Embed Size (px)

Citation preview

Ž .Journal of Risk and Uncertainty, 19:1]3; 7]42 1999Q 1999 Kluwer Academic Publishers. Manufactured in The Netherlands.

The Effects of Financial Incentives in Experiments:A Review and Capital-Labor-ProductionFrameworkCOLIN F. CAMERER [email protected]

Rea and Lela G. Axline Professor of Business Economics, Di ision of Humanities and Social Sciences228-77, California Institute of Technology, Pasadena, CA 91125

ROBIN M. HOGARTH

Wallace W. Booth Professor of Beha¨ioral Science, Graduate School of Business, Uni ersity of Chicago,Chicago, IL 60637

Abstract

We review 74 experiments with no, low, or high performance-based financial incentives. The modalŽ .result is no effect on mean performance though variance is usually reduced by higher payment . Higher

incentive does improve performance often, typically judgment tasks that are responsive to better effort.Ž .Incentives also reduce ‘‘presentation’’ effects e.g., generosity and risk-seeking . Incentive effects are

comparable to effects of other variables, particularly ‘‘cognitive capital’’ and task ‘‘production’’ de-mands, and interact with those variables, so a narrow-minded focus on incentives alone is misguided.We also note that no replicated study has made rationality violations disappear purely by raisingincentives.

Key words: Experimental economics, rationality, bounded rationality, judgment, incentives, experimen-tal methodology

JEL Classification: B41, D80

I. Introduction

The predicted effect of financial incentives on human behavior is a sharp theoreti-cal dividing line between economics and other social sciences, particularly psychol-ogy. The difference is manifested in alternative conventions for running experi-ments. Economists presume that experimental subjects do not work for free andwork harder, more persistently, and more effectively, if they earn more money forbetter performance. Psychologists believe that intrinsic motivation is usually highenough to produce steady effort even in the absence of financial rewards; andwhile more money might induce more effort, the effort does not always improveperformance, especially if good performance requires subjects to induce sponta-neously a principle of rational choice or judgment, like Bayes’ rule.

CAMERER AND HOGARTH8

The effect of incentives is clearly important for experimental methodology. Inaddition, varying incentives can tell us something about human thinking andbehavior which should interest all social scientists, and may be important for

Žjudging the effects of incentives in naturally-occurring settings e.g., compensation.in firms, or public responses to taxation .

Ultimately, the effect of incentives is an empirical question. Indeed, it is anempirical question which has been partly answered, because many studies haveexplored the effect of varying levels of incentive in many different tasks. In thispaper we summarize the results of 74 studies comparing behavior of experimentalsubjects who were paid zero, low or high financial performance-based incentives.

The studies show that the effects of incentives are mixed and complicated. Theextreme positions, that incentives make no difference at all, or always eliminatepersistent irrationalities, are false. Organizing debate around those positions orusing them to make editorial judgments is harmful and should stop.

The presence and amount of financial incentive does seem to affect averageperformance in many tasks, particularly judgment tasks where effort responds to

Žincentives as measured independently by, for example, response times and pupil.dilation and where increased effort improves performance. Prototypical tasks of

Ž .this sort are memory or recall tasks in which paying attention helps , probabilityŽmatching and multicue probability learning in which keeping careful track of past

. Žtrials improves predictions , and clerical tasks e.g., coding words or building.things which are so mundane that monetary reward induces persistent diligence

when intrinsic motivation wanes. In many tasks incentives do not matter, presum-ably because there is sufficient intrinsic motivation to perform well, or additionaleffort does not matter because the task is too hard or has a flat payoff frontier. Inother tasks incentives can actually hurt, if increased incentives cause people to

Ž .overlearn a heuristic in problem-solving ‘‘insight’’ tasks , to overreact to feedbackŽ .in some prediction tasks to exert ‘‘too much effort’’ when a low-effort habit would

Ž .suffice choking in sports or when arousal caused by incentives raises self-con-Ž .sciousness test-taking anxiety in education .

In the kinds of tasks economists are most interested in, like trading in markets,bargaining in games and choosing among risky gambles, the overwhelming finding

Žis that increased incentives do not change average behavior substantively although.the variance of responses often decreases . When behavior does change, incentives

can be interpreted as shifting behavior away from an overly socially-desirablepresentation of oneself to a more realistic one: When incentives are low subjectssay they would be more risk-preferring and generous than they actually are whenincentives are increased.

II. Capital, labor, and production

Take a subject’s point of view. An experiment is a cognitive activity for whichŽ .subjects volunteer usually , somewhere between playing ‘‘charades’’ with friends at

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 9

a party and doing a neighbor’s taxes for extra pocket money. Subjects come to theexperiment with knowledge and goals. Earning more money is presumably onegoal. Subjects surely have other goals as well: They may be intrinsically motivatedto perform well, may want to appear intelligent by making quick decisions,sometimes try to amuse other subjects or fulfill the experimenter’s implicit ‘‘de-

Žmands,’’ and may want to exhibit socially desirable behavior like generosity and.risk-taking .

In economic terms, we can think of a subject’s goals as an objective function heor she is trying to maximize. Knowledge is ‘‘cognitive capital.’’ The requirements ofthe task, which we call ‘‘production,’’ are also important for determining perfor-mance. Psychologists ask: How well can subjects with particular knowledge, in aspecific task, achieve their goals? Equivalently, economists ask: How well cansubjects maximize their objective function, given available capital, and a particularproduction function?

Previous discussions in experimental economics have focussed almost exclusivelyon the objectives of minimizing effort cost and maximizing monetary reward,because economists instinctively assume thinking as a costly activity. For example,

Ž .in Smith and Walker’s 1993 ‘‘labor theory,’’ subjects respond to increased incen-tive by expending more cognitive effort, which is presumed to reduce variance

Ž .around responses. The simplest kind of labor theory rests on two intuitions: 1Mental effort is like physical effort}people dislike both, and will do more of both

Ž .if you pay them more; and 2 effort improves performance because, like scholars,subjects have access to a wide range of all-purpose analytical tools to solveexperimental problems. This simple view ignores two important factors}intrinsic

Žmotivation some people like mental effort, and those people disproportionately.volunteer for experiments! ; and the match between the analytical skills possess

and the demands of the tasks they face. Effort only improves performance if thematch is good. This latter omission is remedied by introducing the concepts ofcapital and production into the labor theory.

Capital

Cognitive psychologists distinguish ‘‘declarative knowledge’’}facts about the world}from ‘‘procedural knowledge’’}a repertoire of skills, rules and strategies forusing declarative knowledge to solve problems. Knowing that Pasadena is northeastof Hollywood is declarative knowledge; knowing how to read a map of Los Angelesis procedural knowledge.

Experimenters are usually interested in the procedural knowledge of subjects,Žnot the declarative knowledge. In a sense, good instruction-writing ensures that all

subjects have the declarative knowledge to understand how their decisions affect.their performance. We take procedural knowledge and ‘‘cognitive capital’’ to be

roughly the same. ‘Pieces’ of capital are a variety of tricks or approaches to solvingan experimental task, like the many specialized tools on a carpenter’s tool belt or a

CAMERER AND HOGARTH10

cook’s knowledge of foods, kitchen utensils, and recipes. In economics experiments,cognitive capital includes heuristics like anchoring on a probability of .5 andadjusting, rules of thumb like cutoffs for rejecting ultimatum offers, analytical

Žformulas or algorithms, personal skills or traits e.g., unusual ability to concentrate,.terrific short-term memory, perceptual skill, high ‘need for achievement’ , domain-

Ž .specific procedures ‘‘always wait until the end of the period to buy’’ and so forth.An important feature of capital is how it is acquired. In the time horizon of a

laboratory experiment, subjects probably acquire capital through learning-by-doingŽ .rather than from learning-by-thinking. As Smith 1991 wrote,

Many years of experimental research have made it plain that real people do notsolve decision problems by thinking about them in the way we do as economictheorists. Only academics learn primarily by reading and thinking. Those whorun the world, and support us financially, tend to learn by watching, listening

Ž .and doing p. 12 .

Furthermore, useful cognitive capital probably builds up slowly, over days ofmental fermentation or years of education rather than in the short-run of an

Ž . Žexperiment 1]3 hours . Cognitive psychologists say it takes 10 years or 10,000hours of practice to become expert at difficult tasks; see e.g., Ericcson and Smith,

.1991 . However, incentives surely do play an important role in inducing long-runcapital formation.

Production

A task’s production requirements are the kinds of capital necessary to achieve goodperformance. Some tasks, like clerical ones, require simple attention and diligence.Ž .Trading in markets might be like this, but includes perhaps patience and memory.Other tasks, like probability judgments, might use analytical skill or domain-specificknowledge. Complicated games might require special analytical devices like back-ward induction.

Adding capital and production to the labor theory has several general implica-tions.

First, capital variables}like educational background, general intelligence, andexperience with a task}can have effects that are as strong as the effect of

Ž .financial incentives and interact with incentives . If experimenters manipulateincentives because of a prior belief that incentive effects are large, they shouldspend more time measuring and manipulating capital variables as well.

Second, asking how well capital is suited to the production task at hand isimportant because poorly-capitalized subjects may perform worse when incentives

Žare stronger just as running too fast, without proper stretching or coaching, can.injure muscles .

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 11

Third, the nature of the production task matters because some tasks are simplyŽ .easier or have ‘‘floor effects’’ }that is, almost every subject has some kind of

Žcapital which enables good production}while others are hard ‘‘ceiling effects’’;.few subjects have the necessary capital .

Fourth, elements of experimental design can affect the production function andalter performance systematically. Simplicity of instructions, stimulus display, oppor-tunities for communication, and so forth, can affect performance and may also

Žinteract with incentives. For example, tasks that are designed to be engaging mayincrease attention, lowering the ‘‘cost’’ of effort or raising intrinsic motivation, and

.reducing the marginal effect of higher financial incentives.Fifth, considering capital and production together implies that in some tasks,

people should sacrifice short-run performance to learn better decision rules}toacquire cognitive capital useful for production}which raises a fresh empirical

Žquestion of whether people sacrifice earning for learning optimally see Merlo and.Schotter, 1999 .

III. A review of studies

The concepts of capital, labor, and production were introduced to provide a looseframework within which empirical effects of incentives can be understood.

The empirical heart of our paper is an informal review of 74 studies comparingbehavior of experimental subjects who were not paid, or were paid low or highfinancial incentives, according to their performance. The studies are those we knewof and which came to our attention, so the sampling is nonrandom. However, wealso sampled every article which varied financial incentives published in theAmerican Economic Re¨iew, Econometrica, Journal of Political Economy, and Quar-terly Journal of Economics from 1990]98. More careful surveys of studies were

Ž . Ž .done by Bonner et al. 1996 , Hertwig and Ortmann 1998 , and Jenkins et al.Ž .1998 ; we compare our conclusions with theirs below. Because of the opportunisticsampling we used, the reader is entitled to regard the paper as an informed essayor collection of conjectures, which may or may not prove true after a more careful

Ž .meta-analysis of studies and further research .Ž .Studies were included if they satisfied two rules: i Incentive levels were

Ž .reported and varied substantially within the study; and ii the study reportedenough detail of the level of incentive and size of any performance effects toenable us to classify the effects of incentive. Thus, studies were excluded if theylacked a within-study control group or underreported details of incentive effects.As far as we could tell, subjects always knew the payoff functions they faced.

Ž . Ž .Studies satisfying the control and reporting criteria i and ii are summarized inTable 1. The studies are classified in several groups}incentives help meanperformance, incentives hurt mean performance, incentives have no effect onmean performance, incentives affect behavior but behavior cannot be judged by aperformance standard, and incentive effects are confounded with effects of other

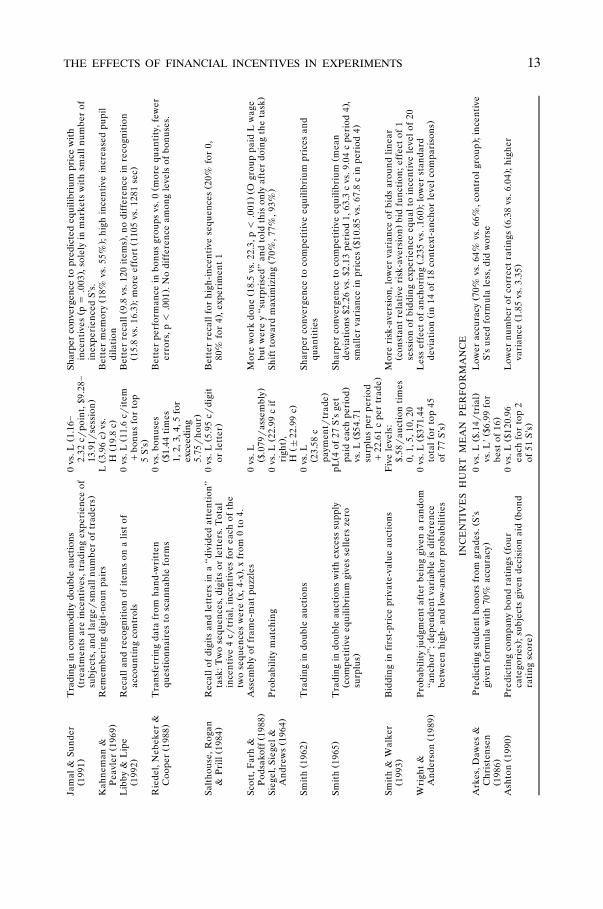

CAMERER AND HOGARTH12T

able

1.R

evie

wof

expe

rim

ents

mea

suri

ngef

fect

son

finan

cial

ince

ntiv

eson

perf

orm

ance

Ž.

Aut

hor

year

Tas

kIn

cent

ives

Eff

ect

ofhi

gher

ince

ntiv

es

INC

EN

TIV

ES

IMP

RO

VE

ME

AN

PE

RF

OR

MA

NC

EŽ

Ž.

ŽŽ

.A

shto

n19

90,

Pre

dict

ing

com

pany

bond

rati

ngs

four

cate

gori

es0

vs.L

$120

.96

Hig

her

num

ber

ofco

rrec

tra

ting

s4.

64vs

.5.5

8;l

ower

vari

ance

.Ž

.gr

oups

1]2

from

thre

enu

mer

ical

mea

sure

sof

fina

ncia

lea

chfo

rto

p2

3.57

vs.1

.74

;fee

dbac

k,w

ritt

enju

stif

icat

ion

rais

ednu

mbe

r.

Ž.

perf

orm

ance

of51

S’s

corr

ect

too

5.55

,5.3

1.

Ž.

Ž.

Ž.

Atk

inso

n19

58A

rith

met

ic,d

raw

ing

task

sL

$5.1

0,

Bet

ter

perf

orm

ance

48.3

7vs

.51.

96,p

-.0

1L

vs.H

;inv

erte

dŽ

.Ž

H$1

0.20

for

high

U-s

hape

def

fect

ofpr

obab

ility

ofw

inni

ng48

.03,

51.3

9,.

scor

ein

grou

psof

53.2

1,49

.18

;hig

h‘‘n

eed

for

achi

evem

ent’

’S’s

dobe

tter

.N

s20

,3,2

,or

top

3of

4Ž

.Ž

.A

was

thi&

Pra

ttJu

dgm

ent

prob

lem

s:co

njun

ctio

n,sa

mpl

esi

ze,

0vs

.L$2

.42

Slig

htde

clin

ein

erro

rra

te.4

6vs

..41

,red

uced

erro

rm

ore

for

Ž.

1990

and

sunk

cost

S’s

high

in‘‘p

erce

ptua

ldif

fere

ntia

tion

’’.4

4vs

..21

;mor

eti

me

Ž.

spen

tin

Lco

ndit

ion

4.2

vs.5

.7m

inŽ

.C

amer

er,H

o&

Dom

inan

ce-s

olva

ble

‘‘bea

uty

cont

est

gam

es’’

L$1

rro

und

vs.

Slig

htly

clos

erto

Nas

heq

uilib

rium

Ž.

Ž.

Wei

gelt

1997

mea

suri

ngle

vels

ofit

erat

edof

dom

inan

ceH

$4r

roun

dŽ

.Ž

.Ž

Ž.

Cas

tella

n19

69P

roba

bilit

ym

atch

ing:

sequ

enti

albe

ttin

gon

L3.

96cr

tria

l,

Shif

tto

war

dm

axim

izin

gtr

ials

81]

180

58%

vs.6

1%,p

Es

.6;

ŽŽ

.Ž

..

inde

pend

ent

draw

sof

even

tsS’

ssh

ould

H39

.6cr

tria

l83

%vs

.87%

,p-

.01,

pE

s.7

75al

way

sbe

ton

the

mos

tlik

ely

even

tE

,whi

chŽ

..

has

pE

chan

ceŽ

.Ž

.Ž

.C

oope

ret

al.

Sign

alin

gga

mes

wit

hou

tput

-quo

tara

tche

tef

fect

s;L

30yu

anr

Svs

.H

ighe

rfr

eque

ncy

ofst

rate

gic

pool

ing

choi

ces

50%

vs.6

0%,

Ž.

Ž.

Žin

pres

sC

hine

sest

uden

tsr

man

ager

ssu

bjec

tsH

150

yuan

rS

;no

diff

eren

cein

freq

uenc

yof

plan

ner

‘‘mis

take

s’’

66%

vs.

Ž.

30yu

ans

$3.7

5at

69%

;eff

ect

dim

inis

hed

byex

peri

ence

,mim

icke

dby

offi

cial

FX

;mgr

sin

stru

ctio

nco

ntex

t.

earn

100

yuan

rda

yŽ

Ž.

Dra

go&

Hey

woo

dC

hoic

eof

deci

sion

num

ber

ein

piec

e-ra

tean

dL

8.81

cga

infr

omM

ean

clos

erto

pred

icti

onof

3748

.7vs

.37.

2,ro

und

12,l

ower

Ž.

.Ž

.19

89ra

nk-o

rder

labo

r;in

cent

ive

trea

tmen

tis

es

0to

e*s

37vs

.va

rian

ce96

4vs

.51,

roun

d12

.Ž

.‘‘f

latn

ess’

’of

expe

cted

payo

fffu

ncti

onH

84.4

cga

inŽ

.Ž

.Ž

Ž.

Glu

cksb

erg

1962

Eas

ypr

oble

m-s

olvi

ngw

ith

ahe

lpfu

lvis

ualc

lue

0vs

.Lfa

stes

tP

robl

em-s

olvi

ng:f

aste

r5.

0vs

.3.7

min

,mor

eso

luti

ons

Ž.

Ž.

and

reco

gnit

ion

offa

mili

arw

ords

25%

S’s

$23.

5826

vs.3

0;w

ord

reco

gnit

ion:

fast

er47

.0vs

.34.

0se

cea

ch,f

aste

stS

.$9

4.34

ŽŽ

Gre

ther

1980

,P

roba

bilit

yju

dgm

ents

ofev

ents

and

choi

ceof

0vs

.L$1

0fo

rSi

mila

rno

n-B

ayes

ian

patt

erns

,but

ince

ntiv

eS’

sle

ssfa

rfr

om.

.Ž

.19

92ex

ps1]

2m

ost-

likel

yev

ents

,bas

edon

sam

ple

info

rmat

ion

corr

ect

choi

ceB

ayes

ian;

few

erer

rone

ous

resp

onse

s12

%vs

.4%

.Ž

.So

me

use

ofsc

orin

gru

les

Ž.

ŽŽ

ŽH

arri

son

1994

Cho

ices

ofga

mbl

esto

test

EU

theo

ry‘‘A

llais

0vs

.LE

Vs

$.55

]Sm

allr

educ

tion

inA

llais

para

dox

35%

vs.1

5%,c

ondi

tion

s.

..

Ž.

para

dox’

’$6

.45

AP

0-A

P1

,sta

tist

ical

lym

argi

nal

ps

.14

two-

taile

dz-

test

ŽH

ogar

thet

al.

Pre

dict

ion

ofst

ocha

stic

outc

ome

from

two

cues

0vs

.LH

ighe

rac

cura

cyw

hen

pena

lty

func

tion

was

‘‘len

ient

’’sm

all

Ž.

Ž.

.19

911.

16cr

poin

tw

eigh

ton

squa

red

erro

rin

eval

uati

onfu

ncti

on,m

eans

358

vs.

Ž.

288

expe

rim

ent

1

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 13Ž

Jam

al&

Sund

erT

radi

ngin

com

mod

ity

doub

leau

ctio

ns0

vs.L

1.16

]Sh

arpe

rco

nver

genc

eto

pred

icte

deq

uilib

rium

pric

ew

ith

Ž.

ŽŽ

.19

91tr

eatm

ents

are

ince

ntiv

es,t

radi

ngex

peri

ence

of2.

32cr

poin

t,$9

.28]

ince

ntiv

esp

s.0

03,s

olel

yin

mar

kets

wit

hsm

alln

umbe

rof

..

subj

ects

,and

larg

ersm

alln

umbe

rof

trad

ers

13.9

1rse

ssio

nin

expe

rien

ced

S’s.

Ž.

Ž.

Kah

nem

an&

Rem

embe

ring

digi

t-no

unpa

irs

L3.

96c

vs.

Bet

ter

mem

ory

18%

vs.5

5%;h

igh

ince

ntiv

ein

crea

sed

pupi

lŽ

.Ž

.P

eavl

er19

69H

19.8

cdi

lati

onŽ

Ž.

Lib

by&

Lip

eR

ecal

land

reco

gnit

ion

ofit

ems

ona

list

of0

vs.L

11.6

crit

emB

ette

rre

call

9.8

vs.1

20it

ems

,no

diff

eren

cein

reco

gnit

ion

Ž.

Ž.

Ž.

1992

acco

unti

ngco

ntro

lsq

bonu

sfo

rto

p15

.8vs

.16.

3;m

ore

effo

rt11

05vs

.128

1se

c.

5S’

sŽ

Rie

del,

Neb

eker

&T

rans

ferr

ing

data

from

hand

-wri

tten

0vs

.bon

uses

Bet

ter

perf

orm

ance

inbo

nus

grou

psvs

.0m

ore

quan

tity

,few

erŽ

.Ž

.C

oope

r19

88qu

esti

onna

ires

tosc

anna

ble

form

s$1

.44

tim

eser

rors

,p-

.001

.No

diff

eren

ceam

ong

leve

lsof

bonu

ses.

1,2,

3,4,

5fo

rex

ceed

ing.

5.75

rho

urŽ

ŽSa

ltho

use,

Rog

anR

ecal

lof

digi

tsan

dle

tter

sin

a‘‘d

ivid

edat

tent

ion’

’0

vs.L

5.95

crdi

git

Bet

ter

reca

llfo

rhi

gh-i

ncen

tive

sequ

ence

s20

%fo

r0,

Ž.

..

&P

rill

1984

task

:Tw

ose

quen

ces,

digi

tsor

lett

ers.

Tot

alor

lett

er80

%fo

r4

,exp

erim

ent

1in

cent

ive

4cr

tria

l,in

cent

ives

for

each

ofth

eŽ

.tw

ose

quen

ces

wer

ex,

4-x

,xfr

om0

to4.

Ž.Ž

Scot

t,F

arh

&A

ssem

bly

offr

ame-

mat

puzz

les

0vs

.LM

ore

wor

kdo

ne18

.5vs

.22.

3,p

-.0

01O

grou

ppa

idL

wag

eŽ

.Ž

..

Pod

sako

ff19

88$.

079r

asse

mbl

ybu

tw

ere

y‘‘s

urpr

ised

’’an

dto

ldth

ison

lyaf

ter

doin

gth

eta

skŽ

Ž.

Sieg

el,S

iege

l&P

roba

bilit

ym

atch

ing

0vs

.L22

.99

cif

Shif

tto

war

dm

axim

izin

g70

%,7

7%,9

3%Ž

..

And

rew

s19

64ri

ght

,Ž

.H

"22

.99

cŽ

.Sm

ith

1962

Tra

ding

indo

uble

auct

ions

0vs

.LSh

arpe

rco

nver

genc

eto

com

peti

tive

equi

libri

umpr

ices

and

Ž 23.

58c

quan

titi

es.

paym

entr

trad

eŽ

.Ž

ŽSm

ith

1965

Tra

ding

indo

uble

auct

ions

wit

hex

cess

supp

lypL

4of

27S’

sge

tSh

arpe

rco

nver

genc

eto

com

peti

tive

equi

libri

umm

ean

Ž.

.co

mpe

titi

veeq

uilib

rium

give

sse

llers

zero

paid

each

peri

odde

viat

ions

$2.2

6vs

.$2.

13pe

riod

1,63

.3c

vs.9

.04

cpe

riod

4,

.Ž

Ž.

surp

lus

vs.L

$54.

71sm

alle

rva

rian

cein

pric

es$1

0.85

vs.6

7.8

cin

peri

od4

surp

lus

per

peri

od.

q22

.61

cpe

rtr

ade

Smit

h&

Wal

ker

Bid

ding

infi

rst-

pric

epr

ivat

e-va

lue

auct

ions

Fiv

ele

vels

:M

ore

risk

-ave

rsio

n,lo

wer

vari

ance

ofbi

dsar

ound

linea

rŽ

.Ž

.19

93$.

58r

auct

ion

tim

esco

nsta

ntre

lati

veri

sk-a

vers

ion

bid

func

tion

;eff

ect

of1

0,1,

5,10

,20

sess

ion

ofbi

ddin

gex

peri

ence

equa

lto

ince

ntiv

ele

velo

f20

ŽŽ

.W

righ

t&

Pro

babi

lity

judg

men

taf

ter

bein

ggi

ven

ara

ndom

0vs

.L$3

71.4

4L

ess

effe

ctof

anch

orin

g.2

35vs

..16

0;l

ower

stan

dard

Ž.

Ž.

And

erso

n19

89‘‘a

ncho

r’’;

depe

nden

tva

riab

leis

diff

eren

ceto

talf

orto

p45

devi

atio

nin

14of

18co

ntex

t-an

chor

leve

lcom

pari

sons

.be

twee

nhi

gh-

and

low

-anc

hor

prob

abili

ties

of77

S’s

INC

EN

TIV

ES

HU

RT

ME

AN

PE

RF

OR

MA

NC

EŽ

Ž.

Ž.

Ark

es,D

awes

&P

redi

ctin

gst

uden

tho

nors

from

grad

es.

S’s

0vs

.L$.

14r

tria

lL

ower

accu

racy

70%

vs.6

4%vs

.66%

,con

trol

grou

p;i

ncen

tive

.Ž

Chr

iste

nsen

give

nfo

rmul

aw

ith

70%

accu

racy

vs.L

9$6

.99

for

S’s

used

form

ula

less

,did

wor

seŽ

..

1986

best

of16

Ž.

ŽŽ

Ž.

Ash

ton

1990

Pre

dict

ing

com

pany

bond

rati

ngs

four

0vs

.L$1

20.9

6L

ower

num

ber

ofco

rrec

tra

ting

s6.

38vs

.6.0

4;h

ighe

r.

ŽŽ

.ca

tego

ries

;sub

ject

sgi

ven

deci

sion

aid

bond

each

for

top

2va

rian

ce1.

85vs

.3.3

5.

.ra

ting

scor

eof

51S’

s

CAMERER AND HOGARTH14Ž

.T

able

1.C

ontin

ued

Ž.

Aut

hor

year

Tas

kIn

cent

ives

Eff

ect

ofhi

gher

ince

ntiv

es

INC

EN

TIV

ES

HU

RT

ME

AN

PE

RF

OR

MA

NC

EŽ

.Ž

.Ž

Fri

edm

an19

98D

ecid

ing

whe

ther

tosw

itch

chos

en‘‘d

oor’

’in

Lq

$.40

rq

$.10

Les

ssw

itch

ing

athi

gher

ince

ntiv

es43

.9vs

.48.

7,p

s.0

0to

.10

Ž.

Ž.

.‘‘t

hree

-doo

r’’p

robl

emsw

itch

ing

isB

ayes

ian

vs.H

q$1

ry

$.50

inpr

obit

regr

essi

ons

Ž.

ŽŽ

Ž.

Glu

cksb

erg

1962

Dif

ficu

lt‘‘i

nsig

ht’’

prob

lem

-sol

ving

Dun

cker

0vs

.Lfa

stes

tP

robl

em-s

olvi

ng:f

ewer

solu

tion

s22

vs.1

6,s

low

er.

Ž.

cand

lepr

oble

man

dre

cogn

itio

nof

fam

iliar

25%

S’s

$23.

587.

4vs

.11.

1m

in;w

ord

reco

gnit

ion:

fast

erre

cogn

itio

nfo

rŽ

.Ž

.Ž

.‘‘c

hurc

h’’

and

unfa

mili

ar‘‘

vign

ette

’’w

ords

each

,fas

test

Sfa

mili

arw

ords

47vs

.34

sec

,slo

wer

for

unfa

mili

arw

ords

.Ž

.$9

4.34

151.

9vs

.199

.8Ž

ŽG

reth

er&

Plo

ttC

hoic

e-pr

icin

gpr

efer

ence

reve

rsal

sov

erm

oney

0vs

.LE

Vfr

omH

ighe

rra

teof

reve

rsal

sfo

rP

-bet

choi

ces

55.9

%vs

.69.

7%,

Ž.

..Ž

.19

79ga

mbl

es$2

.79]

7.97

ps

.05

expe

rim

ent

1Ž

Hog

arth

etal

.P

redi

ctio

nof

stoc

hast

icou

tcom

efr

omtw

ocu

es0

vs.L

Low

erac

cura

cyw

hen

pena

lty

func

tion

was

‘‘exa

ctin

g’’

high

Ž.

Ž.

.19

911.

16cr

poin

tw

eigh

ton

squa

red

erro

rin

eval

uati

onfu

ncti

on,m

eans

319

vs.

Ž.

301

expe

rim

ent

1Ž

.Ž

Ž.

McG

raw

&Se

t-br

eaki

ngpr

oble

mL

uchi

nsw

ater

jug

:nin

e0

vs.L

$.10

qSl

ower

solu

tion

tim

eon

10th

prob

lem

181

vs.2

89se

cŽ

McC

ulle

rssi

mila

rpr

oble

ms,

follo

wed

by10

thdi

ffer

ent

one;

$2.0

7if

all

diff

eren

ceno

tdu

eto

extr

ach

ecki

ngti

me,

but

tosl

ower

Ž.

..

1979

depe

nden

tva

riab

leis

perf

orm

ance

on10

than

swer

sco

rrec

tid

enti

fica

tion

of‘‘s

et-b

reak

ing’

’sol

utio

nŽ

Ž.

Mill

er&

Est

esId

enti

fica

tion

ofvi

sual

stim

uli

two

face

sw

ith

0vs

.LM

ore

erro

rsin

Lan

dH

than

021

%,3

2%,3

4%;n

oŽ

..

Ž.

1961

diff

eren

tey

ebro

ws

$0.0

48r

tria

ldi

ffer

ence

inre

spon

seti

mes

;S’s

wer

e9-

year

old

boys

Ž.

H$2

.38r

tria

lŽ

.Ž

Schw

artz

1982

Lea

rnin

gru

les

gove

rnin

gw

hich

sequ

ence

sof

0vs

.LN

egat

ive

effe

ctof

tria

l-by

-tri

alpa

yoff

from

L,H

63%

ofru

les

Ž.

.le

ver

pres

ses

are

rew

arde

d$.

016r

succ

ess

disc

over

edvs

.80%

for

0,83

%M

,for

pret

rain

edsu

bjec

tson

ly;

ŽŽ

.vs

.M$1

.62

for

noef

fect

for

inex

peri

ence

dsu

bjec

ts95

%ru

les

disc

over

ed;

.Ž

.ru

ledi

scov

ery

vs.

cf.M

erlo

and

Scho

tter

inpr

ess

.Ž

.H

Lan

dM

INC

EN

TIV

ES

DO

NO

TA

FF

EC

TM

EA

NB

EH

AV

IOR

Ž.

Ž.

ŽB

ohm

1994

Cho

ice-

pric

ing

Vic

krey

-auc

tion

buyi

ngpr

ice

0vs

.L1r

10Sm

all,

insi

gnif

ican

tre

duct

ion

inov

eral

lper

cent

age

ofŽ

pref

eren

cere

vers

als

over

futu

rem

oney

chan

ceof

gett

ing

pref

eren

cere

vers

als

choo

sing

one

clai

mbu

tbi

ddin

gm

ore

for

Ž.

Ž.

paym

ents

1072

Swed

ish

kron

erin

3m

ovs

.pr

efer

red

choi

ce,

anot

her

,19%

vs.2

9%T

able

1,fi

nanc

est

uden

tson

ly;b

igge

r.

1290

SEK

in15

mo

or10

S’s

inV

ickr

eyre

duct

ion

inre

vers

alfo

rth

ose

who

choo

se3-

mon

thpa

ymen

t,au

ctio

n,hi

gh15

%vs

.63%

.bi

dder

win

sŽ

.Ž

.Ž

.B

olle

1990

Ult

imat

umba

rgai

ning

:off

erta

ke-i

t-or

-lea

ve-i

tL

2.42

DM

,N

odi

ffer

ence

inm

ean

offe

rs41

%,3

6%,4

1%,4

5%or

low

est

ŽŽ

.Ž

.Ž

Ž.

part

ofam

ount

Xpr

edic

tion

sof

fer

of$.

01,

H24

.2D

M,

amou

ntac

cept

ed38

%,3

3%,2

8%,3

2%no

te:

pL,L

.Ž

Ž.

Ž.

acce

ptan

ceof

any

posi

tive

amou

ntpL

ps

1r10

ofan

dpH

,Hha

veso

me

expe

cted

payo

ffs

but

pL,H

wer

e.

.24

.2D

M,

mor

esi

mila

rŽ

pHp

s1r

10of

.24

2D

M

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 15Ž

.Ž

.Ž

.B

ull,

Scho

tter

&C

hoic

esof

deci

sion

num

bers

sim

ulat

ing

effo

rtin

L0]

$1.9

6rtr

ial

,D

ecis

ion

num

bers

‘‘did

not

diff

er’’

fn8,

node

tails

repo

rted

Ž.

Ž.

Wei

gelt

1987

rank

-ord

erla

bor

‘‘tou

rnam

ents

’’H

0]$7

.89r

tria

lŽ

.Ž

.Ž

Cam

erer

1987

Tra

ding

indo

uble

auct

ions

for

risk

yas

sets

whe

reL

$.47

5ras

set

vs.

No

diff

eren

cein

amou

ntof

bias

.09

vs..

14bi

asin

1-re

dŽ

..

‘‘rep

rese

ntat

iven

ess’

’jud

gmen

tsca

nbi

asas

set

H$2

.38r

asse

tsa

mpl

es,.

10vs

..01

in2-

red

sam

ples

pric

esŽ

.Ž

Cam

erer

1989

Cho

ices

ofga

mbl

es0

vs.L

expe

cted

No

sign

ific

ant

diff

eren

ces

inri

sk-a

vers

ion

orte

st-r

etes

tre

liabi

lity

.va

lue

$6.3

0Ž

Ž.

Ž.

Cam

erer

1990

,U

ltim

atum

barg

aini

ngpL

Xs

$12.

17N

odi

ffer

ence

inof

fers

39%

vs.3

8%or

low

est

amou

ntac

cept

ed.

Ž.

Ž.

p.31

5pH

Xs

$121

.70

21%

vs.1

5%Ž

.p

s1r

39Ž

.C

ox&

Gre

ther

Pre

fere

nce

reve

rsal

s:di

scre

panc

ies

betw

een

0vs

.L.5

ofH

No

diff

eren

cebe

twee

nra

tes

ofpr

edic

ted

and

unpr

edic

ted

Ž.

ŽŽ

Ž.

1996

gam

ble

choi

ces

and

valu

atio

nes

tabl

ishe

dus

ing

vs.H

mea

n$6

0.57

reve

rsal

sus

ing

BD

M60

%,7

3%,4

6%,p

erio

d1

,sm

all

.Ž

.B

ecke

r-D

eGro

ot-M

arsc

hak

proc

edur

eor

seal

ed-

for

1-1r

2hr

diff

eren

cein

seco

nd-p

rice

auct

ion

37%

,76%

,73%

,opp

osit

eŽ

.bi

dau

ctio

n,or

Eng

lish

cloc

kde

scen

ding

-pri

cedi

ffer

ence

inE

nglis

hcl

ock

auct

ion

93%

,79%

,47%

..

auct

ion

repe

titi

onel

imin

ates

pred

icte

dP

Rin

seco

nd-p

rice

auct

ion

Ž.

0,29

%,2

7%in

roun

d5

,Eng

lish

cloc

kau

ctio

non

lyin

L,H

Ž.

cond

itio

ns.L

and

HS’

sm

ore

risk

-ave

rse

46%

vs.5

4%.N

oŽ

.di

ffer

ence

inin

tran

siti

vity

16%

0vs

.11%

for

L-H

Ž.

Ž.

ŽC

raik

&T

ulvi

ngL

earn

ing

tore

mem

ber

wor

dsL

2.76

cM

8.29

c,

No

effe

cton

amou

ntof

accu

rate

reca

ll65

%,6

4%,6

6%,

Ž.

Ž.

.19

75H

16.6

cex

peri

men

t10

Ž.

Feh

r&

Tou

gare

vaC

hoic

esof

wag

esan

def

fort

sin

expe

rim

enta

lL

upto

$1r

peri

odN

oef

fect

onav

erag

ew

age,

wor

ker

effo

rt,o

rsl

ope

ofef

fort

-Ž

.Ž

Ž.

1996

labo

rm

arke

tvs

.Hup

tow

age

rela

tion

.007

4vs

..00

72.A

vera

gesu

bjec

tin

com

e.

Ž.

$10r

peri

od$1

7rm

onth

Rus

sian

sŽ

.F

iori

na&

Plo

tt5-

pers

onco

mm

itte

ech

oice

sof

atw

o-di

men

sion

alL

2.3]

11.6

crun

itM

argi

nally

sign

ific

ant

redu

ctio

nin

devi

atio

nof

aver

aged

data

Ž.

Ž.

ŽŽ

1978

poin

tcf

.Kor

men

dian

dP

lott

,198

0H

$2.3

2]fr

omth

eco

re2.

5un

its

vs.1

,ps

.08

and

.11

ondi

ffer

ent

..

$6.9

6run

itdi

men

sion

sby

Epp

s-Si

ngle

ton

test

;red

ucti

onin

%of

poin

tsŽ

.Ž

.ou

tsid

ene

ar-c

ore

regi

onp

s.0

6;l

ess

vari

ance

20vs

.7Ž

.Ž

Fou

rake

r&

Sieg

elD

uopo

lyan

dtr

iopo

lyqu

anti

tych

oice

sC

ourn

otL

vs.H

$37.

27,

No

diff

eren

cein

mea

nor

vari

ance

ofpr

ofit

sŽ

.19

6323

.29,

9.32

bonu

s.

toto

p3

Ž.

For

syth

eet

al.

Ult

imat

umba

rgai

ning

0vs

.L$5

.36

vs.

No

diff

eren

cein

offe

rsor

low

est

amou

ntac

cept

ed;l

ess

cros

s-Ž

.Ž

.19

94H

$10.

73se

ssio

nva

rian

ce;m

ean

offe

rs40

%,4

5%,4

7%Ž

.G

uth,

Schm

itt-

Ult

imat

umba

rgai

ning

L1.

62D

MN

odi

ffer

ence

inof

fers

orlo

wes

tam

ount

acce

pted

Ž.

berg

er&

H16

.2D

MŽ

.Sc

hwar

ze19

82Ž

.Ž

ŽH

ey19

82,1

987

Sear

ch:d

ecis

ions

abou

tw

hich

pric

eto

acce

pt0

vs.L

expe

cted

No

sign

ific

ant

effe

cton

amou

ntof

opti

mal

stop

ping

25%

vs.

..

from

ase

quen

ceof

pric

es£8

.15

33%

orap

pare

ntse

arch

rule

sŽ

.Ž

Hof

fman

,McC

abe

Ult

imat

umba

rgai

ning

L$1

0.73

rpa

irvs

.N

osi

gnif

ican

tdi

ffer

ence

cont

estr

exch

ange

,mea

nof

fer

31%

Ž.

Ž.

&Sm

ith

1996

aH

$107

.27r

pair

vs.2

8%,m

ean

reje

cted

offe

r20

%vs

.18%

;ran

dom

,mea

nof

fer

.44

%vs

.44%

,mea

nre

ject

edof

fer

35%

vs.4

0%Ž

.Ir

win

etal

.B

ids

for

$3ti

cket

elic

ited

byB

ecke

r-D

eGro

ot-

L1

cfo

r$1

erro

rN

osi

gnif

ican

tef

fect

onm

ean

devi

atio

nfr

omtr

uthf

ulbi

ddin

gŽ

.Ž

Ž.Ž

.in

pres

sM

arsc

hak

met

hod

wit

hdi

ffer

ent

pena

litie

sfo

rvs

.H20

cfo

r$.

62vs

.$.5

0ex

peri

men

t2,

full

info

rmat

ion

.su

bopt

imal

ity

$1er

ror

CAMERER AND HOGARTH16

Ž.

Tab

le1.

Con

tinue

d

Ž.

Aut

hor

year

Tas

kIn

cent

ives

Eff

ect

ofhi

gher

ince

ntiv

es

INC

EN

TIV

ES

DO

NO

TA

FF

EC

TM

EA

NP

ER

FO

RM

AN

CE

Ž.

Ž.

Kah

nem

an,

Men

tala

rith

met

ic:r

emem

beri

ngfo

ur-d

igit

stri

ngs

L8.

26c

No

effe

cton

accu

racy

88%

vs.8

2%;i

ncre

ased

pupi

ldila

tion

Ž.

Pea

vler

&an

dad

ding

0or

1to

each

digi

tH

41.3

cin

easi

erad

d-0

cond

itio

nŽ

.O

nusk

a19

68Ž

Loo

mes

&T

aylo

rC

hoic

esov

er3

gam

ble

pair

sar

eth

ere

regr

et-

0vs

.LN

odi

ffer

ence

,21.

6%cy

cles

vs.1

8.5%

cycl

esŽ

..

Ž.

1992

indu

ced

intr

ansi

tive

cycl

es?

EV

s£4

.22

Ž.

ŽM

cKel

vey

&P

alfr

eyC

hoic

esin

mul

ti-s

tage

‘‘cen

tipe

dega

mes

’’L

$.20

-$vs

.HN

osi

gnif

ican

tdi

ffer

ence

.06

vs..

15eq

uilib

rium

taki

ngat

Ž.

Ž.

.19

92$6

0]$2

4fi

rst

node

Ž.

Ž.

Nee

lin,

Sequ

enti

alba

rgai

ning

:sub

ject

sal

tern

ate

offe

rsL

Xs

$6.5

6vs

.N

odi

ffer

ence

inm

ean

perc

enta

geof

Xof

fere

d34

%vs

.34%

orŽ

.Ž

.So

nnen

sche

in&

divi

ding

a‘‘s

hrin

king

pie’

’of

size

Xac

ross

five

HX

s$1

9.69

mea

nof

fer

reje

cted

26%

vs.3

0%Ž

.Sp

iege

l19

88ro

unds

Ž.

ŽŽ

.Ž

Nils

son

1987

Rec

alla

ndre

cogn

itio

nof

wor

ds0

vs.L

$13.

58fo

rN

odi

ffer

ence

inre

call

35%

vs.3

3%or

reco

gnit

ion

58%

vs.

..

best

S,n

s10

55%

;inc

enti

veS’

sse

lf-r

epor

ted

wor

king

hard

er.

Ž.

ŽR

oth

etal

.U

ltim

atum

barg

aini

ngL

$11.

60r

pair

vs.

No

diff

eren

cein

ulti

mat

umga

mes

med

ian

48]

50%

inro

unds

1,Ž

.Ž

..

1991

H$3

4.79

rpa

ir10

for

both

L,H

;sm

all,

insi

gnif

ican

tdi

ffer

ence

in‘‘m

arke

t’’

Ž.

gam

esw

ith

9pr

opos

ers

com

peti

ngm

edia

n58

%vs

.78%

ŽŽ

Sam

uels

on&

Buy

ers

bidd

ing

agai

nst

anin

form

edse

ller

0vs

.Lq

$7.1

9to

No

effe

cton

med

ian,

mod

albi

ds

50,v

ersi

on3,

com

pare

Ž.

Ž.

..

Baz

erm

an19

85‘‘a

cqui

re-a

-com

pany

’’pr

oble

my

$14.

39F

igs.

3,10

a.

ŽŽ

.Si

egal

&F

oura

ker

Buy

er-s

elle

rba

rgai

ning

over

pric

e-qu

anti

typa

irs

L48

.5c]

77.6

5c

No

sign

ific

ant

diff

eren

cein

mea

npr

ofit

266.

92c

vs.4

3.68

c.

Ž.

Ž.

Ž.

1960

ince

ntiv

eis

diff

eren

tial

betw

een

Par

eto-

opti

mal

diff

eren

cevs

.m

uch

low

erva

rian

ce24

26c

vs.9

2.21

c.

Ž.

and

adja

cent

-qua

ntit

you

tcom

eH

$2.9

1Ž

.Ž

Stra

ub&

Ult

imat

umof

fers

and

acce

ptan

ceth

resh

olds

,pL

$10.

47pi

eN

osi

gnif

ican

tdi

ffer

ence

inm

ean

offe

rs31

%to

26%

for

Ž.

Mur

nigh

anco

mpl

ete

and

part

iali

nfor

mat

ion

resp

onde

rsdo

tim

es1,

3,5,

8,10

mul

tipl

ier

1to

10or

mea

nac

cept

ance

thre

shol

dsŽ

..

ŽŽ

.19

95no

tkn

owpi

esi

zeP

rob

ofpl

ayin

g19

%vs

.20%

.p

s2r

1813

ŽŽ

Wal

lste

n,B

udes

cuP

roba

bilit

yju

dgm

ents

usin

gnu

mer

ical

orve

rbal

0vs

.Lto

tal$

20N

osi

gnif

ican

tdi

ffer

ence

inac

cura

cym

easu

red

byan

Ž.

.&

Zw

ick

1993

expr

essi

ons

bonu

sfo

rto

p4

ince

ntiv

e-co

mpa

tibl

esp

heri

cals

cori

ngru

le;s

ome

diff

eren

ce.

Ž.

Ž.

Žof

7S’

sin

posi

tive

Pan

dne

gati

veN

cond

itio

nsP

,Ngu

aran

tee

)0,

.-

0pa

yoff

sfo

rst

atin

gpr

obab

ility

.5Ž

.Ž

Ž.

Web

eret

al.

1997

Tra

ding

risk

yas

sets

indo

uble

auct

ions

wit

h0

vs.L

EV

‘‘No

diff

eren

cein

mar

ket

pric

es’’

p.17

.di

ffer

ent

endo

wm

ent

cond

itio

ns.2

2D

Mr

unit

vs.H

Ž.

Ž.

long

,neu

tral

,sho

rtE

V2.

20D

Mr

unit

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 17

INC

EN

TIV

ES

AF

FE

CT

BE

HA

VIO

R,

BU

TN

OP

ER

FO

RM

AN

CE

STA

ND

AR

DB

atta

lio,J

iran

yaku

lC

hoic

eof

gam

bles

Mor

eri

sk-a

vers

eŽ

.&

Kag

el19

90Ž

Ž.

Bea

ttie

&L

oom

esC

hoic

eof

gam

bles

0vs

.pL

1r4

No

diff

eren

ceq’

s1]

3;n

odi

ffer

ence

in‘‘c

omm

onra

tio

effe

ct’’;

Ž.

.Ž

Ž.

1997

chan

cevs

.LE

Vm

ore

risk

-ave

rsio

nq

4;36

%,2

2%,8

%.

£3to

£7.8

1Ž

.Ž

.Ž

Bin

swan

ger

1980

Cho

ice

ofga

mbl

esby

poor

Indi

anfa

rmer

s0

vs.L

EV

86.5

4M

ore

risk

-ave

rsio

nat

high

erst

akes

,.86

,8.6

5,86

.54

rupe

es;n

oru

pees

s.2

%of

diff

eren

cein

mea

nri

sk-a

vers

ion,

hypo

thet

ical

vs.r

eal8

6.54

.Ž

.av

erag

eS’

sw

ealt

hru

pees

p.39

8;h

ypot

heti

calc

hoic

esm

ore

disp

erse

dŽ

Ž.

Cub

itt,

Star

mer

&C

hoic

eof

gam

bles

0vs

.LE

Vfr

omM

ore

risk

-ave

rse

50%

vs.6

0%,g

roup

s3.

1]3.

2Ž

..

Sugd

en19

98£2

.5to

12Ž

.Ž

.Ž

Edw

ards

1953

Cho

ice

ofga

mbl

esp,

$Xw

ith

pXhe

ldco

nsta

nt0

vs.H

pXs

53c,

Mor

eri

sk-s

eeki

ng.L

arge

rde

viat

ions

from

EV

and

EU

.0,

y53

cm

axim

izat

ion

for

bets

wit

hpX

s53

cor

0;fe

wer

intr

ansi

tivi

ties

ŽŽ

.Ž

For

syth

eet

al.

Dic

tato

r‘‘g

ames

’’on

epe

rson

divi

des

$10.

730

vs.L

$5.3

6vs

.M

ore

self

-int

eres

ted

offe

rs50

%of

fer

half

and

15%

offe

r0

vs.

Ž.

.Ž

..

1994

betw

een

self

and

othe

rH

$10.

7320

%of

fer

half

and

35%

offe

r0

;mea

ns48

%,2

8%,2

3%Ž

Ž.Ž

.G

reth

er&

Plo

ttC

hoic

eof

gam

bles

0vs

.LE

Vfr

omM

ore

risk

-see

king

p-

.01

expe

rim

ent

1Ž

..

1979

$2.7

9to

7.97

ŽŽ

.C

umm

ings

,Har

riso

nC

hoic

eof

whe

ther

tobu

yco

nsum

erpr

oduc

ts0

vs.L

hypo

thet

ical

Few

erpu

rcha

ses

9%vs

.31%

.Ž

..

&R

utst

rom

1995

vs.a

ctua

lpur

chas

e¨

Ž.

Ž.

Hog

arth

&E

inho

rnC

hoic

eof

gam

bles

LE

Vs

$.12

vs.

Mor

eri

sk-a

vers

e40

%vs

.73%

gain

s,24

%vs

.36%

loss

esŽ

.Ž

.Ž

.19

90H

EV

s$1

2.10

expe

rim

ent

3Ž

Irw

in,M

cCle

lland

Vic

krey

auct

ions

for

insu

ranc

eag

ains

tri

sky

loss

es0

vs.L

.011

,M

ore

risk

-ave

rse:

med

ian

bids

high

er,f

ewer

zero

bids

and

very

Ž.

.&

Schu

lze

1992

y$4

5.06

high

bids

ŽŽ

.Ž

Kac

helm

eier

&C

hoic

eof

gam

bles

Can

adia

nan

dC

hine

sest

uden

ts:

L1.

13yu

anvs

.M

ore

risk

-ave

rse

cert

aint

y-eq

uiva

lent

shi

gher

than

expe

cted

Ž.

.Ž

..

Sheh

ata

1992

67.5

8yu

ans

mon

thly

inco

me

H11

.26

yuan

valu

efo

rL

ince

ntiv

e;b

oth

Lan

dH

over

wei

ght

low

win

ning

prob

abili

ties

ŽŽ

.L

ist

&Sh

ogre

nV

alua

tion

sof

rece

ived

Chr

istm

asgi

fts

0vs

.L4t

h-pr

ice

Hig

her

valu

atio

nsin

actu

alau

ctio

n$9

6vs

.$13

7Ž

.19

98V

ickr

eyau

ctio

n.

for

244

gift

sŽ

.Ž

Seft

on19

92D

icta

tor

gam

es0

vs.p

L1r

4M

ore

self

-int

eres

ted

offe

rsin

Lco

ndit

ion,

mea

ns$2

.15,

$2.0

6,.

Ž.

chan

ceof

play

ing

$1.2

30,

pLth

esa

me,

both

sign

ific

antl

ydi

ffer

ent

from

LŽ

.vs

.L$5

.63r

pair

Ž.

ŽŽ

Scho

emak

er19

90C

hoic

eof

gam

bles

0vs

.pL

7r24

2Sl

ight

lym

ore

risk

-ave

rse

75%

vs.7

7%ga

ins,

23%

vs34

%.

chan

ceof

play

ing

loss

es,p

s.2

0E

Vs

$60.

48,

.y

60.4

8Ž

.Sl

onim

&R

oth

Ult

imat

umba

rgai

ning

L$1

.90

,R

ejec

tion

rate

sof

perc

enta

geof

fers

low

erw

ith

incr

ease

dst

akes

Ž.

Ž.

Ž.

Ž.

1998

M$9

.70

,44

%,1

9%,1

3%fo

rof

fers

25]

40%

,pM

vs.L

s.0

4,Ž

.Ž

.Ž

.H

$48.

4p

Hvs

.Ls

.002

;bar

gain

ing

inSl

ovak

crow

ns60

,300

,150

0Ž

.Ž

.Ž

.Sl

ovic

1969

Cho

ice

ofga

mbl

es0

vs.L

EV

$7.1

2M

ore

risk

-ave

rse

p-

.01

CAMERER AND HOGARTH18

Ž.

Tab

le1.

Con

tinue

d

Ž.

Aut

hor

year

Tas

kIn

cent

ives

Eff

ect

ofhi

gher

ince

ntiv

es

INC

EN

TIV

EE

FF

EC

TS

AR

EC

ON

FO

UN

DE

DW

ITH

EF

FE

CT

SO

FO

TH

ER

TR

EA

TM

EN

TS

Ž.

Ž.

Ž.

Bah

rick

1954

Lea

rnin

gna

mes

ofge

omet

ric

form

s;pe

riph

eral

0vs

.Lm

ax$8

.55

Fas

ter

lear

ning

offo

rms

16.9

tria

lsvs

.19.

6;w

orse

lear

ning

ofŽ

Ž.

lear

ning

ofco

lors

isw

orse

ince

ntiv

epa

idfo

rco

lors

6.1

vs.7

.6.

form

lear

ning

only

;0su

bjec

tsto

ldno

tto

try

hard

Ž.

Ž.

Bau

mei

ster

1984

Phy

sica

lgam

eof

hand

-eye

coor

dina

tion

:mov

ing

0vs

.W

orse

scor

esin

firs

ttr

ial

33.6

vs.2

8.3

,sam

esc

ores

inse

cond

Ž.

Ž.

two

rods

soa

ball

rolls

betw

een

them

,the

nL

$1.4

9rtr

ial

tria

l34

.1vs

.33.

2;n

ova

rian

ces

repo

rted

.Ž

drop

ping

the

ball

into

asl

otco

nfou

ndbe

twee

n.

ince

ntiv

ean

dst

ated

perf

orm

ance

goal

ŽŽ

.E

ger

&D

ickh

aut

Pos

teri

orpr

obab

ility

judg

men

t;se

arch

ing

for

0vs

.L$6

4.66

,R

educ

edju

dgm

ent

erro

rco

nser

vati

sm,m

easu

red

bysl

ope

ofŽ

.Ž

.19

82ev

iden

ceof

‘‘con

serv

atis

m’’

inB

ayes

ian

upda

ting

$40.

41,$

24.2

5fo

rlo

god

dsag

ains

tlo

gB

ayes

ian

odds

.63

vs.1

.04

;les

ser

ror

inŽ c

onfo

und

betw

een

ince

ntiv

ean

del

icit

atio

nto

p3

S’s

inea

chac

coun

ting

vs.a

bstr

act

cont

ext

.te

chni

que;

no-i

ncen

tive

S’s

give

odds

,inc

enti

vegr

oup

of9]

10.

S’s

pick

‘‘pay

offs

tabl

es’’

whi

chE

bets

agai

nst

Fou

rake

r&

Sieg

elB

uyer

-sel

ler

barg

aini

ngov

erpr

ice

and

quan

tity

Lvs

.HN

odi

ffer

ence

inm

ean

pric

esor

quan

titi

es;v

aria

nce

1]4

tim

esŽ

.Ž

1963

exps

3]5

conf

ound

betw

een

ince

ntiv

ean

dex

peri

ence

:sm

alle

r.

Htr

ialw

as21

stof

21tr

ials

Ž.

ŽK

roll

etal

.19

88In

vest

ing

inri

sky

asse

tsco

nfou

ndbe

twee

nL

vs.H

Mor

eri

sk-a

vers

e,cl

oser

toop

tim

alpo

rtfo

lio,w

ork

hard

er.

high

erin

cent

ive

and

risk

-ave

rsio

nŽ

ŽŽ

.P

hilli

ps&

Edw

ards

Pos

teri

orpr

obab

ility

judg

men

tco

nfou

nd0

vs.L

$.44

Low

erB

ayes

ian

erro

rs30

%lo

wer

;low

ercr

oss-

Sva

rian

ceŽ

..

Ž.

1966

betw

een

ince

ntiv

ean

dus

eof

two

prop

eran

dm

axr

tria

l.0

05vs

..01

2.

one

impr

oper

scor

ing

rule

sŽ

Ž.

Slov

ic&

Mul

ticu

epr

edic

tion

wit

hm

issi

ngva

lues

e.g.

,0

vs.L

max

$12.

18N

odi

ffer

ence

infr

acti

onof

S’s

wei

ghti

ngco

mm

onte

stm

ore

Ž.

Mac

Phi

llarn

yad

mit

ting

stud

ents

who

each

have

two

test

scor

es,

heav

ily70

%,7

7%Ž

..Ž

1974

wit

hon

lyon

ete

stin

com

mon

conf

ound

betw

een

ince

ntiv

ean

dtr

ial-

by-t

rial

feed

back

,.

mis

sing

cue

dist

ribu

tion

info

rmat

ion

ŽŽ

.W

righ

t&

Judg

men

tsof

prob

abili

tydi

stri

buti

onof

GM

AT

,0

vs.L

$157

.48

Low

erm

ean

squa

red

erro

r.0

07vs

..00

4;l

ower

cros

s-S

ŽŽ

.A

boul

l-E

zzag

e,an

dsa

lary

ofM

BA

stud

ents

conf

ound

tota

lfor

10be

stva

rian

ceha

lfin

LŽ

..

1988

betw

een

ince

ntiv

ean

dus

ean

dex

plan

atio

nof

S’s,

ns

51.

scor

ing

rule

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 19

treatments. The table reports the authors, task, and incentive level in each study.The rightmost column summarizes the effects of the incentive levels given in thethird column. The table was constructed by the first author and every entry waschecked by a research assistant.

Ž .An example will show how to read the table. In the Awasthi and Pratt 1990study there were two performance-based incentive levels, denoted 0 and L. Zeromeans choices were hypothetical so there was no performance-based incentiveŽ .usually subjects were paid a few dollars for participating . L means the stakes were

Ž .low they were paid $2.42 for answering each judgment problem correctly ; Hdenotes higher stakes. For comparability, all payments were inflated to 1997 dollarsusing the GDP deflator.

Note that L and H denote lower and higher levels within a study, not absolutelevels. The absolute levels are generally reported as well. This reporting conventiondoes make it difficult to compare across studies, since the L level in one study may,in absolute terms, be higher than the H level in another study. However, thisconvention does make it possible to tell whether, in general, raising stakes from L

Ž .to H improves performance regardless of what those levels are .The table reports that the fraction of subjects making errors was 46% in the 0

condition and 41% in the L condition, so higher incentives reduced error slightly.The fourth column also notes that L subjects took more time to complete the taskŽ .5.7 minutes instead of 4.2 , and the reduction in error caused by higher incentive,from 44% to 21%, was greatest for subjects who were high in ‘‘perceptual

Ž .differentiation’’ measured by a psychological test .Rather than reviewing each study, we will describe some regularities in the

several categories of results, which are summarized in Table 2.

When incenti es help

There are many studies in which higher incentives do improve mean performance.Table 2 suggests that incentives appear to help most frequently in judgment and

Ž .decision tasks they also sometimes hinder performance in this class of tasks . Theyimprove recall of remembered items, reduce the effect of anchoring bias onjudgment, improve some kinds of judgments or predictions, improve the ability tosolve easy problems, and also sharpen incentives to make zero-profit trades inauctions or do piece-rate clerical work.

Ž .An example is Libby and Lipe 1992 , who studied recall and recognition of 28Žinternal firm controls which accountants might look for when auditing a firm e.g.,

.‘‘spoiled checks are mutilated and kept on file’’ . Subjects then had to recall asŽ .many of the controls as they could in the ‘‘recall’’ task or recognize controls seen

Žearlier, on a new list which included some spurious controls in the ‘‘recognition’’. Ž . Ž .task . Some subjects were paid a flat fee $2 for participating the 0 condition and

Ž .others earned 10 11.6 cents in 1997 cents for each item correctly recalled orrecognized, along with a $5 bonus for each of the top five subjects. Incentives

CAMERER AND HOGARTH20

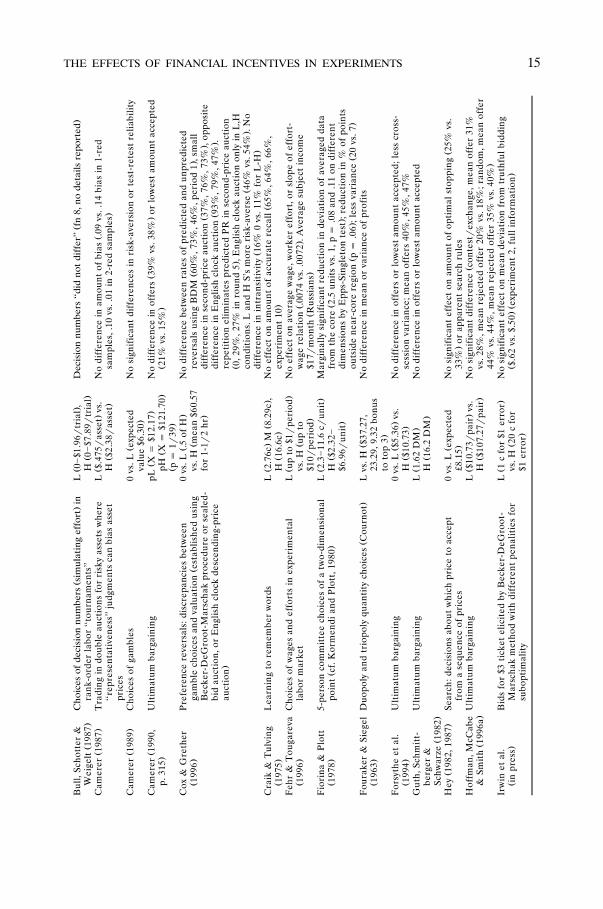

Table 2. The number of studies exhibiting various incentive effects

Has an effect, but noType of task Helps Has no effect Hurts performance standard

Judgments and decisionsProbability judgment 3 2

ŽBinary choice including 2 1.‘‘three door’’ problem

Multivariate prediction 2 4Problem solving 2 2Item recognitionrrecall 3 3 1

ŽClerical drawing, data 3.transfer, assembly

Games and marketsDominance-solvable games 1Tournaments 1 1Signaling games 1Sequential bargaining 2

ŽUltimatum games 6 1 fewer rejections offixed-% offers at

.higher stakesŽTrust games labor markets, 2.centipede

Auctions: double 3 1ŽAuctions: private value 1 1 Vickrey for gifts,

.higher valuationsAuctions: common value 1Spatial voting 1Duopoly, triopoly 1

Individual choicesDictator tasks 2 more self-interestedRisky choices 3 8 more risk-averse, 2

more risk-seekingNon-EU choice patterns 1 1Preference reversals 2 1Consumer purchases 1 fewer actual

purchasesŽ .Search wages 1

Ž .caused subjects to work harder about 3 minutes longer . Incentives also causedŽ .subjects to recall more items correctly 12.0 vs. 9.8 but did not improve recognition

Ž .much 16.3 vs. 15.8 . Libby and Lipe suggest that incentives do induce more effort,but effort helps a lot in recalling memories, and only helps a little in recognizing anitem seen previously. Their study is a glimpse of how incentive effects can dependdramatically on the kind of task a person performs.

Ž .Kahneman and Peavler’s 1969 study is notable because it measures a physicalmanifestation of the effort induced by higher incentives}pupil dilation. Their

Ž .subjects learned a series of eight digit-noun pairs from an audiotape e.g., ‘‘3-frogs’’ .

THE EFFECTS OF FINANCIAL INCENTIVES IN EXPERIMENTS 21

Ž .Then subjects were told a digit e.g., 3 and asked to say which noun had beenpaired with that digit. For some digits, subjects had a low incentive to guess the