Embed Size (px)

Citation preview

OXFORD INSTITUTE

E N E R G Y STUDIES

- FOR-

The Economic Consequences of the Fall in

Future Energy Demand in the Arab World

Robert Mabro

Oxford Institute for Energy Studies

F4

1985

THE ECOHCMIC COHSEQUERCES OF TEE F U IB FUTWE EBBBGY DIMBaD Il? THE ARAB WORLD

Paper presented a t the Third Arab Energy

Conference, 4-9th May 1985, Algiers.

Also, published in the Middle East Economic Survey, 13 t h Hay 1985,

Vol. mIII, no. 31

F4

OxPOBD IBISTITTRE FOR ENERGY STUDIES

1985

The contents of this paper are for the purposes of study and d i s c u s s i o n and do not represent the views of the Oxford Institute for Energy Studies or any of its members.

Copyright 0 1984 Oxford I n s t i t u t e for Energy Studies

ISBN 0 948061 09 X

TAELE OF CORTERTS

1. INTRODUCTION

2. THE OIL DEMAND SHOCK

3 . THE OIL DEMAND AND O I L PRICES I N 1985-1990 13

4. THE CASE FOR FAVOURABLE IMPLICATIONS 20

5 . TBE UNFAVOURABLE IMPLICATIONS 28

6 . CONCLUDING REMARKS 32

F

TABLES

Table 1 Oil Production i n Major Arab Oil-Export ing Countries

2 O i l Revenues of Arab OPEC Member Countries

3 Rates of Growth of Main Economic Indicators

10

14

31

The economic development of t he Arab r eg ion i n r ecen t

years has become h e a v i l y dependent on the fo r tunes of o i l . The

sudden and s i g n i f i c a n t i n c r e a s e s in o i l p r i c e s and r e v e n u e s of

1973/74 and 1979180 have had a cons ide rab le impact on t h e l e v e l s

and p a t t e r n s of economic development i n the o i l - expor t ing and i n

the non-oil coun t r i e s of t he Arab world.

The o i l e x p o r t e r s a c h i e v e d h i g h r a t e s o f economic

growth , and some of them, p a r t i c u l a r l y t h e Gulf c o u n t r i e s and

Libya enjoyed the b e n e f i t s of h igh l e v e l s of per c a p i t a incomes.

O i l was r e s p o n s i b l e f o r fundamental changes i n the s t r u c t u r e of

t h e i r economies and the c h a r a c t e r i s t i c s of t h e i r s o c i e t i e s .

The economies became i m p o r t - o r i e n t e d , a d e v e l o p m e n t

which induced a c o n s i d e r a b l e e x p a n s i o n of t h e s e r v i c e s s e c t o r ,

a n d a v i r t u a l a n n i h i l a t i o n o f t r a d i t i o n a l a c t i v i t i e s i n

a g r i c u l t u r e , f i s h e r i e s , h a n d i c r a f t s , s m a l l - s c a l e t r a d i n g and

manufacturing. Governments were a b l e t o devote huge r e sources t o

investment and a s p e c i f i c p a t t e r n of c a p i t a l format ion began t o

emerge. Much money was spent on t h e t r a n s p o r t i n f r a s t r u c t u r e , on

t e l e c o m m u n i c a t i o n s , h o u s i n g , and on s o c i a l s e r v i c e s , m a i n l y

educat ion and hea l th . Some coun t r i e s were unable t o absorb a l l

o f t h e i r r e v e n u e s d o m e s t i c a l l y , and p l a c e d s u r p l u s f u n d s i n

1

p o r t f o l i o s of fo re ign assets h e l d abroad. Product ive investments

i n t h e d o m e s t i c economy t ended t o b e c o n c e n t r a t e d i n t h e heavy

indus t ry s e c t o r , mainly i n t he process ing of hydrocarbons and i n

energy-intensive metal i n d u s t r i e s .

O i l revenues f i l t e r e d through government expendi tures

t o the p r i v a t e sec tor . A v a r i e t y of r e d i s t r i b u t i o n mechanisms - con t rac t s , high-wage government employment, purchases and g i f t s

of land , ex tens ion of c r e d i t f a c i l i t i e s a t low o r ze ro r a t e s of

i n t e r e s t e t c . - l ed t o the c r e a t i o n of p r i v a t e fo r tunes .

Rapid economic d e v e l o p m e n t and h i g h r a t e s of income

growth were r e s p o n s i b l e for a b i g i n c r e a s e i n t h e demand f o r

labour which soon outs t r ipped l o c a l manpower a v a i l a b i l i t i e s . The

labour gap was f i l l e d by inf lows of migrants from neighbouring

Arab c o u n t r i e s , from Asia and t o a lesser ex ten t from Europe and

t h e USA. Manpower s h o r t a g e s were not o n l y e x p e r i e n c e d by t h e

u n d e r - p o p u l a t e d c o u n t r i e s of t h e G u l f , t h e y a l s o a f f e c t e d

coun t r i e s w i t h r e l a t i v e l y l a r g e popula t ions such as I r a q .

O i l wea l th shaped s o c i a l a t t i t u d e s towards consumption,

i n v e s t m e n t , employment and b u s i n e s s 1 i f e . The d e m o n s t r a t i o n

e f f e c t , which we may d e f i n e i n t h i s context a s an und i sc ip l ined

u r g e t o a d o p t and i m i t a t e t h e consumpt ion p a t t e r n s of r i c h

i n d u s t r i a l i z e d c o u n t r i e s , a f f e c t e d t h e s e s o c i e t i e s . The

r e l a t i o n s h i p b e t w e e n g o v e r n m e n t s and c i t i z e n s a l t e r e d .

Governments , b e i n g i n r e c e i p t of t h e p r o c e e d s o f o i l w e a l t h

incur red the ob1 i g a t i o n t o r e d i s t r i b u t e revenues t o t h e i r people ,

and c i t i z e n s were l e d t o e x p e c t government b o u n t i e s as an

i n a l i e n a b l e r i g h t . The phenomenon of r i s i n g expec ta t ions became

an i m p o r t a n t c h a r a c t e r i s t i c of s o c i a l a t t i t u d e s . I n some

2

i n s t a n c e s t h e f r u s t r a t i o n caused by u n f u l f i l l e d e x p e c t a t i o n s

caused tens ions and l a t e n t r i f t s .

The re i s no doub t t h a t o i l bestowed c o n s i d e r a b l e

b e n e f i t s on the expor t ing count r ies . The g a i n s from investments

i n t h e i n f r a s t r u c t u r e , from the expansion of educat ion and h e a l t h

f a c i l i t i e s , from improved housing, p u b l i c u t i l i t i e s , t r a n s p o r t

and s o c i a l s e r v i c e s , from b e t t e r n u t r i t i o n and higher l e v e l s of

consumer’s wel fa re a r e both s i g n i f i c a n t and extremely valuable .

O i l a l s o had an impact on the economic development of

Arab S t a t e s which h a v e l i t t l e or no h y d r o c a r b o n r e s o u r c e s .

C o u n t r i e s such a s Egypt , T u n i s i a and S y r i a , wh ich a r e minor oil

expor t e r s , gained d i r e c t l y from the f a v o u r a b l e change i n t h e i r

terms of t r a d e . They a l s o g a i n e d , t o g e t h e r w i t h n o n - o i l

economies such as Jordan, t he Sudan, t he Yemens and Morocco, from

t h e d e v e l o p m e n t of c l o s e r economic l i n k s w i t h t h e major o i l -

e x p o r t i n g c o u n t r i e s . These economic r e l a t i o n s h i p s i n c l u d e d

m i g r a t i o n , a i d f l o w s , d i r e c t i n v e s t m e n t s and some i n c r e a s e s i n

t r a d e . The major c o n t r i b u t i o n of o i l t o t h e i r economies came

from the remit tances of migrants .

I t i s f a i r t o s ay t h a t i n t h e 1970s and e a r l y 1 9 8 O s ,

e i t h e r d i r e c t l y o r i n d i r e c t l y , o i l became t h e dominant f a c t o r of

economic growth and d e v e l o p m e n t throughout t h e Arab region, i n

both major o i l - expor t ing and non-oil coun t r i e s . This f a c t o r made

p o s i t i v e con t r ibu t ions and had some n e g a t i v e o r adverse e f f e c t s .

It is important t o recognize t h a t a l though the ba lance shee t of

o i l i n v o l v e s c r e d i t s a s w e l l as d e b i t s , t h e g a i n s were much

l a r g e r t h a n t h e l o s s e s . However, t h e oil s i t u a t i o n r a d i c a l l y

3

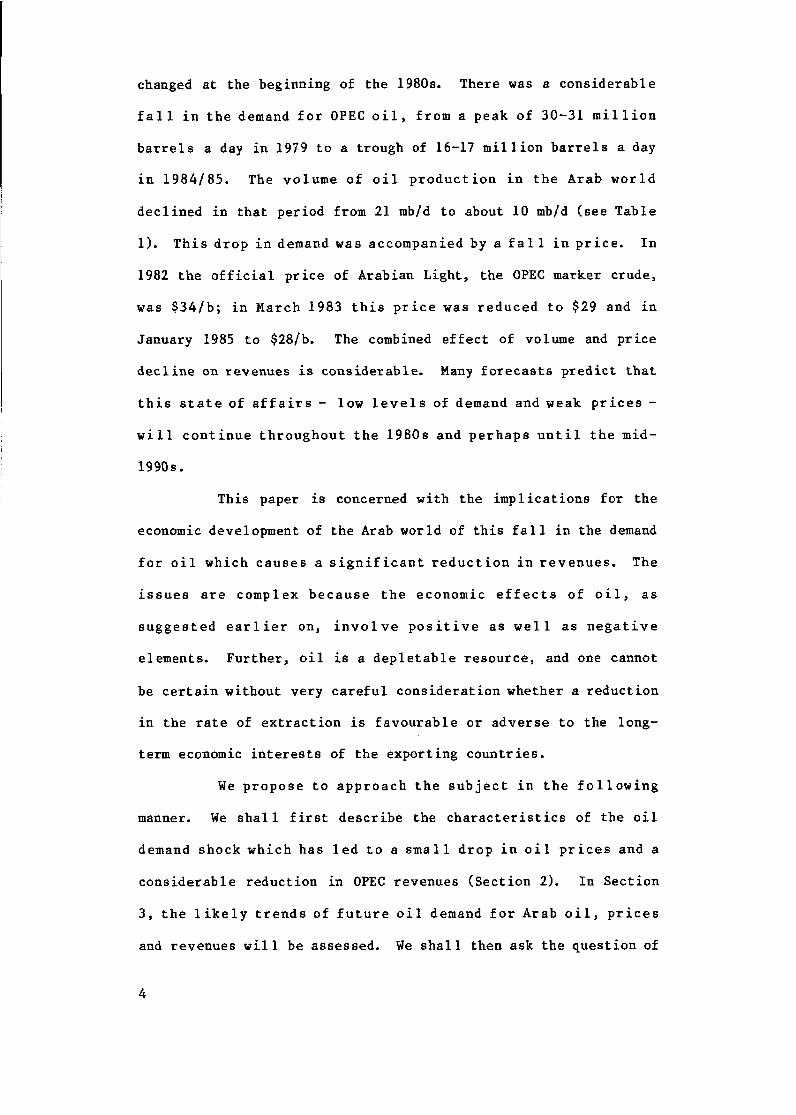

changed a t the beginning of t he 1980s. There w a s a cons ide rab le

f a 1 1 in t h e demand f o r OPEC o i l , f rom a peak of 30-31 m i l 1 i o n

b a r r e l s a day i n 1979 t o a trough of 16-17 m i l l i o n b a r r e l s a day

in 1984/85. The volume of o i l p r o d u c t i o n i n t h e Arab w o r l d

dec l ined in t h a t per iod from 21 mb/d t o about 10 mb/d ( see Table

1). T h i s d r o p i n demand w a s accompanied by a f a 1 1 i n p r i c e . In

1982 t h e o f f i c i a l p r i c e of Arabian Light, t h e OPEC marker crude,

was $ 3 4 / b ; i n March 1983 t h i s p r i c e was r e d u c e d t o $29 and i n

January 1985 to $28/b. The combined e f f e c t of volume and p r i c e

d e c l i n e on revenues is cons iderable . Many f o r e c a s t s p r e d i c t t h a t

t h i s s t a t e of a f f a i r s - low l e v e l s of demand and weak p r i c e s -

w i l l c o n t i n u e t h r o u g h o u t t h e 1980s and p e r h a p s u n t i l t h e mid-

1990s.

This paper is concerned wi th the imp l i ca t ions f o r t he

economic development of t h e Arab world of t h i s f a l l i n t he demand

f o r o i l which c a u s e s a s i g n i f i c a n t r e d u c t i o n i n r e v e n u e s . The

i s s u e s a r e complex b e c a u s e t h e economic e f f e c t s of o i l , a s

s u g g e s t e d e a r l i e r on, i n v o l v e p o s i t i v e a s w e l l a s n e g a t i v e

elements. Fur ther , o i l i s a d e p l e t a b l e resource , and one cannot

be c e r t a i n without very c a r e f u l cons ide ra t ion whether a r educ t ion

i n the ra te of e x t r a c t i o n i s f a v o u r a b l e o r adve r se t o t he long-

term economic i n t e r e s t s of t h e export ing coun t r i e s .

We propose t o a p p r o a c h t h e s u b j e c t i n t h e f o l l o w i n g

manner. We s h a l l f i r s t d e s c r i b e the c h a r a c t e r i s t i c s of t h e o i l

demand shock which has l e d t o a s m a l l d r o p in o i l p r i c e s and a

cons ide rab le reduct ion i n OPEC revenues (Sec t ion 2). In Sect ion

3, t h e l i k e l y t r e n d s o f f u t u r e o i l demand f o r Arab o i l , p r i c e s

and revenues w i l l be assessed. We s h a l l then ask t h e ques t ion of

4

whether t h i s r e d u c t i o n i n demand has some m e r i t s and may be

construed as a “bless ing i n d isguise” (Section 4). In Section 5

the main economic and p o l i t i c a l implications of the o i l demand

c r i s i s w i l l be d i s c u s s e d , and i n S e c t i o n 6 some t e n t a t i v e

conclusions w i l l be drawn.

5

The 1970s has become known i n o i l h i s t o r y a s t h e decade

of t h e p r i c e shocks; i n the same v e i n t h e 1980s w i l l undoubtedly

be r e f e r r e d t o as t h e decade of t he demand shock. The changes i n

t h e b e h a v i o u r of o i l demand which began i n 1980 a f f e c t e d i n a

u n i q u e way OPEC Member C o u n t r i e s b e c a u s e t h e O r g a n i z a t i o n

c o n t i n u e d t o p l a y t h e r o l e of t h e r e s i d u a l o i l s u p p l i e r t o t h e

wor Id.

The per fo rmance of t h i s r o l e caused OPEC t o i n c r e a s e

i t s o i l p r o d u c t i o n a t a v e r y h i g h r a t e i n t h e twenty years

l e a d i n g t o 1973; and t h i s r e l e n t l e s s growth i n o i l o u t p u t t h e n

r a i s e d l e g i t i m a t e f e a r s a b o u t t h e f a s t d e p l e t i o n o f p r e c i o u s

p e t r o l e u m r e s o u r c e s . High r a t e s of e x t r a c t i o n , which were

r a p i d l y reducing t h e l i f e of remaining r e s e r v e s t o 30 or 40 years

i n t h e p r o l i f i c Gu l f r e g i o n , were c o n s i d e r e d by many o b s e r v e r s

and by the governments themselves as undes i rab le . Most Arab o i l -

expor t ing coun t r i e s were unable t o absorb the revenues generated

by t h e r i s i n g volumes of o i l expor t s i n t o product ive inves tments

w i t h i n t h e n a t i o n a l economy. The h i g h e x t r a c t i o n r a t e s were

d e p l e t i n g a r e a l asset and r e p l a c i n g it by a f o r e i g n p o r t f o l i o of

p a p e r a s se t s s u b j e c t t o t h e v a g a r i e s of i n f l a t i o n , c u r r e n c y

f l u c t u a t i o n changes in r a t e s of i n t e r e s t , and t o t h e r i s k s of

6

d e f a u l t o r e x p r o p r i a t i o n . More f u n d a m e n t a l l y t h e Arab o i l

e x p o r t e r s were a w a r e t h a t t h e t i m e h o r i z o n o f e c o n o m i c

development was exceedingly long because t h e i r coun t r i e s su f fe red

from se r ious imbalances i n r e sources and from a lops ided economic

s t ruc tu re , Many o i l - expor t ing coun t r i e s have a small popula t ion

r e l a t i v e t o o t h e r f a c t o r s of p r o d u c t i o n s u c h as f i n a n c i a l

c a p i t a l . I n mos t o f them t h e a g r i c u l t u r a l s e c t o r was

unproduct ive because of a sho r t age of water and of s u i t a b l e l and ;

indus t ry was v i r t u a l l y non-exis tent a t t he beginning of t he o i l

e r a because of poverty and under-development; and the s e r v i c e s

were geared t o the l imi ted needs of small popu la t ion se t t lements .

Given t h e s e i n i t i a l condi t ions economic deve 1 opment i s bound t o

be a very long process. In t h i s context , t he conse rva t ion of o i l

resources f o r t he purpose of f i nanc ing development ove r s e v e r a l

decades becomes a v i t a l economic and p o l i t i c a l o b j e c t i v e .

As swing p r o d u c e r s t h e OPEC c o u n t r i e s were f o r c e d t o

e x t r a c t t o o much o i l in t h e y e a r s l e a d i n g t o 1973 and i n t h e

per iod 1973-1979. Today, through t h e i r performing t h e same r o l e ,

they f i n d themselves on a s h a r p l y d e c l i n i n g output trend. This

r e v e r s a l i s s o sudden and so r a p i d as t o g i v e rise t o s e r i o u s

w o r r i e s a b o u t i t s economic e f f e c t s . D i s q u i e t a b o u t h i g h

d e p l e t i o n r a t e s which may c o n s t r a i n t h e f i n a n c i n g of economic

development i n the d i s t a n t f u t u r e has now g i v e n way t o d i s q u i e t

a b o u t r a p i d r e d u c t i o n s i n r e v e n u e s and in marke t s h a r e s which

c o n s t r a i n the f inanc ing of economic development i n the immediate

f u t u r e .

To s u g g e s t t h a t t h i s change i n t h e c o u r s e of demand

should be welcome because i t removes e a r l i e r wor r i e s about r ap id

7

d o e s n o t do f u l l j u s t i c e to t h e problem. We h a v e

acknowledged t h a t t h e p r o d u c t i o n l e v e l s a t t a i n e d i n t h e 1970s

were d e t r i m e n t a l t o t h e i n t e r e s t s of o i l - expor t ing coun t r i e s ; but

t h e remedy f o r t h i s u n s a t i s f a c t o r y s i t u a t i o n i s not t o be found

i n t h i s sudden r e d u c t i o n i n o u t p u t b r o u g h t a b o u t b y outside

f o r c e s on which t h e p r o d u c e r s t h e m s e l v e s h a v e l i t t l e or no

con t ro l .

The roo t of a l l problems l i e s i n t h e r o l e of r e s i d u a l

s u p p l i e r which OPEC i s o b l i g e d t o perform on i t s own without h e l p

from non-OPEC producers. This r o l e makes i t imposs ib le f o r OPEC

members t o d e t e r m i n e f o r t h e m s e l v e s a p r o d u c t i o n p o l i c y

c o n s i s t e n t w i th t h e i r development ob jec t ives . They have neve r

been i n a p o s i t i o n t o d e f i n e an optimal product ion path, and they

have n o t succeeded i n r e g u l a t i n g demand through jud ic ious p r i c i n g

p o l i c i e s in such a way as t o avoid too r a p i d a r a t e of growth or

too sha rp a ra te of dec l ine . In t h e 1960s, o i l p r i c e s were kept

low because OPEC's barga in ing power v i s - a -v i s t h e oil companies

and t h e ma jo r consuming c o u n t r i e s was v e r y weak. I n t h e l a t e

1970s , t h e second o i l p r i c e shock s e n t p r i c e s w e l l a b o v e the

l e v e l r equ i r ed for an opt imal adjustment of f u t u r e o i l demand.

Whether OPEC cou ld have ac ted d i f f e r e n t l y i n 1979-80,

g i v e n t h a t o i l buyers played an a c t i v e p a r t i n b idding p r i c e s up

b e c a u s e of s u p p l y u n c e r t a i n t i e s and sudden changes i n t he

s t r u c t u r e of t h e petroleum market, is a moot question. Whatever

t h e answer t o t h i s ques t ion , t h e f a c t i s t h a t demand f o r OPEC o i l

has d e c l i n e d by almost 45% i n fou r years, and our main concern i s

about t h e imp l i ca t ions and consequences of t h i s b r u t a l f a c t .

8

The mechanism through which the demand f o r OPEC o i l has

s u f f e r e d such a b i g r educ t ion i s f a m i l i a r . The s t agna t ion of t h e

world economy i n r e c e n t years (which should not be a t t r i b u t e d t o

t h e o i l p r i c e rises on t h e i r own but t o a combination of f a c t o r s

i n wh ich t h e economic p o l i c y of t h e major OECD c o u n t r i e s p l a y s

t h e most i m p o r t a n t p a r t ) and t h e r i s e s i n e n e r g y p r i c e s (which

a r e c l o s e l y a s s o c i a t e d t o t h e o i l p r i c e i n c r e a s e s ) h a v e

d r a s t i c a l l y reduced the growth of world energy consumption. High

p r i c e s h a v e encouraged c o n s e r v a t i o n or g r e a t e r e f f i c i e n c y i n

e n e r g y u s e , and economic s t a g n a t i o n h a s e l i m i n a t e d t h e income

p u l l o n demand. The l a c k of growth i n e n e r g y demand d o e s n o t

e x p l a i n by i t s e l f t he f a l l i n t he demand for OPEC o i l . Two o t h e r

f a c t o r s p l a y e d a major p a r t . The f i r s t i s a change i n t h e

s t r u c t u r e of energy s u p p l i e s wi th c o a l , n u c l e a r and, t o a l e s s e r

e x t e n t , gas growing a t t h e expense of o i l . T h i s s t r u c t u r a l

change was p a r t l y due t o t h e e f f e c t s of r e l a t i v e p r i c e s and

p a r t l y t o p o l i c i e s implemented by consuming coun t r i e s i n order t o

reduce t h e i r dependence on o i l imports. The second f a c t o r i s t h e

growth of non-OPEC o i l product ion p a r t i c u l a r l y i n the North Sea,

Mexico, South-Eas t A s i a b u t a l s o i n a l a r g e number of s m a l l

producing countr ies . I n sho r t , t he demand f o r OPEC o i l s u f f e r e d

a doub le squeeze, one from the growth of non-oi l energy s u p p l i e s

and t h e o the r from the expansion of non-OPEC o i l production.

The ex ten t of t h e o i l product ion d e c l i n e (as f a r as t he

Arab member coun t r i e s of OPEC a r e concerned) i s apparent from t h e

f i g u r e s p r e s e n t e d i n T a b l e 1. Between 1973 and 1978 t h e t o t a l

o i l product ion of t h e seven coun t r i e s l i s t e d f l u c t u a t e d s l i g h t l y

a round 18 rnbld. The i n c r e a s e of o i l o u t p u t t o t h e much h i g h e r

9

m (U .rl U U G 5 0 U

h 0 .rl U U 0 P X w I d *rl 0

P d U 4 U 0

a E: E:

P

-4

G 0 .rl U c1 1 a 0 N PI

4 .rl 0

d

a, l-4 Q Id H

N m N

0 4

QI m r-

4 4

m rD rD

d

0 0 VI

N

ul * d

N

0 N 0

el

Q\ CO Q\

N

U .rl d 3

b4 a

0 m 00

4

4 Q\ 0

N

N m m d

e t- 4

N

CO 4 m m

c,

4

F rd h U .d A

ri 0 h

4

0 m 00

d

a el Q\

4

eJ m m

4

m r- h

0

W 4 P

I I 1 I I I

I I I I I I

1 1 1 I 1 1

1 I I I I I

L I I I I I

.. .. el Qo o\ ri

I o e

l e v e l o f 21 mb/d i n 1979 was e n t i r e l y due t o t h e I r a n i a n

Revolut ion. As r e s i d u a l s u p p l i e r s w i t h i n OPEC i t s e l f t he Arab

coun t r i e s made up f o r t he s h o r t f a l l i n I r a n i a n production.

Thus, t h e 1979 product ion l e v e l should be construed as

excep t iona l ; i t cannot be taken a s a base f o r t h e measurement of

t h e subsequent dec l ine . It would be more appropr ia te t o t a k e a

product ion volume of 18 mb/d (1973-1978) as our re ference p o i n t

and t o measure t h e r e d u c t i o n i n oil o u t p u t a g a i n s t t h i s

benchmark. We f i n d t h a t t he reduct ion remains very s i g n i f i c a n t :

i n 1 9 8 4 a c t u a l p r o d u c t i o n was 45% be low t h e r e f e r e n c e l e v e l !

Arab o i l product ion w a s v i r t u a l l y ha lved in 3 t o 4 years.

The p a r a l l e l c o l l a p s e i n o i l revenues i s documented in

T a b l e 2. A b a s e l i n e o r a r e f e r e n c e is r e q u i r e d t o a s s e s s t h i s

d e c l i n e i n revenues. It would c l e a r l y be mis leading t o t a k e t h e

peak y e a r of 1980 w i t h r e v e n u e s of a b o u t $205 b i l l i o n as t h e

s t andpo in t from which changes are t o be measured. The base l i n e

for revenues should be cons i s t en t with the product ion r e fe rence

l e v e l which w e have s e t a t 18 mb/d. We es t ima te the base l e v e l

of o i l r e v e n u e s a t $172 b i l l i o n on t h e a s sumpt ion t h a t t h e

a v e r a g e p e r b a r r e l p r i c e is $28 and t h a t t h e a v e r a g e vo lume o f

domestic o i l consumption i n the seven Arab coun t r i e s considered

is 1.1 mb/d. On t h i s b a s i s , it appears t h a t a revenue s h o r t f a l l

emerged i n 1982, and t h a t it increased s u b s t a n t i a l l y i n 1983 and

1984.

The s h o r t f a l l from our n o t i o n a l base l i n e ($172b) and

from peak revenues i n 1980 ($205.7b) is as f o l l o w s (US$ b i l l i o n ) :

11

Year Revenue shor t fa l l from peak (1980)

Revenue shortf a1 1 from reference 1 ine

1981

1982

1983

1984

19

70.7

108.7

108.2

(14.7)

37

75

74.5

No f u r t h e r e l a b o r a t i o n i s requ ired . The s i m p l e and

stark f a c t i s that the demand shock of 1981-84 has had rapid and

s i g n i f i c a n t effects on the o i l revenues of the seven Arab member

countries of OPEC.

12

3, OIL DEHAHD Bw OIL PRICES ZR 1985-1990

A study of t he economic impl i ca t ions of changes i n the

demand for Arab o i l r equ i r e s a f o r e c a s t of l i k e l y t r ends in t h e

coming y e a r s . T h e r e is an abundance of ene rgy and o i l demand

p r o j e c t i o n s t o 1990, 1995 and t h e year 2000. But t h e t r a c k

r e c o r d of o i l f o r e c a s t e r s h a s been s o bad i n t h e p a s t twenty

years ( p a r t i c u l a r l y when they concerned themselves w i t h demand)

t h a t w e d o n o t f e e l v e r y c o n f i d e n t w i t h t h e i r more r e c e n t

p r o j e c t ions.

Y e t w e h a v e no o p t i o n but t o u s e e x i s t i n g m a t e r i a l

s i n c e any new f o r e c a s t w i l l be l i a b l e t o t h e same objec t ions . I n

order t o reduce the r i s k of s e r i o u s misjudgments w e s h a l l proceed

c a u t i o u s l y s u b j e c t i n g both the methodology of f o r e c a s t s and t h e i r

r e s u l t s t o q u a l i f i c a t i o n s and c r i t i c a l a n a l y s i s .

L e t us t a k e as our base the behaviour of t o t a l p r imary

energy consumpt ion i n t h e w o r l d o u t s i d e t h e c e n t r a l l y p l a n n e d

economies a t t h e beginning of t h i s decade.

There w a s a marked d e c l i n e i n world energy consumption

i n 1979-1983, w h i l e i n e a r l i e r years growth was t h e d i s t i n c t i v e

f ea tu re . Between 1979 and 1983, primary energy consumption f e l l

by some 4.25%; b u t i t i s n o t i c e a b l e t h a t t h e r a t e of f a l l h a s

t ended t o d e c r e a s e a f t e r a s h a r p s t a r t i n 1979180. Many

13

U1 PI -4 $4 U c 3 0 U

b PI P

01 c U w h 0

0 a $4 4 rcI 0

m aJ 3 G W 3 W c4

a

d -4 0

N

W rl

tu h

e

o o o o c \ 1 o o 0 0 0 0 0 0 0 0 m r - m m o o o l n

4 r - 4

f/ 4

f 1 4

O o m O N m o o o I c I o o I v r o h r n n C O r n O h 0 m O O I c I r - N O r -

m

N m * N 4

rn m e

14

o b s e r v e r s b e l i e v e t h a t t h e downward trend i n p r i m a r y energy

consumpt ion h a s bottomed out. I n million t o n n e s of o i l

e q u i v a l e n t , p r imary energy consumption was:

Year

1979

1980

1981

1982

1983

L e t U no1 C ns i d r

Primary Energy mtoe

4769

4695

4642

4573

4568

r o j e c t i o n s of t h e g owth f

primary energy consumption for t he per iod 1985-2000 made by t h r e e

d i f f e r e n t i n s t i t u t i o n s . The p r o j e c t i o n s considered are those of

( a ) t h e OECD/ZEA, (b) 8 major o i l company and ( c ) an i n d e p e n d e n t

consul tan t .

OECD/IfA i n t h e i r study World Energy Outlook publ i shed

in 1982 p r e s e n t h i g h and low demand p r o j e c t i o n s f o r t h e OECD

r e g i o n . The growth r a t e s of p r imary ene rgy consumpt ion a re a s

f 01 lows :

1985-1990 1990-2000

High Demand 2.3% 2.7%

Low Demand 1.7X 1.8%

O E C D / I E A i s more c a u t i o u s about i t s p r o j e c t i o n s o f

p r i m a r y energy consumption in deve lop ing coun t r i e s (OPEC and non-

OPEC) acknowledging the ex i s t ence of cons ide rab le u n c e r t a i n t i e s .

Thei r estimates f o r 1980-2000 put t he l i k e l y growth ra tes i n the

r a n g e of 4.9-5.7% p e r annum in non-OPEC d e v e l o p i n g c o u n t r i e s .

15

For OPEC coun t r i e s t h e i r e s t ima te is 5.9-7.3% per annum f o r 1985-

1990, and 5.5-5.92 i n 1990-2000. Assuming t h a t t h e r e l a t i v e

w e i g h t s of OPEC and non-OPEC in energy consumpt ion a r e of t h e

order of 0.3 and 0.7 t h i s would y i e l d the f o l l o w i n g growth r a t e s

f o r the t h i r d world a s a whole:

1980-1985 1985-1990 1990-2000

Third World 5.6-6.7 5.2-6.2 5.1-5.7

As a c t u a l d a t a for 1980-83 a r e now a v a i l a b l e one can

t e n t a t i v e l y a s s e s s t h e v a l i d i t y of t h e e s t i m a t e f o r t h e f i r s t

period. It appears t h a t t h e a c t u a l growth ra te i n 1980-83 was of

t he o rde r of 3.4-3.52 per annum, w e l l ou t s ide t h e pro jec ted range

of 5.6-6.7% f o r 1980-85. As i t i s d o u b t f u l t h a t g rowth i n 1984

and 1985 would compensate for t h i s very l a r g e discrepancy w e can

but i n f e r t h a t t he O E C D l I E A p r o j e c t i o n s f o r t he t h i r d world a r e

exceedingly op t imis t i c .

The major oil company i n a study completed i n 1983 put

t he r a t e of growth of primary energy consumption between 1983 and

2000 a t 2.3% p e r annum i n t h e wor I d o u t s i d e c e n t r a l l y p l a n n e d

economies. The IEA/OECD low demand case has 1.7-1.8% i n OECD and

mid -po in t e s t i m a t e s of 5.4-5.7% f o r t h e t h i r d w o r l d . The

we igh ted a v e r a g e f o r t h e w o r l d o u t s i d e c e n t r a l l y p l a n n e d

economies is of t h e o r d e r of 2.5-2.7%. Even in i t s low demand

case OECDlIEA i s more o p t i m i s t i c than the major o i l company.

More r ecen t p r o j e c t i o n s by an independent i n t e r n a t i o n a l

c o n s u l t a n t (1984) p u t t h e growth r a t e i n 1985-2000 a t 2.22 p e r

annum. The e s t i m a t e is c l o s e t o t h a t of t h e ma jo r o i l company

though m a r g i n a l l y lower. C l e a r l y more r ecen t f o r e c a s t s tend t o

be more pess imis t i c than e a r l i e r ones. Our own judgment is t h a t

t h e p r o b a b l e r a n g e of f u t u r e g rowth r a t e s of pr imary e n e r g y

consumpt ion is 2.0-2.4% p e r annum. These a v e r a g e r a t e s may

c o n c e a l , however , c o n s i d e r a b l e s h o r t - t e r m v a r i a t i o n s t h a t a r e

l i k e l y t o ob ta in dur ing 1985-2000.

P r o j e c t i o n s of pr imary e n e r g y consumpt ion a r e j u s t a

f i r s t step t owards a f o r e c a s t of demand f o r OPEC and Arab o i l .

The OECD/IEA study e s t ima tes OPEC s u p p l i e s as f o l l o w s (mbld):

1985 1990 2000

OPEC supply 23 - 26 27-29 24-28

Call on OPEC 23-26 27-33 33-49

There i s no doubt t h a t t hese p r o j e c t i o n s a r e a l r e a d y out of l i n e

for 1985, s i n c e OPEC p r o d u c t i o n unde r t h e most f a v o u r a b l e

c o n d i t i o n s i s u n l i k e l y to exceed 18-19 mb/d i n t h a t y e a r . It

seems t h a t t he OECD/IEA f o r e c a s t s should be discarded d e s p i t e t h e

a u t h o r i t y of t h e i r authors .

The major o i l company r e f e r r e d t o above p r o j e c t s OPEC's

product ion a s f o l l o w s :

1985-1990 1990-1995 1995-2000

OPEC supply 20-21 21-23 25-27

Call on OPEC o i l 20-21 21-23 27

The f o r e c a s t provided by t h e i n t e r n a t i o n a l c o n s u l t a n t

OPEC's s u p p l y i s e x p e c t e d i s c l o s e t o t h a t of t h e o i l company.

by t h e consu l t an t t o reach 22 mb/d in 1990, and 27 mb/d i n 2000.

T a k i n g t h e two l a t t e r f o r e c a s t s (company and

c o n s u l t a n t ) a s t h e more p l a u s i b l e p i c t u r e of f u t u r e t r e n d s , we

17

e s t i m a t e c r u d e o i l p r o d u c t i o n of

1985-2000 as f o l l o w s :

1985

Alger i a 0.70

Iraq 1.70"

Kuwait 1 .oo Libyan A.J . 1.10

Qatar 0.30

Saudi Arabia 4.70

UAE 1.10

T o t a l

T o t a l OPEC

10.60

18.50

t h e Arab members of OPEC i n

1990

0.70

2.75

1.15

1.15

0 .30

4.70

1.25

12.00

21 .00

2000

0.60

4.00

1 S O

1.50

0.15

8.00

1.80

17.55

27 .OO

* I n c l u d e s Kuwait and S a u d i Arabia 's p r o d u c t i o n on b e h a l f of Iraq.

This shows s m a l l increases i n Arab product ion between

1985 and 1990 and a more s i g n i f i c a n t r i s e towards the end of t h e

1990s. However, Arab o i l p r o d u c t i o n w i l l b a r e l y r e a c h i n year

2000 t h e l e v e l of 18.0 mb/d p o s t u l a t e d e a r l i e r on a s t h e

r e fe rence for asses s ing changes.

Our o i l p r i c e f o r e c a s t , a t c o n s t a n t 1985 d o l l a r s ,

assumes no rises u n t i l 1992. I n f a c t real p r i c e s may d i p between

1985 and 1 9 8 8 / 9 and t h e n r e c o v e r i n 1992 to t h e i r 1985 l e v e l .

A f t e r 1992 o i l p r i c e s may r ise s i g n i f i c a n t l y reaching $40-45 (in

cons tan t 1985 terms) by year 2000.

A r e v e n u e f o r e c a s t ( a t 1985 c o n s t a n t d o l l a r s ) i s

presented below.

T h i s f o r e c a s t s u g g e s t s t h a t the o i l r e v e n u e s of Arab

members of OPEC w i l l no t r e t u r n t o the base l e v e l of $172/b u n t i l

l a t e i n t h e 1990s. Meanwhile o i l r e v e n u e s ( a t 1985 c o n s t a n t

d o l l a r s ) could w e l l f a l l down by 50% from t h i s base v a l u e before

they s t a g e up a slow recovery.

1985 1988 1990 1992 2000

Output mb/d 10.60 11.00 12.00 13.50 17.55

Domestic Con- 1.16 1.27 1.35 1.46 2.00 sumpt ion mb/d

Exports mb/d 9.44 9.73 10.65 12.04 15.55

P r i c e $/b ( cons t an t 27.5 25.0 26 .O 27.5 40 .0 1985 d o l l a r s )

Gross revenues $/b 94.75 88.8 101.0 120.8 227.0

The d r o p i n r e v e n u e can now be p u t into p e r s p e c t i v e .

The d e c l i n e starts i n 1982 and i s e x p e c t e d t o bo t tom o u t i n

198819 but t he subsequent upswing s t r e t c h e s ove r t e n years. It

i s only i n 1997 that revenues (measured i n r e a l terms) r ecove r t o

t h e r e f e r e n c e l e v e l . The p r e d i c t e d d u r a t i o n of t h e " r evenue

c r i s i s " i s t h e r e f o r e very long being est imated, from beginning t o

end, a t 15 years.

19

4. THE CASE FOB FAVOUBdllLE IIZPLICATIOWS

Is it p o s s i b l e t o argue t h a t t h e f a l l i n o i l revenues

is a b l e s s i n g i n d i s g u i s e ? Such an argument was made by

d i s t ingu i shed and a u t h o r i t a t i v e p e r s o n a l i t i e s and the reasoning

they proposed d id not l a c k e i t h e r mer i t or convic t ion . Whether

t h e same p e r s o n a l i t i e s would de fend t h e c a s e today , now t h a t

p e r c e p t i o n s a b o u t t h e d e p t h and t h e p o s s i b l e d u r a t i o n of t h e

r e v e n u e c r i s i s h a v e s h a r p e n e d so much, is a moot q u e s t i o n .

Indeed, t he percept ions have s i g n i f i c a n t l y changed. I n 1982, t h e

f a 1 1 i n r e v e n u e s was p a i n f u l b u t n o t d r a m a t i c , and t h e g e n e r a l

expec ta t ion w a s t h a t t h e c r i s i s would t ake the form of a s a l u t a r y

b u t temporary shock. Today i t i s more d i f f i c u l t t o see t h e

s i l v e r l i n i n g of t he c loud because the shock has turned out t o be

deep , and i t s e f f e c t s a r e e x p e c t e d t o be f e l t o v e r a v e r y l o n g

per iod of time.

The " s i l v e r l i n i n g " theory rests on two propos i t i ons ,

though most of i t s proponents u s u a l l y chose t o s t ress one or t h e

o the r bu t r a r e l y both.

The F i r s t p r o p o s i t i o n h a s a l r e a d y b e e n d i s c u s s e d i n

S e c t i o n 2 of t h i s pape r . It f o c u s s e s on t h e i s s u e of r a p i d

d e p l e t i o n of o i l r e s e r v e s . A f a l l i n o i l demand ( t h e f a l l in

revenues being s i m p l y i t s consequence) e n a b l e s Arab coun t r i e s t o

20

c o n s e r v e t h e i r n a t u r a l r e s o u r c e s and t o b r ing e x t r a c t i o n r a t e s

c l o s e t o an optimum path.

However, t he poin t about conse rva t ion of resources i s

t h a t it should be a mat te r of e x p l i c i t po l i cy on t h e p a r t of t h e

producing count r ies , no t t he r e s u l t of e x t e r n a l fo rces on which

they have no con t ro l . The l i k e l i h o o d t h a t t hese o u t s i d e f a c t o r s

w i l l determine product ion rates c l o s e t o the l e v e l s d e s i r e d by

the o i l expor t e r s (given t h e s i z e of t h e i r r e s e r v e s , t h e l e n g t h

of t h e i r development horizon and o the r r e l e v a n t c o n s t r a i n t s ) i s

v i r t u a l l y n i l . A s we have seen, Arab o i l producers were induced

t o p r o d u c e much more t h a n t h e i r p r e f e r r e d vo lumes in t h e 1 9 6 0 s

and 1 9 7 0 s . It a l s o seems t h a t t h e e x p e c t e d p r o d u c t i o n p a t h

throughout t he 1981- la te 1990s c y c l e w i l l be a t times w e l l below

t h e d e s i r e d l e v e l s .

It is d i f f i c u l t t o b e more p r e c i s e on t h i s i s s u e

b e c a u s e v e r y few c o u n t r i e s h a v e a c l e a r l y d e f i n e d d e p l e t i o n

ob jec t ive . Kuwai t is t h e only s i g n i f i c a n t except ion a s t h e r e a r e

a u t h o r i t a t i v e s ta tements on record (Shaikh A l i K h a l i f a A 1 Sabah

t o t h e O x f o r d E n e r g y S e m i n a r i n 1980) s u g g e s t i n g t h a t a

r e s e r v e / p r o d u c t i o n r a t i o of 100 y e a r s is t h e government 's

p r e f e r r e d g o a l . Saud i Arabia's v i e w s on t h i s i s s u e a r e l e s s

c l e a r l y s t a t e d , a l though i t s dec i s ion i n the l a t e 1970s t o set a

maximum a l l o w a b l e o u t p u t l e v e l a t 8.5 mb/d may b e t a k e n a s an

i n d i c a t i o n of an i m p l i c i t d e p l e t i o n pol icy .

Our c o n c l u s i o n is t h a t t h e f a l l i n w o r l d demand f o r

Arab o i l , though i n v o l v i n g by n e c e s s i t y g r e a t e r conse rva t ion of

r e s o u r c e s , h a s n o t y e t made a n a p p r o p r i a t e c o n t r i b u t i o n t o t h e

d e p l e t i o n issue. OPEC - and by impl i ca t ion , i t s Arab members -

21

a r e s t i l l p e r f o r m i n g t h e r o l e of a r e s i d u a l s u p p l i e r , a r o l e

which e f f e c t i v e l y p r e v e n t s them from choosing and fo l lowing t h e i r

p re fe r r ed e x t r a c t i o n rates.

The second p r o p o s i t i o n which unde r 1 i e s t h e " s i 1 v e r

l i n i n g " argument i s t h a t t h e sudden i n c r e a s e i n o i l wea l th of t he

1970s has caused was te fu l expendi ture , g r e a t se l f - indulgence i n

matters of economic p o l icy, d e s t a b i l i z i n g expec ta t ions and s o c i a l

t e n s i o n s . The r e d u c t i o n i n r e v e n u e s can b e s e i z e d upon a s an

o p p o r t u n i t y f o r improv ing t h e economic management of t h e o i l -

expor t ing country and f o r s t e e r i n g economic development onto an

e f f i c i e n t pa th .

The re i s much f o r c e i n t h i s a rgument b u t i t may n o t b e

accepted without a few q u a l i f i c a t i o n s .

It is t r u e t h a t t h e sudden a c c r u a l of o i l wea l th i n t h e

1 9 7 0 s caused economic p r o b l erns and s o c i a l t e n s i o n s which h a v e

reduced i ts obvious bene f i t s . Put b l u n t l y t h e immediate b e n e f i t

o f oil w e a l t h r e l a t e s t o h i g h e r i n v e s t m e n t and h i g h e r

consumption. The u t i l i t a r i a n v i ew of economics i s t h a t t h e

p u r p o s e of d e v e l o p m e n t i s t o r a i s e t h e l e v e l of p r e s e n t

consumpt ion ( t h r o u g h income growth) and t h e expected l e v e l s of

f u t u r e consumption ( t h r o u g h i n v e s t m e n t ) . A more s o p h i s t i c a t e d

v i ew emphas izes two f u r t h e r a s p e c t s of d e v e l o p m e n t : ( a )

q u a l i t a t i v e and s t r u c t u r a l changes i n t h e economy and (b) an

enhanced a b i l i t y t o s u s t a i n economic g rowth i n t h e long-run .

These two aspec t s a r e obv ious ly r e l a t e d because the a b i l i t y t o

s u s t a i n growth o f t e n depends on a f u n d a m e n t a l s t r u c t u r a l

t ransformat ion of t he o i l economy.

22

The sudden a c c r u a l of o i l w e a l t h i n t h e 1970s w a s

d i f f i c u l t t o a b s o r b immedia t e ly as i t caused some s h o r t - t e r m

problems of i n f l a t i o n , t r anspor t b o t t l e n e c k s , land s p e c u l a t i o n

e tc . These were t h a n k f u l l y overcome w i t h i n a few years but more

fundamental problems arose which proved d i f f i c u l t t o t ack le .

The f i r s t p r o b l e m w a s c o n s i d e r a b l e i n v e s t m e n t

e x p e n d i t u r e i n w a s t e f u l p r o j e c t s . These do not o n l y i n c l u d e

p r o j e c t s undertaken f o r p r e s t i g e reasons o r t o s e r v e t h e purpose

of conspicuous consumption. Waste was incur red because p lanning

a u t h o r i t i e s and o t h e r dec is ion-making a g e n c i e s l a c k e d t h e t i m e

and r e s o u r c e s t o s t u d y t h e economics of p r o j e c t s and t o e n s u r e

t h a t investments would carry a p o s i t i v e r a t e of r e tu rn .

The argument t h a t a f a l l in o i l r e v e n u e s need n o t

r ep resen t an e q u i v a l e n t l o s s t o the economy t a k e s i n t o account

expendi ture on t hese uneconomical p ro jec t s . I f o i l revenues a r e

wasted i n p a r t t hen t h e r e a l drop in o i l income (so long as t h i s

d r o p i s due t o q u a n t i t y and n o t p r i c e ) i s n o t as l a r g e as i t m a y

appea r . On t h e c o n t r a r y , i t is p r e f e r a b l e t o p r o d u c e l e s s o i l

than t o exchange a d d i t i o n a l volumes f o r was te fu l p r o j e c t s which

d r a i n r e s o u r c e s away f rom t h e economy i n s t e a d o f g e n e r a t i n g

economic re turns .

The second problem is was te fu l c u r r e n t expendi ture by

governments. These m a y i nc lude e x c e s s i v e spending on defense, as

happened i n I r a n d u r i n g t h e 1970s; u n n e c e s s a r y e x p a n s i o n of

government employment; payment of l a r g e commissions € o r agents

of c o n t r a c t o r s ; p u r c h a s e s of l a n d a t i n f l a t e d p r i c e s f o r

subsequent resale a t lower p r i c e s ; l a r g e s u b s i d i e s t o va r ious

a c t i v i t i e s i nc lud ing i n t e r e s t f r e e loans etc.

23

Once a g a i n a f a l l i n o i l r e v e n u e s which wou-ld cause

gove rnmen t s t o c u r t a i l t h e s e e x p e n d i t u r e s can b e c o n s t r u e d a s

b e n e f i c i a l . Incremental o i l i s b e t t e r conserved than spent away

i n was tefu l expenditure.

The t h i r d p r o b l e m i s t h a t o i l r i c h e s i n h i b i t e d

governments from adopting sound economic p o l i c i e s i n ma t t e r s of

t a x a t i o n , ene rgy and food p r i c i n g , i n t e r e s t r a t e s e tc . Good

economics r e q u i r e s commodities t o be pr iced a t t h e i r oppor tuni ty

c o s t s i n order t o avoid m i s a l l o c a t i o n of resources. Most o i l -

e x p o r t i n g c o u n t r i e s p r i c e o i l , g a s and e l e c t r i c i t y i n t h e

d o m e s t i c economy a t a smal l f r a c t i o n of t h e i r t r u e o p p o r t u n i t y

cos t , thus encouraging high r a t e s of was te fu l consumption. This

p o l i c y is sometimes ex tended t o s t a p l e food and water. The

j u s t i f i c a t i o n o f t e n g iven which r e l a t e s t o income r e d i s t r i b u t i o n

and s o c i a l w e l f a r e i s n o t v a l i d . P r i c i n g p o l i c y is n o t t h e

appropr i a t e instrument f o r i m p l e m e n t i n g t h e s e o b j e c t i v e s . The

sound approach is t o a 1 low pr ices t o perform e f f i c i e n t l y t h e i r

r o l e i n t h e a l l o c a t i o n of r e s o u r c e s and t o u s e t a x e s and

subs id i e s f o r t h e purposes of income o r weal th d i s t r i b u t i o n and

o the r s o c i a l o b j e c t i v e s .

If t h e f a l l i n o i l r e v e n u e s f o r c e s g o v e r n m e n t s t o

r e v i s e t h e i r p r i c i n g p o l i c i e s and t o in t roduce a t a x a t i o n system

which would d e v e l o p (a h i t h e r t o non-exis tent) f i s c a l d i s c i p l i n e ,

t h e n one c o u l d say t h a t t h e c l o u d h a s a s i l v e r l i n i n g . Such

reforms a r e necessary f o r t he purpose of long-term developments.

The f o u r t h p rob lem i s t h a t t h e sudden a c c r u a l of o i l

revenues and t h e concomitant r ise i n expendi ture has induced such

24

r a p i d s o c i a l t r a n s f o r m a t i o n a s t o s t r a i n s o c i e t y ' s a b i l i t y t o

r e spond t o changes and t o a d a p t t o new c i r c u m s t a n c e s . These

changes i n v o l v e d a f a s t r a t e of i n t e r n a l m i g r a t i o n f rom r u r a l

a r e a s t o towns and a h i g h i n f l o w of e m i g r a n t worke r s . They

changed a t t i t u d e s towards work, educat ion and t h e a c q u i s i t i o n of

w e a l t h , a n d t h e y p u t u n d e r s t r a i n f a m i l y and s o c i a l

r e l a t i o n s h i p s . The f a 1 1 in o i l revenues, because i t n e c e s s a r i l y

s l o w s t h e p a c e of income g rowth , m a y p r o v i d e a b r e a t h i n g s p a c e

and a l l o w soc ie ty the t i m e it needs t o absorb t h e r e v o l u t i o n a r y

changes of t h e 1970s.

The f i f t h p rob lem i s t h a t t h e o i l p r i c e e x p l o s i o n of

t h e p rev ious decade has induced expec ta t ions of cont inuing income

growth a t very h igh r a t e s which a r e t o t a l l y unsus ta inable . These

expec ta t ions have d i s t o r t e d t h e percept ions of f u t u r e prospec ts

and f o s t e r e d an u n r e a l i s t i c understanding of what an o i l economy

- g i v e n i t s lopsided s t r u c t u r e and i t s l a c k of non-oi l resources

- could poss ib ly achieve. I n t h a t sense the f a l l in o i l revenues

i s a sober ing experience which may lower expec ta t ions and focus

p e r c e p t i o n s on t h e r e a l i s t i c p r o s p e c t s of f u t u r e economic

development. The medicine may be b i t t e r but s a l u t a r y consider ing

t h a t those r i s i n g expec ta t ions which can never be f u l f i l l e d o r

s a t i s f i e d tend t o d e - s t a b i l i z e the soc ie ty .

As mentioned e a r l i e r on, t h i s 1 i n e of r e a s o n i n g h a s

c o n s i d e r a b l e m e r i t s ; y e t some q u a l i f i c a t i o n s a r e i n o r d e r .

F i r s t , w e s h o u l d n o t e x p e c t t h a t t h e f a 1 1 i n r e v e n u e w i l l h e l p

governments t o do away wi th a l l was t e fu l inves tments and w a s t e f u l

cu r ren t expenditure. Undoubtedly some progress w i l l be achieved

on t h i s f r o n t b u t major d i f f i c u l t i e s may b e e n c o u n t e r e d on t h e

25

road to improvements. Although investments w i l l i n e v i t a b l y be

c u r t a i l e d , t h e r e i s no g u a r a n t e e t h a t good p r o j e c t s would

s u r v i v e and uneconomic p ro jec t s would be re jec ted . Such an

o u t come r e q u i r e s cons i d e r a b 1 e improvements i n t h e economic

d e c i s i o n - m a k i n g p r o c e s s ; y e t t h e f a l l in r e v e n u e s wh ich

c o n s t r a i n s t h e p u r s e d o e s n o t n e c e s s a r i l y t r a n s f o r m t h e

p r o f e s s i o n a l a b i l i t y of p l anne r s and o the r r e l e v a n t a u t h o r i t i e s .

V e r y o f t e n bad p r o j e c t s are undertaken i n response to p r e s s u r e s

from powerful groups w i t h a ves ted i n t e r e s t i n s p e c i f i c ventures .

These groups w i l l cont inue t o exe rc i se an i n f l u e n c e and lobby f o r

some of t h e i r favoured p r o j e c t s d e s p i t e the f a l l in revenues.

Fur ther , many governments i n t h e Arab world w i l l f i n d

i t d i f f i c u l t t o c u r t a i l d e f e n s e e x p e n d i t u r e s g i v e n t h e l o n g -

s tanding Arab-Israel i conf 1 i c t and the con t inua t ion of t he I raq-

I r a n w a r . F u r t h e r , much of Arab a i d s u p p o r t s f e l l o w Arab

c o u n t r i e s ( i n c l u d i n g P a l e s t i n e ) w h i c h a r e e i t h e r o n t h e

conf ron ta t ion l i n e with Israel o r engaged i n t h e Gulf war. V i t a l

p o l i t i c a l o b j e c t i v e s may c o n s t r a i n t h e a b i l i t y of Arab o i l

e x p o r t e r s t o r e d u c e t h i s a id . In o r d e r t o make room for

e s s e n t i a l defense and a i d expendi tures , development budgets may

have to be d r a s t i c a l l y cut.

I t i s t r u e t h a t t h e f a l l in r e v e n u e s may i m p r o v e

economic p o l i c i e s . In f a c t , modest s t e p s have a l r e a d y been t aken

i n t h i s d i r e c t i o n i n s e v e r a l Arab o i l - expor t ing countr ies . The

domest ic p r i c e s of f u e l s have been r a i s e d in some p l a c e s and some

i n d i r e c t p r i c e subs id i e s reduced. But governments, however w e 1 1-

disposed on t h e s e matters, are c o n s t r a i n e d p o l i t i c a l l y b e c a u s e

26

t h e p o p u l a t i o n h a s become accustomed t o low p r i c e s and would

r e s e n t changes t h a t may reduce s tandards of l i v i n g . The i s sue

c a n b e v e r y s e n s i t i v e and i t i s e a s y t o u n d e r s t a n d why

government s hes it a t e t o imp0 s e unpopu 1 a r me asur e s . W e a r e i n c l i n e d t o t h i n k t h a t t h e s t r o n g a rgumen t s i n

f avour of t he " s i l v e r l i n i n g " theory r e l a t e t o problems of s o c i a l

changes and r e a l i s t i c expectat ions. Arab soc ie ty needs t i m e t o

a d j u s t t o t he r a p i d t ransformat ion of t h e 1970s, and a per iod of

t i m e i n which t h e pace of growth slows down may be b e n e f i c i a l i f

p u t t o good u s e . I t is u p t o g o v e r n m e n t s t o s e i z e t h i s

o p p o r t u n i t y and t o u s e i t for r e a l i s t i c and e f f i c i e n t

a d j u s t m e n t s . I t i s e s s e n t i a l , however , t o a v o i d t h e e x t r e m e

s o l u t i o n of l e t t i n g t h e r a t e of economic growth d r o p s u d d e n l y

from a h i g h t o a v e r y low l e v e l . Such a f a l l c a n c a u s e s o c i a l

t e n s i o n s a n d e c o n o m i c d i s t o r t i o n s , as s e r i o u s i n t h e i r

consequences as t h o s e c r e a t e d by a sudden a c c e l e r a t i o n i n

economic growth. It is also important t o take advantage of t h e

oppor tuni ty t o d e f i n e t h e long-term development o b j e c t i v e s of t h e

country and t o choose a f e a s i b l e and d e s i r a b l e p a t t e r n of s o c i a l

and economic changes. The w o r s t outcome i s f o r gove rnmen t s

e i t h e r t o panic o r t o remain pass ive .

27

r v enu

5 . THE UFlFhVOUBBBLE IWLICATIORS

We ment ioned e a r l i e r on t h a t t h e r e d u c t i o n i n o i l

i n t h e 1980s and e a r l y 1990s i s e x p e c t e d t o be

s i g n i f i c a n t and t o a f f e c t o i l economies ove r a f a i r l y long per iod

of t i m e . Unf avourab le economic consequences ar ise because of the

a n t i c i p a t e d l e n g t h and depth of t he o i l demand c r i s i s .

The economic e f f e c t s m a i n l y r e l a t e to t h e r a t e s of

economic g rowth and t h e r a t e s of c a p i t a l a c c u m u l a t i o n . T h e i r

adverse impact extends ou t s ide the main o i l - impor t ing coun t r i e s

because o the r Arab na t ions depend t o some e x t e n t on the fo r tune

of oil. Some ( l i k e Egypt , B a h r a i n , Oman, S y r i a or T u n i s i a ) a r e

themselves o i l exporters . They a r e cushioned a g a i n s t a volume-

induced f a l l i n r e v e n u e s b e c a u s e they a r e n o t bound by O P E C

q u o t a s and a r e a b l e t o maximize o u t p u t and e x p o r t s , b u t t h e y

s u f f e r from reduc t ions i n the p r i c e of o i l which are themselves a

consequence of t h e demand c r i s i s .

But t h e s e s m a l l o i l - e x p o r t e r s t o g e t h e r w i t h n o n - o i l

Arab coun t r i e s (such as Jordan or t h e Yemens) b e n e f i t i n d i r e c t l y

f rom economic growth i n t h e ma jo r e x p o r t i n g economies t h r o u g h

r e m i t t a n c e s , d i r e c t i n v e s t m e n t , t r a d e , a i d and o t h e r economic

r e l a t i o n s h i p s . The o i l demand c r i s i s is t h e r e f o r e bound t o

a f f e c t them adve r se ly even i f they themselves have no o i l .

28

I n order t o i l l u s t r a t e t h e impact on rates of economic

growth and c a p i t a l accumulat ion of t he f a l l i n o i l revenues w e

s h a l l draw on the r e s u l t s of t he very important OAFEClENI study

of economic i n t e r d e p e n d e n c e and i n t e r - A r a b c o - o p e r a t i o n .

Although the assumptions of t he OAPEC/ENI models as regards t h e

f u t u r e demand f o r and t h e p r i c e of o i l are n o t i d e n t i c a l t o ou r s ,

t h e y a r e n o t s u f f i c i e n t l y d i f f e r e n t t o j u s t i f y a r e - r u n of t h e

exerc ise . The r e s u l t s s e r v e w e l l t he purpose of i l l u s t r a t i n g the

magnitude of the l i k e l y economic impact of t h e reduct ion i n o i l

revenues.

We have taken as r e l e v a n t i n d i c a t o r s of growth the r a t e

of i n c r e a s e of n o n - o i l GDP ( s i n c e o i l i s t h e exogenous f a c t o r )

and t h e r a t e of c a p i t a l accumulation.

The fo l lowing m a y be i n f e r r e d from Tab le 3. F i r s t , t h e

impact on growth r a t e s of t h e " o i l demand c r i s i s " a l t h o u g h

v a r y i n g i n e x t e n t f r o m c o u n t r y t o c o u n t r y , t e n d s t o b e

s i g n i f i c a n t . S e c o n d l y , t h e impact i s much more s e v e r e f o r t h e

low absorbers (Kuwait, UAE, Libya and Saudi Arabia) than f o r t h e

high absorbers such as I r a q or Algeria . Th i rd ly , a s expected t h e

impact is not very g r e a t on coun t r i e s whose dependence on o i l is

e i t h e r s m a l l o r i n d i r e c t , such as Egypt and Syria .

The t e n t a t i v e conclus ion i s t h a t economic growth will

be r e t a r d e d i n t h e main Arab o i l - e x p o r t i n g c o u n t r i e s . Once

a g a i n , t h e r a t e s t h a t m a y o b t a i n i n 1985-1995 s h o u l d not b e

compared w i t h t h e v e r y h i g h pe r fo rmance of t h e 1970s . We h a v e

argued c o n s i s t e n t l y t h a t t he 1970s was an unusual per iod and t h a t

t he growth explos ion of t h a t decade i n v o l v e d many problems and

29

unfavourable s i d e e f f e c t s . Growth of non-oil GDP of the o rde r of

10-20 p e r c e n t p.a. may b e p a r t l y i l l u s o r y o r w a s t e f u l . The

r e fe rence should r a t h e r be s u s t a i n a b l e rates of 6 t o 8 per cent

which may b e c o n s i s t e n t w i t h e f f i c i e n t , non-inf l a t i o n a r y and

smooth developments. The worry is t h a t t he models suggest t h a t

t h e s e r e a s o n s b l e r e f e r e n c e r a t e s w i l l n o t b e a c h i e v e d d u r i n g

1985-1995.

The "oil demand c r i s i s " h a s a l s o b r o a d e r economic and

p o l i t i c a l i m p l i c a t i o n s . A d e e p and l o n g c r i s i s may u p s e t t h e

s o l i d a r i t y of OPEC and weaken i t s g r i p on t h e d e t e r m i n a t i o n of

world o i l p r ices . Should t h a t happen, t h e revenue l o s s e s could

b e h i g h e r t h a n p r e d i c t e d i n this p a p e r and t h e e c o n o m i c

consequences could be bleaker .

The o i l demand c r i s i s may a l s o weaken the Arab world on

t h e i n t e r n a t i o n a l p o l i t i c a l scene. O i l i s no t only a source of

revenues but an important f a c t o r of i n t e r n a t i o n a l p o l i t i c a l 1 i f e.

The weakening of OPEC may diminish the barga in ing power of Arab

c o u n t r i e s i n p o l i t i c a l f o r a p a r t i c u l a r l y v is -a -v is t he West.

Table 3: Bates of Growth of Main Economic I n d i c a t o r s 1975-1995 per cent

1975-80 1983-90 1990-95

1. Kuwait

GDP non-oil Gross c a p i t a l formation

2 . Libya kl

GDP non-oil Gross c a p i t a l formation

3. UAE

GDP non-oil Gross c a p i t a l formation

4. Saudi Arabia

GDP non-oil Gross c a p i t a l formation

5 . Alger ia

GDP non-oil Gross c a p i t a l formation

6. Iraq

GDP non-oil Gross c a p i t a l formation

GDP non-oil Gross c a p i t a l formation

8 . S y r i a

GDP non-oil Gross c a p i t a l formation

11.74 2.83 8.50 2.41 1.42 4.60

17 .OO 1.60 3.19 2.34 0.36 1.04

10.52 3.89 4.72 9.82 4.21 3.50

12.79 3.94 4.69 22.67 4.14 3 .OO

11.12 6.89 9.30 7.98 6.01 7.51

12.61 5.06 3.09 6 .27 4.38 1.13

6 .00 4.56 4.41 16.13 5 025 6.84

7.30 5.35 7.02 6.82 4.07 5 .OO

31

6. COBCwlDIBG REMARKS

O i l is an important source of w e a l t h f o r t he Arab world

and i t s in f luence extends to t h e whole reg ion - o i l - expor t e r s and

n o n - o i l economies a l i k e . The w o r l d p e t r o l e u m m a r k e t h a s gone

through dramatic convuls ions i n the 1970s and e a r l y 1980s. The

c y c l e of ups and downs i s unusual ly long w i t h an upswing phase of

1 5 t o 20 y e a r s and a downswing which may w e l l e x t e n d o v e r 10 o r

1 5 years .

Because of t h e unique dependence of t h e Arab economy on

t h i s f a c t o r t h e impact of s u c h a l o n g and v i o l e n t c y c l e can b e

e x t r e m e l y d i s t u r b i n g . OPEC power which m a n i f e s t e d i t s e l f so

d r a m a t i c a l l y i n t h e 1970s o v e r p r i c e s i s c o n s t r a i n e d i n o t h e r

respec ts . OPEC has not been a b l e to r e g u l a t e t h e c y c l e in order

t o smooth o u t p r o d u c t i o n movements. The d e p l e t i o n r a t e of o i l

has been imposed by o u t s i d e f a c t o r s on t h e OPEC c o u n t r i e s , y e t

t he d e p l e t i o n ra te is a a most c r i t i c a l f a c t o r i n terms of long-

term d e v e l o p m e n t p l a n n i n g . The upswing and t h e o i l p r i c e

e x p l o s i o n e n t a i l e d many i m p o r t a n t b e n e f i t s as w e l l a s a few

troublesome costs. The downswing i n v o l v e s some bene f i t s , which

we have d u l y recognized, but a l s o cons ide rab le costs .

Governments, however, are not t o t a l l y powerless i n t h i s

c u r r e n t a d v e r s e s i t u a t i o n . They c o u l d a t t e m p t t o t a k e b e t t e r

advantage of t he p o t e n t i a l developmental b e n e f i t s of a f a l l i n

revenues and reduce the l o s s e s by adopt ing appropr i a t e f i s c a l and

i n v e s t m e n t p o l i c i e s . They s h o u l d a l s o do t h e i r u tmost t o keep

OPEC toge the r during the d i f f i c u l t c r i s e s which m a y l i e ahead of

us. A f a i l u r e on t h a t s c o r e will compound f u t u r e p rob lems and

losses . I n t h i s c o n t e x t O P E C s h o u l d t a k e a c l o s e look a t i t s

r o l e a s r e s i d u a l s u p p l i e r , renew t h e i r e f f o r t s t o i n v o l v e non-

OPEC e x p o r t e r s i n t h i s r o l e , and des ign a more s o p h i s t i c a t e d o i l

po l i cy than the single-minded defense of the o i l p r i c e l ine . It

i s as important t o a t tempt some management of t h e demand f o r o i l

a s i t i s t o d e f e n d t h e o i l p r i c e l e v e l . O t h e r w i s e OPEC member

c o u n t r i e s would c o n t i n u e t o f a l l v i c t i m t o s e v e r e c y c l i c a l

movements which can d e s t a b i l i z e t h e i r economies and t h e i r

s o c i e t i e s . F i n a l l y , t h e most i m p o r t a n t task i s t o d e f i n e t h e

o b j e c t i v e s and t h e d e s i r e d p a t t e r n of economic deve lopmen t .

I n t h e end o i l w i l l be d e p l e t e d and we s h a l l b e l e f t w i t h t h e

economic d e v e l o p m e n t s a c h i e v e d t h r o u g h t h e e x p e n d i t u r e of

revenues. In the long-run economic development is a l l t h e t

mat ters . The opportuni ty of t ak ing a completely new look a t t h i s

i s s u e is now w i t h us. I t would be a p i t y t o m i s s i t .

33

OXFORD INSTlTUTE FOR ENERGY STUDIES 57 WOODSTOCK ROAD, OXFORD OX2 6FA ENGLAND

TELEPHONE (01865) 311377 FAX (01865) 310527

E-mail: pu [email protected] rg http:Ilwww.oxfordenerg y.org