Embed Size (px)

Citation preview

THE CENTRAL BANK & THE ECONOMY

Monetary Transmission Mechanism

Interbank Interest Rate

Money Market Rates

Forex

Rate

s

Economy

Stock P

ricesLT

Inter

est R

ates

Inventories

Trade Balance

Investment

Consumption

Policy Feedback• How does the central bank gauge whether the current

monetary policy is effective in guiding the economy toward its goals?

• If it is not, how do they choose the level of the operating target in order to guide the economy toward its goals?

Policymakers Modelof the Economy

Real Interest Rates and Demand• Components of aggregate demand are sensitive to the

real interest rate in a negative way. • Consumer Durables• Residential Housing• Corporate Investment

• High interest rates means an exchange rate appreciation which hurts the trade balance.

Expenditure Curve

r

Y

AE

• Expenditure is negatively related to the real interest rate.

Shifts in Aggregate Expenditure

r

Y

AE

AE’

AE’’

•But other factors like consumer or

business confidence, fiscal policy, or foreign

demand factors will shift spending at any

given interest rate.

Monetary PolicyThe central bank stabilizes inflation using the interest rate target.

• If inflation is above target, πTGT, central bank will raise interest rate• If inflation is below target, πTGT, central bank will cut interest rate

Under Taylor Principle, inflation above target is associated with rising real rates.

Monetary Policy Reaction Curve

* TGTt tr r b

r* - Neutral real interest target b – inflation sensitivity

Monetary Policy Reaction Curve

r

π

r*

πTGT

MPR

• Real interest rate is an increasing function of the interest rate

Aggregate Demand Curve

Y

π

AD

• The reaction of monetary policy to inflation exacerbates the effect of inflation on AD.

Increasing π→Increasing r → Decreasing AD

• The more sharply that monetary policy responds to inflation, the more sharply demand responds to inflation.

Relationship between inflation and aggregate

demand depends on how sensitive MPC is to inflation

r

π

π

Insensitive

SensitiveInsensitive

Sensitive

MPR

AD

AD

MPR

Y

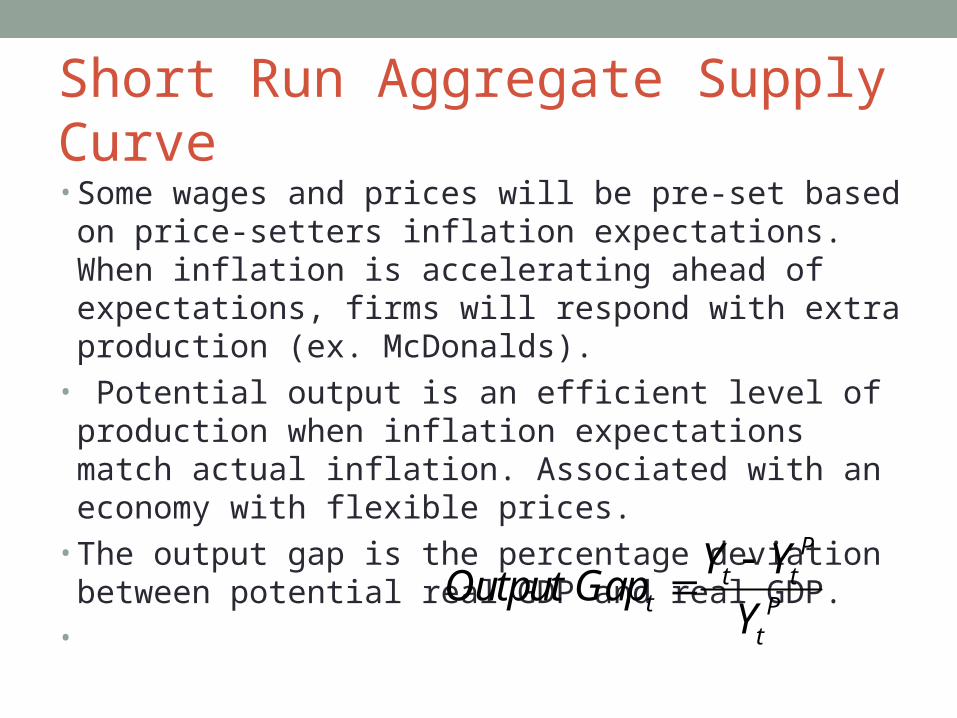

Short Run Aggregate Supply Curve• Some wages and prices will be pre-set based on price-

setters inflation expectations. When inflation is accelerating ahead of expectations, firms will respond with extra production (ex. McDonalds).

• Potential output is an efficient level of production when inflation expectations match actual inflation. Associated with an economy with flexible prices.

• The output gap is the percentage deviation between potential real GDP and real GDP.

• P

t tt P

t

Y YOutput Gap

Y

π

YYP

Aggregate Supply Short-run & Long Run

SRAS

πE

Rise in Household-Business Confidence\Stock-Real Estate Market Booms\

Expansionary Fiscal policy The AD Curve

Shifts Out

Y

π

AD

AD'• Various events may shift demand out for goods at any given interest rate• Household

consumption may increase because of optimism or wealth effect

• Corporate investment may increase because of optimism

• Government Deficit Spending

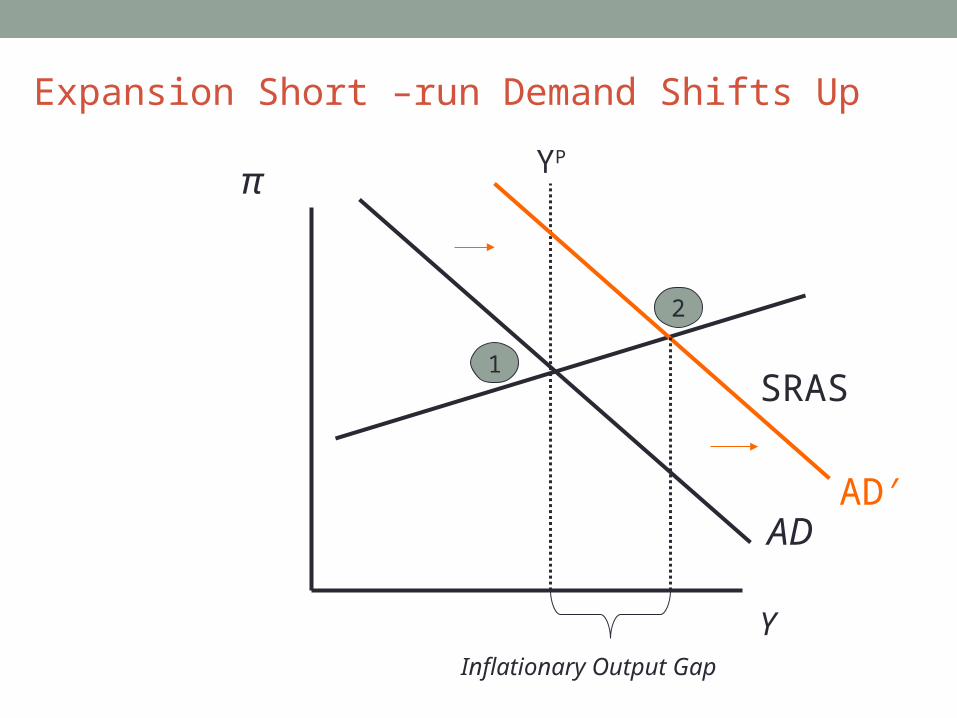

Expansion Short –run Demand Shifts Up

Y

π

AD

YP

SRAS1

AD′

2

Inflationary Output Gap

Recession Short –run Demand Shifts Down

Y

π

AD

YP

SRAS1

AD′

2

Recessionary Output Gap

Adaptive Expectations• Adaptive Expectations: Inflation expectations adjust to

actual inflation

• Et-E

t-1= [t-Et-1]

• The SRAS adjusts to self-correct the output gap.• Eventually, inflation expectations catch up with inflation.

Inflation Expectations Shift Upward

Y

π

AD

YP

SRAS1

AD′

2

Inflationary Output Gap

3

π

Y

YP

SRAS

AD Insensitive

AD Sensitive

1

2a2b

• The more sensitive is monetary policy, the flatter is the AD curve.

• The flatter the AD curve, the less that inflation will need to decline to return the economy to potential output.

Inflation Targeting:Inflation Sensitive Interest Rate Rule

• Under inflation targeting, central bank is sensitive to the inflation rate in setting the interest rate, raising interest rates in response to increasing inflation, cutting interest rates

• A benefit of this approach is not only stable inflation and inflation expectations, but also more stability of output and shorter duration business cycles in the face of demand shocks.

21

Short-term Stabilization

• When output gap is negative, inflation tends to be decelerating. Stabilizing inflation can also stabilize the business cycle

Japan

-3

-2

-1

0

1

2

3

-8 -6 -4 -2 0 2 4 6

Output Gap

Infla

tion

Acc

eler

atio

n

Inflation Acceleration =

Today LastYearInflation Inflation

Supply Shocks• Inflation itself may be subject to cost-push shocks such as

energy prices etc.• A monetary policy committee which strives to maintain a

fixed inflation target with a very sensitive MPR will face a relatively large decline in output to maintain the target.

• Central bank often adjusts the inflation target to supply side conditions

Supply Shock

Stagflation

Y

π

AD

YP

SRAS

12

SRAS′

π

Y

YP SRAS

AD Insensitive

AD Sensitive

A

B

SRAS

An MPR for HK

,

1 , 1E HK HK Et t t t HK t

HK US USA HKt t t t

r i

r r

• Remember in HK, the nominal interest rate is equal to the US$ interest rate.

• Again, assume that inflation expectations respond to actual inflation

• In HK, as inflation rises, real interest rate falls!

Negative Relationship between inflation and real

interest rate with fixed exchange rates

r

π

MPRHK

Under fixed exchange rate, domestic interest rate & demand may be insensitive to domestic inflation

r

π

π

Fixed S

SensitiveFixed S

Sensitive

MPR

AD

AD

MPR

Y