Embed Size (px)

Citation preview

February 21, 2008

This monthly brief was prepared by a team of the Development Economics Prospects Group (DECPG), led by Hans Timmer, and comprising Mick Riordan (world economy); John Baffes and Cristina Savescu (trade); Betty Dow and Shane Streifel (primary commodities), Eung Ju Kim (finance) and Gauresh Rajadhyaksha (high-frequency data and

Annex). The note reflects the views of the team, but is not formally cleared by the World Bank Group.

The External Environment for Developing Countries February 2008

Overview

A Perfect Storm in the making? Write-downs of mortgage-backed securities in the banking sector reached $150 billion and counting. Equities in emerging markets lost more than 10% in January, and corporate default risk moved up in the United States and Europe. Global IP growth halved from 5% in the third quarter to 2.5% in the fourth quarter of 2007 (saar). Oil prices hit $100 per barrel on supply fears, while in the United States core inflation moved up to 2.4%, imposing limits to stimulus policies.

Heavy weather in the ECA region. In January capital flows to developing countries were $21 billion, less than half the monthly average for 2007, with a sharp decline in bank lending. That is potentially bad news for many ECA countries that rely heavily on capital inflows- and where in January such flows dropped to 20% of monthly 2007 averages. Moreover a sharp slowdown in industrial production is now expected for western Europe. Leading indicators point to a contraction of European IP early this year.

Other parts of the world should experience sunny periods between the clouds. According to leading indicators, recession in the United States might be avoided. Growth in developing Asia and the southern part of Latin America is holding up well. Import growth for developing countries as a group remains robust at 30% (US$, saar). Linked to that strength, growth in Japan surprised to the upside at 3.7% in the fourth quarter, of which 1.8 points of growth derived from net exports. And after falling 5.5% in November and December, metals prices moved up 4% in January, confirming underlying strength in global demand. Spreads on sovereign debt have increased roughly by the same amount as U.S. Treasury yields have declined, implying stable yields on emerging-market government bonds.

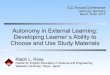

Equities tumbled in JanuaryS&P/Citi-Group BMI Global Index, ch%

-20

-15

-10

-5

0

5

10

15

20

25

Emerging MarketsMature Markets

Source: Standard & Poor’s.January 2008

3 months:from October 2007

1 year:from January 2007 140

240

340

440

540

640

740

Jan-07

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Source: JPMorgan-Chase and Thomson/Datastream

Spreads widen, but yields stable EMBIG spread and U.S. 10-year T-note, basis points

EMBIG spreads

U.S. 10-year Treasury note

EMBIG yields

February 21, 2008 External Environment for Developing Countries page 2

Projections found in the indicators table there are sourced from the final version of Global Economic Prospects-2008, which was released on January 10. The ANNEX TABLES at the back of this report now feature updated projections for 2008-09 from various private- and public organizations. And the DECPG website Global Economic Monitor (GEM) continues to be enhanced—broadening the coverage of daily data and improving means of data access. We hope you find GEM useful for your daily work.

Global Indicators

Global Indicators (Percentage change per annum, unless otherwise specified)

2005 2006 2007e 2008f

GDP volume: World 3.4 3.9 3.6 3.3 Memo item: World GDP at PPP weights 4.8 5.3 5.2 4.9 High-income countries 2.6 2.9 2.6 2.2 Developing countries 6.8 7.5 7.4 7.1 Industrial production: World (incl China) 4.5 5.9 5.5 ... High-income countries 2.0 3.7 2.6 2.5 ... Developing countries (incl China) 9.5 10.1 11.4 5.9 ...

Export volume (GNFS): World (incl China) 7.8 10.1 9.2 7.6 High-income countries 6.3 9.2 8.2 6.3 Developing countries (incl China) 12.3 12.7 12.0 11.0 Trade Prices ($): Manufacturing (MUV) 0.0 1.6 2.3 0.8 Oil ($/bbl) 53.4 64.3 71.2 84.1 Non-oil commodities 13.4 24.5 13.1 -3.1

Nominal interest rates: $LIBOR (percent p.a.) 3.73 5.23 5.30 4.80 €LIBOR (percent p.a.) 2.24 3.23 4.30 4.00 Financial flows FDI ($billion) 282 288 ... Gross Capital flowsa ($billion) 361 494 683 ... Equity placement ($bn) 59 111 194 ... Bond financing ($bn) 126 137 146 ... Lending ($bn) 175 246 343 ...

Source: DECPG, February 2008.

Note(s): a. Gross inflows 2007 actual. Figures in bold represent changes this month.

High-tech markets: Snapshot (Dec-07 data) Nov-07 Dec-07

World semiconductor sales ($) 0.6 -6.5 G-3 new high-tech orders ($) -3.0 -7.8 Production (ch%) World 15.0 14.8 United States 17.4 17.2 Japan -2.0 8.3 East Asia 19.9 16.3 Exports ($, ch%) World 10.0 14.7 United States -0.8 6.7 Japan 19.1 16.1 East Asia 10.3 16.2 Sources: SIA, National agencies, Haver Analytics, Thomson/Datastream. Note: growth computed as 3m/3m saar rates. Sales, orders and exports in USD terms; production in volume.

February 21, 2008 External Environment for Developing Countries page 3

United States GDP growth falters. The United States registered 0.6% growth in the fourth quarter (saar) down from 4.9% in the third, as the housing slump intensified, export growth lost momentum and inventories were reduced. Residential investment continued in free-fall, dropping 24% and subtracting 1 point from growth. Final sales were met from stocks, carrying them sharply lower and exerting drag of 1.1 points. But a number of factors (and recent data) suggest that the growth falloff may be less dramatic (and marked higher) than first estimates. Consumption (2%) and business investment (7.5%) were still solid; stocks will be revised (December data suggest a large increase in inventories), and trade figures show stronger exports in December than initially envisioned. In response to GDP and other less encouraging indicators, the FOMC cut Fed Funds by an additional 50 basis points to 3% on January 30; and a $168 billion stimulus package was passed by Congress. Housing recession: end in sight? New home sales fell 4.7% in December on the heels of a 12.6% drop in November. And sales accumulated to a decline of 33% by year end, the worst in 45 years. Existing home sales showed no sign of recovery, falling 2% in December and 20% (y/y). And the median price for new homes fell 5.5% in 2007, the first decline registered by the Department of Commerce. The present downturn has now eclipsed housing slumps of the 1980s and 90s: since the third quarter of 2005: home affordability worsened by 10.7 points; residential investment fell 28.6%; home starts dropped 45% and new home sales declined 50%. Employment contracting. For the first time in 4 years the United States witnessed a net monthly loss of jobs. Employers shed 17,000 staff in January capping a downtrend in employment over 2006-07, when smoothed growth eased from 250,000 per month in January 2006 to 40,000 by January 2008. Consumer confidence, incomes and sales are now being affected, with the former down to 16-year lows, and retail outlays slipping to a 4.4% pace in January.

-35-30-25-20-15-10-505

1015

Jan-0

5

Apr-0

5

Jul-0

5

Oct-0

5

Jan-0

6

Apr-0

6

Jul-0

6

Oct-0

6

Jan-0

7

Apr-0

7

Jul-0

7

Oct-0

7

Source: National Assn of Realtors and Department of Commerce.

Existing home sales

U.S. new home sales drop 33%over 2007– worst in 45 years

existing and new home sales, ch% 3mma y/y

New home sales

4.8 4.9

0.6

-4.0

-2.0

0.0

2.0

4.0

6.0

Q3-2007 P Q3-2007 F Q4-2007

Source: Department of Commerce and DECPG calculations.

U.S. GDP growth falls to 0.6% in fourth quarter as housing takes a toll

growth of real GDP, and contributions to growth in percentage pointsNet exportsGovernment

ConsumptionFixed InvestmentChange in stocks

Growth 2007 2.2%

3.0

4.5

6.0

7.5

9.0

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-0840

80

120

160

200

240

280

Source: Departments of Labor and Commerce.

Employment [R]

Retail sales [L]

Employment decline in Januarypoints to weaker retail spending ahead

retail sales, ch% 3mma y/y [L], change in employment 3mma [R]

February 21, 2008 External Environment for Developing Countries page 4

Japan

Japan GDP surprises to the upside. Monthly indicators for Japan offered little clue as to the strong 3.7% GDP growth results for the fourth quarter (saar). Continued strong export performance (12%) largely buoyed by East Asian demand; a strong pick-up in business investment (12%) and 0.5 point contribution to growth from inventories; 1.8 point contribution from net exports were sufficient to underpin a major step-up in GDP. To the downside, third quarter growth was revised from 1.5% earlier to 1.3% (saar) as consumer spending gains disappointed at 0.5% and fixed investment dropped 3.4%. Household outlays were lackluster during the final quarter as well, advancing a modest 0.8%. Japan’s GDP picked up 2.1% in the year, well above expectations in GEP-2008 for growth of 1.8%. Shifts in investment patterns. Since 2005, a shift in Japanese fixed investment has taken place. Business investment has picked up a full percentage point of investment outlays (to 16.1% of GDP in the final quarter of 2007) due to fairly strong growth in corporate capital expenditures (17% over the period), combined with a sharp decline in government project spending and recent steep fall-off in residential investment. Public capital outlays compressed 17.5% over the period; while declines in home construction have been most prominent during 2007, falling at 30% rates during the second half of the year (saar) and dropping 9.3% for 2007. To a degree, this reflects recent regulatory changes, but attention will need be paid to this development in coming quarters. Orders are key. Export growth was a key factor in supporting GDP in the fourth quarter, and goods exports maintained a double-digit pace (10.3%, saar) into year end. At the same time machinery orders slumped in the final 2 months of 2007, dropping 6% per month after an 18% October surge. As orders momentum fades, export prospects may come into question, with strong market growth in East Asia easing from current rates and U.S. demand growth dropping further.

1.5 1.3

3.7

-2.5

0.0

2.5

5.0

Q3-2007 P Q3-2007 F Q4-2007 P

Source: Cabinet Office and DECPG calculations.

Japanese GDP jumps to 3.7% growth in fourth quarter on exports

growth of real GDP, and contributions to growth in percentage points

Net exportsStocks

Fixed InvestmentGovernment

Consumption

Growth 2007 2.1%

Japan’s public-sector and residential investment show sharp declines

public- and residential investment, share of real GDP, percent

0

3

6

9

Q1 2005 Q3 2005 Q1 2006 Q3 2006 Q1 2007 Q3 2007

Source: Cabinet Office through Thomson/Datastream.

Public investment

Residential investment

Japan’s orders momentum up in December supporting exports and production

export volume and IP, ch% saar [L] machinery orders ch% saar [R]

-15

-10

-5

0

5

10

15

20

25

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07-25

-15

-5

5

15

25

35

45Exports [L]

Industrial production [L]

New machinery orders [R]

Source: Cabinet Office through Thomson/Datastream.

February 21, 2008 External Environment for Developing Countries page 5

Euro Area

GDP slows in fourth quarter. Growth in the Euro Area eased in the fourth quarter from 3.1% during the third to 1.7%—below most expectations. Though first estimates provide little background on demand categories, data for France offers a preview—sluggish consumer spending, a falloff in export growth and little vitality in private investment. Growth in Germany fell from a strong 2.7% pace in the third quarter to a weak 1.1% (saar); that in France from 3.2% to 1.4%, while GDP in Spain accelerated to 3.2% from 2.8% in the preceding quarter. Data for retail sales and production add to evidence for the slowdown. Sales declined sharply in December, down 1.6% on a year-over-year comparison, the biggest drop since data series began in 1995. Production declined 0.2% in December (m/m) dropping 1% on an annualized basis for the fourth quarter. German exports under pressure. German export shipments dropped 1.2% in December (m/m) on the heels of a 0.5% falloff in November, as the strong euro and slackening U.S. demand take a toll. These factors are outweighing more buoyant export market conditions for German products in Central Europe and the CIS, the Middle East and North Africa and Asia. The two-month falloff in exports carried the growth pace to near 2% in December from highs of 16% at the turn of 2007 (y/y). Export orders dropped 2.8% in December a reversal of strong November showings. ECB hints at rate cut. After 5 years of citing the prospective inflationary consequences of loosening European monetary policy prematurely (now with HICP at 3.2% y/y) ECB president Jean-Claude Trichet for the first on February 7th intimated that interest rate reductions could be in the offing. This against the background of the cut in Fed Funds to 3% and increasing evidence of a slowing European economy. Futures markets are now pricing-in 2 reductions of 25 basis points each during the course of 2008, carrying the repurchase rate to 3.5% by year end.

0

1

2

3

4

Euro Area Germany France Spain

2007-Q2 2007-Q3 2007-Q4

Euro Area growth eases in fourth quarter on consumer and exports

percent change

Source: EuroStat.

German exports and production dampened by euro strength

export volumes and IP ch% 3mma, y/y

0

2

4

6

8

10

12

14

16

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Source: Eurostat through Thomson/Datastream.

Production

Exports

ECB hints at cut in policy ratesas Euro Area growth slows

HICP inflation (ch% y/y) [L]; Germany IP ch% saar [R]

1.0

1.5

2.0

2.5

3.0

3.5

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-080

3

6

9

12

Source: Eurostat and Bundesbank.

Germany IP [R]

HICP inflation (y/y) [L]

February 21, 2008 External Environment for Developing Countries page 6

Industrial Production Industrial output to contract in the Eurozone... Weak consumer and private investment spending, and slower export growth sapped industrial output growth in the last quarter of 2007 in the Euro Area. And it appears likely that tighter credit conditions, high energy prices, weaker global demand and a stronger currency will coalesce to further weaken industrial sector performance in the Eurozone in coming months. DECPG’s latest forecast calls for a mild contraction in output in the first quarter of 2008. Deterioration in manufacturing business confidence in recent months and weaker retail sales offer some support for this view. …while there are signs of a possible bottoming out in the United States. IP in the United States is expected to bounce back, albeit by a modest margin, following decline in the fourth quarter of 2007. To date in 2008, robust external demand has offset the negative effects of tighter credit conditions and high energy prices, with industrial output up 0.1% in January (m/m). Following the lead of its main trading partner, Mexico is also expected to see a modest bounce back in industrial output growth this quarter. Mexico’s industrial production could outperform, as Mexican firms have continued to gain market share relative to their Asian counterparts, and have liquidated most excess inventories in 2007 following the introduction of a new corporate tax law. Moderate weakening in developing East Asia. Following strong growth during the first three quarters of 2007, IPs underlying momentum slowed in the fourth quarter, but is expected to rebound in the first quarter of 2008. Lunar holiday effects and the leap year complicate the forecasting of industrial production growth, as firms front-load output and export shipments ahead of the holidays, a pattern that is not extracted when using standard seasonal adjustment methods. We expect industrial production to continue to move sideways in developing Asia, in part dampened by slackening growth in high-tech markets.

-6

-4

-2

0

2

4

6

8

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Possible contraction of industrial production in the Euro-zone in 2008-Q1

Euro Area industrial production, 3mma ch%, saar

Source: DECPG

Forecast

-10

-5

0

5

10

15

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Has the slowdown in U.S.- and Mexican IP bottomed out?

Industrial production, 3mma, ch% saar

United States

Mexico

data forecast

Source: DECPG

-15

-5

5

15

25

35

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

IP growth appears to be moving “sideways” in East Asia

Other EAP countries

China

forecastdata

Source: DECPG

Industrial production, 3mma, ch% saar

February 21, 2008 External Environment for Developing Countries page 7

High-tech markets

Tech rally falters. Slowing growth in the United States and Europe together with deterioration in financing conditions for manufacturers of high-tech equipment, have likely put an early “end” to what appeared to be a fresh rally in tech sales, production and exports. From April 2007, global semiconductor sales–a good proxy for the wide range of high-tech equipment and consumer goods in which these are an increasing component–pulled up from negative territory to post peak gains of 35% (saar) by September. However, as market conditions took a turn for the worse in the months following the August onset of financial turmoil in the United States, sales returned to decline of 6.5% in December. Though production and exports are showing some residual momentum, a downturn appears imminent. Production starts a downward move. Underlying data for U.S. fourth quarter GDP shows that consumer spending on high-tech equipment eased from a 9% pace during the third quarter to 5.5%. At the same time business outlays on equipment and software, by far the larger component of U.S. tech demand, dropped to a 3.7% pace from 5.1% during the previous quarter. And January readings for U.S. retail sales of tech goods displayed a sharp compression to decline of 11% (y/y). Global high-tech output has now eased from 27% in September to 14.8% as of December, with growth in East Asia (x Japan) falling more keenly to 16.3% from near 30% over the period. A difficult 2008. Looking forward, with the global economic environment anticipated to remain subject to financial uncertainties; a general slowing of growth among the OECD countries, in large measure driven by slumping business confidence and a falloff in investment, prospects for the tech industry are waning into 2008. G-3 orders have dropped once more to negative ground (-7.8%, saar), from recent 20% peaks in July. And 2007 outturns, disappointing in perspective, are unlikely to be matched this year. During 2007: semiconductors sales declined 5%, global IP gained 4.4% and world tech exports closed the year with a 6% advance.

The tech-cycle has been truncatedby global growth uncertainties and delayed

investment spendingglobal semi-chip sales and high-tech exports, ch% saar

-20

-10

0

10

20

30

40

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Source: SIA, Thomson/Datastream, Haver.

Exports

Semiconductor sales

-20

-10

0

10

20

30

40

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Source: National Agencies and DECPG calculations.

G-3 high-tech ordersback in negative territory

G-3 orders for high-tech manufactures, US dollar terms, ch% saar

G-3 High-tech orders

Production trends still at lofty ratesbut signs of downturn emerging

unit value index in USD terms, ch% year-on-year

0

5

10

15

20

25

30

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Global

East Asia x Japan

Source: National Agencies and DECPG calculations.

February 21, 2008 External Environment for Developing Countries page 8

International Trade

Developing countries are now the key drivers of global trade growth. During 1991-2002 the contribution to world nominal import growth (in dollar terms, y/y percent) from the United States and the developing countries was similar—1.5% and 2% respectively. Since 2003 however, growth of developing country imports increased to a 7% pace, while that of the United States remained at 2%. The gap (i.e. the difference in growth rates) appears to be widening, as it reached 6.35% in 2007 (January-November), the highest of the last 15 years. Slowing in U.S. domestic demand and the falling dollar has contributed to the general weakness of U.S. imports. At the same time, a buildup in demand growth among emerging markets, and increase in intra-trade has underpinned imports to higher growth. De-linking is evident between developing countries export and high-income import growth. Annual import volume growth in high-income countries continues to trend downward, while export growth on a similar measure in developing countries remains robust. In value terms, developing countries exports expanded by more than 30% (saar) in the three month through August 2007, while imports in high-income countries grew at half that pace (almost flat in real terms). Meanwhile, import value growth among emerging markets stood above 30% (saar), suggesting that trade among developing countries is increasing at a quite rapid rate. Import growth of large emerging economies strengthens. China sustained 1.5% monthly import growth during 2007 (11 months to November, y/y percent), similar to the pace achieved during 2006. And the remaining three large emerging economies—Russia, India, and Brazil—each stepped-up their import gains. Apart from China, which exceeded 2% monthly advances during 2003-04, Russia-, India-, and Brazil’s recent import surge was the strongest in the last decade. Import growth in all four countries is in sharp contrast to the continued weakening of high-income country import growth of the last 21/2 years.

Developing countries are now key drivers of global imports and trade contribution to global import growth, ch% year-on-year

-6

-4

-2

0

2

4

6

8

10

1991

M1

1992

M1

1993

M1

1994

M1

1995

M1

1996

M1

1997

M1

1998

M1

1999

M1

2000

M1

2001

M1

2002

M1

2003

M1

2004

M1

2005

M1

2006

M1

2007

M1

Source: National Agencies through Thomson/Datastream.

Developing country imports

U.S. imports

Gap between developing export- and high-income import- growth widens

growth (USD, y/y percent) developing country exports and high-income imports

-10

0

10

20

30

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Source: National Agencies through Thomson/Datastream.

Developing country export volumes

High-income import volumes

Large emerging economies’ import growth and contributions strengthen

contribution to global import growth, ch% year-on-year

-1.0-0.50.00.51.01.52.02.53.03.5

1991

M3

1992

M3

1993

M3

1994

M3

1995

M3

1996

M3

1997

M3

1998

M3

1999

M3

2000

M3

2001

M3

2002

M3

2003

M3

2004

M3

2005

M3

2006

M3

2007

M3

Source: National Agencies through Thomson/Datastream.

China

Russia

India

Brazil

February 21, 2008 External Environment for Developing Countries page 9

Commodity Prices

Oil prices hit $100/bbl on supply fears. Crude oil prices increased recently on production disruptions in Nigeria and the North Sea, and as Venezuela halted small volumes of oil to ExxonMobil (40,000 b/d), and threatened to stop oil shipments to the United States (the government has since said they will not do so). Crude oil inventories—which plunged in 2H-07 and contributed to the price surge last fall—have started to increase as refiners begin winter maintenance. Further builds are expected before the upturn in spring demand. Product stocks are ample, particularly for gasoline, and lower refinery runs will likely lead to draws in the coming weeks. For the latest 4-week period, U.S oil demand fell 1%, following gains of just 0.3% in 2007. OPEC production moves higher. OPEC production has been edging higher in recent months, partly in response to weaker growth in non-OEPC supplies, the latter constrained by project delays and disruptions. Much of the increase in OPEC output has been in Saudi Arabia, Iraq and Kuwait. Iraq’s production hit 2.4mb/d in late-2007, due to higher exports from its northern fields through Turkey, but output has slipped this year due to various accidents and outages. OPEC left its production levels unchanged when it met February 1st, and will reassess production requirements when it next meets on March 5th. OPEC appears to be focusing mainly on a possible cut in production, given rising stocks and worries about recession. Coal prices soar on supply issues. Spot coal prices surged due to production disruptions associated with flooding in Australia, heavy snows in China and power cuts in South Africa. Australian spot coal prices spiked to nearly $140/ton, and come as producers and Asian buyers are set to negotiate contract prices that take affect April 1st. Snow storms in China caused transport bottlenecks and power outages, and led the government to halt coal exports until April. In South Africa, heavy rains reduced coal supply to the state power utility which was running flat out with critically low stocks of generally poor quality coal. It is now seeking higher-quality volumes which will inevitably constrain coal exports.

OPEC maintaining production levels

21

22

23

24

25

26

27

28

29

30

31

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

OPEC-10 Quota

OPEC-10

Including Iraqmb/d

Source: OPEC and DECPG Commodities Group.

Thermal coal prices surge on weather supply problems in Australia, China and South

Africa

0

20

40

60

80

100

Jan-96 Jan-98 Jan-00 Jan-03 Jan-04 Jan-06 Jan-08

Australia Thermal Coal $/ton (fob)

WB Oil Price $/bbl

Source: DECPG Commodities Group.

Crude oil prices remain elevated

50

60

70

80

90

100

Jan-07Apr-0

7Jul-07

Oct-07

Jan-08

$/bblWTI

BrentDubai

Source: DECPG Commodities Group.

February 21, 2008 External Environment for Developing Countries page 10

Grains, fats & oils, and beverage prices sharply higher. Agriculture prices have recorded some of the strongest gains this year on tight supplies and strong buying by investment funds. Rice prices are up 28% due to an earlier ban on India exports and a demand shift away from higher-priced wheat. Wheat prices have climbed 19% on low global stocks and strong import demand. Soybean prices are up 15% and corn prices 14%, on strong demand for food, feed and biofuels. There is now strong competition for land among the main crops, and high prices for wheat and soybeans are expected to draw plantings away from corn which surged last year. Coffee (robusta) prices have risen 25% on expected lower supplies from Vietnam, while cocoa prices are up 20% on concerns about dry weather in Ghana. Aluminum prices surge on power shortages. The price of energy-intensive aluminum surged 19% this month due to power disruptions in China and South Africa. The loss of power sent some 10% of China’s aluminum capacity offline, and aluminum exports fell more than 6% in January. In South Africa, power shortages led Eskom to consider buying back significant amounts of power from industrial users, including aluminum smelters, which would curtail output. Elsewhere, lead prices have gained 21% this year on extremely low stocks, strong battery demand and lingering supply constraints. Copper prices are up 20% this year on declining LME stocks and expectations of continuing strong double-digit demand growth in China. Steel production sees stellar growth in 2007. Global steel production grew 10% in 2007, up from 9.5% a year earlier. Output in China—the world’s largest producer—rose 21%, but growth fell across the year from 26% in January to well below 10% in November and December, in part because of shortages of coke and iron ore. Steel production outside of China grew less than 5%, with output in other Asian countries up 8%. Production grew in all regions except for North America and Eastern Europe. Steel producers are set to pay 65% more for iron ore starting April 1st. Brazil’s Vale—the world’s largest iron ore producer—has just settled with Japanese and Korean steel producers.

Grains prices surge on strong competition for feed, food and fuel

4

6

8

10

12

14

Jan-06Jul-06

Jan-07Jul-07

Jan-08

1

2

3

4

5$/bushel

Soybeans

Corn

Wheat

$/bushel

Source: DECPG Commodities Group.

Aluminum prices rise on electric power disruptions

1600

1800

2000

2200

2400

2600

2800

3000

3200

Jan-05Jan-06

Jan-07Jan-08

400

600

800

1000

1200

1400

1600

$/ton ‘000 tons

Aluminum price

LME stocks

Source: LME and DECPG Commodities Group.

Global steel production growth slowing

0

5

10

15

20

25

30

35

40

45

Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-0

China Other Asia Europe

FSU Other N America

mil tons

Source: LME and DECPG Commodities Group.

February 21, 2008 External Environment for Developing Countries page 11

International Finance

Slow start to 2008. Capital flows to developing countries began 2008 on a decidedly weak note—at $21 billion in January, some 63% below the $57 billion monthly average for 2007. A downturn in banking and equity led to the overall decline in the month, while bond issuance registered an increase to $7 billion from December’s $2 billion—in-line with traditional seasonal patterns. East Asia and Latin America cornered the lion’s share of bond financing (about 85%). Bank lending slumped to $8 billion in January, the lowest monthly volume since 2006. Emerging Europe accounted for much of this decline, after averaging $12 billion in borrowing per month in 2007. Equity placement fell 66% to $6 billion, tied to lack of issuance from Brazil and China. Equity valuations hit hard by the January market sell-off. World stock markets lost $5.2 trillion in market valuation during January as fears of a global economic slowdown and the fallout from the continued sub-prime turmoil led to a sharp decline in key markets, according to Standard & Poor’s. Fifty of 52 major world bourses lost ground, with 25 of them posting double-digit declines. Emerging markets fell 12.4% and mature markets lost 7.8% to post one of the worst-ever starts to a new year. This development is also emerging in global initial public offering (IPO) activity, with the January volume hitting a three-year low adverse conditions have prompted companies to shun the IPO market. Information tech led the decline. Global equities opened 2008 with heavy losses. All ten market sectors registered decline over 2008 to date, in contrast to 2007 when 8 sectors advanced. Info-technology posted the largest loss (14%) followed by the financial sector with an 11.8% falloff, which has deteriorated further this year. The Telecom sector was close behind with a 10.6% drop. Among other sectors, cyclicals such as Industrials and Consumer-Discretionary have performed poorly contrasted with more “defensive” sectors such as Healthcare and Utilities amid lingering fears of a U.S. recession.

Sharp decline in bank lending and equity placement in January

Source: DECPG Finance Team.

G ross capital flow s to em erging m arkets

$ billion 2005 2008

Total H 1 H 2 T otal H1 H 2 Tota l Jan

Tota l 361 209 285 494 357 326 683 21

Bonds 126 63 74 137 107 39 146 7

Banks 175 103 142 246 164 180 343 8

Equity 59 43 67 111 86 107 194 6

Lat. Am erica 87 51 65 116 69 88 157 6

Bonds 43 17 24 41 31 14 45 4

E. Europe 129 76 103 179 156 96 252 4

Bonds 55 28 36 64 50 14 64 1

Asia 107 56 97 153 100 113 213 10

Bonds 21 8 11 19 18 6 23 3

O thers 38 26 20 45 32 28 60 1

2006 2007

Equities tumbled in JanuaryS&P/Citi-Group BMI Global Index, ch%

-20

-15

-10

-5

0

5

10

15

20

25

Emerging MarketsMature Markets

Source: Standard & Poor’s.

January 2008

3 months:from October 2007

1 year:from January 2007

All sectors lost ground in January Total return by sector (based on MSCI world stock indices)

-20 -10 0 10 20 30 40

Utilities

Telecomm

Info-tech

Financials

Healthcare

Consumer Staple

Consumer Disr

Industrials

Materials

Energy

2008 to date

2007

Source: Bloomberg and DECPG calculations.

February 21, 2008 External Environment for Developing Countries page 12

EM sovereign spreads continue to widen. Benchmark spreads for emerging market debt continued to increase over the last months. Spreads over U.S. Treasuries widened from 150 basis points at the start of June 2007 to a recent high of 310 basis points. But in historic context, spreads remain low, reflecting improved EM credit fundamentals. And the yield on the U.S. 10-year T-note has eased 135 basis points over the same period, indicating that EM spreads have been heavily influenced by the rally in Treasuries. Meanwhile, emerging market debt-prices remain largely firm as investors appear to be holding on to higher-yielding bonds during the current period of heightened volatility. Banks at risk of additional write-downs. Banks worldwide have taken about $150 billion in write-downs to date, for losses related to sub-prime mortgages and collateralized debt obligations (CDOs), and could report additional write-downs of up to $200 billion, according to UBS AG. While major banks and securities firms such as Citigroup Inc. and Merrill Lynch & Co. accounted for most of the write-downs thus far, Standard & Poor’s expects that the next round will be borne largely by smaller financial institutions in Europe, Asia and the United States. Furthermore, the potential downgrading of major bond insurers, such as MBIA and Ambac, could trigger another round of write-downs. Corporate default risk at record highs. The risk of companies defaulting on their debt has increased to records levels in recent weeks, in both the United States and Europe, indicating a widespread perception of worsening credit quality. Banks are driving credit-default swaps (CDSs)—financial instruments based on bonds and loans that are used to speculate or hedge upon a company’s ability to repay debt—to the highest on record, as they seek to hedge mounting losses on sub-prime related securities. CDSs on the benchmark U.S. index traded at 365 basis points on February 18, after soaring earlier to as high as 385 basis points. The index has widened about 41%, or 27 basis points year-to-date. The European version of the benchmark is currently trading at a record 565 basis points, up sharply from 352 basis points in January.

Large credit write-downsreported by major banks

0 5 10 15 20 25

Barclay's

Wachovia

Deutsche Bank

JP Morgan

HSBC

Bank of America

Morgan Stanley

UBS

Merrill Lynch

Citigroup

Total write-downs, billions U.S. dollars

Source: Bloomberg.

100

200

300

400

500

600

Jan-07

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Source: JPMorgan-Chase.

Corporate default risk at record highsCredit default swaps, basis points

CDSs on benchmark European exchange

CDSs on the North American index

140

240

340

440

540

640

740

Jan-07

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Source: JPMorgan-Chase and Thomson/Datastream

Spreads widen, but yields stable EMBIG spread and U.S. 10-year T-note, basis points

EMBIG spreads

U.S. 10-year Treasury note

EMBIG yields

February 21, 2008 External Environment for Developing Countries page 13

Currencies

Dollar in trading range. Following the dollar’s fall of late 2007—brought about by developments in financial markets, monetary policy decisions and change in expectations regarding the economic outlook—the greenback appears to have settled into a trading range against the major currencies. Over January through mid-February 2008, the U.S. unit traded within a band of 2.5% around the euro, from trough levels of $1.48 to a peak of $1.45. Against the yen, the trading range has been larger (5.8%, from ¥105 to ¥112). Interest differentials with Europe continue to move against dollar-based assets (now at 140 basis points), though continued net capital inflow to the United States is providing some support for the greenback. Inflows to U.S. assets surprisingly strong. Data covering gross purchases and sales of U.S. and foreign long-term securities (the Treasury’s TICS system) offered upside surprises in developments through December. Following an exodus from U.S. securities in August (net foreign sales of $35 billion, the first such monthly decline since 1998), a return to net purchases occurred quickly, to $117 billion in September, and flows of $70 over the last 2 months of the year. But a notable shift in foreign preferences is underway: as yields on Treasuries dropped sharply, foreigners turned net sellers of official securities in December with an upturn in demand for private-sector paper. Amid uncertain financial conditions, net flows will remain volatile and clearly come to affect the dollar’s value. Commodity currencies shifting with views for economic growth. Tracking a set of so-called ‘commodity currencies’, those linked tightly to movements of particular energy- metals or agricultural goods, has shown diverse developments over late 2007 and early 2008. A tendency toward appreciation (decline in LCU per dollar) appears to have set in more recently, as markets take on board today’s prices and shifting prospects. Strength in grains benefit Australia and Brazil, and energy supports the C$ and Russian ruble. Stay tuned!

88

90

93

95

98

100

103

105

Jan-07

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Source: Thomson/Datastream.

Dollar in holding pattern against the majors since mid-January

index, LCU per USD, January 1, 2007 = 100

euro

yen

U.S. capital inflows up since August 2007– demand for Treasuries falling

billions U.S. dollars

-60

-30

0

30

60

90

120

150

180

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Source: TICS data system: U.S. Treasury.

o/w Treasuries/Agencies

Net foreign purchases of U.S. securities

o/w Private securities

88

90

93

95

98

100

103

105

108

110

Jul-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07 Jan-08 Feb-08

Source: Thomson/Datastream.

Commodity currencies tradingslightly stronger against the dollar

index, LCU per USD, July 1, 2007 = 100

A$rubleBrazil Rl

C$

February 21, 2008 External Environment for Developing Countries page 14

Weights Average 2007 2007 2007 2008

2000 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

World 100.0 3.4 4.5 5.9 5.5 5.3 7.6 5.7 3.7 0.5 0.0 0.4 ..

High-income countries 77.5 1.9 2.0 3.7 2.6 1.1 2.6 5.6 0.7 0.4 -0.6 0.4 ..

Industrial countries 73.0 1.9 2.0 3.9 2.8 1.0 2.6 5.9 0.9 0.4 -0.5 0.5 ..

United States 25.2 2.4 3.2 4.0 1.9 1.1 3.5 3.6 -1.0 -0.6 0.4 0.1 0.1

Japan 17.5 0.8 1.6 4.3 2.8 -5.6 1.6 8.0 6.2 1.4 -1.3 1.7 ..

Euro Area 23.0 1.9 0.8 3.4 2.9 3.9 0.6 5.3 0.2 0.5 -0.7 0.5 ..

United Kindgom 4.1 0.0 -2.0 0.1 0.4 -0.3 2.7 -0.1 0.4 0.5 -0.1 -0.1 ..

Other high income 4.5 .. 4.6 1.8 .. -2.8 6.7 7.5 .. 2.5 -1.7 .. ..

Hong Kong (China) 0.2 .. 2.4 2.5 .. -1.2 -3.8 -1.9 .. .. .. .. ..

Singapore 0.4 6.4 9.1 12.2 6.1 -12.5 23.2 29.8 -28.5 2.3 3.2 -5.1 ..

Taiwan (China) 1.1 5.5 3.7 5.7 8.2 6.6 22.9 23.2 5.9 4.7 -2.1 -2.3 ..

Developing countries 22.5 7.1 9.5 10.1 11.4 14.7 17.5 5.2 9.6 0.9 0.9 0.4 ..

East Asia and Pacific 8.7 11.0 13.7 14.3 15.9 19.3 27.3 8.3 10.6 0.0 1.4 1.2 ..

China 6.3 13.4 15.6 16.6 17.7 21.4 30.4 8.6 11.5 0.3 1.1 1.3 ..

Indonesia 0.9 .. 1.9 -1.9 .. 16.1 9.4 -4.4 .. -6.9 7.3 .. ..

Thailand 0.6 7.0 9.1 7.4 8.2 7.2 5.9 20.3 16.0 2.7 1.2 -0.5 ..

Malaysia 0.5 5.1 3.6 5.1 2.3 -2.7 8.5 3.8 8.4 -2.0 5.1 -0.2 ..

Europe and Central Asia 3.2 4.8 4.9 7.2 6.9 13.0 2.5 -1.3 7.1 1.4 1.3 -2.1 ..

Russian Federation 1.0 4.0 4.3 4.8 6.1 11.5 6.9 -8.4 8.9 1.4 -0.2 2.5 -2.1

Turkey 0.5 3.8 5.9 5.9 4.8 -4.8 2.3 4.8 14.3 -0.3 10.7 -12.5 ..

Poland 0.6 6.5 4.6 11.8 9.5 22.6 -3.2 6.6 7.9 1.8 0.1 -2.0 ..

Czech Republic 0.2 5.3 7.3 11.0 8.0 25.6 -7.1 -1.3 5.6 3.5 0.9 -3.9 ..

Latin America and Caribbean 5.9 2.0 3.9 4.3 4.4 3.7 6.4 4.6 6.5 2.6 -0.9 -0.5 ..

Brazil 1.5 2.8 3.4 2.9 5.9 5.9 9.9 7.0 7.7 3.3 -2.0 -0.6 ..

Mexico 1.7 2.5 2.1 5.1 1.3 -1.4 4.6 2.8 -0.2 0.3 -0.1 -0.1 ..

Argentina 0.8 .. 7.3 7.4 .. 1.2 6.6 3.0 .. 2.6 1.7 .. ..

Colombia 0.3 .. 3.9 10.9 .. 13.6 9.7 3.3 .. 2.4 .. .. ..

Middle East and North Africa 1.9 .. 4.2 -0.3 .. 0.5 -0.6 -4.0 .. 0.8 1.1 .. ..

Saudi Arabia 1.2 .. 4.9 -4.1 .. -5.4 -3.3 -1.8 .. 1.2 1.9 .. ..

Iran 0.4 .. 3.4 -2.7 .. -6.1 -3.6 -3.9 .. 0.8 0.2 .. ..

Egypt 0.4 .. .. .. .. .. .. .. .. .. ..

Algeria 0.3 .. 7.2 1.0 .. 2.9 0.2 -1.5 .. 0.7 0.9 .. ..

South Asia 1.6 6.9 9.1 10.6 9.6 15.5 10.0 2.5 8.4 1.2 0.9 0.9 ..

India 1.3 6.7 7.9 10.6 9.9 15.7 6.7 2.3 8.7 1.2 0.9 0.9 ..

Pakistan 0.2 .. 15.0 10.7 .. 14.0 34.2 .. .. .. .. .. ..

Bangladesh 0.1 .. 12.6 .. .. .. .. .. .. .. .. .. ..

Sri Lanka 0.0 .. .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa 1.1 .. 5.0 4.5 .. .. .. .. .. .. .. .. ..

South Africa 0.4 2.2 3.6 4.8 4.2 6.3 0.6 -3.2 10.5 7.1 -0.7 -2.5 ..

Nigeria 0.2 .. 0.0 0.1 .. .. .. .. .. .. .. .. ..

Memo:

OECD 76.2 2.0 2.1 4.1 2.9 1.6 2.2 5.5 1.0 0.4 -0.3 0.2 ..

Developing excl. China 16.2 .. 4.8 5.0 .. 8.3 5.8 1.5 .. 1.4 1.0 .. ..

Developing oil exporters 2.8 .. 2.6 -1.2 .. 2.2 3.1 -3.3 .. -2.1 3.1 .. ..

Dev. non-oil exporters 19.7 7.9 10.4 11.5 12.4 15.8 18.6 5.8 10.5 1.1 0.8 0.4 ..

Asian high tech exporters .. .. .. .. .. .. .. .. .. .. ..

Table A.1 Global industrial production growth(constant prices; percent; seasonally adjusted annual rates except monthly figures which are in percent change over previous month a/)

aIn general, series refer to industrial production excluding construction (e.g. manufacturing, mining and utilitites). Where this is not available the closest proxy is used, often manufacturing output or oil output, if the country is a major oil producer.

February 21, 2008 External Environment for Developing Countries page 15

Weights Average 2007 2007 2007 2008

1995 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

Real GDP a

High-income countries 78.4 .. 2.5 2.9 .. 1.9 2.2 4.2 .. .. .. .. ..

Industrial countries 75.3 .. 2.4 2.8 .. 2.3 2.2 3.6 .. .. .. .. ..

United States 10.9 2.9 3.1 2.9 2.2 0.6 3.8 4.9 0.6 .. .. .. ..

Japan 20.7 1.2 1.9 2.4 2.1 3.9 -1.4 1.3 3.7 .. .. .. ..

Euro Area 27.4 .. 1.6 2.9 .. 3.3 1.2 3.1 .. .. .. .. ..

United Kindgom 6.4 .. 1.8 2.9 .. 3.1 3.4 2.7 .. .. .. .. ..

Other high income 3.1 .. 5.5 5.8 .. -10.0 3.0 24.2 .. .. .. .. ..

Hong Kong (China) 0.7 .. 7.1 6.8 .. -27.3 4.9 37.7 .. .. .. .. ..

Singapore 0.4 5.2 7.3 8.2 7.7 9.2 13.4 5.1 -4.8 .. .. .. ..

Taiwan (China) 1.4 .. 4.2 4.9 .. -10.3 -2.2 31.9 .. .. .. .. ..

Real merchandise imports b

High-income countries 100.0 .. 6.6 6.8 .. 4.4 3.1 3.9 .. .. .. .. ..

Industrial countries 88.3 .. 6.0 6.3 2.5 3.4 1.4 2.8 2.3 1.5 -0.5 -1.0 ..

United States 23.8 8.2 5.9 5.7 1.1 2.8 2.1 0.4 -0.7 -0.4 0.6 -1.2 ..

Japan 6.7 5.2 3.5 3.9 -3.0 -0.3 -3.6 -4.5 -3.6 1.0 3.2 0.3 ..

Euro Area 37.1 .. 5.7 5.4 6.2 9.1 5.1 5.9 4.8 3.5 -4.3 0.7 ..

United Kindgom 6.7 6.3 6.8 10.9 -5.6 -10.9 -14.3 2.7 2.0 -0.2 0.1 -2.8 ..

Other high income 11.7 5.5 9.4 9.3 .. 8.8 11.0 9.2 .. .. .. .. ..

Hong Kong (China) 4.1 6.6 8.5 10.1 10.4 8.6 13.0 9.9 10.2 1.3 1.6 0.7 ..

Singapore 2.3 5.2 8.6 11.2 6.3 7.5 6.1 3.5 8.4 2.1 2.5 -1.6 9.2

Taiwan (China) 2.2 .. 1.1 3.6 -0.1 -4.5 1.2 2.8 0.2 -3.1 -8.6 18.7 -2.9

Import Prices c

High-income countries 100.0 .. 6.7 6.2 .. 4.5 4.6 5.4 .. .. .. .. ..

Industrial countries 88.3 .. 7.2 6.6 7.4 4.9 5.3 6.2 13.1 1.6 4.4 -0.1 ..

United States 23.8 -0.1 7.5 4.9 4.2 1.3 1.9 3.2 10.5 1.5 3.1 -0.2 1.7

Japan 6.7 -1.4 10.2 8.2 10.3 4.3 8.0 10.2 18.6 1.2 4.5 2.6 ..

Euro Area 37.1 .. 7.6 9.1 8.6 6.7 6.7 7.1 14.0 0.9 7.2 -0.9 ..

United Kindgom 6.7 -1.1 3.6 5.0 10.1 10.6 9.1 8.7 12.0 2.2 2.7 -1.5 ..

Other high income 11.7 -1.0 4.4 4.6 .. 2.8 2.0 2.1 .. .. .. .. ..

Hong Kong (China) 4.1 -1.2 1.9 1.2 -0.3 0.0 -0.5 -0.9 0.1 0.3 -0.1 -0.2 ..

Singapore 2.3 -0.2 6.4 7.5 3.4 1.3 0.6 1.5 10.2 2.6 2.4 0.5 1.8

Taiwan (China) 2.2 -1.6 6.4 7.6 8.0 6.5 6.2 5.8 13.2 1.9 3.4 -0.1 1.6

Real effective exchange rates d

Euro Area 33.5 1.5 -0.8 0.9 4.1 4.1 3.2 2.8 6.3 1.0 1.9 -0.6 0.7

United States 14.4 -0.9 -2.7 -2.7 -4.7 -3.0 -3.7 -4.3 -7.8 -2.1 -1.5 1.5 -1.0

Japan 7.4 -2.5 -5.1 -8.9 -6.5 -6.8 -9.5 -6.2 -3.2 -2.0 2.6 -0.8 3.4

United Kindgom 5.4 0.0 -2.4 -0.2 2.2 5.8 3.7 2.1 -2.6 -0.5 -1.1 -1.4 -3.7

Canada 3.5 0.5 3.4 3.3 0.8 -6.3 -1.8 2.8 8.8 3.7 -0.2 -4.5 -1.6

Hong Kong (China) 3.5 -2.7 -3.7 -2.6 -4.9 -4.0 -5.1 -4.4 -6.0 -0.1 -0.5 0.1 -2.8

Korea, Rep. 2.5 0.6 10.4 6.9 -0.5 0.9 0.4 -0.6 -2.7 1.2 -1.8 -0.5 -3.7

Singapore 2.3 0.9 4.6 5.4 7.3 9.2 9.7 6.1 4.5 0.8 -1.3 -0.1 0.2

Taiwan (China) 2.1 -2.1 -1.9 0.2 -1.2 0.9 0.3 -2.6 -3.2 0.1 -1.0 0.4 -2.7

Switzerland 1.7 -0.7 -3.8 -4.3 -4.8 -4.3 -6.0 -4.9 -4.1 0.1 1.6 -0.2 1.2

Table A.2 Demand conditions in high-income countries(US dollar values unless otherwise indicated; percent change; seasonally adjusted annual rates except monthly figures, which are m/m change)

a/ Real GDP aggregated using 1995 weights.b/ On a customs or BoP basis, as available. Weights are 1995 merchandise import: aggregate calculated as sum of components.c/ Aggregate prices are implicit prices of aggregate US dollar value divided by aggregate constant 1995 dollar volume.d/ JP Morgan Trade Weighted Indices (Real, Broad basis). Data are averages of monthly data for the period in question.

February 21, 2008 External Environment for Developing Countries page 16

Weights Average 2007 2007 2007 2008 Latest

1995 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Nov Dec Jan 20-Feb

Policy Rates

United States .. 3.78 3.21 4.96 5.02 5.26 5.25 5.09 4.48 4.50 4.21 3.90 2.97

Japan .. 0.31 0.10 0.24 0.70 0.55 0.75 0.75 0.75 0.75 0.75 0.75 0.75

Euro Area .. .. 2.02 2.76 3.84 3.55 3.80 4.00 4.00 4.00 4.00 4.00 4.00

United Kindgom .. 5.05 4.65 4.64 5.51 5.22 5.39 5.74 5.68 5.75 5.54 5.50 5.25

Ten year bond

United States .. 4.86 4.28 4.78 4.63 4.67 4.82 4.74 4.27 4.24 4.05 3.75 3.69

Japan .. 1.49 1.38 1.74 1.67 1.66 1.73 1.72 1.56 1.52 1.49 1.43 1.42

Euro Area .. .. 3.35 3.73 4.20 3.92 4.31 4.35 4.23 4.13 4.25 4.07 3.95

United Kindgom .. 4.88 4.41 4.48 5.01 4.85 5.17 5.19 4.82 4.77 4.70 4.46 4.61

Spreads (Basis points)b,c

Developing countries .. 455 306 198 197 176 162 216 235 248 250 279 292

East Asia and Pacific .. 243 265 180 161 138 129 181 197 211 211 250 252

China .. 76 58 64 71 51 51 76 104 105 121 129 137

Indonesia .. .. .. .. .. .. .. .. .. .. .. .. ..

Thailand .. .. 50 54 .. .. .. .. .. .. .. .. ..

Malaysia .. 134 84 84 87 70 70 97 109 108 119 120 125

Europe and Central Asia .. 352 185 149 158 147 134 165 185 196 194 219 229

Russian Federation .. 348 156 111 121 106 97 131 152 165 158 178 188

Turkey .. 476 274 223 214 216 193 219 229 238 235 269 277

Poland .. 106 51 59 61 52 52 69 73 73 78 89 115

Czech Republic .. .. .. .. .. .. .. .. .. .. .. .. ..

Latin America and Caribbean .. 549 364 213 208 183 167 231 251 264 270 296 315

Brazil .. 635 394 233 180 186 150 187 198 211 214 242 261

Mexico .. 221 167 137 126 122 102 130 150 158 165 187 196

Argentina .. 3020 2586 343 320 210 267 414 388 399 394 442 475

Colombia .. 412 323 194 161 166 127 167 182 197 188 240 255

Middle East and North Africa .. .. 324 338 476 418 434 514 539 552 529 549 538

Saudi Arabia .. .. .. .. .. .. .. .. .. .. .. .. ..

Iran .. .. .. .. .. .. .. .. .. .. .. .. ..

Egypt .. .. 65 79 86 57 52 80 154 163 187 212 222

Algeria .. .. .. .. .. .. .. .. .. .. .. .. ..

South Asia d .. .. .. .. .. .. .. .. .. .. .. .. ..

India .. .. .. .. .. .. .. .. .. .. .. .. ..

Pakistan .. .. 199 199 283 166 171 374 423 483 443 584 552

Bangladesh .. .. .. .. .. .. .. .. .. .. .. .. ..

Sri Lanka .. .. .. .. .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa .. 443 277 266 288 283 270 285 315 324 337 374 402

South Africa .. 169 95 90 100 76 68 118 138 142 154 193 234

Nigeria .. 746 417 245 77 96 23 .. .. .. .. .. ..

Gross inflows e

Developing countries .. .. 361 494 683 166 191 179 147 53 40 21 ..

East Asia and Pacific .. .. 85 111 145 18 50 38 38 17 8 7 ..

Europe and Central Asia .. .. 129 179 252 81 74 47 49 19 15 4 ..

Latin America and Carribean .. .. 87 116 157 38 31 57 32 9 6 6 ..

Middle East and North Africa .. .. 22 16 15 4 2 6 3 1 1 0 ..

South Asia .. .. 22 42 69 12 20 22 15 5 6 3 ..

Sub-Saharan Africa .. .. 15 30 46 13 14 9 10 2 4 1 ..

Table A.3 Global credit conditions(percent unless otherwise indicated a/)

a/Monthly figures are simple averages of the daily figures, except the last month, which are the values reported on the mentioned date. Quarterly and Annual figures are simple averages of the monthly figures.b/Average values for Spreads are for the period 1996-2003.c/Aggregates as defined by JP Morgan.d/East Asia and Pacific including South Asian countries.e/In billions of US dollars.

February 21, 2008 External Environment for Developing Countries page 17

Weightsb Average 2007 2007 2007 2008

1990 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

Energy .. .. 233.4 281.0 310.8 250.1 289.1 321.2 382.9 358.3 399.2 391.3 396.4

Coal, Australia .. 6.5 120.1 123.8 165.7 134.1 146.0 172.4 210.4 188.6 213.3 229.4 231.3

Crude oil, average .. 14.0 233.4 281.0 310.8 250.1 289.1 321.2 382.9 358.3 399.2 391.3 396.4

Natural gas , Europe .. 12.1 248.1 332.2 335.5 333.6 313.9 326.9 367.6 359.2 371.4 372.2 419.6

Non-energy 100.00 .. 121.9 151.8 175.7 163.6 176.9 177.8 184.7 185.1 184.2 184.8 194.8

Agriculture 69.10 .. 113.0 126.6 145.6 135.6 140.4 147.0 159.3 155.4 159.3 163.3 170.6

Beverages 16.90 .. 116.9 122.5 139.4 132.2 135.2 141.3 149.0 147.3 146.4 153.4 158.5

Cocoa 3.90 1.9 121.4 125.7 154.1 143.1 157.9 157.8 157.7 150.9 155.4 166.8 173.8

Coffee, arabica 8.00 -4.2 128.4 127.9 138.1 135.5 129.4 137.4 150.1 150.1 146.4 153.8 156.3

Coffee, robusta 2.80 1.0 94.3 126.0 161.6 146.3 159.3 169.6 171.1 170.0 172.7 170.5 185.1

Food 29.40 .. 109.9 120.6 146.0 129.9 136.5 149.4 168.3 161.6 168.3 174.9 185.8

Fats and oils 10.10 .. 122.9 126.4 191.2 155.3 174.3 196.7 238.4 224.5 240.9 249.7 266.9

Palm oil 2.30 3.6 145.7 165.1 269.3 210.1 263.1 283.8 320.2 304.1 328.6 327.9 365.5

Soybean meal 4.10 1.1 107.1 104.5 153.3 127.7 130.1 154.6 200.9 191.8 198.3 212.5 216.8

Soybeans 2.00 2.7 111.3 108.9 155.6 128.7 137.1 160.3 196.5 182.4 198.2 208.8 219.3

Grains 6.90 .. 103.2 120.9 148.8 137.5 135.8 149.9 172.1 166.1 167.2 182.8 192.6

Maize 1.70 3.4 90.3 111.5 149.8 156.4 145.9 139.5 157.3 150.2 156.7 165.0 188.8

Rice, Thailand, 5% 2.90 0.7 105.7 112.6 120.5 116.5 117.8 120.8 127.0 121.5 126.3 133.2 138.7

Wheat, US, HRW 1.90 4.8 112.4 141.7 188.3 146.4 151.8 202.8 252.3 247.3 237.5 272.0 273.5

Other food 12.40 .. 103.1 115.7 107.5 104.9 105.9 110.4 108.7 107.5 109.4 109.2 115.6

Bananas, US 2.30 2.7 111.5 125.2 125.0 119.7 130.4 129.2 120.6 121.8 120.4 119.7 127.4

Sugar, world 7.50 -0.2 94.0 112.3 95.5 95.6 92.6 95.3 98.4 96.6 98.3 100.3 105.8

Raw materials 22.80 .. 114.1 137.4 149.5 145.3 149.2 148.2 155.4 153.4 157.3 155.6 159.9

Cotton ("A" Index) 5.90 -2.2 66.9 69.6 76.7 70.8 70.0 81.8 84.1 83.6 84.5 84.3 89.6

Rubber, Singapore 4.80 8.5 173.7 243.8 264.9 258.2 270.4 247.3 283.5 272.6 289.8 288.0 296.7

Sawnwood, Malaysia 2.90 2.0 123.7 140.6 151.3 149.0 151.5 154.0 150.5 152.5 151.2 147.9 150.2

Fertilizers 2.70 .. 134.9 136.8 227.2 149.6 213.3 252.6 293.0 266.1 276.1 336.9 431.0

Triple superphosphate 0.90 7.0 152.8 153.0 257.2 171.2 251.1 284.5 322.0 305.6 321.5 339.0 409.0

Metals and minerals 28.20 .. 142.5 215.0 244.9 233.9 263.0 246.1 236.6 250.3 236.5 223.0 231.5

Aluminum 7.90 5.1 115.8 156.8 160.9 170.9 168.4 155.3 149.1 149.0 152.9 145.3 149.2

Copper 9.30 12.1 138.2 252.6 267.5 222.9 287.1 289.8 270.1 300.9 261.8 247.5 265.3

Gold .. 7.7 116.0 157.6 181.7 169.6 174.1 177.6 205.5 196.8 210.3 209.5 232.0

Nickel 2.20 18.3 166.3 273.6 420.0 467.5 542.1 340.8 329.6 350.4 345.3 293.2 312.4

Memo:

Crude Oil (US$) .. 14.0 53.4 64.3 71.1 57.2 66.1 73.5 87.6 82.0 91.3 89.5 90.7

Table A.4 Commodity price indices(current US dollar index,index unless otherwise indicated; a/)

a/ The World Bank primary commodity price indices are computed from 1987-89 export values in US dollars for low- and middle-income economies, rebased to 1990.b/ Energy and gold prices are not included in the index.

February 21, 2008 External Environment for Developing Countries page 18

Weightsb Average 2007 2007 2007 2007

2004 1998-04 2005 2006 2007 Q1 Q2 Q3 Q4 Sep Oct Nov Dec

Global semiconductor sales /a

World 100.00 8.9 6.8 8.9 3.4 -10.7 -1.8 35.1 -6.5 -1.7 3.8 -4.6 -0.1

North America 22.29 10.3 4.3 10.3 -5.9 -29.9 3.4 46.9 -19.1 1.3 10.7 -15.1 1.3

Europe 19.67 1.6 -0.4 1.6 3.0 1.2 2.0 13.6 -10.2 -5.7 3.3 -2.1 -0.3

Japan 21.76 5.3 -3.7 5.3 4.3 6.4 5.3 25.1 9.4 -1.4 2.1 -0.3 3.2

Other Asia 36.29 12.7 16.5 12.7 6.8 -6.4 -8.6 39.0 -8.3 -1.6 1.5 -2.9 -2.4

Semiconductor prices

World /a 0.4 1.9 -4.8 -7.4 -26.3 -36.0 15.1 11.6 3.2 -4.0 3.3 5.9

United States PPI -2.6 -2.3 -1.8 -6.2 -11.6 -11.2 -6.2 -6.2 0.0 -0.1 -1.7 0.1

U.S. computer/software prices -19.3 -13.7 -13.3 -14.0 -3.9 -8.8 -14.8 -14.8 -0.3 -1.1 -3.1 -0.4

Memo:PHLX Semichip Equity Index 7.2 20.3 -3.4 8.6 1.7 -1.7 0.0 0.0 1.0 -10.0 -8.8 -1.7

G-3 high-tech orders 100.00 -1.1 -1.7 6.1 -1.1 -9.2 14.0 11.9 -7.8 0.8 -3.5 1.8 2.4

United States 70.00 -1.9 -0.4 11.0 -1.9 -13.4 15.6 24.0 -15.5 5.5 -8.2 -0.2 4.1

Japan 17.00 0.6 -3.8 -2.6 0.6 -0.5 10.4 -9.2 9.6 -9.0 7.7 6.1 -0.8

Germany 13.00 4.6 8.7 9.6 4.6 38.3 39.3 -8.0 72.0 -3.1 12.7 4.8 -0.7

Euro Area -2.6 -3.1 -2.1 -2.6 7.3 3.5 1.7 ..... 2.0 1.4 -7.3 .....

High-tech industrial production

Selected high-income countries 100.00 13.7 13.7 20.8 15.5 5.7 15.0 24.3 14.2 -1.1 3.1 0.8 0.4

United States 68.00 19.3 18.6 26.6 19.6 9.2 16.6 26.4 17.2 0.8 2.2 1.3 1.0

Japan 15.50 -0.9 0.5 4.0 4.2 -9.9 11.6 26.5 8.3 -11.2 10.7 -1.4 -1.9

Germany 11.50 4.6 7.7 14.5 11.3 5.6 13.6 15.9 8.5 0.8 0.4 0.7 0.5

Finland 5.00 3.9 1.7 8.9 5.2 6.8 7.9 6.7 4.1 1.0 -0.4 2.4 -2.0

Euro Area 0.9 3.5 9.8 23.3 30.0 22.0 28.3 16.4 0.7 2.5 0.8 -0.5

East Asian NIEs 100.00 6.3 3.5 6.1 4.1 -3.8 21.2 40.0 -10.9 -5.0 4.8 -1.7 -1.5

Korea 38.00 9.2 5.8 11.3 8.5 -3.1 19.7 18.3 0.0 0.1 3.6 -0.5 -0.4

Singapore 30.00 7.1 9.5 11.9 5.8 -15.6 26.4 28.2 -28.0 -8.4 2.3 3.3 -4.8

Taiwan 32.00 2.3 -4.9 -5.4 -2.6 6.5 18.1 76.8 -7.8 -7.8 8.6 -7.9 0.2

ASEAN countries 100.00 15.2 19.0 14.0 11.3 3.6 5.9 35.5 26.3 -1.0 0.8 5.5 1.1

Malaysia 60.00 9.0 5.1 7.5 1.9 -2.8 4.5 7.9 9.6 0.7 -2.7 6.0 1.6

Thailand 40.00 24.5 39.7 23.7 25.3 13.2 7.9 76.8 51.5 -3.5 6.0 4.6 0.3

High-tech exports

Selected high-income countries 100.00 3.7 10.3 14.4 0.9 -1.2 -10.2 11.7 11.7 -1.0 1.3 -0.3 3.1

United States 47.00 1.4 3.7 7.9 2.4 -8.6 -12.2 11.0 6.7 0.4 0.3 -1.3 6.4

Japan 53.00 5.7 16.2 20.1 -0.4 5.3 -8.4 12.4 16.1 -2.2 2.1 0.7 0.1

East Asian NIEs 100.00 8.7 9.5 11.9 ..... -3.2 8.0 16.7 ..... -3.6 4.6 -0.5 -1.3

Hong Kong (SAR, China) 30.00 14.0 19.7 12.2 14.1 2.8 10.9 3.4 23.8 -2.0 4.9 0.8 -0.5

Korea 17.00 5.3 11.0 13.4 ..... 16.2 0.8 -4.7 ..... -17.4 17.9 1.7 -5.2

Singapore 13.00 2.8 3.5 3.5 -6.6 -49.9 -14.4 49.8 -6.4 -6.6 5.2 -3.4 -8.6

Taiwan 40.00 8.2 3.1 13.7 ..... -0.7 16.3 25.0 ..... 2.0 -1.5 -1.6 2.2

ASEAN countries 100.00 11.1 8.9 11.8 13.4 10.2 17.2 19.6 20.4 -5.5 3.3 6.0 -3.9

Malaysia 60.00 10.0 11.3 13.8 9.8 2.7 14.4 16.9 35.1 -2.5 2.4 16.0 -12.1

Thailand 40.00 12.6 5.3 8.9 18.9 21.4 21.3 23.6 -1.6 -10.1 4.7 -8.9 8.3

Memo:

U.S. retail sales, electronics 6.6 8.2 6.6 3.1 3.2 -3.3 6.1 5.3 0.7 0.4 2.2 -3.2

Semiconductor production

United States 30.0 20.9 36.3 18.6 -6.9 9.5 43.7 19.5 1.0 2.9 0.5 1.2

Japan 3.2 -0.9 15.2 6.9 -16.4 11.7 32.1 30.3 0.9 9.7 -3.1 -0.3

Singapore 17.7 9.8 30.6 15.9 -2.2 31.5 37.7 5.3 17.5 -1.1 -8.5 2.4

China 51.0 34.6 26.1 3.0 -43.9 103.8 63.1 18.6 19.4 -3.3 -1.2 -7.4

Table A.5 High-tech Market Indicators(U.S. dollar values, unless otherwise indicated; percent change saar, except monthly figures which are m/m change).

/a Source: Semiconductor Industry Association.

February 21, 2008 External Environment for Developing Countries page 19

Weights Average 2007 2007 2007 2008

2000 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

Export valuesDeveloping countries 100.0 14.1 23.1 22.1 19.6 21.6 21.8 17.5 33.1 9.6 -0.1 -3.1 ..

East Asia and Pacific 36.3 15.7 23.0 23.4 21.7 34.7 12.5 16.7 21.3 10.0 -2.1 -3.7 ..

China 16.7 20.9 28.4 27.2 25.7 50.5 10.3 20.8 11.4 9.1 -1.7 -5.2 27.7

Indonesia 4.2 7.8 19.7 17.7 13.1 5.3 22.1 0.8 26.7 2.6 8.2 -1.2 ..

Thailand 4.6 10.1 15.0 16.9 17.5 17.2 21.6 -0.1 63.8 12.9 1.6 -3.0 ..

Europe and Central Asia 20.7 16.2 21.9 22.9 23.0 22.5 22.3 21.8 59.0 12.7 2.1 -3.1 ..

Russian Federation 7.1 15.1 33.1 24.7 16.9 6.3 33.2 18.7 110.3 21.3 3.5 -1.2 ..

Turkey 1.8 15.1 16.3 16.4 25.3 48.2 13.7 20.3 23.1 13.0 -3.5 -10.3 ..

Poland 2.1 .. 19.3 24.3 .. 16.2 25.2 21.1 .. 6.7 3.3 .. ..

Latin America and Caribbean 24.0 9.5 20.4 18.5 12.6 5.2 24.9 13.7 32.0 6.1 -0.4 -1.2 ..

Brazil 3.7 11.7 22.6 16.3 16.7 21.9 24.9 -3.2 39.6 8.2 -2.8 -0.6 7.6

Mexico 11.2 9.4 14.0 16.7 8.9 0.6 23.1 24.2 11.5 -1.5 3.4 -0.3 ..

Argentina 1.8 7.8 16.8 15.1 20.4 -7.4 17.9 45.3 94.3 15.1 -1.0 2.0 ..

Middle East and North Africa 8.3 .. 31.8 27.4 .. -8.9 .. .. .. .. .. .. ..

Saudi Arabia 5.2 .. 39.4 21.0 .. -15.9 .. .. .. .. .. .. ..

Iran 1.9 .. .. .. .. .. .. .. .. .. .. .. ..

Egypt 0.3 .. 34.6 32.5 .. 32.9 10.4 2.5 .. 12.9 11.9 .. ..

South Asia 4.3 13.5 27.8 15.7 20.9 3.6 65.2 29.0 16.3 6.0 -0.8 -4.3 ..

India 2.8 15.8 31.5 17.0 23.8 7.6 72.5 35.0 14.9 6.2 -3.0 -1.0 ..

Pakistan 0.6 7.2 23.2 6.1 3.0 -24.9 20.1 3.5 22.0 4.4 18.9 -28.4 27.4

Bangladesh 0.4 .. 14.1 .. .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa 6.3 .. 27.2 21.1 .. 17.4 .. .. .. .. .. .. ..

South Africa 2.0 8.5 12.7 12.0 20.1 21.6 25.0 -5.3 49.1 1.1 14.8 -2.5 ..

Nigeria 1.4 .. 30.6 23.8 .. -9.1 .. .. .. .. .. .. ..

Export prices b,c

Developing countries 100.0 .. 7.3 6.4 .. 8.3 6.8 1.3 .. 4.7 .. .. ..

East Asia and Pacific 36.3 0.3 4.6 3.1 1.6 1.4 2.7 -0.6 10.0 2.0 0.5 0.6 ..

China 16.7 -1.2 2.9 0.8 0.5 -1.5 2.0 1.5 4.2 0.8 -0.3 0.3 ..

Indonesia 4.2 5.1 15.6 17.0 8.8 0.1 47.5 -1.8 29.9 4.3 3.4 1.8 ..

Thailand 4.6 3.3 7.2 5.2 5.7 9.5 11.9 -0.3 13.4 1.5 1.5 0.3 ..

Europe and Central Asia 20.7 .. 8.2 8.7 .. .. .. .. .. .. .. .. ..

Russian Federation 7.1 .. 22.8 17.1 .. 11.1 50.4 30.0 .. 1.7 4.9 .. ..

Turkey 1.8 1.8 5.7 3.5 12.7 20.7 17.9 11.6 28.7 3.3 3.7 1.3 ..

Poland 2.1 .. -12.8 6.4 .. 0.1 -14.7 1.2 .. 1.1 .. .. ..

Latin America and Caribbean 24.0 .. 11.1 10.9 .. -2.4 16.7 15.1 .. .. .. .. ..

Brazil 3.7 2.3 12.1 12.5 10.5 -0.4 16.1 19.1 24.8 3.0 1.4 2.4 ..

Mexico 11.2 4.2 8.2 7.5 5.1 -2.7 15.4 12.8 19.7 2.4 2.1 -0.4 ..

Argentina 1.8 .. 1.7 8.5 .. 12.6 12.8 11.5 .. .. .. .. ..

Middle East and North Africa 8.3 .. .. .. .. .. .. .. .. .. .. .. ..

Saudi Arabia 5.2 .. 46.0 22.7 .. -14.8 91.0 28.7 .. -2.6 .. .. ..

Iran 1.9 .. 71.6 .. .. .. .. .. .. .. .. .. ..

Egypt 0.3 .. -0.4 .. .. .. .. .. .. .. .. .. ..

South Asia 4.3 .. 1.5 4.0 .. 14.1 12.1 .. .. .. .. .. ..

India 2.8 2.4 11.0 3.3 9.4 10.7 12.0 12.2 11.2 0.9 0.9 0.8 0.8

Pakistan 0.6 .. 0.4 2.5 .. -2.4 24.5 .. .. .. .. .. ..

Bangladesh 0.4 .. -38.2 .. .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa 6.3 .. 10.7 .. .. .. .. .. .. .. .. .. ..

South Africa 2.0 .. 6.6 8.1 .. 13.8 26.0 7.5 .. .. .. .. ..

Nigeria 1.4 .. 35.0 .. .. .. .. .. .. .. .. .. ..

Table A.6 Developing countries' merchandise export growth(US dollar values unless otherwise indicated; percent change; seasonally adjusted annual rates except monthly figures, which are m/m change /a)

/a Merchandise export (F.O.B), customs basis./b Implicit export unit values, U.S. Dollar basis./c In many cases countries are very late in reporting trade prices. To estimate more timely figures individual trade prices were updated using the median (mean) regional trade price for developing (developed) countries whenever 60% or more of reporters by trade weight reported.

February 21, 2008 External Environment for Developing Countries page 20

Weights Average 2007 2007 2007 2008

2000 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

Import valuesDeveloping countries 100.0 .. .. .. .. 12.7 17.7 27.5 39.0 11.7 -0.2 -2.1 ..

East Asia and Pacific 35.2 14.3 17.4 16.7 18.6 24.9 -1.3 32.9 45.5 13.8 0.2 -1.1 ..

China 19.3 21.0 17.6 19.9 20.8 33.7 -10.1 45.1 42.3 11.7 1.2 -1.7 15.0

Indonesia 2.1 5.9 24.0 5.8 21.6 22.4 53.5 19.5 45.1 -0.2 11.2 -2.2 ..

Thailand 4.2 8.3 25.7 9.0 8.7 -19.9 26.0 25.6 39.9 10.3 -0.9 0.0 ..

Europe and Central Asia 24.1 .. .. .. .. 23.6 26.5 25.3 .. 9.7 0.7 .. ..

Russian Federation 3.9 12.0 28.8 31.3 35.4 -10.4 73.3 37.5 51.1 15.4 -2.3 -2.3 ..

Turkey 3.2 13.3 19.7 19.5 21.8 53.0 13.9 18.9 41.2 13.4 -3.3 -10.3 ..

Poland 3.6 .. 13.5 25.5 .. 11.1 29.0 15.7 .. 3.9 5.8 .. ..

Latin America and Caribbean 22.9 8.6 18.0 19.3 18.6 18.8 19.3 34.1 21.9 5.2 -1.6 2.6 ..

Brazil 3.2 7.3 17.2 24.2 32.0 40.0 26.7 57.2 47.0 10.5 -1.7 -0.2 10.8

Mexico 11.6 9.9 12.7 15.4 10.6 6.3 25.3 16.1 2.5 -0.9 -2.5 4.1 ..

Argentina 0.6 3.9 27.8 19.0 31.1 44.1 10.7 99.9 11.6 8.3 -2.4 -0.6 ..

Middle East and North Africa 6.9 .. 18.0 8.9 .. 23.9 .. .. .. .. .. .. ..

Saudi Arabia 2.0 .. 18.5 20.2 .. 34.2 32.9 3.4 .. -8.8 .. .. ..

Iran 1.4 .. 13.1 7.3 .. 9.5 .. .. .. .. .. .. ..

Egypt 0.8 .. 54.4 3.9 .. 67.1 20.0 -4.3 .. 18.4 10.1 .. ..

South Asia 5.5 15.6 37.2 21.4 22.1 -14.5 97.1 -0.9 39.8 24.1 -2.3 -13.9 ..

India 3.7 18.5 42.0 21.9 26.4 -18.9 124.8 -6.6 36.6 24.1 -0.9 -11.8 ..

Pakistan 0.7 10.9 41.3 17.6 9.3 6.6 1.5 35.3 40.2 25.1 -10.6 -27.4 71.2

Bangladesh 0.5 .. 12.0 25.0 .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa 5.5 .. 34.4 88.4 .. -33.8 .. .. .. .. .. .. ..

South Africa 1.9 11.0 15.6 23.3 18.1 1.2 10.4 14.0 38.2 11.0 -5.0 25.4 ..

Nigeria 0.5 .. 19.6 20.0 .. 50.0 .. .. .. .. .. .. ..

Import prices b,c

Developing countries 100.0 .. .. .. .. .. .. .. .. .. .. .. ..

East Asia and Pacific 35.2 .. .. .. .. .. .. .. .. .. .. .. ..

China 19.3 .. .. .. .. .. .. .. .. .. .. .. ..

Indonesia 2.1 8.9 5.1 17.1 14.8 8.3 42.6 -2.7 46.3 5.3 5.3 0.1 ..

Thailand 4.2 1.8 6.3 6.5 5.4 -1.3 13.8 11.8 18.5 1.7 2.3 1.4 ..

Europe and Central Asia 24.1 .. .. .. .. .. .. .. .. .. .. .. ..

Russian Federation 3.9 .. 7.3 7.6 .. .. .. .. .. .. .. .. ..

Turkey 3.2 3.2 6.9 10.0 9.2 1.8 2.3 14.4 30.8 1.5 2.9 1.1 ..

Poland 3.6 .. -8.6 6.9 .. 7.9 -18.8 -4.5 .. -1.0 .. .. ..

Latin America and Caribbean 22.9 2.3 6.9 5.4 7.0 4.8 13.0 11.6 10.1 0.4 2.1 0.6 ..

Brazil 3.2 3.0 11.2 6.9 8.2 2.5 26.0 14.4 14.7 0.7 3.4 1.4 ..

Mexico 11.6 2.4 5.1 4.5 5.4 5.2 8.6 2.4 7.3 0.7 1.1 0.5 ..

Argentina 0.6 0.4 4.1 2.3 7.7 8.1 9.7 39.5 -2.6 -5.6 1.9 1.6 ..

Middle East and North Africa 6.9 .. 3.5 .. .. .. .. .. .. .. .. .. ..

Saudi Arabia 2.0 .. 3.4 3.1 .. 6.3 4.4 7.6 .. .. .. .. ..

Iran 1.4 .. 3.3 3.2 .. .. .. .. .. .. .. .. ..

Egypt 0.8 .. 0.8 .. .. .. .. .. .. .. .. .. ..

South Asia 5.5 .. 10.5 -5.2 .. .. .. .. .. .. .. .. ..

India 3.7 .. 21.2 -8.7 .. .. .. .. .. .. .. .. ..

Pakistan 0.7 .. 12.9 10.1 .. 6.5 .. .. .. .. .. .. ..

Bangladesh 0.5 .. -36.4 -0.8 .. .. .. .. .. .. .. .. ..

Sub-Saharan Africa 5.5 .. -1.8 .. .. .. .. .. .. .. .. .. ..

South Africa 1.9 .. 5.9 3.5 .. -1.8 17.0 14.0 .. .. .. .. ..

Nigeria 0.5 .. 6.6 .. .. .. .. .. .. .. .. .. ..

Table A.7 Developing countries' merchandise import growth(US dollar values unless otherwise indicated; percent change; seasonally adjusted annual rates except monthly figures, which are m/m change /a)

/a Merchandise import (C.I.F.), customs basis./b Implicit import unit values, U.S. Dollar basis./c In many cases countries are very late in reporting trade prices. To estimate more timely figures individual trade prices were updated using the median (mean) regional trade price for developing (developed) countries whenever 60% or more of reporters by trade weight reported.

February 21, 2008 External Environment for Developing Countries page 21

US$ bn. % GDP 2007 2007 2007 2008

2007 2007 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

World 0.0 0.0 -254 -355 -358 -308 -273 -361 -491 -363 -480 -630 ..

High-income countries a -415.0 -1.1 -383 -448 -379 -352 -352 -362 -451 -347 -456 -550 ..

Industrial countries -512.9 -1.4 -537 -638 -548 -510 -512 -539 -631 -542 -640 -712 ..

United States -765.4 -5.6 -767 -817 -790 -782 -793 -777 -809 -783 -849 -796 ..

Japan 209.8 4.8 78 66 93 95 91 101 88 105 89 69 ..

Euro Area 41.1 0.4 22 -14 41 52 60 41 12 38 35 -37 ..

United Kindgom -88.2 -3.2 -125 -143 -175 -163 -160 -187 -191 -192 -197 -184 ..

Other high income 97.9 6.5 154 190 170 158 162 179 184 199 183 169 ..

Hong Kong (China) 22.9 11.1 -10 -18 -23 -16 -23 -24 -30 -27 -31 -31 ..

Singapore 41.4 28.8 29 33 36 43 36 41 25 35 16 23 28

Taiwan (China) 28.3 7.7 15 20 27 30 21 24 31 32 41 20 26

Developing countries 0.0 0.0 133 100 26 52 89 6 -44 -31 -27 -75 ..

East Asia and Pacific 392.1 9.7 140 240 336 324 379 347 293 340 297 244 ..

China 339.4 11.1 101 174 263 252 305 276 220 260 225 176 358

Indonesia 10.7 3.0 28 40 40 43 41 38 37 37 37 38 ..

Thailand 10.5 4.9 -7 1 12 15 14 6 13 12 16 11 ..

Malaysia 25.8 15.2 26 30 31 20 24 40 38 42 39 34 ..

Europe and Central Asia .. .. 14 -5 .. -38 -49 -59 .. -42 -25 .. ..

Russian Federation 75.2 6.1 120 143 136 128 124 122 168 155 175 175 ..

Turkey -35.8 -7.3 -43 -54 -64 -59 -61 -63 -73 -77 -74 -67 ..

Poland -16.7 -4.1 -12 -17 .. -20 -23 -22 .. -22 -27 .. ..

Czech Republic -5.9 -3.6 2 2 4 4 2 5 7 1 5 14 ..

Latin America and Caribbean 22.8 0.7 30 32 -2 3 11 -18 -4 0 8 -20 ..

Brazil 5.5 0.5 45 46 40 46 48 33 34 36 34 33 31

Mexico -8.6 -1.0 -7 -6 -11 -13 -15 -11 -5 -12 5 -8 ..

Argentina 6.3 2.2 12 12 11 10 11 8 17 16 16 18 ..

Colombia -6.2 -1.8 0 -2 .. -5 -3 -4 .. -7 1 .. ..

Middle East and North Africa .. .. 10 46 .. 15 .. .. .. .. .. .. ..

Saudi Arabia 98.4 25.5 100 122 .. 89 .. .. .. .. .. .. ..

Iran 21.2 7.6 .. .. .. .. .. .. .. .. .. .. ..

Egypt 3.1 2.4 -9 -7 .. -10 -11 -10 .. -13 -14 .. ..

Algeria 28.8 22.8 20 28 .. 22 .. .. .. .. .. .. ..

South Asia .. -55 -73 -94 -79 -102 -89 -106 -122 -116 -80 ..

India .. .. -39 -52 -69 -56 -79 -64 -76 -83 -86 -59 ..

Pakistan -6.9 -4.8 -9 -13 -15 -14 -13 -16 -18 -24 -16 -12 -28

Bangladesh 0.7 1.0 -3 .. .. .. .. .. .. .. .. .. ..

Sri Lanka .. .. -2 -3 .. -3 -3 -4 .. .. .. .. ..

Sub-Saharan Africa -7.8 -1.0 -1 -136 .. -179 .. .. .. .. .. .. ..

South Africa -18.2 -6.9 -3 -10 -10 -10 -8 -12 -11 -14 1 -21 ..

Nigeria 19.7 14.3 19 24 .. 16 .. .. .. .. .. .. ..

Memo:

OECD .. .. .. .. .. .. .. .. .. .. .. .. ..

Developing excl. China .. .. .. .. .. .. .. .. .. .. .. .. ..

Developing oil exporters 148.2 .. .. .. .. .. .. .. .. .. .. .. ..

Developing non-oil exporters .. .. .. .. .. .. .. .. .. .. .. .. ..

Asian high tech exporters .. .. .. .. .. .. .. .. .. .. .. .. ..

Table A.8 Merchandise trade balances(Billion US dollars; annual rates)

a/ Seasonally adjusted

CAB

February 21, 2008 External Environment for Developing Countries page 22

Weights Average

Levelb2007 2007 2007 2008 Latest

1995 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Nov Dec Jan 20-Feb

World 100.0 95.2 1.1 0.8 5.8 4.8 4.5 5.6 8.7 2.0 -0.8 0.8 0.0

High-income countries 77.7 .. 0.8 0.5 6.1 5.7 4.4 5.6 9.2 2.3 -1.2 0.9 -0.1

Industrial countries 70.1 .. 0.8 0.6 7.0 6.5 5.0 6.4 10.4 2.6 -1.3 1.0 -0.2

United States (SDR/USD) 15.6 0.7 -0.3 -0.4 3.9 3.9 3.0 3.3 5.6 1.8 -0.7 -4.6 5.1

Japan 7.3 116.8 -1.8 -5.2 -1.2 -2.1 -5.2 -1.3 4.1 4.1 -0.9 4.3 0.4

Euro Area 29.4 .. 0.0 1.0 9.1 9.0 7.4 7.9 12.3 3.1 -0.9 1.1 -0.5

United Kindgom 5.5 0.6 -0.7 1.2 8.7 11.5 8.8 7.8 6.8 1.3 -2.3 -2.7 -0.5

Other high income 7.6 101.7 1.1 -0.1 0.4 0.2 -0.2 0.3 1.4 0.3 -0.2 0.4 0.7

Hong Kong (China) 3.6 7.8 0.1 0.1 -0.4 -0.6 -0.7 -0.4 0.1 -0.3 -0.3 -0.1 0.1

Singapore 2.3 1.7 1.6 4.7 5.4 6.3 4.3 4.1 7.2 1.3 -0.1 1.2 1.1

Taiwan (China) 2.1 33.1 3.9 -1.1 -0.9 -1.8 -2.8 -0.4 1.3 0.7 -0.3 0.2 1.5

Developing countries 22.3 110.4 1.9 1.6 5.0 2.5 4.7 5.6 7.2 0.9 0.2 0.5 0.2

East Asia and Pacific 7.4 101.8 -0.8 4.2 5.6 5.2 5.7 5.7 6.1 0.6 0.7 1.3 1.1

China 2.7 8.2 1.0 2.8 4.8 3.7 4.4 5.4 5.8 1.0 0.7 1.7 0.9

Indonesia 1.1 9138.6 -7.9 6.0 0.2 1.8 1.6 -1.5 -1.2 -1.9 -0.5 -0.7 2.0

Thailand 1.3 40.1 0.0 6.2 9.7 10.5 9.9 10.7 7.8 0.8 0.5 1.4 1.2

Malaysia 1.4 3.8 0.3 3.2 6.7 6.5 6.4 5.9 8.0 0.6 0.7 2.0 1.2

Europe and Central Asia 4.9 98.5 4.1 1.6 8.5 5.9 7.2 8.8 12.1 2.2 -0.1 0.4 -0.4

Russian Federation 1.5 26.4 1.9 4.0 6.3 7.1 5.2 5.1 7.9 1.7 -0.4 0.3 -0.6

Turkey 0.6 1.1 6.1 -5.9 9.6 -5.6 7.5 16.6 22.4 0.6 1.0 0.1 -1.7

Poland 0.5 3.7 13.0 4.3 12.1 7.4 11.2 12.5 18.2 4.5 0.7 0.9 -0.1

Czech Republic 0.4 29.7 7.3 6.0 11.3 11.2 7.8 9.5 17.6 5.6 0.9 1.9 1.4

Latin America and Caribbean 5.3 129.6 5.5 1.4 3.0 -0.3 4.0 3.7 5.2 0.3 0.1 0.2 1.1

Brazil 1.0 2.3 20.2 11.9 11.7 4.2 10.3 13.3 20.5 1.8 -0.9 0.7 1.3

Mexico 1.6 10.2 3.6 0.0 -0.3 -3.9 2.5 0.0 0.4 -0.2 0.2 -0.6 1.3

Argentina 0.4 2.2 0.7 -4.9 -1.3 -1.0 -0.5 -1.6 -2.2 0.8 -0.1 -0.8 -0.5

Colombia 0.3 2234.1 13.3 -1.7 13.6 2.0 20.5 19.0 14.1 -2.3 1.5 1.9 3.5

Middle East and North Africa 1.7 146.1 -0.3 -0.4 1.9 1.3 1.3 1.9 3.0 0.8 -0.4 0.5 -0.3

Saudi Arabia 0.8 3.7 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.1 0.0 0.0 -0.1

Iran 0.3 5815.4 -3.9 -2.3 -1.2 -1.2 -1.1 -1.2 -1.2 0.3 -0.7 0.9 -0.7

Egypt 0.3 4.8 7.2 0.8 1.7 0.6 1.1 1.6 3.5 0.4 -0.3 0.4 -0.1

Algeria 0.3 72.2 -1.7 0.9 4.8 3.0 3.5 6.3 6.7 1.1 -0.4 0.4 -0.2

South Asia 1.5 102.3 1.1 -2.8 6.2 -0.4 6.7 9.6 9.6 0.2 0.0 0.2 -0.8

India 1.1 44.8 2.8 -2.7 9.6 0.5 10.3 14.4 14.0 0.2 0.0 0.2 -0.6

Pakistan 0.2 56.6 -2.1 -1.3 -0.8 -1.5 -1.0 -0.2 -0.4 -0.5 -0.4 0.0 -2.7

Bangladesh 0.1 58.2 -7.5 -6.7 0.1 -1.9 1.2 0.6 0.5 0.1 0.1 0.0 0.0

Sri Lanka 0.1 91.0 0.7 -3.3 -6.1 -6.0 -6.9 -8.0 -3.5 2.3 1.3 0.8 0.4

Sub-Saharan Africa 1.5 104.9 -0.2 -3.0 0.3 -6.2 -2.8 2.5 7.9 1.8 -0.5 -1.3 -4.2

South Africa 0.5 7.2 1.6 -6.1 -3.9 -15.0 -8.9 0.8 8.4 1.0 -1.6 -3.0 -8.3

Nigeria 0.3 109.5 1.2 2.0 2.3 1.0 0.7 1.4 6.5 3.4 1.2 0.4 0.2

Memo:

OECD 73.8 .. 1.1 0.6 6.9 6.1 5.2 6.4 10.3 2.5 -1.2 0.9 -0.2

Developing excl. China 19.6 112.2 2.1 1.5 5.0 2.3 4.8 5.6 7.4 0.9 0.1 0.4 0.1

Developing oil exporters 2.7 147.7 -5.8 1.9 0.7 1.0 1.0 0.0 0.7 -0.3 -0.2 -0.1 0.7

Developing non-oil exporters 19.5 105.9 3.1 1.6 5.6 2.7 5.3 6.4 8.2 1.1 0.2 0.6 0.1

Asian high tech exporters .. .. .. .. .. .. .. .. .. .. .. ..

Table A.9 Exchange Rates (USD/LCU)(annual percent change except monthly data which is change over previous month a/)

a/ An increase in the USD per LCU implies appreciation of the local currency. The aggregates computed by using trade weights and rebased to year 2000=100 (bilateral total trade i.e. imports plus exports in 1995 constant USD).Aggregates are reported when at least 60% (by weight) of countries reported data in that time period.b/ Average levels are LCU vis-a-vis the USD

February 21, 2008 External Environment for Developing Countries page 23

Weights Average 2007 2007 2007 2008

1995 1998-07 2005 2006 2007 Q1 Q2 Q3 Q4 Oct Nov Dec Jan

World 2.6 2.8 2.9 3.0 2.8 2.4 2.6 2.5 3.6 3.3 3.9 3.7 ..

High-income countries 1.8 2.0 2.1 2.2 2.0 1.8 1.9 1.7 2.8 2.5 3.0 3.0 ..

Industrial countries 1.8 2.0 2.2 2.3 2.0 1.8 1.9 1.7 2.8 2.5 3.0 3.0 ..

United States 4.3 2.9 3.4 3.2 2.9 2.4 2.7 2.3 4.0 3.5 4.3 4.1 ..

Japan 0.8 0.1 -0.3 0.2 0.1 -0.1 -0.1 -0.1 0.5 0.3 0.6 0.7 ..

Euro Area 2.5 2.1 2.2 2.2 2.1 1.9 1.9 1.9 2.9 2.5 3.0 3.1 ..

United Kindgom 1.5 2.3 2.1 2.3 2.3 2.8 2.6 1.8 2.1 2.0 2.1 2.1 ..

Other high income 2.0 .. 1.5 1.6 .. 1.5 1.2 2.4 .. 4.3 .. .. ..

Hong Kong (China) 3.1 2.0 0.9 2.0 2.0 1.7 1.3 1.6 3.5 3.2 3.4 3.8 ..

Singapore 4.0 2.1 0.5 1.0 2.1 0.5 1.0 2.7 4.1 3.6 4.2 4.4 ..

Taiwan (China) 6.3 1.8 2.3 0.6 1.8 1.0 0.3 1.5 4.5 5.3 4.8 3.3 3.0

Developing countries 6.0 5.9 6.4 6.2 5.9 5.2 5.7 6.2 6.7 6.9 7.4 6.6 ..

East Asia and Pacific 5.1 4.8 7.2 5.1 4.8 4.6 4.9 6.0 4.9 5.1 5.0 5.1 6.0

China 6.2 4.8 1.8 1.5 4.8 2.7 3.6 6.1 6.6 6.5 6.9 6.5 7.1

Indonesia 6.3 6.4 10.5 13.1 6.4 6.4 6.0 6.5 6.7 6.9 6.7 6.6 7.4

Thailand 3.2 2.2 4.5 4.6 2.2 2.5 1.9 1.6 2.9 2.5 3.0 3.2 4.3

Malaysia 1.7 2.0 3.0 3.6 2.0 2.6 1.5 1.8 2.2 1.9 2.3 2.4 ..

Europe and Central Asia 5.6 7.3 4.4 5.0 7.3 4.8 4.8 6.8 8.0 7.6 8.4 8.3 ..

Russian Federation 11.3 9.0 12.7 9.7 9.0 7.7 7.9 8.9 11.4 10.8 11.5 11.9 ..

Turkey 7.3 8.8 8.2 9.6 8.8 10.3 9.5 7.1 8.2 7.7 8.4 8.4 8.2

Poland 3.4 2.4 2.1 1.1 2.4 1.9 2.4 2.0 3.3 2.6 3.3 3.9 4.3

Czech Republic 4.8 2.9 1.8 2.5 2.9 1.6 2.5 2.6 4.9 4.0 5.1 5.5 7.6

Latin America and Caribbean 6.1 5.8 5.4 5.6 5.8 5.2 6.2 6.0 7.7 7.2 8.3 7.1 6.7

Brazil 4.0 3.6 6.9 4.2 3.6 3.0 3.3 4.0 4.3 4.1 4.2 4.5 4.6

Mexico 3.1 4.0 4.0 3.6 4.0 4.1 4.0 4.0 3.8 3.7 3.9 3.8 3.7

Argentina 7.9 8.8 9.6 10.9 8.8 9.5 8.8 8.6 8.5 8.4 8.5 8.5 8.2

Colombia 5.6 5.5 5.0 4.3 5.5 5.2 6.2 5.3 5.4 5.2 5.4 5.7 6.0

Middle East and North Africa 4.4 .. 2.8 5.4 .. 4.7 3.4 5.2 .. 4.5 4.9 .. ..

Saudi Arabia 5.6 .. 0.5 2.2 .. 3.1 3.0 4.6 .. 5.4 .. .. ..

Iran 17.5 .. 13.4 11.9 .. 15.8 16.5 17.4 .. 18.1 19.1 .. ..

Egypt 8.1 9.5 4.8 7.6 9.5 12.7 10.1 8.4 7.1 7.5 6.9 6.9 10.5

Algeria 1.6 0.1 1.6 2.5 3.5 2.8 2.0 5.2 4.1 4.0 4.3 3.9 ..

South Asia 7.2 7.0 7.0 7.6 7.0 7.1 6.7 6.9 7.2 9.3 7.1 7.2 ..

India 6.7 6.4 4.2 6.2 6.4 7.0 6.3 6.7 5.5 5.5 5.5 5.5 ..

Pakistan 9.7 7.6 9.1 7.9 7.6 7.2 7.1 7.1 8.9 9.3 8.7 8.8 11.9