Embed Size (px)

DESCRIPTION

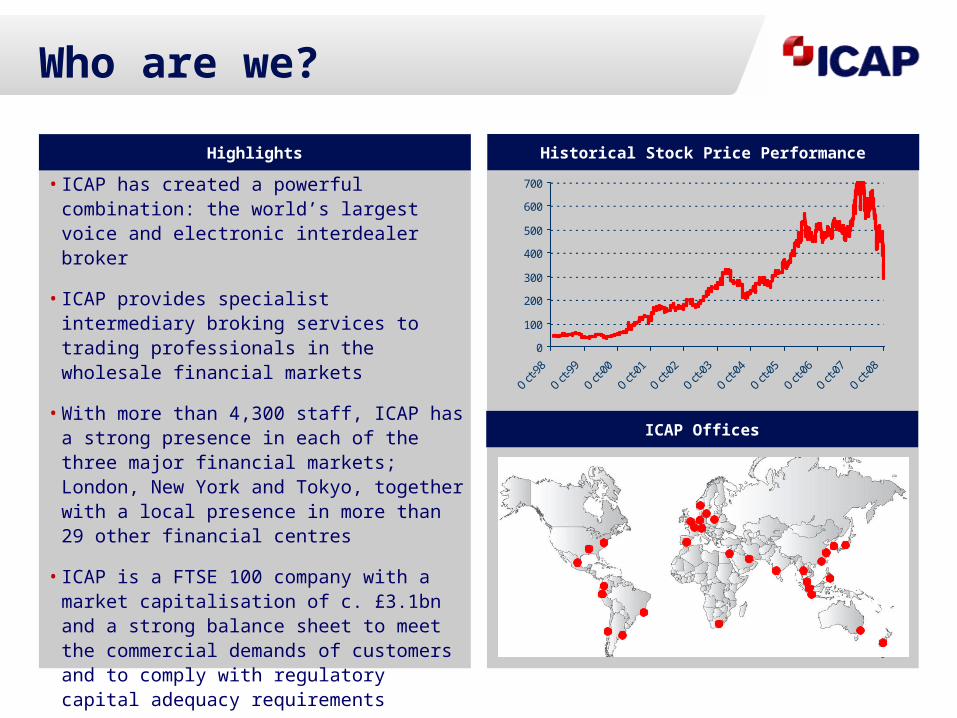

Who are we? ICAP has created a powerful combination: the world’s largest voice and electronic interdealer broker ICAP provides specialist intermediary broking services to trading professionals in the wholesale financial markets With more than 4,300 staff, ICAP has a strong presence in each of the three major financial markets; London, New York and Tokyo, together with a local presence in more than 29 other financial centres ICAP is a FTSE 100 company with a market capitalisation of c. £3.1bn and a strong balance sheet to meet the commercial demands of customers and to comply with regulatory capital adequacy requirements. Highlights ICAP Offices Historical Stock Price Performance.

Citation preview

The Changing Role Of Inter-Dealer BrokersFinExpo - 16th October 2008

Cathryn LyallCOO Exchange Projects

Contents• Overview of ICAP

• Developments in OTC Markets

• IDBs and Exchanges: Protagonists or Partners?

• Evolving IDB business models

• Electronic, Voice, and Hybrid business

• Product Innovation and Diversification

• Post-Trade Services

Who are we?

• ICAP has created a powerful combination: the world’s largest voice and electronic interdealer broker

• ICAP provides specialist intermediary broking services to trading professionals in the wholesale financial markets

• With more than 4,300 staff, ICAP has a strong presence in each of the three major financial markets; London, New York and Tokyo, together with a local presence in more than 29 other financial centres

• ICAP is a FTSE 100 company with a market capitalisation of c. £3.1bn and a strong balance sheet to meet the commercial demands of customers and to comply with regulatory capital adequacy requirements

.

Highlights

ICAP Offices

Historical Stock Price Performance

0

100

200

300

400

500

600

700

Oct-98

Oct-99

Oct-00

Oct-01

Oct-02

Oct-03

Oct-04

Oct-05

Oct-06

Oct-07

Oct-08

.

Who are we?

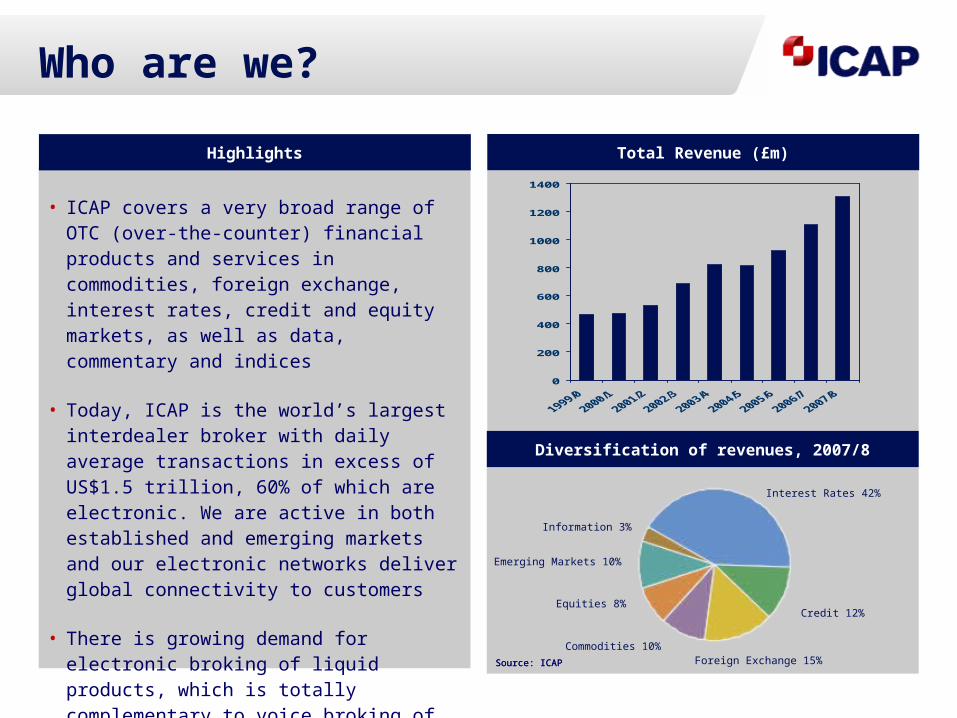

• ICAP covers a very broad range of OTC (over-the-counter) financial products and services in commodities, foreign exchange, interest rates, credit and equity markets, as well as data, commentary and indices

• Today, ICAP is the world’s largest interdealer broker with daily average transactions in excess of US$1.5 trillion, 60% of which are electronic. We are active in both established and emerging markets and our electronic networks deliver global connectivity to customers

• There is growing demand for electronic broking of liquid products, which is totally complementary to voice broking of more bespoke, less liquid products

Highlights Total Revenue (£m)

Diversification of revenues, 2007/8

Source: ICAPSource: ICAP

Interest Rates 42%

Equities 8%

Commodities 10%Foreign Exchange 15%

Credit 12%

Emerging Markets 10%

0

200

400

600

800

1000

1200

1400

Information 3%

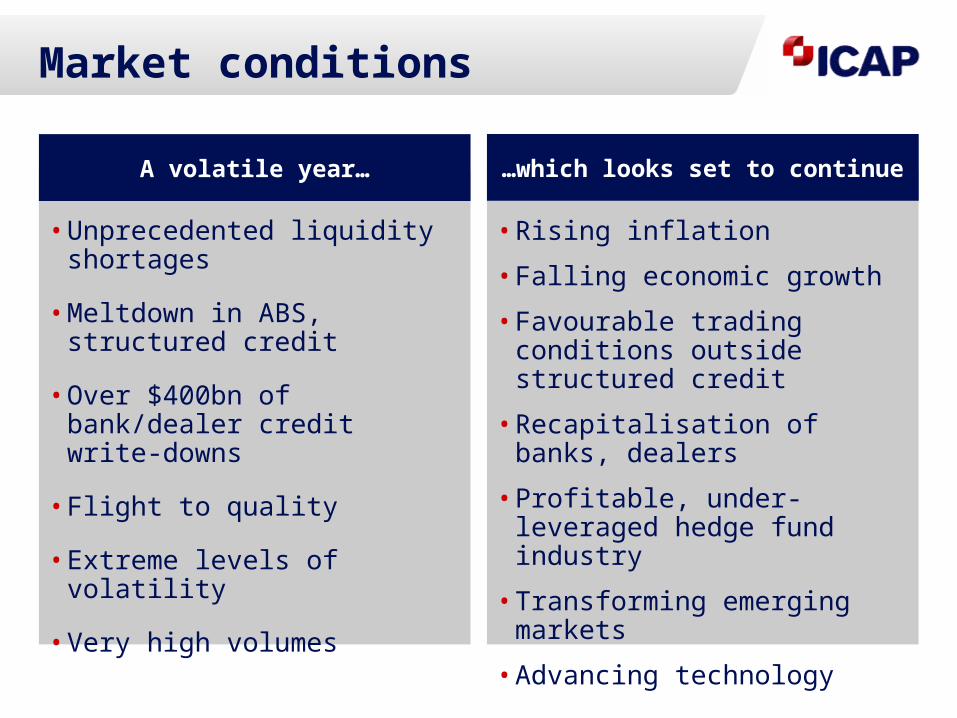

Market conditions

• Unprecedented liquidity shortages

• Meltdown in ABS, structured credit

• Over $400bn of bank/dealer credit write-downs

• Flight to quality

• Extreme levels of volatility

• Very high volumes

• Rising inflation

• Falling economic growth

• Favourable trading conditions outside structured credit

• Recapitalisation of banks, dealers

• Profitable, under-leveraged hedge fund industry

• Transforming emerging markets

• Advancing technology

A volatile year… …which looks set to continue

Developments in OTC Markets

• Growth of derivatives trading• Growth of electronic trading• Best execution requirements• Rapid growth/change in buy-side demographics• Bank/dealer consolidation• Need to improve dealers/clients post trade processing

capabilities• Counterparty credit risk• Potential for increased regulation

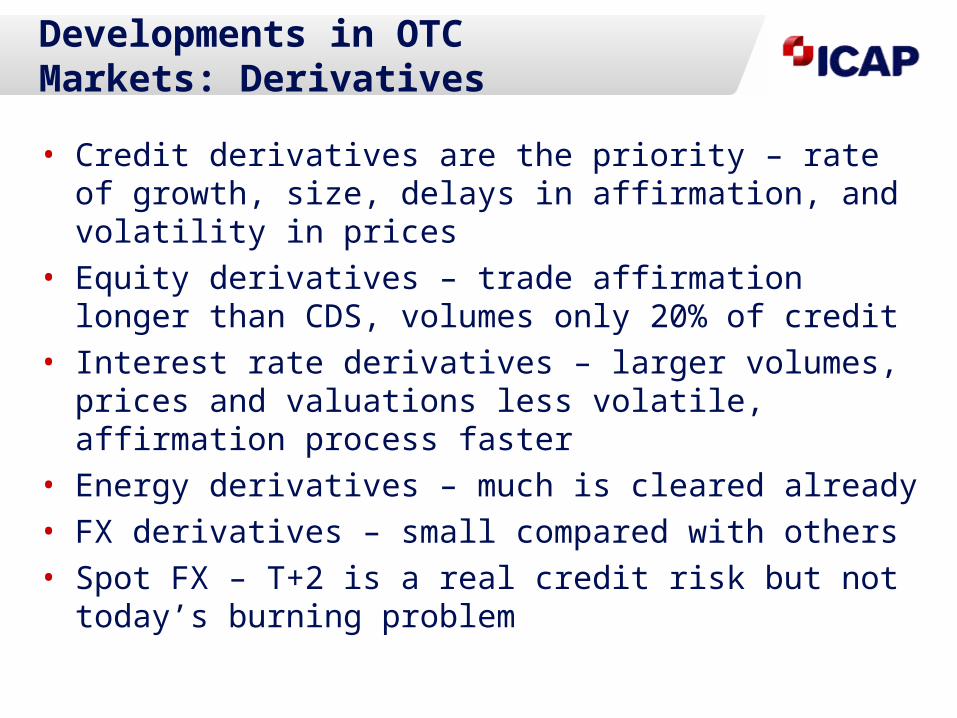

Developments in OTC Markets: Derivatives

• Credit derivatives are the priority – rate of growth, size, delays in affirmation, and volatility in prices

• Equity derivatives – trade affirmation longer than CDS, volumes only 20% of credit

• Interest rate derivatives – larger volumes, prices and valuations less volatile, affirmation process faster

• Energy derivatives – much is cleared already• FX derivatives – small compared with others• Spot FX – T+2 is a real credit risk but not today’s burning

problem

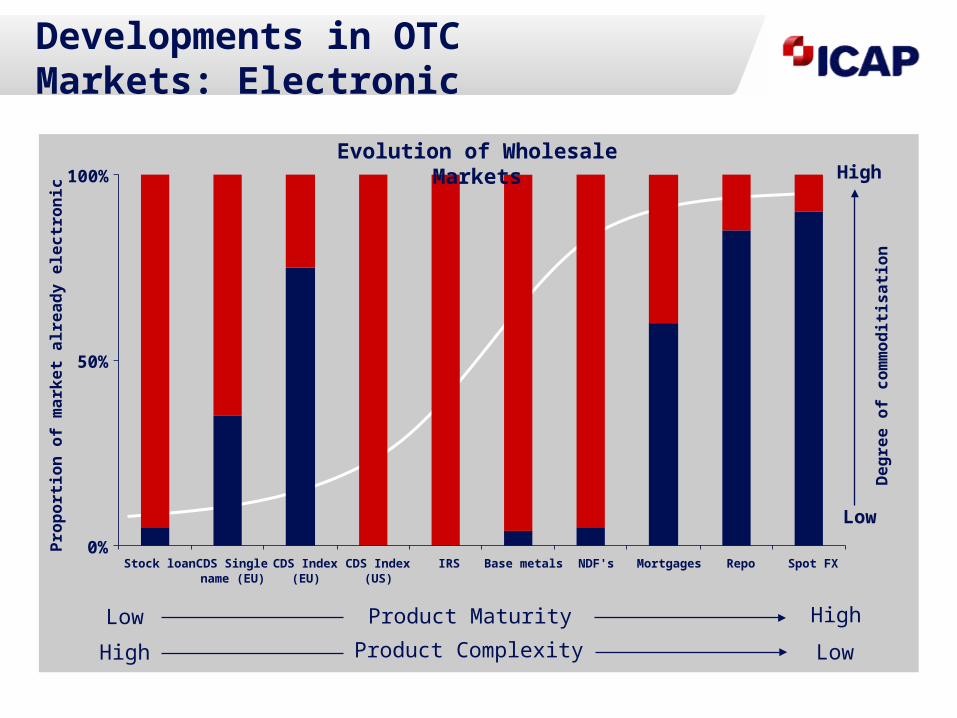

Developments in OTC Markets: Electronic

Low

High

High

LowProduct ComplexityProduct Maturity

High

LowProp

ortio

n of

mar

ket a

lread

y el

ectr

onic

Deg

ree

of c

omm

oditi

satio

n

0%

50%

100%

Stock loan CDS Singlename (EU)

CDS Index(EU)

CDS Index(US)

IRS Base metals NDF's Mortgages Repo Spot FX

Evolution of Wholesale Markets

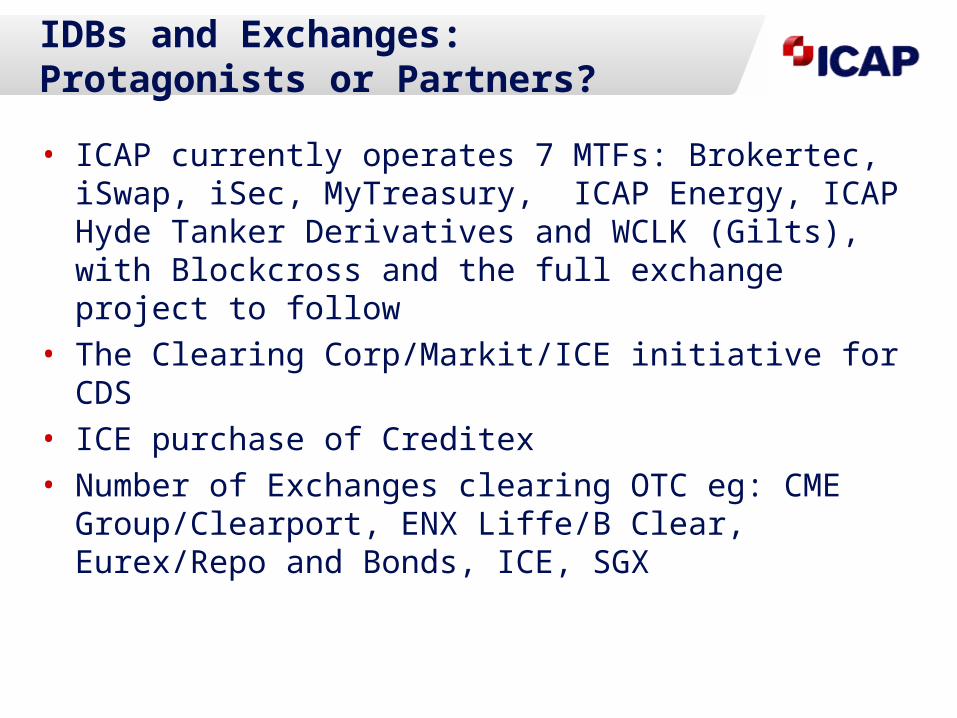

IDBs and Exchanges: Protagonists or Partners?

• ICAP currently operates 7 MTFs: Brokertec, iSwap, iSec, MyTreasury, ICAP Energy, ICAP Hyde Tanker Derivatives and WCLK (Gilts), with Blockcross and the full exchange project to follow

• The Clearing Corp/Markit/ICE initiative for CDS• ICE purchase of Creditex• Number of Exchanges clearing OTC eg: CME

Group/Clearport, ENX Liffe/B Clear, Eurex/Repo and Bonds, ICE, SGX

Evolving IDB Business Models

• Current market turmoil will create opportunities despite the wider customer base consolidating and the continued de-leveraging

• OTC market structures functioned very successfully during exceptionally busy period following collapse of Lehman Brothers

• Diversified across asset classes and customer types: no single customer accounts for more than 5% of ICAP Group revenues

• Reducing counterparty, market and operational risk: increasing capacity and lowering costs for customers and other market participants

• Clearing of OTC products will become more prevalent

• Significant portion of ICAP’s OTC business is cleared

• Post Trade Services: processing, portfolio compression, reconciliation, risk management

• Opportunities in exchange traded and clearing space

ICAP: Goals and Strategies

• To be the leading global intermediary in the wholesale OTC markets

• 35% share of overall market revenues

• 50% of profit derived from electronic broking

• To generate superior EPS growth for our investors

• Build and maintain close long term relationships with customers

• Leverage people and technology in a unique business model

• Provide customers with more efficient electronic trade execution, reduced integration costs and deep liquidity across a wide product range

• Extend product and service innovation - post-trade services business is an area where technology innovation is creating exciting new business opportunities

• Grow the business, both organically and by selective acquisition

Goals

Strategy

Electronic, Voice & Hybrid

• The outlook for the hybrid business model remains positive• IDBs are strong and innovative• ICAP is investing significantly in the development of its

voice, electronic and post-trade businesses. • Key growth areas for broking over the next 3-5 years –

emerging markets, credit, equities, energy/commodities and transport

• Favourable conditions for the businesses we have invested in heavily in the past – particularly rates and FX

• Substantial competitive advantage in critical electronic broking arena

• Post trade services businesses are growing very rapidly

Technology

• Well developed e-commerce strategy• Evolution from spot/cash markets to complex derivatives• ICAP operates a number of globally distributed electronic

platforms: Brokertec, EBS, MIT• Competitors recognise value in the strategy eg: GFI

purchase of Trayport, BGC/Espeed, ICE/Creditex

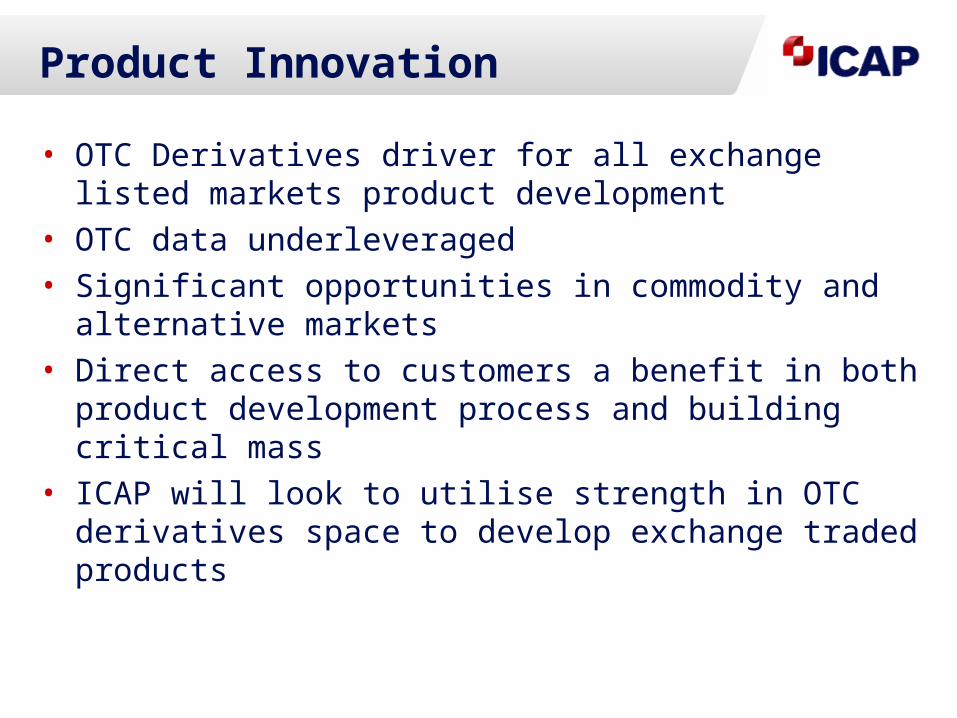

Product Innovation

• OTC Derivatives driver for all exchange listed markets product development

• OTC data underleveraged• Significant opportunities in commodity and alternative

markets• Direct access to customers a benefit in both product

development process and building critical mass• ICAP will look to utilise strength in OTC derivatives space

to develop exchange traded products

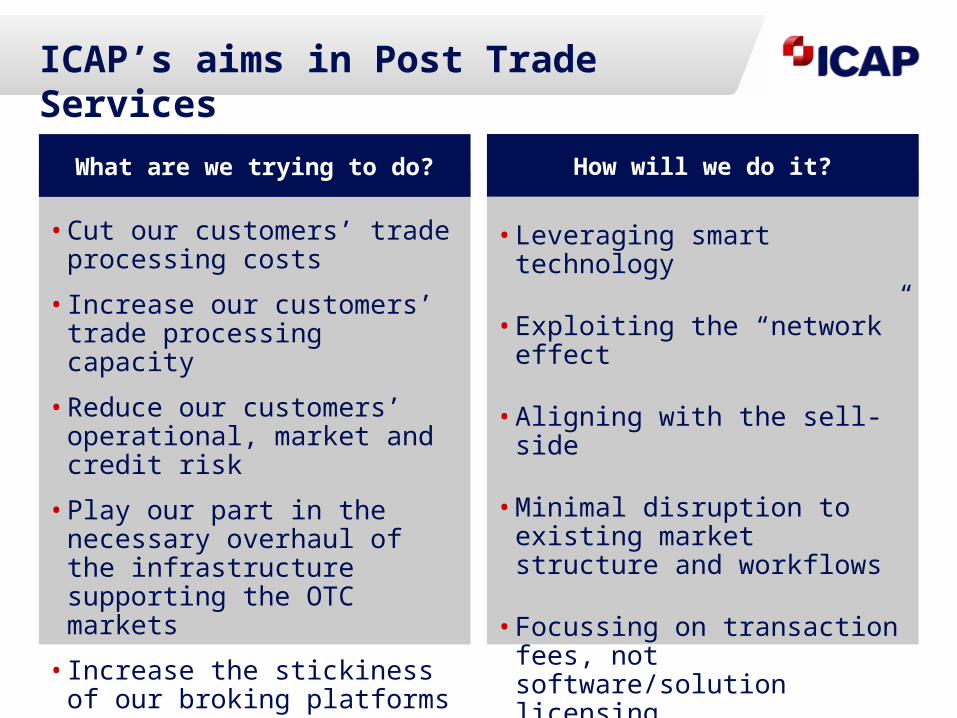

ICAP’s aims in Post Trade Services

• Cut our customers’ trade processing costs

• Increase our customers’ trade processing capacity

• Reduce our customers’ operational, market and credit risk

• Play our part in the necessary overhaul of the infrastructure supporting the OTC markets

• Increase the stickiness of our broking platforms

• Leveraging smart technology

• Exploiting the “network” effect

• Aligning with the sell-side

• Minimal disruption to existing market structure and workflows

• Focussing on transaction fees, not software/solution licensing

• Leveraging other people’s capital

What are we trying to do? How will we do it?

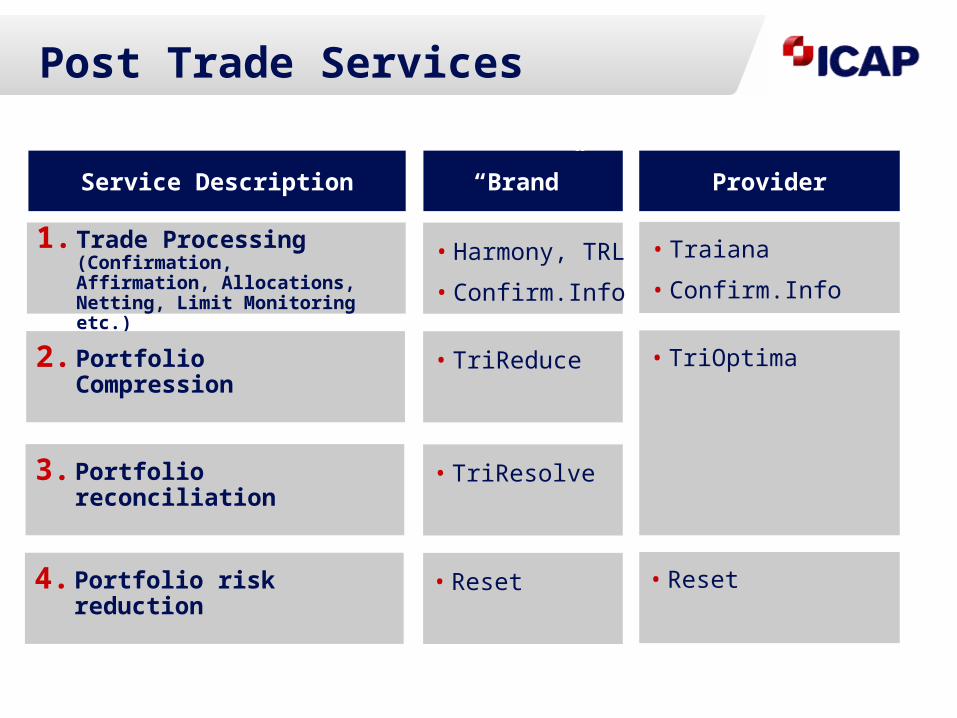

Post Trade Services

1. Trade Processing (Confirmation, Affirmation, Allocations, Netting, Limit Monitoring etc.)

Service Description Provider“Brand”

2. Portfolio Compression

3. Portfolio reconciliation

4. Portfolio risk reduction

• Traiana

• Confirm.Info

• TriOptima

• Reset

• Harmony, TRL

• Confirm.Info

• TriReduce

• TriResolve

• Reset

Post Trade Services: Traiana

• The leading post trade processing service provider for FX• Comprehensive confirmation/affirmation, allocation, limit

monitoring and netting services to prime brokers and banks• Overall market size: 1 million tickets/day wholesale plus 1m

tickets/day retail – and growing• Harmony ticket numbers growing +40 % pa. In July 08 daily

tickets were 134k.• Harmony volumes growing +50% pa.

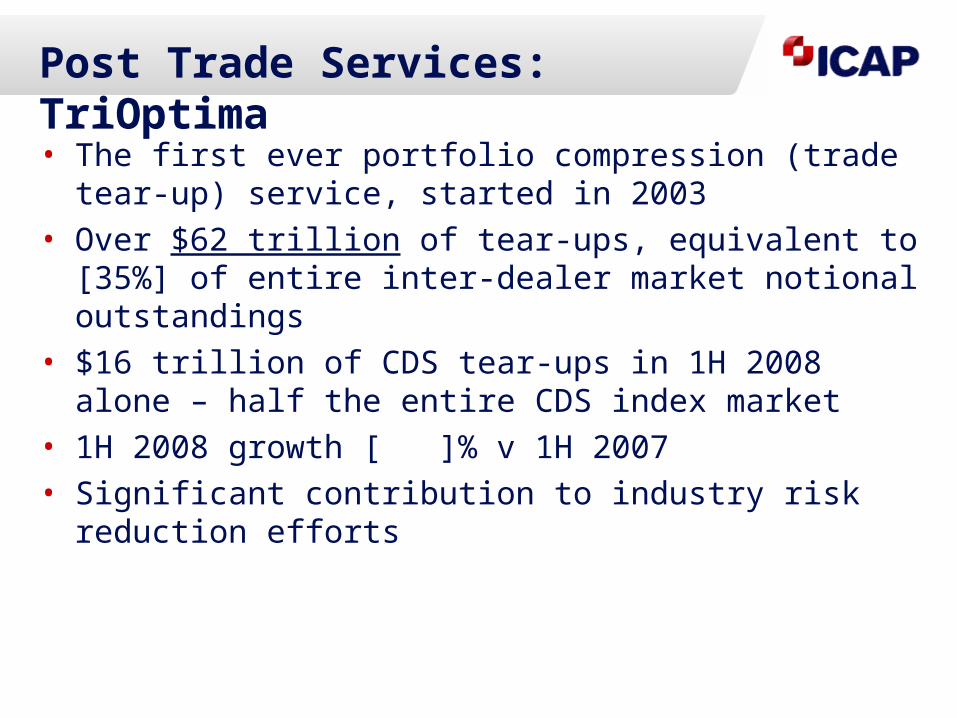

Post Trade Services: TriOptima

• The first ever portfolio compression (trade tear-up) service, started in 2003

• Over $62 trillion of tear-ups, equivalent to [35%] of entire inter-dealer market notional outstandings

• $16 trillion of CDS tear-ups in 1H 2008 alone – half the entire CDS index market

• 1H 2008 growth [ ]% v 1H 2007• Significant contribution to industry risk reduction efforts

Post Trade Services: Reset

• The leading LIBOR reset matching engine for the wholesale IRS market

• Total addressable market: ~$[125] trillion outstanding

• Eliminated floating rate reset risk of $36.8 trillion IRS in 1H 2008 approximately 30% of entire outstanding inter-dealer IRS market

• 1H 2008 volume growth 110% vs. 1H 2007

• Very substantial reduction in basis risk for dealers (at a time of high volatility)

• Technique applicable in other asset classes

Improving Post Trade Processing

• Better trade capture

• Improved trade affirmation/matching/confirmation tools

• Efficient OTC central counterparty clearing

• Better collateral management tools

• Robust, automated, independent valuation tools

• Payment processing as close to T+0 a possible

• Securities settlement as close to real time as possible

OTC and the CCPs

• Competition in clearing: EMCF, OCC/NYSE Euronext

• Horizontal (independent) v Vertical (integrated) models

• Proliferation of MTFs altered CCPs attitude to potential customers/partners

• Diversified Independent CCP preferred

• Shift to clearing OTC a major focus post sub prime fallout

Outlook

• Powerful, structural reasons to be optimistic about the medium term future for diversified IDBs

• The credit and liquidity squeeze continues to drive volume growth and volatile markets look set to continue for the foreseeable future

• Favourable conditions for the big businesses ICAP have invested in – particularly rates and FX

• More attractive opportunities to acquire businesses and hire people than there have been for a long time. 2008/9- a year of investment in the future

• Key growth areas for IDBs over the next 3-5 years – emerging markets, credit, equities, energy/commodities and transport

• ICAP has a significant competitive advantage in critical electronic broking arena

• Post trade services businesses are growing very rapidly