Embed Size (px)

Citation preview

Economy and Economy and Interest RatesInterest Rates

1

31st Meeting of CEO’s of HFCs

Presentation by Mr. Keki Mistry

Vice Chairman & CEO – HDFC

February 18, 2011

GDP registering consistent growth GDP registering consistent growth

• Quarter Ended Sep 10- GDP growth at an impressive 8.90% (highest in any quarter in the last 3 years)-driven mainly by farm and services sector

• Manufacturing growth slowed down - expected to slow down further • GDP expected to grow at about 8.6% during the FY 2010-11

Quarter GDP Growth (%)

Jul-Sep ‘08 7.70

Oct-Dec‘08 5.80

Jan-Mar ‘09 5.80

Apr-Jun ‘09 6.10

Jul-Sep‘09 7.90

Sep-Dec ‘09 6.00

Jan-Mar ‘10 8.60

Apr-Jun’10 8.80

Jul-Sep’10 8.90

2

RBI Monetary Policy Review – January 25, 2011RBI Monetary Policy Review – January 25, 2011

• Liquidity and Inflation are RBI’s primary concerns

• Key actions in Monetary Policy on Jan 25, 2011 Reverse Repo & Repo increased by 25 bps to 5.50% & 6.50% CRR retained at 6.00% Temporary reduction of SLR from 24% to 23% of NDTL extended till April 8, 2011

• March 2011 Inflation target revised from 5.5% to 7%

• Stance of the policy Contain the spill-over of rise in food and fuel prices to general inflation Rein in inflationary expectations Moderate enough so as to not disrupt growth Provide comfort on liquidity management

• Credit growth at 24% against projection of 20% - growth is broad based across sectors and not just infrastructure. Housing including PSL growth was at 13.2%

• Current Account Deficit at 3.7% of GDP a cause of concern

3

Tight Liquidity conditions Tight Liquidity conditions persistpersist

• Liquidity shortfall of around Rs 60000-90,000 cr in the system; peak shortage of Rs 1,70,485 cr on Dec 22, 2010.

• Liquidity expected to tighten further in March 11-High level of bank CDs maturing in March 11 4

Source: Reuters

Projection of system Projection of system liquidityliquidity

5Projected average shortfall till March 2011 : approx Rs 62,000 cr Projected govt spending from now till March 2011 : approx Rs 108,000 cr Source: J P Morgan Chase Bank

1 2 3 4 5 6 7Week ending

Change in currency in circulation

Net Gov Borrowings (Net of redemptions and

coupon payments)

Net discretionary govt spending (includes tax)

Issuance of sterilization securities/

OMO

Othes incl Tax

Payments/3G/IPO

System Liquidity (+ = surplus)

1-Oct-10 7 (12) 17 13 - -27

8-Oct-10 (13) (14) 15 - (11) -50

15-Oct-10 (12) (16) 12 - - -66

22-Oct-10 2 (5) 4 - - -66

29-Oct-10 3 (21) 11 2 - -72

5-Nov-10 (24) 6 33 - (15) -73

12-Nov-10 (11) (11) 3 3 (13) -101

19-Nov-10 (0) (5) 2 - - -104

26-Nov-10 8 (7) 8 4 (8) -99

3-Dec-10 (2) 1 24 - - -76

10-Dec-10 (9) (11) 2 - (21) -115

17-Dec-10 (1) (3) 7 20 (56) -148

24-Dec-10 3 (2) 1 8 - -139

31-Dec-10 4 (6) 17 12 - -112

7-Jan-11 (9) 17 28 12 (14) -79

14-Jan-11 (10) (9) 10 8 - -81

21-Jan-11 (0) (13) 11 (9) - -93

28-Jan-11 2 (11) 9 - - -92

4-Feb-11 (5) 9 31 - - -57

11-Feb-11 (3) (9) 1 - (16) -85

18-Feb-11 (1) (9) 7 - - -88

25-Feb-11 0 18 2 - - -67

4-Mar-11 (7) 4 30 - - -39

11-Mar-11 (8) 4 5 - (12) -50

18-Mar-11 (2) (7) 5 - (49) -103

25-Mar-11 1 (1) 18 - - -85

1-Apr-11 3 (7) 40 - - -49* Grey indicates projected liquidity

+ indicates money market liquidity will improve -- all amounts in INR 000 crores

Systemic Liquidity Shortage Systemic Liquidity Shortage

6

Source: RBI

• High cash surplus lying with govt after 3G/BWA outflows-Currently at Rs.114290 crores

• Increase in currency in circulation - 3.4% higher than PY

• Higher government spending in rural areas – (NREGA USD 9bn)

• High Credit Deposit Ratios causing a drain on banking system liquidity

• Currency with public at INR 888,120 crs (as on 28/01/2011) against Rs 768,033 crs (as on 31/03/2010)

Deposit Growth trailing Credit Deposit Growth trailing Credit Demand Demand

7

• Has added to liquidity pressures• RBI in its recent credit policy, reiterated that rapid credit growth without

commensurate increase in deposits not sustainable • Approx 4 % credit growth is on account of credit offtake for 3G/BWA auctions

Source: RBI

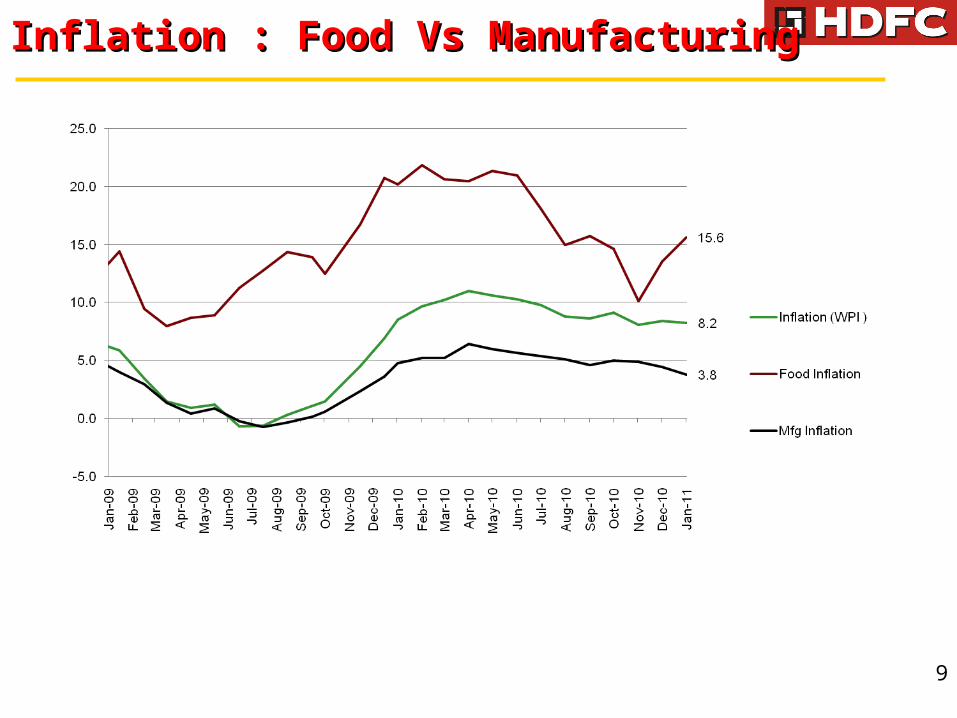

Inflation remains worrisomeInflation remains worrisome

• WPI eased to 8.23% in January 2011 (8.43% in December 2010)• Food Inflation eased to a 7-week low of 13.07% for the week ended 29th Jan 2011

(17.05% in the previous week) • RBI’s inflation projection increased to 7% (from 5.5%) by March 2011

Source: Bloomberg8

Inflation : Food Vs ManufacturingInflation : Food Vs Manufacturing

9

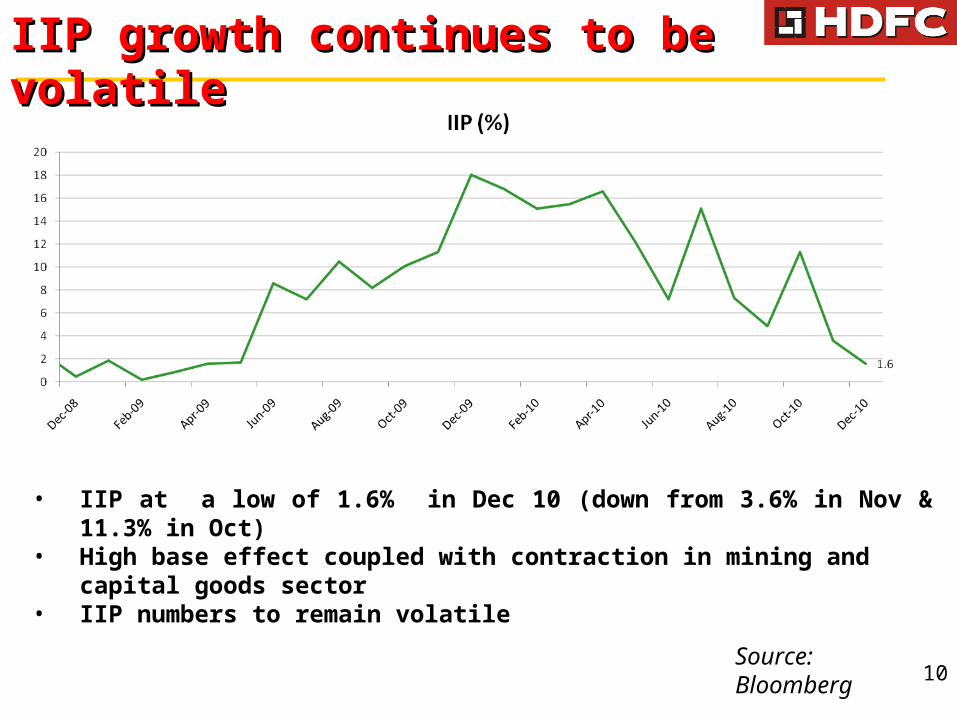

IIP growth continues to be IIP growth continues to be volatilevolatile

10

• IIP at a low of 1.6% in Dec 10 (down from 3.6% in Nov & 11.3% in Oct)

• High base effect coupled with contraction in mining and capital goods sector

• IIP numbers to remain volatile

Source: Bloomberg

Rupee in the range of 45-48Rupee in the range of 45-48

11

Factors supporting a strong Rupee• Robust domestic growth• Favourable Interest Rate differentials• Easy global liquidity augurs well for FII inflows

Risks• Widening Current Account Deficit 3.7% of GDP in H1 of FY 11 (as

against 2.2% in PY H1)• Higher Oil Prices• FDI flows slowing down , FII flows volatile and vulnerable to external

factors • Global Event risk – euro-zone sovereign crisis

In the short term, INR is highly correlated to movements in the equity market indices

FII & FDI flows in IndiaFII & FDI flows in India

12Source – SEBI website/Min of Com website

• Total FDI /FII flows of USD 58 bn in 2010 –all time high •Net accretion in Fx Reserves Jan 10 till date : USD 13.81 bn

Interest Rate Outlook Interest Rate Outlook

• Rate hikes of 150 bps in repo and 200 bps in reverse repo by RBI in FY 11 till date - another hike possible in March 2011

• Tight liquidity conditions - Call rates average 6.62% since Jan 2011

• Most banks have hiked their Base Rates thrice since July 2010. Overall increase by 125 bps - 150ps. Most Base Rates in the range of 9%-9.5%

• Similar increases in the PLRs of banks

• Short end rates continue to increase, yield curve has inverted

• Higher inflation can lead to future rate hikes Domestic and Global food prices Global commodity prices Demand side pressures – wage inflation

13

14

CHANGES IN BASE RATE TILL DATEBase Rate as on Base Rate as on Change Since

1-Jul-10 14-Feb-11 1-Jul-10

Allahabad Bank 8.00% 9.50% 1.50%Andhra Bank 8.25% 9.50% 1.25%Bank of Baroda 8.00% 9.50% 1.50%Bank of India 8.00% 9.50% 1.50%Bank of Maharashtra 8.25% 9.50% 1.25%Canara Bank 8.00% 9.50% 1.50%Central Bank of India 8.00% 9.50% 1.50%Corporation Bank 7.75% 9.40% 1.65%Dena Bank 8.25% 9.45% 1.20%Indian Bank 8.00% 9.50% 1.50%Indian Overseas Bank 8.25% 9.50% 1.25%IndusInd Bank Ltd. 7.00% 8.25% 1.25%Oriental Bank of Commerce 8.00% 9.50% 1.50%Punjab & Sind Bank 8.20% 9.50% 1.30%Punjab National Bank 8.00% 9.50% 1.50%South Indian Bank Ltd 8.10% 8.80% 0.70%State Bank of Bikaner & Jaipur 7.75% 8.50% 0.75%State Bank of Hyderabad 7.75% 8.50% 0.75%State Bank of Travancore 7.75% 8.50% 0.75%Syndicate Bank 8.25% 9.50% 1.25%The Federal Bank Ltd. 7.75% 8.50% 0.75%UCO Bank 8.00% 9.50% 1.50%Union Bank of India 8.00% 9.50% 1.50%United Bank of India 8.25% 9.45% 1.20%Vijaya Bank 8.25% 9.50% 1.25%Yes Bank Ltd 7.00% 8.00% 1.00%

1.25%

Axis Bank Ltd. 7.50% 8.25% 0.75%HDFC Bank Limited 7.25% 7.75% 0.50%ICICI Bank Ltd. 7.50% 8.25% 0.75%State Bank of India 7.50% 8.25% 0.75%

Name of the Bank

15

CHANGES IN BPLR TILL DATEBPLR as on BPLR as on Change Since

1-Apr-10 14-Feb-11 1-Apr-10

Allahabad Bank 12.00% 13.50% 1.50%

Andhra Bank 12.00% 13.75% 1.75%Bank of Baroda 12.00% 13.75% 1.75%Bank of India 12.00% 13.75% 1.75%Bank of Maharashtra 12.25% 13.50% 1.25%Canara Bank 12.00% 13.75% 1.75%Central Bank of India 12.00% 13.75% 1.75%Corporation Bank 12.00% 13.60% 1.60%Dena Bank 12.50% 14.50% 2.00%Indian Bank 12.00% 13.50% 1.50%Indian Overseas Bank 12.25% 13.75% 1.50%IndusInd Bank Ltd. 17.00% 18.25% 1.25%Oriental Bank of Commerce 12.00% 13.75% 1.75%Punjab & Sind Bank 13.50% 14.25% 0.75%Punjab National Bank 11.00% 13.00% 2.00%State Bank of Bikaner & Jaipur 12.25% 13.50% 1.25%State Bank of Hyderabad 12.25% 13.50% 1.25%State Bank of Travancore 12.50% 13.50% 1.00%Syndicate Bank 12.00% 13.75% 1.75%UCO Bank 12.25% 13.75% 1.50%Union Bank of India 11.75% 13.75% 2.00%United Bank of India 12.00% 13.50% 1.50%Vijaya Bank 12.00% 13.50% 1.50%Yes Bank Ltd 16.50% 18.00% 1.50%

1.55%

Axis Bank Ltd. 15.00% 15.75% 0.75%HDFC Bank Limited 16.00% 16.50% 0.50%ICICI Bank Ltd. 15.75% 17.00% 1.25%State Bank of India 12.25% 13.00% 0.75%

Name of the Bank

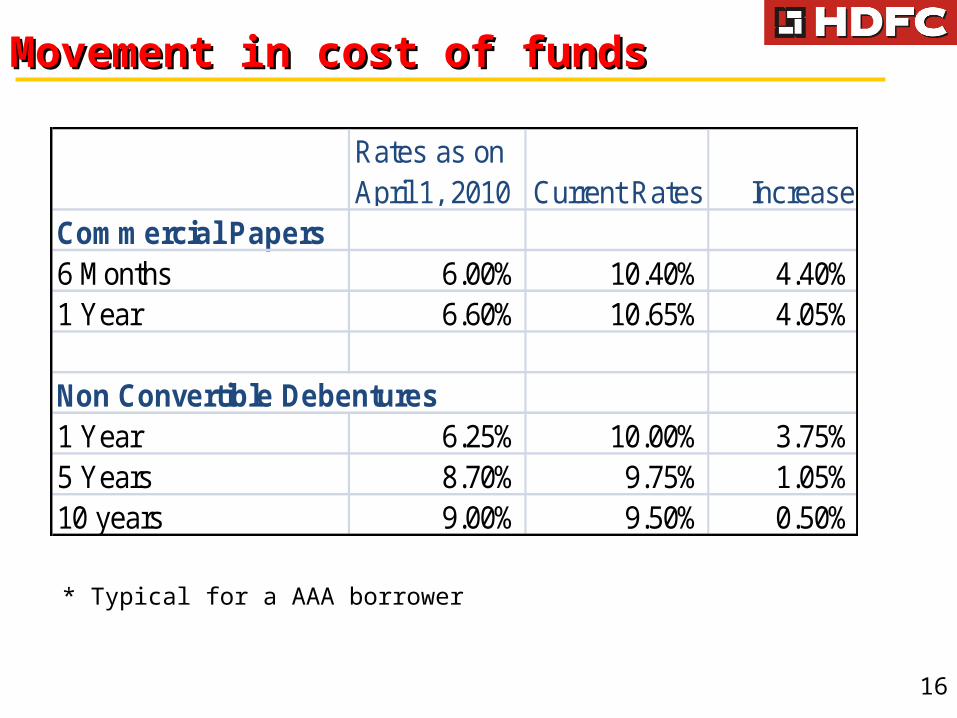

Movement in cost of funds Movement in cost of funds

16

Rates as on April 1, 2010 Current Rates Increase

Commercial Papers6 Months 6.00% 10.40% 4.40%1 Year 6.60% 10.65% 4.05%

Non Convertible Debentures1 Year 6.25% 10.00% 3.75%5 Years 8.70% 9.75% 1.05%10 years 9.00% 9.50% 0.50%

* Typical for a AAA borrower

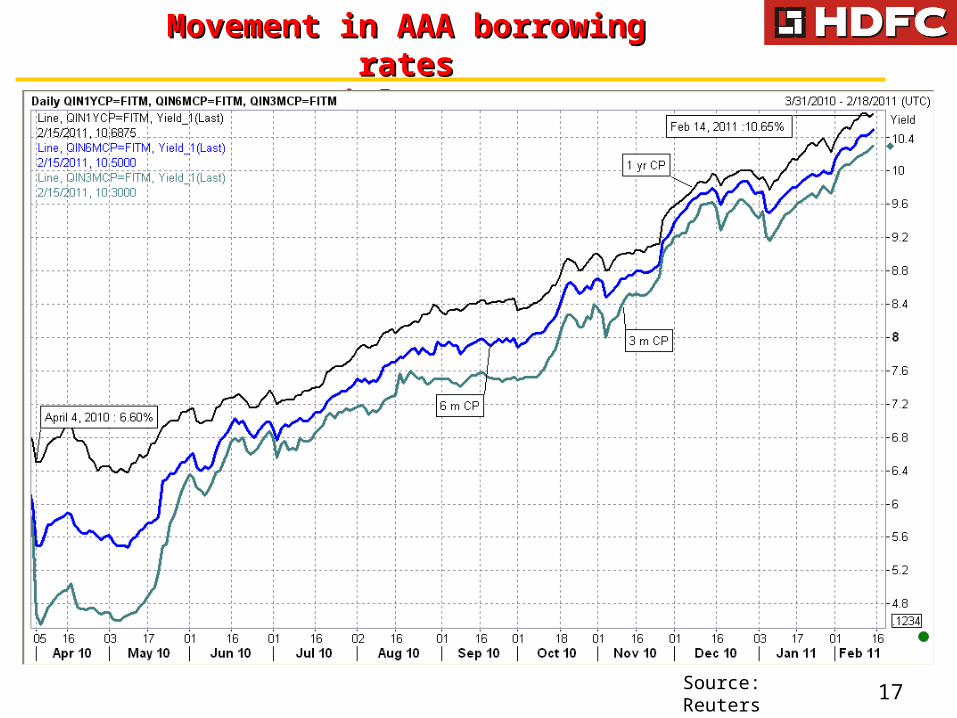

Movement in AAA borrowing ratesMovement in AAA borrowing ratesCommercial Paper (CP)Commercial Paper (CP)

17Source: Reuters

Movement in AAA borrowing ratesMovement in AAA borrowing ratesTerm Borrowings (NCD) Term Borrowings (NCD)

18Source: Reuters

Owing to sharp increase in short term rates, interest rate curve has inverted

19

Movement in G-Sec RatesMovement in G-Sec Rates

Source : Reuters

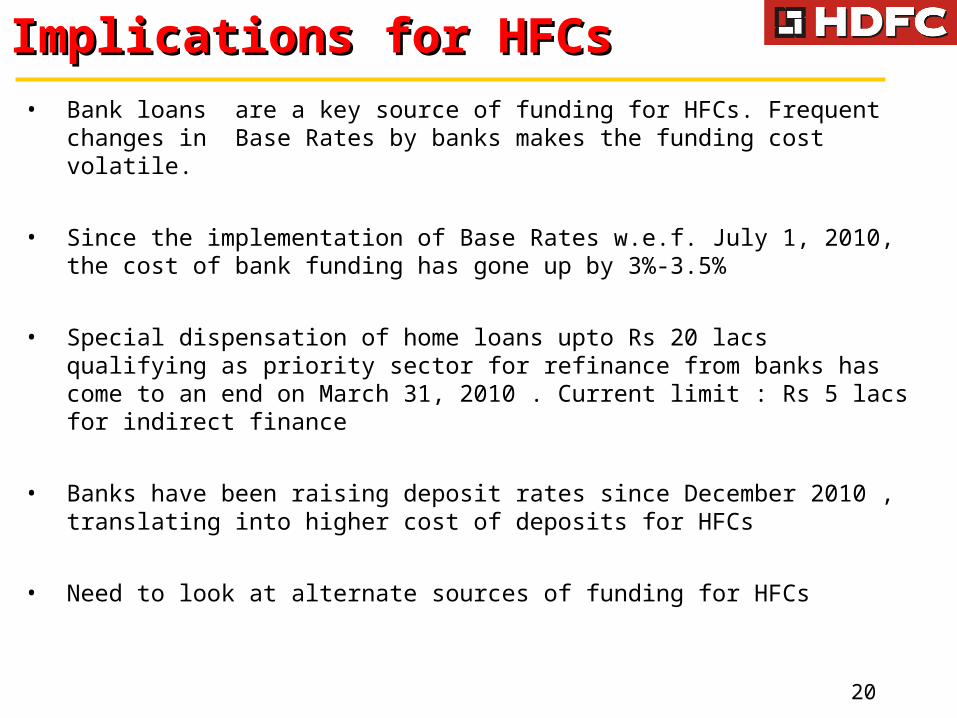

Implications for HFCsImplications for HFCs• Bank loans are a key source of funding for HFCs. Frequent changes in

Base Rates by banks makes the funding cost volatile.

• Since the implementation of Base Rates w.e.f. July 1, 2010, the cost of bank funding has gone up by 3%-3.5%

• Special dispensation of home loans upto Rs 20 lacs qualifying as priority sector for refinance from banks has come to an end on March 31, 2010 . Current limit : Rs 5 lacs for indirect finance

• Banks have been raising deposit rates since December 2010 , translating into higher cost of deposits for HFCs

• Need to look at alternate sources of funding for HFCs

20

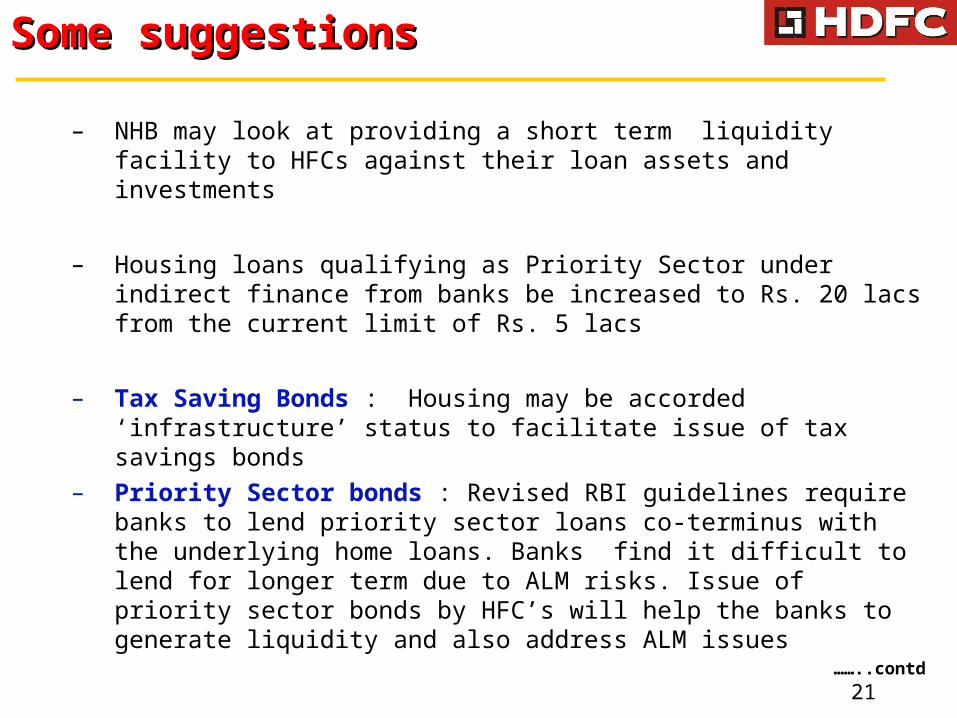

Some suggestionsSome suggestions

– NHB may look at providing a short term liquidity facility to HFCs against their loan assets and investments

– Housing loans qualifying as Priority Sector under indirect finance from banks be increased to Rs. 20 lacs from the current limit of Rs. 5 lacs

– Tax Saving Bonds : Housing may be accorded ‘infrastructure’ status to facilitate issue of tax savings bonds

– Priority Sector bonds : Revised RBI guidelines require banks to lend priority sector loans co-terminus with the underlying home loans. Banks find it difficult to lend for longer term due to ALM risks. Issue of priority sector bonds by HFC’s will help the banks to generate liquidity and also address ALM issues

……..contd

21

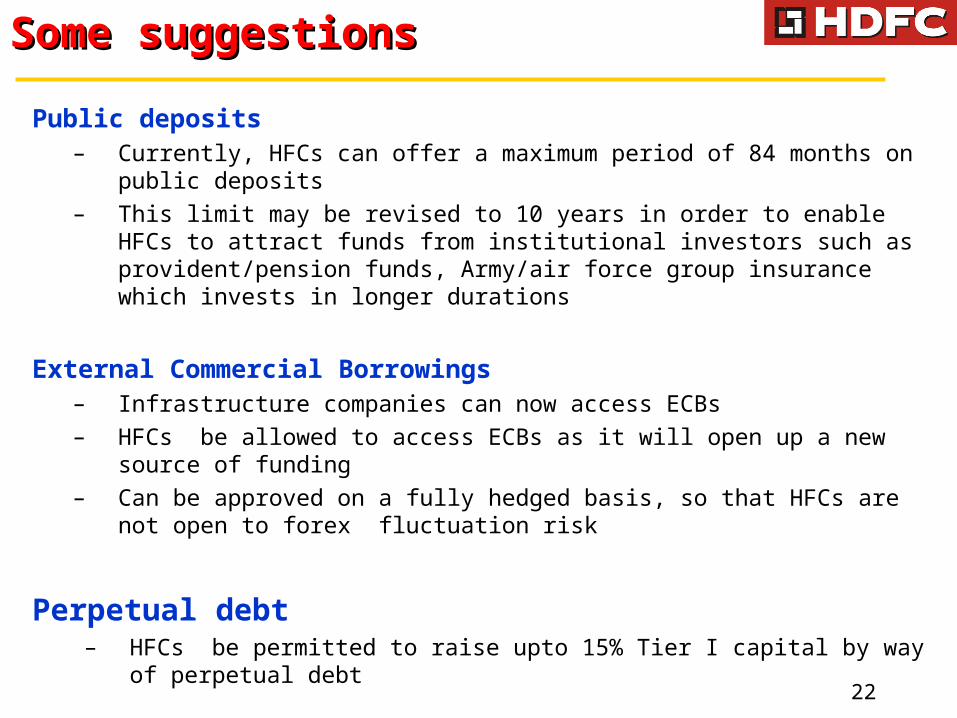

Public deposits– Currently, HFCs can offer a maximum period of 84 months on public

deposits

– This limit may be revised to 10 years in order to enable HFCs to attract funds from institutional investors such as provident/pension funds, Army/air force group insurance which invests in longer durations

External Commercial Borrowings – Infrastructure companies can now access ECBs

– HFCs be allowed to access ECBs as it will open up a new source of funding

– Can be approved on a fully hedged basis, so that HFCs are not open to forex fluctuation risk

Perpetual debt– HFCs be permitted to raise upto 15% Tier I capital by way of perpetual

debt22

Some suggestionsSome suggestions

Thank you Thank you

23