Embed Size (px)

Citation preview

The cost of equity for RIIO-2

A review of the evidence

Prepared for Energy Networks Association

28 February 2018

www.oxera.com

Oxera Consulting LLP is a limited liability partnership registered in England no. OC392464, registered office: Park Central, 40/41 Park End Street, Oxford OX1 1JD, UK; in Belgium, no. 0651 990 151, registered office: Avenue Louise 81, 1050 Brussels, Belgium; and in Italy, REA no. RM - 1530473, registered office: Via delle Quattro Fontane 15, 00184 Rome, Italy. Oxera Consulting GmbH is registered in Germany, no. HRB 148781 B (Local Court of Charlottenburg), registered office: Rahel-Hirsch-Straße 10, Berlin 10557, Germany.

Although every effort has been made to ensure the accuracy of the material and the integrity of the analysis presented herein, Oxera accepts no liability for any actions taken on the basis of its contents.

No Oxera entity is either authorised or regulated by the Financial Conduct Authority or the Prudential Regulation Authority within

the UK or any other financial authority applicable in other countries. Anyone considering a specific investment should consult their own broker or other investment adviser. Oxera accepts no liability for any specific investment decision, which must be at the investor’s own risk.

© Oxera 2018. All rights reserved. Except for the quotation of short passages for the purposes of criticism or review, no part may be used or reproduced without permission.

The cost of equity for RIIO-2 Oxera

Contents

Executive summary 1

1 Introduction 9

2 Market parameters: the risk-free rate, total market return, and equity risk premium 11

2.1 Risk-free rate 11 2.2 Total market return and equity risk premium 14 2.3 Conclusion 33

3 Risk and beta 36

3.1 Choice of comparators 36 3.2 Technical estimation issues 38 3.3 Gearing and the relationship between equity beta and asset

beta 40 3.4 Estimation results 40 3.5 Concluding remarks: risk and CAPM-based beta estimates 44

4 Required equity returns for RIIO-2 46

4.1 Reducing the risk of underinvestment 46 4.2 Providing a stable framework for long-term investment 47 4.3 Summary of the CAPM cost of equity estimates 47

5 Alternative sources of evidence 49

5.1 Asset risk premium 49 5.2 Individual stock dividend discount model 49 5.3 Regulatory precedent 50 5.4 Conclusion 54

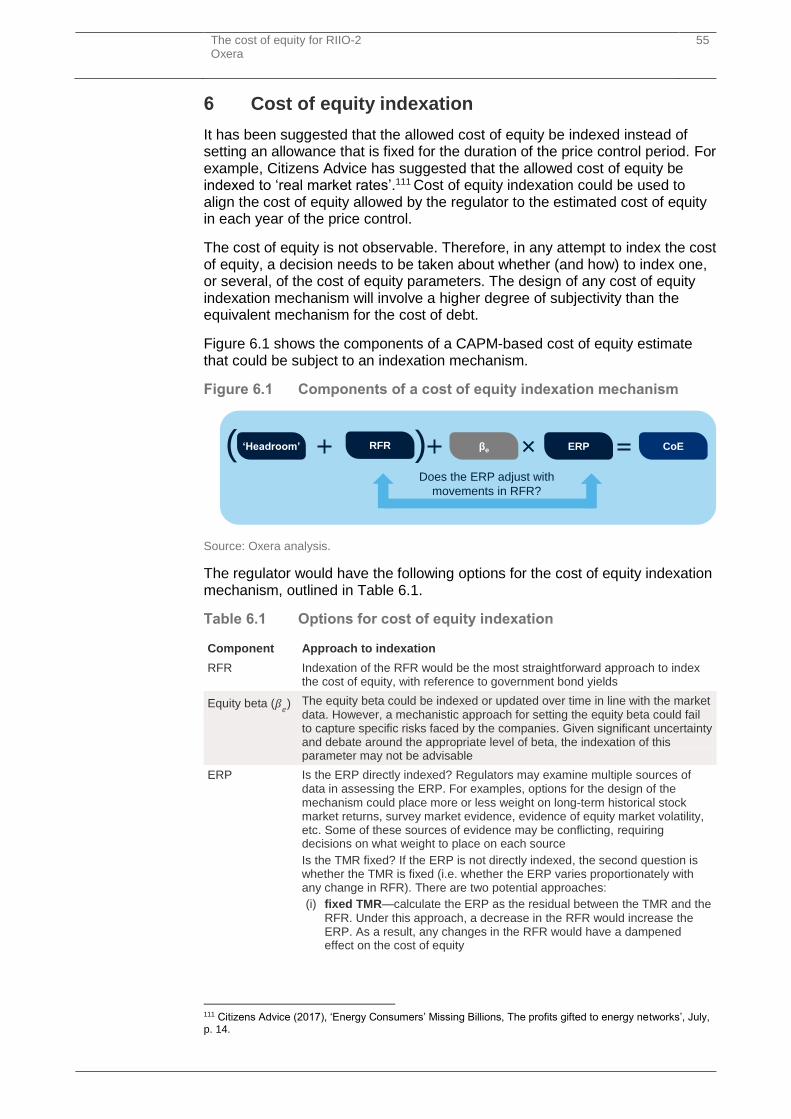

6 Cost of equity indexation 55

6.1 Indexation of the market parameters 56 6.2 Conclusion 57

A1 Methodologies for estimating the cost of equity 58

A1.1 The capital asset pricing model 58 A1.2 Conclusion 60

The cost of equity for RIIO-2 Oxera

3

Figures and tables

Box 2.1 Geometric versus arithmetic means 19

Box A1.1 The capital asset pricing model 58

Box A1.2 Arbitrage pricing theory 59

Box A1.3 Fama–French three-factor model 60

Figure 2.1 Nominal spot rates on government bonds 11

Figure 2.2 Nominal and real forward rates derived from the nominal yield curve and a 3.0% inflation rate 12

Figure 2.3 UK government bond yields: historical volatility 13

Figure 2.4 UK real TMR, 1900–2016 21

Figure 2.5 Real TMR vs real interest rates: DMS analysis, 1900–2012 21

Figure 2.6 Real TMR versus real interest rates: Oxera analysis, 1900–2012 22

Figure 2.7 TMR (nominal) survey data for the USA: Graham & Harvey study 24

Figure 2.8 ERP survey data from Fernandez et al. for the UK and USA 25

Figure 2.9 3i Infrastructure portfolio-weighted average discount rate 25

Figure 2.10 INPP risk capital-weighted average discount rate 26

Figure 2.11 Nominal TMR and ERP based on a DDM for the FTSE All-share index 28

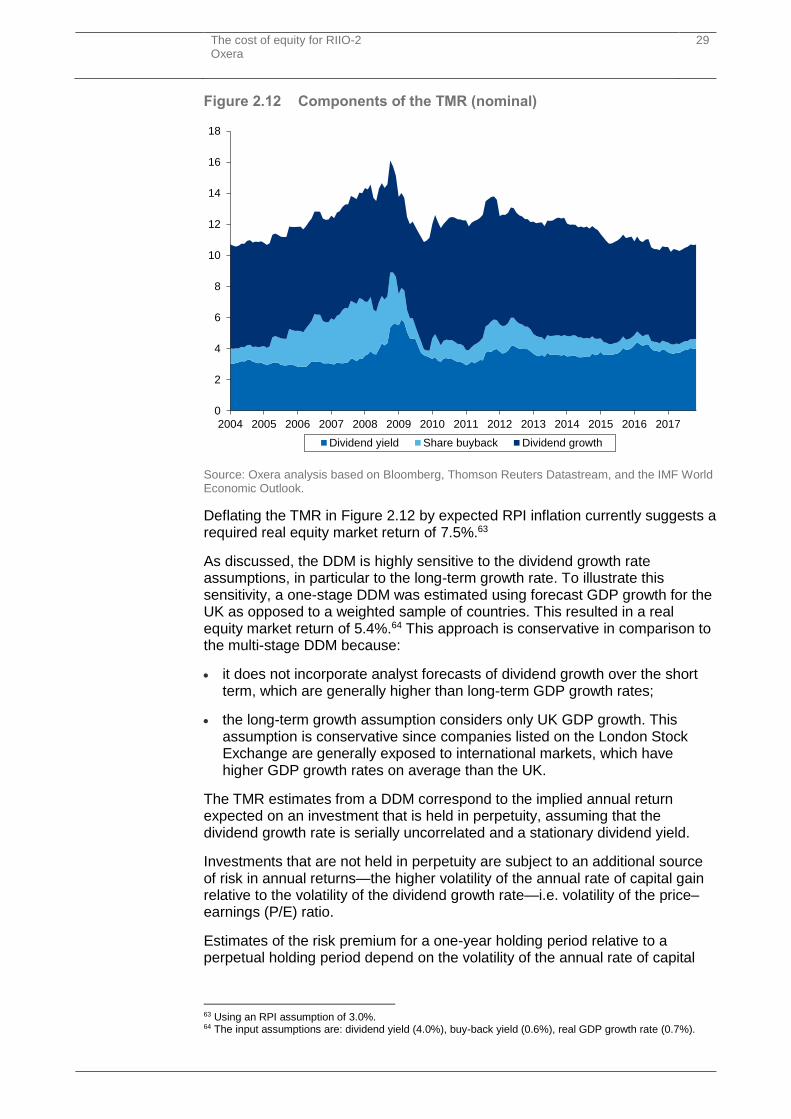

Figure 2.12 Components of the TMR (nominal) 29

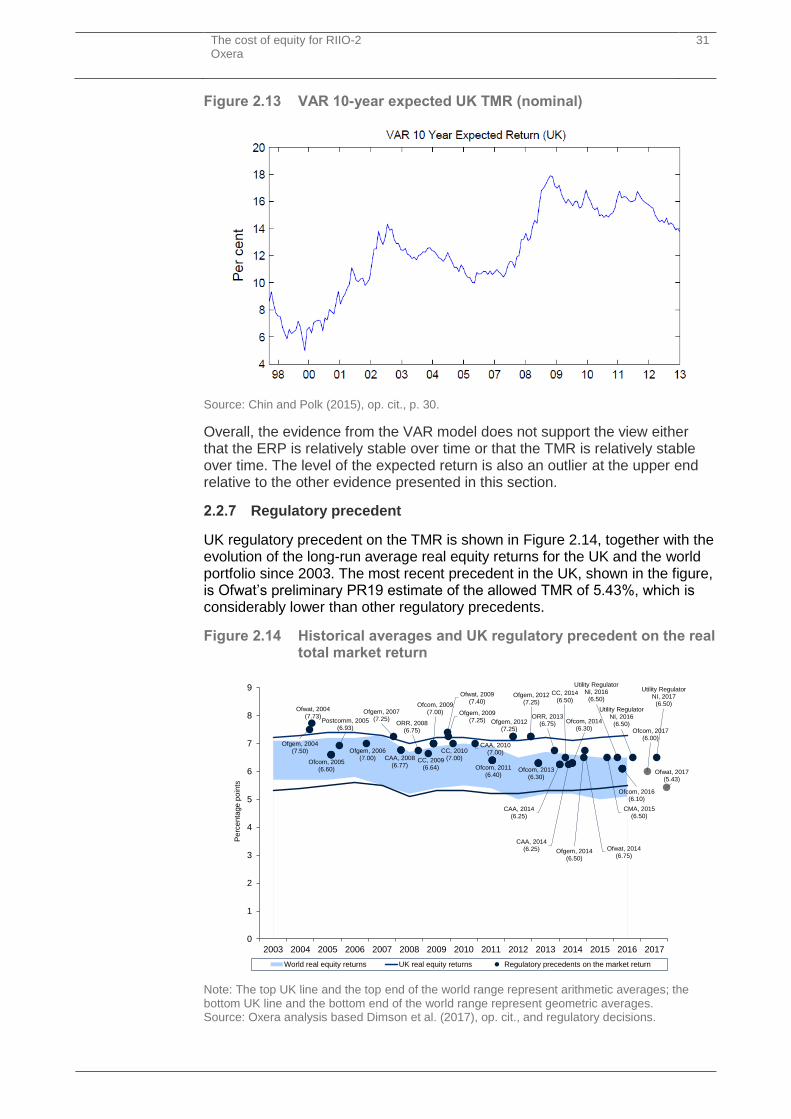

Figure 2.13 VAR 10-year expected UK TMR (nominal) 31

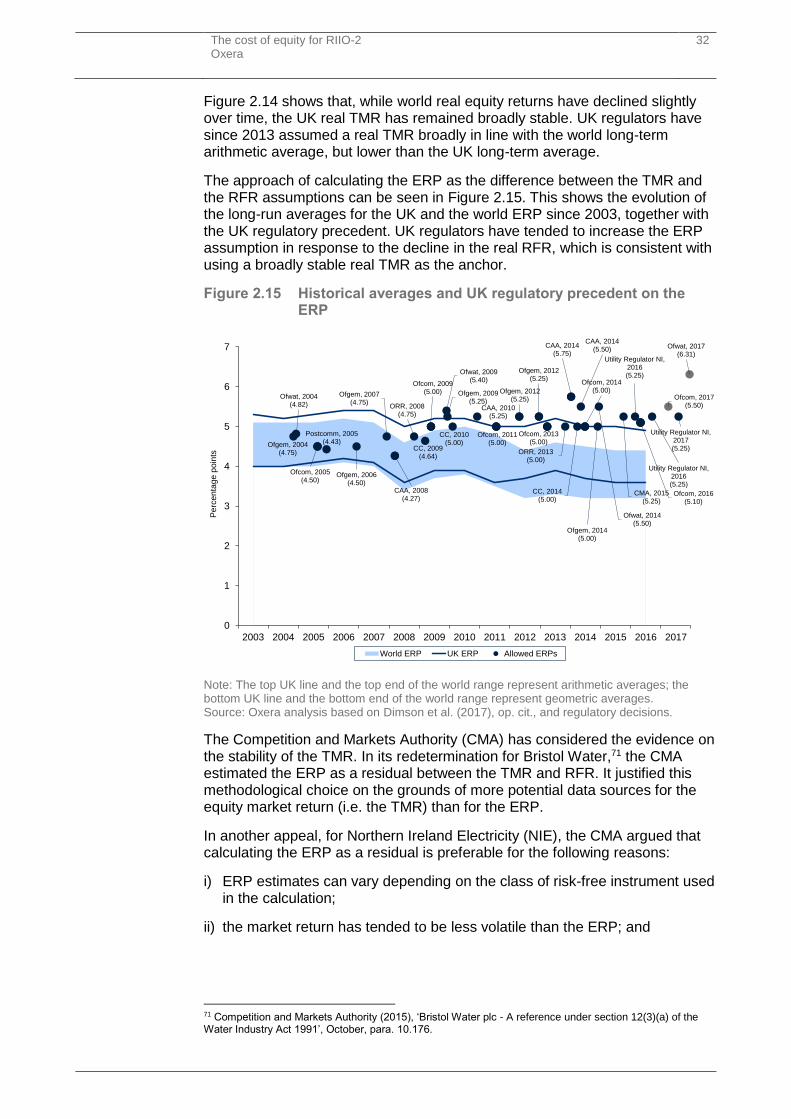

Figure 2.14 Historical averages and UK regulatory precedent on the real total market return 31

Figure 2.15 Historical averages and UK regulatory precedent on the ERP 32

Figure 3.1 Daily asset betas (two years) for listed UK comparator companies and Centrica 41

Figure 3.2 Daily asset betas (2 years) for listed European comparator companies 43

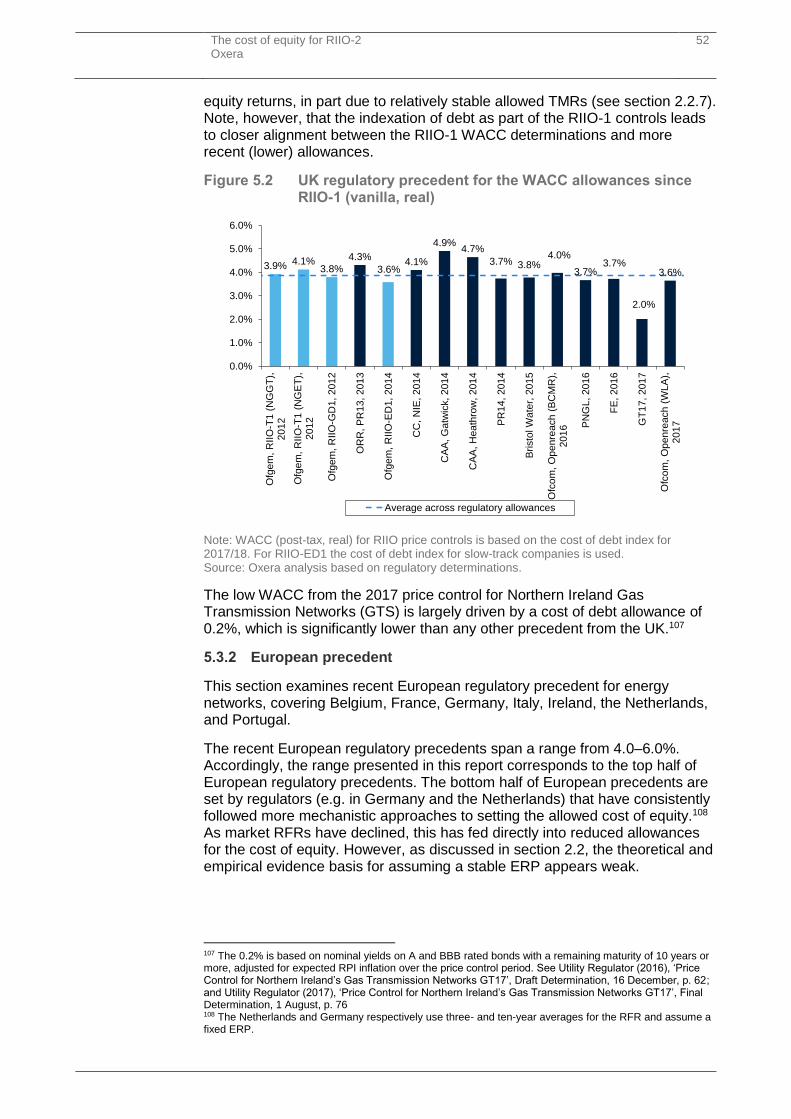

Figure 5.1 UK regulatory precedent for the allowed cost of equity since RIIO-1 (post-tax, real) 51

Figure 5.2 UK regulatory precedent for the WACC allowances since RIIO-1 (vanilla, real) 52

Figure 5.3 European regulatory precedent for the cost of equity (post-tax, real) 53

Figure 5.4 European regulatory precedent for the WACC (vanilla, real) 53

Figure 5.5 Allowed return on equity for US investor-owned electric utilities (nominal) 54

Figure 6.1 Components of a cost of equity indexation mechanism 55

Table 2.1 Historical data on the UK economy and financial markets 17

Table 2.2 Model-based estimates of the historical market return 18

The cost of equity for RIIO-2 Oxera

4

Table 3.1 Liquidity measures for European comparators 38

Table 3.2 Equity and asset beta estimates for UK comparators (debt beta = 0.05) 42

Table 3.3 Equity and asset beta estimates for European comparators (debt beta = 0.05) 44

Table 4.1 Cost of equity for RIIO-2 (real, RPI-deflated) 47

Table 5.1 DDM cost of equity estimates (%) 49

Table 6.1 Options for cost of equity indexation 55

The cost of equity for RIIO-2 Oxera

1

Executive summary

In preparation for the upcoming RIIO-2 electricity and gas transmission and distribution price controls, the Energy Networks Association (ENA) has commissioned Oxera to provide advice on issues relating to the cost of equity.

This report sets out a framework for applying the capital asset pricing model (CAPM) in the context of setting allowed returns for long-lived network investments during RIIO-2. The estimated range for the required equity returns based on the CAPM is compared against alternative sources of evidence on the cost of equity.

There are a number of challenges when determining appropriate estimates of the parameters of the CAPM for RIIO-2. For example:

how to translate from current market data on government bond yields into a risk-free rate (RFR) assumption that will remain valid for the period up to at least 2026 and potentially as far as 2031;1

how to account for the possibility that ‘flight to safety’ effects have increased the equity risk premium (ERP) and thereby mitigated the impact of low RFRs on the expected equity market return;

how to determine an asset beta when the only UK energy network with an equity market listing (National Grid) derives less than half of its revenues from businesses regulated under the RIIO framework.

The way these challenges have been addressed in this report is summarised below. This report also considers some of the implications for the concept of indexing the allowance for the cost of equity, rather than fixing the allowance for the duration of the price control period.

The start of RIIO-2 is more than three years away, therefore the analysis provided in this report is based on current data and may alter by the time the next price controls start.

Risk-free rate

Real, RPI-deflated rates on government bonds of ten-year maturity are currently negative, at around -1.5%. Throughout the expected period of the RIIO-2 price controls (2021–31), the implied forward rate is around -0.5% on average. While interest rates are low, they exhibit marked volatility, such that setting the allowed RFR for RIIO-2 exactly equal to the level of forward rates may not be appropriate. This consideration is especially relevant in the context of current unusual monetary policy and uncertainty in relation to the pace and timing of future changes in the quantitative easing programme and its resulting effect on interest rates.

As the start of RIIO-2 is over three years away, an initial estimate for the RFR (real, RPI-deflated) of -0.5 to 0.0% appears appropriate based on forward rates and allowing for volatility and uncertainty. We suggest that the evidence is monitored to ensure that it is incorporated into the final estimate of the cost of equity for RIIO-2, although it will still be necessary to allow for uncertainty regarding market developments during the RIIO-2 price control period.

1 RIIO-T2/GD2 starts in 2021 and RIIO-ED2 starts in 2023. These controls would finish in 2029 and 2031 respectively if the length of the control period remains eight years.

The cost of equity for RIIO-2 Oxera

2

The estimation of the RFR cannot be considered in isolation from the ERP. A central conclusion of this report is that the RFR and ERP are negatively correlated, with the result that the total market return (TMR) is more stable than the ERP alone.

Equity risk premium and total market return

Forming a precise view on the real expected TMR is made challenging by the wide range of estimates from the various sources of evidence. The central issue in the current debate over the TMR is the degree to which the expected ERP adjusts to offset changes in the RFR. The theoretical and empirical evidence basis for assuming a stable ERP appears weak.

Consumption-based asset pricing models find that higher economic uncertainty simultaneously places downward pressure on the RFR and upward pressure on the ERP.2

Historical data shows that the RFR and ERP have been very volatile while total equity market returns have been relatively more stable over time, and calls into question the assertion that equity markets are going through a period of ‘secular stagnation’.3

Estimates from dividend discount models (DDMs) suggest that the TMR is relatively stable over time and is currently no lower than its estimated value in the early 2000s.

The reliability of survey evidence and discount rate assumptions used by infrastructure funds is lower than more direct market evidence, but is inconclusive about whether the ERP or the TMR is the more stable parameter.

This suggests that an appropriate TMR assumption would place more weight on the view that the expected TMR is relatively stable, and close to its long-run average of 7.3%,4 than the view that the ERP is close to its long-run average of 4.9% (implying a TMR of 4.4% when combined with forward interest rates, which are on average -0.5% for the RIIO-2 period).5

Attenuation of the upper end of the range—the version of the DDM used by the Bank of England (BoE) indicates a real TMR of at least 7.5%, while the historical arithmetic average of the real TMR from Dimson, Marsh and Staunton (DMS) is 7.3%.6 It might be argued that some weight should be given to the view that the increase in the ERP has not fully offset the decline in the RFR, and as a result, for the purpose of establishing a range for RIIO-2, an attenuated TMR of up to 6.5% is assumed. This is approximately 80bp lower than would be justified by the historical average of the real TMR and 100bp lower than justified by the version of the DDM used by the BoE. The top end of the range is therefore lower than implied by the view that the TMR is completely stable.

Attenuation of the lower end of the range—the historical average of the ERP from DMS (4.9%) combined with forward rates, which are on average -0.5% for the RIIO-2 period, suggests a TMR of 4.4%. It appears likely that

2 Martin, I. (2013), ‘Consumption-Based Asset Pricing with Higher Cumulants’, Review of Economic Studies, 80, pp. 746; Vlieghe, G. (2017), ‘Real interest rates and risk’, Society of Business Economists' Annual conference, 15 September. 3 Òscar, J., Knoll, K., Kuvshinov, D., Schularick, M. and Taylor, A. (2017), ‘The Rate of Return on Everything, 1870–2015’, Federal Reserve Bank of San Francisco Working Paper 2017-25, p. 41. 4 Dimson, E., Marsh, P. and Staunton, M. (2017), 'Credit Suisse Global Investment Returns Yearbook 2017', p. 14. 5 Ibid., p. 31. 6 Ibid., p. 14.

The cost of equity for RIIO-2 Oxera

3

the decrease in the RFR has been associated with an increase in the ERP, and as a result, for the purpose of RIIO-2, an attenuated lower bound of the TMR of 5.5% appears more appropriate. This would position the TMR assumption approximately 110bp higher than would be justified by the historical average of the real ERP combined with forward rates. The lower end of the range is therefore higher than implied by the view that the ERP is completely stable.

This provides an attenuated range of 5.5–6.5% for the real (RPI-deflated) TMR. In combination with an RFR assumption of -0.5–0.0%, this would imply an ERP of 6.0–6.5%. This attenuation of the range has been broadly symmetric and does not take adequate account of the weight of evidence in support of a relatively stable TMR. If the range had not been attenuated, it would have been 4.4–7.4%7 with a midpoint of 5.9%, compared to a 6.0% midpoint of the attenuated range. In light of the fact that both the financial theory and the empirical evidence support a relatively stable TMR with an estimate towards the top end of the range (6.5%), we recommend a range of 6.0–6.5% for the TMR (real, RPI-deflated). Combined with the preliminary recommended range of -0.5–0.0% for the RFR (real, RPI-deflated), this implies an ERP of 6.5%, taking the midpoints of these two parameters.

Selecting a TMR towards the top end of the range is consistent with the view of the Competition Commission in the Northern Ireland Electricity (2014) price control appeal, where a point estimate at the top end of the range for the weighted average cost of capital (WACC) was selected.8 One of the reasons for this choice of point estimate was that the CC was less confident in the numbers at the low end of the TMR range.9

13.187 We consider that the lower bound of 5 per cent for the expected return on the market was less well supported than the upper end of the range of 6.5 per cent. We consider that the weight of evidence tended to support numbers between 5.5 and 6.5 per cent for the expected market return. While we decided to retain 5 per cent as a possibility, we were less confident with this estimate and, as a corollary, with numbers at the low end of the WACC range.

This view was reaffirmed in the Bristol Water (2015) appeal.10

In summary, the updated evidence presented in this report suggests that a range of 6.0–6.5% for the TMR (real, RPI-deflated) is appropriate for RIIO-2.

Risk and beta

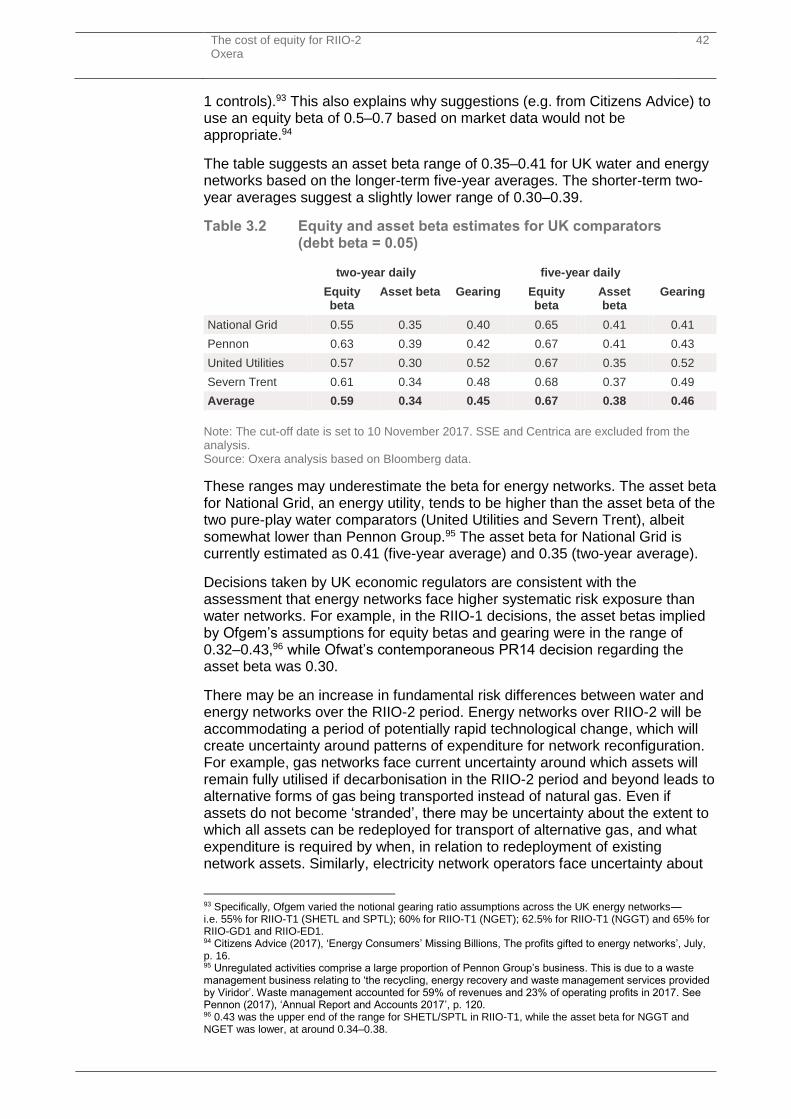

The sample of National Grid and three listed water companies produces a range of estimates for the asset beta (un-levered equity beta) of 0.35–0.41 based on the longer-term five-year averages. This assumes a debt beta of 0.05. The shorter-term two-year averages suggest a lower range, of 0.30–0.39, which highlights the sensitivity of the estimates to the choice of measurement period.

These ranges may underestimate the beta for energy networks. The asset beta for National Grid, an energy utility, tends to be higher than that of the two pure-

7 The lower bound (4.4%) is the long-run arithmetic average ERP from Dimson et al. (2017) plus an average forward interest rate of -0.5% for the RIIO-2 period. The upper bound (7.4%) is the average of the long-run arithmetic average TMR (7.3%) from Dimson et al. (2017) and the TMR from the BoE’s DDM (7.5%). 8 Competition Commission (2014), ‘Northern Ireland Electricity Limited; A reference under Article 15 of the Electricity (Northern Ireland) Order 1992’, 26 March, para. 13.187. 9 Competition Commission (2014), op. cit., paras 13.87 and 13.189. 10 Competition and Markets Authority (2015), ‘Bristol Water plc; A reference under Section 12 of the Water Industry Act 1991’, 6 October, para. 10.185.

The cost of equity for RIIO-2 Oxera

4

play water comparators (United Utilities and Severn Trent), and is currently estimated as 0.41 (five-year average) and 0.35 (two-year average).

Decisions taken by UK economic regulators are consistent with the assessment that energy networks face higher systematic risk exposure than water networks. For example, in the RIIO-1 decisions, the asset betas implied by Ofgem’s assumptions for equity betas and gearing were in the range of 0.32–0.43,11 while Ofwat’s contemporaneous PR14 decision regarding the asset beta was 0.30.

There may be an increase in fundamental risk differences between water and energy networks over the RIIO-2 period. Energy networks over RIIO-2 will be accommodating a period of potentially rapid technological change, which will create uncertainty around patterns of expenditure for network reconfiguration. It is unlikely that exposure to such risks can be fully mitigated through regulatory mechanisms (e.g. indexation, pass-through, volume drivers, re-openers, etc.). The residual risk will be borne by equity.

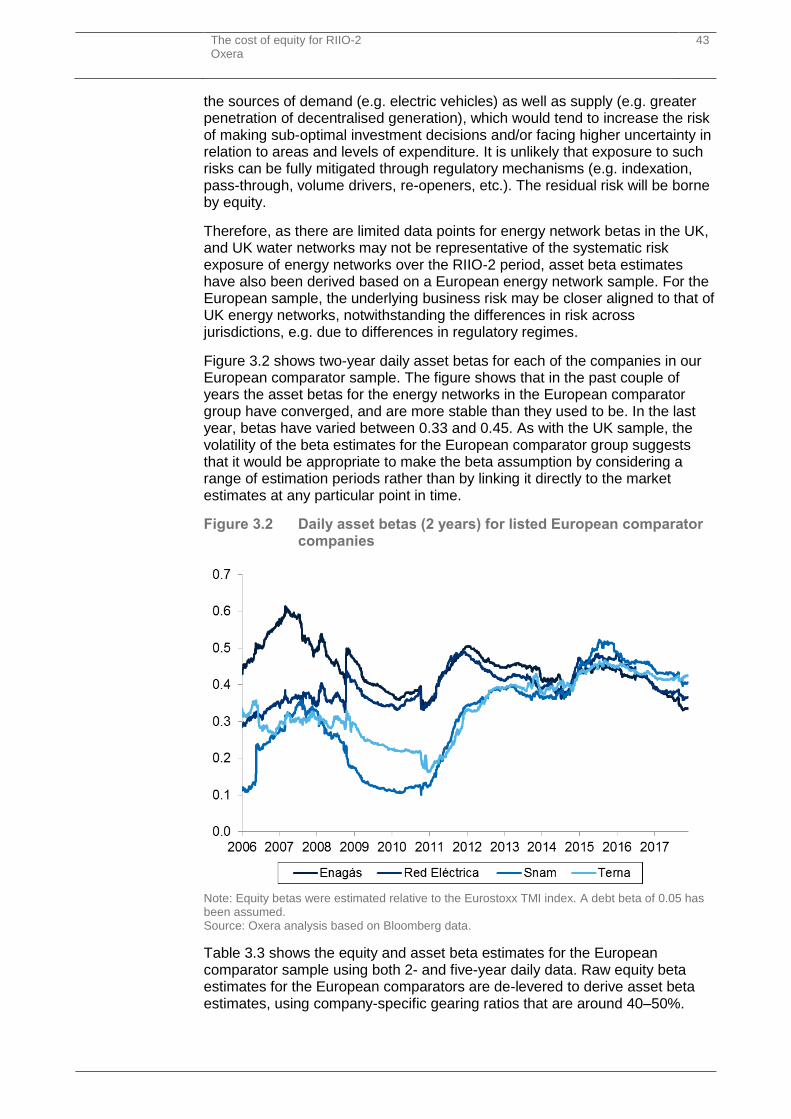

Therefore, as there are limited data points for energy network betas in the UK, and UK water networks may not be representative of the systematic risk exposure of energy networks over the RIIO-2 period, asset beta estimates have also been derived based on a European sample, where the business risk may be closer aligned to that of UK energy networks, notwithstanding the differences in risk across jurisdictions—e.g. due to differences in regulatory regimes. Asset betas for a sample of four European energy networks (Enagas, Red Eléctrica, Snam, Terna) have been assessed, and are in the range of 0.40–0.45 based on the longer-term five-year averages. As with the UK sample, this assumes a debt beta of 0.05. The shorter-term two-year averages suggest a lower range of 0.33–0.42. This points towards a higher asset beta for energy networks compared with the water companies that dominate the UK sample.

On balance, the evidence from the UK and European samples and the five- and two-year averages suggests an attenuated asset beta range of 0.38–0.42. This is consistent with energy networks having greater exposure to risk than water companies.

Tests of the empirical performance of the CAPM have revealed many ‘anomalies’ that suggest that the accuracy of the standard CAPM in predicting the cost of equity decreases the further away the equity beta is from unity.12 In particular, the CAPM tends to under-predict returns for companies with equity betas lower than one. As the comparator companies used in this report have equity betas significantly lower than one when measured at market levels of gearing, adopting an asset beta estimate in the top half of the range would provide some offset to this downward bias.

Furthermore, the literature on arbitrage pricing theory and multi-factor models suggests that there could be systematic risk factors that are not picked up in the CAPM market beta but are nevertheless priced by investors.13 The impact of the wider risk environment faced by energy networks can be accounted for

11 0.43 was the upper end of the range for SHETL/SPTL in RIIO-T1, while the asset beta for NGGT and NGET was lower, at around 0.34–0.38. 12 Asness, C., Moskowitz, T.J. and Pedersen, L.H. (2013), ‘Value and momentum everywhere’, The Journal of Finance, LXVIII:3; Fama, E. and French, K. (2015), ‘Dissecting Anomalies with a Five-Factor Model’, The Review of Financial Studies, 29:1, 1 January 2016, pp. 69–103. 13 Chen, N., Roll, R. and Ross, S. (1986), ‘Economic Forces and the Stock Market’, The Journal of Business, 59:3, pp. 383–403; Ross, S. (1976), ‘The Arbitrage Theory of Capital Asset Pricing’, Journal of Economic Theory, 13, pp. 341–360.

The cost of equity for RIIO-2 Oxera

5

when interpreting the outputs from the CAPM. In the context of UK energy networks, the extent and nature of the changes required to both electricity and gas distribution, and transmission, networks to facilitate energy decarbonisation and the necessary innovations in technologies required have created uncertainty over the future configuration of the energy system.

Consideration of the risks facing energy networks and the empirical shortcomings of the CAPM suggests selecting a beta point estimate in the top half of the attenuated range based on listed comparator companies. We recommend a range of 0.40–0.42 to inform the asset beta assumption for RIIO-2.

The asset beta range has been derived from comparator companies with gearing broadly in the range of 40–50% based on market values. The RIIO-1 price control decisions assumed gearing of 55–65% relative to the regulatory asset value (RAV), which was applied in the calculation of the WACC.14 Therefore, the cost of equity has been calculated in this report using a midpoint gearing assumption of 60% to re-lever the asset beta range. This is to achieve consistency with the second proposition of Modigliani and Miller (1958):

the expected yield of a share of stock is equal to the appropriate [expected rate of return] for a pure equity stream in the class, plus a premium related to financial risk equal to the debt-lo-equity ratio times the spread between [the expected rate of return] and [the risk-free rate of interest].15

With a gearing assumption of 60% and a debt beta assumption of 0.05, an equity beta range of 0.93–0.98 is recommended for RIIO-2.

The higher the notional gearing relative to the gearing ratios for the comparator companies used to derive the asset beta range, the more sensitive the estimation of the re-levered equity beta is to the assumed relationship between debt beta and gearing. Due to this additional estimation uncertainty we therefore do not include a 65% gearing ratio within our recommended range in this report. Were a 65% gearing ratio to be used in RIIO-2 we would expect the equity betas to be higher than the range set out above, but not as high as a simple application of a re-levering formula would imply and would be expected to be close to 1.

Required equity returns for RIIO-2

A range of 5.51–6.34% is recommended to inform the assumption for the real (RPI-deflated) cost of equity in RIIO-2. This takes account of the following factors when moving from the attenuated range to a recommended range.

the attenuated range does not take full account of the weight of evidence in support of a relatively stable TMR;

the attenuated range relies on equity betas estimated for comparator companies that are significantly less than unity. Empirical tests find that the CAPM tends to under-predict returns for companies with equity betas lower than one;

14 Specifically, Ofgem varied the notional gearing ratio assumptions across the UK energy networks—55% for RIIO-T1 (SHETL and SPTL); 60% for RIIO-T1 (NGET); 62.5% for RIIO-T1 (NGGT) and 65% for RIIO-GD1 and RIIO-ED1. 15 Modigliani, F. and Miller, M. (1958), ‘The Cost of Capital, Corporation Finance and the Theory of Investment’, The American Economic Review, 48:3, June, p. 271.

The cost of equity for RIIO-2 Oxera

6

the attenuated range may not fully reflect the wider risk environment faced by energy networks—in particular, the relatively high exposure of the sector to technological and political risks.

When selecting a point estimate within the recommended range, it is important to balance the long-term cost of potentially creating an underinvestment problem against the short-term cost of setting customer prices that are unnecessarily high.

Furthermore, regulated networks make investment decisions and receive returns over very long horizons spanning multiple price control periods, which would be supported by a regulatory regime that has a stable methodology and limits volatility in allowed returns from one price control period to the next. Limiting the change in the allowed return on equity for the RIIO-2 controls compared with the RIIO-1 controls would support long-term investment decisions.

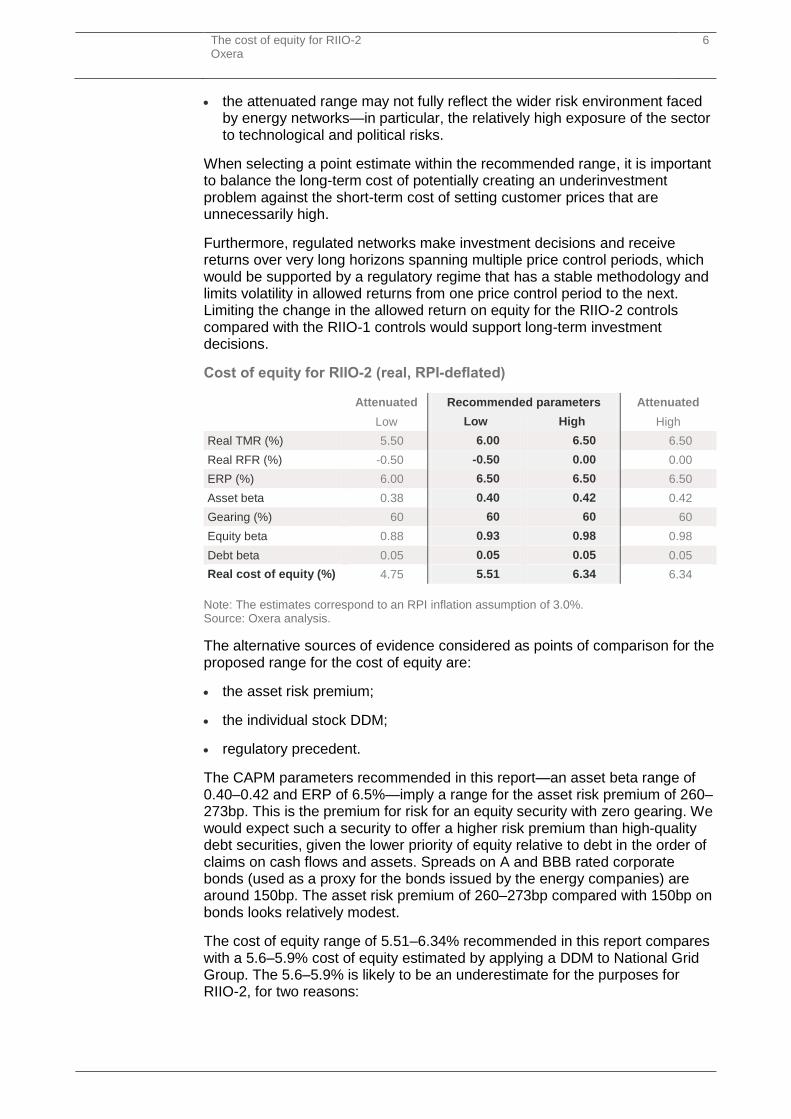

Cost of equity for RIIO-2 (real, RPI-deflated)

Attenuated Recommended parameters Attenuated

Low Low High High

Real TMR (%) 5.50 6.00 6.50 6.50

Real RFR (%) -0.50 -0.50 0.00 0.00

ERP (%) 6.00 6.50 6.50 6.50

Asset beta 0.38 0.40 0.42 0.42

Gearing (%) 60 60 60 60

Equity beta 0.88 0.93 0.98 0.98

Debt beta 0.05 0.05 0.05 0.05

Real cost of equity (%) 4.75 5.51 6.34 6.34

Note: The estimates correspond to an RPI inflation assumption of 3.0%. Source: Oxera analysis.

The alternative sources of evidence considered as points of comparison for the proposed range for the cost of equity are:

the asset risk premium;

the individual stock DDM;

regulatory precedent.

The CAPM parameters recommended in this report—an asset beta range of 0.40–0.42 and ERP of 6.5%—imply a range for the asset risk premium of 260–273bp. This is the premium for risk for an equity security with zero gearing. We would expect such a security to offer a higher risk premium than high-quality debt securities, given the lower priority of equity relative to debt in the order of claims on cash flows and assets. Spreads on A and BBB rated corporate bonds (used as a proxy for the bonds issued by the energy companies) are around 150bp. The asset risk premium of 260–273bp compared with 150bp on bonds looks relatively modest.

The cost of equity range of 5.51–6.34% recommended in this report compares with a 5.6–5.9% cost of equity estimated by applying a DDM to National Grid Group. The 5.6–5.9% is likely to be an underestimate for the purposes for RIIO-2, for two reasons:

The cost of equity for RIIO-2 Oxera

7

the DDM analysis is based on market gearing (net debt/enterprise value) in the range of 40–50%. To inform a RIIO-2 assumption, the cost of equity estimates would need to be re-levered using the regulatory gearing assumption, which, based on the RIIO-1 controls, is likely to be closer to 60%;

the long-term forecasts for UK GDP growth that have been used as an input to the company-specific DDM may be lower than company-specific dividend growth. For example, the real rate of growth observed for the RAV of National Grid Electricity Transmission during RIIO-T1 (around 4% per annum) has exceeded UK GDP growth.

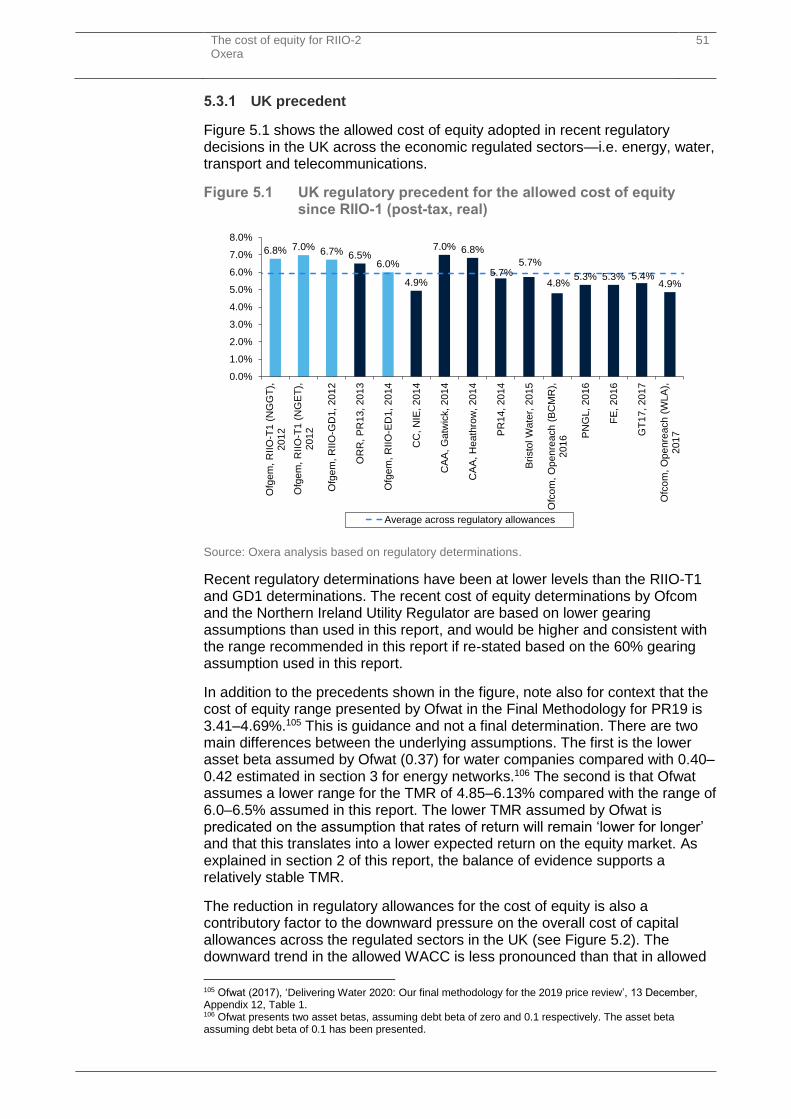

The recent cost of equity determinations by Ofcom and the Northern Ireland Utility Regulator are based on lower gearing assumptions than used in this report, and would be higher and consistent with the range recommended in this report if re-stated based on the 60% gearing assumption used in this report.

The cost of equity range presented by Ofwat in the Final Methodology for PR19 is 3.41–4.69%.16 This is guidance and not a final determination. There are two main differences between the underlying assumptions. The first is the lower asset beta assumed by Ofwat (0.37) for water companies compared with 0.40–0.42 estimated in this report for energy networks.17 As explained in this report, the evidence from betas of comparator energy networks, and the exposure of energy networks to uncertainty relating to energy decarbonisation and the necessary innovations in technologies required, support the use of a higher asset beta relative to water companies. The second is that Ofwat assumes a lower range for the TMR of 4.85–6.13% compared with the range of 6.0–6.5% assumed in this report. The lower TMR assumed by Ofwat is predicated on the assumption that rates of return will remain ‘lower for longer’ and that this translates into a lower expected return on the equity market. As explained in this report, the balance of evidence supports a relatively stable TMR.

Recent European regulatory precedents on the cost of equity span a range from 4.0% to 6.0% (post-tax, real). The range presented in this report corresponds to the top half of European regulatory precedents. The bottom half of European precedents are set by regulators (e.g. in Germany and the Netherlands) that have consistently followed more mechanistic approaches to setting the allowed cost of equity. The Netherlands and Germany respectively use three- and ten-year averages for the RFR and assume a fixed ERP. As market RFRs have declined, this has fed directly into reduced allowances for the cost of equity. As discussed in section 2.2, the theoretical and empirical evidence basis for assuming a stable ERP appears weak.

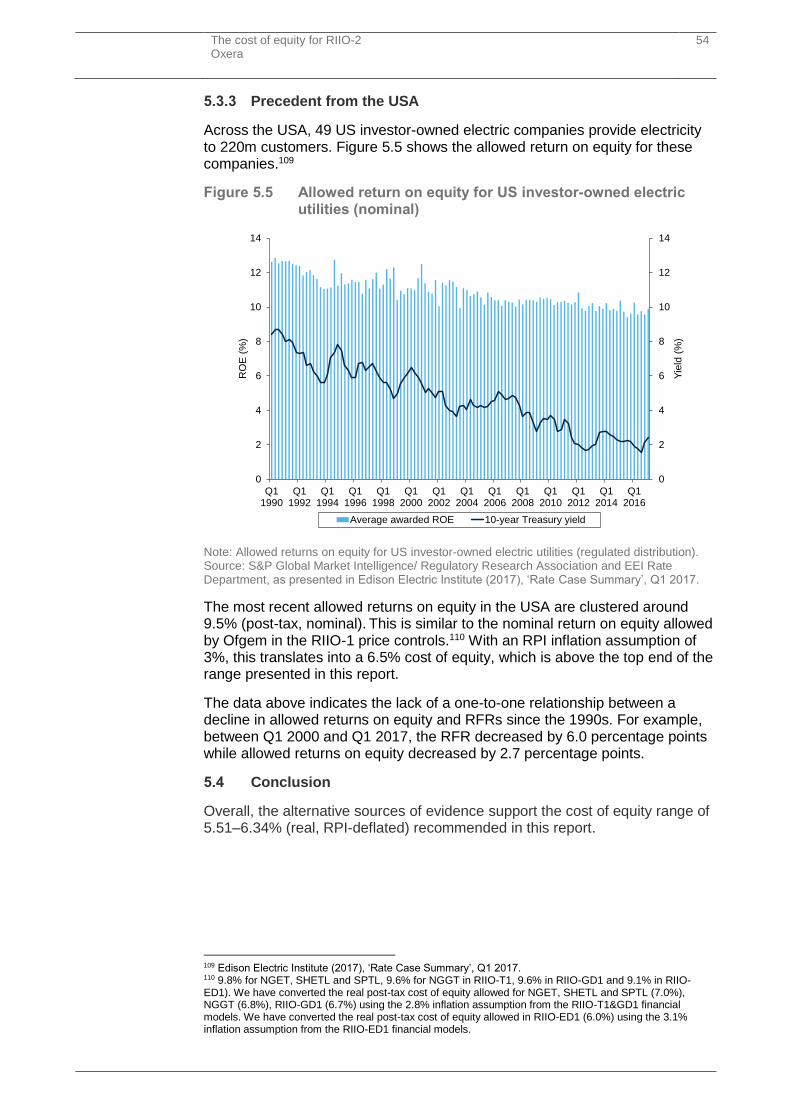

The most recent allowed returns on equity in the USA are clustered around 9.5% (post-tax, nominal). This is similar to the nominal return on equity allowed by Ofgem in the RIIO-1 price controls. With an RPI inflation assumption of 3%, this translates into a 6.5% cost of equity, which is above the top end of the range presented in this report.

Overall, the alternative sources of evidence support the cost of equity range of 5.51–6.34% (real, RPI-deflated) recommended in this report.

16 Ofwat (2017), ‘Delivering Water 2020: Our final methodology for the 2019 price review’, 13 December, Appendix 12, Table 1. 17 Ofwat presents two asset betas, assuming debt beta of zero and 0.1 respectively. The asset beta assuming debt beta of 0.1 has been presented.

The cost of equity for RIIO-2 Oxera

8

Cost of equity indexation

It has been suggested that the allowed cost of equity be indexed instead of setting an allowance that is fixed for the duration of the price control period. Cost of equity indexation could be used to align the cost of equity allowed by the regulator to the estimated cost of equity in each year of the price control.

The cost of equity is not observable. Therefore, in any attempt to index the cost of equity, a decision needs to be taken about whether (and how) to index one, or several, of the cost of equity parameters. The design of any cost of equity indexation mechanism will involve a higher degree of subjectivity than the equivalent mechanism for the cost of debt.

The following principles for indexing the cost of equity emerge from the evidence examined in this report.

there is a negative correlation between the ERP and the RFR, which implies that indexation of only the RFR would create large errors;

the TMR is relatively stable over time, which implies that the TMR generated by the indexation mechanism should be relatively stable over time;

equity beta estimates are more volatile over time than would be expected given the relatively stable risk characteristics of the businesses. This implies that the beta parameters of the indexation mechanism should be more stable than the market estimates, or should be fixed.

Overall, a move to cost of equity indexation would represent a considerable change in methodology. Such a change in methodology would need to fully take into account the principles above, be appropriately signalled and introduced with appropriate transitional arrangements such that it does not undermine investor confidence.

The cost of equity for RIIO-2 Oxera

9

1 Introduction

In preparation for the upcoming RIIO-2 electricity and gas transmission and distribution price controls, the Energy Networks Association (ENA) has commissioned Oxera to provide advice on issues relating to the cost of equity. RIIO-2 will govern the allowed revenue arrangements for the ENA member organisations.

There are many ways to estimate the cost of equity. By far the most common one used by regulators and practitioners is the capital asset pricing model (CAPM).18 This report estimates the required equity returns for long-lived network asset investments based on the CAPM and considers alternative sources of evidence.

The report analyses a number of the challenges when determining appropriate estimates of the parameters of the CAPM for RIIO-2. For example:

how to translate from current market data on government bond yields into a risk-free rate (RFR) assumption that will remain valid for the period up to at least 2026 and potentially as far as 2031;19

how to account for the possibility that ‘flight to safety’ effects have increased the equity risk premium (ERP) and thereby mitigated the impact of low RFRs on the expected equity market return;

how to determine an asset beta when the only UK energy network with an equity market listing (National Grid) derives less than half of its revenues from businesses regulated under the RIIO framework?

The report is structured as follows.

Section 2 discusses the estimation of the market parameters, considering the current theoretical and empirical evidence on the RFR, total market return (TMR) and ERP. The RFR cannot be considered in isolation from the ERP and TMR.

Section 3 considers the latest evidence on equity betas and gearing, to derive an estimate of the asset beta for energy networks in the UK. It also considers energy sector risks that may not be captured in an equity beta estimate.

Section 4 brings together the evidence from the previous two sections to give an initial cost of equity range for RIIO-2.

Section 5 provides alternative sources of evidence on the estimated required equity returns based on asset risk premia, company-specific dividend discount model (DDM) estimates, UK and international regulatory precedent.

Section 6 discusses cost of equity indexation mechanisms as a potential alternative to setting a fixed allowance.

Appendix A1 evaluates the CAPM and its multi-factor alternatives such as arbitrage pricing theory and other factor models.

18 A more detailed review of the CAPM and its alternatives is provided in Appendix A1. 19 RIIO-T2/GD2 starts in 2021 and would finish in 2026 if the length of the control is shortened to five years. RIIO-ED2 starts in 2023 and would finish in 2031 if the length of the control remains eight years.

The cost of equity for RIIO-2 Oxera

10

The start of RIIO-2 is more than three years away; therefore, the analysis provided in this report is based on current data and may alter by the time the next price controls start.

The cost of equity for RIIO-2 Oxera

11

2 Market parameters: the risk-free rate, total market return, and equity risk premium

This section reviews the estimation of the market parameters (the RFR and the ERP) and their interdependency with the TMR. The TMR is the sum of the RFR and a risk premium for investing in equity; when implementing the CAPM, the estimation of the RFR cannot be considered in isolation from the ERP and TMR.

This section looks at:

the RFR (section 2.1);

the ERP and the evidence for setting the market parameters using either the ERP or the TMR as the anchor for the parameters (section 2.2).

It then concludes on the market parameters (section 2.3).

2.1 Risk-free rate

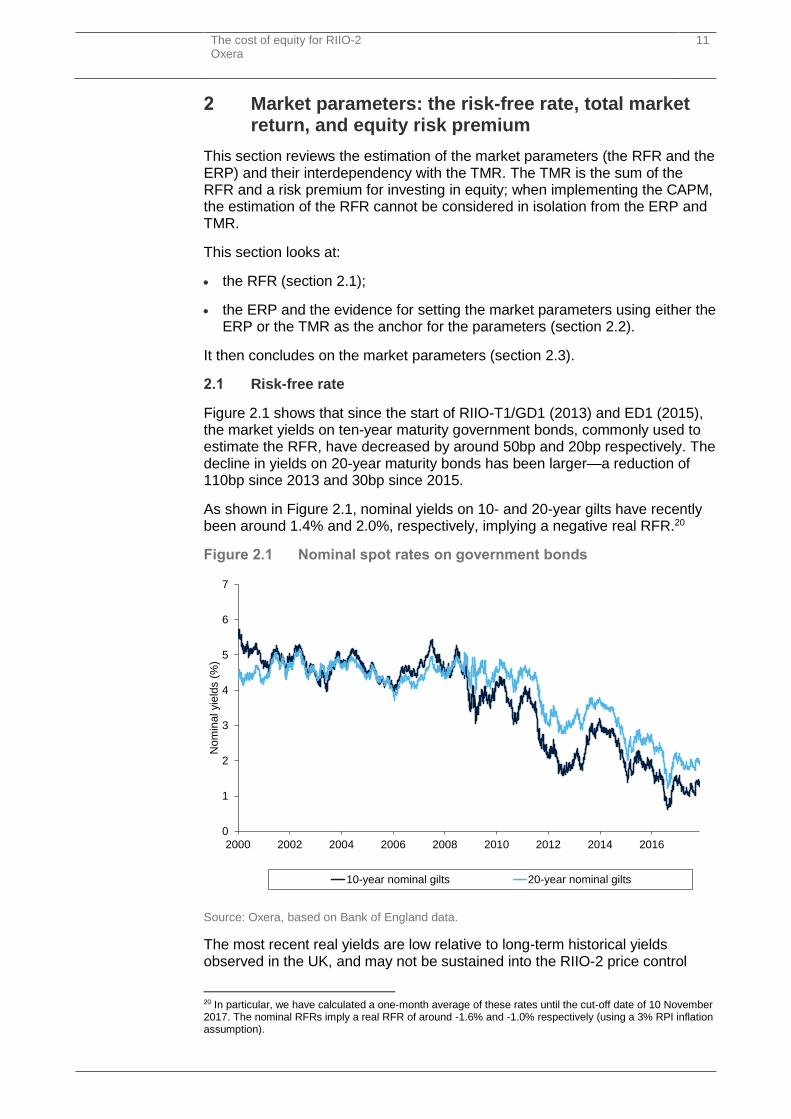

Figure 2.1 shows that since the start of RIIO-T1/GD1 (2013) and ED1 (2015), the market yields on ten-year maturity government bonds, commonly used to estimate the RFR, have decreased by around 50bp and 20bp respectively. The decline in yields on 20-year maturity bonds has been larger—a reduction of 110bp since 2013 and 30bp since 2015.

As shown in Figure 2.1, nominal yields on 10- and 20-year gilts have recently been around 1.4% and 2.0%, respectively, implying a negative real RFR.20

Figure 2.1 Nominal spot rates on government bonds

Source: Oxera, based on Bank of England data.

The most recent real yields are low relative to long-term historical yields observed in the UK, and may not be sustained into the RIIO-2 price control

20 In particular, we have calculated a one-month average of these rates until the cut-off date of 10 November 2017. The nominal RFRs imply a real RFR of around -1.6% and -1.0% respectively (using a 3% RPI inflation assumption).

0

1

2

3

4

5

6

7

2000 2002 2004 2006 2008 2010 2012 2014 2016

No

min

al yie

lds (

%)

10-year nominal gilts 20-year nominal gilts

The cost of equity for RIIO-2 Oxera

12

periods. It is important to consider how to allow for this eventuality in the selection of an appropriate RFR assumption for energy networks in RIIO-2.

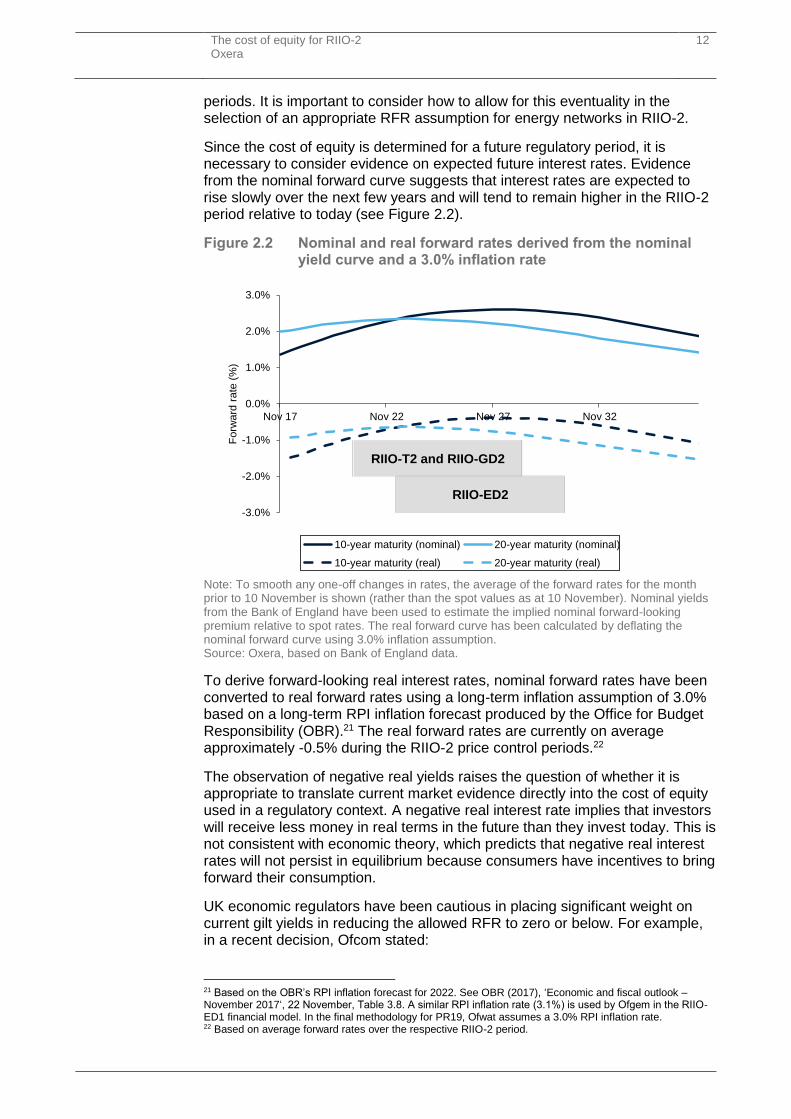

Since the cost of equity is determined for a future regulatory period, it is necessary to consider evidence on expected future interest rates. Evidence from the nominal forward curve suggests that interest rates are expected to rise slowly over the next few years and will tend to remain higher in the RIIO-2 period relative to today (see Figure 2.2).

Figure 2.2 Nominal and real forward rates derived from the nominal yield curve and a 3.0% inflation rate

Note: To smooth any one-off changes in rates, the average of the forward rates for the month prior to 10 November is shown (rather than the spot values as at 10 November). Nominal yields from the Bank of England have been used to estimate the implied nominal forward-looking premium relative to spot rates. The real forward curve has been calculated by deflating the nominal forward curve using 3.0% inflation assumption. Source: Oxera, based on Bank of England data.

To derive forward-looking real interest rates, nominal forward rates have been converted to real forward rates using a long-term inflation assumption of 3.0% based on a long-term RPI inflation forecast produced by the Office for Budget Responsibility (OBR).21 The real forward rates are currently on average approximately -0.5% during the RIIO-2 price control periods.22

The observation of negative real yields raises the question of whether it is appropriate to translate current market evidence directly into the cost of equity used in a regulatory context. A negative real interest rate implies that investors will receive less money in real terms in the future than they invest today. This is not consistent with economic theory, which predicts that negative real interest rates will not persist in equilibrium because consumers have incentives to bring forward their consumption.

UK economic regulators have been cautious in placing significant weight on current gilt yields in reducing the allowed RFR to zero or below. For example, in a recent decision, Ofcom stated:

21 Based on the OBR’s RPI inflation forecast for 2022. See OBR (2017), ‘Economic and fiscal outlook – November 2017‘, 22 November, Table 3.8. A similar RPI inflation rate (3.1%) is used by Ofgem in the RIIO-ED1 financial model. In the final methodology for PR19, Ofwat assumes a 3.0% RPI inflation rate. 22 Based on average forward rates over the respective RIIO-2 period.

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Nov 17 Nov 22 Nov 27 Nov 32

Fo

rwa

rd r

ate

(%

)

10-year maturity (nominal) 20-year maturity (nominal)

10-year maturity (real) 20-year maturity (real)

RIIO-T2 and RIIO-GD2

RIIO-ED2

The cost of equity for RIIO-2 Oxera

13

We continue to believe that caution is required in interpreting the evidence available. Given that we are attempting to estimate a forward-looking real RFR appropriate for the end of the charge control period, it would be inappropriate to simply adopt the current low rates on index-linked gilts without considering the reasons why they could be depressed.23

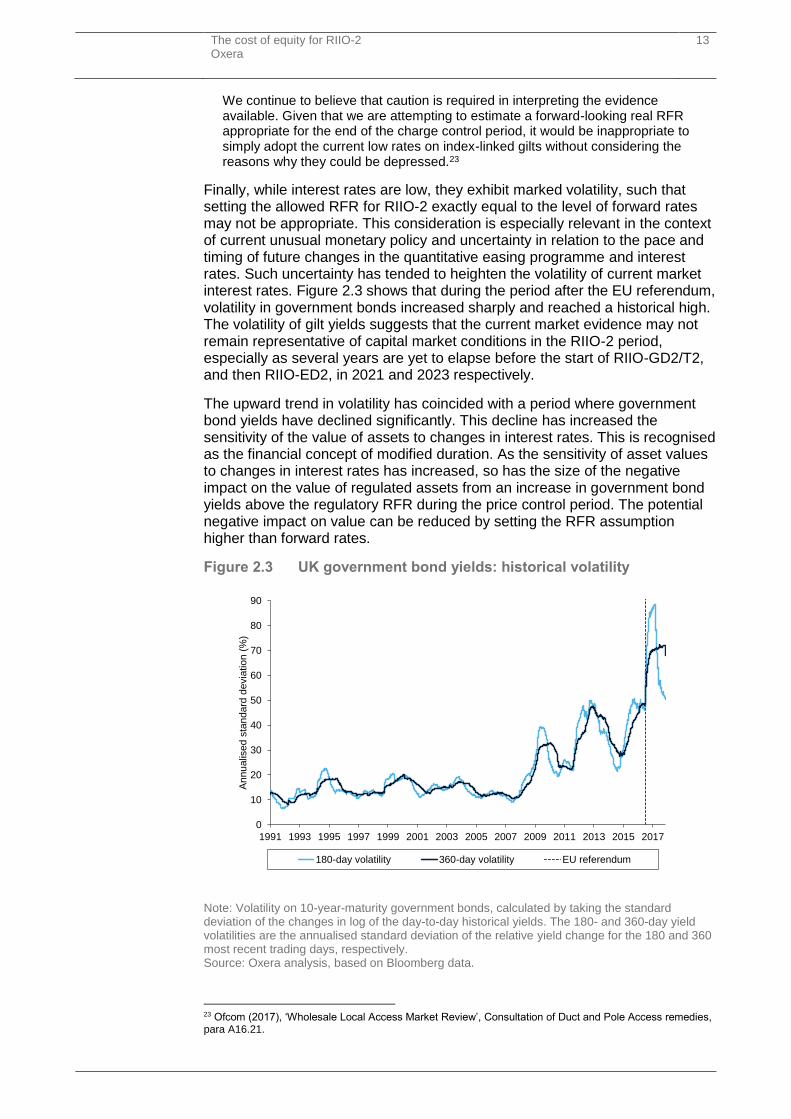

Finally, while interest rates are low, they exhibit marked volatility, such that setting the allowed RFR for RIIO-2 exactly equal to the level of forward rates may not be appropriate. This consideration is especially relevant in the context of current unusual monetary policy and uncertainty in relation to the pace and timing of future changes in the quantitative easing programme and interest rates. Such uncertainty has tended to heighten the volatility of current market interest rates. Figure 2.3 shows that during the period after the EU referendum, volatility in government bonds increased sharply and reached a historical high. The volatility of gilt yields suggests that the current market evidence may not remain representative of capital market conditions in the RIIO-2 period, especially as several years are yet to elapse before the start of RIIO-GD2/T2, and then RIIO-ED2, in 2021 and 2023 respectively.

The upward trend in volatility has coincided with a period where government bond yields have declined significantly. This decline has increased the sensitivity of the value of assets to changes in interest rates. This is recognised as the financial concept of modified duration. As the sensitivity of asset values to changes in interest rates has increased, so has the size of the negative impact on the value of regulated assets from an increase in government bond yields above the regulatory RFR during the price control period. The potential negative impact on value can be reduced by setting the RFR assumption higher than forward rates.

Figure 2.3 UK government bond yields: historical volatility

Note: Volatility on 10-year-maturity government bonds, calculated by taking the standard deviation of the changes in log of the day-to-day historical yields. The 180- and 360-day yield volatilities are the annualised standard deviation of the relative yield change for the 180 and 360 most recent trading days, respectively. Source: Oxera analysis, based on Bloomberg data.

23 Ofcom (2017), ‘Wholesale Local Access Market Review’, Consultation of Duct and Pole Access remedies, para A16.21.

0

10

20

30

40

50

60

70

80

90

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Annu

alis

ed s

tandard

devia

tion (

%)

180-day volatility 360-day volatility EU referendum

The cost of equity for RIIO-2 Oxera

14

As the start of RIIO-2 is more than three years away, an initial estimate for the RFR of -0.5 to 0.0% appears appropriate based on forward rates and allowing for volatility and uncertainty. We suggest that the evidence is monitored to ensure that it is incorporated into the final estimate of the cost of equity for RIIO-2, although it will still be necessary to allow for uncertainty regarding market developments during the RIIO-2 price control period.

The TMR is the sum of the RFR and a risk premium for investing in equity. When implementing the CAPM, the estimation of the RFR cannot be considered in isolation from the ERP. The next sub-section considers the evidence on the relationship between the TMR, RFR and ERP.

2.2 Total market return and equity risk premium

Forming a precise view on the real expected total market return is made challenging by the wide range of estimates from the various sources of evidence. The central issue in the current debate over the TMR (and the estimation of the ERP, either directly, or a residual from an overall TMR estimate) is the degree to which the expected ERP adjusts to offset changes in the RFR. One view is that the ERP is approximately constant over time and largely independent of the RFR. The second view suggests that the expected TMR reverts to a long-term average, and that changes in the RFR are largely offset by changes in the ERP.

One of the clearest expositions of the first view—that the ERP is approximately constant over time (especially in the long run) and largely independent from the RFR—is that of Dimson, Marsh and Staunton (DMS):

There are good reasons to expect the equity premium to vary over time. Market volatility clearly fluctuates, and investors’ risk aversion also varies over time. However, these effects are likely to be brief. Sharply lower (or higher) stock prices may have an impact on immediate returns, but the effect on long-term performance will be diluted. Moreover volatility does not usually stay at abnormally high levels for long, and investor sentiment is also mean reverting. For practical purposes, we conclude that to forecast the long-run equity premium, it is hard to beat extrapolation from the longest history available when the forecast is being made.24

This view effectively assumes that, in the long run, the risk-free asset provides a unique anchor point for the pricing of all other assets. Expected returns for all asset classes increase or decrease one-for-one with changes in the RFR.

One of the clearest expositions of the second view—that the expected TMR reverts to a long-term average and that changes in the RFR are offset by changes in the ERP—is the analysis undertaken by the Bank of England (BoE) based on a dividend discount model (DDM), as well as theoretical work linking required returns to economic uncertainty. In this view, changes in the way risk is priced affect the risk-free and risky assets simultaneously. When economic uncertainty increases, there is a ‘flight to safety’, which raises demand for the risk-free asset and lowers demand for risky assets. This reduces the yield on the risk-free asset and increases the premium required to hold risky assets.

Until recent years, these two views could co-exist, as they produced similar estimates of the ERP. However, low and negative real interest rates have caused the ERP estimates implied by these views to diverge materially. This

24 Dimson, E., Marsh, P. and Staunton, M. (2017), 'Credit Suisse Global Investment Returns Yearbook 2017', p. 41.

The cost of equity for RIIO-2 Oxera

15

divergence has been increasingly problematic for regulators that need to determine the cost of equity to use in price controls.

So far, UK regulators and competition authorities have tended to follow the second view. They typically formed a view on the TMR and RFR first, based on the latest available evidence. The ERP is then calculated as the difference between the two.25

This section looks at the following evidence for and against both views, and derives an appropriate range for the ERP and TMR:

academic literature (section 2.2.1);

historical data (section 2.2.2);

survey evidence (section 2.2.3);

target returns of infrastructure funds (section 2.2.4);

variants of the DDM (section 2.2.5);

the vector autoregression (VAR) model (section 2.2.6);

regulatory precedent (section 2.2.7).

The section concludes that the balance of evidence suggests an appropriate TMR assumption would place more weight on the view that the expected TMR is stable, and close to its long-run average. The theoretical and empirical evidence basis for assuming a stable ERP appears weak.

2.2.1 Academic literature

The early theoretical work on the pricing of risky assets was focused on deriving risk premiums relative to a risk-free interest rate—i.e. the slope of the capital market line26 or the security market line.27 The RFR was generally assumed to be a fixed input to these asset pricing models, which were single-period models with no scope for the interest rate to change. The following quotation is an example of how the determinants of the RFR and the ERP as well as the relationship between them was not the primary focus of the research.

In order to derive conditions for equilibrium in the capital market we invoke two assumptions. First, we assume a common pure rate of interest, with all investors able to borrow or lend funds on equal terms. Second, we assume homogeneity of investor expectations: investors are assumed to agree on the prospects of various investments—the expected values, standard deviations and correlation coefficients described in Part II. Needless to say, these are highly restrictive and undoubtedly unrealistic assumptions. However, since the proper test of a theory is not the realism of its assumptions but the acceptability of its implications, and since these assumptions imply equilibrium conditions which form a major part of classical financial doctrine, it is far from clear that this

25 For example, the Competition Commission (the predecessor of the CMA) noted: ‘Our preferred approach [to estimating the cost of equity] is to deduct our estimate of the RFR from our estimate of the equity market return to derive the ERP. There are two principal reasons for preferring to calculate the ERP in this manner: first, ERP estimates can vary depending on the class of risk-free instrument used in the calculation; second the market return has tended to be less volatile than the ERP (as measured, for example, by the ratio of standard deviation to mean), and there is some evidence of the ERP being negatively correlated with Treasury bill rates over the short term.’ See Competition Commission (2014), ‘Northern Ireland Electricity Limited price determination, A reference under Article 15 of the Electricity (Northern Ireland) Order 1992’, Final determination, para. 13.82. 26 The relationship between the risk and return of the market portfolio. 27 The relationship between the risk and return of an individual stock or share.

The cost of equity for RIIO-2 Oxera

16

formulation should be rejected—especially in view of the dearth of alternative models leading to similar results.28

The view that the expected ERP is relatively stable over time is consistent with the early theoretical work.

Later theoretical work considered the determinants of the RFR and the ERP in an attempt to solve the various ‘puzzles’ related to the ERP, the RFR, and the volatility of equity returns.29 Much of this work has focused on allowing for rare economic disasters and the implications for asset prices.30 Although the results of such models are sensitive to assumptions about the frequency and size of disasters, they can generate values for the RFR and ERP that resolve the ‘puzzles’ surrounding these parameters.

As a stark example, take a consumption-based model in which the representative agent has relative risk aversion equal to 4. Now add to the model a certain type of disaster that strikes, on average, once every 1,000 years, and reduces consumption by 64% (Barro (2006) documents that Germany and Greece each suffered such a fall in per capital real GDP during the Second World War). The introduction of this disaster drives the riskless rate down by 5.9 percentage points and increases the equity premium by 3.7%.31

The most recent theoretical work has derived results that are better able to match the empirical evidence on the RFR and ERP while making more moderate assumptions about the frequency and size of disasters. This is achieved by allowing for more realistic descriptions of the utility functions of consumers and investors.32 An example is the consumption-based asset pricing model developed by the BoE, which predicts that consumers and investors will respond to an increase in economic uncertainty by increasing demand for risk-free assets and reducing demand for risky assets.33 In this model, higher economic uncertainty simultaneously puts downward pressure on the RFR and upward pressure on the equity risk premium.

The BoE model also assumes that consumers and investors care about large negative shocks as well as the local volatility of consumption and investment returns. When the distribution of expected consumption and GDP growth is more negatively skewed and has a higher probability of extreme events (kurtosis), the equity risk premium is higher and the RFR is lower.34

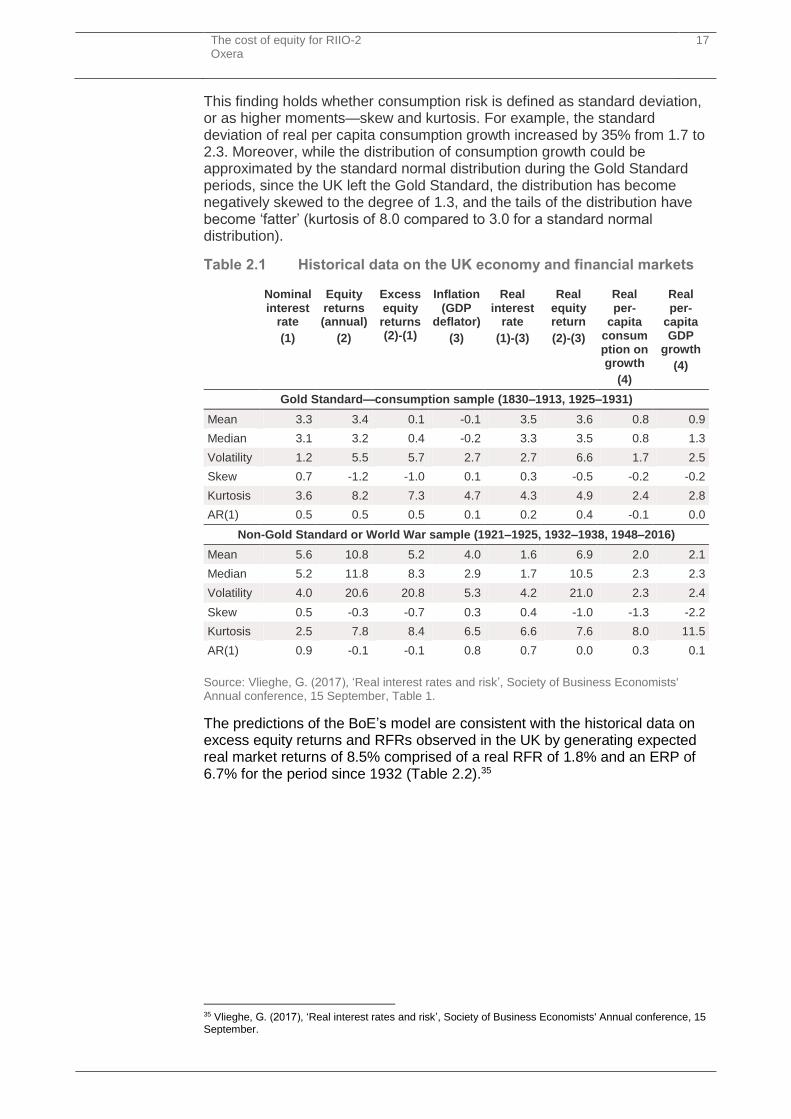

Over time the distribution of consumption outcomes in the UK has become more volatile and more negatively skewed. Risk of the UK economy measured by either consumption growth or GDP growth increased over the period 1718–2016 (Table 2.1). More precisely, the distribution of economic outcomes was more dispersed during the periods when the UK was off the Gold Standard compared with when it was on the Gold Standard.

28 Sharpe, W. (1964), ‘Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk’, The Journal of Finance, 19: 3, September, pp. 433–34. 29 The ERP (observed excess equity returns), RFR, and volatility of equity returns have been respectively higher, lower, and higher than predicted by traditional finance theory. 30 Rietz, T.A. (1988), ‘The Equity Risk Premium: A Solution’, Journal of Monetary Economics, 22, July, pp. 91–115; Barro, R.J. (2009), ‘Rare Disasters, Asset Prices, and Welfare Costs’, American Economic Review, 99:1, pp. 243–64. 31 Martin, I. (2013), ‘Consumption-Based Asset Pricing with Higher Cumulants’, Review of Economic Studies, 80, pp. 746. 32 Specifically, Epstein-Zin preferences are used. This allows for the elasticity of intertemporal substitution and risk aversion to be independent of each other rather than jointly determined, as in the standard CAPM. 33 Summarised in Vlieghe, G. (2017), ‘Real interest rates and risk’, Society of Business Economists' Annual conference, 15 September. 34 Martin, I. (2013), ‘Consumption-Based Asset Pricing with Higher Cumulants’, Review of Economic Studies, 80, pp. 750–51.

The cost of equity for RIIO-2 Oxera

17

This finding holds whether consumption risk is defined as standard deviation, or as higher moments—skew and kurtosis. For example, the standard deviation of real per capita consumption growth increased by 35% from 1.7 to 2.3. Moreover, while the distribution of consumption growth could be approximated by the standard normal distribution during the Gold Standard periods, since the UK left the Gold Standard, the distribution has become negatively skewed to the degree of 1.3, and the tails of the distribution have become ‘fatter’ (kurtosis of 8.0 compared to 3.0 for a standard normal distribution).

Table 2.1 Historical data on the UK economy and financial markets

Nominal interest

rate

(1)

Equity returns (annual)

(2)

Excess equity returns (2)-(1)

Inflation (GDP

deflator)

(3)

Real interest

rate

(1)-(3)

Real equity return

(2)-(3)

Real per-

capita consumption on growth

(4)

Real per-

capita GDP

growth

(4)

Gold Standard—consumption sample (1830–1913, 1925–1931)

Mean 3.3 3.4 0.1 -0.1 3.5 3.6 0.8 0.9

Median 3.1 3.2 0.4 -0.2 3.3 3.5 0.8 1.3

Volatility 1.2 5.5 5.7 2.7 2.7 6.6 1.7 2.5

Skew 0.7 -1.2 -1.0 0.1 0.3 -0.5 -0.2 -0.2

Kurtosis 3.6 8.2 7.3 4.7 4.3 4.9 2.4 2.8

AR(1) 0.5 0.5 0.5 0.1 0.2 0.4 -0.1 0.0

Non-Gold Standard or World War sample (1921–1925, 1932–1938, 1948–2016)

Mean 5.6 10.8 5.2 4.0 1.6 6.9 2.0 2.1

Median 5.2 11.8 8.3 2.9 1.7 10.5 2.3 2.3

Volatility 4.0 20.6 20.8 5.3 4.2 21.0 2.3 2.4

Skew 0.5 -0.3 -0.7 0.3 0.4 -1.0 -1.3 -2.2

Kurtosis 2.5 7.8 8.4 6.5 6.6 7.6 8.0 11.5

AR(1) 0.9 -0.1 -0.1 0.8 0.7 0.0 0.3 0.1

Source: Vlieghe, G. (2017), ‘Real interest rates and risk’, Society of Business Economists' Annual conference, 15 September, Table 1.

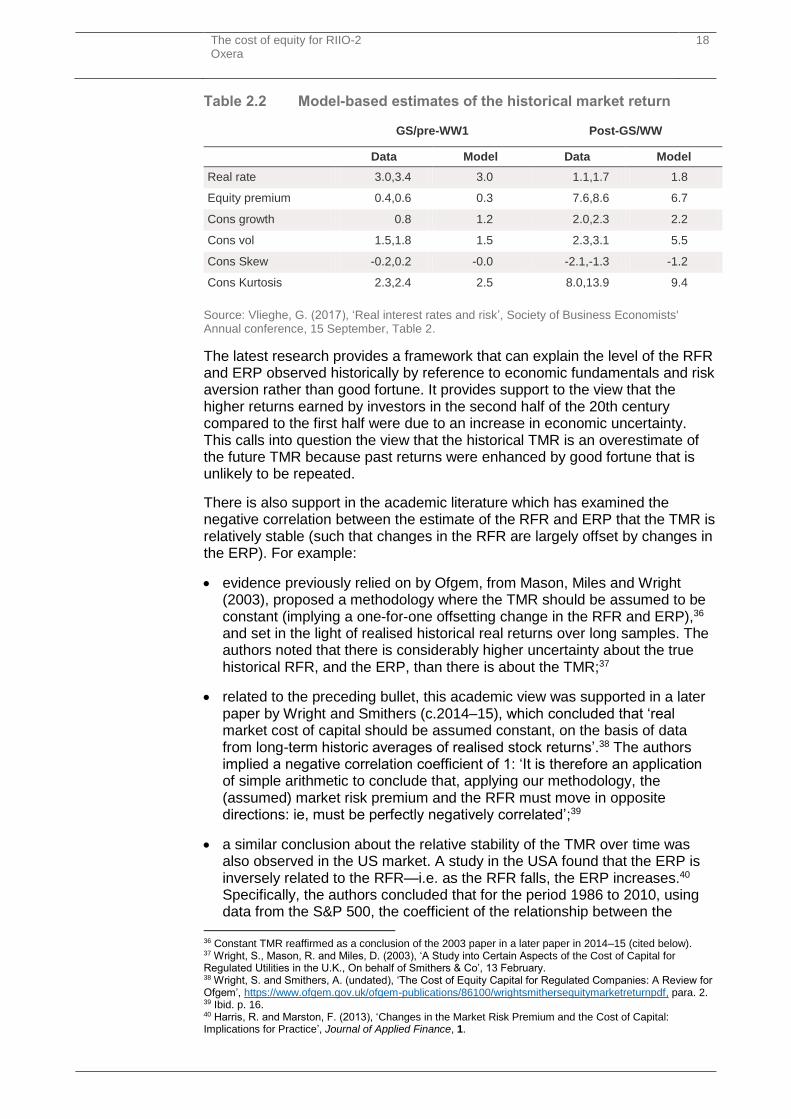

The predictions of the BoE’s model are consistent with the historical data on excess equity returns and RFRs observed in the UK by generating expected real market returns of 8.5% comprised of a real RFR of 1.8% and an ERP of 6.7% for the period since 1932 (Table 2.2).35

35 Vlieghe, G. (2017), ‘Real interest rates and risk’, Society of Business Economists' Annual conference, 15 September.

The cost of equity for RIIO-2 Oxera

18

Table 2.2 Model-based estimates of the historical market return

GS/pre-WW1 Post-GS/WW

Data Model Data Model

Real rate 3.0,3.4 3.0 1.1,1.7 1.8

Equity premium 0.4,0.6 0.3 7.6,8.6 6.7

Cons growth 0.8 1.2 2.0,2.3 2.2

Cons vol 1.5,1.8 1.5 2.3,3.1 5.5

Cons Skew -0.2,0.2 -0.0 -2.1,-1.3 -1.2

Cons Kurtosis 2.3,2.4 2.5 8.0,13.9 9.4

Source: Vlieghe, G. (2017), ‘Real interest rates and risk’, Society of Business Economists' Annual conference, 15 September, Table 2.

The latest research provides a framework that can explain the level of the RFR and ERP observed historically by reference to economic fundamentals and risk aversion rather than good fortune. It provides support to the view that the higher returns earned by investors in the second half of the 20th century compared to the first half were due to an increase in economic uncertainty. This calls into question the view that the historical TMR is an overestimate of the future TMR because past returns were enhanced by good fortune that is unlikely to be repeated.

There is also support in the academic literature which has examined the negative correlation between the estimate of the RFR and ERP that the TMR is relatively stable (such that changes in the RFR are largely offset by changes in the ERP). For example:

evidence previously relied on by Ofgem, from Mason, Miles and Wright (2003), proposed a methodology where the TMR should be assumed to be constant (implying a one-for-one offsetting change in the RFR and ERP),36 and set in the light of realised historical real returns over long samples. The authors noted that there is considerably higher uncertainty about the true historical RFR, and the ERP, than there is about the TMR;37

related to the preceding bullet, this academic view was supported in a later paper by Wright and Smithers (c.2014–15), which concluded that ‘real market cost of capital should be assumed constant, on the basis of data from long-term historic averages of realised stock returns’.38 The authors implied a negative correlation coefficient of 1: ‘It is therefore an application of simple arithmetic to conclude that, applying our methodology, the (assumed) market risk premium and the RFR must move in opposite directions: ie, must be perfectly negatively correlated’;39

a similar conclusion about the relative stability of the TMR over time was also observed in the US market. A study in the USA found that the ERP is inversely related to the RFR—i.e. as the RFR falls, the ERP increases.40 Specifically, the authors concluded that for the period 1986 to 2010, using data from the S&P 500, the coefficient of the relationship between the

36 Constant TMR reaffirmed as a conclusion of the 2003 paper in a later paper in 2014–15 (cited below). 37 Wright, S., Mason, R. and Miles, D. (2003), ‘A Study into Certain Aspects of the Cost of Capital for Regulated Utilities in the U.K., On behalf of Smithers & Co’, 13 February. 38 Wright, S. and Smithers, A. (undated), ‘The Cost of Equity Capital for Regulated Companies: A Review for Ofgem’, https://www.ofgem.gov.uk/ofgem-publications/86100/wrightsmithersequitymarketreturnpdf, para. 2. 39 Ibid. p. 16. 40 Harris, R. and Marston, F. (2013), ‘Changes in the Market Risk Premium and the Cost of Capital: Implications for Practice’, Journal of Applied Finance, 1.

The cost of equity for RIIO-2 Oxera

19

interest rate and the ERP was -0.79, such that a 1% decline in the RFR would be offset by a 0.79% increase in the ERP.41

Overall, the latest asset pricing research refutes the view that the ERP is a stable parameter and that the main source of variation over time in the TMR is the RFR.

2.2.2 Historical data

The latest estimate of the average of UK real equity returns over the period 1900–2016 is 5.5–7.3%.42 The lower bound of this range is the geometric average of the historical data and the upper bound is the arithmetic average. In light of the evidence presented in Box 2.1, it is appropriate to select an estimate close to the arithmetic average.

Box 2.1 Geometric versus arithmetic means

The geometric mean of any set of numbers is always lower than the arithmetic mean unless all the numbers are equal (in which case the means are the same). For a series of returns, equality between the geometric and arithmetic means would occur only if there is no volatility at all (i.e. if returns are constant). While there is debate about which is the more appropriate averaging method in any given context, the academic literature is broadly supportive of placing more weight on the arithmetic averages for estimating the ERP to use when computing required equity returns. Indeed, DMS themselves write:43

This [the arithmetic mean risk premium] is our estimate of the expected long-run equity risk premium for use in asset allocation, stock valuation, and corporate budgeting applications.

This is consistent with a number of analytical studies that suggest that greater weight should be placed on arithmetic than on geometric estimates of returns.44 Cooper (1996) analyses the properties of three approximately unbiased estimators of expected returns from the academic literature, and notes:

The use of the arithmetic mean ignores estimation error and serial correlation in returns. Unbiased discount factors have been derived that correct for both these effects. In all cases, the corrected discount rates are closer to the arithmetic than the geometric mean.45

and that:

the geometric mean is a significantly downward biased estimate of discount rates even when ‘market overreaction’ is taken into account.46

This conclusion is further supported by Jacquier, Kane and Marcus (2003), who derive a relatively simple formula for a correct estimator for the

41 Harris, R. and Marston, F. (2013), ‘Changes in the Market Risk Premium and the Cost of Capital: Implications for Practice’, Journal of Applied Finance, 1, pp. 6–7. 42 Dimson, E., Marsh, P. and Staunton, M. (2017), 'Credit Suisse Global Investment Returns Yearbook 2017', p. 14. 43 Dimson, E., Marsh, P. and Staunton, M. (2015), ‘Credit Suisse Investment Returns Sourcebook 2015’, p. 34. 44 For further details, see Cooper, I. (1996), ‘Arithmetic versus geometric mean estimators: Setting discount rates for capital budgeting’, European Financial Management, 2:2, p. 157. 45 Ibid. 46 Ibid., p. 165.

The cost of equity for RIIO-2 Oxera

20

expected future ERP.47 The authors suggest a weighted average between the arithmetic and geometric means, with the weight on the geometric mean being the ratio of the investment horizon to the sample period. This means that, for short investment horizons, the best estimator is very close to the arithmetic mean, whereas for long investment horizons the weight of the geometric mean increases.

In our case, the sample period is 116 years, since the DMS database contains 116 years of data. If RIIO-2 will be the same duration as RIIO-1, the weight on the geometric mean would be 8/116 = 7%. For a shorter price control period, the weight on the geometric mean would be even smaller.

The estimator by Jacquier, Kane and Marcus (2003) has been used in regulatory discussions—for example, in the Competition Commission (CC) referrals concerning Bristol Water,48 and NIE.49

The revisions to the calculation of the RPI inflation statistic made by the Office for National Statistics (ONS) in 2010 created a structural increase in the RPI measure of inflation.50 All else equal, this would make the historical real equity market returns an upwardly biased estimate of the future TMR calculated relative to RPI. However, there are likely to have been other revisions to the calculation of RPI during the 116-year history of the UK equity returns dataset, some of which may have introduced a downward bias to average historical real equity market returns. For example, in 2015, the OBR stated that its estimate of the long-run wedge between RPI and CPI would be reduced by about 40bp.51 A comprehensive examination of the historical inflation data would be needed before concluding that the 2010 revision to the RPI calculation has made the historical real equity market returns an upwardly biased estimate of the future TMR.

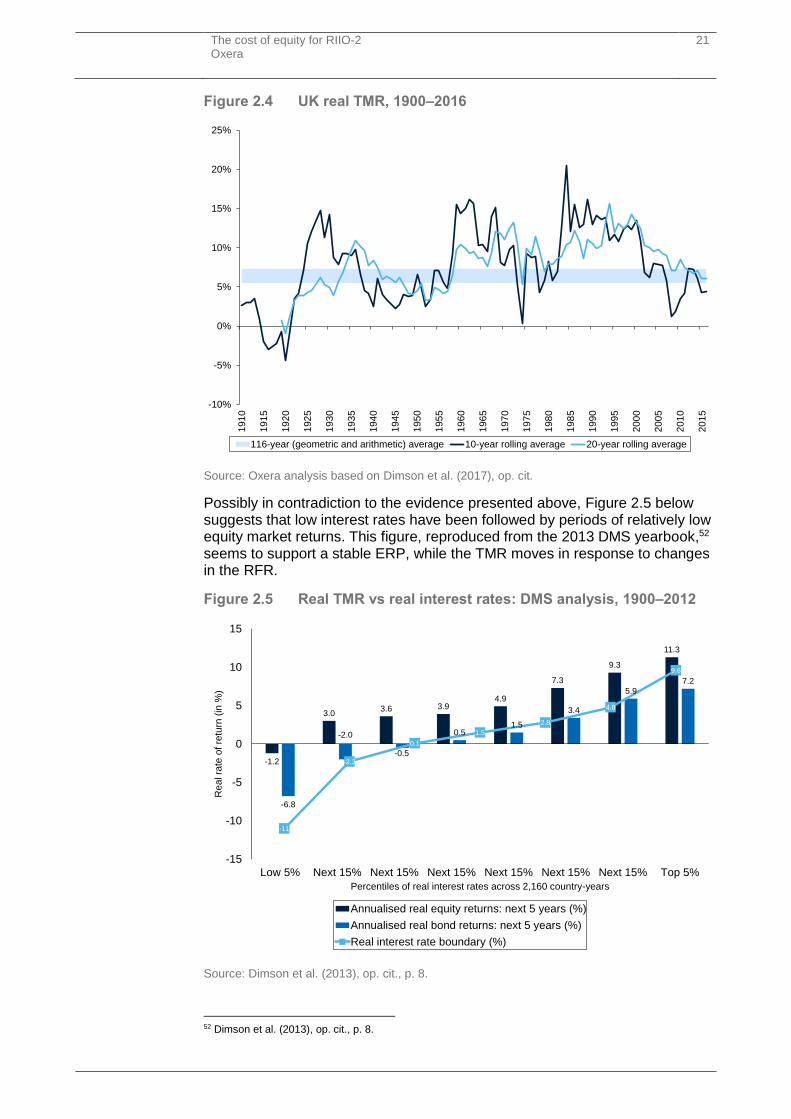

Turning to the question of what the historical data suggests about the stability of either the ERP or the TMR, the 10- and 20-year rolling averages of the historical real TMR data for the UK from DMS (see Figure 2.4) suggest that the TMR fluctuates around the long-term average, rather than exhibiting a sustained upwards or downwards trend.

47 Jacquier, E., Kane, A. and Marcus, A. J. (2003), ‘Geometric or Arithmetic Mean: A Reconsideration’, Financial Analyst Journal, November/December. 48 Competition Commission (2010), ‘A reference under section 12(3)(a) of the Water Industry Act – Report presented to Ofwat on 4 August 2010’, Appendix N, http://webarchive.nationalarchives.gov.uk/20121212135622/www.competition-commission.org.uk/our-work/directory-of-all-inquiries/bristol-water-plc-water-price-limits-determination, accessed 15 December 2017. 49 Competition Commission (2014), ‘Northern Ireland Electricity Limited price determination – A reference under Article 15 of the Electricity (Northern Ireland) Order 1992’, Final determination, 23 March, https://assets.digital.cabinet-office.gov.uk/media/535a5768ed915d0fdb000003/NIE_Final_determination.pdf, accessed 15 December 2017. 50 In particular, changes in how clothing prices were collected led to an increase in the difference between the CPI and the RPI. See Office for National Statistics (2010), ‘CPI and RPI: increased impact of the formula effect in 2010’, Information note. 51 Due to a cumulative effect of changes in the estimate of the housing effect, coverage of the index, and other differences including weights. See Office for Budget Responsibility (2015), ‘Economic and fiscal outlook’, Cm 9024, March.

The cost of equity for RIIO-2 Oxera

21

Figure 2.4 UK real TMR, 1900–2016

Source: Oxera analysis based on Dimson et al. (2017), op. cit.

Possibly in contradiction to the evidence presented above, Figure 2.5 below suggests that low interest rates have been followed by periods of relatively low equity market returns. This figure, reproduced from the 2013 DMS yearbook,52 seems to support a stable ERP, while the TMR moves in response to changes in the RFR.

Figure 2.5 Real TMR vs real interest rates: DMS analysis, 1900–2012

Source: Dimson et al. (2013), op. cit., p. 8.

52 Dimson et al. (2013), op. cit., p. 8.

-10%

-5%

0%

5%

10%

15%

20%

25%

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

116-year (geometric and arithmetic) average 10-year rolling average 20-year rolling average

-1.2

3.03.6 3.9

4.9

7.3

9.3

11.3

-6.8

-2.0

-0.5

0.51.5

3.4

5.9

7.2

-11

-2.3

0.1

1.5

2.8

4.8

9.6

-15

-10

-5

0

5

10

15

Low 5% Next 15% Next 15% Next 15% Next 15% Next 15% Next 15% Top 5%

Re

al ra

te o

f re

turn

(in

%)

Percentiles of real interest rates across 2,160 country-years

Annualised real equity returns: next 5 years (%)

Annualised real bond returns: next 5 years (%)

Real interest rate boundary (%)

The cost of equity for RIIO-2 Oxera

22

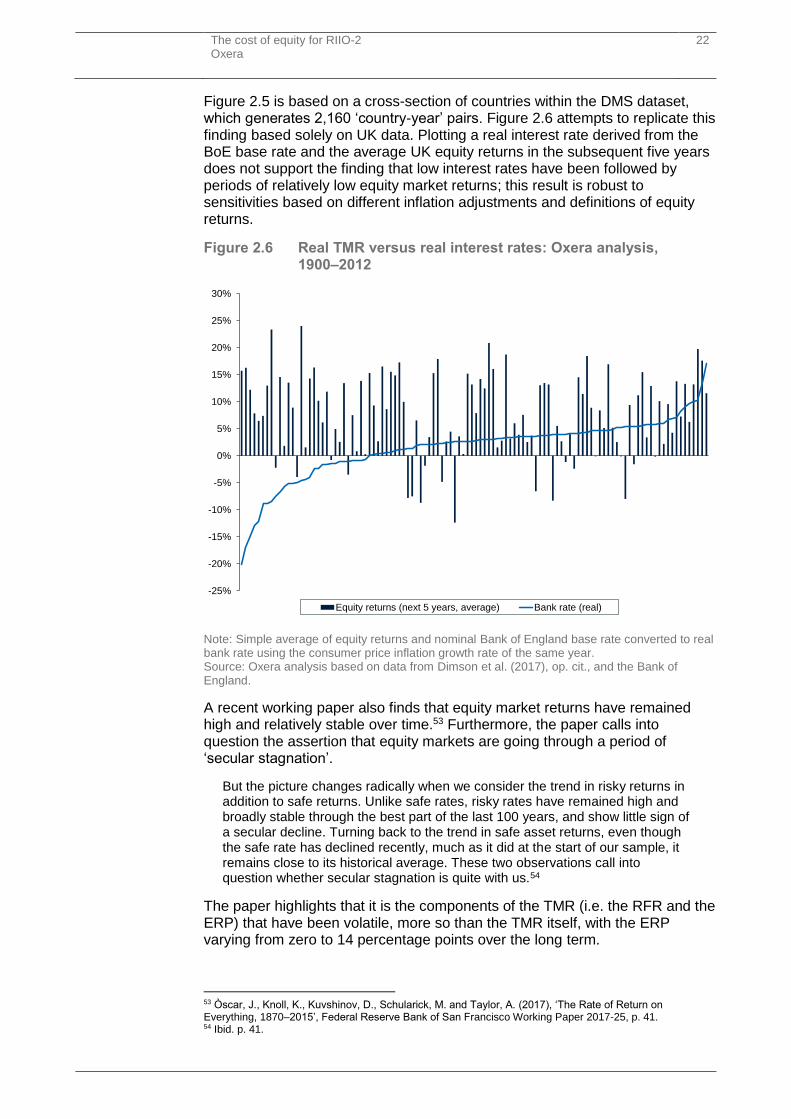

Figure 2.5 is based on a cross-section of countries within the DMS dataset, which generates 2,160 ‘country-year’ pairs. Figure 2.6 attempts to replicate this finding based solely on UK data. Plotting a real interest rate derived from the BoE base rate and the average UK equity returns in the subsequent five years does not support the finding that low interest rates have been followed by periods of relatively low equity market returns; this result is robust to sensitivities based on different inflation adjustments and definitions of equity returns.

Figure 2.6 Real TMR versus real interest rates: Oxera analysis, 1900–2012

Note: Simple average of equity returns and nominal Bank of England base rate converted to real bank rate using the consumer price inflation growth rate of the same year. Source: Oxera analysis based on data from Dimson et al. (2017), op. cit., and the Bank of England.

A recent working paper also finds that equity market returns have remained high and relatively stable over time.53 Furthermore, the paper calls into question the assertion that equity markets are going through a period of ‘secular stagnation’.

But the picture changes radically when we consider the trend in risky returns in addition to safe returns. Unlike safe rates, risky rates have remained high and broadly stable through the best part of the last 100 years, and show little sign of a secular decline. Turning back to the trend in safe asset returns, even though the safe rate has declined recently, much as it did at the start of our sample, it remains close to its historical average. These two observations call into question whether secular stagnation is quite with us.54

The paper highlights that it is the components of the TMR (i.e. the RFR and the ERP) that have been volatile, more so than the TMR itself, with the ERP varying from zero to 14 percentage points over the long term.

53 Òscar, J., Knoll, K., Kuvshinov, D., Schularick, M. and Taylor, A. (2017), ‘The Rate of Return on Everything, 1870–2015’, Federal Reserve Bank of San Francisco Working Paper 2017-25, p. 41. 54 Ibid. p. 41.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Equity returns (next 5 years, average) Bank rate (real)

The cost of equity for RIIO-2 Oxera

23

We now turn to examine the long-run developments in the risk premium, i.e. the spread between safe and risky returns. This spread was low and stable at around 5 percentage points before WW1. It rose slightly after the WW1, before falling to an all-time low of near zero by around 1930. The decades following the onset of the WW2 saw a dramatic widening in the risk premium, with the spread reaching its historical high of around 14 percentage points in the 1950s, before falling back to around its historical average.55

On balance, evidence from historical data supports the view that the expected TMR is broadly stable and that changes in the RFR are largely offset by changes in the ERP.

2.2.3 Survey evidence

Another source of evidence for the ERP and TMR is surveys. Survey evidence needs to be interpreted with caution, however. Issues with interpretation of survey evidence include the following:

respondents’ answers may be influenced by the way questions are phrased—for example, whether the question asks about required returns to equity or expected returns on a specified stock market index;

there is a tendency for respondents to extrapolate from recent realised returns, making the estimates less forward-looking and prone to be anchored on recent short-term market performance;

the results are based purely on judgement, which may also be influenced by the respondent’s own position or biases, and are less reliable than estimates based on direct market evidence on pricing.

As stated by Brealey and Myers (2017):

Do not trust anyone who claims to know what returns investors expect. History contains some clues, but ultimately we have to judge whether investors on average have received what they expected.56

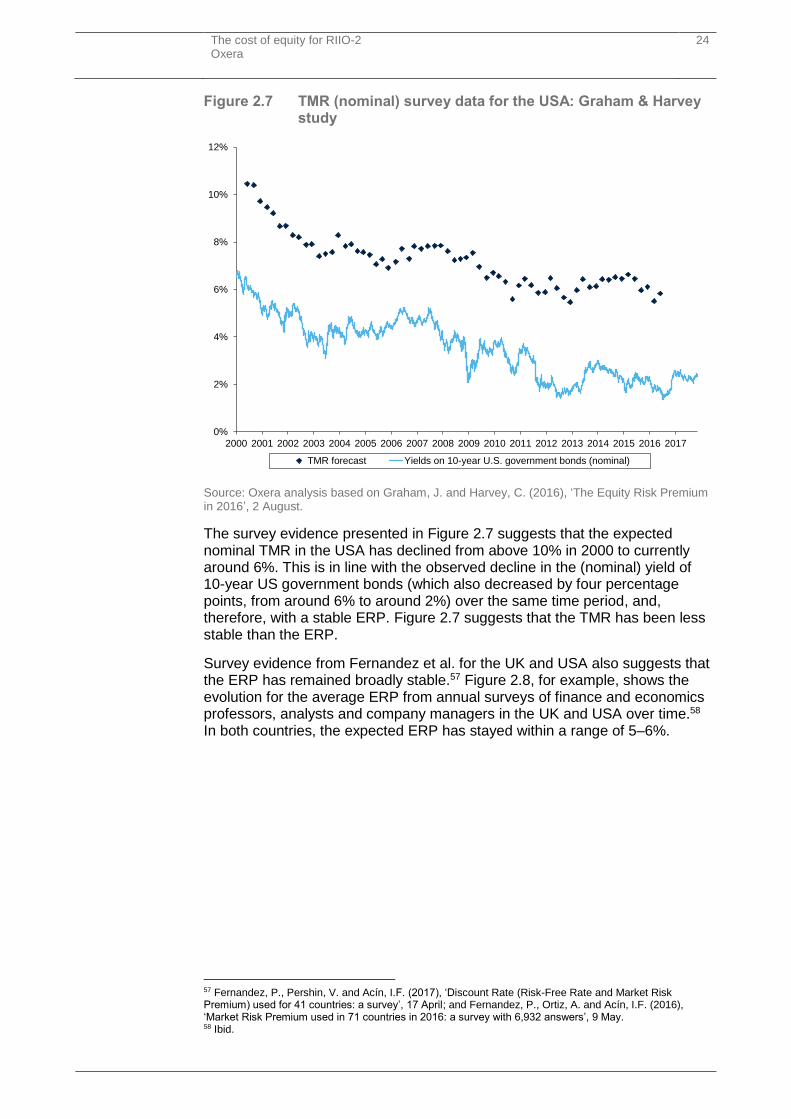

Notwithstanding the need to interpret the survey evidence with caution, this sub-section presents evidence in relation to respondents’ expectations about ERP and TMR. First, Figure 2.7 shows TMR survey evidence for the USA, based on a quarterly survey of Chief Financial Officers in the USA conducted by Duke University and the CFO Magazine. Among other questions, the CFOs were asked about their view of the long-term expected return on the S&P 500.

55 Ibid. p. 42. 56 Brealey, R., Myers, S., Allen F. (2016), Principles of Corporate Finance, 12th edition, McGraw-Hill International Edition, p. 169.

The cost of equity for RIIO-2 Oxera

24

Figure 2.7 TMR (nominal) survey data for the USA: Graham & Harvey study

Source: Oxera analysis based on Graham, J. and Harvey, C. (2016), ‘The Equity Risk Premium in 2016’, 2 August.

The survey evidence presented in Figure 2.7 suggests that the expected nominal TMR in the USA has declined from above 10% in 2000 to currently around 6%. This is in line with the observed decline in the (nominal) yield of 10-year US government bonds (which also decreased by four percentage points, from around 6% to around 2%) over the same time period, and, therefore, with a stable ERP. Figure 2.7 suggests that the TMR has been less stable than the ERP.

Survey evidence from Fernandez et al. for the UK and USA also suggests that the ERP has remained broadly stable.57 Figure 2.8, for example, shows the evolution for the average ERP from annual surveys of finance and economics professors, analysts and company managers in the UK and USA over time.58 In both countries, the expected ERP has stayed within a range of 5–6%.

57 Fernandez, P., Pershin, V. and Acín, I.F. (2017), ‘Discount Rate (Risk-Free Rate and Market Risk Premium) used for 41 countries: a survey’, 17 April; and Fernandez, P., Ortiz, A. and Acín, I.F. (2016), ‘Market Risk Premium used in 71 countries in 2016: a survey with 6,932 answers’, 9 May. 58 Ibid.

0%

2%

4%

6%

8%

10%

12%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TMR forecast Yields on 10-year U.S. government bonds (nominal)

The cost of equity for RIIO-2 Oxera

25

Figure 2.8 ERP survey data from Fernandez et al. for the UK and USA

Source: Oxera analysis based on Fernandez et al. (2017), op. cit., and (2016), op. cit.

Overall, the evidence from surveys seems to support the first view—that the ERP is approximately constant over time and largely independent of the RFR.

2.2.4 Discount rates used by infrastructure funds

The discount rates used by infrastructure funds to value their portfolios may provide another source of evidence for the TMR and ERP. Figure 2.9 shows the nominal discount rate used by 3i Infrastructure plc for its portfolio of infrastructure equity investments over time.

Figure 2.9 3i Infrastructure portfolio-weighted average discount rate

Source: Oxera analysis based on RBC Capital Markets (2017), ‘3i Infrastructure plc–Solid 7.1% return and cash generation in 1H18’, 9 November, p. 2.

5.3%5.5% 5.5%

5.1% 5.2% 5.3%

5.9%

5.5% 5.5%5.7%

5.4% 5.5%5.3%

5.7%

0%

1%

2%

3%

4%

5%

6%

7%

2011 2012 2013 2014 2015 2016 2017

United Kingdom USA

12.4%

13.8%

12.5%

13.2%12.6%

12.0% 11.8%10.9%

10.2%

9.9%

10.1%10.0%

10.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Mar-

08

Sep-0

8

Mar-

09

Sep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

Sep-1

2

Mar-

13

Sep-1

3

Mar-

14

Sep-1

4

Mar-

15

Sep-1

5

Mar-

16

Sep-1

6

Mar-

17

Sep-1

7

Discount rate

The cost of equity for RIIO-2 Oxera

26

The decrease in the discount rate over time is broadly in line with the decrease in the real RFR over the same time period. This supports the view that the ERP is stable, but may also be driven by changes in the mix of assets and the equity risk of the portfolio (i.e. the equity beta).

Removing 3% RPI inflation from the current nominal portfolio discount rate of 10.0% yields a real discount rate of around 7% cost of equity for infrastructure. The implied TMR would also be around 7%, assuming an equity beta close to one.

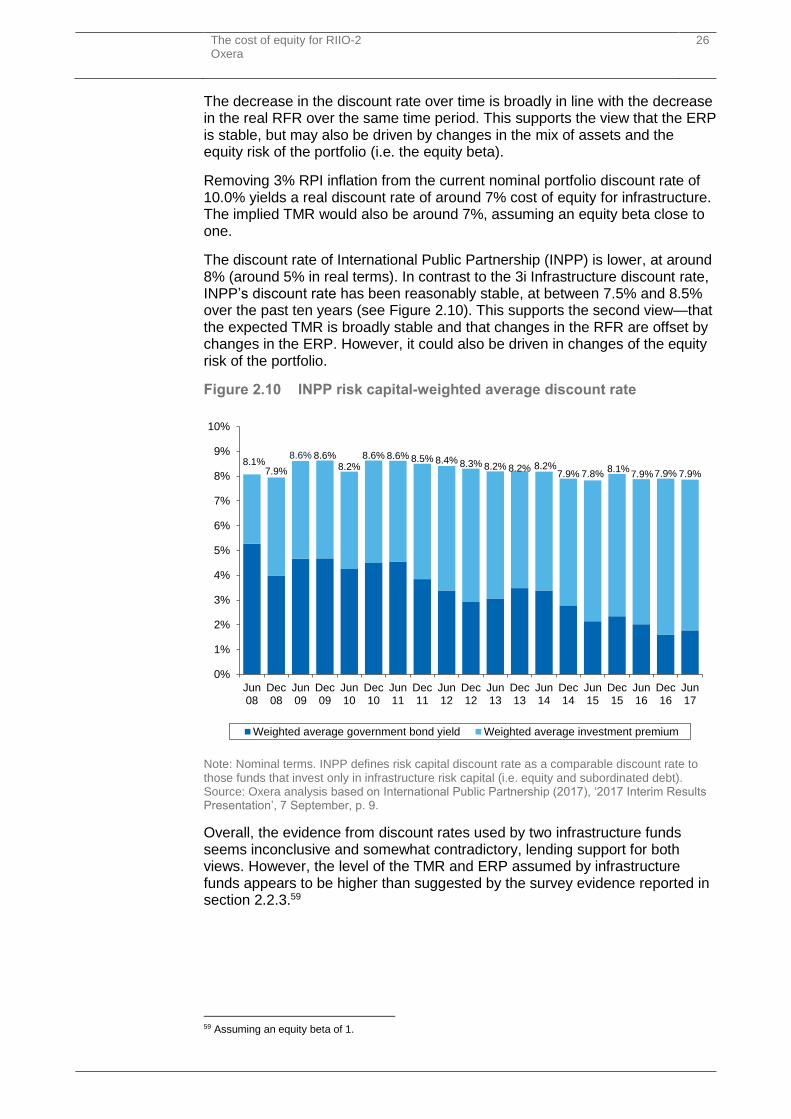

The discount rate of International Public Partnership (INPP) is lower, at around 8% (around 5% in real terms). In contrast to the 3i Infrastructure discount rate, INPP’s discount rate has been reasonably stable, at between 7.5% and 8.5% over the past ten years (see Figure 2.10). This supports the second view—that the expected TMR is broadly stable and that changes in the RFR are offset by changes in the ERP. However, it could also be driven in changes of the equity risk of the portfolio.

Figure 2.10 INPP risk capital-weighted average discount rate

Note: Nominal terms. INPP defines risk capital discount rate as a comparable discount rate to those funds that invest only in infrastructure risk capital (i.e. equity and subordinated debt). Source: Oxera analysis based on International Public Partnership (2017), ‘2017 Interim Results Presentation’, 7 September, p. 9.

Overall, the evidence from discount rates used by two infrastructure funds seems inconclusive and somewhat contradictory, lending support for both views. However, the level of the TMR and ERP assumed by infrastructure funds appears to be higher than suggested by the survey evidence reported in section 2.2.3.59

59 Assuming an equity beta of 1.

8.1%7.9%

8.6% 8.6%8.2%

8.6% 8.6% 8.5% 8.4% 8.3% 8.2% 8.2% 8.2%7.9% 7.8%

8.1%7.9%7.9% 7.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Jun08

Dec08

Jun09

Dec09

Jun10

Dec10

Jun11

Dec11

Jun12

Dec12

Jun13

Dec13

Jun14

Dec14

Jun15

Dec15

Jun16

Dec16

Jun17

Weighted average government bond yield Weighted average investment premium

The cost of equity for RIIO-2 Oxera

27

2.2.5 Variants of the dividend discount model

The BoE regularly estimates the ERP based on a DDM.60 The BoE has suggested that ERPs are facing upward pressure based on estimates derived from the DDM:

The Bank’s calculations show that the equity risk premium (ERP) may have roughly doubled from its perhaps unsustainably low level at the turn of the century during the dot-com boom. This rise in the ERP has been working vigorously against the fall in the risk-free rate…Members of the Bank’s Monetary Policy Committee have argued that interest rates are as low as they are not because of coordinated central bank whim but because there is so much caution in the system…People seem to think some catastrophic outcome is possible, and this in turn pushes up the ERP. Whatever is going on, it hangs over the economy as well as the banks, and it should not be underestimated.61

As mentioned in section 2.2.1, asset pricing models that incorporate the potential for catastrophic (i.e. negatively skewed) economic outcomes or less restrictive assumptions about the preferences of consumers and investors will generate a higher ERP. This provides a theoretical basis for the ERP estimates implied by the DDM.

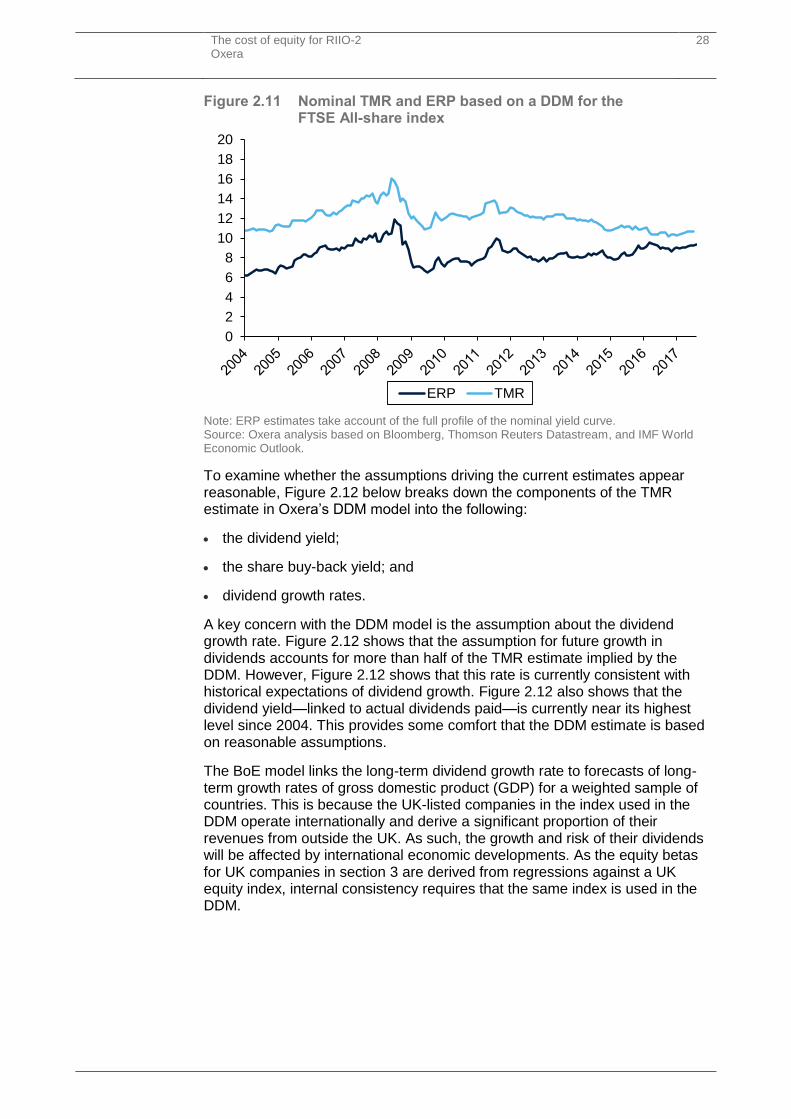

In the DDM, the expected TMR is the discount rate at which the present value of future dividends is equal to the current market price of the shares. In the context of estimating the return for the whole UK equity market, data on the FTSE All-share index is typically used.

Oxera has constructed a DDM following the BoE methodology. The outputs from the Oxera model closely match those reported by the BoE: the ERP calculated from the model for February 2017 is 8.9% compared with approximately 9.0% reported by the BoE.62 This estimate is 400bp higher than the historical arithmetic average excess equity return reported by DMS, consistent with the view that changes in the RFR are largely offset by changes in the ERP.