Embed Size (px)

Citation preview

The European LeasingThe European Leasing& Automotive Rental Markets & Automotive Rental Markets ––

State of PlayState of Play

Jurgita BucyteJurgita BucyteAdviser in Statistics and Economic Affairs,Adviser in Statistics and Economic Affairs,

LeaseuropeLeaseurope

LeaseuropeLeaseurope’’ss 2011 Seminar for2011 Seminar forLessors in Central, Eastern and SouthLessors in Central, Eastern and South--Eastern EuropeEastern Europe

15 April 2011, 15 April 2011, LjubljanaLjubljana

Agenda

Evolution of the European Leasing MarketEvolution of the European Leasing MarketEuropean Leasing Market in 2010 European Leasing Market in 2010

-- Leased AssetsLeased Assets-- Leasing ClientsLeasing Clients-- Regional PerformanceRegional Performance

Evolution of the Leasing Market in CEE Evolution of the Leasing Market in CEE CEE Leasing Market in 2010CEE Leasing Market in 2010

-- Individual Country PerformanceIndividual Country Performance-- Leased AssetsLeased Assets

European Leasing Penetration European Leasing Penetration

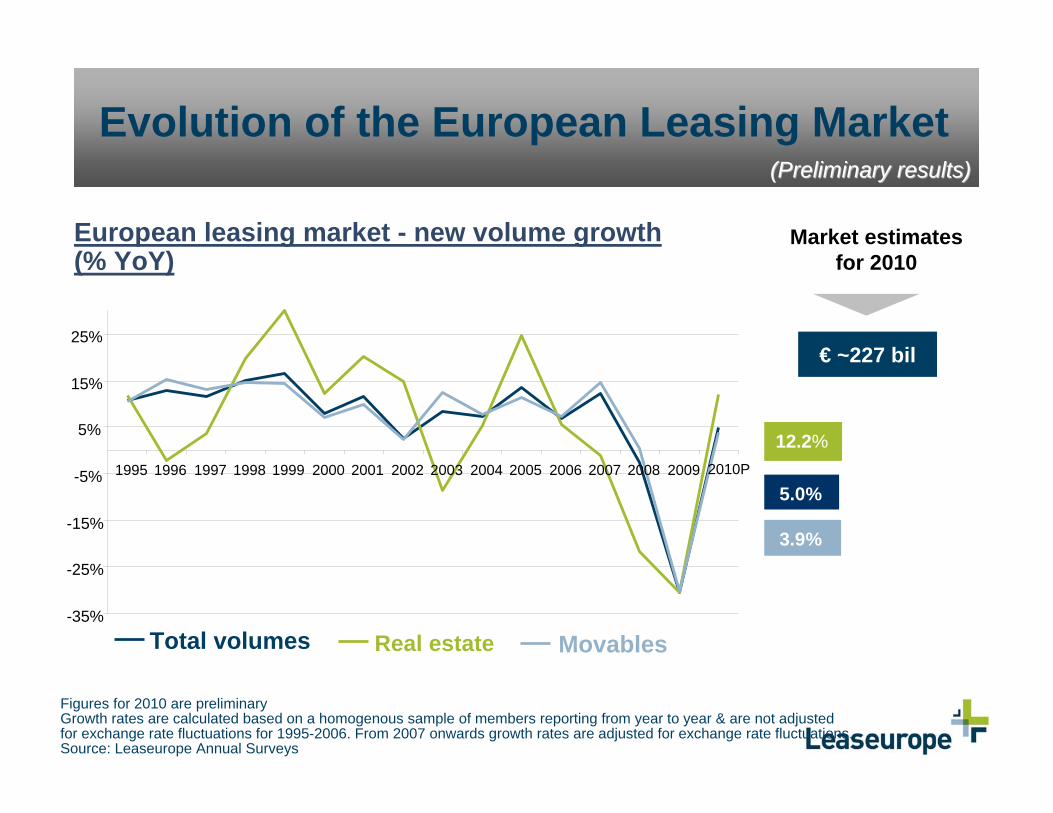

Evolution of the European Leasing Market

3.9%

12.2%

5.0%

European leasing market - new volume growth(% YoY)

€ ~227 bil

Figures for 2010 are preliminaryGrowth rates are calculated based on a homogenous sample of members reporting from year to year & are not adjusted for exchange rate fluctuations for 1995-2006. From 2007 onwards growth rates are adjusted for exchange rate fluctuations. Source: Leaseurope Annual Surveys

Market estimates for 2010

-35%

-25%

-15%

-5%

5%

15%

25%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010P

Total volumes Real estate Movables

(Preliminary results)(Preliminary results)

-5%

0%

5%

10%

15%

0%

5%Equipment Vehicles

2.2%

6.1%

-10%

-15%

-40%

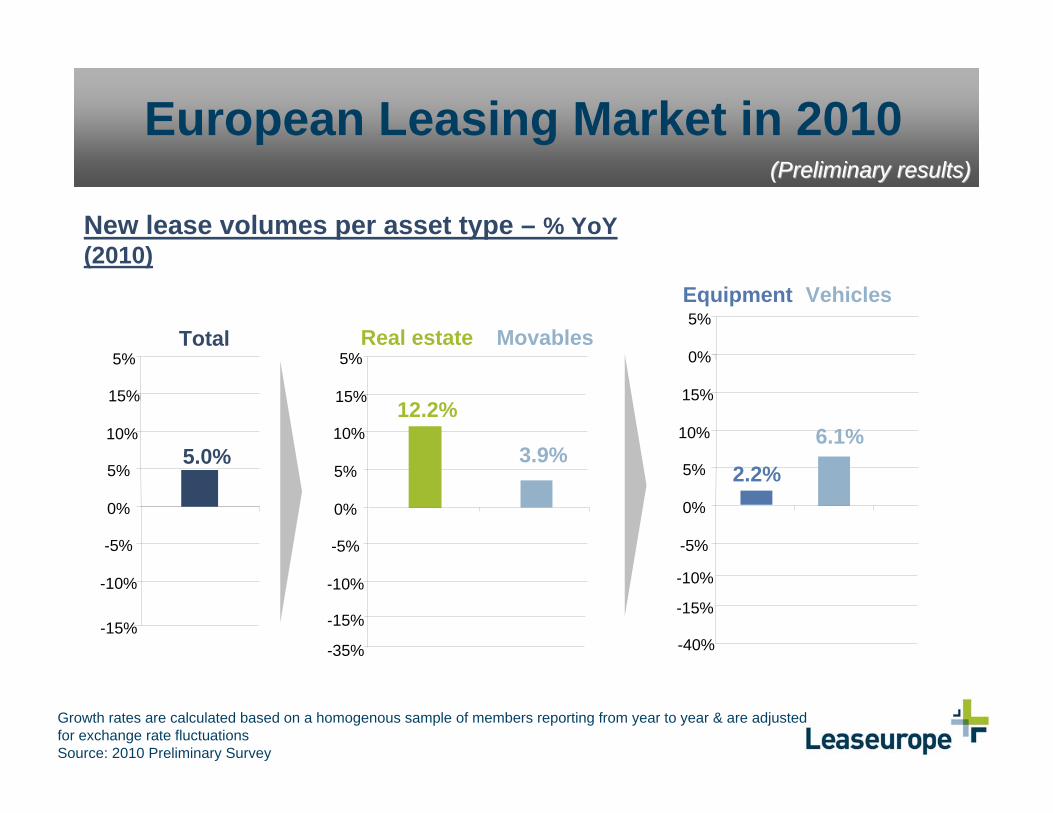

European Leasing Market in 2010

-10%

-5%

0%

5%

10%

15%

5%Total

New lease volumes per asset type – % YoY(2010)

5.0%

-15%

-10%

-5%

0%

5%

10%

15%

5%Real estate Movables

12.2%

3.9%

-15%

-35%

Growth rates are calculated based on a homogenous sample of members reporting from year to year & are adjusted for exchange rate fluctuationsSource: 2010 Preliminary Survey

(Preliminary results)(Preliminary results)

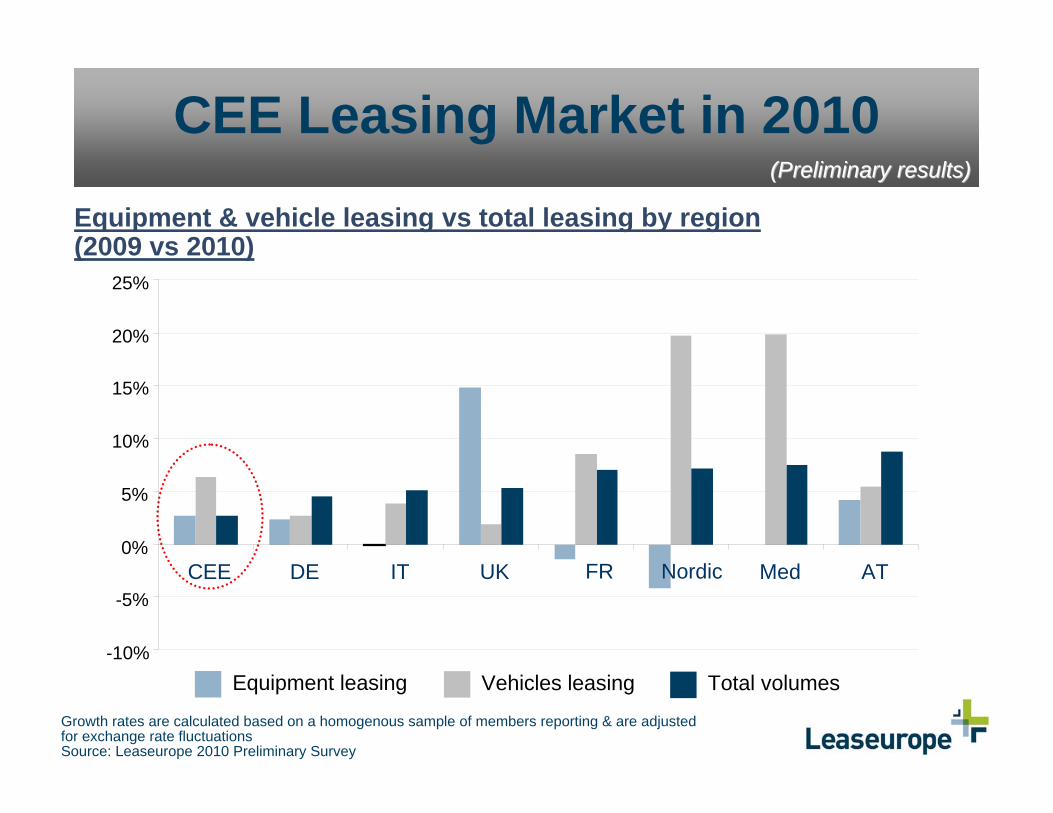

CEE Leasing Market in 2010

Equipment & vehicle leasing vs total leasing by region (2009 vs 2010)

Equipment leasing Total volumesVehicles leasing

Growth rates are calculated based on a homogenous sample of members reporting & are adjusted for exchange rate fluctuationsSource: Leaseurope 2010 Preliminary Survey

-10%

-5%

0%

5%

10%

15%

20%

25%

CEE DE IT UK FR Nordic Med AT

(Preliminary results)(Preliminary results)

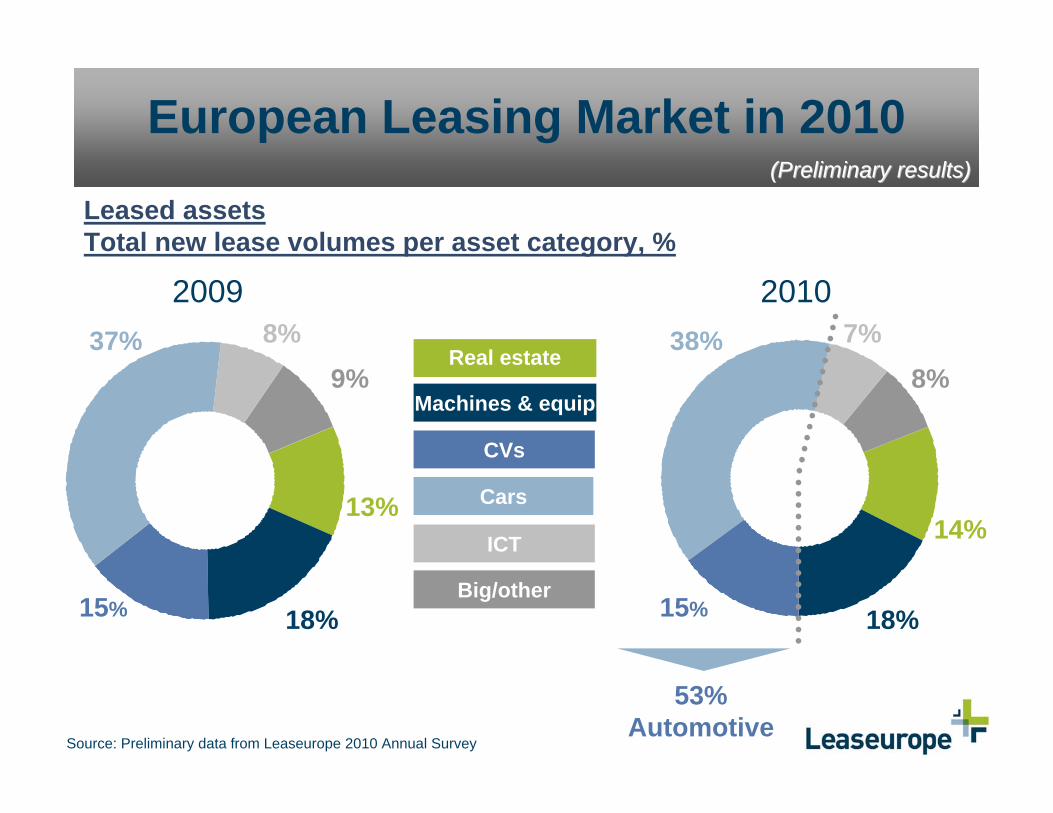

European Leasing Market in 2010

Leased assetsTotal new lease volumes per asset category, %

Source: Preliminary data from Leaseurope 2010 Annual Survey

Machines & equip

Cars

CVs

ICT

Big/other

Real estate

20102009

9%

13%

18%15%

37% 8%8%

14%

18%15%

38% 7%

53% Automotive

(Preliminary results)(Preliminary results)

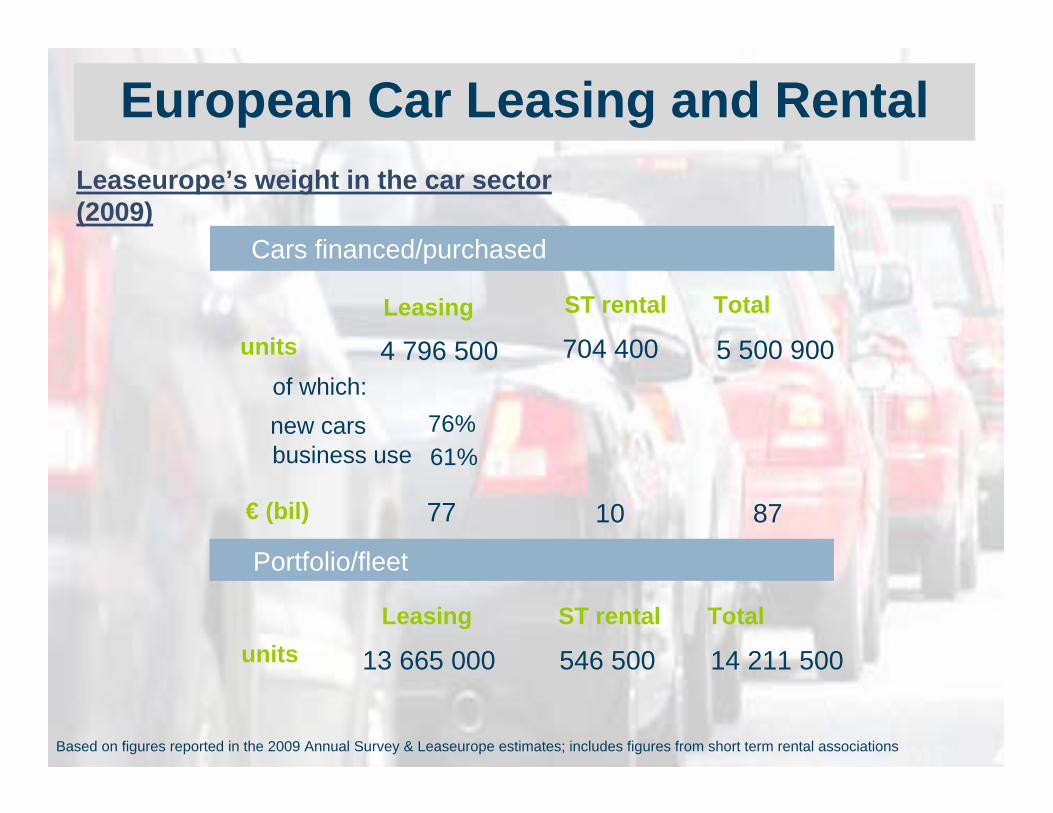

Based on figures reported in the 2009 Annual Survey & Leaseurope estimates; includes figures from short term rental associations

Leaseurope’s weight in the car sector (2009)

European Car Leasing and Rental

14 211 500546 500unitsTotal ST rentalLeasing

Portfolio/fleet

13 665 000

871077€ (bil)

5 500 900704 4004 796 500units

Total ST rentalLeasing

Cars financed/purchased

new carsbusiness use

76%61%

of which:

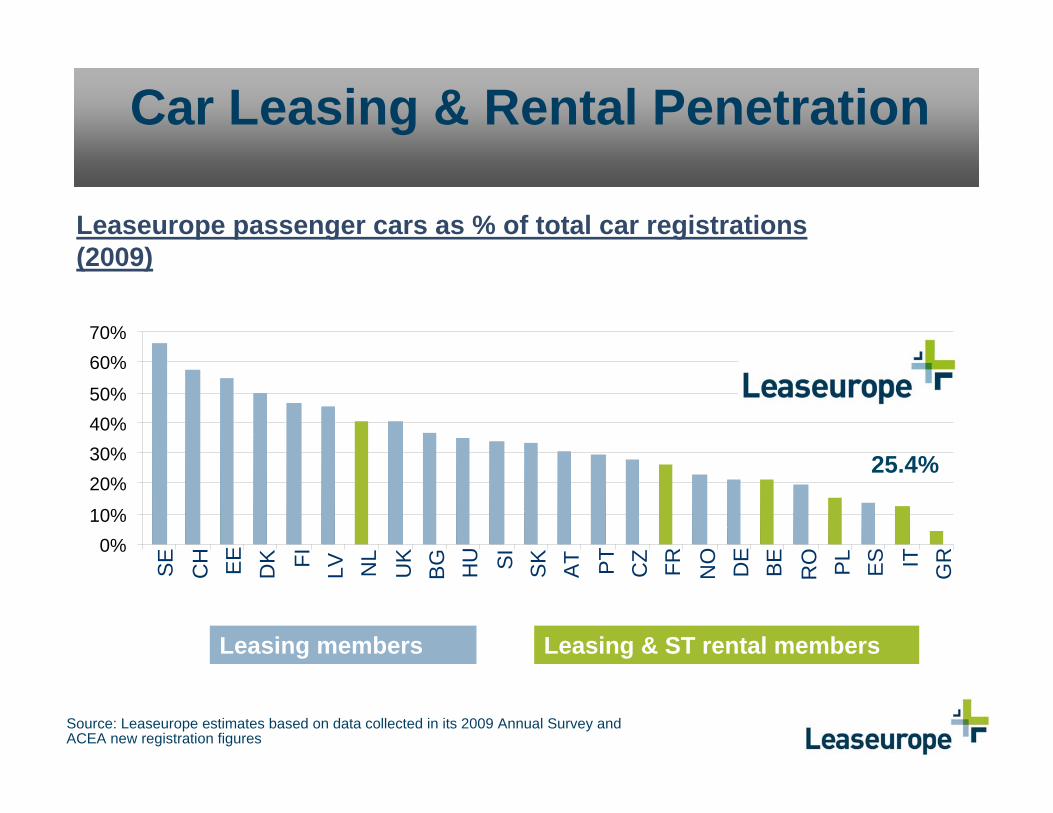

Car Leasing & Rental Penetration

Source: Leaseurope estimates based on data collected in its 2009 Annual Survey and ACEA new registration figures

Leaseurope passenger cars as % of total car registrations (2009)

0%10%

20%30%40%50%

60%70%

SE CH EE DK FI LV NL

UK

BG HU SI

SK AT PT

CZ FR NO DE

BE RO PL

ES IT GR

Leasing & ST rental membersLeasing members

25.4%

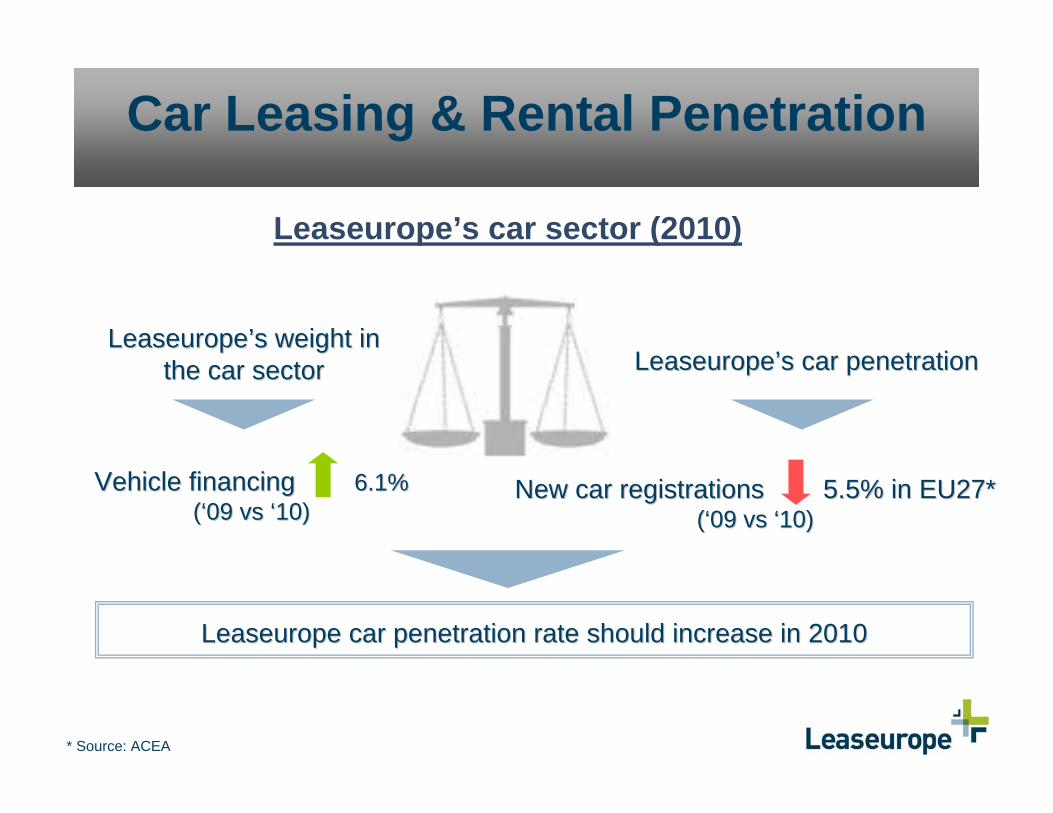

Car Leasing & Rental Penetration

Leaseurope’s car sector (2010)

Vehicle financing Vehicle financing 6.1%6.1%((‘‘09 09 vsvs ‘‘10) 10)

Leaseurope car penetration rate should increase in 2010 Leaseurope car penetration rate should increase in 2010

* Source: ACEA

New car registrations 5.5% in EU27*New car registrations 5.5% in EU27*((‘‘09 09 vsvs ‘‘10)10)

LeaseuropeLeaseurope’’ss weight in weight in the car sectorthe car sector LeaseuropeLeaseurope’’ss car penetrationcar penetration

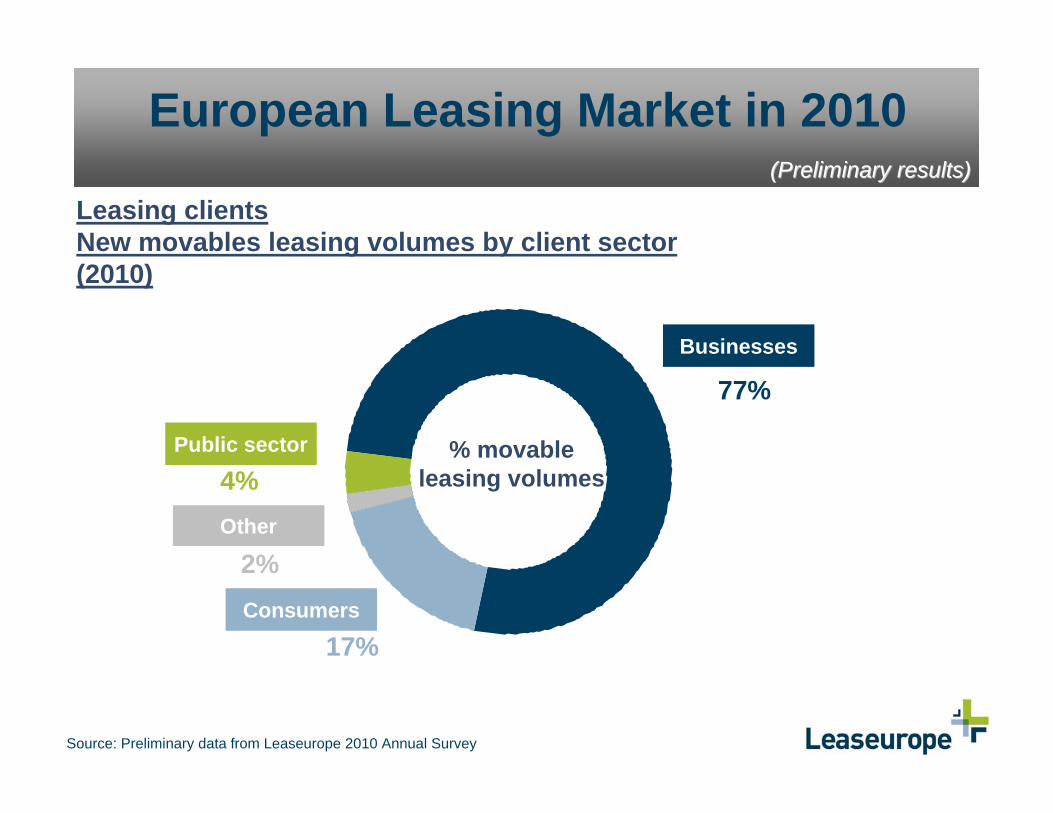

European Leasing Market in 2010

Leasing clientsNew movables leasing volumes by client sector (2010)

Businesses

Public sector

Other

Consumers

2%

77%

17%

4%

Source: Preliminary data from Leaseurope 2010 Annual Survey

% movable leasing volumes

(Preliminary results)(Preliminary results)

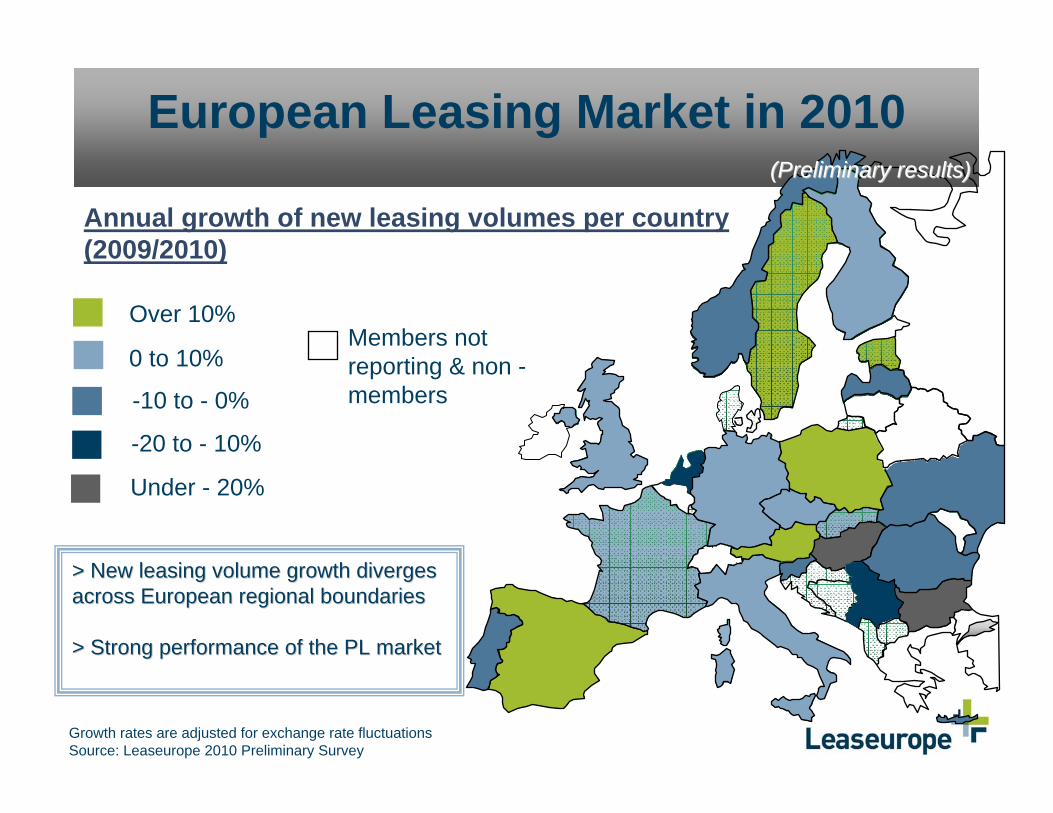

European Leasing Market in 2010

Annual growth of new leasing volumes per country (2009/2010)

Members not reporting & non -members

Growth rates are adjusted for exchange rate fluctuationsSource: Leaseurope 2010 Preliminary Survey

0 to 10%

Over 10%

-20 to - 10%

> New leasing volume growth diverges > New leasing volume growth diverges across European regional boundaries across European regional boundaries

> Strong performance of the PL market > Strong performance of the PL market

-10 to - 0%

Under - 20%

(Preliminary results)(Preliminary results)

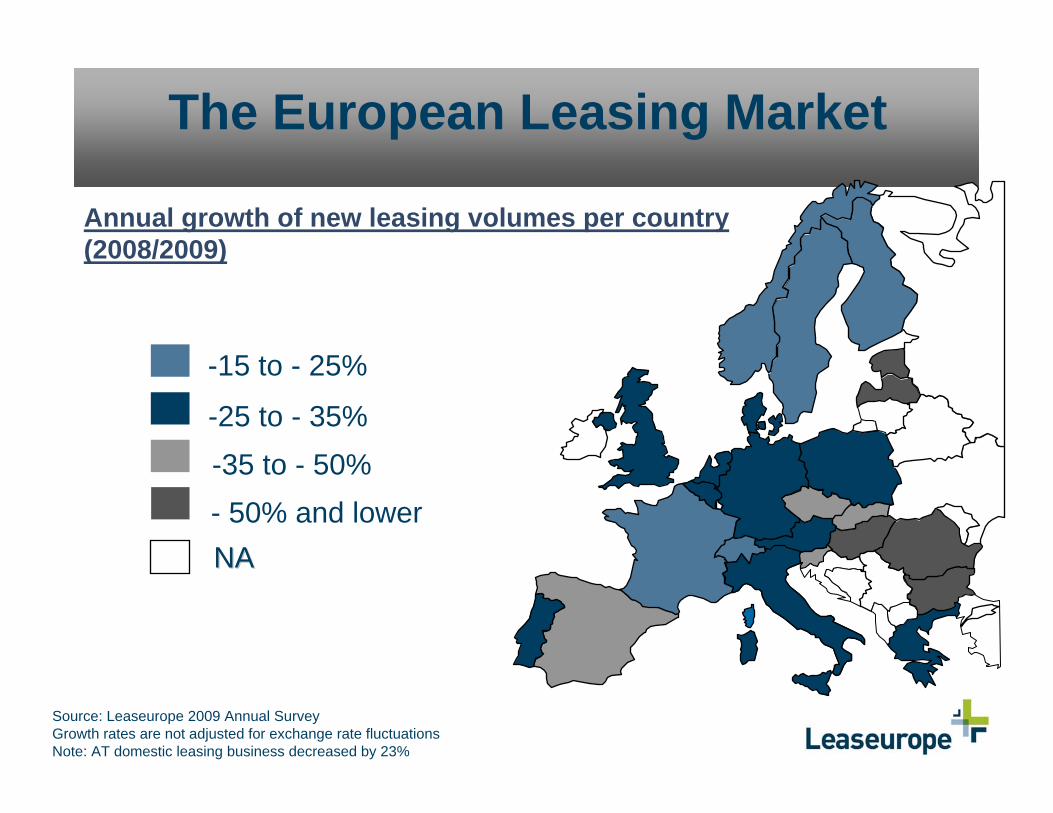

The European Leasing Market

Source: Leaseurope 2009 Annual SurveyGrowth rates are not adjusted for exchange rate fluctuationsNote: AT domestic leasing business decreased by 23%

NANA

-25 to - 35%

-15 to - 25%

- 50% and lower-35 to - 50%

Annual growth of new leasing volumes per country (2008/2009)

Evolution of the Leasing Market in CEE

CEE leasing market - new volume growth (% YoY)

Figures for 2010 are preliminaryGrowth rates are calculated based on a homogenous sample of members reporting from year to year (CZ, EE, HU, PL, RO, SK, SI) & are not adjusted for exchange rate fluctuations for 1995-2006. From 2007 onwards growth rates are adjusted for exchange rate fluctuations. Source: Leaseurope Annual Surveys

-60%

-40%

-20%

0%

20%

40%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010P

2.7%

(Preliminary results)(Preliminary results)

CEE Leasing Market in 2010

Individual CEE market growth (2009 vs 2010)

Growth rates are calculated based on a homogenous sample of members reporting from year to year & are adjusted for exchange rate fluctuationsSource: Leaseurope 2009 Annual Survey & 2010 Preliminary Survey

-90% -70% -50% -30% -10% 10% 30%

HU

BG

RS

SI

RO

UA

LVCZ

SK

EE

PL

2010

2009(2010P)

CEE region2.7%

5.0%

(Preliminary results)(Preliminary results)

CEE Leasing Market in 2010

Equipment & vehicle leasing vs total leasing by region (2009 vs 2010)

Equipment leasing Total volumesVehicles leasing

Growth rates are calculated based on a homogenous sample of members reporting & are adjusted for exchange rate fluctuationsSource: Leaseurope 2010 Preliminary Survey

-10%

-5%

0%

5%

10%

15%

20%

25%

CEE DE IT UK FR Nordic Med AT

(Preliminary results)(Preliminary results)

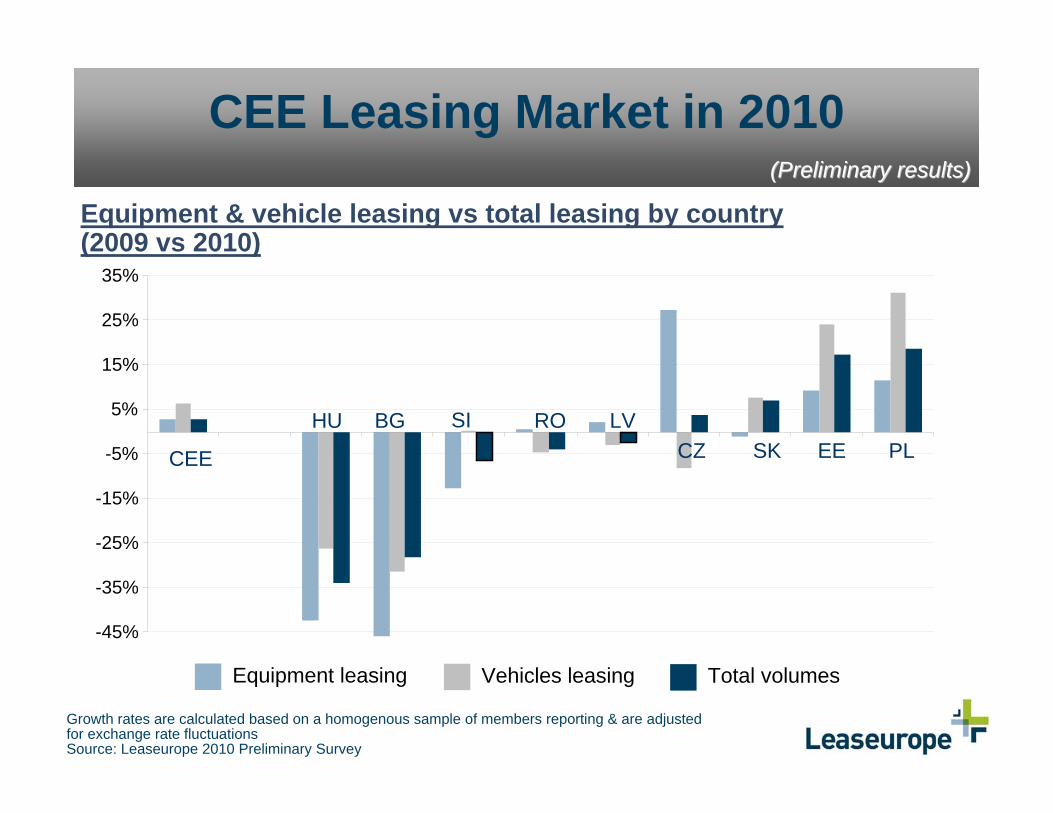

CEE Leasing Market in 2010

Equipment & vehicle leasing vs total leasing by country(2009 vs 2010)

Growth rates are calculated based on a homogenous sample of members reporting & are adjusted for exchange rate fluctuationsSource: Leaseurope 2010 Preliminary Survey

Equipment leasing Total volumesVehicles leasing

-45%

-35%

-25%

-15%

-5%

5%

15%

25%

35%

CEE

HU BG SI RO LVCZ SK EE PL

(Preliminary results)(Preliminary results)

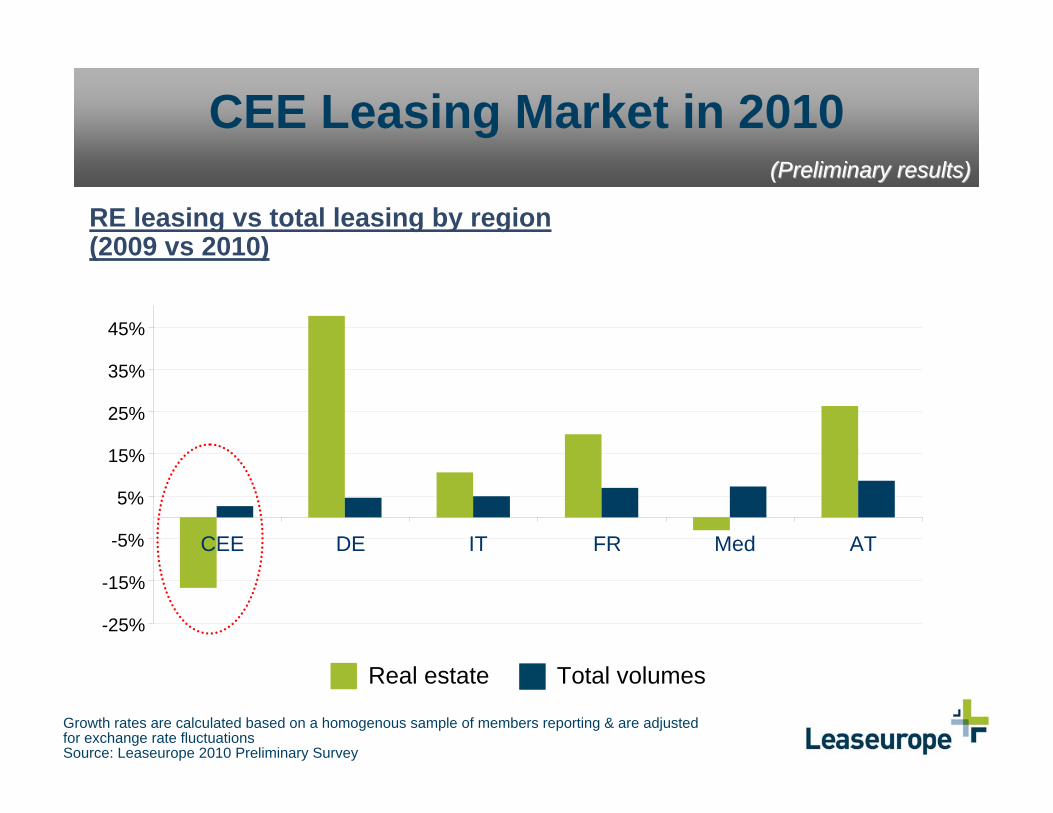

CEE Leasing Market in 2010

RE leasing vs total leasing by region (2009 vs 2010)

Growth rates are calculated based on a homogenous sample of members reporting & are adjusted for exchange rate fluctuationsSource: Leaseurope 2010 Preliminary Survey

Real estate Total volumes

-25%

-15%

-5%

5%

15%

25%

35%

45%

CEE DE IT FR Med AT

(Preliminary results)(Preliminary results)

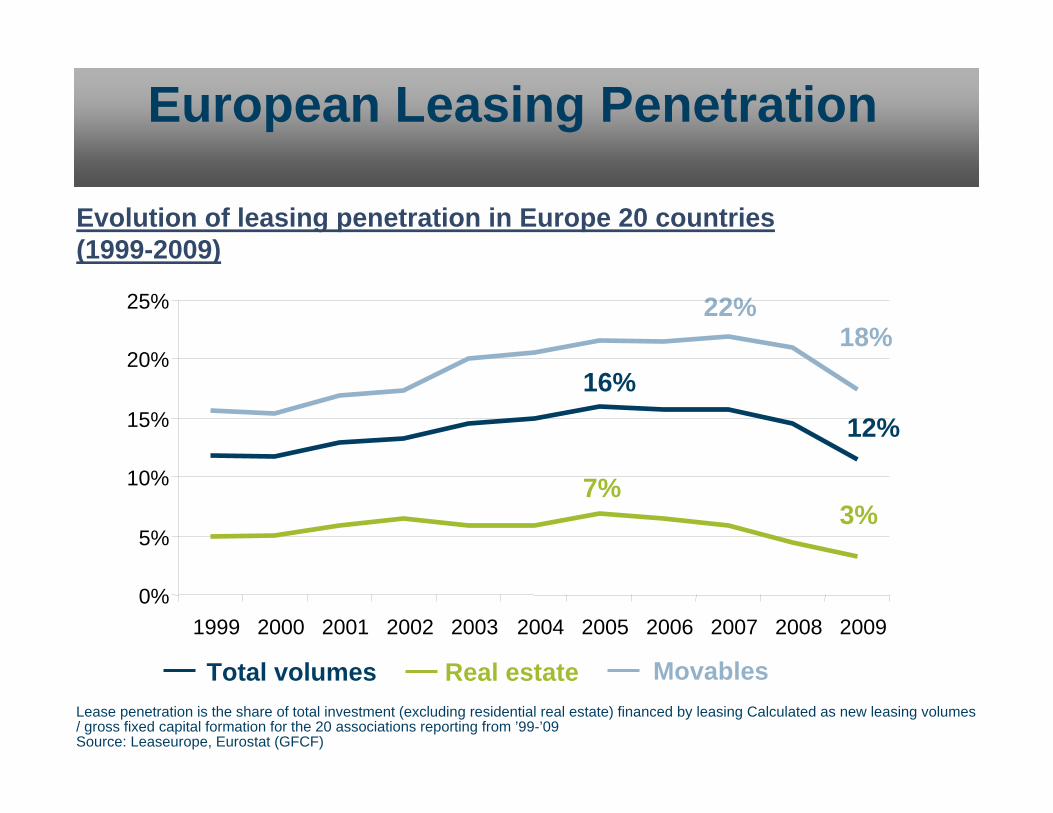

European Leasing Penetration

Total volumes Real estate MovablesLease penetration is the share of total investment (excluding residential real estate) financed by leasing Calculated as new leasing volumes / gross fixed capital formation for the 20 associations reporting from ’99-’09Source: Leaseurope, Eurostat (GFCF)

Evolution of leasing penetration in Europe 20 countries (1999-2009)

16%

7%

22%18%

12%

3%

0%

5%

10%

15%

20%

25%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

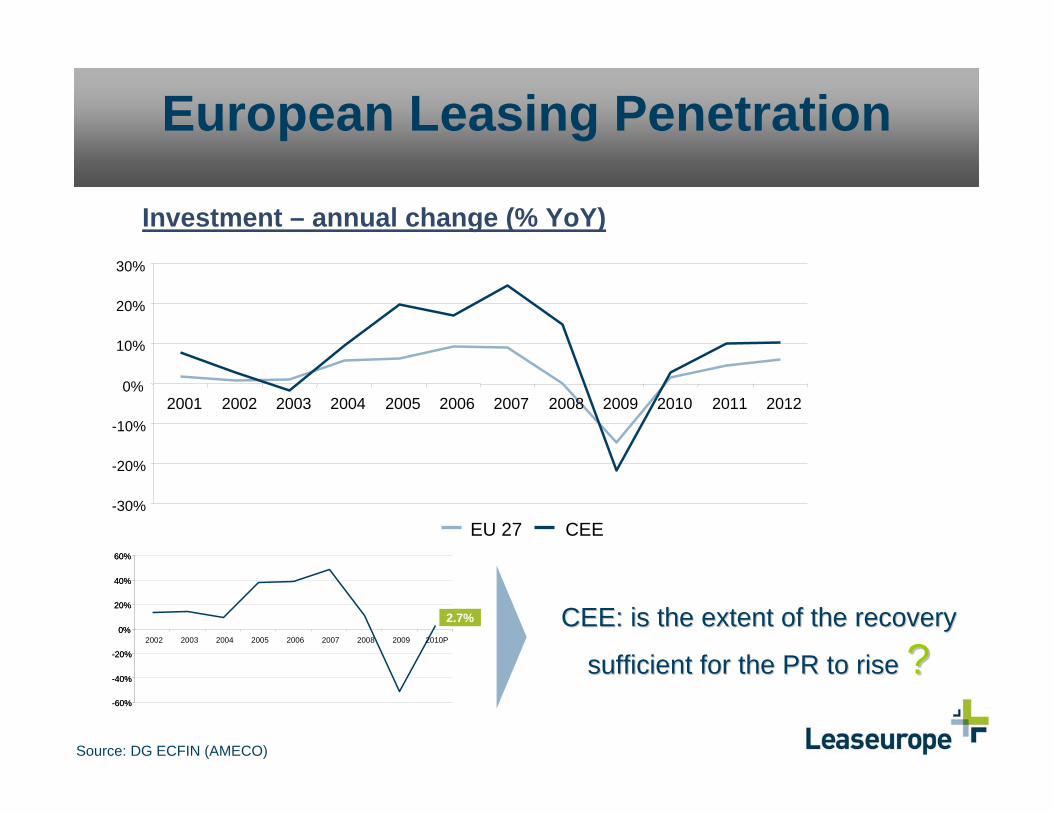

European Leasing Penetration

Source: DG ECFIN (AMECO)

Investment – annual change (% YoY)

-30%

-20%

-10%

0%

10%

20%

30%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EU 27 CEE

CEE: is the extent of the recovery CEE: is the extent of the recovery

sufficient for the PR to rise sufficient for the PR to rise ??-60%

-40%

-20%

0%

20%

40%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010P

2.7%

-60%

-40%

-20%

0%

20%

40%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010P

2.7%

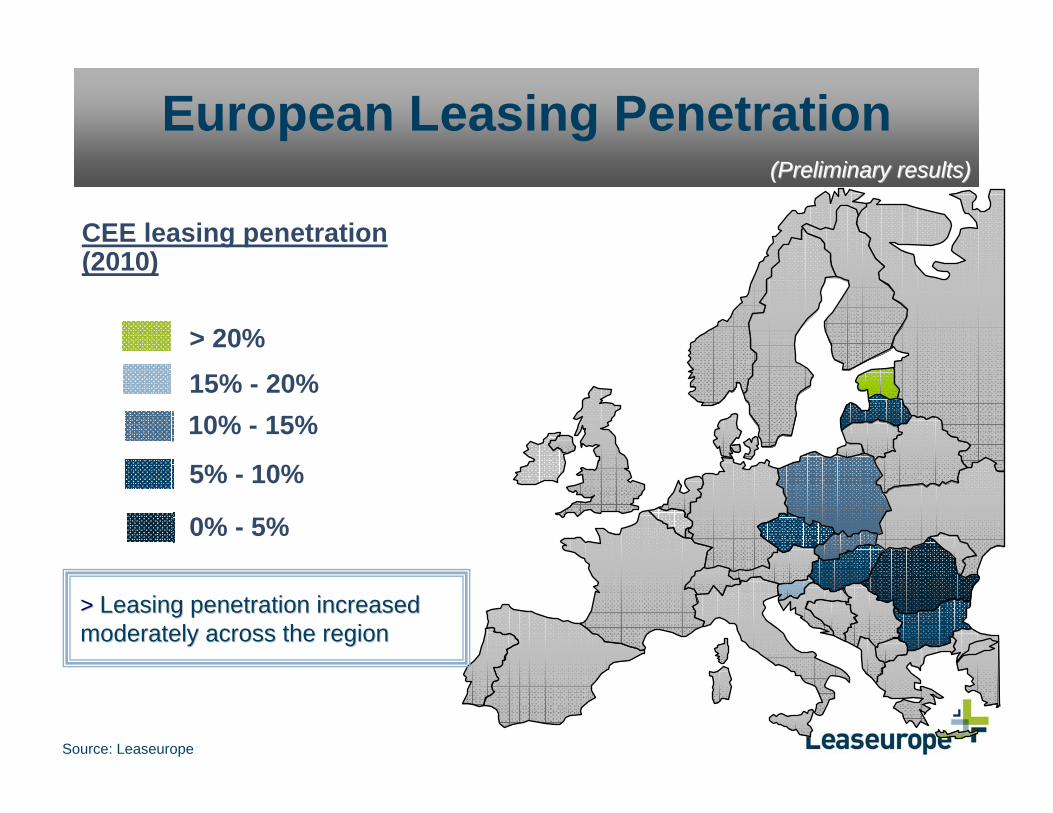

European Leasing Penetration

Source: Leaseurope

CEE leasing penetration (2010)

> > Leasing penetration increased Leasing penetration increased moderately across the regionmoderately across the region

5% - 10%

10% - 15%15% - 20%> 20%

0% - 5%

(Preliminary results)(Preliminary results)

Concluding Remarks

Leasing regained new ground …

…however the situation diverges across different European leasing markets.

The cautious optimism expressed by the European leasing firms last year in Hamburg hasbeen confirmed.

The most important factors which helped to bring us out of the downturn were improved added-value services & higher profitability followed by the increased asset & channel specialisation.

The overall positive trends in the European leasing market and improved prospects for the EU economy suggests that leasing industry will remain an attractive business proposition for its shareholders over the coming years.

2010 in short

Concluding Remarks

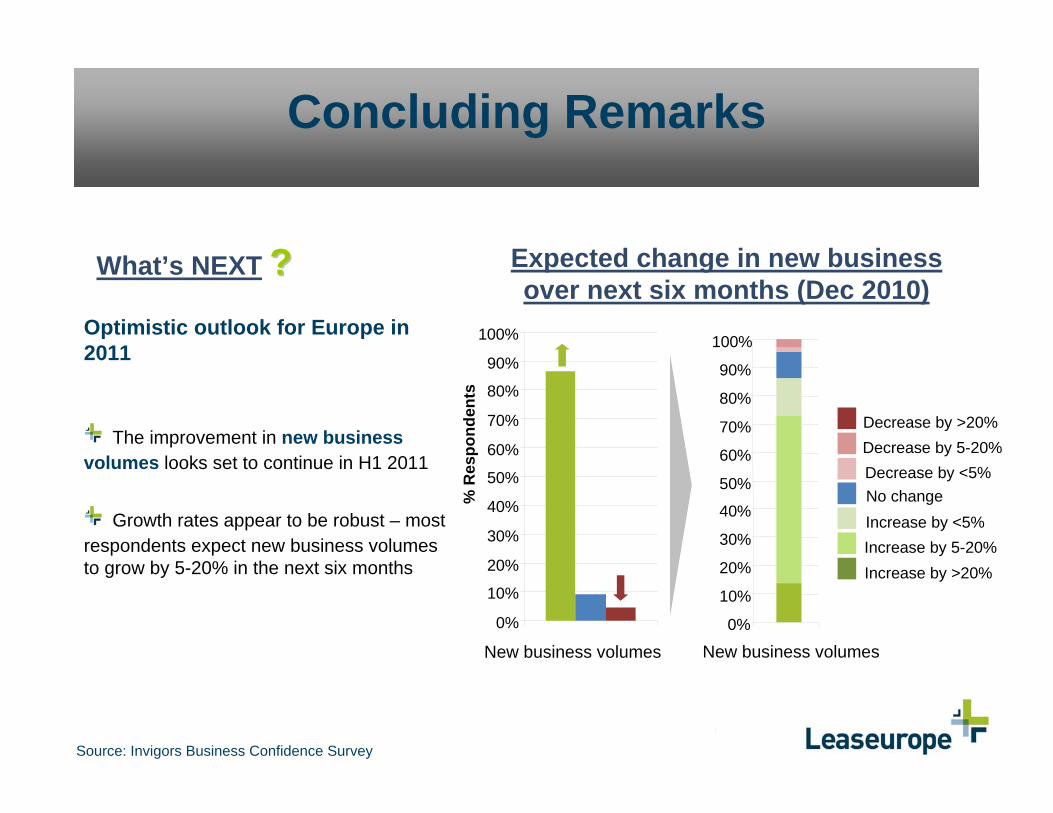

Source: Invigors Business Confidence Survey

What’s NEXT ?? Expected change in new business over next six months (Dec 2010)

% R

espo

nden

ts

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

New business volumes

Optimistic outlook for Europe in 2011

The improvement in new business volumes looks set to continue in H1 2011

Growth rates appear to be robust – most respondents expect new business volumes to grow by 5-20% in the next six months

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Decrease by >20%Decrease by 5-20%Decrease by <5%No changeIncrease by <5%Increase by 5-20%Increase by >20%

New business volumes

Concluding Remarks

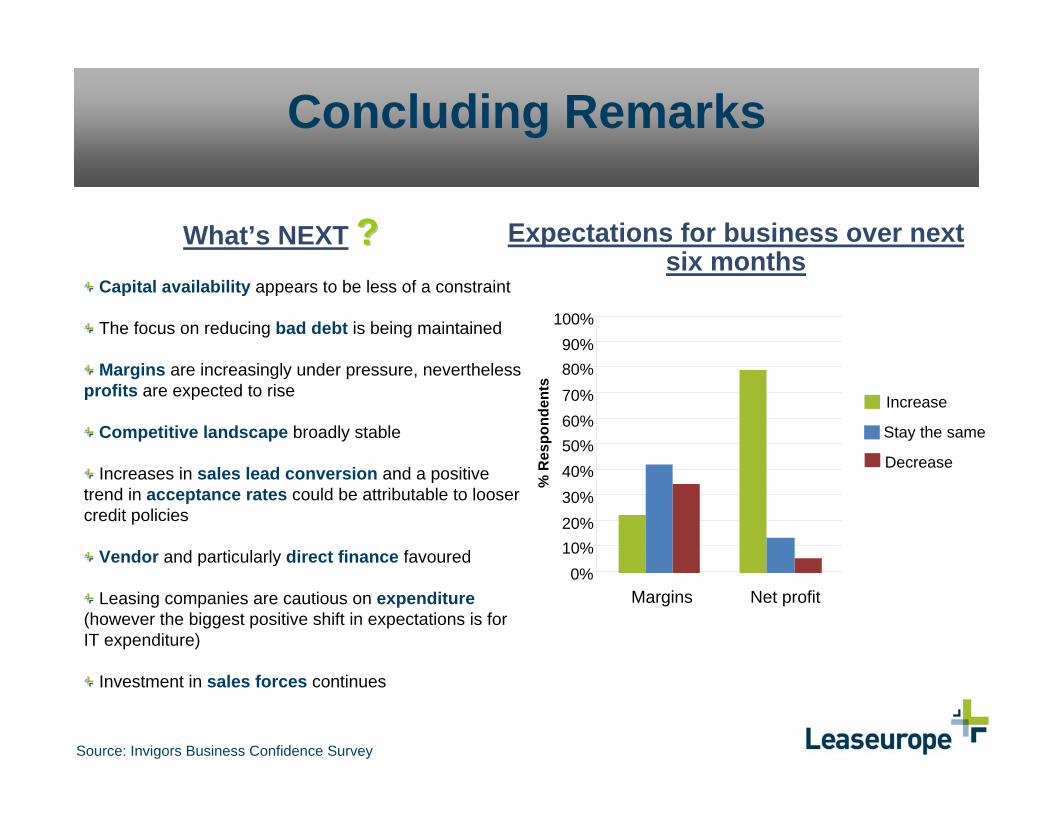

Source: Invigors Business Confidence Survey

Expectations for business over next six months

Capital availability appears to be less of a constraint

The focus on reducing bad debt is being maintained

Margins are increasingly under pressure, nevertheless profits are expected to rise

Competitive landscape broadly stable

Increases in sales lead conversion and a positive trend in acceptance rates could be attributable to looser credit policies

Vendor and particularly direct finance favoured

Leasing companies are cautious on expenditure (however the biggest positive shift in expectations is for IT expenditure)

Investment in sales forces continues

What’s NEXT ??

% R

espo

nden

ts

Stay the same

0%10%20%30%40%50%60%70%80%90%

100%

Margins Net profit

Increase

Decrease

Leaseurope Market Research

Leaseurope surveys & projects

2010 Annual Survey

2010 Ranking Survey of TOP European leasing companies

Leaseurope Index

Study on SMEs’ use of leasing at European level

European Asset Finance Business Confidence Survey

The European Yellow Goods Leasing Report

For more information about Leaseurope’s projects & surveys, please contact [email protected]

The European LeasingThe European Leasing& Automotive Rental Markets & Automotive Rental Markets ––

State of PlayState of Play

Jurgita BucyteJurgita [email protected]@leaseurope.org

LeaseuropeLeaseurope’’ss 2011 Seminar for2011 Seminar forLessors in Central, Eastern and SouthLessors in Central, Eastern and South--Eastern EuropeEastern Europe

15 April 2011, 15 April 2011, LjubljanaLjubljana