Embed Size (px)

Citation preview

The Capital Asset Pricing Model (CAPM) Applied to Paintings

Montreal, June 2014

Arturo Cifuentes CREM University of Chile Santiago, CHILE

Ventura Charlin VC Consultants Santiago, CHILE

Question: Does the CAPM Work in the Art Market (Paintings)?

Answer: Most Definitively NO Furthermore, Most Previous “Findings” Based on CAPM-Related Studies Should Be Taken With a Great Deal of Skepticism

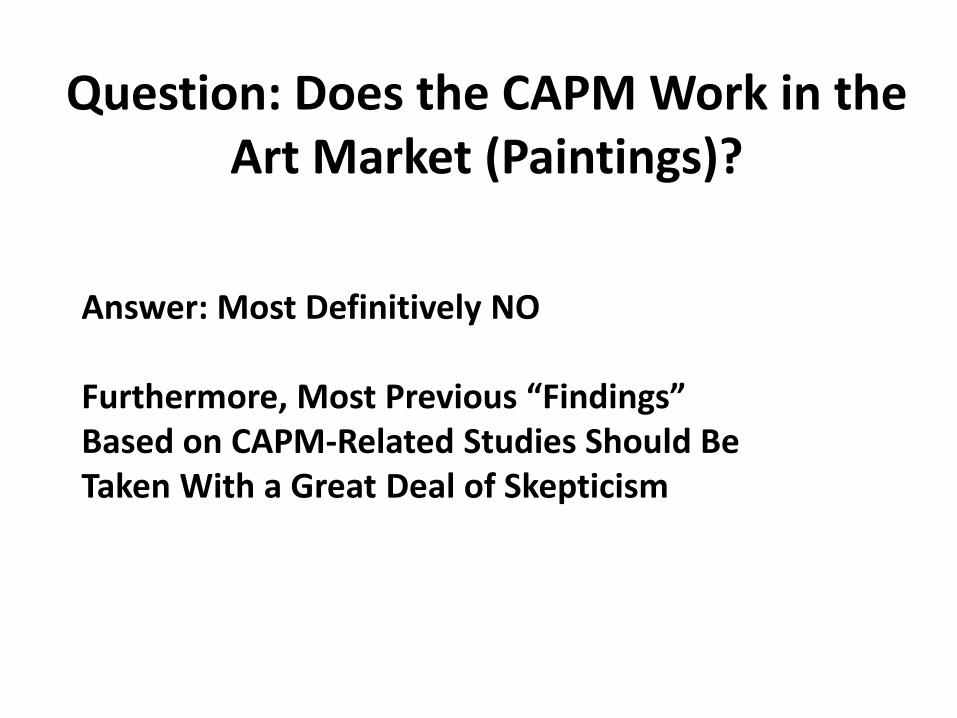

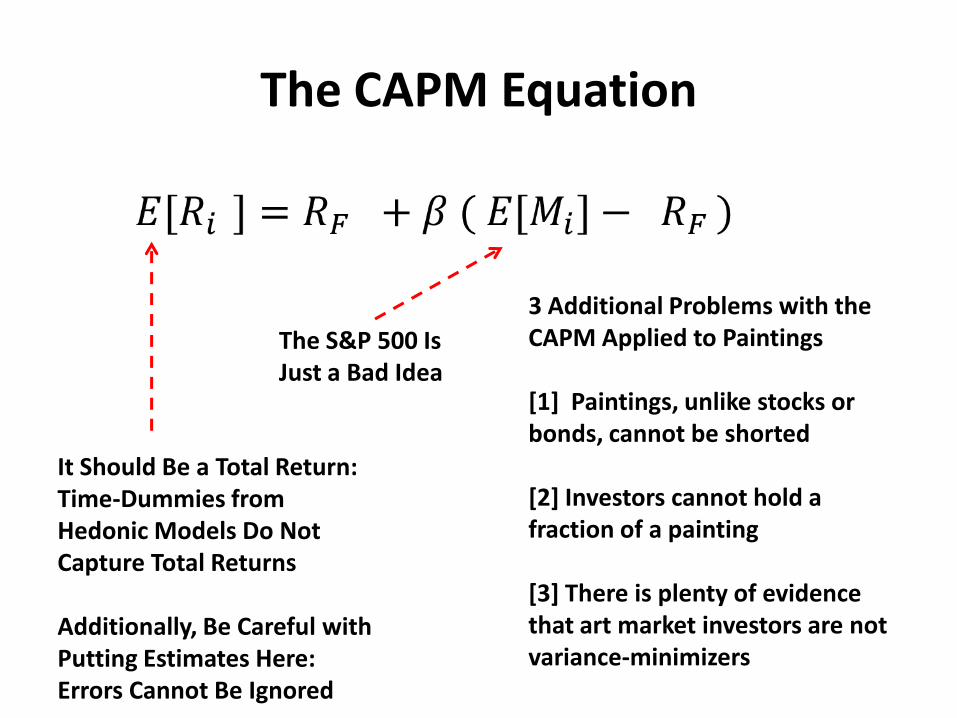

The CAPM Equation

How Do We Account for the “Market”?

Which Return Do We Put Here?

The CAPM Equation

The S&P 500 Is Just a Bad Idea

It Should Be a Total Return: Time-Dummies from Hedonic Models Do Not Capture Total Returns Additionally, Be Careful with Putting Estimates Here: Errors Cannot Be Ignored

3 Additional Problems with the CAPM Applied to Paintings [1] Paintings, unlike stocks or bonds, cannot be shorted [2] Investors cannot hold a fraction of a painting [3] There is plenty of evidence that art market investors are not variance-minimizers

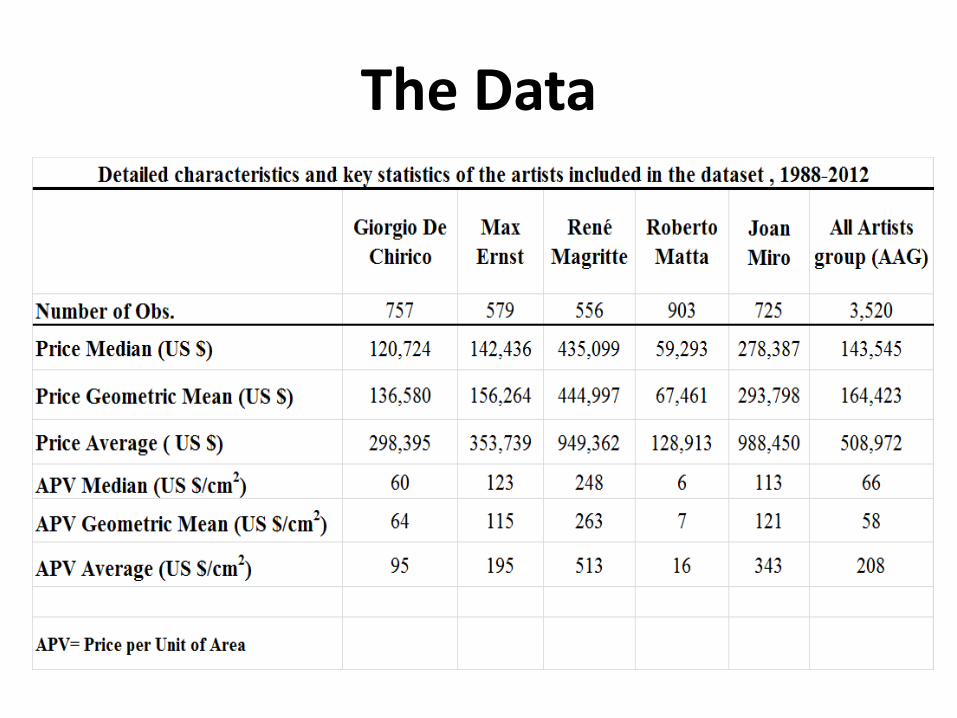

The Data

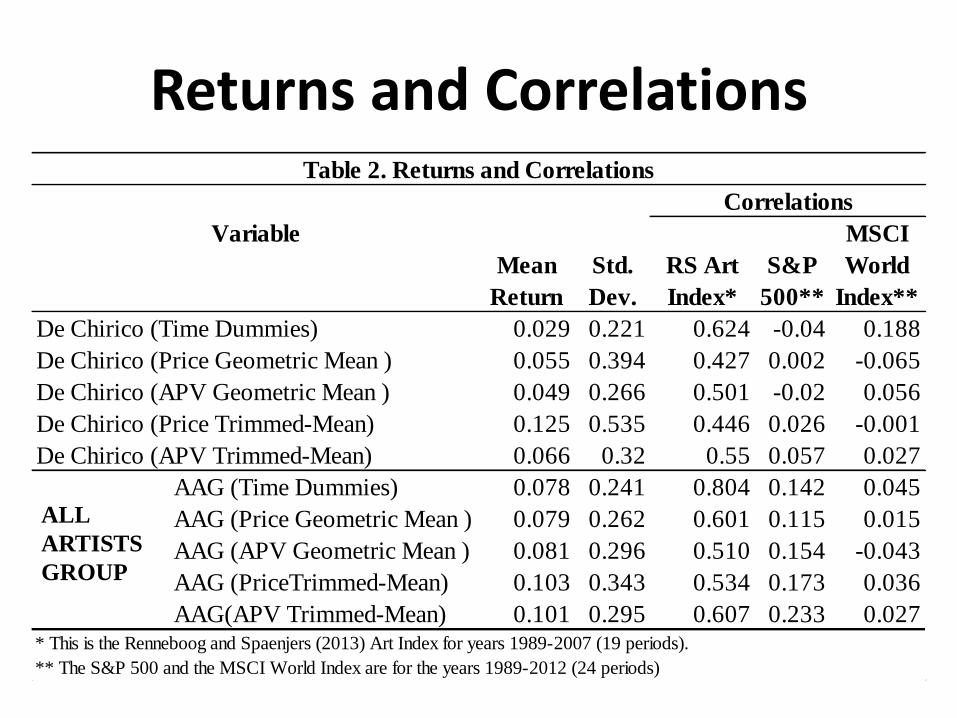

Returns and Correlations

Variable

De Chirico (Time Dummies) 0.029 0.221 0.624 -0.04 0.188

De Chirico (Price Geometric Mean ) 0.055 0.394 0.427 0.002 -0.065

De Chirico (APV Geometric Mean ) 0.049 0.266 0.501 -0.02 0.056

De Chirico (Price Trimmed-Mean) 0.125 0.535 0.446 0.026 -0.001

De Chirico (APV Trimmed-Mean) 0.066 0.32 0.55 0.057 0.027

AAG (Time Dummies) 0.078 0.241 0.804 0.142 0.045

AAG (Price Geometric Mean ) 0.079 0.262 0.601 0.115 0.015

AAG (APV Geometric Mean ) 0.081 0.296 0.510 0.154 -0.043

AAG (PriceTrimmed-Mean) 0.103 0.343 0.534 0.173 0.036

AAG(APV Trimmed-Mean) 0.101 0.295 0.607 0.233 0.027* This is the Renneboog and Spaenjers (2013) Art Index for years 1989-2007 (19 periods).

** The S&P 500 and the MSCI World Index are for the years 1989-2012 (24 periods)

Table 2. Returns and Correlations

Correlations

Mean

Return

Std.

Dev.

RS Art

Index*

S&P

500**

MSCI

World

Index**

ALL

ARTISTS

GROUP

CAPM (Betas) Results

Conclusions (1)

1. The market for paintings and stocks do seem to be highly disconnected

• Not much can be concluded from any CAPM analysis using stock market indexes as a proxy for the market

2. Using return estimates for individual artists based on the time-dummies of hedonic models is not correct, for these returns do not fully capture supply-demand market dynamics; they are not total returns

Conclusions (2)

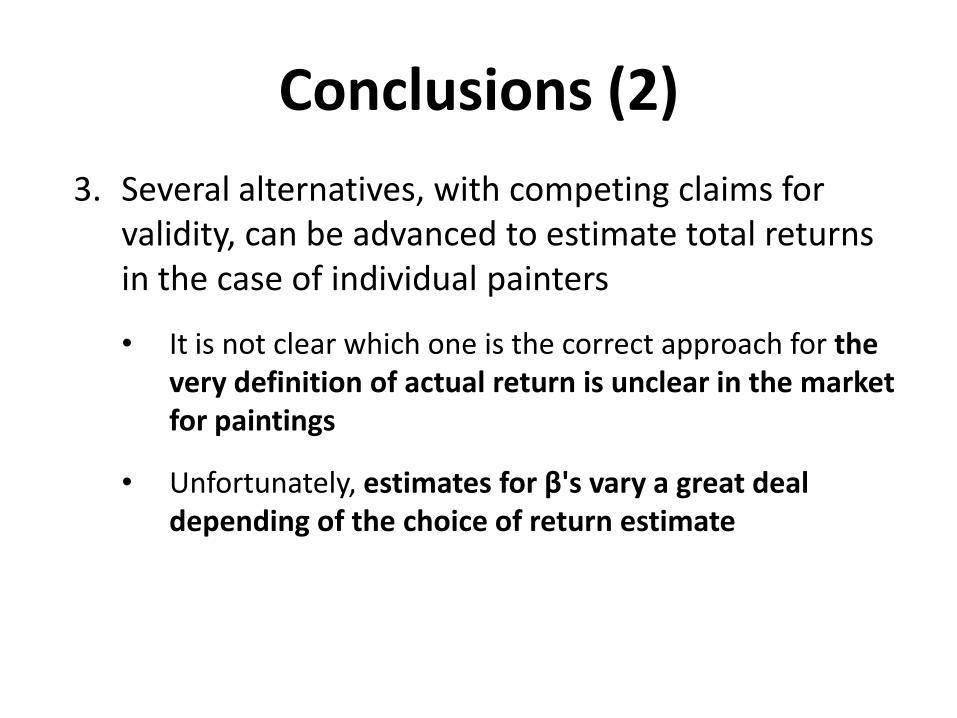

3. Several alternatives, with competing claims for validity, can be advanced to estimate total returns in the case of individual painters

• It is not clear which one is the correct approach for the very definition of actual return is unclear in the market for paintings

• Unfortunately, estimates for β's vary a great deal depending of the choice of return estimate

Conclusions (3) 4. In the case of an index aimed at capturing broader

art market tendencies--not aimed at estimating the total return for an artist or group of artists-- the use of the time-dummies of the hedonic model seems to be, at least in principle, a valid choice

• However, the fact that price-indices based on the time-dummies do not satisfy Fisher’s monotonicity condition, casts doubt on the reliability of such return estimates

• It is difficult to ascertain whether these estimates are spurious or not

Conclusions (4)

5. Finally, we must consider that the previously estimated returns ―regardless of the method used― are just that, estimates

• And therefore they contain an error

• If the error is taken into account ―which for the sake of simplicity was not considered in these analyses― the estimated β's from the CAPM equation would have even broader confidence intervals

In Summary,

The Use of the CAPM in the Market for Paintings Does Not Seem to Add Any

Value

Appendices

References [[ 1 ]] V. Charlin & A. Cifuentes, A New Financial Metric for the Art Market, to be published in September 2014 by the Journal of Alternative Investments; also available from the SSRN website (paper ID Number=2291569). [[ 2 ]] V. Charlin & A. Cifuentes, Towards a Monotonicity-Compliant Price Index for the Art Market, available from the SSRN website (paper ID Number=2411101). Additionally, [[ 3 ]] Dollars and Sense in the Art Market; [[ 4 ]] The Capital Asset Pricing Model (CAPM) Applied to Paintings; and [[ 5 ]] Art Market Returns: Misgivings and Certainties These three papers by V. Charlin & A. Cifuentes will be presented at the upcoming ACEI Conference, Montreal, Canada, June 2014.

Ventura Charlin, Ph.D. E-mail: [email protected] Ventura is a seasoned Applied Statistician with more than fifteen years of hands-on experience using analytical techniques in marketing and consumer credit risk. She specializes in the use of quantitative techniques to provide strategic and tactical solutions to clients' challenges, thereby maximizing the return on their database, marketing and customer acquisition investments. A native of Santiago, Chile, Ventura speaks fluent Spanish and holds a Psychologist Degree (with honors) from the University of Chile. She also earned a M.S. in Finance from the Zicklin School of Business at Baruch College (valedictorian), and a Ph.D. in Quantitative Psychology (Applied Statistics) from the University of Southern California. Arturo Cifuentes, Ph.D. E-mail: [email protected] Dr. Cifuentes joined the Faculty of Economics and Business of the University of Chile in May 2013, as Academic Director of the CREM (Financial Regulation and Macro-Stability Center). Currently, he also president of the investment committee that manages the Chilean Sovereign Fund (US$ 25 billion in assets). Previously, he served for four years as a member of the Advisory Board of the Division of Humanities and Social Sciences of the California Institute of Technology, Caltech, (2008-2013). Finally, from August 2010 until March 2011 he was a member of the Financial Regulation Reform Committee that was appointed by the Minister of Finance (Chile). He holds a Ph.D. in applied mechanics and a M.S. in civil engineering from the California Institute of Technology (Caltech); an MBA in finance from New York University (Stern scholar award); and a civil engineering degree from the University of Chile.