Embed Size (px)

Citation preview

THE EFFECT OF COMMITMENT, SELF-EFFICATION, AND

PRESSURE OF TIME BUDGET ON AUDITOR

PERFORMANCES

SKRIPSI

Presented in Partial Fullfillment of the requirements for The Bachelor’s

Degree in Accounting

by

Valencius Pangestu

008201500130

FACULTY OF BUSINESS

ACCOUNTING STUDY PROGRAM

PRESIDENT UNIVERSITY

CIKARANG, BEKASI

2019

i

ii

iii

iv

v

ACKNOWLEDGEMENT

First of all I would like to express my gratitude to the Lord Jesus for the

blessing and guidance during completing my thesis writing as the requirment for

finishing my education in President University. I would like also to give

appreciation to these people who contribute in assorted ways who deserve this

special mention:

First, Mr. Christanto Hadinata and Mrs. Marlina as my parents for the

prayer, motivation and support. For all I have been through from kindegarten until

the university stage. Thank you so much for everything you have done for me.

Second, my thesis advisor Mrs. Setyarini Santosa SE.,MAFIS.,Ak.who has

given me support and advices from the very beginning until the very last part of

making this thesis successfully happen.

Third, to Head of Accounting Study Program Mrs. Andi Ina Yustina,

M.Sc.,CMA. And accounting lectures and staff for being supportive and keep

cooperative during the thesis writing

Fourth, my beloved friends from President University particularly the

accounting batch 2015 students. For the countless help, support and motivation

throughout our togetherness.

Fifth, to those who involved during my internship at BDO and EY start from

partner, manager and senior who has give me advice and opportunity to finish my

thesis writing.

Finally, I would like to thank everybody who was important to the

successful realization of this thesis, as well as expressing my apology that I could

not mention personally one by one. May God bless you.

Table of Content PLAGIARISM CHECK ........................................................................................... i

DECLARATION OF ORIGINALITY ................................................................... ii

PANEL EXAMINERS APPROVAL SHEET ....................................................... iii

vi

ACKNOWLEDGEMENT ..................................................................................... iv

TABLE OF CONTENT ........................................................................................... v

ABSTRACT ........................................................................................................... ix

INTISARI .................................................................................................................. x

CHAPTER I - INTRODUCTION ........................................................................ 1

1.1 Research Background ............................................................................... 1

1.2 Research Questions ................................................................................... 4

1.3 Research Objectives.................................................................................. 4

1.4 Research Scope and Limitation ................................................................ 5

1.5 Research Benefits ..................................................................................... 5

CHAPTER II – LITERATURE REVIEW .......................................................... 6

2.1.1 Organizational Commitment ....................................................... 6

2.1.2 Self - Efficacy .............................................................................. 7

2.1.3 Time Budget Pressure ................................................................. 9

2.1.4 Auditor Performance .................................................................. 10

2.2 Research Model ................................................................................... 11

2.3 Hypothesis Development .................................................................... 12

2.3.1 Relationship of Organizational Commitment to Auditors

Performance ....................................................................................... 12

2.3.2 Relationship of Self - Efficacy to Auditors Performance ......... 12

2.3.3 Independent Variables .............................................................. 13

CHAPTER III – RESEARCH METHOD ......................................................... 14

3.1 Sampling Design ..................................................................................... 14

3.2 Operational Definition of Variables ........................................................ 15

3.2.1 Independent Variables .............................................................. 14

3.2.2 Dependent Variable ................................................................... 15

3.3 Research Instrument ............................................................................... 16

3.4 Statistical Analysis.................................................................................. 17

vii

CHAPTER IV – RESULT ANALYSIS, DISCUSSION &IMPLICATION ... 20

4.1 Respondent Variable ............................................................................... 20

4.2 Measurement Model Analysis ................................................................ 21

4.3 Structural Model Analysis ..................................................................... 26

4.4 Discussions and Implications ................................................................ 29

CHAPTER V – CONCLUSION, LIMITATION, & SUGGESTIONS ........... 31

5.1 Conclusion .............................................................................................. 31

5.2 Limitation and Suggestions .................................................................... 32

REFERENCES ..................................................................................................... 33

APPENDICES ...................................................................................................... 37

List of Figures

Figure 1. Research Model ...................................................................................... 11

viii

Figure 2. Full PLS Model ..................................................................................... 28

ix

List of Tables

Table 1. Demographic Data ................................................................................... 21

Table 2. Descriptive Statistics and Correlation ...................................................... 22

Table 3. Convergent and Reliability Test .............................................................. 24

Table 4. Discriminant Validity .............................................................................. 26

Table 5. PLS Results .............................................................................................. 28

x

ABSTRACT

Public accounting firms typically have high work pressure and tend to make

employee stress will need an auditor who possesses the exellence performance,

objective and high commitment employees. Therefore, public accounting firms

need to do something to attract potential auditors with their current auditors. As to

increase the auditors performances it self. This research has an objective of

examining the relationship of indepent variables which are organizational

commitment, self – efficacy, and time budget pressure towards the dependent

variable which are auditor performance. The data was collected by using

questionaire that aims the auditor profession in Jakarta. The sample of this research

are 215 respondents. The data are then processed by using Structural Equation

Model-Partial Least Squares (SEM-PLS) analysis. The result from hypothesis

testing shows that organizational commitment , self – efficacy, and time budget

pressure are significantly effect the auditor performance.

Keywords : organizational commitment, auditor performance, self – efficacy, and

time budget pressure.

xi

INTISARI

Kantor akuntan publik biasanya memiliki tekanan kerja yang tinggi dan

cenderung membuat karyawan stres akan membutuhkan auditor yang memiliki

kinerja yang unggul, obyektif dan komitmen yang tinggi pada karyawan. Oleh

karena itu, kantor akuntan publik perlu melakukan sesuatu untuk menarik auditor

potensial dengan auditor mereka saat ini. Salah satu hal penting adalah

meningkatkan kinerja auditor itu sendiri. Penelitian ini bertujuan untuk menguji

hubungan variabel independen yaitu komitmen organisasi, efikasi diri, dan tekanan

anggaran waktu terhadap variabel dependen yaitu kinerja auditor. Data

dikumpulkan dengan menggunakan kuesioner yang bertujuan untuk profesi auditor

di Jakarta. Sampel penelitian ini adalah 215 responden. Data kemudian diproses

dengan menggunakan analisis Structural Equation Model-Partial Least Squares

(SEM-PLS). Hasil dari pengujian hipotesis menunjukkan bahwa komitmen

organisasi, efikasi diri, dan tekanan anggaran waktu berpengaruh signifikan

terhadap kinerja auditor.

Kata Kunci : komitment organisasi, , efikasi diri , tekanan anggaran waktu, dan

kinerja

1

CHAPTER I

INTRODUCTION

1.1 Research Background

Auditors are professions that have certain qualifications for auditing

financial statements. The role of the auditor is considered important because this

profession ensures to provide opinions about the fairness of the financial

statements. Moreover, the results of the report will be useful for three biggest users

such as : the clients, external parties , goverment and legal administration. First, the

clients use the result to enhance credibility of financial statements. Second, the

external parties are shareholders, investors, and potential investors as the results can

be used as guidelines to increase or decrease the investment. Third, goverment uses

the financial report as measurement to calculate the tax and the legal parties use it

in facing legal problems in the future. According to (Sukrisno, 2004)auditing is a

detail and planned examination done by an auditor to provide the financial

statements based on the support of evidence and records. Surely the results of the

audit will be very useful for all parties but the interest of the auditor is to assure that

reports are made independently with good quality. As the result auditor’s

performance play an important role. Performance is the work that can be achieved

by a person and group of people in an organization. The performances in accordance

with the authority and duties of their respective responsibilities. In effort to achieve

the objectives of the organization legally, it is required not to violate with morals

and ethics (Moeheriono, 2009). External auditor are expected to be fair and does

2

not take sides to certain party. (Kalbers & Forgaty, 1995) stated that the task

achieved by auditors is that they are delegated and become part of a measuring tool

to determine whether or not the task being done is auditor performance.

Unfortunately, in the last two decades there has been abuse in authority from

auditor’s such as opinions and investigation done by auditor’s both at domestic and

abroad. As an example: Enron, WorldCom, Kimia Farma, Telkom, and Lippo. In

result it shaken up the world and lead those companies to banckruptcy.

Consequently the auditor losing the trust and considered as non-credible instituton.

Simultaneously crisis in economic as the company went bankrupt and has to dismiss

the employees. Therefore the institution required to work optimally and regain the

trust from public. There are at least three factors that are believed to improve the

quality of the auditor's performance.

The first factor is ccommitment where commitment in the organization is

often interpreted as a combination of attitude and behavior. (Aranya & Ferris, 1984)

stated commitment to the organization includes three parts, namely the sense of

identifying with the goals of the organization, the sense of involvement with the

work of the organization, and a sense of loyalty to the organization. Auditors who

are commited to the accounting firm will show positive attitudes towards the

institution, colleagues, and have the soul to defend its accounting firm, cconcretely

helping to realizing the goals of the accounting firm. At the end it will cause a sense

of belonging from the auditor to the accounting firm he or she works for.

3

The second factor is self-efficacy which can be interpreted as an individual's

belief in their ability to manage an organization by performs a task and achieve a

goal with certain skills. (Maryati, 2008) explained self-efficacy is an individual's

mental representation of reality, formed by past and present experiences, and stored

in long-term memory. As the higher self –efficacy, the bigger the chance to be

succesfull. On the contrary, the low self –efficacy will vulnerable to failure.

(Bandura, A., 1997)reveals that individual belief about their abilities play an

important role in reacting to the various pressures they face.

The third factor is time budget pressure which makes auditors feel under

pressure because of the tight budget given to complete the entire audit program.

The pressure experienced by the auditor when conducting an audit due to limitation

of the time to complete all tasks (DeZoort & Lord, 1997). Temporary, the tight

pressure of time budget will bring the response of the auditor to be functional and

dysfunctional (Kelley,Tim and Seiler,Robert E., 1982)stated auditors feels the time

budget pressure make imbalance between the allocated time to task that must be

completed.

Therefore, the author very interested in raising this issue as a material for

writting scientific research since author are curious with the phenomenon of auditor

performance. In result, to determine what are the factor might effecting the auditor

peformance. The author agree to test organizational commitment, self-efficacy,and

time budget pressure into the auditor peformance. As the organizational

commitment, self-efficacy, and time budget pressure become independent variable.

Meanwhile the auditors perfomance become dependent variable. Since then the

4

auditor giving the title "THE EFFECT OF ORGANIZATIONAL

COMMITMENT, SELF-EFFICATION, AND TIME BUDGET PRESSURE ON

AUDITOR PERFORMANCES".

1.2 Research Questions

1) Does the relationship between commitment positively influence to auditor

performance in pubic accounting firm?

2) Does the relationship between self –efficacy positively influence to auditor

performance in public accounting firm?

3) Does the relationship between time budget pressure positively influence to

auditor performance?

1.3 Research Objective

Based on the formulation of the problem above, the purpose of this

research is to find out:

1) Explain the auditor performance through organizational commitment.

2) Explain the auditor performance through self-efficacy.

3) Explain the auditor performance through time budget pressure.

5

1.4 Research scope and limitation

The research background is about the auditor performance in the public

accounting firm in Jakarta. This research concern more about what factor might

effecting the auditor performance. Hence, the researcher decides to test

orgaizational commitment, self-efficacy, and time budget pressure toward the

auditors performance. In this study, researcher used questionaire as the instrument

to collect the data. Then analyzed it using Warp PLS Software ( version 3.0).

1.5 Research Benefits

1) Public Accounting Firm

This research is expected to give a reference and insight for the public accountant

firm to be able in managing the employee of getting maximum results since their

performance will reflect the accounting firm it self.

2) Future Research

This research is to be a guideline and reference for the future research regarding the

relationship of commitment, self-efficacy, and time budget pressure to auditor

performance. The result of this research hopefully able to contribute more on

behavioral literatures.

3) Readers

The researcher hope this research would be beneficial for readers on knowing

what are the factors might effecting the auditor performance.

6

CHAPTER II

LITERATURE REVIEW

2.1.1 Organizational Commitment

Organizational commitment is employee alignment with a particular

organization as well as goals and the desire to retain members in the

organization. Organizational commitment has become an important

element in the world of work especially for auditor. (Allen & Meyer, 1997)

stated that organizational commitment is a characteristic of relationships

between members of an organization to the accounting firm itself and has

an impact on individual decisions to continue. According to (Aranya &

Ferris, 1984) organization commitment involves three attitudes such as a

sense of identifying the organization goals, a sense of involvement with

organization, and a sense of loyalty to the organization. (Luthans, 2002)

stated that organizational commitment is a strong desire to stay as a

member of the organization, desire to try according to the wishes of the

organization, certain beliefs and acceptance of the values and goals of the

organization.

Therefore a high commitment to the organization of an auditor will

encourage work climate to achieve satisfying performance. Commitment

in organization is divided into two namely, affective and continuance

(Kalbers & Forgaty, 1995). Affective organizational commitment relates

to a view of professionalism and dedication to profession. Meanwhile

7

continuance organizational commitment is positively related to

experience. However negatively effect to professionalism in social

obligations. (Grifin, 2004) mention there are three ways to strengthen

organizational commitment by determining: compensation, benefit, and

employee career path. Compensation is the financial advantage given by

organization for remuneration. While benefit are things outside

compensation given by organization. Latter part is employee career path

to help the employee looking for a better position in organization. As the

result auditor need to have these charactheristics. Such as training, higher

level of knowledge, and higher financial rewards.

2.1.2 Self Efficacy

Self- efficacy is individual confidence or trust in the organization to

achieve that goal. According to (Chen, 2011) self-efficacy is an individual

trust in capacity of skills, knowledge, and ability to perform challenge

tasks very well. (Baron & Byrne, 2000) stated that self-efficacy is an

individual assessment towards the ability or competence to do a task,

achieve a goal, and produce something. Moreover, based on the study done

by (Bandura, 1986)self-efficacy is defined as the desire to commit in self

confidence as the ability to control physical, intellectual, and motivation

to do for his or her career. Self-efficacy can be different in each dimension

that the auditor has to achieve satisfactory performance. (Bandura, A.,

1997)stated that there are 3 dimensions of self-efficacy namely magnitude,

strength,and generality. (Bandura, A., 1997)believe that individual is able

8

to control thoughts, feelings, and actions. The ability to control is strongly

influenced by individual perception. An individual who consider him or

herself very effective will attempted enough to produce successful

outcomes.Therefore, employees with high self-efficacy set career goals

and put more effort in pursuing their career, even facing in challenges to

accomplish the task. The higher self –efficacy has positive impact to

master the task decision and behaviour in their career making decision.

According to (Stjakovic & Luithans, 1998) auditors who are very

efficacious would exert sufficient effort to produce sucessfull outcomes.

On the contrary, auditor who less efficacious would be likely effort to be

useless. It is believed that self-efficacy improves performance in a variety

of work settings including education, training, sports, and management.

(Bandura, A., 1997) stated performances being achieved and past

experience are important parts of self –efficacy. Because the ability of

individuals depend on negative and possitive impact. Since then self –

efficacy is expected to influence behavior of individuals and to obtain great

outcome.

2.1.3 Time Budget Pressure

Time budget pressure is defined as the time budgeted to carry out

the steps in each audit program. During the audit process, the auditor is

required to be able to carry out the task to get efficiency in costs and time.

Time budget pressure is a condition that shows the auditor is required to

make efficiency due to limitation of time that is very strict and rigid

9

(Jemada, 2013). As the results of deadline it is causing time budget pressure.

Time budget pressure is a time constraint that and may arise from the limited

resources allocated to finish the task (DeZoort & Lord, 1997). (Kelly &

Margheim, 1990)stated time budget pressure is related to the pressure

experienced when trying to complete the audit work in the time that is

allocated by the public accounting firm. Therefore, the pressure bring the

auditors into problem. Due to the limited of time allocation the auditor

should finish their job faster or nearly the deadline. Surely sometimes the

auditors feel desperate and frustrated in order to finish the task given.

(DeZoort & Lord, 1997) stated when faced with time budget pressure, the

auditor will respond in two ways namely; functional and dysfunctional

behavior. Functional type is the behavior of the auditor to work better and

maximizing time effectively. Meanwhile, dysfunctional is behavior of the

auditor that generate a low quality of performance. Having dysfunctional

situation probably bring the auditor into two conditions. First, the auditor

will finish the task with a bad quality. Since the auditor will just focus on

how to finish the task as soon as possible without seeing the procedure.

Second, the auditor unable to finish the task in the allocated time. Because

the auditors failed to plan their schedule, time, and strategy in achieving the

task.

2.1.4 Auditor Perfomance

Performance is the result of an evaluation of the work being done

compared to determine criteria. An organization needs employees to operate

10

and improve the quality of products and services. Considering employees

are important assets of organization, so many things need to be considered

related to increased auditor performance. Performance also known for

pattern to achieve goals and measured by comparison with standard.

(Campbell,C., 1998) stated that performance is visible, where individuals

are relevant to attain the goals of the organization. Having an outstanding

performances done by employee is the main goal of organization. All of it

can not be separated from the quality of human resources. (Hellriegel,

Slocum and Woodman, 2001)stated that outstanding performance could be

attain by achieving the main goals, ability being owned, and persistence. In

auditor profession the auditor performance will affect the audit quality and

audit opinion. (Fisher,R.T, 2001) stated the lower auditor performance will

increase potential error, lack of credibility and legal liability. Different with

auditor own interest such as effectiveness, length of service and promotion.

The auditor performance assesment can be determine from the

professionalism work on auditing standards. (Mathis & Jackson, 2006)

stated factors affecting performances such as ability, motivation, support

and relationship with organizations. Therefore the auditor performance

considered for the main outcome in this research.

11

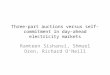

2.1 Research Model

Based on a description of the background, literature review and previous

studies described, the scheme of thought framework of this research is as

follow:

Figure 1. Research Model

2.3 Hypothesis Development

2.3.1 Relationship of Organizational Commitment to Auditor Performances

Organizational

Commitment ( OC )

SELF –

EFFICACY ( SE )

TIME

BUDGET

PRESSURE ( TBP )

AUDITOR

PEFORMANCES ( AP )

12

Auditor who want to remain in the company will try to achieve the desired

performance stated by the accounting firm which ultimately impacts on auditor

performance. Organizational commitment has an influence on auditor performance

since auditor who have high organizational commitment will try to maintain their

membership in the accounting firm (Robbins & Judge, 2008). With the awareness

of organizational commitment it will improve the auditor performances. It is in line

with the research done by (Yeh & Hong, 2012) and (Sarpariyah, 2011) which states

that organizational commitment has a positive and significant effect on employee

performance. Therefore, the hypothesis for relationship of organizational

commitment to auditor performance as follows.

H1 : Organizational Commitment positively effecting auditor performances

2.3.2 Relationship of Self – Efficacy to Auditor Performances.

Self-efficacy is a perception or belief about individual ability. Employee

who have high self-efficacy will be able to achieve certain goals. They will also try

to set other goals higher. Self-efficacy is a person's belief that he can carry out a

task at a certain level, which affects personal activities towards achieving goals

(Bandura, 1986)Based on that employee going to work harder and more to achieve

significant result. It is in line with the result of (Afifah, U., 2015) and (Stjakovic &

Luithans, 1998) that stated self-efficacy positively effecting auditor performances.

Therefore, the hypothesis for relationship of self-efficacy to auditor performances

as follow.

H2 : Self – efficacy positively effecting auditor performances

13

2.3.3 Relationship of Time Budget Pressure to Auditor Performances

Time budget pressure is a condition where the auditor are required to be

efficient in using the time allocated and very tight budget constraints (Christina,

2003) However auditor who often having time budget pressure tend to have

disfunctional behavior which effecting the auditor performance as a whole. It is in

line by the research by (Prasista & Priyo Hari Adi, 2007)) as well as (Suwardi,

2010)that stated time budget pressure negatively effecting auditor performance.

Limitation of time will bring a serious problem for auditor to finish the task.

Therefore, the hypothesis for relationship of time budget pressure to auditor

performance as follows.

H3: Time budget pressure negatively effecting auditor performances

pressure

14

CHAPTER III

RESEARCH METHODOLOGY

3.1 Sampling Design

The target population of this study is external auditor who work in public

accounting firm in Jakarta. The sample taken using purposive sampling method.

The purposive sampling method is a nonprobability sampling technique which refer

to non – random sampling. Which mean in choosing sample the researcher will be

considering the criteria and characteristic that will be suitable for the research. Thus,

this sampling technique will give a relevant information to the study.

The type of data that used in this study is primary data. The primary data was

collected through questionnaire using Likert Scale. The source of data is from

external auditor in Jakarta.

In determining the sample size, this study use requirement by (Hair,

Multivariate Data Analysis, 2010) In result each question in the questionnaire, the

researcher must collect five respondents. This study consists of independent

variable and dependent variable with total 25 questions. As required by (Hair,

Multivariate Data Analysis, 2010) that the minimum sample of research is 100

respondents.

3.2 Operational Definition of Variables

3.2.1 Independent Variable

This study use commitment, self-efficacy, and time budget pressure as

independent variables. The first one is to measure commitment variable. The

15

researcher used six items statements which adopted from (Shankar, 1996). One of

item include was “I am proud to be a part of this organization”. Five items Likert

scale were used in this research ranging from 1 = strongly disagree to 5 = strongly

agree.

Second, to measure the self- efficacy variable.The researcher used eight items

statements which adopted from (Gilad Chen, 2001). One of the item include was

“I will be able to achieve most of the goals that I have set for myself”. Five items

Likert scale were used in this research ranging from 1 = strongly disagree to 5 =

strongly agree.

Third, to measure the time budget pressure. The researcher used three items

statements which adopted from (McNair, 1991). One of the item include was “I

have to put in longer hours than others to complete the same number of tasks”. Five

items Likert scale were used in this research ranging from 1 = strongly disagree to

5 = strongly agree.

3.2.2 Dependent Variable

This study use auditor performance as the dependent variable. To measure

auditor performance, the researcher used eight items statements which adopted

from external evaluation KPMG (2015). “The external audit firm has a strong

reputation” was one of the items. In measuring this variable, the researcher also

used five items Likert scale ranging from 1 = strongly disagree to 5 = strongly agree.

3.3 Research Instrument

16

This study use survey method for collecting data. This method uses

questionnaire that will be filled by respondents through the google form. This

questionnaire is divided into two section. The first section of the questionnaire

consists of questions about the variable that measured using 5 Likert scale. Variable

of organizational commitment consists of six questions. Variable of self – efficacy

consists of eight questions. Variable of time budget pressure consists of three

questions. Variable of auditor performance consist of eight questions. The list of

questionnaire can be seen in the appendices. Then the second section is a typical

questions for personal respondents. It is include demographic data such as age,

gender, workplace, and positions. Thus the total questions are 25 item. The

questionnaire is distributed via web-survey.

Since all population of this study is located in Jakarta and to create more

convenience and understanding to the respondents. The questionnaire is presented

in two language which are Indonesian and English. To avoid bias response.

Moreover, in order to improve the questionnaire and avoid some errors. The

researcher conduct a pilot test to ten students that have been internship in public

accounting firms in President University. The pilot test was expected to ensure that

the statements presented were easy to understand since the researcher got several

feedbacks after conducting the pilot test. The feedbacks received in the pilot test

were used by the researcher to revise the translation of the question so the sample

can understand more while filling the questionnaire. Thus, the real questionnaire is

ready to be distributed and answered by the respondent.

17

3.4 Statistical Analysis

The researcher used Structural Equation Modeling (SEM) with Partial Least

Squares (PLS) in running the data. (Hair, 2013) stated using SEM-PLS as statistical

tools is quite significant. According to (Sarstedt, 2014) SEM able to handle

complex constructs and suitable to a small sample size. Since this research

conducted only with small sample size. The researcher used SEM-PLS to run the

data. The software used is Warp PLS software (Version 3.0). The first step to use

the Warp PLS is create the file project which come from the excel file. The second

step is to read the raw data for analyzing SEM, as we have to make sure that the

excel file consist only of 1 worksheet that contain the raw data. Furthermore, the

next step is pre-process data for analyzing the SEM. This step is to ensure that the

sample size is not too small and to avoid the sample being repeated in the same

values. As we passed the fourth step, we proceed to determine the SEM model. The

SEM model consist of variable latent that is filled with the direct link. Since this

research did not use any mediating variable, all of the independent variable are

directly connected with the direct link to dependent variable. Moreover, the last step

is to run the SEM analysis and finally we can see the output. On this step we are

able to see many important result such as output latent variable, output combine

loading and cost loading, output correlation among latent variable, pls result and

hypothesis checking. As the further information the output may be seen on the

Chapter IV. Thus, it is important also to determine some information regarding the

research word terminology.

18

A.Convergent Validity

Convergent validity is a tool to measure the conformity between the

attributes of measurement result of measuring instruments and theoretical concepts

that explain the existence of attributes of the variables. Convergent validity is

assessed based on the correlation between items score that can be seen from loading

factor. The minimum of loading factor should be 0.50, where if the value below

0.50 then the loading should be dropped. The loading with value 0.70 will be

categorized as an ideal value.

B.Discriminant Validity

Discriminant validity refers to the incompatibility between the attributes

that should not be measured by measuring instruments and theoretical concepts

about the variables. Discriminant can be seen from comparing the square root of

AVE to the other construct. The rules is the square root of AVE should be higher

compare to other construct.

c. Composite Reliability and Cronbach Alpha

Composite reiliability and cronbach alpha can be seen from the software

application where we need to open the view latent variable coefficients. It is provide

an ouput where the value of composite reliability and cronbach alpha should reach

at least 0.70 as their minimum standard. If the construct met the minimum standard

then the construct consider as reliable.

19

d. Hypothesis Testing

Hypothesis testing is used to determine the correlation between the independent

variable into the dependent variable. The hypothesis testing can determine

supported or not supported the hypothesis itself. This testing can be seen from path

analysis table.

20

CHAPTER IV

RESULT ANALYSIS, DISCUSSION AND IMPLICATION

4.1 Respondent Profile

More than 800 questionnaires distributed to professional in public

accounting firms from Indonesia to fill-in web-based survey. 215 professionals or

26.87% who filled-in the questionnaires came from various public accounting firms

in Jakarta. Among 215 respondents, 45.58% are professional came from big 4

public accounting firms, and 53.95% came from non-big 4 public accounting firms.

The genders of the respondents were 51.16% of male and 48.84% was female.

Professionals who aged between 22-26 years old are the majority of the respondents

which is 86.98%. Among these respondents, 3.26% of respondents had working

experience more than seven years, 7.44% had five to seven years working

experience, 40.47% had two to four years working experience, and 48.37% had less

than one year working experience. Demographics of respondent profile are

presented in Table 1 below.

21

Table 1. Demograhpic Data

% of

respondens

Gender Male 51,16%

Female 48,84%

Groups of Age 22-26 86,98%

27-31 9,77%

32-36 1,86%

37-41 0,93%

> 42 years 0,00%

Public Accounting Firm Big 4 45,58%

Non Big 4 53,95%

Working Experience < 1 year 48,37%

2-4 year 40,47%

5-7 year 7,44%

> 7 years 3,26%

4.2 Descriptive Analysis

Table 2 present the mean, standard deviation and correlation between

variable into another variable. The mean value for each variable such organizational

commitment ( OC), self –efficacy (SE), budget time pressure (BTP), and auditor

performances (AP) are nearly 4.00. It concludes that auditors in Jakarta are satisfied

with their organizational commitment, self – efficacy, time budget pressure, and

auditor perfromance. Table 2 also shown the two main independent variable

positively influence the auditor performance. Furthermore, another one

22

independent variable negatively influence the auditor performance. Respectively

with result of orgaizational commitment (r =0.39, p <0.01) and self – efficacy (r

=0.36, p <0.01), and time budget pressure (r = -0.21, p <0.01).

Table 2. Descriptive Statistics and Correlation

Latent Variable Mean SD OC SE TBP AP

Organizational Commitment 3.95 0.85

Self – Efficacy 3.92 0.77

Time Budget Pressure 3.91 0.86

AP 4.03 0.73 0.39 0.36 -0.21

Validity and Reliability Test

Before testing the hypotheses the researcher should measure the variable

passed of the validity and reliability tests. The test of validity and reliability is use

to test the construct validity there are a type of it which are convergent validity and

discriminant validity. The test of convergent validity is the test that included some

of indicator which is reliability, factor of loading, Average Variance Extracted

(AVE). The minimum range of loading is between 0.50 and 0.70 as a result then

the convergent validity is considered reached (Hair, 2013). Due to the criteria, the

researcher dropped one construct from budget time pressure because the loading

less than the minimum standard. The loading was 0.497 so it does not meet the

minimum standard. The table can be seen in the appendices. The time budget

pressure originally consist of three questions. The researcher decided to eliminate

23

the first out of three questions. The question being eliminate is “I have to put in

longer hours than others to complete the same number of tasks”. Consequently all

the results can be shown in Table 3. Along with 24 items, 18 items had the factor

loadings greater than 0.7 and 6 items had the loading exceeding 0.5 all of the

indicators have met the acceptable standard of AVE which is above 0.5. In sum, all

evidence above indicated that the convergent validity of the measurement model

had qualified.

For measuring the reliability, according to (Sholihin & Ratmono, 2013)there

are two measurements for reliability which are cronbach alpha and composite

reliability. According to (Hair, 2013) the accpetable standard for cronbach alpha

and composite reliability is above 0.70. Furthermore the cronbach alpha and

composite reliability of organizational commitment is 0.878 and 0.908. As well as

the cronbach alpha and composite reliability of self – efficacy which is 0.887 and

0.911. Next, the cronbach alpha and composite reliability of auditor performance

which is 0.858 and 0.890. Lastly, the cronbach alpha and composite reliability of

time budget pressure which is 0.708 and 0.873. Therefore the organizational

commitment, self – efficacy, auditor performance and time budget pressure has met

the minimum standard.

24

Table 3. Convergent and Reliability Test

Items Mean SD Loading

Organizational Commitment ( AVE = 0.623; CA = 0.878 CR=

0.908 )

I am proud to be a part of this accounting firm 4,15 0,81 0.840

I enjoy discussing the accounting firm with people outside 3,92 0,85 0.722

I really care about the fate of this accounting firm 3,62 0,90 0.780

I am glad that I choose to work for this accounting firm 3,97 0,86 0.828

I will be able to achieve most of the goals that I have set for myself 3,97 0,84 0.784

When facing difficult tasks, I am certain that I will accomplish them 4,06 0,73 0.775

Self -Efficacy ( AVE = 0.563; CA = 0.887 CR= 0.911)

In general, I think I can obtain outcomes that are important to me 4,12 0,65 0.599

I believe I can succeed at most any endeavor to which I set my mind 4,20 0,66 0.759

My values are similar to these accounting firm 3,63 0,88 0.800

I am willing to put extra effort beyond expected to make this

accounting firm successful

3,67 0,89 0.776

I will be able successfully overcome many challenges 4,12 0,67 0.766

I am confident that I can perform effectively on many different task 4,09 0,67 0.828

Compared to other people, I can do most tasks very well 3,71 0,75 0.687

Even when things are tough, I can perform quite well 3,83 0,71 0.763

Auditor Performances ( AVE = 0.503; CA = 0.858 CR= 0.890 )

I think my accounting firm has a strong reputation 4,14 0,87 0.690

I think my accounting firm has a strong internal quality control in

place

3,95 0,92 0.682

I have appropriate qualifications on my role 4,04 0,65 0.737

I have to put in longer hours than others to complete the same

number of tasks

3,14 1,09 0.670

25

After measuring reliability and validity test the researcher proceed to

assessing the discriminant validity. Discriminant validity was measured through

comparing the square root of AVE to the correlation among latent variables.

According to (Fornell & Larcker, 1981) stated that discriminant validity is fulfilled

if the value square root of AVE is higher than the correlation between other latent

variable in the same column. The square root number is painted with the bold

colour. The square root of organizational commitment has a greater result than the

other variable which is 0.789. Likewise the square root of self – efficacy has a

greater result than the other variable which is 0.750. Furthermore the square root of

time budget pressure has a greater result than the auditor performance which is

0880. It is in line according to research of (Hair, 2013)where the square roots of

AVE should be higher than the construct. The correlation among the construct and

I complete most audit tasks faster than a typical auditor with my

level of experience

3,58 0,77 0.751

I usually finish my work within the allocated time budget 3,98 0,69 0.701

I am able to work effectively 4,05 0,69 0.760

I think the audit plan appropriately addresses the areas of higher risk 4,20 0,66 0.677

Budget Time Pressure ( AVE = 0.774; CA = 0.708 CR= 0.873 )

I keep demonstrating a high degree of integrity in dealings with the

audit committee

4,12 0,64 0.880

I believe that audit fee is appropriate give in the scope of external

audit

3,95 0,79 0.880

26

square roots of the AVE can be seen in the diagonal. Hence all the variable met the

requirements of discriminant validity.

Table 4. Discriminant Validity

LatentVariable OC SE TBP AP

1. Organizational Commitment ( OC) 0,789

2. Self - Efficacy ( SE) 0,554 0,750

3. Time Budget Pressure ( TBP ) 0,373 0,693 0,880

4. Auditor Performances ( AP) 0,673 0,726 0,604 0,790

4.3 Structural Model Analysis

To test the result of the hypothesis statements we used structural model

analysis, particularly to examine whether the organizational commitment, self –

efficacy, and time budget pressure affecting the auditor performance. The R-

squared is to measure the relationship between the independent variable towards

dependent variable. According to (Chin, 1998) R- squared with result 0.67 indicate

the model is categorized as good. Here the R – squared of auditor performances

construct is 0.66 which showing the model is almost good or reaching the target.

66% out of 100% have significant impact by organizational commitment, self –

efficacy, and time budget pressure towards auditor performances. The hypothesized

model was shown completely in Figure 2. Meanwhile the Table 5 showing the

27

linkages of each independent variable toward the dependent variable. As the result

all of the three hypothesis were supported. Hence, the path coefficient for the

hypothesis 1 are : 0.39; p <0.01, R2=0.66 . The hypothesis H1 which states the

relationship between the organizational commitment positively influence the

auditor performance is fully supported. Second, the path coefficient for the

hypothesis 2 are : 0.36; p <0.01, R2=0.66 which states the relationship between the

self – efficacy positively influence the auditor performance is fully supported.

Third, the path coefficient for hypothesis 3 are : -0.21; p <0.01, R2=0.66 which state

the relationship between time budget pressure negatively influence the auditor

performance is fully supported. Therefore all of the three hypotesis in this research

was fully supported.

28

Figure 2. Full PLS Model

0,39

0,36

R2 =

0,66

-0,21

Table 5. PLS

Result

Path to

Variable Auditor Performances

Full Model

Organizational Commitment ( OC )

0,39***

Self-Efficacy ( SE ) 0,36***

Time Budget Pressure ( TBP ) -0,21***

R2 0,66

***significant at p<0.01

Organizational Commitment

( OC )

SELF - EFFICACY ( SE )

TIME BUDGET PRESSURE

( TBP )

AUDITOR PEFORMANCES

( AP )

29

4.4 Discussion and Implication

The motivation of this research conducted is to examine the relationship

between the organizational commitment, self – efficacy, and time budget pressure

toward auditor performance. This research did not use any mediating variable to

bridge the independent variable into the dependent variable. The result has

answered the research question and fullfilled the research objectives. As the first

result, the organizational commitment is positively affecting the auditor

performance. This happens because auditor with high professional commitment

will work professionally and work accordance to the audit standard. The higher the

commitment from employee also bring a desire to retain in the accounting firm.

These results support the (Ketchand & Strawser, 2001) where the research examine

various dimensions of professional commitment and shows a positive relationship

between the organizational commitment towards performance. Then the self

efficacy also positively affecting the auditor performance since the higher self

efficacy will lead the auditor able and confidence to finish all the task being given.

Self-efficacy is expected to influence the initiating behavior of individuals to

provide a positive effect on the performmance. This result is similar to the study by

(Takiah, 2012)who also found that higher self –efficacy leads to better audit

performance. Likewise as supported by (Stjakovic & Luithans, 1998)auditor who

are very efficacious would exert to produce sucessfull outcomes. Lastly, the time

budget pressure is negatively affecting the auditor performance because the auditor

tend to fail in managing the schedule to finish the task on time. The time budget

bring an auditors in confusion on how to finish task. Even though they are able to

30

finish on time, yet their final result may not maximum as being expected.The

pressure bring the auditor deal with the efficiency in cost and time. Hence the

auditor will not work effectively to achieve the target. This result is similar to the

study by (Prasista & Priyo Hari Adi, 2007) as well as (Suwardi, 2010)where the

time budget pressure bring a negative impact for auditor toward the performance.

31

CHAPTER V

CONCLUSION, LIMITATION, AND SUGGESTIONS

5.1 Conclusions

The researcher conducted this study to test the effect of organizational

commitment, self – efficacy, and time budget pressure toward the auditor

performance. 215 data were collected from public accounting firm in Jakarta over

web-based survey. This research used SEM-PLS as the statistical analysis tools to

test 3 hypotheses. The outcome of all the hypotheses are supported. The

organizational commitment and self – efficacy positively affecting on the auditor

peformance. Meanwhile the time budget pressure negatively affecting the auditor

performance.

This study contributes to behavioral accounting literatures by examining

the auditors reaction through behavioral factors toward the auditor performance and

even the accounting firm it self. This study demonstrate that bigger organizational

commitment create a satisfaction for the auditor toward the accounting firm. As

the result hypothesis 1 are: 0.39; p <0.01, R2=0.66. Which mean the auditor will be

encourage to achieve a satisfying performance as the same time they will earn more

financial advantages for their outstanding performance. These results support the

(Ketchand & Strawser, 2001) where the research examine various dimensions of

professional commitment and shows a positive relationship between the

organizational commitment towards performance. Furthermore, the self-efficacy

bring an auditor confidence to achieve the goals. As the result of hypothesis 2 are:

32

0.36; p <0.01, R2=0.66. This research proven that higher self-efficacy cause the

auditors achieve the goals and looking for another goals if one is finished. This

result is similar to the study by (Takiah, 2012) who also found that higher self –

efficacy leads to better audit performance. Meanwhile, the time budget pressure

bring the auditor deal with the efficiency in cost and time. Hence the auditor will

not work effectively to achieve the target. This result is similar to the study by

(Prasista & Priyo Hari Adi, 2007) as well as (Suwardi, 2010) where the time budget

pressure bring a negative impact for auditor toward the performance. As the result

of hypothesis 3 are: -0.21; p <0.01, R2=0.66. Thus, the result of this study has

answered the research questions and fulfilled the research objectives.

5.2 Limitation and Suggestions

This research is subjected to several limitations. First, the researcher only

collected 215 data from public accounting firm in Jakarta where it does not reflect

a bigger picture. Therefore, future research should could use a bigger sample size

and try to collect the data from various region around Indonesia. Second, this

research only using four kind of variable and the research model was a direct model.

Perhaps the future research could add more variable particularly for the mediating

variable. Third, the questionaire was sent using web –based survey. Hence, the

future research can send a questionaire directly to the auditor to make it easier to

monitor the response.

33

REFERENCES

Afifah, U. (2015). Pengaruh Role Conflict, Role Ambiguity, Self- Efficacy,

Sensitivitas Etika Profesi terhadap Kinerja Auditor dengan Emotional

Quotient sebagai Variabel Moderating. Jom FEKON, 1-15.

Allen, & Meyer. (1997). Commitment in The Workplace. London: Sage Publication.

Aranya & Ferris. (1984). A Reexamination of Accountant Organizational -

Professional Conflict. Journal of Accounting Literature, 1-15.

Bandura. (1986). The Explanatory and Predictive Scope of Self Efficacy Theory.

Journal of Clinical and Social Psychology, 359-373.

Bandura, A. (1997). Self Efficacy: The Exercise of Control. New York: Freeman.

Baron & Byrne. (2000). Social Psychology. New York: Allyn & Bacon.

Campbell,C. (1998). Psychlogical Climate: Relevance for Sales Manager and

Impact on Concequent Job Satisfication. Journal of Marketing Theory, 27-

37.

Chen. (2011). Job and Career Influences on the Career Commitment of Health Care

Executives. Journal of Health Organization and Management, 693-771.

Chin. (1998). The Partial Least Squares Approach to Structural Equation

Modeling. London: Lawrence Erlbaum Associates.

Christina, S. (2003). Hubungan Tekanan Anggaran Waktu dengan Perilaku

Disfungsional serta Pengaruhnya terhadap Kualitas Audit. Surabaya:

Simponsium Nasional Akutansi.

DeZoort & Lord. (1997). A Review and Synthesis of Pressure Effects Research in

Accounting. Journal of Accounting Literature, 28-86.

Fisher,R.T. (2001). Role Stress, the Type A Behavior Pattern, and External Audito

Job Satisfaction and Performance. Behavioral Research in Accounting, 13-

143.

Fornell & Larcker. (1981). Evaluating Structural Equation Models with

Unobservable Variables and Measurement Error. Journal of Marketing

Research, 39-50.

Ganesan.Shankar.Barton. (1996). The Impact of Staffing Policies on Retail Buyer

Job Attitudes and Behavior. Journal of Retailing, 31-56.

Gilad Chen. (2001). Validation of a new General Self- Efficacy Scale.

Organizational Research Model, 1-4.

34

Grifin. (2004). Manajemen Jilid 1. Jakarta: Gelora Askara Pratama.

Hair. (2010). Multivariate Data Analysis. New Jersey: Pearson Prentice Hall.

Hair. (2013). A Primer on Partial Least Square Equation Modelling. Sage

Publication.

Hellriegel, Slocum and Woodman. (2001). Organizational Behavior. Cincinanati:

South- Western College Publishing.

Jemada. (2013). Pengaruh Tekanan Anggaran Waktu, Kompleksitas Tugas dan

Reputasi Auditor terhadap Fee Audit kepada Kantor Akuntan Publik di Bali.

E- Journal Akuntansi Universitas Udayana, 132-146.

Kalbers, & Forgaty. (1995). Professionalism Its Consequences: A Study of Internal

Auditors. Journal of Practice, 64-86.

Kelley,Tim and Seiler,Robert E. (1982). Auditor Stress and Time Budget. The CPA

Journal, 24-34.

Kelly & Margheim. (1990). The Impact of Time Budget Pressure, Personality and

Leadership Variable on Dysfucntional Auditor Berhavior. Journal of

Accounting, 26-38.

Ketchand & Strawser. (2001). Multiple Dimensions of Organizational

Commitment: Implications for Future Accounting Research. Behavioral

Research in Accounting, 221-251.

Luthans. (2002). Organizational Behavior. New York: McGraw-Hill Inc.

Maryati. (2008). Manajemen Perkantoran Efektif. Yogyakarta: Sekolah Tinggi

Ilmu Manajemen YKPN.

Mathis & Jackson. (2006). Human Resource Management: Manajemen Sumber

Daya Manusia. Jakarta: Salemba Empat.

McNair. (1991). The Management Control Dilemma in Public Accounting and Its

Impact on Auditor Behavior, Accounting, Organization, and Society. 635-

653.

Moeheriono. (2009). Pengukuran Kinerja Berbasis Kompetensi. Jakarta: Ghalia

Indonesia.

Prasista & Priyo Hari Adi. (2007). Pengaruh Kompleksitas Audit dan Tekanan

Anggaran Waktu terhadap Kualitas Audit Moderasi Pemahaman terhadap

Sistem Informasi. Jurnal Ekonomi dan Bisnis, 80-126.

Robbins & Judge. (2008). Perilaku Organisasi. Jakarta: Salemba Empat.

35

Sarpariyah. (2011). Pengaruh Good Governance dan Independensi Auditor

terhadap Kinerja Auditor dan Komitmen Organisas. Jurnal Ekonomi Bisnis

dan Perbankan, 19-16.

Sarstedt. (2014). Partial Least Squares Structural Equation Modeling (PLS - SEM):

A usefull tool for Family Business Researchers. Journal of Family Business

Strategy, 90-118.

Shankar, G. &. (1996). The Impact of Staffing Policies on Retail Buyer Job and

Behaviors. Journal of Retailling\, 72.

Sholihin & Ratmono. (2013). Analisis SEM-PLS dengan Wrap PLS 3.0 untuk

Hubungan Nonlinier dalam Penelitian Sosial dan Bisnis. Yogyakarta:

ANDI.

Shome, Anamitra. (1998). Locus of Control and Going - Concern Judgements: The

Mediating Effect of Nondiagnostic Information and Decision Aid

Availability. Journal of Business, 56-64.

Stjakovic & Luithans. (1998). Self - Efficacy and Work - Related Performance: A

Meta - Analysis. Pyschological Bulletin, 240-261.

Sukrisno, A. (2004). Auditing (Pemeriksaan Akuntan) oleh Kantor Akuntan Publik.

Fakultas Ekonomi Universitas Ekonomi Indonesia, 67-73.

Suwardi. (2010). Pengaruh Tekanan Anggaran Waktu dan Kompleksitas Audit

terhadap Kualitas Audit. Yogyakarta: Universitas Atma Jaya Yogyakarta.

Takiah. (2012). Enhancing Auditor Performance: The Importance of Motivational

Factors and The Mediation Effect of Effort. Managerial Auditing Journal,

462-476.

Yeh & Hong. (2012). The Mediating Effect of Organizational Commitment on

Leadership Type and Job Performance. Journal of Human Resources and

Audit Learning, 50-59.

36

Figure 1. Research Model

SELF –

EFFICACY ( SE )

TIME

BUDGET

PRESSURE ( TBP )

AUDITOR

PEFORMANCES ( AP )

Organizational

Commitment

( OC )

37

Figure 2. Direct Effect

0,39

0,36

R2 =

0,66

-0,21

Organizational Commitment

( OC )

SELF - EFFICACY ( SE )

TIME BUDGET PRESSURE

( TBP )

AUDITOR PEFORMANCES

( AP )

38

LIST OF TABLE

Table 1. Demograhpic Data

% of

respondens

Gender Male 51,16%

Female 48,84%

Groups of Age 22-26 86,98%

27-31 9,77%

32-36 1,86%

37-41 0,93%

> 42 years 0,00%

Public Accounting Firm Big 4 45,58%

Non Big 4 53,95%

Working Experience < 1 year 48,37%

2-4 year 40,47%

5-7 year 7,44%

> 7 years 3,26%

39

Table 2. Descriptive Statistics and Correlation

Latent Variable Mean SD OC SE TBP AP

Organizational Commitment 3.95 0.85

Self – Efficacy 3.92 0.77

Time Budget Pressure 3.91 0.86

AP 4.03 0.73 0.39 0.36 -0.21

Table 3. Convergent and Reliability Test

Items Mean SD Loading

Organizational Commitment ( AVE = 0.623; CA = 0.878 CR=

0.908 )

I am proud to be a part of this accounting firm 4,15 0,81 0.840

I enjoy discussing the accounting firm with people outside 3,92 0,85 0.722

I really care about the fate of this accounting firm 3,62 0,90 0.780

I am glad that I choose to work for this accounting firm 3,97 0,86 0.828

I will be able to achieve most of the goals that I have set for myself 3,97 0,84 0.784

When facing difficult tasks, I am certain that I will accomplish them 4,06 0,73 0.775

Self -Efficacy ( AVE = 0.563; CA = 0.887 CR= 0.911)

In general, I think I can obtain outcomes that are important to me 4,12 0,65 0.599

I believe I can succeed at most any endeavor to which I set my mind 4,20 0,66 0.759

My values are similar to these accounting firm 3,63 0,88 0.800

I am willing to put extra effort beyond expected to make this

accounting firm successful

3,67 0,89 0.776

I will be able successfully overcome many challenges 4,12 0,67 0.766

I am confident that I can perform effectively on many different task 4,09 0,67 0.828

40

Compared to other people, I can do most tasks very well 3,71 0,75 0.687

Even when things are tough, I can perform quite well 3,83 0,71 0.763

Auditor Performances ( AVE = 0.503; CA = 0.858 CR= 0.890 )

I think my accounting firm has a strong reputation 4,14 0,87 0.690

I think my accounting firm has a strong internal quality control in

place

3,95 0,92 0.682

I have appropriate qualifications on my role 4,04 0,65 0.737

I have to put in longer hours than others to complete the same

number of tasks

3,14 1,09 0.670

I complete most audit tasks faster than a typical auditor with my

level of experience

3,58 0,77 0.751

I usually finish my work within the allocated time budget 3,98 0,69 0.701

I am able to work effectively 4,05 0,69 0.760

I think the audit plan appropriately addresses the areas of higher risk 4,20 0,66 0.677

Budget Time Pressure ( AVE = 0.774; CA = 0.708 CR= 0.873 )

I keep demonstrating a high degree of integrity in dealings with the

audit committee

4,12 0,64 0.880

I believe that audit fee is appropriate give in the scope of external

audit

3,95 0,79 0.880

41

Table 4. Discriminant Validity

LatentVariable OC SE TBP AP

1. Organizational Commitment ( OC) 0,789

2. Self - Efficacy ( SE) 0,554 0,750

3. Time Budget Pressure ( TBP ) 0,373 0,693 0,880

4. Auditor Performances ( AP) 0,673 0,726 0,604 0,790

Table 5. PLS

Result

Path to

Variable Auditor Performances

Full Model

Organizational Commitment ( OC )

0,39***

Self-Efficacy ( SE ) 0,36***

Time Budget Pressure ( TBP ) -0,21***

R2 0,66

***significant at p<0.01

42

MEASUREMENT SCALE

Organizational Commitment, based on Ganesan (1996)

1. Iam proud to be a part of this organization.

2. I enjoy discussing this organization with people outside it.

3. I really care about the fate of this organization.

4. I am glad that I choose to work for this organization.

5. My values are similar to those of the organization.

6. I am willing to put extra effort beyond expected to make this organization

successful.

Self- Efficacy, based on Gilad Chen (2001)

1. I will be able to achieve most of the goals that I have set for my self.

2. When facing difficult tasks, I am certain that I will accomplish them.

3. In general, I think I can obtain outcomes that are important to me.

4. I believe I can succeed at most any endeavor to which I set my mind.

5. I will be able to successfully overcome many challenges.

6. I am confident that I can perform effectively on many different task.

7. Compared to other people, I can do most task very well.

8. Even when things are tough, I can perform quite well.

Performance, based on KPMG (2015)

1. The external audit firm has a strong reputation.

2. The audit firm has strong internal quality control processes in place.

3. Audit team members have appropriate qualifications for their roles.

4. There is a strong audit team that works together effectively.

5. The audit plan appropriately addresses the areas of higher risk.

6. All communications from the audit team are clear and relevant.

43

7. External audit partners and staff demonstrate a high degree of integrity in their

dealings with the audit committee.

8. The external audit fee is appropriate given the scope of the external audit.

Time Budget Pressure, based on McNair (1991)

1. I have to put in longer hours than others to complete the same number of tasks.

2. I complete most audit tasks faster than a typical auditor with my level of

experience.

3. I usually finish my work within the allocated time budget.