Embed Size (px)

Citation preview

10/7/2014

1

The 2014 TRACS Annual Conference

Orlando, Florida

October 22, 2014

Jan M. Haas, Sr. VP,

Finance & Administration

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Objectives• Definition

• Relationship to strategic planning

• Types of budgets

• Process preparation

• Presentation

• Monitoring

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 2

Definitions• Institutional budgeting is the process whereby the

plans of an institution are translated into an itemized, authorized, and systematic plan of operation, expressed in dollars for a given period.

• Budgets are the blueprints for the orderly execution of program plans; they serve as control mechanisms to match anticipated and actual revenues and expenditures.

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 3Source: National Association of College and Universities Business Officers, College and University Business Administration, 4th Edition, 1982.

10/7/2014

2

Definitions (continued)

• Budgeting is a management tool for both planning and control.

• Fundamentally, the budgeting process is a method to improve operations - a continuous effort to specify what should be done to get the job completed in the best possible way.

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 4Source: Managerial Finance, Seventh Edition, J. Fred Watson & Eugene F. Brigham, The Dryden Press, Hinsdale, IL, 1981.

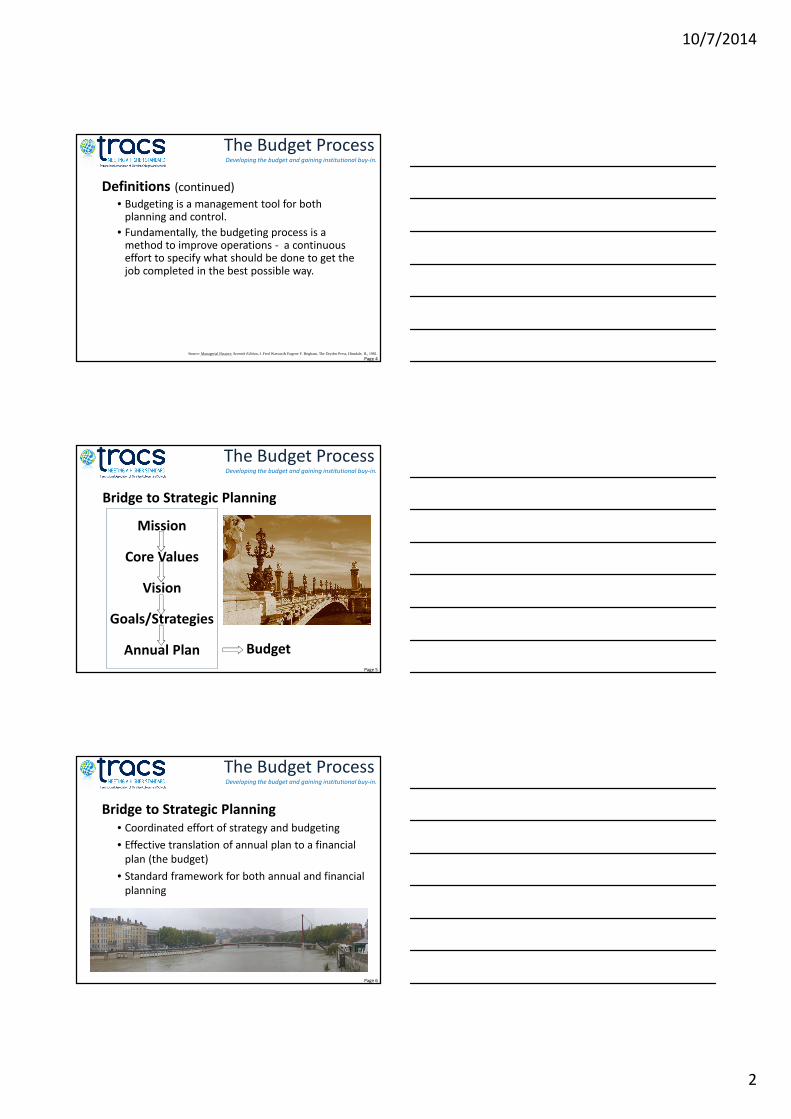

Bridge to Strategic Planning

Budget

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 5

Mission

Core Values

Vision

Goals/Strategies

Annual Plan

Bridge to Strategic Planning

• Coordinated effort of strategy and budgeting

• Effective translation of annual plan to a financial

plan (the budget)

• Standard framework for both annual and financial

planning

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 6

10/7/2014

3

Operating Budget• Revenue

• Expenses

� Salary and Benefits

� Operations

Capital Budget• Relationship to the mission

• Strategic importance

• Multi year, committed projects

• Essential projects (e.g., safety, accreditation)

• Financial return (NPV, IRR, Break-Even)

• Probability of success

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 7

Factors Affecting the Budget ProcessInternal Factors

• Mission

• Fiscal policies

• Compensation goals and policies

• Pricing policies

• Management style

• Accountability

• Debt policies

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 8

Source: National Association of College and Universities Business Officers, College and University Business Administration, 4th Edition, 1982.

Factors Affecting the Budget ProcessExternal factors

• Sources of support

• Government regulations - OSHA, EPA, ADA, FERPA,

PPACA, Title IX, etc.

• Competition for students

• Demographic trends

• Inflation

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 9

10/7/2014

4

Process

• The process should communicate:

� institutional priorities to various

constituencies,

� identify specific commitments, and

� establish preliminary control over

institutional resources.

• The result of this process is a document

that is used to monitor and control the

ongoing operations of an institution.

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 10

Process

Major participants include:

• The Governing Board

• Chief Executive Officer

• Senior Administrators

• Budget Officer

• Planning and Budgeting group

• Faculty

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 11

Key Success Factors• Process must provide a clear mission as well

as strategic and financial context for decision making

• Overall capacity should be communicated early in the process

• Budget calendar must provide adequate timeframes for completion of tasks

• A process for ongoing feedback should be implemented to promote continuous improvement of the process

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 12

10/7/2014

5

Preparation1. Create a budget calendar

2. Determination and communication of budget

guidelines

3. Estimates of revenues and expenditures

4. Internal budget hearings with academic and

support units

5. Preparation of budget requests

6. Standards/Targets/Benchmarks

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 13

Source: Budgeting, Ken Martin, Ph.D., Messiah College, February 11, 2003.

Preparation1. Develop a budget calendar

• Leadership discusses preliminary targets

• Present budget parameters to budget group

• Set budget targets

• Distribute budget materials

• Budget workshops

• Budget submissions reviewed

• Reviews consolidated for leadership

• Report to Finance Committee

• Board of Trustees approval

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 14

Preparation2. Determination and communication of budget guidelines

• Salary and wage increases

• Tuition rates

• Levels of support for student aid

• Increased operational expenses

• Improvements in certain programs

• Implementation f new programs

• Reduction or elimination of existing programs

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 15

10/7/2014

6

Preparation3. Estimating Revenues …

• Enrollment data

• Economic conditions

• Investment earnings

• Revenues from gifts

• Auxiliary enterprises

and Expenditures• Improvement of existing programs

• Development of new programs

• Policies for salaries, promotions & employee benefits

• Student-faculty ratios, class size, teaching loads

• Increased costs

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 16

Preparation4. Internal budget hearings with academic and

support units

5. Preparation of budget request

Standardized forms

• Personnel

• Operating expenses

• Capital expenditures

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 17

Source: Managerial Finance, Seventh Edition, J. Fred Watson & Eugene F. Brigham, The Dryden Press, Hinsdale, IL, 1981.

Preparation6. Standards/Targets/Benchmarks

• Accreditation agency guidelines

• National association recommendations

• ABACC financial benchmarking

• State agency reports

• Key Performance Indicators

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 18

10/7/2014

7

Presentation

• Costs and benefits of offering programs

• Consequences of reducing support services

• Effects of demographic trends

• Effects of other factors (both internal and external)

• Assumptions

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 19

Presentation (continued)

• Comparison to budgets of prior years

• Explanations of major changes

• Description of programs added or eliminated

• Wage and salary policies

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 20

Source: Budgeting, Ken Martin, Ph.D., Messiah College, February 11, 2003.

Lessons Learned

• New positions = permanent $

• Leadership needs to assess departmental needs

early in the process

• Provide feedback on priorities and communicate

decisions firmly

• Remain flexible

• Encourage staff to become involved in cost

reduction efforts

• Communication builds alliances

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 21

10/7/2014

8

)

Lessons Learned (continued)

• Decisions should be based on trends and

introduce increment tally; it is difficult to retract

• Quick fixes can increase deferred maintenance

with expensive consequences

• Managing the budget process is different than

controlling revenues and expenditures

• Educate others by saying it often and in a variety

of ways

• Avoid the “shotgun” approach

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Page 22

Q & A

The Budget ProcessDeveloping the budget and gaining institutional buy-in.

Jan M. Haas

Sr. VP, Finance & Administration

www.cairn.edu

215-702-4312