Embed Size (px)

Citation preview

The Bridge to Mexican Infrastructure

September 16, 2014

NET Mexico Pipeline is a lean gas transportation pipeline that will transport natural gas from Agua Dulce Hub to a location near Rio Grande City, TX at the Mexico border and will interconnect with the Los Ramones Pipeline. At 2.3 Bcf/d capacity, NETMEX will become the largest natural gas export pipeline from US to Mexico.

Asset Map Asset Overview

• NET Mexico Pipeline is a 2.3 Bcf/d, 120 mile, 42” and 48” pipeline from the Agua Dulce Hub to the US / Mexico border, which will be completed in December 2014

– Pipeline will be completed on-time and under budget

– Mainline construction complete, all permits received, all ROW acquired

• Pipeline extends across the Rio Bravo River (Rio Grande) and interconnects with the Los Ramones pipeline in Mexico,

– Los Ramones is a 48” pipeline that spans five Mexican states and ends in Mexico’s largest industrial corridor

– Commercial operation for first phase of Los Ramones scheduled to begin in December 2014

• Anchored by a 20-year gas transportation agreement with MGS, an affiliate of PEMEX

– 2.1 Bcf/d firm, ship-or-pay agreement

– Guaranteed by PGPB

• Significant compression

– 100,000 HP of compression at the Agua Dulce Hub

– 20,000 HP of compression at three connecting processing plants

• PEMEX owns a 10% equity interest

NET Mexico Asset Overview

2

September 16, 2014

The Bridge to Mexican Infrastructure

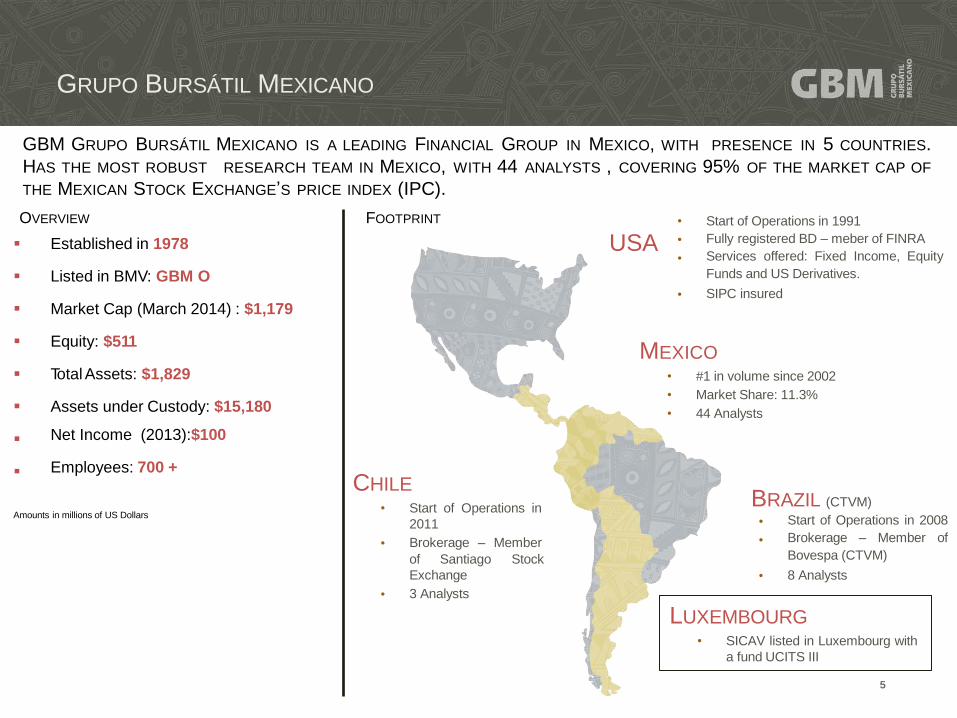

GBM GRUPO BURSÁTIL MEXICANO IS A LEADING FINANCIAL GROUP IN MEXICO, WITH PRESENCE IN 5 COUNTRIES.

HAS THE MOST ROBUST RESEARCH TEAM IN MEXICO, WITH 44 ANALYSTS , COVERING 95% OF THE MARKET CAP OF

THE MEXICAN STOCK EXCHANGE’S PRICE INDEX (IPC).

GRUPO BURSÁTIL MEXICANO

Established in 1978

Listed in BMV: GBM O

Market Cap (March 2014) : $1,179

Equity: $511

Total Assets: $1,829

Assets under Custody: $15,180

Net Income (2013):$100

Employees: 700 +

Amounts in millions of US Dollars

Start of Operations in 1991

Fully registered BD – meber of FINRA

Services offered: Fixed Income, Equity

Funds and US Derivatives.

SIPC insured •

CHILE • Start of Operations in

2011

Brokerage – Member •

of Santiago

Exchange

3 Analysts

Stock

•

LUXEMBOURG • SICAV listed in Luxembourg with

a fund UCITS III

USA

MEXICO

•

•

•

#1 in volume since 2002

Market Share: 11.3%

44 Analysts

•

•

Start of Operations in 2008

Brokerage – Member of

Bovespa (CTVM)

8 Analysts •

BRAZIL (CTVM)

OVERVIEW FOOTPRINT •

•

•

5

GBM HAS A SUCCESSFUL TRACK RECORD AS AN ASSET MANAGER,

PERFORMANCE AWARD, GRANTED BY FUND PRO, AMONG OTHERS.

CONSISTENTLY ACHIEVING THE PLATINUM

GBM ASSET MANANGEMENT

More than 30 years of experience

Mexico Investment Solutions

• Mexican debt and equity funds

Portfolios and investment mandates •

• Record Keeping

Global Investment Solutions

• SIC Funds

• Hedge Funds

International Wealth Management •

• UCITS III

6

GBM team has been enhanced with independent advisors and the hiring of experts in the development of infrastructure projects.

INFRAESTRUCTURA SEEKS TO CAPITALIZE ON ITS EXPERIENCE IN PRIVATE EQUITY AND INFRASTRUCTURE, TAKING INTO

ACCOUNT THAT MOST SUCCESSFUL INFRASTRUCTURE FUNDS WORLDWIDE HAVE BEEN PROMOTED BY FINANCIAL

INSTITUTIONS.

PRIVATE EQUITY WITH IPO EXIT

PRIVATE EQUITY AND INFRASTRUCTURE

(Divested)

Punta Venus

OTHER SUBSTANTIAL INVESTMENTS

Real Estate

Portfolio

PRIVATE INVESTMENT IN PUBLIC EQUITY OTHER INVESTMENTS

IN PRIVATE EQUITY

SINCA GBM

CA

PIT

AL

IN

CR

EA

SE

(AC

QU

IRE

D O

UT

RIG

HT)

7

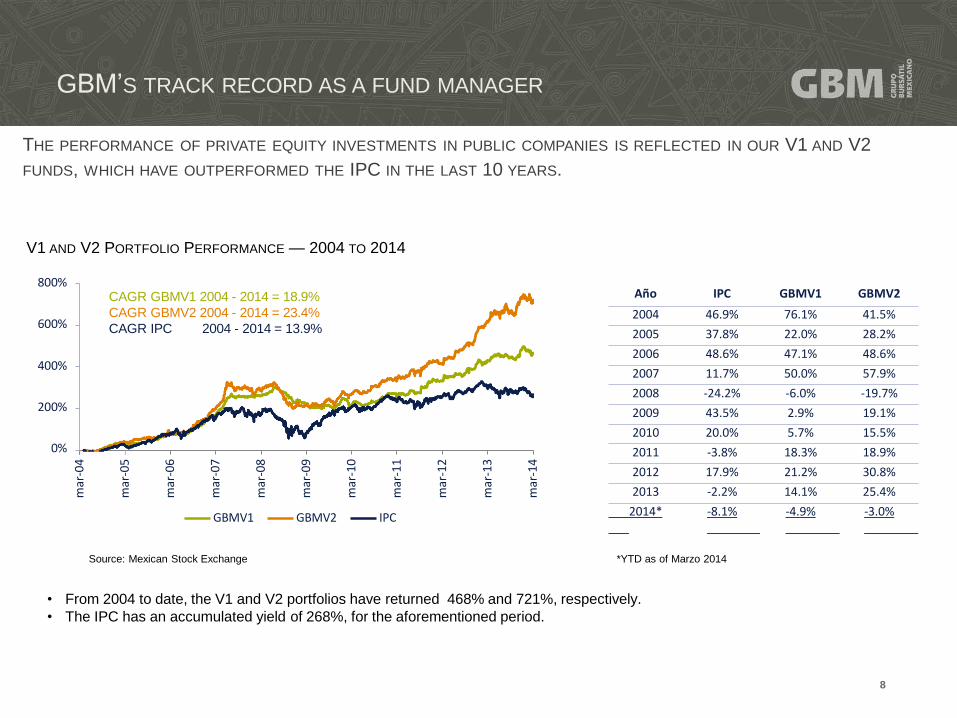

THE PERFORMANCE OF PRIVATE EQUITY INVESTMENTS IN PUBLIC COMPANIES IS REFLECTED IN OUR V1 AND V2

FUNDS, WHICH HAVE OUTPERFORMED THE IPC IN THE LAST 10 YEARS.

GBM’S TRACK RECORD AS A FUND MANAGER

• From 2004 to date, the V1 and V2 portfolios have returned 468% and 721%, respectively.

• The IPC has an accumulated yield of 268%, for the aforementioned period.

*YTD as of Marzo 2014

V1 AND V2 PORTFOLIO PERFORMANCE — 2004 TO 2014

800%

Source: Mexican Stock Exchange

400% 200%

0%

600%

mar

-04

mar

-05

mar

-06

mar

-07

mar

-08

mar

-09

mar

-10

mar

-11

mar

-12

mar

-13

mar

-14

GBMV1 GBMV2 IPC

8

CAGR GBMV1 2004 - 2014 = 18.9%

CAGR GBMV2 2004 - 2014 = 23.4%

CAGR IPC 2004 - 2014 = 13.9%

Año IPC GBMV1 GBMV2

2004 46.9% 76.1% 41.5%

2005 37.8% 22.0% 28.2%

2006 48.6% 47.1% 48.6%

2007 11.7% 50.0% 57.9%

2008 -24.2% -6.0% -19.7%

2009 43.5% 2.9% 19.1%

2010 20.0% 5.7% 15.5%

2011 -3.8% 18.3% 18.9%

2012 17.9% 21.2% 30.8%

2013 -2.2% 14.1% 25.4%

2014*

-8.1%

-4.9%

-3.0%

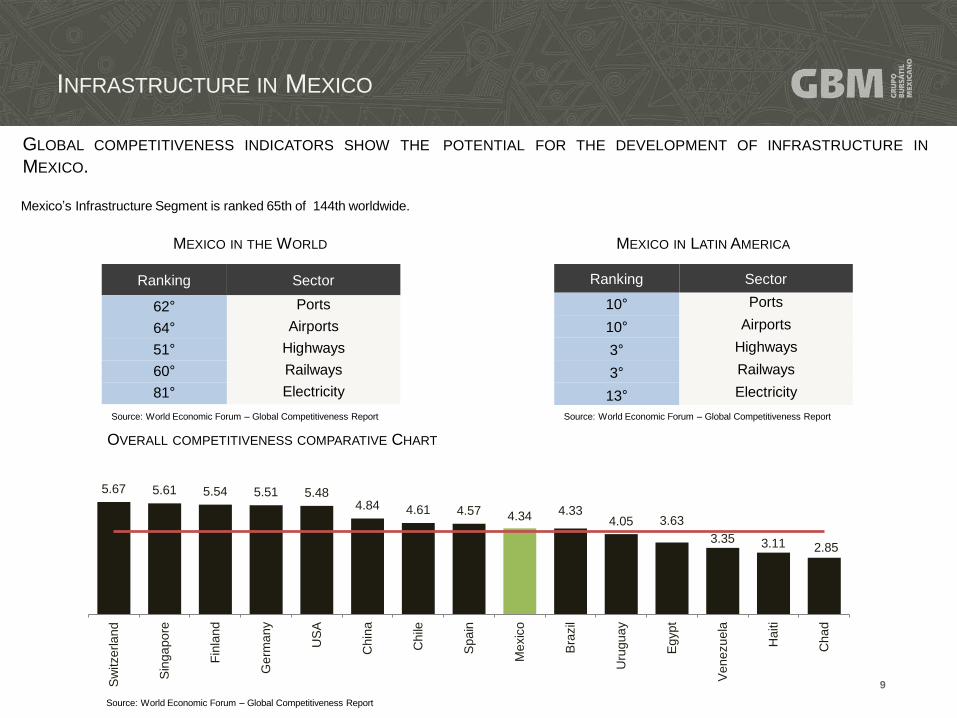

GLOBAL COMPETITIVENESS INDICATORS SHOW THE

MEXICO.

POTENTIAL FOR THE DEVELOPMENT OF INFRASTRUCTURE IN

INFRASTRUCTURE IN MEXICO

Mexico’s Infrastructure Segment is ranked 65th of 144th worldwide.

MEXICO IN THE WORLD

Ranking Sector

MEXICO IN LATIN AMERICA

Ranking Sector

62°

64°

51°

60°

81°

Ports

Airports

Highways

Railways

Electricity

10°

10°

3°

3°

13°

Ports

Airports

Highways

Railways

Electricity

OVERALL COMPETITIVENESS COMPARATIVE CHART

Source: World Economic Forum – Global Competitiveness Report Source: World Economic Forum – Global Competitiveness Report

Source: World Economic Forum – Global Competitiveness Report

5.67 5.61 5.54 5.51 5.48 4.84 4.61 4.57 4.34 4.33

4.05 3.63

3.35 3.11 2.85

Sw

itze

rla

nd

Sin

ga

po

re

Fin

lan

d

Ge

rma

ny

US

A

Ch

ina

Ch

ile

Spain

Me

xic

o

Bra

zil

Uru

gu

ay

Eg

yp

t

Vene

zu

ela

Ha

iti

Ch

ad

9

THE PPP LAW*, ENACTED ON JANUARY 15 2012, BOOSTS THE DEVELOPMENT OF NEW INFRASTRUCTURE

PROJECTS IN MEXICO • Prioritizes private over public investment.

• Promotes new financing schemes based on multi-year budgets.

• Distributes the risks involved in projects execution, in an equitable manner.

• Establishes agile and flexible contracting procedures with greater security and legal certainty.

• Beholds the constructive assent of the authorizations required to start projects.

• Supports projects that investors present without these haven’t been called (or tendered), with the possibility of reimbursement

of incurred expenses.

• Stipulates that the assessment of proposals is based on a cost-benefit criteria and rules that enable agility in tenders.

• Allows negotiation and if applicable the expropriation of property to develop the projects, as in the case of rights of way.

• Allows the modification of contracts to recognize the existence of some circumstances.

• Grants reimbursement of investments made in the case of an early termination.

• Solves disputes regarding technical or economic differences between parties, based on expert judgment or arbitration

NEW PPP LAW

*Project of Decree issuing the Public Private Partnerships Act and amending, supplementing or repealing certain provisions of the Law on Public Works and Related Services , the Law

of Acquisitions, Leasing and Services of the Public Sector, Law Expropriation, the National Assets Law and the Code of the Federation of Civil Procedure.

10

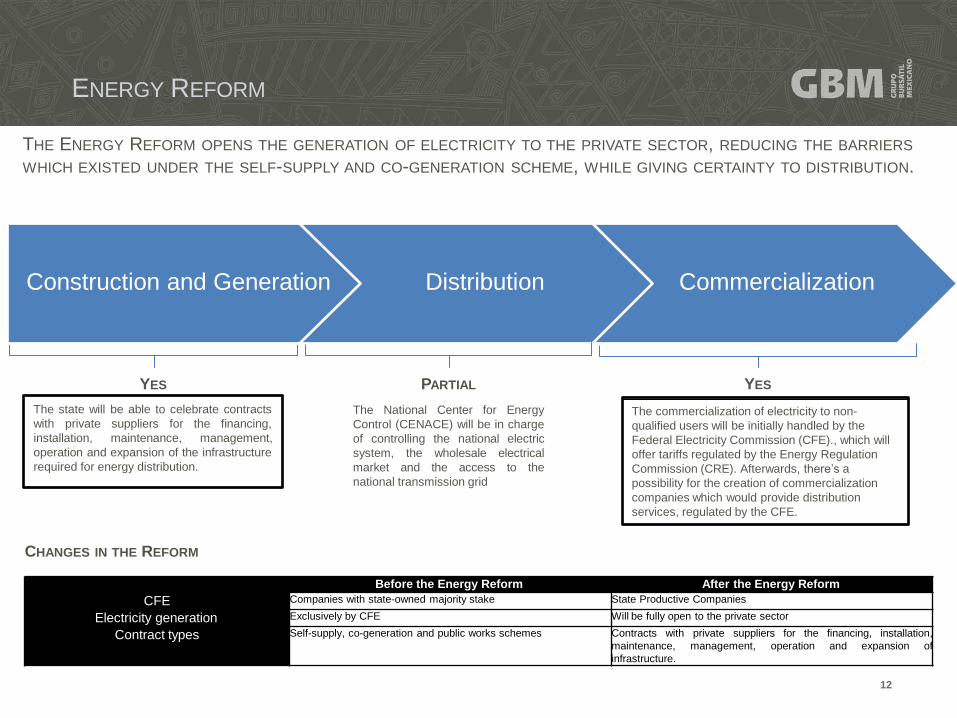

The Energy Reform authorizes integrated services

and operational yield contracts as well as shared

production schemes.

ENERGY REFORM

THE 2013 ENERGY REFORM REPRESENTS A KEY MOMENT FOR THE ENTIRE HYDROCARBON VALUE CHAIN, GENERATING

OPPORTUNITIES FOR PRIVATE INVESTORS.

CHANGES IN THE REFORM

The Energy Reform creates opportunities for investing in the production, refining, distribution, storage and commercialization of hydrocarbons.

YES YES YES

The Energy Reform will allow the

treatment and refining of oil, as well

the processing of natural gas, to be

handled through permits.

With the Energy Reform, oil exploration and extraction

activities will be carried out through awards to state-owned

productive companies or contracts to private players.

Refining

Field

Abandonment Production Fields’

Development

Production

Delimitation of

Reservoirs Assessment

of Prospects

Analysis and

Strategy

Assestment

Analysis and

Assessment

of Hypothesis

Analysis and

Assessment

of oil systems

Analysis and

Assessment of

Basins

Exploration

Assessment of Potential Reservoirs

Characterization

Reserves

Incorporation

Before the Energy Reform After the Energy Reform

PEMEX Company with state-owned majority stake State Productive Company

Contract types Incentivized contracts Shared profit or production contracts

Accounting and Financial effects Awards and contracts cannot be reported for accounting effects. Companies will be able to report awards and contracts for

accounting effects.

Storage, transportation and distribution Regulated by PEMEX Regulated by the National Hydrocarbon Commission

11

The state will be able to celebrate contracts

with private suppliers for the financing,

installation, maintenance, management,

operation and expansion of the infrastructure

required for energy distribution.

ENERGY REFORM

THE ENERGY REFORM OPENS THE GENERATION OF ELECTRICITY TO THE PRIVATE SECTOR, REDUCING THE BARRIERS

WHICH EXISTED UNDER THE SELF-SUPPLY AND CO-GENERATION SCHEME, WHILE GIVING CERTAINTY TO DISTRIBUTION.

CHANGES IN THE REFORM

YES

Construction and Generation Distribution Commercialization

PARTIAL

The National Center for Energy

Control (CENACE) will be in charge

of controlling the national electric

system, the wholesale electrical

market and the access to the

national transmission grid

YES

The commercialization of electricity to non-

qualified users will be initially handled by the

Federal Electricity Commission (CFE)., which will

offer tariffs regulated by the Energy Regulation

Commission (CRE). Afterwards, there’s a

possibility for the creation of commercialization

companies which would provide distribution

services, regulated by the CFE.

Before the Energy Reform After the Energy Reform

CFE Companies with state-owned majority stake State Productive Companies

Electricity generation Exclusively by CFE Will be fully open to the private sector

Contract types Self-supply, co-generation and public works schemes Contracts with private suppliers for the financing, installation,

maintenance, management, operation and expansion of

infrastructure.

12

OPPORTUNITIES IN GREENFIELD PROJECTS GO BEYOND THOSE CONTEMPLATED IN THE NIP AND ARE PRESENTED IN

DIVERSE INFRASTRUCTURE SECTORS, THUS BEING ABUNDANT AND DIVERSIFIED. MAIN SECTORS VALUE PROPOSITION IDENTIFIED OPPORTUNITIES

INVESTMENT IN GREENFIELD PROJECTS

Highways

Commuter Transportation

Port Terminals

Multimodal Terminals

Touristic Infrastructure

Com

munic

ations &

Tra

nsport

E

nerg

y

Hid

raulic

Airports

Hydrocarbons

Pipelines

Renewable Energy

Aqueducts

Adjacent business development;

Real Estate value release

Efficient operating structures;

Creating synergies with urban transportation

Exploiting geographical advantages vs US

Development of new container terminals

Efficient operating structures;

Key locations’ development

Standardizing service offers;

Integrating touristic routes

Strategic relocation

New airport development

Creating new companies for the operation of oil fields,

implementing best practices.

Integration of polyethylene chain to address the market

deficit in Mexico.

Development of new hidraulic networks and efficient

Siglo XXI, Tuxpan –Tampico, Paquete Chiapas, Cardel

–Poza Rica, Guanajuato – San Miguel

Line 3 of Mexico City’s suburban train Mexico – Toluca,

México – Querétaro and Mérida – Q Roo.

Mazatlan, Lazaro Cardenas, Tuxpan, Veracruz

Mexico City and Monterrey

Calica, Los Cabos, Puerto Morelos

Mexico City, Riviera Maya, Puerto Vallarta

Oil E&P in mature fields in Chicontepec

Etileno XXI

Hermosillo, Monterrey VI

Wind in Tamaulipas, Solar in BCS.

Bio-jet fuel, ethanol Wind, solar, mini-hydro, biofuel

Petrochemicals

Power Generation from Cogeneration and

Combined Cycle Power Plants (CCPP)

Combined Cycle Power Plants in the area of influence

of new pipelines.

Utilization of both existing production chains, and of

gas prices to generate power to provide a wholesale

market.

operations to supply urban populations.

Dams Solve shortage in big cities. Xalapa Dam

13

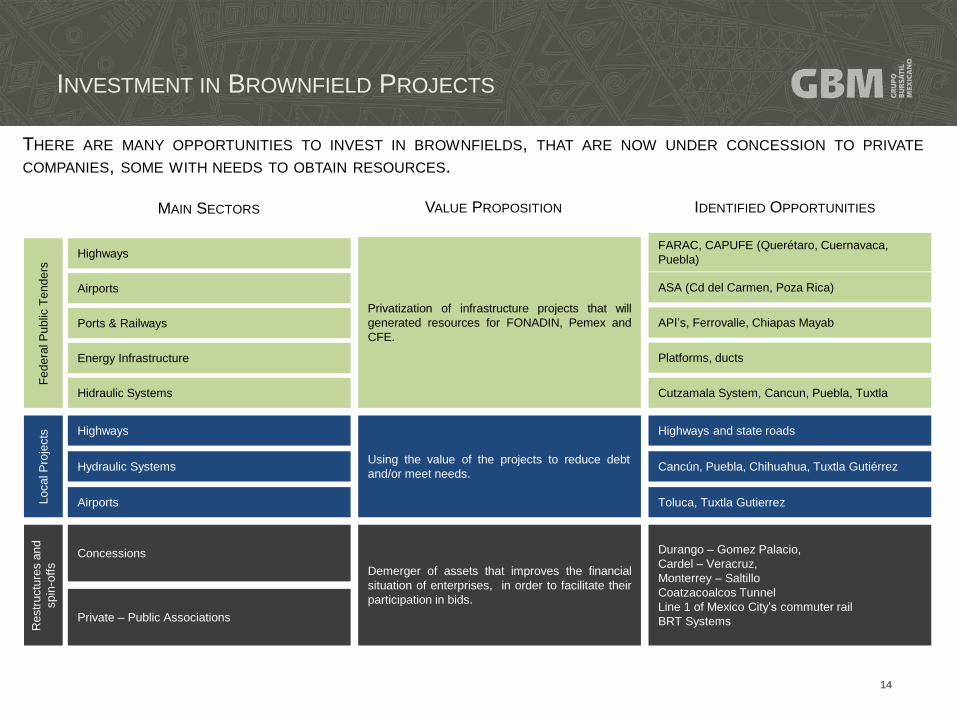

Fe

dera

l P

ublic

Tenders

Local P

roje

cts

R

estr

uctu

res a

nd

spin

-offs

Privatization of infrastructure projects that will

generated resources for FONADIN, Pemex and

CFE.

Using the value of the projects to reduce debt

and/or meet needs.

Highways

Airports

Ports & Railways

Energy Infrastructure

Hidraulic Systems

FARAC, CAPUFE (Querétaro, Cuernavaca,

Puebla)

ASA (Cd del Carmen, Poza Rica)

API’s, Ferrovalle, Chiapas Mayab

Platforms, ducts

Cutzamala System, Cancun, Puebla, Tuxtla

Highways

Hydraulic Systems

Airports

Highways and state roads

Cancún, Puebla, Chihuahua, Tuxtla Gutiérrez

Toluca, Tuxtla Gutierrez

Concessions

Private – Public Associations

Demerger of assets that improves the financial

situation of enterprises, in order to facilitate their

participation in bids.

THERE ARE MANY OPPORTUNITIES TO INVEST IN BROWNFIELDS, THAT ARE NOW UNDER CONCESSION TO PRIVATE

COMPANIES, SOME WITH NEEDS TO OBTAIN RESOURCES.

MAIN SECTORS VALUE PROPOSITION IDENTIFIED OPPORTUNITIES

Durango – Gomez Palacio,

Cardel – Veracruz,

Monterrey – Saltillo

Coatzacoalcos Tunnel

Line 1 of Mexico City’s commuter rail

BRT Systems

INVESTMENT IN BROWNFIELD PROJECTS

14

Financial restructuring of

construction companies and / or

concession operators

Consolidations

Nontraditional financial products

New Business Models

Asset Utilization: Federal, regional

and local

Private equity investments in both

Mexican and international companies

with operations in Mexico that have

solid business plans but whose

capital structures are compromised.

In fragmented industries

where there is the opportunity

to implement an acquisition

strategy for projects to achieve

synergies and economies of

scale to increase its market

share and strength of the

company.

Use of financial engineering through novel products where

traditional financial intermediaries do not participate

(examples: Mezzanine loans, convertible loans, etc…).

Redesign of the current

business model, allowing the

company to generate and

capture greater value, in order

to optimize its resource use and

returns on its operation

Transactions with governments

with assets that can be used to

solve the lag between income

and expenditure.

The presence of these

factors will be essential for

the projects’ feasibility

SOURCE OF INVESTMENT

THE CURRENT STATE OF THE INFRASTRUCTURE SECTOR WILL GENERATE OPPORTUNITIES MATCHING

INFRAESTRUCTURA’S EXPERIENCE AND CAPACITY.

15

INFRAESTRUCTURA WILL INVEST IN ACTIVITIES RELATED TO PLANNING, DESIGN, CONSTRUCTION, DEVELOPMENT,

OPERATION AND MAINTENANCE OF INFRASTRUCTURE PROJECTS.

INFRASTRUCTURE CHARACTERISTICS

1. Relatively inelastic demand resulting from demographic and assets trade. The demand does not change substantially, regardless of

variations in the price of related goods or services

2. Regulated revenue flow resulting mainly from concessions or long-term contracts for services that generally offer predictable cash

flows and inflation coverage.

3. A limited level of competition in view of the entry and technological barriers and of government approvals.

INVESTMENT OBJECTIVE

INSTRUMENTS

Once the asset or assets have been selected, Infraestructura

will seek to invest through a flexible vehicle capable of

optimizing the capital structures with a clear exit strategy.

• Convertible debt,

• Mezzanine debt,

• Preferred, at a discount (stock or private),

• and Private companies’ equity, among others.

These instruments will be used depending on the case, and at

the different stages of the project’s life.

SECTORS

Infraestructura will focus on the following sectors:

Communication Sector: Roads, bypasses, ports, airports, railroads, commuter rail, cargo

terminals and logistics facilities, among others.

Hydraulic Sector: Water purification and treatment plants, aqueducts, water

distribution networks, among others.

Energy Sector : Oilfield operation, power generation, development of alternative

energy sources, biofuels and other clean energy sources, among

others.

16

STRATEGY

THE INVESTMENT STRATEGY SHOULD BE BASED ON ADDING VALUE TO A RIGOROUS SELECTION OF ASSETS AND

OPERATING PARTNERS IN ORDER TO ENSURE ATTRACTIVE RETURNS.

Asset Selection Suitable Operating

Partner Added Value + + Higher returns than

market returns =

Synergies with adjacent projects

Growth Potential

Optimization of Tariff Structures

Elements that add value

Operating Efficiencies

Financial Structure Improvements

Creation of platforms seeking to exit

investments through financial markets

17

GBM HAS THE PROVEN ABILITY TO CREATE, ANALYZE, STRUCTURE, INVEST, NEGOTIATE, MONITOR, AND CARRY OUT

INVESTMENT OPPORTUNITIES WITH AN EXPECTED RETURN BETWEEN 16%,AND 19% WHICH IS HIGHER THAN THE

AVERAGE RETURN IN THE INFRASTRUCTURE SECTOR.

PERFORMANCE AND RISK

Clear origination in the way of entering, managing risks, and exiting.

Rigorous analysis of the sector and the asset, as well as of the parties involved, to find

the right price and determine the feasibility of the project.

Negotiation of minority rights to ensure adequate strategic decisions and avoid

inappropriate behavior.

Optimization of funding sources to boost the growth of the business and managing risk.

Institutionalization in order to increase accountability and facilitate access to capital

markets.

Choosing and implementing the appropriate mechanism based on market knowledge.

Vision

Due Diligence

Terms and Conditions

Corporate

Governance

Capital Structure

Successful Exit

18

GBM’S INFRASTRUCTURE FUND HAS THE SUPPORT OF GBM TO ACHIEVE A PROPER STRUCTURE, MANAGEMENT AND

CONTROL.

SUPPORT OF CORPORATIVO GBM

MANAGEMENT CONTROL SUPPORT AND OPERATION OF ASSETS

GBM Infraestructura.

• Portfolio management

• Sales

• Monitoring of asset performance.

• Risk assessment.

• Corporate governance.

• Report (valuation and justification of

investment objectives).

• Periodic performance evaluation.

GBM Brokerage

• Market research.

• Evaluation of returns.

• Covenants.

• Sponsorship (channeling).

• exit strategies.

Holders’ Assembly

Technical

Committee

Investment

Comittee

Investment

Management

Regulation and

Accountability

Investment

origination,

monitoring and

analysis

Fiduciary

Independent Auditor

Operating Partners

Independent Apraiser

Common

Representative

• Fund Accounting and Reporting

• Cash management

• Buy/Sell Execution

• Monitoring the operations of the Trust

• Audit the Fund’s Accounting.

• Independent valuation

of the fund’s assets

• Origination, co-

investment and operation

of the projects.

C o r p o r a t i v o G B M

P o r t f o l i o I n v e s t m e n t s

I n c G B M C a p i t a l

G B M C a s a d e B o l s a

O p e r a d o r a G B M F o m e n t a G B M

S o f o m G B M

I n f r a e s t r u c t u r a

G B M B r a s i l

H o u s t o n B r o k e n D e a l e r

G B M C h i l e

19

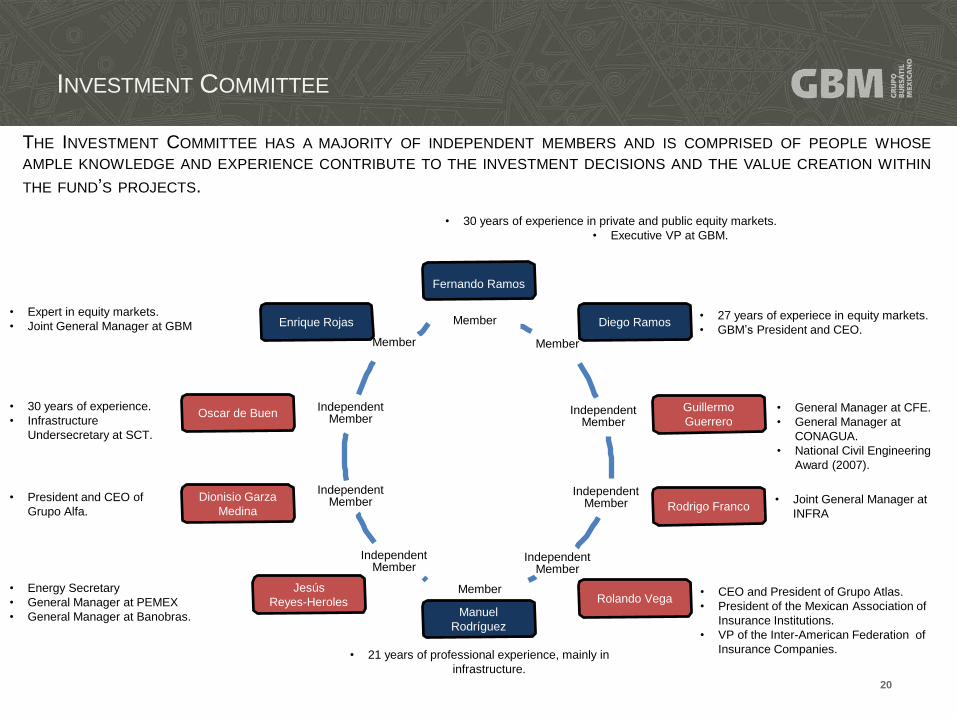

THE INVESTMENT COMMITTEE HAS A MAJORITY OF INDEPENDENT MEMBERS AND IS COMPRISED OF PEOPLE WHOSE

AMPLE KNOWLEDGE AND EXPERIENCE CONTRIBUTE TO THE INVESTMENT DECISIONS AND THE VALUE CREATION WITHIN

THE FUND’S PROJECTS.

• 30 years of experience in private and public equity markets.

• Executive VP at GBM.

Fernando

Ramos

INVESTMENT COMMITTEE

Member

Member

Independent Member

Independent Member

Independent Member

Member

Independent Member

Independent Member

Independent Member

Member

Manuel

Rodríguez

Guillermo

Guerrero

Diego Ramos Enrique Rojas

Rolando Vega

Oscar de Buen

Jesús

Reyes-Heroles

Fernando Ramos

• Expert in equity markets.

• Joint General Manager at GBM

• General Manager at CFE.

• General Manager at

CONAGUA.

• National Civil Engineering

Award (2007).

• 30 years of experience.

• Infrastructure

Undersecretary at SCT.

• Energy Secretary

• General Manager at PEMEX

• General Manager at Banobras.

• 21 years of professional experience, mainly in

infrastructure.

• 27 years of experiece in equity markets.

• GBM’s President and CEO.

• CEO and President of Grupo Atlas.

• President of the Mexican Association of

Insurance Institutions.

• VP of the Inter-American Federation of

Insurance Companies.

Rodrigo Franco Dionisio Garza

Medina

• President and CEO of

Grupo Alfa. • Joint General Manager at

INFRA

20

THE TECHNICAL COMMITTEE HAS A MAJORITY OF INDEPENDENT MEMBERS AND IS FORMED BY REPRESENTATIVES OF

THE CKD’S HOLDERS AND OF GBM. WITH THE SUPPORT OF EXTERNAL ADVISORS, THE TECHNICAL COMMITTEE

MAKES THE FUND’S INVESTMENT DECISIONS AND FOLLOWS THE DEVELOPMENT OF THE ITS INVESTMENTS.

Independent

TECHNICAL COMMITTEE

Manuel Rodríguez Ginger Evans

Diego

Ramos

Enrique

Rojas

Guillermo Guerrero

Oscar de Buen

Louis Ranger

Jeff Shane

Jesús

Reyes-Heroles

Fernando Ramos

• Joint CEO at GBM.

• Variable income

investments expert.

• CEO at CFE.

• CEO at CONAGUA.

• National Civil Engineering

Award (2007).

• 30 years of experience.

• Undersecretary of

infrastructure at SCT.

• Secretary of Energy.

• General Manager of

PEMEX.

• CEO at Banobras.

• Managing Director of GBM

Infraestructura.

• 21 years of professional

experience, mainly in

infrastructure.

• Deputy Minister of

Transport, Infrastructure

and Communities for the

Canadian government.

• VP of Engineering at

Metropolitan Washington

Airports Authority

• Director of Aviation and Sr.

VP at Parsons Corporation.

• Experience in infrastructure,

mainly in the US

Department of

Transportation (DOT).

• Undersecretary of policies

at the DOT.

• Executive Vice-President at

GBM.

• 30 years of experience in

private and public equity

investments.

• President and CEO of GBM.

• 27 years of experience in

equity markets.

AFORE Banamex

AFORE

SURA

• Assets under

management: MXP$270,

643 million.

• Assets under

management:

MXP$335,655 million.

AFORE Principal Financial

• Assets under

management:

MXP$130,651 million.

GBM Investors Members Advisors

21

INFRAESTRUCTURA ADOPTS MARKET

TRANSPARENCY. FOR THIS REASON,

ASSOCIATION (ILPA).

PRACTICES WHICH ENABLE THE ALIGNMENT OF INCENTIVES AS WELL AS

IT FOLLOWS THE GUIDELINES OF THE INTERNATIONAL LIMITED PARTNERS

ALIGNMENT WITH BEST PRACTICES

THE 3 AXIS OVER WHICH THE FUND IS MANAGED:

ALIGNMENT OF INTERESTS FUND MANAGEMENT TRANSPARENCY

• Remuneration: Mainly based on the success of

the investments, through Performance

Distributions.

• Management fee: Competitive.

• Joint venture: Obligation to co-invest with the

Fund in each investment and disinvestment.

• Investment opportunities: Obligation not to

take advantage of investment opportunities that

are within the fund’s objectives, except for

specific exceptions (eg, after completion of the

Investment Period or investments rejected by

the Technical Committee).

• Subsequent funds: Obligation not to complete

a subsequent offer of a fund with similar

strategies and objectives until 80% of the Fund

has been invested.

• Investment Period: 5 years with the obligation

to invest 20% in the first 2 years.

• Investment strategy: Aligned to FONADIN’s

investment strategy.

• Capital calls and distributions: Subject to

market practices.

• Corporate

Shareholders’

Committee

bodies: Fiduciary, trustee,

Meeting, and Technical

in accordance with legal

requirements and market practices.

• Key Officials: Involve key persons leading the

daily businesses of the Trust

• Manager Replacement: With or without cause,

in accordance with market practices.

• Risk management. Infraestructura will have the

workgroup and support from GBM and its

analysts to identify and manage potential risks

of the

• Cascade, Accounts

Transparent.

and Expenses:

• Valuation: By independent appraiser.

• Independent Auditor: To audit the Fund’s

financial information.

• Financial information: In accordance with

market practices.

• Reserve and Independent Advisors. Set up

in order to be used by the Shareholders to hire

independent advisors.

• Reserved Matters: The Independent

Members of the Technical Committee will

decide on transactions where there is a conflict

of interest, as well as appoint a new

independent appraiser, Trustee or External

Auditor.

22

CONCLUSIONS

GBM Infraestructura meets all the requirements to ensure the success of the listed private equity fund

Alignment of incentives through the joint venture of 20% from GBM Investment and Technical Committees with a majority of Independent Members GBM Professional team with vast experience in various types of infrastructure projects. GBM track record in Infrastructure and adjacent businesses in Mexico. Alignment of incentives through Capital Calls Experience as fund manager in Mexico Strategy aligned to the NIP that identifies investment opportunities for Private Equity. Relationships Network to select proper partners and promote projects. Detailed Due Diligence and asset management processes. Experience in optimizing capital structures. Knowledge of the different stages of a project’s life cycle. Capacity to generate business exits (IPO, securitization, etc.). Accountability with best practices for corporate governance and reports. Proven commitment, assigning human and material resources by GBM.

23

September 16, 2014

The Bridge to Mexican Infrastructure

Mexico in a North American Context Historical Underdevelopment Implies Remaining Potential

Mexico today has 5% of the oil reserves and 4% of

the gas reserves in NAM…

…but it has not always been that way (1984)

There’s also shale potential

___________________________________

Source: EIA, CIA.

10 5%

201 95%

Oil Proved Reserves (Bbbl)

Mexico US & Canada

17 4%

395 96%

Gas Proved Reserves (Tcf)

Mexico US & Canada

13 16%

67 84%

Shale Oil Resource (Bbbl)

Mexico US & Canada

545 31%

1,238 69%

Shale Gas Resource (Tcf)

Mexico US & Canada

5642%

7758%

Oil Proved Reserves (Bbbl)

Mexico US & Canada

77 21%

297 79%

Gas Proved Reserves (Tcf)

Mexico US & Canada

25

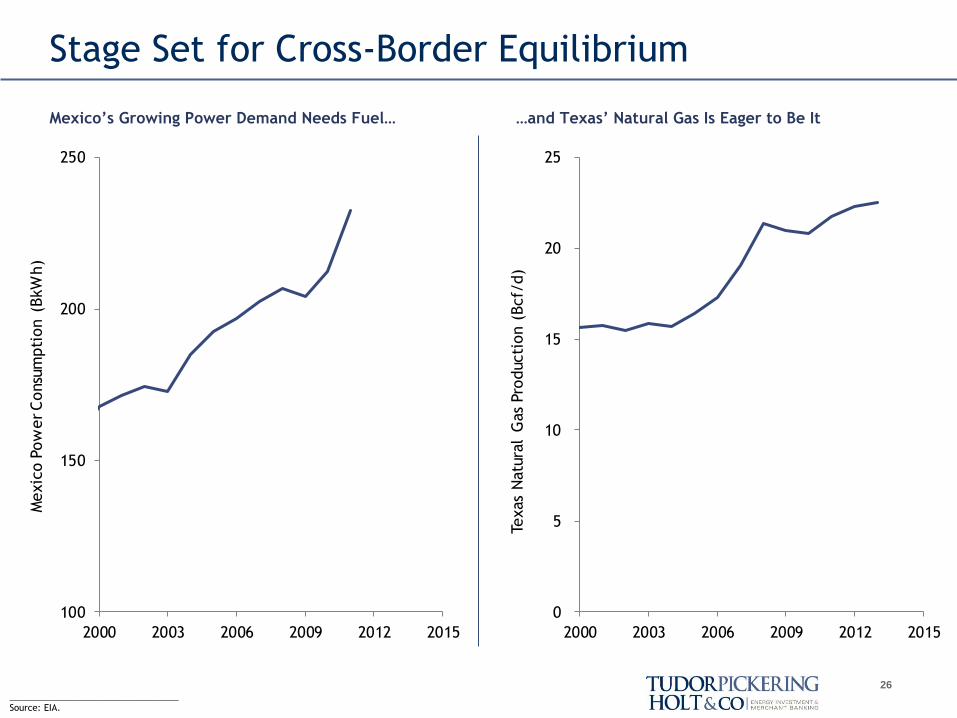

Stage Set for Cross-Border Equilibrium

Mexico’s Growing Power Demand Needs Fuel… …and Texas’ Natural Gas Is Eager to Be It

100

150

200

250

2000 2003 2006 2009 2012 2015

Mexic

o P

ow

er C

onsu

mpti

on (

BkW

h)

___________________________________

Source: EIA.

0

5

10

15

20

25

2000 2003 2006 2009 2012 2015

Texas

Natu

ral

Gas

Pro

ducti

on (

Bcf/

d)

26

Midstream Investments Needed to Keep Pace

Power Plants and LNG Terminals Will Fuel Demand for Additional Natural Gas Pipeline Capacity

___________________________________

Source: Woodmac, RBN Energy, Platt, Shalemag, KMI.

LNG Terminal

New or Expansion CCGT

Existing Pipelines

Expansion Pipelines

US exporting ~2 Bcf/d to Mexico

~3% of entire US output

>4 Bcf/d in next decade

$34B needed in pipeline

infrastructure investment

55 GW of new generation

needed over next few years

27

©2014 Vinson & Elkins LLP Confidential & Proprietary

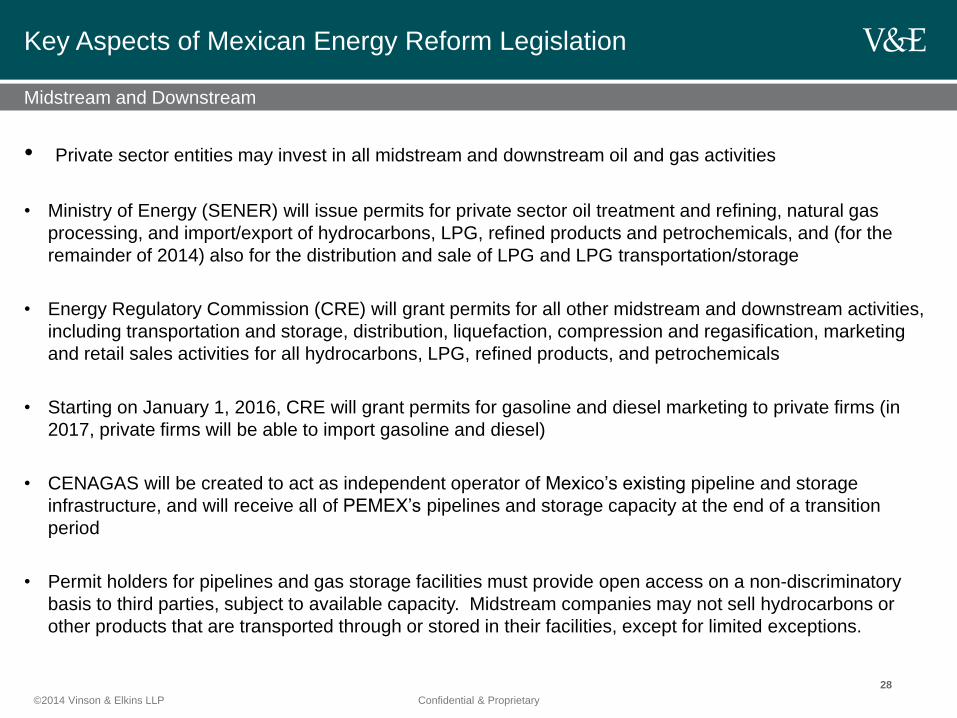

Midstream and Downstream

• Private sector entities may invest in all midstream and downstream oil and gas activities

• Ministry of Energy (SENER) will issue permits for private sector oil treatment and refining, natural gas

processing, and import/export of hydrocarbons, LPG, refined products and petrochemicals, and (for the

remainder of 2014) also for the distribution and sale of LPG and LPG transportation/storage

• Energy Regulatory Commission (CRE) will grant permits for all other midstream and downstream activities,

including transportation and storage, distribution, liquefaction, compression and regasification, marketing

and retail sales activities for all hydrocarbons, LPG, refined products, and petrochemicals

• Starting on January 1, 2016, CRE will grant permits for gasoline and diesel marketing to private firms (in

2017, private firms will be able to import gasoline and diesel)

• CENAGAS will be created to act as independent operator of Mexico’s existing pipeline and storage

infrastructure, and will receive all of PEMEX’s pipelines and storage capacity at the end of a transition

period

• Permit holders for pipelines and gas storage facilities must provide open access on a non-discriminatory

basis to third parties, subject to available capacity. Midstream companies may not sell hydrocarbons or

other products that are transported through or stored in their facilities, except for limited exceptions.

Key Aspects of Mexican Energy Reform Legislation

28

September 16, 2014

The Bridge to Mexican Infrastructure

Rio Grande City Bore Site

Tool placement prior to drill

30

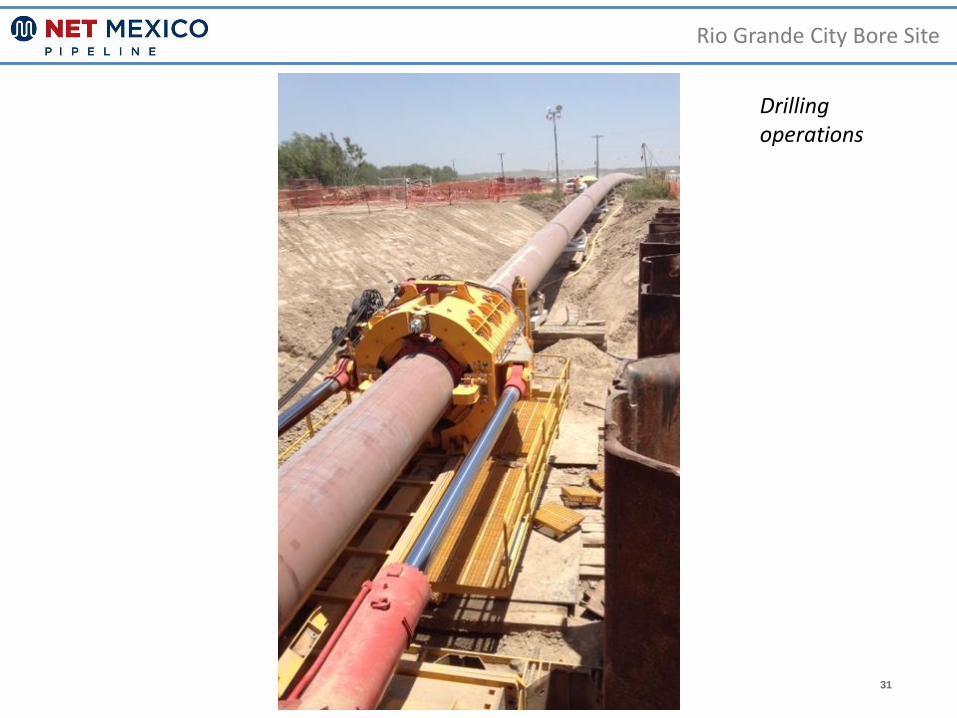

Rio Grande City Bore Site

Drilling operations

31

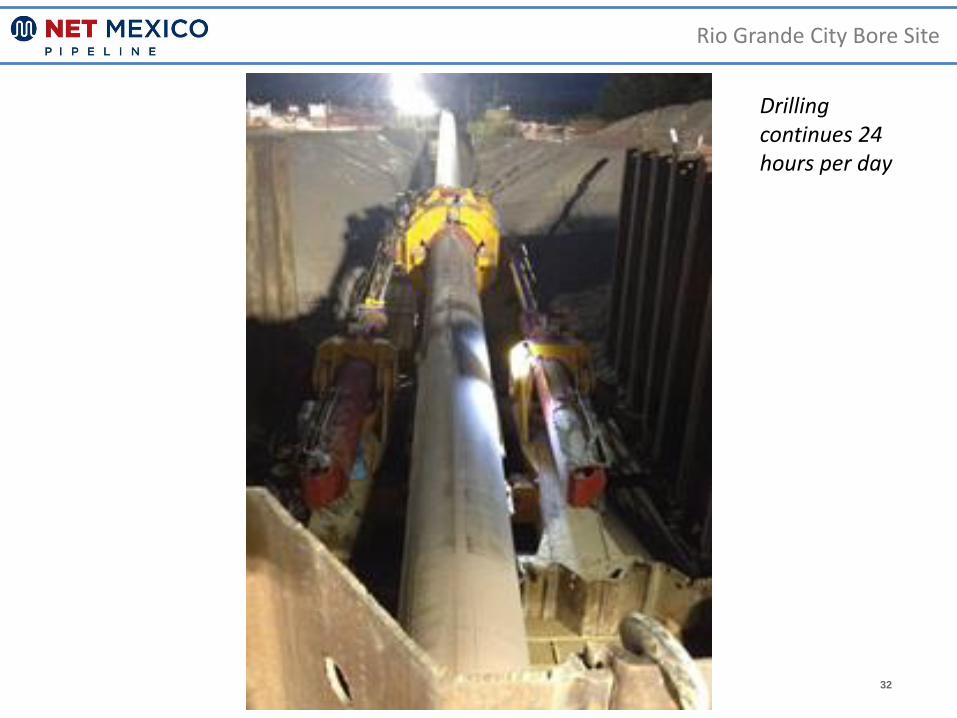

Rio Grande City Bore Site

Drilling continues 24 hours per day

32

Mainline Pipeline Construction

Welding operations

33

Mainline Pipeline Construction

Welding shacks on the mainline

34

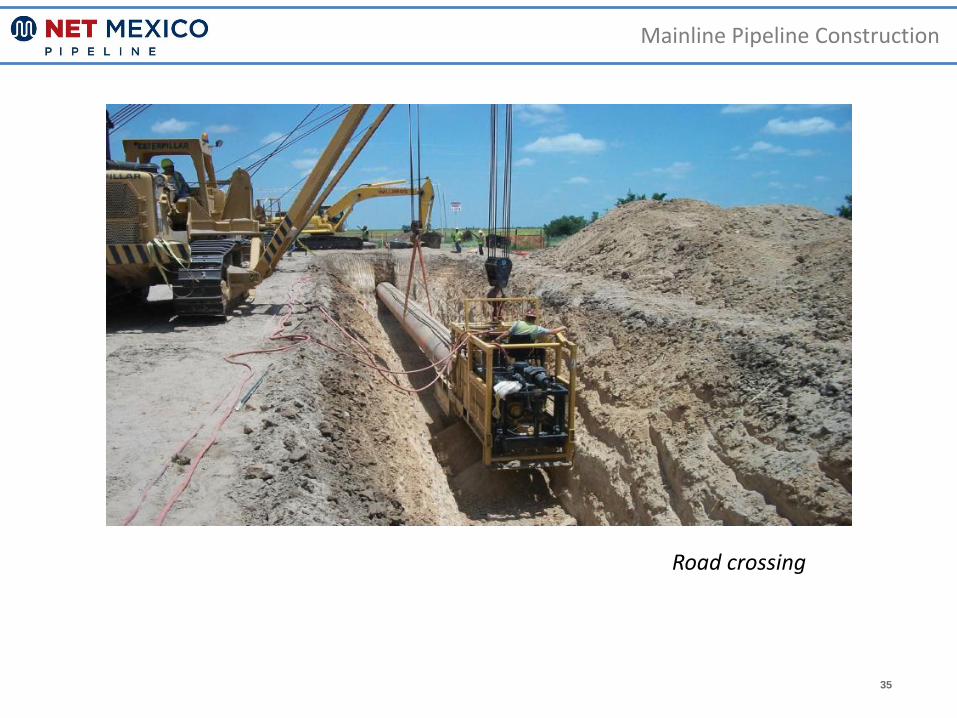

Mainline Pipeline Construction

Road crossing

35

Mainline Pipeline Construction

36

Agua Dulce Compressor and Header

24” flow valve

37

Agua Dulce Compressor and Header

Solar compressors arrive on-site

38

Agua Dulce Compressor and Header

Gas cooler installation

39

Agua Dulce Compressor and Header

40

Agua Dulce Compressor and Header

Compressor building (1 of 4)

41