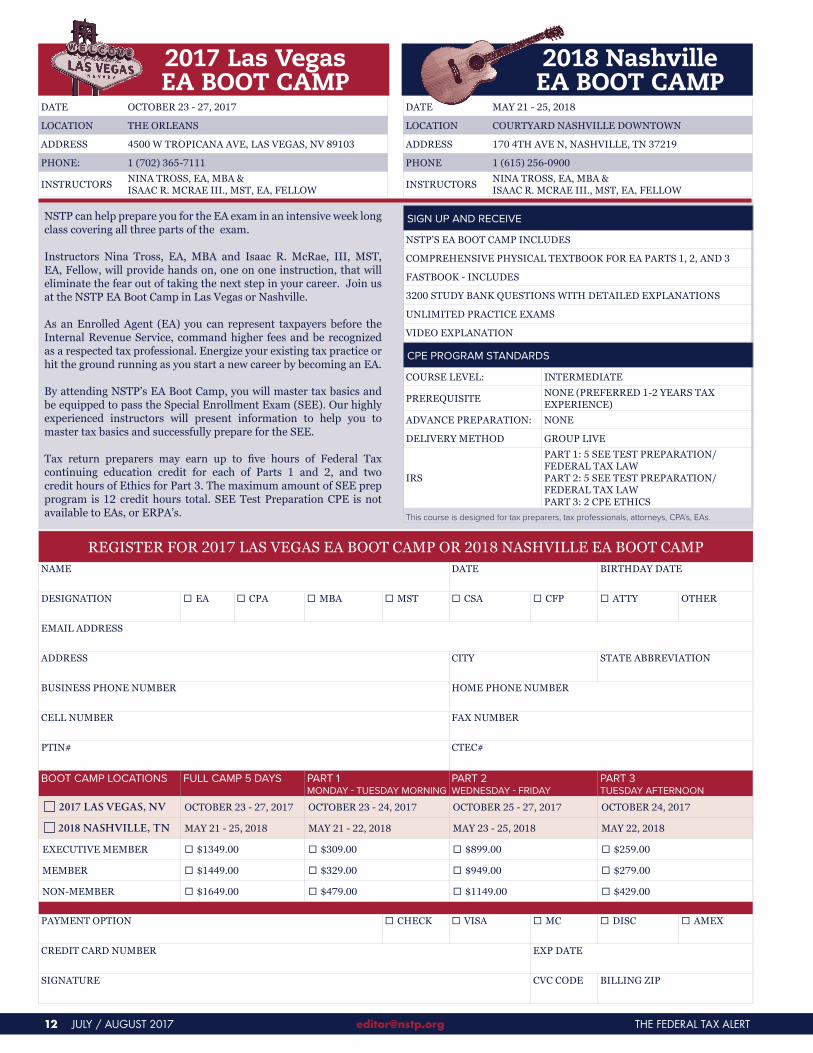

2017 Las Vegas EA BOOT CAMP

2018 Nashville EA BOOT CAMP2017 LAS VEGAS EA BOOT CAMP

DATE OCTOBER 23 - 27, 2017

LOCATION THE ORLEANS

ADDRESS 4500 W TROPICANA AVE, LAS VEGAS, NV 89103

PHONE: 1 (702) 365-7111

INSTRUCTORS NINA TROSS, EA, MBA &ISAAC R. MCRAE III., MST, EA, FELLOW

REGISTER FOR 2017 LAS VEGAS EA BOOT CAMP OR 2018 NASHVILLE EA BOOT CAMPNAME DATE BIRTHDAY DATE

DESIGNATION � EA � CPA � MBA � MST � CSA � CFP � ATTY OTHER

EMAIL ADDRESS

ADDRESS CITY STATE ABBREVIATION

BUSINESS PHONE NUMBER HOME PHONE NUMBER

CELL NUMBER FAX NUMBER

PTIN# CTEC#

BOOT CAMP LOCATIONS FULL CAMP 5 DAYS PART 1MONDAY - TUESDAY MORNING

PART 2WEDNESDAY - FRIDAY

PART 3TUESDAY AFTERNOON

2017 LAS VEGAS, NV OCTOBER 23 - 27, 2017 OCTOBER 23 - 24, 2017 OCTOBER 25 - 27, 2017 OCTOBER 24, 2017

2018 NASHVILLE, TN MAY 21 - 25, 2018 MAY 21 - 22, 2018 MAY 23 - 25, 2018 MAY 22, 2018

EXECUTIVE MEMBER � $1349.00 � $309.00 � $899.00 � $259.00

MEMBER � $1449.00 � $329.00 � $949.00 � $279.00

NON-MEMBER � $1649.00 � $479.00 � $1149.00 � $429.00

PAYMENT OPTION � CHECK � VISA � MC � DISC � AMEX

CREDIT CARD NUMBER EXP DATE

SIGNATURE CVC CODE BILLING ZIP

NSTP can help prepare you for the EA exam in an intensive week long class covering all three parts of the exam.

Instructors Nina Tross, EA, MBA and Isaac R. McRae, III, MST, EA, Fellow, will provide hands on, one on one instruction, that will eliminate the fear out of taking the next step in your career. Join us at the NSTP EA Boot Camp in Las Vegas or Nashville.

As an Enrolled Agent (EA) you can represent taxpayers before the Internal Revenue Service, command higher fees and be recognized as a respected tax professional. Energize your existing tax practice or hit the ground running as you start a new career by becoming an EA.

By attending NSTP’s EA Boot Camp, you will master tax basics and be equipped to pass the Special Enrollment Exam (SEE). Our highly experienced instructors will present information to help you to master tax basics and successfully prepare for the SEE.

Tax return preparers may earn up to five hours of Federal Tax continuing education credit for each of Parts 1 and 2, and two credit hours of Ethics for Part 3. The maximum amount of SEE prep program is 12 credit hours total. SEE Test Preparation CPE is not available to EAs, or ERPA’s.

2018 NASHVILLE EA BOOT CAMPDATE MAY 21 - 25, 2018

LOCATION COURTYARD NASHVILLE DOWNTOWN

ADDRESS 170 4TH AVE N, NASHVILLE, TN 37219

PHONE 1 (615) 256-0900

INSTRUCTORS NINA TROSS, EA, MBA &ISAAC R. MCRAE III., MST, EA, FELLOW

CPE PROGRAM STANDARDS

COURSE LEVEL: INTERMEDIATE

PREREQUISITE NONE (PREFERRED 1-2 YEARS TAX EXPERIENCE)

ADVANCE PREPARATION: NONE

DELIVERY METHOD GROUP LIVE

IRS

PART 1: 5 SEE TEST PREPARATION/FEDERAL TAX LAWPART 2: 5 SEE TEST PREPARATION/FEDERAL TAX LAWPART 3: 2 CPE ETHICS

This course is designed for tax preparers, tax professionals, attorneys, CPA’s, EAs.

SIGN UP AND RECEIVE

NSTP’S EA BOOT CAMP INCLUDES

COMPREHENSIVE PHYSICAL TEXTBOOK FOR EA PARTS 1, 2, AND 3

FASTBOOK - INCLUDES

3200 STUDY BANK QUESTIONS WITH DETAILED EXPLANATIONS

UNLIMITED PRACTICE EXAMS

VIDEO EXPLANATION

2017 LAS VEGAS, NV

2018 NASHVILLE, TN