Embed Size (px)

Citation preview

Knowledge Leadership

MasterCard Worldwide Insights3Q 2011

The Challenges of Urbanization in Sub-Saharan Africa: A Tale of Three Cities

by Yuwa Hedrick-Wong and George Angelopulo

MasterCard WorldwideA Global Knowledge Leader

MasterCard Worldwide is widely recognized as aknowledge leader around the world. Over the years,the global payment solutions company has devotedextensive resources to developing a deeper under-standing of the payments card markets and the busi-ness and economic environment through surveys andindependent research studies. Some of these initia-tives include the MasterCard Worldwide Index of Con-sumer Confidence, MasterCard Worldwide Index ofWomen’s Advancement, MasterCard Worldwide Cen-ters of Commerce, MasterCard Worldwide Index ofConsumer Purchasing Priorities, MasterCard World-wide Index of Consumer Resilience and MasterCardWorldwide Index of Consumer Spending Capability.Today, these MasterCard offerings are much soughtafter by analysts, academics and decisionmakers infinancial institutions, government agencies and multi-national organizations.

Launched in 1993, the MasterCard WorldwideIndex of Consumer Confidence has proven to be anexcellent barometer of the general consumer pulse inAsia/Pacific. The twice-annual survey analyzes prevail-ing consumer perceptions of economic conditions forthe next six months. Its insights into the dynamics ofconsumer sentiment, and the market paradigm delivervalue to a variety of audiences, including customersand business partners.

In 2003, MasterCard established the MasterIntelli-gence Knowledge Panel, which comprises leadingeconomists and business strategists from China, HongKong, India, Japan, Korea and South East Asia. In2006, it was expanded to become a global knowledgepanel, which now conducts research and providesinsights on the economic and business environmentglobally. The panel is headed by Dr. Yuwa Hedrick-Wong, Economic Advisor, MasterCard Worldwide. In2009, an African Knowledge Panel was established.

Today, MasterCard continues to demonstrate itscommitment by not only adding value with cuttingedge research but also through sharing knowledge innew areas. Its knowledge leadership is well recog-nized and unrivaled.

1 MasterCard Worldwide Insights

Q3 2011 2

Foreword: A Tale of Three Cities

Urbanization is one of the most significant trends inSub-Saharan Africa at present, with rural populationsmigrating at unprecedented rates to urban hubs insearch of employment and economic growth.

In this report, the second in the MasterCard seriesof research reports into Africa entitled: “The Chal-lenges of Urbanization in Sub-Saharan Africa: A Taleof Three Cities”, the research team of Dr. YuwaHedrick-Wong and Professor George Angelopulooffer insights into urbanization in three significantAfrican cities– Lagos, Nairobi and Maputo.

The report highlights that urbanization is key toboosting productivity and economic activity in devel-oping markets, but unless it is carefully planned andimplemented, it can lead to structural weaknessesand even breaking points in cities that are not ade-quately prepared for the uncontrolled influx of ruralpopulations seeking to improve their lives.

Each of the three cities discussed in the report hasnoteworthy successes in servicing their growing pop-ulations, but each has also been challenged in under-estimating the scale of urbanization and the planningand development needed to accommodate it.

The consequence of this includes, among others,the mushrooming of slums, pressure on infrastructureand the social problems that accompany unemploy-ment in an urban setting. Failing to prepare for these,or to address them adequately, could see emergingmarkets fall into the trap of replacing rural underde-velopment with urban underdevelopment - a destruc-tive scenario that betrays the enormous potential thatis so apparent on the African continent.

So where and how can African markets find thebalance between the benefit of increased economicactivity of urban dwellers with the costs of accommo-dating them with appropriate infrastructure and sys-tems?

While getting urbanization right is key to position-ing for future economic growth, it is important tonote that there is no single fast-fix that can be

applied to any of the problems afflicting Africa’surbanized populations. There is significant cultural,social and economic diversity from region to region,and indeed city to city – and the key to success inthese markets will be careful management of theresource-driven expansion, with local solutions thatrespond to local situations.

Earlier this year, the first in a series of four Master-Card Worldwide Insights reports on Africa wasreleased entitled: “Taking Stock: The State of Sub-Saharan Africa” by Dr. Azar Jammine and Dr. MartynDavies - and offered an overview of the current statusquo on the continent and insights into the opportuni-ties and inhibitors for those seeking to do business ona continent that is variously seen as challenging toinvest in or as the world’s current greatest opportuni-ty for significant growth. Should you wish to viewthat report, please visit www.masterintelligence.com

I trust that you will find this second MasterCardInsights report into African markets a comprehensiveand useful tool for your future business planning.

Yours sincerely,

Michael MiebachDivision President, Middle East & AfricaMasterCard Worldwide

3 MasterCard Worldwide Insights

The Challenges of Urbanizationin Sub-Saharan Africa: A Tale ofThree Cities

Introduction: Urbanization and Development

Urbanization is today a truly global phenomenon.Even though many of the developed markets hadexperienced rapid urbanization when they industrial-ized in the 19th and 20th centuries, their urbaniza-tion process has never really stopped, and has beengaining new momentum recently. A dramatic illustra-tion of this is in Germany, where in the last decadethe wolves have returned to rural regions as smalltowns and villages are increasingly becoming depop-ulated as young people continue to move to live incities.1 For the developed markets, a renewedmomentum in urbanization is critical for revitalizingtheir economies. Their large urban regions havebecome the cradle for nurturing their creative indus-tries, facilitating business innovations, and drivingeconomic growth with ideas and human ingenuity.

In emerging markets, urbanization is even moreimportant as a key driver of development andgrowth. Shifting underemployed rural people to moreproductive employment in urban areas is fundamen-tal to lifting productivity overall, which in turn consti-tutes a sustainable platform for future investmentand growth. Getting urbanization right, however, hasbeen a major challenge for emerging markets every-where. Indeed, managing urbanization effectivelyrequires emerging markets to succeed in areas wherethey are typically the weakest: sufficient investmentin physical and human infrastructure, effective policycoordination between central and municipal govern-ments, appropriate and forward planning andenforcement, creating a supportive environment forprivate businesses to thrive and create jobs, provisionof law and order, and assuring effective governanceat all levels of administration. It is therefore not sur-prising that in many emerging markets urbanizationhas been poorly managed. The results are plain for allto see in many cities in emerging markets: massiveslums, lack of basic services for most urban dwellers,high urban unemployment and underemployment,chronic traffic congestion and gridlocks, chaotic zon-

ing and lack of enforcement, and overall poor anddeteriorating urban quality of life. Thus, in failing toget urbanization right, many emerging markets riskfalling into the trap of creating massive urban sprawlof poverty that merely replaces rural underdevelop-ment with urban underdevelopment.

Among the most important emerging marketstoday, rapid urbanization has been one of the mostsalient features of China’s development success.China appears to have gotten urbanization right. It istherefore worthwhile examining China’s urbanizationexperience in some detail to identify appropriatelessons learned. The record so far is an impressiveone. In the mid-1980s, urban population representedless than a quarter of China’s total population. By2009, urban population had risen to over half of thetotal population. In the past decade and a half, over20 million people were urbanized each year on aver-age. Thus, the net addition of urban population eachyear in China is about equal to the entire populationof Australia. This rate of urbanization is historicallyunprecedented. Urbanization in China is expected tocontinue to grow at a high rate of about 2.7% peryear in the foreseeable future. Rapid growth of urbanpopulation in China has not been limited to a few keycities, however. In the last decade and a half, sec-ondary cities away from the coastal region have actu-ally been growing faster than the big three of Beijing,Shanghai and Guangzhou, making urbanizationmore evenly spread than in many other emergingmarkets.

In spite of this rapid pace of urbanization, there issomething distinctive about China’s cities; makingthem unique among cities in the developing world.Many first time visitors notice it the moment theyleave the airport in one of the big cities on their driveto downtown; or when they travel within China fromone city to the next. Chinese cities do not have thesprawling slums that are the hallmarks of cities inemerging markets such as Philippines, India, Nigeria,or Brazil. The fact that Chinese cities have escapedthe curse of urban slums is a result of both its socialistlegacy of highly centralized control of people’s move-ment, and an unintended consequence of its ruralreform.

Q3 2011 4

5 MasterCard Worldwide Insights

Under socialist central planning, populationmovement was strictly controlled in China. For muchof the period from 1949 when the Communist Partywon the civil war to 1978 when economic reformbegan; permission was needed from one’s govern-ment work unit to buy a simple bus or train ticket togo to a nearby city. For the first three decades afterthe founding of the People’s Republic, there was vir-tually no rural-urban migration. In order to stay in acity, a person had to have an official permit, thehukou, without which they would not have been ableto find a job, rent a flat, enroll their children inschool, or receive medical care. In other words, arural person would have all the basic amenitiesdenied them without a hukou, even if they wereenterprising enough to sneak into a city unofficially.Given that the government owned and allocated allurban housing, ran all the healthcare facilities andschools, and assigned all the jobs, it was very easy toenforce migration control: no hukou, no nothing.

Today, an urban hukou can be obtained relativelyeasily once a person can prove that they have a job inthe city. In fact, the city governments of many second-and third-tier cities, in order to expand faster, offer anofficial hukou to anyone from the outside who haspurchased a private condo above a certain minimumvalue. Under these conditions, rural-urban migrationcould have exploded into uncontrolled torrents ofopportunity-seeking migrants, following the patternsseen in many other other third-world cities. But it did-n’t happen in China.

The fact that it didn’t has a lot to do with landownership in rural China. There is, strictly speaking, noprivate land ownership yet. Land reform had givenrural households a long-term lease (30 years) for theuse of a plot of land; and recent reform measuresallow them to use the land as collateral for investmentloans, or to lease it to other households to consolidatethe plots into a a larger-size farm, etc. But, if the ruralhousehold were to obtain an urban hukou, it wouldautomatically lose the right to the land in its home vil-lage. So it is an either/or choice; no household can beboth urban and rural at the same time. This creates ade facto cost-benefit calculus that the rural householdhas to consider carefully. Is the urban job secureenough to give up the land in the village? Is the pay

sufficiently high to compensate for the higher costs ofliving in the city? Or is it better to work in the city as amigrant worker (officially defined as working in a hostcity for more than six months at a time) and thenreturn to the home village to work on the land justbefore the planting season starts, with extra cash inpocket saved from working in the city? Thus, becauseof the trade-off between the land in the village andthe hukou, in the city, rural-urban migration is self-reg-ulated. A new arrival in the city tends to be someonewith a relatively secure job and a pay level goodenough to cover the higher costs of urban living withsomething to spare. Rural-urban migrants with no jobsand poor employment prospects in a city, in otherwords, potential slum dwellers, are therefore extreme-ly rare; and hence the absence of sprawling urbanslums in China’s cities.

This self-regulated nature of rural-urban migrationthen responds directly to employment opportunitiescreated in the cities. Between 1995 and 2007, about150 million new urban jobs were created in China,which were sufficient to lure some 300 million people(workers and their families) to resettle in China’s cities.So China’s cities are very powerful job creationmachines. And an important factor that enablesChina’s cities to function as job creation machines istheir rapidly improving infrastructure. Better infrastruc-ture has been critically important in lowering the costsof logistics and enhancing information flow, therebyattracting new investments into urban areas. It alsoallows cities to expand physically.

A more detailed look at the components of the300-million increase in urban population over the lastdecade and a half reveals the importance of infrastruc-ture development. Based on official data,2 about one-third of this increase has come from rural migrationand about 15% from organic growth. The majority,about 52%, however, has come from cities expandinginto adjacent rural areas –– a process where areas pre-viously rural are transformed into urban. Both expand-ing cities and newly-urbanized rural areas require sig-nificant infrastructure improvements, including trans-portation and telecommunications links, water andelectricity supply, housing development, and typicalurban facilities such as shopping malls, tertiary healthcare and higher education services, and financial dis-

tricts–– all of which require massive investment. Whileinvestment in infrastructure creates jobs, this is onlythe beginning of the process. Once the infrastructureis in place, business development then follows, creat-ing even more jobs. Infrastructure development, busi-ness investment, and urbanization are therefore threemutually-reinforcing trends that characterize China’seconomic growth.

This quick review of China’s urbanization experi-ence shows both lessons learned that could be trans-ferred to other emerging markets, and the limits ofthis transferability. A high level of investment in infra-structure is clearly crucial to ensure that urbanization isgenerating the kind of economic efficiency thatattracts business investment and job creation, whilebuilding a better environment for people to live andwork. This is true for urbanization generally, and espe-cially so for emerging markets that lack such infra-structure to begin with. On the other hand, China’spolitical system and its central planning allow theauthorities to control rural-urban migration, fast trackinvestment projects, and direct the flow of financialresources to fund the investment, often with dracon-ian means.3 These conditions are not easily replicablein most emerging markets, especially in places wherethe democratic process is better established, andwhere decision-making requires at least some form of

consensus at grassroots level. So China’s model ofurbanization, as successful as it may have been, couldnot be simply copied, nor should it be. So for better orworse, many emerging markets will have to meet thechallenge of urbanization by the means that are attheir disposal, inadequate as they frequently are. TheSub-Saharan Africa region is no exception.

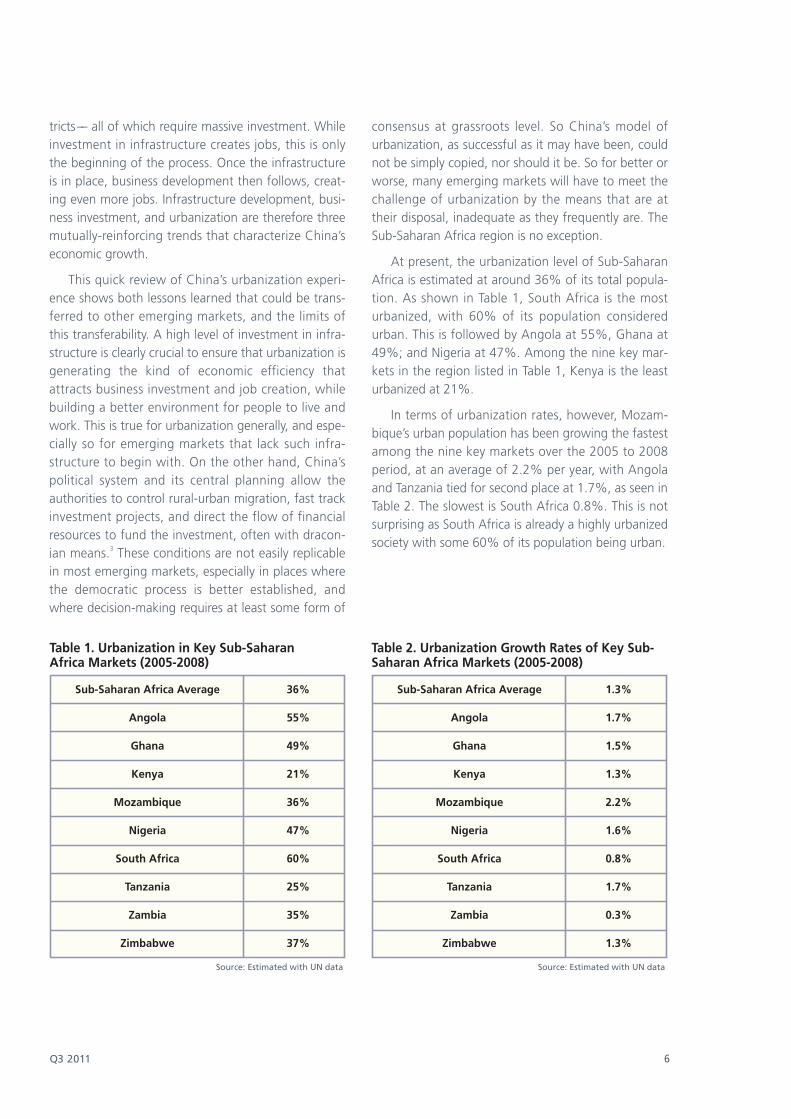

At present, the urbanization level of Sub-SaharanAfrica is estimated at around 36% of its total popula-tion. As shown in Table 1, South Africa is the mosturbanized, with 60% of its population consideredurban. This is followed by Angola at 55%, Ghana at49%; and Nigeria at 47%. Among the nine key mar-kets in the region listed in Table 1, Kenya is the leasturbanized at 21%.

In terms of urbanization rates, however, Mozam-bique’s urban population has been growing the fastestamong the nine key markets over the 2005 to 2008period, at an average of 2.2% per year, with Angolaand Tanzania tied for second place at 1.7%, as seen inTable 2. The slowest is South Africa 0.8%. This is notsurprising as South Africa is already a highly urbanizedsociety with some 60% of its population being urban.

Q3 2011 6

Source: Estimated with UN data

Table 1. Urbanization in Key Sub-Saharan Africa Markets (2005-2008)

Sub-Saharan Africa Average

Angola

Ghana

Kenya

Mozambique

Nigeria

South Africa

Tanzania

Zambia

Zimbabwe

36%

55%

49%

21%

36%

47%

60%

25%

35%

37%

Source: Estimated with UN data

Table 2. Urbanization Growth Rates of Key Sub-Saharan Africa Markets (2005-2008)

Sub-Saharan Africa Average

Angola

Ghana

Kenya

Mozambique

Nigeria

South Africa

Tanzania

Zambia

Zimbabwe

1.3%

1.7%

1.5%

1.3%

2.2%

1.6%

0.8%

1.7%

0.3%

1.3%

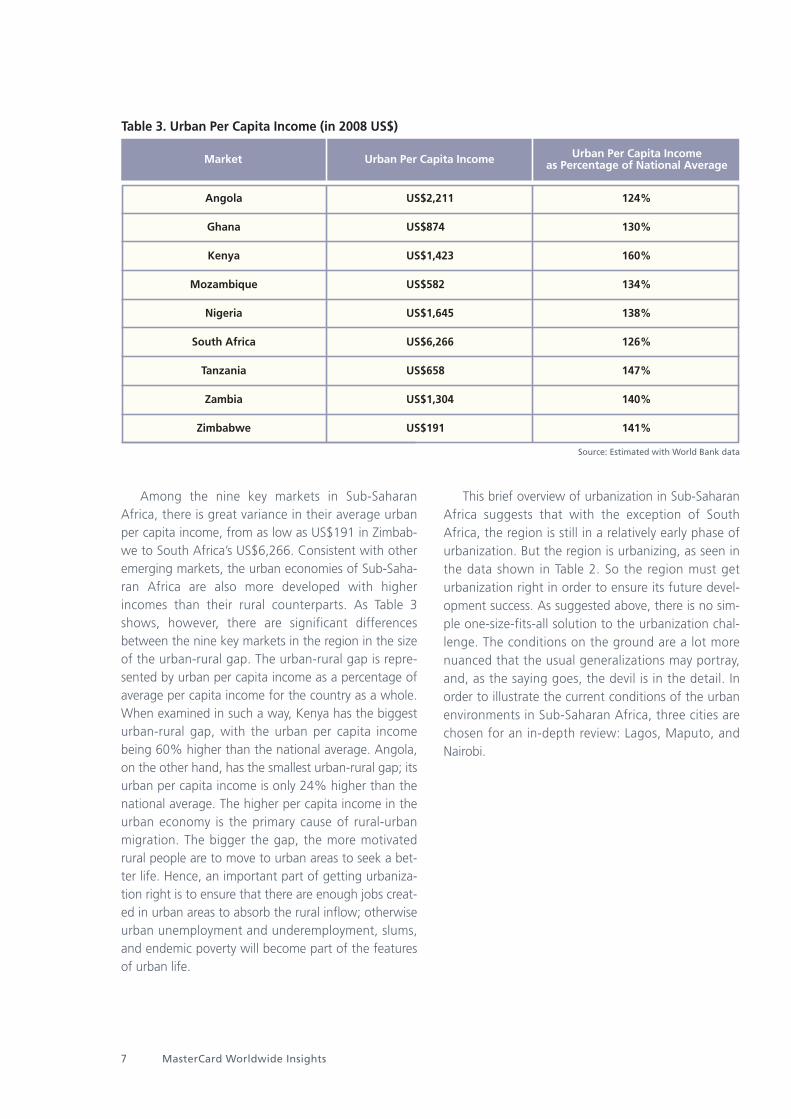

Among the nine key markets in Sub-SaharanAfrica, there is great variance in their average urbanper capita income, from as low as US$191 in Zimbab-we to South Africa’s US$6,266. Consistent with otheremerging markets, the urban economies of Sub-Saha-ran Africa are also more developed with higherincomes than their rural counterparts. As Table 3shows, however, there are significant differencesbetween the nine key markets in the region in the sizeof the urban-rural gap. The urban-rural gap is repre-sented by urban per capita income as a percentage ofaverage per capita income for the country as a whole.When examined in such a way, Kenya has the biggesturban-rural gap, with the urban per capita incomebeing 60% higher than the national average. Angola,on the other hand, has the smallest urban-rural gap; itsurban per capita income is only 24% higher than thenational average. The higher per capita income in theurban economy is the primary cause of rural-urbanmigration. The bigger the gap, the more motivatedrural people are to move to urban areas to seek a bet-ter life. Hence, an important part of getting urbaniza-tion right is to ensure that there are enough jobs creat-ed in urban areas to absorb the rural inflow; otherwiseurban unemployment and underemployment, slums,and endemic poverty will become part of the featuresof urban life.

This brief overview of urbanization in Sub-SaharanAfrica suggests that with the exception of SouthAfrica, the region is still in a relatively early phase ofurbanization. But the region is urbanizing, as seen inthe data shown in Table 2. So the region must geturbanization right in order to ensure its future devel-opment success. As suggested above, there is no sim-ple one-size-fits-all solution to the urbanization chal-lenge. The conditions on the ground are a lot morenuanced that the usual generalizations may portray,and, as the saying goes, the devil is in the detail. Inorder to illustrate the current conditions of the urbanenvironments in Sub-Saharan Africa, three cities arechosen for an in-depth review: Lagos, Maputo, andNairobi.

7 MasterCard Worldwide Insights

Source: Estimated with World Bank data

Table 3. Urban Per Capita Income (in 2008 US$)

Angola

Ghana

Kenya

Mozambique

Nigeria

South Africa

Tanzania

Zambia

Zimbabwe

US$2,211

US$874

US$1,423

US$582

US$1,645

US$6,266

US$658

US$1,304

US$191

124%

130%

160%

134%

138%

126%

147%

140%

141%

Market Urban Per Capita Income Urban Per Capita Income as Percentage of National Average

A Tale of Three Cities:Lagos, Nairobi, and Maputo

The prognosis for Africa’s cities remains mixed. In thepast three decades few have predicted a bright futurefor Africa’s urban areas. The overriding sentiment isencapsulated by the assessment that “Africa boastsmany huge, rapidly growing cities, but it's hard toidentify many of these places–– like Lagos, Luanda orKinshasa –– as bright prospects.’ 4 But an alternativeview is increasingly being heard. “Africa has a largermiddle-class population than India. It is undergoingrapid urbanization, bringing millions out of ruralemployment. Growth in Sub-Saharan Africa will bebetween 4% and 7% this year, a figure at least doubleanything expected in Europe or America. There will beplenty of traps for the unwary, but just as five yearsago everyone said investors should look to China, wemay be on the verge of a dash to Africa.”

5The view of

Africa and its urban environment is certainly changing.

In assessing urbanization in Sub-Saharan Africa, it isworthwhile looking at specific cases, and in this dis-cussion it is three prominent cities in the African land-scape that fall under the microscope. Lagos, Maputoand Nairobi are geographically dispersed and they varyin size and importance in their regions and on the con-tinent as a whole. They are unique, but they also sharecertain characteristics with many of Africa’s urbanagglomerations, and serve well to reflect the currentstate of the African city.

Lagos

Lagos was originally part of the Kingdom of the Yoru-ba. Following the arrival of the Portuguese in the early1400s it became a major slave port, continuing withthe trade of slaves up to the mid 1800s. It wasannexed by Britain in 1861, ostensibly to stop the slavetrade but also as a way of controlling palm and othertrade in the region. In 1914 Nigeria became a British

Q3 2011 8

Chart 1. Lagos

colony with Lagos as its capital, and it remained thecapital through Nigeria’s independence in 1960 up to1991 when Abuja was made the capital. Despite itsloss of political status, Lagos has continued to developand grow.

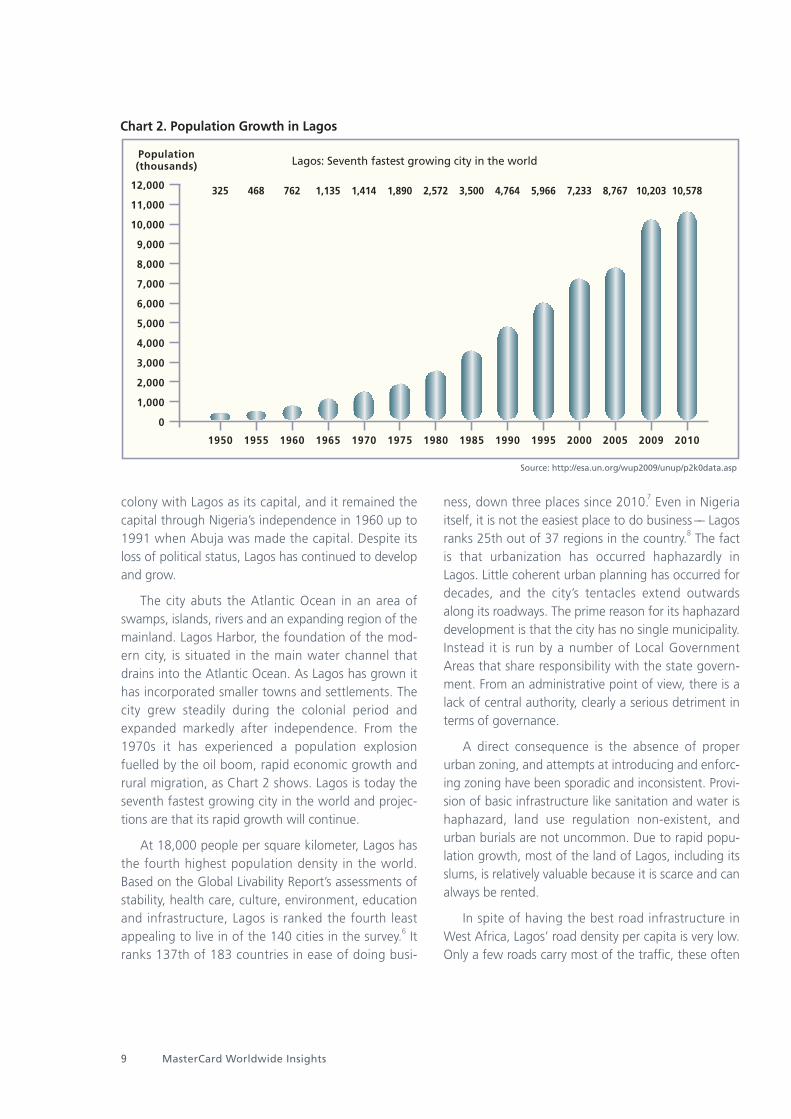

The city abuts the Atlantic Ocean in an area ofswamps, islands, rivers and an expanding region of themainland. Lagos Harbor, the foundation of the mod-ern city, is situated in the main water channel thatdrains into the Atlantic Ocean. As Lagos has grown ithas incorporated smaller towns and settlements. Thecity grew steadily during the colonial period andexpanded markedly after independence. From the1970s it has experienced a population explosionfuelled by the oil boom, rapid economic growth andrural migration, as Chart 2 shows. Lagos is today theseventh fastest growing city in the world and projec-tions are that its rapid growth will continue.

At 18,000 people per square kilometer, Lagos hasthe fourth highest population density in the world.Based on the Global Livability Report’s assessments ofstability, health care, culture, environment, educationand infrastructure, Lagos is ranked the fourth leastappealing to live in of the 140 cities in the survey.6 Itranks 137th of 183 countries in ease of doing busi-

ness, down three places since 2010.7 Even in Nigeriaitself, it is not the easiest place to do business –– Lagosranks 25th out of 37 regions in the country.8 The factis that urbanization has occurred haphazardly inLagos. Little coherent urban planning has occurred fordecades, and the city’s tentacles extend outwardsalong its roadways. The prime reason for its haphazarddevelopment is that the city has no single municipality.Instead it is run by a number of Local GovernmentAreas that share responsibility with the state govern-ment. From an administrative point of view, there is alack of central authority, clearly a serious detriment interms of governance.

A direct consequence is the absence of properurban zoning, and attempts at introducing and enforc-ing zoning have been sporadic and inconsistent. Provi-sion of basic infrastructure like sanitation and water ishaphazard, land use regulation non-existent, andurban burials are not uncommon. Due to rapid popu-lation growth, most of the land of Lagos, including itsslums, is relatively valuable because it is scarce and canalways be rented.

In spite of having the best road infrastructure inWest Africa, Lagos’ road density per capita is very low.Only a few roads carry most of the traffic, these often

9 MasterCard Worldwide Insights

Chart 2. Population Growth in Lagos

1950

325

1955

468

1960

762

1965

1,135

1970

1,414

1975

1,890

1980

2,572

1985

3,500

1990

4,764

1995

5,966

2000

7,233

2005

8,767

2009

10,203

2010

10,578

Lagos: Seventh fastest growing city in the worldPopulation(thousands)

12,000

11,000

10,000

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Source: http://esa.un.org/wup2009/unup/p2k0data.asp

flood when it rains, and many roads are in poor condi-tion. No allowance is made for parking, even in thebusiness districts. Road safety is negligible and Lagoshas one of the highest accident rates in the world.Water transportation is underutilized, carrying lessthan 1% of Lagos’ traffic, and Nigerian Railways oper-ate only one train per day within the city.

The city faces the ongoing problem of supplyingsufficient water for an ever-increasing population.Only half of Lagos’ population receives potable water,but much of this is intermittent. Many inhabitantsbuild wells and boreholes for their water needs andprivate water distribution is a thriving business. Lagos’power supply is notoriously inadequate and unpre-dictable due to intermittent gas supply, faulty infra-structure, lack of maintenance and corruption. In thepast four years, the city has experienced a decrease inpower supply, and those who can, utilize generatorsfor their own electricity.

Lagos has no central sewage system and manydwellings resort to the use of septic tanks. The city hasa little over half the treatment plant capacity it needs,and trucks empty surplus sewage into the adjacentlagoon. Life can be difficult even for the middle classesin Lagos. As one commentator observed, they are“resigned to doing everything for themselves. There'slittle public transport, so you drive. The state schoolsaren't good, so you aspire to send your children to aprivate school. There are few landlines, so you havemobile phones. There is almost no central water sup-ply, so you dig your own well. There are no sewers, soyou have a septic tank. Mains electricity works only afew hours a day, so you have your own generator. Nomoney? Work harder, pray harder, get bettercronies.”

9

These unavoidable facts certainly dominate anyassessment of Lagos. So what is the upside? Much ofNigeria’s wealth is concentrated in Lagos. It is thecountry’s most prosperous city and the centre of itseconomic activity. Its $30bn economy is roughly thesize of Kenya’s. While there is massive poverty in thecity there is also a huge spread of affluence. Lagosattracts the best skills from Nigeria and West Africa.Many professionals who had emigrated returned toLagos after the global financial crisis in 2008/09 with

their international experience and scarce skills. Whilecorruption remains a problem, wholesale looting bypoliticians is a thing of the past.

Quality of life is also relative. In spite of the litanyof woes mentioned above, Lagos nevertheless offers ahigher standard of living than other cities in the regionand the best opportunities for success. A variety ofindustries are thriving in Lagos’ urban economy. Lagoshas a thriving commercial music industry and is thehome of Nigerian hip-hop, highlife, juju, fuji andAfrobeat. It is the centre of ‘Nollywood,’ the namegiven to the Nigerian movie industry, which producesmore movies than the USA and fewer only than India.Nollywood is the second-largest employer in Nigeriaafter the oil industry. Most of its low budget films areshot in Lagos and move directly to market throughoutAfrica. Lagos has one of the most vibrant mediascenes in Africa with multiple print media, state-runand private radio and TV stations. Despite a number ofrestrictive media regulations, the press is relatively free.Twenty-nine percent of Nigerians use the internet, andwithin Lagos the percentage is higher. Bandwidthincreased fivefold in 2010 with a new undersea fiber-optic cable. While mobile phone usage far outstripsfixed line, the increase in demand for internet servicesand broadband capabilities support the fixed-line sec-tor, which still has a market penetration of less than5%.

Affluent Nigerians spend $1.2 billion on luxurygoods in Dubai every year, and Lagos State is intent oncreating an alternative retail industry in Lagos. Retailopportunities have increased with more outlets andaccessibility to greater numbers of people. Lagos hasnumerous higher-end retail outlets such as the PalmsShopping Mall with 20,000 square meters of retailspace, 69 stores, a cinema complex and parking for athousand cars that was originally developed as anActis Capital/Tayo Amusan joint venture.

Lagos is also the end point of major trans-Africanroads to Algiers, Benin and further on to Dakar. ThePort of Lagos is one of the busiest in Africa, with threesections that include a container terminal and a rail-head. The port is a major point for the export of petro-leum products. More than five million airline passen-gers, half of all Nigeria’s, pass through Murtala

Q3 2011 10

Mohammed International Airport every year. The air-port has recently been expanded with the addition ofa terminal, and a new cargo complex is to be added.

Lagos’ strategic location has attracted foreigninvestment in recent years. For example, the Leki FreeZone, a multi-billion dollar free trade zone is beingdeveloped with Chinese investment on the edge ofLagos in order to develop a local manufacturing base.Complete basic infrastructure including water, powerand roads will be provided. A joint Nigerian-Chineseproject will see one of three new oil refineries built inthe city. Together, these should supply Nigeria’s refinedoil needs (currently Nigeria is a net importer of refinedpetrol products).

There has been steady progress in infrastructuredevelopment in the past five years. A Bus Rapid Transitscheme was launched in 2006 and its first phase com-pleted in 2008. Okada motorbike taxis have beenbanned from central roads in an attempt to reducetraffic injuries and congestion. Lagos is working withprivate companies to develop new toll roads in addi-tion to those that already exist. A railway line runningthrough Lagos is being constructed with planned com-pletion in 2012. Ferry transport has been regulatedand new waterway routes with regular services areplanned.

The supply of potable water should reach 70% ofthe population in the next decade with the improvedsupply of electricity to pumping stations and projectslike the recently commissioned Independent PowerProject. Plans are in place to supply a minimum of 16hours per day of continuous supply ‘soon’ by restruc-turing the national grid and increasing power supplywith projects such as the construction of an indepen-dent power plant in partnership with the SingaporePower Company. Besides the municipal waste authori-ty, there are 211 small and four large private wastedisposal operators who in combination dispose ofmore than two million metric tons of waste per year.The city has just developed the capacity to dispose ofmedical waste. A high profile and ambitious project isEko Atlantic City, an urban development on landreclaimed from the Atlantic Ocean. The developmentwill return a section of the Lagos coast to its positionin the 1950s and 1960s, reversing the damage of ero-

sion. Most of the land has been reclaimed, and whencomplete the development will have 400,000 resi-dents and 250,000 daily commuters.

These developments will not, even if they are suc-cessfully implemented as planned, supply the needs ofthe whole population of Lagos, but they will certainlyimprove the current situation. It is also encouraging tosee that many of these projects are developed by theprivate sector, including foreign investors, or in public-private partnerships, which is a very positive breakfrom patterns of the past. Compared to Stockholm orTokyo, conditions in Lagos will certainly be considereddire for the foreseeable future, but if one considers thecity’s prospects, it is easy to recognize the upside.Lagos is beginning to exhibit the positive characteris-tics of economies of scale and economies of scope,especially in creative industries and services–– hall-marks of a successful city. By most standards Lagos isWest Africa’s dominant city, and some believe that itwill become the continent’s dominant city within thenext decade. Rem Koolhaas, an architect and urbanist,believes that Lagos’ chaos is the reason why it thrivesand grows. Its inhabitants have learned to convertsome of its disadvantages to advantages.

10

Maputo

The region in which Maputo is now situated wasoriginally occupied by the Shangaan people. Vasco daGama explored the area in 1498, and it was colo-nized by Portugal in 1505. Lourenço Marques wascreated by Portugal as a minor fortress settlement,which it remained until 1850. In that year it wasdeveloped as a port, primarily as a conduit for theneighboring Transvaal Republic’s trade, and in 1898 itwas declared the capital of Mozambique. The citywas renamed Maputo following Mozambique’s inde-pendence in 1975. Two years after independence,Mozambique suffered a civil war that lasted until1992, resulting in economic collapse. Between 1987and 1990 Mozambique changed from a commandeconomy to a free market with one of the fastestgrowing economies in the world, albeit off a very lowbase. Maputo is a cultural melting pot. IndigenousAfrican culture dominates with strong Portugueseand South African influences, and Chinese, Arab andIndian cultural influences are also evident. It is adiverse metropolis, a tourist destination, and is inde-

11 MasterCard Worldwide Insights

pendently administered as a province. Maputo is ashort distance from Swaziland and South Africa, andis an important harbor that serves both countries.

Modern day Maputo has been clearly molded by itsrecent history. Following independence in 1975, large-scale emigration drained the city of its professionals,businesspeople and administrators. The colonial struc-ture of its society, the 1977-92 civil war and the eco-nomic policies that followed independence madeMaputo one of the world’s poorest cities. In the early1990s for example, it was impossible for a family tosurvive on the income of a single formal sector job andit was common that middle-income households pro-duced their own food to supplement what they couldbuy. Mozambique is still classified by the UnitedNations as a ‘least developed’ country.

Social, economic and political conditions inMozambique have resulted in high rates of urbaniza-tion. As mentioned in the introductory section,

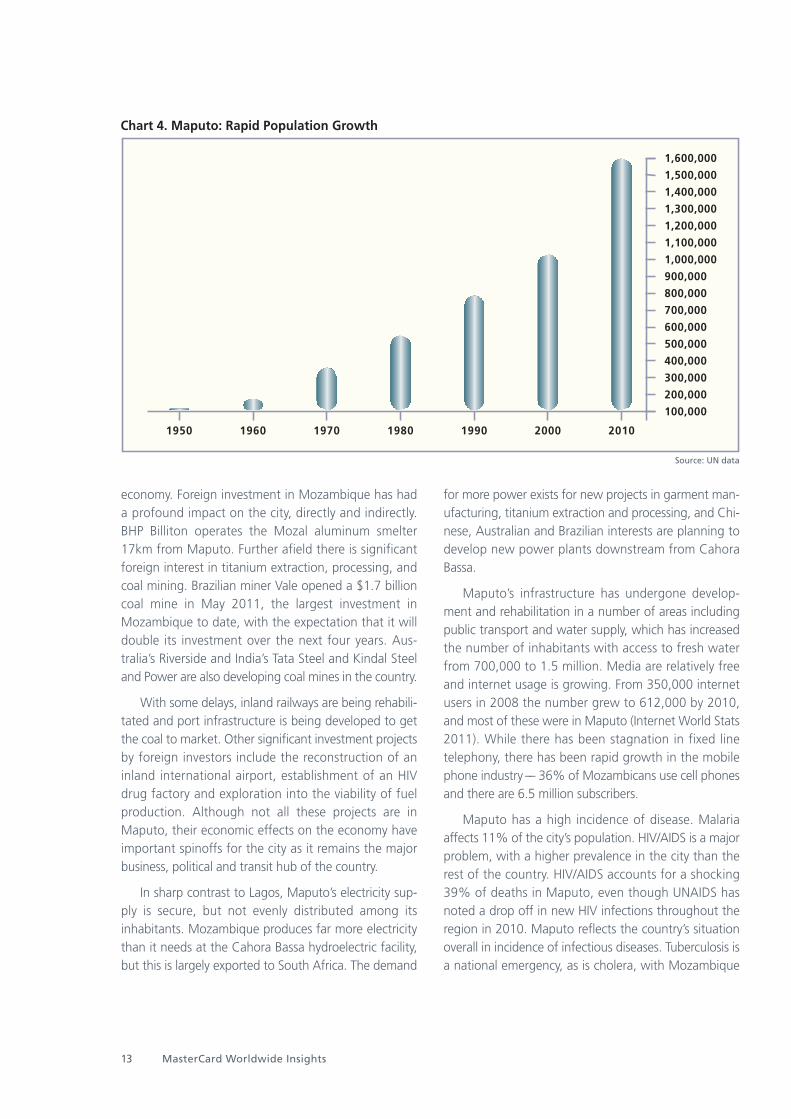

Mozambique has the highest urbanization growth rateamong the nine key Sub-Saharan African marketsreviewed –– estimated at 2.2% a year. Maputo’s popu-lation, which is currently estimated at over 1.6 millionas seen in Chart 4, continues to grow rapidly.

With market reform and liberalization, the econo-my has been improving. In 2010, Mozambique’s GDPgrew by 8.3%, the 11th highest growth rate interna-tionally, and industrial production growth was around8%, the 36th highest in the world (CIA 2011). Growthover the past decade has been over 8%, and currentgrowth projections remain higher than the 4-5% fore-cast by the World Bank for southern Africa as a whole.

For the city of Maputo, the harbor, industry pro-duction, and tourism are its economic foundations.Existing industries in the city include food, beverages,chemicals, petroleum products, textiles, cement, glass,asbestos and tobacco. But Maputo also benefits signif-icantly from activity in the rest of the Mozambican

Q3 2011 12

Chart 3. Maputo

economy. Foreign investment in Mozambique has hada profound impact on the city, directly and indirectly.BHP Billiton operates the Mozal aluminum smelter17km from Maputo. Further afield there is significantforeign interest in titanium extraction, processing, andcoal mining. Brazilian miner Vale opened a $1.7 billioncoal mine in May 2011, the largest investment inMozambique to date, with the expectation that it willdouble its investment over the next four years. Aus-tralia’s Riverside and India’s Tata Steel and Kindal Steeland Power are also developing coal mines in the country.

With some delays, inland railways are being rehabili-tated and port infrastructure is being developed to getthe coal to market. Other significant investment projectsby foreign investors include the reconstruction of aninland international airport, establishment of an HIVdrug factory and exploration into the viability of fuelproduction. Although not all these projects are inMaputo, their economic effects on the economy haveimportant spinoffs for the city as it remains the majorbusiness, political and transit hub of the country.

In sharp contrast to Lagos, Maputo’s electricity sup-ply is secure, but not evenly distributed among itsinhabitants. Mozambique produces far more electricitythan it needs at the Cahora Bassa hydroelectric facility,but this is largely exported to South Africa. The demand

for more power exists for new projects in garment man-ufacturing, titanium extraction and processing, and Chi-nese, Australian and Brazilian interests are planning todevelop new power plants downstream from CahoraBassa.

Maputo’s infrastructure has undergone develop-ment and rehabilitation in a number of areas includingpublic transport and water supply, which has increasedthe number of inhabitants with access to fresh waterfrom 700,000 to 1.5 million. Media are relatively freeand internet usage is growing. From 350,000 internetusers in 2008 the number grew to 612,000 by 2010,and most of these were in Maputo (Internet World Stats2011). While there has been stagnation in fixed linetelephony, there has been rapid growth in the mobilephone industry –– 36% of Mozambicans use cell phonesand there are 6.5 million subscribers.

Maputo has a high incidence of disease. Malariaaffects 11% of the city’s population. HIV/AIDS is a majorproblem, with a higher prevalence in the city than therest of the country. HIV/AIDS accounts for a shocking39% of deaths in Maputo, even though UNAIDS hasnoted a drop off in new HIV infections throughout theregion in 2010. Maputo reflects the country’s situationoverall in incidence of infectious diseases. Tuberculosis isa national emergency, as is cholera, with Mozambique

13 MasterCard Worldwide Insights

Chart 4. Maputo: Rapid Population Growth

1,600,000

1,500,000

1,400,000

1,300,000

1,200,000

1,100,000

1,000,000

900,000

800,000

700,000

600,000

500,000

400,000

300,000

200,000

100,000

1950 1960 1970 1980 1990 2000 2010

Source: UN data

accounting for a third of notified cholera cases in Africaover the past decade. Life expectancy is 48 years andthe death rate per 1000 is the 5th highest in the world.In Mozambique, Maputo is most at risk for the rapidspread of disease because of its population density.

Unemployment in Maputo is high at around 20%,and more than half the city’s population lives below thepoverty line. Unfortunately, extreme income inequalityexists and is growing, and patronage, corruption, orga-nized and violent crime are on the increase in Maputo.Car hijackings, rape and armed robbery occur, andmugging, bag snatching and pick-pocketing areincreasingly common.

The city is also highly susceptible to extremeweather and climactic conditions, including rising sealevels, storms and cyclones. A rise in sea level willhave a significant impact on the harbor and easternresidential areas. The government has undertaken anumber of steps to protect the city from the sea fol-lowing the devastating floods of 2000. It has builtembankments and water channels, but more exten-sive measures are required to adequately protect thecity from sustained, extreme weather events.

With its extreme poverty and increasing income dis-parity, the threat of social instability in Maputo remains

relatively high. In 2008 and 2010 soaring food, trans-port, water and electricity costs sparked riots. Maputo’s2010 riots coincided with the government’s announce-ment that it was ending it unsustainable subsidy of fuel,bread and rice, but these were reintroduced in the faceof the violence. The subsidies were phased out in mid-2011 and replaced by a more targeted system that isaimed specifically at the urban poor, and includes subsi-dies for transport and a wider range of food thanbefore.

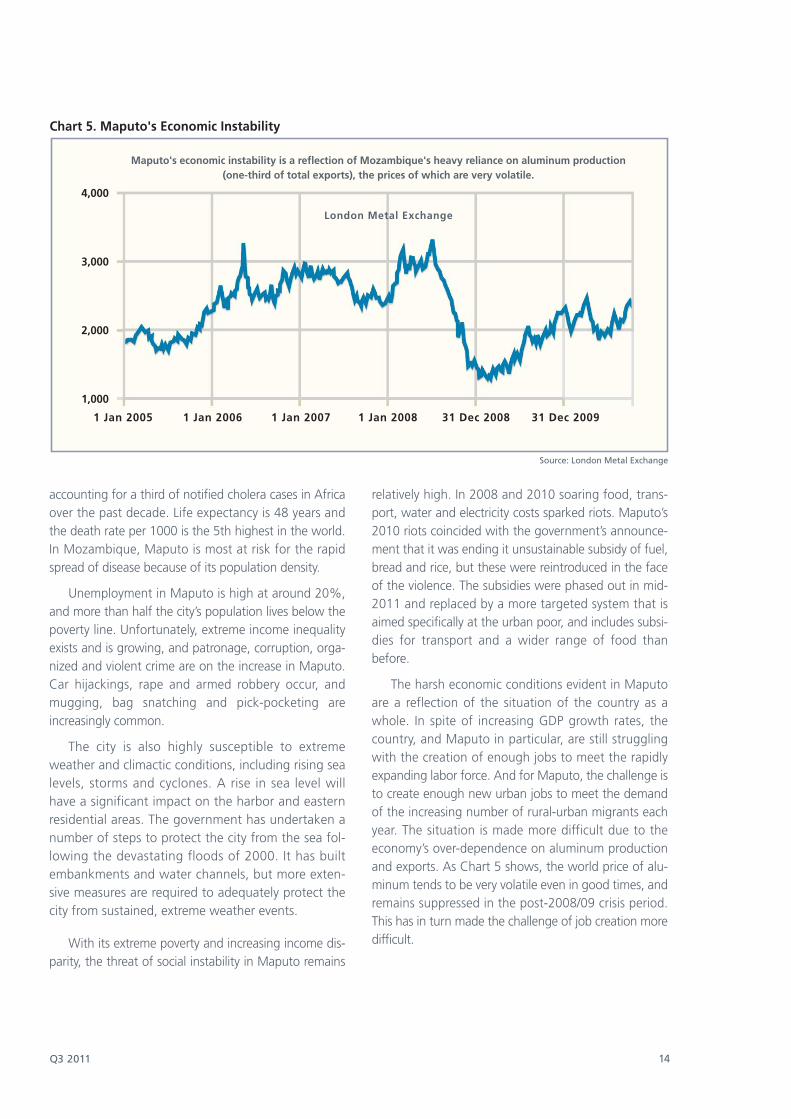

The harsh economic conditions evident in Maputoare a reflection of the situation of the country as awhole. In spite of increasing GDP growth rates, thecountry, and Maputo in particular, are still strugglingwith the creation of enough jobs to meet the rapidlyexpanding labor force. And for Maputo, the challenge isto create enough new urban jobs to meet the demandof the increasing number of rural-urban migrants eachyear. The situation is made more difficult due to theeconomy’s over-dependence on aluminum productionand exports. As Chart 5 shows, the world price of alu-minum tends to be very volatile even in good times, andremains suppressed in the post-2008/09 crisis period.This has in turn made the challenge of job creation moredifficult.

Q3 2011 14

Chart 5. Maputo's Economic Instability

Maputo's economic instability is a reflection of Mozambique's heavy reliance on aluminum production(one-third of total exports), the prices of which are very volatile.

4,000

3,000

2,000

1,000

1 Jan 2005 1 Jan 2006 1 Jan 2007 1 Jan 2008 31 Dec 2008 31 Dec 2009

London Metal Exchange

Source: London Metal Exchange

Maputo’s development has clearly been handi-capped by the massive social and economic disloca-tion as a result of the civil war and its aftermath. Thechallenge today is that it is experiencing one of thefastest urbanization rates in Sub-Saharan Africa, withits employment growth clearly lagging behind itspopulation growth (organic growth plus rural-urbanin-migration). While high urban unemployment posesthe risk of political instability, there is as yet no realevidence of the kind of innovative energy that is seenin Lagos that results from the agglomeration effectsof concentrated human interactions and exchangesin large urban areas. In spite of its fast growth,Maputo’s population, at around 1.6 million, is afterall much smaller than Lagos’ over 10 million. Recentincreases in foreign investment in the resource sectoroffers only a partial solution at best, as production inthis sector is typically very capital intensive but weakin job creation. For the time being, there appears lessreason for optimism for Maputo there is for Lagos.

Nairobi

Of the three cities, Nairobi is the youngest, not havinghad a settled population for most of the 1800s. Thearea was sparsely populated by the Kikuyu and occa-sionally traversed by the Maasai until the British choseit as a railway camp when building the Uganda Rail-road in the 1890’s. It was the midpoint between Mom-basa and Lake Victoria, and was selected because ofits highland location, temperate weather, good accessto water and productive farmland. By 1907 Nairobihad become a commercial centre, and it replacedMombasa as the capital of what was then known asBritish East Africa. The city expanded, supported bythe growth of its administrative functions and tourism,which initially began in the form of big game hunting.A significant Indian community, originally brought toKenya to work on the railways, settled in Nairobi. Theability of the indigenous population to live off the sur-rounding land was curtailed with the development offarms owned by white settlers, and a rural exodus toNairobi ensued.

15 MasterCard Worldwide Insights

Chart 6. Nairobi

Nairobi developed as a racially segregated colonialtown with specific areas allocated to Europeans, Indi-ans and Africans. The European areas enjoyed goodinfrastructure, but for the other groups infrastructurevaried from fair to non-existent. What is now the Kib-era informal settlement, for example, was allocated todemobilized African soldiers returning from the Sec-ond World War who expected, but never received,land tenure. People streaming in from the surroundingcountryside rapidly occupied the informal settlement.The legacy of this is that segregated infrastructureremains. Parts of Nairobi today are affluent with goodinfrastructure while the less affluent areas have poorinfrastructure.

By many standards Nairobi is the most importantcity in East Africa. It is the capital of the largest econo-my in the region, Kenya, and a centre of industry, edu-cation, tourism and diplomacy. It is the world head-quarters of two UN agencies and the regional head-quarters of others. It is the primary communicationand financial hub in East and Central Africa. Leadingdomestic and international banks such as Kenya Com-mercial Bank, Barclays, Standard Chartered andCitibank operate out of Nairobi. International compa-nies such as Goodyear, GE, Siemens, Coca-Cola,Citibank, Toyota and Google have regional headquar-ters and manufacturing plants in the city, and it is seenas an alternative to cities such as Johannesburg orLagos for entry into the African market. Ease of doingbusiness compares very favorably to Lagos andMaputo, ranking substantially better than the othertwo at 98th of 183 countries.

11

Manufacturing accounts for only 14% of Kenya’sGDP, but it is mostly concentrated around Nairobi.Other industries with a strong presence in the cityinclude cement production, consumer goods and foodprocessing, and small-scale manufacturing in theinformal sector. Although inadequate for the demand,Nairobi has the best human resources and communi-cations infrastructure in the region. The Nairobi StockExchange, established in 1920, has around 50 compa-nies listed, and ranks 4th in Africa in terms of marketcapitalization.

The areas around Nairobi are prime agriculturallands with food and cash crops such as maize,sorghum, cassava, beans, fruit and coffee. Horticulture

is a developing agricultural sector and flower exportsare an important source of foreign exchange. Tourism,and particularly wildlife tourism, has replaced coffee asthe primary source of foreign exchange, and it con-tributes significantly to the local and nationaleconomies with well-developed infrastructure andresources. Jomo Kenyatta International Airport is amajor point of entry into East Africa.

Nairobi has crowded markets and trading areas,with ample evidence of affluence in its middle-classsuburbs, cinemas and restaurants. It also has vast,overcrowded tenements and slums, and high unem-ployment. Most of the land in Nairobi is public land, ofwhich half is privately leased for 99-year periods. Thecity experienced a boom in top and middle level hous-ing that peaked in 2007, and in this sector substantialgentrification is evident. Housing investment has a pri-marily local base, but is supported by the Kenyan dias-pora and Somalis, Southern Sudanese, Rwandan andCongo nationals who see Nairobi as a safe investment.

Low-income housing has also grown but the finan-cial burden for this has fallen on government. There isa massive shortfall of low income and informal hous-ing upwards of 120,000 units per year, with the prob-lem exacerbated by the inflow of refugees fromKenya’s neighboring countries, particularly Somaliaand Sudan. In the early 2000s Kenya was absorbing400,000 Sudanese refugees per year, with many mov-ing to Nairobi and avoiding the refugee camps. Half ofNairobi’s population live in informal settlements, andKibera, the largest of these, has over a million inhabi-tants. Despite government attempts to involve the pri-vate sector, and a number of innovative private sectorprojects such as Bora Capital’s establishment of a low -cost property fund, the extent of public-private part-nerships in the sector has not met expectations. Inlarge part this is because of government’s delay inintroducing adequate regulation for real estate invest-ment. Roughly 80% of Nairobi’s population rent, and20% own their dwellings.

The population density of the city is 3,080 peopleper sq km, but density is unevenly spread, rangingfrom 22,000 per square kilometer in Central to 2,100per square kilometer in the Westlands suburb. Nairobiwas characterized from the beginning by a severe

Q3 2011 16

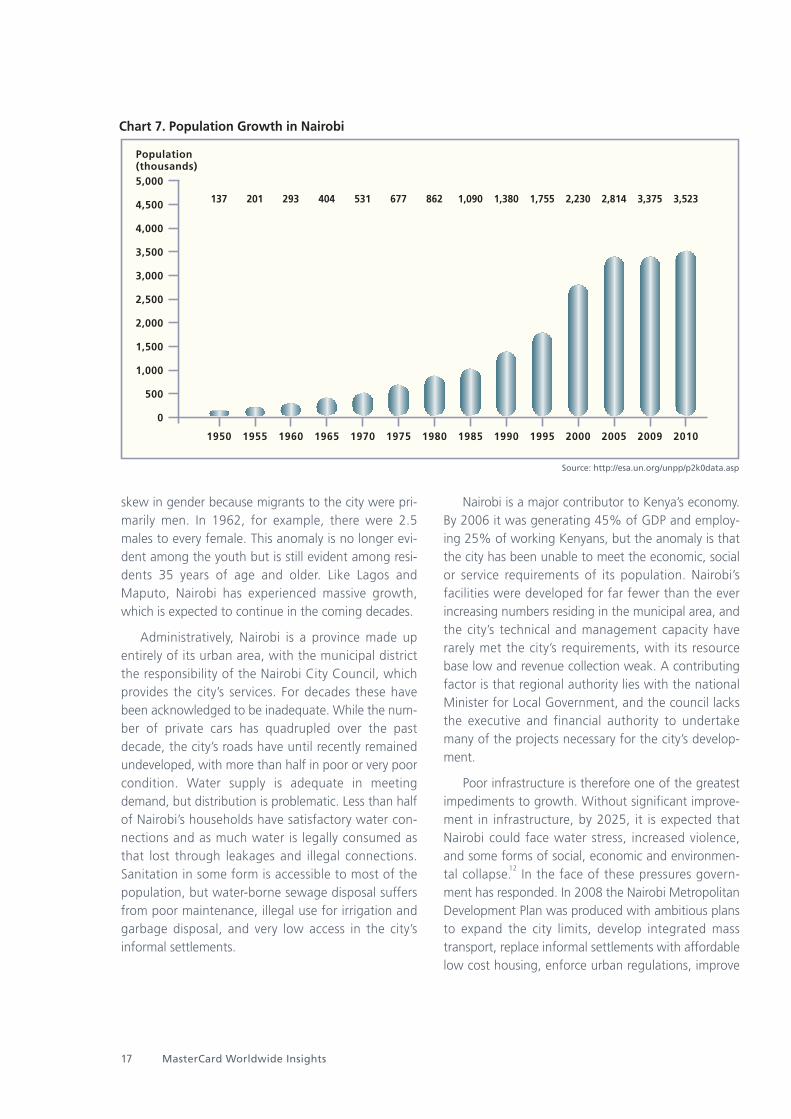

skew in gender because migrants to the city were pri-marily men. In 1962, for example, there were 2.5males to every female. This anomaly is no longer evi-dent among the youth but is still evident among resi-dents 35 years of age and older. Like Lagos andMaputo, Nairobi has experienced massive growth,which is expected to continue in the coming decades.

Administratively, Nairobi is a province made upentirely of its urban area, with the municipal districtthe responsibility of the Nairobi City Council, whichprovides the city’s services. For decades these havebeen acknowledged to be inadequate. While the num-ber of private cars has quadrupled over the pastdecade, the city’s roads have until recently remainedundeveloped, with more than half in poor or very poorcondition. Water supply is adequate in meetingdemand, but distribution is problematic. Less than halfof Nairobi’s households have satisfactory water con-nections and as much water is legally consumed asthat lost through leakages and illegal connections.Sanitation in some form is accessible to most of thepopulation, but water-borne sewage disposal suffersfrom poor maintenance, illegal use for irrigation andgarbage disposal, and very low access in the city’sinformal settlements.

Nairobi is a major contributor to Kenya’s economy.By 2006 it was generating 45% of GDP and employ-ing 25% of working Kenyans, but the anomaly is thatthe city has been unable to meet the economic, socialor service requirements of its population. Nairobi’sfacilities were developed for far fewer than the everincreasing numbers residing in the municipal area, andthe city’s technical and management capacity haverarely met the city’s requirements, with its resourcebase low and revenue collection weak. A contributingfactor is that regional authority lies with the nationalMinister for Local Government, and the council lacksthe executive and financial authority to undertakemany of the projects necessary for the city’s develop-ment.

Poor infrastructure is therefore one of the greatestimpediments to growth. Without significant improve-ment in infrastructure, by 2025, it is expected thatNairobi could face water stress, increased violence,and some forms of social, economic and environmen-tal collapse.

12In the face of these pressures govern-

ment has responded. In 2008 the Nairobi MetropolitanDevelopment Plan was produced with ambitious plansto expand the city limits, develop integrated masstransport, replace informal settlements with affordablelow cost housing, enforce urban regulations, improve

17 MasterCard Worldwide Insights

Chart 7. Population Growth in Nairobi

1950

137

1955

201

1960

293

1965

404

1970

531

1975

677

1980

862

1985

1,090

1990

1,380

1995

1,755

2000

2,230

2005

2,814

2009

3,375

2010

3,523

Population(thousands)5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Source: http://esa.un.org/unpp/p2k0data.asp

water and waste management, develop public utilities,and boost the infrastructure required to make Nairobia regional capital for finance, information and com-munications technologies, health, education, businessand tourism. A number of these plans have passed thetalk stage, have budgets allocated, and the city is visi-bly undergoing physical change. Government invest-ment has increased 20% compounded per year for anumber of years on these and similar programs, at arate that outstrips economic growth, even though thelonger-term sustainability of this program is by nomeans assured.

Today, Nairobi’s immediate future appears morepromising than its recent past. Following governmentderegulation, the middle class has grown swiftly andcontinues to grow. Upward of 17% of Nairobi’s popu-lation can be considered middle class, and they are adriving economic force in the city. Literacy in Nairobi isthe highest in Kenya at roughly 93%. Free primaryschool education has been accessible to all since 2003,even though education is inadequately funded, and itsquality relatively low.

There has also been a significant reduction in thelevel of absolute poverty in the city. The absolutepoor–– those who live below the threshold of beingable to afford minimal standards of food, clothing,health and shelter–– has decreased from 51% of thepopulation in 1997 to 44% in 2006.

13It is estimated

that the percentage has fallen further since then. Thefigure in slum areas is higher, at about 73%, but eventhese areas hold some promise as a significant numberof households in the slums operate an enterprise orhave at least one member with some education–– twoconditions that show a negative correlation with con-tinuing poverty in Nairobi. Interestingly, the groupcalled “jua kali,” Swahili for ‘hot sun,’ describes thosethat subsist as outdoor vendors and entrepreneurs inthe informal sector but are officially listed as unem-ployed. Their numbers increased from 27% in theearly 1990s to 38% in the latter 2000s–– three and ahalf times the growth rate of employed wage-earnersduring the same time period.

14

But the city still faces enormous challenges. It is anintegral part of Kenya’s low-income economy withannual per capita income averaging about $360, rank-

ing 148th of the 177 countries in the UNDP's HumanDevelopment Index and 106th of the 139 countries inthe WEF’s 2010 Global Competitiveness Index.Although ameliorated by the growth of the middleclass, Nairobi is one of the world’s most economicallyunequal cities. The gap between the urban affluentand the rural poor is smaller than that between theurban affluent and the urban poor. If the current trendcontinues, in a decade Kenya’s starkest poverty will befound in cities like Nairobi, and not in the remote ruralareas.

The greatest differences in health status are also tobe found between urban affluent and urban poor andno longer between urban affluent and the rural poor.Philippa Crosland Taylor of Oxfam GB observes that,“An increasingly disenfranchised and poverty-strickenurban underclass is set to be the country’s defining cri-sis over the next decade. [Nairobi] is a city of a smallminority of ‘haves’ and millions of ‘have nothings’...Nairobi is one of the biggest and most prestigiouscities in East Africa, yet it is crumbling before oureyes.”

15 Among this ‘urban underclass’ there is resent-

ment over patronage, inequality, poor economicprospects and harsh living conditions. From its earliestdays Nairobi has been at the centre of Kenyan politics.During the Mau Mau insurrection in the 1950s the citywas practically in a state of siege. More recently,events like the 1988 American embassy bombing andthe riots of the 2007 presidential elections emphasizethe symbolic importance of the city and its centralposition in Kenyan society and politics.

With a population size midway between Lagos andMaputo, Nairobi is distinctive in its better and improv-ing infrastructure, and, more importantly, an apparent-ly more responsive and capable administrative struc-ture, with more effective project implementation. Theeconomic, social and environmental challenges facingNairobi are certainly no less intense than those facingLagos and Maputo, but its record of policy response sofar seems to be more successful.

Q3 2011 18

Conclusion

Lagos, Maputo and Nairobi vividly illustrate the realityof many Sub-Saharan cities. While most of Africa’scities are defined by their large and rapidly growingpopulations, resource limitations and inability to meetthe health, security, education, governance and skillsrequirements of all their inhabitants, this tale of threecities shows that important differences also existbetween them. Africa’s cities are in fact very differentsocieties, and in many ways better societies, than theywere a decade ago. How they perform in the comingyears and decades will influence the future of the con-tinent in many important ways. At present, Africa isbenefiting from the resource-driven expansion of itseconomies and this is having a significant impact on itsurban and rural communities. How to leverage thisresource-based boom to benefit other sectors of theeconomy as well as the general population, includingits urban development, will be the defining challengeof the region.

As this tale of three cities shows, there is unlikely tobe a magic pill that can solve all the development diffi-culties of the region’s cities, even though there is agreat deal in common in terms of the challenges thatthey face. More specifically, there is not going to besome kind of a “China model” that Sub-SaharanAfrica can copy to repeat China’s urbanization experi-ence. Successful solutions to the region’s urbanizationchallenges will have to be crafted locally, one at atime, taking full account of local conditions thatinclude location-specific constraints and capabilities.The origins of Africa’s prosperity may well reside in itsmines and oil wells, but its extent and sustainabilitywill largely depend on the resourcefulness of its peopleand the dynamism of the enterprise that exists in itscities.

19 MasterCard Worldwide Insights

1. See http://www.thelocal.de/national/2010022625525.html

2. Data published by the National Statistics Bureau, vari-ous years.

3. There is also a darker side to China’s rapid urbaniza-tion, which are the social costs incurred. For example,forced land acquisition by local governments with inade-quate compensation to rural people has been a chronicsource of social unrest in recent years.

4. Kotkin, J. 2010. The world’s fastest-growing cities.http://www.forbes.com/2010/10/07/cities-china-chicago-opinions-columnists-joel-kotkin.html Accessed 31 May2011.

5. Watkins, S. 2010. Mail Online, ‘TAKING STOCK: Brightfuture for Africa's dark continent.’http://www.dailymail.co.uk/money/article-1315218/TAK-ING-STOCK-Bright-future-dark-continent-Africa.htmlAccessed 31 May 2011.

6. EIU 2011. Global liveability report. Economist Intelli-gence Unit.http://www.eiu.com/site_info.asp?info_name=The_Glob-al_Liveability_Report Accessed 31 May 2011.

7. World Bank 2011a. Doing Business 2011: Nigeria.http://www.doingbusiness.org/data/exploreeconomies/nigeria Accessed 31 May 2011.

8. World Bank 2010a. Doing Business 2010.http://www.doingbusiness.org/data/exploreeconomies/nigeria/sub/lagos/ Accessed 31 May 2011.

9. Meek J. 2009. The Guardian, 'Everyone's sleeping withone eye open.' http://www.guardian.co.uk/lifeand-style/2009/may/09/lagos-city-life Accessed 31 May 2011.

10. Aether 2007. Rem Koolhaas - Building the UnmaterialWorld. http://aether.com/archives/rem_koolhaas.htmlAccessed 31 May 2011.

11. World Bank 2011c. Doing Business 2011: Kenya.http://www.doingbusiness.org/data/exploreeconomies/kenya Accessed 31 May 2011.

12. City of Nairobi 2007. City of Nairobi EnvironmentalOutlook. http://www.unep.org/geo/pdfs/NCEO_Report_FF_New_Text.pdf Accessed 31 May 2011.

13. CBS 2009. Geographic dimensions of well-being inKenya. http://www.scribd.com/doc/2224390/geographic-Dimensions-of-WellBeing-in-Kenya Accessed 31 May2011. Gulyani S. 2006. Inside informality: Poverty, jobs,housing and services in Nairobi’s slums. http://sitere-sources.worldbank.org/INTKENYA/Resources/Inside_Infor-mality.pdf Accessed 31 May 2011.

14. City of Nairobi 2007. City of Nairobi EnvironmentalOutlook.http://www.unep.org/geo/pdfs/NCEO_Report_FF_New_Text.pdf Accessed 31 May 2011.

15. Oxfam 2009. Kenya threatened by new urban disas-ter. http://www.oxfam.org/fr/pressroom/pressre-lease/2009-09-10/kenya-threatened-new-urban-disasterAccessed 31 May 2011.

About the Authors

Yuwa Hedrick-Wong, Ph.D.

Yuwa Hedrick-Wong is currently HSBC Visiting Pro-fessor of International Business at the University ofBritish Columbia, Canada. Yuwa is an economist andbusiness strategist with 25 years of experience gainedin over thirty countries. He is a Canadian who grewup in Vancouver, British Columbia, and spent the last20 years working in Europe, Africa, the Indian sub-continent, and Asia /Pacific. He has served as strategyadvisor to over thirty leading multinational companiesin the Asia /Pacific region.

In 2010, Yuwa was appointed as Global EconomicAdvisor to MasterCard Worldwide. Prior to this role,he was Economic Advisor to MasterCard in Asia /Pacific, a position he held since 2001. As economicadvisor, he chairs a MasterCard Knowledge Panel ofleading economists, policy analysts, academics andbusiness strategists for regular exchange and knowl-edge sharing. His other appointments are: Advisor atSouthern Capital Group, a private equity fund (since2007); member of the Investment Council of ICICI,India’s largest private bank (since 2008); Global Econ-omist at The Insight Bureau (since 2009); and mem-ber of the Board of Advisors, Center for Macro Con-sumer Research, India (since 2010).

Yuwa is a frequent commentator in the broadcastand print media on current economic, policy andbusiness issues, and is a published author in con-sumer market dynamics, economic development,trade, and international relations. He was voted“Communicator of the Year” in Asia in 2006 by theAsia/Pacific Association of Public Relations Profession-als. He wrote a regular column in Forbes Asia called“Asian Angles” in 2005 and 2006. He was adjunctprofessor at the School of Management, Fudan Uni-versity, Shanghai, China; from 2005 to 2008; andguest lecturer at the Graduate School of Business,University of Chicago.

Professor George Angelopulo

Professor George Angelopulo’s area of interest is therelationship between corporate integration, commu-nication and sustainable competitive advantage. Hehas published in peer-reviewed journals; producedstandard academic works that are used throughoutsouthern Africa; edited and authored a number ofbooks; and produced academic papers for confer-ences in Africa, Europe, America and Australia,always retaining a focus on the corporate world.George has worked with organizations that includelisted and unlisted companies, multinationals, NGOs,most of South Africa’s government departments anda number of parastatals. He holds a particular interestin research methodology and has developed diagnos-tics for stakeholder perception analysis in marketingand communication that include the iBrand Barome-ter

®and the Communication Prioritisation Index

®.

George has undertaken research in Finland, Germany,Great Britain, Italy, Namibia, the Netherlands, Nor-way, Peru, South Africa, the USA and Zimbabwe. Heis a member of the MasterCard Africa KnowledgePanel, holds a DLitt et Phil (UJ) and holds academicpositions at the Department of Communication Sci-ence at the University of South Africa (Unisa), andCENTRUM Catolica, the business school of the Pontif-icia Catolica del Peru. Prior to his academic careerGeorge worked in media and advertising in Africa.

Q3 2011 20

21 MasterCard Worldwide Insights

MasterCard Worldwide InsightsOngoing research and analysis on global economic dynamics, business conditions and public policy challenges

For additional copies of Insights or for additional infor-mation contact Ms. Georgette Tan, MasterCard Worldwideat [email protected] or you can visitwww.masterintelligence.com

2004Second Quarter 2004Focus on Korea–– An Examination of Korea’s Consumer Debt BubbleFocus on Hong Kong–– Hong Kong’s Rapid Rise in Personal BankruptcyBenefiting from the Synergy Between Travel and RetailTowards a World-Class Payment Card System in ChinaEstimating the Social Cost of Cash–– Thailand and Malaysia

Third Quarter 2004How the Consumer Debt Bubble in Korea Could Have Been AvoidedHow Comprehensive Positive Credit Reporting Could Enhance Capital Productivity in AustraliaThe Cost of Cash in Japan

Fourth Quarter 2004Credit Card Outstanding and Household Debt–– Myth and Reality

2005First Quarter 2005A Challenging and Promising Future: Potential Impact of Low Cost Carriers in Asia/PacificShocks, Resilience and Consumer Confidence in Asia/Pacific–– 2003-2005Women Travelers of Asia/Pacific–– A New PowerhouseThailand’s Consumer Market–– The Next 10 Years of Rising Prosperity and Sophistication

Second Quarter 2005The Future of Malaysia’s Consumer Market–– Dynamic Transformation and Rising AffluenceTaiwan’s Future Consumer Market–– Achieving Maturity Women Consumer Market in Australia–– Uniquely AustralianCan Asia/Pacific Stand Alone Economically and What Could Happen in the Next US Economic Downturn?Third Quarter 2005Chip Migration in Asia/Pacific–– The Payments Industry’s New Frontier

Women Consumer Market in Japan–– The Super-Aging SocietyKuala Lumpur as a Travel-Shopping DestinationWomen Consumers of Korea–– Demographic Trends and Women’s Changing RolesThe Corporate Superpower of the 21st Century: Synergy Between Chinese and Indian BusinessFourth Quarter 2005Women Consumers of China–– The Powerhouse Wit hin a PowerhouseRewards and Risks of Living in an Inter-Connected WorldThe Future of Tourism in Asia/Pacific

2006First Quarter 2006The Changing Asian Banking Landscape: Challenges and OpportunitiesBenefiting from Globalization:Lessons Learned From China2006 Interest Rate Outlook in Asia and Potential Impact on Consumer Spending

Second Quarter 2006China’s Emerging Consumer Market–– A Geographical Perspective10 Dynamic Trends Shaping the Future Consumer Markets of AsiaThe Interest Rate Outlook and Implications for Consumer Banking in Thailand, Indonesia and MalaysiaChina and the New Global EconomyChina’s Currency in the Global Currency Market–– Challenges of Asymmetry

Third Quarter 2006Visions of the Future–– Perspectives of the Young Elite of IndonesiaVietnam’s Economic Future and Banking Sector ImplicationsThe Heart of Commerce: Driving Global Business

Fourth Quarter 2006Global Economic Resilience: Five Years After 9/11Visions of the Future–– Perspectives of the Young Elite of ThailandAsian Economic Integration: Prospects and Business Implications 2007First Quarter 2007The Sun Also Rises: Japan’s Long Term Growth Prospects and Regional ImplicationsMyths and Reality of Household Debt in KoreaInterchange Regulation: Lessons Learned From RBA Intervention in AustraliaReal Costs of Foreign Currency Transactions

Second Quarter 2007Understanding the Affluent Consumers of ChinaHousehold Debt in Taiwan: An Analysis of the Consumer Debt CrisisSmall-Medium Sized Enterprises in SingaporeWomen Entrepreneurship in SingaporeAn Analysis of Household Debt in Singapore–– Past and FutureWorldwide Centers of Commerce IndexTM

The Dynamics of Global Cities and Global CommerceAsia/Pacific 10 Years After the '97 Crisis

Third Quarter 2007MasterCard Worldwide Index of China’s Affluents–– Discretionary Spending and LifestylesThe Demand for Luxuries in Asia/Pacific

Fourth Quarter 2007China and Sustainable Economic Growth–– Outlook for the Next 15 YearsDynamic Drivers of China’s Consumer Market–– the Middle Class, Modern Women and DINKsThe Future of Consumer Credit in Indonesia

2008First Quarter 2008Brand Preference of the China AffluentUrbanization and Environmental Challenges in Asia/Pacific, Middle East and Africa–– Ranking of Worldwide Centers of CommerceChina’s Dynamic Consumers–– the Young Singles

Second Quarter 2008Trade and Economic Growth in Asia: The Paradox of Globalization and DecouplingShocks and Resilience–– Hong Kong’s Dynamic Household Credit MarketWorldwide Centers of Commerce IndexTM

Third Quarter 2008Online Shopping in Asia/Pacific–– Patterns, Trends and Future GrowthThe CDI-MasterCard Worldwide Index of Emerging Urban China–– The Pearl River Delta Region

Fourth Quarter 2008MasterCard Worldwide Worldwide Centers of CommerceIndex:TM Emerging Markets IndexGlobal Economic Crisis andConsumer Confidence in Asia/PacificSaving and Expenditure in Asia/Pacific: Consumers’ Priorities

2009First Quarter 2009Global Crisis and Consumer Confidence, Savings, and Spending Priorities in Middle East and AfricaPost-Crisis China: Saving and Consumption DynamicsCredit Cards as the Optimal Way to Pay: A Cost/BenefitAnalysis from the Consumer Perspective

Second Quarter 2009India’s Past and Future Economic GrowthEconomic Crisis and Preference for Online Shopping in Asia/Pacific, Middle-East, and AfricaConsumer Confidence and Recovery Prospects inAsia/Pacific, Middle-East, and Africa

Third Quarter 2009Networked Cities in Asia/Pacific, Middle East and AfricaGovernment Stimulus and Consumer Response in China–Implications for Future Growth by Yuwa Hedrick-WongGlobal Recession and the Middle East– Perspective fromthe Europe Linkage by Yuwa Hedrick-WongFourth Quarter 2009Changing Perceptions of Foreign and Domestic FinancialInstitutions in China

2010First Quarter 2010Africa 10/21: The Ten Markets in Sub-Saharan Africa ThatWill Lead the Transformation of the Continent in the 21stCentury; Part AConsumption Trends in the US and China: Prospects ofRebalancing the Global Economy by Yuwa Hedrick-Wong

Second Quarter 2010Growth Prospects of Australia and New Zealand in thePost-Recovery Global Economy by Yuwa Hedrick-WongThe New “Animal Spirits” in India’s Economy and How it will Change India’s Growth Trajectory by Yuwa Hedrick-WongConsumer Spending Outlook in Asia/PacificAfrica 10/21: The Ten Markets in Sub-Sahara Africa and Their Engagement with China and India in the 21st Century; Part B

Fourth Quarter 2010Asia/Pacific, Middle East and Africa Online ShoppingStudy 2010

2011First Quarter 2011How Well Do Women Know Their Money: Financial LiteracyAcross Asia/Pacific, Middle East and AfricaChina’s Economic Rebalancing and Global Implications by Yuwa Hedrick-Wong

Second Quarter 2011Taking Stock: The State of Sub-Saharan Africa by Dr. AzarJammine and Dr. Martyn Davies

Q3 2011 22

©2011 MasterCard

www.mastercardworldwide.com