Embed Size (px)

Citation preview

The Business Casefor CUSP

William J. Ward, Jr., MBA

Associate Professor of Health Finance and Management

Associate Professor of NursingDirector, Master of Health Administration Degree

The Johns Hopkins Bloomberg School of Public Health

Your Feedback is Important

https://www.surveymonkey.com/s/Z6FJ28T

Framing the Business Case

• How hospitals operate• Revenue & expense behavior• Connecting the dots• The valid business case• Why CUSP matters – the financial pay-off• Questions and Answers

The Process of Hospital Care The orchestrated application of caregiver

knowledge, skills, and expertise; technologies; supplies and medications

A process as opposed to a single intervention or a series of isolated events

The Process of Hospital Care The orchestrated application of caregiver

knowledge, skills, and expertise; technologies; supplies and medications

A process as opposed to a single intervention or a series of isolated events

A System

A System

How Hospitals are Paid

• Fee For Service (FFS)– Payments for individual services rendered– Per lab test, patient day– Less work equals less revenue

• DRG or Case Based– Payment for a case regardless of work performed – Less work equals more profit

How Hospitals are PaidHospital Charges Case 1 Case 2 Case 3

Room & Board $ 4,500 $ 5,000 $ 5,500

Laboratory

500

600

700

Diagnostic Imaging

400

500

600

Medications

800

1,000

1,200

Other Charges

800

900

1,000

Total Billed $ 7,000 $ 8,000 $ 9,000

DRG Payment $ 8,000 $ 8,000 $ 8,000

How Hospital Costs Behave

• Fixed costs– hold constant regardless of volume

• Variable costs– rise and fall along with volume

• Semi-variable– fixed over a range of volume,

then vary sharply, then fixed again

– “step costs”

Profile of Fixed & Variable CostsProfile of Fixed & Variable Costs

Expense CategoryExpense Category

Percent of Percent of Total CostTotal Cost

Fixed Fixed ProportionProportion

Variable Variable ProportionProportion

Salary & BenefitsSalary & Benefits 65%65% 60%60% 5%5%

Supplies & ServicesSupplies & Services 15%15% 10%10% 5%5%

InterestInterest 10%10% 10%10% 0%0%

DepreciationDepreciation 10%10% 10%10% 0%0%

TotalTotal 100%100% 90%90% 10%10%

How Hospital Costs Behave

• Fixed costs– hold constant regardless of volume

• Variable costs– rise and fall along with volume

• Semi-variable– fixed over a range of volume,

then vary sharply, then fixed again

– “step costs”

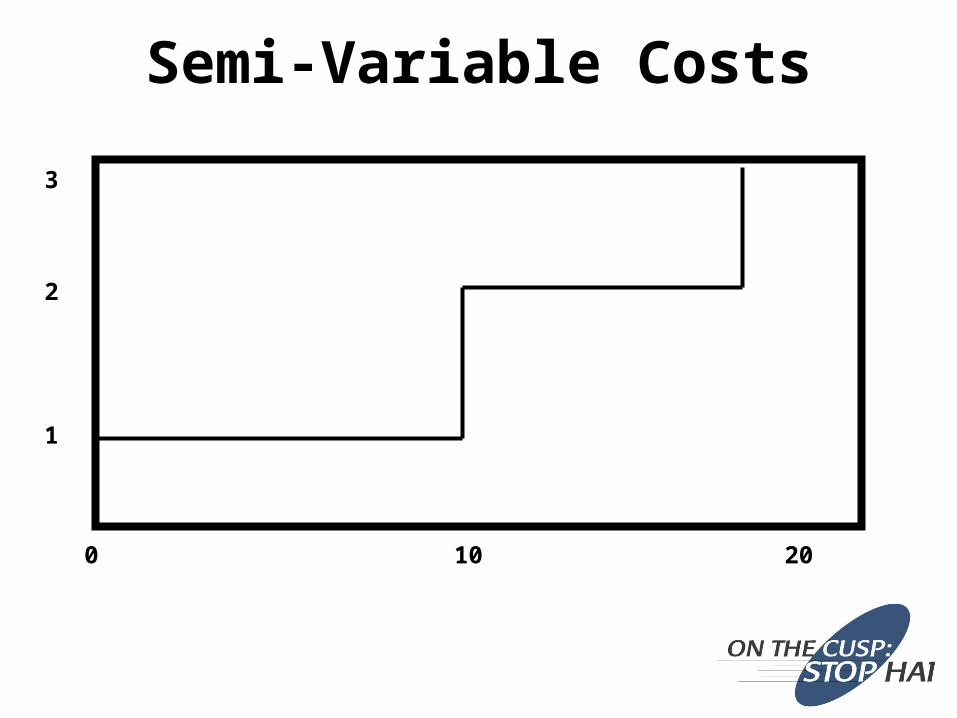

Semi-Variable Costs

0 10

1

20

2

3

Semi-Variable Costs and Revenue

0 10

1

20

2

3

Semi-Variable Costs and Revenue

Profit

Loss

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

??

????

??

??

??

????

??

??

??

??

??

??

????

??

Connecting the Dots(from fewer infections to more profit)

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

Connecting the Dots(from fewer infections to more profit)

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

Connecting the Dots(from fewer infections to more profit)

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

Connecting the Dots(from fewer infections to more profit)

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

Connecting the Dots(from fewer infections to more profit)

ImprovedProfits

ControlledCosts

IncreasedRevenue

Increased BedTurnover

ReducedALOS

ReducedInfections

Static BedCount

IncreasedAdmits

Connecting the Dots(from fewer infections to more profit)

An ounce of prevention is worth a pound of cure.”

Benjamin Franklin

Importance of Infection Control

DISCHARGE

ADMISSION

Infections

Nursing CareNursing CareNursing CareNursing Care

Ancillary ServicesAncillary ServicesAncillary ServicesAncillary Services

Support ServicesSupport Services Support ServicesSupport Services

Other FactorsOther FactorsOther FactorsOther Factors

• Improvements in quality and patient safety can yield . . .– Cost efficiency– Real cost reduction– Revenue enhancement– Balance sheet improvements– Intangible improvements

Connecting the Dots(from fewer infections to more profits)

Improved HAI rate yieldsImproved HAI rate yields■ Increased capacityIncreased capacity■ Increased work output Increased work output ■ No change in total costNo change in total cost

Same cost ÷ increased work outputSame cost ÷ increased work output= Reduced Cost per Unit of Work= Reduced Cost per Unit of Work

Cost Efficiency ModelCost Efficiency Model

Improved HAI rate yieldsImproved HAI rate yields■ Increased capacityIncreased capacity■ No change in work output No change in work output ■ Reduction in staffing levelsReduction in staffing levels

Workload Reduction ÷ Original WorkloadWorkload Reduction ÷ Original Workload= Potential Percentage Staff Reduction= Potential Percentage Staff Reduction

Real Cost ReductionReal Cost Reduction

Improved HAI rate yieldsImproved HAI rate yields Increased patient throughputIncreased patient throughput Reduced OR case cancellationsReduced OR case cancellations Increased surgical casesIncreased surgical cases Reduced ER divert hoursReduced ER divert hours Increased ER visits and admissionsIncreased ER visits and admissions Increased follow-up visits and proceduresIncreased follow-up visits and procedures Increased revenue and increased cashIncreased revenue and increased cash

Hospital ThroughputHospital Throughput

• Improvements in HAI rate leads to improved throughput– Maximized brick & mortar investments– Additional funds available for

capital purchases– Reduced need for cash or

borrowing to increase capacity

Balance Sheet Improvement

Reduced malpractice claimsHigher satisfaction scores

patient, family & staff Better reputationBetter market position

Intangible Hospital Benefits

Getting Down to Cases # 1

• 66 years old• Medicare patient• Grandmother of 2• Diabetic, hypertensive,

obese, nonsmoker• Elective admission for

CABG

Getting Down to Cases # 1

• 66 years old• Medicare patient• Grandmother of 2• Diabetic, hypertensive,

obese, nonsmoker• Elective admission for

CABG Day 5 – fever of 103o

Day 9 – 15 vent dependent Day 22 – transferred to LTAC

OoopsOoops

Revenue ImpactDay 1Day 1 Day 22Day 22

Case # 1 – DRG payment $12,689

Case # 1 – $12,689Case # 1 – $12,689

Case # 2 – $12,689Case # 2 – $12,689

Case # 3 – $12,689Case # 3 – $12,689

One case w/complicationsOne case w/complicationsVersus three cases w/o complicationsVersus three cases w/o complicationsRevenue of Revenue of $ 12,689 $ 12,689 versus Revenue of versus Revenue of $ 38,067$ 38,067

One case w/complicationsOne case w/complicationsVersus three cases w/o complicationsVersus three cases w/o complicationsRevenue of Revenue of $ 12,689 $ 12,689 versus Revenue of versus Revenue of $ 38,067$ 38,067

Source: NEJM Archive / NEJM.org / December 15, 2011 / Copyright © 2010 NEJM

April 2010

“… they are disappointed when the reduction in the number of HAIs does not yield the anticipated cost savings.”

“… and, so, seek the opportunity cost …”

The Real CUSP Payoff

Values shown are strictly for purposes of illustration and are not meant to approximate real results

Average Length of Stay - CLABSI Cases (days) 28.8 A

Average Length of Stay - All Cases (days) 4.8 B

Reduction in ALOS (days) (1) 24.0 C

Potential Incremental Case Throughput 5.0 D = C / B

Average Net Revenue per Case (2) $7,078.00 E

Potential Incremental Net Revenue Opportunity per Avoided CLABSI $35,390 F = D x E

Potential Annual Avoided CLABSI Cases 100 G

Potential Annual Incremental Profit Opportunity $3,539,000 H = F x G

Sources:1. CDC2. HFMA (William O. Cleverley and James O. Cleverley)

Your Feedback is Important

https://www.surveymonkey.com/s/Z6FJ28T

Questions and Answers