Embed Size (px)

Citation preview

Raj Chetty, HarvardJohn N. Friedman, BrownNathaniel Hendren, HarvardMichael Stepner, University of Torontoand the Opportunity Insights Team

June 2021

The Economic Impacts of COVID-19:

Evidence from a New Public DatabaseBuilt Using Private Sector Data

How has COVID-19 affected the American economy and what policies can best mitigate its adverse impacts going forward?

Since Kuznets (1941), macroeconomic policy decisions have been based on data from surveys of households and businesses

These data provide vital aggregate information (GDP, unemployment rates), but have two key limitations

1. Some statistics available only at low frequencies, often with significant lags

2. Some statistics cannot be disaggregated to examine variation across areas or subgroups

Motivation: Measuring the Impacts of COVID-19

We build a publicly available economic tracker using transaction data from several private companies to measure daily economic activity by ZIP code, income group, and industry

Use these new data to analyze economic impacts of COVID-19 pandemic:

1. [Mechanisms] Why did COVID-19 lead to unprecedented job losses?

2. [Policy Responses] Causal effects of fiscal stabilization policies enacted to date

This work serves as a prototype motivating further development in collaboration with federal statistical agencies

This Project

Data Construction

DataCase Study:

StimulusImpacts of COVID-19

Consumer Spending

Small Business Revenues

Employment

Job Postings

Education

Data Partners

Starting from raw data, construct series suitable for economic analysis as follows:

1. Clean series to remove artifacts that arise in transaction data

2. Smooth seasonal fluctuations using data from 2019

3. Protect privacy: index to January 2020 values, exclude small cells, combine data from multiple companies

4. Benchmark to national statistics to characterize group each dataset represents to mitigate bias from non-representative selection

Constructing Publicly Available Economic Indices Based on Private-Sector Data

-50

-40

-30

-20

-10

0

10

Cha

nge

in E

mpl

oym

ent v

s. J

anua

ry 2

020

(%)

Jan2020

Feb2020

Mar2020

Apr2020

May2020

Jun2020

Jul2020

Aug2020

Sep2020

Oct2020

Nov2020

Dec2020

Jan2021

Feb2021

Mar2021

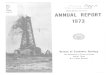

Low-Income (Unadjusted) CPS Low-Income

Pooled (Unadjusted) CPS Pooled

National Employment Trends (Paychex, Intuit, Earnin)Tracker vs CPS

-50

-40

-30

-20

-10

0

10

Cha

nge

in E

mpl

oym

ent v

s. J

anua

ry 2

020

(%)

Jan2020

Feb2020

Mar2020

Apr2020

May2020

Jun2020

Jul2020

Aug2020

Sep2020

Oct2020

Nov2020

Dec2020

Jan2021

Feb2021

Mar2021

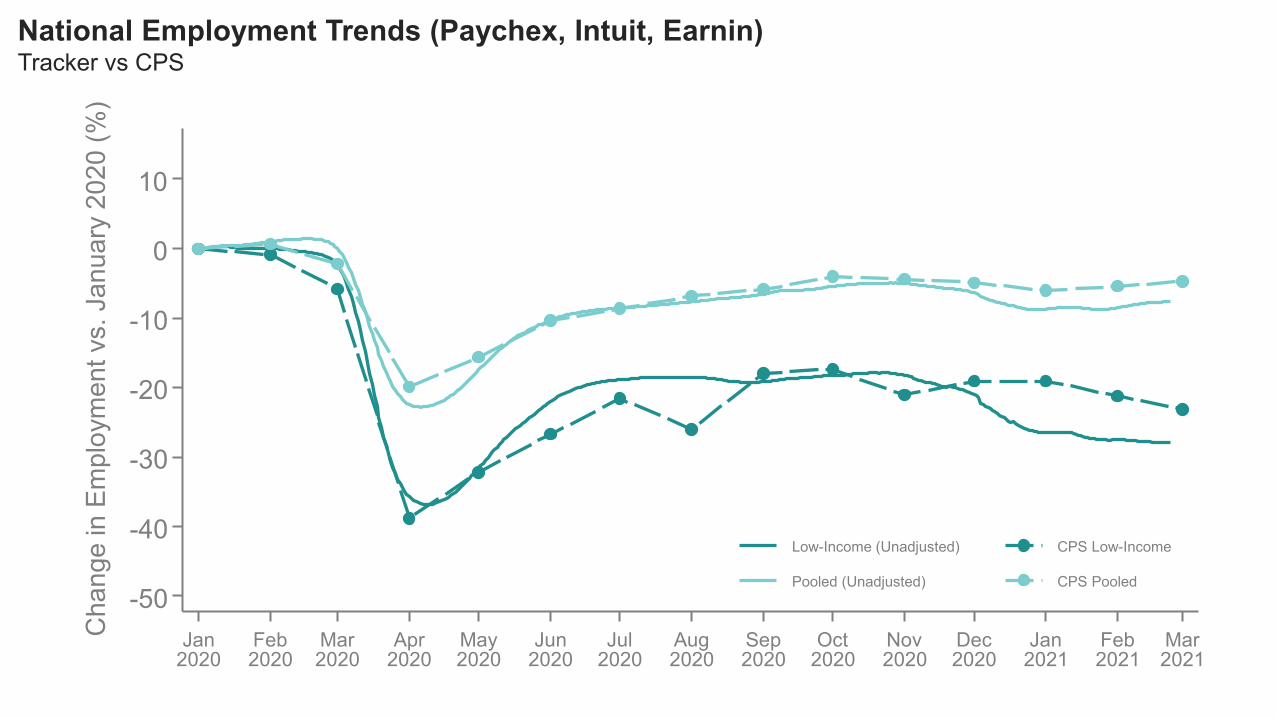

Q1 Q2

Employment Trends - California

-50

-40

-30

-20

-10

0

10

Cha

nge

in E

mpl

oym

ent v

s. J

anua

ry 2

020

(%)

Jan2020

Feb2020

Mar2020

Apr2020

May2020

Jun2020

Jul2020

Aug2020

Sep2020

Oct2020

Nov2020

Dec2020

Jan2021

Feb2021

Mar2021

Low-Income (Unadjusted) CPS Low-Income

Pooled (Unadjusted) CPS Pooled

National Employment Trends (Paychex, Intuit, Earnin)Tracker vs CPS

-50

-40

-30

-20

-10

0

10

Cha

nge

in E

mpl

oym

ent v

s. J

anua

ry 2

020

(%)

Jan2020

Feb2020

Mar2020

Apr2020

May2020

Jun2020

Jul2020

Aug2020

Sep2020

Oct2020

Nov2020

Dec2020

Jan2021

Feb2021

Mar2021

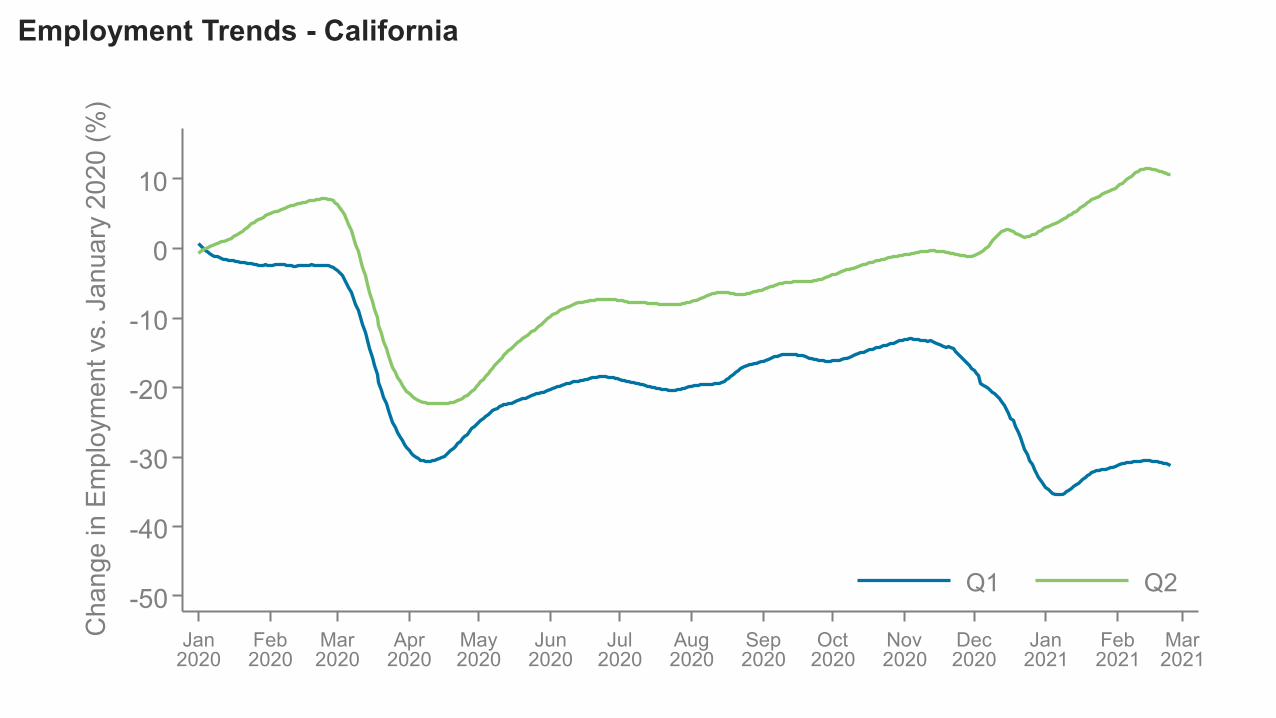

Low-Income (Unadjusted) CPS Low-Income Low-Income (Adjusted)

Pooled (Unadjusted) CPS Pooled Pooled (Adjusted)

National Employment Trends (Paychex, Intuit, Earnin)Tracker vs CPS

Impacts of COVID-19

DataCase Study:

StimulusImpacts of COVID-19

-$1.73T

0

-.4

-.8

-1.2

-1.6

-2

Cha

nge

in R

eal G

DP

from

Q1

2020

to Q

2 20

20(in

trilli

ons

of c

hain

ed 2

012

dolla

rs)

GrossDomesticProduct

National Accounts Data: Changes in GDP and its Components

(-31.7%)

$0.04T $0.05T

-$1.73T

-$0.47T

-$1.35T

0

-.4

-.8

-1.2

-1.6

-2

Cha

nge

in R

eal G

DP

from

Q1

2020

to Q

2 20

20(in

trilli

ons

of c

hain

ed 2

012

dolla

rs)

GrossDomesticProduct

PrivateDomestic

Investment

Govt.Expend.

NetExports

PersonalConsumption

Expend. (PCE)

National Accounts Data: Changes in GDP and its Components

(-31.7%)

$0.04T $0.05T

-$1.73T

-$0.47T

-$1.35T

-$1.03T

(-31.7%)

0

-.4

-.8

-1.2

-1.6

-2

Cha

nge

in R

eal G

DP

from

Q1

2020

to Q

2 20

20(in

trilli

ons

of c

hain

ed 2

012

dolla

rs)

GrossDomesticProduct

PrivateDomestic

Investment

Govt.Expend.

NetExports

PersonalConsumption

Expend. (PCE)

Credit CardSpendingin PCE

National Accounts Data: Changes in GDP and its Components

2019 Top Income Quartile 2020 Top Income Quartile

$-0.7 Billion(-7.3%)

2

4

6

8

10

Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1

$-3.1 Billion(-37.5%)

Consumer Spending by Income QuartileC

onsu

mer

Spe

ndin

g Pe

r Day

($ B

illion

s)

2019 Top Income Quartile 2020 Top Income Quartile2019 Bottom Income Quartile 2020 Bottom Income Quartile

$+0.2 Billion(+4.5%)

$-0.7 Billion(-7.3%)

2

4

6

8

10

Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1

$-1.0 Billion(-26.7%)

$-3.1 Billion(-37.5%)

Consumer Spending by Income QuartileC

onsu

mer

Spe

ndin

g Pe

r Day

($ B

illion

s)

Changes in Small Business Revenues from January to April by ZIP CodeSan Francisco

Changes in Small Business Revenues vs. Rent, by ZIP CodeFrom January to April 2020

Slope = -13% per $1000 (s.e. = 0.38)-60%

-50%

-40%

-30%

-20%

$500 $1,000 $1,500 $2,000

Median Two Bedroom Monthly Rent in 2018

Change in Small Business RevenueRelative to January

Top Income Quartile

Third Quartile

Second Quartile

Bottom Income Quartile

Apr 15 June 10 Apr 1

-24%(7.6m)

-8%(2.6m)

-1%(0.3m)

2%(-0.7m)

-35%(11.2m)

-24%(7.7m)

-17%(5.5m)

-11%(3.7mjobs lost)

-22%(7.0m)

-12%(3.8m)

-6%(2.0m)

-1%(0.2m)

-40%

-30%

-20%

-10%

0%

Cha

nge

in E

mpl

oym

ent (

%)

Rel

ativ

e to

Jan

uary

202

0

Jan 1 Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1 Jan 1 Feb 1Mar 1 Apr 1 May 1

Employment Changes by Income Quartile

29.0%

-60%

-40%

-20%

0%

20%

40%

60%

80%C

hang

e R

elat

ive

to J

anua

ry 2

020

(%)

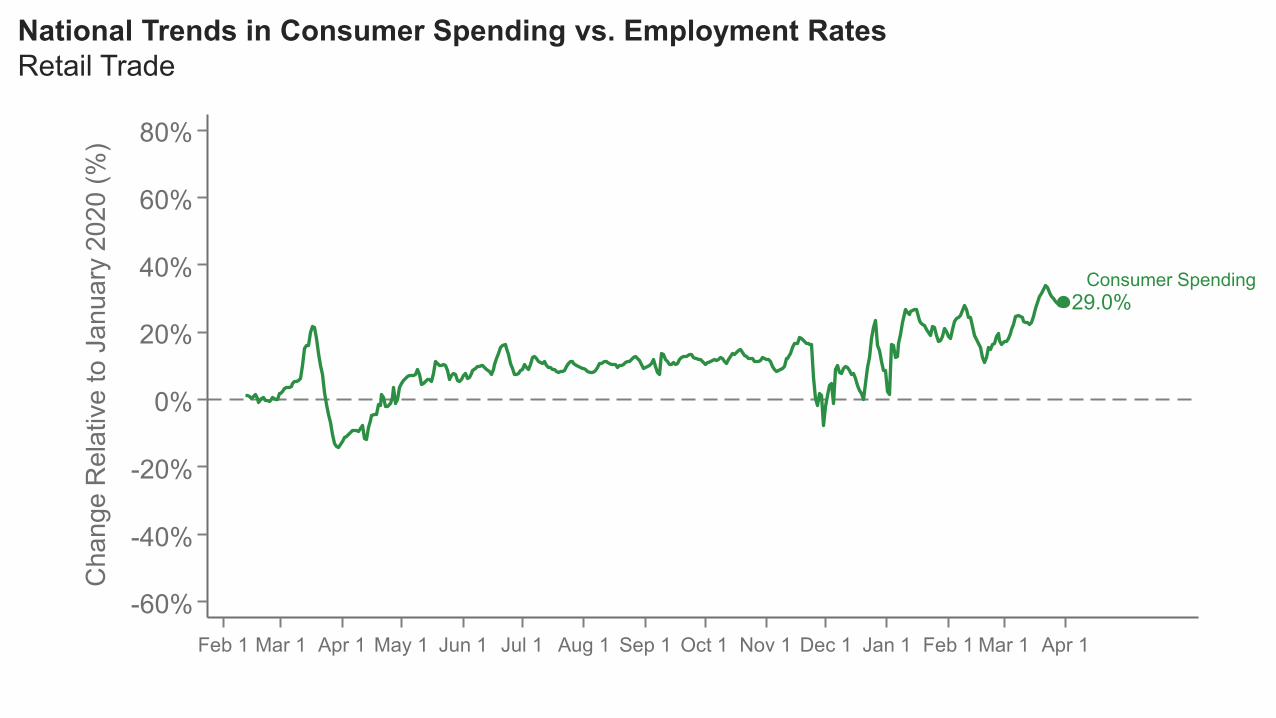

Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1 Jan 1 Feb 1 Mar 1 Apr 1

National Trends in Consumer Spending vs. Employment RatesRetail Trade

Consumer Spending

6.4%

-14.8%

29.0%

-60%

-40%

-20%

0%

20%

40%

60%

80%C

hang

e R

elat

ive

to J

anua

ry 2

020

(%)

Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1 Jan 1 Feb 1 Mar 1 Apr 1

National Trends in Consumer Spending vs. Employment RatesRetail Trade

Consumer Spending

Top Wage QuartileEmployment

Bottom Wage QuartileEmployment

6.4%

-14.8%

29.0%

62.6%

-60%

-40%

-20%

0%

20%

40%

60%

80%C

hang

e R

elat

ive

to J

anua

ry 2

020

(%)

Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov 1 Dec 1 Jan 1 Feb 1 Mar 1 Apr 1

National Trends in Consumer Spending vs. Employment RatesRetail Trade

Consumer Spending

Top Wage QuartileEmployment

Bottom Wage QuartileEmployment

Minimum Req.’sJob Postings

Effects of Stimulus Payments

DataCase Study:

StimulusImpacts of COVID-19

Coronavirus Aid, Relief, and Economic Security (CARES) Act of April 2020

$1200 checks (phased out at higher incomes, supplement for children)

April 15, 2020 deposits for the majority of payments

Coronavirus Response and Relief Act of December 2020

$600 checks (phased out at higher incomes, supplement for children)

January 4, 2021 or January 6, 2021 deposits for the majority of payments

Were stimulus payments effective in increasing consumer spending?

Estimating the Effects of Stimulus Payments

4th 7th 10th 13th 4th 7th 10th 13th 16th 19th

December January

Consumer SpendingSeasonally Adjusted

Spending Increased 7.9 p.p.(s.e. = 2.2 p.p)

$600 Stimulus ChecksDisbursed on Jan 4

Effect of the January 2021 Stimulus Checks on Daily Consumer Spending

–10 p.p.

0 p.p.

+10 p.p.

+20 p.p.

+30 p.p.

Bottom Income Quartile ZIP CodesMedian Household Income < $46,000

holidayspermutation

December January4th 7th 10th 13th 4th 7th 10th 13th 16th 19th

December January

Consumer SpendingSeasonally Adjusted

4th 7th 10th 13th 4th 7th 10th 13th 16th 19th

Spending Increased 7.9 p.p.(s.e. = 2.2 p.p)

Spending Increased 0.2 p.p.(s.e. = 1.6 p.p)

$600 Stimulus ChecksDisbursed on Jan 4

$600 Stimulus ChecksDisbursed on Jan 4

Effect of the January 2021 Stimulus Checks on Daily Consumer Spending

–10 p.p.

0 p.p.

+10 p.p.

+20 p.p.

+30 p.p.

–10 p.p.

0 p.p.

+10 p.p.

+20 p.p.

+30 p.p.

Bottom Income Quartile ZIP CodesMedian Household Income < $46,000

Top Income Quartile ZIP CodesMedian Household Income > $78,000

holidayspermutation

$126$140

$90

$45

0

50

100

150

200

COVID Relief Act (January 2021)

Consumer SpendingEstimate of 1-monthspending per $600

Effect of the COVID Stimulus Bills on Spending, by Income Group

<$46,000 $46,000 to $59,000 $59,000 to $78,000 >$78,000

ZIP Code Median Household Income

$189

$225 $229 $235

$126$140

$90

$45

0

50

100

150

200

CARES Act (April 2020)

COVID Relief Act (January 2021)

Consumer SpendingEstimate of 1-monthspending per $600

Effect of the COVID Stimulus Bills on Spending, by Income Group

<$46,000 $46,000 to $59,000 $59,000 to $78,000 >$78,000

ZIP Code Median Household Income

$0

$1000

$2000

$3000

$4000

January 12020

Mar 15 Apr 15 December 312020

Top Quartile

$2,500

$2,000

$1,300

Estimated Cumulative Increase in SavingsSavings = Earnings + Unemployment Insurance + Stimulus Checks – Spending

Δ Savings Per Personcompared to 2019

$4,000

Bottom Quartile

Q3

Q2

Aug 1

January 2021Stimulus Policy

Projected Effect of Stimulus Checks on SpendingCouple with No Children

$600

$0 $150,000 $174,000$75,000

$1400

$0 $150,000 $200,000$75,000

Household Income

March 2021Stimulus Policy

Proposal

January 2021Stimulus Policy

Projected Effect of Stimulus Checks on SpendingCouple with No Children

$600

$0 $150,000 $174,000$75,000

$1400

$0 $150,000 $200,000$75,000

Household Income

March 2021Stimulus Policy

Proposal

Fiscal cost = $200 billion

Projected 1-month spendingincrease < $15 billion

January 2021Stimulus Policy

Projected Effect of Stimulus Checks on SpendingCouple with No Children

$600

$0 $150,000 $174,000$75,000

$1400

$0 $160,000 $200,000$75,000

Household Income

March 2021Stimulus Policy

$20 billionreallocated

1. Research: we hope these new public data (www.tracktherecovery.org) will be helpful in supporting future work in this recession and beyond

2. Policy: fine tuning based on state of the economy and observed policy impacts

Help target proposed $100 billion in job re-training programs, avert jobless recovery

3. Contribute to Economic Statistics

On-going collaboration with federal statistical agencies using these data to improve existing methodologies and develop new statistics

Broader Implications and Future Work

Appendix

Consumer Spending BenchmarkingCredit/Debit Card Data (Affinity Solutions) vs. National Accounts (Advance Monthly Retail Trade Survey)

Change in Consumer SpendingRelative to January

Retail

-50%

-25%

0%

+25%

+50%

January2019

April July October January2020

April July October January2021

Affinity

NationalAccounts

Affinity

NationalAccounts

Food and Accommodation

In-PersonServices (68%)

In-PersonServices: (33%)

0%

25%

50%

75%

100%

Share of Decline(Jan to Mar 25-Apr 14)

Share of Pre-COVID Spending

Remote Services

Health Care

Transportation

Hotels & Food

Durable Goods

Non-Durable Goods

Recreation

Other In-Person Services

Health Care

Remote Services

Recreation

Transportation

Hotels & Food

Durable Goods

Non-Durable Goods

Other In-Person Services

Change in Consumer Spending by Sector

58.6%

44.3%

19.5%13.3%

67.2%

-2.9%0%

25%

50%

75%Sh

are

of P

eak

to T

roug

h D

eclin

e in

Pe

rson

al C

onsu

mpt

ion

Expe

nditu

re (%

)

Durables Non-Durables Services

Great Recession COVID-19

Change in Consumer Spending by SectorCOVID vs Great Recession

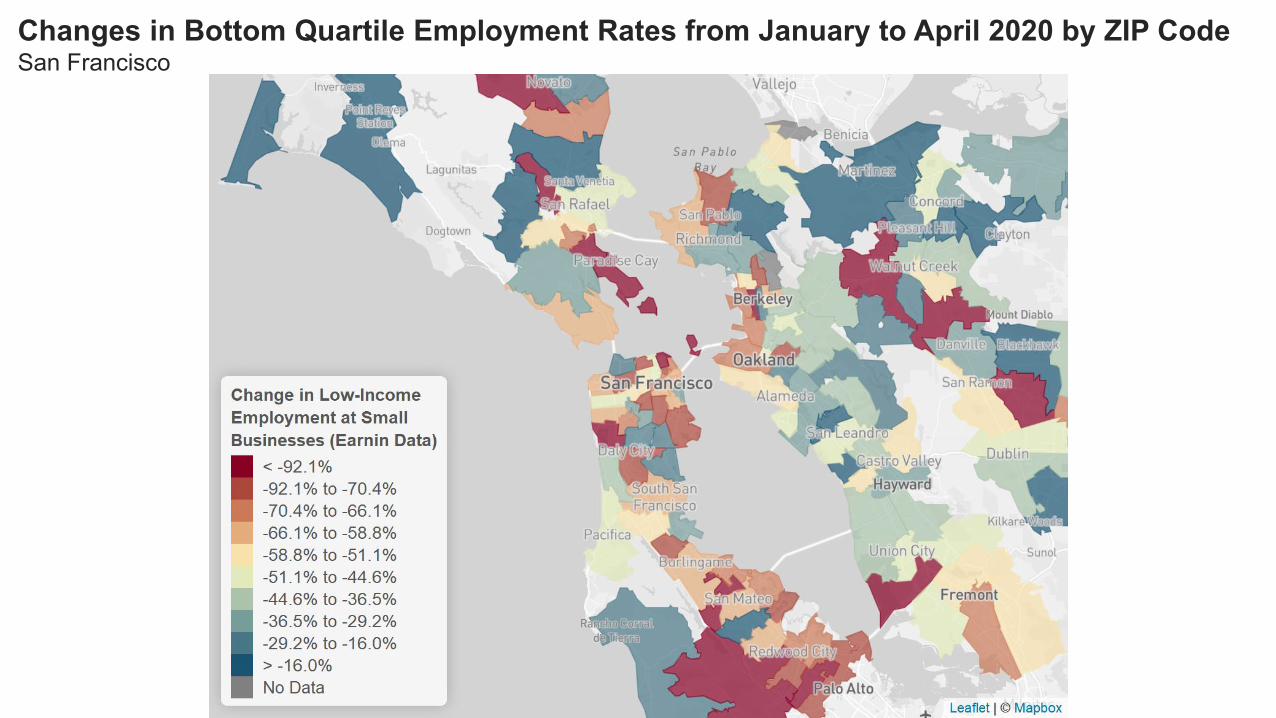

Changes in Bottom Quartile Employment Rates from January to April 2020 by ZIP CodeSan Francisco

CARES Act also provided $500 billion in loans to small businesses starting on April 3

Loans were forgivable if payroll was not reduced significantly relative to pre-COVID levels

Firms with fewer than 500 employees were eligible for these loans (with some exceptions)

Paycheck Protection Program

PPP Program BeginsApril 3

Estimated Effect to August 15:1.78 p.p. (s.e. = 1.99 p.p.)

501-800 Employees (ineligible)

100-500 Employees (eligible)

-25%

-20%

-15%

-10%

-5%

0%

Cha

nge

in E

mpl

oym

ent (

%)

Rel

ativ

e to

Jan

uary

202

0

Feb 15 Mar 15 Apr 15 May 15 Jun 15 Jul 15 Aug 15 Sep 15

Impact of Paycheck Protection Program on EmploymentReweighted to Match Industries (Excl. Food Services), with NAICS x County x Income Quartile FEs

-25%

-20%

-15%

-10%

-5%

0%

Cha

nge

in E

mpl

oym

ent (

%)

Rel

ativ

e to

Jan

uary

202

0

Feb 15 Mar 15 Apr 15 May 15 Jun 15 Jul 15 Aug 15 Sep 15

Impact of Paycheck Protection Program on EmploymentReweighted to Match Industries (Excl. Food Services), with NAICS x County x Income Quartile FEs

Cost Per Job Saved = $377K($119K at lower bound of 95% CI)

501-800 Employees (ineligible)

100-500 Employees (eligible)

PPP Program BeginsApril 3

Estimated Effect to August 15:1.78 p.p. (s.e. = 1.99 p.p.)

Why has PPP had limited impact on employment despite substantial expenditure?

Businesses who took up loans may not have intended to lay off their workers to begin with

Ex: very high take-up rate among firms providing professional and scientific services despite low job losses in that sector

Consistent with evidence that loans flowed to areas with smaller employment losses in March [Granja, Makridis, Yannelis, Zwick 2020]

Paycheck Protection Program