Embed Size (px)

Citation preview

P a g e | 1

NKALU, Chigozie Nelson PG/MSc/14/69634

THE EFFECTS OF BUDGET DEFICITS ON SELECTED MACROECONOMIC VARIABLES IN

NIGERIA AND GHANA

DEPARTMENT OF ECONOMICS

FACULTY OF THE SOCIAL SCIENCES

Ebere Omeje Digitally Signed by: Content manager’s Name DN : CN = Webmaster’s name O= University of Nigeria, Nsukka OU = Innovation Centre

P a g e | 2

THE EFFECTS OF BUDGET DEFICITS ON SELECTED MACROECONOMIC

VARIABLES IN NIGERIA AND GHANA

By

NKALU, Chigozie Nelson

PG/MSc/14/69634

DEPARTMENT OF ECONOMICS

FACULTY OF THE SOCIAL SCIENCES

UNIVERSITY OF NIGERIA, NSUKKA

SEPTEMBER, 2015

P a g e | 3

THE EFFECTS OF BUDGET DEFICITS ON SELECTED MACROECONOMIC

VARIABLES IN NIGERIA AND GHANA

AnMSc. Thesis

By

NKALU, Chigozie Nelson

PG/MSc/14/69634

DEPARTMENT OF ECONOMICS

FACULTY OF THE SOCIAL SCIENCES

UNIVERSITY OF NIGERIA, NSUKKA

SUPERVISOR: PROF. C. C. AGU

SEPTEMBER, 2015

P a g e | 4

TITLE PAGE

The Effects of Budget Deficits on Selected Macroeconomic Variables in

Nigeria and Ghana

P a g e | 5

CERTIFICATION

This is to certify that NKALU, Chigozie Nelson, a post-graduate student of the Department

of Economics, University of Nigeria, Nsukka with Registration Number: PG/MSc/14/69634

has satisfactorily completed the requirements for the award of Master of Science (MSc.) in

Economics

____________________________ ____________________

Nkalu, Chigozie Nelson Date

PG/MSc/14/69634

(The Researcher)

________________ ___________________

Prof. C. C. Agu Date

(Supervisor)

________________ ___________________

Prof. S. I. Madueme Date

(Head of Department)

P a g e | 6

APPROVAL PAGE

This research work titled: “The Effects of Budget Deficits on Selected Macroeconomic

Variables in Nigeria and Ghana” has followed due process and has been approved to have

met the minimum requirement for the award of the Master of Science degree in the

Department of Economics, Faculty of the Social Sciences, University of Nigeria, Nsukka.

________________ ___________________

Prof. C. C. Agu Date

(Supervisor)

________________ ___________________

Prof. S. I. Madueme Date

(Head of Department, Economics)

________________ ____________________

Prof. A. I. Madu Date

(Dean, Faculty of the Social Sciences)

________________ ____________________

Date

(External Examiner)

P a g e | 7

DEDICATION

To:

My beloved mother

P a g e | 8

ACKNOWLEDGMENT

This study would not have been a huge success without the inputs of some men of goodwill.

Let me first and foremost express my deep gratitude to my family for whom I derive

unquenchable zeal to surmount some constraints in the course of this study. Special thanks to

my mother, brothers and sisters for the much love and encouragements which indeed has

reshaped my entire being. My most and sincere thanksgiving goes to the Almighty God for

His infinite mercies throughout my existence.

I must as a matter of fact recognize my able and capable supervisor and academic adviser –

Prof. C. C. Agu for his ever and relentless guidance and mentorship. My heartfelt gratitude

goes to my brothers, lecturers and senior colleagues in the Department of Economics,

University of Nigeria, Nsukka for their immeasurable contributions towards making this

study a colossal success. Special thanks to Dr. Jude O. Chukwu, Dr. Richard K. Edeme, Dr,

Emmanuel Nwosu, Dr. Ezebuilo R. Ukwueze, Dr. I. Ifelunini, Dr. (Mrs) Gladys Aneke, Prof.

(Mrs) S. I. Madueme, Miss Anaduaka Uchechi S., Emecheta Chisom, Nnetu Vivian, Mr.

Ekene and Mr. Nchege Johnson. Regrettably enough, others whose names cannot contain on

this page due to time and space constraints should bear with me.

Thank you all, and may our good Lord shower you with abundant blessings - Amen!

P a g e | 9

TABLE OF CONTENTS

Title Page - - - - - - - - - - i Certification - - - - - - - - - - ii Approval Page - - - - - - - - - iii Dedication - - - - - - - - - - iv Acknowledgement - - - - - - - - - v Table of Contents - - - - - - - - - vi List of Figures - - - - - - - - - ix List of Tables - - - - - - - - - - x Abstract - - - - - - - - - - xi CHAPTER ONE: INTRODUCTION

1.1 Background of the Study - - - - - - - 1

1.2 Statement of the Problem - - - - - - - 4

1.3 Research Questions - - - - - - - 7

1.4 Objectives of the Study - - - - - - - 8

1.5 Hypotheses of the Study - - - - - - - 8

1.6 Policy Relevance of the Study- - - - - - - 8

1.7 Scope of the study - - - - - - - 9

1.8 Conceptual Framework - - - - - - - 9

1.9 Structure of the Study - - - - - - - 13

CHAPTER TWO: REVIEW OF RELATED LITERATURE

2.1 Review of Theoretical Literature - - - - - - 14

2.1.1 Budget Deficits, Crowding In and Crowding Out Effects Schools of Thought- 14

2.2 Thematic Issues - - - - - - - - 17

2.2.1 Budget Deficits in Ghana: An Overview - - - - - 17

2.2.2 Determinants of Budget Deficit Growth in Ghana - - - - 18

2.2.3 Fiscal Policy in Ghana - - - - - - - 19

2.2.4 Interest Rate Policy in Ghana - - - - - - - 20

2.2.5 Fiscal Policy in Nigeria - - - - - - - 20

2.2.6 Macroeconomic Environments & Analytical Comparison between Nigeria & Ghana-

22

2.3 Empirical Literature - - - - - - - - 24

2.3.1 International Evidence - - - - - - - 25

2.3.2 Nigerian–Ghanaian Evidence - - - - - - - 31

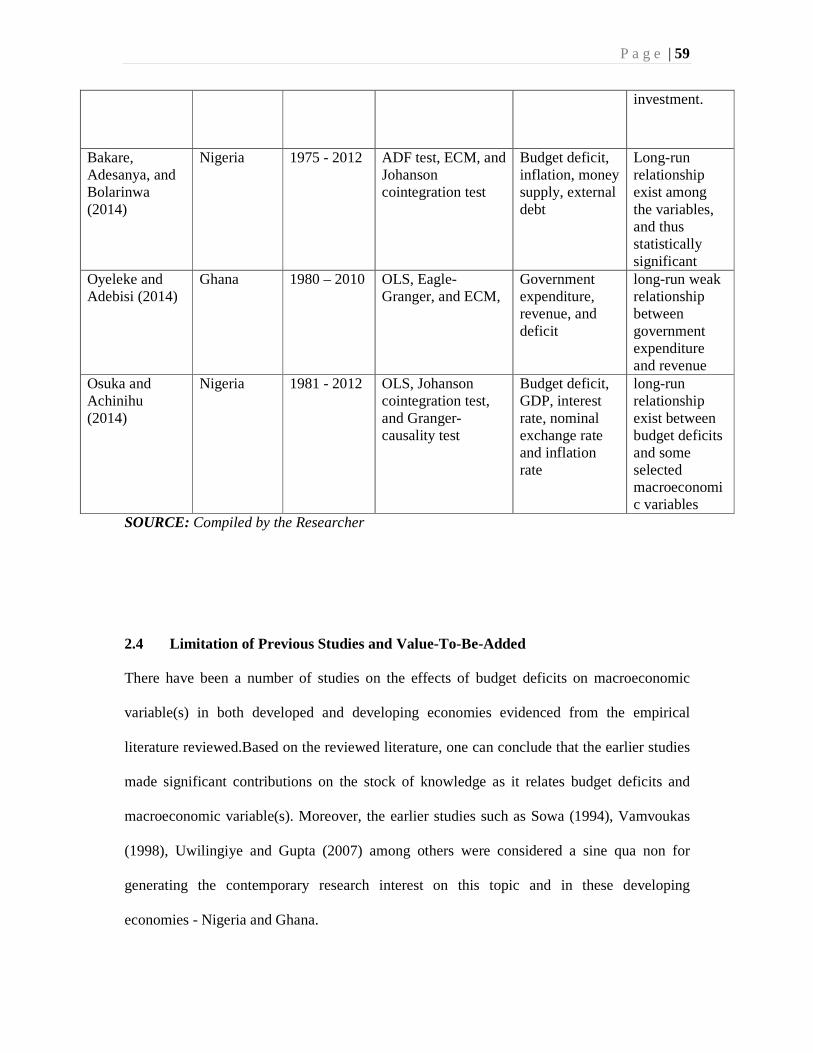

2.4 Limitation of Previous Studies and Value-To-Be-Added - - - 46

P a g e | 10

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Theoretical Framework- - - - - - - - 48

3.2 Model Specification - - - - - - - - 51

3.3 Estimation Procedure - - - - - - - - 53

3.3.1 Empirical Models: Seemingly Unrelated Regression (SUR) - - - 53

3.3.1.1 Two Stage Least Squares and Instrumental Variables - - - 54

3.3.2 Lag/Length/Bandwidth Selection - - - - - 55

3.3.3 Stationarity/Unit Rood Test - - - - - - - 55

3.3.4 Cointegration Test - - - - - - - - 56

3.4 Model Justification - - - - - - - - 57

3.5 Data Sources - - - - - - - - - 58

3.6 Econometric Software for Analyses - - - - - - 58

CHAPTER FOUR: DATA ANALYSES AND EMPIRICAL RESULTS

4.1 Presentation of Results - - - - - - - 59

4.1.1 Presentation of Nigerian Data - - - - - - 59

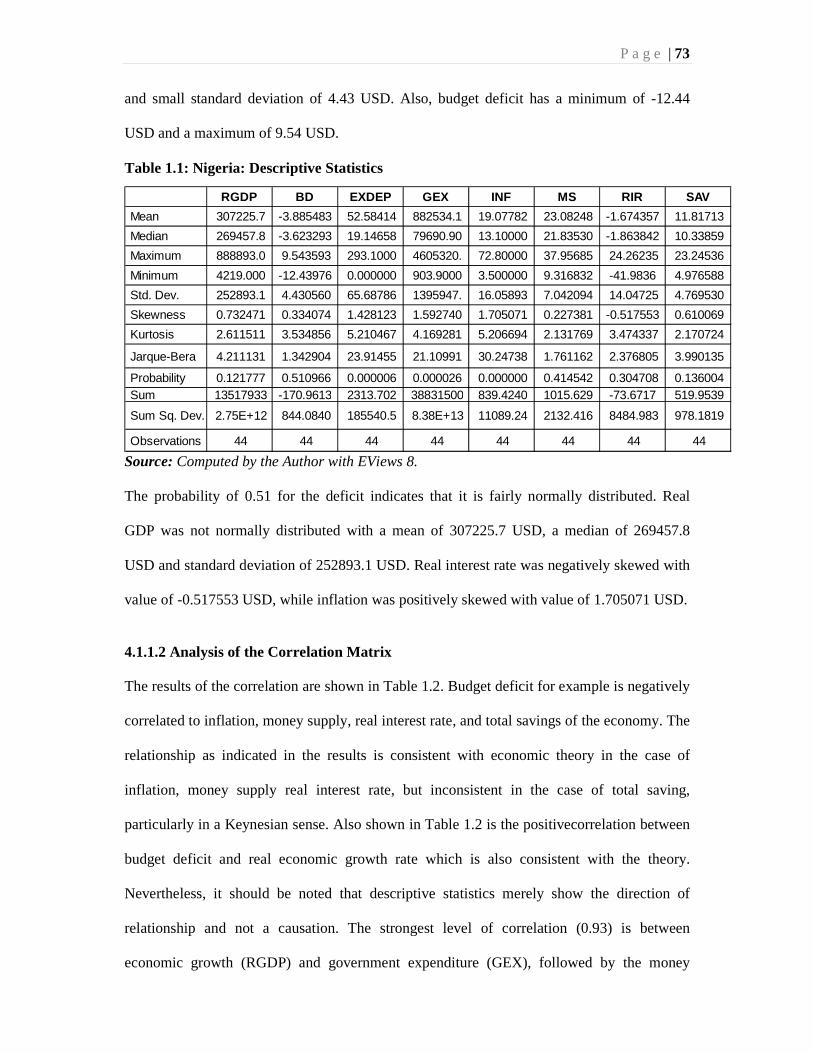

4.1.1.1 Descriptive Statistics for all Variables - - - - - 59

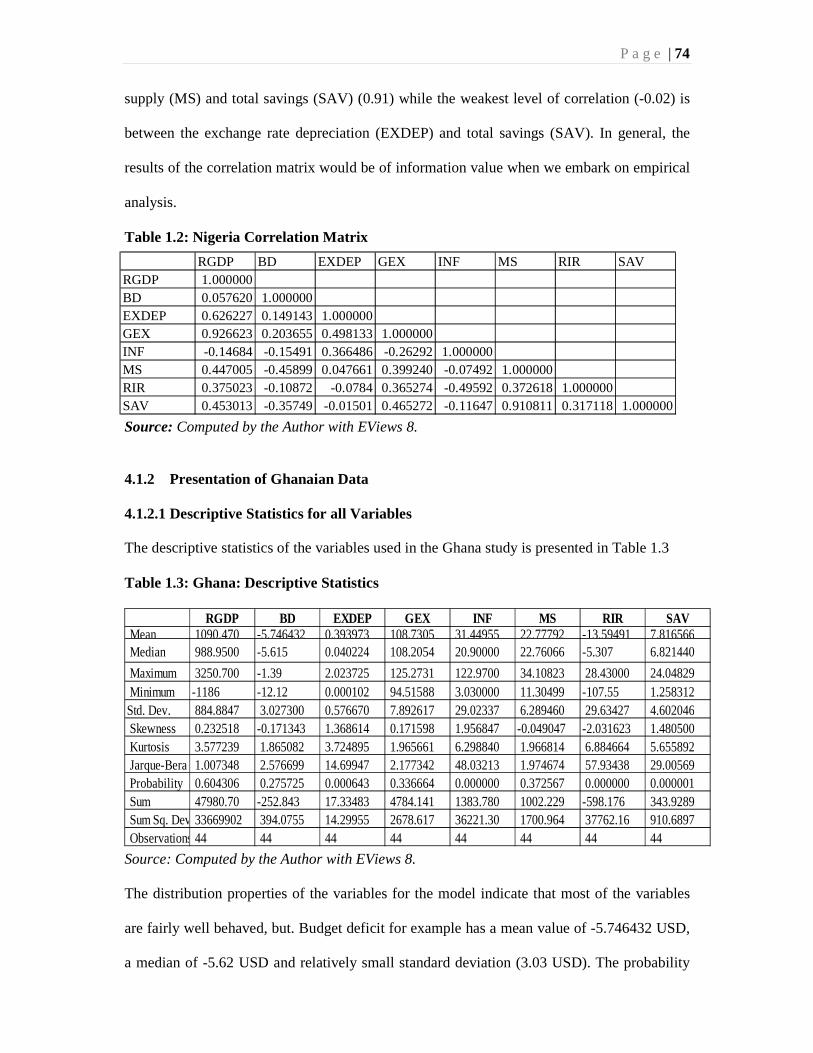

4.1.1.2 Analysis of the Correlation Matrix - - - - - - 60

4.1.2 Presentation of Ghanaian Data - - - - - - 61

4.1.2.1 Descriptive Statistics for all Variables - - - - - 61

4.1.2.2 Analysis of the Correlation Matrix - - - - - - 62

4.2 Stationary (Unit Root) Tests Results - - - - - - 62

4.2.1 Lag Length/Bandwidth Selections - - - - - - 64

4.3 Cointegration Tests - - - - - - - - 64

4.4 Analysis of the SUR Models and Two-Stage Least Squares Estimation Results 65

4.4.1 Analysis of the SUR Estimation based on Economic Criteria - - 69

4.4.2 Analysis of the SUR Results based on Statistical Criteria - - - 70

4.4.3 Analysis of the SUR Estimation based on Econometric Criteria - - 70

4.4.3.1 Autocorrelation - - - - - - - - 70

4.4.3.2 Other Diagnostic Tests - - - - - - - 72

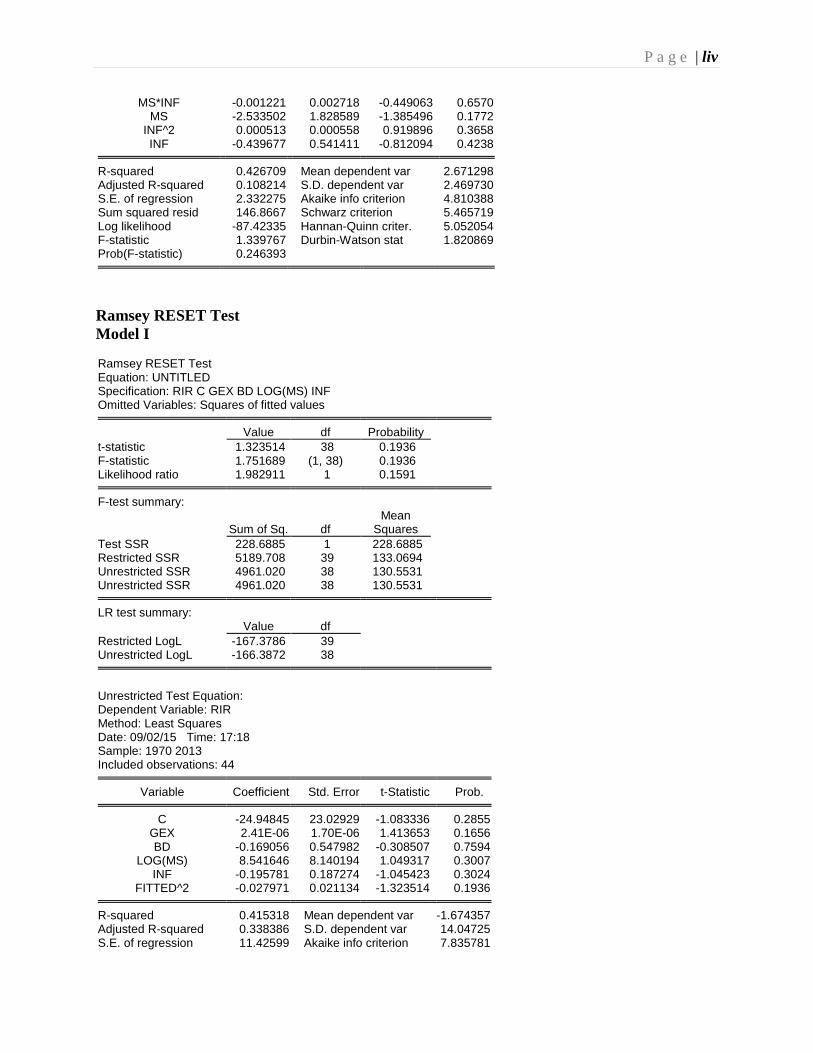

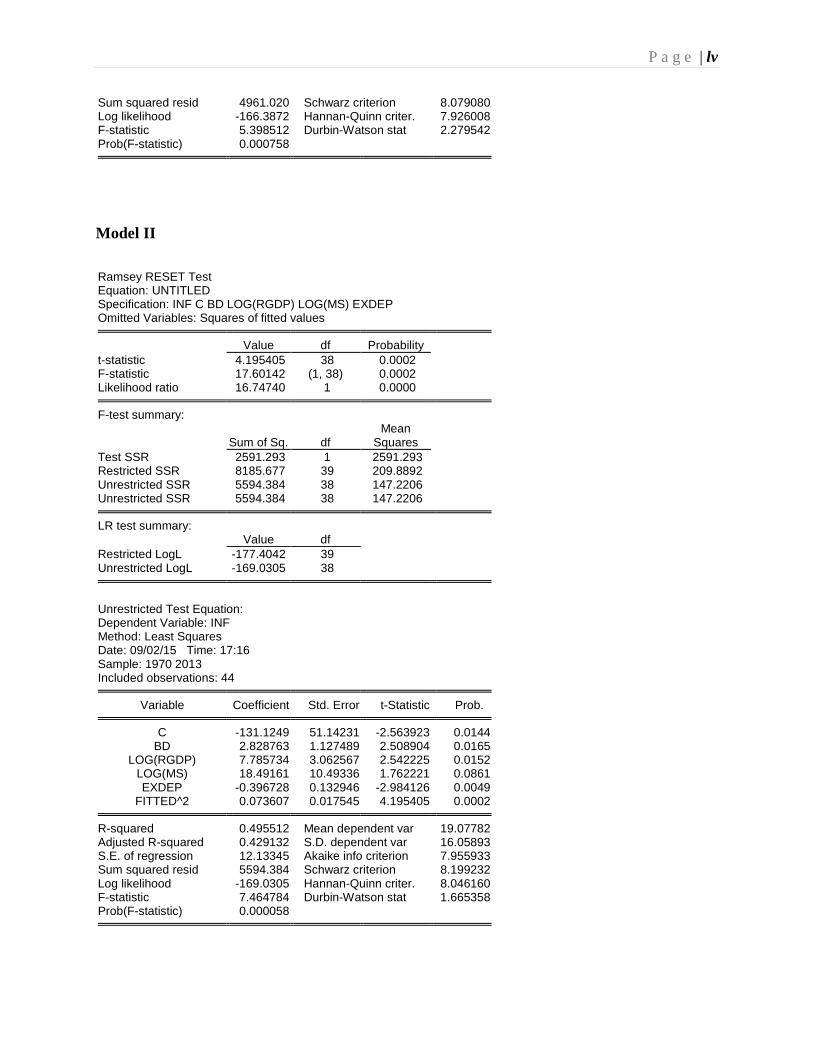

4.4.3.3 Functional Form Specification (Ramsey Reset) Test - - - - 72

4.5 Evaluation of Hypotheses - - - - - - - 71

CHAPTER FIVE: SUMMARY, CONCLUSION AND POLICY IMPLIC ATIONS

5.1 Summary of Findings - - - - - - - - 76

5.2 Policy Implications of Findings - - - - - - 76

P a g e | 11

5.3 Policy Recommendations - - - - - - - 77

5.4 Conclusion - - - - - - - - - 79

REFERENCES - - - - - - - - - 80

APPENDIX - - - - - - - - - - 90

LIST OF FIGURES

Figure 1.1 Graph showing Inflation and Budget Deficit interactions in Nigeria (1970 -2013) -

5

Figure 1.2 Graph showing, Inflation, and Budget Deficit interactions in Ghana (1970 -2013) -

6

P a g e | 12

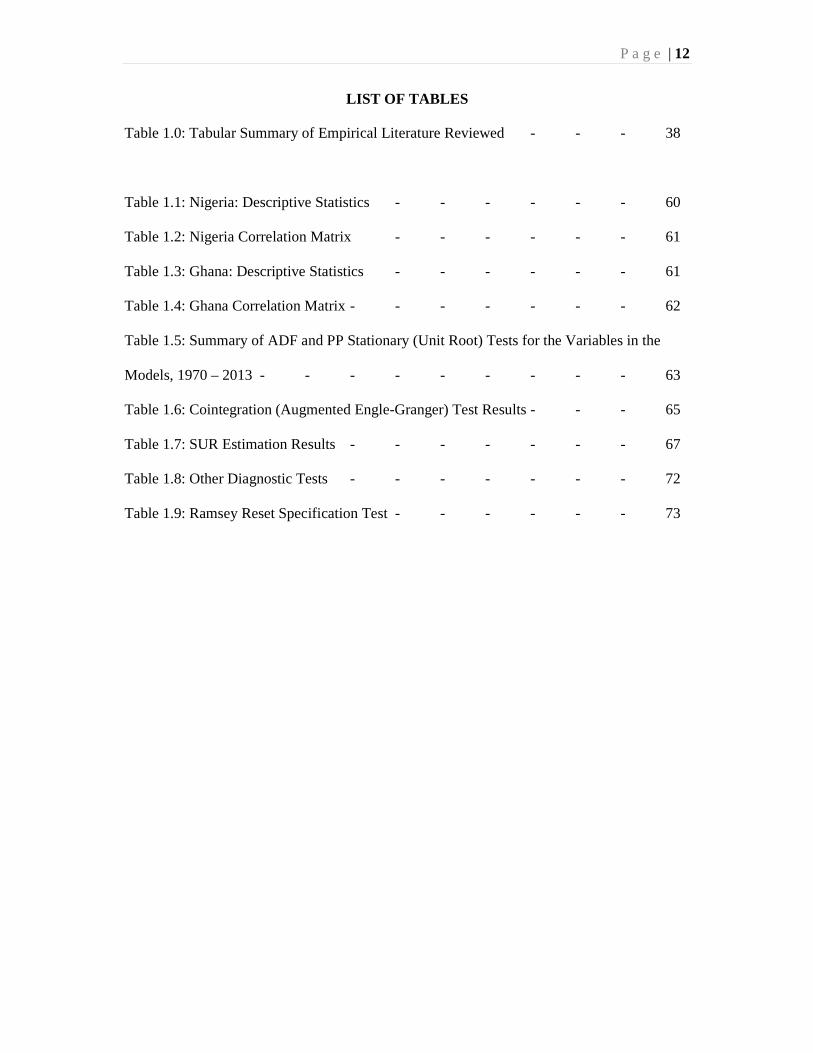

LIST OF TABLES

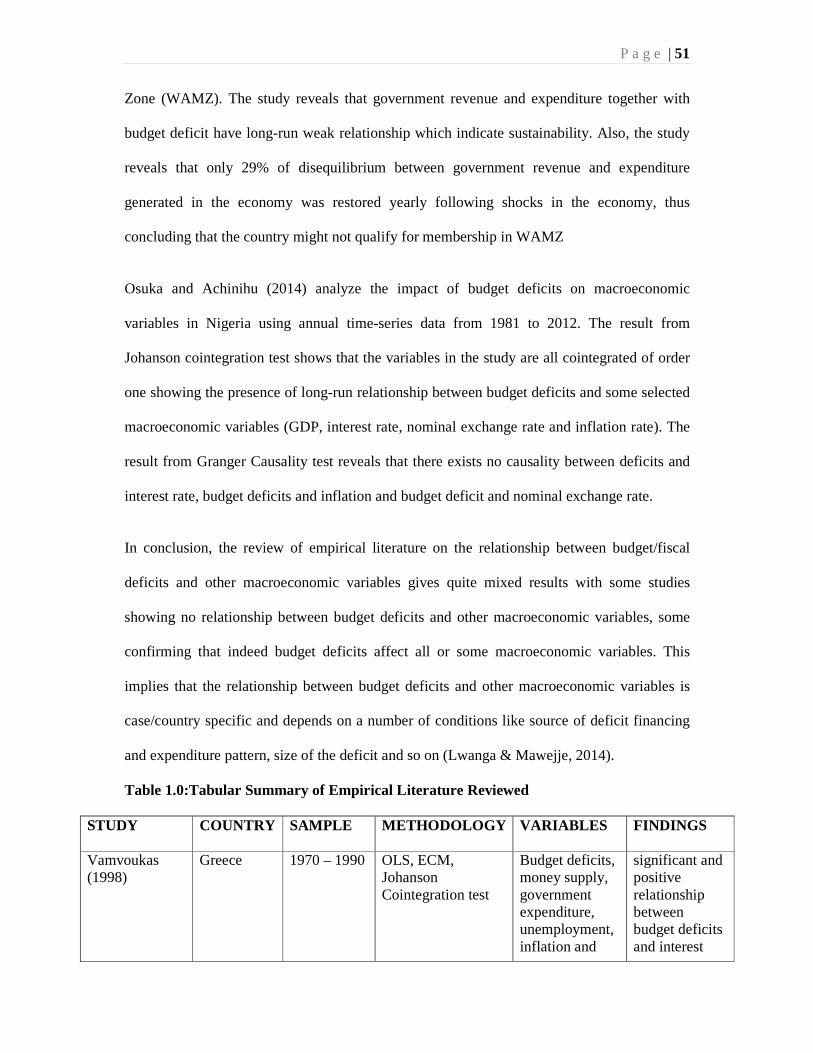

Table 1.0: Tabular Summary of Empirical Literature Reviewed - - - 38

Table 1.1: Nigeria: Descriptive Statistics - - - - - - 60

Table 1.2: Nigeria Correlation Matrix - - - - - - 61

Table 1.3: Ghana: Descriptive Statistics - - - - - - 61

Table 1.4: Ghana Correlation Matrix - - - - - - - 62

Table 1.5: Summary of ADF and PP Stationary (Unit Root) Tests for the Variables in the

Models, 1970 – 2013 - - - - - - - - - 63

Table 1.6: Cointegration (Augmented Engle-Granger) Test Results - - - 65

Table 1.7: SUR Estimation Results - - - - - - - 67

Table 1.8: Other Diagnostic Tests - - - - - - - 72

Table 1.9: Ramsey Reset Specification Test - - - - - - 73

P a g e | 13

ABSTRACT

This study investigates the effects of budget deficits on selected macroeconomic variables in Nigeria and Ghana using annual time-series data of both economies covering from 1970 to 2013; and taking previous empirical studies as its point of departure. The specific objectives of the study include: to examine the effects of budget deficits on interest rates, inflation, and economic growth in Nigeria and Ghana within the methodological framework of Seemingly Unrelated Regression (SUR) model and Two-Stage Least Squares (2SLS). The study employs Eagle-Granger Cointegration test, Augmented Dickey Fuller (ADF) and Phillips-Perron (PP) tests in estimating the systems equations. Data sourced from World Bank, IMF - World Economic Outlook, Central Bank of Nigeria, Bank of Ghana and others, were analyzed using SUR model with several diagnostic and specification tests to examine the objectives of the study. From the perspective of this study, the empirical findings demonstrated that budget deficit has statistically negative effects on interest rate, inflation, and economic growth for both economies thereby supporting the neoclassical argument in the literature that budget deficit slows growth of the economy through resources crowding-out. Based on the empirical findings, many recommendations were made for both Nigeria and Ghana economies one of which stated that the government of Nigeria and Ghana should be mindful of the sources of financing the budget deficits so as to effectively manage the economic fluctuations and increase activities in the real sector. Also, it was recommended that both economies should pursue policies that will boost production of goods for both domestic consumption and exports in the long run through a combination of import substitution and export promotion strategies.

P a g e | 14

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Budget deficit and its effects on macroeconomic variables is one of the most discussed issues

amongst economists and policy makers in both developed and developing countries (Saleh,

2003; Aisen & Hauner, 2008; Georgantopoulos & Tsamis, 2011). Intuitively, it is a

commonplace to construe that huge budget deficits have adverse macroeconomic effects such

as high interest rates, current account deficits, inflation, exchange rates volatility, with

implications on growth and development (Bernheim, 1989).

The budget deficit effects could either be negative, positive or a no positive or negative

relationship on macroeconomic variables. Budget deficit and its effects on any given

economy could be attributable to different methodologies countries employed and the nature

of data used by different researchers as most of the studies regress the macroeconomic

variable(s) on the fiscal deficit or the deficit on the macroeconomic variable(s)(Anyanwu,

1997).

Budget deficit refers to government expenditure exceeding government revenue over a period

of time (Anyanwu, 1997). When a deficit occurs in a country, it becomesimperative to find

remedy for financing such deficits so as to eradicate its negative implications. Nigeria and

Ghana as a developing economies have blamed prolonged economic crisis as one of the

major causes of budget deficit(s) in both economies as it has resulted in over indebtedness

and debt crisis, high inflation, poor investment performance and growth (Ezeabasili,

Mojekwu & Herbert, 2012). In Nigeria, public expenditure has led to increase in the fiscal

imbalances that siphon funds from the private sector investment, retarding growth and

reducing standard of living (Mpia & Ogrike, 2014). Fiscal imbalances create potential large

P a g e | 15

burden on future generations as workers may be forced to finance unfunded social

programmes. Budget deficits, therefore, lead to incurring debts which is a stock of liabilities

of the government (Udu & Agu, 2000). Budget deficit is generally associated with recession

because of the effect on revenues and expenditures (Dernberg, 1985).

The Ghanaian economy embarked recently, on the second leg of its centenary of

independence and democracy, announcing bold objectives that included an accelerated gross

domestic product (GDP) growth rate of 8% in 2009 and 10% before 2015 and achievement of

middle-income status of US$1000 dollars per capita by 2015 (Ackah, Aryeetey & Aryeetey,

2009). In the five decades since her independence from British rule in 1957, Ghana has gone

through different cycles of growth, marked by poor economic performance and military coup

d’états through to the 1980s. National economic policies during this period were often devoid

of market principles, and characterized by frequent price and income controls. At best, the

economy muddled through, with low productivity, high and volatile prices, an overvalued

currency and high interest rates (Ndulu & Connell, 2008).

The choice of this study which brought the economies of Nigeria and Ghana into focal point

for empirical investigation is formed by a number of reasons. Besides the obvious reason that

both economies share similarities in political and economic structures, the economies have

experienced very large fluctuations in the government budget deficits and high accumulation

of foreign debt, poor export performance, huge service account deficits, external debt

amortization, low inflow of foreign direct investment, misappropriation of external funding

support, excessive domestic monetary and credit expansion; price distortions and a

deterioration in the terms of trade (Ogiogio, 1996; & Obioma,1998).

In Nigeria, available data from the CBN (2012) statistical bulletin, show that deficit of -

8.62% of GDP was recorded in 1970 which rose to a surplus of 2.58% of GDP in 1971 and

P a g e | 16

declined to -0.82% of GDP in 1972. In 1974, Nigeria experienced a remarkable improvement

in the overall fiscal balances from 1970 to 2013 as surplus rose from 1.92% of GDP in 1973

to a surplus unit of about 9.54% of GDP. The Nigeria overall fiscal balance deteriorated

between 1980 and 1994 and recorded greater deficit of about -12.44% of GDP in 1982 on the

average. However, between 1995 and 2013, the Nigerian economy recorded a surplus of

about 1.19% of GDP on the average in 1996 with other years experiencing different deficit

percentages to GDP.

In Ghana, there has been huge and continuous deterioration in government fiscal position.

The economy has been in a persistent tendency towards budget deficit since independence as

a result of over expanding government expenditure, inadequate revenue generation capacity

of government and increasing debt levels (Pomeyie, 2001). The available statistics from

World Bank (2014) show that the Ghanaian economy has not recorded any surplus since their

independence and between 1970 and 2013.It is evidenced that the trends of the overall fiscal

balances of Ghanaian economy between 1970 and 2012 has been on the deficit side with a

huge deficit records of about -10.79% of GDP and -12.12% of GDP in 1982 and 2012

respectively. Apart from the period between 1981 and 1990 when there was remarkable fiscal

discipline, the government budget was consistently in deficit in the 1990s. On average, the

deficits was more than 5% of GDP in 1993.

As the economy of Ghana grows, policy makers have been concerned with the extent to

which the budget deficit is sustainable, and its effects on macroeconomic variables. However,

a deficit policy plays a vital role in assisting countries to achieve macroeconomic stability,

poverty reduction, income redistribution and sustainable growth. For this reason, most

governments use the budget as effective tool in achieving their economic objectives. This

means that large and accumulating budget deficit may not necessarily be a bad policy

objective if such deficits are effectively utilized to enhance economic growth. It is in line

P a g e | 17

with this that an appropriate operational definition and measure of budget deficit must be

clearly stated. Otherwise, the occurrence of large nominal budget deficit may be misleading

depending on the operational measure adopted by a particular country (Antwi, & Mills,

2013).

In Nigeria, the economy was caught in the deficit trap since early 1980s when the world oil

market collapsed, and since then, there have been frantic efforts to exit the trap but all to no

avail(Wosowei, 2013). Nevertheless, the fiscal policy adoption of Nigeria and Ghana in

financing deficits are attributable to major factors causing rapid monetary growth, exchange

rate depreciation and rising inflation. Thus the motivation for this study is to examine the

short and long run effect of budget deficit on interest rate, inflation and economic growth in

Nigeria and Ghana.

1.2 Statement of the Problem

Different schools of thought have demonstrated their opinions on budget deficits. Most

common are the Keynesian and the Ricardian Schools of Thought. While the Keynesian

posits that budget deficit affects mainly macroeconomic variables, Ricardian School refutes

the proposition (by the Keynesian school) and posits that budget deficits do not affect mainly

macroeconomic variables. However, budget deficit in developing economy like Nigeria and

Ghana plays a pivotal role in achieving economic and social objectives including

macroeconomic stability, sustainable growth and poverty reduction.

In recent times, the deficit positions of the Ghanaian budgets have worsened, drawing

attention to its long term sustainability (Bank of Ghana, 2005). As the two countries (Ghana

and Nigeria) consistently operate budget deficits, this lead to accumulation of government

debts. As past deficit adds up to current borrowings, it creates higher interest payments,

raising inflation with high volatility in real interest rate, depreciates exchange rate and retards

P a g e | 18

growth. This calls for further borrowing to cover the interest payment and the increasing

primary deficit which affects the rate of future borrowing.

Figure 1.1 Graph showing Inflation and Budget Deficit interactions in Nigeria (1970 -

2013)

Source: Researcher’s computation using data from CBN Bulletin of various years As seen in figure 1.1 above, the greater percentage of the overall budget balance in Nigeria

were on the deficit side with high inflation rate and unstable real interest rate. In 1990s the

average inflation rate soared to 72.8%. But, by 2007, the economy experienced a sharp

average fall of 6.57% in the inflationary trend.The interactions of real interest rate and budget

deficits in the figure 1.3 clearly distinguish between inflation and real interest rate.

In Ghana, the stock of government debt to GDP has been rising steadily from 17.2% in 2006

to 24.9% in 2007 and to 28.1% in 2008 (Bank of Ghana, 2007). Clearly, Ghana cannot use

new borrowing indefinitely to finance interest payments since changes in taxes and

government spending is followed by adjustment in future taxation and spending (Luporini,

1999).

-20.00

0.00

20.00

40.00

60.00

80.00

% of GDP

Year

Budget Deficit (% of GDP), and Inflation in Nigeria

BD(% of GDP) INFL

P a g e | 19

Figure 1.2 Graph showing, Inflation, and Budget Deficit interactions in Ghana (1970 -

2013)

Source: Researcher’s computation using data from World Bank, WEO Database, (2014)

In figure 1.2 above, Ghana recorded a deficit of -7.05% of GDP on the average in 1981 with

inflation soaring to about 117.8%. In 1982, budget deficit worsen on the average of -10.79%

of GDP with low inflation of about 21.3%. This shows that even if Ghana meets its interest

payment on debt by borrowing more, it must roll over its debt indefinitely because tax

revenue is not enough to pay for other expenditure. This has led to growing debt and

increasing tax rate.

Generally, in the case of Nigeria and Ghana, it has been claimed thatthe main causes of these

high rates of inflation were the widening fiscal imbalances, sources of deficit financing,

economic growth and the depreciation of the exchange rate. Nonetheless, the transition to

high inflation rates over the period resulted in substantial real cost and large losses in income,

at the same time as the performance of the economy as a whole declined as a result of

widening fiscal deficits and exacerbated by poor macroeconomic management and political

uncertainty(Arestis & Sawyer, 2006).

P a g e | 20

Nevertheless, empirical studies on the effects of budget deficit on macroeconomic variables

such as interest rate, inflation and growth seem not to lay credence on Keynesian proposition

or Ricardian Equivalence Hypothesis (REH). The major trust of this study is to examine the

short and long-run effect of budget deficits on interest rate, inflation and economic growth in

Nigerian and Ghana. This is necessitated by the fact that the previous empirical studies in this

area have no conclusive evidence in support of Keynesian-Ricardian paradigms in Nigeria

and Ghana. This is because, none of the previous studies conducted on the effects of budget

deficits in both economies used all the relevant variables and a few do not employ the

appropriate methodology. This is one of the motivations behind this study.Hence, this study

departs from previous studies due to the inclusion of relevant variables and thus employs the

most appropriate and robust methodology to explore the budget deficits and how it affect the

selected macroeconomic variables of these economies in both short and long run.

Against this background, the study contributes to the large body of the existing literature on

fiscal policies in Nigeria and Ghana in two ways. First, unlike many empirical studies, the

study employs a more vigorous and robust approach; the Seemingly Unrelated Regression

(SUR) model to analyze the effect of budget deficit on the selected macroeconomic variables

in Nigeria and Ghana over the period covering from 1970 to 2013. Second, the study

provides empirical evidence for the economies with recent fiscal policies for which

researches have not been conducted recently. Besides, previous studies have advanced in

characterizing the implications of alternative sources and composition of deficits spending

without investigating the effects of budget deficits on the selected macroeconomic variables

in the two economies.

1.3 Research Questions

In the light of the above discussions, the following research questions shall be addressed:

i. What are the effects of budget deficiton interest rate?

P a g e | 21

ii. What are the effects of budget deficit on inflation?

iii. Does budget deficit have any impact on economic growth?

1.4 Objectives of the Study

The broad objective of this study is to investigatethe short and long run effects of budget

deficits on selected macroeconomic variables in Nigeria and Ghana. Specific objectives of

the study are:

i. To examine the effects of budget deficits on interest rates in Nigeria and Ghana.

ii. To ascertain the effects of budget deficits on inflation in Nigeria and Ghana.

iii. To evaluate the effects of budget deficits on economic growth in Nigeria and Ghana.

1.5 Hypotheses of the Study

In view of the above research questions, the following hypotheses are formulated in order to

ascertain the answers to the questions:

H01: Budget deficitshavenosignificant effects on interest rate in Nigeria and Ghana.

H02: Budget deficitshavenosignificant effects on inflation in Nigeria andGhana

H03: Budget deficits have no significant effects on economic growth in Nigeria and Ghana.

1.6 Policy Relevance of the Study

Developing economies like Nigeria and Ghana are in search of long-term policies not only

for macroeconomic stabilization but also for sustainable economic growth and development.

The private sector has always mourned that the fiscal deficit and its inflationary financing has

led to a slow-down in economic activity. There is need for a comprehensive study which

exposes the dynamics of the government fiscal deficit and its effects on the economy. This

study is designed to investigatethe short and long run effects of budget deficits on some

selected macroeconomic variables in Nigeria and Ghana. An academic study such as this is

P a g e | 22

crucial to both the Nigerian and Ghanaian economy in ascertaining the extent to which

budget deficit affects some macroeconomic variables in both short and long run. However,

the justification of this study is that it will add value to policy making especially in fiscal

adjustment and macroeconomic management. The findings of the study will also assist policy

makers to understand the centrality of the government fiscal deficit in policy formulation. It

is further hoped that the findings of the study will assist policy makers to place the right

emphasis on the role of fiscal adjustment in economic policy.

Furthermore, given the Keynesian-Ricardian dichotomy on budget deficit, it is needful to

investigate the effects of budget deficits on some selected macroeconomic variables in

Nigeria and Ghana. As a result, this research work seeks to contribute to the ongoing debate

on the relationship of budget deficits and some selected macroeconomic variables in Nigeria

and Ghana. Therefore, policy makers, experts, institutions, government agencies, researchers

and students in areas of public sector economics, development economics, international

economics, and econometrics are likely to find the outcome of this study very useful.

1.7 Scope of the Study

The study, as stated abinitio tends to investigate the short and long run effects of budget

deficits on selected macroeconomic variables in Nigeria and Ghana. It is pertinent to note that

the nexus between budget deficits and macroeconomic variables are still not well ascertained

especially when viewed in both short and long run. However, the study covers from 1970 to

2013. The range is chosen to ensure high level of degree of validity and precision in the

study. The variables of interest which are used to investigate the short and long run effects of

budget deficits on the selected macroeconomic variables in Nigeria and Ghana are: budget

deficit, interest rates, inflation,exchange rate depreciation, government expenditure, money

supply (M2), total savings, and real GDP.

1.8 Conceptual Framework

P a g e | 23

Awe and Funlay (2014) state that budget deficit occurs when government expenditures

exceed its revenues, thus the level of public savings is negative. This may harm the economic

growth of a country. Budget deficits lead to incurring debts which is a stock of liabilities of

the government (Keating, 2000). Budget deficit is a situation where the government budgets

to spend more than it intends to collect as revenue (Udu and Agu, 2000). Dernberg (1985)

posits that budget deficits are generally associated with recession because of the effect on

revenues and expenditures.

Fiscal deficit has gathered substantial attention in the literature in the area of macroeconomic

theory due to its impact on the macroeconomic variables. When budget deficit is financed by

borrowing, it expands government’s demand for credit through competition with households

and business firms (Hyman, 1994). This puts upward pressure on interest rate and slows

down the rate of capital formation. In Keynesian models, this occurs through a rise in real

interest rate which reduces investment purchases through the transmission mechanism.

However, this depends on the responsiveness of interest rate to increased demand for credit

and the reaction of private investors to higher interest rate. For instance, if investment

demand is unresponsive to changes in interest rate, the effect on investment will be very

small. Also, if the economy is in deep recession, any extra borrowing by government may put

little upward pressure on interest rate because the supply curve for funds will be quiet flat.

Yet, if the return on private investment exceeds the return on government investment

particularly on infrastructure, the rise in public investment would crowd in private investment

(Barua, 2005).

Also, large budget deficit increases the debt crisis in terms of its services and levels. As the

national debt grows, interest payment also grows which serves as tax on investment. This

reduces private investment, increases unemployment, lowers tax revenue and leads to higher

future deficits. Hence, the economy continues to incur mounting debts which may lead to its

P a g e | 24

collapse. Most countries trapped in debt servicing difficulties did run huge budget deficits at

some point in time. Yet, it is argued that public debt growth compels government to target

higher economic growth and revenue in order to finance any rising debt obligations.

Otherwise it will force the economy into a deficit trap (Barua, 2005).

On the burden of future generations, most economists agree that financing budget deficit

through external debt means the postponement of tax increases. However, it is asserted that

such burden depends on how the contracted loan is utilized. If the funds are spent on current

consumption expenditure, future generations are likely to be worse-off but if spent on

productive activities such as education and health then future generations are likely to be

better-off (Mankiw, 2003).

In addition, if budget deficit is monetized, it increases aggregate demand through increase in

government purchases without a corresponding increase in taxes. Hence, governments need

to run fiscal deficit particularly in the early stages of development to lead the economy in the

path of growth and development (Xiomara & Greenidge, 2003). Secondly, it increases money

supply. This exerts downward pressure on interest rate and upward pressure on equilibrium

money stock and price level unless the economy is in deep recession. This leads to higher

inflation, uncertainty and instability of real interest rate which tends to lower real tax revenue.

Hence, monetized deficit should be kept low and effectively managed in the short-to-medium

term (Bebi, 2000; Turnovsky, 2000).

Causes and Determinants of Budget Deficit Growth

In general, changes in budget deficit is attributed to changes in government spending or tax

revenue or both. Government receives revenue in its daily transactions and on capital items in

the form of taxes and interests. On the other hand, government pays for daily activities and

capital items such as administrative expenses, loans and grants. Thus, budget deficit increases

when government spending persistently exceeds its revenue. If expenditure continue to mount

P a g e | 25

up throughout the years whereas revenues especially taxes are poorly collected, it widens the

budget deficit position of the country. In this case, the accumulated value of past deficit

creates increase debts which must be financed together with the accompanying interest

payments.

With reference to political-economic models of government behaviour, it is recognized that

incumbent administrations tend to stimulate their economies on the eve of political elections

through tax cuts, increase spending and transfer payments. This occurs in countries where

political power changes frequently between rival parties. In such cases, each rival

administration spends over and above its budget and deliberately wait until after election

before implementing policies to reduce the deficit. These ad hoc policies tend to widen the

overall budget deficit and debt levels of the countries (Sachs & Larrain, 1993).

However, the extent of the impact of budget deficit on an economy is blamed by

macroeconomic factors such as expected inflation, cyclical position of the economy which

influences tax revenues and changes in expenditure. Theory predicts that cyclical fluctuations

in output which is caused by economic boom and/or recession impact significantly on budget

deficit. In periods of recession when output is low, budgets tend to be in deficit because direct

taxes fall sharply due to contraction in tax base. Also, certain categories of government

spending become countercyclical and rise during business cycle downturn. Yet, such

fluctuations in output growth are endemic in free market economies (Gebhard & Silika,

2006).

Budget Deficit Growth and Economic Sustainability

Financing of budget deficit in Ghana and other developing economies like Nigeria have had

diverse macroeconomic burden on the economy (Antwi et al, 2013). For instance central

bank financing of budget deficit have expanded the monetary base and money supply.

P a g e | 26

According to Wetzel and Roumeen (1991) central bank financing of budget deficit in Ghana

has distorted the distinction between monetary and fiscal policies whereas the sale of

domestic bond increased interest rate and this has led to increase in the net domestic

financing from 0.49 percent of GDP in 2004 to 4.15 percent in 2006. As a result, money

supply (currency and deposits) increased from 6.84 percent in 2005 to 34.4 percent in 2006,

and thus the domestic interest and bank rate reduced due to low demand for bonds (ISSER,

2007). Also, Ghana has accumulated large external debt and so borrow externally only on

short term bases at high interest rate. This is because foreign financing raises the cost of

servicing external debt. For this reason, Ghana’s access to external borrowing prior to 1984

had been limited, ranging between -0.74 and 1.62 percent of GDP. In recent times however,

debt levels have been falling. External debt fell from 72.5 percent in 2004 to 26.9 percent in

2006 with debt service to GDP reducing from 6.8 percent in 2004 to 6.0 percent in 2006

(Wetzel and Roumeen, 1991: 48; ISSER, 2007)

1.9 Structure of the Study

This study will be organized in five chapters. Following this introduction as Chapter 1,

Chapter 2 presents a review of literature on both thetheoretical and empirical evidences.

Chapter 3 discusses the methodology used in the study, Chapter 4 presents the analysis and

interpretation of the results obtained using the methodologies in previous chapter. Finally,

Chapter 5 highlights the conclusion and recommendations on fiscal policy management in the

Nigeria and Ghana.

P a g e | 27

CHAPTER TWO

REVIEW OF RELATED LITERATURE 2.1 Review of Theoretical Literature

This section reveals the theoretical framework related to budget deficit and macroeconomic

variables. Some of the economist such as Keynesian, Neoclassical and Ricardian Schools of

Thought gave either positive or negative support to the relationship between budget deficits

and macroeconomic variables.

2.1.1 Budget Deficits, Crowding In and Crowding Out Effects Schools of Thought

In analyzing the literatures on the relationship between budget deficits and macroeconomic

variables, Bernhein (1989) provides a brief summary of the three paradigms, and the cursory

of the paradigms are presented below.

The Neoclassical School

The neoclassical school proposes an adverse relationship between budget deficits and

macroeconomic variables. They argue that budget deficits lead to higher interest rates,

discourages the issue of private bonds, private investments, and private spending, increases

inflation level, and cause a similar increase in the current account deficits and finally slows

the growth rate of the economy through resources crowding out.

P a g e | 28

The Neoclassical school considers individuals planning their consumption over their entire

cycle. By shifting taxes to future generations, budget deficits increase current consumption.

By assuming full employment of resources the neoclassical school argues that increased

consumption implies a decrease in savings. Interest rate must rise to bring equilibrium in the

capital markets. Higher interest rates, in turn, result in a decline in private investment,

domestic production and an increase in the aggregate price level. Furthermore, Yellen (1989)

in Onuorah, and Ogomegbunam (2013) argues that in standard Neoclassical Macroeconomic

models, if resources are fully employed, so that output is fixed, higher current consumption

implies an equal and offsetting reduction in other forms of spending. Therefore, there will be

fully crowding-out of investment and/or net exports.

It is worth noting that it is important to distinguish between “financial” crowding out and

“resource” crowding-out. “Resource” crowding out occurs when the government competes

with the private sector on purchasing certain resources (skilled labour, raw materials and so

on). When the government sector expands, the private sector will contract because of the

increase in prices on these resources due to an excess demand by the government, hence this

leads to a fall in investment and consumption by the private sector. Thus the government

sector’s expansion crowds out the private sector. It is worth noting here as well that resource

crowding out is an important issue to take into account especially in developing countries

where resources are scarce even sometimes to the private sector, so any excess demand for

these resources by the government will severely impinge on private sector productivity.

The Keynesian School

The Keynesian economists propose a positive relationship between budget deficits and

macroeconomic variables. They argue that usually budget deficits result in an increase in

domestic production, increases aggregate demand, increases savings and private investment

at any given level of interest rate. The Keynesian absorptive theory suggests that an increase

P a g e | 29

in the budget deficits would induce domestic absorption and thus, import expansion, causing

current account deficit. In the Mundell-Fleming framework, an increase in the budget deficit

would induce an upward pressure on interest rate, causing capital inflows and an appreciation

of the exchange rate that will increase the current account balance.

The Keynesians provide a counter argument to the crowd-out effect by making reference to

the expansionary effects of budget deficits. They argue that usually budget deficits result in

an increase in domestic production, which makes private investors more optimistic about the

future course of the economy resulting in them investing more. This is known as the

“crowding-in” effect. It is worth noting here that the traditional Keynesian view differs from

the standard neoclassical paradigm in two fundamental ways. First, it permits the possibility

that some economic resources are unemployed. Second, it presupposes the existence of a

large number of liquidity-constrained individuals. This second assumption guarantees that

aggregate consumption is very sensitive to changes in disposable income. Many traditional

Keynesians argue that deficits need not crowd out private investment. Eisner (1989) suggests

that increased aggregate demand enhances the profitability of private investments and leads

to a higher level of investment at any given rate of interest. Hence deficits may stimulate

aggregate savings and investment, despite the fact that they raise interest rates. He concludes

that “evidence is thus that deficits have not crowded-out investment. There has rather been

crowding-in”. Heng (1997) utilized an overlapping-generations (OLG) model to provide a

theoretical framework to analyze the “crowding-in” issue of private capital by public capital.

He shows that public capital crowds-in private capital through two channels, namely, via its

impact on the marginal productivity of labour and savings, and via (gross)

complementarity/substitutability between public and private capital.

The Ricardian School

P a g e | 30

Finally, there is another contrary approach advanced by Barro (1989) known as the Ricardian

Equivalence Hypothesis (REH). Ricardian equivalence, or the Barro-Ricardo equivalence

proposition, is an economic theory which suggests that government budget deficits do not

affect the total level of demand in an economy. It was initially proposed by the 19th century

economist David Ricardo. In simple terms, the theory can be described as follows.

Governments may either finance their spending by taxing current taxpayers, or they may

borrow money. However, they must eventually repay this borrowing by raising taxes above

what they would otherwise have been in future. The choice is therefore between "tax now"

and "tax later". Suppose that the government finances some extra spending through deficits -

i.e. tax later. Ricardo argued that although taxpayers would have more money now, they

would realize that they would have to pay higher tax in future and therefore save the extra

money in order to pay the future tax. The extra saving by consumers would exactly offset the

extra spending by government, so overall demand would remain unchanged.

More recently, economists such as Robert Barro have developed more sophisticated

variations on the same idea, particularly using the theory of rational expectations. Ricardian

Equivalence suggests that government attempts to influence demand using fiscal policy will

prove fruitless. He argues that an increase in budget deficits, due to an increase in

government spending, must be paid for either now or later, with total present value of receipts

fixed by the total present value of spending. Thus, a cut in today’s taxes must be matched by

an increase in future taxes, leaving real interest rates, and thus private investment, and the

current account balance, exchange rate and domestic production unchanged. Therefore,

budget deficits do not crowd-in nor crowd out macroeconomic variables i.e. no positive or

negative relationship exists.

2.2 Thematic Issues

2.2.1 Budget Deficits in Ghana: An Overview

P a g e | 31

Ghana’s economy has maintained commendable growth trajectory with an average annual

growth of about 6.0% over the past six years. In 2013 growth decelerated to 4.4%,

considerably lower than the growth of 7.9% achieved in 2012. Growth has, however, been

broad-based, driven largely by service-oriented sectors and industry, which on average have

been growing at a rate of 9.0% over the five years up to 2013. Over the medium term to 2015,

the economy is expected to register robust growth of around 8%, bolstered by improved oil

and gas production, increased private-sector investment, improved public infrastructure

development and sustained political stability (African Economic Outlook, 2014).

According to AEO (2014), the continued widening budget deficit has been a major constraint

to fiscal and debt sustainability. Following an expenditure overrun in 2012, marked by an

unprecedented budget deficit of around 12% of GDP, the situation persisted in 2013, with

about the same level of budget deficit. Revenue enhancing and expenditure consolidation

measures underway in 2014 are expected to ease the fiscal deficit to 9%. In conjunction with

fiscal constraints, inflation has been on the rise resulting from a number of factors including

the removal of subsidies on petroleum prices and a gradual rise in electricity and water tariffs.

It is also worth noting the rise in public debt from 43% of GDP in 2011 to 48% in 2012, and

further to 53.5% in September 2013, resulting from a widened budget deficit. The external

sector will continue to experience a widened current-account deficit of around 12% of GDP

in 2014, exacerbated by a decline in commodity prices of major export commodities,

particularly on gold and cocoa.

2.2.2 Determinants of Budget Deficit Growth in Ghana

A model involving variation in inflation, government expenditure during wartime, cyclical

fluctuation in output during economic boom and recession in the postwar period was tested to

ascertain if it differs significantly from those during the world wars in the Swiss federal state.

The estimate showed some cyclical fluctuation in the world war periods. This supports the

P a g e | 32

assertion that significant determinant of budget deficit is increase in state expenditure during

wartime. In this case, civilian expenditure was reduced and/or taxes increased to finance

military expenditure during the war (Gebhard and Silika, 2006). In Ghana, changes in

inflation, interest rate and real GDP have reacted negatively to changes in budget deficit. For

instance, Antwi and Mills (2013) observed that high inflation in 1983 caused budget deficit to

increase by 35.8 percent due to decline in direct tax revenue. Also, changes in real interest

rate increased budget deficit by 11.3 percent of GDP in 1984. Again, high wage bill increased

the deficit by 2.5 percent in 1985. Thus, changes in macroeconomic variables have had strong

impact on the fiscal deficit in Ghana. However, these effects have become less pronounced

over the past years as the Ghanaian economy has grown more stable (Wetzel & Roumeen,

1991).

2.2.3 Fiscal Policy in Ghana

The government of Ghana is committed to fiscal consolidation with the ultimate objective of

reducing the budget deficit to around 5% of GDP by 2016. However, trend performance of

government operations continues to register widened budget deficit. Following an

expenditure overrun in 2012, marked by a significant budget deficit of around 6% of GDP,

the situation persisted in 2013 with a deficit of 7.8%. Fiscal measures implemented in the

second half of 2013 are expected to yield dividends in 2014. Key contributors to widened

budget deficit have been increased spending on wages and salaries, interest payments,

subsidies and arrear payments (African Economic Outlook, 2014).

According to AEO (2014), for the government of Ghana to address fiscal constraints

effectively, efforts should aim to raise tax revenue, in view of its substantial share (80%) of

total domestic revenue. Oil revenue is still low, accounting for just 0.2% of total revenue.

Grants from development partners are marginal and have maintained a diminishing trend,

accounting for only 7% of total revenues in 2013, down from around 14% in 2010. Despite

P a g e | 33

the marginal contribution of oil receipts, it is worth noting the distribution formula of such

receipts. In compliance with the Ghana Petroleum Revenue Management Act, about 30% of

total oil revenue to government is retained by the Ghana National Petroleum Commission

(GNPC) for the development of the oil and gas industry, while the remaining 70% is

appropriated through the Annual Budget Funding Amount (ABFA) and Ghana Petroleum

Funds (GPF) at around 40% and 60% respectively. While resources under ABFA are

reserved for funding priority projects, petroleum funds (GPF) are partly invested for future

generations through the established Ghana Heritage Fund.

2.2.4 Interest Rate Policy in Ghana

Interest rates were administratively controlled by the Bank of Ghana (BOG). The rationale

for the controls was that credit had to be cheap so as to promote investment and support that

favors borrowers (Daumont, Le Gall, & Leroux, 2004). It was the BOG that determined the

structure of the bank interest rates, which include the minimum interest rates for deposits and

maximum lending rates. Preferential lending rates were given to priority sectors such as

agriculture. The structure of interest rates determined by the BOG made no allowance for

loan maturity or risk; indeed, incentives for banks to extend credit were often perverse

because riskier sectors such as agriculture were accorded preferential inflation rates. In most

of the years, nominal interest rates were held below the prevailing inflation rates. However,

when inflation escalated in the middle of 1970s and the early 1980s, real interest rates were

highly negative (Antwi, 2009)

2.2.5 Fiscal Policy in Nigeria

Fiscal policy Management in 2012 and 2013 has centred on consolidation in order to ensure

macroeconomic stability. The fiscal deficit as a percentage of GDP has been estimated at -

1.8% in 2013, up from -1.4% in 2012, but well below the fiscal stance of a maximum of 3.0%

deficit enshrined in the Fiscal Responsibility Act. The Medium Term Expenditure

P a g e | 34

Framework (2014-2016)and Fiscal Strategy Paper proposed benchmark oil prices of USD 74,

USD 75 and USD 76 per barrel (pb) for 2014, 2015 and 2016 respectively. A benchmark oil

price of USD 77.5 pb was however set in the 2014 budget presentation to the national

assembly.

The 2012 budget was signed into law by the president of the Federal Republic of Nigeria in

April of the year following its passage into law by the legislative arm of government. The

level of implementation of the budget was 71.6%. The 2013 budget was signed into law by

the president in February, which was two months earlier than the preceding year as the

disagreement between the executive and the legislature over appropriation were resolved

early. The eventual implementation rate was around 70.0%. The ratio of capital expenditure

to total expenditure diminished to an estimated 23.9% in 2013 from 24.3% in 2012. The share

of capital expenditure on social community services (Health, Education and other allied

services) in the total rose from 10.0% in 2011 to 11.1% in 2012 while economic services

(agriculture and infrastructures) declined from 42.1% to 36.7%, respectively. The capital

component of Subsidy Reinvestment and Empowerment Programme (SURE-P) contributed

about NGN 272.5 billion, or USD 1.72 billion, thus raising the total capital expenditure to

NGN 2 059 billion (USD 13.03 billion) in 2013 (AEO, 2014).

In pursuance of fiscal prudence and the burgeoning debt profile, the government limits its

borrowing requirements in compliance with the Fiscal Responsibility Act (2007). Figures

from the Debt Management Office as at 31 December 2013 showed that Nigeria’s public debt

stock was USD 64.51 billion. Of this amount, the external debt of both the federal and state

governments was only USD 8.82 billion, of which the state governments constituted about

38.2%. The balance of USD 55.69 billion (about 86.3% of the total) drawn by both the

federal and state governments makes up the domestic debt component. In this regard, new

borrowing in 2014 is estimated to be NGN 572 billion (USD 3.62 billion), slightly down

from NGN 577 billion (USD 3.65 billion) in 2013 (AEO, 2014).

P a g e | 35

The observed persistent decline in oil revenues portends risk for fiscal policy and will shape

the trajectory of the medium-term fiscal outcome. Total revenue was on a declining trend

throughout 2013. It is noteworthy, though, that non-oil revenues have been rising

significantly over the same period, thereby compensating for the shortfall in oil revenues,

albeit inadequately. If the declining oil revenues are not contained and the rise in non-oil

revenues is not sustained, fiscal risks may set in. This could hinder the success of the

country’s ongoing reforms, and an overall negative impact on economic activities may result.

In addition, the government has been adjusting expenditures to accommodate the shortfall in

revenues. Capital expenditure, however, suffers huge downward adjustments because

recurrent expenditures, which are mainly salaries and overhead, can hardly be adjusted

automatically. These downward adjustments in capital expenditure may further slowdown

total economic activities and growth.

2.2.6 Macroeconomic Environmentsand Analytical Comparison between Nigeria and

Ghana

This section provides a review of economic developments in Nigeria and Ghana; and trends

in the major macroeconomic variables in recent years. The variables discussed in this section

include Gross Domestic Product (GDP), Inflation, the Value of Total Trade, Imports and

Exports.

The Nigerian economy faced numerous challenges which impacted overall economic activity

in 2012. Declines in the real growth rates of economic activity were experienced in both the

oil and non-oil sectors. Oil production was less than expected due to security challenges, and

floods which occurred in the latter part of the year, while the non-oil sector (notably

Agriculture, Wholesale & Retail Trade) was mostly affected by the floods and weaker

consumer demand (National Bureau of Statistics, 2013). The revised data for the NBS (2012)

indicates that real GDP grew by 6.34 % in the first quarter and 6.39% in the second quarter of

P a g e | 36

2012. The rate of economic activity was slightly higher than the initial estimates of 6.17%

and 6.28% respectively.

According to the Nigerian National Petroleum Corporation (NNPC), oil production was

estimated at 2.37 million barrels per day (mbpd) during the first half of 2012, as against

2.48mbpd produced in the first half of 2011. The 4.4% decline in crude production levels was

attributed to disruptions in production due to cases of oil theft and vandalization in the oil

producing areas. On the other hand, non-oil sector was affected by the incidence of flooding,

as well as muted consumer demand for the most part of the year, as seen in the Wholesale

and Retail Trade, Telecommunication and Post sectors while infrastructure challenges still

hampered Manufacturing. However, the Manufacturing sector did record a slight uptick in the

second quarter as a result of positivedevelopments in the power sector.

In Ghana, the economy is expected to slow down for the fourth consecutive year to an

estimated 3.9% growth rate in 2015, owing to a severe energy crisis, unsustainable domestic

and external debt burdens, and deteriorated macroeconomic and financial imbalances

(African Economic outlook, 2015). However, the provisional gross domestic product (GDP)

figures issued by the Ghana Statistical Services (GSS) further suggest that the economy

expanded by 4.2% in 2014, less than the growth of 7.3% recorded in 2013. The drivers of

growth continue to be the service sectors, which constitute 50.2% of the economy, followed

by industry and agriculture at 28.4% and 19.9% respectively (AEO, 2015).

High growth rates in Ghana over the recent years have been accompanied by the build-up of

macroeconomic imbalances. In 2014 current account and fiscal deficits widened to 9.2% and

10.4% of GDP respectively, and the rate of inflation averaged 17.0%. By the end of

December 2014, foreign reserves were at 3.2 months of import cover. The domestic currency,

the cedi (GHS) depreciated by over 30% in nominal terms over the first nine months of the

P a g e | 37

year compared to a depreciation of 4.1% during the corresponding period in 2013. The

continued growth in the budget deficit resulted in public debt increasing from 55.8% of GDP

in December 2013 to 67.1% of GDP by the end of December 2014. To address the

increasingly unsustainable fiscal and current account imbalances, the Ghanaian authorities

started negotiations for a stabilization programme with the International Monetary Fund

(IMF) that was expected to begin in early 2015(AEO, 2015).

According to National Bureau of Statistics(NBS) (2013) as at December 2012, the headline

inflation rate showed a general downward trend during the year, despite the economic

challenges that the country witnessed. From the 12.6% recorded in January (year- on-year),

the headline inflation rate reached12.9% in April and June before slowing to 11.3% through

September. It rose further to 12.3% in November before falling slightly to 12.0% in

December. As a result, the average inflation rate for the year stood at 12.2%. On a month-on-

month basis, the headline inflation rate rose sharpest in March (1.6%). The major sources of

inflationary pressure in 2012 still appear to be structural and infrastructural constraints.

Nevertheless, the removal of fuel subsidies early in the year, the devastating flood that

occurred in the third and fourth quarters of 2012 as well as seasonal effects also played major

roles in driving up prices at various times.

In Nigeria, as at the third quarter of 2012, the value of total Merchandise Trade for the

country was estimated at N20,885.4 billion over the first three quarters of the year. Compared

to levels recorded during the first three quarters in 2011, the value of total merchandise trade

had remained roughly unchanged, increasing marginally by 0.4%. The value of total

merchandise trade points to increasing exports over the period while imports have been on

the decline. Specifically, imports have continued to trend downwards since the second quarter

of 2011, while the value of exports which increased substantially in late 2011, dipped in the

P a g e | 38

first quarter of 2012, but picked up in the second and third quarters of 2012(National Bureau

of Statistics (NBS), 2013).

2.3 Empirical Literature

On the empirical front, there is a large body of literature documenting the effects (both short

and long run) of budget deficits on macroeconomic variables in both developed and

developing economies. This large body of literature on the topic could be divided into

international, and Nigerian-Ghanaian evidence for distinctive purposes; and thus logically

arranged in order of objectives of the study and year(s) in which the study was carried out.

2.3.1 International Evidence

Vamvoukas (1998) empirically examines the short and long-run effects of budget deficits on

interest rates for Greece using annual time series data from 1970 to 1990 within the

methodological framework of cointegration, ECM strategy, and several diagnostic and

specification tests. The estimation results support the Keynesian model of a significant and

positive relationship between budget deficits and interest rates

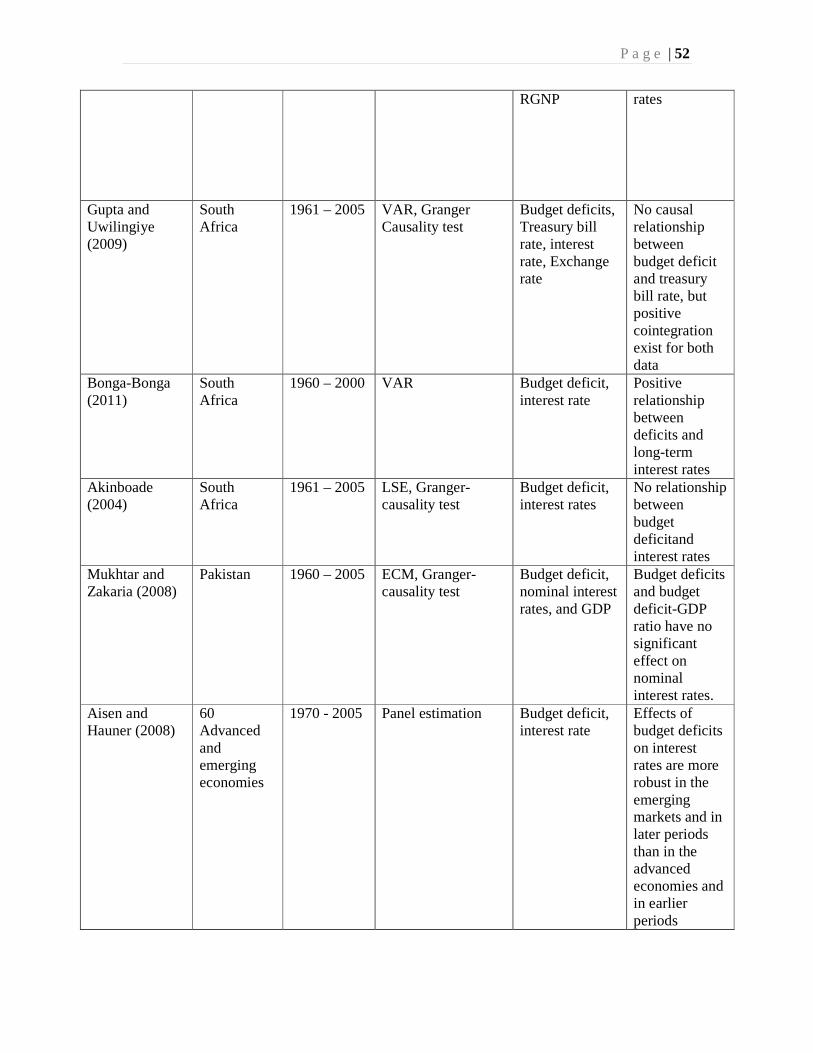

Gupta and Uwilingiye (2009) investigate the direction of temporal causality between budget

deficit and interest rate for South Africa using quarterly and annual data for the period of

1961 to 2005. The results show that budget deficit Granger causes interest rate in the

quarterly data. However, for the annual data, the study finds no causal relationship between

the budget deficit and the Treasury bill rate. The two variables are positively cointegrated for

both data frequency.

Similarly, Bonga-Bonga (2011) investigates the extent of the effects of the systematic and

surprise changes in budget deficits on the long-term interest rate in South Africa between

1960 and 2000 using vector autoregressive (VAR) techniques. The study finds a positive

P a g e | 39

relationship between the budget deficits and long-term interest rates. On the other hand,

Akinboade (2004) uses the LSE approach and Granger-causality methods to investigate the

nexus between budget deficit and interest rate in South Africa, the study finds no relationship

between the budget deficit and interest rates.

Mukhtar and Zakaria (2008) uses Granger Causality test and Error Correction Model (ECM)

to examine long run relationship between budget deficits and interest rates for Pakistan using

quarterly time-series data for the period 1960 to 2005. The regression results show that

budget deficits have no significant effect on nominal interest rates. The results equally reveal

that budget deficit-GDP ratio has significant positive impact on nominal interest rates.

Aisen and Hauner (2008)asses the relationship between budget deficits and interest rates in

60 advanced and emerging economies with a panel dataset spinning from 1970 to 2005.The

result shows a significant and positive relationship between budget deficits and interest rates.

The study also finds that the effects of budget deficits on interest rates varied by country

group and period. The resultequally shows that the effects were larger and more robust in the

emerging markets and in later periods than in the advanced economies and in earlier periods.

The study further reveals that the effect of budget deficits on interest rates depends on

interaction terms and is only significant under one of several conditions such as sources of

deficit financing (mostly domestically financed), and/or interact with high domestic debt; low

financial openness, and/or interest rates liberalization.

Noula (2012) examines the determination of fiscal deficit and nominal interest rate in

Cameroon using annual time series data from 1974 to 2009. The study employs a loanable

funds model to test for fluctuations in the economy budget deficits and nominal lending rates.

Moreover, the empirical assessmentcarried out using ADF test and Error Correction Model

reveals a significant positive association between budget deficits and domestic nominal

P a g e | 40

lending interest rate. Also, the result from the Pairwise Granger Causality test conducted

shows a bi-directional causality between budget deficits and nominal interest rate.

Guess and Koford (1984) utilizes the Granger Causality test to study the causal relationship

between budget deficits and inflation, GNP and private investment using annual time-series

data for seventeen OECD countries for the period 1949 to 1981. The results show that budget

deficits do not exert negative changes in these variables. In the same vein, Darrat (1985)

applies Ordinary Least Square (OLS) technique in examining empirically the linkage

between deficits and inflation in the US during the post-1960 period. The estimation results

show that both monetary growth and federal deficits significantly influenced inflation during

the 1960s and 1970s. In addition, the study concluded that federal deficits bore a stronger and

more reliable relationship to inflation than monetary growth.

Easterly and Schmidt-Hebbel (1993) analyze data from a sample of 10 countries and find

strong evidence that over the medium term, money financing of the deficit leads to higher

inflation, while debt financing leads to higher real interest rates or increased repression of

financial markets. Moreover, Tekin-Kuru and Ozmen (1998) examine the long run

relationship among budget deficits, money supply and inflation in Turkey. The results reveal

that while the endogeneity of supply of money and inflation reject the validity of the

monetarist view, lack of direct relationship between inflation and budget deficit repudiate the

pure fiscal theory explanations.

Darrat (2000) utilizes an Error Correction Model (ECM) to investigate if high budget deficits

have any inflationary consequences in Greece over the period 1957- 1993. The empirical

result shows that the deficit variable exerts a positive and statistically significant impact on

inflation in Greece. More also, Catão and Terrones (2005) find a strong link between fiscal

deficits and inflation using a sample of 107 countries over the period 1960 to 2001. Their

P a g e | 41

results show that, a 1 percent reduction in the ratio of the budget deficit to GDP is associated

with an 8.75 percent lower inflation rate.

Makochekanwa (2008)studies the impact of budget deficit on inflation in Zimbabwe for the

period 1980 to 2005. The study finds a positive and stable long run relationship between the

budget deficit, exchange rate, GDP and inflation. Habibullah, Cheah and Baharom (2011)

examine the relationship between budget deficit and inflation in thirteen Asian developing

countries using annual data for the period 1950 – 1999. The study employs Granger causality

test and their result shows the existence of a long run relationship between budget deficit and

inflation thus concluding that budget deficits are inflationary in Asian developing countries.

Ndashau (2012) adopts Granger causality techniques, augmented by vector error correction

model (VECM) to highlight the existence of a causality effect from inflation to budget

deficits scaled by the money base. However, the effect of budget deficits on inflation was not

statistically significant. On the other hand, Lin and Chu (2013) employ a dynamic panel

quantile regression (DPQR)model following the autoregressive distributive lag (ARDL)

regime to examine the extent to which fiscal deficits are inflationary in 91 countries between

1960 and 2006. The results of the study show that fiscal deficits are inflationary only in high

inflation countries.

Dwyer (1982) applies a Vector Autoregression (VAR) Model to test for the linkage between

government deficits and macroeconomic variables (such as prices, spending, interest rates

and the money stock) in the U.S. over the period 1952 – 1978. The results are consistent with

the hypothesis that there are no perceived wealth effects of predictable changes in

government debt held by the public and as a result, no effects of the debt on inflation. No

evidence is found that larger government deficits increase prices, spending, interest rates, or

P a g e | 42

the money stock. The study also shows that the reason for the decline in inflation rates can be

attributed to the decline of money growth despite borrowing.

Barro (1990; 1991) investigates the effects of tax financed government expenditure on

investment and output in a cross-sectional study of 98 countries over the period 1960-85. The

study reveals that the ratio of real government consumption to real GDP (gc/y) has a negative

association with growth and investment. The result shows that government consumption exert

no direct effect on private productivity, but lowers savings and growth through the distorting

effects from taxation or government-expenditure programs.

Karras (1994) studies the relationship between budget deficits and macroeconomic variables

in a Cross-sectional study involving 32 countries for the period 1950-1980, using OLS and

generalized least square (GLS). The results show that deficits do not lead to inflation, they

are negatively correlated with the rate of growth of real output and increased deficits appear

to retard investment. Similarly, Al-Khedir (1996) investigates the relationship between

budget deficits and macroeconomic performance of the G-7 countries for the period 1964-

1993 using VAR. The study reveals that budget deficits lead to higher short-term interest

rates in the 7 countries. However, the results show that deficits have no impact on the long-

term interest rates. The trade balance has been worsened by the budget deficit and economic

growth in all 7 countries.

Mugume and Obwona (1998) examine the interaction between fiscal deficits and other

macro-level variables for Uganda in the post reform period. The results show that the

unsustainability of the budget deficit has implications for public, external and monetary

sectors. In particular, the study finds a negative relationship between fiscal deficits and

economic growth. Also the study reveals that fiscal deficit is linked to inflation, exchange

rate depreciation and the widening of current account deficit.

P a g e | 43

Vuyyuri and Seshaiah (2004), study the interaction of budget deficit with other

macroeconomic variables (Nominal effective exchange rate, GDP, Consumer Price Index and

money supply) for India, using Cointegration approach and Variance Error Correction

Models (VECM) for the period 1970 – 2002. The study reveals that exchange rate, GDP,

consumer price index and money supply to be cointegrated. Also the study find a bi-

directional causality between budget deficit and nominal effective exchange rates. But the

results find no significant relationship between budget deficit and GDP, Money supply and

consumer price index. The results also show that the GDP Granger causes budget deficit.

Brownbridge and Mutebile (2007) analyze the impact of an increase in the fiscal deficit on

macroeconomic policy management and the fiscal sustainability in Uganda between 1980 and

2005. The study argue that aid funded deficits may have effects akin to the Dutch disease

through the appreciation of the exchange rate with adverse effects for export sector

competitiveness. In addition, Keho (2010) investigates the causal relationship between budget

deficits and economic growth for seven West African countries over the period 1980-2005.

The author finds mixed results with three out of the seven countries showing no evidence of

causality, one showing a unidirectional causality running from deficit to growth and the rest

showing two-way causality between budget deficits and economic growth.

Georgantopoulos and Tsamis, (2011) investigate the casual link between budget deficit and

other macroeconomic variables (Consumer Price Index (CPI), Gross Domestic Product

(GDP) and Nominal Effective Exchange Rate for Greece during the period 1980-2009. Their

findings reveal no link between the budget deficit and CPI but they find casual links between

budget deficit and GDP and Nominal Effective Exchange Rate.

Odhiambo, Momanyi, Othuon and Aila (2013)also study the relationship between budget

deficits and economic growth in Kenya for the period 1970 to 2007. The regression results

P a g e | 44

show a positive relationship between budget deficit and economic growth. Buscemi and

Yallwe, (2012) using GMM technique to test for the nexus between budget deficit and

economic growth using dataset of China, India and South Africa.The study shows that fiscal

deficit results are significant and positively correlated to economic growth and saving in

China, India and South Africa. However, the authors reveal that real interest rates are

negatively and significantly correlated with economic growth and saving. The main

conclusion by the authors is that, fiscal deficit affects the economic growth and saving

through the means financing the deficit.

On the other, Najid (2013) uses Granger-causality test in estimating the relationship between

budget deficit and economic growth of Pakistan using time series data for the period of 1971

to 2007. The result shows that bi-directional causality runs from budget deficit to GDP and

GDP to budget deficit. The study concluded by analyzing that Budget deficit has no role in

bringing back the economy of the country to a stable level of equilibrium.

Lwanga and Mawejje (2014) use a vector autoregressive (VAR) and vector error correction

model (VECM) approach, pairwise granger causality test, and variance decomposition

techniques in investigating the macroeconomic effects of budget deficits in Uganda for the

period 1999 to 2011. The cointegration results indicate that the variables under study are

cointegrated and thus have a long run relationship. Similarly, the results based on the VECM

reveal unidirectional causal relationships running from budget deficits to current account

balance, inflation to budget deficit and budget deficit to lending interest rates. But the results

show no causal relationship between gross domestic product (GDP) and budget deficits in

Uganda. The Pairwise Granger Causality test results reveal unidirectional causal relationships

running from budget deficit to current account, budget deficit to GDP, inflation to budget

deficit, and a bi-directional causal relationship between the current account balance and GDP.

P a g e | 45

The study concluded that budget deficits in Uganda are responsible for widening current

account deficit and raising interest rates

2.3.2 Nigerian-Ghanaian Evidence

Obi and Nurudeen (2008) empirically investigate the effects of fiscal deficits and government

debt on interest rate in Nigeria between 1970 and 2005 using Vector Autoregression

approach (VAR).The empirical findings of the study reveal that the explanatory variables

account for approximately 73.6 percent variation in interest rate in Nigeria. The estimation

also shows that fiscal deficits and government debt are economically and statistically

significant.

Chukwu (2009) employs Johansen and Juselius (2009) multivariate cointegration technique

and Vector Error Correction Model (VECM) to comparatively examine the causal

relationships between internal and external deficits using Nigerian quarterly and annual data

from 1971 to 2006. The cointegration test result suggests a long run stable relationship

between internal deficits and external deficits for both low and high frequency series. Thus

the study supported the Richardian Equivalence hypothesis for quarterly series but validates

the conventional Keynesian view for annual series.

Odionye and Uma (2013) employ augmented Granger causality test approach in examining

the relationship between budget deficit and interest rate in Nigeria using Vector Error

Correction model (VECM) for the period of 1970:1 – 2010:1. The results reveal that in the

long run co-integrating equation, budget deficit exert a positive and significant impact on

interest rate implying that a high budget deficit will increase interest rate in the country. The

result supports the Keynesian proposition. Also, evidence from Johansen co-integration result

indicates that there is a long run relationship between budget deficit and interest rate.

P a g e | 46

Sowa (1994) utilizes Error Correction Model (ECM) in estimating an inflation equation for

Ghana over the period 1963 - 1990. The study shows that inflation in Ghana is influenced

more by output volatility than by monetary factors, both in the long run and in the short run.

In Nigeria, Onwioduokit (1995) employs Granger causality test in investigating the causal

relationship between inflation and fiscal deficits using annual data from 1970 to 1994. The

variables in the empirical model are ratio of fiscal deficit to gross domestic product (GDP),

level of fiscal deficit and inflation rate. The study shows that fiscal deficit causes inflation

without a feedback effect but however feedback exist between inflation and the ratio of fiscal

deficit to gross domestic product.

Omoka and Oruka (2010) employ pair-wise Granger causality test in an attempt to offer

evidence on the causal long term relationship between budget deficit, money growth and

inflation in Nigeria using annual time-series data covering from 1980 to 2005. In considering

the broadest definition of money supply, the study reveal that money supply causes budget

deficit which means that the level of money supply in the Nigerian economy determines

whether there has been or there will be budget deficits. Inflation and budget deficit show a

bilateral or feedback causality proving that the changes that occur in inflation could be

explained by its own lag and also the lag values of budget deficit and in the same vein,

changes that occur in budget deficits are explained by its lagged values and the lagged values

of inflation. The implication of their findings is that both budget deficit and inflation could be